Exhibit 99.2

2nd Quarter 2005 Analyst Conference

July 7, 2005

Forward-Looking Statements

Today’s discussion may include “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. Such statements relate to future events and expectations and involve known and unknown risks and uncertainties. Alcoa’s actual results or actions may differ materially from those projected in the forward-looking statements. For a summary of the specific risk factors that could cause results to differ materially from those expressed in the forward-looking statements, please refer to Alcoa’s Form 10-K for the year ended December 31, 2004, in addition to the Quarterly Report on Form 10-Q for the quarter ended March 31, 2005 filed with the Securities and Exchange Commission.

2

Alain J. P. Belda

Chairman and Chief Executive Officer

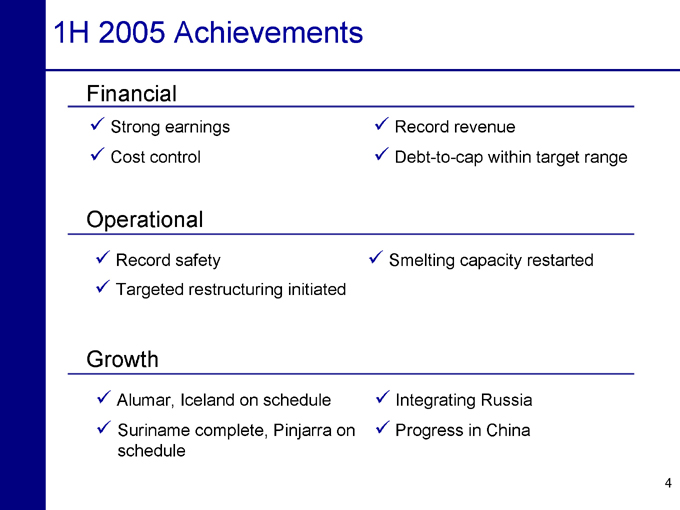

1H 2005 Achievements

Financial

Strong earnings Cost control

Record revenue

Debt-to-cap within target range

Operational

Record safety

Targeted restructuring initiated

Smelting capacity restarted

Growth

Alumar, Iceland on schedule Suriname complete, Pinjarra on schedule

Integrating Russia Progress in China

4

Top Priorities

Capitalize on the current market environment Strong Aero/Commercial Vehicle recovery Robust upstream markets Strong demand in key geographies

Execute the Productivity Projects Further deploy ABS, focused on margin improvement Capture the restructuring benefits Accelerate global competitive sourcing Integrate Russia

Drive growth beyond 2005 Exploit unmatched growth opportunities across the business portfolio Leverage platforms in Brazil, Russia and China to capture share in growth markets

Maintain balance sheet strength Maintain debt-to-cap within target range Manage working capital Ensure that sustaining capital spend is less than depreciation

Manage for the long term Live our values

5

Richard B. Kelson

Executive Vice President and Chief Financial Officer

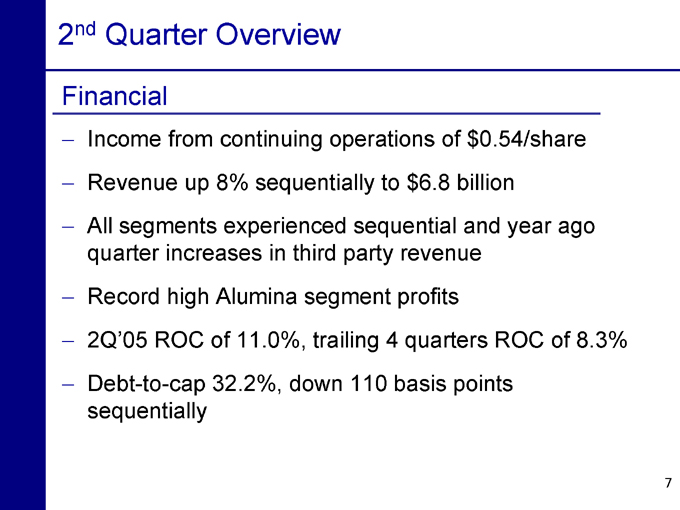

2nd Quarter Overview

Financial

Income from continuing operations of $0.54/share Revenue up 8% sequentially to $6.8 billion All segments experienced sequential and year ago quarter increases in third party revenue Record high Alumina segment profits 2Q’05 ROC of 11.0%, trailing 4 quarters ROC of 8.3% Debt-to-cap 32.2%, down 110 basis points sequentially

7

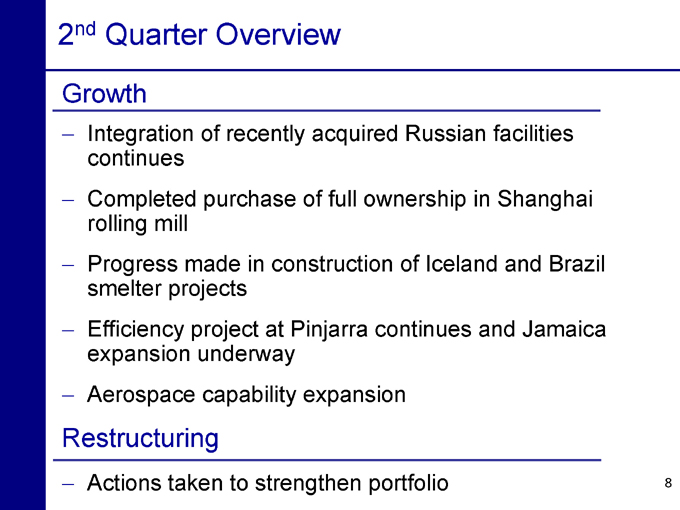

2nd Quarter Overview

Growth

Integration of recently acquired Russian facilities continues Completed purchase of full ownership in Shanghai rolling mill Progress made in construction of Iceland and Brazil smelter projects Efficiency project at Pinjarra continues and Jamaica expansion underway Aerospace capability expansion

Restructuring

Actions taken to strengthen portfolio

8

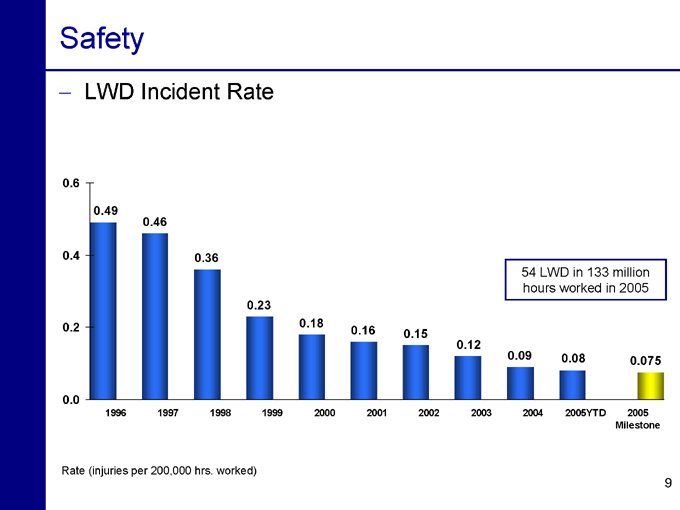

Safety

LWD Incident Rate

0.6 0.4 0.2 0.0

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005YTD 2005 Milestone

0.49 0.46 0.36 0.23 0.18 0.16 0.15 0.12 0.09 0.08 0.075 54 LWD in 133 million hours worked in 2005

Rate (injuries per 200,000 hrs. worked)

9

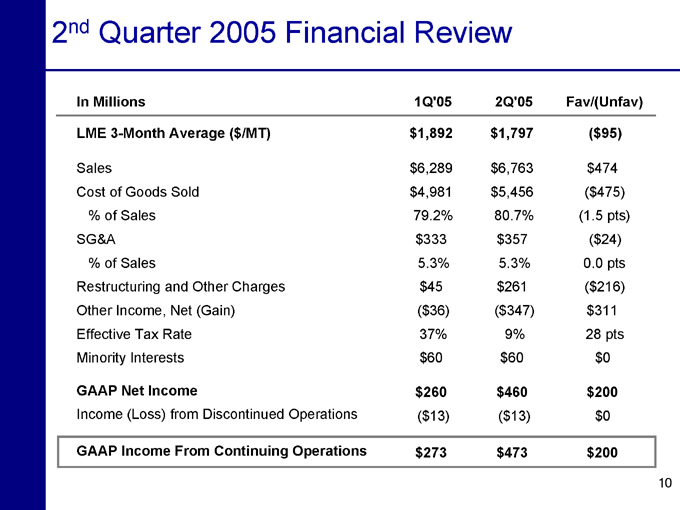

2nd Quarter 2005 Financial Review

In Millions 1Q’05 2Q’05 Fav/(Unfav)

LME 3-Month Average ($/MT) $1,892 $1,797 ($95)

Sales $6,289 $6,763 $474

Cost of Goods Sold $4,981 $5,456 ($475)

% of Sales 79.2% 80.7% (1.5 pts)

SG&A $333 $357 ($24)

% of Sales 5.3% 5.3% 0.0 pts

Restructuring and Other Charges $45 $261 ($216)

Other Income, Net (Gain) ($36) ($347) $311

Effective Tax Rate 37% 9% 28 pts

Minority Interests $60 $60 $0

GAAP Net Income $260 $460 $200

Income (Loss) from Discontinued Operations ($13) ($13) $0

GAAP Income From Continuing Operations $273 $473 $200

10

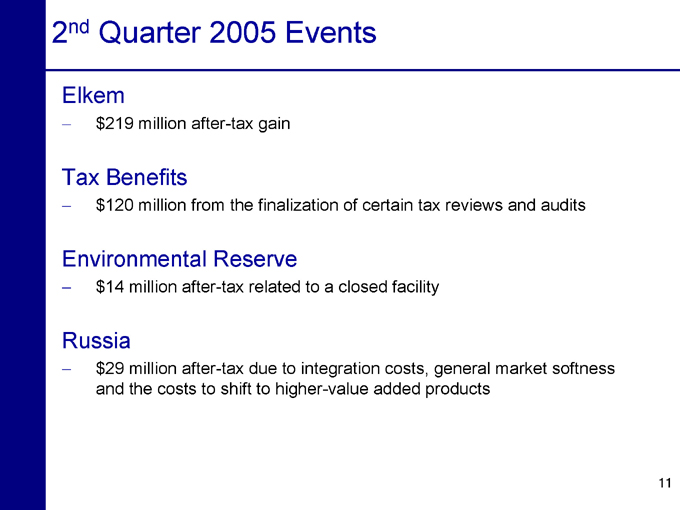

2nd Quarter 2005 Events

Elkem $219 million after-tax gain

Tax Benefits $120 million from the finalization of certain tax reviews and audits

Environmental Reserve $14 million after-tax related to a closed facility

Russia $29 million after-tax due to integration costs, general market softness and the costs to shift to higher-value added products

11

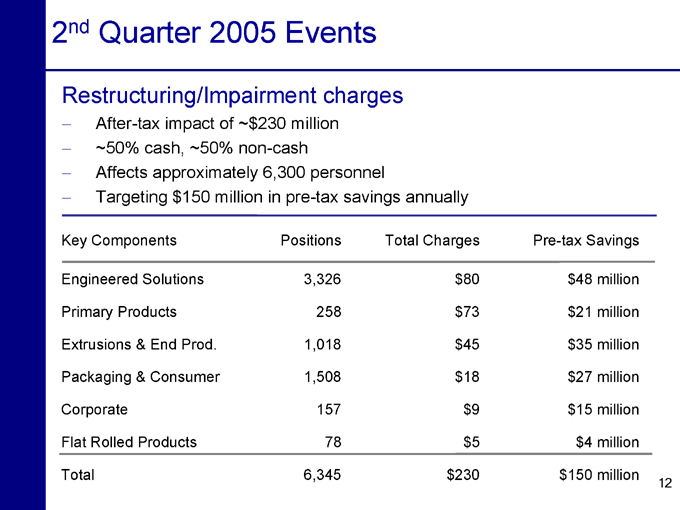

2nd Quarter 2005 Events

Restructuring/Impairment charges

After-tax impact of ~$230 million ~50% cash, ~50% non-cash Affects approximately 6,300 personnel

Targeting $150 million in pre-tax savings annually

Key Components Positions Total Charges Pre-tax Savings

Engineered Solutions 3,326 $80 $48 million

Primary Products 258 $73 $21 million

Extrusions & End Prod. 1,018 $45 $35 million

Packaging & Consumer 1,508 $18 $27 million

Corporate 157 $9 $15 million

Flat Rolled Products 78 $5 $4 million

Total 6,345 $230 $150 million

12

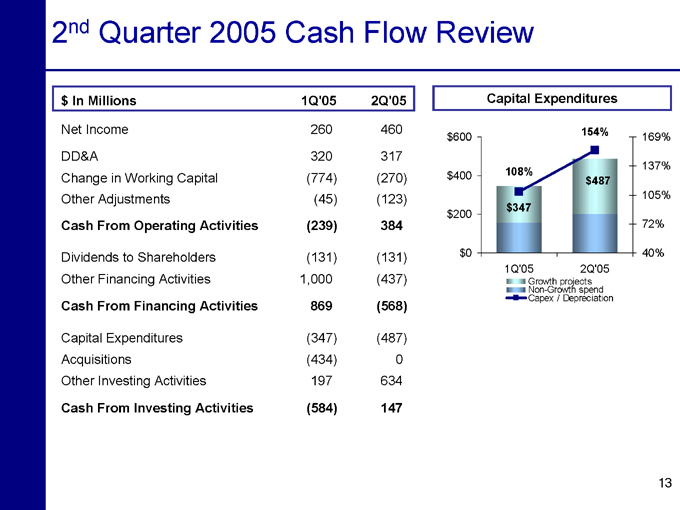

2nd Quarter 2005 Cash Flow Review

$ In Millions 1Q’05 2Q’05

Net Income 260 460

DD&A 320 317

Change in Working Capital (774) (270)

Other Adjustments (45) (123)

Cash From Operating Activities (239) 384

Dividends to Shareholders (131) (131)

Other Financing Activities 1,000 (437)

Cash From Financing Activities 869 (568)

Capital Expenditures (347) (487)

Acquisitions (434) 0

Other Investing Activities 197 634

Cash From Investing Activities (584) 147

Capital Expenditures $600 $400 $200 $0

1Q’05 2Q’05

Growth projects Non-Growth spend Capex / Depreciation

169% 137% 105% 72% 40% $347

108%

154% $487

13

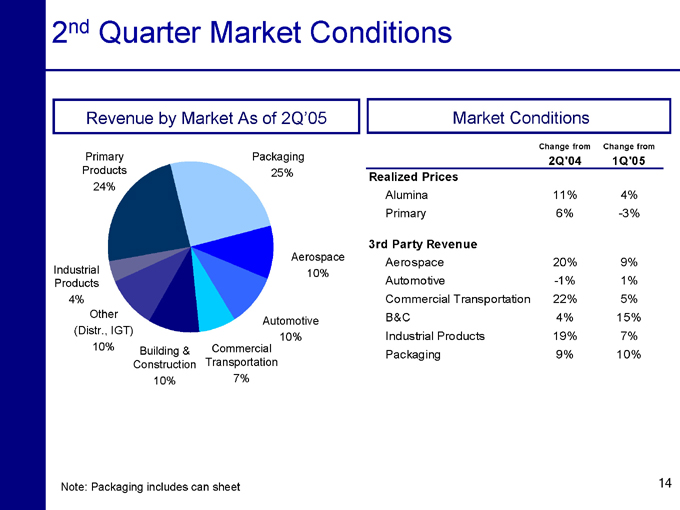

2nd Quarter Market Conditions

Revenue by Market As of 2Q’05

Primary Products 24%

Packaging 25%

Industrial Products 4%

Other (Distr., IGT) 10%

Building & Construction 10%

Commercial Transportation 7%

Automotive 10%

Aerospace 10%

Market Conditions

Change from Change from

2Q’04 1Q’05

Realized Prices

Alumina 11% 4%

Primary 6% -3%

3rd Party Revenue

Aerospace 20% 9%

Automotive -1% 1%

Commercial Transportation 22% 5%

B&C 4% 15%

Industrial Products 19% 7%

Packaging 9% 10%

Note: Packaging includes can sheet

14

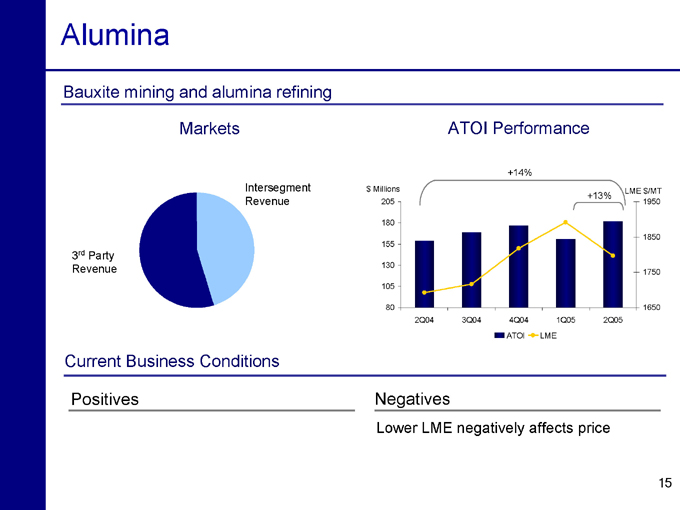

Alumina

Bauxite mining and alumina refining

Markets

3rd Party Revenue

Intersegment Revenue

Current Business Conditions

Positives

ATOI Performance $ Millions

205 180 155 130 105 80

2Q04 3Q04 4Q04 1Q05 2Q05 ATOI LME

LME $/MT

1950 1850 1750 1650

+14%

+13%

Negatives

Lower LME negatively affects price

15

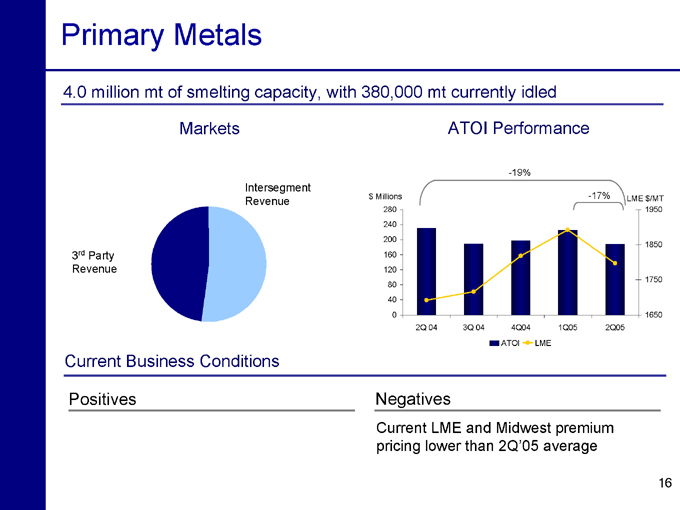

Primary Metals

4.0 million mt of smelting capacity, with 380,000 mt currently idled

Markets

3rd Party Revenue

Intersegment Revenue

Current Business Conditions

Positives

ATOI Performance $ Millions 280 240 200 160 120 80 40 0

2Q 04 3Q 04 4Q04 1Q05 2Q05 ATOI LME

LME $/MT

1950 1850 1750 1650

-19%

-17%

Negatives

Current LME and Midwest premium pricing lower than 2Q’05 average

16

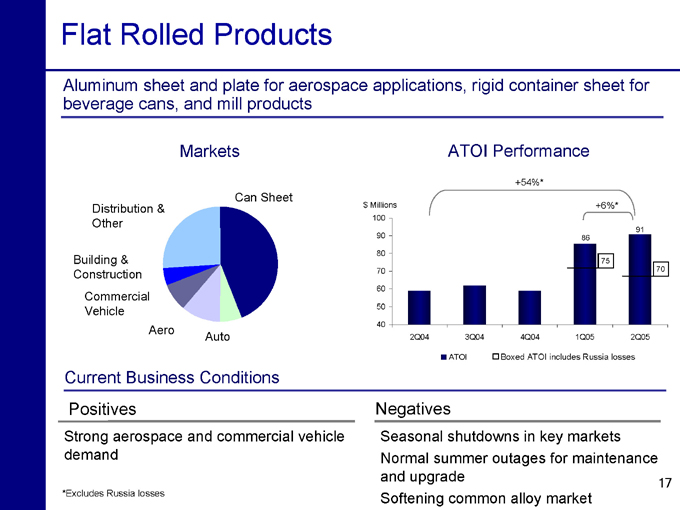

Flat Rolled Products

Aluminum sheet and plate for aerospace applications, rigid container sheet for beverage cans, and mill products

Markets

Distribution & Other

Building & Construction

Commercial Vehicle

Aero

Auto

Can Sheet

Current Business Conditions

Positives

Strong aerospace and commercial vehicle demand

*Excludes Russia losses

ATOI Performance $ Millions 100

90 80 70 60 50 40

2Q04 3Q04 4Q04 1Q05 2Q05

ATOI Boxed ATOI includes Russia losses

+54%*

+6%*

86

91

75

70

Negatives

Seasonal shutdowns in key markets Normal summer outages for maintenance and upgrade Softening common alloy market

17

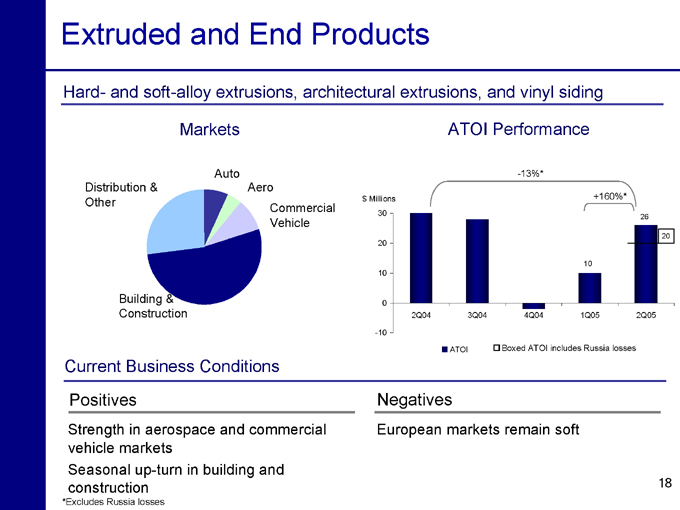

Extruded and End Products

Hard- and soft-alloy extrusions, architectural extrusions, and vinyl siding

Markets

Distribution & Other

Auto Aero

Commercial Vehicle

Building & Construction

ATOI Performance $ Millions 30

20 10 0 -10

2Q04 3Q04 4Q04 1Q05 2Q05

ATOI Boxed ATOI includes Russia losses

-13%*

+160%*

10

26

20

Current Business Conditions

Positives

Strength in aerospace and commercial vehicle markets Seasonal up-turn in building and construction

*Excludes Russia losses

Negatives

European markets remain soft

18

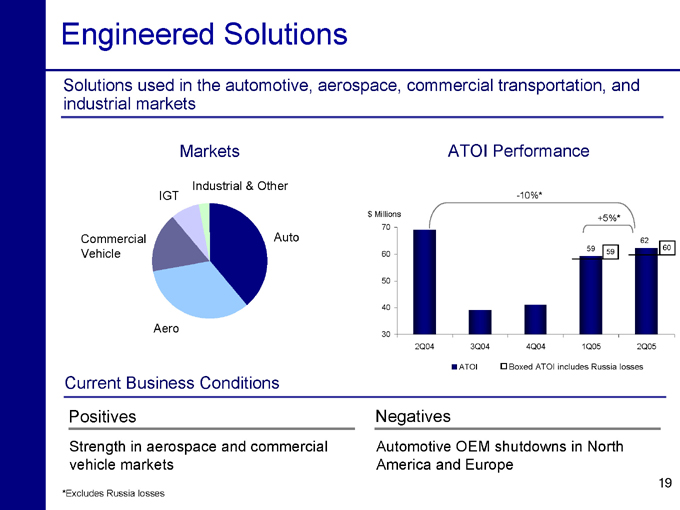

Engineered Solutions

Solutions used in the automotive, aerospace, commercial transportation, and industrial markets

Markets

Industrial & Other

IGT

Commercial Vehicle

Aero

Auto

Current Business Conditions

Positives

Strength in aerospace and commercial vehicle markets

*Excludes Russia losses

Negatives

Automotive OEM shutdowns in North America and Europe

$ Millions 70

60 50 40 30

2Q04 3Q04 4Q04 1Q05 2Q05

ATOI Boxed ATOI includes Russia losses

ATOI Performance

-10%*

+5%*

59 59

62 60

19

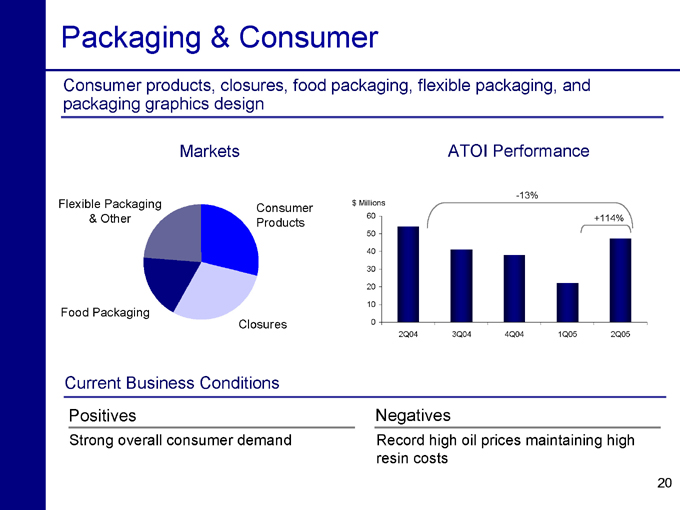

Packaging & Consumer

Consumer products, closures, food packaging, flexible packaging, and packaging graphics design

Markets

Flexible Packaging & Other

Consumer Products

Food Packaging

Closures

Current Business Conditions

Positives

Strong overall consumer demand

ATOI Performance $ Millions 60

50 40 30 20 10 0

-13%

+114%

2Q04 3Q04 4Q04 1Q05 2Q05

Negatives

Record high oil prices maintaining high resin costs

20

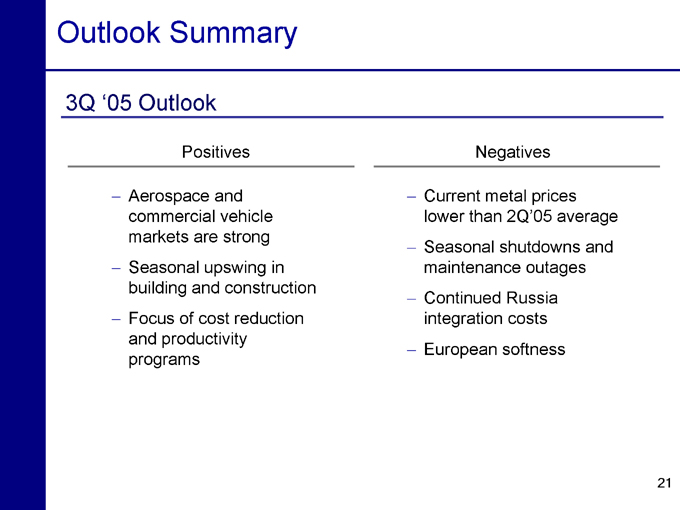

Outlook Summary

3Q ‘05 Outlook

Positives

Aerospace and commercial vehicle markets are strong

Seasonal upswing in building and construction

Focus of cost reduction and productivity programs

Negatives

Current metal prices lower than 2Q’05 average

Seasonal shutdowns and maintenance outages

Continued Russia integration costs

European softness

21

For Additional Information, contact:

William F. Oplinger Director, Investor Relations

Alcoa

390 Park Avenue

New York, N.Y. 10022-4608 Telephone: (212) 836-2674 Facsimile: (212) 836-2813 www.alcoa.com

22

Appendix

Reconciliation of Return on Capital

In Millions 2Q’05 Bloomberg Method 2Q’05 Annlzd 1Q’05 Bloomberg Method 1Q’05 Annlzd 4Q’04 Bloomberg Method 4Q’04 Annlzd 3Q’04 Bloomberg Method 3Q’04 Annlzd 2Q’04 Bloomberg Method 2Q’04 Annlzd

Net Income $1,271 $1,840 $1,215 $1,040 $1,310 $1,072 $1,333 $1,132 $1,330 $1,616

Minority Interest $239 $240 $252 $240 $242 $192 $238 $288 $220 $296

Interest

Expense $234 $313 $206 $198 $201 $240 $198 $192 $207 $200

(After-tax)

Numerator

(Sum Total) $1,744 $2,393 $1,673 $1,478 $1,753 $1,504 $1,769 $1,612 $1,757 $2,112

ST Borrowings $981 $1,710 $1,269 $1,482 $767 $753 $370 $547 $332 $540

LT Borrowings $5,922 $5,391 $6,025 $5,307 $6,019 $5,727 $6,883 $6,219 $7,137 $6,556

Preferred Equity $55 $55 $55 $55 $55 $55 $55 $55 $55 $55

Minority Interest $1,253 $1,188 $1,263 $1,293 $1,378 $1,389 $1,321 $1,330 $1,407 $1,328

Common Equity $12,761 $13,325 $12,766 $13,297 $12,633 $12,873 $11,781 $12,360 $11,277 $12,230

Denominator

(Sum Total) $20,971 $21,668 $21,377 $21,432 $20,852 $20,798 $20,410 $20,511 $20,208 $20,709

ROC 8.3% 11.0% 7.8% 6.9% 8.4% 7.2% 8.7% 7.9% 8.7% 10.2%

Notes:

Note: Bloomberg Methodology calculates ROC based on trailing 4 quarters.

24

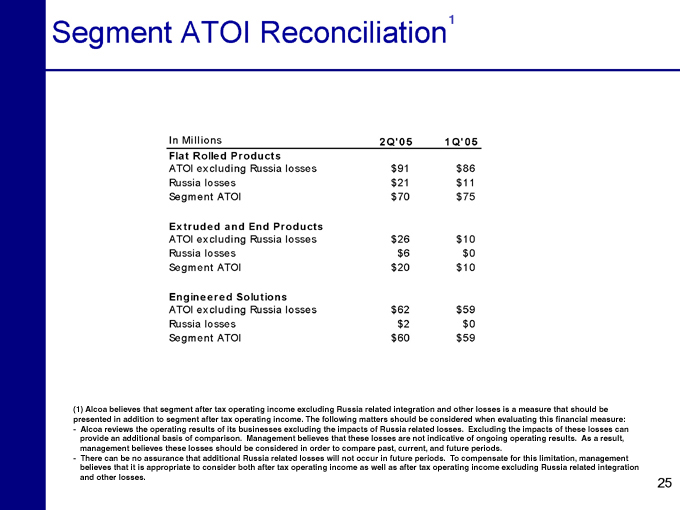

Segment ATOI Reconciliation

In Millions 2Q’05 1Q’05

Flat Rolled Products

ATOI excluding Russia losses $91 $86

Russia losses $21 $11

Segment ATOI $70 $75

Extruded and End Products

ATOI excluding Russia losses $26 $10

Russia losses $6 $0

Segment ATOI $20 $10

Engineered Solutions

ATOI excluding Russia losses $62 $59

Russia losses $2 $0

Segment ATOI $60 $59

(1) Alcoa believes that segment after tax operating income excluding Russia related integration and other losses is a measure that should be presented in addition to segment after tax operating income. The following matters should be considered when evaluating this financial measure:

– |

| Alcoa reviews the operating results of its businesses excluding the impacts of Russia related losses. Excluding the impacts of these losses can provide an additional basis of comparison. Management believes that these losses are not indicative of ongoing operating results. As a result, management believes these losses should be considered in order to compare past, current, and future periods. |

– |

| There can be no assurance that additional Russia related losses will not occur in future periods. To compensate for this limitation, management believes that it is appropriate to consider both after tax operating income as well as after tax operating income excluding Russia related integration and other losses. |

25