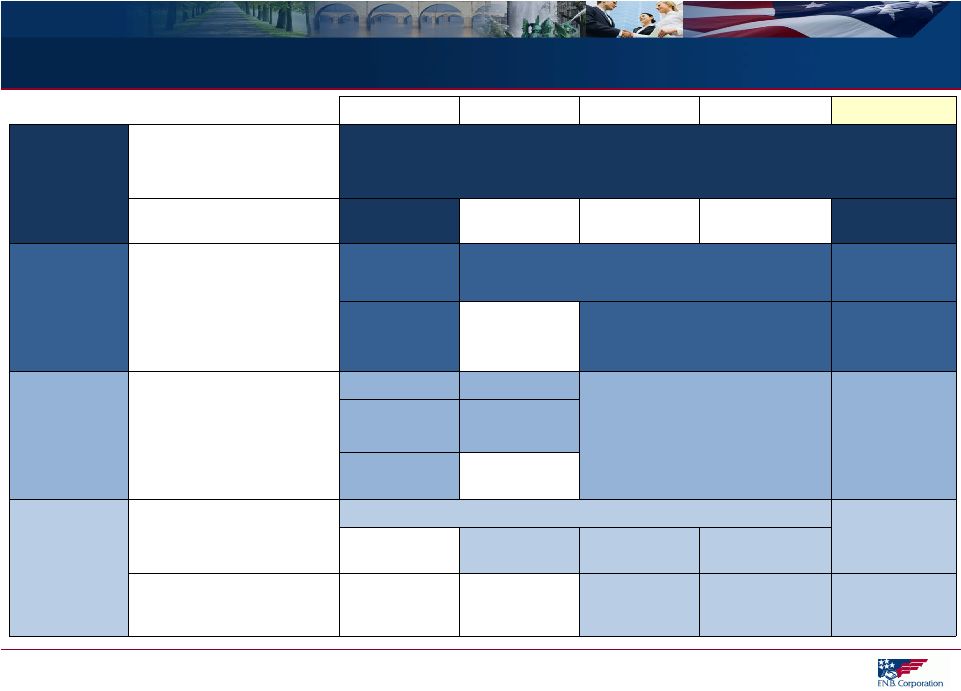

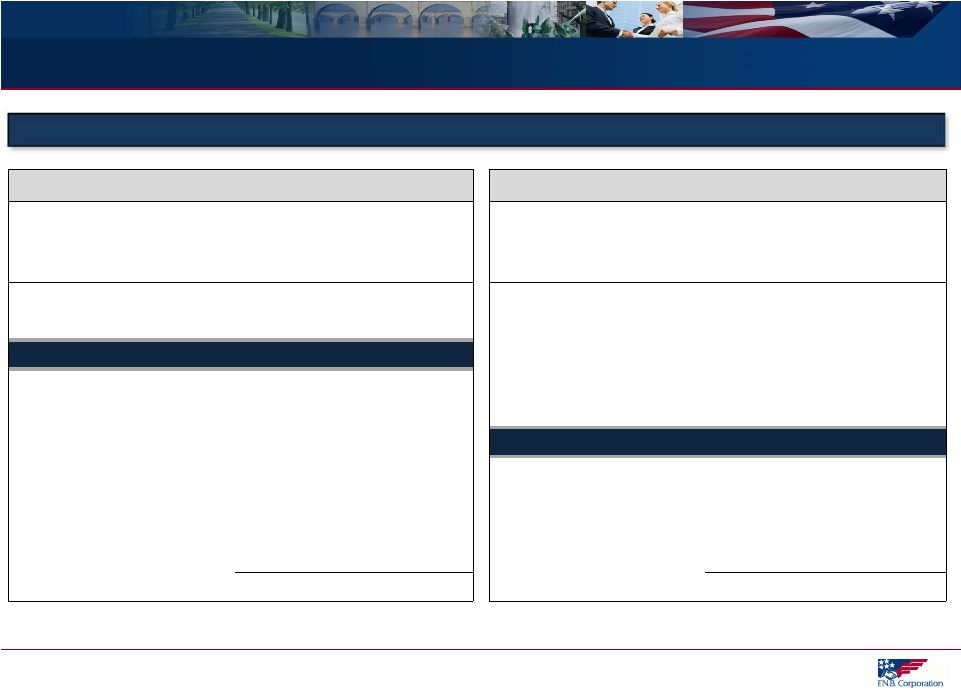

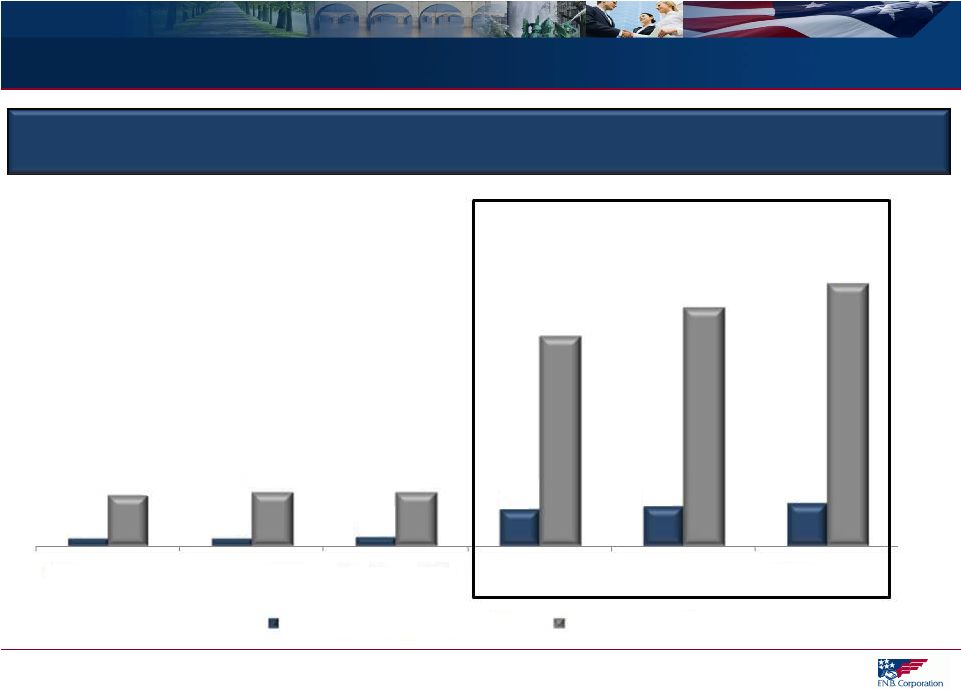

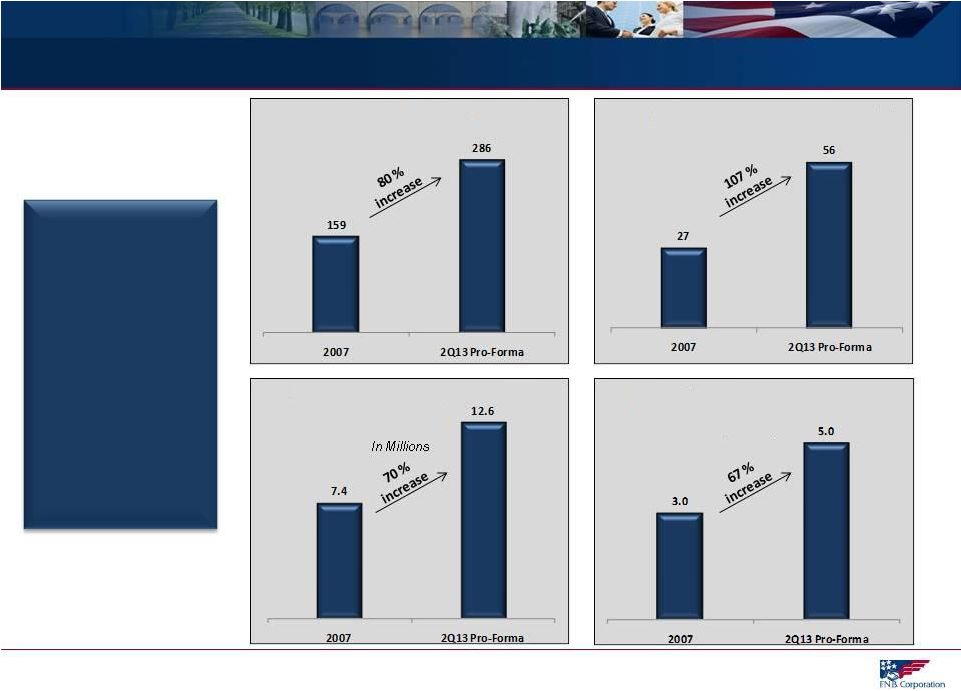

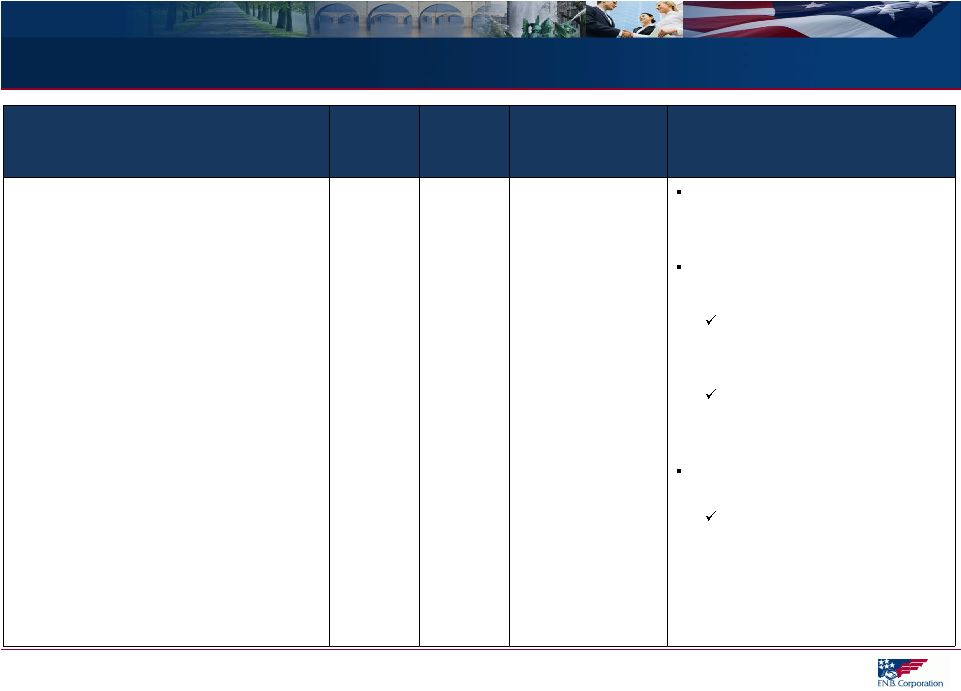

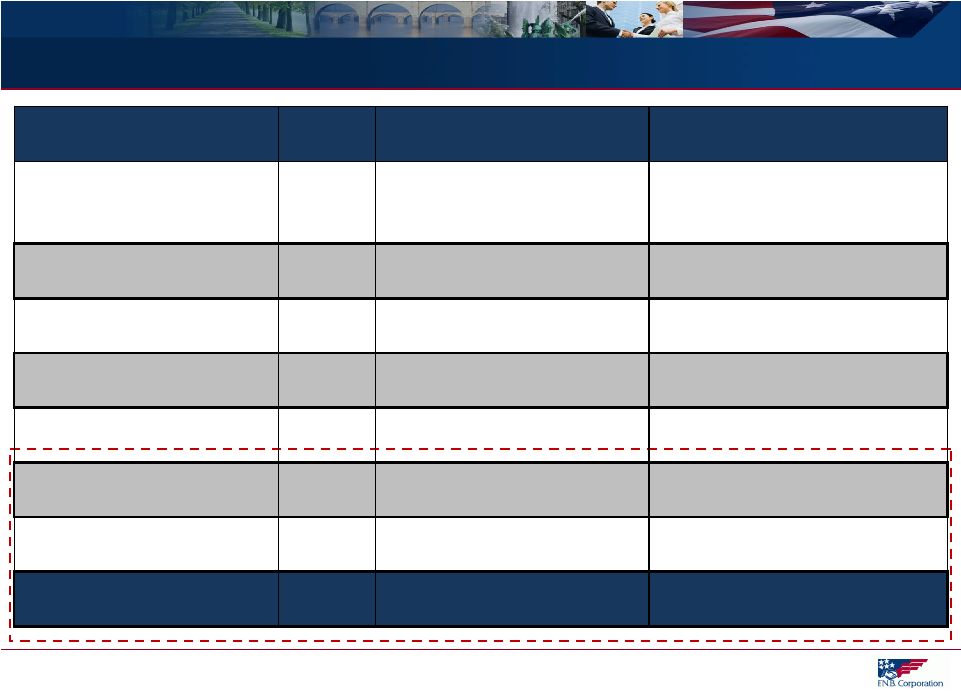

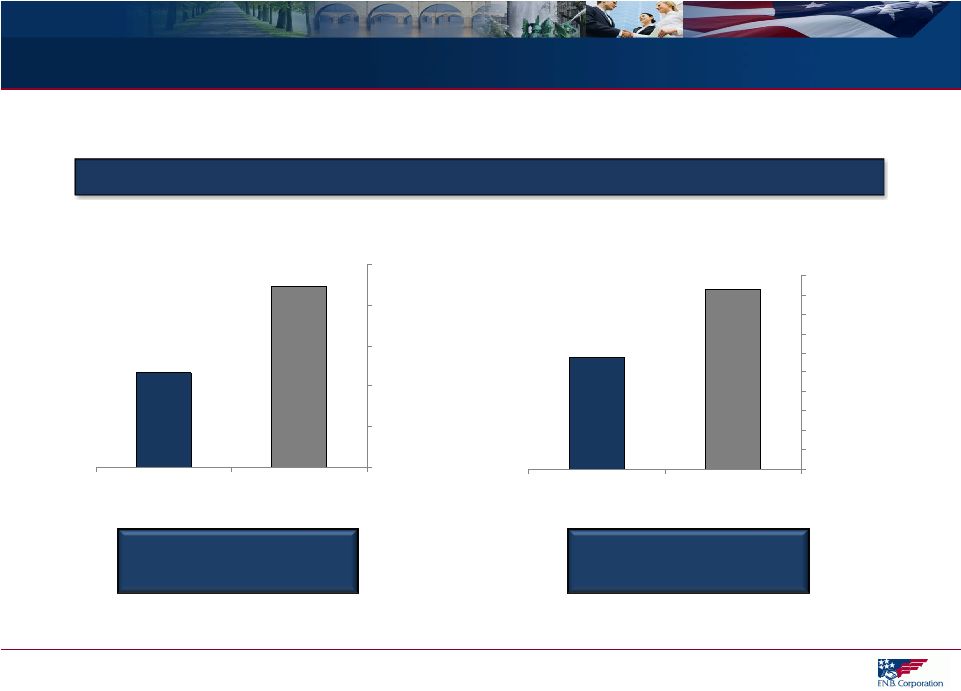

GAAP to Non-GAAP Reconciliation 46 Operating: Earnings, Return on Avg Tangible Equity, Return on Avg Tangible Assets June 30, 2013 March 31, 2013 June 30, 2012 2012 2011 2010 Operating net income Net income $29,192 $28,538 $29,130 $110,410 $87,047 $74,652 Add: Merger and severance costs, net of tax 1,915 229 206 5,203 3,238 402 Add: Litigation settlement accrual, net of tax - - - 1,950 - - Add: Branch consolidation costs, net of tax - - - 1,214 - - Less: Gain on extinguishment of debt, net of tax 1,013 - - 942 - - Less: One-time pension expense credit, net of tax - - - - - 6,853 Operating net income $30,094 $28,767 $29,336 $117,835 $90,285 $68,201 Operating diluted earnings per share Diluted earnings per share $0.20 $0.20 $0.21 $0.79 $0.70 $0.65 Add: Merger and severance costs, net of tax 0.01 0.00 0.00 0.04 0.03 0.00 Add: Litigation settlement accrual, net of tax - - - 0.01 - - Add: Branch consolidation costs, net of tax - - - 0.01 - - Less: Gain on extinguishment of debt, net of tax (0.01) - - 0.01 - - Less: One-time pension expense credit - - - - - 0.06 Operating diluted earnings per share $0.21 $0.20 $0.21 $0.84 $0.72 $0.60 Operating return on average tangible equity Operating net income (annualized) $120,706 $116,668 $117,991 $117,835 $90,285 $68,201 Amortization of intangibles, net of tax (annualized) 5,538 5,237 6,192 5,938 4,698 4,364 $126,244 $121,904 $124,182 $123,773 $94,983 $72,565 Average shareholders' equity $1,473,945 $1,410,827 $1,367,333 $1,376,493 $1,181,941 $1,057,732 Less: Average intangible assets 745,458 712,466 718,507 717,031 599,851 564,448 Average tangible equity $728,487 $698,361 $648,826 $659,462 $582,090 $493,284 Operating return on average tangible equity 17.33% 17.46% 19.14% 18.77% 16.32% 14.71% Operating return on average tangible assets Operating net income (annualized) $120,706 $116,668 $117,991 $117,835 $90,285 $68,201 Amortization of intangibles, net of tax (annualized) 5,538 5,237 6,192 5,938 4,698 4,364 $126,244 $121,904 $124,182 $123,773 $94,983 $72,565 Average total assets $12,470,029 $12,004,759 $11,734,221 $11,782,821 $9,871,164 $8,906,734 Less: Average intangible assets 745,458 712,466 718,507 717,031 599,851 564,448 Average tangible assets 11,724,570 $ 11,292,292 $ 11,015,714 $ 11,065,790 $ 9,271,313 $ 8,342,286 $ Operating return on average tangible assets 1.08% 1.08% 1.13% 1.12% 1.02% 0.87% For the Quarter Ended Year Ended December 31, |