UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

[X] ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2007

or

[ ] TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from ________ to ________

Commission file number 1-10006

FROZEN FOOD EXPRESS INDUSTRIES, INC.

(Exact name of registrant as specified in its charter)

TEXAS (State or other jurisdiction of incorporation or organization) | | 75-1301831 (I.R.S. Employer Identification No.) |

1145 EMPIRE CENTRAL PLACE, DALLAS, TEXAS (Address of principal executive offices) | | 75247-4305 (Zip Code) |

Registrant's telephone number, including area code: (214) 630-8090

Securities registered pursuant to Section 12(b) of the Act:

| | Name of Each Exchange on Which Registered |

| i) Common Stock $1.50 par value ii) Rights to purchase Common Stock | | The NASDAQ Stock Market LLC (NASDAQ Global Select Market) |

Securities registered pursuant to Section 12(g) of the Act: NONE

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act: Yes [ ] No [ X ]

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act: Yes [ ] No [ X ]

Indicate by check mark whether the registrant (l) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes [ X ] No [ ]

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. [ X ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or smaller reporting company. See the definition of “large accelerated filer”, “accelerated filer”, and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer [ ] Accelerated filer [ X ] Non-accelerated filer [ ] Smaller reporting company [ ]

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes [ ] No [ X ]

The aggregate market value of 15,969,049 shares of the registrant’s $1.50 par value common stock held by non-affiliates as of June 30, 2007 was approximately $161,926,000 million (based upon $10.14 per share).

As of February 29, 2008, the number of outstanding shares of the registrant’s common stock was 16,650,992.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant's Annual Report to Stockholders for the year ended December 31, 2007 and Proxy Statement for use in connection with its Annual Meeting of Stockholders to be held on May 14, 2008, to be filed with the Securities and Exchange Commission pursuant to Regulation 14A not later than 120 days after December 31, 2007, are incorporated by reference in Part III (Items 10, 11, 12, 13 and 14).

| | | PAGE |

| | | |

| Business | 1 |

| | | |

| Risk Factors | 5 |

| | | |

| Unresolved Staff Comments | 7 |

| | | |

| Properties | 7 |

| | | |

| Legal Proceedings | 8 |

| | | |

| Submission of Matters to a Vote of Security Holders | 8 |

| | | |

| | | |

| | | |

| Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | 9 |

| | | |

| Selected Financial Data | 11 |

| | | |

| Management's Discussion and Analysis of Financial Condition and Results of Operations | 11 |

| | | |

| Quantitative and Qualitative Disclosures about Market Risk | 25 |

| | | |

| Financial Statements and Supplementary Data | 26 |

| | | |

| Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | 43 |

| | | |

| Controls and Procedures | 43 |

| | | |

| Other Information | 44 |

| | | |

| | | |

| | | |

| Directors and Executive Officers of the Registrant and Corporate Governance | 44 |

| | | |

| Executive Compensation | 44 |

| | | |

| Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | 44 |

| | | |

| Certain Relationships and Related Transactions and Director Independence | 44 |

| | | |

| Principal Accountant Fees and Services | 44 |

| | | |

| | | |

| | | |

| Exhibits and Financial Statement Schedules | 44 |

| | | |

| | | |

| | | |

| | | |

| Exhibit 10.8 | FFE Transportation Services, Inc. Restated Wrap Plan | 48 |

| Summary of Compensation Arrangements for Timothy L. Stubbs | 63 |

Exhibit 10.21 | Dividend and Compensation Arrangements of Certain Officers | 64 |

| Subsidiaries of Frozen Food Express Industries, Inc. | 65 |

| Consent of Independent Public Accounting Firm | 66 |

Exhibit 23.2 | Consent of Independent Public Accounting Firm | 67 |

| Certification of Chief Executive Officer Required by Rule 13a-14(a)(17 CFR 240.13a-14(a)) | 68 |

| Certification of Chief Financial Officer Required by Rule 13a-14(a)(17 CFR 240.13a-14(a)) | 69 |

| Certification of Chief Executive Officer Pursuant to 18 U.S.C. Section 1350 to Section 906 | 70 |

| Certification of Chief Financial Officer Pursuant to 18 U.S.C. Section 1350 to Section 906 | 71 |

PART I

ITEM 1. Business.

Frozen Food Express Industries, Inc. is a publicly-owned motor carrier with core operations in the transport of temperature-controlled products and perishable goods including food products, health care products and confectionary items. Service is offered in over-the-road and intermodal modes for temperature-controlled truckload and less-than-truckload, as well as dry truckload. We also provide brokerage, or logistics services, as well as dedicated fleets. We were incorporated in Texas in 1969, as successor to a company formed in 1946. Our principal office is located at 1145 Empire Central Place, Dallas, Texas 75247-4305. References to “we” or “us”, unless the context requires otherwise, include Frozen Food Express Industries, Inc. and our subsidiaries, all of which are wholly-owned. Our services are further described below:

- TRUCKLOAD LINEHAUL SERVICE: This service provides for the shipment of a load, typically weighing between 20,000 and 40,000 pounds and usually from a single shipper, which fills the trailer. Normally, a truckload shipment has a single destination, although we are also able to provide multiple deliveries. According to industry publications and based on 2006 revenue (the most recent year for which data is available), we are one of the largest temperature-controlled, truckload carriers in North America.

- DEDICATED FLEETS: In providing certain truckload services, we contract with a customer to provide service involving the assignment of specific trucks and drivers to handle certain of the customer's transportation needs. Frequently, we and our customers anticipate that dedicated fleet logistics services will lower the customer's transportation costs and improve the quality of service.

- LESS-THAN-TRUCKLOAD ("LTL") LINEHAUL SERVICE: This service provides for the shipment of a load, typically consisting of up to 30 shipments, each weighing as little as 50 pounds or as much as 20,000 pounds, from multiple shippers destined to multiple receivers. Our temperature-controlled LTL operation is the largest in the United States and the only one offering regularly scheduled nationwide service. In providing refrigerated LTL service, multi-compartment trailers enable us to haul products requiring various levels of temperature control as a single load.

- BROKERAGE: Our brokerage operation helps us to balance the level of demand in our core trucking business. Orders for shipments to be transported for which we have no readily available transportation assets are assigned to other unaffiliated motor carriers through our brokerage service. We establish the price to be paid by the customer and we invoice the customer. Accordingly, we also assume the credit risk associated with the transaction. Our brokerage service also pays the other motor carrier and earns a margin on the difference.

- OTHER: During the last four months of 2005, many of our resources were engaged in providing relief to the regions affected by Hurricanes Katrina and Rita. We provided dedicated fleet services, which contributed revenue of $5.7 million in 2005 and $500 thousand for similar services in 2006. No such revenue was generated during 2007. We also provided temperature-controlled trailers, which were rented on a per-day basis for storage and transportation of perishable items. Such hurricane-related trailer rentals generated revenue of $3.2 million during the final three months of 2005 and $2.2 million for rentals that continued into 2006.

The following table summarizes and compares the components of our revenue for each of the years in the five-year period ended December 31, 2007 (in millions): | Revenue from: | | 2007 | | | 2006 | | | 2005 | | | 2004 | | | 2003 | |

| Truckload linehaul services | | $ | 212.4 | | | $ | 237.5 | | | $ | 263.2 | | | $ | 258.7 | | | $ | 239.8 | |

| Dedicated fleets | | | 17.9 | | | | 21.1 | | | | 31.5 | | | | 20.3 | | | | 14.5 | |

| Less-than-truckload linehaul services | | | 127.4 | | | | 129.8 | | | | 131.2 | | | | 123.2 | | | | 115.5 | |

| Fuel surcharges | | | 73.4 | | | | 75.1 | | | | 63.5 | | | | 31.7 | | | | 15.7 | |

| Brokerage | | | 15.6 | | | | 12.5 | | | | 15.6 | | | | 24.9 | | | | 15.0 | |

| Equipment rental | | | 5.5 | | | | 7.7 | | | | 9.0 | | | | 5.9 | | | | 5.4 | |

| | | $ | 452.2 | | | $ | 483.7 | | | $ | 514.0 | | | $ | 464.7 | | | $ | 405.9 | |

Additional information regarding our business is presented in the Notes to Consolidated Financial Statements included in Item 8 and in Management's Discussion and Analysis of Financial Condition and Results of Operations in Item 7 of this Annual Report on Form 10-K.

We offer nationwide services to nearly 10,000 customers, none of which accounted for more than 10% of total revenue during each of the past five years. Revenue from international activities was less than 10% of total revenue during each of the past five years.

MARKETING

Our temperature-controlled and non-temperature-controlled ("dry") trucking operations serve nearly 10,000 customers in the United States, Mexico and Canada. Temperature-controlled shipments account for about 75% of our total revenue. Our customers are involved in a variety of products including food products, pharmaceuticals, medical supplies and household goods. Our customer base is diverse in that our 5, 10 and 20 largest customers accounted for 22%, 32% and 42%, respectively, of our revenue during 2007. None of our markets are dominated by any single competitor. We compete with several thousand other trucking companies. The principal methods of competition are price, quality of service and availability of equipment needed to satisfy customer requirements.

Temperature-Controlled Trucking: The products we haul include meat, ice, poultry, seafood, processed foods, candy and other confectionaries, dairy products, pharmaceuticals, medical supplies, fresh and frozen fruits and vegetables, cosmetics, film and Christmas trees. In the temperature-controlled market, it may be necessary to keep freight frozen, as with ice; to keep freight cool, as with candy; or to keep freight from freezing, for example, when delivering fresh produce or flowers to Minnesota during winter. The common and contract hauling of temperature-sensitive cargo is highly fragmented and comprised primarily of carriers generating less than $50 million in annual revenue. Industry publications report that only twelve other temperature-controlled carriers generated $100 million or more of revenue in 2006, the most recent year for which data is available. In addition, many major food companies, food distribution firms and grocery chain companies transport a portion of their freight with their own fleets ("private carriage").

High-volume shippers frequently seek to lower their cost structures by reducing their private carriage capabilities by turning to common and contract carriers ("core carriers") for their transportation needs. As core carriers continued to improve their service capabilities through such means as satellite communications systems and electronic data interchange, some shippers abandoned their private carriage fleets in favor of common or contract carriage.

Non-Temperature-Controlled Trucking: Our non-temperature-controlled (“dry”) trucking fleet conducts business under the name American Eagle Lines ("AEL"). AEL accounts for about 35% of our truckload linehaul revenue. AEL serves the dry truckload market throughout the United States and Canada. Also, during 2007, about 10% of the truckload shipments transported by our temperature-controlled fleets were of dry commodities.

Intermodal: In providing our truckload linehaul service, we often engage railroads to transport shipments between major cities. In such an arrangement (called "intermodal" service), loaded trailers are transported to a rail facility and placed on flat cars for transport to their destination. On arrival, we pick up the trailer and deliver the freight to the consignee. Intermodal service is generally less costly than using one of our own trucks for such movements, but other factors also influence our decision to utilize intermodal services.

OPERATIONS

The management of a number of factors is critical to a trucking company's growth and profitability, including:

Employee-Drivers: We maintain an active driver recruiting program. Driver shortages and high turnover can reduce revenue and increase operating expenses through reduced operating efficiency and higher recruiting costs. Since 2002, our operations have periodically been affected by driver shortages. At various times, we have not been able to attract and retain a sufficient number of qualified drivers.

For much of 2003, the labor market remained soft, and we experienced less difficulty in attracting qualified employee-drivers than in 2002. From 2003 into the first part of 2007, the economy has improved and our ability to attract such drivers has been negatively impacted. During 2007 and into 2008, the economy has weakened and driver retention has improved. If the economy strengthens during 2008, the availability of qualified drivers could continue to diminish. Effective April 2006, we implemented a general rate increase of $0.02 per mile, an increase of about 6%, for all employee-drivers.

During 2007, our employee-driver turnover rate was approximately 90%, depending on a number of factors, as compared to industry averages exceeding 120% during the same period. If we can retain a driver through the fairly difficult first six- to twelve-month period, we usually have the opportunity to retain them for the long-term. For example, the average tenure for all of our drivers at the end of 2007 was 3.4 years, but for trainees, the average tenure was 2.5 months. Among drivers who have been with us for at least one year, the average tenure was 5.6 years.

Owner-Operators: We actively seek to expand our fleet with equipment provided by owner-operators, who act as independent contractors. Owner-operators provide tractors and drivers to pull our loaded trailers. Each owner-operator pays for the drivers' wages, fuel, equipment-related expenses and other transportation expenses and receives either a portion of the revenue from each load or a guaranteed rate per mile. At the end of 2007, we had contracts for 412 owner-operator tractors in our truckload operations and 162 in our LTL operations. Of the 412 truckload tractors, 264 were owned by us and leased to the involved owner-operators.

The percent of linehaul truckload and LTL revenue generated from shipments transported by owner-operators during each of the last five years is summarized below:

Percent of Linehaul Revenue from Shipments Transported by Owner-Operators | | 2007 | | | 2006 | | | 2005 | | | 2004 | | | 2003 | | |

| Truckload | | | 24 | % | | 24 | % | | 26 | % | | 29 | % | | 31 | % | |

| LTL | | | 54 | % | | 56 | % | | 59 | % | | 62 | % | | 63 | % | |

To compensate owner-operators for the use of their trucks, we pay them commissions that are based either upon the amount of revenue we earn from the shipments they transport or upon the miles their trucks travel to haul our freight. Freight hauled by an owner-operator is transported under operating authorities and permits issued to us by various state and federal agencies. We, and not the owner-operator, are accountable to the customers for any problems encountered related to the shipment. We, and not the owner-operator, have sole discretion as to the price the customer will pay for the service, and owner-operators may decline to haul specific loads for any reason, including their belief that their revenue-based commission will not be to their satisfaction. Further, we, and not the owner-operator, are 100% at risk for credit losses should the customer fail to pay us for the service. For these reasons, revenue from shipments hauled by owner-operators is recorded as gross of owner-operator commissions, rather than as an agent net of such commissions.

Fuel: Our average cost per gallon of fuel doubled between 2003 and 2007, including an increase of approximately 14% in 2006, and an increase of 7% during 2007, each as compared to the prior year. Through February of 2008, the cost per gallon of fuel has increased an additional 19% over that of 2007. Owner-operators are responsible for all costs associated with their equipment, including fuel. Therefore, the cost of such fuel is not a direct expense of ours. Fuel price fluctuations result from many external market factors that cannot be influenced or predicted by us.

In most years states increase fuel and road use taxes. Our recovery of future increases or realization of future decreases in fuel prices and fuel taxes, if any, will continue to depend upon competitive freight market conditions.

We do not hedge our exposure to volatile energy prices. We are able to mitigate the impact of such volatility by adding fuel surcharges to the basic rates for the services we provide. Surcharges are designed to, but often do not, fully offset the increased fuel expenses we incur when prices escalate rapidly.

Though we will continue to add fuel surcharges whenever possible, there can be no assurance that we can add them in an amount sufficient to minimize the impact of fuel prices on our results of operations.

Factors that could prevent us from fully recovering fuel cost increases include the competitive environment, deadhead (empty) miles, tractor engine idling and fuel to power our trailer refrigeration units. Such fuel consumption often cannot be attributed to a particular load and therefore, there is no incremental revenue to which a fuel surcharge may be applied. Also, our fuel surcharges are computed by reference to federal government indices that are released weekly for the preceding week. When prices are rising, our fuel cost in a given week is more than the price indicated by the government reports for the preceding week. Accordingly, we are unable to recover the excess of the current week's actual price to the preceding week's indexed price.

The Environmental Protection Agency (“EPA”) has mandated lower emission standards for newly manufactured tractor engines. We scheduled our new equipment purchases to accommodate these new standards to allow adequate testing of the new engines. The 2007 EPA-compliant engines are equipped with a diesel particulate filter and will require more costly ultra-low-sulfur diesel (ULSD) fuel. ULSD fuel costs approximately $0.04 to $0.05 more per gallon.

Risk Management: Liability for accidents is a significant concern in the trucking industry. Exposure can be large and occurrences can be unpredictable. The cost and human impact of work-related injury claims can also be significant. We maintain a risk management program designed to minimize the frequency and severity of accidents and to manage insurance coverage and claims expense.

Our risk management program is founded on the continual enhancement of safety in our operations. Our safety department conducts programs that include driver education and over-the-road observation. All drivers must meet or exceed specific guidelines relating to safety records, driving experience and personal standards, including a physical examination and mandatory drug testing.

Drivers must also complete our training program, which includes tests for motor vehicle safety and over-the-road driving. They must have a current commercial driving license before being assigned to a tractor. Student drivers undergo a more extensive training program with an experienced instructor-driver. In accordance with federal regulations, we conduct drug tests on all driver candidates and maintain a continuing program of random testing for use of such substances. Applicants who test positive for drugs are turned away and drivers who test positive for such substances are immediately disqualified.

As of December 31, 2007, our liability insurance provides for a $3 million deductible for each occurrence. We are fully insured between $3 million and $5 million per occurrence. The insurance company and we share in losses on a 75%/25% basis between $5 million and $10 million per occurrence. Accordingly, our maximum exposure for a $10 million insured loss is $4.25 million. We are fully insured for liability exposures between $10 million and $50 million. Our liability insurance policies will expire in mid-2008, at which time these coverage levels may change. Insurance premiums do not significantly contribute to our operating costs, primarily because we carry large deductibles under our policies of liability insurance.

Because of our retained liability, a series of very serious traffic accidents, work-related injuries or unfavorable developments in the outcomes of existing claims could materially and adversely affect our operating results. Claims and insurance expense can vary significantly from year to year. Reserves representing our estimate of ultimate claims outcomes are established based on the information available at the time of an incident. As additional information regarding the incident becomes available, any necessary adjustments are made to previously recorded amounts. The aggregate amount of open claims, some of which involve litigation, is significant.

During December, 2007, a major ice storm hit the mid-section of the United States. One of our trucks was involved in a chain-reaction accident on an icy bridge. Due to various factors and events that occurred relative to this incident, we established a significant reserve for the outcome of this event.

We engage the services of an independent actuarial firm to analyze our claims history and to establish reasonable estimates of our claims reserves. In addition, the actuarial firm provided us procedures with which to establish appropriate claims reserves in future periods.

Customer Service: Major shippers continue to require increasing levels of service and rely on their core carriers to provide transportation and logistics solutions, such as providing the shipper real-time information about the movement and condition of any shipment.

Temperature-controlled truckload service requires a substantially lower capital investment for terminals and lower costs for shipment handling and information management than does LTL. At the end of 2007, our truckload tractor fleet consisted of 1,271 tractors owned or leased by us and 412 tractors contracted to us by owner-operators, making us one of the seven largest temperature-controlled truckload carriers in North America.

We conduct operations involving "dedicated fleets". In such an arrangement, we contract with a customer to provide service involving the assignment of specific trucks to handle the transportation needs of a specific customer. Frequently, we and our customers anticipate that dedicated fleet logistics services will lower the customer's transportation costs and improve the quality of the service the customer receives. We continuously improve our capability to provide and to market our dedicated fleet services. About 9% of our company-operated truckload fleet is now engaged in dedicated fleet operations.

Temperature-controlled LTL trucking is service and capital intensive. LTL freight rates are higher than those for truckload and are based on mileage, weight, commodity type, trailer space, and pick-up and delivery locations. Temperature-controlled LTL trucking requires a system of terminals capable of temporarily holding refrigerated and frozen products. Our LTL terminals are strategically located in or near New York City, Philadelphia, Atlanta, Lakeland (Florida), Miami, Chicago, Memphis, Dallas, Salt Lake City, Modesto (California) and Los Angeles. Some of these LTL terminals also serve as truckload driver centers where company-operated, truckload fleets are based. Additional truckload operations are based in our Ft. Worth, Texas facility.

Information Management: Information management is essential to a successful temperature-controlled trucking operation. On a typical day, our LTL system handles about 6,000 shipments - about 4,000 on the road, 1,000 being delivered and 1,000 being picked up. In 2007, our LTL operation handled almost 280,000 individual shipments.

Our truckload fleets use computer and satellite technology to enhance efficiency and customer service. The satellite-based communications system provides automatic hourly position updates of each truckload tractor and permits real-time communication between operations personnel and drivers. Dispatchers relay pick-up, delivery, weather, road and other information to the drivers while shipment status and other information is relayed by the drivers to our computers via the satellite.

International Operations: Service to and from Canada is provided using tractors from our fleets. We partner with Mexico-based trucking companies to facilitate freight moving both ways across the southern United States border. Freight moving from Mexico is hauled in our trailers to the border by the Mexico-based carrier, where the trailers are exchanged. Southbound shipments work much the same way. This arrangement has been in place for more than ten years.

In February, 2007, the United States Department of Transportation (“DOT”) announced a new program to allow United States-based trucks into Mexico for the first time ever and to change how some Mexico-based trucks may operate within the United States. Regarding the ability of Mexican trucks to operate within the United States, the DOT has put in place a rigorous inspection program to ensure the safe operation of Mexico-based trucks crossing the border. Mexican trucking companies that may be allowed to participate in this program will be required to have insurance with a U.S. licensed firm and meet all U.S. safety standards. Companies that meet these standards will be allowed to make international pick up and deliveries only and will not be able to move goods from one U.S. city for delivery to another.

We do not expect to change our manner of dealing with freight to or from Mexico. Although we serve customers in Mexico, less than 10% of our consolidated linehaul revenue during 2007 involved international shipments, all of which was billed in United States currency.

EQUIPMENT

We operate premium company-owned tractors in order to help attract and retain qualified employee-drivers, promote safe operations, minimize maintenance and repair costs and assure dependable service to our customers. We believe the higher initial investment for our equipment is recovered through more efficient vehicle performance offered by such premium tractors and improved resale value. Repair costs are mostly recovered through manufacturers' warranties, but routine and preventative maintenance is our expense.

When we put a new truck into service, we and the manufacturer typically agree that the manufacturer will purchase that truck from us at the end of the truck’s service life, typically after 42 months.

Changes in the size of our fleet depend upon acquisitions, if any, of other motor carriers, developments in the nation's economy, demand for our services and the availability of qualified drivers. Continued emphasis will be placed on improving the operating efficiency and increasing the utilization of the fleet through enhanced driver training and retention and reducing the percentage of empty, non-revenue producing miles. Due to the current softness in customer demand for our services, we do not plan to add trucks to our company-operated, truckload fleet during 2008.

The federal government has required new technology for truck engines. The new technology is designed to reduce emission from diesel engines. Our cost of new trucks increased 12.5% largely due to the new engines. The newer engines are also more costly to maintain over the service life of the trucks. In order to delay the purchase price increase, the additional maintenance expenses and other uncertainties involved with the new technology engines, we took delivery during late 2006 and early 2007 of 720 trucks without the new technology, and retired a number of older 2003 and 2004 model trucks from service. In late 2007, we placed 34 trucks with the EPA compliant engines in service, and expect to add another 518 as replacements for older tractors in 2008. Because we retired older equipment with our pre-purchase strategy, we did not have an excess number of trucks sitting idle, as did many other companies who purchased the old-technology trucks.

REGULATION

Our trucking operations are regulated by the DOT. The DOT generally governs matters such as safety requirements, registration to engage in motor carrier operations, certain mergers, insurance, consolidations and acquisitions. The DOT conducts periodic on-site audits of our compliance with its safety rules and procedures. Our most recent audit, which was completed in March of 2008, resulted in a rating of "satisfactory", the highest safety rating available. A "conditional" or "unsatisfactory" DOT safety rating could have an adverse effect on our business, as some of our contracts with customers require a satisfactory rating and our qualification to self-insure our liability claims would be impaired.

During 2005, the Federal Motor Carrier Safety Administration ("FMCSA") began to enforce changes to the regulations which govern drivers' hours of service. Hours of Service ("HOS") rules issued by the FMCSA, in effect since 1939, generally limit the number of consecutive hours and consecutive days that a driver may work. The new rules reduced by one hour the number of hours that a driver may work in a shift, but increased by one hour the number of hours that a driver may drive during the same shift. Drivers often are working at a time they are not driving. Duties such as fueling, loading and waiting to load count as part of a driver's shift that are not considered driving. Under the old rules, a driver was required to rest for at least eight hours between shifts. The new rules increased that to ten hours, thereby reducing the amount of time a driver can be "on duty" by two hours.

Because of the two additional hours of required rest period time and the amount of time our drivers spend loading and waiting to load, we believe the new rules have reduced our productivity and may negatively impact our profitability during 2008 and beyond. Accordingly, we are seeking pricing concessions from our customers to mitigate the impact on our profitability.

We have experienced higher prices for new tractors over the past few years, partially as a result of government regulations applicable to newly manufactured tractors and diesel engines, in addition to higher commodity prices and better pricing power among equipment manufacturers. More restrictive EPA emissions standards for 2007 required vendors to introduce new engines. Additional EPA-mandated emission standards will become effective for newly manufactured trucks beginning in January 2010. Our business could be harmed if we are unable to continue to obtain an adequate supply of new tractors and trailers. We expect to continue to pay increased prices for equipment. At December 31, 2007, only 2% of our tractor fleet was comprised of tractors with pre-2007 engines that meet EPA-mandated clean air standards. By year-end 2008, approximately one-third of our fleet will have the new engines. We are also subject to regulation by various state regulatory agencies with respect to certain aspects of our operations. State regulations generally involve safety and the weight and dimensions of equipment.

SEASONALITY

Our temperature-controlled truckload operations are somewhat affected by seasonal changes. The growing seasons for fruits and vegetables in Florida, California and Texas typically create increased demand for trailers equipped to transport cargo requiring refrigeration. Our LTL operations are also impacted by the seasonality of certain commodities. LTL shipment volume during the winter months is normally lower than other months. Shipping volumes of LTL freight are usually highest during July through October. LTL volumes also tend to increase in the weeks preceding holidays such as Thanksgiving, Christmas and Easter when significant volumes of food and candy are shipped. Severe winter driving conditions can be hazardous and impair all of our trucking operations from time to time.

EMPLOYEES

The number of our employees, none of whom are subject to collective bargaining arrangements, as of December 31, 2007 and 2006 was as follows:

| | | 2007 | | 2006 | |

| Drivers and trainees | | | 1,577 | | 1,694 | |

| Non-driver personnel | | | | | | |

| Full time | | | 815 | | 922 | |

| Part time | | | 48 | | 58 | |

| Total motor carrier | | | 2,440 | | 2,674 | |

| Logistics and brokerage | | | 37 | | 17 | |

| | | | 2,477 | | 2,691 | |

OUTLOOK

This report contains information and forward-looking statements that are based on management's current beliefs and expectations and assumptions we made based upon information currently available. Forward-looking statements include statements relating to our plans, strategies, objectives, expectations, intentions and adequacy of resources and may be identified by words such as "will", "could", "should", "believe", "expect", "intend", "plan", "schedule", "estimate", "project" and similar expressions. These statements are based on our current expectations and are subject to uncertainty and change.

Although we believe the expectations reflected in such forward-looking statements are reasonable, actual results could differ materially from the expectations reflected in such forward-looking statements. Should one or more of the risks or uncertainties underlying such expectations not materialize, or should underlying assumptions prove incorrect, actual results may vary materially from those we expect.

Factors that are not within our control that could cause actual results to differ materially from those in such forward-looking statements include demand for our services and products, and our ability to meet that demand, which may be affected by, among other things, competition, weather conditions and the general economy, the availability and cost of labor and owner-operators, our ability to negotiate favorably with lenders and lessors, the effects of terrorism and war, the availability and cost of equipment, fuel and supplies, the market for previously-owned equipment, the impact of changes in the tax and regulatory environment in which we operate, operational risks and insurance, risks associated with the technologies and systems we use and the other risks and uncertainties described in Item 1A, Risk Factors of this report and risks and uncertainties described elsewhere in our filings with the Securities and Exchange Commission (“SEC”).

INTERNET WEB SITE

We maintain a web site, www.ffex.net, on the Internet where additional information about our company is available. Our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, press releases, earnings releases and other reports filed with and furnished to the SEC, pursuant to Section 13 or 15(d) of the Exchange Act are available, free of charge, on our web site as soon as practical after they are filed.

We have adopted a Code of Business Conduct and Ethics for our Board of Directors, our Chief Executive Officer, principal financial and accounting officers and other persons responsible for financial management and our employees generally. We also have charters for the Audit Committee, Compensation Committee, and Nominating Committee of our Board of Directors. Copies of the foregoing documents may be obtained on our website as noted in the above paragraph, and such information is available in print to any shareholder who requests it.

SEC FILINGS

The annual, quarterly, special and other reports we file with and furnish to the SEC are available at the SEC's Public Reference Room, located at 100 F Street, NE, Room 1580, Washington, D.C. 20549. Information may be obtained on the operation of the Public Reference Room by calling the SEC at 1-800-732-0330. The SEC also maintains a web site at www.sec.gov. The SEC site also contains information we file with and furnish to the agency.

ITEM 1A. Risk Factors.

There are numerous factors that affect our business and our operating results, many of which are beyond our control. The following is a description of significant factors that might cause our future operating results to differ materially from those currently expected. The risks described below are not the only risks facing us. Additional risks and uncertainties not specified herein, not currently known to us or currently deemed to be immaterial also may materially adversely affect our business, financial condition and/or operating results.

We are subject to general economic factors and business risks that are beyond our control, any of which could significantly reduce our operating margins and income. Recessionary economic cycles, changes in customers' business activity and outlook and excess tractor or trailer capacity in comparison with shipping demands could impact our operations. Economic conditions that decrease shipping demand or increase the supply of tractors and trailers generally available in the transportation sector of the economy can exert downward pressure on our equipment utilization, thereby decreasing asset productivity. Economic conditions also may harm our customers and their ability to pay for our services. Customers encountering adverse economic conditions represent a greater potential for loss, and we may be required to increase our allowance for uncollectible accounts.

We are also subject to increases in costs that are outside of our control that could materially reduce our profitability if we are unable to increase our rates sufficiently. Such cost increases include, but are not limited to, declines in the resale value of used equipment, increases in interest rates, fuel prices, taxes, tolls, license and registration fees, insurance, revenue equipment, and wages and health care for our employees.

In addition, we cannot predict the effects on the economy or consumer confidence of actual or threatened armed conflicts or terrorist attacks, efforts to combat terrorism, military action against a foreign state or group located in a foreign state, or heightened security requirements. Enhanced security measures could impair our operating efficiency and productivity and result in higher operating costs.

Future insurance and claims expense could reduce our earnings. Our future insurance and claims expense might exceed historical levels, which could reduce our earnings. We self-insure significant portions of our claims exposure resulting from work-related injuries, auto liability, general liability, cargo and property damage claims, as well as employees' health insurance. We reserve currently for anticipated losses and expenses. We periodically evaluate and adjust our claims reserves to reflect our experience. However, ultimate results usually differ from our estimates.

We maintain insurance above the amounts for which we self-insure. Although we believe the aggregate insurance limits should be sufficient to cover reasonably expected claims, it is possible that one or more claims could exceed our aggregate coverage limits. Insurance carriers have raised premiums for many businesses, including trucking companies. As a result, our insurance and claims expense could increase, or we could raise our self-insured retention when our policies are renewed. If these expenses increase, if we experience a claim in excess of our coverage limits, or if we experience a claim for which coverage is not provided, results of our operations and financial condition could be materially and adversely affected.

Higher fuel prices could reduce our income. We are subject to risk with respect to purchases of fuel for use in our tractors and refrigerated trailers. Fuel prices are influenced by many factors that are not within our control. Because our operations are dependent upon diesel fuel, significant increases in diesel fuel costs could materially and adversely affect our results of operations and financial condition unless we are able to pass increased costs on to customers through rate increases or fuel surcharges. Historically, we have sought to recover increases in fuel prices from customers through fuel surcharges. Fuel surcharges that can be collected have not always fully offset the increase in the cost of diesel fuel in the past and there can be no assurance that fuel surcharges that can be collected will offset the increase in the cost of diesel fuel in the future.

We will have significant ongoing capital requirements which could negatively impact our growth and profitability. The trucking industry is capital intensive, and replacing older equipment requires significant investment. If we elect to expand our fleet in future periods, our capital needs would increase. We expect to pay for our capital expenditures with cash flows from operations, leasing and borrowings under our revolving credit facility. If we are unable to generate sufficient cash from operations and obtain financing on favorable terms, we may need to limit our growth, enter into less favorable financing arrangements or operate our revenue equipment for longer periods, any of which could impact our profitability.

We rely on our key management and other employees and depend on recruitment and retention of qualified personnel; difficulty in attracting or retaining qualified employee-drivers and independent contractors who provide tractors for use in our business could impede our growth and profitability. A small number of key executives manage our business. Their departure could have a material adverse effect on our operations. In addition, our performance is primarily dependent upon our ability to attract and retain qualified drivers. Our independent contractors are responsible for paying for their own equipment, labor, fuel, and other operating costs. Significant increases in these costs could cause them to seek higher compensation from us or other opportunities. Competition for employee-drivers continues to increase. If a shortage of employee-drivers occurs, or if we were unable to continue to sufficiently contract with independent contractors, we could be forced to limit our growth or experience an increase in the number of our tractors without drivers, which would lower our profitability. During April 2006, we increased our employee-driver pay scale by about 6%. We could be required to further adjust our driver compensation, which could impact our profitability if not offset by a corresponding increase in the rates we charge for our services. Reductions in service by the railroads or increases in railroad rates can impact our intermodal operations, which could reduce our income. Our intermodal operations are dependent on railroads, and our dependence on railroads may increase if we expand our intermodal services. In most markets, rail service is limited to a few railroads or even a single railroad. Any reduction in service by the railroads may increase the cost of the rail-based services we provide and reduce the reliability, timeliness and overall attractiveness of our rail-based services. Railroads are relatively free to adjust their rates as market conditions change. That could result in higher costs to our customers and impact our ability to offer intermodal services. There is no assurance that we will be able to negotiate replacement of or additional contracts with railroads, which could limit our ability to provide this service.

Interruptions in the operation of our computer and communications systems could reduce our income. We depend on the efficient and uninterrupted operation of our computer and communications systems and infrastructure. Our operations and those of our technology and communications service providers are vulnerable to interruption by fire, earthquake, power loss, telecommunications failure, terrorist attacks, Internet failures, computer viruses and other events beyond our control. In the event of a system failure, our business could experience significant disruption. To mitigate this risk, we have established an off-site facility where our data and processing functions are replicated.

Changes in the availability of or the demand for new and used trucks could reduce our growth and negatively impact our income. More restrictive federal emissions standards for 2007 model year trucks require new technology diesel engines. As a result, we expect to continue to pay increased prices for equipment and incur additional expenses and related financing costs for the foreseeable future. The new engines are also expected to reduce equipment productivity, increase fuel consumption and be more expensive to maintain.

We have a conditional commitment from our principal tractor vendor regarding the amount that we will be paid on the disposal of most of our tractors. We could incur a financial loss upon disposition of our equipment if the vendor cannot meet its obligations under these agreements.

We are subject to various environmental and zoning laws and regulations, and costs of compliance with and liabilities for violations of existing or future regulations could significantly increase our costs of doing business. We operate in industrial areas, where truck terminals and other industrial facilities are located, and where groundwater or other forms of environmental contamination may have occurred. Our operations involve the risks of fuel spillage, environmental damage and hazardous waste disposal, rezoning and eminent domain, among others. If we are involved in a spill or other accident involving hazardous substances, if one of our properties is rezoned, if a governmental agency should assert a right involving eminent domain or if we are found to be in violation of applicable laws or regulations, such an event could significantly increase our cost of doing business. Additionally, under specific environmental laws, we could be held responsible for all of the costs relating to any contamination at our past or present terminals and at third-party waste disposal sites.

We operate in an industry subject to extensive government regulations, and costs of compliance with and liability for violation of existing or future regulations could significantly increase our costs of doing business. Our operations are overseen by various agencies. Our drivers must comply with federal safety and fitness regulations, including those relating to drug and alcohol testing and hours of service. Such matters as weight and equipment dimensions are also the subject of federal and state regulations. We are also governed by federal and state regulations regarding fuel emissions, and other matters affecting safety or operations. Future laws and regulations may be more stringent and may influence the demand for transportation services, may require us to make changes in our operating practices, or may require us to incur significant additional costs. Higher costs incurred by us or by our suppliers who pass the costs onto us through higher prices could adversely affect our results of operations.

We may not be able to improve our operating efficiency rapidly enough to meet market conditions. Because the markets in which we operate are highly competitive, we must continue to improve our operating efficiency in order to maintain or improve our profitability. Although we have been able to improve efficiency and reduce costs in the past, there is no assurance that we will continue to do so in the future. In addition, the need to reduce ongoing operating costs may result in significant up-front costs to reduce workforce, close or consolidate facilities, or upgrade equipment and technology. An extended disruption of vital infrastructure could negatively impact our business, results of operations and financial condition. Our operations depend upon, among other things, our infrastructure, including equipment and facilities. Extended disruption of vital infrastructure by fire, power loss, natural disaster, telecommunications failure, computer hacking or viruses, technology failure, terrorist activity or the domestic and foreign response to such activity, or other events outside of our control could have a materially adverse impact on the transportation services industry as a whole and on our business, results of operations, cash flows, and financial condition in particular. Our business recovery plan may not work as intended or may not prevent significant interruptions of our operations.

Our operations could be adversely affected by a work stoppage at locations of our customers. Although none of our employees are covered by a collective bargaining agreement, a strike or other work stoppage at a customer could negatively affect our revenue and earnings and could cause us to incur unexpected costs to redeploy or deactivate assets and personnel.

We operate in a competitive and somewhat fragmented industry. Numerous factors could negatively impair our growth and profitability and impair our ability to compete with other carriers and private fleets.

Some of these factors include: | - | We compete with many other transportation carriers of varying sizes and with less-than-truckload carriers, some of which have more equipment and greater capital resources than we do. |

| - | Some of our competitors periodically reduce their freight rates to gain business, especially during times of reduced growth rates in the economy, which may limit our ability to maintain or increase freight rates or maintain our profit margins. |

| - | Many customers reduce the number of carriers they use by selecting so-called “core carriers” as approved transportation service providers, and in some instances we may not be selected. |

| - | Many customers periodically accept bids from multiple carriers for their shipping needs, and this process may depress freight rates or result in the loss of some business to competitors. |

| - | Certain of our customers that operate private fleets to transport their own freight could decide to expand their operations. |

| - | The trend toward consolidation in the trucking industry may create other large carriers with greater financial resources and other competitive advantages relating to their size. |

| - | Advances in technology require increased investments to remain competitive, and our customers may not be willing to accept higher freight rates to cover the cost of these investments. |

We are subject to anticipated future increases in the statutory federal tax rate. An increase in the statutory rate would increase our tax expense. In addition, our net deferred tax liability is stated net of offsetting deferred tax assets. The assets consist of anticipated future tax deductions for items such as personal and work-related injuries and bad debt expenses which have been reflected on our financial statements but which are not yet tax deductible. At current federal tax rates, we will need to generate sufficient future taxable income in order to fully realize our deferred tax assets. Due to probable tax rate increases in the future, we would be required to adjust our deferred tax liabilities at that time to reflect higher federal tax rates.

Other Risks Related to Our Business. Other risk factors include, but are not limited to, changes in the mix of our services, changes in legislation applicable to us, changes in market demand or our business strategies, potential litigation and claims arising in the normal course of business, credit risk of customers and other risk factors.

None

The following tables set forth certain information regarding our revenue equipment at December 31, 2007 and 2006:

| | | Age in Years | | | | |

| Tractors | | Less than 1 | | 1 through 3 | | More than 3 | | Total |

| | | 2007 | | 2006 | | 2007 | | 2006 | | 2007 | | 2006 | | 2007 | | 2006 |

| Company-owned and leased | | | 204 | | 490 | | | 918 | | 891 | | | 379 | | 207 | | | 1,501 | | 1,588 |

| Owner-operator provided | | | 161 | | 109 | | | 311 | | 37 | | | 102 | | 453 | | | 574 | | 599 |

| | | | 365 | | 599 | | | 1,229 | | 928 | | | 481 | | 660 | | | 2,075 | | 2,187 |

| | | Age in Years | | | | |

| Trailers | | Less than 1 | | 1 through 5 | | More than 5 | | Total |

| | | 2007 | | 2006 | | 2007 | | 2006 | | 2007 | | 2006 | | 2007 | | 2006 |

| Company-owned and leased | | | 456 | | 493 | | | 2,345 | | 2,521 | | | 1,241 | | 898 | | | 4,042 | | 3,912 |

| Owner-operator provided | | | -- | | -- | | | -- | | 3 | | | 4 | | 4 | | | 4 | | 7 |

| | | | 456 | | 493 | | | 2,345 | | 2,524 | | | 1,245 | | 902 | | | 4,046 | | 3,919 |

Approximately three-fourths of our trailers are insulated and equipped with refrigeration units capable of providing the temperature control necessary to handle perishable freight. Trailers that are used primarily in LTL operations are equipped with movable partitions permitting the transportation of goods requiring maintenance of different temperatures. We also operate a fleet of non-refrigerated trailers in our "dry freight" truckload operation. Company-operated trailers are primarily 102 inches wide. Truckload trailers used in dry freight linehaul operations are 53 feet long. Linehaul temperature-controlled operations are conducted with both 48- and 53-foot refrigerated trailers.

Our general policy is to replace our company-operated, heavy-duty tractors after 42 months, subject to cumulative mileage and condition. Our refrigerated and dry trailers are usually retired after seven or ten years of service, respectively. Occasionally, we retain older equipment for use in local delivery operations.

At December 31, 2007, in addition to a number of smaller rented recruiting and sales offices around the United States, we maintained terminal or office facilities of 10,000 square feet or more in or near the cities listed below. Lease terms range from one month to twelve years. We expect that our present facilities are sufficient to support our operations. We also own three properties in Texas that we lease to W&B Service Company, L. P. (“W&B”), an entity in which we hold a minority ownership interest.

| | | Approximate Square Footage | | Acreage | | (O)wned or (L)eased | |

| Dallas, TX | | | | | | | | | |

| Maintenance, terminal, and freight handling | | | 100,000 | | 80.0 | | | O | |

| Corporate office | | | 34,000 | | 1.7 | | | O | |

| Ft. Worth, TX | | | 34,000 | | 7.0 | | | O | |

| Chicago, IL | | | 37,000 | | 5.0 | | | O | |

| Lakeland, FL | | | 26,000 | | 15.0 | | | O | |

| Newark, NJ | | | 17,000 | | 5.0 | | | O | |

| Atlanta, GA | | | 50,000 | | 13.0 | | | O | |

| Los Angeles, CA | | | 40,000 | | 6.0 | | | L | |

| Salt Lake City, UT | | | 12,500 | | * | | | L | |

| Miami, FL | | | 17,500 | | * | | | L | |

| Memphis, TN | | | 11,000 | | * | | | L | |

*Facilities are part of an industrial park in which we share acreage with other tenants.

Most of our terminals serve as satellite offices for our brokerage operation, FFE Logistics, Inc. (“FFEL”). In other markets, FFEL also leases small sales offices. FFEL has also expanded from one office at the end of 2006 to twelve as of December 31, 2007.

During 2007, we learned that the (owned) terminal near Newark and the (leased) facility near Los Angeles have been targeted for eminent domain proceedings by the cities in which they are located. We are currently working with the appropriate authorities to accommodate our need to sell the New Jersey property and vacate the premises in an orderly fashion. We have owned the New Jersey property for about 20 years, and it is not subject to any liens. When we sell the property to a user that meets the standards of the city, we project that we will realize a substantial gain and receive cash for the full sales price. We are currently searching for a new location in the northern and central sections of New Jersey. We currently are planning to lease, rather than own, the new facility. This matter should be concluded during 2008.

With regard to the leased southern California location, the city in which it is located has informed the property owner and us that it plans to construct a water tower and pumping station on the property. Our lease expires late in 2011, and we do not expect the city to take action until at least that time. We are currently looking for a replacement facility, which we intend to lease on a long-term basis.

ITEM 3. Legal Proceedings.

We are party to routine litigation incidental to our business, primarily involving claims for personal injury, property damage, work-related injuries of employees and cargo losses incurred in the ordinary and routine highway transportation of freight. As of December 31, 2007, the aggregate amount of reserves for such claims on our consolidated balance sheet was nearly $21.7 million. We also primarily insure for employee health care claims. We maintain excess insurance programs and accrue for expected losses in amounts designed to cover liability resulting from such claims.

On January 4, 2006, Owner Operator Independent Drivers Association, Inc., Warrior Transportation, Roy Clark, and Gregory Colvin d/b/a Wolverine Trucking, Inc. filed a lawsuit in the U.S. District Court for the Northern District of Texas, Dallas Division, on behalf of themselves and all others similarly situated against our principal operating subsidiary FFE Transportation Services, Inc. (“FFE”). Plaintiffs alleged that FFE’s Independent Contractor Agreements (“ICA”) violated the federal Truth in Leasing Regulations that govern the content of agreements, such as the ICAs, between independent drivers and trucking companies. Plaintiffs seek certification of a class consisting of every contractor who signed an ICA with FFE since January 4, 2002. According to Plaintiffs, FFE violated the regulations by deducting amounts from the proposed class members’ escrow accounts to pay obligations that were not specified with particularity. Plaintiffs further alleged that FFE improperly deducted certain fees and charges from proposed class members' compensation at the time of payment. Plaintiffs also allege improper forced purchases in violation of the regulations. Plaintiffs seek damages, interest, costs and attorneys’ fees, as well as declaratory and injunctive relief.

On June 15, 2007, the Court denied Plaintiffs’ motion for class certification, leaving only the Plaintiffs’ individual claims for adjudication. The trial of those claims has been set for July 28, 2008. Plaintiffs have indicated an interest in settling the remaining claims. If the matter is not settled, FFE intends to vigorously contest Plaintiffs' claims.

On January 8, 2008, a shareholders’ derivative action was filed in the District Court of Dallas County, 192nd District, entitled James L. and Eleanor A. Gayner, Individually and as Trustees of The James L. & Eleanor 81 UAD 02/04/1981 Trust, Derivatively On Behalf of Frozen Food Express Industries, Inc. v. Stoney M. Stubbs, Jr., et al. This action alleges that certain of our current and former officers and directors breached their respective fiduciary duties in connection with our equipment lease arrangements with certain related-parties, which were terminated in September 2006. The shareholders seek, putatively on our behalf, an order that the lease arrangements were null and void from their origination, an unspecified amount of damages, the imposition of a constructive trust on any benefits received by the defendants as a result of their alleged wrongful conduct, and recovery of attorneys’ fees and costs. A special litigation committee (“SLC”) consisting solely of independent directors has been created to investigate the claims in the derivative action. As permitted by Texas law, we have requested the derivative action be stayed while the SLC conducts its investigation, which request has been opposed by the plaintiffs. The Court has not ruled on the Company’s request to stay the action.

No matters were submitted to a vote of our shareholders during the fourth quarter of 2007.

ITEM 5. Market for Registrant's Common Equity, Related Shareholder Matters and Issuer Purchases of Equity Securities.

Market for Registrant's Common Equity and Related Shareholder Matters.

During each of the five quarters ended December 31, 2007, we paid a cash dividend of $0.03 per share. Our Board of Directors intends to continue to declare such dividends on a quarterly basis in the future, subject to provisions in our credit agreement that may restrict our ability to do so without first obtaining consent from our lenders. We have not set any pre-established guidelines as to the per-share or aggregate quarterly amount of such dividends relative to net income or any other measurement.

As of March 7, 2008, we had approximately 3,000 beneficial shareholders, including participants in our retirement plans. Our $1.50 par value common stock trades on the Global Select Market tier of the Nasdaq Stock Market under the symbol FFEX. Information regarding our common stock is as follows:

| 2007 | | Year | | | First Quarter | | | Second Quarter | | | Third Quarter | | | Fourth Quarter | |

| Common stock sales price per share | | | | | | | | | | | | | | | |

| High | | $ | 10.91 | | | $ | 8.83 | | | $ | 10.91 | | | $ | 10.82 | | | $ | 7.05 | |

| Low | | | 5.45 | | | | 7.41 | | | | 7.74 | | | | 6.41 | | | | 5.45 | |

| Cash dividends paid per share | | $ | .12 | | | $ | .03 | | | $ | .03 | | | $ | .03 | | | $ | .03 | |

Common stock trading volume (a) | | | 15,759 | | | | 4,413 | | | | 4,501 | | | | 4,116 | | | | 2,729 | |

| 2006 | | Year | | | First Quarter | | | Second Quarter | | | Third Quarter | | | Fourth Quarter | |

| Common stock sales price per share | | | | | | | | | | | | | | | |

| High | | $ | 14.28 | | | $ | 14.28 | | | $ | 11.91 | | | $ | 11.25 | | | $ | 8.88 | |

| Low | | | 6.94 | | | | 9.90 | | | | 9.31 | | | | 6.94 | | | | 7.14 | |

| Cash dividends paid per share | | $ | .03 | | | $ | -- | | | $ | -- | | | $ | -- | | | $ | .03 | |

Common stock trading volume (a) | | | 29,994 | | | | 9,101 | | | | 9,763 | | | | 8,167 | | | | 2,963 | |

Issuer Purchases of Equity Securities

| Period | Total Number of Shares Purchased (a) | | Average Price Paid per Share (b) | | Total Number of Shares Purchased as Part of Publicly Announced Plans or Programs (c) | | Maximum Number (or Approximate Dollar Value) of Shares (or Units) that May Yet Be Purchased Under the Plans or Programs (1) (d) | |

| October 1, 2007 to October 31, 2007 | -- | | $ | -- | | -- | | | 357,900 | |

November 1, 2007 to November 30, 2007(2) | 247,233 | | | 5.76 | | 246,400 | | | 1,111,500 | |

December 1, 2007 to December 31, 2007(2) | 7,500 | | $ | 5.81 | | -- | | | 1,111,500 | |

| | 254,733 | | $ | 5.76 | | 246,400 | | | | |

| | (1) | On November 9, 2007, our Board of Directors renewed our authorization to purchase up to 1,357,900 shares of our common stock. The authorization allows purchases from time to time on the open market or through private transactions at such times as management deems appropriate. The authorization does not specify an expiration date. Purchases may be increased, decreased or discontinued by our Board of Directors at any time without prior notice. |

| | (2) | During the fourth quarter of 2007, current and former employees exchanged 8,333 shares they owned for more than one year as consideration for the exercise of stock options, as permitted by our share option plans. Such transactions are not deemed as having been purchased as part of our publicly announced plans or programs. |

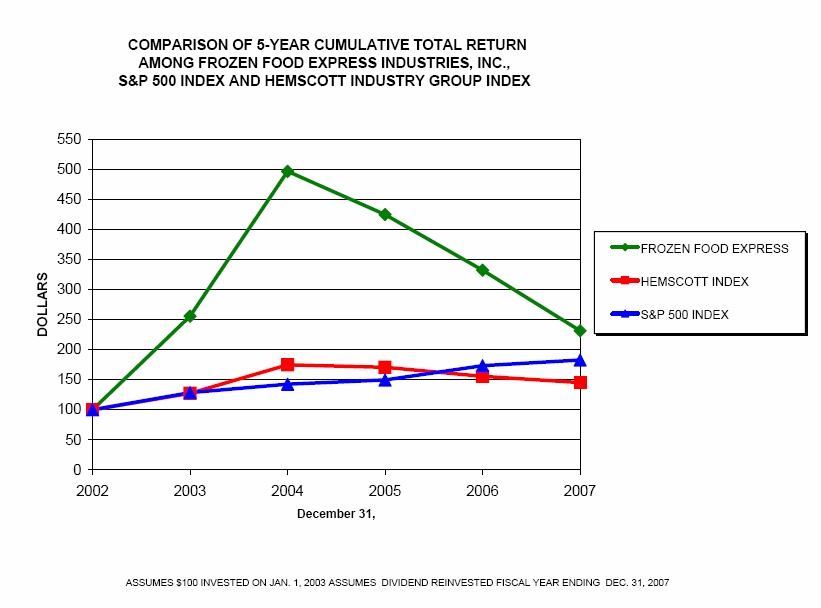

5-YEAR SHAREHOLDER RETURN COMPARISON

The following graph compares the cumulative total shareholder return on our common stock for the last five years to the S&P 500 Index and the Hemscott Industry Group Index #774- Trucking Companies (assuming the investment of $100 in our common stock, the S&P 500 Index and the Hemscott Industry Index on December 31, 2002 and reinvestment of all dividends).

| | December 31, | |

| | 2002 | | 2003 | | 2004 | | 2005 | | 2006 | | 2007 | |

| FROZEN FOOD EXPRESS INDUSTRIES, INC. | | $ | 100 | | | $ | 256 | | | $ | 497 | | | $ | 425 | | | $ | 332 | | | $ | 232 | |

| HEMSCOTT GROUP INDEX #774-TRUCKING COMPANIES | | | 100 | | | | 127 | | | | 175 | | | | 171 | | | | 156 | | | | 145 | |

| S&P 500 INDEX | �� | | 100 | | | | 129 | | | | 143 | | | | 150 | | | | 173 | | | | 183 | |

ITEM 6. Selected Financial Data.

The following unaudited data for each of the years in the five-year period ended December 31, 2007 should be read in conjunction with our Consolidated Financial Statements and Notes thereto included at Item 8 of this report and "Management's Discussion and Analysis of Financial Condition and Results of Operations" contained in Item 7. The historical information is not necessarily indicative of future results or performance:

| Summary of Operations | | 2007 | | 2006 | | 2005 | | 2004 | | 2003 | |

Revenue(a) | | | 452.2 | | 483.7 | | | 514.0 | | 464.7 | | | 405.9 | |

Net (loss) income (a) | | | (7.7 | ) | 11.2 | | | 20.4 | | 10.8 | | | 4.3 | |

| Net (loss) income per common share, diluted | | | (.45 | ) | .61 | | | 1.09 | | .59 | | | .24 | |

Operating expenses (a) | | | 462.7 | | 472.2 | | | 484.4 | | 448.3 | | | 394.0 | |

| Financial Data | | | | | | | | | | | | | | |

Total assets (a) | | | 173.7 | | 191.8 | | | 201.0 | | 174.5 | | | 155.2 | |

Working capital (a) | | | 32.3 | | 41.4 | | | 33.0 | | 19.2 | | | 37.1 | |

Current ratio (b) | | | 1.7 | | 1.9 | | | 1.5 | | 1.3 | | | 1.9 | |

Cash provided by operating activities (a) | | | 12.5 | | 21.0 | | | 30.0 | | 41.6 | | | 14.3 | |

Long-term debt (a) | | | -- | | 4.9 | | | -- | | 2.0 | | | 14.0 | |

Shareholders' equity (a) | | | 107.3 | | 122.5 | | | 119.1 | | 97.0 | | | 84.1 | |

Debt-to-equity ratio (c) | | | -- | | -- | | | -- | | -- | | | .2 | |

| Common Stock | | | | | | | | | | | | | | |

Weighted average diluted shares (a) | | | 17.2 | | 18.5 | | | 18.7 | | 18.1 | | | 17.8 | |

Book value per share (d) | | | 6.41 | | 6.99 | | | 6.64 | | 5.50 | | | 4.88 | |

| Market value per share | | | | | | | | | | | | | | |

| High | | | 10.91 | | 14.28 | | | 13.50 | | 13.86 | | | 8.85 | |

| Low | | | 5.45 | | 6.94 | | | 9.08 | | 5.64 | | | 2.18 | |

| Revenue From | | | | | | | | | | | | | | |

Truckload linehaul services (a) | | | 212.4 | | 237.5 | | | 263.2 | | 258.7 | | | 239.8 | |

Dedicated fleets (a) | | | 17.9 | | 21.1 | | | 31.5 | | 20.3 | | | 14.5 | |

Less-than-truckload linehaul services (a) | | | 127.4 | | 129.8 | | | 131.2 | | 123.2 | | | 115.5 | |

Fuel surcharges (a) | | | 73.4 | | 75.1 | | | 63.5 | | 31.7 | | | 15.7 | |

Brokerage (a) | | | 15.6 | | 12.5 | | | 15.6 | | 24.9 | | | 15.0 | |

Equipment rental (a) | | | 5.5 | | 7.7 | | | 9.0 | | 5.9 | | | 5.4 | |

| Equipment in Service at Year-end | | | | | | | | | | | | | | |

| Tractors | | | | | | | | | | | | | | |

| Company operated | | | 1,501 | | 1,588 | | | 1,607 | | 1,573 | | | 1,534 | |

| Provided by owner-operators | | | 574 | | 599 | | | 659 | | 716 | | | 757 | |

| Total tractors | | | 2,075 | | 2,187 | | | 2,266 | | 2,289 | | | 2,291 | |

| Trailers | | | 4,046 | | 3,919 | | | 4,293 | | 4,147 | | | 3,802 | |

| Computational notes: |

| (a) | In millions. |

| (b) | Current assets divided by current liabilities. |

| (c) | Debt divided by shareholders’ equity. |

| (d) | Shareholders’ equity divided by the number of total shares issued less the number of treasury shares (excluding treasury shares held in the rabbi trust), all as of year-end. |

ITEM 7. Management's Discussion and Analysis of Financial Condition and Results of Operations.

OVERVIEW

We are principally a motor-carrier, also commonly referred to as a trucking company. We offer various transportation services to customers in the United States, Canada and Mexico. Our services primarily involve the over-the-road movement of freight. In the United States, we sometimes arrange for the use of railroads to transport our loaded trailers between major cities. Most of our revenue is from service which is order-based, meaning that we separately bill our customers for each shipment. A minority of our revenue is from services which are asset-based, meaning that we bill our customer for the use of a truck and driver or the use of a trailer for a period of time, without regard to the number of shipments hauled. We also refer to such truck and driver asset-based service as "dedicated fleets", because the trucks and drivers involved are dedicated for use by a specific customer on a full-time basis.

Order-based services are either truckload or LTL. Our trailers are designed to carry up to 40,000 pounds of freight. Shipments weighing 20,000 pounds or more are truckload, while smaller shipments are classified as LTL.

Customers let us know that they have shipments requiring transportation, and inform us as to any special requirements, such as an identification of the type of product to be shipped, the origin and destination of the load and the expected time by which delivery must occur. We inform our customers of our availability to haul the freight and of the price we will charge. If these fit with the needs of the customer, we pick up the freight.

Shipments have three stages: pick-up, linehaul and delivery. The linehaul stage is over-the-road and involves longer distances. Most of our truckload shipments will have all of these stages performed by the same truck and trailer.

LTL shipments typically involve different trucks and trailers for each of the three stages, including the linehaul stage, as the freight moves within our network of terminals. For example, an LTL truck bound from Los Angeles to Dallas may carry shipments destined for Dallas, Chicago and Atlanta. Once the truck arrives in Dallas, the freight will be sorted and sent out from Dallas on different trucks to Chicago and Atlanta with other LTL shipments that originated in Dallas or arrived there on trucks from other areas of the country. The freight destined for Dallas will be delivered by the city fleet. A linehaul load of LTL typically weighs 25,000 to 35,000 pounds and is comprised of between 5 and 30 individual shipments.

We are the only company that provides nation-wide, temperature-controlled LTL service. Other such LTL providers tend to operate on a regional basis. Our LTL trucks operate according to published schedules. That enables our customers to know when we will arrive to pick up or deliver a shipment. We rarely haul “dry” LTL freight.

We operate under four primary brand names, FFE Transportation Services ("FFE"), Lisa Motor Lines ("LML"), AEL and FFE Logistics, Inc. (“FFEL”). FFE and LML specialize in products that require temperature control. All of our LTL service is provided by FFE.

Most shipments require the maintenance of a temperature between minus 10 degrees and plus 60 degrees Fahrenheit. Examples include perishable food, beverages, candy, pharmaceuticals, photographic supplies and electronics. Other products require maintenance of a warm temperature in the colder months to prevent freezing while in transit, such as nursery stock and liquid products. FFE conducts all of our LTL business, and also has significant order-based and asset-based truckload operations. LML has specialized in order-based truckload operations, but in the second half of 2007 has focused more on asset-based dedicated fleet operations. AEL serves the market for order-based and asset-based truckload activities that do not require temperature control. FFE Logistics is our brokerage service, negotiating third-party truckload transportation of both dry and refrigerated freight.

The assets we must have for temperature-controlled service are costly to acquire and maintain. The rates we charge for our temperature-controlled services are usually higher than other companies who offer no temperature-controlled services. Many products that require protection from the heat during the warmer months of the year do not require protection during the colder months. Therefore, during the warmer months, demand for our temperature-controlled truckload and LTL services expands. Demand for our LTL service also swells in the weeks before a holiday, when retailers are stocking extra food and candy to meet the seasonal demands of their customers.

There are several companies that provide national temperature-controlled truckload services. We know of no other company providing nationwide LTL temperature-controlled service. The vast majority of trucking companies that are nationwide in scope, such as our AEL brand, offer only truckload service with no temperature control. Therefore, the markets that are served by AEL tend to be very price-competitive and generally lack the level of seasonality present in our FFE and LML operations. Because consumer demand for products requiring temperature control is often less sensitive to economic cycles, linehaul revenue from FFE and LML tends to be less volatile during such cycles.

The trucking business is highly competitive. During 2006, the last year for which data is available, there were several thousand companies operating in all sectors of the trucking business in the United States. Among those, the top five companies offering primarily temperature-controlled services collectively generated 2006 revenue of $2.6 billion. The next 20 such companies collectively generated revenues of $2.2 billion. In 2006, we ranked third in terms of revenue generated among all temperature-controlled motor carriers.

We have nearly 10,000 active customers for our trucking business. We generally collect payment for our services between 30 and 50 days after our service is provided.

Trucking companies of our size face challenges to be successful. Costs for labor, maintenance, fuel and insurance typically change every year. Fuel prices can increase or decrease quite rapidly. Due to the high level of competitiveness, it is often difficult to pass these rising costs on to our customers. Over the past few years, many trucking companies have ceased operations, resulting in a reduced number of alternatives and increasing the awareness among customers that price increases for trucking services are likely.

The capacity of the trucking industry to haul freight increased during 2006. Over the same time, customer demand for such services diminished. One result was increased industry-wide downward pressure on the rates truckers can charge for their services. Although there can be no assurance this supply/demand imbalance will be corrected in the near-term, such situations have occurred periodically in the past, and are likely to recur in the future.

During the latter part of 2005, many of our resources were engaged in providing relief to the regions affected by Hurricanes Katrina and Rita. We provided dedicated fleet services in these hurricane relief efforts, which contributed revenue of $5.7 million during 2005 and $500 thousand during 2006, respectively. We also provided refrigerated trailers, which were rented on a per-day basis for storage and transportation of perishable items. Such hurricane-related trailer rentals generated $3.2 million of revenue during 2005 and $2.2 million in 2006.

During 2007, the commodities we hauled most frequently included the following:

-Candy/confectionaries -Christmas trees -Cosmetics -Dairy products -Film -Food products (dry and frozen) -Fresh produce | -Frozen fruits and vegetables -Ice -Meat products (including poultry and fish) -Medical supplies -Paper products -Pharmaceuticals -Processed foods |

In last year’s annual report, we outlined a few areas that we expected to explore during 2007. Below is a comparison of what we said then and what the current status is:

| | Status |

- Expand our intermodal operation and focus on brokerage, dedicated and less capital intensive areas of our business. | -Intermodal revenue for 2007 was 78% above 2006, and 75% of 2007’s intermodal revenue was hauled during the last half of the year. |