November 29, 2006

SECURED FINANCING

PRESENTATION

Alan Mulally

President and CEO

SLIDE 1

•

Sales and Revenue -- About 6.8 million unit sales and $150 billion of Automotive revenue in 2005

•

Valuable Brands -- Ford, Lincoln, Mercury, Volvo, Jaguar, Land Rover, Ford Credit

•

Global Reach -- Manufacture on six continents, with distribution in over 200 markets

FORD MOTOR COMPANY

SUBSTANTIAL RESOURCES

SLIDE 2

Industry

•

Increasingly competitive, changing consumer preferences, and excess capacity

•

Rising health care and commodity costs

•

Fragile supply base in North America

Ford

•

Market share declining in North America, stable in Europe and South America, growing in Asia, and stable / growing for Ford’s premium brands (P.A.G.)

•

Manufacturing capacity exceeds demand

•

Cost structure not competitive

•

Business units not well integrated; complexity level high

DEALING WITH OUR REALITY

PRESENT SITUATION

SLIDE 3

•

Operate as one company

–

Leverage global assets

–

Integrate regional business units

–

Accelerate product development efforts -- increase scale and efficient designs

•

North America is top priority

–

Home market drives profitability

–

New products to stabilize share

–

Align capacity with demand

•

Working together

DEVELOPING A BETTER PLAN

OPPORTUNITIES GOING FORWARD

SLIDE 4

KEY INVESTMENT HIGHLIGHTS

•

Dealing with our reality

–

Identifying opportunities to enhance our business model

•

Accelerating actions to improve our cost structure

–

Personnel reductions

–

Capacity reductions

–

Supply base restructuring

•

Continue to invest in new products

–

Leveraging our global product development and production systems

–

Developing more new products to deliver profitable growth

•

Building substantial liquidity to

–

Execute the plan

–

Provide cushion for unexpected events

TRANSFORMING THE COMPANY

SLIDE 5

Don Leclair

Chief Financial Officer

SLIDE 6

OVERVIEW

•

Present Results

•

Key Elements of Plan

–

North America Automotive

–

International Automotive

–

Ford Credit

•

Outlook

SLIDE 7

* Excludes special items; see Appendix (pages 1 and 2) for reconciliation to GAAP

Memo:

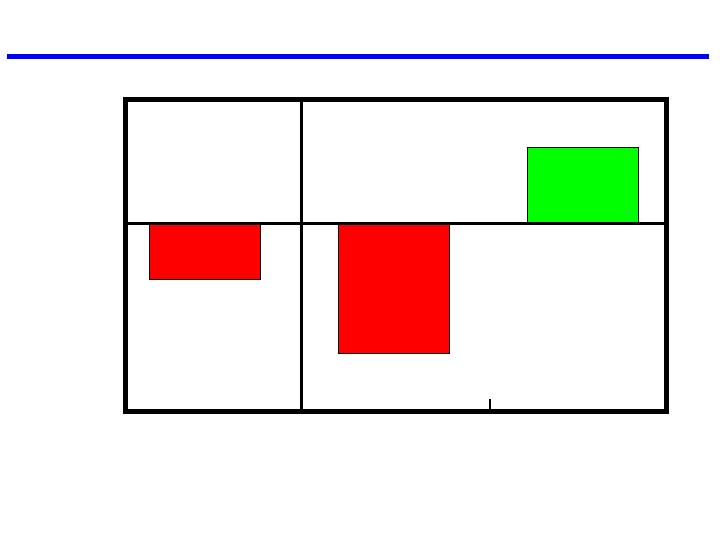

Net Income $(6,988) $(7,992) $1,004

Financial

Services

Automotive

(Mils.)

Total

$(1,208)

$1,550

$(2,758)

TOTAL COMPANY

2006 FIRST NINE MONTHS PRE-TAX PROFIT / (LOSS) BY SECTOR*

SLIDE 8

* Excludes special items; see Appendix (pages 1 and 2) for reconciliation to GAAP

Other

Auto.

North

America

Europe

Asia Pacific

& Africa

(Mils.)

$(2,758)

$306

$(3,287)

P.A.G.

South

America

$(518)

$117

Mazda &

Assoc.

Operations

$(50)

Total

Automotive

$237

$437

AUTOMOTIVE SECTOR

2006 FIRST NINE MONTHS PROFIT / (LOSS) BY SEGMENT*

SLIDE 9

* Excludes special items; see Appendix (pages 1 and 2) for reconciliation to GAAP

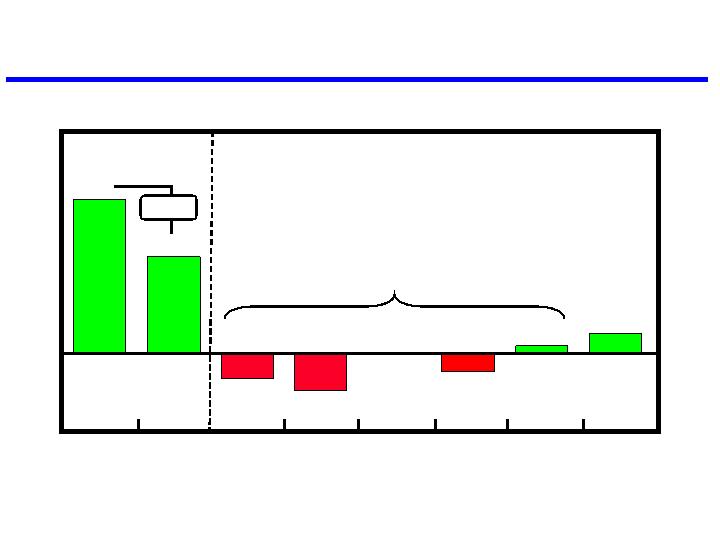

(Bils.)

$(1.5)

2005

Net

Pricing

Cost

Changes

$1.1

Volume /

Mix

2006

$(2.8)

Other

$(0.4)

$(1.9)

$(0.9)

$(0.5)

Exchange

$(1.0)

Interest

$0.4

AUTOMOTIVE SECTOR

2006 FIRST NINE MONTHS AUTOMOTIVE PRE-TAX PROFIT

COMPARED WITH 2005*

SLIDE 10

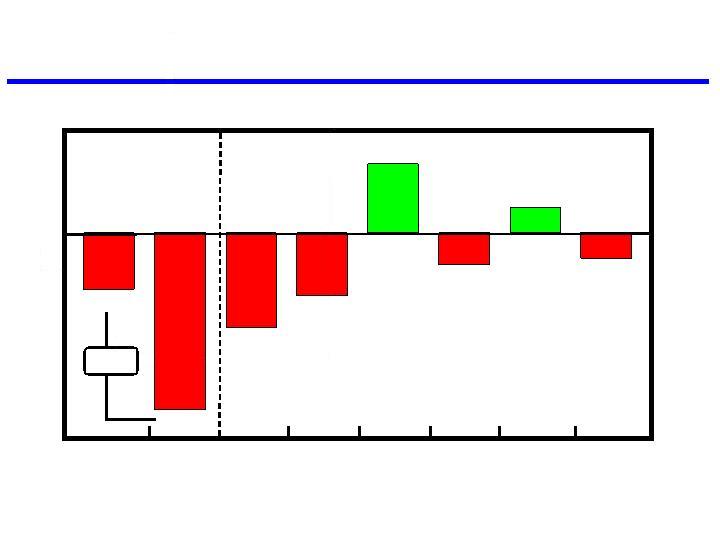

(Bils.)

$(0.6)

$(0.4)

Financing

Margin

Lease

Residual

$0

Volume

2006

$(0.3)

SFAS 133

2005

Credit

Loss

$1.5

$2.4

Other

$0.1

$0.3

$(1.2)

FINANCIAL SERVICES SECTOR

2006 FIRST NINE MONTHS FORD CREDIT PRE-TAX PROFIT

COMPARED WITH 2005*

$(0.9)

* Excludes special items; see Appendix (pages 1 and 2) for reconciliation to GAAP

SLIDE 11

OVERVIEW

•

Present Results

•

Key Elements of Plan

–

North America Automotive

–

International Automotive

–

Ford Credit

•

Outlook

SLIDE 12

AUTOMOTIVE SECTOR -- FORD NORTH AMERICA

KEY ELEMENTS OF PLAN

•

Restructuring

–

Rationalize capacity

–

Salaried-related and hourly personnel reductions

–

Sell / close Automotive Component Holdings plants

•

Competitive costs

–

Achieve competitive levels of engineering and investment

efficiency

–

Leverage global resources and assets (i.e., greater product commonality) and enable greater supplier efficiencies

–

Competitive manufacturing footprint

•

Rebuild the brand strength and reputation

–

Customer focused, exciting products

–

Competitive quality

SLIDE 13

AUTOMOTIVE SECTOR -- FORD NORTH AMERICA

SIXTEEN NEW / MAJOR PRODUCT ACTIONS BY END OF 2008

2006

2007

2008

Expedition Navigator L “Fairlane”

Expedition EL F-Series Super Duty MKS (new Lincoln sedan)

Navigator Escape F-150

Edge Mariner Fusion

MKX Focus Milan

MKZ

SLIDE 14

Ford Edge

Lincoln MKX

AUTOMOTIVE SECTOR -- FORD NORTH AMERICA

These photos cannot be guaranteed to be product correct.

SLIDE 15

AUTOMOTIVE SECTOR -- FORD NORTH AMERICA

These photos cannot be guaranteed to be product correct.

2008 F-250 Super Duty

SLIDE 16

AUTOMOTIVE SECTOR -- FORD NORTH AMERICA

These photos cannot be guaranteed to be product correct.

“Fairlane” Concept

SLIDE 17

AUTOMOTIVE SECTOR -- FORD NORTH AMERICA

These photos cannot be guaranteed to be product correct.

Lincoln MKS

SLIDE 18

17.2%

15.5%

Second

Quarter

Third

Quarter

Fleet

Retail

16.7%

6.1%

6.4%

3.8%

10.8%

11.7%

10.6%

2008 Target

Total Share: 14-15%

Fleet Share: Lower

* Ford and Lincoln Mercury

16.4%

5.4%

11.0%

First Nine

Months

2006

AUTOMOTIVE SECTOR -- FORD NORTH AMERICA

U.S. MARKET SHARE*

First

Quarter

SLIDE 19

Salaried Equivalent Positions

December 31,

2005

September 30,

2006

Hourly ACH Employees

42,500

38,500

85,600

55,000 – 60,000

Hourly (Excluding ACH)

13,900

12,200

AUTOMOTIVE SECTOR -- FORD NORTH AMERICA

PERSONNEL REDUCTIONS FROM YEAR-END 2005

December 31,

2005

2008

Target

September 30,

2006

28,500

79,300

December 31,

2005

2008

Target

September 30,

2006

2008

Target

Redeploy /

Separate

Reduction

From

12/31/2005

14,000

25,000 – 30,000

Redeploy /

Separate

SLIDE 20

(Millions - Annualized)

Maximum Installed Capacity

Manned Straight-Time Capacity

Fourth Quarter

2005

Fourth Quarter

2006

2008 Targets

AUTOMOTIVE SECTOR -- FORD NORTH AMERICA

ASSEMBLY CAPACITY

Installed 84%

Manned 100

2008

Utilization

SLIDE 21

AUTOMOTIVE SECTOR -- FORD NORTH AMERICA

AUTOMOTIVE PRE-TAX PROFIT -- 2009 COMPARED WITH 2006

* Excluding special items; see Appendix (pages 1 and 2)

2006

2008

2009

(Bils.)

$0

Loss*

Profit

Cost

Reductions

Non-Repeat

of 2006

Dealer Inventory

Reductions

Cost

Reductions

Loss

~ $4.0

+

2006 - 2008

Cost Improvement

2006 ~ $1.0

2007 - 2008 ~ 4.0

Total $5.0

Other

Market

Factors

Market

Factors

-

-

SLIDE 22

OVERVIEW

•

Present Results

•

Key Elements of Plan

–

North America Automotive

–

International Automotive

–

Ford Credit

•

Outlook

SLIDE 23

Financial Results - Profitable with three year trend of improving results

Market Share - Stable in Western Europe

- Growth in Central and Eastern Europe

Product - Increasing use of global platforms

Manufacturing - Continuing to migrate to lower-cost areas

AUTOMOTIVE SECTOR

FORD EUROPE

SLIDE 24

Volvo

Financial Results - - 2006 challenging year; reflects end of several old models prior to major new

product introductions

Market Share - - Product-driven improvements expected

Product - More common platforms, shared across brands

Manufacturing - Reducing structure; improving efficiency

Jaguar / Land Rover

Financial Results - Working to return Jaguar to profitability and continued improvement in

Land Rover

Market Share - - Declining at Jaguar, consistent with planned brand repositioning

- Improving at Land Rover, reflecting new products

Product - New Freelander / LR2 based on global platform

Manufacturing - Reduced structure through consolidation

AUTOMOTIVE SECTOR

PREMIER AUTOMOTIVE GROUP

SLIDE 25

Asia Pacific and Mazda

Financial Results - 2006 difficult; reflects segment shifts in Australia and industry weakness in

Taiwan

- Mazda continues to perform well

Market Share - Strong growth in China and India

Product - More common platforms

- Continued introduction of new products

Manufacturing - Plan to rationalize product development, manufacturing operations, and

supply base

South America Performing well on all fronts

AUTOMOTIVE SECTOR

REST OF WORLD

SLIDE 26

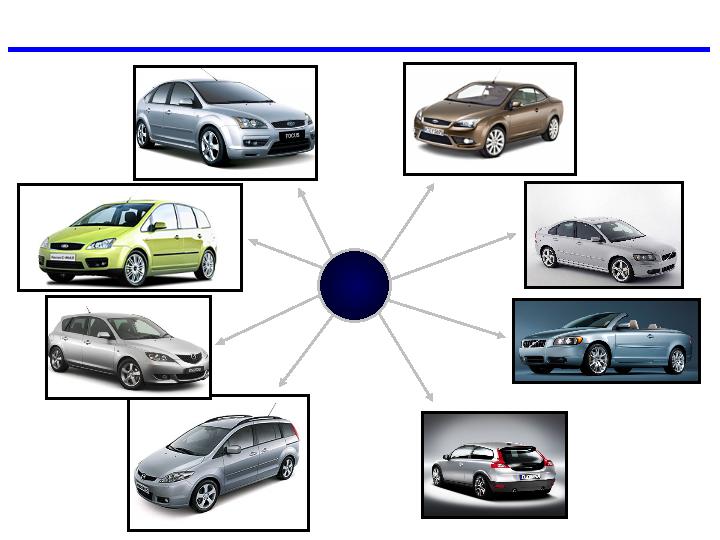

Global Focus

Focus Coupe / Cabriolet

Volvo C70

C-MAX

Mazda5 Hatchback

Volvo C30

INCREASED APPLICATION OF COMMON PLATFORMS

AUTOMOTIVE SECTOR -- INTERNATIONAL OPERATIONS

Mazda3 Hatchback

C

Volvo S40

SLIDE 27

CD

Ford Mondeo

Ford Galaxy

Ford S-MAX

Land Rover LR2

INCREASED APPLICATION OF COMMON PLATFORMS

AUTOMOTIVE SECTOR – INTERNATIONAL OPERATIONS

Volvo S80

Next-Gen Volvo V70 / XC70

Next –Gen Volvo S60

SLIDE 28

OVERVIEW

•

Present Results

•

Key Elements of Plan

–

North America Automotive

–

International Automotive

–

Ford Credit

•

Outlook

SLIDE 29

Receivables (Bils.)

On-Balance Sheet $114 $135

Securitized Off-Balance Sheet 35 13

Managed $149 $148

Charge-Offs (Mils.)

On-Balance Sheet $493 $334

Managed 609 399

Loss-to-Receivables Ratio

On-Balance Sheet 0.53% 0.33%

Managed

- U.S. Retail and Lease 0.75 0.50

- Worldwide Total 0.50 0.36

Allowance for Credit Losses

Worldwide Amount (Bils.) $ 1.8 $ 1.3

Percentage Of EOP Receivables 1.52% 0.93%

Leverage (To 1)

Financial Statement 10.6 11.4

Managed 12.5 11.4

Dividend (Bils.) $ 2.6 $ 1.0

2005

2006

Key Metrics**

Net Income (Mils.) $1,599 $1,004

ROE 17.7% 11.8%

* Excludes special items; see Appendix (pages 1 and 2) for reconciliation to GAAP

Pre-Tax Profits (Mils.)*

2005

2006

$2,441

$1,547

Nine Months

**See Appendix (pages 3-5) for calculation, definitions and

reconciliation to GAAP

FINANCIAL SERVICES SECTOR

FORD CREDIT RESULTS AND METRICS -- 2006 FIRST NINE MONTHS

$(894)

SLIDE 30

Operating

•

Ford Credit is a key part of Ford Motor Company’s strategy

•

Continuing to improve on operating excellence

-

Consolidating field and customer operations to improve process efficiencies, reduce costs, and provide flexibility

-

Receivables are high quality; portfolio continues to perform well

Funding

•

Ford Credit plan consistent with Ford Motor Company strategy

-

Reduce managed receivables

-

Suspend dividend to Ford Motor Company beginning in 2007

-

Increase equity in Ford Credit as earnings are retained to support funding

•

Maintain strong and diverse funding sources

-

Keep large cash balance and substantial committed capacity

-

Continue to add committed asset-backed funding capacity and capabilities

beyond present needs (including outside U.S.)

-

Participate in whole-loan market

-

Issue unsecured term debt when it makes sense

-

Participate in various alternative business arrangements

FINANCIAL SERVICES SECTOR

FORD CREDIT STRATEGY

Continue to add committed asset-backed funding capacity and capabilities beyond present needs (including outside U.S.)

Participate in various alternative business arrangements

-

Participate in whole-loan market

Issue unsecured term debt when it makes sense

-

-

-

SLIDE 31

OVERVIEW

•

Present Results

•

Key Elements of Plan

–

North America Automotive

–

International Automotive

–

Ford Credit

•

Outlook

SLIDE 32

(Bils.)

2006

2007

2008

2009

2010

$0

TOTAL COMPANY

PROJECTED CORPORATE EARNINGS BEFORE TAXES*

Total

Automotive

Total

Company

* Excluding special items; see Appendix (pages 1 and 2) for 2006 year-to-date reconciliation to GAAP

SLIDE 33

(Bils.)

2006

2007

2008

2009

2010

$0

-

Adverse product mix

in Ford N.A.

-

Market share in N.A.

-

Dealer inventory adj.

-

Commodity costs

-

Currency exchange

+

Reduce low-margin business

(e.g., daily rental)

-

Lower N.A. production in 1H

+

Growth in volume outside U.S.

+

Structural cost reductions

-

Commodity costs

+

Volume and mix stabilized in N.A.

+

Growth in volume continues outside U.S.

+

Further product cost improvement:

»

Supply base restructuring

»

Product complexity reducing

»

Manufacturing / supply “footprint”

improving around world

AUTOMOTIVE SECTOR

PROJECTED AUTOMOTIVE EARNINGS BEFORE INTEREST AND TAXES*

* Excluding special items; see Appendix (pages 1 and 2) for 2006 year-to-date reconciliation to GAAP

+

Favorable

-

Unfavorable

SLIDE 34

AUTOMOTIVE SECTOR

PRESENT LIQUIDITY

$6

Auto. Credit Lines

~$(3)

Operating Cash Flow**

* Cash and cash equivalents, marketable and loaned securities, and short-term VEBA assets. See Appendix (page 6) for September 30

reconciliation to GAAP

** Includes affect of dealer inventory reductions

$12

New Liquidity

$24

Automotive

Gross Cash *

$30

(Bils.)

$20

Automotive

Gross Cash*

$10

Funded New Debt

$8

Auto. Credit Lines

$38

September 30, 2006

2006 Fourth Quarter Sources and Uses

Year-End 2006

Cash Restructuring Costs

~ $(1)

SLIDE 35

AUTOMOTIVE SECTOR

FORD PLANS TO MAINTAIN SUBSTANTIAL ON-GOING LIQUIDITY

$10

Funded New Debt

~$(7)

Cash

Restructuring Costs

~$(10)

Operating-Related

Cash Outflow

~$4

Long-Term VEBA,

Divestitures & Other

Liquidity for operating

needs and a cushion

for recession and

other unexpected events

for recession and

other unexpected events

$20

Automotive

Gross Cash*

$8

Auto. Credit Lines

$38

~$25

$8

Auto. Credit Lines

$17

Automotive

Gross Cash*

Year-End 2006

Sources and Uses

Year-End 2009

(Bils.)

* Cash and cash equivalents, marketable and loaned securities, and short-term VEBA assets

SLIDE 36

•

Large global enterprise with well known brands

•

Plan to restore Automotive profitability and operating cash flow by 2009

•

Substantial liquidity resources to support the plan

•

New credit facilities are secured by a substantial portion of Automotive assets (including equity in foreign subsidiaries and Ford Credit)

KEY CREDIT STRENGTHS

SLIDE 37

Ann Marie Petach

Vice President and Treasurer

SLIDE 38

Backup

Secured Bank Revolver $ 8 2011

New Funding

Secured Term Loan B $ 7 2013

Unsecured Capital Markets Transactions* 3 TBD

New Funding $10ü

Total Facilities $ 18

* May include unsecured convertible debt securities

Amount

(Bils.)

Maturity

TRANSACTION OVERVIEW

SLIDE 39

$38

At December 31, 2006 (Bils.)

$8

Auto. Credit Lines

$30

Automotive

Gross Cash*

Liquidity

Debt

Liquidity Net

of Debt

$13

Unsecured

Debt

$5

Unsecured

Subordinated Debt**

$7

Funded New Secured

$28

$10

Assumes $8 Billion Revolver and

$10 Billion Funded New Debt --

Total $18 Billion

Total $18 Billion

* Cash and cash equivalents, marketable and loaned securities, and short-term VEBA assets

** Related to Convertible Trust Preferred securities

$3 -- Funded New Unsecured

PRO FORMA AUTOMOTIVE LIQUIDITY

SLIDE 40

$27.7

December 31, 2006 (Bils.)

0-5

Years

6-10

Years

11-15

Years

16-20

Years

21-25

Years

26-30

Years

31-50

Years

►

50

Years

$10.0

$0.5

$0.7

$5.7

$5.5***

$3.1*

$1.7

$0.5

$7.0

New

Secured

Term

Loan B

$3.0

New

Unsecured

Debt**

PRO FORMA AUTOMOTIVE DEBT MATURITIES

* 2007 maturities total $1 billion

** May include unsecured convertible debt

*** Includes Convertible Trust Preferred securities

SLIDE 41

U.S. Receivables $ 0.3 75% $ 0.2

U.S. Inventory 3.3 60 2.0

Pledge of Intercompany Notes 7.8 N/A 4.6

Pledge of Equity in Ford Credit and

Certain Foreign Subsidiaries 11.9 75 9.0

U.S. PP&E Subject to Bond Indenture Limitation 6.8 N/A 3.2

Other U.S. Machinery and Equipment 3.9 40 1.6

Intellectual Property & U.S. Trademarks** 7.9 N/A 2.5

Eligible Value / Borrowing Base $41.9 $23.1

Memo:

Secured Debt Coverage with Revolver Unfunded*** 4.93 2.71

Secured Debt Coverage with Revolver Funded*** 2.54 1.40

* Based on formula set forth in credit documentation and not necessarily indicative of fair market value, which

could be materially higher or lower

could be materially higher or lower

** Value reflects independent third party valuation of trademarks only

*** Includes $1.5 billion of potential non-loan exposure

Eligible

Value*

(Bils.)

Advance

Rate

Borrowing

Base

(Bils.)

COLLATERAL AND BORROWING BASE OVERVIEW

SLIDE 42

S&P

Issuer Rating B Negative

Secured Facility TBA TBA

Senior Unsecured Debt CCC+

Moody’s

Issuer Rating B3 Negative

Secured Facility Ba3 Negative

Senior Unsecured Debt Caa1 Negative

Fitch

Issuer Rating B Negative

Secured Facility TBA TBA

Senior Unsecured Debt B Negative

Rating

Outlook

CREDIT RATINGS -- FORD

SLIDE 43

KEY TERMS -- SENIOR SECURED CREDIT FACILITIES

Borrower: Guarantors: Facility: Security: Purpose: | Ford Motor Company Substantially all existing and future, direct and indirect, material domestic subsidiaries other than Ford Motor Credit Company Tranche Amount Maturity Bank Revolver $8 billion 5 years Term Loan B $7 billion 7 years - U.S. Account Receivables and Inventory - U.S. Plant, Property, and Equipment (subject to debt indenture limitations) - 100% pledge of the stock of primary U.S. subsidiaries (including Ford Credit) - 66% to 100% pledge of the stock of first tier foreign subsidiaries - Certain intercompany notes from foreign subsidiaries and U.S. intellectual property and trademarks General corporate purposes |

SLIDE 44

KEY TERMS -- SENIOR SECURED CREDIT FACILITIES

Facility Fee: Pricing: Term Loan Amortization: Term Loan Optional Redemption: Non-loan Exposure: Incremental Facilities: Borrowing Base: | 50 basis points per annum Market based 1% per annum with balance due at maturity Non-callable for 2 years. Thereafter, callable as a percentage of par value as follows: Year 3 (102%), Year 4 (101%), thereafter 100% Up to $1.5 billion of non-loan exposure of extending lenders and other non-lenders permitted on pari passu basis • Up to $2 billion pari passu first lien facilities or notes • Up to $4 billion of second lien debt Minimum 1.0x coverage |

SLIDE 45

TRANSACTION TIMETABLE

Lenders’ Meeting and Conference Call November 29

Final Commitments on Loans Due

from Lenders December 7

Closing and Funding December 15

Timing Plan

SLIDE 46

QUESTIONS AND ANSWERS

SLIDE 47

•

Continued decline in market share;

•

Continued or increased price competition resulting from industry overcapacity, currency fluctuations or other factors;

•

A market shift (or an increase in or acceleration of market shift) away from sales of trucks or sport utility vehicles, or from sales of other more profitable vehicles in the United States;

A significant decline in industry sales, particularly in the United States or Europe, resulting from slowing economic growth, geo-political events (e.g., an escalation or expansion of armed conflict in or beyond the Middle East) or other factors;

•

•

Lower-than-anticipated market acceptance of new or existing products;

•

Continued or increased high prices for or reduced availability of fuel;

•

Currency or commodity price fluctuations;

•

Adverse effects from the bankruptcy or insolvency of, change in ownership or control of, or alliances entered into by a major competitor;

•

Economic distress of suppliers that has in the past and may in the future require us to provide financial support or take other measures to ensure supplies of components or materials;

•

Work stoppages at Ford or supplier facilities or other interruptions of supplies;

•

Single-source supply of components or materials;

•

Labor or other constraints on our ability to restructure our business;

•

Worse-than-assumed economic and demographic experience for our postretirement benefit plans (e.g., discount rates, investment returns, and health care cost trends);

•

The discovery of defects in vehicles resulting in delays in new model launches, recall campaigns or increased warranty costs;

•

Increased safety, emissions, fuel economy or other (e.g., pension funding) regulation resulting in higher costs, cash expenditures, and/or sales restrictions;

•

Unusual or significant litigation or governmental investigations arising out of alleged defects in our products or otherwise;

•

A change in our requirements for parts or materials where we have entered into long-term supply arrangements that commit us to purchase minimum or fixed quantities of certain parts or materials, or to pay a minimum amount to the seller ("take-or-pay contracts");

•

Inability to access debt or securitization markets around the world at competitive rates or in sufficient amounts due to additional credit rating downgrades, unfavorable capital market conditions, insufficient collateral, greater-than-expected negative operating-related cash flow or otherwise;

•

Higher-than-expected credit losses;

•

Increased competition from banks or other financial institutions seeking to increase their share of financing Ford vehicles;

•

Changes in interest rates;

•

Collection and servicing problems related to finance receivables and net investment in operating leases;

•

Lower-than-anticipated residual values or higher-than-expected return volumes for leased vehicles;

•

New or increased credit, consumer or data protection or other regulations resulting in higher costs and/or additional financing restrictions; and

•

Inability to implement the Way Forward plan.

Statements included or incorporated by reference herein may constitute “forward-looking statements” within the meaning of the Private Securities

Litigation Reform Act of 1995. Forward-looking statements are based on expectations, forecasts and assumptions by our management and involve a number of risks, uncertainties, and other factors that could cause actual results to differ materially from those stated, including, without limitation:

We cannot be certain that any expectation, forecast or assumption made by management in preparing these forward-looking statements will prove accurate, or that any projection will be realized. It is to be expected that there may be differences between projected and actual results. Our forward-looking statements speak only as of the date of their initial issuance, and we do not undertake any obligation to update or revise publicly any forward-looking statement,

whether as a result of new information, future events or otherwise.

whether as a result of new information, future events or otherwise.

SAFE HARBOR

SLIDE 48

APPENDIX

North America $(2,004) $ (9,955) $(736) $(6,668) $(1,268) $(3,287)

South America 268 547 0 110 268 437

Total Americas $(1,736) $ (9,408) $(736) $(6,558) $(1,000) $(2,850)

Europe $ 0 $ 193 $ (49) $ (44) $ 49 $ 237

P.A.G. (217) (2,208) (66) (1,690) (151) (518)

Total Europe / P.A.G. $ (217) $ (2,015) $ (115) $ (1,734) $ (102) $ (281)

Asia Pacific and Africa $ 114 $ (50) $ 14 $ 0 $ 100 $ (50)

Mazda & Assoc. Operations 223 254 0 137 223 117

Total AP and Africa / Mazda $ 337 $ 204 $ 14 $ 137 $ 323 $ 67

Total International $ 120 $ (1,811) $(101) $(1,597) $ 221 $ (214)

Other Automotive 41 306 146 0 (105) 306

Total Automotive $(1,575) $(10,913) $(691) $(8,155) $ (884) $(2,758)

Financial Services 2,912 1,550 84 0 2,828 1,550

Total Company $ 1,337 $ (9,363) $ (607) $(8,155) $ 1,944 $(1,208)

Pre-Tax Profits

(Incl. Special Items)

Special Items

Pre-Tax Profits

(Excl. Special Items)

2006

(Mils.)

2006

(Mils.)

2005

(Mils.)

2005

(Mils.)

2005

(Mils.)

2006

(Mils.)

TOTAL COMPANY

2005 – 2006 FIRST NINE MONTHS PRE-TAX RESULTS*

* From continuing operations

Appendix 1 of 6

Americas

Jobs Bank / Employee Separation $ (2.5) $ (2.5)

Fixed Asset Impairment -- North America (2.2) (2.2)

Pension / OPEB Curtailment Charges (1.3) (2.4) - (1.9)

Additional North America Personnel Reductions (0.4) (1.5) - (1.1)

Facility-Related U.S. Plant Idling Costs (0.3) (0.3)

South American Legal Settlement 0.1 0.1

Total Americas $ (6.6) $ (8.8) - (7.9)

International

Fixed Asset Impairment -- Jaguar / Land Rover $ (1.6) $ (1.6)

European Personnel Reductions (0.1) (0.6) - (0.5)

Asia Pacific and Africa Personnel Actions - - (0.1)

Mazda Pension Adjustment 0.1 0.1

Total International $ (1.6) $ (2.2) - (2.1)

Total Special Items $ (8.2) $ (11.0) - (10.0)

Full Year

Projection

(Bils.)

First

Nine Months

(Bils.)

TOTAL COMPANY

2006 PRE-TAX SPECIAL ITEMS

Memo: 2006 Cash Impact $ (1.0) $ (1.5)

Appendix 2 of 6

FORD CREDIT KEY METRIC DEFINITIONS

In addition to evaluating Ford Credit’s financial performance on a GAAP financial statement basis, Ford Credit management also uses other criteria, some of which were previously disclosed in this presentation and are defined below. Information about the impact of on-balance sheet securitization is also included below:

Managed Receivables -- receivables reported on Ford Credit’s balance sheet and receivables Ford Credit sold in off-balance-sheet securitizations and continues to service

Serviced Receivables -- includes managed receivables and receivables Ford Credit sold in whole-loan sale transactions (i.e., receivables for which Ford Credit has no continuing exposure or risk of loss)

Charge-offs on Managed Receivables -- charge-offs associated with receivables reported on Ford Credit’s balance sheet plus charge-offs associated with receivables Ford Credit sold in off-balance sheet securitizations and continues to service

Impact of On-Balance Sheet Securitization -- finance receivables (retail and wholesale) and investments in operating leases reported on Ford Credit’s balance sheet include assets transferred in securitizations that do not qualify for accounting sale treatment. These assets have been legally transferred to Ford Credit sponsored special purpose entities and are available only to pay the obligations of the special purpose entities and are not available to pay the other obligations of Ford Credit or the claims of Ford Credit’s other creditors. Debt reported on Ford Credit’s balance sheet includes debt issued by these special purpose entities to securitization investors which is payable out of collections on the assets supporting the securitizations and is not the legal obligation of Ford Credit or its other subsidiaries

Appendix 3 of 6

FORD CREDIT RATIO DEFINITIONS

In addition to evaluating Ford Credit’s financial performance on a GAAP financial statement basis, Ford Credit management also uses other criteria, some of which were previously disclosed in this presentation and are defined below:

Leverage:

Total Debt

- Financial Statement Leverage

=

Equity

Total Debt

Securitized

Off-Balance

Sheet

Receivables

Cash, Cash

Equivalents &

Marketable

Securities*

Fair Value

Hedge Acctg.

Adjustments

Adjustments

on Total Debt

Equity

Minority

Interest

Fair Value

Hedge Acctg.

Adjustment

on Equity

- Managed Leverage

+

-

-

-

=

+

-

Retained

Interest in

Securitized

Off-Balance

Sheet

Receivables

Charge-offs

=

Average Receivables

Loss-to-Receivables Ratio

* Excluding marketable securities related to insurance activities

Appendix 4 of 6

FORD CREDIT RECONCILIATIONS OF MANAGED

LEVERAGE TO FINANCIAL STATEMENT LEVERAGE

Total Debt* $120.4 $134.5

Securitized Off-Balance Sheet Receivables Outstanding 35.0 12.9

Retained Interest in Securitized Off-Balance Sheet Receivables (4.4) (1.1)

Adjustments for Cash, Cash Equivalents and Marketable Securities** (19.0) (17.4)

Fair Value Hedge Accounting Adjustments (0.8) (0.2)

Total Adjusted Debt $131.2 $ 128.7

Total Stockholder’s Equity (incl. minority interest) $ 11.4 $ 11.8

Fair Value Hedge Accounting Adjustments (0.9) (0.5)

Total Adjusted Equity $ 10.5 $ 11.3

Managed Leverage (to 1) 12.5 11.4

Financial Statement Leverage (to 1) 10.6 11.4

*Includes $23.9 billion and $55.9 billion on September 30, 2005 and September 30, 2006 respectively of debt issued by securitization SPEs

which is payable solely out of collections on the receivables sold to the SPEs and is not the legal obligation of Ford Credit

** Excluding marketable securities related to insurance activities

Sep. 30,

2006

(Bils.)

Leverage Calculation

Sep. 30,

2005

(Bils.)

Appendix 5 of 6

AUTOMOTIVE SECTOR

GROSS CASH RECONCILIATION TO GAAP

Cash and Cash Equivalents $13.4 $13.5 $ 0.1 $ 9.1

Marketable Securities 6.9 7.8 0.9 7.9

Loaned Securities 3.4 0.6 (2.8) 0.6

Total $23.7 $21.9 $(1.8) $17.6

Short-Term VEBA 1.4 1.7 0.3 2.0

Gross Cash $25.1 $23.6 $(1.5) $19.6

Sept. 30, 2006

B / (W)

Dec. 31, 2005

(Bils.)

Sept. 30,

2006

(Bils.)

Dec. 31,

2005

(Bils.)

Memo:

Sept. 30, 2005

(Bils.)

Appendix 6 of 6