UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-02383

AB BOND FUND, INC.

(Exact name of registrant as specified in charter)

1345 Avenue of the Americas, New York, New York 10105

(Address of principal executive offices) (Zip code)

Joseph J. Mantineo

AllianceBernstein L.P.

1345 Avenue of the Americas

New York, New York 10105

(Name and address of agent for service)

Registrant’s telephone number, including area code: (800) 221-5672

Date of fiscal year end: October 31, 2016

Date of reporting period: April 30, 2016

| ITEM 1. | REPORTS TO STOCKHOLDERS. |

APR 04.30.16

SEMI-ANNUAL REPORT

AB ALL MARKET REAL RETURN PORTFOLIO

Investment Products Offered

• Are Not FDIC Insured • May Lose Value • Are Not Bank Guaranteed |

Investors should consider the investment objectives, risks, charges and expenses of the Fund carefully before investing. For copies of our prospectus or summary prospectus, which contain this and other information, visit us online at www.abglobal.com or contact your AB representative. Please read the prospectus and/or summary prospectus carefully before investing.

This shareholder report must be preceded or accompanied by the Fund’s prospectus for individuals who are not current shareholders of the Fund.

You may obtain a description of the Fund’s proxy voting policies and procedures, and information regarding how the Fund voted proxies relating to portfolio securities during the most recent 12-month period ended June 30, without charge. Simply visit AB’s website at www.abglobal.com, or go to the Securities and Exchange Commission’s (the “Commission”) website at www.sec.gov, or call AB at (800) 227-4618.

The Fund files its complete schedule of portfolio holdings with the Commission for the first and third quarters of each fiscal year on Form N-Q. The Fund’s Forms N-Q are available on the Commission’s website at www.sec.gov. The Fund’s Forms N-Q may also be reviewed and copied at the Commission’s Public Reference Room in Washington, DC; information on the operation of the Public Reference Room may be obtained by calling (800) SEC-0330. AB publishes full portfolio holdings for the Fund monthly at www.abglobal.com.

AllianceBernstein Investments, Inc. (ABI) is the distributor of the AB family of mutual funds. ABI is a member of FINRA and is an affiliate of AllianceBernstein L.P., the Adviser of the funds.

The [A/B] logo is a registered service mark of AllianceBernstein and AllianceBernstein® is a registered service mark used by permission of the owner, AllianceBernstein L.P.

June 24, 2016

Semi-Annual Report

This report provides management’s discussion of fund performance for AB All Market Real Return Portfolio (the “Fund”) for the semi-annual reporting period ended April 30, 2016.

Investment Objective and Policies

The Fund’s investment objective is to maximize real return. Real return is the rate of return after adjusting for inflation. The Fund pursues an aggressive investment strategy involving a variety of asset classes. The Fund invests primarily in instruments that AllianceBernstein L.P. (“the Adviser”) expects to outperform broad equity indices during periods of rising inflation. Under normal circumstances, the Fund expects to invest its assets principally in the following instruments that, in the judgment of the Adviser, are affected directly or indirectly by the level and change in rate of inflation: inflation-indexed fixed-income securities, such as Treasury inflation-protected securities (“TIPS”) and similar bonds issued by governments outside of the United States, commodities, equity securities, such as commodity-related stocks, real estate securities, utility securities, infrastructure-related securities, securities and derivatives linked to the price of other assets (such as commodities, stock indices and real estate) and currencies. The Fund expects its investments in fixed-income securities to have a broad range of maturities and quality levels.

The Fund will seek inflation protection from investments around the globe, both in developed- and emerging-market countries. In selecting securities for purchase and sale, the Adviser will utilize its qualitative

and quantitative resources to determine overall inflation sensitivity, asset allocation and security selection. The Adviser assesses the securities’ risks and inflation sensitivity as well as the securities’ impact on the overall risks and inflation sensitivity of the Fund. When its analysis indicates that changes are necessary, the Adviser intends to implement them through a combination of changes to underlying positions and the use of inflation swaps and other types of derivatives, such as interest rate swaps.

The Fund anticipates that its investments, other than its investments in inflation-indexed securities, will focus roughly equally on commodity-related equity securities, commodities and commodity derivatives, and real estate equity securities to provide a balance between expected return and inflation protection. Its commodities investments will include significant exposure to energy commodities, but will also include agricultural products, and industrial and precious metals, such as gold. The Fund’s investments in real estate equity securities will include real estate investment trusts (“REITs”), other real estate-related securities and infrastructure-related securities.

The Fund will invest in both US and non-US dollar-denominated equity or fixed-income securities. The Fund may invest in currencies for hedging or for investment purposes, both in the spot market and through long or short positions in currency-related derivatives. The Fund does not ordinarily expect to hedge its foreign currency exposure because it will be balanced by investments in US dollar-denominated securities, although it

| AB ALL MARKET REAL RETURN PORTFOLIO • | 1 |

may hedge the exposure under certain circumstances. The Fund may invest significantly to the extent permitted by applicable law in derivatives, such as options, futures contracts, forwards, swaps or structured notes. The Fund intends to use leverage for investment purposes through the use of cash made available by derivatives transactions to make other investments in accordance with its investment policies. In determining when and to what extent to employ leverage or enter into derivatives transactions, the Adviser will consider factors such as the relative risks and returns expected of potential investments and the cost of such transactions. The Adviser will consider the impact of derivatives in making its assessments of the Fund’s risks. The resulting exposures to markets, sectors, issuers or specific securities will be continuously monitored by the Adviser.

The Fund may seek to gain exposure to physical commodities traded in the commodities markets through investments in a variety of derivative instruments, including investments in commodity index-linked notes. The Adviser expects that the Fund will seek to gain exposure to commodities and commodity-related instruments and derivatives primarily through investments in AllianceBernstein Cayman Inflation Strategy, Ltd., a wholly-owned subsidiary of the Fund organized under the laws of the Cayman Islands (the “Subsidiary”). The Subsidiary is advised by the Adviser and has the same investment objective and substantially similar investment policies and restrictions as the Fund except that the Subsidiary, unlike the Fund, may invest, without limitation, in commodities and commodity-related instruments. The

Fund will be subject to the risks associated with the commodities, derivatives and other instruments in which the Subsidiary invests, to the extent of its investment in the Subsidiary. The Fund limits its investment in the Subsidiary to no more than 25% of its net assets. Investment in the Subsidiary is expected to provide the Fund with commodity exposure within the limitations of federal tax requirements that apply to the Fund.

The Fund is “non-diversified”, which means that it may concentrate its assets in a smaller number of issuers than a diversified fund.

Investment Results

The table on page 7 shows the Fund’s performance compared to its primary benchmark, the Morgan Stanley Capital International All Country (“MSCI AC”) World Commodity Producers Index (net) and the All Market Real Return Portfolio Benchmark, composed of equal weightings of the MSCI AC World Commodity Producers Index, the Financial Times Stock Exchange European Public Real Estate Association/National Association of Real Estate Investment Trusts (“FTSE EPRA/NAREIT”) Global Index and the Dow Jones-UBS Commodity Index, for the six- and 12-month periods ended April 30, 2016.

All share classes of the Fund underperformed the primary benchmark, the MSCI AC World Commodity Producers Index, for the six-month period, but outperformed for the 12-month period, before sales charges. All share classes of the Fund underperformed the secondary benchmark, the All Market Real Return Portfolio Benchmark for both periods.

The outperformance versus the primary benchmark during the 12-month

| 2 | • AB ALL MARKET REAL RETURN PORTFOLIO |

period was driven by a strategic exposure to global real estate, which strongly outperformed the benchmark. The Fund’s strategic allocation to commodity futures detracted slightly from performance. Over the six-month period, both the strategic exposure to commodity futures and global real estate detracted, as commodity producers rallied strongly, especially gold producers that benefitted initially from gold’s safe haven status and subsequently by falling yields. During both periods, an overweight to the US dollar and gold futures, in addition to security selection, outperformed relative to the benchmark, which helped returns; long-dated oil futures detracted for both periods.

The underperformance versus the secondary benchmark during both periods was driven by an overweight to energy and energy futures, while security selection and foreign exchange exposure contributed to performance. An underweight to mining equities detracted for the six-month period, but contributed during the 12-month period.

The Fund utilized derivatives for hedging and investment purposes, including Treasury futures, inflation swaps and written options, which detracted for both periods, in absolute terms; currency forwards and total return swaps added for the six-month period and detracted for the 12-month period; purchased options detracted for the six-month period and added for the 12-month period. Interest rate swaps for hedging purposes added for both periods.

Market Review and Investment Strategy

The six- and 12-month periods were marked by materially different risk episodes. After a relatively calm fourth

quarter in 2015, risk assets fell sharply in the first quarter of 2016, moving in lockstep with commodities such as oil and metals, as uncertainty regarding Chinese economic policy reverberated around global financial markets. Another major headwind for commodities was that the US dollar continued to strengthen against most major currencies, as markets continued to price in monetary policy divergence between the US and the rest of the world.

February was a turning point for risk assets, as a combination of stimulus measures announced by Chinese officials and a dovish stance by most central banks helped ease frayed investor nerves. As a result, commodities rallied sharply on short covering, Chinese stimulus and a change in course for the US dollar as markets started pricing a materially more dovish US Federal Reserve (the “Fed”). TIPS had positive returns as commodities rebounded and inflation readings were firmer than in the past.

Real estate moved in parallel and experienced a large rally in February and March. A dovish Fed is positive for risk assets, and REITs in particular, because they pay dividends and are yield instruments that do well as rates fall.

On June 23, 2016, the UK voted to leave the European Union (“EU”) in a popular referendum. At this moment in time, the UK remains a member of the EU and the rules and regulations remain unchanged, as do all the protections in place. Exactly how the UK’s role in the EU will change will become clear over time. The Adviser continues to monitor the heightened market volatility.

| AB ALL MARKET REAL RETURN PORTFOLIO • | 3 |

DISCLOSURES AND RISKS

Benchmark Disclosure

The MSCI AC World Commodity Producers Index (net), the FTSE® EPRA/NAREIT Global Index and the Dow Jones-UBS Commodity Index are unmanaged and do not reflect fees and expenses associated with the active management of a mutual fund portfolio. The MSCI AC World Commodity Producers Index is a free float-adjusted, market capitalization index designed to track the performance of global listed commodity producers, including emerging markets. Net returns include the reinvestment of dividends after deduction of non-US withholding tax. The All Market Real Return Portfolio Benchmark is an equally-weighted blend of the MSCI AC World Commodity Producers Index, the FTSE EPRA/NAREIT Global Index and the Dow Jones-UBS Commodity Index. The FTSE EPRA/NAREIT Global Index (market-value-weighted index based upon the last closing price of the month) represents the performance of tax-qualified REITs listed on the NYSE, AMEX and the NASDAQ. The Dow Jones-UBS Commodity Index measures price movements of the commodities included in the appropriate sub index. It does not account for effects of rolling futures contracts or costs associated with holding the physical commodity. Commodities sectors include: energy, grains, industrial metals, petroleum, precious metals and softs. MSCI makes no express or implied warranties or representations, and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used as a basis for other indices, any securities or financial products. This report is not approved, reviewed or produced by MSCI. An investor cannot invest directly in an index, and its results are not indicative of the performance for any specific investment, including the Fund.

A Word About Risk

Market Risk: The value of the Fund’s assets will fluctuate as the stock, commodity and bond markets fluctuate. The value of the Fund’s investments may decline, sometimes rapidly and unpredictably, simply because of economic changes or other events that affect large portions of the market.

Credit Risk: An issuer or guarantor of a fixed-income security, or the counterparty to a derivatives or other contract, may be unable or unwilling to make timely payments of interest or principal, or to otherwise honor its obligations. The issuer or guarantor may default, causing a loss of the full principal amount of a security. The degree of risk for a particular security may be reflected in its credit rating. There is the possibility that the credit rating of a fixed-income security may be downgraded after purchase, which may adversely affect the value of the security. Investments in fixed-income securities with lower ratings tend to have a higher probability that an issuer will default or fail to meet its payment obligations.

Interest Rate Risk: Changes in interest rates will affect the value of investments in fixed-income securities. When interest rates rise, the value of investments in fixed-income securities tends to fall and this decrease in value may not be offset by higher income from new investments. The Fund may be subject to a heightened risk of rising interest rates as the current period of historically low rates is beginning to end and rates have begun rising. Interest rate risk is generally greater for fixed-income securities with longer maturities or durations.

Commodity Risk: Investing in commodities and commodity-linked derivative instruments, either directly or through the Subsidiary, may subject the Fund to greater volatility than investments in traditional securities. The value of commodity-linked derivative instruments may be affected by changes in overall market movements, commodity index volatility, changes in interest rates, or factors affecting a particular industry or commodity, such as drought, floods, weather, livestock disease, embargoes, tariffs and international economic, political and regulatory developments.

(Disclosures, Risks and Note about Historical Performance continued on next page)

| 4 | • AB ALL MARKET REAL RETURN PORTFOLIO |

Disclosures and Risks

DISCLOSURES AND RISKS

(continued from previous page)

Derivatives Risk: Derivatives may be illiquid, difficult to price, and leveraged so that small changes may produce disproportionate losses for the Fund, and may be subject to counterparty risk to a greater degree than more traditional investments.

Leverage Risk: To the extent the Fund uses leveraging techniques, its net asset value (“NAV”) may be more volatile because leverage tends to exaggerate the effect of changes in interest rates and any increase or decrease in the value of the Fund’s investments.

Liquidity Risk: Liquidity risk occurs when certain investments become difficult to purchase or sell. Difficulty in selling less liquid securities may result in sales at disadvantageous prices affecting the value of your investment in the Fund. Causes of liquidity risk may include low trading volumes and large positions. Foreign fixed-income securities may have more liquidity risk because secondary trading markets for these securities may be smaller and less well-developed and the securities may trade less frequently. Liquidity risk may be higher in a rising interest rate environment, when the value and liquidity of fixed-income securities generally go down.

Foreign (Non-US) Risk: Investments in securities of non-US issuers may involve more risk than those of US issuers. These securities may fluctuate more widely in price and may be less liquid due to adverse market, economic, political, regulatory or other factors.

Currency Risk: Fluctuations in currency exchange rates may negatively affect the value of the Fund’s investments or reduce its returns.

Subsidiary Risk: By investing in the Subsidiary, the Fund is indirectly exposed to the risks associated with the Subsidiary’s investments. The derivatives and other investments held by the Subsidiary are generally similar to those that are permitted to be held by the Fund and are subject to the same risks that apply to similar investments if held directly by the Fund. The Subsidiary is not registered under the Investment Company Act of 1940, as amended (the “1940 Act”), and, unless otherwise noted in the Fund’s prospectus, is not subject to all of the investor protections of the 1940 Act. However, the Fund wholly owns and controls the Subsidiary, and the Fund and the Subsidiary are managed by the Adviser, making it unlikely the Subsidiary will take actions contrary to the interests of the Fund or its shareholders.

Real Estate Risk: The Fund’s investments in real estate securities have many of the same risks as direct ownership of real estate, including the risk that the value of real estate could decline due to a variety of factors that affect the real estate market generally. Investments in REITs may have additional risks. REITs are dependent on the capability of their managers, may have limited diversification, and could be significantly affected by changes in taxes.

Diversification Risk: The Fund may have more risk because it is “non-diversified”, meaning that it can invest more of its assets in a smaller number of issuers and that adverse changes in the value of one security could have a more significant effect on the Fund’s NAV.

Management Risk: The Fund is subject to management risk because it is an actively managed investment fund. The Adviser will apply its investment techniques and risk analyses in making investment decisions, but there is no guarantee that its techniques will produce the intended results.

These risks are fully discussed in the Fund’s prospectus. As with all investments, you may lose money by investing in the Fund.

(Disclosures, Risks and Note about Historical Performance continued on next page)

| AB ALL MARKET REAL RETURN PORTFOLIO • | 5 |

Disclosures and Risks

DISCLOSURES AND RISKS

(continued from previous page)

An Important Note About Historical Performance

The investment return and principal value of an investment in the Fund will fluctuate, so that shares, when redeemed, may be worth more or less than their original cost. Performance shown on the following pages represents past performance and does not guarantee future results. Current performance may be lower or higher than the performance information shown. You may obtain performance information current to the most recent month-end by visiting www.abglobal.com.

Investors should consider the investment objectives, risks, charges and expenses of the Fund carefully before investing. For copies of our prospectus or summary prospectus, which contain this and other information, visit us online at www.abglobal.com. For Class 1 shares, click on “Private Clients”, then “Investments”, then “Stocks” or “Bonds”, then “Prospectuses, SAIs, and Shareholder Reports”. Please read the prospectus and/or summary prospectus carefully before investing.

All fees and expenses related to the operation of the Fund have been deducted. NAV returns do not reflect sales charges; if sales charges were reflected, the Fund’s quoted performance would be lower. SEC returns reflect the applicable sales charges for each share class: a 4.25% maximum front-end sales charge for Class A shares; a 1% 1-year contingent deferred sales charge for Class C shares. Returns for the different share classes will vary due to different expenses associated with each class. Performance assumes reinvestment of distributions and does not account for taxes.

| 6 | • AB ALL MARKET REAL RETURN PORTFOLIO |

Disclosures and Risks

HISTORICAL PERFORMANCE

THE FUND VS. ITS BENCHMARK PERIODS ENDED APRIL 30, 2016 (unaudited) | NAV Returns | |||||||||

| 6 Months | 12 Months | |||||||||

| AB All Market Real Return Portfolio | ||||||||||

Class 1* | 1.55% | -13.69% | ||||||||

| ||||||||||

Class 2* | 1.56% | -13.49% | ||||||||

| ||||||||||

Class A | 1.38% | -13.87% | ||||||||

| ||||||||||

Class C | 1.07% | -14.48% | ||||||||

| ||||||||||

Advisor Class† | 1.50% | -13.68% | ||||||||

| ||||||||||

Class R† | 1.28% | -14.09% | ||||||||

| ||||||||||

Class K† | 1.42% | -13.85% | ||||||||

| ||||||||||

Class I† | 1.64% | -13.52% | ||||||||

| ||||||||||

Class Z† | 1.58% | -13.56% | ||||||||

| ||||||||||

Primary Benchmark: MSCI AC World Commodity Producers Index (net) | 7.82% | -14.60% | ||||||||

| ||||||||||

| All Market Real Return Portfolio Benchmark | 3.33% | -10.42% | ||||||||

| ||||||||||

* Class 1 shares are only available to Bernstein Global Wealth Management private client accounts. Class 2 shares are only available to the Adviser’s institutional clients or through other limited arrangements.

† Please note that these share classes are for investors purchasing shares through accounts established under certain fee-based programs sponsored and maintained by certain broker-dealers and financial intermediaries, institutional pension plans and/or investment advisory clients of, and certain other persons associated with, the Adviser and its affiliates or the Fund. | ||||||||||

See Disclosures, Risks and Note about Historical Performance on pages 4-6.

(Historical Performance continued on next page)

| AB ALL MARKET REAL RETURN PORTFOLIO • | 7 |

Historical Performance

HISTORICAL PERFORMANCE

(continued from previous page)

| AVERAGE ANNUAL RETURNS AS OF APRIL 30, 2016 (unaudited) | ||||||||

| NAV Returns | SEC Returns (reflects applicable sales charges) | |||||||

| Class 1 Shares* | ||||||||

1 Year | -13.69 | % | -13.69 | % | ||||

5 Years | -6.94 | % | -6.94 | % | ||||

Since Inception† | -1.51 | % | -1.51 | % | ||||

| Class 2 Shares* | ||||||||

1 Year | -13.49 | % | -13.49 | % | ||||

5 Years | -6.72 | % | -6.72 | % | ||||

Since Inception† | -1.28 | % | -1.28 | % | ||||

| Class A Shares | ||||||||

1 Year | -13.87 | % | -17.50 | % | ||||

5 Years | -7.02 | % | -7.82 | % | ||||

Since Inception† | -1.58 | % | -2.27 | % | ||||

| Class C Shares | ||||||||

1 Year | -14.48 | % | -15.33 | % | ||||

5 Years | -7.68 | % | -7.68 | % | ||||

Since Inception† | -2.28 | % | -2.28 | % | ||||

| Advisor Class Shares‡ | ||||||||

1 Year | -13.68 | % | -13.68 | % | ||||

5 Years | -6.76 | % | -6.76 | % | ||||

Since Inception† | -1.31 | % | -1.31 | % | ||||

| Class R Shares‡ | ||||||||

1 Year | -14.09 | % | -14.09 | % | ||||

5 Years | -7.23 | % | -7.23 | % | ||||

Since Inception† | -1.81 | % | -1.81 | % | ||||

| Class K Shares‡ | ||||||||

1 Year | -13.85 | % | -13.85 | % | ||||

5 Years | -6.98 | % | -6.98 | % | ||||

Since Inception† | -1.55 | % | -1.55 | % | ||||

| Class I Shares‡ | ||||||||

1 Year | -13.52 | % | -13.52 | % | ||||

5 Years | -6.72 | % | -6.72 | % | ||||

Since Inception† | -1.28 | % | -1.28 | % | ||||

| Class Z Shares‡ | ||||||||

1 Year | -13.56 | % | -13.56 | % | ||||

Since Inception† | -9.23 | % | -9.23 | % | ||||

See Disclosures, Risks and Note about Historical Performance on pages 4-6.

(Historical Performance and footnotes continued on next page)

| 8 | • AB ALL MARKET REAL RETURN PORTFOLIO |

Historical Performance

HISTORICAL PERFORMANCE

(continued from previous page)

The Fund’s prospectus fee table shows the Fund’s total annual operating expense ratios as 1.16%, 0.92%, 1.42%, 2.16%, 1.17%, 1.64%, 1.34%, 0.96% and 0.96% for Class 1, Class 2, Class A, Class C, Advisor Class, Class R, Class K, Class I and Class Z shares, respectively, gross of any fee waivers or expense reimbursements. Contractual fee waivers and/or expense reimbursements limit the Fund’s annual operating expense ratios to 1.25%, 1.00%, 1.30%, 2.05%, 1.05%, 1.55%, 1.30%, 1.00% and 1.00% for Class 1, Class 2, Class A, Class C, Advisor Class, Class R, Class K, Class I and Class Z shares, respectively. These waivers/reimbursements may not be terminated before January 29, 2017 and may be extended by the Adviser for additional one-year terms. Absent reimbursements or waivers, performance would have been lower, with the exception of Class 1, Class 2, Class I and Class Z shares, as these share classes are currently operating below their respective contractual expense caps. The Financial Highlights section of this report sets forth expense ratio data for the current reporting period; the expense ratios shown above may differ from the expense ratios in the Financial Highlights sections since they are based on different time periods.

| * | Class 1 shares are only available to Bernstein Global Wealth Management private client accounts. Class 2 shares are only available to the Adviser’s institutional clients or through other limited arrangements. |

| † | Inception dates: 3/8/2010 for all share classes excluding Class Z shares; 1/31/2014 for Class Z shares. |

| ‡ | These share classes are offered at NAV to eligible investors and their SEC returns are the same as their NAV returns. Please note that these share classes are for investors purchasing shares through accounts established under certain fee-based programs sponsored and maintained by certain broker-dealers and financial intermediaries, institutional pension plans and/or investment advisory clients of, and certain other persons associated with, the Adviser and its affiliates or the Fund. |

See Disclosures, Risks and Note about Historical Performance on pages 4-6.

(Historical Performance continued on next page)

| AB ALL MARKET REAL RETURN PORTFOLIO • | 9 |

Historical Performance

HISTORICAL PERFORMANCE

(continued from previous page)

SEC AVERAGE ANNUAL RETURNS AS OF THE MOST RECENT CALENDAR QUARTER-END MARCH 31, 2016 (unaudited) | ||||

SEC Returns (reflects applicable sales charges) | ||||

| Class 1 Shares* | ||||

1 Year | -14.49 | % | ||

5 Years | -7.53 | % | ||

Since Inception† | -2.59 | % | ||

| Class 2 Shares* | ||||

1 Year | -14.30 | % | ||

5 Years | -7.31 | % | ||

Since Inception† | -2.36 | % | ||

| Class A Shares | ||||

1 Year | -18.27 | % | ||

5 Years | -8.42 | % | ||

Since Inception† | -3.36 | % | ||

| Class C Shares | ||||

1 Year | -16.07 | % | ||

5 Years | -8.27 | % | ||

Since Inception† | -3.36 | % | ||

| Advisor Class Shares‡ | ||||

1 Year | -14.37 | % | ||

5 Years | -7.33 | % | ||

Since Inception† | -2.38 | % | ||

| Class R Shares‡ | ||||

1 Year | -14.87 | % | ||

5 Years | -7.82 | % | ||

Since Inception† | -2.89 | % | ||

| Class K Shares‡ | ||||

1 Year | -14.64 | % | ||

5 Years | -7.57 | % | ||

Since Inception† | -2.63 | % | ||

| Class I Shares‡ | ||||

1 Year | -14.43 | % | ||

5 Years | -7.34 | % | ||

Since Inception† | -2.38 | % | ||

| Class Z Shares‡ | ||||

1 Year | -14.38 | % | ||

Since Inception† | -12.32 | % | ||

| * | Class 1 shares are only available to Bernstein Global Wealth Management private client accounts. Class 2 shares are only available to the Adviser’s institutional clients or through other limited arrangements. |

| † | Inception dates: 3/8/2010 for all share classes excluding Class Z shares; 1/31/2014 for Class Z shares. |

| ‡ | Please note that these share classes are for investors purchasing shares through accounts established under certain fee-based programs sponsored and maintained by certain broker-dealers and financial intermediaries, institutional pension plans and/or investment advisory clients of, and certain other persons associated with, the Adviser and its affiliates or the Fund. |

See Disclosures, Risks and Note about Historical Performance on pages 4-6.

| 10 | • AB ALL MARKET REAL RETURN PORTFOLIO |

Historical Performance

EXPENSE EXAMPLE

(unaudited)

As a shareholder of a mutual fund, you may incur two types of costs: (1) transaction costs, including sales charges (loads) on purchase payments, contingent deferred sales charges on redemptions and (2) ongoing costs, including management fees; distribution (12b-1) fees; and other fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The Example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period as indicated below.

Actual Expenses

The table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The table below provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed annual rate of return of 5% before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds by comparing this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads), or contingent deferred sales charges on redemptions. Therefore, the hypothetical example is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| Beginning Account Value November 1, 2015 | Ending Account Value April 30, 2016 | Expenses Paid During Period* | Annualized Expense Ratio* | |||||||||||||

| Class A | ||||||||||||||||

Actual | $ | 1,000 | $ | 1,013.80 | $ | 6.51 | 1.30 | % | ||||||||

Hypothetical** | $ | 1,000 | $ | 1,018.40 | $ | 6.52 | 1.30 | % | ||||||||

| Class C | ||||||||||||||||

Actual | $ | 1,000 | $ | 1,010.70 | $ | 10.10 | 2.02 | % | ||||||||

Hypothetical** | $ | 1,000 | $ | 1,014.82 | $ | 10.12 | 2.02 | % | ||||||||

| Advisor Class | ||||||||||||||||

Actual | $ | 1,000 | $ | 1,015.00 | $ | 5.16 | 1.03 | % | ||||||||

Hypothetical** | $ | 1,000 | $ | 1,019.74 | $ | 5.17 | 1.03 | % | ||||||||

| Class R | ||||||||||||||||

Actual | $ | 1,000 | $ | 1,012.80 | $ | 7.66 | 1.53 | % | ||||||||

Hypothetical** | $ | 1,000 | $ | 1,017.26 | $ | 7.67 | 1.53 | % | ||||||||

| Class K | ||||||||||||||||

Actual | $ | 1,000 | $ | 1,014.20 | $ | 6.41 | 1.28 | % | ||||||||

Hypothetical** | $ | 1,000 | $ | 1,018.50 | $ | 6.42 | 1.28 | % | ||||||||

| AB ALL MARKET REAL RETURN PORTFOLIO • | 11 |

Expense Example

EXPENSE EXAMPLE

(unaudited)

(continued from previous page)

| Beginning Account Value November 1, 2015 | Ending Account Value April 30, 2016 | Expenses Paid During Period* | Annualized Expense Ratio* | |||||||||||||

| Class I | ||||||||||||||||

Actual | $ | 1,000 | $ | 1,016.40 | $ | 4.66 | 0.93 | % | ||||||||

Hypothetical** | $ | 1,000 | $ | 1,020.24 | $ | 4.67 | 0.93 | % | ||||||||

| Class 1 | ||||||||||||||||

Actual | $ | 1,000 | $ | 1,015.50 | $ | 5.81 | 1.16 | % | ||||||||

Hypothetical** | $ | 1,000 | $ | 1,019.10 | $ | 5.82 | 1.16 | % | ||||||||

| Class 2 | ||||||||||||||||

Actual | $ | 1,000 | $ | 1,015.60 | $ | 4.56 | 0.91 | % | ||||||||

Hypothetical** | $ | 1,000 | $ | 1,020.34 | $ | 4.57 | 0.91 | % | ||||||||

| Class Z | ||||||||||||||||

Actual | $ | 1,000 | $ | 1,015.80 | $ | 4.71 | 0.94 | % | ||||||||

Hypothetical** | $ | 1,000 | $ | 1,020.19 | $ | 4.72 | 0.94 | % | ||||||||

| * | Expenses are equal to the Portfolio’s annualized expense ratio, multiplied by the average account value over the period, multiplied by 182/366 (to reflect the one-half year period). |

| ** | Assumes 5% annual return before expenses. |

| 12 | • AB ALL MARKET REAL RETURN PORTFOLIO |

Expense Example

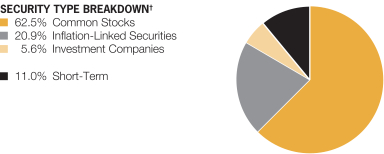

PORTFOLIO SUMMARY

April 30, 2016 (unaudited)

PORTFOLIO STATISTICS

Net Assets ($mil): $568.0

| PORTFOLIO BREAKDOWN* | ||||||

Commodity Related Derivatives | 41.2 | % | ||||

Commodity Related Stocks | 34.9 | % | ||||

Real Estate Stocks | 26.3 | % | ||||

Other | (2.4 | )% | ||||

| * | All data are as of April 30, 2016. The portfolio breakdown is expressed as an approximate percentage of the Fund’s net assets inclusive of derivative exposure, based on the Adviser’s internal classification guidelines. |

| † | The Fund’s security type breakdown is expressed as a percentage of total investments and may vary over time. The Fund also enters into derivative transactions, which may be used for hedging or investment purposes (see “Portfolio of Investments” section of the report for additional details). |

| AB ALL MARKET REAL RETURN PORTFOLIO • | 13 |

Portfolio Summary

TEN LARGEST EQUITY HOLDINGS*

April 30, 2016 (unaudited)

| Company | U.S. $ Value | Percent of Net Assets | ||||||

Exxon Mobil Corp. | $ | 29,598,707 | 5.2 | % | ||||

Royal Dutch Shell PLC – Class A & Class B | 25,471,193 | 4.5 | ||||||

SPDR S&P Dividend ETF | 17,546,040 | 3.1 | ||||||

TOTAL SA | 15,179,473 | 2.7 | ||||||

Chevron Corp. | 14,573,320 | 2.5 | ||||||

Vanguard Dividend Appreciation ETF | 11,322,624 | 2.0 | ||||||

Simon Property Group, Inc. | 8,558,576 | 1.5 | ||||||

BP PLC | 7,391,429 | 1.3 | ||||||

Occidental Petroleum Corp. | 7,389,749 | 1.3 | ||||||

EOG Resources, Inc. | 7,327,485 | 1.3 | ||||||

| $ | 144,358,596 | 25.4 | % | |||||

| * | Long-term investments. |

| 14 | • AB ALL MARKET REAL RETURN PORTFOLIO |

Ten Largest Equity Holdings

CONSOLIDATED PORTFOLIO OF INVESTMENTS

April 30, 2016 (unaudited)

| Company | Shares | U.S. $ Value | ||||||

| ||||||||

COMMON STOCKS – 61.1% | ||||||||

Energy – 26.8% | ||||||||

Integrated Oil & Gas – 17.6% | ||||||||

BP PLC | 1,341,608 | $ | 7,391,429 | |||||

Chevron Corp. | 142,624 | 14,573,320 | ||||||

China Petroleum & Chemical Corp. – Class H | 2,214,000 | 1,562,993 | ||||||

Eni SpA | 8,990 | 146,869 | ||||||

Exxon Mobil Corp. | 334,827 | 29,598,707 | ||||||

Galp Energia SGPS SA | 83,690 | 1,149,853 | ||||||

LUKOIL PJSC (Sponsored ADR) | 48,330 | 2,054,025 | ||||||

Petroleo Brasileiro SA (Sponsored ADR)(a) | 172,330 | 1,016,747 | ||||||

Royal Dutch Shell PLC (Euronext Amsterdam) – Class A | 307,616 | 8,126,563 | ||||||

Royal Dutch Shell PLC – Class A | 412,416 | 10,802,494 | ||||||

Royal Dutch Shell PLC – Class B | 249,178 | 6,542,136 | ||||||

Statoil ASA | 8,085 | 142,306 | ||||||

TOTAL SA | 300,341 | 15,179,473 | ||||||

YPF SA (Sponsored ADR) | 78,350 | 1,578,753 | ||||||

|

| |||||||

| 99,865,668 | ||||||||

|

| |||||||

Oil & Gas Drilling – 0.2% | ||||||||

Helmerich & Payne, Inc. | 18,390 | 1,215,947 | ||||||

|

| |||||||

Oil & Gas Equipment & Services – 0.8% | ||||||||

Aker Solutions ASA(a)(b) | 221,750 | 847,707 | ||||||

Petrofac Ltd. | 89,160 | 1,104,647 | ||||||

RPC, Inc. | 39,140 | 591,797 | ||||||

Schlumberger Ltd. | 7,560 | 607,370 | ||||||

Tenaris SA | 92,000 | 1,244,070 | ||||||

|

| |||||||

| 4,395,591 | ||||||||

|

| |||||||

Oil & Gas Exploration & Production – 7.5% | ||||||||

Anadarko Petroleum Corp. | 77,900 | 4,110,004 | ||||||

California Resources Corp. | 3,488 | 7,674 | ||||||

Canadian Natural Resources Ltd. | 147,040 | 4,415,771 | ||||||

CNOOC Ltd. | 2,513,200 | 3,104,607 | ||||||

Concho Resources, Inc.(a) | 5,600 | 650,552 | ||||||

ConocoPhillips | 103,142 | 4,929,156 | ||||||

Det Norske Oljeselskap ASA(a) | 149,987 | 1,334,442 | ||||||

EOG Resources, Inc. | 88,689 | 7,327,485 | ||||||

Gran Tierra Energy, Inc.(a) | 207,720 | 612,548 | ||||||

Hess Corp. | 70,855 | 4,224,375 | ||||||

Inpex Corp. | 98,100 | 779,879 | ||||||

Murphy Oil Corp. | 54,590 | 1,951,047 | ||||||

Occidental Petroleum Corp. | 96,409 | 7,389,749 | ||||||

Pioneer Natural Resources Co. | 7,527 | 1,250,235 | ||||||

Woodside Petroleum Ltd. | 35,335 | 756,522 | ||||||

|

| |||||||

| 42,844,046 | ||||||||

|

| |||||||

Oil & Gas Refining & Marketing – 0.7% | ||||||||

Cosan SA Industria e Comercio | 82,300 | 761,920 | ||||||

JX Holdings, Inc. | 442,200 | 1,900,534 | ||||||

Tupras Turkiye Petrol Rafinerileri AS | 46,920 | 1,237,536 | ||||||

|

| |||||||

| 3,899,990 | ||||||||

|

| |||||||

| 152,221,242 | ||||||||

|

| |||||||

| AB ALL MARKET REAL RETURN PORTFOLIO • | 15 |

Consolidated Portfolio of Investments

| Company | Shares | U.S. $ Value | ||||||

| ||||||||

Equity: Other – 8.8% | ||||||||

Diversified/Specialty – 6.8% | ||||||||

Alexandria Real Estate Equities, Inc. | 4,974 | $ | 462,333 | |||||

Armada Hoffler Properties, Inc. | 33,380 | 390,546 | ||||||

Ayala Land, Inc. | 696,260 | 513,717 | ||||||

Azrieli Group Ltd. | 2,418 | 96,864 | ||||||

Beni Stabili SpA SIIQ | 70,381 | 52,255 | ||||||

British Land Co. PLC (The) | 66,299 | 697,564 | ||||||

Bumi Serpong Damai Tbk PT | 513,600 | 71,699 | ||||||

Buzzi Unicem SpA | 24,870 | 472,394 | ||||||

CA Immobilien Anlagen AG(a) | 28,362 | 541,765 | ||||||

Canadian Real Estate Investment Trust | 4,912 | 173,390 | ||||||

CapitaLand Ltd. | 168,600 | 388,358 | ||||||

CBRE Group, Inc. – Class A(a) | 16,430 | 486,821 | ||||||

Central Pattana PCL | 89,851 | 135,690 | ||||||

Cheung Kong Property Holdings Ltd. | 400,500 | 2,735,210 | ||||||

Ciputra Development Tbk PT | 760,173 | 71,498 | ||||||

City Developments Ltd. | 41,400 | 256,074 | ||||||

Cofinimmo SA(a) | 1,329 | 165,203 | ||||||

Colony Starwood Homes | 35,080 | 854,900 | ||||||

Country Garden Holdings Co., Ltd. | 480,000 | 188,778 | ||||||

Dalian Wanda Commercial Properties Co., Ltd. – Class H(b)(c)(d) | 45,000 | 291,776 | ||||||

Digital Realty Trust, Inc. | 9,274 | 815,926 | ||||||

East Japan Railway Co. | 4,400 | 387,095 | ||||||

Emira Property Fund Ltd. | 243,820 | 273,361 | ||||||

Evergrande Real Estate Group Ltd. | 355,250 | 263,418 | ||||||

Fastighets AB Balder – Class B(a) | 6,015 | 153,425 | ||||||

Fibra Uno Administracion SA de CV | 155,170 | 368,609 | ||||||

Fonciere Des Regions(a) | 2,331 | 220,526 | ||||||

Forest City Realty Trust, Inc. – Class A | 17,824 | 370,383 | ||||||

Fortress Income Fund Ltd. – Class A | 35,319 | 39,716 | ||||||

Fortress Income Fund Ltd. – Class B | 35,319 | 93,447 | ||||||

Frasers Centrepoint Ltd. | 163,500 | 202,761 | ||||||

Fukuoka REIT Corp. | 210 | 382,730 | ||||||

Gecina SA | 2,459 | 355,349 | ||||||

Globe Trade Centre SA(a) | 22,291 | 41,172 | ||||||

Goldin Properties Holdings Ltd.(a) | 84,000 | 34,748 | ||||||

GPT Group (The) | 311,726 | 1,187,208 | ||||||

Gramercy Property Trust | 144,235 | 1,221,670 | ||||||

Great Portland Estates PLC | 22,410 | 248,487 | ||||||

Growthpoint Properties Ltd. | 166,863 | 295,290 | ||||||

H&R Real Estate Investment Trust | 18,832 | 329,001 | ||||||

Henderson Land Development Co., Ltd. | 66,457 | 414,196 | ||||||

Hufvudstaden AB – Class A | 7,235 | 112,276 | ||||||

Hulic Co., Ltd. | 23,750 | 236,383 | ||||||

IMMOFINANZ AG(a) | 431,620 | 1,018,177 | ||||||

IOI Properties Group Bhd | 128,900 | 79,851 | ||||||

Kaisa Group Holdings Ltd.(a)(c)(d) | 805,000 | 80,947 | ||||||

Kennedy Wilson Europe Real Estate PLC | 56,583 | 901,051 | ||||||

Kiwi Property Group Ltd. | 83,867 | 86,587 | ||||||

| 16 | • AB ALL MARKET REAL RETURN PORTFOLIO |

Consolidated Portfolio of Investments

| Company | Shares | U.S. $ Value | ||||||

| ||||||||

KLCCP Stapled Group | 30,200 | $ | 55,687 | |||||

Land & Houses PCL | 249,200 | 61,355 | ||||||

Land Securities Group PLC | 51,402 | 851,392 | ||||||

Lippo Karawaci Tbk PT | 1,265,600 | 97,242 | ||||||

Longfor Properties Co., Ltd. | 96,700 | 136,159 | ||||||

Mah Sing Group Bhd | 104,150 | 38,902 | ||||||

Mapletree Greater China Commercial Trust(b) | 125,000 | 95,562 | ||||||

Merlin Properties Socimi SA | 97,233 | 1,131,759 | ||||||

Mitsubishi Estate Co., Ltd. | 116,600 | 2,215,704 | ||||||

Mitsui Fudosan Co., Ltd. | 103,400 | 2,525,278 | ||||||

New World Development Co., Ltd. | 541,182 | 538,905 | ||||||

Nomura Real Estate Master Fund, Inc. | 235 | 368,656 | ||||||

Orix JREIT, Inc. | 153 | 254,837 | ||||||

Pakuwon Jati Tbk PT | 1,550,500 | 61,433 | ||||||

Premier Investment Corp. | 470 | 599,731 | ||||||

Pruksa Real Estate PCL | 44,500 | 32,805 | ||||||

Quality Houses PCL | 306,483 | 19,479 | ||||||

Redefine Properties Ltd. | 268,028 | 231,359 | ||||||

Resilient REIT Ltd. | 15,711 | 150,105 | ||||||

SA Corporate Real Estate Fund Nominees Pty Ltd. | 479,843 | 169,223 | ||||||

SM Prime Holdings, Inc. | 517,300 | 249,451 | ||||||

SP Setia Bhd Group | 59,900 | 49,374 | ||||||

Sponda Oyj | 15,599 | 67,929 | ||||||

STORE Capital Corp. | 35,580 | 913,339 | ||||||

Sumitomo Realty & Development Co., Ltd. | 61,700 | 1,794,006 | ||||||

Summarecon Agung Tbk PT | 721,800 | 85,159 | ||||||

Sun Hung Kai Properties Ltd. | 180,923 | 2,280,195 | ||||||

Sunac China Holdings Ltd. | 116,600 | 74,397 | ||||||

Suntec Real Estate Investment Trust | 160,000 | 199,908 | ||||||

Supalai PCL | 40,400 | 23,710 | ||||||

Swiss Prime Site AG (REG)(a) | 4,133 | 362,325 | ||||||

TLG Immobilien AG | 13,470 | 285,324 | ||||||

United Urban Investment Corp. | 438 | 755,990 | ||||||

UOL Group Ltd.(a) | 215,364 | 980,708 | ||||||

VEREIT, Inc. | 62,249 | 552,771 | ||||||

Wallenstam AB – Class B | 13,072 | 109,955 | ||||||

WHA Corp. PCL(a) | 266,200 | 23,168 | ||||||

Wharf Holdings Ltd. (The) | 88,000 | 475,078 | ||||||

WP Carey, Inc. | 6,037 | 368,800 | ||||||

|

| |||||||

| 38,547,785 | ||||||||

|

| |||||||

Health Care – 1.6% | ||||||||

Assura PLC | 288,170 | 238,530 | ||||||

Care Capital Properties, Inc. | 13,582 | 362,232 | ||||||

Chartwell Retirement Residences | 11,684 | 128,788 | ||||||

HCP, Inc. | 31,479 | 1,064,935 | ||||||

LTC Properties, Inc. | 16,470 | 764,043 | ||||||

Medical Properties Trust, Inc. | 43,430 | 578,053 | ||||||

Omega Healthcare Investors, Inc. | 11,278 | 380,858 | ||||||

Ventas, Inc. | 53,543 | 3,326,091 | ||||||

Welltower, Inc. | 31,608 | 2,194,228 | ||||||

|

| |||||||

| 9,037,758 | ||||||||

|

| |||||||

| AB ALL MARKET REAL RETURN PORTFOLIO • | 17 |

Consolidated Portfolio of Investments

| Company | Shares | U.S. $ Value | ||||||

| ||||||||

Triple Net – 0.4% | ||||||||

National Retail Properties, Inc. | 28,926 | $ | 1,265,801 | |||||

Realty Income Corp. | 17,819 | 1,054,885 | ||||||

|

| |||||||

| 2,320,686 | ||||||||

|

| |||||||

| 49,906,229 | ||||||||

|

| |||||||

Materials – 7.3% | ||||||||

Commodity Chemicals – 0.4% | ||||||||

LyondellBasell Industries NV – Class A | 25,480 | 2,106,432 | ||||||

|

| |||||||

Diversified Chemicals – 0.2% | ||||||||

Arkema SA | 15,332 | 1,223,746 | ||||||

|

| |||||||

Diversified Metals & Mining – 2.5% | ||||||||

Antofagasta PLC | 143,740 | 1,018,004 | ||||||

Boliden AB | 58,600 | 1,024,934 | ||||||

First Quantum Minerals Ltd. | 134,060 | 1,142,187 | ||||||

Glencore PLC(a) | 1,526,046 | 3,647,125 | ||||||

Korea Zinc Co., Ltd. | 2,450 | 1,062,394 | ||||||

Lundin Mining Corp.(a) | 164,300 | 645,572 | ||||||

Rio Tinto PLC | 118,040 | 3,959,807 | ||||||

South32 Ltd.(a) | 818,580 | 1,023,747 | ||||||

Syrah Resources Ltd.(a) | 170,230 | 607,483 | ||||||

|

| |||||||

| 14,131,253 | ||||||||

|

| |||||||

Fertilizers & Agricultural Chemicals – 1.2% | ||||||||

Agrium, Inc. (Toronto) | 5,012 | 431,894 | ||||||

CF Industries Holdings, Inc. | 8,364 | 276,598 | ||||||

Monsanto Co. | 33,268 | 3,116,546 | ||||||

Potash Corp. of Saskatchewan, Inc. | 30,968 | 547,931 | ||||||

Syngenta AG (REG) | 3,339 | 1,339,490 | ||||||

UPL Ltd. | 158,480 | 1,287,067 | ||||||

|

| |||||||

| 6,999,526 | ||||||||

|

| |||||||

Forest Products – 0.0% | ||||||||

West Fraser Timber Co., Ltd. | 2,524 | 83,161 | ||||||

|

| |||||||

Gold – 1.7% | ||||||||

Agnico Eagle Mines Ltd. | 32,207 | 1,522,433 | ||||||

Barrick Gold Corp. | 33,890 | 656,449 | ||||||

Barrick Gold Corp. (Toronto) | 69,604 | 1,347,478 | ||||||

Franco-Nevada Corp. | 8,769 | 615,724 | ||||||

Goldcorp, Inc. | 125,997 | 2,538,619 | ||||||

Newcrest Mining Ltd.(a) | 41,327 | 602,615 | ||||||

Newmont Mining Corp. | 30,792 | 1,076,796 | ||||||

Randgold Resources Ltd. | 14,134 | 1,411,820 | ||||||

Real Gold Mining Ltd.(a)(c)(d) | 124,500 | – 0 | –^ | |||||

|

| |||||||

| 9,771,934 | ||||||||

|

| |||||||

Paper Packaging – 0.3% | ||||||||

International Paper Co. | 14,773 | 639,228 | ||||||

Smurfit Kappa Group PLC | 31,450 | 833,646 | ||||||

|

| |||||||

| 1,472,874 | ||||||||

|

| |||||||

| 18 | • AB ALL MARKET REAL RETURN PORTFOLIO |

Consolidated Portfolio of Investments

| Company | Shares | U.S. $ Value | ||||||

| ||||||||

Paper Products – 0.2% | ||||||||

Mondi PLC | 38,183 | $ | 731,378 | |||||

Oji Holdings Corp. | 29,000 | 119,090 | ||||||

Stora Enso Oyj – Class R | 19,796 | 173,078 | ||||||

UPM-Kymmene Oyj | 19,368 | 370,744 | ||||||

|

| |||||||

| 1,394,290 | ||||||||

|

| |||||||

Precious Metals & Minerals – 0.1% | ||||||||

Fresnillo PLC | 12,143 | 197,938 | ||||||

Industrias Penoles SAB de CV | 7,793 | 121,751 | ||||||

Silver Wheaton Corp. | 22,914 | 480,122 | ||||||

|

| |||||||

| 799,811 | ||||||||

|

| |||||||

Silver – 0.2% | ||||||||

Silver Wheaton Corp. | 42,990 | 900,779 | ||||||

|

| |||||||

Specialty Chemicals – 0.1% | ||||||||

Johnson Matthey PLC | 12,674 | 535,665 | ||||||

|

| |||||||

Steel – 0.4% | ||||||||

NLMK PJSC (GDR)(b) | 67,720 | 919,872 | ||||||

Severstal PAO (GDR)(b) | 53,830 | 626,919 | ||||||

voestalpine AG | 16,120 | 581,688 | ||||||

|

| |||||||

| 2,128,479 | ||||||||

|

| |||||||

| 41,547,950 | ||||||||

|

| |||||||

Residential – 5.9% | ||||||||

Multi-Family – 4.6% | ||||||||

Advance Residence Investment Corp. | 85 | 228,937 | ||||||

Apartment Investment & Management Co. – Class A | 10,666 | 427,280 | ||||||

AvalonBay Communities, Inc. | 22,072 | 3,902,109 | ||||||

BUWOG AG(a) | 3,923 | 82,585 | ||||||

Camden Property Trust | 15,498 | 1,251,154 | ||||||

Canadian Apartment Properties REIT | 7,462 | 177,406 | ||||||

China Overseas Land & Investment Ltd. | 834,140 | 2,647,782 | ||||||

China Resources Land Ltd. | 733,908 | 1,801,101 | ||||||

China Vanke Co., Ltd. – Class H | 227,574 | 569,783 | ||||||

CIFI Holdings Group Co., Ltd. | 1,414,000 | 327,212 | ||||||

Comforia Residential REIT, Inc. | 171 | 388,121 | ||||||

Corp. GEO SAB de CV Series B(a) | 236 | 127 | ||||||

Cyrela Brazil Realty SA Empreendimentos e Participacoes | 18,000 | 53,750 | ||||||

Desarrolladora Homex SAB de CV(a) | 1,460 | 289 | ||||||

Deutsche Wohnen AG | 22,404 | 686,948 | ||||||

Emlak Konut Gayrimenkul Yatirim Ortakligi AS | 499,408 | 536,723 | ||||||

Equity Residential | 33,307 | 2,267,207 | ||||||

Essex Property Trust, Inc. | 4,471 | 985,632 | ||||||

Greentown China Holdings Ltd.(a) | 269,500 | 199,929 | ||||||

Independence Realty Trust, Inc. | 120,160 | 861,547 | ||||||

Kenedix Residential Investment Corp. | 130 | 364,455 | ||||||

Killam Apartment Real Estate Investment Trust | 45,570 | 427,480 | ||||||

LEG Immobilien AG(a) | 3,829 | 355,194 | ||||||

| AB ALL MARKET REAL RETURN PORTFOLIO • | 19 |

Consolidated Portfolio of Investments

| Company | Shares | U.S. $ Value | ||||||

| ||||||||

Mid-America Apartment Communities, Inc. | 16,832 | $ | 1,610,990 | |||||

Mirvac Group | 473,460 | 669,866 | ||||||

MRV Engenharia e Participacoes SA | 18,450 | 64,482 | ||||||

Shenzhen Investment Ltd. | 192,000 | 77,202 | ||||||

Shimao Property Holdings Ltd. | 82,500 | 113,864 | ||||||

Sino-Ocean Land Holdings Ltd. | 239,080 | 107,216 | ||||||

Stockland | 150,545 | 497,927 | ||||||

Sun Communities, Inc. | 14,556 | 987,916 | ||||||

UDR, Inc. | 17,751 | 619,865 | ||||||

UNITE Group PLC (The) | 81,573 | 754,308 | ||||||

Urbi Desarrollos Urbanos SAB de CV(a)(c)(d) | 120,400 | – 0 | –^ | |||||

Vonovia SE | 44,901 | 1,513,530 | ||||||

Wing Tai Holdings Ltd. | 620,000 | 863,013 | ||||||

|

| |||||||

| 26,422,930 | ||||||||

|

| |||||||

Self Storage – 1.3% | ||||||||

Big Yellow Group PLC | 43,380 | 510,992 | ||||||

CubeSmart | 28,784 | 852,294 | ||||||

Extra Space Storage, Inc. | 18,416 | 1,564,439 | ||||||

National Storage Affiliates Trust | 11,151 | 217,668 | ||||||

Public Storage | 12,569 | 3,077,017 | ||||||

Safestore Holdings PLC | 68,550 | 339,855 | ||||||

Sovran Self Storage, Inc. | 6,970 | 740,353 | ||||||

|

| |||||||

| 7,302,618 | ||||||||

|

| |||||||

| 33,725,548 | ||||||||

|

| |||||||

Retail – 5.7% | ||||||||

Regional Mall – 2.4% | ||||||||

BR Malls Participacoes SA | 27,840 | 137,045 | ||||||

CapitaLand Mall Trust | 171,300 | 262,971 | ||||||

General Growth Properties, Inc. | 41,687 | 1,168,487 | ||||||

Macerich Co. (The) | 10,735 | 816,719 | ||||||

Multiplan Empreendimentos Imobiliarios SA | 4,980 | 85,359 | ||||||

Pennsylvania Real Estate Investment Trust | 23,990 | 550,331 | ||||||

Simon Property Group, Inc. | 42,544 | 8,558,576 | ||||||

Westfield Corp. | 280,623 | 2,143,287 | ||||||

|

| |||||||

| 13,722,775 | ||||||||

|

| |||||||

Shopping Center/Other Retail – 3.3% | ||||||||

Aeon Mall Co., Ltd. | 25,400 | 349,330 | ||||||

Capital & Counties Properties PLC | 46,655 | 241,388 | ||||||

Capitaland Malaysia Mall Trust | 72,900 | 26,853 | ||||||

Citycon Oyj | 25,490 | 64,631 | ||||||

DDR Corp. | 47,763 | 835,852 | ||||||

Federal Realty Investment Trust | 4,673 | 710,670 | ||||||

Fibra Shop Portafolios Inmobiliarios SAPI de CV | 452,304 | 436,408 | ||||||

Frontier Real Estate Investment Corp. | 92 | 461,466 | ||||||

Hammerson PLC | 50,485 | 432,046 | ||||||

Hyprop Investments Ltd. | 42,535 | 366,775 | ||||||

IGB Real Estate Investment Trust | 110,100 | 42,557 | ||||||

Intu Properties PLC | 60,614 | 269,924 | ||||||

Japan Retail Fund Investment Corp. | 161 | 395,556 | ||||||

| 20 | • AB ALL MARKET REAL RETURN PORTFOLIO |

Consolidated Portfolio of Investments

| Company | Shares | U.S. $ Value | ||||||

| ||||||||

Kimco Realty Corp. | 28,090 | $ | 789,891 | |||||

Kite Realty Group Trust | 31,380 | 854,477 | ||||||

Klepierre | 32,431 | 1,525,310 | ||||||

Link REIT | 326,923 | 1,981,299 | ||||||

Mercialys SA | 29,660 | 660,649 | ||||||

Ramco-Gershenson Properties Trust | 48,983 | 867,489 | ||||||

Regency Centers Corp. | 24,058 | 1,773,075 | ||||||

Retail Opportunity Investments Corp. | 25,637 | 504,280 | ||||||

RioCan Real Estate Investment Trust (Toronto) | 21,724 | 472,329 | ||||||

Scentre Group | 603,779 | 2,143,125 | ||||||

Shaftesbury PLC | 18,034 | 239,879 | ||||||

Smart Real Estate Investment Trust | 7,519 | 201,833 | ||||||

Unibail-Rodamco SE | 6,368 | 1,706,912 | ||||||

Vicinity Centres | 233,980 | 588,129 | ||||||

|

| |||||||

| 18,942,133 | ||||||||

|

| |||||||

| 32,664,908 | ||||||||

|

| |||||||

Office – 3.0% | ||||||||

Office – 3.0% | ||||||||

Allied Properties Real Estate Investment Trust | 25,473 | 717,678 | ||||||

alstria office REIT-AG(a) | 80,173 | 1,125,769 | ||||||

Ascendas India Trust | 45,900 | 32,594 | ||||||

Befimmo SA | 1,103 | 73,772 | ||||||

Boston Properties, Inc. | 25,234 | 3,251,653 | ||||||

Brandywine Realty Trust | 62,870 | 939,906 | ||||||

Castellum AB | 10,700 | 171,398 | ||||||

Cominar Real Estate Investment Trust | 11,472 | 157,995 | ||||||

Derwent London PLC | 6,442 | 309,617 | ||||||

Dream Office Real Estate Investment Trust | 36,075 | 602,064 | ||||||

Entra ASA(b) | 4,099 | 38,706 | ||||||

Fabege AB | 8,676 | 144,884 | ||||||

Green REIT PLC | 43,704 | 72,162 | ||||||

Highwoods Properties, Inc. | 17,330 | 809,831 | ||||||

Hongkong Land Holdings Ltd. | 77,800 | 492,841 | ||||||

ICADE | 8,940 | 703,341 | ||||||

Ichigo Office REIT Investment | 594 | 459,977 | ||||||

Inmobiliaria Colonial SA(a) | 1,166,909 | 896,451 | ||||||

Investa Office Fund | 160,050 | 505,361 | ||||||

Japan Real Estate Investment Corp. | 80 | 498,161 | ||||||

Kenedix Office Investment Corp. – Class A | 127 | 743,593 | ||||||

Kilroy Realty Corp. | 6,323 | 409,794 | ||||||

Liberty Property Trust | 10,245 | 357,551 | ||||||

Mori Hills REIT Investment Corp. | 253 | 379,647 | ||||||

Nippon Building Fund, Inc. | 89 | 563,815 | ||||||

Norwegian Property ASA(a) | 16,700 | 18,646 | ||||||

PSP Swiss Property AG (REG) | 2,632 | 253,841 | ||||||

SL Green Realty Corp. | 6,796 | 714,124 | ||||||

Vornado Realty Trust | 11,687 | 1,118,797 | ||||||

Workspace Group PLC | 57,349 | 700,299 | ||||||

|

| |||||||

| 17,264,268 | ||||||||

|

| |||||||

| AB ALL MARKET REAL RETURN PORTFOLIO • | 21 |

Consolidated Portfolio of Investments

| Company | Shares | U.S. $ Value | ||||||

| ||||||||

Industrials – 1.9% | ||||||||

Industrial Warehouse Distribution – 1.4% | ||||||||

Ascendas Real Estate Investment Trust | 129,200 | $ | 235,801 | |||||

DCT Industrial Trust, Inc. | 24,750 | 999,158 | ||||||

Duke Realty Corp. | 23,622 | 516,613 | ||||||

Global Logistic Properties Ltd. | 205,700 | 291,693 | ||||||

GLP J-Reit | 398 | 483,453 | ||||||

Granite Real Estate Investment Trust | 14,058 | 419,069 | ||||||

Macquarie Mexico Real Estate Management SA de CV(a) | 378,169 | 525,337 | ||||||

PLA Administradora Industrial S de RL de CV(a) | 170,060 | 312,747 | ||||||

Prologis, Inc. | 50,543 | 2,295,157 | ||||||

Pure Industrial Real Estate Trust | 100,660 | 401,132 | ||||||

Rexford Industrial Realty, Inc. | 46,450 | 871,867 | ||||||

Segro PLC | 47,935 | 292,876 | ||||||

Warehouses De Pauw CVA | 5,100 | 464,611 | ||||||

|

| |||||||

| 8,109,514 | ||||||||

|

| |||||||

Mixed Office Industrial – 0.5% | ||||||||

Axiare Patrimonio SOCIMI SA | 31,140 | 474,236 | ||||||

BR Properties SA | 12,640 | 37,745 | ||||||

Goodman Group | 269,617 | 1,404,667 | ||||||

Kungsleden AB | 76,252 | 524,888 | ||||||

|

| |||||||

| 2,441,536 | ||||||||

|

| |||||||

| 10,551,050 | ||||||||

|

| |||||||

Lodging – 0.7% | ||||||||

Lodging – 0.7% | ||||||||

Chesapeake Lodging Trust | 32,160 | 792,101 | ||||||

Host Hotels & Resorts, Inc. | 52,851 | 836,103 | ||||||

Pebblebrook Hotel Trust | 18,890 | 522,120 | ||||||

RLJ Lodging Trust | 26,498 | 558,313 | ||||||

Summit Hotel Properties, Inc. | 67,010 | 763,914 | ||||||

Wyndham Worldwide Corp. | 5,070 | 359,716 | ||||||

|

| |||||||

| 3,832,267 | ||||||||

|

| |||||||

Food Beverage & Tobacco – 0.6% | ||||||||

Agricultural Products – 0.5% | ||||||||

Archer-Daniels-Midland Co. | 52,129 | 2,082,032 | ||||||

Bunge Ltd. | 5,458 | 341,125 | ||||||

Wilmar International Ltd. | 70,700 | 194,211 | ||||||

|

| |||||||

| 2,617,368 | ||||||||

|

| |||||||

Packaged Foods & Meats – 0.1% | ||||||||

Tyson Foods, Inc. – Class A | 8,750 | 575,925 | ||||||

|

| |||||||

| 3,193,293 | ||||||||

|

| |||||||

Real Estate – 0.2% | ||||||||

Developers – 0.0% | ||||||||

Daelim Industrial Co., Ltd. | 3,160 | 250,078 | ||||||

|

| |||||||

Diversified Real Estate Activities – 0.2% | ||||||||

MMC Norilsk Nickel PJSC (ADR) | 64,370 | 950,963 | ||||||

|

| |||||||

| 1,201,041 | ||||||||

|

| |||||||

| 22 | • AB ALL MARKET REAL RETURN PORTFOLIO |

Consolidated Portfolio of Investments

| Company | Shares | U.S. $ Value | ||||||

| ||||||||

Mortgage – 0.2% | ||||||||

Mortgage – 0.2% | ||||||||

Blackstone Mortgage Trust, Inc. – Class A | 14,360 | $ | 394,613 | |||||

Concentradora Hipotecaria SAPI de CV | 251,130 | 364,478 | ||||||

First American Financial Corp. | 10,240 | 368,845 | ||||||

|

| |||||||

| 1,127,936 | ||||||||

|

| |||||||

Total Common Stocks | 347,235,732 | |||||||

|

| |||||||

| Principal Amount (000) | ||||||||

INFLATION-LINKED SECURITIES – 20.4% |

| |||||||

United States – 20.4% | ||||||||

U.S. Treasury Inflation Index | ||||||||

Total Inflation-Linked Securities | $ | 112,855 | 115,924,879 | |||||

|

| |||||||

| Shares | ||||||||

INVESTMENT COMPANIES – 5.5% | ||||||||

Funds and Investment Trusts – 5.5% | ||||||||

iShares US Real Estate ETF | 27,630 | 2,118,392 | ||||||

SPDR S&P Dividend ETF | 217,450 | 17,546,040 | ||||||

Vanguard Dividend Appreciation ETF | 139,820 | 11,322,624 | ||||||

|

| |||||||

Total Investment Companies | 30,987,056 | |||||||

|

| |||||||

WARRANTS – 0.1% | ||||||||

Equity: Other – 0.1% | ||||||||

Diversified/Specialty – 0.0% | ||||||||

Eastern & Oriental Bhd, | 12,100 | 596 | ||||||

|

| |||||||

Health Care – 0.1% | ||||||||

Emaar Properties PJSC, Merrill Lynch Intl & Co., expiring 9/06/18(a) | 75,327 | 139,479 | ||||||

|

| |||||||

| 140,075 | ||||||||

|

| |||||||

Financial: Other – 0.0% | ||||||||

Financial: Other – 0.0% | ||||||||

DLF Ltd., Merrill Lynch Intl & Co., expiring 5/23/18(a) | 29,860 | 58,219 | ||||||

|

| |||||||

Total Warrants | 198,294 | |||||||

|

| |||||||

| AB ALL MARKET REAL RETURN PORTFOLIO • | 23 |

Consolidated Portfolio of Investments

| Company | Contracts | U.S. $ Value | ||||||

| ||||||||

OPTIONS PURCHASED – CALLS – 0.0% | ||||||||

Options on Equity Indices – 0.0% | ||||||||

PowerShares DB US Dollar Index Bullish Fund Expiration: Jun 2016, | 5,100 | $ | 30,600 | |||||

PowerShares DB US Dollar Index Bullish Fund Expiration: Jun 2016, | 63,749 | 159,373 | ||||||

|

| |||||||

Total Options Purchased – Calls | 189,973 | |||||||

|

| |||||||

| Shares | ||||||||

SHORT-TERM INVESTMENTS – 10.7% | ||||||||

Investment Companies – 10.7% | ||||||||

AB Fixed Income Shares, Inc. – Government STIF Portfolio, 0.36%(g)(h) | 60,779,634 | 60,779,634 | ||||||

|

| |||||||

Total Investments – 97.8% | 555,315,568 | |||||||

Other assets less liabilities – 2.2% | 12,694,038 | |||||||

|

| |||||||

Net Assets – 100.0% | $ | 568,009,606 | ||||||

|

| |||||||

FUTURES (see Note D)

| Type | Number of Contracts | Expiration Month | Original Value | Value at April 30, 2016 | Unrealized Appreciation/ (Depreciation) | |||||||||||||||

Purchased Contracts |

| |||||||||||||||||||

Cattle Feeder Futures | 18 | August 2016 | $ | 1,302,039 | $ | 1,263,375 | $ | (38,664 | ) | |||||||||||

Copper Futures | 16 | July 2016 | 868,839 | 913,400 | 44,561 | |||||||||||||||

Corn Futures | 69 | July 2016 | 1,262,041 | 1,351,537 | 89,496 | |||||||||||||||

Gasoline RBOB Futures | 86 | May 2016 | 4,602,785 | 5,795,093 | 1,192,308 | |||||||||||||||

Gasoline RBOB Futures | 47 | June 2016 | 2,557,261 | 3,174,982 | 617,721 | |||||||||||||||

Gold 100 OZ Futures | 91 | June 2016 | 11,137,131 | 11,743,550 | 606,419 | |||||||||||||||

KC HRW Wheat Futures | 14 | July 2016 | 320,466 | 334,950 | 14,484 | |||||||||||||||

Live Cattle Futures | 28 | June 2016 | 1,354,946 | 1,287,160 | (67,786 | ) | ||||||||||||||

LME Nickel Futures | 15 | May 2016 | 764,828 | 847,530 | 82,702 | |||||||||||||||

LME Zinc Futures | 9 | June 2016 | 426,632 | 435,375 | 8,743 | |||||||||||||||

Palladium Futures | 9 | June 2016 | 449,483 | 564,885 | 115,402 | |||||||||||||||

Platinum Futures | 5 | July 2016 | 249,838 | 269,600 | 19,762 | |||||||||||||||

Silver Futures | 78 | July 2016 | 6,614,076 | 6,949,410 | 335,334 | |||||||||||||||

Soybean Futures | 31 | July 2016 | 1,464,842 | 1,596,113 | 131,271 | |||||||||||||||

Soybean Meal Futures | 47 | July 2016 | 1,374,978 | 1,573,560 | 198,582 | |||||||||||||||

Sold Contracts | ||||||||||||||||||||

LME Nickel Futures | 8 | May 2016 | 436,724 | 452,016 | (15,292 | ) | ||||||||||||||

LME PRI Aluminum Futures | 46 | June 2016 | 1,820,597 | 1,931,713 | (111,116 | ) | ||||||||||||||

|

| |||||||||||||||||||

| $ | 3,223,927 | |||||||||||||||||||

|

| |||||||||||||||||||

| 24 | • AB ALL MARKET REAL RETURN PORTFOLIO |

Consolidated Portfolio of Investments

FORWARD CURRENCY EXCHANGE CONTRACTS (see Note D)

| Counterparty | Contracts to Deliver | In Exchange For | Settlement Date | Unrealized Appreciation/ (Depreciation) | ||||||||||||||||||||

Bank of America, NA | JPY | 598,476 | USD | 5,386 | 6/17/16 | $ | (244,539 | ) | ||||||||||||||||

Bank of America, NA | SEK | 10,036 | USD | 1,188 | 6/17/16 | (63,279 | ) | |||||||||||||||||

Bank of America, NA | USD | 2,554 | JPY | 287,240 | 6/17/16 | 148,717 | ||||||||||||||||||

Bank of America, NA | USD | 3,121 | RUB | 243,742 | 6/17/16 | 599,470 | ||||||||||||||||||

Bank of America, NA | USD | 3,467 | RUB | 226,995 | 6/17/16 | (1,511 | ) | |||||||||||||||||

Barclays Bank PLC | AUD | 5,200 | USD | 3,853 | 6/17/16 | (93,221 | ) | |||||||||||||||||

Barclays Bank PLC | EUR | 1,262 | USD | 1,377 | 6/17/16 | (69,851 | ) | |||||||||||||||||

Barclays Bank PLC | GBP | 5,237 | USD | 7,299 | 6/17/16 | (353,892 | ) | |||||||||||||||||

Barclays Bank PLC | INR | 55,489 | USD | 812 | 6/17/16 | (16,798 | ) | |||||||||||||||||

Barclays Bank PLC | KRW | 5,460,984 | USD | 4,505 | 6/17/16 | (254,855 | ) | |||||||||||||||||

Barclays Bank PLC | TWD | 134,575 | USD | 4,089 | 6/17/16 | (76,909 | ) | |||||||||||||||||

Barclays Bank PLC | USD | 3,551 | EUR | 3,112 | 6/17/16 | 17,519 | ||||||||||||||||||

Barclays Bank PLC | USD | 1,618 | JPY | 179,774 | 6/17/16 | 73,092 | ||||||||||||||||||

Barclays Bank PLC | USD | 5,973 | RUB | 437,081 | 6/17/16 | 699,030 | ||||||||||||||||||

BNP Paribas SA | USD | 5,669 | JPY | 604,411 | 6/17/16 | 18,299 | ||||||||||||||||||

BNP Paribas SA | USD | 10,833 | NOK | 89,099 | 6/17/16 | 230,045 | ||||||||||||||||||

BNP Paribas SA | USD | 568 | SGD | 788 | 6/17/16 | 16,941 | ||||||||||||||||||

Citibank | EUR | 26,798 | USD | 29,868 | 6/17/16 | (858,445 | ) | |||||||||||||||||

Citibank | GBP | 2,968 | USD | 4,224 | 6/17/16 | (113,506 | ) | |||||||||||||||||

Deutsche Bank AG | BRL | 4,054 | USD | 1,147 | 5/03/16 | (31,279 | ) | |||||||||||||||||

Deutsche Bank AG | USD | 1,175 | BRL | 4,054 | 5/03/16 | 3,945 | ||||||||||||||||||

Deutsche Bank AG | USD | 1,127 | BRL | 4,054 | 7/05/16 | 28,264 | ||||||||||||||||||

Goldman Sachs Bank USA | JPY | 396,789 | USD | 3,539 | 6/17/16 | (194,341 | ) | |||||||||||||||||

Goldman Sachs Bank USA | RUB | 192,367 | USD | 2,750 | 6/17/16 | (186,846 | ) | |||||||||||||||||

Goldman Sachs Bank USA | USD | 4,207 | CNY | 27,428 | 6/17/16 | 14,535 | ||||||||||||||||||

Goldman Sachs Bank USA | USD | 8,966 | JPY | 1,005,295 | 6/17/16 | 493,177 | ||||||||||||||||||

Goldman Sachs Bank USA | USD | 2,292 | RUB | 174,276 | 6/17/16 | 368,757 | ||||||||||||||||||

HSBC Bank USA | CAD | 1,869 | USD | 1,406 | 6/17/16 | (83,144 | ) | |||||||||||||||||

HSBC Bank USA | GBP | 1,153 | USD | 1,647 | 6/17/16 | (38,277 | ) | |||||||||||||||||

HSBC Bank USA | USD | 5,197 | CAD | 6,560 | 6/17/16 | 31,594 | ||||||||||||||||||

HSBC Bank USA | USD | 1,565 | SEK | 12,839 | 6/17/16 | 35,863 | ||||||||||||||||||

JPMorgan Chase Bank | NOK | 42,726 | USD | 5,024 | 6/17/16 | (281,769 | ) | |||||||||||||||||

JPMorgan Chase Bank | USD | 4,332 | GBP | 3,028 | 6/17/16 | 92,548 | ||||||||||||||||||

JPMorgan Chase Bank | USD | 2,448 | JPY | 265,759 | 6/17/16 | 52,794 | ||||||||||||||||||

JPMorgan Chase Bank | USD | 5,681 | NOK | 45,824 | 6/17/16 | 8,853 | ||||||||||||||||||

JPMorgan Chase Bank | USD | 5,343 | TRY | 15,678 | 6/17/16 | 190,989 | ||||||||||||||||||

Morgan Stanley & Co., Inc. | EUR | 1,688 | USD | 1,914 | 6/17/16 | (21,874 | ) | |||||||||||||||||

Morgan Stanley & Co., Inc. | USD | 5,690 | AUD | 7,366 | 6/17/16 | (99,308 | ) | |||||||||||||||||

Morgan Stanley & Co., Inc. | USD | 5,598 | AUD | 7,382 | 6/17/16 | 4,712 | ||||||||||||||||||

Morgan Stanley & Co., Inc. | USD | 10,696 | EUR | 9,519 | 6/17/16 | 218,356 | ||||||||||||||||||

Morgan Stanley & Co., Inc. | USD | 2,324 | ZAR | 36,491 | 6/17/16 | 216,489 | ||||||||||||||||||

Nomura Global Financial Products, Inc. | JPY | 329,801 | USD | 2,950 | 6/17/16 | (152,771 | ) | |||||||||||||||||

Nomura Global Financial Products, Inc. | USD | 4,863 | TWD | 156,895 | 6/17/16 | (7,116 | ) | |||||||||||||||||

Royal Bank of Scotland PLC | GBP | 1,376 | USD | 1,968 | 6/17/16 | (43,159 | ) | |||||||||||||||||

Royal Bank of Scotland PLC | USD | 5,691 | BRL | 20,861 | 6/17/16 | 287,694 | ||||||||||||||||||

Royal Bank of Scotland PLC | USD | 5,083 | CAD | 6,633 | 6/17/16 | 203,428 | ||||||||||||||||||

Royal Bank of Scotland PLC | USD | 3,210 | HKD | 24,889 | 6/17/16 | 259 | ||||||||||||||||||

Royal Bank of Scotland PLC | USD | 4,841 | KRW | 5,604,850 | 6/17/16 | 44,285 | ||||||||||||||||||

Royal Bank of Scotland PLC | USD | 887 | MYR | 3,695 | 6/17/16 | 55,166 | ||||||||||||||||||

Royal Bank of Scotland PLC | USD | 5,179 | ZAR | 82,675 | 6/17/16 | 577,306 | ||||||||||||||||||

Societe Generale | EUR | 3,112 | USD | 3,457 | 6/17/16 | (111,670 | ) | |||||||||||||||||

Societe Generale | NOK | 47,032 | USD | 5,471 | 6/17/16 | (369,096 | ) | |||||||||||||||||

| AB ALL MARKET REAL RETURN PORTFOLIO • | 25 |

Consolidated Portfolio of Investments

| Counterparty | Contracts to Deliver (000) | In Exchange For | Settlement Date | Unrealized Appreciation/ (Depreciation) | ||||||||||||||||||||

Standard Chartered Bank | CNY | 23,168 | USD | 3,524 | 6/17/16 | $ | (41,197 | ) | ||||||||||||||||

Standard Chartered Bank | GBP | 2,012 | USD | 2,859 | 6/17/16 | (81,245 | ) | |||||||||||||||||

Standard Chartered Bank | USD | 754 | IDR | 10,096,953 | 6/17/16 | 5,188 | ||||||||||||||||||

State Street Bank & Trust Co. | USD | 1,009 | BRL | 4,054 | 5/03/16 | 170,087 | ||||||||||||||||||

State Street Bank & Trust Co. | CAD | 16,175 | USD | 12,080 | 6/17/16 | (812,018 | ) | |||||||||||||||||

State Street Bank & Trust Co. | EUR | 1,163 | USD | 1,300 | 6/17/16 | (33,819 | ) | |||||||||||||||||

State Street Bank & Trust Co. | NOK | 2,365 | USD | 278 | 6/17/16 | (15,407 | ) | |||||||||||||||||

State Street Bank & Trust Co. | NZD | 58 | USD | 39 | 6/17/16 | (1,454 | ) | |||||||||||||||||

State Street Bank & Trust Co. | TRY | 3,455 | USD | 1,154 | 6/17/16 | (65,750 | ) | |||||||||||||||||

State Street Bank & Trust Co. | USD | 4,583 | JPY | 516,306 | 6/17/16 | 274,495 | ||||||||||||||||||

State Street Bank & Trust Co. | USD | 5,766 | NOK | 49,397 | 6/17/16 | 367,842 | ||||||||||||||||||

UBS AG | CAD | 2,600 | USD | 1,897 | 6/17/16 | (175,176 | ) | |||||||||||||||||

UBS AG | USD | 1,729 | CHF | 1,709 | 6/17/16 | 55,607 | ||||||||||||||||||

|

| |||||||||||||||||||||||

| $ | 611,824 | |||||||||||||||||||||||

|

| |||||||||||||||||||||||

INFLATION (CPI) SWAPS (see Note D)

| Rate Type | ||||||||||||||||

Swap Counterparty | Notional Amount (000) | Termination Date | Payments made by the | Payments received by the Fund | Unrealized Appreciation/ (Depreciation) | |||||||||||

Deutsche Bank AG | $ | 43,120 | 3/09/19 | 1.508% | CPI# | $ | 221,811 | |||||||||

Deutsche Bank AG | 8,719 | 3/25/25 | 2.205% | CPI# | (88,056 | ) | ||||||||||

Deutsche Bank AG | 38,982 | 3/25/25 | 2.205% | CPI# | (393,691 | ) | ||||||||||

Deutsche Bank AG | 46,779 | 3/25/25 | 2.205% | CPI# | (472,435 | ) | ||||||||||

Deutsche Bank AG | 18,987 | 3/26/25 | 2.195% | CPI# | (182,288 | ) | ||||||||||

Deutsche Bank AG | 37,975 | 3/26/25 | 2.170% | CPI# | (318,556 | ) | ||||||||||

Deutsche Bank AG | 54,500 | 7/30/25 | 2.278% | CPI# | (656,629 | ) | ||||||||||

JPMorgan Chase Bank, NA | 76,719 | 3/30/25 | 2.170% | CPI# | (637,744 | ) | ||||||||||

JPMorgan Chase Bank, NA | 76,719 | 4/01/25 | 2.170% | CPI# | (637,425 | ) | ||||||||||

|

| |||||||||||||||

| $ | (3,165,013 | ) | ||||||||||||||

|

| |||||||||||||||

| # | Variable interest rate based on the rate of inflation as determined by the Consumer Price Index (CPI). |

TOTAL RETURN SWAPS (see Note D)

Counterparty & Referenced Obligation | # of Shares or Units | Rate Paid/ Received | Notional Amount (000) | Maturity Date | Unrealized Appreciation/ (Depreciation) | |||||||||||||||

Receive Total Return on Reference Obligation |

| |||||||||||||||||||

Goldman Sachs International Bloomberg Commodity Index 2 Month Forwards | 457,386 | 0.11 | % | 81,292 | 6/15/16 | $ | 5,026,520 | |||||||||||||

JPMorgan Chase Bank, NA BBG industrial Metals | 29,150 | 0.09 | % | 2,737 | 7/15/16 | 150,059 | ||||||||||||||

BBG industrial Metals | 28,610 | 0.09 | % | 2,780 | 7/15/16 | 54,112 | ||||||||||||||

Bloomberg Agriculture Subindex | 99,297 | 0.15 | % | 5,615 | 7/15/16 | 50,483 | ||||||||||||||

Bloomberg Commodity Index 2 Month Forwards | 478,021 | 0.11 | % | 84,960 | 6/15/16 | 5,253,292 | ||||||||||||||

Bloomberg Commodity Index 2 Month Forwards | 55,933 | 0.11 | % | 9,941 | 6/15/16 | 614,685 | ||||||||||||||

|

| |||||||||||||||||||

| $ | 11,149,151 | |||||||||||||||||||

|

| |||||||||||||||||||

| 26 | • AB ALL MARKET REAL RETURN PORTFOLIO |

Consolidated Portfolio of Investments

| ^ | Less than $0.50. |

| (a) | Non-income producing security. |

| (b) | Security is exempt from registration under Rule 144A of the Securities Act of 1933. These securities are considered liquid and may be resold in transactions exempt from registration, normally to qualified institutional buyers. At April 30, 2016, the aggregate market value of these securities amounted to $2,820,542 or 0.5% of net assets. |

| (c) | Illiquid security. |

| (d) | Fair valued by the Adviser. |

| (e) | Position, or a portion thereof, has been segregated to collateralize OTC derivatives outstanding. |

| (f) | One contract relates to 100 shares. |

| (g) | Investment in affiliated money market mutual fund. The rate shown represents the 7-day yield as of period end. |

| (h) | To obtain a copy of the fund’s financial statements, please go to the Securities and Exchange Commission’s website at www.sec.gov, or call AB at (800) 227-4618. |

Currency Abbreviations:

AUD – Australian Dollar

BRL – Brazilian Real

CAD – Canadian Dollar

CHF – Swiss Franc

CNY – Chinese Yuan Renminbi

EUR – Euro

GBP – Great British Pound

HKD – Hong Kong Dollar

IDR – Indonesian Rupiah

INR – Indian Rupee

JPY – Japanese Yen

KRW – South Korean Won

MYR – Malaysian Ringgit

NOK – Norwegian Krone

NZD – New Zealand Dollar

RUB – Russian Ruble

SEK – Swedish Krona

SGD – Singapore Dollar

TRY – Turkish Lira

TWD – New Taiwan Dollar

USD – United States Dollar

ZAR – South African Rand

Glossary:

ADR – American Depositary Receipt

ETF – Exchange Traded Fund

GDR – Global Depositary Receipt

J-REIT – Japanese Real Estate Investment Trust

KC HRW – Kansas City Hard Red Winter

LME – London Metal Exchange

PJSC – Public Joint Stock Company

REG – Registered Shares

REIT – Real Estate Investment Trust

SPDR – Standard & Poor’s Depository Receipt

See notes to consolidated financial statements.

| AB ALL MARKET REAL RETURN PORTFOLIO • | 27 |

Consolidated Portfolio of Investments

CONSOLIDATED STATEMENT OF ASSETS & LIABILITIES

April 30, 2016 (unaudited)

| Assets | ||||

Investments in securities, at value | ||||

Unaffiliated issuers (cost $486,760,676) | $ | 494,535,934 | ||

Affiliated issuers (cost $60,779,634) | 60,779,634 | |||

Cash collateral due from broker | 2,244,995 | |||

Foreign currencies, at value (cost $2,522,383) | 2,545,230 | |||

Unrealized appreciation on total return swaps | 11,149,151 | |||

Unrealized appreciation on forward currency exchange contracts | 5,605,346 | |||

Receivable for investment securities sold and foreign currency transactions | 3,550,043 | |||

Interest and dividends receivable | 1,447,406 | |||

Receivable for capital stock sold | 789,412 | |||

Receivable for variation margin on exchange-traded derivatives | 325,292 | |||

Unrealized appreciation on inflation swaps | 221,811 | |||

|

| |||

Total assets | 583,194,254 | |||

|

| |||

| Liabilities | ||||

Unrealized depreciation on forward currency exchange contracts | 4,993,522 | |||