Exhibit 99(b)

Complete Revised Management's Discussion and Analysis,

Other Financial Data and

Consolidated Financial Statements from Our 2014 Form 10-K.

Financial Statements in this Exhibit are Now Our Historical

Financial Statements

MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS (MD&A)

PRESENTATION

The consolidated financial statements of General Electric Company (the Company) combine the industrial manufacturing and services businesses of General Electric Company (GE) with the financial services businesses of General Electric Capital Corporation (GECC or financial services). Unless otherwise indicated by the context, we use the terms "GE" and "GECC" on the basis of consolidation described in Note 1 to the consolidated financial statements.

Net earnings of GECC and the effect of transactions between segments are eliminated to arrive at total consolidated data.

Prior to January 28, 2011, we operated a media company, NBC Universal, Inc. (NBCU). Effective January 28, 2011, we held a 49% interest in a media entity that included the NBC Universal businesses (NBCU LLC). On March 19, 2013, we completed the sale of our remaining 49% common equity interest to Comcast Corporation.

We integrate acquisitions as quickly as possible. Revenues and earnings from the date we complete the acquisition through the end of the following fourth quarter are considered the acquisition effect of such businesses.

Discussion of GECC's total assets excludes deferred income tax liabilities, which are presented within assets for purposes of our consolidating statement of financial position presentations for this filing.

See the Glossary section for a definition of equipment and services sales as used in this MD&A as compared to the product and services split on the Statement of Earnings.

Amounts reported in billions in graphs and tables within MD&A are computed based on the amounts in millions. As a result, the sum of the components reported in billions may not equal the total amount reported in billions due to rounding. Discussions throughout this MD&A are based on continuing operations unless otherwise noted.

THE GE CAPITAL EXIT PLAN

The sale of the Real Estate business and most of our CLL business is part of a plan (the GE Capital Exit Plan) that is described below. Information in our 2014 annual financial statements and related Management's Discussion and Analysis has not been updated to reflect aspects of the GE Capital Exit Plan, other than the required reclassification of the Real Estate business and most of our CLL business to discontinued operations. For example, we have not updated such financial information for the effects of the GE Capital Exit Plan as it relates to our strategy to achieve a certain percentage of our operating earnings from industrial businesses, our ending net investment (ENI) reduction targets, our expected repatriation of non-U.S. earnings, our liquidity and borrowings plans or debt rating changes. For additional information about our discontinued Real Estate business and most of our CLL business, refer to our 2014 Form 10-K.

Page 1

On April 10, 2015, the Company announced the GE Capital Exit Plan to reduce the size of its financial services businesses through the sale of most of the assets of GECC over the following 24 months, and to focus on continued investment and growth in the Company's industrial businesses. Under the GE Capital Exit Plan, which was approved on April 2, 2015 and aspects of which were approved on March 31, 2015, the Company will retain certain GECC businesses, principally its vertical financing businesses—GE Capital Aviation Services (GECAS), Energy Financial Services and Healthcare Equipment Finance—that directly relate to the Company's core industrial domain and other operations, including Working Capital Solutions and our run-off insurance activities. The assets planned for disposition include Real Estate, most of CLL and all Consumer platforms (including all U.S. banking assets). The Company expects to execute this strategy using an efficient approach for exiting non-vertical assets that works for the Company's and GECC's debt holders and the Company's shareowners. An element of this approach involves a merger of GECC into the Company to assure compliance with debt covenants as GECC exits non-vertical assets, and the creation of a new intermediate holding company to hold GECC's businesses after the merger. The Company has discussed the GE Capital Exit Plan, aspects of which are subject to regulatory review and approval, with its regulators and staff of the Financial Stability Oversight Council (FSOC) and will work closely with these bodies to take the actions necessary over time to terminate the FSOC's designation of GECC (and the new intermediate holding company, as applicable) as a nonbank systemically important financial institution (nonbank SIFI).

As part of the GE Capital Exit Plan, we agreed to sell the substantial majority of GECC's Real Estate debt and equity portfolio to funds managed by The Blackstone Group (which, at closing, intends to sell a portion of this portfolio to Wells Fargo & Company), and also have letters of intent with other buyers for the majority of the remaining commercial real estate assets. In total, these deals are valued at approximately $26.5 billion.

As part of the GE Capital Exit Plan, on April 10, 2015, the Company and GECC entered into an amendment to their existing financial support agreement. Under this amendment (the Amendment), the Company has provided a full and unconditional guarantee (the Guarantee) of the payment of principal and interest on all tradable senior and subordinated outstanding long-term debt securities and all commercial paper issued or guaranteed by GECC identified in the Amendment. In the aggregate, the Guarantee applied to approximately $210 billion of GECC debt as of April 10, 2015. The Guarantee replaced the requirement that the Company make certain income maintenance payments to GECC in certain circumstances. GECC's U.S. public indentures were concurrently amended to provide the full and unconditional guarantee by the Company set forth in the Guarantee.

In connection with the GE Capital Exit Plan, the Company estimates it will incur approximately $23 billion in after-tax charges through 2016, approximately $6 billion of which are expected to result in future net cash expenditures. These charges are expected to relate to: business dispositions, including goodwill allocations (approximately $13 billion), tax expense related to expected repatriation of foreign earnings and write-off of deferred tax assets (approximately $7 billion), and restructuring and other charges (approximately $3 billion).

In the first and second quarters of 2015, GE recorded $16.1 billion and $4.6 billion, respectively, of after-tax charges related to the GE Capital Exit Plan. As a result of certain businesses meeting discontinued operations criteria, $6.7 billion of first quarter after-tax charges and $4.4 billion of second quarter after-tax charges (including $4.3 billion related to CLL) were reported in discontinued operations.

As a result of the GE Capital Exit Plan, GE's consolidated financial statements reflect GECC's Real Estate business and most of CLL business as discontinued operations, including reclassification of all comparative prior period information.

REFERENCES

The MD&A should be read in conjunction with the Financial Statements and Notes to the consolidated financial statements.

Page 2

NON-GAAP FINANCIAL MEASURES

We use certain "non-GAAP financial measures" throughout the MD&A. The reasons we use these non-GAAP financial measures and the reconciliations to their most directly comparable GAAP financial measures are included in the "Supplemental Information" section within the MD&A. Specifically, we have referred, in various sections of the MD&A, to:

| · | Operating earnings and operating EPS |

| · | Industrial operating earnings |

| · | Industrial segment organic revenue growth |

| · | Industrial cash flows from operating activities (Industrial CFOA) |

| · | Operating and non-operating pension costs (income) |

| · | GE pre-tax earnings from continuing operations, excluding GECC earnings from continuing operations and the corresponding effective tax rates |

| · | GE Capital ending net investment (ENI), excluding liquidity |

| · | GECC Tier 1 common ratio estimate |

Non-GAAP financial measures referred to within the MD&A are designated with an asterisk (*).

Page 3

KEY PERFORMANCE INDICATORS

(Dollars in billions; per-share amounts in dollars)

| REVENUES PERFORMANCE | EARNINGS PER SHARE | ||||

¢ ¢ Earnings ¢ ¢ Operating Earnings*  | |||||

| 2013 | 2014 | ||||

| Industrial Segment | 1% | 6% | |||

Industrial Segment Organic* | Flat | 7% | |||

Financial Services | 2% | (2)% | |||

INDUSTRIAL SEGMENT PROFIT | INDUSTRIAL SEGMENT MARGIN | ||||

|  | ||||

INDUSTRIAL ORDERS | INDUSTRIAL BACKLOG(a) | ||||

| Equipment Services |  (a)Periods reflect an update for Oil & Gas services backlog | Equipment Services | ||

*Non-GAAP Financial Measure

Page 4

KEY PERFORMANCE INDICATORS

(Dollars in billions)

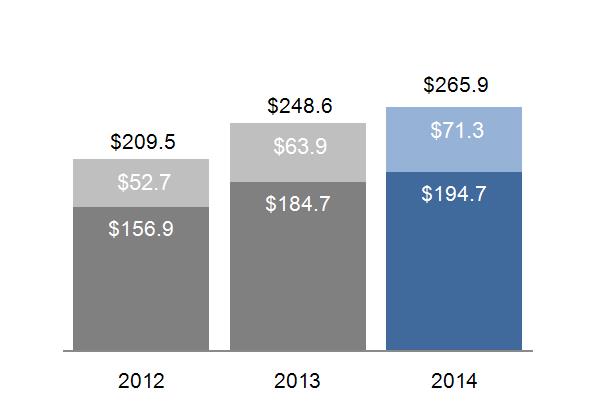

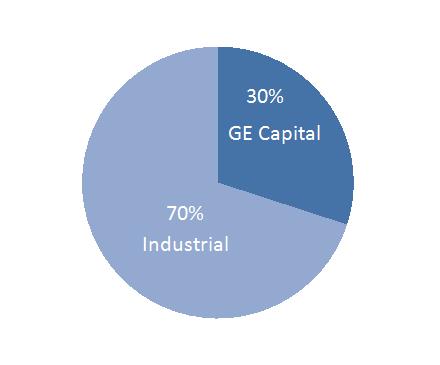

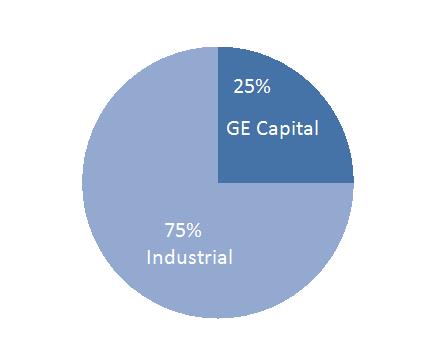

| INDUSTRIAL/GE CAPITAL OPERATING EARNINGS* | |||

2014 Actual*  | GE IS EXECUTING ON ITS STRATEGY TO ACHIEVE 75% OF ITS OPERATING EARNINGS FROM ITS INDUSTRIAL BUSINESSES BY 2016. The effects of the Synchrony Financial split-off and the Alstom acquisition and alliances will result in progression towards this target. | ||

2016 Goal  | |||

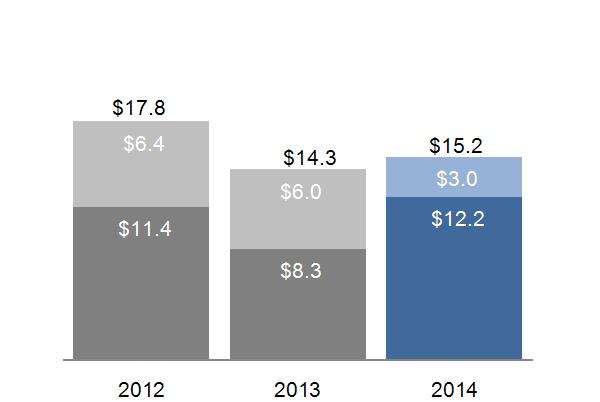

| GE CFOA | SHAREHOLDER INFORMATION | ||

¢ ¢ Industrial* ¢ ¢ GECC Dividend  | GECC Dividend Industrial CFOA* | RETURNED $10.8 BILLION TOSHAREOWNERS IN 2014 Dividends $8.9 billion Stock buyback $1.9 billion ANNUAL MEETING General Electric's 2015 Annual Meeting of Shareowners will be held on April 22, 2015, in Oklahoma City, Oklahoma. | |

| 2013 GE CFOA excluding NBC Universal deal-related taxes was $17.4 billion* | |||

*Non-GAAP Financial Measure

Page 5

KEY PERFORMANCE INDICATORS

(Amounts in dollars)

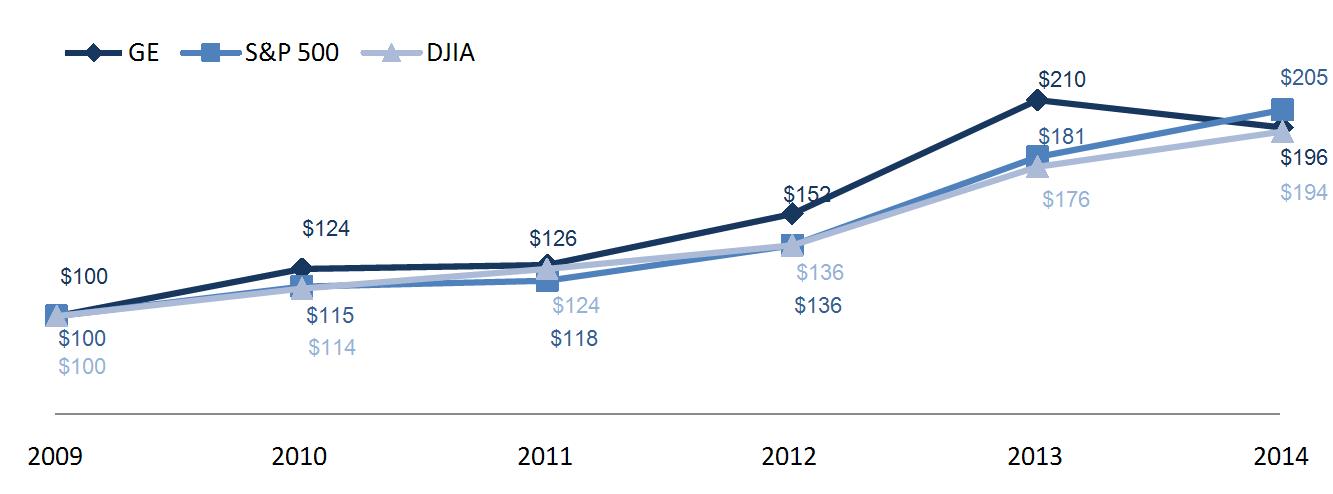

| FIVE-YEAR PERFORMANCE GRAPH |

|

The annual changes for the five-year period shown in the graph on this page are based on the assumption that $100 had been invested in General Electric common stock, the Standard & Poor's 500 Stock Index (S&P 500) and the Dow Jones Industrial Average (DJIA) on December 31, 2009, and that all quarterly dividends were reinvested. The total cumulative dollar returns shown on the graph represent the value that such investments would have had on December 31, 2014.

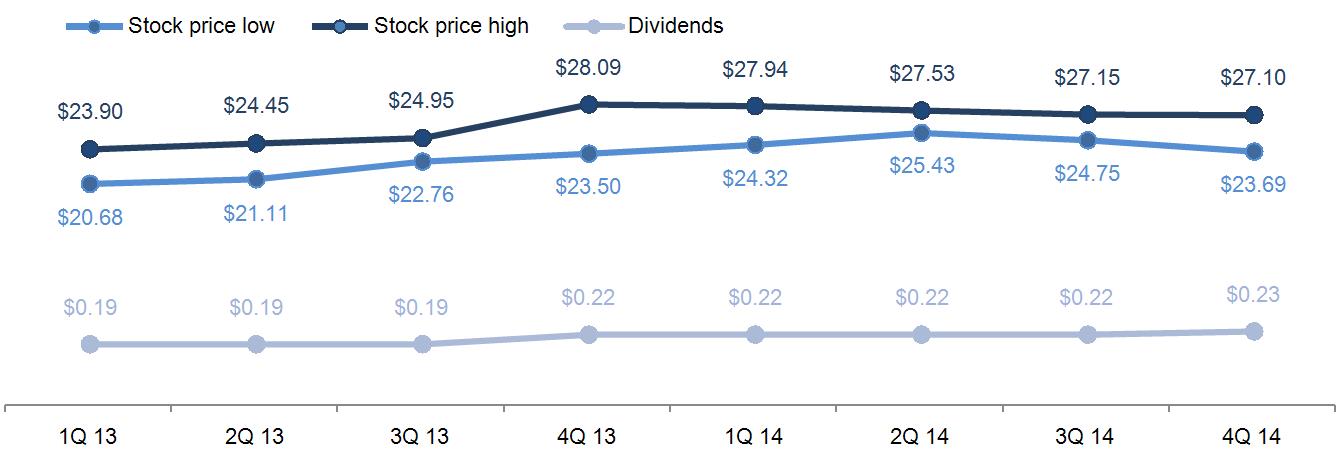

| STOCK PRICE RANGE AND DIVIDENDS |

|

With respect to "Market Information," in the United States, General Electric common stock is listed on the New York Stock Exchange (its principal market). General Electric common stock is also listed on the London Stock Exchange and the Frankfurt Stock Exchange. The chart above shows trading prices, as reported on the New York Stock Exchange, Inc., Composite Transactions Tape.

As of January 31, 2015, there were approximately 480,000 shareowner accounts of record.

On February 6, 2015, our Board of Directors approved a quarterly dividend of $0.23 per share of common stock, which is payable April 27, 2015, to shareowners of record at close of business on February 23, 2015.

Page 6

CONSOLIDATED RESULTS

(Dollars in billions)

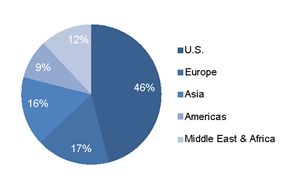

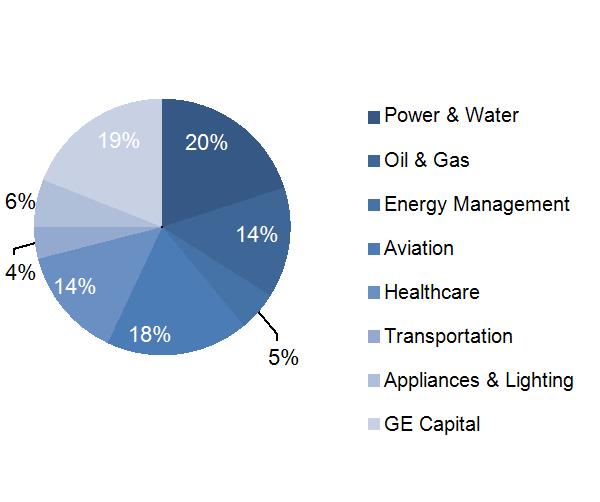

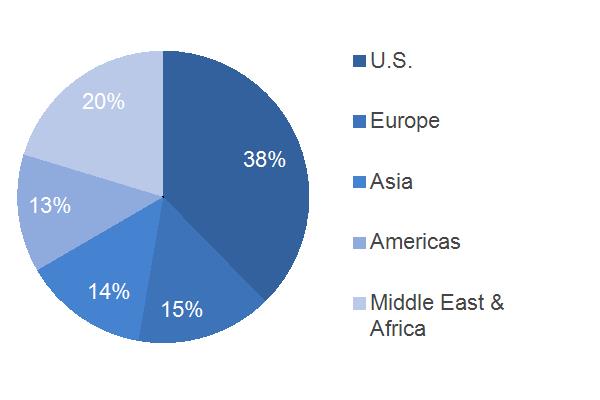

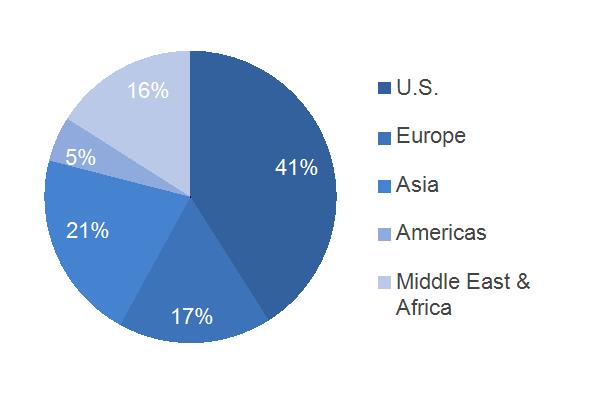

2014 GEOGRAPHIC REVENUES | 2014 SEGMENT REVENUES | |

|  |

| SIGNIFICANT DEVELOPMENTS IN 2014 | |||

| We completed the initial public offering of our North American Retail Finance business, Synchrony Financial, resulting in proceeds of $2.8 billion and target to complete the exit through a split-off transaction. We sold GE Money Bank AB, our consumer finance business in Sweden, Denmark and Norway to Santander for $2.3 billion. We acquired Milestone Aviation Group for approximately $1.8 billion on January 30, 2015. We signed an agreement to sell our consumer finance business in Hungary (Budapest Bank) to Hungary's government. | ||

| We agreed to sell our Appliances business to Electrolux for $3.3 billion; targeted to close in mid-2015. | ||

| We acquired Cameron's Reciprocating Compression division for $0.6 billion. | ||

| We acquired API Healthcare for $0.3 billion and certain Thermo Fisher Scientific Inc. life-science businesses for $1.1 billion. | ||

| We signed an agreement to sell our Signaling business to Alstom for approximately $0.8 billion. | ||

| We offered to acquire the Thermal, Renewables and Grid businesses of Alstom. The proposed transaction is targeted to close in 2015. See the "Segment Operations" section within the MD&A for additional information related to the proposed transaction. | ||

Page 7

CONSOLIDATED RESULTS

(Dollars in billions)

REVENUES | INDUSTRIAL SEGMENT EQUIPMENT & SERVICES REVENUES | ||

|  | Equipment Services | |

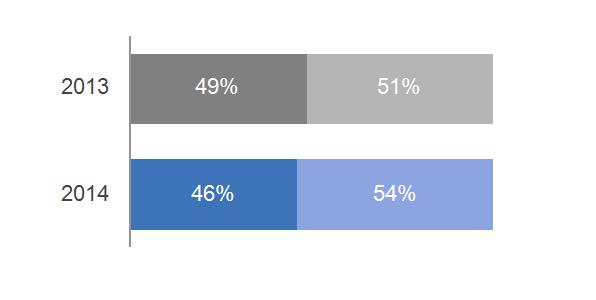

COMMENTARY: 2014 – 2013 | 2013 – 2012 | ||

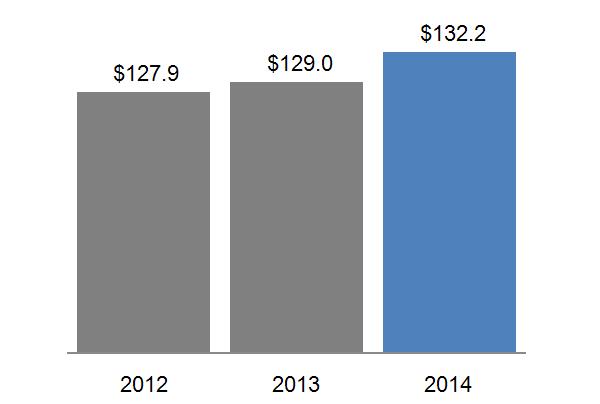

Consolidated revenues increased $3.2 billion, or 2%. ·Industrial segment revenues increased 6%, reflecting organic growth* of 7% and the effects of acquisitions (primarily Lufkin Industries, Inc. (Lufkin), Avio S.p.A. (Avio) and certain Thermo Fisher Scientific Inc. businesses). ·Financial Services revenues decreased 2% as a result of the effects of dispositions, lower gains and the effects of currency exchange, partially offset by organic revenue growth and lower impairments. ·Other income decreased $2.3 billion, primarily due to the sale of our remaining 49% common equity interest in NBCU LLC in 2013 ($1.6 billion). ·The effects of acquisitions increased consolidated revenues $1.7 billion and $1.6 billion in 2014 and 2013, respectively. Dispositions affected our ongoing results through lower revenues of $4.0 billion in 2014 and an increase of $0.1 billion in 2013. ·The effects of a stronger U.S. dollar compared to mainly the Japanese yen, Canadian dollar, and Brazilian real, partially offset by the British pound, decreased consolidated revenues by $0.8 billion. | Consolidated revenues increased $1.1 billion, or 1%. ·Industrial segment revenues increased 1%. Organic revenue growth* was flat. ·Financial Services revenues increased 2%, as a result of higher gains, the effects of dispositions and lower impairments, partially offset by organic revenue declines. ·Other income increased $0.5 billion, primarily due to gains related to the sale of NBCU LLC. ·The effects of acquisitions increased consolidated revenues $1.6 billion and $2.0 billion in 2013 and 2012, respectively. Dispositions affected our ongoing results through an increase of $0.1 billion in 2013 and lower revenues of $4.6 billion in 2012. ·The effects of a stronger U.S. dollar compared to mainly the Japanese yen and Brazilian real, partially offset by the euro, decreased consolidated revenues by $0.5 billion. | ||

*Non-GAAP Financial Measure

Page 8

CONSOLIDATED RESULTS

(Dollars in billions)

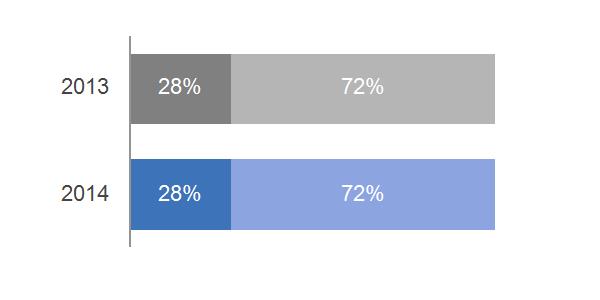

EARNINGS | INDUSTRIAL SELLING, GENERAL & ADIMINSTRATIVE (SG&A) AS A % OF SALES | |

¢ ¢ Earnings ¢ ¢ Operating Earnings*  |  | |

COMMENTARY: 2014 – 2013 | 2013 – 2012 | |

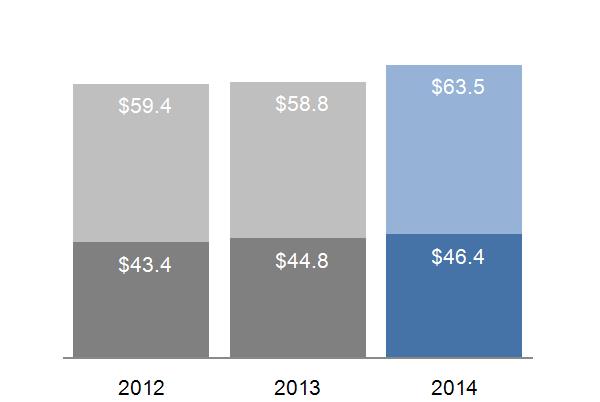

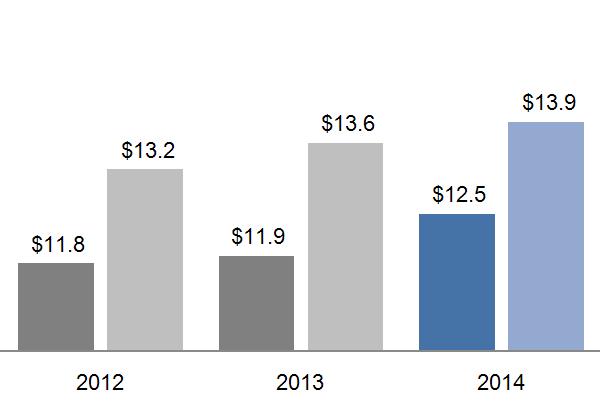

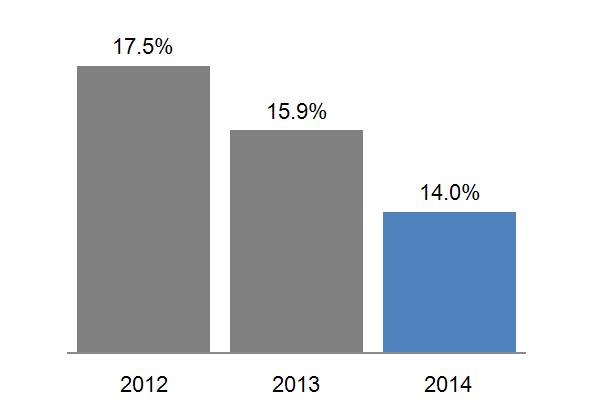

Consolidated earnings increased 5% primarily due to an increase in the operating profit of the industrial segments, partially offset by lower financial services income and the absence of the NBCU LLC related income. ·Industrial segment profit increased 10% with growth driven by Aviation, Oil & Gas and Power & Water. ·Industrial segment margin increased 50 basis points (bps) driven by higher productivity and pricing, partially offset by negative business mix and the effects of inflation. ·Financial Services earnings decreased 10% as a result of the effects of dispositions, lower gains and the effects of currency exchange, partially offset by lower impairments, lower provisions for losses on financing receivables and core increases. ·The effects of acquisitions on our consolidated net earnings were increases of $0.2 billion and $0.1 billion in 2014 and 2013, respectively. The effects of dispositions on net earnings were a decrease of $2.4 billion in 2014 and an increase of $1.3 billion in 2013. ·Industrial SG&A as a percentage of total sales decreased to 14.0% as a result of global cost reduction initiatives, primarily at Power & Water and Healthcare. This was partially offset by higher acquisition-related costs. | Consolidated earnings increased 1% primarily due to a decrease in financial services, partially offset by strong industrial segment growth. ·Industrial segment profit increased 5% with growth driven by Aviation and Oil & Gas. ·Industrial segment margin increased 60 bps driven by higher pricing and favorable business mix, partially offset by the effects of inflation. ·Financial Services earnings increased 6%, as a result of the effects of dispositions and higher gains, partially offset by higher provisions for losses on financing receivables, core decreases and higher impairments. ·The effects of acquisitions on our consolidated net earnings were increases of $0.1 billion in both 2013 and 2012. The effects of dispositions on net earnings were an increase of $1.3 billion in 2013 and a decrease of $0.2 billion in 2012. ·Industrial SG&A as a percentage of total sales decreased to 15.9% as a result of global cost reduction initiatives related to simplification efforts both in the industrial segments and corporate. This was partially offset by increased acquisition-related costs and higher restructuring. |

See the "Other Consolidated Information" section within the MD&A for a discussion of postretirement benefit plans costs, income taxes and geographic data.

*Non-GAAP Financial Measure

Page 9

SEGMENT OPERATIONS

SEGMENT REVENUES AND PROFIT

Segment revenues include both revenues and other income related to the segment.

Segment profit is determined based on internal performance measures used by the Chief Executive Officer (CEO) to assess the performance of each business in a given period. In connection with that assessment, the CEO may exclude matters such as charges for restructuring; rationalization and other similar expenses; acquisition costs and other related charges; technology and product development costs; certain gains and losses from acquisitions or dispositions; and litigation settlements or other charges, for which responsibility preceded the current management team.

Segment profit excludes results reported as discontinued operations and accounting changes. Segment profit also excludes the portion of earnings or loss attributable to noncontrolling interests of consolidated subsidiaries, and as such only includes the portion of earnings or loss attributable to our share of the consolidated earnings or loss of consolidated subsidiaries.

Segment profit excludes or includes interest and other financial charges and income taxes according to how a particular segment's management is measured:

| · | Interest and other financial charges and income taxes are excluded in determining segment profit (which we sometimes refer to as "operating profit") for the industrial segments. |

| · | Interest and other financial charges and income taxes are included in determining segment profit (which we sometimes refer to as "net earnings") for the GE Capital segment. |

Certain corporate costs, such as shared services, employee benefits and information technology are allocated to our segments based on usage. A portion of the remaining corporate costs are allocated based on each segment's relative net cost of operations.

Effective in the second quarter of 2014, we began including the effects of the GECC preferred stock dividends in our GE Capital segment. Previously, such dividends had been reported in the caption "Corporate items and eliminations" in the Company's Summary of Operating Segments table. Presenting GE Capital segment results including the effects of the GECC preferred stock dividends is consistent with the way management measures the results of our financial services business. Prior-period segment information has been recast to be consistent with how we currently evaluate the performance of the GE Capital segment.

POTENTIAL ACQUISITIONS IMPACTING MULTIPLE SEGMENTS

GE's offer to acquire the Thermal, Renewables and Grid businesses of Alstom for approximately €12.4 billion (to be adjusted for the assumed net cash or liability at closing) was positively recommended by Alstom's board of directors. In addition, GE, Alstom and the French Government signed a memorandum of understanding for the formation of three joint ventures in grid technology, renewable energy, and global nuclear and French steam power and Alstom will invest approximately €2.6 billion in these joint ventures. In the fourth quarter of 2014, Alstom completed its review of the proposed transaction with the works council and obtained approval from its shareholders. Also in the fourth quarter of 2014, GE and Alstom entered into an amendment to the original agreement where GE has agreed to pay Alstom a net amount of approximately €0.3 billion of additional consideration at closing. In exchange for this funding, Alstom has agreed to extend the trademark licensing of the Alstom name from 5 years to 25 years as well as other contractual amendments. The proposed transaction continues to be subject to regulatory approvals. The transaction is targeted to close in 2015. The acquisition and alliances will impact our Power & Water and Energy Management segments.

Page 10

| SUMMARY OF OPERATING SEGMENTS | ||||||||||||||

| General Electric Company and consolidated affiliates | ||||||||||||||

| (In millions) | 2014 | 2013 | 2012 | 2011 | 2010 | |||||||||

| Revenues | ||||||||||||||

| Power & Water | $ | 27,564 | $ | 24,724 | $ | 28,299 | $ | 25,675 | $ | 24,779 | ||||

| Oil & Gas | 18,676 | 16,975 | 15,241 | 13,608 | 9,433 | |||||||||

| Energy Management | 7,319 | 7,569 | 7,412 | 6,422 | 5,161 | |||||||||

| Aviation | 23,990 | 21,911 | 19,994 | 18,859 | 17,619 | |||||||||

| Healthcare | 18,299 | 18,200 | 18,290 | 18,083 | 16,897 | |||||||||

| Transportation | 5,650 | 5,885 | 5,608 | 4,885 | 3,370 | |||||||||

| Appliances & Lighting | 8,404 | 8,338 | 7,967 | 7,693 | 7,957 | |||||||||

| Total industrial segment revenues | 109,902 | 103,602 | 102,811 | 95,225 | 85,216 | |||||||||

| GE Capital | 26,344 | 27,008 | 26,571 | 28,330 | 28,848 | |||||||||

| Total segment revenues | 136,246 | 130,610 | 129,382 | 123,555 | 114,064 | |||||||||

| Corporate items and eliminations | (4,038) | (1,624) | (1,491) | 2,993 | 14,496 | |||||||||

| Consolidated revenues | $ | 132,208 | $ | 128,986 | $ | 127,891 | $ | 126,548 | $ | 128,560 | ||||

| Segment profit | ||||||||||||||

| Power & Water | $ | 5,352 | $ | 4,992 | $ | 5,422 | $ | 5,021 | $ | 5,804 | ||||

| Oil & Gas | 2,585 | 2,178 | 1,924 | 1,660 | 1,406 | |||||||||

| Energy Management | 246 | 110 | 131 | 78 | 156 | |||||||||

| Aviation | 4,973 | 4,345 | 3,747 | 3,512 | 3,304 | |||||||||

| Healthcare | 3,047 | 3,048 | 2,920 | 2,803 | 2,741 | |||||||||

| Transportation | 1,130 | 1,166 | 1,031 | 757 | 315 | |||||||||

| Appliances & Lighting | 431 | 381 | 311 | 237 | 404 | |||||||||

| Total industrial segment profit | 17,764 | 16,220 | 15,486 | 14,068 | 14,130 | |||||||||

| GE Capital | 4,208 | 4,696 | 4,410 | 4,996 | 3,498 | |||||||||

| Total segment profit | 21,972 | 20,916 | 19,896 | 19,064 | 17,628 | |||||||||

| Corporate items and eliminations | (6,225) | (6,002) | (4,718) | (288) | (1,012) | |||||||||

| GE interest and other financial charges | (1,579) | (1,333) | (1,353) | (1,299) | (1,600) | |||||||||

| GE provision for income taxes | (1,634) | (1,668) | (2,013) | (4,839) | (2,024) | |||||||||

| Earnings from continuing operations | ||||||||||||||

| attributable to the Company | 12,534 | 11,913 | 11,812 | 12,638 | 12,992 | |||||||||

| Earnings (loss) from discontinued | ||||||||||||||

| operations, net of taxes | 2,699 | 1,144 | 1,829 | 1,513 | (1,348) | |||||||||

| Consolidated net earnings | ||||||||||||||

| attributable to the Company | $ | 15,233 | $ | 13,057 | $ | 13,641 | $ | 14,151 | $ | 11,644 | ||||

Page 11

POWER & WATER

POWER & WATERBUSINESS OVERVIEW

Leader: Steve Bolze | Headquarters & Operations | |||

| ·Senior Vice President (SVP) and President & CEO, GE Power & Water ·Over 20 years of service with General Electric |  | ·20% of segment revenues in 2014 ·25% of industrial segment revenues ·30% of industrial segment profit ·Headquarters: Schenectady, NY ·Serving customers in125+ countries ·Employees: approximately 38,000 | |

| Products & Services | |||

| Power & Water serves power generation, industrial, government and other customers worldwide with products and services related to energy production and water reuse. Our products and technologies harness resources such as wind, oil, gas, diesel, nuclear and water to produce electric power. | ||

| · | Power Generation Products and Services (PGP and PGS) – offers a wide spectrum of heavy-duty gas turbines and supplies machines and services for utilities, independent power producers, and industrial application, from pure power generation to cogeneration and district heating. |

| · | Renewable Energy – primarily our Wind business, which manufactures wind turbines and provides support services ranging from development assistance to operation and maintenance. |

| · | Distributed Power – provides technology-based products to generate reliable and efficient power at or near the point of use. The product portfolio features aero derivative gas turbines, Jenbacher gas engines, and Waukesha gas engines. |

| · | Water Process Technologies – provides water treatment, wastewater treatment and process system solutions. |

| · | Nuclear – offers advanced reactor technologies solutions, including reactors, fuels and support services for boiling water reactors, and is offered through joint ventures with Hitachi and Toshiba, for safety, reliability and performance for nuclear fleets. |

| Competition & Regulation |

Worldwide competition for power generation products and services is intense. Demand for power generation is global and, as a result, is sensitive to the economic and political environments of each country in which we do business.

Our Wind business is subject to certain global policies and regulation including the U.S. Production Tax Credit and incentive structures in China and various European countries. Changes in such policies may create unknown impacts or opportunities for the business.

Page 12

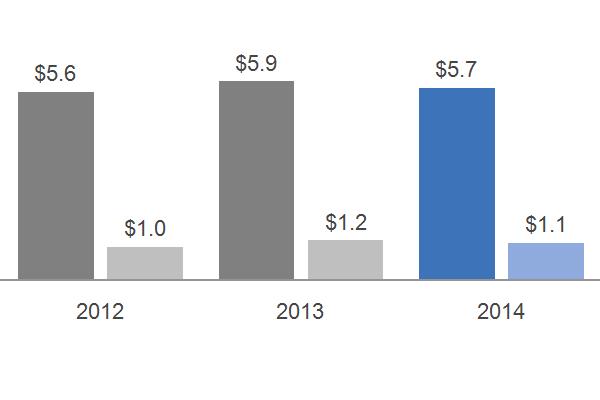

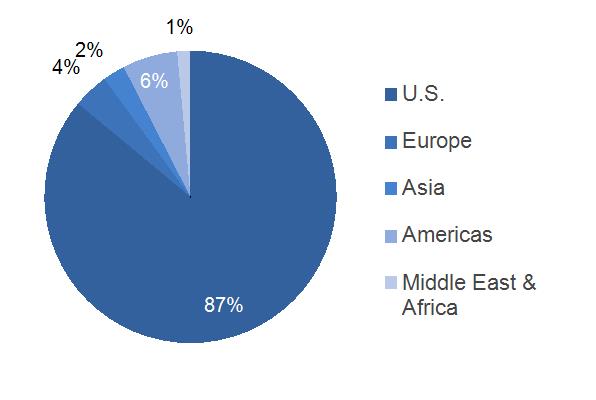

OPERATIONAL OVERVIEW

(Dollars in billions)

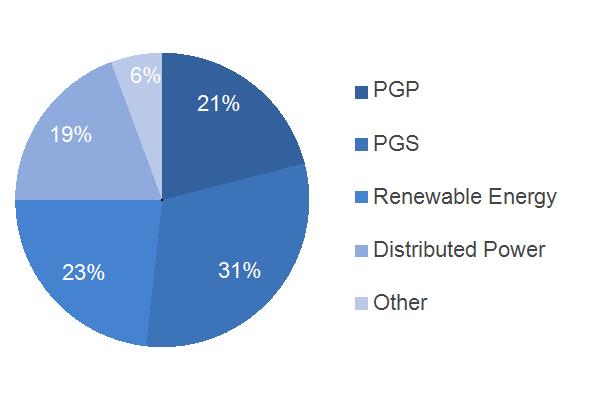

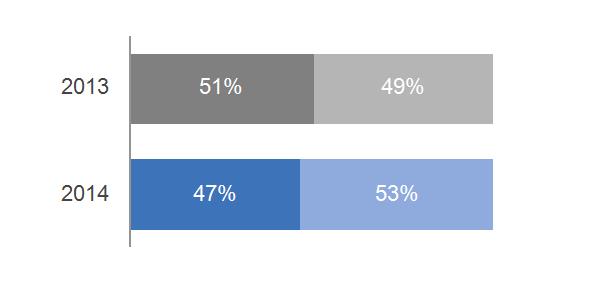

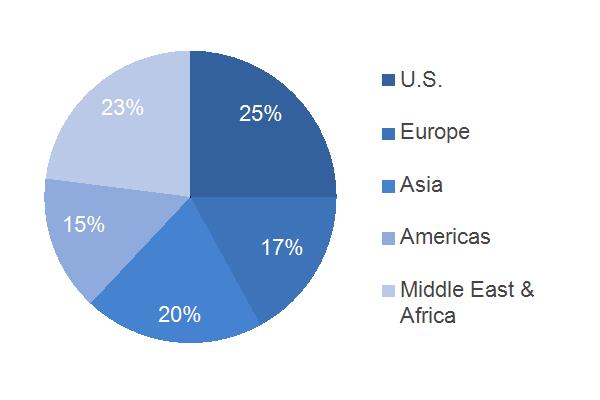

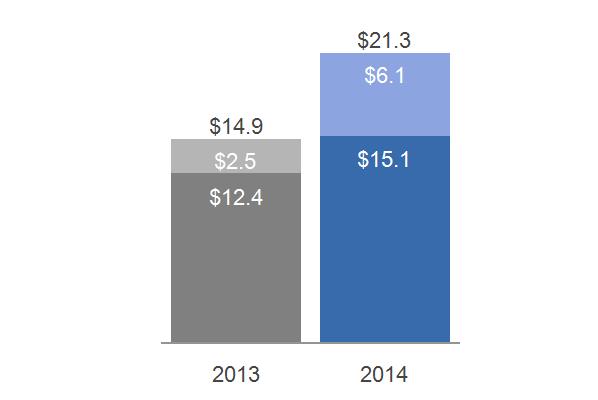

| 2014 GEOGRAPHIC REVENUES: $27.6 BILLION | ORDERS | ||

|  | Equipment Services | |

| 2014 SUB-SEGMENT REVENUES | BACKLOG | ||

|  | Equipment Services | |

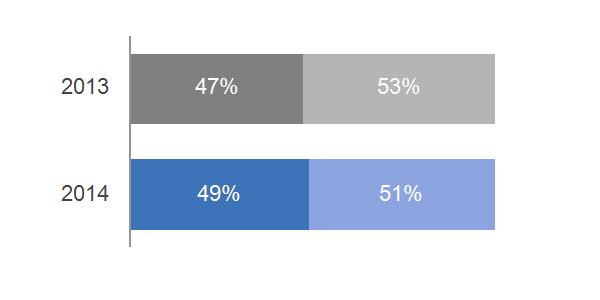

| EQUIPMENT/SERVICES REVENUES | UNIT SALES | ||

|  | ||

| Services Equipment | |||

| SIGNIFICANT TRENDS & DEVELOPMENTS |

| · | The Alstom transaction is expected to advance our strategic priorities and industrial growth. Alstom's Thermal and Renewables businesses are complementary in technology, operations and geography to our business. We expect the integration to yield efficiencies in supply chain, service infrastructure, new product development and SG&A. |

| · | The business continues to invest in new product development, such as our new H-Turbine, larger wind turbines and advanced upgrades, to expand our equipment and services offerings. |

| · | Excess capacity in developed markets and macroeconomic and geopolitical environments result in uncertainty for the industry and business. |

Page 13

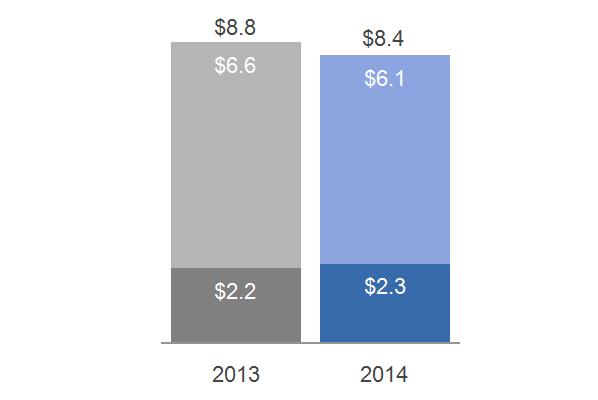

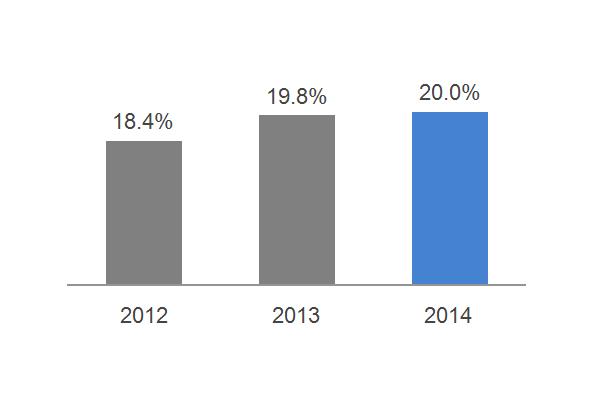

FINANCIAL OVERVIEW

(Dollars in billions)

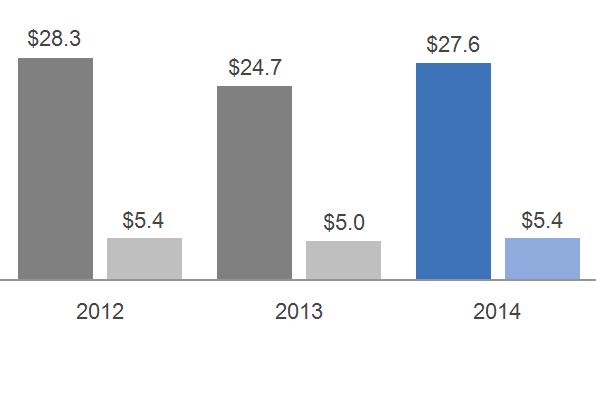

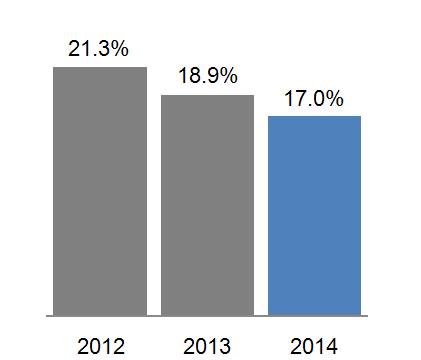

| SEGMENT REVENUES & PROFIT | SEGMENT PROFIT MARGIN | |||||

¢ ¢ Revenue ¢ ¢ Profit  |  | |||||

| SEGMENT REVENUES & PROFIT WALK: | COMMENTARY: | |||||

| 2014 – 2013 | 2014 – 2013 | |||||

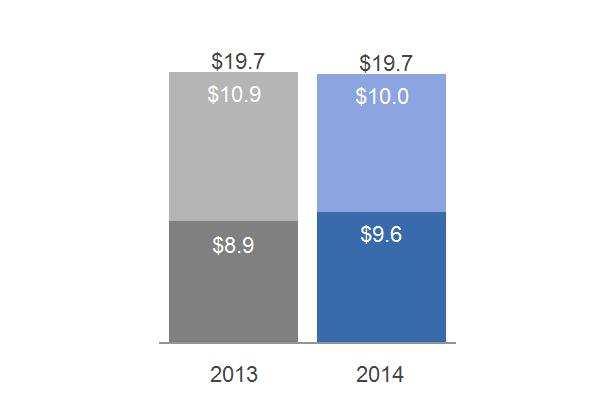

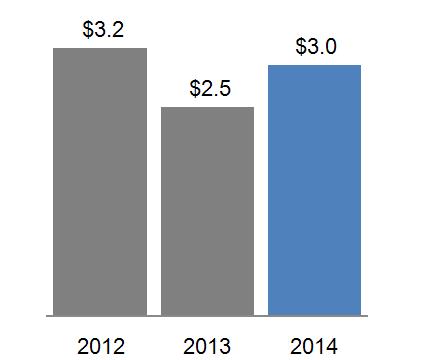

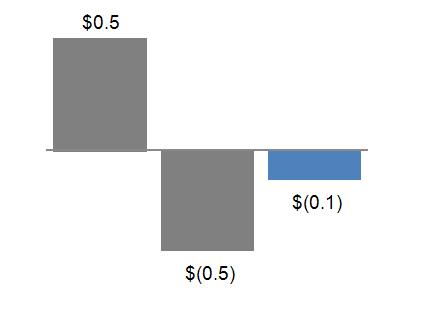

Segment revenues up $2.8 billion (11%); Segment profit up $0.4 billion (7%) as a result of: ·The increase in revenues was driven by higher volume, primarily higher equipment sales at PGP and Renewables, partially offset by lower prices at PGP and Renewables and the impact of a stronger U.S. dollar. ·The increase in profit was mainly due to the higher volume at PGP and Renewables, and higher productivity reflecting a 10% reduction in SG&A cost, partially offset by negative business mix with equipment revenue up 20% and lower prices. | ||||||

| Revenues | Profit | |||||

| 2013 | $ | 24.7 | $ | 5.0 | ||

| Volume | 3.7 | 0.7 | ||||

| Price | (0.4) | (0.4) | ||||

| Foreign Exchange | (0.2) | - | ||||

| (Inflation)/Deflation | N/A | 0.1 | ||||

| Mix | N/A | (0.5) | ||||

| Productivity | N/A | 0.7 | ||||

| Other | (0.2) | (0.2) | ||||

| 2014 | $ | 27.6 | $ | 5.4 | ||

| 2013 – 2012 | 2013 – 2012 | |||||

Segment revenues down $3.6 billion (13%); Segment profit down $0.4 billion (8%) as a result of: ·The decrease in revenues was driven by lower volume, primarily equipment sales at PGP and Renewables, and the impact of a stronger U.S. dollar. These decreases were partially offset by higher prices and higher other income related to a sale of assets. ·The decrease in profit was mainly due to lower volume, primarily equipment sales at PGP and Renewables, and lower productivity despite decreases in SG&A cost. These decreases were partially offset by positive business mix, the effects of deflation, higher prices and higher other income. | ||||||

| Revenues | Profit | |||||

| 2012 | $ | 28.3 | $ | 5.4 | ||

| Volume | (3.9) | (0.7) | ||||

| Price | 0.2 | 0.2 | ||||

| Foreign Exchange | (0.1) | - | ||||

| (Inflation)/Deflation | N/A | 0.2 | ||||

| Mix | N/A | 0.3 | ||||

| Productivity | N/A | (0.6) | ||||

| Other | 0.2 | 0.2 | ||||

| 2013 | $ | 24.7 | $ | 5.0 | ||

Page 14

OIL & GAS

OIL & GASBUSINESS OVERVIEW

Leader: Lorenzo Simonelli | Headquarters & Operations | |||||

| ·President & CEO, GE Oil & Gas ·20 years of service with General Electric |  | ·14% of segment revenues in 2014 ·17% of industrial segment revenues ·15% of industrial segment profit ·HQ: London, UK ·Serving customers in 150+ countries ·Employees: approximately 44,000 | |||

| Products & Services | ||||||

| Oil & Gas serves all segments of the oil and gas industry, from drilling, completion, production and oil field operations, to transportation via liquefied natural gas (LNG) and pipelines. In addition, Oil & Gas provides industrial power generation and compression solutions to the refining and petrochemicals segments. Oil & Gas also delivers pipeline integrity solutions and a wide range of sensing, inspection and monitoring technologies. Oil & Gas exploits technological innovation from other GE businesses, such as Aviation and Healthcare, to continuously improve oil and gas industry performance, output and productivity. |

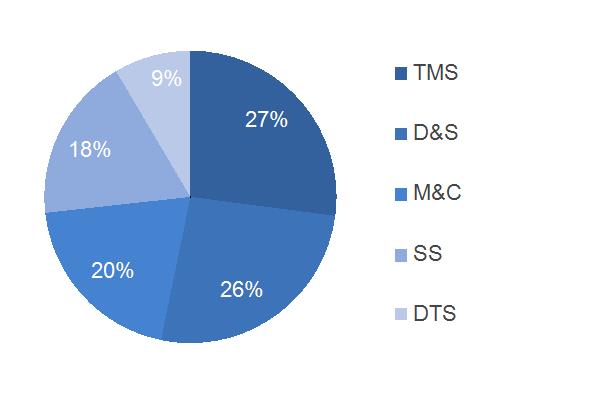

| · | Turbomachinery Solutions (TMS) – provides equipment and related services for mechanical-drive, compression and power-generation applications across the oil and gas industry. Our designs deliver high capacities and efficiencies, increase product flow and decrease both operational and environmental risks in the most extreme conditions, pressures and temperatures. Our portfolio includes drivers (aero-derivative gas turbines, heavy-duty gas turbines and synchronous and induction electric motors), compressors (centrifugal and axial, direct drive high speed, integrated, subsea compressors and turbo expanders), and turn-key solutions (industrial modules and waste heat recovery). |

| · | Drilling & Surface (D&S) – provides drilling, completion and production products and services for onshore & offshore oil & gas wells, and manufactures artificial lift equipment for well production and gears. The products & services portfolio includes blowout preventers, choke valves, drilling systems, drill stem valves, elastomers, pulsation dampeners wellheads, and surface production equipment. |

| · | Measurement & Controls (M&C) – provides equipment and services for a wide range of industries, including oil & gas, power generation, aerospace, metals, and transportation. The offerings include sensor-based measurement; non-destructive testing and inspection; flow and process control; turbine, generator and plant controls and condition monitoring, as well as pipeline integrity solutions. |

| · | Subsea Systems (SS) – offers our customers equipment and services for subsea well completion and production and integrated systems for enhanced recovery and comprehensive well lifecycle support. From new subsea field design and installation to mature field intervention and enhancement, SS offers all the equipment and expertise needed to safely and reliably maximize long-term resource value and overall efficiency. Specific products include flow control valves (known as "Christmas trees"), pressure control systems, wellheads, manifolds, integrated work over control systems and flexible subsea risers. |

| · | Downstream Technology Solutions (DTS) – provides products and services to serve the downstream segments of the industry including refining, petrochemical, distributed gas, and other industrial applications. Products include steam turbines, reciprocating and centrifugal compressors, blowers, pumps, valves, and compressed natural gas (CNG) and small-scale LNG solutions used primarily for shale oil and gas field development. |

| Competition & Regulation |

Demand for oil and gas equipment and services is global and, as a result, is sensitive to the economic and political environment of each country in which we do business. We are subject to the regulatory bodies of the countries in which we operate. Our products are subject to regulation by U.S. and non-U.S. energy policies.

Page 15

OPERATIONAL OVERVIEW

(Dollars in billions)

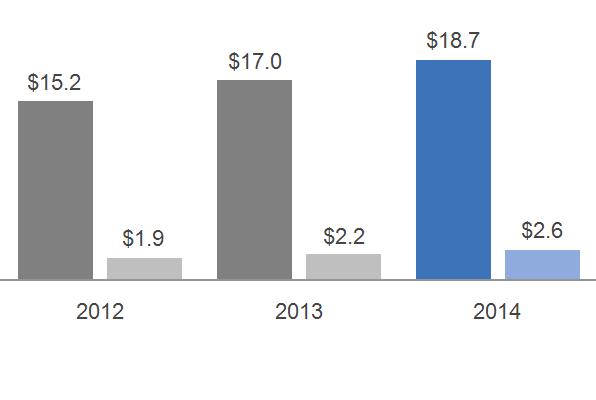

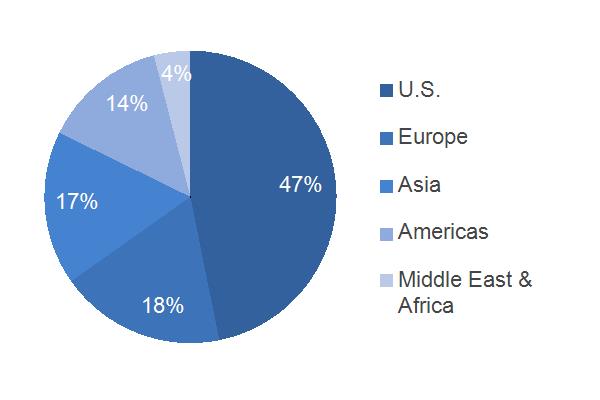

| 2014 GEOGRAPHIC REVENUES: $18.7 BILLION | ORDERS | ||

|  | Equipment Services | |

| 2014 SUB-SEGMENT REVENUES | BACKLOG(a) | ||

|  | Equipment Services | |

| (a)Periods reflect an update for Oil & Gas services backlog | |||

| EQUIPMENT/SERVICES REVENUES | |||

| |||

| Services Equipment | |||

| SIGNIFICANT TRENDS & DEVELOPMENTS |

| · | On June 2, 2014, we acquired Cameron's Reciprocating Compression division for $0.6 billion. The division provides reciprocating compression equipment and aftermarket services for oil and gas production, gas processing, gas distribution and independent power industries. |

| · | In July 2013, we completed the acquisition of Lufkin, a leading provider of artificial lift technologies for the oil and gas industry and a manufacturer of gears, for $3.3 billion. Revenues for Lufkin are included in the D&S sub-segment. |

| · | Relatively lower oil prices leading to reductions in customers' forecasted capital expenditures create industry challenges, the effects of which are uncertain. |

| · | We are impacted by volatility in foreign currency exchange rates mainly due to a high concentration of non-U.S. dollar denominated business as well as long-term contracts denominated in multiple currencies. |

Page 16

FINANCIAL OVERVIEW

(Dollars in billions)

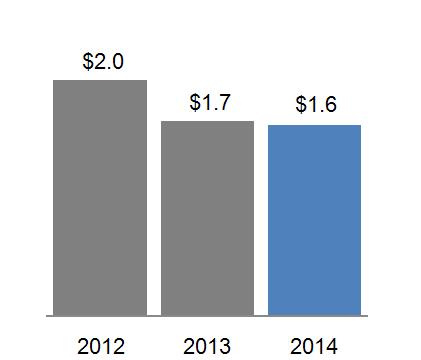

| SEGMENT REVENUES & PROFIT | SEGMENT PROFIT MARGIN | |||||

¢ ¢ Revenue ¢ ¢ Profit  |  | |||||

| SEGMENT REVENUES & PROFIT WALK: | COMMENTARY: | |||||

| 2014 – 2013 | 2014 – 2013 | |||||

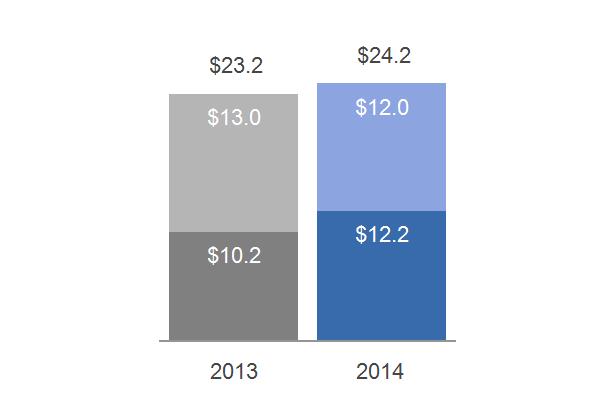

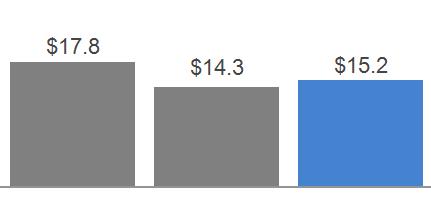

Segment revenues up $1.7 billion (10%); Segment profit up $0.4 billion (19%) as a result of: ·The increase in revenues was primarily due to higher volume, mainly driven by higher equipment sales at SS, D&S and TMS, as well as the $0.3 billion net impact of acquisitions, primarily Lufkin, and dispositions, primarily Wayne. Higher prices primarily at SS also increased revenues. These increases were partially offset by the effects of a stronger U.S. dollar. ·The increase in profit was primarily due to higher productivity, higher volume and higher prices. These increases were partially offset by negative business mix. | ||||||

| Revenues | Profit | |||||

| 2013 | $ | 17.0 | $ | 2.2 | ||

| Volume | 1.7 | 0.2 | ||||

| Price | 0.1 | 0.1 | ||||

| Foreign Exchange | (0.1) | - | ||||

| (Inflation)/Deflation | N/A | - | ||||

| Mix | N/A | (0.2) | ||||

| Productivity | N/A | 0.4 | ||||

| Other | - | - | ||||

| 2014 | $ | 18.7 | $ | 2.6 | ||

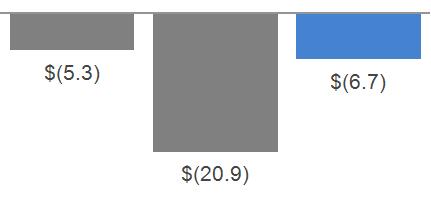

| 2013 – 2012 | 2013 – 2012 | |||||

Segment revenues up $1.7 billion (11%); Segment profit up $0.3 billion (13%) as a result of: ·The increase in revenues was primarily due to higher volume, mainly driven by increased equipment sales as well as the impact of acquisitions ($0.7 billion), higher prices at TMS, and the effects of a weaker U.S. dollar. ·The increase in profit was due to higher volume, which was positively impacted by acquisitions and organic growth in the SS and D&S business, as well as higher prices at TMS. This was partially offset by lower cost productivity. | ||||||

| Revenues | Profit | |||||

| 2012 | $ | 15.2 | $ | 1.9 | ||

| Volume | 1.5 | 0.2 | ||||

| Price | 0.2 | 0.2 | ||||

| Foreign Exchange | 0.1 | - | ||||

| (Inflation)/Deflation | N/A | - | ||||

| Mix | N/A | - | ||||

| Productivity | N/A | (0.1) | ||||

| Other | - | - | ||||

| 2013 | $ | 17.0 | $ | 2.2 | ||

Page 17

ENERGY MANAGEMENT

ENERGY MANAGEMENTBUSINESS OVERVIEW

Leader: Mark W. Begor | Headquarters & Operations | ||||||||

| ·President & CEO, GE Energy Management ·Over 30 years of service with General Electric |  | ·5% of segment revenues in 2014 ·7% of industrial segment revenues ·1% of industrial segment profit ·Headquarters: Atlanta, GA ·Serving customers in 150+ countries ·Employees: approximately 30,000 | ||||||

| Products & Services | |||||||||

| Energy Management designs, manufactures and services leading technology solutions for the delivery, management, conversion and optimization of electrical power. Our energy solutions allow customers across multiple energy-intensive industries such as oil & gas, marine, data centers, metals and mining to efficiently manage electricity from the point of generation to the point of consumption. | ||||||||

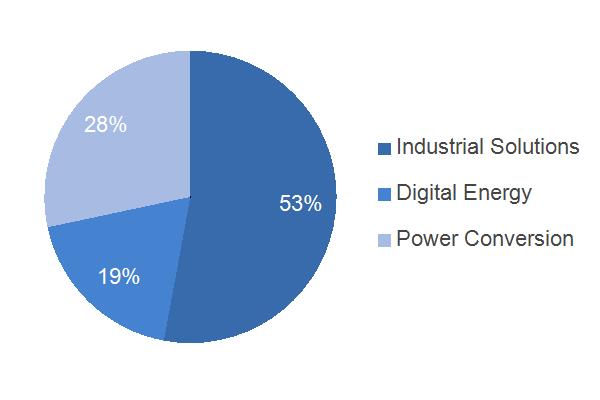

| · | Industrial Solutions – creates advanced technologies that safely, reliably and efficiently distribute and control electricity to protect people, property and equipment. We provide high performance software and control solutions and offer products such as circuit breakers, relays, arresters, switchgear, panel boards and repair for the commercial, data center, healthcare, mining, renewables, oil & gas, water and telecom markets. |

| · | Digital Energy – maximizes the reliability, efficiency and resiliency of the grid by preventing and detecting grid power failures, digitizing substations, and reducing outages. We provide advanced products and services that modernize the grid, from the power plant to the power consumer, such as protection and control, industrial strength communications, smart meters, monitoring & diagnostics, visualization software and advanced analytics. We provide high voltage and medium voltage (HV/MV) equipment, smart controls and sensors, software solutions and power projects for industries such as generation, transmission, distribution, oil and gas, telecommunication, mining and water. We currently have several strategic partnership ventures, primarily in Mexico and China, which allow us to support our customers through various product and service offerings. |

| · | Power Conversion – applies the science and systems of power conversion to help drive the electric transformation of the world's energy infrastructure. Our product portfolio includes motors, generators, automation & control equipment & drives for energy intensive industries such as marine, oil & gas, renewable energy, mining, rail, metals, test systems and water. |

| Competition & Regulation |

Energy Management faces competition from businesses operating with global presence and with deep energy domain expertise. Our products and services sold to end customers are often subject to a number of regulatory specification and performance standards under different federal, state, foreign and energy industry standards.

Page 18

OPERATIONAL OVERVIEW

(Dollars in billions)

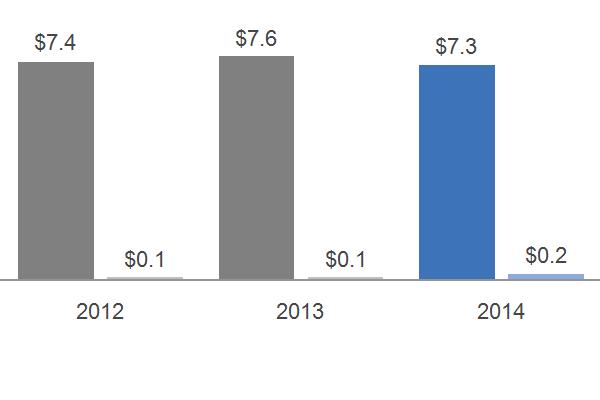

| 2014 GEOGRAPHIC REVENUES: $7.3 BILLION | ORDERS | ||

|  | Equipment Services | |

| 2014 SUB-SEGMENT REVENUES | BACKLOG | ||

|  | Equipment Services | |

| EQUIPMENT/SERVICES REVENUES | |||

| |||

| Services Equipment | |||

| SIGNIFICANT TRENDS & DEVELOPMENTS |

| · | We are seeing growth in the liquefied natural gas, onshore electrification, offshore marine, and wind & solar industries, which is driving demand in our Power Conversion business for equipment and services. |

| · | While we see signs of growth in the North American electrical distribution market, the European economic recovery is slow, and demand remains soft in other parts of the developed world. |

| · | The U.S. electrical grid capacity is high and load growth is expected to be slow in the near term; spending by utilities in the U.S. continues to be focused more heavily on sustaining operations versus capital investment. |

| · | We plan to complement and expand the Digital Energy business with the acquisition of Alstom's Grid business. |

| · | We expect continued reinvestment in our key products to drive growth and continued margin accretion in 2015 and beyond. |

Page 19

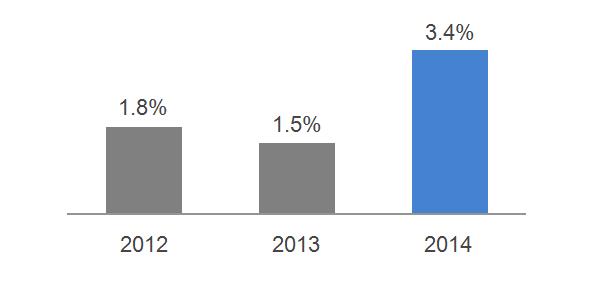

FINANCIAL OVERVIEW

(Dollars in billions)

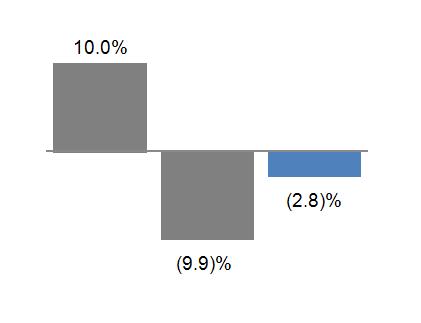

| SEGMENT REVENUES & PROFIT | SEGMENT PROFIT MARGIN | ||

¢ ¢ Revenue ¢ ¢ Profit  |  |

| COMMENTARY: | ||

| 2014 – 2013 | 2013 – 2012 | |

| Segment revenues down $0.3 billion (3%) as a result of: | Segment revenues up $0.2 billion (2%) as a result of: | |

·Lower volume ($0.2 billion) from weakness in North American utility and electrical distribution markets, partially offset by higher sales in Power Conversion. | ·Higher volume ($0.2 billion), partially offset by the effects of the stronger U.S. dollar ($0.1 billion). | |

Segment profit up $0.1 billion as a result of: | Segment profit down 16% as a result of: | |

·Higher productivity ($0.1 billion) reflecting an 8% reduction in SG&A cost. | ·Lower productivity ($0.1 billion). | |

Page 20

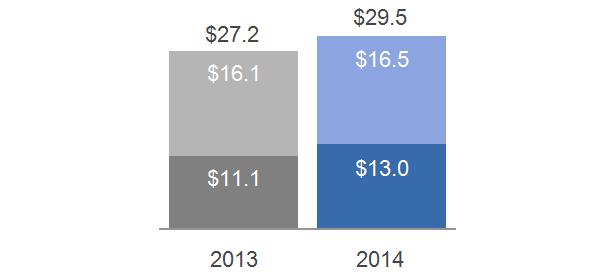

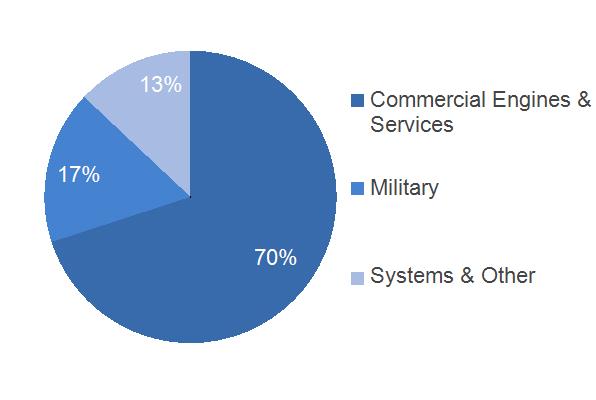

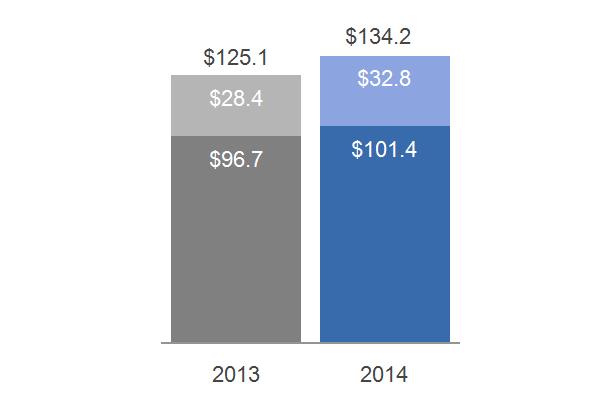

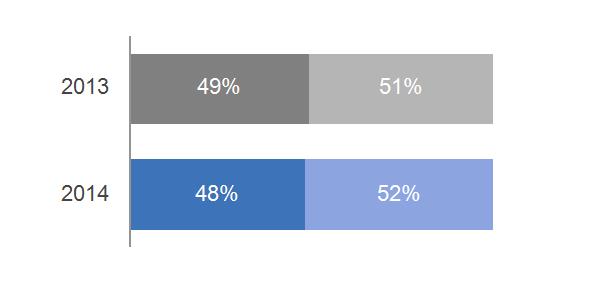

AVIATION

AVIATIONBUSINESS OVERVIEW

Leader: David Joyce | Headquarters & Operations | ||||||||

| ·SVP and President & CEO, GE Aviation ·Over 30 years of service with General Electric |  | ·18% of segment revenues in 2014 ·22% of industrial segment revenues ·28% of industrial segment profit ·Headquarters: Cincinnati, OH ·Serving customers in 125+ countries ·Employees: approximately 44,000 | ||||||

| Products & Services | |||||||||

| Aviation designs and produces commercial and military aircraft engines, integrated digital components, electric power and mechanical aircraft systems. We also provide aftermarket services to support our products. | ||||||||

| · | Commercial Engines (CEO) – manufactures jet engines and turboprops for commercial airframes. Our commercial engines power aircraft in all categories; regional, narrowbody and widebody. We also manufacture for Business and General Aviation segments. |

| · | Commercial Services – provides maintenance, component repair and overhaul services (MRO), including sales of replacement parts. |

| · | Military – manufactures jet engines for military airframes. Our military engines power a wide variety of military aircraft including fighters, bombers, tankers, helicopters and surveillance aircraft, as well as marine applications. We provide maintenance, component repair and overhaul services (MRO), including sales of replacement parts. |

| · | Systems – provides components, systems and services for commercial and military segments. This includes avionics systems, aviation electric power systems, flight efficiency and intelligent operation services, aircraft structures and Avio Aero. |

| · | We also produce and market engines through CFM International, a company jointly owned by GE and Snecma, a subsidiary of SAFRAN of France, and Engine Alliance, LLC, a company jointly owned by GE and the Pratt & Whitney division of United Technologies Corporation. New engines are also being designed and marketed in a joint venture with Honda Aero, Inc., a division of Honda Motor Co., Ltd. |

| Competition & Regulation |

The global businesses for aircraft jet engines, maintenance component repair and overhaul services (including parts sales) are highly competitive. Both U.S. and non-U.S. markets are important to the growth and success of the business. Product development cycles are long and product quality and efficiency are critical to success. Research and development expenditures are important in this business, as are focused intellectual property strategies and protection of key aircraft engine design, manufacture, repair and product upgrade technologies. Aircraft engine orders and systems tend to follow military and airline procurement transactions.

Our product, services and activities are subject to a number of regulators such as by the U.S. Federal Aviation Administration (FAA), European Aviation Safety Agency (EASA) and other regulatory bodies.

Page 21

OPERATIONAL OVERVIEW

(Dollars in billions)

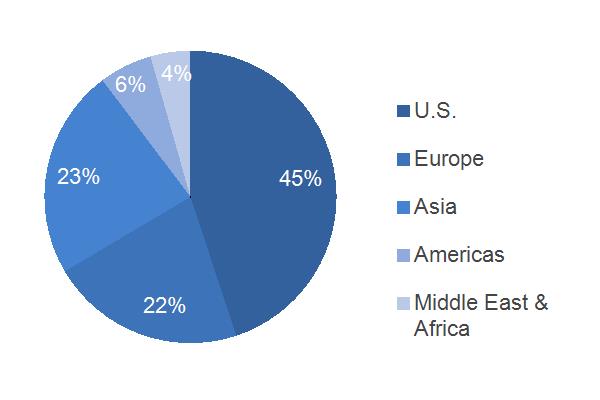

| 2014 GEOGRAPHIC REVENUES: $24.0 BILLION | ORDERS | ||||

|  | Equipment Services | |||

| 2014 SUB-SEGMENT REVENUES | BACKLOG | ||||

|  | Equipment Services | |||

| EQUIPMENT/SERVICES REVENUES | UNIT SALES | ||||

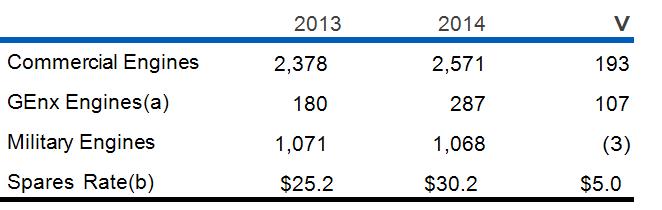

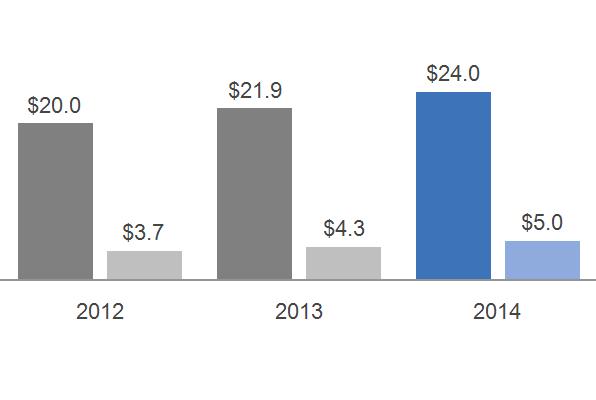

|  (a)GEnx engines are a subset of commercial engines (b)Commercial spares shipment rate in millions of dollars per day | ||||

| Services Equipment | |||||

| SIGNIFICANT TRENDS & DEVELOPMENTS | |||||

| · | On August 1, 2013, we completed the acquisition of the aviation business of Avio, a manufacturer of aviation propulsion components and systems for $4.4 billion. |

| · | We expect military shipments to be lower due to continued pressure on the U.S. military budget. |

| · | The installed base continues to grow with new product launches. |

| · | Lower fuel costs are expected to result in increased airline profitability and continued growth in passenger traffic and freight. |

| · | Revenue sharing programs are a standard form of cooperation for specific product programs in the aviation industry. These programs are controlled by Aviation, but counterparties (with interests ranging from 1% to 39%) have an agreed share of revenues as well as development and component production responsibilities. |

Page 22

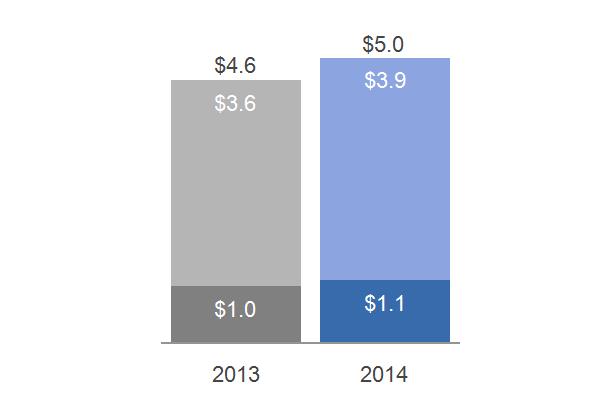

FINANCIAL OVERVIEW

(Dollars in billions)

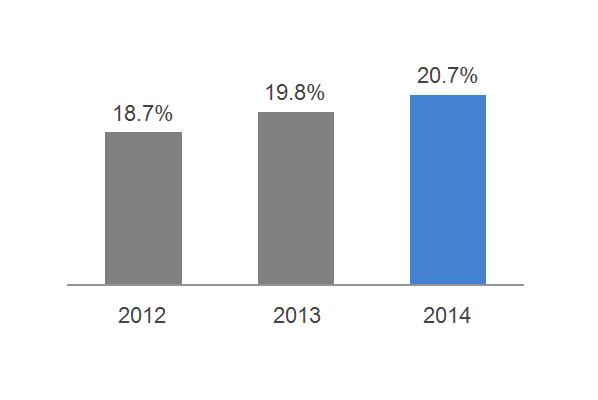

| SEGMENT REVENUES & PROFIT | SEGMENT PROFIT MARGIN | |||||

¢ ¢ Revenue ¢ ¢ Profit  |  | |||||

| SEGMENT REVENUES & PROFIT WALK: | COMMENTARY: | |||||

| 2014 – 2013 | 2014 – 2013 | |||||

Segment revenues up $2.1 billion (9%); Segment profit up $0.6 billion (14%) as a result of: ·The increase in revenues was due to higher volume and higher prices driven by Commercial Engines volume, spare parts volume and the third-quarter 2013 acquisition of Avio. ·The increase in profit was mainly due to higher prices in our Commercial Engines and Commercial Services businesses and higher volume discussed above. These increases were partially offset by effects of inflation and negative business mix. | ||||||

| Revenues | Profit | |||||

| 2013 | $ | 21.9 | $ | 4.3 | ||

| Volume | 1.2 | 0.2 | ||||

| Price | 0.8 | 0.8 | ||||

| Foreign Exchange | - | - | ||||

| (Inflation)/Deflation | N/A | (0.3) | ||||

| Mix | N/A | (0.2) | ||||

| Productivity | N/A | - | ||||

| Other | 0.1 | 0.1 | ||||

| 2014 | $ | 24.0 | $ | 5.0 | ||

| 2013 – 2012 | 2013 – 2012 | |||||

Segment revenues up $1.9 billion (10%) (including $0.5 billion from acquisitions); Segment profit up $0.6 billion (16%) as a result of: ·The increase in revenues was primarily due to higher volume and higher prices. Higher volume and prices were driven by increased services revenues ($0.7 billion) and equipment ($1.2 billion). The increase in service revenue was primarily due to higher commercial spares sales, while the increase in equipment was primarily due to increased Commercial Engine shipments. ·The increase in profit was due to higher prices, higher volume and increased other income, partially offset by the effects of inflation and lower cost productivity. | ||||||

| Revenues | Profit | |||||

| 2012 | $ | 20.0 | $ | 3.7 | ||

| Volume | 1.4 | 0.2 | ||||

| Price | 0.6 | 0.6 | ||||

| Foreign Exchange | - | - | ||||

| (Inflation)/Deflation | N/A | (0.2) | ||||

| Mix | N/A | - | ||||

| Productivity | N/A | (0.1) | ||||

| Other | - | 0.1 | ||||

| 2013 | $ | 21.9 | $ | 4.3 | ||

Page 23

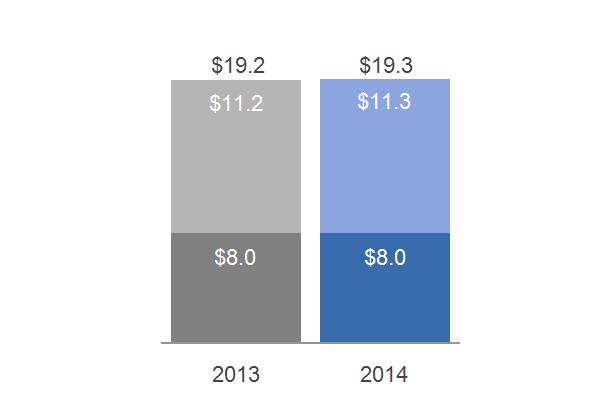

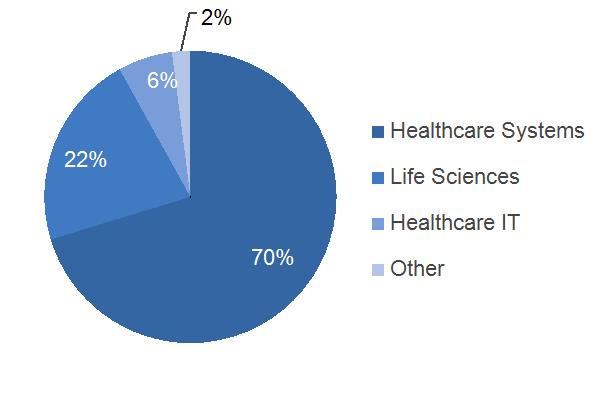

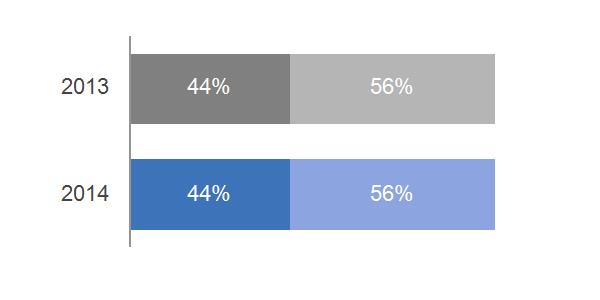

HEALTHCARE

HEALTHCAREBUSINESS OVERVIEW

Leader: John L. Flannery | Headquarters & Operations | ||||||||

| ·President & CEO, GE Healthcare ·Over 25 years of service with General Electric |  | ·14% of segment revenues in 2014 ·17% of industrial segment revenues ·17% of industrial segment profit ·Headquarters: Little Chalfont, UK ·Serving customers in 140+ countries ·Employees: approximately 51,000 | ||||||

| Products & Services | |||||||||

| Healthcare provides essential healthcare technologies to developed and emerging markets and has expertise in medical imaging, software and information technology (IT), patient monitoring and diagnostics, drug discovery, biopharmaceutical manufacturing technologies and performance improvement solutions. Products and services are sold worldwide primarily to hospitals, medical facilities, pharmaceutical and biotechnology companies, and to the life science research market. | ||||||||

| · | Healthcare Systems – provides a wide range of technologies and services that include diagnostic imaging and clinical systems. Diagnostic imaging systems such as X-ray, digital mammography, computed tomography (CT), magnetic resonance (MR), interventional imaging and molecular imaging technologies allow clinicians to see inside the human body more clearly. Clinical systems such as ultrasound, electrocardiography (ECG), bone densitometry, patient monitoring, incubators and infant warmers, respiratory care, and anesthesia management that enable clinicians to provide better care for patients every day - from wellness screening to advanced diagnostics to life-saving treatment. Healthcare systems also offers product services that include remote diagnostic and repair services for medical equipment manufactured by GE and by others. |

| · | Life Sciences – delivers products and services for drug discovery, biopharmaceutical manufacturing and cellular technologies, so scientists and specialists discover new ways to predict, diagnose and treat disease. It also researches, manufactures and markets innovative imaging agents used during medical scanning procedures to highlight organs, tissue and functions inside the human body, to aid physicians in the early detection, diagnosis and management of disease through advanced in-vivo and in-vitro diagnostics. |

| · | Healthcare IT – provides IT solutions including enterprise and departmental Information Technology products, Picture Archiving System (PACS), Radiology Information System (RIS), Cardiovascular Information System (CVIS), revenue cycle management and practice applications, to help customers streamline healthcare costs and improve the quality of care. |

| Competition & Regulation |

Healthcare competes with a variety of U.S. and non-U.S. manufacturers and services providers. Customers require products and services that allow them to provide better access to healthcare, improve the affordability of care, and improve the quality of patient outcomes. Technology innovation to provide products that improve these customer requirements and competitive pricing are among the key factors affecting competition for these products and services. New technologies could make our products and services obsolete unless we continue to develop new and improved products and services.

Our products are subject to regulation by numerous government agencies, including the U.S. Food and Drug Administration (U.S. FDA), as well as various laws that apply to claims submitted under Medicare, Medicaid or other government funded healthcare programs.

Page 24

OPERATIONAL OVERVIEW

(Dollars in billions)

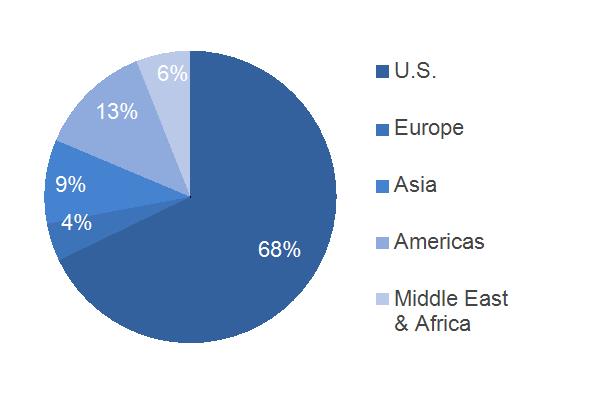

| 2014 GEOGRAPHIC REVENUES: $18.3 BILLION | ORDERS | ||

|  | Equipment Services | |

| 2014 SUB-SEGMENT REVENUES | BACKLOG | ||

|  | Equipment Services | |

| EQUIPMENT/SERVICES REVENUES | |||

| |||

| Services Equipment | |||

| SIGNIFICANT TRENDS & DEVELOPMENTS |

| · | We continue to lead in technology innovation with greater focus on productivity based technology, services, and IT solutions as healthcare providers seek greater productivity and efficiency. |

| · | The U.S. market is improving but uncertainty remains regarding the impact of the Affordable Care Act. Emerging markets are expected to grow long-term with short-term volatility. |

| · | API Healthcare (API), a healthcare workforce management software and analytics solutions provider, was acquired in February 2014 for $0.3 billion. |

| · | Life Sciences is expanding its business through bioprocess growth and the acquisition of certain Thermo Fisher Scientific Inc. life-science businesses, which were acquired in March 2014 for $1.1 billion. |

Page 25

FINANCIAL OVERVIEW

(Dollars in billions)

| SEGMENT REVENUES & PROFIT | SEGMENT PROFIT MARGIN | |||||

¢ ¢ Revenue ¢ ¢ Profit  |  | |||||

| SEGMENT REVENUES & PROFIT WALK: | COMMENTARY: | |||||

| 2014 – 2013 | 2014 – 2013 | |||||

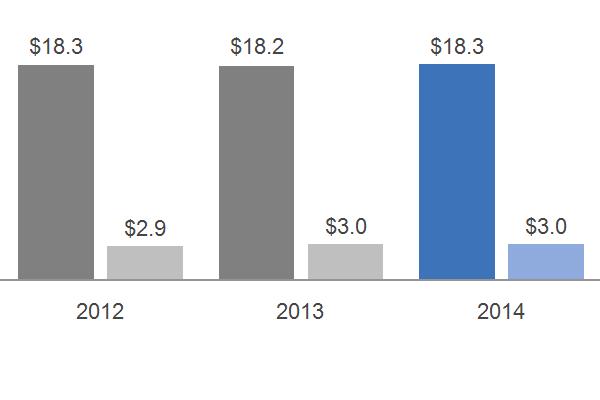

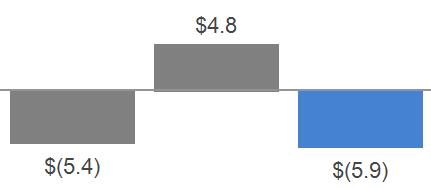

Segment revenues up $0.1 billion (1%); Segment profit flat as a result of: ·The increase in revenues was due to higher volume, driven by the higher sales in Life Sciences. This increase was partially offset by lower prices mainly at Healthcare Systems and the effects of a stronger U.S. dollar. ·Profit was flat as higher productivity, driven by SG&A cost reductions, and higher volume, were offset by lower prices, mainly at Healthcare Systems, inflation and effects of a stronger U.S. dollar. | ||||||

| Revenues | Profit | |||||

| 2013 | $ | 18.2 | $ | 3.0 | ||

| Volume | 0.6 | 0.1 | ||||

| Price | (0.3) | (0.3) | ||||

| Foreign Exchange | (0.2) | (0.1) | ||||

| (Inflation)/Deflation | N/A | (0.2) | ||||

| Mix | N/A | - | ||||

| Productivity | N/A | 0.5 | ||||

| Other | - | - | ||||

| 2014 | $ | 18.3 | $ | 3.0 | ||

| 2013 – 2012 | 2013 – 2012 | |||||

Segment revenues down $0.1 billion; Segment profit up $0.1 billion (4%) as a result of: ·The decrease in revenues was driven by lower prices mainly at Healthcare Systems, effects of a stronger U.S. dollar and lower other income, partially offset by higher volume. ·The increase in profit was mainly driven by higher productivity resulting from SG&A cost reductions and higher volume, partially offset by lower prices mainly at Healthcare Systems, the effects of inflation and the stronger U.S. dollar. | ||||||

| Revenues | Profit | |||||

| 2012 | $ | 18.3 | $ | 2.9 | ||

| Volume | 0.5 | 0.1 | ||||

| Price | (0.3) | (0.3) | ||||

| Foreign Exchange | (0.2) | (0.1) | ||||

| (Inflation)/Deflation | N/A | (0.2) | ||||

| Mix | N/A | - | ||||

| Productivity | N/A | 0.6 | ||||

| Other | - | - | ||||

| 2013 | $ | 18.2 | $ | 3.0 | ||

Page 26

TRANSPORTATION

TRANSPORTATIONBUSINESS OVERVIEW

Leader: Russell Stokes | Headquarters & Operations | ||||

| ·President & CEO, GE Transportation ·Over 15 years of service with General Electric |  | ·4% of segment revenues in 2014 ·5% of industrial segment revenues ·6% of industrial segment profit ·Headquarters: Chicago, IL ·Serving customers in 60+ countries ·Employees: approximately 13,000 | ||

| Products & Services | |||

| Transportation is a global technology leader and supplier to the railroad, marine, drilling and mining industries. Products and services offered by Transportation include: | ||

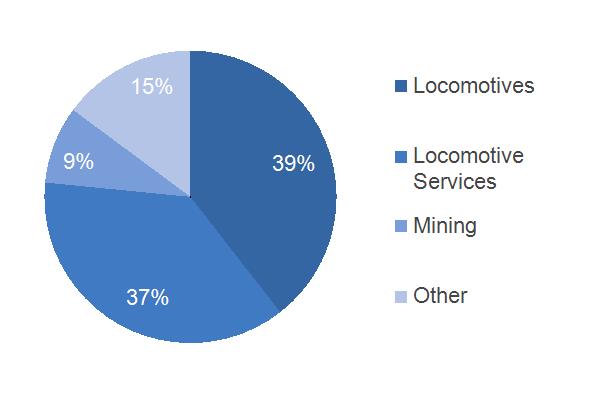

| · | Locomotives – we provide freight and passenger locomotives, signaling and communications systems as well as rail services to help solve rail challenges. We manufacture high-horsepower, diesel-electric locomotives including the Evolution Series TM, which meets or exceeds the U.S. Environmental Protection Agency's (EPA) Tier 4 requirements for freight and passenger applications. |

| · | Locomotive Services & Solutions – we develop partnerships that support advisory services, parts, integrated software solutions and data analytics. Our comprehensive offerings include tailored service programs, high-quality parts for GE and other locomotive platforms, overhaul, repair and upgrade services, and wreck repair. Our portfolio provides the people, partnerships and leading software to optimize operations and asset utilization. |

| · | Mining – we provide mining equipment and services. The portfolio includes drive systems for off-highway vehicles, mining equipment, mining power and productivity. |

| · | Marine, Stationary & Drilling – we offer motors for land and offshore drilling rigs, marine diesel engines and stationary power diesel engines. |

| Competition & Regulation |

The competitive environment for locomotives and mining equipment and services consists of large global competitors and a number of smaller competitors that compete in a limited-size product range, and or geographic region. North America will be of particular focus for the rail industry in 2015 as the EPA Tier 4 emissions standards are implemented. We are positioned with the only locomotive currently available that meets the Tier 4 standards.

Page 27

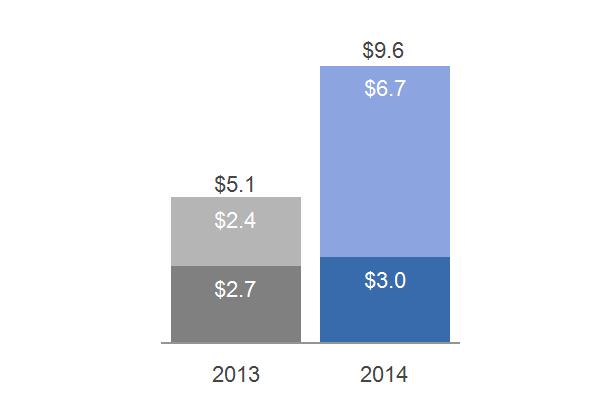

OPERATIONAL OVERVIEW

(Dollars in billions)

| 2014 GEOGRAPHIC REVENUES: $5.7 BILLION | ORDERS | ||

|  | Equipment Services | |

| 2014 SUB-SEGMENT REVENUES | BACKLOG | ||

|  | Equipment Services | |

| EQUIPMENT/SERVICES REVENUES | UNIT SALES | ||

|  | ||

| Services Equipment | |||

| SIGNIFICANT TRENDS & DEVELOPMENTS |

| · | Rail volume, especially in North America, continues to climb and the number of parked locomotives remains low. |

| · | North American locomotives competition remains strong, but GE is positioned with the only locomotive currently available meeting the U.S. EPA's highest (Tier 4) emission standards. We expect U.S. growth to be driven by early demand for Tier 4 locomotives. |

| · | Continued global mining softness has resulted in delayed capital expenditures in the mining industry. |

| · | During the fourth quarter of 2014, we signed an agreement to sell our Signaling business to Alstom for approximately $0.8 billion. |

Page 28

FINANCIAL OVERVIEW

(Dollars in billions)

| SEGMENT REVENUES & PROFIT | SEGMENT PROFIT MARGIN | |

¢ ¢ Revenue ¢ ¢ Profit  |  | |

| COMMENTARY: | ||

| 2014 – 2013 | 2013 – 2012 | |

Segment revenues down $0.2 billion (4%) as a result of: ·Lower volume ($0.2 billion), primarily in Mining reflecting weakness in the industry, partially offset by an increase in volume in the locomotive services business. Segment profit down 3% as a result of: ·Lower volume, primarily in Mining as discussed above, was partially offset by deflation and cost productivity. | Segment revenues up $0.3 billion (5%) as a result of: ·Higher volume ($0.3 billion), due to 2012 acquisitions (primarily Industrea). Segment profit up $0.1 billion (13%) as a result of: ·Material deflation ($0.1 billion), higher volume and productivity. |

Page 29

APPLIANCES & LIGHTING

APPLIANCES & LIGHTINGBUSINESS OVERVIEW

Leaders: Chip Blankenship & Maryrose Sylvester | Headquarters & Operations | |||

| ·President & CEO, Appliances ·Over 20 years of service with General Electric ·President & CEO, Lighting ·Over 25 years of service with General Electric |  | ·6% of segment revenues in 2014 ·7% of industrial segment revenues ·2% of industrial segment profit ·Appliances HQ: Louisville, KY ·Lighting HQ: East Cleveland, OH ·Serving customers in 100+ countries ·Employees: approximately 24,000 | |

| Products & Services | |||

| Appliances & Lighting products, such as major appliances and a subset of lighting products, are primarily directed to consumer applications, while other lighting products are directed towards commercial and industrial applications. We also invest in the development of differentiated, premium products such as energy efficient solutions for both consumers and businesses. | ||

| · | Appliances – sells and services major home appliances including refrigerators, freezers, electric and gas ranges, cooktops, dishwashers, clothes washers and dryers, microwave ovens, room air conditioners, residential water systems for filtration, softening and heating and hybrid water heaters. Our brands include GE Monogram®, GE Café™, GE Profile™, GE®, GE Artistry™, and Hotpoint®. We also manufacture certain products and source finished product and component parts from third-party global manufacturers. A large portion of appliances sales are through a variety of retail outlets for replacement of installed units. Residential building contractors installing units in new construction is the second major U.S. channel. We offer one of the largest original equipment manufacturer (OEM) service organizations in the appliances industry, providing in-home repair and aftermarket parts. |

| · | Lighting – manufactures, sources and sells a variety of energy-efficient solutions for commercial, industrial, municipal and consumer applications across the globe, utilizing light-emitting diode (LED), fluorescent, halogen and high-intensity discharge (HID) technologies. In addition to growing our LED breadth, the business is focused on building lighting connected by state-of-the-art software that will unleash a whole new potential for how we light our world. The business sells products under the reveal® and Energy Smart® consumer brands, and Evolve™, GTx™, Immersion™, Infusion™, Lumination,™ Albeo,™ TriGain™ and Tetra® commercial brands. GE Lighting offers a full range of solutions and services to outfit entire properties with lighting, from ceilings, parking lots, signage, displays, roadways, sports arenas and other areas. |

| Competition & Regulation |

Cost control, including productivity, is key in the highly competitive marketplace in which Appliances & Lighting competes. GE Lighting operates in a complex, global marketplace. Energy regulations impacting traditional lighting technologies are moving demand to energy-saving products that last longer and cost less to operate over time. Evolving these technologies, as well as cost control, is key in the global arena in which the business operates.

Page 30

OPERATIONAL OVERVIEW

(Dollar in billions)

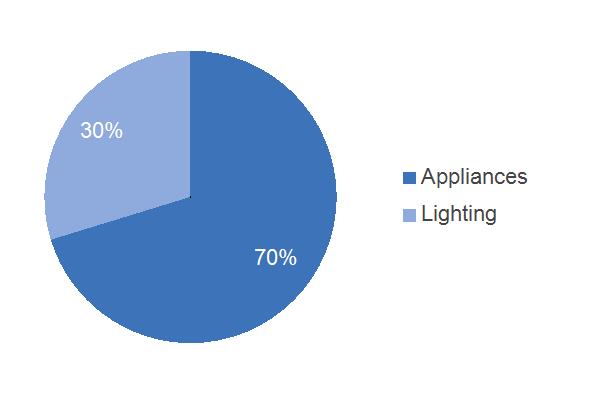

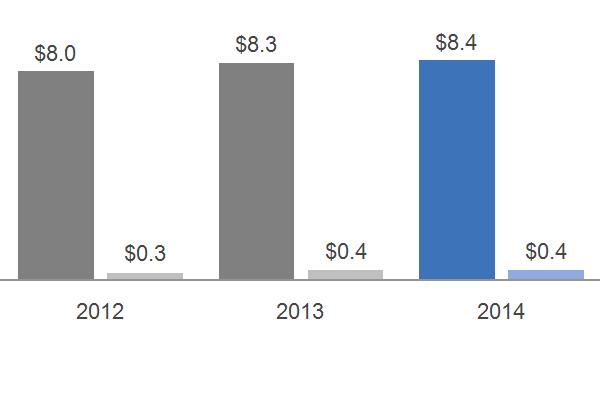

| 2014 GEOGRAPHIC REVENUES: $8.4 BILLION | 2014 SUB-SEGMENT REVENUES | ||

|  | ||

SIGNIFICANT TRENDS & DEVELOPMENTS | |||

·During the third quarter of 2014, GE signed an agreement to sell its Appliances business to Electrolux for $3.3 billion. The transaction has been approved by the boards of directors of GE and Electrolux and remains subject to customary closing conditions and regulatory approvals, and is targeted to close in mid-2015. ·While the demand in the professional non-LED market segment is slowing, there is a strong global shift to energy efficient lighting including continued growth in LED products. | |||

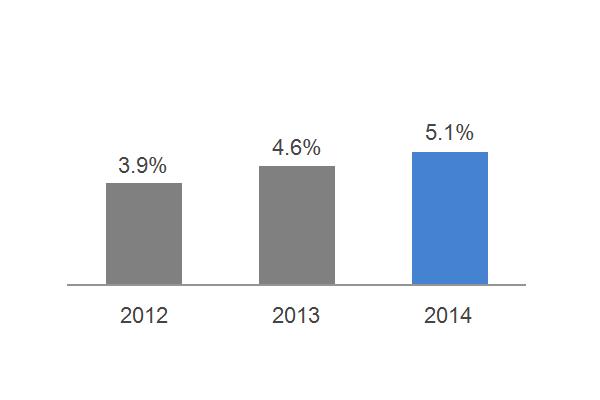

FINANCIAL OVERVIEW

(Dollar in billions)

| SEGMENT REVENUES & PROFIT | SEGMENT PROFIT MARGIN | ||

¢ ¢ Revenue ¢ ¢ Profit  |  | ||

COMMENTARY: | |||

| 2014 – 2013 | 2013 – 2012 | ||

Segment revenues up $0.1 billion (1% ) as a result of: ·Higher volume ($0.1 billion) driven by higher sales at Appliances. Segment profit up $0.1 billion (13%) as a result of: ·Improved productivity ($0.1 billion) including the effects of classifying Appliances as a business held for sale in the third quarter of 2014. | Segment revenues up $0.4 billion (5%) as a result of: ·Higher volume ($0.4 billion) driven by higher sales at Appliances. Segment profit up $0.1 billion (23%) as a result of: ·Improved productivity ($0.1 billion) and higher prices. | ||

Page 31

GE CAPITALBUSINESS OVERVIEW

Leader: Keith Sherin | Headquarters & Operations | |||

| ·Vice Chairman GE, and Chairman & CEO, GE Capital ·Over 30 years of service with General Electric |  | ·19% of segment revenues in 2014 ·Headquarters: Norwalk, CT ·Serving customers in 70+ countries ·Employees: approximately 47,000 | |

| Products & Services | ||||

GE Capital businesses offer a broad range of financial services and products worldwide for businesses of all sizes. Services include commercial loans and leases, financial programs, credit cards, personal loans and other financial services. GE Capital also develops strategic partnerships and joint ventures that utilize GE's industry-specific expertise in aviation, energy, infrastructure and healthcare to capitalize on market-specific opportunities. Products and services are offered through the following businesses: | ||||

| · | Commercial Lending and Leasing (CLL) – includes Healthcare Equipment Finance, a premier provider of capital and services to the healthcare industry and Working Capital Solutions, which purchases GE customer receivables. Our Healthcare Equipment Finance portfolio is collateralized by equipment used in the healthcare industry and our Working Capital Solutions portfolio is substantially recourse to GE or insured. |

| · | Consumer – offers a full range of financial products including private-label credit cards; personal loans; bank cards; auto loans and leases; mortgages; debt consolidation; home equity loans; deposit and other savings products; and small and medium enterprise lending on a global basis. |

| · | Energy Financial Services – invests in long-lived, capital intensive energy projects and companies by providing structured equity, debt, leasing, partnership financing, project finance and broad-based commercial finance. |

| · | GE Capital Aviation Services (GECAS) – our commercial aircraft financing and leasing business, offers a wide range of aircraft types and financing options, including operating leases and secured debt financing, and also provides productivity solutions including spare engine leasing, airport and airline consulting services, and spare parts financing and management. |

As a result of the GE Capital Exit Plan, GE Capital's Real Estate business and most of the CLL business are classified as discontinued operations and are no longer reported as part of the GE Capital segment results. All comparative prior period information has been reclassified to reflect Real Estate and most of CLL as discontinued operations.

| Competition & Regulation |

The businesses in which we engage are subject to competition from various types of financial institutions, including commercial banks, thrifts, investment banks, broker-dealers, credit unions, leasing companies, consumer loan companies, independent finance companies, finance companies associated with manufacturers and insurance and reinsurance companies.

GECC is a regulated savings and loan holding company under U.S. law, subject to Federal Reserve Board (FRB) supervision. In 2013, the U.S. Financial Stability Oversight Council (FSOC) designated GECC as a nonbank systemically important financial institution (nonbank SIFI) under the Dodd-Frank Wall Street Reform and Consumer Protection Act (See Regulations and Supervision for additional information).

Page 32

OPERATIONAL OVERVIEW

(Dollars in billions)

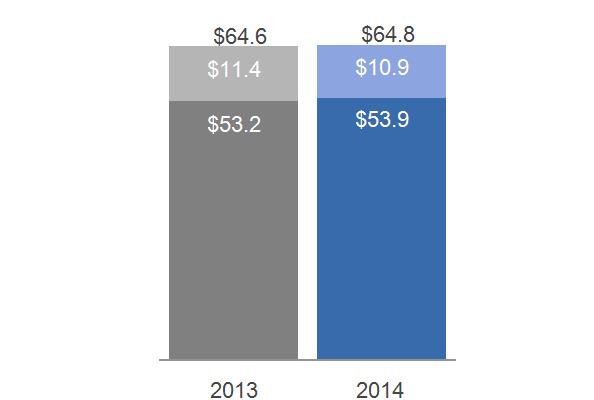

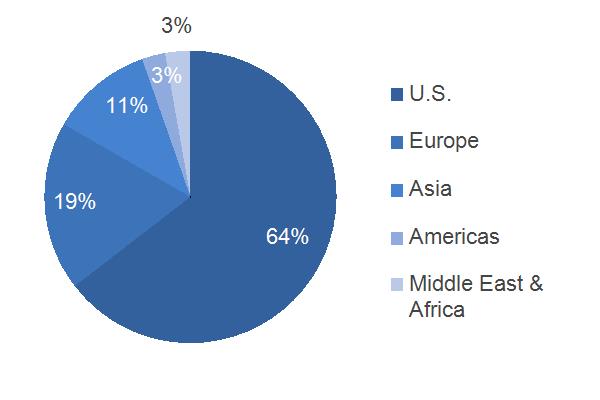

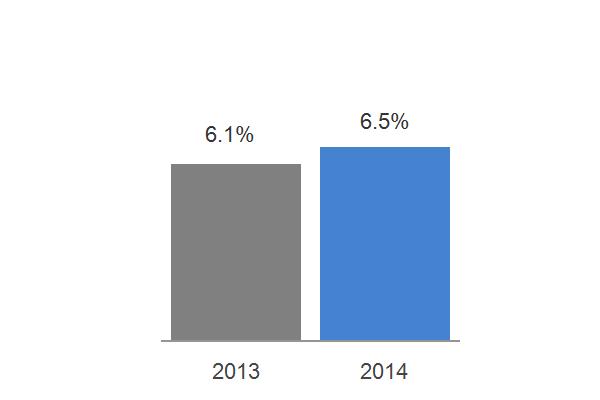

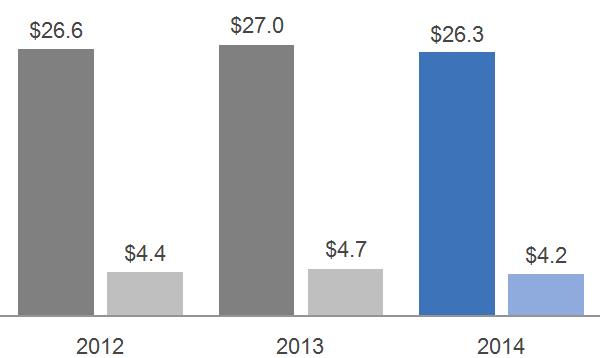

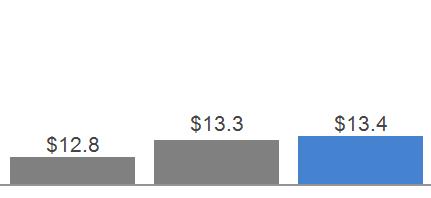

| 2014 GEOGRAPHIC REVENUES: $26.3 BILLION | NET INTEREST MARGIN | |

|  | |

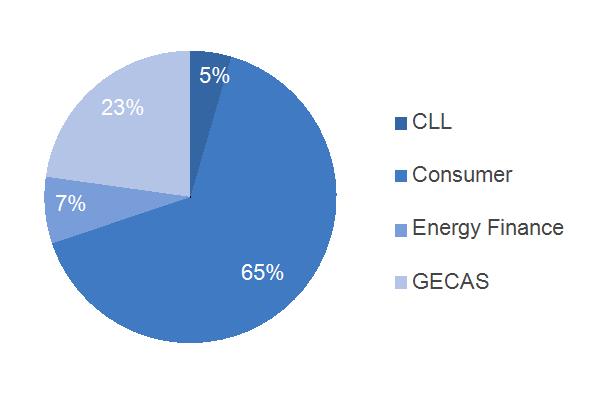

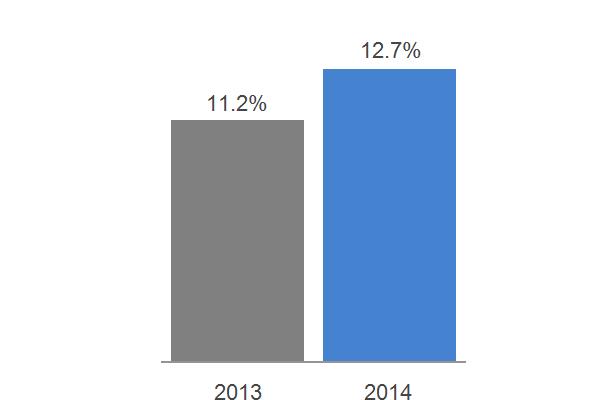

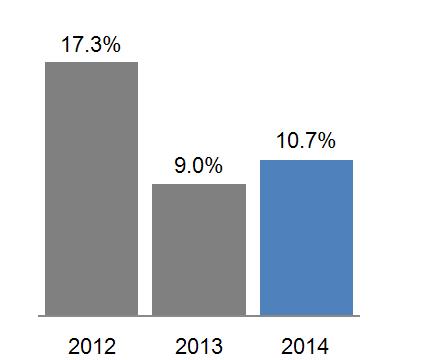

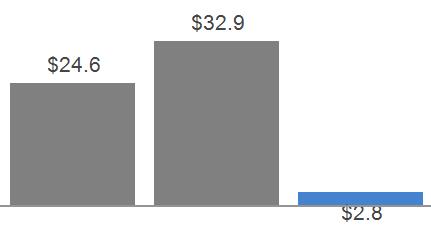

| 2014 SUB-SEGMENT REVENUES | TIER 1 COMMON RATIO ESTIMATE* | |

|  | |

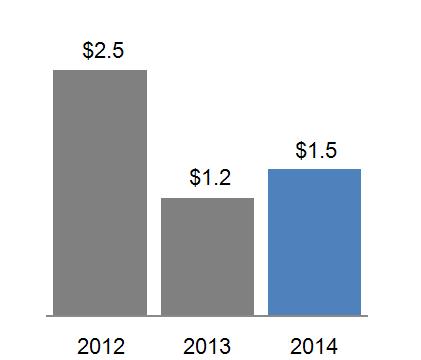

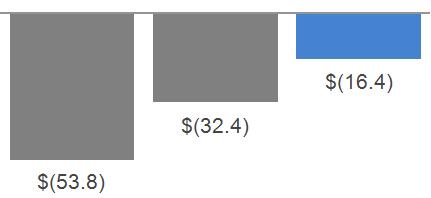

| ENDING NET INVESTMENT, EXCLUDING LIQUIDITY* | DIVIDENDS RETURNED TO PARENT IN 2014 | |

| Quarterly Dividends $2.0 billion Special Dividends $1.0 billion Total $3.0 billion |

* Non-GAAP Financial Measure

Page 33

| SIGNIFICANT TRENDS & DEVELOPMENTS |

ENDING NET INVESTMENT

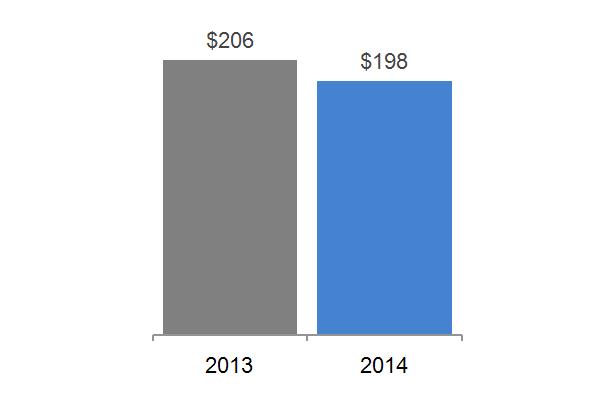

We have communicated our goal of reducing GE Capital's ENI, excluding liquidity. ENI is a metric used by us to measure the total capital we have invested in our financial services business. GE Capital's ENI (excluding liquidity) was $198 billion at December 31, 2014. To achieve this goal, we are more aggressively focusing our businesses on selective financial services products where we have deep domain experience, broad distribution, the ability to earn a consistent return on capital and are competitively advantaged, while managing our overall balance sheet size and risk. We have a strategy of exiting those businesses that are deemed to be non-strategic or that are underperforming. We have completed a number of dispositions in our businesses in the past and will continue to evaluate options going forward.

Accordingly, in the short-term, as we reduce our ENI through exiting non-core businesses, the overall level of our net earnings may be reduced, which potentially could include impairments, restructurings and other non-cash charges. However, over the long-term, we believe that this strategy will improve our long-term performance through higher returns as we will have a larger concentration of assets in our core businesses, as opposed to the underperforming or non-strategic assets we will be exiting; reduce liquidity risk as we pay down outstanding debt and diversify our sources of funding (with less reliance on the global commercial paper markets and an increase in alternative sources of funding such as deposits); and reduce capital requirements while strengthening capital ratios. Additional information about our liquidity and how we manage this risk can be found in the Financial Resources and Liquidity section within the MD&A.

The actions below are consistent with our strategy of reducing GECC ENI and investing in our core businesses.

OTHER TRENDS & DEVELOPMENTS

| · | Milestone Aviation Group – On January 30, 2015, GECAS acquired Milestone Aviation Group, a helicopter leasing business, for approximately $1.8 billion. |

| · | Budapest Bank – During the fourth quarter of 2014, we signed an agreement to sell our consumer finance business Budapest Bank to Hungary's government. |

| · | GEMB – Nordic – During the fourth quarter of 2014, we completed the sale of GE Money Bank AB, our consumer finance business in Sweden, Denmark and Norway (GEMB – Nordic) to Santander for proceeds of $2.3 billion. |

| · | Synchrony Financial – On August 5, 2014, we completed the initial public offering (IPO) of our North American Retail Finance business, Synchrony Financial, as a first step in a planned, staged exit from that business. Synchrony Financial closed the IPO of 125 million shares of common stock at a price to the public of $23.00 per share and on September 3, 2014, Synchrony Financial issued an additional 3.5 million shares of common stock pursuant to an option granted to the underwriters in the IPO (Underwriters' Option). We received net proceeds from the IPO and the Underwriters' Option of $2.8 billion, which remain at Synchrony Financial. Following the closing of the IPO and the Underwriters' Option, we currently own approximately 85% of Synchrony Financial and as a result, GECC continues to consolidate the business. The 15% is presented as noncontrolling interests. In addition, in August 2014, Synchrony Financial completed issuances of $3.6 billion of senior unsecured debt with maturities up to 10 years and $8.0 billion of unsecured term loans maturing in 2019, and in October 2014 completed issuances of $0.8 billion unsecured term loans maturing in 2019 under the New Bank Term Loan Facility with third party lenders. Subsequent to December 31, 2014 through February 13, 2015, Synchrony Financial issued an additional $1.0 billion of senior unsecured debt maturing in 2020. |

We are targeting to complete our exit from Synchrony Financial through a split-off transaction, by making a tax-free distribution of our remaining interest in Synchrony Financial to electing GE stockholders in exchange for shares of GE's common stock. The split-off transaction would be subject to obtaining required bank regulatory approvals. We may also decide to exit by selling or otherwise distributing or disposing of all or a portion of our remaining interest in the Synchrony Financial shares.

Page 34

| · | Cembra – During the fourth quarter of 2013, we completed the sale of 68.5% of our Swiss consumer finance bank, Cembra Money Bank AG (Cembra), through an IPO. |

| · | Consumer – During the fourth quarter of 2013, we completed the sale of our remaining equity interest in the Bank of Ayudhya (Bay Bank). We also committed to sell our consumer banking business in Russia (Consumer Russia) and completed the transaction in the first quarter of 2014. |

| · | MetLife Bank – During the first quarter of 2013, we acquired the deposit business of MetLife Bank, N.A., which is an online banking platform with approximately $6.4 billion in U.S. retail deposits that is now part of Synchrony Financial. |

| · | Consumer Ireland – During 2012, we completed the sale of our consumer mortgage lending business in Ireland (Consumer Ireland) and sold our remaining equity interest in Garanti Bank, which was classified as an available-for-sale security. |

| · | U.S. Customer Base – During 2014, GE Capital provided approximately $116 billion of new financings in the U.S. to various companies, infrastructure projects and municipalities. Additionally, we extended approximately $115 billion of credit to approximately 64 million U.S. consumers. GE Capital provided credit to approximately 29,700 new commercial customers and 33,700 new small businesses in the U.S. during 2014, ending the year with outstanding credit to more than 250,000 commercial customers and 220,000 small businesses through retail programs in the U.S. |

Page 35

FINANCIAL OVERVIEW

(Dollars in billions)

| SEGMENT REVENUES & PROFIT(a) | ||

| ||

¢ ¢ Revenue ¢ ¢ Profit | ||

(a)Interest and other financial charges and income taxes are included in determining segment profit for the GE Capital segment. | ||

COMMENTARY: 2014 – 2013 | ||

Revenues decreased 2% as a result of the effects of dispositions, lower gains and the effects of currency exchange, partially offset by organic revenue growth and lower impairments.

| · | CLL 2014 revenues increased 2% as a result of organic revenue growth. |

| · | Consumer 2014 revenues decreased by $0.7 billion, or 5%, as a result of lower gains ($0.6 billion) and the effects of dispositions ($0.3 billion), partially offset by organic revenue growth ($0.2 billion) and lower impairments ($0.1 billion). |

| · | Energy Financial Services 2014 revenues increased by $0.2 billion, or 11% as a result of organic revenue growth ($0.4 billion) and higher gains ($0.1 billion), partially offset by the effects of dispositions ($0.2 billion) and higher impairments ($0.2 billion). |

| · | GECAS 2014 revenues decreased by $0.1 billion, or 2%, as a result of organic revenue declines ($0.2 billion), partially offset by higher gains ($0.1 billion). |

Segment profit decreased 10% as a result of the effects of dispositions, lower gains and the effects of currency exchange, partially offset by lower impairments, lower provisions for losses on financing receivables and core increases.

| · | CLL 2014 net earnings increased 2% as a result of lower provisions for losses on financing receivables, partially offset by core decreases. |

| · | Consumer 2014 net earnings decreased by $1.3 billion, or 30%, as a result of the effects of dispositions ($0.8 billion) reflecting the 2013 sale of a portion of Cembra and the 2014 sale of GEMB-Nordic, core decreases ($0.5 billion) and lower gains ($0.4 billion) reflecting the 2013 sale of our remaining equity interest in Bay Bank, partially offset by lower provisions for losses on financing receivables ($0.3 billion) and lower impairments ($0.1 billion). |

| · | Energy Financial Services 2014 net earnings decreased slightly as a result of higher impairments ($0.1 billion) and the effects of dispositions ($0.1 billion) offset by core increases ($0.1 billion) and higher gains ($0.1 billion). |

| · | GECAS 2014 net earnings increased by $0.2 billion, or 17%, as a result of lower equipment leased to others (ELTO) impairments ($0.2 billion) related to our operating lease portfolio of commercial aircraft, and higher gains, partially offset by core decreases ($0.1 billion). |

Page 36

| COMMENTARY: 2013 – 2012 |

Revenues increased 2% as a result of higher gains, the effects of dispositions and lower impairments, partially offset by organic revenue declines.

| · | CLL 2013 revenues decreased 2% as a result of organic revenue declines. |

| · | Consumer 2013 revenues increased by $0.4 billion, or 3%, as a result of higher gains ($0.5 billion), the effects of dispositions ($0.3 billion) and the effects of acquisitions ($0.1 billion), partially offset by organic revenue declines ($0.4 billion). |

| · | Energy Financial Services 2013 revenues increased slightly, or 1%, as a result of dispositions ($0.1 billion) and organic revenue growth ($0.1 billion), partially offset by lower gains ($0.1 billion) and higher impairments. |

| · | GECAS 2013 revenues increased by $0.1 billion, or 1%, as a result of lower finance lease impairments and higher gains. |

Segment profit increased 6% as a result of the effects of dispositions, primarily related to the sale of a portion of Cembra through an IPO and higher gains, primarily related to the sale of our remaining equity interest in Bay Bank, partially offset by higher provisions for losses on financing receivables, core decreases and higher impairments.

| · | CLL 2013 net earnings increased 8% as a result of core increases. |