Exhibit 99.1

FMC Corporation

Bear Stearns Fourteenth Annual Global Credit Conference

May 17, 2005

Thomas C. Deas, Jr. Vice President & Treasurer

Disclaimer

Safe Harbor Statement under the Private Securities Litigation Reform Act of 1995

These slides and the accompanying presentation contain “forward-looking statements” that represent management’s best judgment as of the date hereof based on information currently available. Actual results of the Company may differ materially from those contained in the forward-looking statements.

Additional information concerning factors that may cause results to differ materially from those in the forward-looking statements is contained in the Company’s periodic reports filed under the Securities Exchange Act of 1934, as amended.

The Company undertakes no obligation to update or revise these forward-looking statements to reflect new events or uncertainties.

Non-GAAP Financial Terms

These slides contain certain “non-GAAP financial terms” which are defined in the appendix. In addition, we have provided reconciliations of non-GAAP terms to the closest GAAP term in the appendix.

1

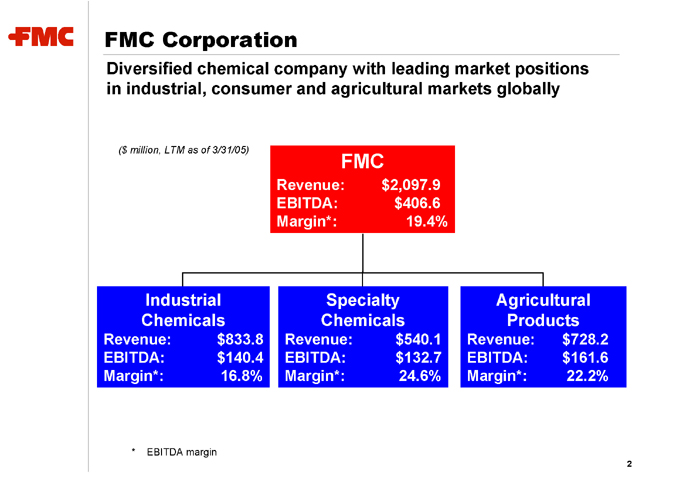

FMC Corporation

Diversified chemical company with leading market positions in industrial, consumer and agricultural markets globally

($ million, LTM as of 3/31/05)

FMC

Revenue: $2,097.9 EBITDA: $406.6 Margin*: 19.4%

Industrial Chemicals

Revenue: $833.8 EBITDA: $140.4 Margin*: 16.8%

Specialty Chemicals

Revenue: $540.1 EBITDA: $132.7 Margin*: 24.6%

Agricultural Products

Revenue: $728.2 EBITDA: $161.6 Margin*: 22.2%

* EBITDA margin

2

Company Strengths

Leading market positions

Global presence

Diversified business mix and high-quality customer base Diversified and integrated cost structure Focused R&D and strong applications expertise Commitment to strong credit profile

3

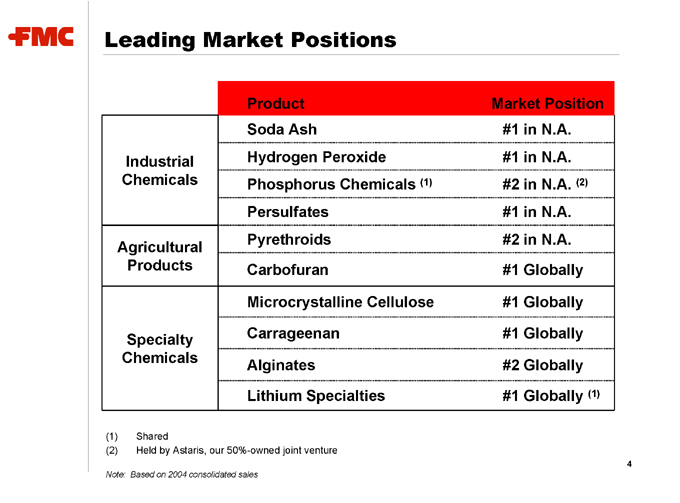

Leading Market Positions

Industrial Chemicals

Agricultural Products

Specialty Chemicals

Product Market Position

Soda Ash #1 in N.A.

Hydrogen Peroxide #1 in N.A.

Phosphorus Chemicals (1) #2 in N.A. (2)

Persulfates #1 in N.A.

Pyrethroids #2 in N.A.

Carbofuran #1 Globally

Microcrystalline Cellulose #1 Globally

Carrageenan #1 Globally

Alginates #2 Globally

Lithium Specialties #1 Globally (1)

(1) Shared

(2) Held by Astaris, our 50%-owned joint venture

Note: Based on 2004 consolidated sales

4

Leading Market Positions

Industrial Chemicals

Agricultural Products

Specialty Chemicals

Product Market Position

Soda Ash #1 in N.A.

Hydrogen Peroxide #1 in N.A.

Phosphorus Chemicals (1) #2 in N.A. (2)

Persulfates #1 in N.A.

Pyrethroids #2 in N.A.

Carbofuran #1 Globally

Microcrystalline Cellulose #1 Globally

Carrageenan #1 Globally

Alginates #2 Globally

Lithium Specialties #1 Globally (1)

(1) Shared

(2) Held by Astaris, our 50%-owned joint venture

Note: Based on 2004 consolidated sales

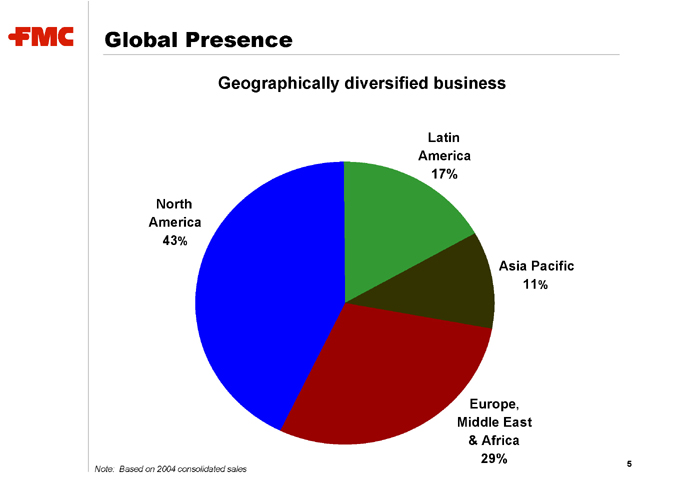

Global Presence

Geographically diversified business

North America

43 %

Latin America 17%

Asia Pacific

11 %

Europe, Middle East & Africa 29%

Note: Based on 2004 consolidated sales

5

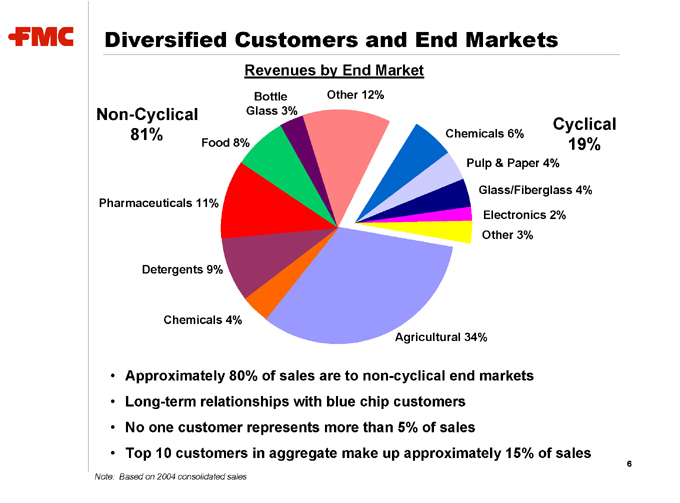

Diversified Customers and End Markets

Revenues by End Market

Non-Cyclical 81%

Other 12%

Bottle Glass 3%

Food 8%

Pharmaceuticals 11%

Detergents 9%

Chemicals 4%

Agricultural 34%

Other 3%

Electronics 2%

Glass/Fiberglass 4%

Pulp & Paper 4%

Chemicals 6%

Cyclical 19%

Approximately 80% of sales are to non-cyclical end markets Long-term relationships with blue chip customers No one customer represents more than 5% of sales

Top 10 customers in aggregate make up approximately 15% of sales

Note: Based on 2004 consolidated sales

6

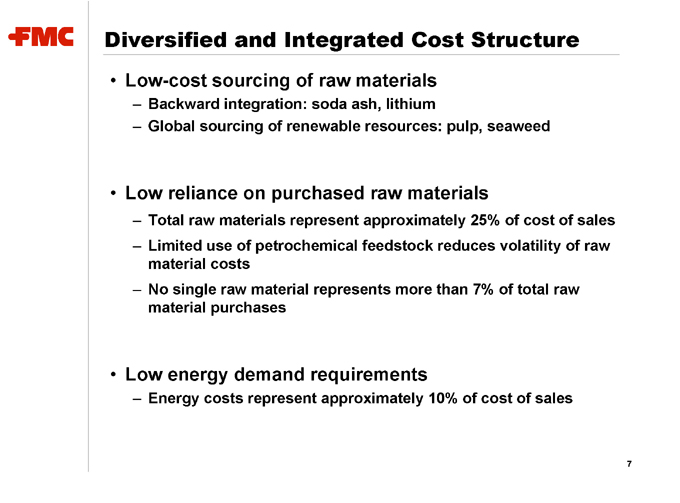

Diversified and Integrated Cost Structure

Low-cost sourcing of raw materials

Backward integration: soda ash, lithium

Global sourcing of renewable resources: pulp, seaweed

Low reliance on purchased raw materials

Total raw materials represent approximately 25% of cost of sales

Limited use of petrochemical feedstock reduces volatility of raw material costs

No single raw material represents more than 7% of total raw material purchases

Low energy demand requirements

Energy costs represent approximately 10% of cost of sales

7

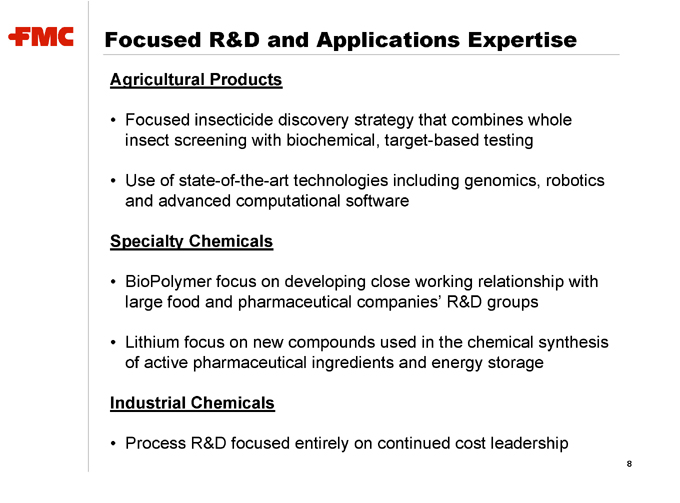

Focused R&D and Applications Expertise

Agricultural Products

Focused insecticide discovery strategy that combines whole insect screening with biochemical, target-based testing

Use of state-of-the-art technologies including genomics, robotics and advanced computational software

Specialty Chemicals

BioPolymer focus on developing close working relationship with large food and pharmaceutical companies’ R&D groups

Lithium focus on new compounds used in the chemical synthesis of active pharmaceutical ingredients and energy storage

Industrial Chemicals

Process R&D focused entirely on continued cost leadership

8

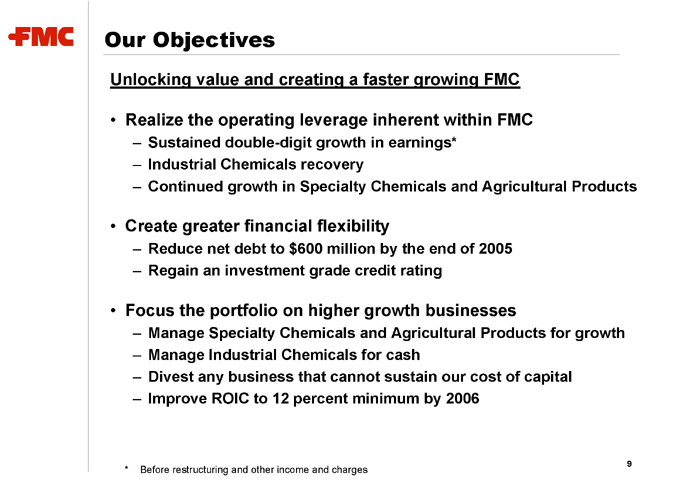

Our Objectives

Unlocking value and creating a faster growing FMC

Realize the operating leverage inherent within FMC

Sustained double-digit growth in earnings*

Industrial Chemicals recovery

Continued growth in Specialty Chemicals and Agricultural Products

Create greater financial flexibility

Reduce net debt to $600 million by the end of 2005

Regain an investment grade credit rating

Focus the portfolio on higher growth businesses

Manage Specialty Chemicals and Agricultural Products for growth

Manage Industrial Chemicals for cash

Divest any business that cannot sustain our cost of capital

Improve ROIC to 12 percent minimum by 2006

Before restructuring and other income and charges

9

Industrial Chemicals

10

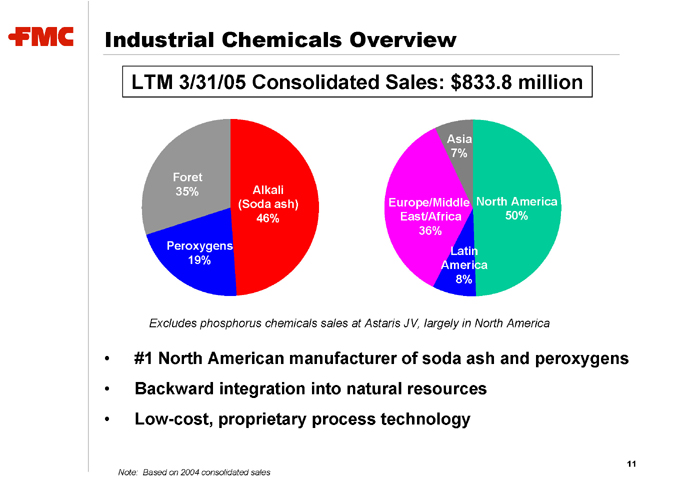

Industrial Chemicals Overview

LTM 3/31/05 Consolidated Sales: $833.8 million

Foret 35%

Peroxygens 19%

Alkali (Soda ash) 46%

Asia 7%

Europe/Middle East/Africa 36%

Latin America 8%

North America 50%

Excludes phosphorus chemicals sales at Astaris JV, largely in North America

#1 North American manufacturer of soda ash and peroxygens

Backward integration into natural resources

Low-cost, proprietary process technology

Note: Based on 2004 consolidated sales

11

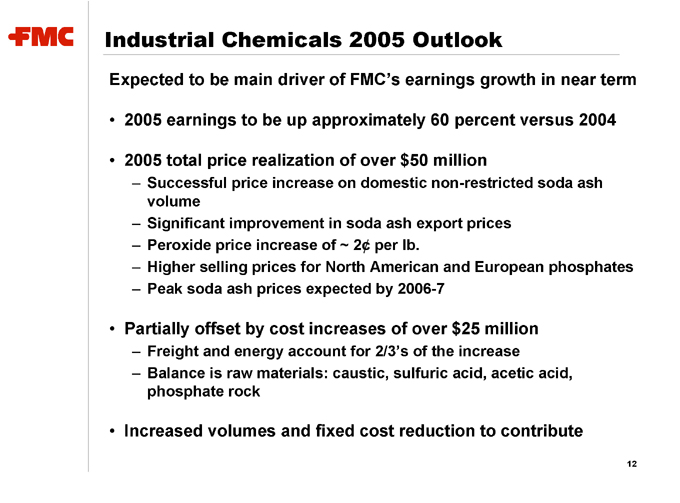

Industrial Chemicals 2005 Outlook

Expected to be main driver of FMC’s earnings growth in near term

2005 earnings to be up approximately 60 percent versus 2004

2005 total price realization of over $50 million

Successful price increase on domestic non-restricted soda ash volume

Significant improvement in soda ash export prices

Peroxide price increase of ~ 2¢ per lb.

Higher selling prices for North American and European phosphates

Peak soda ash prices expected by 2006-7

Partially offset by cost increases of over $25 million

Freight and energy account for 2/3’s of the increase

Balance is raw materials: caustic, sulfuric acid, acetic acid, phosphate rock

Increased volumes and fixed cost reduction to contribute

12

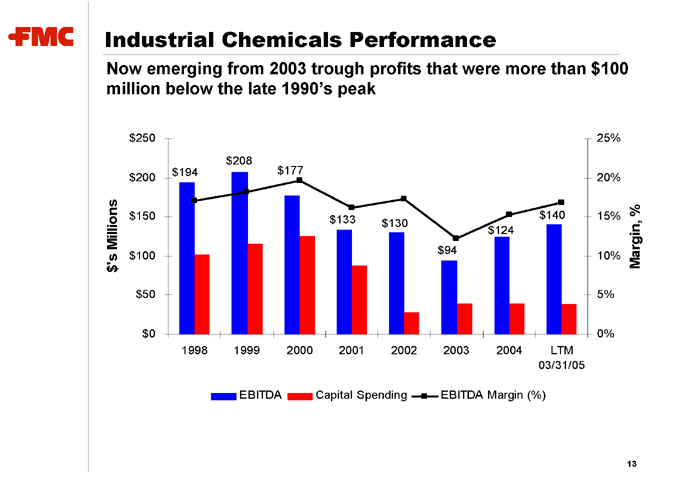

13

Industrial Chemicals Performance

Now emerging from 2003 trough profits that were more than $100 million below the late 1990’s peak

$’s Millions $250 $200 $150 $100 $50 $0 $194 $208 $177 $133 $130 $94 $124 $140

1998 1999 2000 2001 2002 2003 2004 LTM

03/31/05

EBITDA

Capital Spending

EBITDA Margin (%)

Margin, %

25% 20% 15% 10% 5% 0%

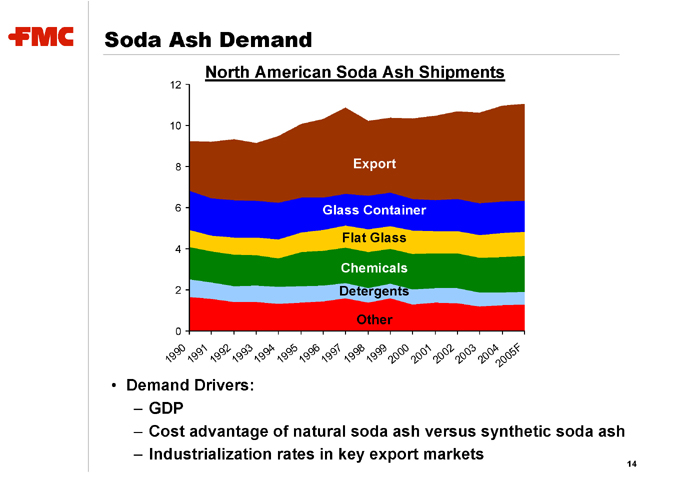

Soda Ash Demand

North American Soda Ash Shipments

Demand Drivers:

GDP

Cost advantage of natural soda ash versus synthetic soda ash

Industrialization rates in key export markets

14

Export

Glass Container

Flat Glass

Chemicals

Detergents

Other

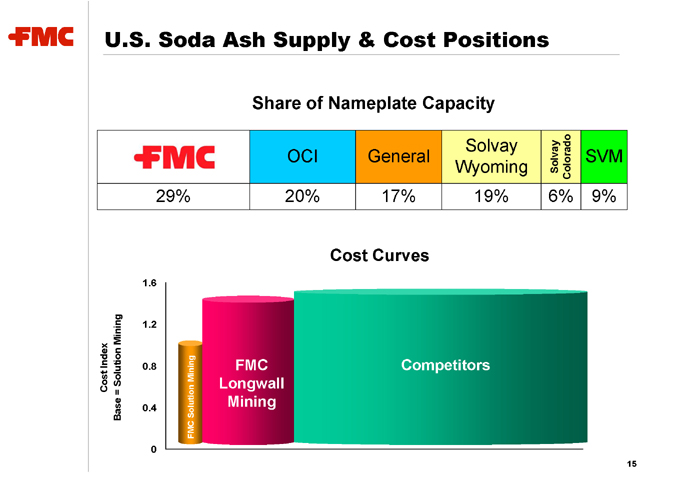

U.S. Soda Ash Supply & Cost Positions

Share of Nameplate Capacity

OCI

General

Solvay Wyoming

Solvay Colorado

SVM

29% 20% 17% 19% 6% 9%

Cost Curves

Cost Index Base = Solution Mining

1.6 1.2 0.8 0.4 0

FMC Solution Mining

FMC Longwall Mining

Competitors

15

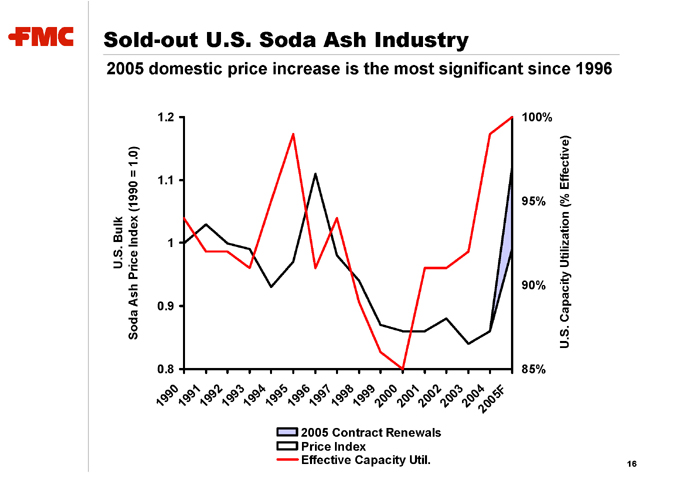

Sold-out U.S. Soda Ash Industry

2005 domestic price increase is the most significant since 1996

U.S. Bulk

Soda Ash Price Index (1990 = 1.0)

1.2 1.1 1 0.9 0.8

1990 19

91

1992 1993 1994 1995 1996 1997

1998 1999

2000

2001 2002

2003 2004

2005F

2005 Contract Renewals Price Index Effective Capacity Util.

100% 95% 90% 85%

U.S. Capacity Utilization (% Effective)

16

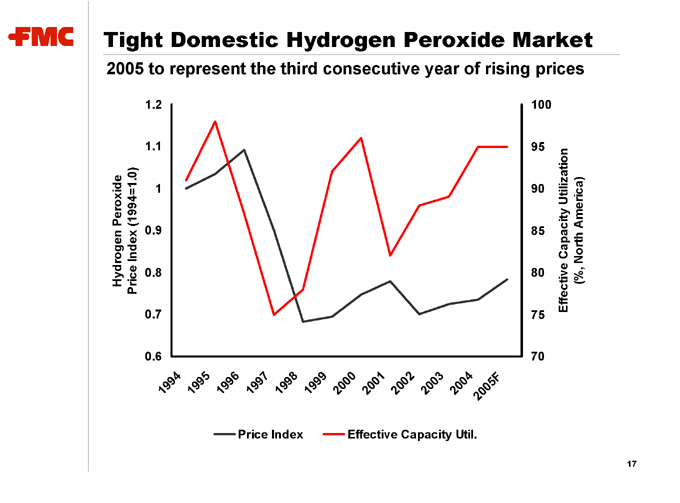

Tight Domestic Hydrogen Peroxide Market

2005 to represent the third consecutive year of rising prices

Hydrogen Peroxide Price Index (1994=1.0)

1.2 1.1 1 0.9 0.8 0.7 0.6

1994 1995

1996 1997

1998

1999

2000

2001

2002 2003

2004

2005F

Price Index

Effective Capacity Util.

100 95 90 85 80 75 70

Effective Capacity Utilization (%, North America)

17

Specialty Chemicals

18

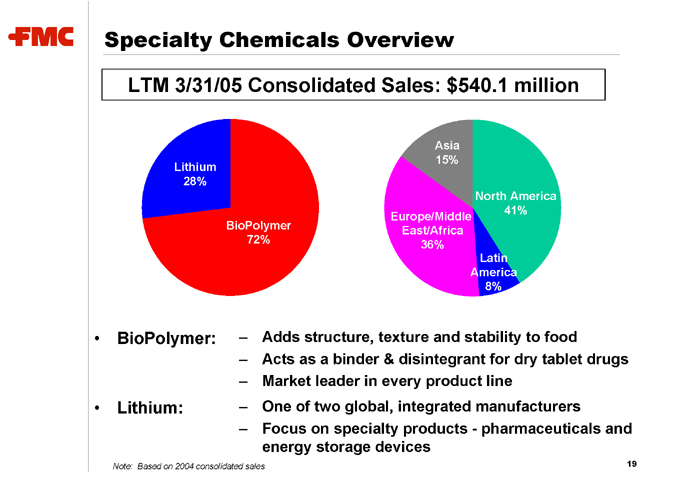

Specialty Chemicals Overview

LTM 3/31/05 Consolidated Sales: $540.1 million

Lithium 28%

BioPolymer 72%

Asia 15%

Europe/Middle East/Africa 36%

North America 41%

Latin America 8%

BioPolymer: – Adds structure, texture and stability to food

Acts as a binder & disintegrant for dry tablet drugs

Market leader in every product line

Lithium: – One of two global, integrated manufacturers

Focus on specialty products - pharmaceuticals and energy storage devices

Note: Based on 2004 consolidated sales

19

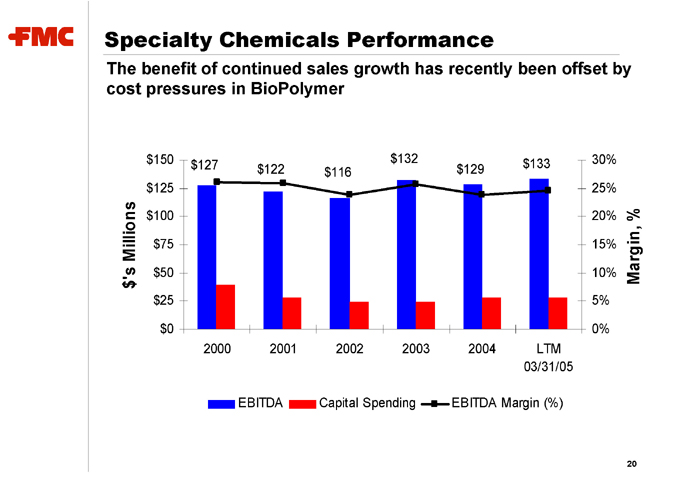

Specialty Chemicals Performance

The benefit of continued sales growth has recently been offset by cost pressures in BioPolymer

$’s Millions $150

$125 $100

$75

$50 $25

$0

2000 2001 2002 2003 2004 LTM

03/31/05

EBITDA Capital Spending EBITDA Margin (%)

$127 $122 $116 $132 $129 $133

30%

25% 20%

15%

10% 5%

0%

Margin, %

20

Specialty Chemicals 2005 Outlook

Expected to be the long-term driver of top- and bottom-line growth

2005 revenue growth in mid-single digits

Strong organic growth in BioPolymer end-markets of 3-6% per year

Focus on lithium specialty markets growing at 4 to >10% per year

Earnings growth rate in excess of revenue growth

Productivity improvements, higher volume and increased selling prices to drive margin expansion in 2005

Raw materials to remain stable versus 2004 and improve thereafter

Promising new products for the future

Oral-dosage-form technologies

Functional food ingredients

Fine chemistry applications of lithium

21

Agricultural Products

22

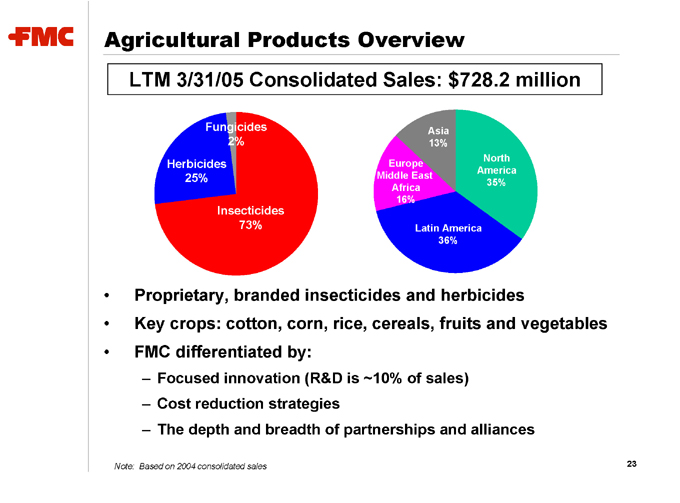

Agricultural Products Overview

LTM 3/31/05 Consolidated Sales: $728.2 million

Fungicides 2%

Herbicides 25%

Insecticides 73%

Asia 13%

Europe Middle East Africa 16%

Latin America 36%

North America 35%

Proprietary, branded insecticides and herbicides

Key crops: cotton, corn, rice, cereals, fruits and vegetables

FMC differentiated by:

Focused innovation (R&D is ~10% of sales)

Cost reduction strategies

The depth and breadth of partnerships and alliances

Note: Based on 2004 consolidated sales

23

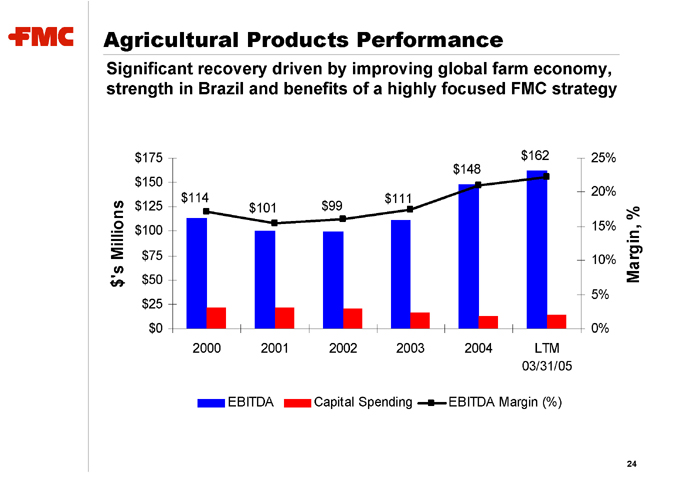

Agricultural Products Performance

Significant recovery driven by improving global farm economy, strength in Brazil and benefits of a highly focused FMC strategy

$’s Millions $175 $150 $125 $100 $75 $50 $25 $0

2000 2001 2002 2003 2004 LTM

03/31/05

Margin, %

25% 20% 15% 10% 5% 0% $114 $101 $99 $111 $148 $162

EBITDA

Capital Spending

EBITDA Margin (%)

24

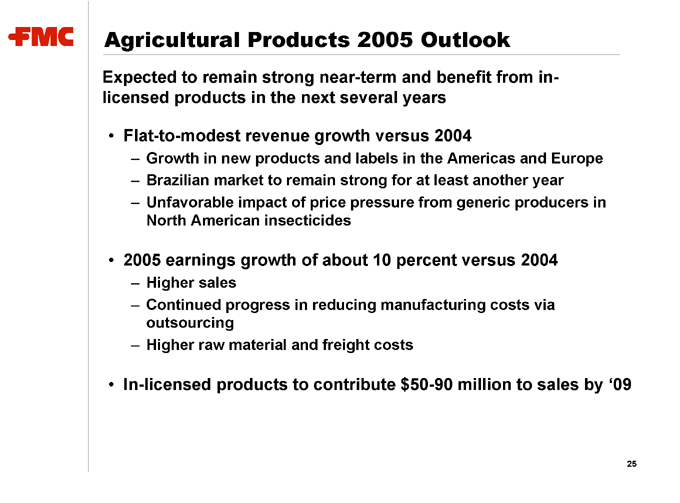

Agricultural Products 2005 Outlook

Expected to remain strong near-term and benefit from in-licensed products in the next several years

Flat-to-modest revenue growth versus 2004

Growth in new products and labels in the Americas and Europe

Brazilian market to remain strong for at least another year

Unfavorable impact of price pressure from generic producers in North American insecticides

2005 earnings growth of about 10 percent versus 2004

Higher sales

Continued progress in reducing manufacturing costs via outsourcing

Higher raw material and freight costs

In-licensed products to contribute $50-90 million to sales by ‘09

25

Financial Overview

26

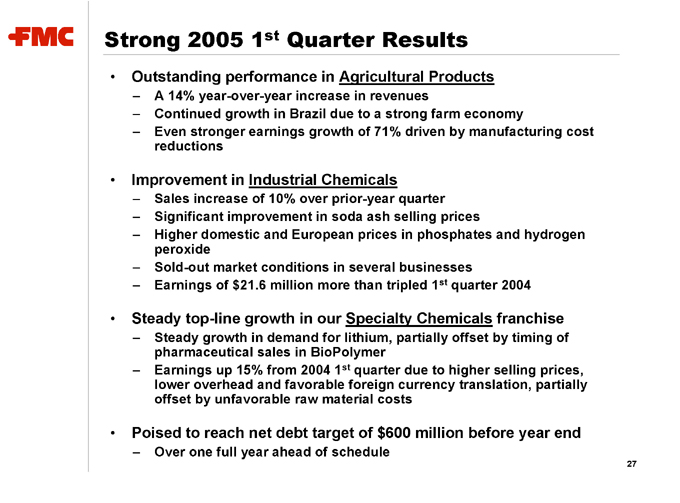

Strong 2005 1st Quarter Results

Outstanding performance in Agricultural Products

A 14% year-over-year increase in revenues

Continued growth in Brazil due to a strong farm economy

Even stronger earnings growth of 71% driven by manufacturing cost reductions

Improvement in Industrial Chemicals

Sales increase of 10% over prior-year quarter

Significant improvement in soda ash selling prices

Higher domestic and European prices in phosphates and hydrogen peroxide

Sold-out market conditions in several businesses

Earnings of $21.6 million more than tripled 1st quarter 2004

Steady top-line growth in our Specialty Chemicals franchise

Steady growth in demand for lithium, partially offset by timing of pharmaceutical sales in BioPolymer

Earnings up 15% from 2004 1st quarter due to higher selling prices, lower overhead and favorable foreign currency translation, partially offset by unfavorable raw material costs

Poised to reach net debt target of $600 million before year end

Over one full year ahead of schedule

27

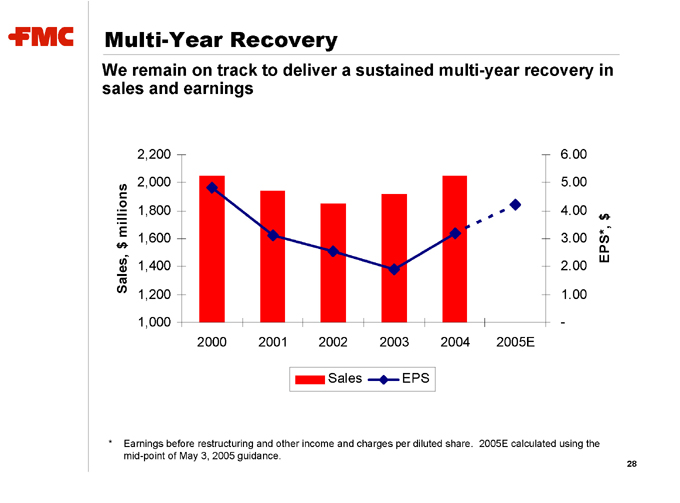

Multi-Year Recovery

We remain on track to deliver a sustained multi-year recovery in sales and earnings

Sales, $ millions

2,200 2,000

1,800 1,600 1,400

1,200 1,000

2000 2001 2002 2003 2004 2005E

Sales

EPS

6.00 5.00

4.00 3.00 2.00

1.00 -

EPS*, $

* Earnings before restructuring and other income and charges per diluted share. 2005E calculated using the mid-point of May 3, 2005 guidance.

28

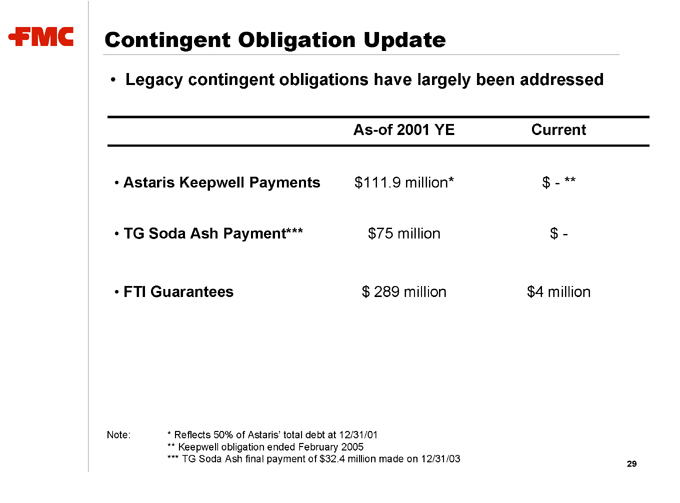

Contingent Obligation Update

Legacy contingent obligations have largely been addressed

As-of 2001 YE Current

Astaris Keepwell Payments $111.9 million* $—**

TG Soda Ash Payment*** $75 million $ -

FTI Guarantees $ 289 million $4 million

Note: * Reflects 50% of Astaris’ total debt at 12/31/01 ** Keepwell obligation ended February 2005

*** TG Soda Ash final payment of $32.4 million made on 12/31/03

29

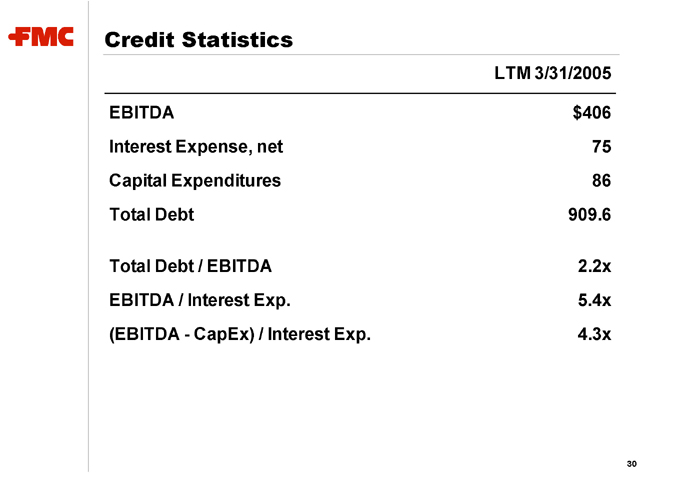

Credit Statistics

LTM 3/31/2005

EBITDA $406

Interest Expense, net 75

Capital Expenditures 86

Total Debt 909.6

Total Debt / EBITDA 2.2x

EBITDA / Interest Exp. 5.4x

(EBITDA - CapEx) / Interest Exp. 4.3x

30

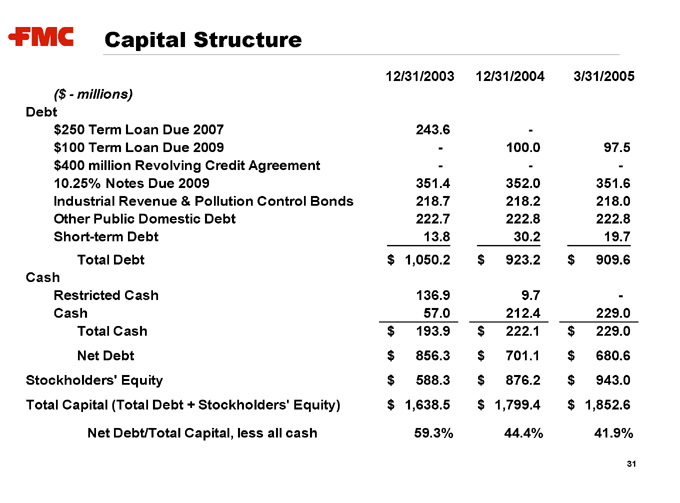

Capital Structure

12/31/2003 12/31/2004 3/31/2005

($ - millions)

Debt

$250 Term Loan Due 2007 243.6 -

$100 Term Loan Due 2009 - 100.0 97.5

$400 million Revolving Credit Agreement - - -

10.25% Notes Due 2009 351.4 352.0 351.6

Industrial Revenue & Pollution Control Bonds 218.7 218.2 218.0

Other Public Domestic Debt 222.7 222.8 222.8

Short-term Debt 13.8 30.2 19.7

Total Debt $1,050.2 $923.2 $909.6

Cash

Restricted Cash 136.9 9.7 -

Cash 57.0 212.4 229.0

Total Cash $193.9 $222.1 $229.0

Net Debt $856.3 $701.1 $680.6

Stockholders’ Equity $588.3 $876.2 $943.0

Total Capital (Total Debt + Stockholders’ Equity) $1,638.5 $1,799.4 $1,852.6

Net Debt/Total Capital, less all cash 59.3% 44.4% 41.9%

31

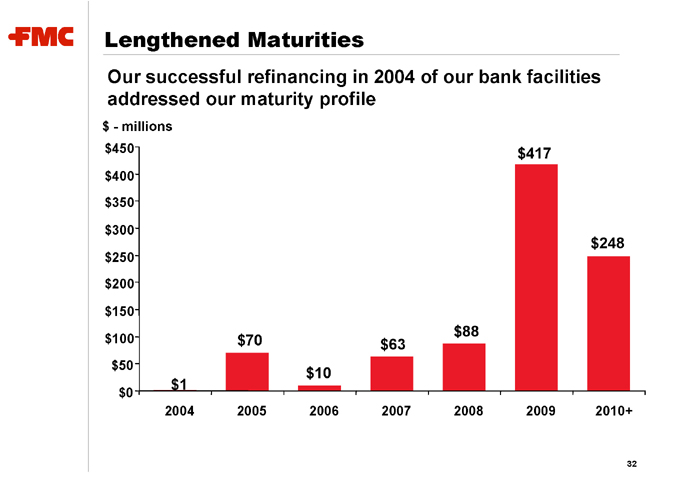

Lengthened Maturities

Our successful refinancing in 2004 of our bank facilities addressed our maturity profile $ - millions $450 $400 $350 $300 $250 $200 $150 $100 $50 $0

2004 2005 2006 2007 2008 2009 2010+ $1 $70 $10 $63 $88 $417 $248

32

Summary

Great businesses, each with EBITDA of at least $130 million Industrial Chemicals earnings only at mid-cycle in 2005 Steady growth in Specialty Chemicals and Ag Products Low capital expenditure requirements Substantial decline in unusual demands on cash flow Continued improvements in credit quality

33

FMC Corporation

Non-GAAP Financial Terms

These slides contain certain “non-GAAP financial terms” which are defined below. In addition, we have provided reconciliations of non-GAAP terms to the closest GAAP term in the appendix of this presentation.

EBITDA (Earnings Before Interest, Taxes, Depreciation and Amortization) is the sum of Income (loss) from continuing operations before income taxes and Depreciation and Amortization.

EBITDA Margin is the quotient of EBITDA (defined above) divided by Revenue.

ROIC (Return on Invested Capital) is the sum of Earnings from continuing operations before restructuring and other income and charges and after-tax Interest expense divided by the sum of Short-term debt, Current portion of long-term debt, Long-term debt and Total shareholders’ equity.

35

Segment Financial Terms

These slides contain references to segment financial items which are presented in detail in Note 18 of FMC’s 2004 Form 10-K. Some of the segment financial terms are “non-GAAP financial terms” and are defined below. In addition, we have provided reconciliations of non-GAAP terms to the closest GAAP term in the appendix of this presentation.

EBITDA (Earnings Before Interest, Taxes, Depreciation and Amortization) for a segment is the sum of Income (loss) from continuing operations before income taxes for that segment and Depreciation and Amortization for that segment.

EBITDA Margin for a segment is the quotient of EBITDA (defined above) divided by Revenue for that segment.

36

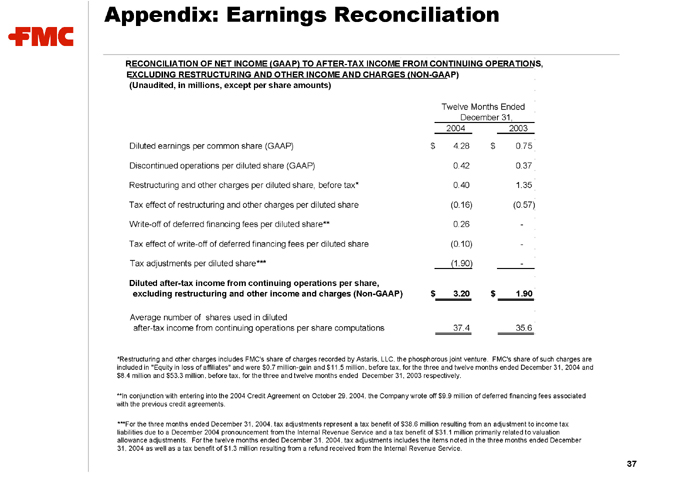

Appendix: Earnings Reconciliation

RECONCILIATION OF NET INCOME (GAAP) TO AFTER-TAX INCOME FROM CONTINUING OPERATIONS, EXCLUDING RESTRUCTURING AND OTHER INCOME AND CHARGES (NON-GAAP) (Unaudited, in millions, except per share amounts)

Twelve Months Ended

December 31,

2004 2003

Diluted earnings per common share (GAAP) $4.28 $0.75

Discontinued operations per diluted share (GAAP) 0.42 0.37

Restructuring and other charges per diluted share, before tax* 0.40 1.35

Tax effect of restructuring and other charges per diluted share (0.16) (0.57)

Write-off of deferred financing fees per diluted share** 0.26 -

Tax effect of write-off of deferred financing fees per diluted share (0.10) -

Tax adjustments per diluted share*** (1.90) -

Diluted after-tax income from continuing operations per share,

excluding restructuring and other income and charges (Non-GAAP) $3.20 $1.90

Average number of shares used in diluted

after-tax income from continuing operations per share computations 37.4 35.6

*Restructuring and other charges includes FMC’s share of charges recorded by Astaris, LLC, the phosphorous joint venture. FMC’s share of such charges are included in “Equity in loss of affiliates” and were $0.7 million-gain and $11.5 million, before tax, for the three and twelve months ended December 31, 2004 and $8.4 million and $53.3 million, before tax, for the three and twelve months ended December 31, 2003 respectively.

**In conjunction with entering into the 2004 Credit Agreement on October 29, 2004, the Company wrote off $9.9 million of deferred financing fees associated with the previous credit agreements.

***For the three months ended December 31, 2004, tax adjustments represent a tax benefit of $38.6 million resulting from an adjustment to income tax liabilities due to a December 2004 pronouncement from the Internal Revenue Service and a tax benefit of $31.1 million primarily related to valuation allowance adjustments. For the twelve months ended December 31, 2004, tax adjustments includes the items noted in the three months ended December 31, 2004 as well as a tax benefit of $1.3 million resulting from a refund received from the Internal Revenue Service.

37

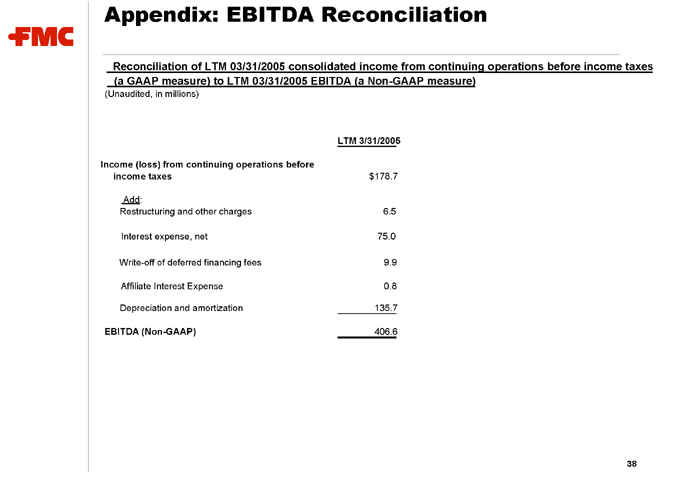

Appendix: EBITDA Reconciliation

Reconciliation of LTM 03/31/2005 consolidated income from continuing operations before income taxes (a GAAP measure) to LTM 03/31/2005 EBITDA (a Non-GAAP measure)

(Unaudited, in millions)

LTM 3/31/2005

Income (loss) from continuing operations before

income taxes $ 178.7

Add:

Restructuring and other charges 6.5

Interest expense, net 75.0

Write-off of deferred financing fees 9.9

Affiliate Interest Expense 0.8

Depreciation and amortization 135.7

EBITDA (Non-GAAP) 406.6

38

Appendix: Segment EBITDA Reconciliation

Reconciliation of LTM 03/31/2005 segment operating profit (a GAAP measure) to LTM 03/31/2005 EBITDA (a Non-GAAP measure)

(Unaudited, in millions)

Industrial Specialty Agricultural

Segment Chemicals Chemicals Products

LTM 03/31/2005 segment operating profit (GAAP) $72.2 $99.9 $132.3

Add:

Depreciation and amortization 68.2 32.8 29.3

LTM 03/31/2005 EBITDA (Non-GAAP) $140.4 $132.7 $161.6

39

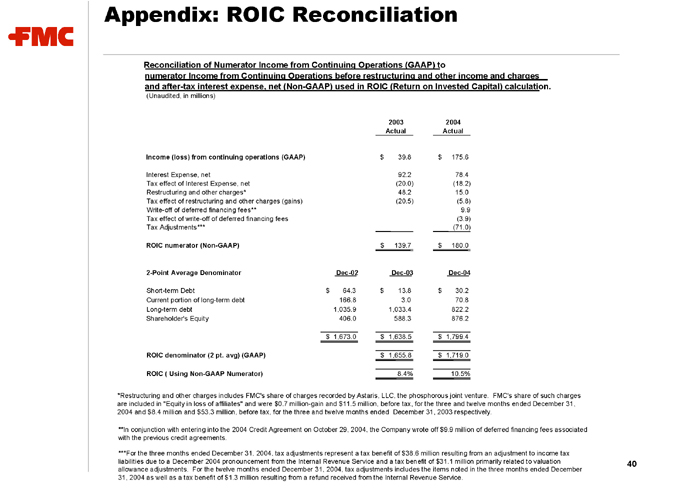

Appendix: ROIC Reconciliation

Reconciliation of Numerator Income from Continuing Operations (GAAP) to numerator Income from Continuing Operations before restructuring and other income and charges and after-tax interest expense, net (Non-GAAP) used in ROIC (Return on Invested Capital) calculation.

(Unaudited, in millions)

2003 2004

Actual Actual

Income (loss) from continuing operations (GAAP) $39.8 $175.6

Interest Expense, net 92.2 78.4

Tax effect of Interest Expense, net (20.0) (18.2)

Restructuring and other charges* 48.2 15.0

Tax effect of restructuring and other charges (gains) (20.5) (5.8)

Write-off of deferred financing fees** 9.9

Tax effect of write-off of deferred financing fees (3.9)

Tax Adjustments*** (71.0)

ROIC numerator (Non-GAAP) $139.7 $180.0

2-Point Average Denominator Dec-02 Dec-03 Dec-04

Short-term Debt $64.3 $13.8 $30.2

Current portion of long-term debt 166.8 3.0 70.8

Long-term debt 1,035.9 1,033.4 822.2

Shareholder’s Equity 406.0 588.3 876.2

$1,673.0 $1,638.5 $1,799.4

ROIC denominator (2 pt. avg) (GAAP) $1,655.8 $1,719.0

ROIC ( Using Non-GAAP Numerator) 8.4% 10.5%

*Restructuring and other charges includes FMC’s share of charges recorded by Astaris, LLC, the phosphorous joint venture. FMC’s share of such charges are included in “Equity in loss of affiliates” and were $0.7 million-gain and $11.5 million, before tax, for the three and twelve months ended December 31, 2004 and $8.4 million and $53.3 million, before tax, for the three and twelve months ended December 31, 2003 respectively.

**In conjunction with entering into the 2004 Credit Agreement on October 29, 2004, the Company wrote off $9.9 million of deferred financing fees associated with the previous credit agreements.

***For the three months ended December 31, 2004, tax adjustments represent a tax benefit of $38.6 million resulting from an adjustment to income tax liabilities due to a December 2004 pronouncement from the Internal Revenue Service and a tax benefit of $31.1 million primarily related to valuation allowance adjustments. For the twelve months ended December 31, 2004, tax adjustments includes the items noted in the three months ended December 31, 2004 as well as a tax benefit of $1.3 million resulting from a refund received from the Internal Revenue Service.

40

FMC Corporation