Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 14A

Proxy Statement Pursuant to Section 14(a)

of the Securities Exchange Act of 1934

Filed by the Registrant

☒

Filed by a Party other than the Registrant

☐

Check the appropriate box:

☐ | Preliminary Proxy Statement | |

☐ | Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) | |

☒ | Definitive Proxy Statement | |

☐ | Definitive Additional Materials | |

☐ | Soliciting Material under §240.14a-12 |

Ally Financial Inc.

(Name of Registrant as Specified In Its Charter)

(Name of Person(s) Filing Proxy Statement, if other than the Registrant)

Payment of Filing Fee (Check all boxes that apply):

☒ | No fee required | |

☐ | Fee paid previously with preliminary materials. | |

☐ | Fee computed on table in exhibit required by Item 25(b) per Exchange Act Rules 14a-6(i)(1) and0-11. |

Table of Contents

Table of Contents

a message from our CEO.

March 21, 2023

| Dear Fellow Stockholders:

We are pleased to invite you to Ally Financial Inc.’s 2023 Annual Meeting of Stockholders. The meeting will be held at the JW Marriott Charlotte, 600 South College Street, Charlotte, North Carolina 28202, on May 3, 2023, at 9:00 a.m. Eastern Daylight Time.

We use the internet as our primary means of furnishing proxy materials to our stockholders, including the notice and proxy statement, a proxy card, and our 2022 annual report. The notice and proxy statement contain important information about proxy voting and the business to be conducted at the meeting. Whether or not you plan to attend the meeting, please vote as promptly as possible to make sure your vote is counted. Every stockholder vote is important, and we want to ensure your shares are represented at the meeting.

In 2022, we exhibited another year of steady execution and delivered solid financial results. The strength and agility of our business model have been demonstrated as we’ve navigated a constantly changing operating environment while simultaneously growing customers, enhancing our digital capabilities, optimizing the balance sheet, and diversifying revenues.

Our long-term success is underpinned by our purpose-driven ‘Do It Right’ culture and relentless focus on delivering for our customers, employees, and communities. For our customers, we introduced CoverDraft, a service that further enhances overdraft protection, building on our decision to eliminate overdraft fees. For our employees, we increased our minimum wage to $23 per hour and announced another year of #OwnIt grants, which further instill an ownership mentality across the organization. And within the communities in which we live and work, Ally teammates volunteered over 44,000 hours of their time, including 2,300 hours dedicated to environmental causes in support of our “Green Teams” initiative.

Staying true to our inclusive culture and LEAD core values has been a key element of our execution against long-term priorities in the past and position us to continue delivering strong financial results and long-term value for our stockholders in the years ahead. | |

Thank you for your continued support of Ally Financial Inc.

Sincerely,

Jeffrey J. Brown Chief Executive Officer | ||

Table of Contents

notice of annual meeting

DATE: DATE: |  TIME: TIME: |

| ||

| Wednesday, May 3, 2023 | 9:00 a.m. Eastern Daylight Time | JW Marriott Charlotte 600 South College Street Charlotte, North Carolina 28202 |

LOCATION:

LOCATION:Matters to be voted on

1. Election of directors |

2. Advisory vote on executive compensation |

3. Ratification of the Audit Committee’s engagement of Deloitte & Touche LLP as the Company’s independent registered public accounting firm for 2023 |

4. Such other business as may properly come before the meeting |

Jeffrey A. Belisle

Corporate Secretary

March 21, 2023

Only stockholders of record at the close of business on March 7, 2023, the record date fixed by the Board of Directors of the Company, will be entitled to notice of and to vote at the meeting or any adjournment thereof. A list of all stockholders of record entitled to vote is on file at the principal executive office of the Company located at 500 Woodward Avenue, MC: MI-01-10-CORPSEC, Detroit, Michigan 48226.

We use the internet as our primary means of furnishing proxy materials to our stockholders, including the notice and proxy statement, a proxy card, and our 2022 annual report. Consequently, most stockholders will not receive paper copies of our proxy materials. We will instead send these stockholders a notice with instructions for accessing the proxy materials and voting via the internet. The notice will also explain how stockholders may obtain paper copies of our proxy materials if they so choose. Internet transmission and voting are designed to be efficient, minimize cost, and conserve natural resources.

Voting procedures are described in the proxy statement. No stockholder has a dissenter’s right of appraisal or similar right in connection with any of the proposals. If you wish to attend the meeting in person, you will need to follow the instructions set forth on page 3 of the proxy statement and otherwise satisfy the eligibility criteria described there. |  |

Table of Contents

table of contents

| GENERAL INFORMATION ABOUT THE ANNUAL MEETING | 1 | |||

| PROPOSAL 1 – ELECTION OF DIRECTORS | 5 | |||

| 5 | ||||

| 7 | ||||

| BOARD GOVERNANCE MATTERS | 15 | |||

| 15 | ||||

| 15 | ||||

| 15 | ||||

| 19 | ||||

| 20 | ||||

| 20 | ||||

| CORPORATE SOCIAL RESPONSIBILITY | 21 | |||

| DIRECTOR COMPENSATION | 26 | |||

| OTHER GOVERNANCE POLICIES AND PRACTICES | 28 | |||

| 28 | ||||

| 28 | ||||

| 29 | ||||

| 29 | ||||

| 29 | ||||

| STOCK OWNERSHIP | 30 | |||

| 30 | ||||

Security Ownership of Directors, Nominees, and Executive Officers | 31 | |||

| COMPENSATION DISCUSSION AND ANALYSIS | 33 | |||

| 34 | ||||

| 35 | ||||

| 37 | ||||

| 39 | ||||

| 40 | ||||

| 44 | ||||

| 50 | ||||

| 52 | ||||

| 52 | ||||

Table of Contents

proxy statement

General Information About the Annual Meeting

|

|

|

| |||||||||

Date and Time: Wednesday, May 3, 2023, at 9:00 a.m. EDT | Location: JW Marriott Charlotte 600 South College Street Charlotte, North Carolina 28202

| Record Date: March 7, 2023 | Proxy Mail Date: On or about March 21, 2023 | |||||||||

Solicitation

The solicitation of your proxy is made on behalf of the Board of Directors of Ally Financial Inc. (Board) for use at our 2023 annual meeting of stockholders to be held on May 3, 2023, and any adjournment of the meeting (Annual Meeting). References in this proxy statement to we, us, our, the Company, and Ally refer to Ally Financial Inc. and its consolidated subsidiaries, unless the context requires otherwise.

This proxy statement and the related form of proxy will first be sent or given on or about March 21, 2023, to the stockholders of record of our common stock at the close of business on March 7, 2023 (record date). This proxy statement and our annual report for the year ended December 31, 2022, also will first be made available on our website at www.ally.com/about/investor/sec-filings/, free of charge, at or about the same time.

The complete mailing address of the Company’s principal executive office is 500 Woodward Avenue, MC: MI-01-10-CORPSEC, Detroit, Michigan 48226. The Annual Meeting will be held at the JW Marriott Charlotte, 600 South College Street, Charlotte, North Carolina 28202.

Electronic Availability of Proxy Materials for the Annual Meeting

Important Notice Regarding the Availability of Proxy Materials for the Stockholder Meeting To Be Held on May 3, 2023. This proxy statement, our annual report to stockholders for fiscal year 2022, and our Form 10-K for fiscal year 2022 are available electronically at www.proxyvote.com/ALLY.

Voting Rights and Procedures

Stockholders of record at the close of business on the record date may vote at the Annual Meeting. As of the record date, 300,810,824 shares of our common stock were issued and outstanding and, therefore, eligible to be voted at the Annual Meeting. Only one class of our common stock exists, and each share is entitled to one vote.

Stockholders of record or record holders have shares of our common stock registered in their names with our transfer agent, Computershare Inc. Beneficial owners, in contrast, own shares of our common stock that are held in “street name” through a broker, bank, or other nominee. Beneficial owners generally cannot vote their shares directly and must instead instruct their brokers, banks, or other nominees how to vote the shares. If you are a beneficial owner of our common stock, your proxy is being solicited through your broker, bank, or other nominee.

| 2023 Proxy Statement | 1 |

Table of Contents

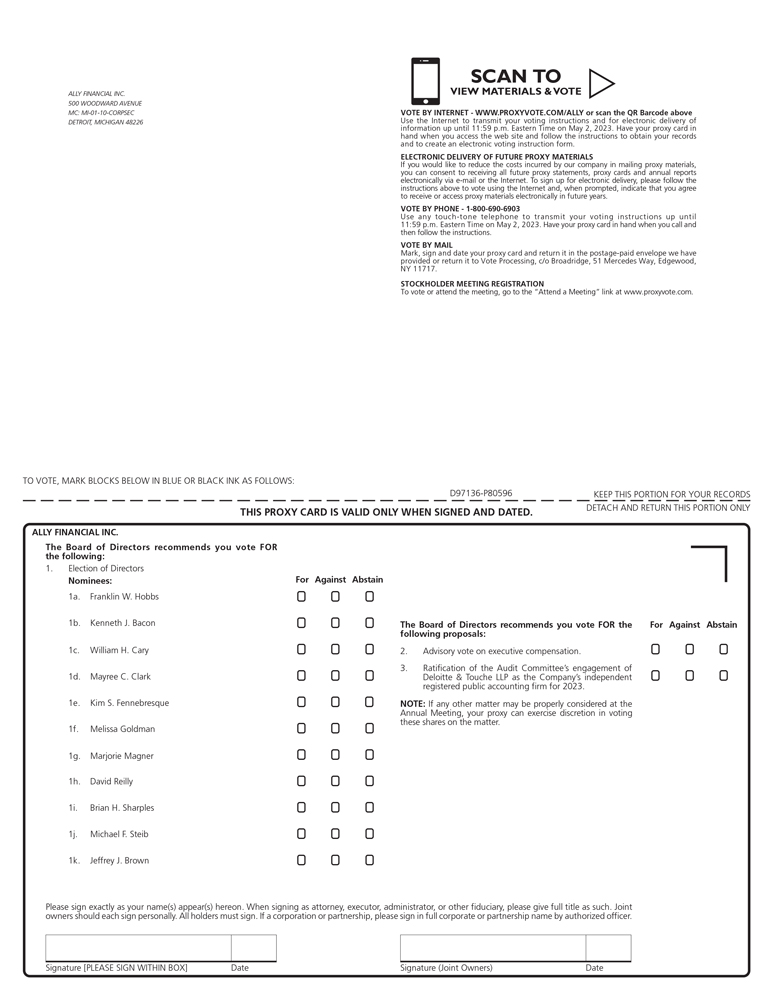

You may vote FOR, AGAINST, or ABSTAIN on each of the three proposals. The Board recommends that you vote as follows:

| Board Voting Recommendations | ||

Proposal 1 | FOR the election of each of the 11 nominees to our Board. | |

Proposal 2 | FOR the advisory resolution approving the compensation paid to our named executive officers. | |

Proposal 3 | FOR the ratification of the Audit Committee’s engagement of Deloitte & Touche LLP as the Company’s independent registered public accounting firm for 2023. | |

When this proxy statement was printed, we did not know of any matter to be presented at the Annual Meeting other than these three proposals. If any other matter may be properly considered at the Annual Meeting, your proxy can exercise discretion in voting your shares on the matter. We currently do not anticipate that any other matter will be presented at the Annual Meeting.

We expect that the election of directors in Proposal 1 will be uncontested—that is, an election where the number of properly nominated director candidates does not exceed the number of directors to be elected. In that case, each director will be elected by a majority of the votes cast with respect to the director. This means that the number of votes cast FOR a director nominee must exceed the number of votes cast AGAINST that director nominee. If an incumbent director nominee fails to receive a majority of the votes cast in an uncontested election, our director resignation policy will apply as described further in Proposal 1. Voting ABSTAIN on Proposal 1 in an uncontested election will have no effect on the outcome.

If the election of directors in Proposal 1 unexpectedly becomes contested—that is, an election where the number of properly nominated director candidates exceeds the number of directors to be elected—plurality voting will apply. This means that the seats on the Board will be filled by the director nominees who receive the highest number of FOR votes. Voting AGAINST or ABSTAIN in a contested election will have no effect on the outcome.

For Proposals 2 and 3, a FOR vote from a majority of the outstanding shares present or represented by proxy at the Annual Meeting and entitled to vote on the proposal will be required for approval. Voting ABSTAIN on any of these proposals will have the same effect as voting AGAINST.

We strongly encourage all stockholders to submit their votes in advance of the Annual Meeting, even if you are planning to attend in person.

Internet |

Telephone |

|

In Person |

If you are a record holder, you may vote your shares (1) through the internet, (2) by telephone, (3) by completing, signing, dating, and returning your proxy card in the provided envelope, or (4) in person by ballot at the Annual Meeting. Other proxy materials that you receive together with this proxy statement contain the website address and the telephone number for internet or telephone voting. Internet or telephone votes or completed, signed, and dated proxy cards must be received prior to the Annual Meeting in order to be counted. If you as a record holder submit a valid proxy prior to the Annual Meeting but do not provide voting instructions, your shares will be voted according to the recommendations of the Board described earlier in this section.

If you are a beneficial owner, you may not vote your shares directly but instead may instruct your broker, bank, or other nominee how to vote your shares. You should receive materials from your broker, bank, or other nominee with directions on how to provide voting instructions. Those materials also will identify the time by which your broker, bank, or other nominee must receive your voting instructions. The availability of internet or telephone voting will depend on the processes adopted by your broker, bank, or other nominee. If you want to vote your shares in person at the Annual Meeting, you will need to obtain a legally enforceable proxy from your broker, bank, or other nominee in advance and present that proxy to the inspectors of election together with a valid form of government-issued photo identification (such as a driver’s license or passport). For Proposals 1 and 2, if you are a beneficial owner of shares, your broker, bank, or other nominee is not permitted to vote your shares if no instruction is received from you. For Proposal 3, your broker, bank, or other nominee can exercise discretion in voting your shares if no instruction is received from you.

| 2023 Proxy Statement | 2 |

Table of Contents

You may revoke or change your proxy at any time before the vote is taken at the Annual Meeting. If you are a record holder, you may revoke or change your proxy by (1) executing and delivering a later-dated proxy for the same shares in compliance with the requirements described in this proxy statement, (2) voting the same shares again over the internet or telephone prior to the Annual Meeting, (3) voting a ballot at the Annual Meeting, or (4) notifying the Secretary of your revocation of the proxy prior to the Annual Meeting. If you are a beneficial owner, you must follow the directions provided to you by your broker, bank, or other nominee. Any beneficial owner of shares who wants to revoke a proxy at the Annual Meeting will need to present to the inspectors of election a legally enforceable proxy from the broker, bank, or other nominee indicating that the person is the beneficial owner of the shares together with a valid form of government-issued photo identification (such as a driver’s license or passport).

We will pay the costs of preparing the proxy materials and soliciting proxies, including the reasonable charges and expenses of brokers, banks, and other nominees for forwarding proxy materials to beneficial owners and updating proxy cards and directions. In addition to our solicitation of proxies, your proxy may be solicited by telephone, facsimile, internet, or e-mail or in person by directors, officers, or regular employees of Ally or its affiliates who will receive no additional compensation for doing so.

Internet and telephone voting procedures are designed to authenticate stockholders’ identities, allow stockholders to provide their voting instructions, and confirm that stockholders’ instructions have been recorded properly. While we and Broadridge Financial Solutions, Inc. do not charge stockholders any fees for voting by internet or telephone, there may still be costs—such as usage charges from internet-service providers and telephone companies—for which stockholders are responsible when voting by internet or telephone.

Meeting Admission

Attendance at the Annual Meeting will be limited to stockholders of record or their proxies, beneficial owners of our common stock, and our guests. A record holder or beneficial owner must request an admission ticket in advance by visiting www.proxyvote.com/ally and following the instructions provided, which will require the 16-digit number included on your proxy card or voting instructions. Requests for admission tickets will be processed in the order in which they are received and must be submitted no later than May 1, 2023. At the Annual Meeting, each record holder, beneficial owner, or guest may be required to present a valid form of government-issued photo identification, such as a driver’s license or passport, to gain admittance.

Cautionary Notice About Forward-Looking Statements and Other Terms

This proxy statement and related communications contain forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. These statements can be identified by the fact that they do not relate strictly to historical or current facts — such as statements about the outlook for financial and operating metrics and performance, and future capital allocation and actions. Forward-looking statements often use words such as “believe,” “expect,” “anticipate,” “intend,” “pursue,” “seek,” “continue,” “estimate,” “project,” “outlook,” “forecast,” “potential,” “target,” “objective,” “trend,” “plan,” “goal,” “initiative,” “priorities,” or other words of comparable meaning or future-tense or conditional verbs such as “may,” “will,” “should,” “would,” or “could.” Forward-looking statements convey our expectations, intentions, or forecasts about future events, circumstances, or results. All forward-looking statements, by their nature, are subject to assumptions, risks, and uncertainties, which may change over time and many of which are beyond our control. You should not rely on any forward-looking statement as a prediction or guarantee about the future.

Actual future objectives, strategies, plans, prospects, performance, conditions, or results may differ materially from those set forth in any forward-looking statement. Some of the factors that may cause actual results or other future events or circumstances to differ from those in forward-looking statements are described in our Annual Report on Form 10-K for the year ended December 31, 2022, our subsequent Quarterly Reports on Form 10-Q or Current Reports on Form 8-K, or other applicable documents that are filed or furnished with the U.S. Securities and Exchange Commission (collectively, our SEC filings). Any forward-looking statement made by us or on our behalf speaks only as of the date that it was made. We do not undertake to update any forward-looking statement to reflect the impact of events, circumstances, or results that arise after the date that the statement was made, except as required by applicable securities laws. You, however, should consult further disclosures (including disclosures of a forward-looking nature) that we may make in any subsequent SEC filings.

This proxy statement and related communications contain specifically identified non-GAAP financial measures, which supplement the results that are reported according to U.S. generally accepted accounting principles (GAAP). These non-GAAP financial

| 2023 Proxy Statement | 3 |

Table of Contents

measures may be useful to investors but should not be viewed in isolation from, or as a substitute for, GAAP results. Differences between non-GAAP financial measures and comparable GAAP financial measures are reconciled in this proxy statement or the related communication.

Unless the context otherwise requires, the following definitions apply. The term “loans” means the following consumer and commercial products associated with our direct and indirect financing activities: loans, retail installment sales contracts, lines of credit, and other financing products excluding operating leases. The term “operating leases” means consumer- and commercial-vehicle lease agreements where Ally is the lessor and the lessee is generally not obligated to acquire ownership of the vehicle at lease-end or compensate Ally for the vehicle’s residual value. The terms “lend,” “finance,” and “originate” mean our direct extension or origination of loans, our purchase or acquisition of loans, or our purchase of operating leases as applicable. The term “consumer” means all consumer products associated with our loan and operating-lease activities and all commercial retail installment sales contracts. The term “commercial” means all commercial products associated with our loan activities, other than commercial retail installment sales contracts. The term “partnerships” means business arrangements rather than partnerships as defined by law.

| 2023 Proxy Statement | 4 |

Table of Contents

proposal 1

election of directors

Board Composition

The Board currently has 12 seats and, effective at the time of the election of directors at the Annual Meeting, will have 11 seats. The Board believes that this size is appropriate at the present time based on its assessment of the need for particular talents or other qualities, the benefits associated with a diversity of perspectives and backgrounds, the availability of qualified candidates, the workloads and needs of the Board’s committees, and other relevant factors. The Board also assesses whether its composition, governance structure, and practices support Ally’s safety and soundness and its ability to promote compliance with applicable law while taking into account its asset size, complexity, scope of operations, risk appetite, risk capacity, and changes in these factors. All seats on the Board are up for election annually. The Compensation, Nominating, and Governance Committee (CNGC) has recommended, and the Board has nominated, the following slate of 11 director candidates for election at the Annual Meeting to hold office until the next annual meeting of stockholders in 2024. Each has agreed to be nominated and named in this proxy statement and to serve if elected. This slate comprises all of the current directors of Ally, except for Maureen A. Breakiron-Evans, who will retire from the Board at the time of the election of directors at the Annual Meeting.

Nominee/Principal Occupation | Age | Director Since | Independent | Audit Committee | Risk Committee | Technology Committee | CNGC | |||||||||||||||||||||

Franklin W. Hobbs Former President and CEO, Ribbon Communications | 75 | 2009 | Yes | ∎ | ||||||||||||||||||||||||

Kenneth J. Bacon Former Executive Officer, Fannie Mae | 68 | 2015 | Yes | Chair | ||||||||||||||||||||||||

William H. Cary Former Executive Officer, General Electric | 63 | 2016 | Yes | Chair | ||||||||||||||||||||||||

Mayree C. Clark Former Executive Officer, Morgan Stanley | 66 | 2009 | Yes | ∎ | ∎ | |||||||||||||||||||||||

Kim S. Fennebresque Former Chairman and CEO, Cowen Group | 72 | 2009 | Yes | ∎ | Chair | |||||||||||||||||||||||

Melissa Goldman Current VP, Corporate Engineering Google, LLC | 51 | 2022 | Yes | ∎ | ∎ | |||||||||||||||||||||||

Marjorie Magner Former Executive Officer, Citigroup | 73 | 2010 | Yes | ∎ | ∎ | |||||||||||||||||||||||

David Reilly Former CIO, Global Banking and Markets Bank of America | 59 | 2022 | Yes | ∎ | ∎ | |||||||||||||||||||||||

Brian H. Sharples Former Chairman and CEO, HomeAway | 62 | 2018 | Yes | ∎ | ∎ | |||||||||||||||||||||||

Michael F. Steib Current CEO, Artsy | 46 | 2015 | Yes | ∎ | Chair | |||||||||||||||||||||||

Jeffrey J. Brown Current CEO, Ally Financial | 50 | 2015 | No | |||||||||||||||||||||||||

Number of meetings in 2022 | 9 | 5 | 5 | 7 | ||||||||||||||||||||||||

| 2023 Proxy Statement | 5 |

Table of Contents

Proposal 1 – Election of Directors | Board Governance Matters | Corporate Social Responsibility | Director Compensation | Other Governance Policies and Practices | Stock Ownership | Compensation | Proposal 2 – Advisory Vote | Proposal 3: Engagement of Auditors | Other Matter |

We expect that this will be an uncontested election of directors—that is, an election where the number of properly nominated director candidates does not exceed the number of directors to be elected. In that case, under our Bylaws, each director will be elected by a majority of the votes cast with respect to the director. A “majority of the votes cast” means that the number of shares voted FOR a director nominee must exceed the number of shares voted AGAINST that director nominee. Voting ABSTAIN in an uncontested election will have no effect on the outcome.

Under Delaware law and our Bylaws, each director will hold office until a successor is duly elected and qualified or until the director’s earlier death, resignation, or removal. The Company has adopted a director resignation policy providing that, if an incumbent director nominee fails to receive a majority of the votes cast in an uncontested election, the director must promptly tender a notice of resignation to the Company’s Chief Executive Officer (CEO) or Secretary, which will become effective only upon acceptance by the Board. The CEO or the Secretary, as applicable, will relay a copy of the notice to the Chair of the Board and the Chair of the CNGC. The CNGC will make a recommendation to the Board as to whether the resignation should be accepted or rejected or whether other action should be taken. The affected director will not take part in any deliberations or actions of the CNGC or the Board relating to the resignation. Within 90 days following certification of the election results, the Board will act on the resignation, taking into account the CNGC’s recommendation and any other information judged by the Board to be relevant, and publicly disclose its decision in a filing with the U.S. Securities and Exchange Commission (SEC). If the Board rejects the director’s resignation, under Delaware law, the director will continue to serve on the Board. If the Board accepts the director’s resignation, the Board may fill the resulting vacancy or may reduce the size of the Board.

If the election of directors unexpectedly becomes contested—that is, an election where the number of properly nominated director candidates exceeds the number of directors to be elected—plurality voting will apply under our Bylaws. “Plurality voting” means that the seats on the Board will be filled by the director nominees who receive the highest number of FOR votes. Voting AGAINST or ABSTAIN in a contested election will have no effect on the outcome.

No cumulative voting rights exist in this election. If you are a beneficial owner of shares, your broker, bank, or other nominee is not permitted to vote your shares on this matter if no instruction is received from you.

We do not anticipate that any nominee will become unavailable for election. If that were to happen for any reason, however, the shares represented by proxies and voting for a nominee who unexpectedly becomes unavailable will be voted instead for a substitute candidate nominated by the Board, unless the Board elects to reduce its size.

The Board recommends that stockholders vote FOR the election of each of the 11 nominees to our Board.

| 2023 Proxy Statement | 6 |

Table of Contents

Proposal 1 – Election of Directors | Board Governance Matters | Corporate Social Responsibility | Director Compensation | Other Governance Policies and Practices | Stock Ownership | Compensation | Proposal 2 – Advisory Vote | Proposal 3 – Engagement of Auditors | Other Matter |

Director Qualifications and Responsibilities

The CNGC and the Board believe that the Company’s directors should possess a diverse array of backgrounds, skills, and qualifications, whether in terms of education, business acumen, accounting and financial expertise, risk-management experience, or experience with other organizations. When considering director candidates, the CNGC and the Board take into account these factors as well as other characteristics that, in their judgment, will enhance the effectiveness of the Board. These characteristics include independence, the ability to understand Ally’s primary risks and to advise management on Ally’s strategic plan and objectives in the context of its risk profile, the ability to make independent and disinterested decisions in the balanced and best interests of Ally’s stockholders as a whole, the ability and willingness to devote sufficient time and attention to Ally, personal and professional integrity, honesty, ethics, and values, and the candidate’s overall fit within the existing mix of director characteristics. While not intended to be exhaustive, the following matrix highlights a number of relevant skills and qualifications possessed by some or all of the 11 nominees.

Skills and Qualifications |  |  |  |  |  |  |  |  |  |  |  | |||||||||||

Senior Executive Leadership 100% | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | |||||||||||

Financial-Services Industry 82% | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | |||||||||||||

Regulatory / Governmental 82% | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | |||||||||||||

Risk Management 100% | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | |||||||||||

Finance / Accounting 73% | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ||||||||||||||

Other Public-Company Board 73% | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ||||||||||||||

Technology 82% | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | |||||||||||||

In addition, the CNGC and the Board consider diversity in the characteristics of director candidates, including each candidate’s perspective and background, with the ultimate aim of enhancing the Board’s ability to perform its oversight function most effectively. The CNGC and the Board strive to complement the institutional knowledge of longer tenured directors with fresh perspectives brought by newer directors and believe that the diversity of our nominees contributes to enhancing the efficacy of the Board, increasing the fundamental value of our Company, and creating long-term value for stockholders.

| 2023 Proxy Statement | 7 |

Table of Contents

Proposal 1 – Election of Directors | Board Governance Matters | Corporate Social Responsibility | Director Compensation | Other Governance Policies and Practices | Stock Ownership | Compensation | Proposal 2 – Advisory Vote | Proposal 3 – Engagement of Auditors | Other Matter |

Diversity Attributes | | | | | | | | | | | | |||||||||||

Age 62 - average age | 75 | 68 | 63 | 66 | 72 | 51 | 73 | 59 | 62 | 46 | 50 | |||||||||||

Tenure 8.5 - average tenure | 2009 | 2015 | 2016 | 2009 | 2009 | 2022 | 2010 | 2022 | 2018 | 2015 | 2015 | |||||||||||

Gender | Male | Male | Male | Female | Male | Female | Female | Male | Male | Male | Male | |||||||||||

Race/Ethnicity | White | Black | White | White | White | White | White | White | White | White | White | |||||||||||

In their consideration of director candidates, the CNGC and the Board also take into account the Board’s responsibility to provide direction and oversight for the Company’s business and affairs. In its oversight role, the Board’s primary responsibilities are the following:

| • | overseeing a clear strategy for Ally, including reviewing, advising management on, approving, and monitoring performance against Ally’s strategic plan and objectives while taking into account Ally’s asset size, complexity, scope of operations, risk appetite, risk capacity, and changes in these factors; |

| • | selecting the CEO, and through the CNGC, (a) approving goals and compensation for, and evaluating the performance of, the CEO and other identified members of senior management, (b) overseeing succession plans for the CEO and other identified members of senior management, and (c) overseeing compensation policies relative to risks and applicable law; |

| • | through the Risk Committee (RC), overseeing Ally’s risk-management policies and global risk-management framework, including approving and monitoring a clear risk appetite for Ally that aligns with its strategy and risk capacity and reviewing Ally’s program for managing compliance risk; |

| • | overseeing Ally’s financial performance and condition, and through the Audit Committee (AC), monitoring the integrity of Ally’s financial statements and financial-reporting process and the adequacy of its financial and other internal controls, including disclosure controls and procedures; and |

| • | establishing the proper “tone at the top” for the culture and values of Ally, including approving Ally’s code of conduct and ethics and monitoring management’s promotion of integrity, honesty, and ethical and legal conduct throughout Ally. |

The CNGC and the Board are dedicated to assembling directors who excel in fulfilling these responsibilities, exercise independent leadership and oversight of management, and operate in a cohesive and effective manner. Each director candidate possesses valued backgrounds, skills, qualifications, and other characteristics, and collectively, these director candidates are positioned to meaningfully contribute to increasing the fundamental value of Ally and creating long-term value for stockholders.

The Board has affirmatively determined in its business judgment that each of Mr. Hobbs, Mr. Bacon, Mr. Cary, Ms. Clark, Mr. Fennebresque, Ms. Goldman, Ms. Magner, Mr. Reilly, Mr. Sharples, and Mr. Steib is independent as defined in the New York Stock Exchange (NYSE) listing standards and applicable SEC rules (each independent and an independent director). The Board has determined that Mr. J. Brown, the Company’s CEO, is not independent due to his position as an executive officer of the Company. In evaluating the independence of each director candidate, transactions, relationships, and arrangements between the director candidate or any related person or interest and the Company or any of its subsidiaries were assessed. These included a variety of financial-services relationships—such as deposit accounts and investment services—and six commercial arrangements involving the provision of services in the ordinary course of business to Ally. All of these transactions, relationships, and arrangements were judged to have been made on terms and under circumstances at least as favorable to the Company or its subsidiaries as those that were prevailing at the time for comparable transactions, relationships, or arrangements with unrelated persons or interests or those that would have applied to unrelated persons or interests. In addition, none of these transactions, relationships, or arrangements were determined to require disclosure under Item 404(a) of SEC Regulation S-K. The Board concluded as well that no independent director has a relationship that would interfere with the exercise of independent judgment in carrying out the responsibilities of a director. No familial relationships exist among the directors.

| 2023 Proxy Statement | 8 |

Table of Contents

Proposal 1 – Election of Directors | Board Governance Matters | Corporate Social Responsibility | Director Compensation | Other Governance Policies and Practices | Stock Ownership | Compensation | Proposal 2 – Advisory Vote | Proposal 3 – Engagement of Auditors | Other Matter |

Set forth here is a brief description of the backgrounds and other characteristics of each director candidate. These, along with the skills and qualifications described earlier in this section, led the CNGC and the Board to conclude that the director candidates should be nominated for election at the Annual Meeting.

Director Since: 2009

Ally Board Committees: • Compensation, Nominating, and Governance

Other Public-Company Directorships: • None |

Franklin W. Hobbs

Biographical Information Director of Ally since May 2009 and the current Chairman of the Board. Mr. Hobbs served as President and Chief Executive Officer of Ribbon Communications Inc. from December 2017 through November 2019. Since 2004, he has been an advisor to One Equity Partners LLC. He was previously the Chief Executive Officer of Houlihan Lokey Howard & Zukin. In that role, he oversaw all operations, which included advisory services for mid-market companies involved in mergers and acquisitions and corporate restructurings. He previously was Chairman of UBS AG’s Warburg Dillon Read Inc. unit. Prior to that, he was President and Chief Executive Officer of Dillon, Read & Co. Inc. Mr. Hobbs earned his bachelor’s degree from Harvard College and master’s degree in business administration from Harvard Business School. He currently serves as a director of privately held Amherst Holdings LLC and Basin Holdings LLC. Mr. Hobbs previously served as a director of Lord Abbett & Company from 2000 through 2018, as Chairman of the Supervisory Board of BAWAG P.S.K. from March 2013 through March 2017, as a director of Ribbon Communications Inc. from December 2017 through November 2019, and as a director of Molson Coors Brewing Company from 2005 through May 2020. |

Director Since: 2015

Ally Board Committees: • Risk (Chair)

Other Public-Company Directorships: • Arbor Realty Trust, Inc. (NYSE: ABR) • Comcast Corporation (NASDAQ: CMCSA) • Welltower, Inc. (NYSE: WELL) |

Kenneth J. Bacon

Biographical Information Director of Ally since February 2015. Mr. Bacon is the co-founder and a partner of RailField Realty Partners, a real estate asset management and private-equity firm based in Bethesda, Maryland. Prior to this, he held a number of leadership positions at Fannie Mae, most recently as Executive Vice President of the multi-family mortgage business. He retired from Fannie Mae in 2012 following a 19-year career. Mr. Bacon also held executive positions at Resolution Trust Corporation, Morgan Stanley & Company, Inc., and Kidder Peabody & Co. He currently serves on the public-company boards of Arbor Realty Trust, Inc., Comcast Corporation, and Welltower, Inc., and on the advisory board of Dominium Management, a privately held housing development and management company. He previously served as a director of Bentall Kennedy L.P. until its acquisition by Sun Life Financial of Canada in 2015 and as a director of Forest City Realty Trust, Inc. until its acquisition by Brookfield in 2018. Mr. Bacon earned a bachelor’s degree from Stanford University, a master’s degree in international relations from the London School of Economics, and a master’s degree from Harvard Business School. |

| 2023 Proxy Statement | 9 |

Table of Contents

Proposal 1 – Election of Directors | Board Governance Matters | Corporate Social Responsibility | Director Compensation | Other Governance Policies and Practices | Stock Ownership | Compensation | Proposal 2 – Advisory Vote | Proposal 3 – Engagement of Auditors | Other Matter |

Director Since: 2016

Ally Board Committees: • Audit (Chair)

Other Public-Company Directorships: • Rush Enterprises, Inc. |

William H. Cary

Biographical Information Director of Ally since June 2016. Mr. Cary is a former executive of General Electric (GE). During his 29 years at GE, he held several leadership positions in consumer and wholesale finance, as well as in the areas of finance, risk, and capital markets. His roles included the President and Chief Operating Officer of GE Capital and the President and Chief Executive Officer of GE Money in London. Mr. Cary began his career at Clorox Company. He currently serves on the public-company board of Rush Enterprises, Inc. and is a director of privately held Landmark Financial Services, LLC. Mr. Cary previously served as a director of BRP, Inc. from September 2015 through May 2019. Mr. Cary received his bachelor’s degree in business administration and finance from San Jose State University. |

Director Since: 2009

Ally Board Committees: • Audit • Compensation, Nominating, and Governance

Other Public-Company Directorships: • Deutsche Bank AG (NYSE: DB) |

Mayree C. Clark

Biographical Information Director of Ally since May 2009. Ms. Clark is the founding partner of Eachwin Capital, an investment management organization which currently serves as her family office. Previously, she was a partner and member of the executive committee of AEA Holdings and held a variety of executive positions at Morgan Stanley over a span of 24 years, serving as Global Research Director, Director of Global Private Wealth Management, deputy to the Chairman, President and Chief Executive Officer, and non-executive Chairman of Morgan Stanley Capital International. Since May 2018, Ms. Clark has been a member of the Supervisory Board of Deutsche Bank AG, where she chairs the Risk Committee and is a member of the Nomination Committee and the Strategy Committee. She currently serves as a director of privately held Allvue Systems Holdings, Inc., and previously served as a director of Taubman Centers, Inc. from January 2018 until its acquisition by Simon Property Group, Inc. in December 2020. Ms. Clark is a member of the Council on Foreign Relations. She received her master’s degree in business administration from Stanford University Graduate School of Business and her bachelor’s degree from the University of Southern California. |

| 2023 Proxy Statement | 10 |

Table of Contents

Proposal 1 – Election of Directors | Board Governance Matters | Corporate Social Responsibility | Director Compensation | Other Governance Policies and Practices | Stock Ownership | Compensation | Proposal 2 – Advisory Vote | Proposal 3 – Engagement of Auditors | Other Matter |

Director Since: 2009

Ally Board Committees: • Compensation, Nominating, • Technology

Other Public-Company Directorships: • Albertsons Companies, Inc. (NYSE: ACI) • BAWAG P.S.K. (VIE: BG) • BlueLinx Holdings Inc. (NYSE: BXC) |

Kim S. Fennebresque

Biographical Information Director of Ally since May 2009. Mr. Fennebresque served as Chairman, President, and Chief Executive Officer of Cowen Group, Inc., a multinational investment bank, from 1999 to 2008. Prior to joining Cowen Group, he served as Head of the Corporate Finance and Mergers & Acquisitions departments at UBS, as General Partner and Co-Head of Investment Banking at Lazard Frères & Co., and in various positions at The First Boston Corporation. Mr. Fennebresque is a graduate of Trinity College and Vanderbilt Law School. He currently serves on the public-company boards of Albertsons Companies, Inc. and BlueLinx Holdings Inc., and on the Supervisory Board of BAWAG P.S.K. Mr. Fennebresque formerly served on the boards of Ribbon Communications Inc., Delta Tucker Holdings, Inc., Rotor Acquisition Corp., TEAK Fellowship, Fountain House, and Common Good. |

Director Since: 2022

Ally Board Committees: • Risk • Technology

Other Public-Company Directorships: • None |

Melissa Goldman

Biographical Information Ms. Goldman currently serves as Vice President, Corporate Engineering for Google, LLC, having joined in January 2022. Previously she held several leadership positions with JPMorgan Chase & Co. (JPM), most recently as Managing Director and Global Corporate Chief Information Officer as well as Chief Data Officer. Her responsibilities spanned governance and execution, with a significant focus on the risk and control environment inclusive of cybersecurity. Prior to joining JPM in March 2014, Ms. Goldman served in a number of roles at Goldman Sachs & Co. dating back to 1994, which included various leadership positions within the areas of technology supporting market, credit and liquidity risk, finance, and collateral management. She began her career as a consultant with Andersen Consulting from 1992 through 1994. Ms. Goldman received her bachelor’s degree in applied mathematics and computer science from Carnegie Mellon University in Pittsburgh, Pennsylvania in May 1992. |

| 2023 Proxy Statement | 11 |

Table of Contents

Proposal 1 – Election of Directors | Board Governance Matters | Corporate Social Responsibility | Director Compensation | Other Governance Policies and Practices | Stock Ownership | Compensation | Proposal 2 – Advisory Vote | Proposal 3 – Engagement of Auditors | Other Matter |

Director Since: 2010

Ally Board Committees: • Compensation, Nominating, and Governance • Risk

Other Public-Company Directorships: • None |

Marjorie Magner

Biographical Information Director of Ally since May 2010. Ms. Magner was a founding member of Brysam Global Partners, a specialized private-equity firm investing in financial services, and served as a partner from 2007 through December 2019. Prior to that, she served as Chairman and Chief Executive Officer of the Global Consumer Group at Citigroup. In this position, she was responsible for the company’s operations, serving consumers through retail banking, credit cards, and consumer finance. She earned a bachelor’s degree in psychology from Brooklyn College and a master’s degree from Krannert School of Management at Purdue University. Ms. Magner previously served on the board of Accenture plc from 2006 through January 2019, most recently as lead director, and also previously served on the board of TEGNA Inc. Ms. Magner currently serves as a member of the Brooklyn College Foundation and is on the Dean’s Advisory Council for the Krannert School of Management. |

Director Since: 2022

Ally Board Committees: • Audit • Technology

Other Public-Company • None |

David Reilly

Biographical Information Mr. Reilly is a former executive of Bank of America Corporation (Bank of America). During his 10 years at Bank of America, he held several leadership positions within the technology area, most recently serving as Chief Information Officer, Global Banking & Markets. Prior to joining Bank of America, Mr. Reilly spent 28 years serving in various technology and network security roles with several large financial institutions, including Morgan Stanley, Credit Suisse First Boston, Goldman Sachs Group, Inc., Merrill Lynch & Co, Inc., and HSBC Group. He currently serves as a director for privately held Data Dynamics, Inc. and is a member of the board of NPower, a nonprofit organization. Mr. Reilly began his career upon completing his A-Level schooling in the United Kingdom. |

| 2023 Proxy Statement | 12 |

Table of Contents

Proposal 1 – Election of Directors | Board Governance Matters | Corporate Social Responsibility | Director Compensation | Other Governance Policies and Practices | Stock Ownership | Compensation | Proposal 2 – Advisory Vote | Proposal 3 – Engagement of Auditors | Other Matter |

Director Since: 2018

Ally Board Committees: • Risk • Technology

Other Public-Company • GoDaddy, Inc. (NYSE: GDDY) |

Brian H. Sharples

Biographical Information Director of Ally since August 2018. Mr. Sharples co-founded Twyla, Inc., a privately held online art sales company, serving as its Chairman from October 2016 until December 2018. From April 2004 through September 2016, Mr. Sharples served as co-founder, Chairman, and Chief Executive Officer of HomeAway, Inc., a global online marketplace for the vacation rental industry, and he continued serving as Chairman through January 2017. Prior to this, he served as President and Chief Executive Officer of IntelliQuest Information Group, Inc., a supplier of marketing data and research to technology companies. He began his career as a consultant at Bain & Company, a global management consulting firm, and has engaged in several entrepreneurial and investment activities since that time. Mr. Sharples currently serves on the public-company board of GoDaddy Inc., and previously served on the boards of Yelp Inc., Avalara, Inc., HomeAway, Inc., RetailMeNot, Inc. and Kayak, Inc. He also serves as a director for privately held RVshare LLC. and Design Pickle, LLC. Mr. Sharples earned a bachelor’s degree in math and economics from Colby College and a master’s degree in business administration from the Stanford Graduate School of Business. |

Director Since: 2015

Ally Board Committees: • Technology (Chair) • Risk

Other Public-Company Directorships: • None |

Michael F. Steib

Biographical Information Director of Ally since July 2015. Mr. Steib currently serves as the Chief Executive Officer of Artsy, a leading platform for buying and selling art by the world’s leading artists. He previously served as Chief Executive Officer of XO Group Inc., a consumer internet-service firm that assisted millions of people in planning their weddings. XO Group Inc. was sold in December 2018 to privately held WeddingWire, Inc. He also previously served as Chief Executive Officer at Vente-Privee USA beginning in 2011. Prior to that, he served at Google, Inc. as Director, Google TV Ads from 2007 to 2009 and Managing Director, Emerging Platforms from 2009 to 2011. From 2001 through 2006, Mr. Steib held positions at NBC Universal/General Electric, where he served as General Manager, Strategic Ventures, and prior to that as Vice President, Corporate Development. In addition, he previously worked on the development of new businesses for Walker Digital, LLC and as a management consultant with McKinsey & Company. Mr. Steib is a director for nonprofit Change.org and previously served as Co-Chair of nonprofit Literacy Partners and as Chair of nonprofit Career Gear. Mr. Steib received bachelor’s degrees in economics and international relations from the University of Pennsylvania. |

| 2023 Proxy Statement | 13 |

Table of Contents

Proposal 1 – Election of Directors | Board Governance Matters | Corporate Social Responsibility | Director Compensation | Other Governance Policies and Practices | Stock Ownership | Compensation | Proposal 2 – Advisory Vote | Proposal 3 – Engagement of Auditors | Other Matter |

Director Since: 2015

Ally Board Committees: • None

Other Public-Company Directorships: • None |

Jeffrey J. Brown

Biographical Information Jeffrey J. Brown (JB) was named Chief Executive Officer of Ally Financial Inc. in February 2015, and also serves on its Board of Directors. Mr. Brown is driving Ally’s evolution as a leading digital financial services company. Under his leadership, Ally is building on its strengths in auto financing, retail deposits and corporate financing, as well as diversifying its offerings to include digital wealth management and online brokerage, mortgage products, point-of-sale lending, and credit card. Mr. Brown has deep financial services experience, previously serving in a variety of executive leadership positions at Ally and other leading financial institutions. Prior to being named CEO, Mr. Brown was President and CEO of Ally’s Dealer Financial Services business where he oversaw the auto finance, insurance, and auto servicing operations. Mr. Brown joined Ally in March 2009 as Corporate Treasurer and, in 2011, was named Executive Vice President of Finance and Corporate Planning, leading finance, treasury and corporate-strategy initiatives. Mr. Brown received a bachelor’s degree in economics from Clemson University and an executive master’s degree in business from Queens University in Charlotte. He serves on the board of the Clemson University Foundation and is Chairman of the Queens University of Charlotte Board of Trustees. Mr. Brown previously served as president of the Federal Advisory Council (FAC) for 2021. In 2018, he was appointed by the Board of Directors of the Federal Reserve Bank of Chicago as representative for the Seventh Federal Reserve District. He completed four years of service in 2021. Passionate about diversity and inclusion, he joined the first 150 members of the CEO Action for Diversity & Inclusion pledge, advancing diversity and inclusion in the workplace as a competitive and societal issue. Mr. Brown was honored as CEO of the year by the Thurgood Marshall College Fund in 2019. In 2022, American Banker named Mr. Brown Banker of the Year, recognizing his culture-first approach to leadership, his efforts to spearhead overdraft fee elimination industry-wide, and Ally’s strong growth during his tenure. |

| 2023 Proxy Statement | 14 |

Table of Contents

board governance matters

In identifying and recommending candidates to stand for election to the Board, the CNGC may consider existing directors for renomination and may use search firms or other resources to identify other potential director candidates. The CNGC also considers potential director candidates who are recommended by stockholders in compliance with applicable law and listing rules and our Bylaws. Stockholders desiring to recommend candidates for membership on the Board for consideration by the CNGC should address their recommendations in writing, including all information required by our Bylaws, to the Compensation, Nominating, and Governance Committee of the Board of Directors, Ally Financial Inc., Attention: Corporate Secretary, 500 Woodward Avenue, MC: MI-01-10-CORPSEC, Detroit, Michigan 48226. The CNGC uses the same criteria to evaluate all potential director candidates regardless of how they have been identified.

The effectiveness of these policies and processes for identifying and considering potential director candidates is assessed by the CNGC in connection with its annual evaluation of the performance of the Board and each committee as contemplated by the Board’s Governance Guidelines (Governance Guidelines).

Meeting Attendance

Directors are strongly encouraged to attend each annual meeting of stockholders in order to provide an opportunity for informal communication between directors and stockholders and to enhance the Board’s understanding of stockholder priorities and perspectives. All existing directors, except one with a conflict, attended the last annual meeting of stockholders on May 3, 2022.

The Board met nine times during 2022. Each nominee who is currently a director attended at least 75% of the aggregate of (1) the total number of meetings held in 2022 by the Board during the period when the director was serving in that capacity and (2) the total number of meetings held in 2022 by all applicable committees during the period when the director was serving on those committees.

The Board’s Leadership Structure

Under our Bylaws, a majority of the full Board elects the chairperson. Whenever the chairperson does not qualify as an independent director, the independent directors—by a majority vote at a meeting consisting solely of independent directors—elects one of the independent directors as lead director. Mr. Hobbs serves as the Chairman of the Board and is a non-executive and independent director. Mr. J. Brown is our CEO.

The Board believes that separating the roles of Chairman and CEO is currently in the best interests of the Company and its stockholders because, based on the Company’s present circumstances, the structure provides a balance between strategic development and independent oversight of management. The Board, however, maintains its flexibility to make this determination at any time to provide appropriate leadership for the Company as circumstances warrant.

Our Bylaws provide that the chairperson (or in the chairperson’s absence, the lead director if one exists or, if none exists, an alternate director designated by a majority of the independent directors then present) will preside at Board meetings. Under the Governance Guidelines, the chairperson also has the following responsibilities: (1) serve as a liaison between the independent directors and management, (2) periodically communicate with the CEO to discuss matters of importance to the independent directors, (3) provide for adequate deliberations on all agenda items and other matters properly brought before the Board, and (4) perform other duties that are appropriate for a non-executive chair and that a majority of the independent directors may identify from time to time.

Committees of the Board

The CNGC annually reviews the structure and membership of the Board’s committees and recommends any appropriate changes to the Board. The Board’s governance structure is designed to support effective oversight (including oversight of senior management),

| 2023 Proxy Statement | 15 |

Table of Contents

Proposal 1 – Election of Directors | Board Governance Matters | Corporate Social Responsibility | Director Compensation | Other Governance Policies and Practices | Stock Ownership | Compensation | Proposal 2 – Advisory Vote | Proposal 3 – Engagement of Auditors | Other Matter |

timely access to information, and sound decision-making. The membership of each committee is driven by its purpose, the expertise or experience needed to achieve that purpose, any requirements of applicable law or listing rules, and other factors that are expected to enhance the effectiveness of the committee. The standing committees of the Board are currently the CNGC, the AC, the RC, and the Technology Committee (TC). The membership of these committees during 2022 and the total number of their meetings in 2022 are detailed in the following summaries, except that Katryn (Trynka) Shineman Blake also served as a member of the AC and the TC until her departure from the Board on February 24, 2022, and John J. Stack also served as a member of the AC, the CNGC, and the RC until his departure from the Board on May 3, 2022.

COMPENSATION, NOMINATING, AND GOVERNANCE COMMITTEE

|  |  |  | |||||

Fennebresque (Chair) | Clark | Hobbs | Magner | |||||

Number of Meetings in 2022: 7

The Board has determined that all members of the CNGC are qualified to serve on the CNGC under applicable SEC rules and NYSE listing standards (including the independence and non-employee-director requirements for compensation-committee members).

Responsibilities: The CNGC assists the Board in overseeing:

| • | the accountability of senior management for effectively implementing Ally’s strategy consistent with its risk appetite, while maintaining an effective risk-management framework and system of internal controls, and consistent with safety and soundness and in compliance with applicable laws (including those related to consumer protection) under a range of conditions—particularly through the establishment, maintenance, and administration of Ally’s executive-compensation plans and the evaluation, determination, and approval of goals and compensation of the CEO, the other individuals who are designated as officers or executive officers (together with the CEO, the Executive Officers) under SEC Rule 16a-1 or 3b-7, respectively, and other executives designated by the CNGC as under its purview (together with the Executive Officers, the Purview Executives); |

| • | Ally’s executive-leadership development and succession planning, the compensation of non-employee directors, and the disclosure of executive-compensation matters as required by applicable law; |

| • | Ally’s human-capital management, including diversity, equity, and inclusion programs, and Environmental, Social, and Governance (ESG) strategies, initiatives, and activities; |

| • | the identification of qualified individuals for membership on the Board, evaluations of the performance of the Board, its committees, and management, and the development and administration of corporate-governance guidelines and other corporate-governance practices; and |

| • | the review and evaluation of all related-person transactions to the extent required by Ally’s governing documents or policies or applicable law. |

A narrative description of the processes for considering and determining executive and director compensation—including (1) the CNGC’s authority and the extent to which that authority may be delegated and (2) the roles of Ally’s executive officers and compensation consultants in determining or recommending the amount or form of executive and director compensation—can be found in Compensation Discussion and Analysis and Director Compensation later in this proxy statement.

The CNGC’s policies on the nomination process for directors can be found in Director Qualifications and Responsibilities earlier in this proxy statement.

| 2023 Proxy Statement | 16 |

Table of Contents

Proposal 1 – Election of Directors | Board Governance Matters | Corporate Social Responsibility | Director Compensation | Other Governance Policies and Practices | Stock Ownership | Compensation | Proposal 2 – Advisory Vote | Proposal 3 – Engagement of Auditors | Other Matter |

AUDIT COMMITTEE

|  | |  | |||||

Cary (Chair) | Breakiron-Evans(a) | Clark | Reilly | |||||

| (a) | Ms. Breakiron-Evans will retire from the Board at the time of the election of directors at the Annual Meeting. |

Number of Meetings in 2022: 9

The AC is a separately designated standing audit committee established in accordance with Section 3(a)(58)(A) of the Securities Exchange Act of 1934 as amended (Exchange Act).

The Board has determined that all members of the AC are qualified to serve on the AC under applicable SEC rules and NYSE listing standards (including the independence and financial-literacy requirements for audit-committee members) and have accounting or related financial-management expertise under applicable NYSE listing standards. The Board also has determined that Mr. Cary, Ms. Breakiron-Evans, and Ms. Clark are audit-committee financial experts under applicable SEC rules. None of the members of the AC simultaneously serve on more than three public-company audit committees.

Responsibilities: The AC assists the Board in overseeing:

| • | Ally’s accounting and financial reporting; |

| • | the appointment, qualifications, independence, and performance of Ally’s independent registered public accounting firm; |

| • | Ally’s internal audit function, including by monitoring the qualifications, stature, and independence of the Chief Audit Executive—who is functionally overseen by and has unrestricted access to the AC—and through its Chair, reviewing and approving the appointment, retention, performance evaluation, and compensation of the Chief Audit Executive; |

| • | Ally’s compliance with legal and regulatory requirements; and |

| • | in conjunction with the RC, the effectiveness of Ally’s risk management and internal controls in connection with the foregoing. |

Additional information about the AC can be found in the Audit Committee Report later in this proxy statement.

RISK COMMITTEE

|  | |  |  | ||||||

Bacon (Chair) | Goldman | Magner | Sharples | Steib | ||||||

Number of Meetings in 2022: 5

The RC assists the Board in overseeing Ally’s risk-management policies and global risk-management framework, including its risk-appetite statement and its program for managing compliance risk. More specifically, the RC approves and oversees Ally’s

| 2023 Proxy Statement | 17 |

Table of Contents

Proposal 1 – Election of Directors | Board Governance Matters | Corporate Social Responsibility | Director Compensation | Other Governance Policies and Practices | Stock Ownership | Compensation | Proposal 2 – Advisory Vote | Proposal 3 – Engagement of Auditors | Other Matter |

enterprise-risk-management framework, including the material-risk taxonomy, and approves and monitors a clear risk appetite for Ally that aligns with its strategy and risk capacity. In addition, the RC oversees management’s responsibility for ensuring that the enterprise-risk-management framework is commensurate with Ally’s structure, risk profile, complexity, activities, and size. The RC also monitors the qualifications, stature, and independence of the Chief Risk Officer—who directly reports and has unrestricted access to both the RC and the CEO—and through its Chair, reviews and approves the appointment, retention, performance evaluation, and compensation of the Chief Risk Officer.

Additional information about the RC can be found in Risk Management later in this proxy statement.

TECHNOLOGY COMMITTEE

| | | | | | |||||||

Steib (Chair) | Breakiron-Evans(a) | Fennebresque | Goldman | Reilly | Sharples | |||||||

| (a) | Ms. Breakiron-Evans will retire from the Board at the time of the election of directors at the Annual Meeting. |

Number of Meetings in 2022: 5

The TC assists the Board in overseeing the execution of digital and other technology strategies, the technology infrastructure and significant investments in it, and information-technology and information-security risks (including cybersecurity risk).

The TC reviews, approves, and recommends to the RC a clear information-technology and information-security risk appetite for Ally that aligns with its strategy and risk capacity. The TC also supports the RC in overseeing the management of information-technology and information-security risks commensurate with Ally’s structure, risk profile, complexity, activities, and size.

| 2023 Proxy Statement | 18 |

Table of Contents

Proposal 1 – Election of Directors | Board Governance Matters | Corporate Social Responsibility | Director Compensation | Other Governance Policies and Practices | Stock Ownership | Compensation | Proposal 2 – Advisory Vote | Proposal 3 – Engagement of Auditors | Other Matter |

Risk Management

The Board’s primary responsibilities include, through the RC, overseeing Ally’s risk-management policies and global risk-management framework, including its risk-appetite statement and its program for managing compliance risk, commensurate with its structure, risk profile, complexity, activities, and size.

The RC is composed of only independent directors. Among the RC’s specific duties are the following:

| • | approve and oversee Ally’s enterprise-risk-management framework, including the material-risk taxonomy; |

| • | approve and monitor a clear risk appetite for Ally that aligns with its strategy and risk capacity (including Committee-set limits)—including by acting on recommendations of the TC on the information-technology and information-security risk appetite for Ally—and approve and periodically review other risk-management policies of Ally’s global operations as delegated to it by the Board; |

| • | oversee management’s responsibility for ensuring that the enterprise-risk-management framework is commensurate with Ally’s structure, risk profile, complexity, activities, and size, and in fulfilling these responsibilities, review as appropriate significant information about information-technology and information-security risks that the RC requires to exercise its duties and responsibilities; |

| • | review reports from the Chief Risk Officer on the risk-management policies of Ally’s global operations and the operation of its enterprise-risk-management framework, including reports on risk-management deficiencies, the resolution of those deficiencies, and emerging risks; |

| • | review reports and trends on Ally’s material risks as set forth in its risk-appetite framework and reports from management on its actions to assess, monitor, and control those risks; |

| • | review reports and trends on Ally’s liquidity planning and capital-management processes, and review and approve the contingency-funding plan, any material revisions to it, and stress-test policies and procedures; |

| • | review reports and trends on Ally’s program for managing compliance risk; |

| • | review reports on the new-product-approval process, including risks and performance of high-risk-rated products and alignment to the risk-appetite framework; |

| • | review and approve Ally’s business-continuity-and-testing plans; |

| • | review and approve Ally’s model-risk-management plan, and review reports and trends on Ally’s model-risk-management program; and |

| • | approve Ally’s loan-review plan, and review reports from Ally’s loan-review function. |

Among Ally’s primary types of risk under the material-risk taxonomy is information-technology and information-security risk. As further described in our Annual Report on Form 10-K for the fiscal year ended December 31, 2022, we devote substantial resources to identifying, monitoring, measuring, mitigating, and reporting on information-technology and information-security risk, including in connection with independent third-party assessments, insurance coverage, and training. Further, the TC is charged with reviewing, approving, and recommending to the RC a clear information-technology and information-security risk appetite for Ally that aligns with its strategy and risk capacity. The TC also supports the RC in overseeing the management of information-technology and information-security risks commensurate with Ally’s structure, risk profile, complexity, activities, and size. Senior management briefs the RC, the TC, or the Board on information-security matters at least quarterly.

The RC also meets in joint session with the AC, at least annually, to discuss with management the guidelines and policies for assessing and managing Ally’s exposure to risks, including major financial risk exposures, and the steps management has taken to monitor, control, report on, and, as necessary, disclose those exposures.

In addition, the CNGC is responsible for overseeing the accountability of senior management for effectively implementing Ally’s strategy consistent with its risk appetite, while maintaining an effective risk-management framework and system of internal controls, and consistent with safety and soundness and in compliance with applicable laws (including those related to consumer protection) under a range of conditions—particularly through the establishment, maintenance, and administration of Ally’s executive-compensation plans and the evaluation, determination, and approval of goals and compensation of the CEO and other Purview Executives. The AC correspondingly has responsibility to oversee the effectiveness of Ally’s risk management and internal controls that are designed to (1) safeguard assets, (2) confirm the accuracy and integrity of accounting, financial reporting, and disclosures, (3) maintain compliance with ethical standards, policies, procedures, and applicable laws, (4) promote effectiveness and efficiency of operations, and (5) address any other related matter that the AC judges to be appropriate for its oversight.

| 2023 Proxy Statement | 19 |

Table of Contents

Proposal 1 – Election of Directors | Board Governance Matters | Corporate Social Responsibility | Director Compensation | Other Governance Policies and Practices | Stock Ownership | Compensation | Proposal 2 – Advisory Vote | Proposal 3 – Engagement of Auditors | Other Matter |

While each of these committees is responsible for evaluating specified risks and overseeing the management of those risks, the full Board is regularly updated by management on the state of Ally’s risk appetite, risk capacity, and enterprise-risk-management framework—including management’s ongoing assessment of identified top and emerging risks—and considers them in assessing and directing Ally’s strategy and business. Our independent Chairman and our CEO are individually focused as well on Ally’s risk-management policies and practices. The Chief Risk Officer, Chief Compliance Officer, and Chief Audit Executive each directly report to our CEO.

Communications with the Board

Under the Governance Guidelines, stockholders and other members of the public may communicate with the Board, the Chairman of the Board, any other individual director, the non-management directors as a group, the independent directors as a group, or any committee of the Board by sending written correspondence in care of the Ally Financial Inc. Corporate Secretary, 500 Woodward Avenue, MC: MI-01-10-CORPSEC, Detroit, Michigan 48226. The Secretary will forward correspondence relating to a director’s duties or responsibilities to the specified recipient. Correspondence that is unrelated to a director’s duties and responsibilities may be discarded or otherwise addressed by the Secretary. Any correspondence that expresses a concern about any governance, conduct, ethical, accounting, financial-reporting, or internal-control matter will be addressed as provided in the Governance Guidelines.

Compensation Committee Interlocks and Insider Participation

No person who served as a member of the CNGC during the year ended December 31, 2022—Kim S. Fennebresque, Franklin W. Hobbs, Mayree C. Clark, Marjorie Magner, and John J. Stack—(1) was an officer or employee of the Company during 2022, (2) was a former officer of the Company, or (3) had any relationship requiring disclosure by the Company under any paragraph of Item 404 of SEC Regulation S-K. No executive officer of Ally served on any board of directors or compensation committee of any other entity for which any of our directors served as an executive officer at any time during the year ended December 31, 2022.

| 2023 Proxy Statement | 20 |

Table of Contents

corporate social responsibility

WE STRIVE TO BE A RELENTLESS ALLY FOR SOCIAL AND ENVIRONMENTAL GOOD

Our Four Key Pillars for Social Impact

|  | |

We are relentless allies for our customers’ financial well-being. We are in business because of them and for them. We are committed to delivering innovative products and services that provide them with the confidence and freedom to make positive financial choices. As a leading digital financial-services company, we seek to be accessible to everyone and to continue investing in the future of finance—from our work on rapid product ideation and prototyping to our sponsorship and support of community initiatives designed to inspire transformative advances in banking.

| We are committed to financial and social inclusion through innovative philanthropy and programming that reduces barriers to economic mobility. Our strategy focuses on three core areas: affordable housing, workforce development, and financial literacy. Our commitment is more than financial support. We provide volunteers, technical assistance, mentoring, and more to support marginalized communities. | |

|  | |

| Our employees—11,600+ strong—bring our mantra to “Do It Right” to life for our customers and communities. We emphasize a One Ally culture, grounded in our LEAD core values, where employees are engaged and feel cared for as individuals in an environment that supports all areas of diversity, while continuing to build Ally as a place where employees can pursue a career with meaning and purpose. We are also focused on diverse representation and retention in the workforce—including different genders, races, nationalities, sexual orientations, and other identities—across all levels of the organization from entry level to leadership. | Ally’s commitment to “Do It Right” extends to the conservation of environmental resources to promote a sustainable future for our customers, employees, stockholders, and the communities in which we live and operate. We have recognized the importance of understanding, preparing for and taking timely preventive action against potentially material climate-change impacts. | |

| 2023 Proxy Statement | 21 |

Table of Contents

Proposal 1 – Election of Directors | Board Governance Matters | Corporate Social Responsibility | Director Compensation | Other Governance Policies and Practices | Stock Ownership | Compensation | Proposal 2 – Advisory Vote | Proposal 3 – Engagement of Auditors | Other Matter |

LIVING OUR PURPOSE

We recognize our long-term success is underpinned by the strength of our purpose-driven culture—a culture that we believe sets us apart from the competition and gives us an advantage as we recruit and retain talented team members. Our people-first approach enables a winning, customer-centric philosophy focused on resiliency, adaptability, and a growth-mindset-oriented drive to “Be (Even) Better.” We strive to uphold our mantra to “Do it Right” through decisions and deeds at all levels of the organization, and we collectively commit to work with integrity and accountability and to uphold our core values in the workplace, the marketplace, and the community.

Living our purpose helped deliver meaningful results for our stockholders and make a real difference for our customers, employees, and communities. We made significant strides in diversity, equity, and inclusion, were relentless allies in improving financial education in a challenging economy, reduced our environmental impact, and led the way with new products and services. Here are some of the ways we made an impact in 2022.

| • Owner’s Mindset. For the fourth consecutive year, all active, regular Ally employees were awarded with 100 RSUs through the company’s #OwnIt Annual Grant Program. • Competitive Compensation. In November 2022, we increased the minimum hourly wage for our U.S. employees from $20 to $23. Beginning January 1, 2023, in concurrence with laws in multiple municipalities in which we operate, we began proactively including pay ranges in job postings nationwide. • Employee Engagement. Sustaining high levels of employee engagement is key as we continue to build a company where our employees want to work, have purposeful careers, and feel empowered to make a difference. For 2022, our employee engagement scores were within the top 10% of all global companies that participated in the survey and at least nine points higher than the financial services industry benchmark as measured by our third-party provider. • Mental Health. In 2022, we announced expanded mental health benefits for our employees, their dependents, and immediate household members. This additional benefit will provide up to 16 free counseling sessions for each individual, regardless of their participation in our medical plans, to address on-going community concerns over affordability and access to mental health care and build resiliency among our employee population. | |

| • Introduced CoverDraft. In January 2022 we announced Ally CoverDraft service, which provides a no fee overdraft allowance to our qualifying customers on debit transactions subject to a certain amount. • Early Direct Deposit. As the economic landscape remained turbulent, we introduced Early Direct Deposit, an account feature that allows customers to access qualifying direct deposits up to two days in advance of receipt. | |