Exhibit 99.1

FMC Corporation

Banc of America Securities 2005 Basic Industries Conference

May 4, 2005

William G. Walter Chairman, President, CEO

Disclaimer

Safe Harbor Statement under the Private Securities Litigation Reform Act of 1995

These slides and the accompanying presentation contain “forward-looking statements” that represent management’s best judgment as of the date hereof based on information currently available. Actual results of the Company may differ materially from those contained in the forward-looking statements.

Additional information concerning factors that may cause results to differ materially from those in the forward-looking statements is contained in the Company’s periodic reports filed under the Securities Exchange Act of 1934, as amended.

The Company undertakes no obligation to update or revise these forward-looking statements to reflect new events or uncertainties.

Non-GAAP Financial Terms

These slides contain certain “non-GAAP financial terms” which are defined in the appendix. In addition, we have provided reconciliations of non-GAAP terms to the closest GAAP term in the appendix.

1

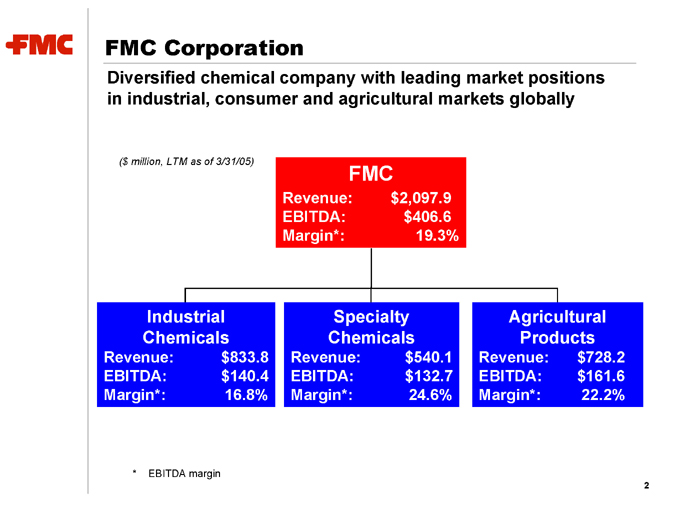

FMC Corporation

Diversified chemical company with leading market positions in industrial, consumer and agricultural markets globally

($ million, LTM as of 3/31/05)

FMC

Revenue: $2,097.9

EBITDA: $406.6

Margin*: 19.3%

Industrial

Chemicals

Revenue: $833.8

EBITDA: $140.4

Margin*: 16.8%

Specialty

Chemicals

Revenue: $540.1

EBITDA: $132.7

Margin*: 24.6%

Agricultural

Products

Revenue: $728.2

EBITDA: $161.6

Margin*: 22.2%

* EBITDA margin

2

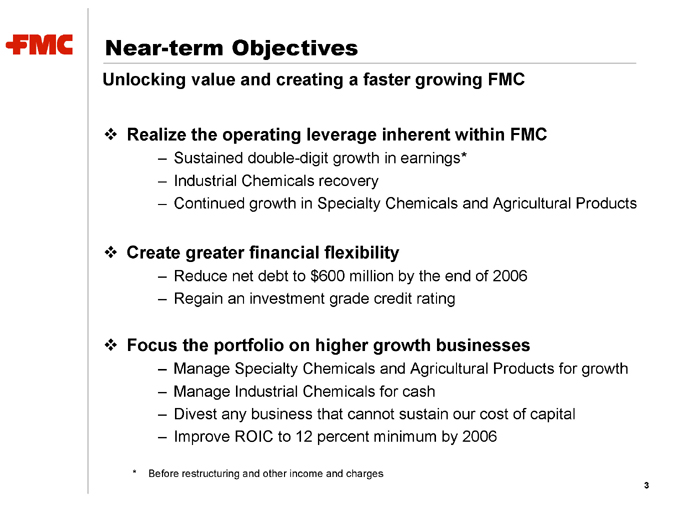

Near-term Objectives

Unlocking value and creating a faster growing FMC

Realize the operating leverage inherent within FMC

Sustained double-digit growth in earnings*

Industrial Chemicals recovery

Continued growth in Specialty Chemicals and Agricultural Products

Create greater financial flexibility

Reduce net debt to $600 million by the end of 2006

Regain an investment grade credit rating

Focus the portfolio on higher growth businesses

Manage Specialty Chemicals and Agricultural Products for growth

Manage Industrial Chemicals for cash

Divest any business that cannot sustain our cost of capital

Improve ROIC to 12 percent minimum by 2006

* Before restructuring and other income and charges

3

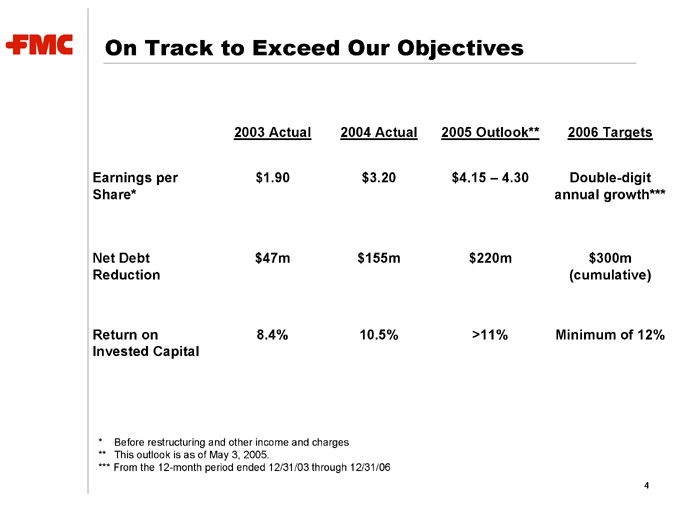

On Track to Exceed Our Objectives

2003 Actual 2004 Actual 2005 Outlook** 2006 Targets

Earnings per $1.90 $ 3.20 $4.15 – 4.30 Double-digit

Share* annual growth***

Net Debt $47m $155m $220m $300m

Reduction (cumulative)

Return on 8.4% 10.5% >11% Minimum of 12%

Invested Capital

* Before restructuring and other income and charges

** This outlook is as of May 3, 2005.

*** From the 12-month period ended 12/31/03 through 12/31/06

4

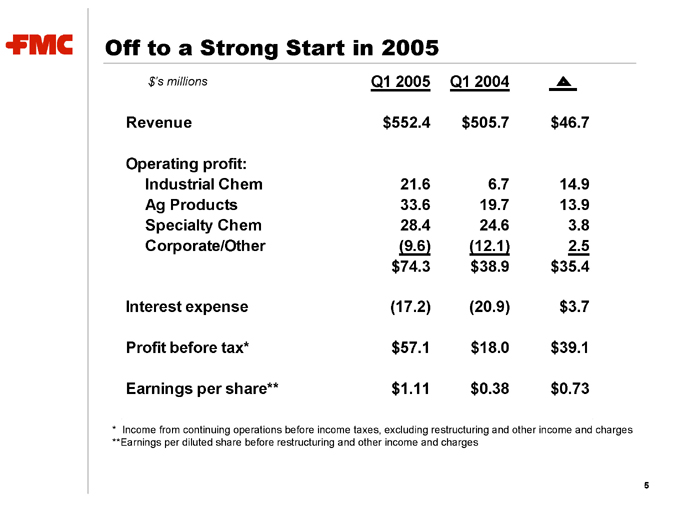

Off to a Strong Start in 2005

$’s millions Q1 2005 Q1 2004

Revenue $552.4 $ 505.7 $46.7

Operating profit:

Industrial Chem 21.6 6.7 14.9

Ag Products 33.6 19.7 13.9

Specialty Chem 28.4 24.6 3.8

Corporate/Other (9.6) (12.1) 2.5

$74.3 $38.9 $35.4

Interest expense (17.2) (20.9) $ 3.7

Profit before tax* $57.1 $18.0 $39.1

Earnings per share** $1.11 $ 0.38 $0.73

* Income from continuing operations before income taxes, excluding restructuring and other income and charges **Earnings per diluted share before restructuring and other income and charges

5

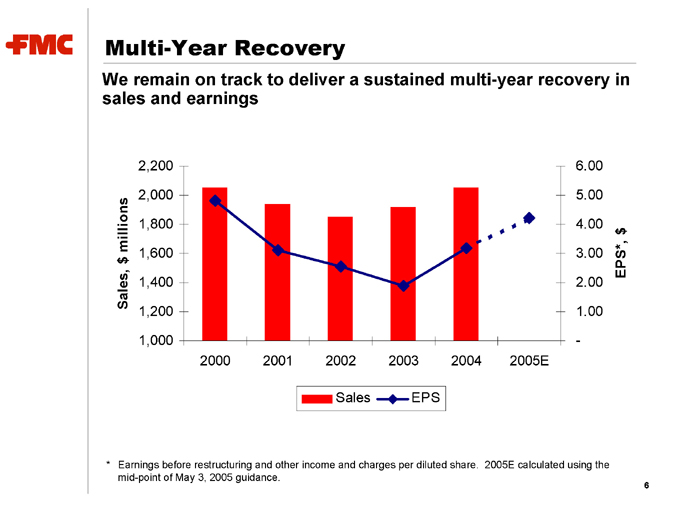

Multi-Year Recovery

We remain on track to deliver a sustained multi-year recovery in sales and earnings

Sales, $ millions

2,200

2,000

1,800

1,600 1,400 1,200

1,000

2000 2001 2002 2003 2004 2005E

6.00

5.00

4.00 3.00

2.00 1.00

EPS*, $

* Earnings before restructuring and other income and charges per diluted share. 2005E calculated using the mid-point of May 3, 2005 guidance.

6

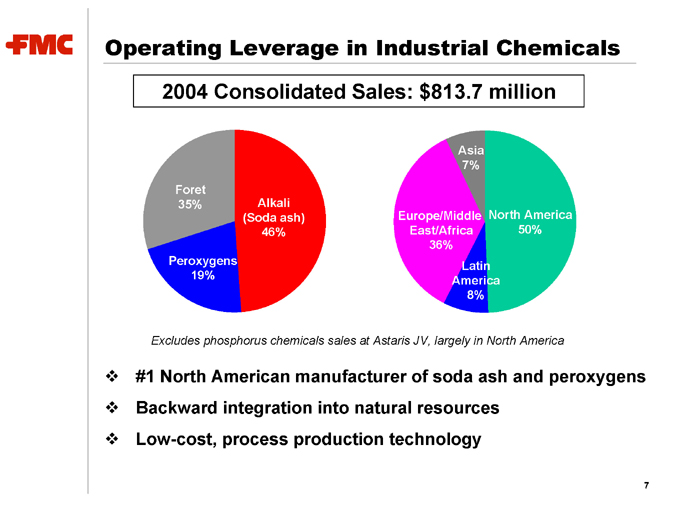

Operating Leverage in Industrial Chemicals

2004 Consolidated Sales: $813.7 million

Foret 35%

Peroxygens 19%

Alkali (Soda ash) 46%

Asia 7%

Europe/Middle East/Africa 36%

North America 50%

Latin America 8%

Excludes phosphorus chemicals sales at Astaris JV, largely in North America

#1 North American manufacturer of soda ash and peroxygens

Backward integration into natural resources

Low-cost, process production technology

7

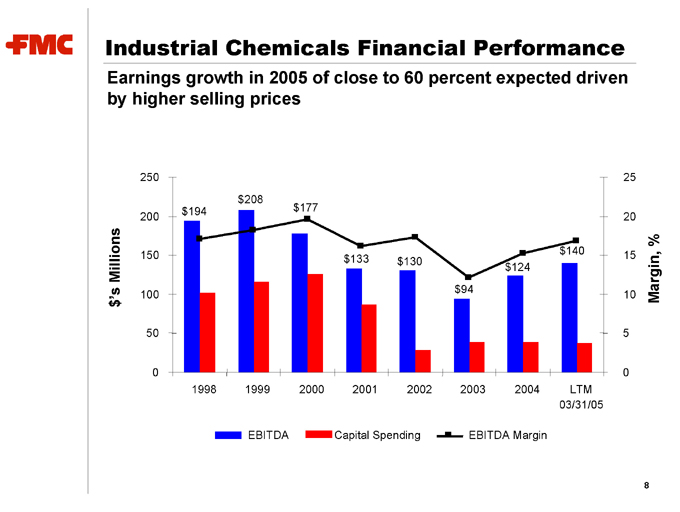

Industrial Chemicals Financial Performance

Earnings growth in 2005 of close to 60 percent expected driven by higher selling prices

$’s Millions

250

200

150

100

50

0

1998 1999 2000 2001 2002 2003 2004 LTM

03/31/05

EBITDA

Capital Spending

EBITDA Margin

Margin, %

25 20 15 10 5 0 $194 $208 $177 $133 $130 $94 $124 $140

8

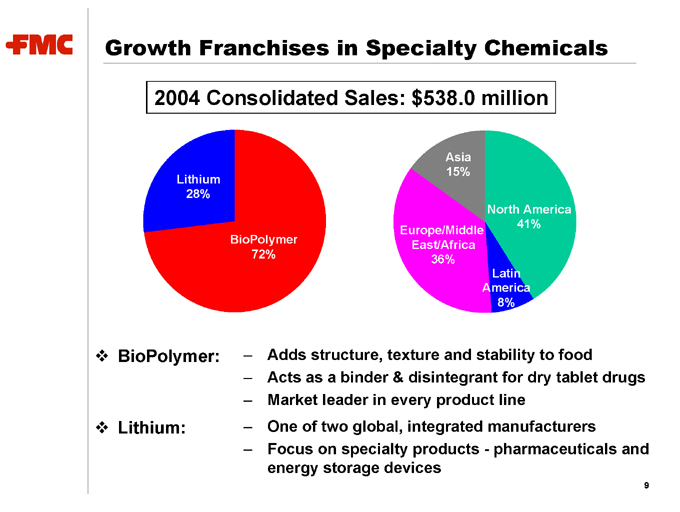

Growth Franchises in Specialty Chemicals

2004 Consolidated Sales: $538.0 million

Lithium 28%

BioPolymer 72%

Asia 15%

Europe/Middle East/Africa 36%

North America 41%

Latin America 8%

BioPolymer: Adds structure, texture and stability to food

Acts as a binder & disintegrant for dry tablet drugs

Market leader in every product line

Lithium: One of two global, integrated manufacturers

Focus on specialty products—pharmaceuticals and energy storage devices

9

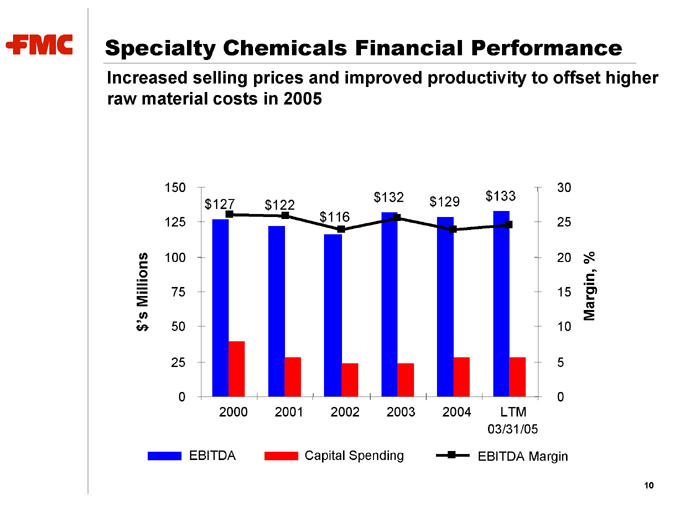

Specialty Chemicals Financial Performance

Increased selling prices and improved productivity to offset higher raw material costs in 2005

$’s Millions

150

125

100

75

50

25

0 $132 $129 $133 $127 $122 $116

2000 2001 2002 2003 2004 LTM

03/31/05

30

25

20 % Margin,

15

10

5

0

EBITDA

Capital Spending

EBITDA Margin

10

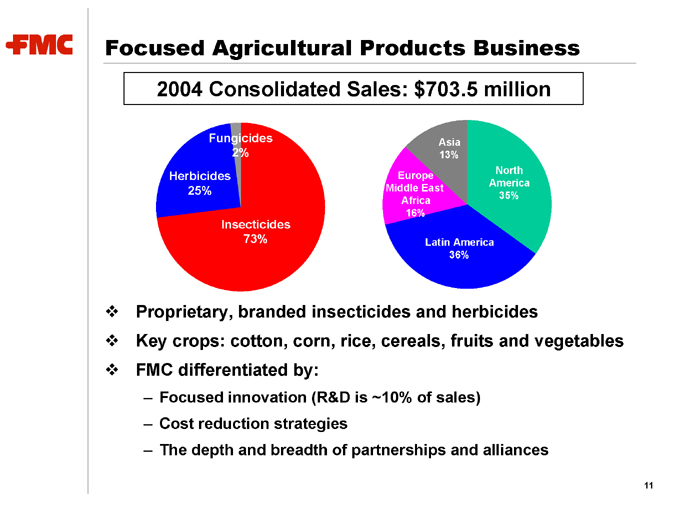

Focused Agricultural Products Business

2004 Consolidated Sales: $703.5 million

Fungicides 2%

Herbicides 25%

Insecticides 73%

Asia 13%

Europe Middle East Africa 16%

North America 35%

Latin America 36%

Proprietary, branded insecticides and herbicides

Key crops: cotton, corn, rice, cereals, fruits and vegetables FMC differentiated by:

Focused innovation (R&D is ~10% of sales)

Cost reduction strategies

The depth and breadth of partnerships and alliances

11

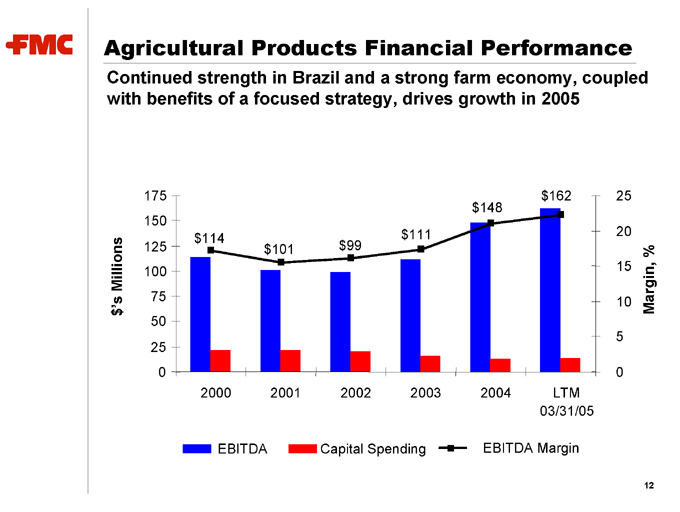

Agricultural Products Financial Performance

Continued strength in Brazil and a strong farm economy, coupled with benefits of a focused strategy, drives growth in 2005

$’s Millions

175

150

125

100

75

50 25 0 $114 $111 $101 $99 $162 $148

2000 2001 2002 2003 2004 LTM

03/31/05

25

20

15

Margin, %

10

5 0

EBITDA

Capital Spending

EBITDA Margin

12

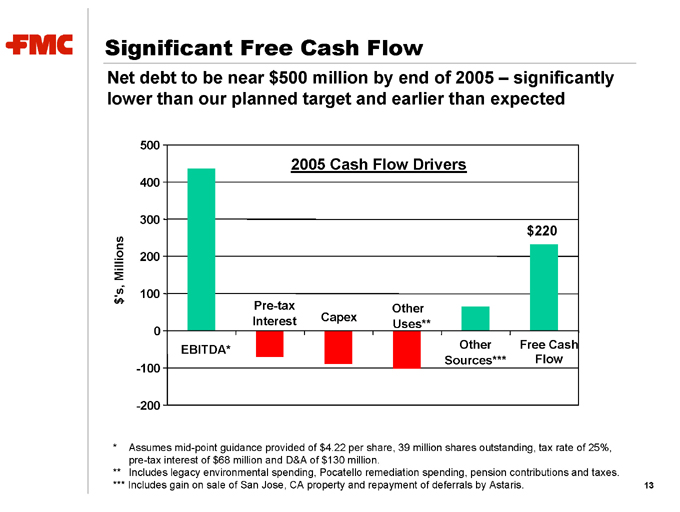

Significant Free Cash Flow

Net debt to be near $500 million by end of 2005 – significantly lower than our planned target and earlier than expected

$’s Millions

500

400

300

200

100

0 -100 -200

2005 Cash Flow Drivers

EBITDA*

Pre-tax Interest

Capex

Other Uses**

Other Sources*** Free Cash Flow

* Assumes mid-point guidance provided of $4.22 per share, 39 million shares outstanding, tax rate of 25%, pre-tax interest of $68 million and D&A of $130 million.

** Includes legacy environmental spending, Pocatello remediation spending, pension contributions and taxes.

*** Includes gain on sale of San Jose, CA property and repayment of deferrals by Astaris.

13

In Summary

Great businesses, each with EBITDA of at least $130 million Industrial Chemicals earnings only at mid-cycle in 2005 Steady growth in Specialty Chemicals and Ag Products Low capital expenditure requirements Substantial decline in unusual demands on cash flow Significant balance sheet deleveraging

14

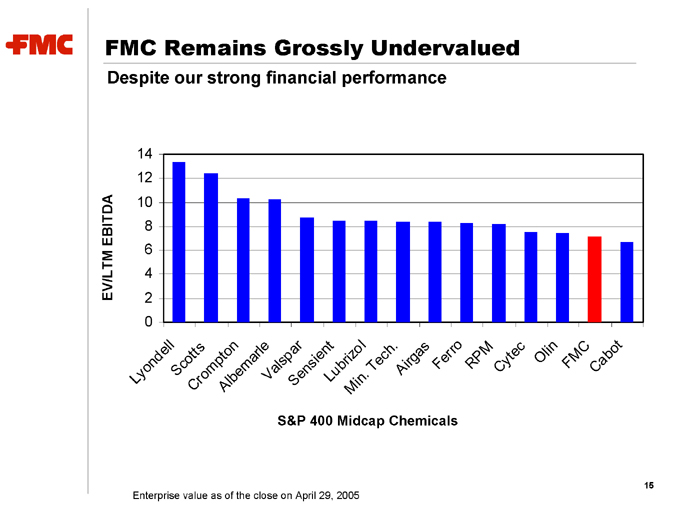

FMC Remains Grossly Undervalued

Despite our strong financial performance

14 12

10

8

6

4

2

0

EV/LTM EBITDA

Lyondell

Scotts

Crompton

Albemarle

Valspar

Sensient

Lubrizol

Min. Tech.

Airgas

Ferro RPM

Cytec

Olin

FMC

Cabot

S&P 400 Midcap Chemicals

Enterprise value as of the close on April 29, 2005

15

Disciplined Approach to Unlocking Value

Our long term objectives are focused on proactively unlocking value once financial flexibility is achieved

Maintain strategic and financial flexibility to invest in growth Actively manage the business portfolio to create value Return capital to shareholders in most efficient manner

16

FMC Corporation

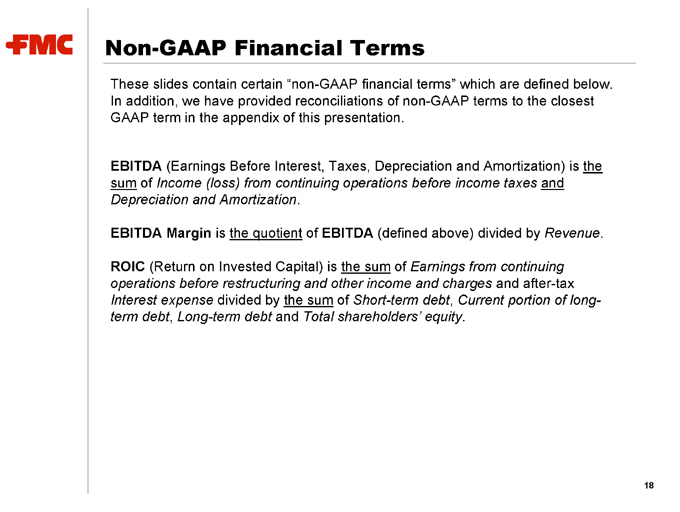

Non-GAAP Financial Terms

These slides contain certain “non-GAAP financial terms” which are defined below. In addition, we have provided reconciliations of non-GAAP terms to the closest GAAP term in the appendix of this presentation.

EBITDA (Earnings Before Interest, Taxes, Depreciation and Amortization) is the sum of Income (loss) from continuing operations before income taxes and Depreciation and Amortization.

EBITDA Margin is the quotient of EBITDA (defined above) divided by Revenue.

ROIC (Return on Invested Capital) is the sum of Earnings from continuing operations before restructuring and other income and charges and after-tax Interest expense divided by the sum of Short-term debt, Current portion of long-term debt, Long-term debt and Total shareholders’ equity.

18

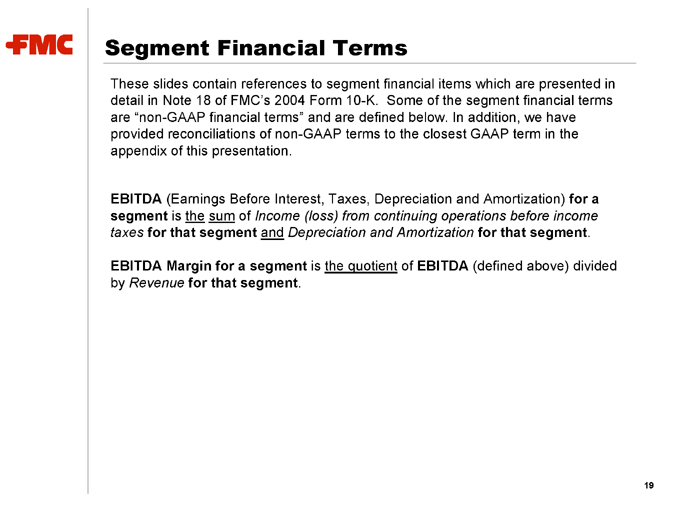

Segment Financial Terms

These slides contain references to segment financial items which are presented in detail in Note 18 of FMC’s 2004 Form 10-K. Some of the segment financial terms are “non-GAAP financial terms” and are defined below. In addition, we have provided reconciliations of non-GAAP terms to the closest GAAP term in the appendix of this presentation.

EBITDA (Earnings Before Interest, Taxes, Depreciation and Amortization) for a segment is the sum of Income (loss) from continuing operations before income taxes for that segment and Depreciation and Amortization for that segment.

EBITDA Margin for a segment is the quotient of EBITDA (defined above) divided by Revenue for that segment.

19

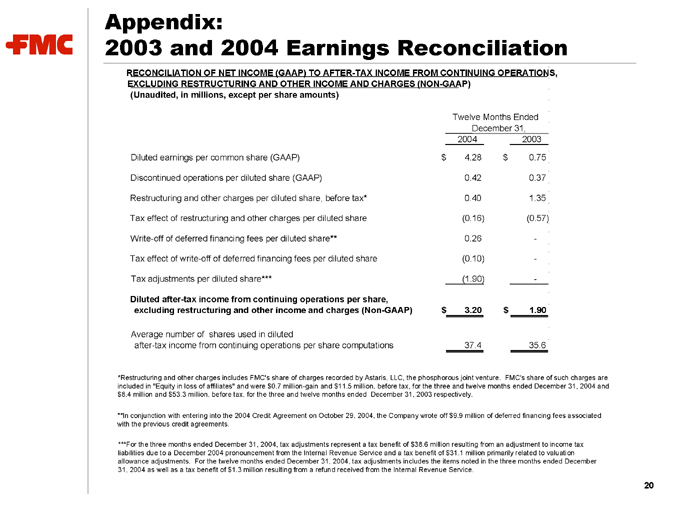

Appendix:

2003 and 2004 Earnings Reconciliation

RECONCILIATION OF NET INCOME (GAAP) TO AFTER-TAX INCOME FROM CONTINUING OPERATIONS, EXCLUDING RESTRUCTURING AND OTHER INCOME AND CHARGES (NON-GAAP) (Unaudited, in millions, except per share amounts)

Twelve Months Ended December 31,

2004 2003

Diluted earnings per common share (GAAP) $4.28 $0.75

Discontinued operations per diluted share (GAAP) 0.42 0.37

Restructuring and other charges per diluted share, before tax* 0.40 1.35

Tax effect of restructuring and other charges per diluted share (0.16) (0.57)

Write-off of deferred financing fees per diluted share** 0.26 -

Tax effect of write-off of deferred financing fees per diluted share (0.10) -

Tax adjustments per diluted share*** (1.90) -

Diluted after-tax income from continuing operations per share,

excluding restructuring and other income and charges (Non-GAAP) $3.20 $1.90

Average number of shares used in diluted

after-tax income from continuing operations per share computations 37.4 35.6

*Restructuring and other charges includes FMC’s share of charges recorded by Astaris, LLC, the phosphorous joint venture. FMC’s share of such charges are included in “Equity in loss of affiliates” and were $0.7 million-gain and $11.5 million, before tax, for the three and twelve months ended December 31, 2004 and $8.4 million and $53.3 million, before tax, for the three and twelve months ended December 31, 2003 respectively.

**In conjunction with entering into the 2004 Credit Agreement on October 29, 2004, the Company wrote off $9.9 million of deferred financing fees associated with the previous credit agreements.

***For the three months ended December 31, 2004, tax adjustments represent a tax benefit of $38.6 million resulting from an adjustment to income tax liabilities due to a December 2004 pronouncement from the Internal Revenue Service and a tax benefit of $31.1 million primarily related to valuation allowance adjustments. For the twelve months ended December 31, 2004, tax adjustments includes the items noted in the three months ended December 31, 2004 as well as a tax benefit of $1.3 million resulting from a refund received from the Internal Revenue Service.

20

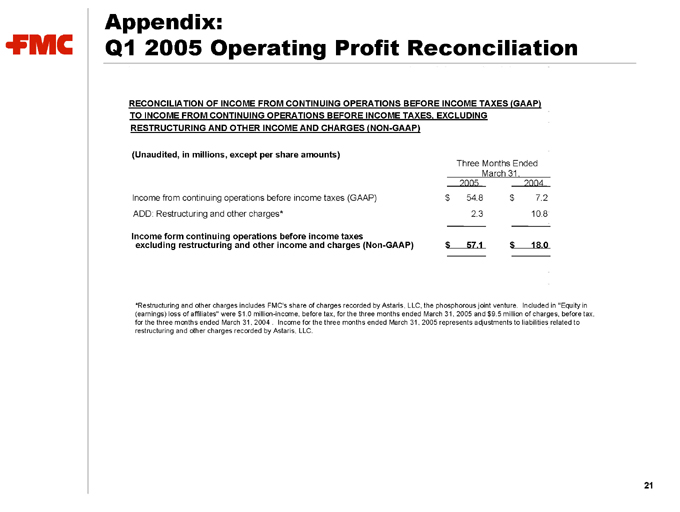

Appendix:

Q1 2005 Operating Profit Reconciliation

RECONCILIATION OF INCOME FROM CONTINUING OPERATIONS BEFORE INCOME TAXES (GAAP) TO INCOME FROM CONTINUING OPERATIONS BEFORE INCOME TAXES, EXCLUDING

RESTRUCTURING AND OTHER INCOME AND CHARGES (NON-GAAP)

(Unaudited, in millions, except per share amounts)

Three Months Ended

March 31,

2005 2004

Income from continuing operations before income taxes (GAAP) $ 54.8 $ 7.2

ADD: Restructuring and other charges* 2.3 10.8

Income form continuing operations before income taxes

excluding restructuring and other income and charges (Non-GAAP) $ 57.1 $ 18.0

*Restructuring and other charges includes FMC’s share of charges recorded by Astaris, LLC, the phosphorous joint venture. Included in “Equity in (earnings) loss of affiliates” were $1.0 million-income, before tax, for the three months ended March 31, 2005. and $9.5 million of charges, before tax, for the three months ended March 31, 2004 . Income for the three months ended March 31, 2005 represents adjustments to liabilities related to restructuring and other charges recorded by Astaris, LLC.

21

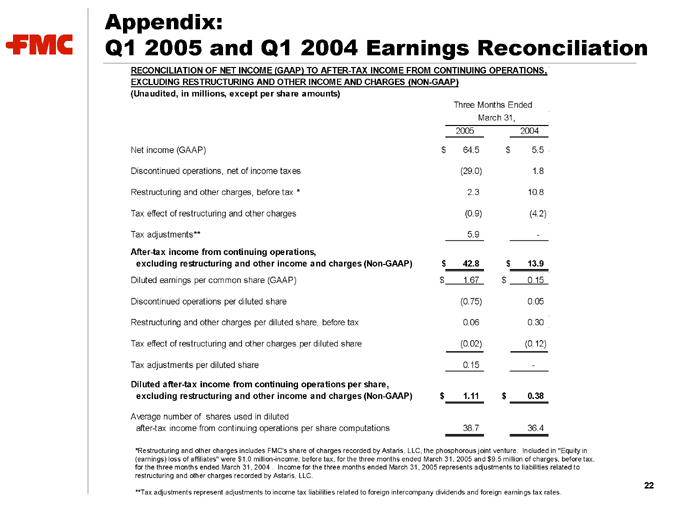

Appendix:

Q1 2005 and Q1 2004 Earnings Reconciliation

RECONCILIATION OF NET INCOME (GAAP) TO AFTER-TAX INCOME FROM CONTINUING OPERATIONS, EXCLUDING RESTRUCTURING AND OTHER INCOME AND CHARGES (NON-GAAP) (Unaudited, in millions, except per share amounts)

Three Months Ended

March 31,

2005 2004

Net income (GAAP) $64.5 $ 5.5

Discontinued operations, net of income taxes (29.0) 1.8

Restructuring and other charges, before tax * 2.3 10.8

Tax effect of restructuring and other charges (0.9) (4.2)

Tax adjustments** 5.9 -

After-tax income from continuing operations,

excluding restructuring and other income and charges (Non-GAAP) $42.8 $ 13.9

Diluted earnings per common share (GAAP) $1.67 $0.15

Discontinued operations per diluted share (0.75) 0.05

Restructuring and other charges per diluted share, before tax 0.06 0.30

Tax effect of restructuring and other charges per diluted share (0.02) (0.12)

Tax adjustments per diluted share 0.15 -

Diluted after-tax income from continuing operations per share,

excluding restructuring and other income and charges (Non-GAAP) $1.11 $0.38

Average number of shares used in diluted

after-tax income from continuing operations per share computations 38.7 36.4

*Restructuring and other charges includes FMC’s share of charges recorded by Astaris, LLC, the phosphorous joint venture. Included in “Equity in (earnings) loss of affiliates” were $1.0 million-income, before tax, for the three months ended March 31, 2005 and $9.5 million of charges, before tax, for the three months ended March 31, 2004 . Income for the three months ended March 31, 2005 represents adjustments to liabilities related to restructuring and other charges recorded by Astaris, LLC.

22

**Tax adjustments represent adjustments to income tax liabilities related to foreign intercompany dividends and foreign earnings tax rates.

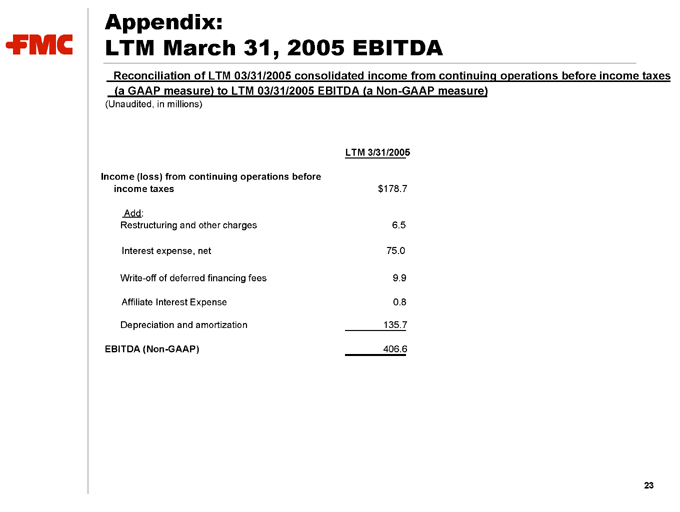

Appendix:

LTM March 31, 2005 EBITDA

Reconciliation of LTM 03/31/2005 consolidated income from continuing operations before income taxes (a GAAP measure) to LTM 03/31/2005 EBITDA (a Non-GAAP measure)

(Unaudited, in millions)

LTM 3/31/2005

Income (loss) from continuing operations before

income taxes $ 178.7

Add:

Restructuring and other charges 6.5

Interest expense, net 75.0

Write-off of deferred financing fees 9.9

Affiliate Interest Expense 0.8

Depreciation and amortization 135.7

EBITDA (Non-GAAP) 406.6

23

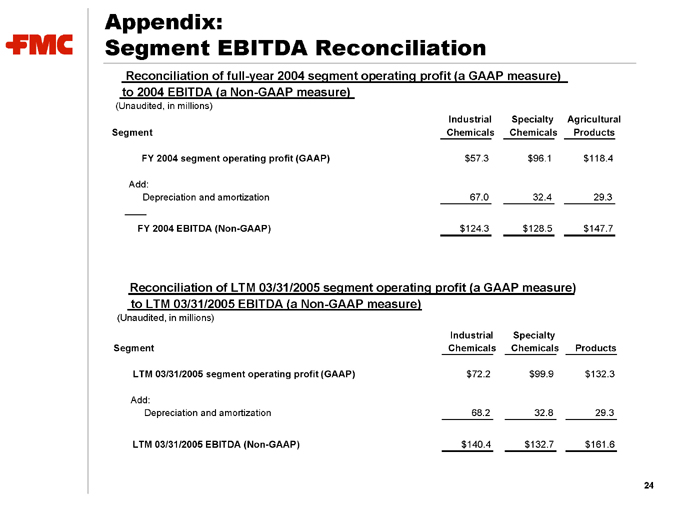

Appendix:

Segment EBITDA Reconciliation

Reconciliation of full-year 2004 segment operating profit (a GAAP measure) to 2004 EBITDA (a Non-GAAP measure)

(Unaudited, in millions)

Industrial Specialty Agricultural

Segment Chemicals Chemicals Products

FY 2004 segment operating profit (GAAP) $ 57.3 $ 96.1 $ 118.4

Add:

Depreciation and amortization 67.0 32.4 29.3

FY 2004 EBITDA (Non-GAAP) $ 124.3 $ 128.5 $ 147.7

Reconciliation of LTM 03/31/2005 segment operating profit (a GAAP measure) to LTM 03/31/2005 EBITDA (a Non-GAAP measure)

(Unaudited, in millions)

Industrial Specialty

Segment Chemicals Chemicals Products

LTM 03/31/2005 segment operating profit (GAAP) $ 72.2 $ 99.9 $ 132.3

Add:

Depreciation and amortization 68.2 32.8 29.3

LTM 03/31/2005 EBITDA (Non-GAAP) $ 140.4 $ 132.7 $ 161.6

24

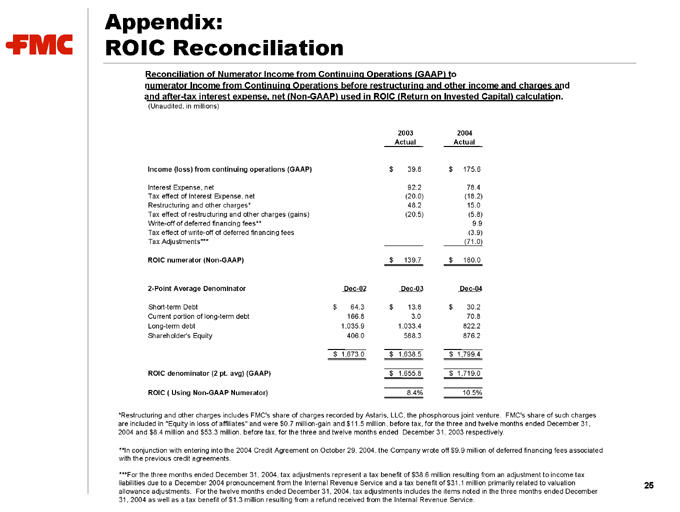

Appendix:

ROIC Reconciliation

Reconciliation of Numerator Income from Continuing Operations (GAAP) to numerator Income from Continuing Operations before restructuring and other income and charges and and after-tax interest expense, net (Non-GAAP) used in ROIC (Return on Invested Capital) calculation.

(Unaudited, in millions)

2003 2004

Actual Actual

Income (loss) from continuing operations (GAAP) $ 39.8 $ 175.6

Interest Expense, net 92.2 78.4

Tax effect of Interest Expense, net (20.0) (18.2)

Restructuring and other charges* 48.2 15.0

Tax effect of restructuring and other charges (gains) (20.5) (5.8)

Write-off of deferred financing fees** 9.9

Tax effect of write-off of deferred financing fees (3.9)

Tax Adjustments*** (71.0)

ROIC numerator (Non-GAAP) $ 139.7 $ 180.0

2-Point Average Denominator Dec-02 Dec-03 Dec-04

Short-term Debt $ 64.3 $ 13.8 $ 30.2

Current portion of long-term debt 166.8 3.0 70.8

Long-term debt 1,035.9 1,033.4 822.2

Shareholder’s Equity 406.0 588.3 876.2

$ 1,673.0 $ 1,638.5 $ 1,799.4

ROIC denominator (2 pt. avg) (GAAP) $ 1,655.8 $ 1,719.0

ROIC ( Using Non-GAAP Numerator) 8.4% 10.5%

*Restructuring and other charges includes FMC’s share of charges recorded by Astaris, LLC, the phosphorous joint venture. FMC’s share of such charges are included in “Equity in loss of affiliates” and were $0.7 million-gain and $11.5 million, before tax, for the three and twelve months ended December 31, 2004 and $8.4 million and $53.3 million, before tax, for the three and twelve months ended December 31, 2003 respectively.

**In conjunction with entering into the 2004 Credit Agreement on October 29, 2004, the Company wrote off $9.9 million of deferred financing fees associated with the previous credit agreements.

***For the three months ended December 31, 2004, tax adjustments represent a tax benefit of $38.6 million resulting from an adjustment to income tax liabilities due to a December 2004 pronouncement from the Internal Revenue Service and a tax benefit of $31.1 million primarily related to valuation allowance adjustments. For the twelve months ended December 31, 2004, tax adjustments includes the items noted in the three months ended December 31, 2004 as well as a tax benefit of $1.3 million resulting from a refund received from the Internal Revenue Service.

25

FMC Corporation