Exhibit 13

FINANCIAL SECTION

ABOUT THESE FINANCIAL STATEMENTS

Keeping our investors well informed about GE is vitally important to us. In 2001, we committed to increasing our transparency, which led to the presentation of significantly more financial information and analysis in our annual report. We continue to be guided by that commitment. We believe the 2003 financial statements will provide you with even more insight about our company.

The pages that follow have been organized to walk you through our financial condition and results from top to bottom.

FINANCIAL TABLE OF CONTENTS

42 | Management's Discussion of Financial Responsibility | We begin withManagement's Discussion of Financial Responsibility. Here our Chief Executive and Financial Officers discuss our unyielding commitment to rigorous oversight, controllership and visibility to investors. |

|

43 | Independent Auditors' Report | Then we present ourIndependent Auditors' Report, submitted by KPMG LLP. Here our auditors express their independent opinion on our consolidated financial statements. |

|

44 44 44 49 55 | Management's Discussion and Analysis Operations Overview of Our Earnings Segment Operations International Operations | The next section isManagement's Discussion and Analysis. We begin the Operations section with an overview of our earnings from 2001 to 2003, which provides perspective on how the global economic environment has affected our businesses over the last three years. We then discuss various key operating results for GE industrial (GE) and financial services (GECS). Because of the fundamental differences in their businesses, reviewing certain information separately for GE and GECS offers a more meaningful analysis. This year's discussion of our segment results includes expanded quantitative and qualitative disclosure about the factors affecting segment revenues and profits, and the effects of recent acquisitions and significant transactions. Next is an overview of our operations from an international perspective. |

|

57 | Financial Resources and Liquidity | We then move to a discussion of ourFinancial Resources and Liquidity. Here we provide an overview of the major factors that affected our consolidated financial position. This section has been significantly expanded and reorganized to provide better insight into the liquidity and cash flow activities of GE and GECS. |

|

65 | Selected Financial Data | Selected Financial Data provides five years of financial information for GE and GECS. This table includes commonly used metrics that facilitate comparison with other companies. |

|

67 | Critical Accounting Estimates | Following that is our discussion ofCritical Accounting Estimates used by management in preparing our financial statements. We discuss what these estimates are, why they are important, how they are developed and what could cause them to change. |

|

70 | Audited Financial Statements | Finally, we present ourAudited Financial Statements, including consolidating data for GE and GECS, and related notes. |

|

114 | Glossary | For your convenience, we provide aGlossary of key terms used in our financial statements. We also continue to present our financial information electronically at www.ge.com/investor. This award-winning site is interactive and informative. |

41 GE 2003 ANNUAL REPORT

MANAGEMENT'S DISCUSSION OF FINANCIAL RESPONSIBILITY

High quality financial reporting is an excellent measure of a company and its management. We demonstrate our commitment to high quality reporting by adopting appropriate accounting policies, devoting our full, unyielding commitment to ensuring that those policies are applied properly and consistently, and presenting our results in a manner that is complete and clear. We welcome suggestions from those who use our reports.

Rigorous Management Oversight

Members of our corporate leadership team review each of our businesses constantly, on matters that range from overall strategy and financial performance to staffing and compliance. Our business leaders constantly monitor real-time financial and operating systems, enabling us to identify potential opportunities and concerns at an early stage, and positioning us to develop and execute rapid responses. Our Board of Directors oversees management's business conduct, and our Audit Committee, which consists entirely of independent directors, oversees our system of controls and procedures. We continually examine our governance practices in an effort to enhance investor trust and improve the board's overall effectiveness. Our Presiding Director, who conducts at least three meetings per year with non-employee directors, has helped us to set more focused and effective meeting agendas. We changed compensation policies for our executives, including modifying CEO compensation to award equity grants only if key performance metrics are met, thereby aligning leadership's interests with the long-term interests of GE investors.

Dedication to Controllership

We maintain a dynamic system of controls and procedures–including internal controls over financial reporting–designed to ensure reliable financial record-keeping, transparent financial reporting and disclosure, protection of physical and intellectual property, and efficient, effective use of resources. We recruit, develop and retain a world-class financial team, including 520 internal auditors who conduct thousands of financial, compliance and process improvement audits each year, in every geographic area, at every GE business. The Audit Committee oversees the scope and results of these reviews. Our global integrity policies–the "Spirit & Letter"–require compliance with law and policy, and pertain to such vital issues as upholding financial integrity and avoiding conflicts of interest. These integrity policies are available in 27 languages, and we have provided them to every one of GE's more than 300,000 global employees, holding each of these individuals–from our top management on down–personally accountable for compliance. Our integrity policies serve to reinforce key employee responsibilities around the world, and we inquire extensively about compliance. Our strong compliance culture reinforces these efforts by requiring employees to raise any compliance concerns and by prohibiting retribution for doing so. We hold our consultants, agents and independent contractors to the same integrity standards.

Visibility to Investors

We are keenly aware of the importance of full and open presentation of our financial position and operating results. To facilitate this, we maintain a Disclosure Committee, which includes senior executives with exceptional knowledge of our businesses and the related needs of our investors. We ask this committee to evaluate the fairness of our financial and non-financial disclosures, and to report their findings to us and to the Audit Committee. We further ensure strong disclosure by holding more than 250 analyst and investor meetings every year, and by communicating any material information covered in those meetings to the public. In testament to the effectiveness of our stringent disclosure policies, investors surveyed annually by Investor Relations magazine have given us 19 awards in the last eight years, including Best Overall Investor Relations Program by a mega-cap company for six of those years. We are in regular contact with representatives of the major rating agencies, and our debt continues to receive their highest ratings. We welcome the strong oversight of our financial reporting activities by our independent audit firm, KPMG LLP, who are engaged by and report directly to the Audit Committee. Their report for 2003 appears on page 43.

A Great Company

GE continues to earn the admiration of the business world. We were named "The World's Most Respected Company" for the sixth consecutive year in the Financial Times annual CEO survey, ranking first for governance and integrity.

Great companies are built on the foundation of reliable financial information and compliance with the law. For GE, the financial disclosures in this report are a vital part of that foundation. We present this information proudly, with the expectation that those who use it will understand our company, recognize our commitment to performance with integrity, and share our confidence in GE's future.

/s/ Jeffrey R. Immelt

Jeffrey R. ImmeltChairman of the Board and

Chief Executive Officer

/s/ Keith S. Sherin

Keith S. SherinSenior Vice President, Finance, and

Chief Financial Officer

February 6, 2004

42 GE 2003 ANNUAL REPORT

INDEPENDENT AUDITORS' REPORT

To Shareowners and Board of Directors of

General Electric Company

We have audited the accompanying statement of financial position of General Electric Company and consolidated affiliates ("GE") as of December 31, 2003 and 2002, and the related statements of earnings, changes in shareowners' equity and cash flows for each of the years in the three-year period ended December 31, 2003. These consolidated financial statements are the responsibility of GE management. Our responsibility is to express an opinion on these consolidated financial statements based on our audits.

We conducted our audits in accordance with auditing standards generally accepted in the United States of America. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the aforementioned financial statements appearing on pages 70, 72, 74, 48 and 76-113 present fairly, in all material respects, the financial position of General Electric Company and consolidated affiliates at December 31, 2003 and 2002, and the results of their operations and their cash flows for each of the years in the three-year period ended December 31, 2003, in conformity with accounting principles generally accepted in the United States of America.

As discussed in note 1 to the consolidated financial statements, GE in 2003 changed its methods of accounting for variable interest entities and asset retirement obligations, in 2002 changed its methods of accounting for goodwill and other intangible assets and for stock-based compensation, and in 2001 changed its methods of accounting for derivative instruments and hedging activities and impairment of certain beneficial interests in securitized assets.

Our audits were made for the purpose of forming an opinion on the consolidated financial statements taken as a whole. The accompanying consolidating information appearing on pages 71, 73 and 75 is presented for purposes of additional analysis of the consolidated financial statements rather than to present the financial position, results of operations and cash flows of the individual entities. The consolidating information has been subjected to the auditing procedures applied in the audits of the consolidated financial statements and, in our opinion, is fairly stated in all material respects in relation to the consolidated financial statements taken as a whole.

/s/ KPMG LLP

KPMG LLP

Stamford, Connecticut

February 6, 2004

43 GE 2003 ANNUAL REPORT

MANAGEMENT'S DISCUSSION AND ANALYSIS

OPERATIONS

Our consolidated financial statements combine the industrial manufacturing and product services businesses of General Electric Company (GE) and the financial services businesses of General Electric Capital Services, Inc. (GECS or financial services).

We present Management's Discussion of Operations in three parts: Overview of Our Earnings from 2001 through 2003, Segment Operations and International Operations.

In the accompanying analysis of financial information, we sometimes refer to data derived from consolidated financial information but not required by U.S. generally accepted accounting principles (GAAP) to be presented in financial statements. Certain of these data are considered "non-GAAP financial measures" under the U.S. Securities and Exchange Commission (SEC) regulations; those rules require the supplemental explanation and reconciliation provided on page 69.

ON JANUARY 1, 2004, WE SIMPLIFIED OUR ORGANIZATION. With 11 operating segments, we will achieve lower costs of operations in platforms that will accommodate our future growth. The new segments most affected by this change follow:

- Advanced Materials–plastics, silicones and quartz

- Infrastructure–water, security, sensors and Fanuc Automation

- Transportation–aircraft engines and rail

- Consumer and Industrial–appliances, lighting and industrial

- Commercial Finance–the combination of Commercial Finance and the Fleet Services business that was previously part of Equipment Management

- Equipment and Other Services–the combination of Equipment Management and the former All Other GECS segments

Results for 2003 in this financial section are reported on the 13 business basis in effect in 2003.

During 2003, we entered into an agreement to acquire U.K.-based Amersham plc, a world leader in medical diagnostics and life sciences. We also entered into an agreement to merge NBC with Vivendi Universal Entertainment to create one of the world's premier media companies, NBC Universal.

We announced in November 2003 our intent for an initial public offering (IPO) of a new company, Genworth Financial, Inc. (Genworth), comprising most of our life and mortgage insurance businesses. We plan to sell approximately one-third of Genworth's equity in the IPO, and we expect (subject to market conditions) to reduce our ownership over the next three years as Genworth transitions to full independence. We commenced the IPO process in January 2004 and expect to complete the IPO in the first half of the year, subject to market conditions and receipt of various regulatory approvals.

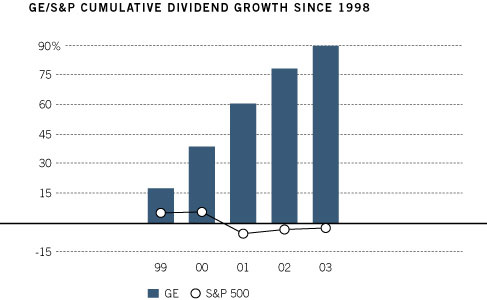

WE DECLARED $7.8 BILLION IN DIVIDENDS IN 2003. Per-share dividends of $0.77 were up 5% from 2002, following an 11% increase from the preceding year. We have rewarded our shareowners with 28 consecutive years of dividend growth. Our dividend growth for the past five years has significantly outpaced dividend growth of companies in the Standard & Poor's 500 stock index.

Except as otherwise noted, the analysis in the remainder of this section presents the results of GE (with GECS included on a one-line basis) and GECS. See the Segment Operations section on page 49 for a more detailed discussion of the businesses within GE and GECS.

Overview of Our Earnings from 2001 through 2003

The global economic environment must be considered when evaluating our 2001 to 2003 results. Important factors for us included slow global economic growth, a mild U.S. recession that did not cause significantly higher credit losses, lower global interest rates, distinct developments in three industries that are significant to us (power generation, property and casualty insurance and commercial aviation), and escalating raw material prices. As you will see in detail in the following pages, our diversification and risk management strategies reduced the earnings effects of many of the significant developments of the last three years.

If, for comparison, we adjust 2001 results for the required accounting change to stop goodwill amortization, our earnings would have increased modestly in percentage terms over this three-year period. This modest increase results from a combination of factors, both positive and negative.

First, consider two businesses whose results were noteworthy.

- Power Systems is significant to our consolidated results, at 16% and 21% of three-year revenues and earnings before accounting changes, respectively. Power Systems was significantly affected by the unprecedented industry dynamics sometimes referred to as the "U.S. power bubble," a phenomenon that dramatically increased demand for power generation

44 GE 2003 ANNUAL REPORT

MANAGEMENT'S DISCUSSION AND ANALYSIS

equipment, peaking during 2002. Power Systems continued shipping large numbers of gas turbine units in 2002, reaching $0.09 per share growth in earnings–up 29% from 2001. (Note that per-share results we present in this discussion are on a diluted basis.) The subsequent 2003 decline in shipments was reflected in the $0.14 per share drop in 2003 earnings. We foresaw the 2002 end of the "bubble" and took appropriate action to cushion the downturn, right-sizing the business and growing and investing in other lines of the power generation business such as product services and GE Wind. The result is a Power Systems business whose results are remarkable from any perspective save its own extraordinary recent history.

- At Employers Reinsurance Corporation (ERC), we, like most of the reinsurance industry, faced volatility throughout the period. We are now confident we have worked through our historical underwriting mistakes. But in 2002 we recognized losses on our 1997-2001 business, increasing loss reserves by $3.5 billion, resulting in a loss of $0.18 per share in 2002, a decline of $0.19 per share from 2001. In 2003, our turnaround efforts started to pay off. We realized benefits from improved ERC operations and ERC earnings rebounded by $0.23 per share to a profit of $0.05 per share.

Most of our operations achieved operating results in line with expectations in the 2001 to 2003 economic environment.

- Commercial and Consumer Finance at 22% and 33% of consolidated three-year revenues and earnings before accounting changes, respectively, are large, profitable growth businesses in which we continue to invest with confidence. In a challenging economic environment, these businesses grew earnings by $0.09 per share in 2003 and $0.06 per share in 2002. Solid core growth, disciplined risk management and successful acquisitions have delivered these strong results.

- Our transportation businesses–Aircraft Engines and Transportation Systems–continued to invest in market-leading technology and services. While our commercial aviation and rail customers were sometimes understandably reluctant to buy new equipment in these markets, our business model also succeeds by diversification. Product services and the military engines business continued strong, and overall these businesses grew 6%, or $0.01 per share, in 2003, following a 3% decline in 2002.

- NBC and Medical Systems contributed strong performances in their distinct markets. NBC's leadership in key demographics yielded higher pricing on strong demand from advertisers. Medical Systems continued to invest in new products and sustained its product leadership position, with strong double-digit growth in Healthcare IT and Ultrasound. The successful acquisitions of Bravo and Instrumentarium also provided growth, and Telemundo improved to a promising position entering 2004. Earnings from these segments increased $0.03 per share in 2003 following a $0.02 per share increase in 2002.

- Plastics, Equipment Management, Consumer Products, Industrial Products and Systems and Specialty Materials are economically sensitive and consequently were affected adversely by the U.S. recession and by slow global growth in developed countries. Even in the difficult environments they face, these businesses continued to succeed in their primary role in GE, to generate cash. Higher capacity, in combination with declining or weak volume growth in many of these industries, resulted in fierce competitive price pressures. Plastics was hit particularly hard because of additional pressures from inflation in certain raw materials such as benzene and natural gas. Earnings from this group of businesses as a whole declined by $0.07 per share over this period with Plastics down $0.03 per share in 2003 and $0.02 per share in 2002. Acquisitions of new growth platforms, such as security and water, offset some of the weakness in these core product lines, and we continue to foresee dramatic growth in these platforms.

Other factors that were important to our recent earnings performance included reduced earnings from our principal postretirement benefit plans (down $0.05 per share in 2003 following a decline of $0.07 per share in 2002) and unusual events in 2002 such as the gains on the sale of Global eXchange Services ($0.03 per share) and the Bravo exchange net of restructuring ($0.03 per share), as well as favorable tax settlements with the U.S. Internal Revenue Service (IRS) in 2002 ($0.04 per share).

Acquisitions affected our operations and contributed $5.4 billion, $7.2 billion and $3.5 billion, respectively, to each of the last three year's consolidated revenues. Our consolidated net earnings in 2003, 2002 and 2001 included approximately $0.5 billion,

45 GE 2003 ANNUAL REPORT

MANAGEMENT'S DISCUSSION AND ANALYSIS

$0.6 billion and $0.2 billion, respectively, from acquired businesses. We integrate acquisitions as quickly as possible and only revenues and earnings during the first 12 months following the quarter in which we complete the acquisition are attributed to such businesses.

Significant matters in our Statement of Earnings, pages 70 and 71, are explained below.

OPERATING MARGIN is sales of goods and services less the costs of goods and services sold, as well as selling, general and administrative expenses. GE operating margin was 15.9% of sales in 2003, down from 19.1% in 2002 and 19.6% in 2001. The decrease in 2003 was attributable to lower operating margins at Power Systems and Plastics. The decline in 2002 was attributable to Plastics and the Lighting business in Consumer Products, and also reflected $0.6 billion of restructuring and other charges, partially offset by improvements in operating margins at Power Systems and NBC. Restructuring and other charges included $0.4 billion for rationalizing certain operations and facilities of GE's worldwide industrial businesses.

Sales of product services were $22.9 billion in 2003, a 10% increase over 2002. Increases in product services in 2003 and 2002 were widespread, led by continued strong growth at Power Systems, Medical Systems and Specialty Materials. Operating margin from product services was approximately $5.3 billion, compared with $5.2 billion in 2002. The increase reflected improvements at Power Systems and Specialty Materials.

TOTAL COST PRODUCTIVITY (sales in relation to costs, both on a constant dollar basis) for GE was negative 1.3% in 2003 on declining volume at Power Systems and Plastics. In 2002 variable cost productivity improvements (led by Industrial Systems and Plastics) and base cost productivity improvements at Plastics were more than offset by lower base cost productivity, primarily at Power Systems, Industrial Systems and Specialty Materials.

PRINCIPAL POSTRETIREMENT BENEFIT PLANS contributed modestly to pre-tax earnings in 2003, compared with $0.8 billion and $1.5 billion in 2002 and 2001, respectively. Benefit costs relating to these plans increased in 2003 primarily because of a reduction in the pension discount rate for the year from 7.25% to 6.75% (which increased the pension obligation), amortization of prior years' investment losses, plan benefit changes resulting from union negotiations and increases in retiree medical and drug costs.

Considering current and expected asset allocations, as well as historical and expected returns on various categories of assets in which our plans are invested, we assumed that long-term returns on our pension plan assets would be 8.5% in 2003 and 2002 and 9.5% in 2001. Reducing the assumed return by 100 basis points in 2002 increased annual pension costs by about $480 million pretax. Actual annual investment returns are extremely volatile. Because this short-term market volatility occurs in context of the long-term nature of pension plans, U.S. accounting principles provide that differences between assumed and actual returns are recognized over the average future service of employees. See notes 5 and 6 for additional information about funding status, components of earnings effects and actuarial assumptions of the plans. See page 68 for discussion of pension assumptions.

We believe our postretirement benefit costs will increase in 2004 for a number of reasons, including a further reduction in the pension discount rate from 6.75% to 6.0%, additional amortization of investment losses, plan benefit changes as a result of union negotiations and continued increases in retiree healthcare costs. We continue to expect that our plan assets will earn 8.5%, on average, over the long term.

We will not make any contributions to the GE Pension Plan in 2004. To the best of our ability to forecast the next five years, we do not anticipate making contributions to that Plan so long as expected investment returns are achieved. The present funding status provides assurance of benefits for our participants, but future effects on operating results and funding depend on economic conditions and investment performance.

GE INTEREST AND OTHER FINANCIAL CHARGES amounted to $0.9 billion, $0.6 billion and $0.8 billion in 2003, 2002 and 2001, respectively. Interest costs in 2003 were higher as a result of our issuing $5.0 billion of long-term bonds in the first quarter of the year and higher average short-term borrowings, partially offset by lower average interest rates. The decrease in 2002 was primarily the result of reduced interest on lower tax liabilities following the 2002 settlements described on page 47.

46 GE 2003 ANNUAL REPORT

MANAGEMENT'S DISCUSSION AND ANALYSIS

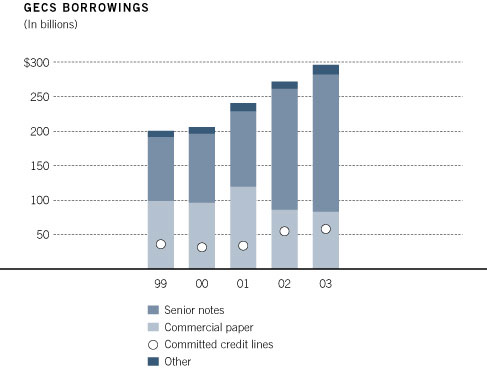

GECS INTEREST EXPENSE ON BORROWINGS was $9.9 billion in 2003 and 2002, compared with $10.6 billion in 2001. Changes over the three-year period reflected the effects of lower interest rates, partially offset by the effects of higher average borrowings of $279.7 billion, $250.1 billion and $212.2 billion in 2003, 2002 and 2001, respectively, used to finance asset growth and acquisitions. The average composite effective interest rate was 3.5% in 2003, compared with 4.1% in 2002 and 5.1% in 2001. In 2003, average assets of $521.6 billion were 15% higher than in 2002, which in turn were 18% higher than in 2001. See page 60 for a discussion of interest rate risk management.

INCOME TAXES on consolidated earnings before accounting changes were 21.7%, compared with 19.9% in 2002 and 28.3% in 2001. Our consolidated income tax rate increased in 2003 by 1.8 percentage points over 2002 because our savings from 2003 business dispositions were less than our 2002 savings from settlements with the IRS. Income tax rates were lower than what they otherwise would have been in both 2003 and 2002 because of the increasing share of earnings from lower taxed international operations. A more detailed analysis of differences between the U.S. federal statutory rate and the consolidated rate, as well as other information about our income tax provisions, is provided in note 7. The nature of business activities and associated income taxes differ for GE and for GECS, and a separate analysis of each is presented in the paragraphs that follow.

Because GE tax expense does not include taxes on GECS earnings, the GE effective tax rate is best analyzed in relation to GE earnings excluding GECS. In 2003, 2002 and 2001, respectively, GE's pre-tax earnings excluding GECS were $10.7 billion, $14.3 billion and $12.7 billion. On this basis, GE's effective tax rate was 26.7% in 2003 and 2002, and 32.9% in 2001. The 2003 GE rate was reduced by approximately 1.7 percentage points because certain reductions in pre-tax earnings–specifically, lower earnings at Power Systems and from our principal pension plans–affected taxes at higher than our average rate. The 2003 GE rate was also reduced by approximately 1.0 percentage point (after adjusting for the effect of the lower pre-tax income at Power Systems and our principal pension plans) from a tax benefit on the disposition of shares of GE Superabrasives U.S., Inc., included in the line, "All other–net" in note 7. In 2002, GE entered into settlements with the IRS concerning certain export tax benefits. The effect of the settlements, the tax portion of which is included on the line "Tax on international activities including exports" in note 7, was a reduction of the GE tax rate of approximately 2.7 percentage points. Also in 2002, GE entered into a tax-advantaged transaction to exchange certain assets for the cable network Bravo. The related reduction of approximately 1.0 percentage point in the GE effective tax rate is reflected in the line, "All other–net" in note 7.

GECS effective tax rate was 15.8% in 2003, negative 1.7% in 2002 and 19.8% in 2001. The increase from 2002 to 2003 reflected the absence of a current year counterpart to the 2002 pre-tax loss at ERC and the IRS settlements discussed below, as well as lower pre-tax losses at GE Equity, partially offset by an approximately three percentage point decrease due to the 2003 pre-tax loss and tax benefit on the disposition of shares of ERC Life Reinsurance Corporation (ERC Life), included in the line "All other–net" in note 7.

GECS 2002 effective tax rate reflected pre-tax losses at ERC and GE Equity, the effects of lower taxed earnings from international operations and favorable tax settlements with the IRS. Pre-tax losses of $2.9 billion at ERC and $0.6 billion at GE Equity reduced the effective tax rate of GECS by approximately 17 percentage points.

During 2002, as a result of revised IRS regulations, GECS reached a settlement with the IRS allowing the deduction of previously realized losses associated with the prior disposition of Kidder Peabody. Also during 2002, we reached a settlement with the IRS regarding the treatment of certain reserves for obligations to policyholders on life insurance contracts in the GE Financial Assurance business. The benefits of these settlements, which reduced the GECS tax rate approximately four percentage points (excluding the ERC and GE Equity losses), are included in the line "All other–net" in note 7.

47 GE 2003 ANNUAL REPORT

MANAGEMENT'S DISCUSSION AND ANALYSIS

SUMMARY OF OPERATING SEGMENTS

| |

| | General Electric Company and consolidated affiliates | |

| |

| |

| For the years ended December 31 (In millions) | | 2003 | | | 2002 | | | 2001 | | | 2000 | | | 1999 | |

| |

| REVENUES | | | | | | | | | | | | | | | |

| Aircraft Engines | $ | 10,703 | | $ | 11,141 | | $ | 11,389 | | $ | 10,779 | | $ | 10,730 | |

| Commercial Finance | | 18,869 | | | 17,781 | | | 15,759 | | | 15,333 | | | 12,302 | |

| Consumer Finance | | 12,845 | | | 10,266 | | | 9,508 | | | 9,320 | | | 7,562 | |

| Consumer Products | | 8,282 | | | 8,456 | | | 8,435 | | | 8,717 | | | 8,525 | |

| Equipment Management | | 4,707 | | | 4,766 | | | 4,904 | | | 5,501 | | | 5,309 | |

| Industrial Products and Systems | | 8,396 | | | 7,441 | | | 6,742 | | | 6,628 | | | 6,284 | |

| Insurance | | 26,194 | | | 23,296 | | | 23,890 | | | 24,766 | | | 19,433 | |

| Medical Systems | | 10,198 | | | 8,955 | | | 8,409 | | | 7,275 | | | 6,171 | |

| NBC | | 6,871 | | | 7,149 | | | 5,769 | | | 6,797 | | | 5,790 | |

| Plastics | | 5,245 | | | 5,245 | | | 5,252 | | | 6,013 | | | 5,315 | |

| Power Systems | | 18,462 | | | 22,926 | | | 20,211 | | | 14,861 | | | 10,099 | |

| Specialty Materials | | 3,126 | | | 2,406 | | | 1,817 | | | 2,007 | | | 1,803 | |

| Transportation Systems | | 2,543 | | | 2,314 | | | 2,355 | | | 2,263 | | | 2,358 | |

| All Other GECS | | 1,664 | | | 2,590 | | | 4,795 | | | 11,789 | | | 11,663 | |

| Corporate items and eliminations | | (3,918 | ) | | (2,522 | ) | | (2,819 | ) | | (1,664 | ) | | (1,194 | ) |

| |

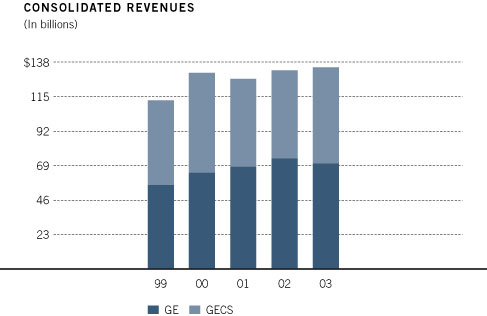

| CONSOLIDATED REVENUES | $ | 134,187 | | $ | 132,210 | | $ | 126,416 | | $ | 130,385 | | $ | 112,150 | |

| |

| SEGMENT PROFIT | | | | | | | | | | | | | | | |

| Aircraft Engines | $ | 2,148 | | $ | 2,060 | | $ | 2,147 | | $ | 2,000 | | $ | 1,739 | |

| Commercial Finance | | 3,765 | | | 3,189 | | | 2,788 | | | 2,416 | | | 1,834 | |

| Consumer Finance | | 2,161 | | | 1,799 | | | 1,602 | | | 1,295 | | | 848 | |

| Consumer Products | | 557 | | | 495 | | | 648 | | | 879 | | | 971 | |

| Equipment Management | | 172 | | | 313 | | | 377 | | | 484 | | | 416 | |

| Industrial Products and Systems | | 631 | | | 597 | | | 626 | | | 676 | | | 611 | |

| Insurance | | 2,102 | | | (95 | ) | | 1,879 | | | 2,201 | | | 2,142 | |

| Medical Systems | | 1,701 | | | 1,546 | | | 1,498 | | | 1,321 | | | 1,107 | |

| NBC | | 1,998 | | | 1,658 | | | 1,408 | | | 1,609 | | | 1,427 | |

| Plastics | | 422 | | | 843 | | | 1,166 | | | 1,518 | | | 1,297 | |

| Power Systems | | 4,076 | | | 6,255 | | | 4,860 | | | 2,523 | | | 1,537 | |

| Specialty Materials | | 381 | | | 282 | | | 267 | | | 347 | | | 293 | |

| Transportation Systems | | 460 | | | 402 | | | 400 | | | 436 | | | 437 | |

| All Other GECS | | (446 | ) | | (580 | ) | | (508 | ) | | (584 | ) | | (285 | ) |

| |

| Total segment profit | | 20,128 | | | 18,764 | | | 19,158 | | | 17,121 | | | 14,374 | |

| GECS goodwill amortization | | — | | | — | | | (552 | ) | | (620 | ) | | (512 | ) |

| GE corporate items and eliminations | | (741 | ) | | 775 | | | 532 | | | 844 | | | 872 | |

| GE interest and other financial charges | | (941 | ) | | (569 | ) | | (817 | ) | | (811 | ) | | (810 | ) |

| GE provision for income taxes | | (2,857 | ) | | (3,837 | ) | | (4,193 | ) | | (3,799 | ) | | (3,207 | ) |

| |

| Earnings before accounting changes | | 15,589 | | | 15,133 | | | 14,128 | | | 12,735 | | | 10,717 | |

| Cumulative effect of accounting changes | | (587 | ) | | (1,015 | ) | | (444 | ) | | — | | | — | |

| |

| CONSOLIDATED NET EARNINGS | $ | 15,002 | | $ | 14,118 | | $ | 13,684 | | $ | 12,735 | | $ | 10,717 | |

| |

The notes to consolidated financial statements on pages 76-113 are an integral part of this summary.

48 GE 2003 ANNUAL REPORT

MANAGEMENT'S DISCUSSION AND ANALYSIS

Segment Operations

REVENUES AND SEGMENT PROFIT FOR OPERATING SEGMENTS are shown on page 48. As discussed in our 2002 Annual Report, effective January 1, 2003, we made changes to the way we report our segments, including the use of business specific, market-based leverage in measuring performance of our financial services businesses. Also, as a result of changes in the way we operated our industrial businesses during 2003, we disaggregated and reported Medical Systems, Plastics, Specialty Materials and Transportation Systems as separate segments. Prior year information has been reclassified to conform to the 2003 presentation. For additional information, including a description of the products and services included in each segment, see pages 112 and 113.

Segment profit is determined based on internal performance measures used by the Chief Executive Officer to assess the performance of each business in a given period. In connection with that assessment, the Chief Executive Officer may exclude matters such as charges for restructuring; rationalization and other similar expenses; certain gains/losses from dispositions; and litigation settlements or other charges, responsibility for which precedes the current management team.

Segment profit always excludes goodwill amortization, the effects of principal pension plans and accounting changes. Segment profit excludes or includes interest and other financial charges and segment income taxes according to how a particular segment management is measured–excluded in determining operating profit for Aircraft Engines, Consumer Products, Industrial Products and Systems, Medical Systems, NBC, Plastics, Power Systems, Specialty Materials and Transportation Systems; included in determining segment profit which we refer to as "segment net earnings" for Commercial Finance, Consumer Finance, Equipment Management, Insurance and All Other GECS.

AIRCRAFT ENGINES revenues decreased 4% to $10.7 billion in 2003 reflecting lower volume ($0.5 billion), primarily related to commercial aircraft and industrial aero-derivative engines, partially offset by higher military spare parts volume. Despite the decrease in revenues, operating profit rose 4% to $2.1 billion reflecting the effects of productivity ($0.2 billion) largely from workforce efficiency, and lower research and development spending upon completion of certain development programs, more than offsetting the effect of decreased volume ($0.1 billion). Aircraft Engines reported a 2% decrease in revenues in 2002 as commercial engine pricing pressures and reduced commercial product services revenues, combined with lower industrial units, were substantially offset by increased military sales. Operating profit in 2002 was 4% lower than in 2001, primarily as a result of lower pricing ($0.1 billion) including pricing for commercial engines, lower product services volume from reduced customer flight hours, and higher labor costs, partially offset by lower material costs and productivity.

See GE Corporate Items and Eliminations on page 55 for a discussion of items not allocated to this segment.

In 2003, revenues from sales to the U.S. government were $2.4 billion, compared with $2.2 billion and $1.9 billion in 2002 and 2001, respectively.

Aircraft Engines received orders of $10.4 billion in 2003, compared with $11.6 billion in 2002 as military orders decreased from $4.3 billion to $2.2 billion and commercial engines increased $0.6 billion to $2.3 billion. The $10.5 billion total backlog at year-end 2003 comprised unfilled product orders of $7.9 billion (of which 37% was scheduled for delivery in 2004) and product services orders of $2.6 billion scheduled for 2004 delivery. Comparable December 31, 2002, total backlog was $11.4 billion.

COMMERCIAL FINANCE

(In millions) | | 2003 | | | 2002 | | | 2001 | |

| |

REVENUES | | | | | | | | | |

Real Estate | $ | 2,386 | | $ | 2,124 | | $ | 1,886 | |

Commercial Equipment Financing | | 4,494 | | | 4,539 | | | 4,212 | |

Corporate Financial Services | | 2,467 | | | 2,350 | | | 1,758 | |

Structured Finance | | 1,423 | | | 1,243 | | | 1,093 | |

Aviation Services | | 2,881 | | | 2,694 | | | 2,173 | |

Vendor Financial Services | | 4,456 | | | 4,130 | | | 3,954 | |

Healthcare Financial Services | | 735 | | | 665 | | | 372 | |

Other Commercial Finance | | 27 | | | 36 | | | 311 | |

| |

Total revenues | $ | 18,869 | | $ | 17,781 | | $ | 15,759 | |

| |

NET REVENUES | | | | | | | | | |

Total revenues | $ | 18,869 | | $ | 17,781 | | $ | 15,759 | |

Interest expense | | 5,577 | | | 5,753 | | | 5,754 | |

| |

Total net revenues | $ | 13,292 | | $ | 12,028 | | $ | 10,005 | |

| |

NET EARNINGS | | | | | | | | | |

Real Estate | $ | 834 | | $ | 650 | | $ | 528 | |

Commercial Equipment Financing | | 817 | | | 719 | | | 640 | |

Corporate Financial Services | | 675 | | | 599 | | | 384 | |

Structured Finance | | 576 | | | 488 | | | 399 | |

Aviation Services | | 506 | | | 454 | | | 497 | |

Vendor Financial Services | | 432 | | | 369 | | | 332 | |

Healthcare Financial Services | | 153 | | | 122 | | | 37 | |

Other Commercial Finance | | (228 | ) | | (212 | ) | | (29 | ) |

| |

Total net earnings | $ | 3,765 | | $ | 3,189 | | $ | 2,788 | |

| |

| | | | | | | | | | |

49 GE 2003 ANNUAL REPORT

MANAGEMENT'S DISCUSSION AND ANALYSIS

December 31 (In millions) | | 2003 | | | 2002 | |

| |

TOTAL ASSETS | | | | | | |

Real Estate | $ | 27,767 | | $ | 29,522 | |

Commercial Equipment Financing | | 53,273 | | | 51,757 | |

Corporate Financial Services | | 29,646 | | | 26,897 | |

Structured Finance | | 21,309 | | | 19,293 | |

Aviation Services | | 33,271 | | | 30,512 | |

Vendor Financial Services | | 24,855 | | | 25,518 | |

Healthcare Financial Services | | 8,367 | | | 7,905 | |

Other Commercial Finance | | 5,495 | | | 2,841 | |

| |

Total assets | $ | 203,983 | | $ | 194,245 | |

| |

Financing receivables–net | $ | 130,129 | | $ | 128,277 | |

| |

| | | | | | | |

Commercial Finance revenues and net earnings increased 6% and 18%, respectively, compared with 2002. The increase in revenues resulted primarily from acquisitions across substantially all businesses ($0.9 billion), higher investment gains at Real Estate ($0.1 billion) and origination growth, partially offset by lower securitization activity at Commercial Equipment Financing ($0.1 billion). The increase in net earnings resulted primarily from origination growth, acquisitions across substantially all businesses ($0.2 billion), higher investment gains at Real Estate as a result of the sale of properties and our investments in Regency Centers and Prologis ($0.1 billion), lower credit losses ($0.1 billion) resulting from continued improvement in overall portfolio credit quality as reflected by lower delinquencies and nonearning receivables, and growth in lower taxed earnings from international operations ($0.1 billion).

The most significant acquisitions affecting Commercial Finance 2003 results were the commercial inventory financing business of Deutsche Financial Services and the structured finance business of ABB, both of which were acquired during the fourth quarter of 2002. These two acquisitions contributed $0.5 billion and $0.1 billion to 2003 revenues and net earnings, respectively.

The 2002 increase in revenues of 13% principally reflected acquisitions and increased originations across substantially all businesses, partially offset by reduced market interest rates and lower securitization activity at Corporate Financial Services and Commercial Equipment Financing. The 2002 net earnings increase of 14% primarily reflected acquisitions ($0.4 billion) and origination growth, productivity across all businesses and growth in lower taxed earnings from international operations, partially offset by increased credit losses and lower securitization activity at Corporate Financial Services and Commercial Equipment Financing.

See All Other GECS on page 54 for a discussion of items not allocated to this segment.

CONSUMER FINANCE

(In millions) | | 2003 | | | 2002 | | | 2001 | |

| |

REVENUES | | | | | | | | | |

Global Consumer Finance | $ | 8,502 | | $ | 6,489 | | $ | 5,561 | |

Card Services | | 4,343 | | | 3,777 | | | 3,947 | |

| |

Total revenues | $ | 12,845 | | $ | 10,266 | | $ | 9,508 | |

| |

NET REVENUES | | | | | | | | | |

Total revenues | $ | 12,845 | | $ | 10,266 | | $ | 9,508 | |

Interest expense | | 2,696 | | | 2,143 | | | 2,179 | |

| |

Total net revenues | $ | 10,149 | | $ | 8,123 | | $ | 7,329 | |

| |

NET EARNINGS | | | | | | | | | |

Global Consumer Finance | $ | 1,478 | | $ | 1,224 | | $ | 1,034 | |

Card Services | | 781 | | | 670 | | | 669 | |

Other Consumer Finance | | (98 | ) | | (95 | ) | | (101 | ) |

| |

Total net earnings | $ | 2,161 | | $ | 1,799 | | $ | 1,602 | |

| |

| | | | | | | | | | |

December 31 (In millions) | | 2003 | | | 2002 | |

| |

TOTAL ASSETS | | | | | | |

Global Consumer Finance | $ | 87,387 | | $ | 58,310 | |

Card Services | | 19,143 | | | 18,655 | |

| |

Total assets | $ | 106,530 | | $ | 76,965 | |

| |

Financing receivables–net | $ | 90,693 | | $ | 63,254 | |

| |

| | | | | | | |

Consumer Finance revenues increased 25% in 2003, a result of acquisitions ($1.1 billion), the net effects of the weaker U.S. dollar ($0.7 billion), origination growth as a result of continued global expansion and the premium on the sale of The Home Depot private label credit card receivables ($0.1 billion). Net earnings increased 20% in 2003 as a result of origination growth, growth in lower taxed earnings from international operations, the premium on the sale of The Home Depot private label credit card receivables ($0.1 billion) and acquisitions. These increases were partially offset by lower securitization activity at Card Services ($0.2 billion) and lower earnings in Japan, principally as a result of increased personal bankruptcies.

The most significant acquisitions affecting Consumer Finance 2003 results were First National Bank, which provides mortgage and sales finance products in the United Kingdom, and the retail sales finance unit of Conseco Finance Corp., both of which were acquired during the second quarter of 2003. These businesses contributed $0.7 billion and $0.1 billion to 2003 revenues and net earnings, respectively.

Revenues increased in 2002 primarily as a result of acquisitions ($0.8 billion) and increased international originations, partially offset by lower securitization activity at Card Services ($0.4 billion). Net earnings increased 12% in 2002, as a result of origination growth, acquisitions ($0.1 billion), growth in lower taxed earnings from international operations and productivity benefits, partially offset by lower securitization activity at Card Services ($0.1 billion).

See All Other GECS on page 54 for a discussion of items not allocated to this segment.

50 GE 2003 ANNUAL REPORT

MANAGEMENT'S DISCUSSION AND ANALYSIS

CONSUMER PRODUCTS revenues decreased 2% to $8.3 billion in 2003, reflecting lower selling prices ($0.2 billion) primarily of home appliances and consumer lighting products. Operating profit rose 13% to $0.6 billion in 2003, as lower base costs ($0.1 billion), primarily achieved by combining the lighting and appliance businesses, and the mix of higher-margin appliances more than offset the effects of lower product pricing ($0.2 billion). In 2002, Consumer Products revenues of $8.5 billion were flat compared with 2001 as 5% higher appliances revenues, reflecting success of new products, were offset by a 9% decline in revenues from lighting products. Operating profit decreased 24% in 2002 to $0.5 billion, with adverse results in the lighting products business, particularly lower prices, higher base costs and higher charges resulting from customer credit issues. Lower prices reduced 2002 operating profit by $0.1 billion.

EQUIPMENT MANAGEMENT

(In millions) | | 2003 | | | 2002 | | 2001 |

|

REVENUES | $ | 4,707 | | $ | 4,766 | $ | 4,904 |

|

NET REVENUES | | | | | | | |

Total revenues | $ | 4,707 | | $ | 4,766 | $ | 4,904 |

Interest expense | | 741 | | | 812 | | 905 |

|

Total net revenues | $ | 3,966 | | $ | 3,954 | $ | 3,999 |

|

NET EARNINGS | $ | 172 | | $ | 313 | $ | 377 |

|

| | | | | | | | |

December 31 (In millions) | | 2003 | | | 2002 | |

| |

TOTAL ASSETS | $ | 25,469 | | $ | 25,222 | |

| |

Equipment leased to others | $ | 12,482 | | $ | 11,285 | |

| |

| | | | | | | |

Equipment Management revenues and net earnings decreased 1% and 45%, respectively, in 2003 compared with 2002. The decrease in revenues resulted primarily from lower asset utilization and lower prices ($0.2 billion), an effect of industry-wide excess equipment capacity reflective of current economic conditions in the road and rail transportation sector. Also contributing to the decrease were $0.1 billion lower gains on asset sales related to our continuing strategy to optimize fleet mix, age and size. These decreases were substantially offset by the net effects of the weaker U.S. dollar ($0.3 billion) and the results of acquisitions. The decrease in net earnings resulted primarily from lower asset utilization, lower price and lower gains on asset sales.

Equipment Management experienced business-wide declining utilization rates throughout 2002, resulting in both lower revenues and lower earnings. Equipment Management realized productivity benefits in 2002, partially offsetting lower utilization rate's effect on earnings.

See All Other GECS on page 54 for a discussion of items not allocated to this segment.

INDUSTRIAL PRODUCTS AND SYSTEMS

(In millions) | | 2003 | | | 2002 | | | 2001 | |

| |

REVENUES | | | | | | | | | |

Industrial Systems | $ | 5,517 | | $ | 4,968 | | $ | 4,440 | |

GE Supply | | 2,879 | | | 2,473 | | | 2,302 | |

| |

Total revenues | $ | 8,396 | | $ | 7,441 | | $ | 6,742 | |

| |

OPERATING PROFIT | | | | | | | | | |

Industrial Systems | $ | 501 | | $ | 488 | | $ | 527 | |

GE Supply | | 130 | | | 109 | | | 99 | |

| |

Total operating profit | $ | 631 | | $ | 597 | | $ | 626 | |

| |

| | | | | | | | | | |

Industrial Products and Systems reported revenues of $8.4 billion, 13% higher than in 2002, primarily as a result of $0.5 billion of sales from recently acquired businesses that more than offset the effects of lower prices, while operating profit rose 6% to $0.6 billion in 2003. Industrial Systems revenues rose $0.5 billion on higher volume ($0.3 billion). Operating profit was slightly higher as productivity ($0.1 billion), higher volume, primarily as a result of recently acquired businesses, and an investment gain were partially offset by $0.1 billion from lower prices. In 2002, Industrial Systems revenues rose 12% compared with 2001 on higher volume ($0.6 billion), but operating profit declined 7%, reflecting the negative effects of lower selling prices ($0.1 billion).

INSURANCE

(In millions) | | 2003 | | | 2002 | | | 2001 | |

| |

REVENUES | | | | | | | | | |

GE Financial Assurance | $ | 13,130 | | $ | 12,317 | | $ | 12,826 | |

Mortgage Insurance | | 1,293 | | | 1,090 | | | 1,075 | |

GE Global Insurance | | | | | | | | | |

Holding (ERC) | | 11,600 | | | 9,432 | | | 9,453 | |

Other Insurance | | 171 | | | 457 | | | 536 | |

| |

Total revenues | $ | 26,194 | | $ | 23,296 | | $ | 23,890 | |

| |

NET EARNINGS | | | | | | | | | |

GE Financial Assurance | $ | 918 | | $ | 934 | | $ | 1,088 | |

Mortgage Insurance | | 564 | | | 538 | | | 500 | |

GE Global Insurance | | | | | | | | | |

Holding (ERC) | | 481 | | | (1,794 | ) | | 78 | |

Other Insurance | | 139 | | | 227 | | | 213 | |

| |

Total net earnings | $ | 2,102 | | $ | (95 | ) | $ | 1,879 | |

| |

| | | | | | | | | | |

Insurance revenues increased $2.9 billion (12%) in 2003 on increased premium revenues ($2.2 billion), a gain of $0.6 billion on sale of GE Edison Life Insurance Company (Edison Life) by GE Financial Assurance, higher investment income ($0.4 billion) and the net effects of the weaker U.S. dollar ($0.7 billion). The premium revenue increase reflected continued favorable pricing at ERC ($0.5 billion), net volume growth in certain ERC and GE Financial Assurance businesses ($0.8 billion), absence of prior year loss adjustments ($0.4 billion), adjustment of current year

51 GE 2003 ANNUAL REPORT

MANAGEMENT'S DISCUSSION AND ANALYSIS

premium accruals to actual ($0.3 billion) and lower levels of ceded premiums resulting from a decline in prior year ERC loss events ($0.1 billion). Partial revenue offsets resulted from absence of revenues following the sale of Edison Life ($0.7 billion) and a $0.2 billion loss on the disposition of Financial Guaranty Insurance Company (FGIC) at the end of 2003. Revenues decreased 2% in 2002, principally the result of ongoing planned run-off of acquired policies at Toho and lower realized investment gains.

Net earnings increased $2.2 billion in 2003, primarily from the substantial improvement in current operating results at ERC ($2.3 billion) reflecting improved underwriting, lower adverse development (discussed below) and generally favorable industry conditions during the year. Net earnings also benefited from the gain on the sale of Edison Life ($0.3 billion). These increases were partially offset by the absence of a current year counterpart to the favorable tax settlement with the IRS in 2002 ($0.2 billion) and the loss on the sale of FGIC ($0.1 billion after tax).

Net earnings decreased $2.0 billion in 2002, primarily the result of adverse development at ERC. Also in 2002, investment gains decreased, an effect partially offset by core premium growth including higher premium pricing at ERC, and benefit from the favorable tax settlement with the IRS at GE Financial Assurance.

As described on page 68 under the caption "Insurance liabilities and reserves," insurance loss provisions are adjusted up or down based on the best available estimates. Reported claims activity at ERC related to prior year loss events, particularly for liability-related exposures underwritten in 1997 through 2001, has performed much worse than we anticipated.

- In the fourth quarter of 2002, considering the continued acceleration in reported claims activity, we concluded that our best estimate of ultimate pre-tax losses was $2.5 billion higher in the range of reasonably possible loss scenarios than we had previously estimated. The more significant 2002 adverse development was in hospital medical malpractice, product liability and professional liability ($0.3 billion each) and umbrella liability, workers compensation, individual liability and asbestos ($0.2 billion each). With amounts recognized in the first three quarters of 2002, our total 2002 pre-tax charge for adverse development at ERC amounted to $3.5 billion.

- In 2003, we continued to monitor our reported claims activity compared with our revised expected loss levels. In a majority of our lines of business, reported claims activity in 2003 was reasonably close to expected amounts. In a few lines–principally medical malpractice, product liability and certain director and officer related coverage–reported claims volumes exceeded our revised loss expectations. Accordingly, we increased our loss reserves to the newly-indicated ultimate levels in 2003, recording adverse development of $0.9 billion pretax. We are confident we have worked through our historical underwriting mistakes.

Throughout 2003, ERC has remained disciplined in rejecting risks that either fail to meet the established standards of price or terms and conditions, or that involve risks for which sufficient historical data do not exist to permit us to make a satisfactory evaluation. For risks that pass our criteria, we have sought to retain and even judiciously expand our business. On the other hand, we have curtailed or exited business in particular property and casualty business channels when expected returns do not appear to justify the risks.

ERC's improved operating performance is illustrated by its "combined ratio"–the sum of claims-related losses incurred plus related underwriting expenses in relation to earned premiums. A combined ratio of less than 100% reflects an underwriting profit, that is, profit before investment income, another significant revenue source for most insurance entities. ERC's 2003 combined ratio was 106%, but, in an early indication of the effectiveness of our revised underwriting standards, the combined ratio excluding prior-year loss events was 93%.

Our Mortgage Insurance business had favorable development throughout the three years ended December 31, 2003, primarily reflecting continued strength in certain real estate markets and the success of our loss containment initiatives in that business.

See All Other GECS on page 54 for a discussion of items not allocated to this segment and the discussion on page 44 of our planned Genworth offering.

MEDICAL SYSTEMS revenues increased 14% to $10.2 billion in 2003 reflecting $0.5 billion of sales from recently acquired businesses, primarily Instrumentarium, and other volume growth ($0.7 billion) that more than offset lower prices ($0.4 billion). Operating profit of $1.7 billion rose 10% as productivity ($0.3 billion) and higher volume ($0.2 billion) more than offset the $0.4 billion effects of lower prices. Medical Systems revenues increased 6% to $9.0 billion in 2002, on higher equipment and product services volume, partially offset by lower prices ($0.4 billion) and weak market conditions in Latin America and Japan. Operating profit rose 3% to $1.5 billion in 2002 as productivity ($0.2 billion) and increased volume ($0.2 billion) were partially offset by a $0.4 billion effect of lower pricing.

52 GE 2003 ANNUAL REPORT

MANAGEMENT'S DISCUSSION AND ANALYSIS

See GE Corporate Items and Eliminations on page 55 for a discussion of items not allocated to this segment.

Orders received by Medical Systems in 2003 were $10.5 billion, compared with $9.4 billion in 2002. The $4.6 billion total backlog at year-end 2003 comprised unfilled product orders of $2.8 billion (of which 95% was scheduled for delivery in 2004) and product services orders of $1.8 billion scheduled for 2004 delivery. Comparable December 31, 2002, total backlog was $4.0 billion.

During 2003, we entered into an agreement to acquire U.K.-based Amersham plc, a world leader in medical diagnostics and life sciences.

NBC revenues decreased 4% to $6.9 billion in 2003 following a 24% increase to $7.1 billion in 2002. Operating profit rose 21% to $2.0 billion in 2003, following an 18% increase in the prior year. Results were affected by several events during the three-year period. Improved pricing and higher syndication and network sales increased revenues by $0.2 billion in 2002 and higher prices and network sales increased revenues $0.5 billion in 2003, but were partially offset in 2003 by advertising reductions because of coverage of the Iraq war ($0.1 billion). The Salt Lake City Olympic Games and final year of NBA coverage contributed $0.7 billion and $0.3 billion, respectively, to 2002 revenues, but the NBA contract resulted in a loss that exceeded profit from the Olympics. We acquired Telemundo and Bravo in 2002; together they added $0.7 billion and $0.3 billion of advertising revenues in 2003 and 2002, respectively, and $0.1 billion operating profit in 2003. The 2002 exchange of certain assets for Bravo resulted in $0.6 billion of gain, $0.2 billion of which was attributed to NBC's segment results, an amount equal to $0.2 billion of other charges for impairments in 2002. The remainder was included in GE Corporate Items and Eliminations as discussed on page 55.

During 2003, we entered into an agreement to merge NBC with Vivendi Universal Entertainment to create one of the world's premier media companies, NBC Universal.

PLASTICS revenues in 2003 were flat at $5.2 billion as lower volume ($0.3 billion) offset the effects of the weaker U.S. dollar ($0.2 billion) and price increases. Operating profit of $0.4 billion was 50% lower than in 2002 reflecting higher material costs ($0.2 billion), primarily benzene, and lower productivity ($0.2 billion). Plastics revenues of $5.2 billion in 2002 were relatively unchanged from 2001 levels, as weakness in pricing ($0.5 billion) offset increased volume ($0.4 billion). Operating profit declined 28% in 2002 to $0.8 billion as productivity was not sufficient to offset the effects of lower prices ($0.5 billion) and increased raw material costs.

See GE Corporate Items and Eliminations on page 55 for a discussion of items not allocated to this segment.

POWER SYSTEMS revenues fell 19% to $18.5 billion as growth in the energy services and wind businesses was more than offset by lower volume ($4.7 billion) reflecting the continued effects of the decline in sales of large gas turbines (208 in 2003 compared with 362 in 2002) and industrial aero-derivative products, partially offset by the net effects of the weaker U.S. dollar ($0.7 billion). Operating profit dropped 35% to $4.1 billion in 2003, principally reflecting the combined effects of lower volume ($1.3 billion), lower productivity ($0.7 billion) and lower prices ($0.4 billion). Customer contract termination fees, net of associated costs, were $0.6 billion in 2003 and $0.9 billion in 2002, reflecting the decline in demand for new power generation equipment that began in 2002, with such fees primarily occurring in that year and the first half of 2003. Power Systems revenues increased 13% to $22.9 billion in 2002 on higher volume ($2.3 billion) and price ($0.2 billion). Operating profit rose 29% to $6.3 billion in 2002 on higher volume ($0.6 billion), and productivity ($0.6 billion) which included the $0.9 billion positive effect of customer contract termination fees, net of associated costs. Results in 2002 also included restructuring and other charges of $0.2 billion as Power Systems adjusted its cost structure.

Power Systems orders were $15.4 billion in 2003, compared with $13.3 billion in 2002, reflecting strong demand for wind turbines, oil and gas turbomachinery, and services. The $12.3 billion total backlog at year-end 2003 comprised unfilled product orders of $7.8 billion (of which 70% was scheduled for delivery in 2004) and product services orders of $4.5 billion scheduled for 2004 delivery. Comparable December 31, 2002, total backlog was $16.1 billion.

SPECIALTY MATERIALS reported a 30% increase in revenues, to $3.1 billion in 2003, on higher volume ($0.5 billion) primarily from acquisitions. Recently acquired businesses, the largest of which were Betz-Dearborn, Osmonics and OSi, contributed $0.6 billion of sales in 2003. Operating profit rose 35% to $0.4 billion on higher volume from acquisitions, the effect of dispositions and productivity, partially offset by price declines and higher material costs. Specialty Materials revenues increased 32% to $2.4 billion in 2002 on higher volume ($0.6 billion), reflecting the contributions of acquisitions, partially offset by lower selling prices ($0.1 billion). Operating profit at Specialty Materials rose 6% to $0.3 billion in 2002, reflecting higher volume ($0.1 billion) and lower material costs, partially offset by lower pricing ($0.1 billion) and higher base costs.

53 GE 2003 ANNUAL REPORT

MANAGEMENT'S DISCUSSION AND ANALYSIS

TRANSPORTATION SYSTEMS revenues of $2.5 billion increased 10% compared with 2002 on higher volume ($0.2 billion), primarily locomotive sales and growth in the global signaling business. Operating profit rose 14% to $0.5 billion in 2003 on the higher volume, partially offset by reduced pricing. In 2002, Transportation Systems revenues of $2.3 billion were 2% lower and operating profit of $0.4 billion was about the same as in 2001, as product services revenues, strong variable cost productivity and lower material costs offset the effects of lower volume and pricing pressures.

Transportation Systems received orders of $2.9 billion in 2003, compared with $2.8 billion in 2002. The $2.4 billion total backlog at year-end 2003 comprised unfilled product orders of $1.3 billion (of which 69% was scheduled for delivery in 2004) and product services orders of $1.1 billion scheduled for 2004 delivery. Comparable December 31, 2002, total backlog was $2.1 billion.

ALL OTHER GECS

(In millions) | | 2003 | | | 2002 | | | 2001 | |

| |

REVENUES | | | | | | | | | |

IT Solutions | $ | 496 | | $ | 1,992 | | $ | 2,301 | |

GE Equity | | (169 | ) | | (384 | ) | | (126 | ) |

Americom | | – | | | – | | | 1,698 | |

Not allocated | | – | | | – | | | (436 | ) |

Other–All Other GECS | | 1,337 | | | 982 | | | 1,358 | |

| |

Total revenues | $ | 1,664 | | $ | 2,590 | | $ | 4,795 | |

| |

NET EARNINGS | | | | | | | | | |

IT Solutions | $ | (45 | ) | $ | (46 | ) | $ | 13 | |

GE Equity | | (176 | ) | | (375 | ) | | (264 | ) |

Americom | | – | | | – | | | 901 | |

Not allocated | | – | | | – | | | (656 | ) |

Other–All Other GECS | | (225 | ) | | (159 | ) | | (502 | ) |

| |

Total net earnings | $ | (446 | ) | $ | (580 | ) | $ | (508 | ) |

| |

| | | | | | | | | |

All Other GECS includes our activities and businesses that we do not measure within one of the other financial services segments.

In addition to comments on All Other GECS elsewhere in this report, the following comments relate to the table above:

- IT Solutions–Revenues decreased by 75% in 2003 primarily as a result of geographic market exits in Europe. Net losses remained flat in 2003 compared with 2002, largely because of tax benefits recorded in 2002 associated with, and offsetting losses generated by, certain European operations that we sold.

- GE Equity–GE Equity manages equity investments in early-stage, early-growth, pre-IPO companies. GE Equity revenues include income, gains and losses on such investments. Revenue and loss performance reflected the overall improvement in equity markets and lower level of losses in 2003. Operating performance during 2002 reflected increased losses on investments, including losses in the telecommunications and software industries, and lower gains. GE Equity ceased making new investments in 2002, but continues to provide financial support to companies in its portfolio which will be managed for maximum value over time, eventually liquidating.

- Americom–On November 9, 2001, we exchanged our satellite operations, comprising the stock of Americom and other related assets and liabilities, for a combination of cash and 31% of the publicly-traded stock of SES Global, a leading satellite company, in order to create the world's largest satellite services provider. The transaction resulted in a gain of $1.2 billion ($0.6 billion after tax), representing the difference between the carrying value of the 69% investment in Americom and the amount of cash plus the market value of SES Global shares received at the closing date. No gain was recorded on the 31% interest in Americom that was indirectly retained by us. Our investment in SES Global is accounted for on the equity method in Commercial Finance.

- Not allocated–Certain amounts are not included in other financial services operating segments or businesses because they are excluded from the measurement of their operating performance for internal purposes. In 2001, after-tax charges of $0.7 billion primarily related to asset impairments and product line exits, including: other-than-temporary impairments of investments totaling $0.3 billion, the largest of which were held by GE Financial Assurance, GE Equity and ERC; charges of $0.1 billion related to loss events and the exit of certain insurance and financing product lines at ERC, primarily non-standard automobile and higher limit industrial property insurance coverages; charges of $0.1 billion related to the exit of certain financing product lines at Consumer Finance; and costs related to restructuring totaling $0.1 billion, consisting of involuntary termination benefits, facilities exit costs, and asset impairments.

- Other–All Other GECS includes GECS corporate expenses, liquidating businesses and other non-segment aligned operations. In 2003, the most significant of these activities were the consolidation of certain entities in our financial statements as a result of our July 1, 2003, adoption of Financial Accounting Standards Board (FASB) Interpretation No. (FIN) 46,Consolidation of Variable Interest Entities (see note 29); Auto Financial Services; the U.S. Auto and Home business, which was sold in the third quarter of 2003; and a tax benefit related to the sale of ERC Life. In 2002 and 2001, the most significant of these activities were Auto Financial Services and the U.S. Auto and Home business.

54 GE 2003 ANNUAL REPORT

MANAGEMENT'S DISCUSSION AND ANALYSIS

GE CORPORATE ITEMS AND ELIMINATIONS

(In millions) | | 2003 | | | 2002 | | | 2001 | |

| |

REVENUES | | | | | | | | | |

Eliminations | $ | (3,918 | ) | $ | (2,522 | ) | $ | (2,819 | ) |

| |

OPERATING PROFIT | | | | | | | | | |

Principal pension plans | $ | 1,040 | | $ | 1,556 | | $ | 2,095 | |

Eliminations | | (717 | ) | | (817 | ) | | (769 | ) |

Underabsorbed corporate overhead | | (582 | ) | | (367 | ) | | (334 | ) |

Not allocated | | (228 | ) | | 115 | | | (545 | ) |

Other | | (254 | ) | | 288 | | | 85 | |

| |

Total | $ | (741 | ) | $ | 775 | | $ | 532 | |

| |

| | | | | | | | | | |

GE Corporate Items and Eliminations include the effects of eliminating transactions between operating segments; cost reductions from our principal pension plans; liquidating businesses; underabsorbed corporate overhead; certain non-allocated amounts described below; a variety of sundry items; and, before 2002, goodwill amortization. Corporate overhead is allocated to GE operating segments based on a ratio of segment net cost of operations, excluding direct materials, to total company cost of operations. This caption also includes internal allocated costs for segment funds on deposit.

Not allocated–Certain amounts are not included in GE operating segments because they are excluded from the measurement of their operating performance for internal purposes. In 2003 and 2002, these comprised charges of $0.2 billion and $0.1 billion, respectively, for settlement of litigation, restructuring and other charges at Medical Systems; in 2002, a portion of NBC's gain from the Bravo exchange; in 2002, a total of $0.1 billion for restructuring and other charges at Aircraft Engines and Plastics; and in 2001, a total of $0.5 billion of goodwill amortization.

Other includes a $0.5 billion gain from the sale of 90% of Global eXchange Services in 2002.

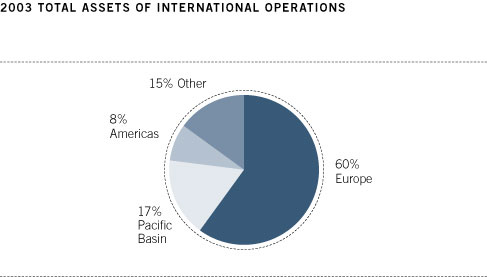

International Operations

Our international activities span all global regions and primarily encompass manufacturing for local and export markets, import and sale of products produced in other regions, leasing of aircraft, sourcing for our plants domiciled in other global regions and provision of financial services within these regional economies. Thus, when countries or regions experience currency and/or economic stress, we often have increased exposure to certain risks, but also often have new profit opportunities. Potential increased risks include, among other things, higher receivables delinquencies and bad debts, delays or cancellation of sales and orders principally related to power and aircraft equipment, higher local currency financing costs and a slowdown in established financial services activities. New profit opportunities include, among other things, more opportunities for lower cost outsourcing, expansion of industrial and financial services activities through purchases of companies or assets at reduced prices and lower U.S. debt financing costs.

Estimated results of international activities include the results of our operations located outside the United States plus all U.S. exports. We classify certain GECS operations that cannot meaningfully be associated with specific geographic areas as "Other international" for this purpose.

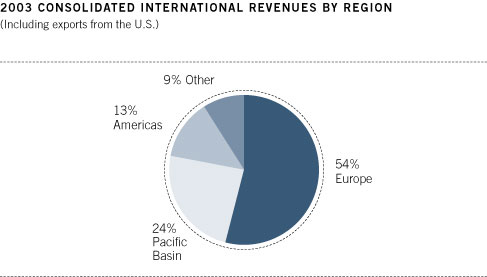

International revenues rose 14% to $60.8 billion in 2003 compared with $53.4 billion and $51.9 billion in 2002 and 2001, respectively. International revenues as a percentage of consolidated revenues were 45% in 2003, compared with 40% and 41% in 2002 and 2001, respectively. The effects of exchange rates on reported results were to increase revenues by $3.8 billion and $0.4 billion in 2003 and 2002, respectively, and increase earnings by $0.1 billion in 2003 and decrease earnings by $0.1 billion in 2002.

CONSOLIDATED INTERNATIONAL REVENUES

(In millions) | | 2003 | | | 2002 | | | 2001 | |

| |

Europe | $ | 30,505 | | $ | 24,813 | | $ | 24,381 | |

Pacific Basin | | 13,119 | | | 12,026 | | | 11,447 | |

Americas | | 5,854 | | | 5,165 | | | 5,507 | |

Other international | | 4,608 | | | 3,911 | | | 3,456 | |

| |

| | | 54,086 | | | 45,915 | | | 44,791 | |

Exports from the U.S. to external customers | | 6,719 | | | 7,481 | | | 7,149 | |

| |

Total | $ | 60,805 | | $ | 53,396 | | $ | 51,940 | |

| |

| | | | | | | | | | |

GE international revenues were $33.0 billion, $29.0 billion and $28.3 billion in 2003, 2002 and 2001, respectively. The $4.0 billion increase in GE international revenues related to increased operations outside the U.S., partially offset by lower U.S. exports.

55 GE 2003 ANNUAL REPORT

MANAGEMENT'S DISCUSSION AND ANALYSIS

GE revenues in Europe rose 25%, led by Power Systems, Medical Systems and Industrial Products and Systems, reflecting the net effects of the weaker U.S. dollar and volume growth. GE revenues in the Pacific Basin increased 14% as most businesses reported improved results. Industrial Products and Systems and Power Systems were the primary contributors to a 16% increase in revenues in the Americas and Power Systems more than accounted for the 10% decrease in U.S. exports. The increase in 2002 related to both an increase in operations outside the U.S. and higher U.S. exports. Revenue increases in Europe were led by Medical Systems and Industrial Systems in 2002. Growth in Specialty Materials revenues across all geographic areas was partially offset by lower sales in all areas by Aircraft Engines. Increases in U.S. export sales in 2002 were primarily in Plastics and Power Systems, partially offset by lower exports by Medical Systems and Transportation Systems.

GECS international revenues were $27.8 billion, $24.4 billion and $23.6 billion in 2003, 2002 and 2001, respectively. The $3.4 billion increase related to a 21% increase in Europe in 2003 as a result of the growth in premiums and price increases at Insurance ($2.1 billion), acquisitions ($1.0 billion) and the net effects of the weaker U.S. dollar ($0.7 billion), primarily at Consumer Finance and Commercial Finance, partially offset by geographic market exits at IT Solutions ($1.3 billion).

International operating profit was $8.8 billion in 2003, an increase of 35% over 2002, which was 7% higher than in 2001. Operating profit in 2003 rose 89% to $4.0 billion in Europe, primarily as a result of lower adverse development at Insurance ($1.1 billion). Operating profit also rose 30% to $1.5 billion in the Americas and was relatively unchanged in the Pacific Basin ($2.4 billion) and "Other international" ($0.9 billion).

Total assets of international operations were $258.9 billion in 2003 (40% of consolidated assets), an increase of $29.9 billion, or 13%, over 2002. GECS international assets grew 12% from $207.5 billion at the end of 2002 to $231.9 billion at the end of 2003. GECS assets increased 31% in Europe as a result of acquisitions ($14.8 billion), primarily at Consumer Finance and Commercial Finance, the net effects of the weaker U.S. dollar ($11.7 billion) and growth at Consumer Finance and Insurance. GECS assets increased 13% in the Americas as a result of growth at Commercial Finance and Insurance.

Financial results of our international activities reported in U.S. dollars are affected by currency exchange. We use a number of techniques to manage the effects of currency exchange, including selective borrowings in local currencies and selective hedging of significant cross-currency transactions. Such principal currencies are the British pound sterling, the euro, the Japanese yen and the Canadian dollar.

Environmental Matters

Our operations, like operations of other companies engaged in similar businesses, involve the use, disposal and cleanup of substances regulated under environmental protection laws.

We have developed environmental, health and safety management systems that are implemented at all of our facilities and track our performance. Since 1996, we have reduced employee injuries by over 70% as well as reducing air and wastewater exceedances and emissions at our facilities. We also actively participate in various programs that recognize facilities with health and safety programs that exceed legal requirements, including the United States Occupational Safety and Health Administration's Voluntary Protection Program (VPP) as well as a similar government program in Mexico. Participation in these programs requires government audits to verify our comprehensive health and safety management systems. We are a leading participant in the U.S. VPP program with 82 sites, and have an additional 25 sites participating in the Mexico program. We have a Global Star program designed to recognize sites with world-class health and safety programs in those countries without government VPP programs. The 44 Global Star sites have passed a rigorous evaluation conducted by GE internal health and safety experts. We also have 79 sites accredited by outside auditors under the ISO 14000 Standard for Environmental Management Systems.

56 GE 2003 ANNUAL REPORT

MANAGEMENT'S DISCUSSION AND ANALYSIS

Over the last two years we spent a total of about $0.1 billion for projects related to the environment. These amounts exclude expenditures for remediation actions, which are principally expensed and are discussed below. Capital expenditures for environmental purposes have included pollution control devices–such as wastewater treatment plants, groundwater monitoring devices, air strippers or separators, and incinerators–at new and existing facilities constructed or upgraded in the normal course of business. Consistent with policies stressing environmental responsibility, we expect our capital expenditures other than for remediation projects to total about $0.1 billion over the next two years for new or expanded programs to build facilities or modify manufacturing processes to minimize waste and reduce emissions.

We also are involved in a sizable number of remediation actions to clean up hazardous wastes as required by federal and state laws. Such statutes require that responsible parties fund remediation actions regardless of fault, legality of original disposal or ownership of a disposal site. Expenditures for site remediation actions amounted to $0.1 billion in each of the last two years. We presently expect that such remediation actions will require average annual expenditures in the range of $0.1 billion to $0.2 billion over the next two years.