Exhibit 99.1

FMC Corporation

Global Soda Ash Outlook E.T. Flynn

UBS Warburg

Grassroots Chemical Conference February 17, 2005

Disclaimer

Safe Harbor Statement under the Private Securities Litigation Reform Act of 1995

These slides and the accompanying presentation contain “forward-looking statements” that represent management’s best judgment as of the date hereof based on information currently available. Actual results of the Company may differ materially from those contained in the forward-looking statements.

Additional information concerning factors that may cause results to differ materially from those in the forward-looking statements is contained in the Company’s periodic reports filed under the Securities Exchange Act of 1934, as amended.

The Company undertakes no obligation to update or revise these forward-looking statements to reflect new events or uncertainties.

1

Non-GAAP Financial Terms

These slides contain certain “non-GAAP financial terms” which are defined below. In addition, we have provided reconciliations of non-GAAP terms to the closest GAAP term in the appendix of this presentation:

EBITDA (Earnings Before Interest, Taxes, Depreciation and Amortization) is the sum of Income (loss) from continuing operations before income taxes and Depreciation and Amortization.

EBITDA Margin is the quotient of EBITDA (defined above) divided by Revenue.

These slides also contain references to segment financial items which are presented in detail in Note 19 of FMC’s 2003 Form 10-K. Some of the segment financial terms are “non-GAAP financial terms” and are defined below. In addition, we have provided reconciliations of non-GAAP terms to the closest GAAP term in the appendix of this presentation:

EBITDA (Earnings Before Interest, Taxes, Depreciation and Amortization) for a segment is the sum of Income (loss) from continuing operations before income taxes for that segment and Depreciation and Amortization for that segment.

EBITDA Margin for a segment is the quotient of EBITDA (defined above) divided by Revenue for that segment.

2

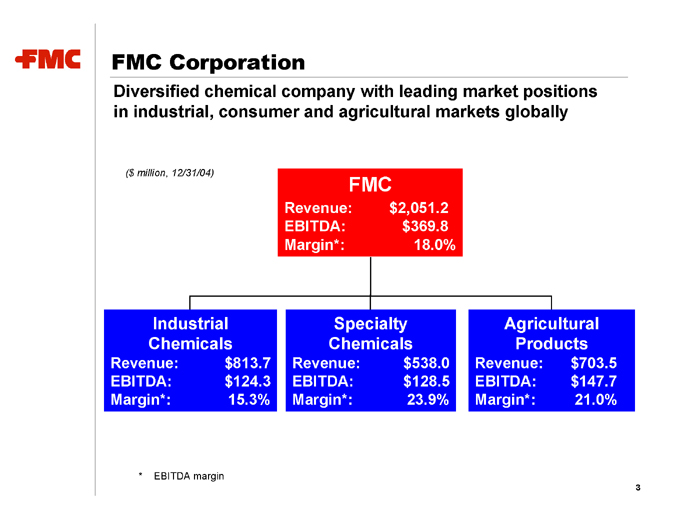

FMC Corporation

Diversified chemical company with leading market positions in industrial, consumer and agricultural markets globally

($ million, 12/31/04)

FMC

Revenue: $2,051.2 EBITDA: $369.8 Margin*: 18.0%

Industrial Chemicals

Revenue: $813.7 EBITDA: $124.3 Margin*: 15.3%

Specialty Chemicals

Revenue: $538.0 EBITDA: $128.5 Margin*: 23.9%

Agricultural Products

Revenue: $703.5 EBITDA: $147.7 Margin*: 21.0%

* EBITDA margin

3

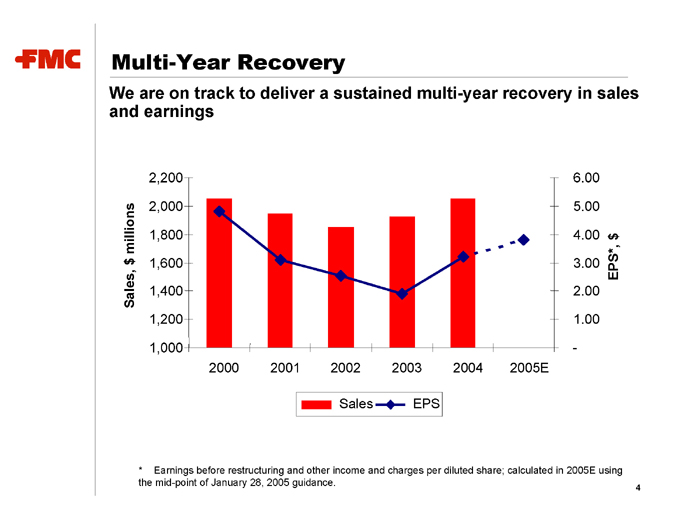

Multi-Year Recovery

We are on track to deliver a sustained multi-year recovery in sales and earnings

2,200

millions 2,000 1,800

$1,600

Sales, 1,400 1,200

1,000

2000 2001 2002 2003 2004 2005E

Sales EPS

6.00

5.00

4.00

$3.00 EPS*,

2.00

1.00

* Earnings before restructuring and other income and charges per diluted share; calculated in 2005E using the mid-point of January 28, 2005 guidance.

4

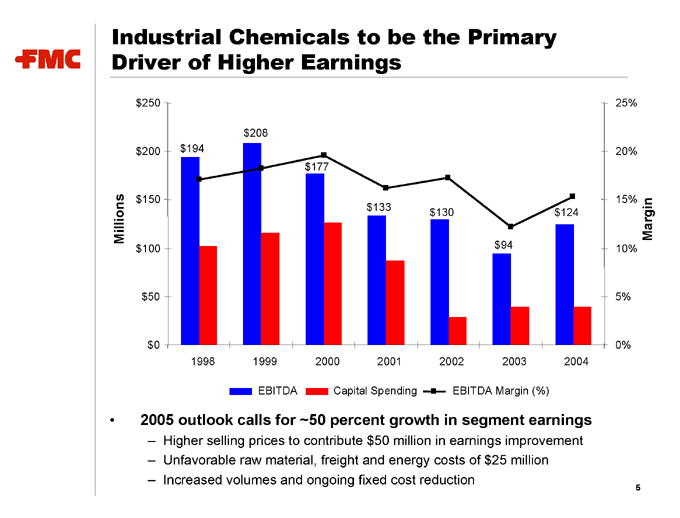

Industrial Chemicals to be the Primary Driver of Higher Earnings $250

$200

Millions $150

$100 $50 $0 $208 $194 $177

$133 $130 $124

$94

25%

20%

15% Margin

10%

5%

0%

1998 1999 2000 2001 2002 2003 2004

EBITDA Capital Spending EBITDA Margin (%)

2005 outlook calls for ~50 percent growth in segment earnings

Higher selling prices to contribute $50 million in earnings improvement Unfavorable raw material, freight and energy costs of $25 million Increased volumes and ongoing fixed cost reduction

5

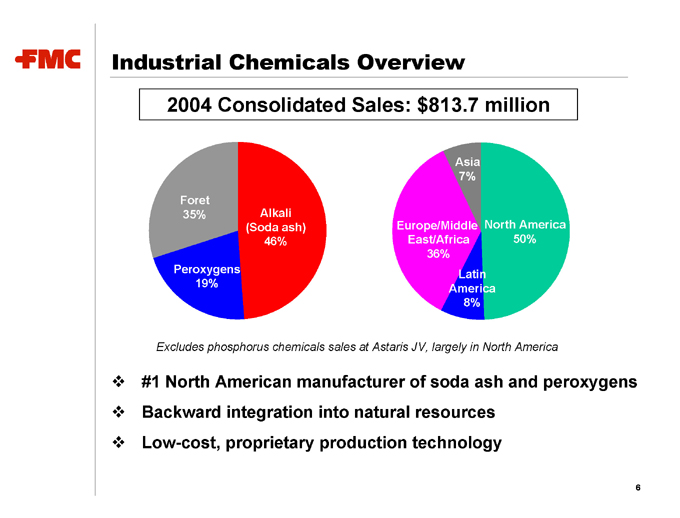

Industrial Chemicals Overview

2004 Consolidated Sales: $813.7 million

Asia 7%

Foret

35% Alkali

(Soda ash) Europe/Middle North America 46% East/Africa 50% 36% Peroxygens Latin 19% America 8%

Excludes phosphorus chemicals sales at Astaris JV, largely in North America

#1 North American manufacturer of soda ash and peroxygens Backward integration into natural resources Low-cost, proprietary production technology

6

Global Soda Ash Outlook

Agenda:

Background

China

Demand

Supply

Pricing

FMC Strengths

Summary

7

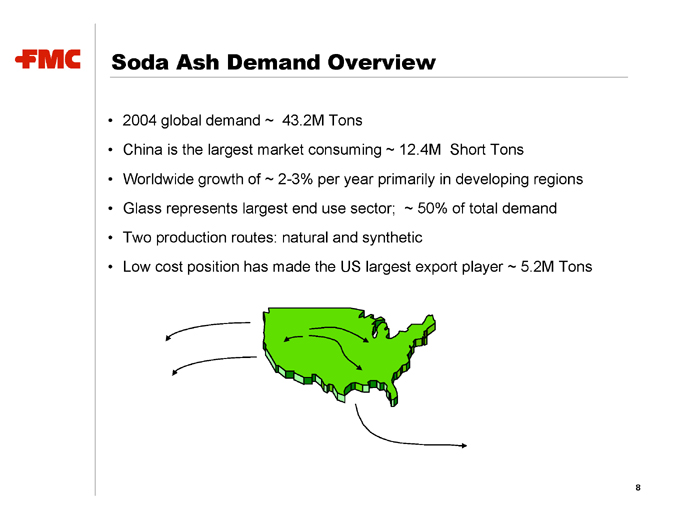

Soda Ash Demand Overview

2004 global demand ~ 43.2M Tons

China is the largest market consuming ~ 12.4M Short Tons

Worldwide growth of ~ 2-3% per year primarily in developing regions

Glass represents largest end use sector; ~ 50% of total demand

Two production routes: natural and synthetic

Low cost position has made the US largest export player ~ 5.2M Tons

8

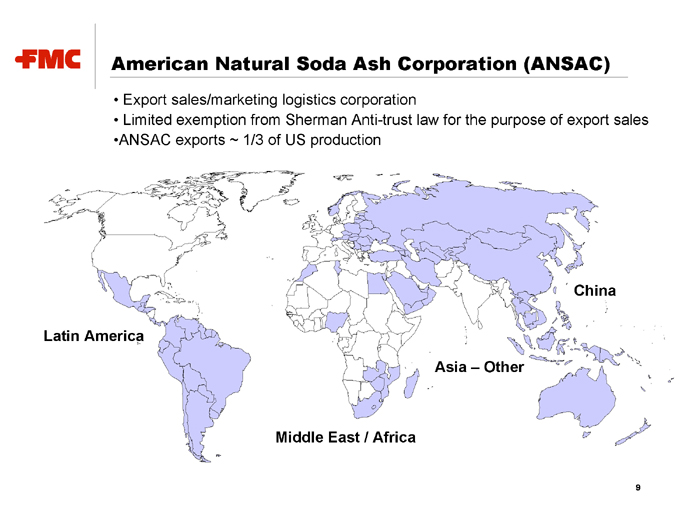

American Natural Soda Ash Corporation (ANSAC)

Export sales/marketing logistics corporation

Limited exemption from Sherman Anti-trust law for the purpose of export sales

ANSAC exports ~ 1/3 of US productionf

Latin America

China

Asia – Other

Middle East / Africa

9

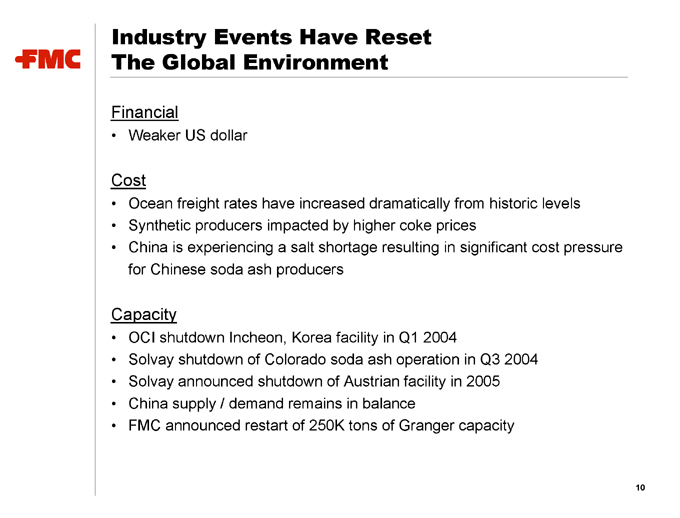

Industry Events Have Reset The Global Environment

Financial

Weaker US dollar

Cost

Ocean freight rates have increased dramatically from historic levels

Synthetic producers impacted by higher coke prices

China is experiencing a salt shortage resulting in significant cost pressure

for Chinese soda ash producers

Capacity

OCI shutdown Incheon, Korea facility in Q1 2004

Solvay shutdown of Colorado soda ash operation in Q3 2004

Solvay announced shutdown of Austrian facility in 2005

China supply / demand remains in balance

FMC announced restart of 250K tons of Granger capacity

10

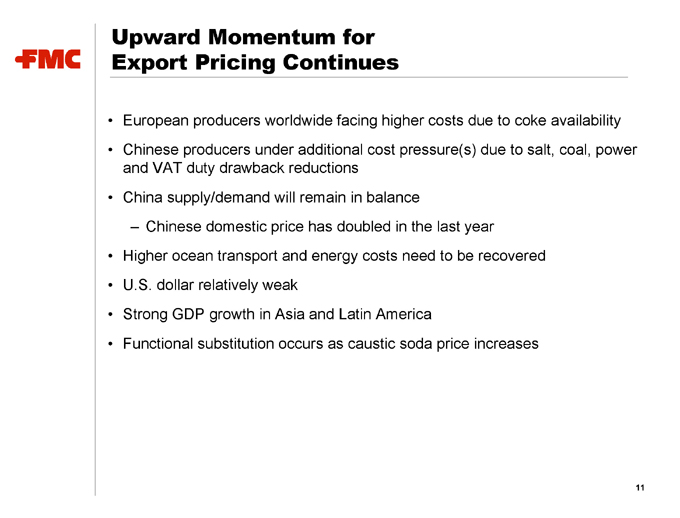

Upward Momentum for Export Pricing Continues

European producers worldwide facing higher costs due to coke availability

Chinese producers under additional cost pressure(s) due to salt, coal, power and VAT duty drawback reductions China supply/demand will remain in balance

Chinese domestic price has doubled in the last year

Higher ocean transport and energy costs need to be recovered

U.S. dollar relatively weak

Strong GDP growth in Asia and Latin America

Functional substitution occurs as caustic soda price increases

11

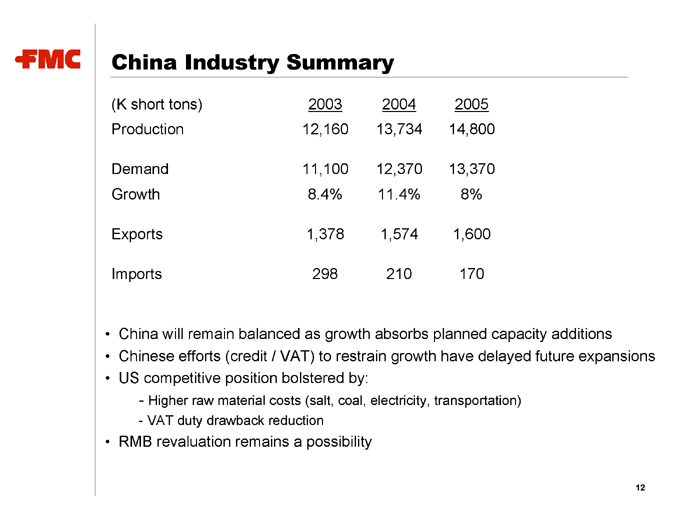

China Industry Summary

(K short tons) 2003 2004 2005

Production 12,160 13,734 14,800

Demand 11,100 12,370 13,370

Growth 8.4% 11.4% 8%

Exports 1,378 1,574 1,600

Imports 298 210 170

China will remain balanced as growth absorbs planned capacity additions Chinese efforts (credit / VAT) to restrain growth have delayed future expansions US competitive position bolstered by:

Higher raw material costs (salt, coal, electricity, transportation) VAT duty drawback reduction

RMB revaluation remains a possibility

12

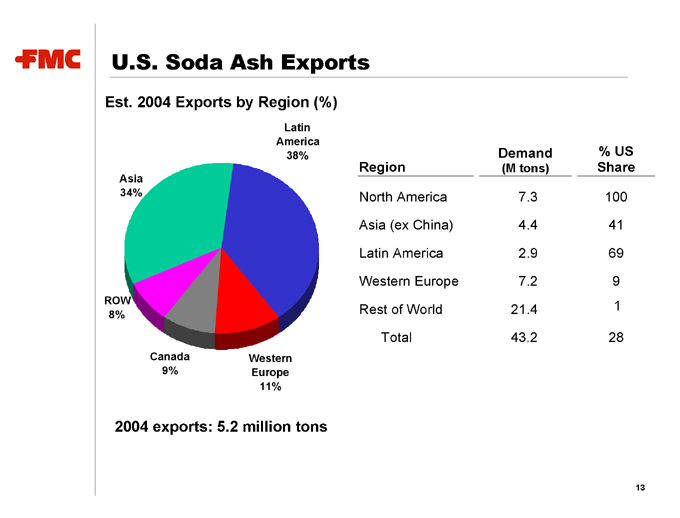

U.S. Soda Ash Exports

Est. 2004 Exports by Region (%)

Latin America 38%

Asia 34%

ROW 8%

Canada Western

9% Europe 11%

2004 exports: 5.2 million tons

U.S. Regional Share

Demand % US

Region (M tons) Share

North America 7.3 100

Asia (ex China) 4.4 41

Latin America 2.9 69

Western Europe 7.2 9

Rest of World 21.4

Total 43.2 28

13

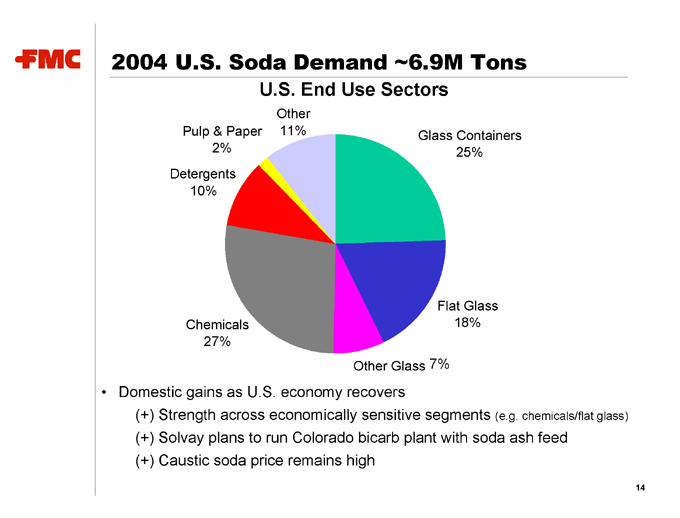

2004 U.S. Soda Demand ~6.9M Tons

U.S. End Use Sectors

Other

Pulp & Paper 11% Glass Containers

2% 25% Detergents 10%

Flat Glass Chemicals 18% 27% Other Glass 7%

Domestic gains as U.S. economy recovers

(+) Strength across economically sensitive segments (e.g. chemicals/flat glass) (+) Solvay plans to run Colorado bicarb plant with soda ash feed (+) Caustic soda price remains high

14

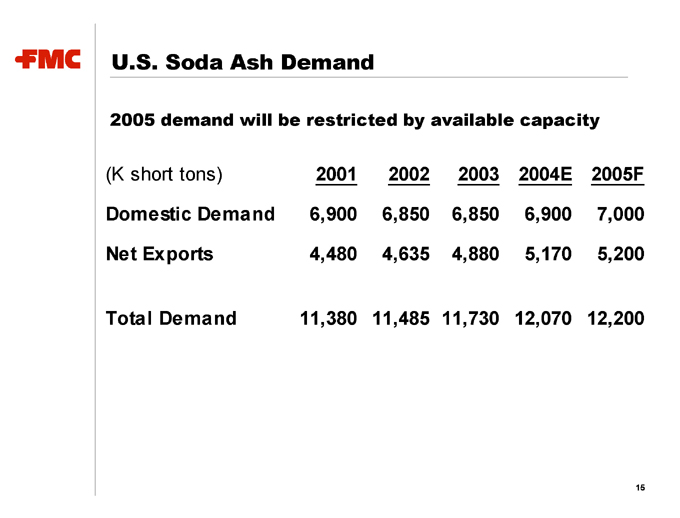

U.S. Soda Ash Demand

2005 demand will be restricted by available capacity

(K short tons) 2001 2002 2003 2004E 2005F

Domestic Demand 6,900 6,850 6,850 6,900 7,000

Net Exports 4,480 4,635 4,880 5,170 5,200

Total Demand 11,380 11,485 11,730 12,070 12,200

15

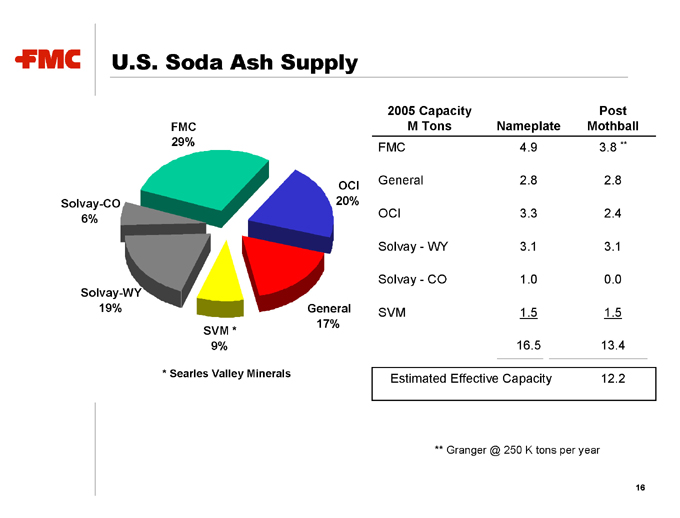

U.S. Soda Ash Supply

FMC 29%

OCI Solvay-CO 20% 6%

Solvay-WY

19% General 17% SVM * 9%

* Searles Valley Minerals

2005 Capacity Post

M Tons Nameplate Mothball

FMC 4.9 3.8 **

General 2.8 2.8

OCI 3.3 2.4

Solvay—WY 3.1 3.1

Solvay—CO 1.0 0.0

SVM 1.5 1.5

16.5 13.4

Estimated Effective Capacity 12.2

** Granger @ 250 K tons per year

16

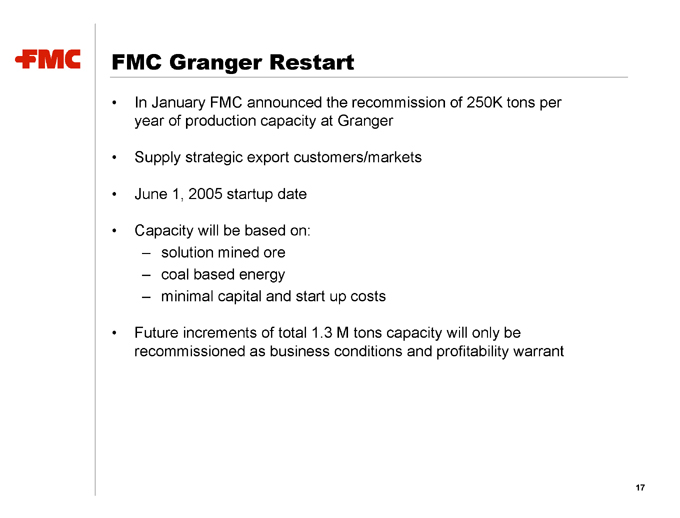

FMC Granger Restart

In January FMC announced the recommission of 250K tons per year of production capacity at Granger

Supply strategic export customers/markets June 1, 2005 startup date Capacity will be based on: solution mined ore coal based energy minimal capital and start up costs

Future increments of total 1.3 M tons capacity will only be recommissioned as business conditions and profitability warrant

17

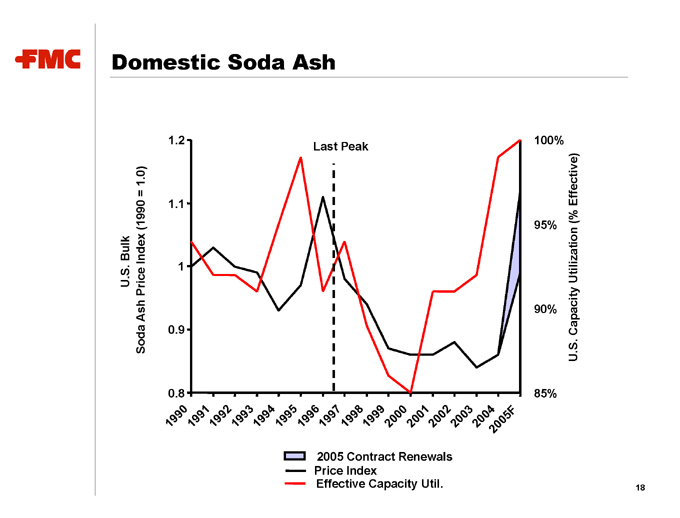

Domestic Soda Ash

U.S. Bulk

Soda Ash Price Index (1990 = 1.0)

1990 0.8 0.9 1 1.1 1.2

1991 1992 1993 1994 1995 1996 1997

Price Index 1998 Last Peak

1999

Effective Capacity Util. 2000 2001 2005 Contract Renewals 2002

2003 2004

2005F

85% 90% 95% 100% U.S. Capacity Utilization (% Effective)

18

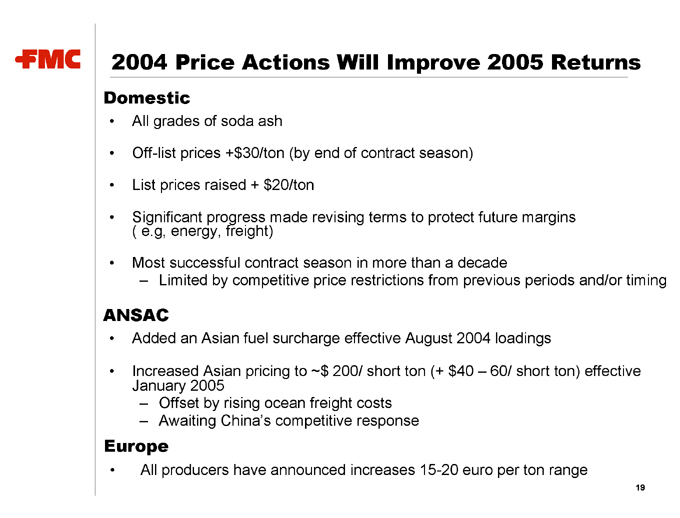

2004 Price Actions Will Improve 2005 Returns

Domestic

All grades of soda ash

Off-list prices +$30/ton (by end of contract season)

List prices raised + $20/ton

Significant progress made revising terms to protect future margins ( e.g, energy, freight)

Most successful contract season in more than a decade

Limited by competitive price restrictions from previous periods and/or timing

ANSAC

Added an Asian fuel surcharge effective August 2004 loadings

Increased Asian pricing to ~$ 200/ short ton (+ $40 – 60/ short ton) effective January 2005

Offset by rising ocean freight costs Awaiting China’s competitive response

Europe

All producers have announced increases 15-20 euro per ton range

19

Alkali Chemicals Division Key Product Offerings

High Volume

High Value (i.e. niche)

Other

Soda Ash

Sodium Sesquicarbonate Sodium Bicarbonate Light Density Soda Ash

Chemical Caustic Soda

20

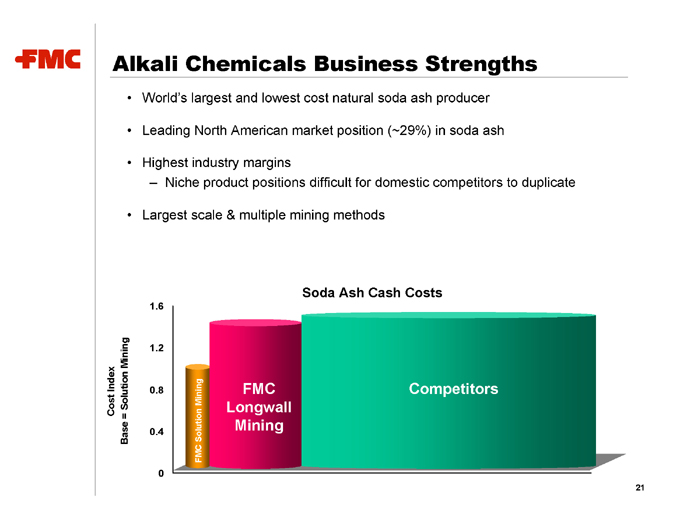

Alkali Chemicals Business Strengths

World’s largest and lowest cost natural soda ash producer Leading North American market position (~29%) in soda ash Highest industry margins

Niche product positions difficult for domestic competitors to duplicate

Largest scale & multiple mining methods

1.6

Mining 1.2

Solution

0.8 Mining FMC Competitors

Cost Index Longwall

Solution

Mining

Base = 0.4

FMC

0

21

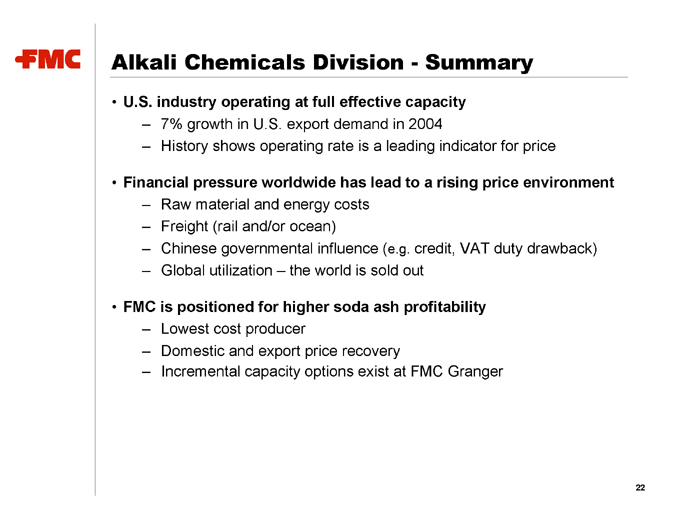

Alkali Chemicals Division—Summary

U.S. industry operating at full effective capacity

7% growth in U.S. export demand in 2004

History shows operating rate is a leading indicator for price

Financial pressure worldwide has lead to a rising price environment

Raw material and energy costs Freight (rail and/or ocean)

Chinese governmental influence (e.g. credit, VAT duty drawback) Global utilization – the world is sold out

FMC is positioned for higher soda ash profitability

Lowest cost producer

Domestic and export price recovery

Incremental capacity options exist at FMC Granger

22

FMC Corporation

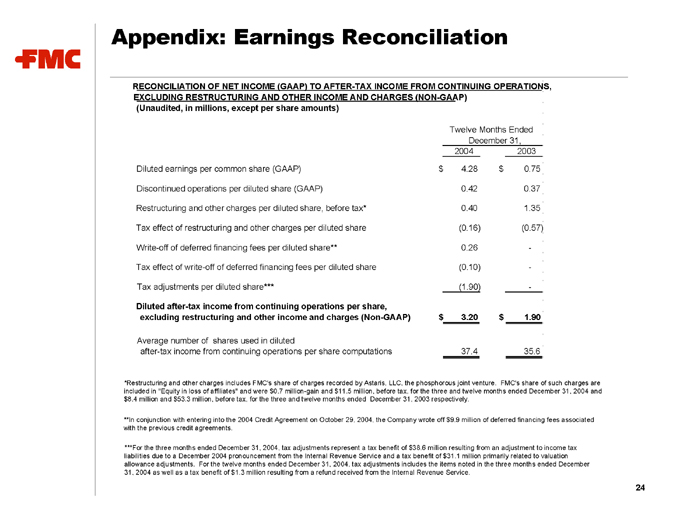

Appendix: Earnings Reconciliation

RECONCILIATION OF NET INCOME (GAAP) TO AFTER-TAX INCOME FROM CONTINUING OPERATIONS, EXCLUDING RESTRUCTURING AND OTHER INCOME AND CHARGES (NON-GAAP) (Unaudited, in millions, except per share amounts)

Twelve Months Ended

December 31, 2004 2003

Diluted earnings per common share (GAAP) $4.28 $0.75

Discontinued operations per diluted share (GAAP) 0.42 0.37

Restructuring and other charges per diluted share, before tax* 0.40 1.35

Tax effect of restructuring and other charges per diluted share (0.16) (0.57)

Write-off of deferred financing fees per diluted share** 0.26 -

Tax effect of write-off of deferred financing fees per diluted share (0.10) -

Tax adjustments per diluted share*** (1.90) -

Diluted after-tax income from continuing operations per share, excluding restructuring and other income and charges (Non-GAAP) $3.20 $1.90

Average number of shares used in diluted after-tax income from continuing operations per share computations 37.4 35.6

*Restructuring and other charges includes FMC’s share of charges recorded by Astaris, LLC, the phosphorous joint venture. FMC’s share of such charges are included in “Equity in loss of affiliates” and were $0.7 million-gain and $11.5 million, before tax, for the three and twelve months ended December 31, 2004 and $8.4 million and $53.3 million, before tax, for the three and twelve months ended December 31, 2003 respectively.

**In conjunction with entering into the 2004 Credit Agreement on October 29, 2004, the Company wrote off $9.9 million of deferred financing fees associated with the previous credit agreements.

***For the three months ended December 31, 2004, tax adjustments represent a tax benefit of $38.6 million resulting from an adjustment to income tax liabilities due to a December 2004 pronouncement from the Internal Revenue Service and a tax benefit of $31.1 million primarily related to valuation allowance adjustments. For the twelve months ended December 31, 2004, tax adjustments includes the items noted in the three months ended December 31, 2004 as well as a tax benefit of $1.3 million resulting from a refund received from the Internal Revenue Service.

24

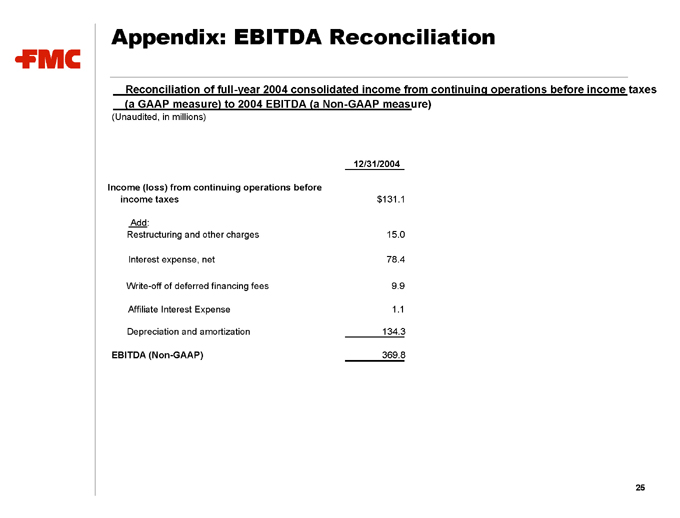

Appendix: EBITDA Reconciliation

Reconciliation of full-year 2004 consolidated income from continuing operations before income taxes (a GAAP measure) to 2004 EBITDA (a Non-GAAP measure)

(Unaudited, in millions)

12/31/2004

Income (loss) from continuing operations before income taxes $ 131.1

Add:

Restructuring and other charges 15.0

Interest expense, net 78.4

Write-off of deferred financing fees 9.9

Affiliate Interest Expense 1.1

Depreciation and amortization 134.3

EBITDA (Non-GAAP) 369.8

25

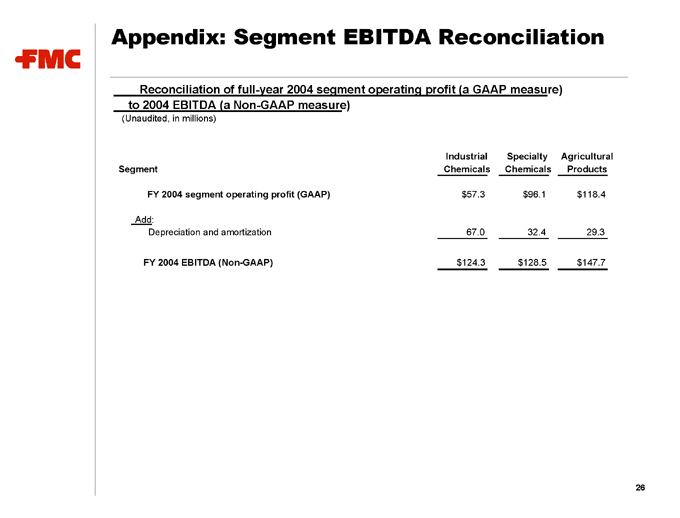

Appendix: Segment EBITDA Reconciliation

Reconciliation of full-year 2004 segment operating profit (a GAAP measure) to 2004 EBITDA (a Non-GAAP measure)

(Unaudited, in millions)

Industrial Specialty Agricultural

Segment Chemicals Chemicals Products

FY 2004 segment operating profit (GAAP) $57.3 $ 96.1 $ 118.4

Add:

Depreciation and amortization 67.0 32.4 29.3

FY 2004 EBITDA (Non-GAAP) $124.3 $128.5 $ 147.7

26

FMC Corporation