UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 14A

(RULE 14a-101)

Information Required In Proxy Statement

Schedule 14a Information

Proxy Statement Pursuant to Section 14(a) of the Securities Exchange Act of 1934

(Amendment No. )

Filed by the Registrant o

Filed by a Party other than the Registrant x

Check the appropriate box:

| o | Preliminary Proxy Statement |

| o | Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) |

| o | Definitive Proxy Statement |

| o | Definitive Additional Materials |

| x | Soliciting Material Under Rule 14a-12 |

FRIENDLY ICE CREAM CORPORATION |

| (Name of Registrant as Specified in Its Charter) |

| THE LION FUND L.P. BIGLARI CAPITAL CORP. WESTERN SIZZLIN CORP. SARDAR BIGLARI PHILIP L. COOLEY |

| (Name of Persons(s) Filing Proxy Statement, if Other Than the Registrant) |

Payment of Filing Fee (Check the appropriate box):

| x | No fee required. |

| o | Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11. |

| (1) | Title of each class of securities to which transaction applies: |

| (2) | Aggregate number of securities to which transaction applies: |

| (3) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined): |

| (4) | Proposed maximum aggregate value of transaction: |

| (5) | Total fee paid: |

| o | Fee paid previously with preliminary materials: |

o Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the form or schedule and the date of its filing.

| (1) | Amount previously paid: |

| (2) | Form, Schedule or Registration Statement No.: |

| (3) | Filing Party: |

| (4) | Date Filed |

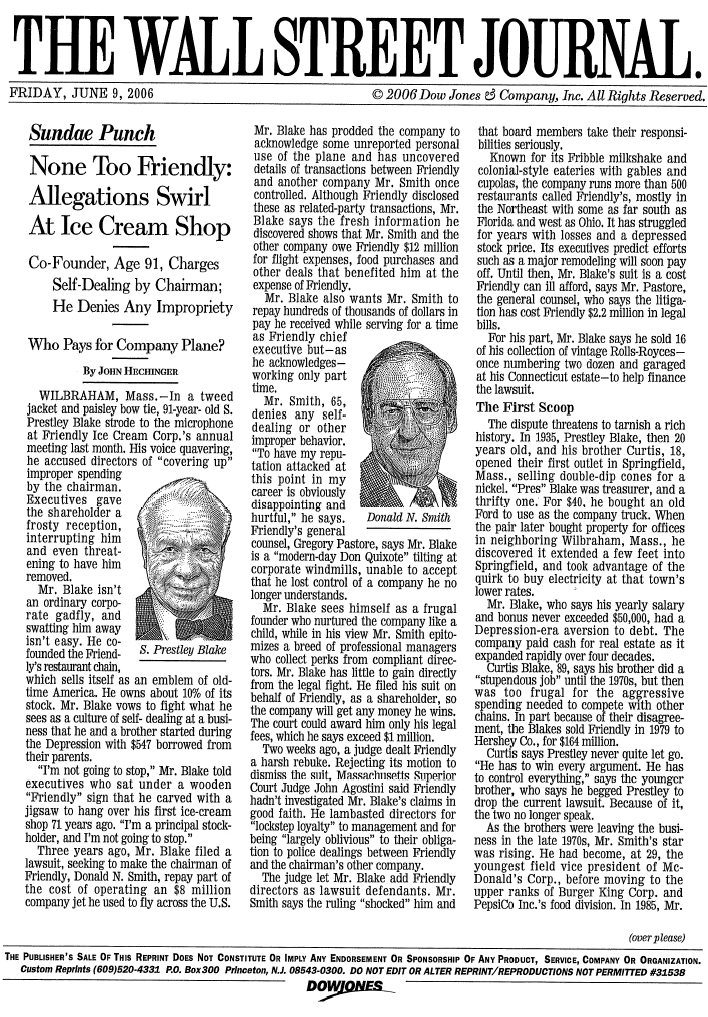

The Lion Fund L.P. (the "Lion Fund"), together with the other participants named herein, is filing materials contained in this Schedule 14A with the Securities and Exchange Commission ("SEC") in connection with the anticipated solicitation of proxies for the election of two nominees as directors at the 2007 annual meeting of stockholders (the "Annual Meeting") of Friendly Ice Cream Corporation ("Friendly"). The Lion Fund has not yet filed a proxy statement with the SEC with regard to the Annual Meeting.

Item 1: The following materials were posted to http://enhancefriendlys.com:

* * * *

HAMPDEN COUNTY

SUPERIOR COURT

FILED MAY 24, 2006

______________________

Clerk-Magistrate

COMMONWEALTH OF MASSACHUSETTS | |

|

|

HAMPDEN, ss. | SUPERIOR COURT CIVIL NO. 03-0003 |

|

|

|

|

|

|

S. PRESTLEY BLAKE | |

v FRIENDLY ICE CREAM CORP. | |

| |

FN1. The special Litigation Committee has filed an appearance, as intervener, with respect to the motion to dismiss.

MEMORANDUM OF DECISION AND ORDER ON SPECIAL LITIGATION COMMITTEE’S MOTION TO DISMISS DERIVATIVE ACTION AND PLAINTIFF’S REQUEST FOR RECONSIDERATION OF THE DENIAL OF MOTION TO AMEND

JOHN A. AGOSTINI, Associate Justice.

INTRODUCTION

In this shareholder derivative lawsuit, the defendant intervener, a Special Litigation Committee (SLC) appointed by the defendant corporation’s board of directors, has moved to dismiss the action pursuant to G.L.c. 156D, s. 7.44. Also before me is the plaintiff’s motion for reconsideration of my order denying his latest motion to amend the complaint. After a non-evidentiary hearing [FN2] and considering the parties’ oral and written arguments and supporting documents, the SLC’s motion to dismiss is DENIED and the plaintiff’s motion to reconsider and motion to amend are ALLOWED.

FN2. Neither party requested an evidentiary hearing.

BACKGROUND

The defendant, Friendly Ice Cream Corporation (Friendly), operates and franchises hundreds of restaurants, primarily in the northeastern United States, and manufactures frozen desserts distributed at retail locations in 15 states. The plaintiff, S. Prestley Blake, founded Friendly with his brother in 1935. Friendly was publicly held from 1968 until 1979, when it was sold to Hershey Food Corporation (Hershey). In 1988, The Restaurant Company (TRC), an investor group led by the defendant, Donald Smith (Smith), acquired Friendly from Hershey and then brought Friendly public again in 1997. In the November 1997 initial public offering (the IPO) of stock, Blake became an owner of Friendly common stock and currently owns approximately 10% of its outstanding common shares.

Smith, widely respected for his expertise in the restaurant business, was simultaneously chief executive officer (CEO) and chairman of the boards of both Friendly and TRC from 1988 through February of 2003. In February of 2003, Smith became the non-executive chairman of Friendly’s Board of Directors (the Board), such that he was no longer CEO but continued to

chair the Board. At all relevant times, Smith has also been the owner of approximately 70% of TRC, which is a management company. [FN3] Two of TRC’s divisions relevant to this action are Perkins Family Restaurants (Perkins), a company which operates restaurants, and Foxtail Foods (Foxtail), a company which from 1998 through 2004 sold between $4.4 and $5.3 million in food products to Friendly.

FN3. Smith has been the CEO of TRC and its predecessor since 1985. In 1999, Smith’s ownership interest in TRC increased to 70%. TRC had been the management company of Perkins and Friendly, both operating companies. Okscin dep. p. 182. |

TRC is the sole stockholder of TRC Realty, LLC, The Restaurant Company of Minnesota, and Perkins Finance Corp. TRC is a wholly-owned subsidiary of The Restaurant Holding Company (RHC), which according to TRC’s 2004 10K Form (exh. 118), is owned principally by Smith and BancBoston Ventures, Inc. |

Friendly had a shareholder deficit of $85 million at the time of the IPO. As of January 2002, this deficit climbed to $89 million, and in 2003 the deficit was $98 million. Between 1999 and 2003, Friendly’s total assets decreased to a greater extent than the Board was able to reduce the debt. [FN4]

FN4. Daly dep. p. 37-38.

A principal activity of the Board has been to undertake financial actions to reduce Friendly’s debt and improve its operating performance. [FN5] From November 1997 to March of 2005, the Board was comprised of the same five members: Smith, Steven Ezzes (Ezzes), Michael J. Daly (Daly), Charles Ledsinger (Ledsinger), and Burton Manning (Manning). In March of 2005, Ledsinger stepped down and was replaced a few months later by Perry Odak (Odak). The Board delegates to management the function of running Friendly. Smith, as former CEO of Friendly, led its management team.

FN5. Daly dep. p. 36.

Within the Board, three committees assume certain responsibilities: the Audit Committee, the Compensation Committee, and the Nominating Committee. One of the primary functions of the Audit Committee is to assist the Board with the oversight of Friendly’s financial reporting process, the systems of internal controls and all audit processes. The Audit Committee reviews the financial results of Friendly, the internal audits on its restaurants, and any other financial matters deemed necessary at its meetings with the Audit Committee and the CFO. Its role is to “ensure, number one, all systems, procedures, and controls in the organization are proper and functioning well.” [FN6] Of particular significance to this action is that the Audit Committee is responsible for scrutinizing related party transactions to ensure that the interests of the shareholders and general public are protected. [FN7] The Audit Committee, as described by Daly, is very active and diligent, and typically meets six times a year. The members of the Audit Committee from 1997 until March of 2005 were Daly, Ledsinger, and Ezzes. [FN8]

FN6. Daly dep. pp. 10-12.

2

FN7. Daly dep. pp. 149-50.

FN8. Daly dep. pp. 10, 12.

The Compensation Committee oversees all compensation practices of the company. The three members of the Compensation Committee since late 1997 were Daly, Ledsinger (up until his departure from the Board in March of 2005), and Manning.

The Nominating Committee considers the ongoing performance of existing directors, evaluates core competencies of Friendly’s “governance oversight capabilities,” or in other words evaluates how well the Board functions. In order to determine whether the directors are participating effectively, the Nominating Committee surveys the five directors on the Board. The survey results collected so far uniformly indicate that the directors feel that their communications with management are satisfactory and that the Board is effectively performing. [FN9] The Nominating Committee also makes recommendations to the Board regarding promotions, directors, and senior officers. Since 1997, the Nominating Committee has been comprised of Daly and Smith, and perhaps also Manning. [FN10]

FN9. Daly dep. pp. 21-24.

FN10. Daly dep. p. 20.

Each director of Friendly receives compensation in the amount of $2,500 per month ($30,000 per year), plus $1,500 for each Board meeting attended, plus expenses. [FN11] Audit Committee members receive $1,500 for attendance at the annual Audit Committee meeting. For serving as chairman, Smith has received additional director compensation, which in 2004 was $8,333.34 per month. [FN12] Friendly’s directors also receive compensation in the form of stock options. [FN13] Pursuant to Friendly’s 1997 Stock Option Plan, each outside director receives stock options reflective of his functions. Although the amounts vary from year to year, for fiscal year 2004, each outside director received at least 3,000 stock options; the Compensation Committee Chairman (Manning) received an additional 1,500 stock options, and the Audit Committee Chairman (Ezzes) received an additional 3,000 stock options. In fiscal year 2004, Ezzes, Ledsinger, Daly and Manning received 6,000, 3,000, 3,000 and 4,500 stock options, respectively. [FN14]

FN11. In fiscal year 2004, the Board met seven times and each director attended at least 75% of the meetings of the Board, thus receiving at least $7,875. Form DEF 14A Friendly SEC filing dated April 8, 2005, Exh. A to Manning affid. of Jan 24, 2006. |

FN12. Form DEF 14A, filed April 8, 2005, exh. A to Ezzes affid. |

FN13. SLC’s counsel stated at the motion hearing that the outside directors’ principal form of compensation is stock options. See 1/20/06 Hearing Tr. p. 78. The exercise price per share has fluctuated between fiscal year 1999 and the present. The plaintiff does not argue that these directors’ compensation in this form has been inordinate. |

3

FN14. Form DEF 14A, filed April 8, 2005, exh. A to Ezzes affid.

Between 1999 and 2002, Blake grew suspicious about possible mismanagement of Friendly’s assets and self-dealing by Smith. On May 15, 2002, at a shareholders’ meeting, Blake voiced his concerns that Smith had caused Friendly to pay costs toward a Learjet which largely benefited TRC and Smith, directly or indirectly. This controversy has its roots in a 1994 agreement between TRC and Friendly to share the fixed and variable costs of a corporate aircraft, then a 1992 Beechjet 400A, for which TRC entered a ten-year contract to lease from General Electric Capital Corporation . [FN15] In 1999, TRC’s Board of Directors decided to dispose of the Beechjet 400A for a cash purchase price of not less than $3.2 million, [FN16] and to acquire a new Learjet 45 for a purchase price of $8,278,950, to be financed with General Electric Corporation pursuant to an Aircraft Lease Agreement. [FN17]

FN15. There is no dispute that the plaintiff lacks standing to assert claims relating to conduct prior to 1997 when he became a shareholder. |

FN16. Exh. 93. There is no record of the Beechjet 400A sale proceeds reaching Friendly. |

FN17. Exh. 93.

Because in 1999, Friendly’s five-year plan called for opening well over one hundred franchises, the Board viewed the use of the Learjet as useful for visiting potential franchise sites. No written agreement exists requiring Friendly to pay for costs of the use of the Learjet. Nonetheless, from 1999 through, at least, August of 2003, Friendly paid TRC for 40% to 50% of the Learjet’s fixed costs plus 100% of any variable costs associated with Friendly’s actual use of the aircraft. [FN18] Friendly’s comptroller, Allan Okscin (Okscin), who was responsible for paying TRC for Friendly’s share of the aircraft, did not receive or request from TRC documentation such as underlying invoices substantiating the variable costs (which included fuel, maintenance, engine costs, landing and parking fees, pilot travel expenses, and catering) and fixed costs (which included lease payments, pilots’ salaries and benefits, pilot relocation costs, hangar rental, crew expenses, property taxes, banking fees, set-up expenses, training, amortization, insurance, dues and subscriptions, supplies and telephone costs) billed to and paid by Friendly. [FN19] Instead, with respect to fixed costs, Okscin never requested more than what TRC sent, which was an annual projection of fixed costs and a monthly payment schedule. As to the variable costs for flights charged to Friendly, Okscin received from TRC bills, usually with flight manifests identifying who was on the plane and where it went. Alter talking to others to make sure each billed flight was taken, Okscin approved payment of these bills, even for some flights lacking manifests. [FN20] Okscin also approved Friendly’s payment for flights carrying Smith’s wife’s children, and assumed that such flights were for business purposes because one of the passengers, Jody Delrey, had been involved with Friendly’s Easter Seal campaign. [FN21]

FN18. Friendly’s former general counsel, Aaron Parker, reported that Friendly paid TRC the following amounts for the Learjet’s fixed and variable costs, respectively, in the fiscal years 2000 through 2002: |

4

| 2000: | $ | 843,858; | $ | 82,756 | ||||

| 2001: | $ | 612,548; | $ | 73,878 | ||||

| 2002: | $ | 449,319; | $ | 0 |

Exh. 53, Parker memorandum dated June 26, 2002, p. 2. Thus in 2002, Friendly paid TRC $449,319 for never using the Learjet that year. |

Smith testified that Friendly’s former chief financial officer (CFO), Paul McDonald, and his counterpart at TRC, Steven McClellan, determined how much of the aircraft costs would be paid by Friendly. Smith dep. pp. 52-53. In contrast, McClellan testified that it was Smith who decided what portion of these costs would be borne by TRC and Friendly. McClellan dep. p. 134. McClellan’s version is supported by a handwritten memo which appears to have been written in December of 1998 in which Smith instructed Michael Donohoe of TRC, “The 'split’ for the plane in '99 will be: 60% Perkins--40% Friendly’s based on projected usage. Don.” Exh. 119, also labelled as plaintiff’s exhibit 57. |

FN19. See Huron Report dated October 24, 2005, p. 7 and exhibit to 1994 Aircraft Reimbursement Agreement. |

FN20. Okscin dep. p. 261. |

FN21. Okscin dep. pp. 258-59. |

By March of 2000, deteriorating economic conditions led Friendly to abandon its ambitious five-year expansion plan. Rather than opening new franchises, Friendly closed 150 locations and implemented a reduction in force. Friendly’s use of the Learjet as a percentage of the total hours it was flown diminished from 33% in 1999 to 21% in 2000 to 16% in 2001 and to 4% in 2002. [FN22] In the fall of 2000, Okscin and Paul Kelley, then Friendly’s CFO, proposed to the Audit Committee that Friendly cease its perceived obligation to share the cost of the Learjet by making a payment to TRC. By late 2000, the Board concurred that Friendly should dispose of the aircraft, and appointed Ezzes and Ledsinger as a committee to handle this task which was difficult due to the weak market. [FN23] In sum, Blake’s major concerns expressed in May of 2002 regarding the Learjet were that Smith was having Friendly subsidize TRC’s use of the Learjet, that Friendly had no enforceable obligation pay toward its costs, and that Smith was using the Learjet for nonbusiness purposes without reimbursing Friendly appropriately.

FN22. Huron Report p. 7; Ledsinger dep. pp. 171-72. |

FN23. Manning dep. pp. 97-100. |

Blake also took issue with Friendly’s payments to TRC toward the costs related to an office in Illinois used by Smith to conduct business for both Friendly and TRC. [FN24] Friendly’s corporate headquarters are in Wilbraham, Massachusetts, and TRC’s corporate headquarters are in Memphis, Tennessee. Friendly has not at any time had operations in Illinois unless one considers the office a Friendly operation. [FN25] Smith maintained his principal residence in the Chicago area until February 2002. [FN26] According to Okscin, Friendly’s “purchasing group” used the office for meetings because Chicago is “sort of the hub of the

5

National Restaurant Association out there.” [FN27] The Board approved of Friendly’s payment to TRC of these office expenses. |

FN24. Ezzes dep. p. 79. |

FN25. Ezzes dep. p. 75. |

FN26. Okscin dep. p. 15. |

FN27. Okscin dep. pp. 143-44. |

The SLC asserts that Friendly’s payments toward the costs of the Illinois office--which totalled $770,630 between 1997 and 2004--were made pursuant to a March 1996 management fee agreement executed by Friendly and TRC. [FN28] The management fee letter agreement relied upon by the SLC is undated, bears no handwritten signatures for either TRC or Friendly, and consists of a three-paragraph letter. It states only that the maximum annual management fee payable by Friendly to TRC would not exceed $800,000 in 1996, $824,000 in 1997, and $848,720 in 1998 unless the Board was to approve of an increase. This document does not provide any information related to the nature of the services covered by the agreement or how Friendly and TRC would allocate the shared expenses. [FN29] Nonetheless, Friendly reported in its 1997 IPO filing that the management fees compensated TRC for Smith’s services to Friendly, the office and secretarial services, and “other related expenses.” [FN30] The SLC asserts that the management fee agreement covers the following: (1) Smith’s compensation in 1997 (but not thereafter); (2) the maintenance of the office in Illinois where Smith conducted business for both TRC and Friendly; (3) the salary and benefits of a secretary at the Illinois office; (4) the salary of one Rich Estlin (Estlin); and (5) fringe benefits for Smith, including his life, medical, dental and AD & D insurance.

FN28. Over $400,000 of that total amount was to compensate Smith in 1997. |

Prior to the IPO, when TRC was the management company of both Perkins and Friendly and when Smith was an employee of TRC but not Friendly, TRC charged both Perkins and Friendly a management fee. Okscin dep. p. 182. See also Huron Report p. 22. |

FN29. See Huron Report p. 17 and exhibit 2 to Huron Report. |

FN30. Huron Report p. 18. |

On May 21, 2002, Blake sent a demand letter to Friendly reiterating his allegations regarding the Learjet and the Illinois office. Blake called for an investigation and the right to inspect corporate records. Three days later, Ledsinger, Ezzes, Manning and Daly signed a document entitled Unanimous Written Consent of the Independent Directors of Friendly Ice Cream Corporation in which they resolved to create a Special Committee (the 2002 Special Committee) ultimately composed of Ledsinger, Daly and Ezzes to investigate Blake’s allegations and to recommend to the Board “what position should be taken by the Corporation in reference thereto.” The 2002 Special Committee, in turn, asked Friendly’s general counsel, Aaron B. Parker (Parker) to conduct the investigation.

6

Parker had been special counsel to TRC from 1986 to 1997. In 1997, he became associate general counsel for Friendly, and on November 22, 2001, Friendly appointed Parker as its president, general counsel and secretary/clerk. Smith, as Parker’s “boss,” reviewed his performance and recommended to the Board whether or not Parker would receive a raise or bonus. [FN31]

FN31. Ledsinger dep. p. 150.

On June 26, 2002, Parker sent to Ledsinger, Daly and Ezzes a three-page memorandum containing what he called background facts and preliminary investigative findings, [FN32] although he never issued a follow-up document with final investigative findings. [FN33] Parker reported that TRC’s comptroller told him that Smith had paid for the variable costs associated with Smith’s personal use of the Learjet. He also reported that the Learjet cost-sharing arrangement replaced that of the Beechjet 400A, but Parker supplied no documentation to support this assertion. The 2002 Special Committee accepted Parker’s conclusion without asking to see a contract or other verification that Friendly actually had a written binding contractual agreement to pay toward the cost of the Learjet.

FN32. Parker attached to his three-page memorandum TRC’s aircraft summaries (showing the total reported costs related to use of the Learjet 45) in 2000 and 2001 and some flight manifests. |

FN33. Ezzes dep. p. 119. |

Parker’s “investigation” did not consider the appropriateness or legitimacy of the TRC-Friendly cost sharing arrangements with respect to either the Learjet or the office. [FN34] Parker reported that Friendly’s expenses incurred in connection with the Illinois office in 2001 totalled $110,146 and in 2002 were $157,458, representing 35% of the office rent, 50% of the salary of Estlin, 35% of secretarial costs, and 35% of Smith’s life, medical, dental and AD & D insurance. [FN35]

FN34. Exh. 53. |

FN35. Exh. 53. |

Friendly’s payments toward Estlin’s salary were $87,960 in 1998, $98,666 in 1999, $107,438 in 2000, and $53,456 in 2001. Although it is clear that Smith determined how TRC and Friendly would bear the cost of Estlin’s salary, [FN36] the reason for Friendly’s payment of Estlin’s salary was not adequately explained in Parker’s report or elsewhere. No substantive or adequate documentation of Estlin’s professional services for Friendly has been presented to the Court. [FN37]

FN36. Exh. 53. |

FN37. TRC’s former CFO, Steven McClellan, testified at his deposition on September 9, 2004, that Estlin “was supposed to represent [Smith] at Perkins when [Smith] was at Friendly’s ... [a]nd he was supposed to represent [Smith] at Friendly’s when [Smith] was at Perkins. In addition to which, he was supposed to |

7

handle managing [Smith’s] personal financial matters, and I say supposed to, because that wound up, not infrequently, falling on my shoulders ... [I]t started out with he was going to be [Smith’s] representative, provide us access to [Smith], because [Smith] was not present a lot ... Although I had been warned by the other members of the management team that--this was another FOD, friend of Don, and that these type of folks had shown up before. Over a period of time, I [began] to question whether it made sense for us to continue to absorb the expenses related to [Estlin]. And, in fact I asked him one time, because I got pretty frustrated. We were going through some challenging financial times, Smith was not cooperating with trying to, really, sell the aircraft, in my view, and we had--we were absorbing [Estlin’s] salary, or at least a significant portion of it. And I did ask [Estlin] one time, you know, Rich, what exactly are you doing, and what’s your goals? And he looked me straight in the eye and said, my goal is to play 200 rounds of golf a year, and he kind of laughed.” Other deponents’ descriptions of Estlin’s role were also sketchy. Okscin testified only that Estlin “helped [Friendly] with treasury and insurance issues” when Friendly’s CFO left. Okscin dep. p. 142. |

There in nothing in the record showing that the 2002 Special Committee made a formal recommendation to the Board regarding Friendly’s response to Blake’s first demand letter. Nonetheless, on September 26, 2002, Parker sent plaintiff’s counsel a letter declining the plaintiff’s request to inspect Friendly’s records, and stating that “a special committee of Friendly’s Board of Directors comprised of three independent members of the Board has reviewed the expenditures relating to the jet and determined that they were legitimate business expenses of Friendly’s.” [FN38] Parker did not address in that letter the plaintiff’s other concerns.

FN38. Exh. 54. |

On January 2, 2003, Blake brought this shareholder derivative suit against Friendly and Smith. The first amended complaint, filed on February 26, 2003, contains four counts: breach of fiduciary duty (Count I), misappropriation of corporate assets (Count II), a request for declaratory judgment that the plaintiff is entitled to inspect Friendly records relating to the Learjet and the Illinois office (Count III), and a claim that Smith and Friendly are estopped from refusing to produce certain financial records concerning the aircraft (Count IV). On the defendants’ motion to dismiss pursuant to Mass.R.Civ.P. 12(b)(6) and Mass.R.Civ.P. 23.1, the Court (Carhart, J.) dismissed the fourth count on October 28, 2003.

On January 31, 2003, at a special meeting, the Compensation Committee resolved to recommend to the Board that Friendly discontinue incurring expenses related to the Illinois office. This came approximately one month after Smith informed Okscin that in February of 2002, he had moved his principal residence from Illinois to Florida. When asked why the use of the Illinois office was discontinued, Okscin replied, “[Smith] wasn’t living in Chicago any longer and the--the use of the office wasn’t needed and it--it wasn’t used anymore, I guess.”[FN39]

FN39. Okscin dep. p. 143. |

8

On August 20, 2003, Ledsinger, Ezzes, Daly and Manning conducted a special meeting, referring to themselves as the independent members of the Board. According to the minutes, Parker and Okscin

“reviewed a proposal from TRC Realty LLC to extinguish the Corporation’s obligations under the Aircraft Reimbursement Agreement between TRC Realty LLC and the Corporation which agreement obligates the Corporation to share in the expenses of a corporate aircraft.” |

That day, the Board approved a payment “not to exceed $900,000 ... to terminate the Aircraft Reimbursement Agreement with TRC Realty LLC” for the costs of the Learjet 45. The directors believed that Friendly had a commitment to share the cost of the Learjet for another six years and viewed the payout as an attractive alternative. [FN40]

FN40. Daly dep. pp. 142-43.

In May of 2004, Blake offered to loan Friendly up to $50 million at 2% over the prime rate (adjustable), so long as the proceeds were used to reduce debt. As consideration for this offer, Blake demanded that the Board “address the improper payments that Friendly made to TRC ... for the Learjet and the Illinois office,” including, by way of reference to earlier correspondence, that Smith resign from the Board. [FN41] The Board rejected the offer on the grounds that if Friendly were to pay down its mortgage debt as required by Blake’s loan offer, it would incur a prepayment penalty of up to $18 million, and that Friendly’s $8.3 senior notes could not be prepaid until June 15, 2008. Additionally, Manning was not willing to accept the offer, believing that it was not in Friendly’s best interest because it would create a relationship with Blake which could subject Friendly to undue influence. [FN42]

FN41. Exh. 92 attached to Manning affid.

FN42. Manning dep. p. 139.

Subsequently, the plaintiff moved to amend his complaint again. In his proposed complaint, Blake names as defendants Smith, individually and as chairman of Friendly’s Board, TRC, The Restaurant Holding Company, TRC Realty, LLC, and Ezzes, Ledsinger, Daly and Manning as members of Friendly’s Board. In Count I of the proposed complaint, Blake asserts that all of the directors violated their fiduciary duty by “ignoring and condoning improper actions between Friendly, Smith and TRC, and by exercising their authority as directors to condone and cover up improper conduct.” This allegation is exemplified in the proposed complaint by the attempt by the Board and the 2002 Special Committee to dismiss Blake’s action without conducting an independent investigation of related transactions with Smith and TRC, and the Board’s approval of payments to TRC for the Learjet after being on notice that Friendly had no obligation to make them. Count II alleges misappropriation of corporate assets by Smith and TRC. Count III alleges that all of the Board members wasted corporate assets. Count IV asserts that the TRC companies and Friendly’s Board members aided, abetted, and directly participated in misappropriating corporate assets by “exercising their authority to consciously ignore, condone or cover up the improper transactions of Smith and TRC after actual or constructive notice of the wrongdoing.” Count V is for restitution and alleges unjust enrichment against Smith, the TRC companies, and “some of the directors” not specified. In Count VI, Blake seeks declaratory relief against Smith and the Board members with respect to their allegedly improper activities, their duty to disclose and their fiduciary duty.

9

In addition to his claims regarding the Learjet and the Illinois office, Blake takes issue in his proposed amended complaint with several types of transactions, including the following: (1) Friendly’s payments to TRC’s division, Foxtail Foods (Foxtail), for the purchase of certain food products; (2) Friendly’s real estate transactions involving Smith’s sons; (3) Friendly’s payment to TRC of management fees; and (4) Friendly’s rejection of Blake’s loan offer.

On July 27, 2005, I denied, without prejudice, the plaintiff’s motion to amend in the absence of a demand letter regarding the additional claims as required by G.L.c. 156D, s.7.42. After filing the motion to amend but prior to entry of my order denying the plaintiff’s motion to amend, on June 27, 2005, Blake sent a second demand letter to the Board pursuant to G.L.c. 156D, s.7.42. Blake’s letter states that his lawsuit, his second demand letter, and the proposed amendment to his complaint seek to redress two fundamental concerns. The first is that Smith has enriched himself by shifting assets or income from Friendly to TRC or by shifting costs from TRC to Friendly. Blake explains in his demand letter that this “category of concern includes any and all conduct that shifts financial benefit from Friendly to TRC regardless of what form the transaction may take”including related party transactions [FN43] and conflict of interest transactions. Blake points to a non-exclusive list of three issues: (1) the difference in the cost of goods sold margin of Friendly and TRC suggests that vendor arrangements (in which Friendly purchased food products from Foxtail) were designed so that Friendly would subsidize TRC without full and fair consideration. (2) Friendly’s financial statements represent that it paid $12.3 million to TRC for airplane expenses, consulting fees, real estate transactions and food purchases between 1997-2003, yet TRC’s financial statements represent that it only received $9.8 million in that period, while Smith was the chairman and CEO of both companies. This discrepancy, asserts the plaintiff, has been ignored and left unexplained by the Board. (3) the Board inexplicably rejected Blake’s offer of a low-interest loan to pay off $50 million in high cost debt, and instead has opted to pay high interest rates, which suggests the existence of an arrangement to favor TRC, Smith, or Ezzes, as some lenders and financial underwriters have conflicts of interest including business relationships with Ezzes or investment relationships with TRC.

FN43. Ledsinger defined related party transactions in these words: “usually it has to do with a transaction where there is an exchange of goods or services or money from one entity to another where there’s perhaps ownership or management ... It could be a public company that has a director and that director has a business and that public company does business with the business that the director is involved with ...” Ledsinger dep. p. 29. |

The second category of concern as described in Blake’s demand letter relates to the Board’s conduct which “inappropriately shields or benefits Mr. Smith and/or TRC” in violation of its fiduciary duty. Blake specifically cites as a non-exhaustive list of evidence of the Board’s misconduct its approval of Smith’s improper conduct, the 2002 Special Committee’s failure to conduct a meaningful or reasonable investigation, the Board’s approval of a $950,000 airplane termination payment, its rejection of Blake’s $50 million loan offer, its apparent position that the interests of Smith and Friendly are one and the same, because the Board retained for Friendly in this litigation the same counsel which represents Smith, Ornate, Hall & Stewart, and its turning a blind eye to conflicts of interest that are detrimental to Friendly, such as Friendly’s payment of up to $107,000 for the annual salary of Estlin, whose professional services to Friendly are unsubstantiated.

10

In July of 2005, the Board members were Smith, Daly, Manning, Ezzes, and Perry Odak (Odak), who became a director of Friendly on May 11, 2005, replacing Ledsinger. In response to the plaintiff’s second demand letter, Daly, Manning, Ezzes and Odak voted to appoint Odak and Daly to the SLC. [FN44] The resolution provides that each member of the SLC would be compensated in the amount of $10,000. On July 19, 2005, the SLC engaged as its legal counsel Wilmer Cutler Pickering Hale and Dorr, LLC (Wilmer Cutler), which in early August of 2005 retained Huron Consulting Group (Huron) to provide forensic accounting services.

FN44. The voting directors signed separate signature pages to a document entitled “Unanimous Written Consent of the Independent Directors of Friendly Ice Cream Corporation” resolving to create the SLC to investigate Blake’s new claims and to decide for Friendly whether to accept, reject or otherwise act upon Blake’s demand. Smith, concededly an interested director, did not participate in the resolution. Ezzes’s signature is dated July 14, 2005; Daly’s signature is dated and was faxed on July 15, 2005: and the signatures of Odak and Manning bear no date of execution. The document states that the signatories “hereby adopt ... the following resolutions with the same force and effect as if they had been unanimously adopted at a duly convened meeting of the Board of Directors ...” |

On October 24, 2005, the SLC filed its 29-page report concluding that all claims that have been brought on behalf of Friendly in this action lack merit and that the continued prosecution of the derivative claims is not in the interest of Friendly. [FN45] The SLC Report is unsigned by either of its members. In its executive summary of the report, the SLC listed seven basic conclusions:

FN45. The SLC also initially determined that: (1) Friendly should seek $70,267 reimbursement from Smith for the variable costs of Smith’s non-business uses of the Learjet between 1998-2002 (although in a supplemental report, Huron reduced this figure to $55,149); (2) Friendly should seek reimbursement from TRC in the amount of $10,174 for the variable costs of flights incurred by TRC but paid incorrectly by Friendly (and concluding that, otherwise, the variable and fixed costs were properly charged to Friendly); and (3) Friendly should review the adequacy of its policies and procedures regarding documentation required prior to the payment of invoices, joint negotiations with common vendors as between Friendly and other companies, oral agreements with other companies, related party transactions and review of the same by outside auditors for Friendly, and the scope of the travel and entertainment policy. |

(1) Friendly and TRC had an implied-in-fact aircraft reimbursement agreement which required Friendly to pay a portion of the fixed costs of the Learjet and the variable costs attributable to Friendly’s use of the aircraft;

(2) there is no evidence that Friendly overpaid for food products purchased from Foxtail;

11

(3) there was insufficient evidence to support Blake’s claim that joint negotiations with vendors common to Perkins and Friendly were detrimental to Friendly;

(4) there was no evidence that financial firms extended inferior credit and other terms to Friendly so as to subsidize financial packages provided by those institutions to TRC. The interest rates on Friendly’s loans do not represent collusion between Societe Generale, Fleet/Bank of America and General Electric Capital, on the one hand, and Smith on the other hand, to advantage TRC at the expense of Friendly. “[P]repayment and other penalties on the existing company obligations approximate $18 million and make Mr. Blake’s [$50 million loan offer at favorable rates] economically unattractive.”

(5) lease payments by Friendly to TRC for restaurants in Florida did not disadvantage Friendly;

(6) Friendly received benefits from services provided by the $770,000 in management fees it paid to TRC from 1997 through 2004, which fees covered, among other things, the salary of Estlin “who assisted Friendly with insurance and treasury functions.”

(7) Friendly’s decision to credit $112,500 in unearned development fees as against amounts due for product purchases by TICC, a franchise owned by Smith’s two sons, was not improper.

On November 2, 2005. Smith reimbursed Friendly $65,323 for aircraft costs.

On November 30, 2005, the SLC submitted a Supplemental Report which contained two conclusions: (1) Smith did not receive excessive compensation for the period 1998 through February 2003, and (2) the corporate aircraft flight variable costs associated with Smith’s non-business use of the aircraft were $15,118 less than that stated in the original SLC Report dated October 24, 2005.

On January 4, 2006, I allowed the SLC’s motion to intervene as a party defendant for purposes of filing a motion to dismiss pursuant to G.L.c. 156D, s.7.44. The SLC moved to dismiss this action pursuant to G.L.c. 156D, s.7.44. [FN46]

FN46. Although the SLC moved to dismiss before it became a defendant intervener in this action, the plaintiff does not challenge the motion on those grounds. The SLC clarified at the hearing that its motion to dismiss is intended to apply to the allegations contained in the first amended complaint and to the allegations in the plaintiff’s second demand letter, upon which the plaintiff has sought to amend his complaint again. |

DISCUSSION

| I. | The Massachusetts Business Corporation Act |

General Laws c. 156D, known as the Massachusetts Business Corporation Act, became effective on July 1, 2004, and governs all Massachusetts business corporations that were formerly governed by G .L.c. 156B. Comment to Introduction to G.L.c. 156D. General Laws c.

12

156D, s.7.44, which sets forth the requirements for the dismissal of derivative actions, provides in pertinent part:

(a) A derivative proceeding commenced after rejection of a demand shall be dismissed by the court on motion by the corporation if the court finds that either (1) 1 of the groups specified in subsections (b)(1) or (f) has determined in good faith after conducting a reasonable inquiry upon which its conclusions are based that the maintenance of a derivative proceeding is not in the best interests of the corporation; or (2) shareholders specified in subsection (b)(3) have determined that the maintenance of the derivative proceeding is not in the best interests of the corporation.

(b) Unless a panel is appointed pursuant to subsection (f), the determination in subsection (a) shall be made by:

(1) a majority vote of independent directors present at a meeting of the board of directors if the independent directors constitute a quorum; [or]

(2) a majority vote of a committee consisting of 2 or more independent directors appointed by a majority vote of independent directors present at a meeting of the board of directors, whether or not the independent directors constituted a quorum; ...

(c) None of the following shall by itself cause a director to be considered not independent for the purposes of this section:

(1) the nomination or election of the director by a person who is a defendant in the derivative proceeding or against whom action is demanded;

(2) the naming of the director as a defendant in the derivative proceeding or as a person against whom action is demanded; or

(3) the approval by the director of the act being challenged in the derivative proceeding or demand if the act resulted in no personal benefit to the director.

(d) If the corporation moves to dismiss the derivative suit, it shall make a written filing with the court setting forth facts to show

(1) whether a majority of the board of directors was independent at the time of the determination by the independent directors and

(2) that the independent directors made the determination in good faith after conducting a reasonable inquiry upon which their conclusions are based. Unless otherwise required by subsection (a), the court shall dismiss the suit unless the plaintiff has alleged with particularity facts rebutting the corporation’s filing in its complaint or an amended complaint or in a written filing with the court ...

(e) If a majority of the board of directors does not consist of independent directors at the time the determination by independent directors is made, the corporation shall have the burden of proving that the requirements of subsection (a) have been met. If a majority of the

13

board of directors consists of independent directors at the time the determination is made ... the plaintiff shall have the burden of proving that the requirements of subsection (a) have not been met.

(f) The court may appoint a panel of 1 or more independent persons upon motion by the corporation to make a determination whether the maintenance of the derivative proceeding is in the best interests of the corporation ....”

| II. | Standard of Judicial Review Applicable to SLC Decisions |

“The special litigation committee is ... the 'only instance in American Jurisprudence where a defendant can free itself from a suit by merely appointing a committee to review the allegations of the complaint ...’” Einhorn v. Culea, 612 N.W.2d 78, 91 (Wis. 2000), quoting Lewis v. Fuqua, 502 A.2d 962, 967 (Del.Ch.1985).

“The value of a special litigation committee is coextensive with the extent to which that committee truly exercises business judgment. In order to ensure that special litigation committees do act for the corporation’s best interest, a good deal of judicial oversight is necessary in each case. At the same time, however, courts must be careful not to usurp the committee’s valuable role in exercising business judgment. At a minimum, a special litigation committee must be independent, unbiased, and act in good faith. Moreover, such a committee must conduct a thorough and careful analysis regarding the plaintiff’s derivative suit, ... The burden of proving that these procedural requirements have been met must rest, in all fairness, on the party capable of making that proof--the corporation.” |

Houle v. Low, 407 Mass. 810, 822 (1990).

A fundamental reason for forming an SLC is “to insulate the company’s decision making process from the influence of those under suspicion.” Biondi v. Scrushy, 820 A.2d 1148, 1156 (Del.Ch.2003). Consequently, in order for an SLC to have rendered a valid determination under the statute, it must have been appointed and constituted in accordance with the independence requirements of s.7.44(b)(2). Section 7.44(b)(2) not only mandates that the SLC consist of “2 or more independent directors,” but also that the independent members of the SLC have been “appointed by a majority vote of independent directors present at a meeting of the board of directors, whether or not the independent directors constituted a quorum.” A motion to dismiss premised upon the determination of an improperly constituted SLC is statutorily insufficient. Cf. Houle v. Low, 407 Mass. at 824 (interpreting predecessor to s.7.44, court reversed entry of summary judgment for corporate defendant which had not shown the absence of a genuine issue of material fact as to SLC’s bias).

Beyond that initial hurdle of showing that the SLC was properly constituted, the party moving to dismiss the derivative action bears the burden of submitting a written filing with the court setting forth facts to show that a majority of the Board was independent when the independent directors made their determination, and that the independent directors--here the SLC--made the determination in good faith after conducting a reasonable inquiry upon which its conclusions are based. See G.L.c. 156D, s.744(d). [FN47] If the SLC makes this showing, the

14

court must dismiss the suit unless the plaintiff alleges with particularity facts rebutting the SLC’s written statement of facts. Id.

FN47. The statute does not instruct whether the “determination” referred to in s.7.44(d) and (e) signifies the independent directors’ appointment of the SLC or the SLC’s determination not to pursue the derivative suit. But see Einhorn v. Culea, 612 N.W.2d at 92 (independence test is concerned with factors at time special litigation committee is formed). In this case, the composition of the directors was the same at both times and therefore it makes no difference which of these interpretations conforms to the intent of the Task Force on the Revision of the Massachusetts Business Corporation Law, which drafted the statute. |

If the SLC satisfies this burden of setting forth such facts regarding independence and the plaintiff alleges with particularity facts rebutting the SLC’s written filing under s.7.44(d), the court assesses the evidence as to whether or not the SLC was independent and whether it determined in good faith after conducting a reasonable inquiry upon which its conclusions are based that maintenance of the derivative proceeding is not in the best interests of the corporation.

General Laws c. 156D, s.7.44(e), places the burden of proving that the requirements of s.7.44(a) have been met upon either the corporation or the plaintiff, depending upon whether or not the majority of the board of directors consists of independent directors “at the time the determination by independent directors is made.” s.7.44(e). If the majority of the board is not independent, the SLC has the burden of proving that its determination was in good faith and after a reasonable inquiry upon which its conclusions were based. See s.7.44(a) & (e). If, on the other hand, the majority of the board is independent, the plaintiff bears the burden of showing that the SLC’s determination was flawed because it was not made in good faith after conducting a reasonable inquiry upon which its conclusions were based. Id. Comment 2 to s.7.44 explains as follows:

“Section 7.44 adopts neither of the so-called New York or Delaware approaches [FN48] to judicial scrutiny of the decisions of special litigation committees ... Section 7.44 steers a middle ground, applying the business judgment rule when a majority of the board is independent ... with the burden of proof being on the plaintiff, .... and the “reasonable and principled” review standard ... with the burden of proof being on the corporation [ ] when a majority of the board is not independent. Unlike Harhen, [431 Mass. 838 (2000),] the corporation is required in either case, in connection with a motion to dismiss, to present to the court a filing containing facts justifying application of the business judgment rule. The plaintiff then has an opportunity to rebut those facts.” |

FN48. The New York approach, also called the traditional version of the “special litigation committee defense,” is described in Auerbach v. Bennett, 47 N.Y.2d 619, 633, 419 N.Y.S.2d 920, 393 N .E.2d (1979). This approach requires the trial court to determine as a matter of fact whether the SLC members were disinterested and whether they conducted an adequate investigation. If the court answers both questions affirmatively, it must dismiss the derivative action. See id. In contrast, the Delaware formulation, set forth in Zapata Corp. v. Maldanado, 430 A.2d 779, 787- 89 (Del.1981), commences with the Auerbach analysis but |

15

adds a second, discretionary step in which the court applies its own business judgment to the SLC’s conclusion. |

Therefore, if the plaintiff bears the burden under s.7.44(e) yet fails to plead and prove that the SLC members were not independent or did not act in good faith after a reasonable inquiry, the SLC is entitled to the business judgment rule and the action must be dismissed. See Comment 2 to s.7.44 (to deprive the SLC of the business judgment rule’s protection, the plaintiff must “plead and prove that the directors making the determination were not independent or did not act in good faith after reasonable inquiry”). The business judgment rule “affords protection to the business decisions of directors, including the decision to institute litigation, because directors are presumed to act in the best interests of the corporation.” Harhen v. Brown, 431 Mass. 838, 845 (2000). The business judgment rule

“limits judicial review of corporate decision-making when corporate directors make business decisions on an informed basis, in good faith and in the honest belief that the action taken is in the best interests of the company. The business judgment rule shields, to a large extent, the substantive bases for a corporate decision from judicial inquiry. The business judgment rule also ensures that management remains in the hands of the board of directors and protects courts from becoming too deeply implicated in internal corporate matters.” |

Einhorn v. Culea, 612 N.W.2d at 84.

| III. | Standard of Independence |

Because the question of independence is fundamental to every aspect of judicial inquiry under s.7.44, it is essential at this point to pin down the principle. The statute contains no definition of this critical term, yet lists three circumstances, none of which by itself shall cause a director to be considered not independent: (1) the director’s nomination or election by a defendant or one against whom action is demanded; (2) the naming of the director as a defendant in the derivative proceeding or as a person against whom action is demanded; or (3) the approval by the director of the act being challenged in the derivative proceeding or demand if the act resulted in no personal benefit to the director. G.L.c. 156D, s.7.44(c). See also Kaplan v. Wyatt, 499 A.2d 1184, 1189 (Del.1985) (“Even a director’s approval of the transaction in question does not establish a lack of independence”).

These factors do not support the conclusion that the Legislature intended to set a low threshold for the standard of independence. See Einhorn v. Culea, 612 N.W.2d at 86-87 (rejecting lower courts’ conclusion that Wisconsin statute, which in relevant part precisely tracks the independence standard of G.L.c. 156D, s.7.44, sets an “extremely low threshold” for examining the independence of directors on a special litigation committee). The statute calls for the court to assess independence based upon whether or not a director has actual bias or a personal interest in the dispute, as a director may be named as a nominal defendant yet still be independent. See id. at 86. See also In re Oracle Corp. Derivative Litig., 824 A.2d 917, 939 (Del.Ch.2003) (independence test permits corporation to terminate derivative suit if board is comprised of directors who can impartially consider a demand).

16

Nor is there any support in the language of s.7.44 or the drafters’ comments for the SLC’s argument that there are only two forms of bias relevant to the inquiry of the SLC members’ independence: structural and pecuniary. [FN49] Rather, the term “independent” as used in Section 7.44 more broadly encompasses both “disinterest” which is a lack of a personal interest in the challenged transaction as opposed to a benefit upon the corporation or shareholders generally, and “independent” which is freedom from influence in favor of the defendants due to personal or other relationships. Comment 1 to G.L.c. 156D, s.7.44, citing Aronson v. Lewis, 473 A.2d 805, 812-16 (Del.1984).

FN49. As observed by the Supreme Judicial Court, legal commentators have described structural bias occurring in a director’s assessment of a suit as generated by a combination of psychosocial mechanisms, including the appointment of directors to the board or special litigation committee, the defendant directors’ control of pecuniary or nonpecuniary rewards to the independent directors, the independent directors’ prior associations with the defendants, and their common cultural and social heritages. Houle v. Low, 407 Mass. at 815-16. These mechanisms can, according to the commentators, generate biases which result in the independent directors reaching a decision which insulates their co-directors from legal sanctions. Id. at 816. |

The SLC shrinks the concept of structural bias considerably and argues that it boils down to domination and financial dependence. (1/20/06 Hrg. Tr. pp. 14-15). In an unpublished decision, the court in Klein v. FPL Group, Inc., 2004 WL 302292 *19, *23 (S.D.Fla.2004), flatly rejected the same argument, that “dominance and control” or “financial interest” are the only two factors in determining the independence of SLC members under Florida’s statute, which in relevant part is similar to G.L.c. 156D, s.7.44(a)- (b). |

Prior to the enactment of s.7.44, the Supreme Judicial Court explained the disinterested aspect of independence.

“The purpose of the distinction between interested and disinterested directors is to ensure that the directors voting on a plaintiff’s demand can exercise their business judgment in the best interests of the corporation, free from significant contrary personal interests and apart from the domination and control of those who are alleged to have participated in wrongdoing.” |

Harhen v. Brown, 431 Mass. at 843.

Directors are considered independent if they are in a position to base their decision on the merits of the subjects before the board rather than being governed by extraneous considerations and influences. See, e.g., Kaplan v. Wyatt, 499 A.2d at 1189; Einhorn v. Culea, 612 N.W.2d at 92 (“[T]he test [of independence] is primarily concerned with whether factors exist at the time the committee was formed that would prevent a reasonable person from basing his or her decisions on the merits of the issue”); Brehn v. Eisner, 746 A.2d 244, 257 (Del.2000) (test of whether majority of board was disinterested and independent is whether they were incapable, due to personal interest or domination and control, of objectively evaluating a demand); Aronson v.

17

Lewis, 473 A.2d at 815 (lack of independence is established where it is shown that directors are so under the influence of other directors that their discretion would be sterilized). Thus, the “director’s position with respect to the allegations of the claim and all extraneous influences are subject to the court’s scrutiny.” Desaigoudar v. Meyercord, 108 Cal.App.4th 173, 189, 133 Cal.Rptr.2d 408, 419-20 (Cal.App.2003). A director’s independence may reasonably be doubted if there is “evidence that in the past the relationship caused the director to act non-independently vis-a-vis an interested director.” Beam ex rel. Martha Stewart Omnimedia, Inc. v. Stewart, 845 A.2d 1040, 1051 (Del.2004) (discussing presuit demand independence standard).

Where, as here, the SLC has unconditional authority to act on behalf of the Board in investigating a shareholder’s demands and in deciding whether or not to litigate the shareholder’s claims, courts assess the SLC’s independence by considering the totality of the circumstances. See, e.g., Johnson v. Hui, 811 F.Sup. 479, 486 (N.D.Cal.1991). The totality of the circumstances test considers the following nonexclusive list of factors: (1) an SLC member’s status as a defendant and whether this potential liability is small or substantial, direct or indirect; (2) whether the SLC member’s participation in or approval of the alleged wrongdoing was substantial or the result of innocent or pro forma involvement or affiliations; (3) an SLC member’s past or present business dealings with the corporation; (4) an SLC member’s past or present business or social dealings with individual defendants; (5) the number of directors on the SLC, such that with the greater number of directors, less weight may be accorded to any disabling interest affecting only one director; and (6) the structural bias of the SLC, such as whether the manner in which the SLC was appointed and proceeded was inevitably bound to be empathetic to the defendants and therefore biased in favor of terminating the litigation. See id.; In re Oracle Securities Litigation, 852 F.Sup. 1437, 1441 (N.D.Cal.1994). Some courts add as a seventh factor the roles of corporate counsel and independent counsel, such that an SLC is more likely to be found independent if it retains counsel who has not represented individual defendants or the corporation in the past. See Einhorn v. Culea, 612 N.W.2d at 90.

| IV. | Whether the SLC Was Properly Constituted |

A. The Independence of the SLC

The determination of whether the SLC was properly appointed and constituted in conformity with the requirements of s.7.44(b)(2) begins with an evaluation of the independence of the SLC, and specifically Daly, as the plaintiff concedes the independence of Odak. As noted above, Section 7.44(b)(2) requires that the SLC consist of “2 or more independent directors.”

In his affidavit filed in support of the SLC’s motion to dismiss, Daly denied having any relationship which might impair his independence and denied being subject to a controlling influence of anyone with a material pecuniary interest in the transactions and conduct at issue in this action which might impair his independence. [FN50] The SLC’s factual submissions and argument that Daly is independent focus upon Daly’s illustrious history with Baystate Health Systems (BHS). [FN51]

FN50. Daly recited in his affidavit that he has no “business, financial or familial relationships with Mr. Smith and/or the Company beyond receipt of standard board compensation and compensation for my service as a member of the SLC that would reasonably be expected to affect my judgment as a member of the SLC |

18

in a manner adverse to the Company ... Neither I, nor any person with whom I have a business, financial or familial relationship has any material pecuniary interest in the transactions and conduct alleged to give rise to this action such that my judgment as a member of the SLC would be affected in a manner adverse to the Company ... I am not subject to a controlling influence by any of the named Defendants or anyone else who has a material pecuniary interest in the transactions or conduct alleged to give rise to the derivative claims that could reasonably be expected to affect my judgment as a member of the SLC with respect to the transactions or conduct in a manner adverse to the Company.” |

FN51. From December 1981 until December 2003, Daly was the president and CEO of BHS, and from January of 2004 to December of 2005 he was its vice chairman. Daly is also currently a director, and previously was chairman of the board, of BHS Insurance Company Limited, which writes group health insurance contracts and which pays money to Baystate Medical Center and other organizations for medical services. |

Daly’s role in Friendly falls within each of the three types of circumstances listed in G.L.c. 156D, s.7.44(c), none of which by itself suffices to label Daly as not independent: Daly was invited to the Board by Smith, Daly is named in the proposed complaint and as a person against whom Blake demanded action in his second demand letter, and Daly approved of the acts or transactions challenged by Blake in the proposed and current complaint, although there is no direct evidence (nor does the plaintiff contend) that they resulted in personal benefits to Daly. See G.L.c. 156D, s.7.44(c) ; Kaplan v.. Wyatt, 499 A.2d at 1189.

Several of the factors in the totality of circumstances test do not impugn Daly’s independence. Nothing indicates that Daly had significant business, economic, personal, family or social dealings with Friendly or the other individuals named in the proposed complaint. The plaintiff points to a recent revelation that Friendly employees in the Springfield area must use BHS or Baystate Medical Center for medical care, but there is no evidence that Daly was personally involved in imposing that requirement or that he has benefited in any way from this arrangement. See Kaplan v. Wyatt, 499 A.2d at 1189 (director’s association with businesses that transact with the corporation being sued does not, by itself, establish a lack of director’s independence). Smith’s invitation to Daly to join the Board does not demonstrate Daly’s bias in favor of Smith or support an inference that Daly would not faithfully discharge his fiduciary duty to Friendly’s shareholders. See In re Oracle Securities Litigation, 852 F.Sup. at 1441-42; Aronson v. Lewis, 473 A.2d at 816 (director’s method of election does not touch on independence). Further supporting a finding of independence of the SLC is its retention of counsel-- Wilmer Cutler--which has not previously represented Friendly or any of the individual defendants. Finally, on its face, Daly’s compensation in the form of stock options, $10,000 for his membership on the SLC, his annual compensation of approximately $30,000 as a director, additional annual payments of approximately $7,875 for attending Board meetings, plus $1,500 for membership on the Audit Committee, while far from de minimis, has not been shown to be beyond the norm so as to demonstrate, by itself, a lack of independence.

19

At first glance, Daly appears to meet many of the requirements for independence. Consideration of other factors, however, highlights the level of Daly’s involvement in conduct which Blake alleges amounts to a breach of fiduciary duty and establishes that he is more than a merely nominal defendant in the proposed complaint. Daly has been a member of Friendly’s largely static, relatively small, five-member Board and on its Audit Committee, Compensation Committee, and Nominating Committee since the November 1997 IPO. As a member of the 2002 Special Committee, Daly was asked to investigate Blake’s allegations that Smith improperly used Friendly funds to pay toward cost of the Illinois office and the Learjet for the direct or indirect benefit of Smith and/or TRC. That investigation therefore implicated Daly’s oversight duties on the Audit Committee, the Compensation Committee, and the Nominating Committee. Daly’s responsibilities on these committees, his decisions as a Board member with respect to the transactions in question, and his passive, largely nonresponsive role on the 2002 Special Committee render his involvement in conduct which Blake alleges to be a breach of his fiduciary duty substantial and direct, rather than merely nominal or pro forma. Contrast In re Oracle Securities Litigation, 852 F.Sup. at 1441 (special litigation committee member who was not a member of board of directors when alleged wrongdoing occurred was independent); Kaplan v. Wyatt, 499 A.2d at 1189 (there was no evidence of a lack of independence of director who abstained from voting on transaction in question).

Daly’s deposition testimony taken in 2004 reveals that neither he nor other members of the 2002 Special Committee sought adequate information or documentation about the Learjet cost-sharing arrangements between TRC and Friendly, even though Blake’s demand raised a red flag which ought to have triggered a meaningful inquiry into the propriety of these payments. Daly did not think it was necessary to find out if there was a contract requiring Friendly to pay TRC toward the Learjet costs. [FN52] Daly further testified that this was never even an issue considered by the Audit Committee or the Compensation Committee, and that he had no reason to doubt the contents of Parker’s superficial report to the 2002 Special Committee. [FN53] Similarly, as a member of the Audit Committee responsible for overseeing Friendly’s financial controls and procedures, Daly failed to detect or correct the comptroller’s payments of large sums over the course of several years for the Learjet without underlying invoices or other sufficient documentation for fixed and variable costs. This is in stark contrast to Daly’s testimony that the Audit Committee and the entire Board reviewed related party transactions with much greater care than normal business activities. [FN54]

FN52. Daly dep. p. 65.

FN53. DaIy dep. pp. 77-78. In his deposition on August 11, 2004, Daly claimed that what he knew about the corporate aircraft arrangement was presented to him in Parker’s three-page memorandum dated June 26, 2002. Daly dep. p. 43. Daly denied knowing when the change in aircraft occurred or that the change was discussed at a Board meeting before the plaintiff made an issue of it. Daly dep. pp. 45-47. |

FN54. Daly dep. pp. 149-50.

Other examples of Daly’s ignorance abound. Daly testified that he was unaware of what Estlin did for Friendly or that Smith owned 70% of TRC. When asked whether it would have

20

been good for Friendly and bad for TRC if Friendly could have obtained the corporate aircraft by paying TRC less than it had, Daly replied, “I don’t know that.” [FN55] Equally ludicrous is Daly’s denial in his deposition that under some circumstances, Friendly payments to TRC could benefit Smith or TRC. [FN56]

FN55. Daly dep. pp. 76-77.

FN56. Daly dep. p. 81.

Daly was sure of one thing: his reliance upon arrangements made by Friendly’s management, including Smith. When asked, “What precautions were taken in this case to make sure that the jet transactions were consistent with the market?” Daly replied,

“I don’t know. If you have confidence in your management--and I am not just speaking of Mr. Smith, I’m talking about the entire senior team--there is no reason to question that the arrangements made were not in the best interest of the company and I have such confidence in the management of this organization.” |

When asked if he continued to have that confidence when he was functioning as a member of the 2002 Special Committee, Daly answered, “Absolutely. This is a senior management team with senior executives who have earned my respect.” Daly’s belief that there was no reason to question the propriety of the aircraft cost-sharing arrangement, even when tasked with investigating it as a member of the 2002 Special Committee, establishes that he was not able to evaluate Blake’s claims impartially at least between 2002 and 2004, when he gave this testimony.

A director must be reasonably informed, which means that he or she is “responsible for considering only material facts that are reasonably available, not those that are immaterial or out of the Board’s reasonable reach.” Brehm v. Eisner, 746 A.2d at 259. [FN57]

FN57. “All corporate power shall be exercised by or under the authority of, and the business and affairs of the corporation shall be managed under the direction of, its board of directors ...” G.L.c. 156D, s.8.01(b). |

“In discharging his duties, a director who does not have knowledge that makes reliance unwarranted is entitled to rely on information, opinions, reports, or statements ... if prepared or presented by ... (1) one or more officers or employees of the corporation whom the director reasonably believes to be reliable and competent with respect to the information, opinions, reports or statements presented; (2) legal counsel, public accountants, or other persons retained by the corporation as to matters involving skills or expertise the director reasonably believes are matters (i) within the particular person’s professional or expert competence or (ii) as to which the particular person merits confidence; or (3) a committee of the board of directors of which the director is not a member if the director reasonably believes the committee merits confidence ...” |

G.L.c. 156D, s.8.30(b) (emphasis supplied). See also Juergens v. Venture Capital Corp., 1 Mass.App.Ct. 274, 278 (1973) (it is the duty of directors to keep themselves informed about the conduct of the business). |

21

“While directors may confer, debate, resolve their differences through compromise, or by reasonable reliance upon the expertise of their colleagues and other qualified persons, the end result, nonetheless, must be that each director has brought his or her own informed business judgment to bear with specificity upon the corporate merits of the issues without regard for or succumbing to influences which convert an otherwise valid business decision into a faithless act.” |

Aronson v. Lewis, 473 A.2d at 816. See also Kaplan v. Wyatt, 499 A.2d at 1189 (“it is the care, attention and sense of individual responsibility to the performance of one’s duties that touch on independence”).

Despite his duty as a director to oversee the business affairs and management of Friendly, and his obligations as a member of the 2002 Special Committee, the Audit Committee, the Compensation Committee, and the Nominating Committee, Daly remained oblivious and failed to apprise himself of reasonably available, material facts regarding the transactions in question. This record fails to show that Daly exercised meaningful oversight in any of these various capacities, for most of which he received compensation. At a bare minimum, Daly ought to have realized from a cursory review of Parker’s three-page memorandum to the 2002 Special Committee that the “investigation” to that committee regarding Blake’s claims was largely devoid of critical analysis and impaired by obvious significant gaps in the documentation. Furthermore, a reasonable director would have questioned whether or not his reliance upon Parker was warranted, in light of the shallow nature of Parker’s memorandum and Smith’s role in recommending to the Board whether or not Parker would receive a bonus. Daly’s unreasonable and unwarranted reliance upon what he was or was not told by Parker, Smith, Okscin; and/or Friendly’s management invites skepticism with respect to his claimed ignorance of or indifference toward the alleged improprieties and casts serious doubt on his ability to be independent in assessing Blake’s claims. See Beam ex rel. Martha Stewart Omnimedia, Inc. v. Stewart, 845 A.2d at 1051.

Moreover, as a member of the SLC investigating Blake’s expanded allegations that, inter alia, the directors breached their fiduciary duty by condoning and ignoring the improper conduct, Daly was essentially being asked to evaluate his own conduct on the Board, its committees, and as a member of the 2002 Special Committee . [FN58] Because Daly was substantially and personally involved in the conduct challenged by Blake he may face personal liability for breach of fiduciary duty as alleged in the proposed complaint. See Allied Freightways, Inc. v. Cholfin, 325 Mass. 630, 634 (1950) (“A director of a corporation cannot avoid liability for losses sustained by the wrongful conduct of corporate officers by showing that he had abandoned his duties as director or that his ignorance of such conduct was due to what amounted to wilful neglect of his duties”). In all these circumstances, it is far from clear that Daly was in a position to have objectively assessed Blake’s demands or to have based his decision as an SLC member on the merits of the issues rather than on extraneous considerations or influences, such as concern about his own liability, a dynamic of group loyalty geared toward insulating other members of the Board from liability, and/or an improperly deferential relationship to Smith, Parker, Okscin, and others in dereliction of his duties.

FN58. The SLC argues strenuously that because Blake did not challenge Daly’s independence as a member of the 2002 Special Committee, he cannot do so now |

22

plausibly. What the SLC ignores is that the conduct of the 2002 Special Committee is being attacked in Blake’s proposed amended complaint. Daly’s independence before the creation of the 2002 Special Committee could only be challenged on the ground that Daly, as a director and member of some Board committees, approved of payments for the Learjet and Illinois office. In contrast, the current independence assessment takes into account Daly’s role on the 2002 Special Committee and as a director acting on that committee’s recommendation. |

The SLC has failed to show Daly’s independence. Because the SLC was not comprised of “two or more independent directors” as required by G.L.c. 156D, s.7.44(b)(2), it was improperly constituted, not independent and lacked authority to render a valid determination as to whether or not to maintain the derivative proceeding. See Houle v. Low, 407 Mass. at 824. Accordingly, the SLC’s motion to dismiss fails.

| B. | Whether the SLC Was Appointed By a Majority of Independent Directors |

Nonetheless, the Court turns to consider another aspect of the validity of the SLC; whether it was appointed by a majority vote of independent directors as required by G.L.c. 156D, s.7.44(b)(2). With Daly’s status settled, at issue is the independence or lack thereof of Ezzes and Manning, since all parties agree that Smith is not independent and Odak is.

| 1. | Ezzes |

Ezzes is a financial expert, securities analyst, and has been a financial advisor and managing director for numerous financial services firms and other entities. He is hailed by Manning as an “extremely sophisticated financial guy, [with a] financial mind.” From 1991 until sometime in 1998 or 1999, Ezzes was a member of the Board of Directors of Perkins, the Perkins Management Corporation, and TRC. [FN59] From 1998 to October 1999, Ezzes was a managing director of S.G. Cowen, a subsidiary of Societe Generale, an international financial services institution. In 1997, Societe Generale was one of three co-managers in the 1997 Friendly IPO.

FN59. Ezzes could not recall at his deposition in February of 2005 how long he served on the TRC board, but instead responded, “I served on the TRC board for a period of time. I’m not sure of the exact dates.” Although Ezzes originally denied being on the board of directors of TRC or Perkins in 1999, he later testified that he did not recall whether or not he was on either of those boards in August of 1999 when it voted to upgrade the corporate aircraft. In his affidavit filed in January of 2006, Ezzes stated that his service on all boards affiliated with Perkins ceased in 1998. |

Ezzes first was a director of Friendly from 1991-1992, and rejoined the Board in 1995 at the request of Don Cameron, who had taken Ezzes’s place on the Board. [FN60] Ezzes has been a director of Friendly continuously since 1995.

FN60. Ezzes dep. p. 10-11; Ezzes affid, p. 9.

Ezzes’s deposition testimony, given on February 1, 2005, was marked by evasion, surliness, and memory loss. [FN61] When asked whether at any time the Audit Committee had

23

discussed or reviewed related party transactions between Friendly and TRC or Perkins, Ezzes eventually disclosed that the Audit Committee had discussed the fact that there are purchases between these companies involving ice cream and pancake mix and that it involves a “fairly de minimis” amount of money. The SLC concedes that Friendly paid TRC or Perkins at least $4.4 million from 1998 trough 2004. [FN62] Ezzes denied that the Audit Committee had ever discussed the corporate aircraft or management fees, and stated that the aircraft issue had been raised only at meetings of the full Board.

FN61. For example, when asked whether Friendly was paying management fees to TRC, Ezzes replied that he could not answer the question without a definition of management fees, despite his roles as a director at both Friendly and TRC when in March of 1996 the two companies purportedly entered the management fee agreement (which appears to have been the sole management fee agreement known to the Friendly directors), and his membership on the Audit Committee. |

FN62. The SLC earlier calculated the total to be $5,389,000, based upon Friendly’s Annual Reports (Forms 10-K) filed for the years in question. |

Ezzes testified that in deciding as a director of Friendly to dispose of the Beechjet and to acquire the Learjet, it was not relevant to him to know the extent of Smith’s ownership interest in TRC or Perkins and that he was unaware of this information at any time. [FN63] Ezzes voted as a Board member to pay an amount not to exceed $900,000 to terminate what he believed was an obligation under an aircraft reimbursement agreement. When asked for the basis of this belief, Ezzes replied that it is not a director’s obligation to examine every contract entered into by the corporation, and that the Board did not perform any more due diligence to determine whether Friendly had such an obligation than if it had to determine whether Friendly had an obligation to pay for butter or milk or trucks. [FN64] This contradicts Daly’s testimony that related party transactions received far more scrutiny by the entire Board as well as by the Audit Committee than normal business activities. [FN65] Ezzes testified that as a member of the 2002 Special Committee he did not discuss whether or not Smith’s use of the Learjet for commuting was a nonbusiness purpose. [FN66]

FN63. Ezzes dep. p. 56.

FN64. Ezzes dep. p. 83.

FN65. Daly dep. pp. 148-52.

FN66. Ezzes dep. p. 127.

When pressed on the issue of whether Smith would have an incentive to put TRC or Perkins first over Friendly if he owned more of TRC/Perkins than Friendly, Ezzes repeatedly attempted to dodge the questions by challenging their relevance and asserting his disagreement with the line of questions because, as Ezzes put it,