The Aluminum Value Chain The Aluminum Value Chain Unlocking Aluminum’s value and building a sustainable future Unlocking Aluminum’s value and building a sustainable future Bernt Reitan Executive Vice President, Alcoa President, Alcoa Primary Products CRU’s 12 th World Aluminium Conference Bahrain 13-16 May 2007 Filed by Alcoa Inc. Pursuant to Rule 425 Under the Securities Act of 1933 Registration Statement: 333-142669 Subject Company: Alcan Inc. Commission File No.: 001-03677 |

2 CRU’s 12 th World Aluminium Conference -- 2007 Forward-Looking Statements Certain statements and assumptions in this communication contain or are based on "forward-looking“ information and involve risks and uncertainties. Forward-looking statements may be identified by their use of words like "anticipates," "believes," "estimates," "expects," "hopes," "targets," "should," "will," "will likely result," "forecast," "outlook," "projects" or other words of similar meaning. Such forward-looking information includes, without limitation, the statements as to the impact of the proposed acquisition on revenues, costs and earnings. Such forward looking statements are subject to numerous assumptions, uncertainties and risks, many of which are outside of Alcoa's control. Accordingly, actual results and developments are likely to differ, and may differ materially, from those expressed or implied by the forward-looking statements contained in this communication. These risks and uncertainties include Alcoa's ability to successfully integrate the operations of Alcan; the outcome of contingencies including litigation, environmental remediation, divestitures of businesses, and anticipated costs of capital investments; general business and economic conditions; interest rates; the supply and demand for, deliveries of, and the prices and price volatility of primary aluminum, fabricated aluminum, and alumina produced by Alcoa and Alcan; the timing of the receipt of regulatory and governmental approvals necessary to complete the acquisition of Alcan and any undertakings agreed to in connection with the receipt of such regulatory and governmental approvals; the timing of receipt of regulatory and governmental approvals for Alcoa's and Alcan's development projects and other operations; the availability of financing to refinance indebtedness incurred in connection with the acquisition of Alcan on reasonable terms; the availability of financing for Alcoa's and Alcan's development projects on reasonable terms; Alcoa's and Alcan's respective costs of production and their respective production and productivity levels, as well as those of their competitors; energy costs; Alcoa's and Alcan's ability to secure adequate transportation for their respective products, to procure mining equipment and operating supplies in sufficient quantities and on a timely basis, and to attract and retain skilled staff; the impact of changes in foreign currency exchange rates on Alcoa's and Alcan's costs and results, particularly the Canadian dollar, Euro, and Australian dollar, may affect profitability as some important raw materials are purchased in other currencies, while products generally are sold in U.S. dollars; engineering and construction timetables and capital costs for Alcoa‘s and Alcan's development and expansion projects; market competition; tax benefits and tax rates; the outcome of negotiations with key customers; the resolution of environmental and other proceedings or disputes; and Alcoa's and Alcan's ongoing relations with their respective employees and with their respective business partners and joint venturers. |

3 CRU’s 12 th World Aluminium Conference -- 2007 Forward-Looking Statements Additional risks, uncertainties and other factors affecting forward looking statements include, but are not limited to, the following: •Alcoa is, and the combined company will be, subject to cyclical fluctuations in London Metal Exchange primary aluminum prices, economic and business conditions generally, and aluminum end-use markets; •Alcoa's operations consume, and the combined company's operations will consume, substantial amounts of energy, and profitability may decline if energy costs rise or if energy supplies are interrupted; •The profitability of Alcoa and/or the combined company could be adversely affected by increases in the cost of raw materials; •Union disputes and other employee relations issues could adversely affect Alcoa's and/or the combined company's financial results; •Alcoa and/or the combined company may not be able to successfully implement its growth strategy; •Alcoa's operations are, and the combined company's operations will be, exposed to business and operational risks, changes in conditions and events beyond its control in the countries in which it operates; •Alcoa is, and the combined company will be, exposed to fluctuations in foreign currency exchange rates and interest rates, as well as inflation and other economic factors in the countries in which it operates; •Alcoa faces, and the combined company will face, significant price competition from other aluminum producers and end-use markets for Alcoa products that are highly competitive; •Alcoa and/or the combined company could be adversely affected by changes in the business or financial condition of a significant customer or customers; •Alcoa and/or the combined company may not be able to successfully implement its productivity and cost-reduction initiatives; •Alcoa and/or the combined company may not be able to successfully develop and implement new technology initiatives; •Alcoa is, and the combined company will be, subject to a broad range of environmental laws and regulations in the jurisdictions in which it operates and may be exposed to substantial costs and liabilities associated with such laws; •Alcoa’s smelting operations are expected to be affected by various regulations concerning greenhouse gas emissions; •Alcoa and the combined company may be exposed to significant legal proceedings, investigations or changes in law; and •Unexpected events may increase Alcoa's and/or the combined company's cost of doing business or disrupt Alcoa's and/or the combined company's operations. See also the risk factors disclosed in Alcoa's Annual Report on Form 10-K for the fiscal year ended December 31, 2006. Readers are cautioned not to put undue reliance on forward-looking statements. Alcoa disclaims any intent or obligation to update these forward- looking statements, whether as a result of new information, future events or otherwise, except as may be required by applicable law. |

4 CRU’s 12 th World Aluminium Conference -- 2007 Additional information WHERE TO FIND ADDITIONAL INFORMATION • In connection with the offer by Alcoa to purchase all of the issued and outstanding common shares of Alcan (the “Offer”), Alcoa has filed with the Securities and Exchange Commission (the “SEC”) a registration statement on Form S-4 (the “Registration Statement”), which contains a prospectus relating to the Offer (the “Prospectus”), and a tender offer statement on Schedule TO (the “Schedule TO”). This communication is not a substitute for the Prospectus, the Registration Statement and the Schedule TO. ALCAN SHAREHOLDERS AND OTHER INTERESTED PARTIES ARE URGED TO READ THESE DOCUMENTS, ALL OTHER APPLICABLE DOCUMENTS AND ANY AMENDMENTS OR SUPPLEMENTS TO ANY SUCH DOCUMENTS WHEN THEY BECOME AVAILABLE, BECAUSE EACH CONTAINS OR WILL CONTAIN IMPORTANT INFORMATION ABOUT ALCOA, ALCAN AND THE OFFER. Materials filed with SEC are available electronically without charge at the SEC’s website, www.sec.gov. Materials filed with the Canadian securities regulatory authorities ("CSRA") are available electronically without charge at www.sedar.com. Materials filed with the SEC or the CSRA may also be obtained without charge at Alcoa’s website, www.alcoa.com, or by directing a request to Alcoa’s investor relations department at (212) 836-2674. In addition, Alcan shareholders may obtain free copies of such materials filed with the SEC or the CSRA by directing a written or oral request to the Information Agent for the Offer, MacKenzie Partners, Inc., toll-free at (800) 322-2885 (English) or (888) 405-1217 (French). While the Offer is being made to all holders of Alcan Common Shares, this communication does not constitute an offer or a solicitation in any jurisdiction in which such offer or solicitation is unlawful. The Offer is not being made in, nor will deposits be accepted in, any jurisdiction in which the making or acceptance thereof would not be in compliance with the laws of such jurisdiction. However, Alcoa may, in its sole discretion, take such action as they may deem necessary to extend the Offer in any such jurisdiction. |

The Aluminum Value Chain Unlocking Unlocking Aluminum’s value and Aluminum’s value and building a sustainable building a sustainable future future |

Alcoa at a glance Alcoa on the leading edge Megatrends that drive our business Unlocking aluminum’s value Industry landscape Agenda |

7 CRU’s 12 th World Aluminium Conference -- 2007 Alcoa at a glance • Leading aluminum products company – Primary aluminum and alumina – Flat-rolled aluminum and hard-alloy extrusions • Active in all major segments of the industry: – Technology – Smelting – Mining – Fabricating – Refining – Recycling Products serving the aerospace, automotive, commercial transportation, packaging, building and construction, and industrial markets. |

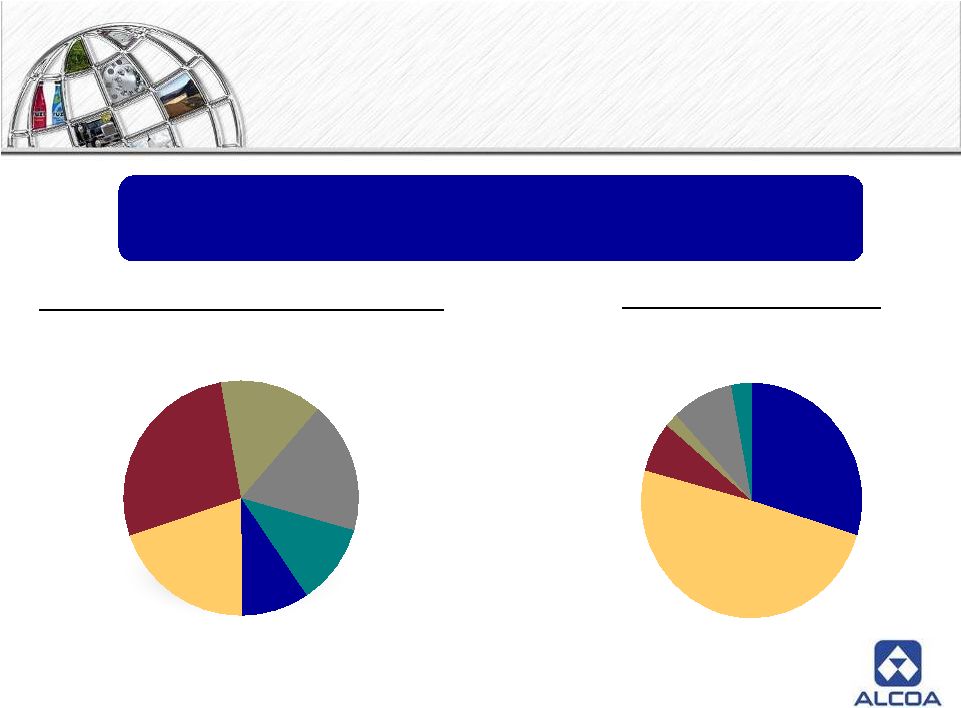

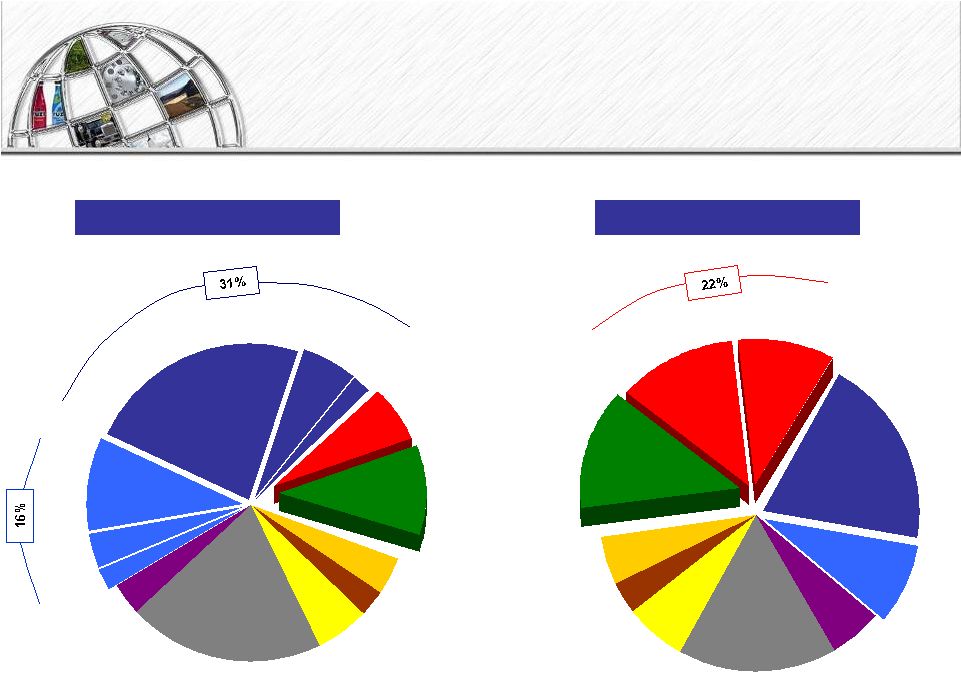

8 CRU’s 12 th World Aluminium Conference -- 2007 Financial performance - 2006 9% 20% 27% 14% 18% 11% Engineered Solutions Alumina Primary Metals Flat Rolled Extruded & End Packaging & Consumer 2006 3 rd Party Revenue by Segment 2006 ATOI by Segment 30% 50% 7% 2% 9% 3% Engineered Solutions Alumina Flat Rolled Primary Metals Packaging & Consumer Extruded & End $30.4 Billion - highest revenue and income in Alcoa history |

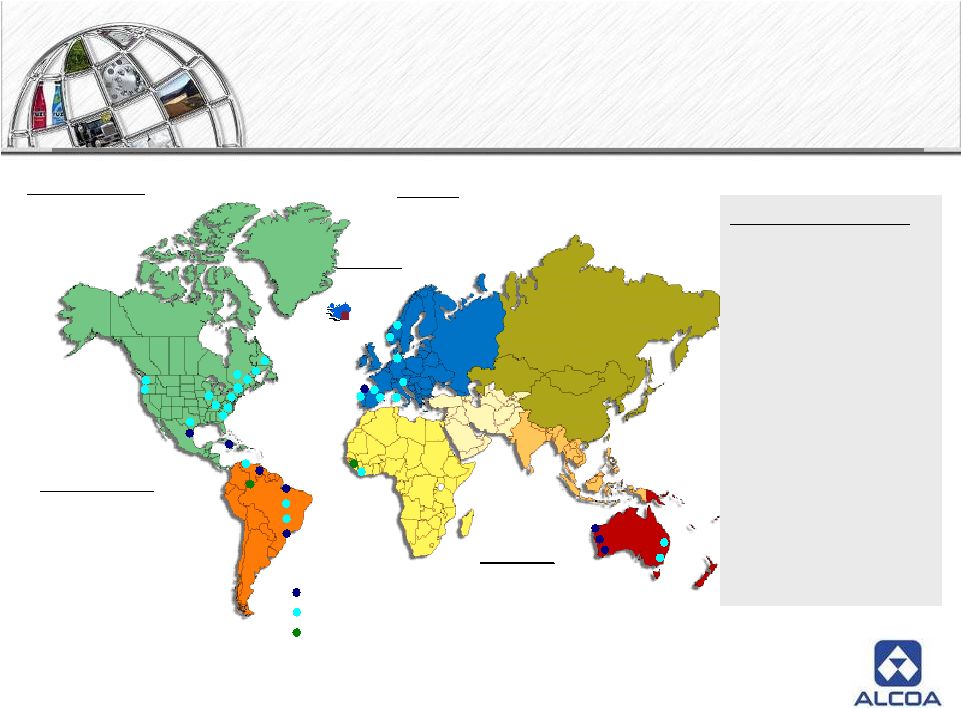

9 CRU’s 12 th World Aluminium Conference -- 2007 44 Countries 123,000 Employees 2006 Sales by Geography Pacific ROW 57% 13% Europe 24% 6% U.S. Global organization |

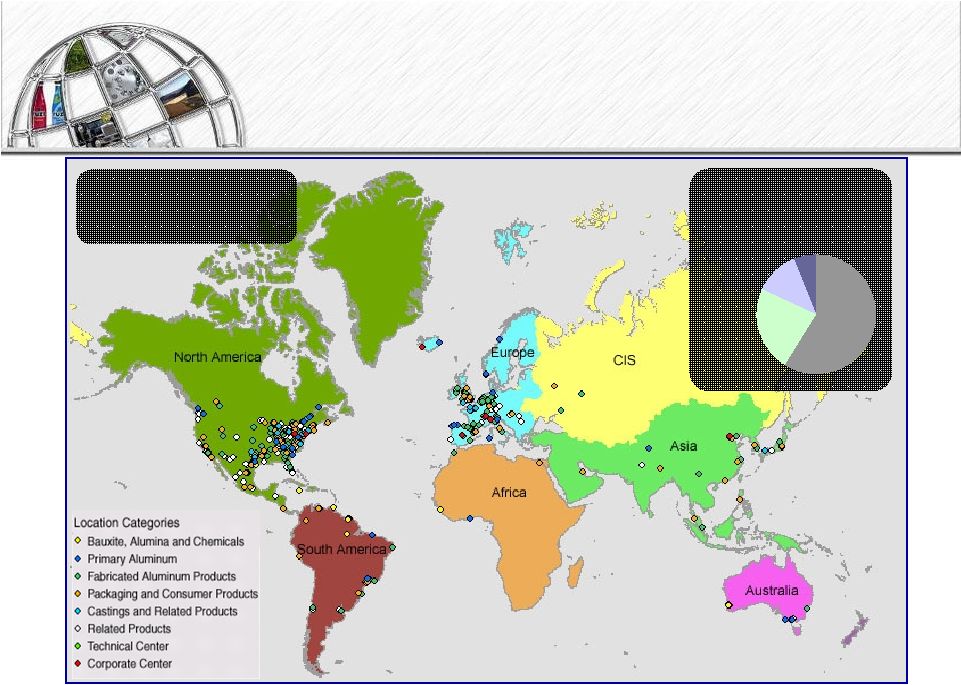

10 CRU’s 12 th World Aluminium Conference -- 2007 Alcoa Primary Operations Refinery Smelter Stand-alone bauxite mine Refinery Smelter Stand-alone bauxite mine North America: Smelting 2.8M tonnes Refining 2.3M tonnes Latin America: Smelting 0.3M tonnes Refining 2.6M tonnes Europe: Smelting 0.6M tonnes Refining 1.3M tonnes Australia: Smelting 0.4M tonnes Refining 7.8M tonnes Refinery Smelter Stand-alone bauxite mine Refinery Smelter Stand-alone bauxite mine North America: Smelting 2.8M tonnes Refining 2.3M tonnes Latin America: Smelting 0.3M tonnes Refining 2.6M tonnes Europe: Smelting 0.6M tonnes Refining 1.3M tonnes Australia: Smelting 0.4M tonnes Refining 7.8M tonnes Iceland Smelting 0.3M tonnes Key Facts (2006) • 25 Smelters on 5 continents • 9 refineries on 4 continents • 3.6 mmt Aluminum Production -- 11% of world output • 15.1 mmt Alumina production – 23% of world output • $8.9 billion in 3 rd Party Revenue • $15 billion total Revenue incl intercompany sales to down-streams |

11 CRU’s 12 th World Aluminium Conference -- 2007 A values-driven company • Integrity • Environment, Health and Safety • Customer • Excellence • People • Profitability • Accountability |

Living the Living the Values Values |

13 CRU’s 12 th World Aluminium Conference -- 2007 Committed to sustainability 2020 Strategic framework |

14 CRU’s 12 th World Aluminium Conference -- 2007 Sustainability goals • From base year 2000: – 60% reduction sulfur dioxide by 2010 – 50% reduction volatile organic compounds by 2008 – 30% reduction nitrogen oxides by 2007 – 80% reduction mercury emissions by 2008 – 50% reduction landfill waste by 2007 – Reduce energy intensity 10% by 2010 – 60% reduction in process water use and discharge by 2009 • From base year 1990: – 25% reduction in greenhouse gas emissions by 2010. |

15 CRU’s 12 th World Aluminium Conference -- 2007 Land stewardship • Reclamation • Conservation/biodiversity • Management Alcoa-sponsored environmental parks, Brazil Award-winning forest restoration, Australia Great Smoky Mountains conservation agreement, USA |

16 CRU’s 12 th World Aluminium Conference -- 2007 Safety leader 0.00 0.50 1.00 1.50 2.00 2.50 3.00 3.50 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 U.S Industry Average Alcoa • Alcoa facilities worldwide are 20 times safer than U.S average • More than 82% of Alcoa facilities had zero lost workdays in 2006 Lost workdays |

17 CRU’s 12 th World Aluminium Conference -- 2007 Community support Commitment to Communities - 2006 • Alcoa and Alcoa Foundation investments totaled $42.3 million • More than 500,000 volunteer work hours, equivalent of 55 years of work • Launched $8.6 million Conservation and Sustainability Fellowship research program Employee volunteers in Australia |

18 CRU’s 12 th World Aluminium Conference -- 2007 United States Climate Action Partnership • Alcoa a founding member • 10 US Corporations and 4 NGOs • Slow, stop and reverse climate change • A call for action to the US Government • Founding principles – Account for the global dimensions of climate change – Recognize the importance of technology – Be environmentally effective – Create economic opportunity and advantage – Be fair to sectors disproportionately impacted – Recognize and encourage early action • “I am convinced that we can build a global plan of action on climate change in ways that create more economic opportunities than risks.” Alain Belda NGO Members • Environmental Defense • Natural Resources Defense Council • Pew Center on Global Climate Change • World Resources Institute Industry Members • Alcoa • BP America • Caterpillar • Duke Energy • DuPont • General Electric • PG&E • PNM Resources |

19 CRU’s 12 th World Aluminium Conference -- 2007 Recognition • Member Dow Jones Sustainability Indexes • Most Sustainable Corporation / World Economic Forum in Davos • Top Green Company by BusinessWeek magazine and the Climate Group for GHG reductions • $8.6 million Conservation & Sustainability Research Fellows Program • Named by CERES as a leader in climate change and governance • UNEP Global 500 Role of Honour • World Environment Center Gold Medal |

Creating value: Creating value: Alcoa at the leading Alcoa at the leading edge of sustainable edge of sustainable production production |

21 CRU’s 12 th World Aluminium Conference -- 2007 Sustainable aluminum production • Recycled content • Sustainable energy sources • Energy conservation • GHG control achievements • Smelting Technology – Anode effect management – Breakthrough smelting technologies • GHG Neutral by 2020 |

22 CRU’s 12 th World Aluminium Conference -- 2007 Leader in recycled content Scrap recycling center, Hungary 30% growth in recycled content -- 2004-2006 0 200 400 600 800 1000 2004 2005 2006 Currently Alcoa uses nearly 1 million mt/year of recycled aluminum – 25% of primary production mt |

23 CRU’s 12 th World Aluminium Conference -- 2007 Anode effect management • Operational excellence in smelting process • Consistent, stable reaction • 26% reduction in CO 2 emissions 5 years ahead of target • 75% reduction in PFC emissions since 1990 • Concurrent energy savings • Best practices shared across the Alcoa system |

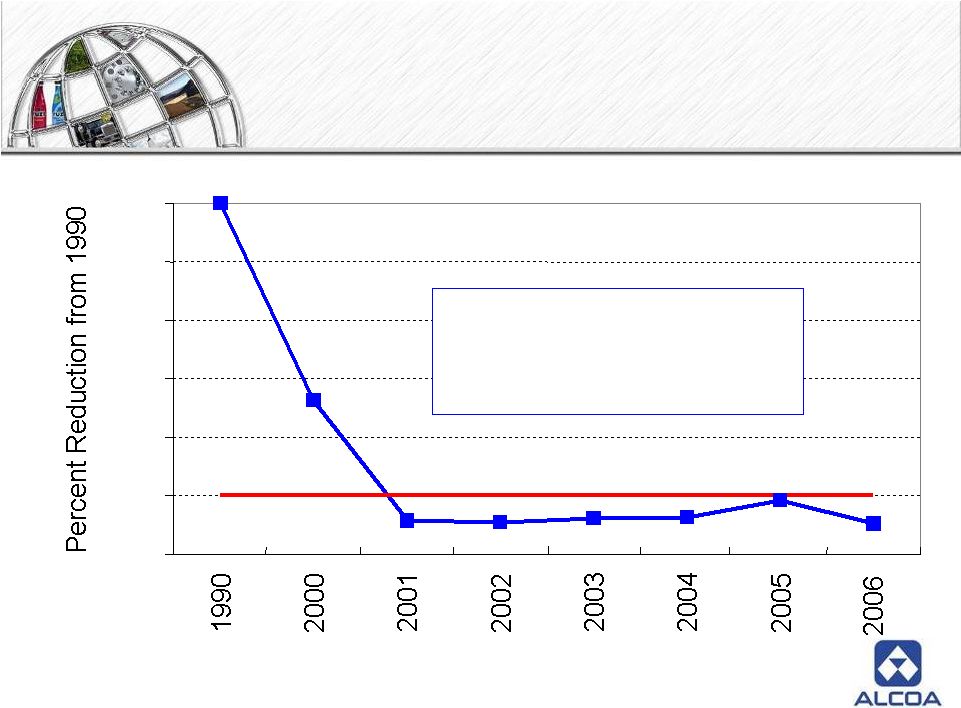

24 CRU’s 12 th World Aluminium Conference -- 2007 Progress - greenhouse gas reductions (Direct GHG Emissions from Managed Facilities) 0% 5% 10% 15% 20% 25% 30% Alcoa primary aluminum production nearly doubled from 1.9 mmt/y to 3.6 mmt/y during this period. |

25 CRU’s 12 th World Aluminium Conference -- 2007 Leader in sustainable energy • More than a century of hydropower expertise – new technology improving yield of existing projects – LIHI certification • Cogeneration at Wagerup and Pinjarra • Biofuels for plant equipment • Green Power – renewable energy contracts • Geothermal – Under consideration for proposed second smelter in Iceland Calderwood dam, Tennessee Pinjarra cogeneration plant |

26 CRU’s 12 th World Aluminium Conference -- 2007 Cogeneration in Australia • Pinjarra and Wagerup refineries, Western Australia • First of four 140 MW plants completed in 06 at Pinjarra • Potential 1.6 million tons/year GHG savings for both plants • 240 tonnes/hour of steam for refineries, electricity for municipal grid • Energy efficiency is 75% compared to 30-35% for coal-fired generation; 50% for gas turbine • Electricity greenhouse gas saved: 450,000 tons/year • Steam greenhouse gas saved: 135,000 tons/year • Alcoa is Australia’s largest cogeneration customer |

27 CRU’s 12 th World Aluminium Conference -- 2007 Energy conservation • US DOE energy reduction program • Nitrogen oxide emissions reduced by 770 mtpy • Sulphur Dioxide emissions reduced by 1600 mtpy • Carbon Dioxide emission reduced by 420,000 mtpy • Operating costs cut by $15 million • Best practices shared worldwide |

28 CRU’s 12 th World Aluminium Conference -- 2007 Carbon capture • Waste CO 2 from neighboring facility used to reduce alkalinity of bauxite residue • Captures 70,000 tonnes/year of CO 2 • Potential 300,000 tonnes/year in Australia • Researching technology for extracting CO 2 from Alcoa’s flue gases Carbon capture plant, Kwinana, Western Australia |

29 CRU’s 12 th World Aluminium Conference -- 2007 Breakthrough smelting technologies Post-Carbon technology • Possible next-generation process • Replaces most CO 2 emissions with O 2 emissions • Reduces operating costs • Eliminates all sulfur and carbon emissions from anodes Carbothermic process • Electrolysis-free process • Significant reduction in energy Alcoa Technical Center |

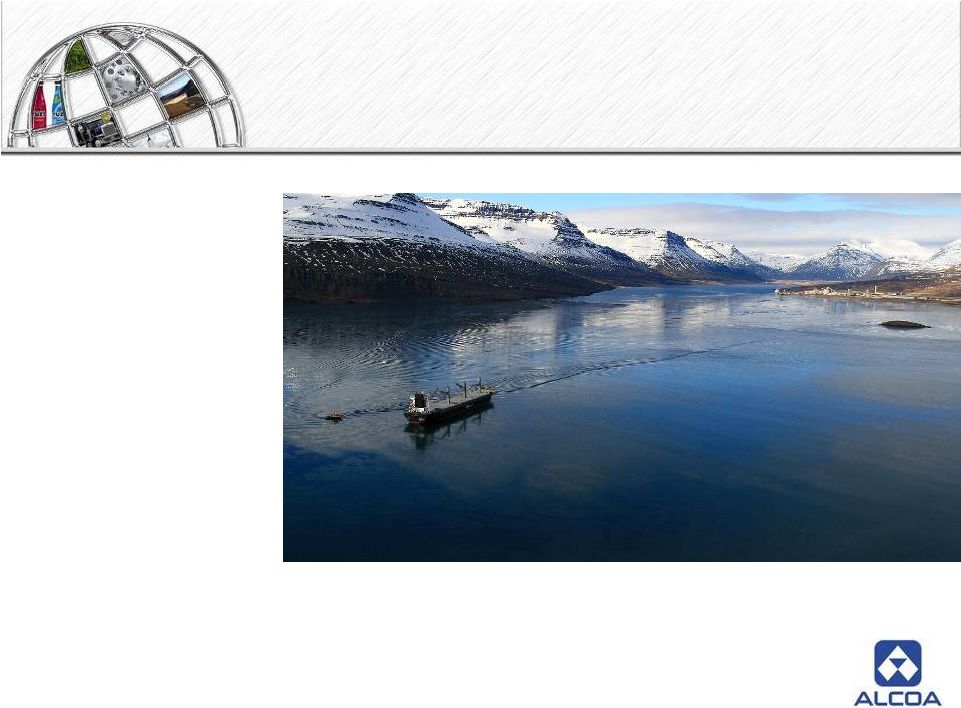

30 CRU’s 12 th World Aluminium Conference -- 2007 Sustainable growth in Iceland Alcoa Fjardaal • 344,000 mtpy capacity • First metal April 2007 • Compliant with Iceland’s stringent environmental requirements North Iceland • Possible second smelter site in Bakki • Phase 2 feasibility study • Geothermal power under consideration First shipment of alumina, Alcoa Fjardaal, Iceland – 28 March 2007 |

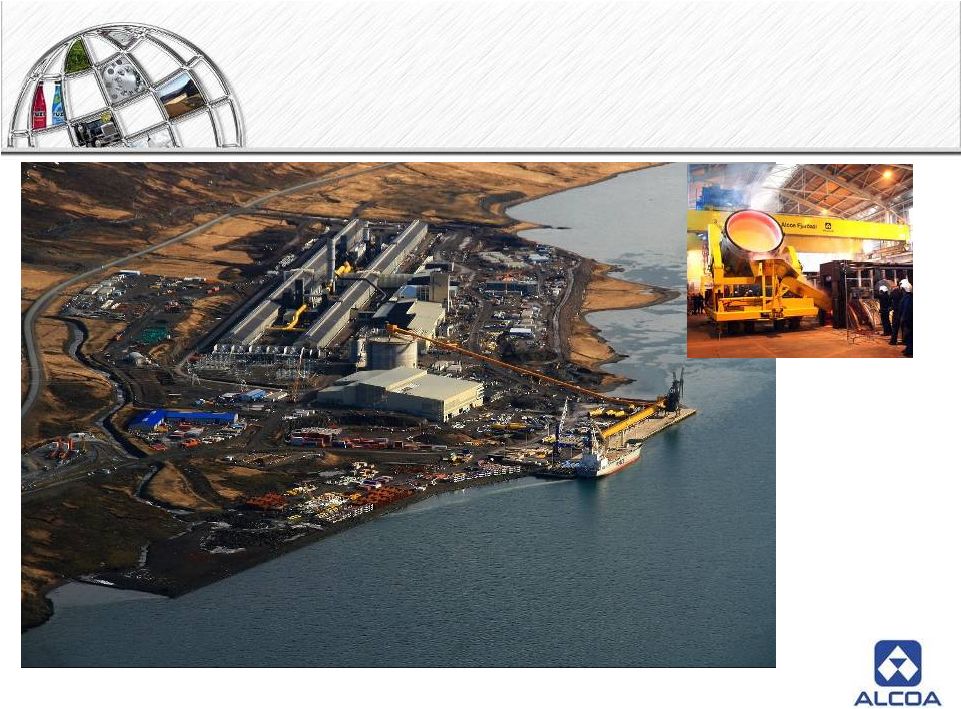

31 CRU’s 12 th World Aluminium Conference -- 2007 Fjardaal on line – April 07 Bath transfer |

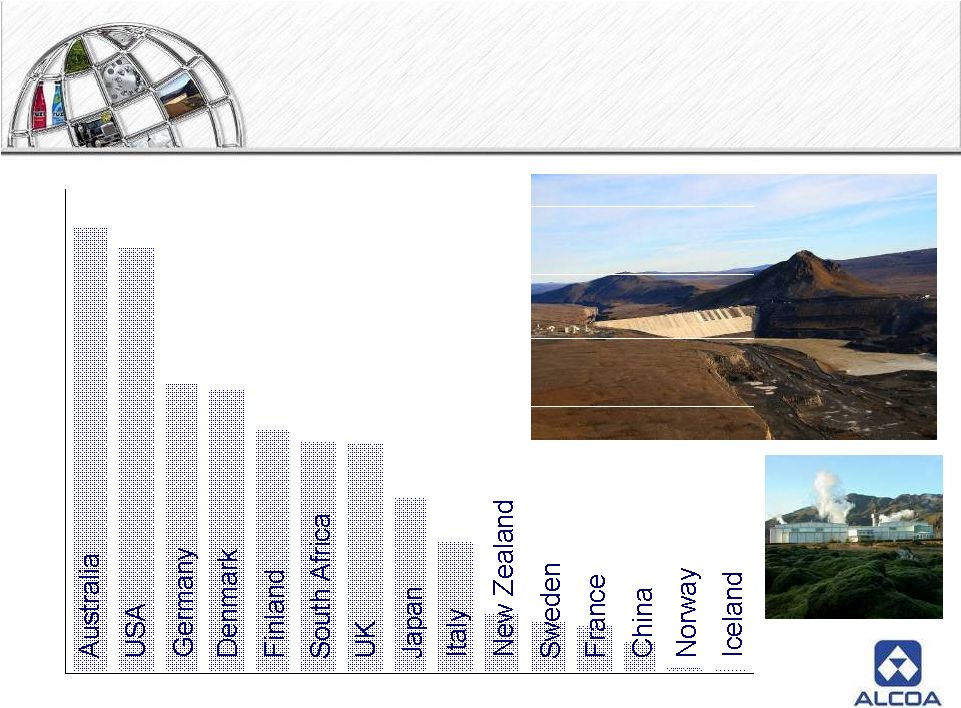

32 CRU’s 12 th World Aluminium Conference -- 2007 0 1 2 3 4 5 6 7 Iceland: a leader in sustainable power Hydro Geothermal Estimated per capita CO 2 emissions from electricity production in selected countries Source: Orkuveita Reykjavikur |

Megatrends Megatrends that drive our that drive our business business • Global urbanization • Climate change |

34 CRU’s 12 th World Aluminium Conference -- 2007 • Rapid growth of cities presents significant opportunities for physical infrastructure utilizing products that we currently make • New opportunities in areas like rail cars, lightweight bridge decks, non corrosive signage, portable power sources, integrated B&C solutions 1 2 3 4 • Lightweight a key enabler of rapid migration – fast ferries, transport planes, containers, payload increases of trucks • Lead the development of technologies and solutions for security products (e.g. lightweight armor, blast proof containers) • Flexible solar energy panels using aluminum substrates as integrated building and construction products • Enhance grid efficiencies by supplying co-extruded, high conductivity Al-Cu wire • Promote the use of aluminum in multi-fuel vehicles • Increased aluminum content in thermal management solutions driven by miniaturization Demographics Globalization Natural Resources & Environment Science and Technology Advances Global Megatrends present opportunities for Alcoa |

35 CRU’s 12 th World Aluminium Conference -- 2007 Building for the future Aluminum consumption World Aluminum Consumption (MT) 2005: 32M 2020E: 60.6M +0.4 +1.1 +0.9 +0.5 +7.1 +0.5 Latin America +4.1 Western Europe +2.4 E. Europe, CIS & Other +4.4 North America +17.2 Asia Source: CRU; McKinsey & Co 1998: 22M 7.2 6.7 1.7 5.6 0.8 14.3 7.2 2.6 6.7 1.2 31.5 11.6 5.0 10.8 1.7 |

36 CRU’s 12 th World Aluminium Conference -- 2007 Climate change • A Megatrend and a global issue – The global dialog has moved from debate to action – Global consumption growth is raising the stakes – Aluminum has tremendous value in addressing the challenge – Aluminum is part of the solution to climate change |

37 CRU’s 12 th World Aluminium Conference -- 2007 Climate change: beyond debate • 10 years ago, UN’s Kyoto Protocol moved the issue to the global stage. It’s currently endorsed by 169 governments • In the US, industries and NGOs are working together to provide proactive and effective voluntary strategies – US Climate Action Partnership • Alcoa founding member – Global Roundtable on Climate Change – Columbia University • EU’s new 2020 Energy Policy will reduce CO2 emissions by 20% by 2020 • Last year’s ASEM 6 Summit pledged Asian/European collaboration on addressing climate change • In Australia, Kyoto and climate change are a key factor in the upcoming election Alcoa began addressing climate change in the late 90s |

Aluminum: part Aluminum: part of solution to of solution to climate change climate change • Recyclabity • Lasting value • Automotive lightweighting • Aerospace growth • Greenhouse gas neutral |

39 CRU’s 12 th World Aluminium Conference -- 2007 Part of the solution: Recycling • One of the most recyclable, reusable materials on earth • Less than 1% melt loss • Saves 95% of mine-to-ingot energy of primary production • Saves 95% of mine-to-ingot GHG emissions |

40 CRU’s 12 th World Aluminium Conference -- 2007 Part of the solution: Lasting value • 73% of all aluminum ever produced is still in use today • Since 1888, about 800 million tonnes of aluminium have been produced. • About 580 million tonnes of this amount is still in productive use. • Recycling the metal currently stored in use would equal 15 years’ primary aluminium output. 580 800 Global Metal Pool (Inventory) (tonnes) Total Metal Produced (tonnes) Source: IAI |

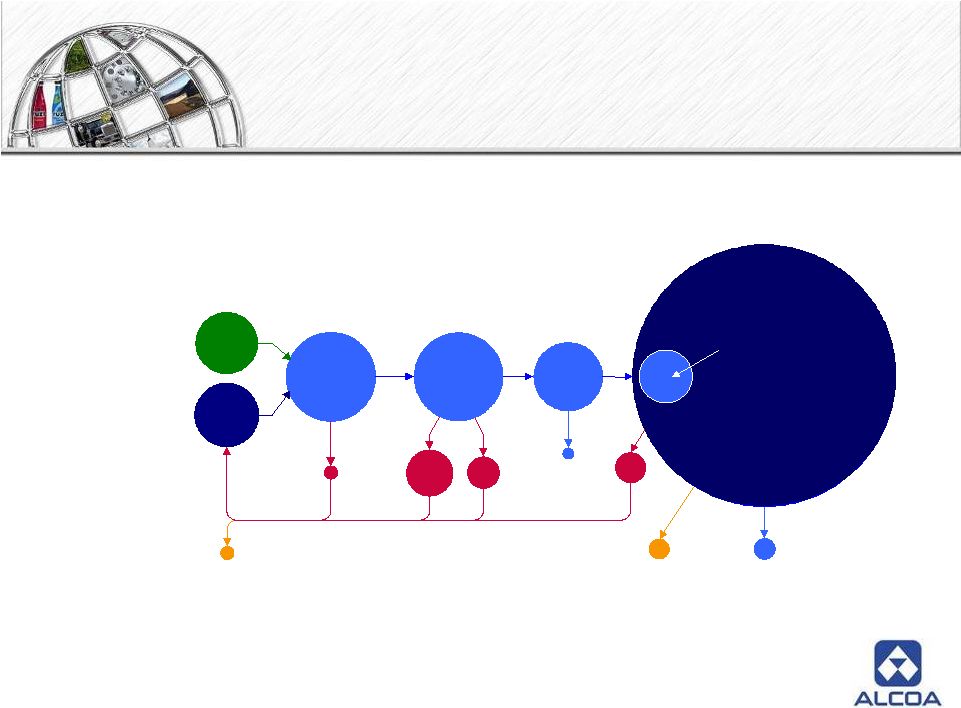

41 CRU’s 12 th World Aluminium Conference -- 2007 Part of the solution: Aluminum lifecycle Source: IAI Total Products Stored in Use Since 1888 586.0 Finished Products 40.4 Oxidized in Applications 0.8 Fabricated and Finished Products 67.4 Traded New Scrap 8.6 Traded New Scrap 1.4 Ingots 68.8 Metal Losses 1.4 Not Recycled in 2006 3.5 Under Investigation 3.7 Old Scrap 7.8 Primary Aluminium used 34.0 Remelted / Recycled 34.8 Net Addition 2006 24.4 Fabricator Scrap 18.4 Internal Values in million of metric tons |

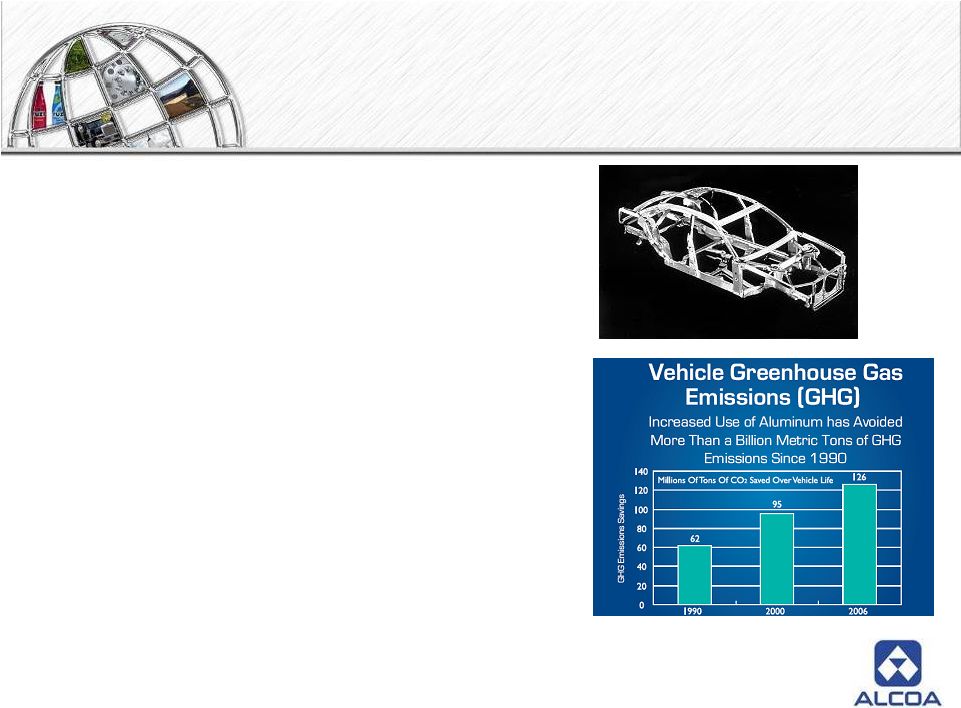

42 CRU’s 12 th World Aluminium Conference -- 2007 Part of the solution: Automotive lightweighting • Aluminum is the most sustainable automotive material in the world • Aluminum is infinitely recyclable. • 95% of the aluminum from a scrapped vehicle is recycled at the end of the vehicle’s useful life • The amount of aluminum used in automobiles has doubled over the last decade Audi spaceframe Source: IAI |

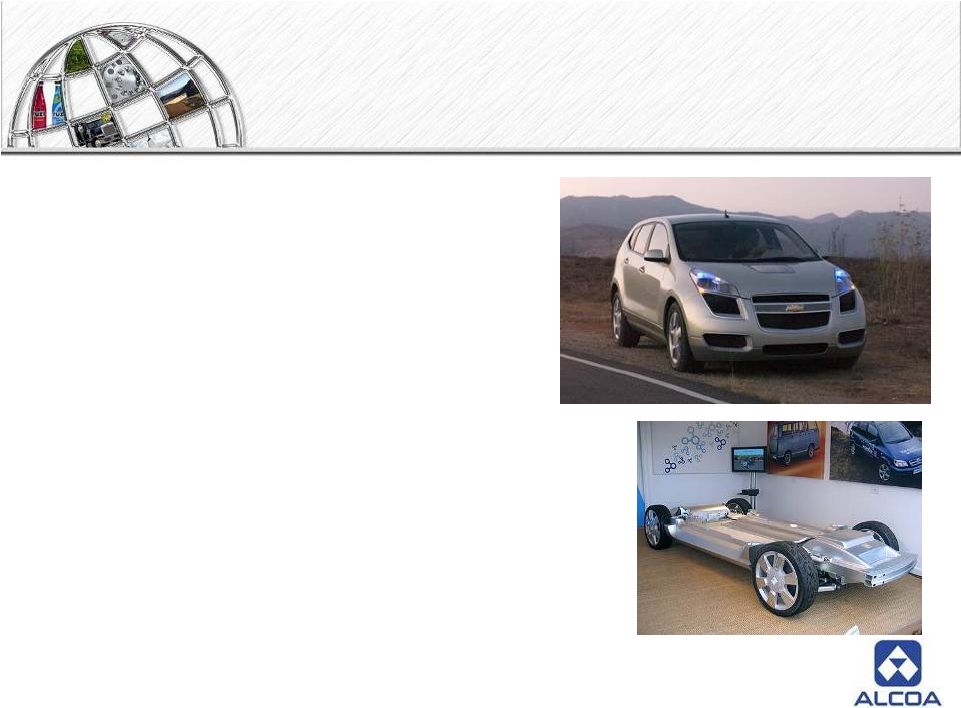

43 CRU’s 12 th World Aluminium Conference -- 2007 Part of the solution: Automotive lightweighting • Aluminum use in transportation saves 250 million tons of CO 2 emissions per year • Using aluminum to replace steel saves 22.9 kg of CO 2 per kg of aluminum • Aluminum adds performance, safety and style without adding weight Body and chassis for GM/Chevrolet Sequel hydrogen- powered vehicle |

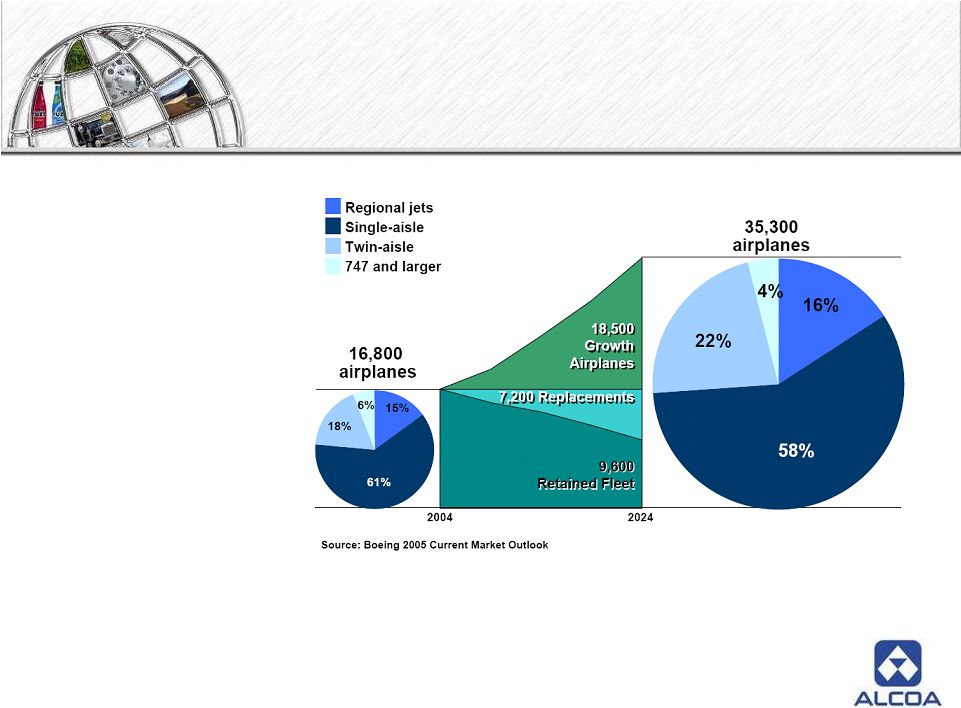

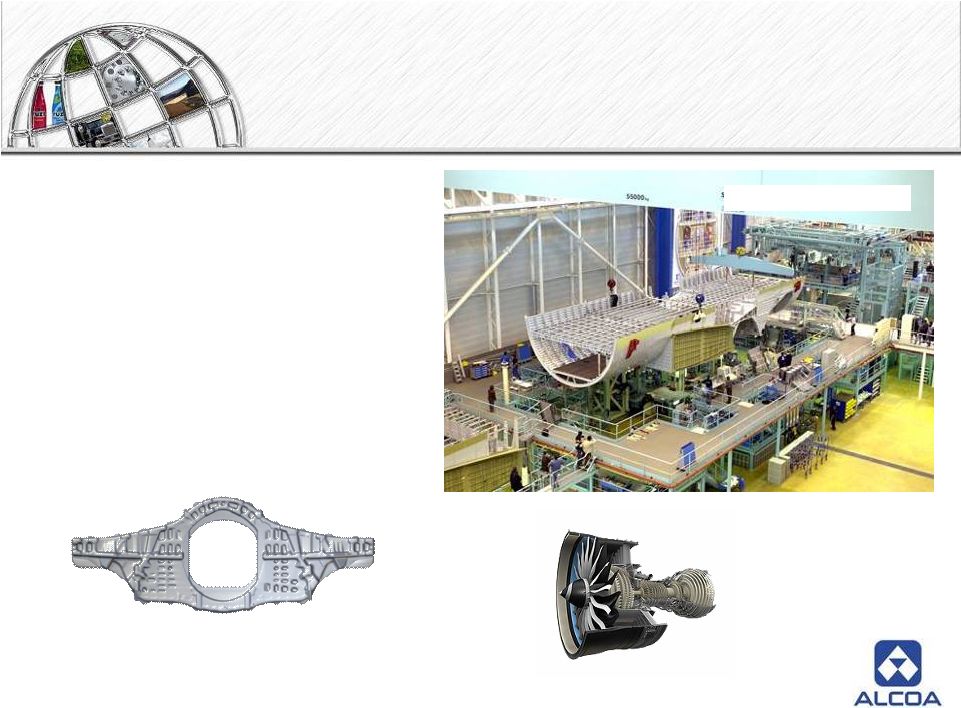

44 CRU’s 12 th World Aluminium Conference -- 2007 Part of the solution: Aerospace • The world fleet will more than double in the next two decades • Alcoa is the leading supplier and innovator in aerospace |

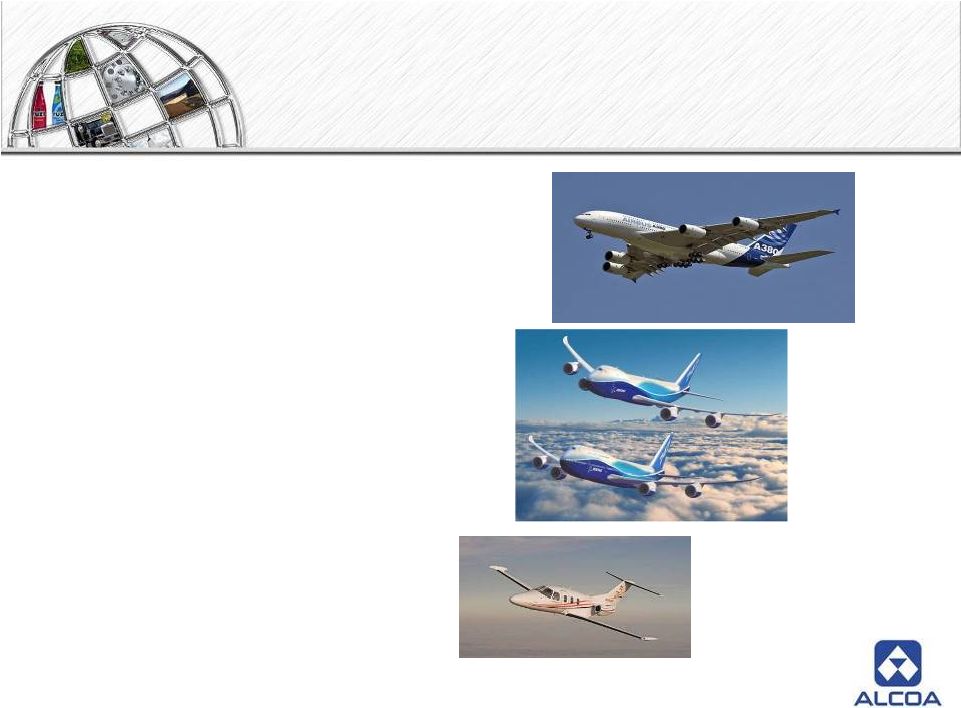

45 CRU’s 12 th World Aluminium Conference -- 2007 Part of the solution: Growth in all areas • Next-generation aircraft will have significant high-value aluminum content – A380: 1000 tonnes of plate – Boeing 787: composite design uses advanced, high-value aluminum alloys • Current generation will continue to use aluminum through 2015 – 737, 777, A320, A330, A340 • Growth in new aircraft categories (VLJ/Very Light Jets) will be strong Boeing 747-8 Eclipse 500 4-passenger jet Airbus A380 |

46 CRU’s 12 th World Aluminium Conference -- 2007 Part of the solution: Aerospace value drivers • Historic durability, inspectability • Alloy and product form flexibility • Aluminum’s weight/strength ratio creates new opportunities for sustainability: – Reducing engine noise – Reducing emissions – Reducing fuel consumption GE NX engine - 787 Forged bulkhead – Joint Strike Fighter Fuselage – Airbus A380 |

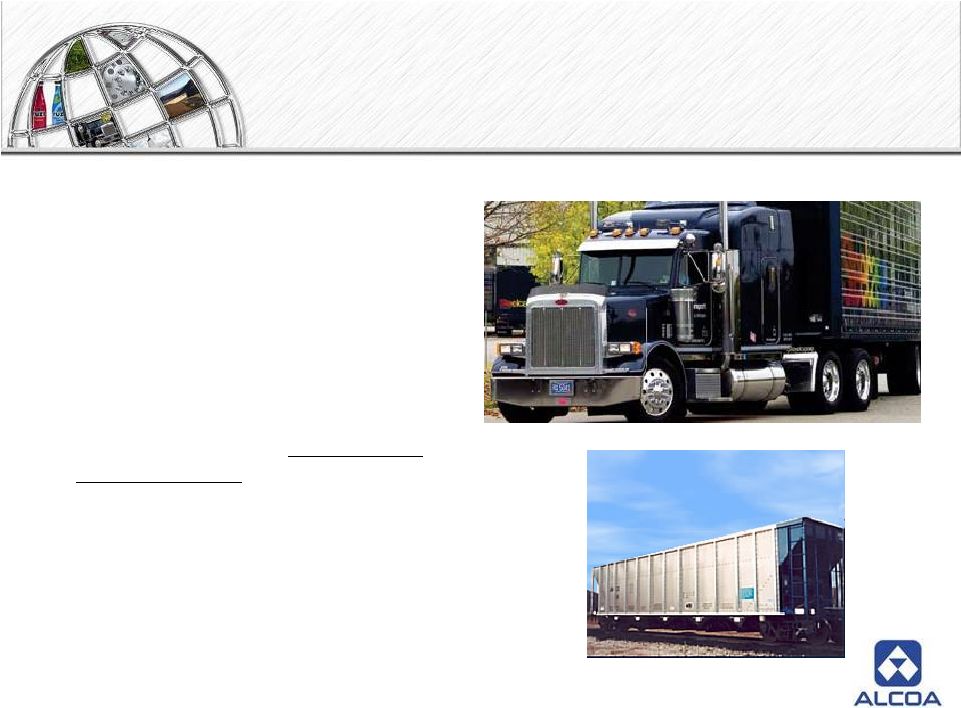

47 CRU’s 12 th World Aluminium Conference -- 2007 Part of the solution: Adding value to everything that moves • Aluminum lightweighting saves energy and emissions in automotive, truck, rail, aerospace and other applications • Emissions saved by aluminum lightweighting can offset the climate impact of aluminum manufacturing • Aluminum can be a greenhouse- neutral material in the foreseeable future |

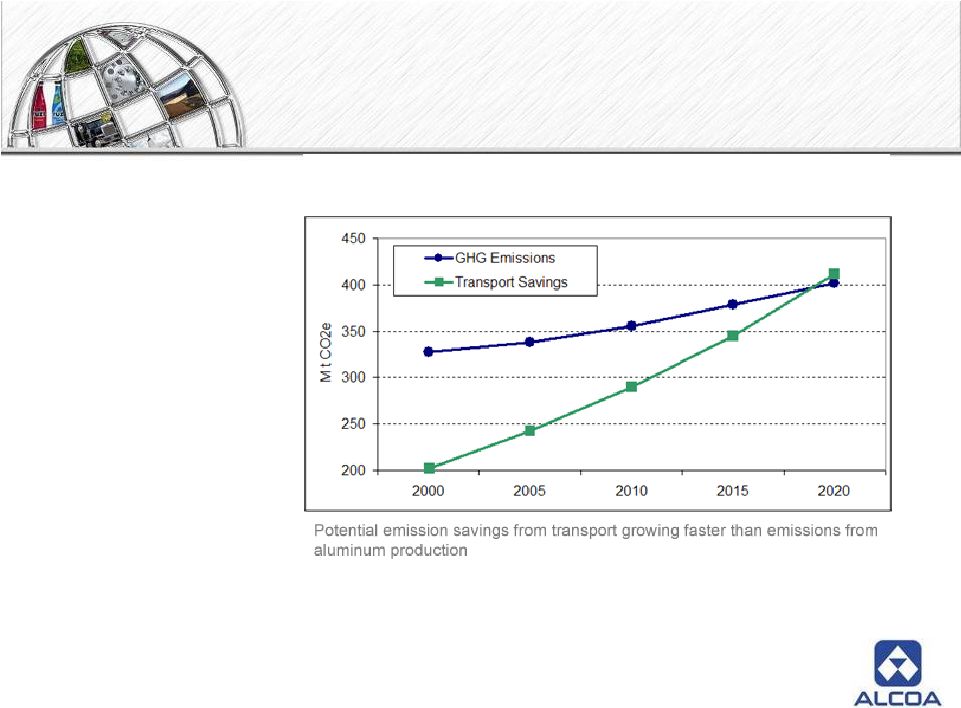

48 CRU’s 12 th World Aluminium Conference -- 2007 Part of the solution: GHG neutral by 2020 • Growing aluminum lightweighting in road and rail vehicles • Production and energy improvements • Recycling • Aluminum’s value in reducing greenhouse gases can offset emissions from production |

Alcoa and Alcan: Alcoa and Alcan: Response to an Response to an evolving industry evolving industry landscape landscape • Creating an industry leader • Evolving competitive landscape and the need for scale • Combined strengths |

50 CRU’s 12 th World Aluminium Conference -- 2007 Creating an industry leader Bauxite & Refining Access to World-Class Reserves 2 nd Quartile on Cost Curve Capacity: 21.5 MMT Energy Self Generation: 34% Long Term Contracts: 54% Smelting Global Rank: #1 2 nd Quartile on Cost Curve Capacity: 7.8 MMT End Markets Renewable Hydro: 54% Building & Construction Packaging Commercial Transportation Automotive Aerospace Global Rank: #1 |

51 CRU’s 12 th World Aluminium Conference -- 2007 Evolving competitive landscape Access to quality bauxite and alumina • Aluminum consumption projected to double over 15 years • Emerging global competitors in Russia, China, India and the Middle East • Scale required to maintain competitiveness • Evolving end markets demanding product innovation Industry Fundamentals Access to long-term, low cost energy Innovation through world-class technology and R&D Proven commitment to sustainability Keys to Success Alcoa / Alcan well positioned to compete with large global peers and deliver profitable growth |

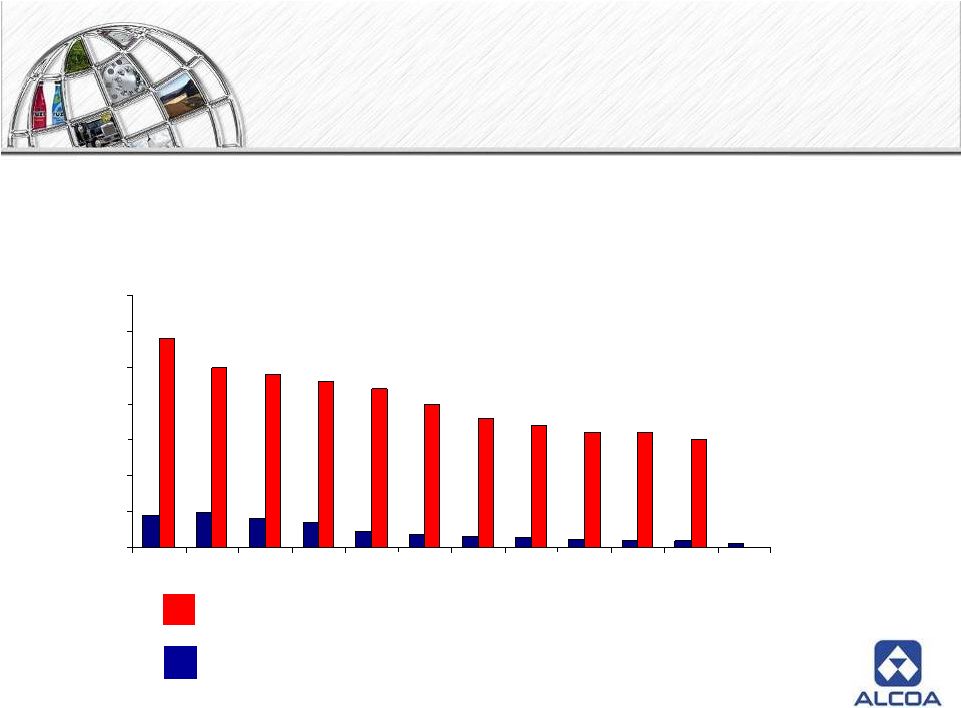

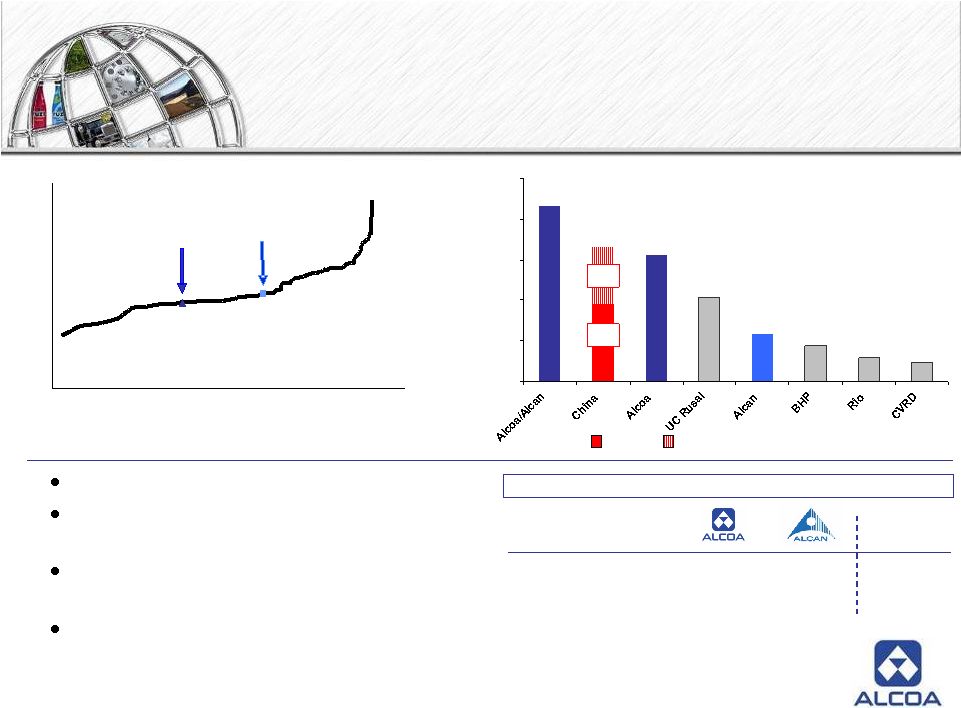

52 Industry landscape demands large scale Source: Factset and public filings. Market data as of May 4, 2007. Note: Alcoa / Alcan represents the combined enterprise value pro forma for shares and new debt issued for transaction. (1) United Company Rusal. Enterprise value estimate per Wall Street research. $155 $121 $93 $91 $66 $55 $41 $41 $41 $38 $30 $29 $28 $27 $25 $74 $0 $20 $40 $60 $80 $100 $120 $140 $160 $180 Top 15 Metals & Mining Companies Combination creates the 5 th largest metals & mining company in the world |

53 South America 6.5% CIS/E. Europe 5.1% BHP Billiton 5.6% India 3.2% Alcan 8.3% Alcoa 19.8% Transforming alumina landscape Alcoa 23.2% Reynolds 5.7% Pechiney 3.5% India 2.8% E. Europe 3.9% South America 5.8% Alcan 9.8% Alusuisse 2.3% Billiton 3.4% Inespal 2.1% 1998 2006 Total Market: 53 MMT Total Market: 79 MMT Source: CRU Note: Percentages may not add to 100% Significant Growth in the East Alumina Capacity Rusal 13.2% Chalco 12.1% Other China 9.8% Hydro 2% RTZ Comalco 4% Other W. World 10% China 6.8% CIS 10.8% Hydro 1% VAW 1% Comalco 3% Other W. World 15% |

54 Alcan 9.4% Alcoa 10.9% Middle East 4.2% BHP Billiton 3.5% India 2.1% CIS/E. Europe 2.8% South America 3.9% Transforming aluminum landscape Rusal 10.3% Chalco 9.2% Other China 21.0% Alcoa 8.9% Pechiney 3.3% Reynolds 4.5% E. Europe 1.9% Middle East 3.6% Alcan 6.7% Alusuisse 1.1% Billiton 4.2% Inespal 1.4% Alumax 2.8% 1998 2006 Significant Growth in the East Aluminum Capacity Total Market: 25 MMT Total Market: 39 MMT Source: CRU Note: Percentages may not add to 100% Hydro 3% VAW 2% Comalco 3% Other W. World 29% Hydro 4% RTZ Comalco 2% Other W. World 16% China 10.4% CIS 14.9% |

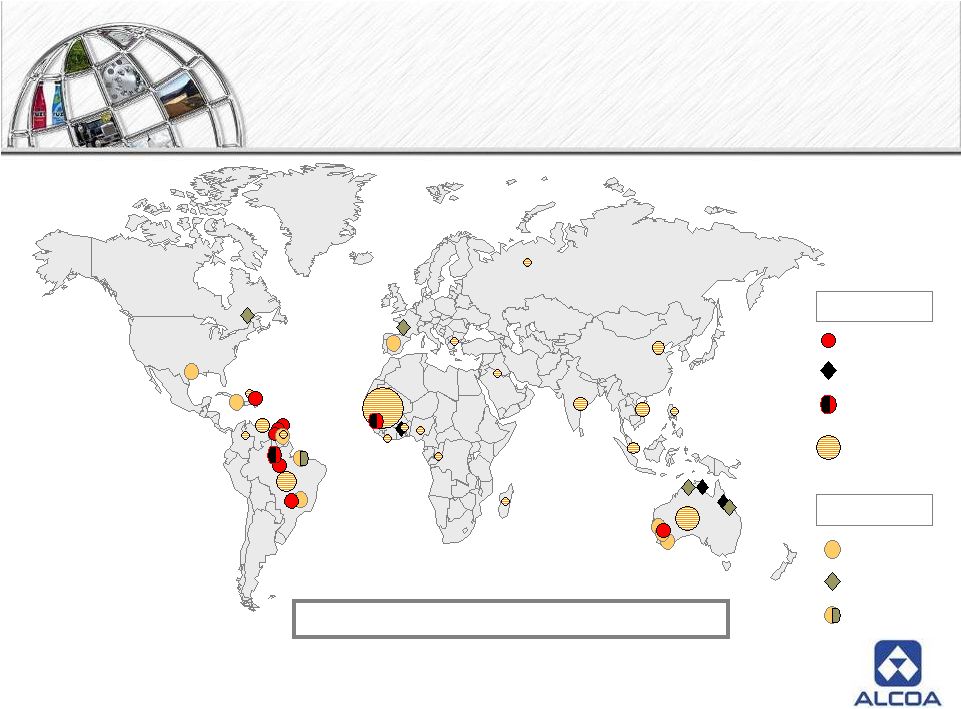

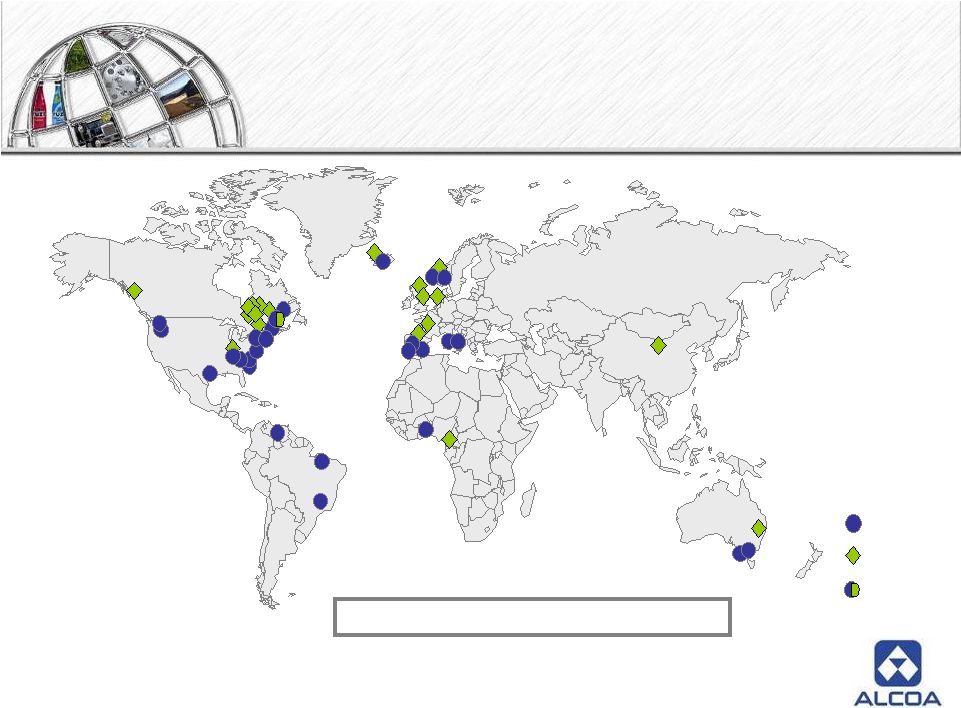

55 CRU’s 12 th World Aluminium Conference -- 2007 Access to quality bauxite & alumina Alcoa Alcan Shared Alcoa Alcan Shared Total Potential Bauxite Alumina 12 mines and 13 refineries on 6 continents Note: Includes ownership in JVs |

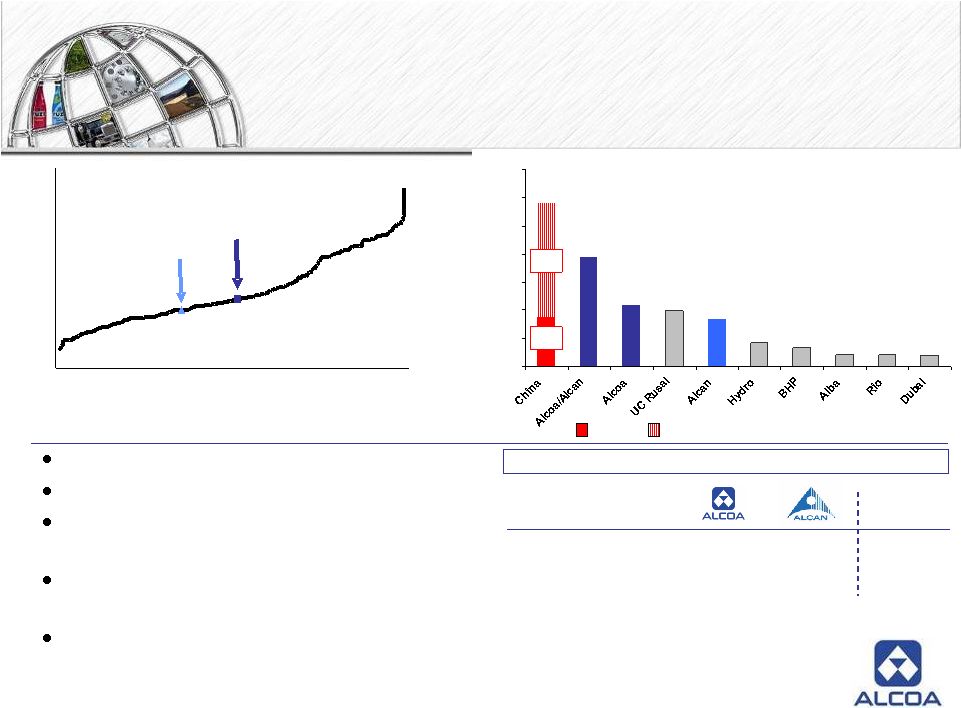

56 CRU’s 12 th World Aluminium Conference -- 2007 World class bauxite and alumina franchise 9,564 2,269 2,930 4,448 5,907 10,443 15,617 21,524 6,926 16,490 0 5,000 10,000 15,000 20,000 25,000 Alumina Refinery Cash Costs ($/MT) 0 50 100 150 200 250 300 350 400 450 0 10,000 20,000 30,000 40,000 50,000 60,000 70,000 Worldwide Production - 000 MT 2006 Cost Curve Alcan Average Alcoa Average 66 th Percentile 38 th Percentile Bauxite & Alumina 2006 ($Millions) 2006 Refining Capacity (kMT) Chalco Other China Source: CRU full operating cost, Alcoa analysis; Company filings Global supplier with premier facilities Low cost production base - majority of production in bottom half of cost curve Best in class operational expertise and technology Investing in high return growth projects Combined Total Revenue 4,929 3,845 8,774 EBITDA 1,670 609 2,279 |

57 CRU’s 12 th World Aluminium Conference -- 2007 Attractive smelter portfolio Alcoa Alcan Shared 46 smelters on 6 continents Note: Includes ownership in JVs |

58 CRU’s 12 th World Aluminium Conference -- 2007 Attractive smelter portfolio 7,788 855 1,364 1,683 3,418 3,985 4,370 3,534 853 771 8,096 11,630 0 2,000 4,000 6,000 8,000 10,000 12,000 14,000 Primary Metals Aluminum Smelter Cash Costs ($/MT) 1,000 1,200 1,400 1,600 1,800 2,000 2,200 2,400 2,600 2,800 3,000 0 5,000 10,000 15,000 20,000 25,000 30,000 Worldwide Production - 000 MT 2006 Cost Curve Alcan Average Alcoa Average 34 th Percentile 51 st Percentile 2006 Smelting Capacity (kMT) Chalco Other China 2006 ($Millions) Global supplier with premier facilities Low cost production base Best in class operational expertise and technology 88% of power requirement self-generated or under long-term contracts Investing in high return growth projects Source: CRU full operating cost, Alcoa analysis; Company filings Combined Total Revenue 12,379 11,147 23,526 EBITDA 2,881 2,962 5,843 |

Alcoa aspires to be the best company in the world. |