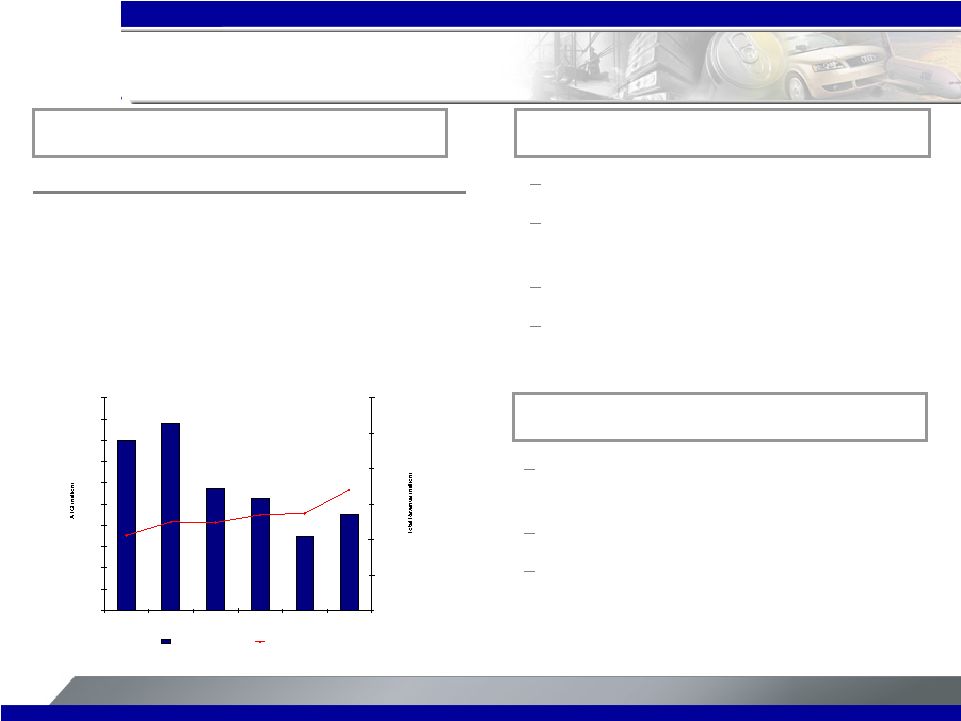

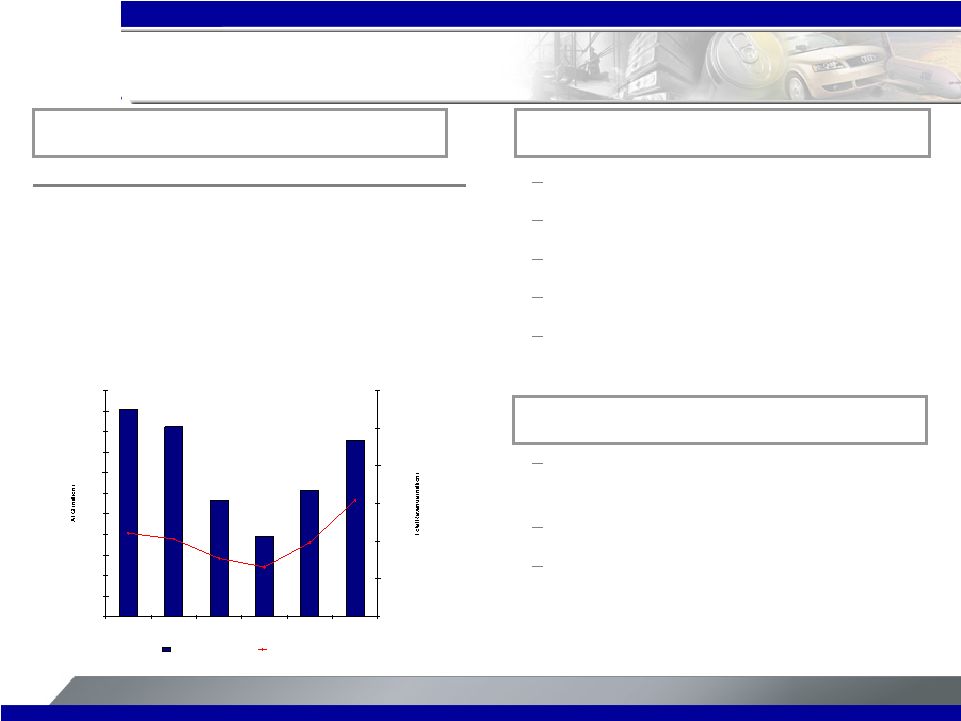

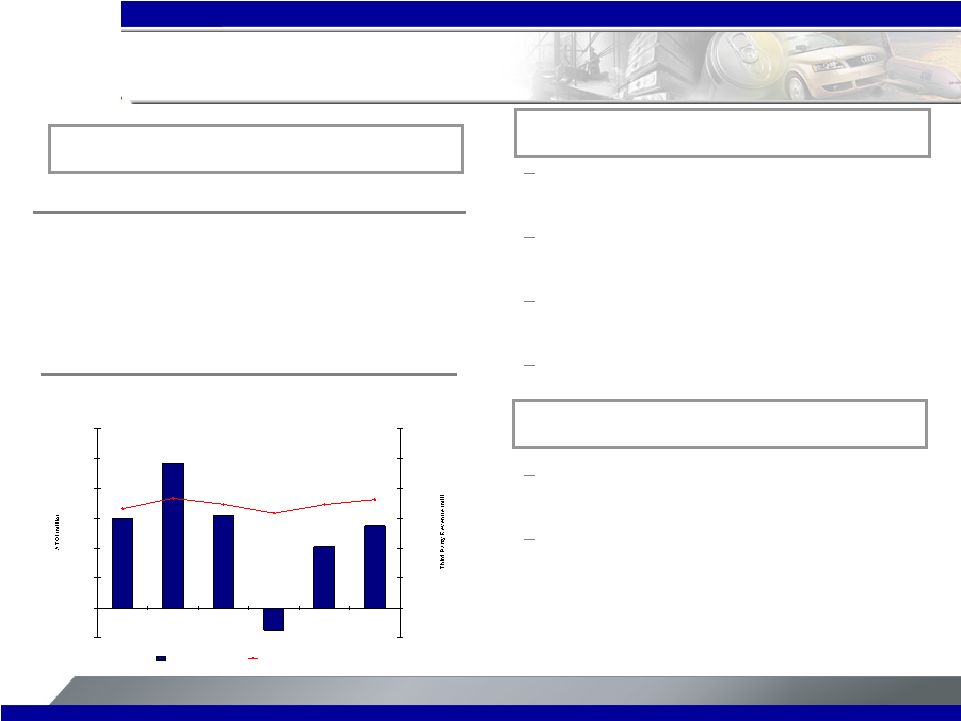

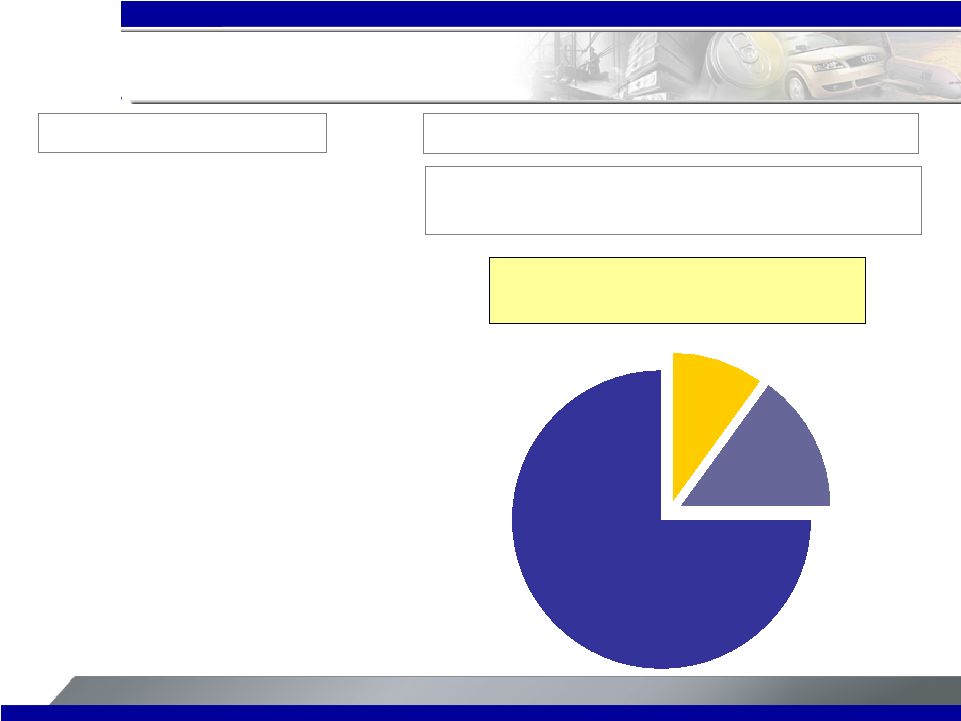

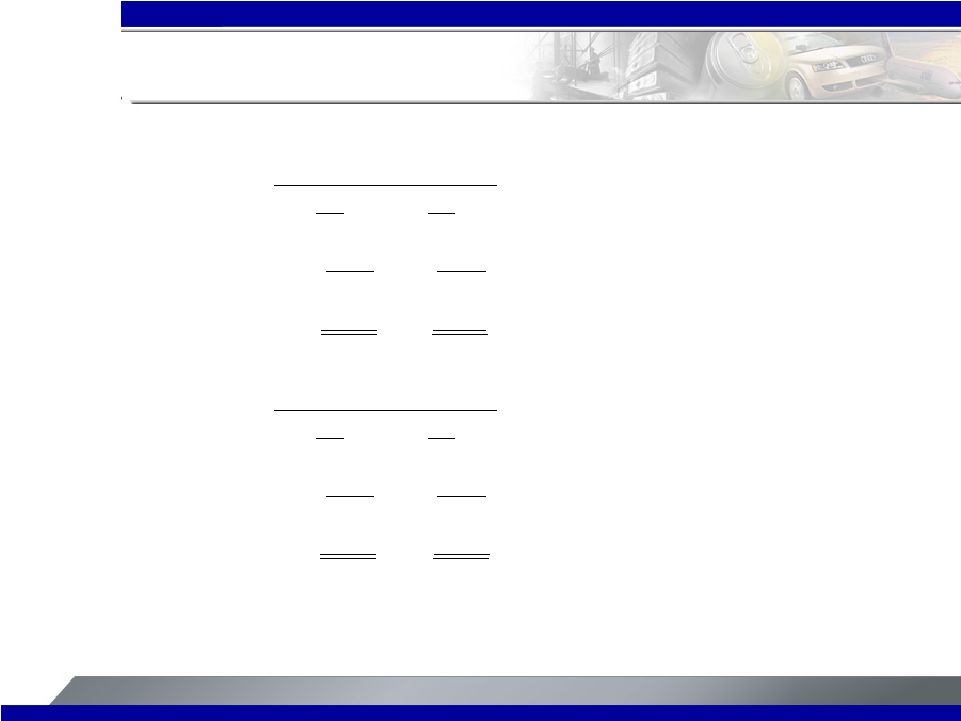

[Alcoa logo] 46 Engineered Products & Solutions Segment Realignment Summary EPS SEGMENT RESTATED SEGMENT INFO - 2005 ($ in millions, shipments in thousands of metric tons) ENGINEERED PRODUCTS AND SOLUTIONS SEGMENT 2005 Third-Party Shipments, as previously reported 145 Add: Building and construction systems Less: Russia Forgings and other 77 Third-Party Shipments, as reclassified 222 Third-Party Sales, as previously reported 5,032 $ Add: Building and construction systems Less: Russia Forgings and other 685 Third-Party Sales, as reclassified 5,717 $ ATOI, as previously reported 203 $ Add: Building and construction systems Less: Russia Forgings and other 29 ATOI, as reclassified 232 $ In the first quarter of 2008, management approved a realignment of Alcoa's reportable segments to better reflect the core businesses in which Alcoa operates and how it is managed. This realignment consisted of eliminating the Extruded and End Products segment, and realigning its component businesses, which had the following effect on the Engineered Products and Solutions segment: the building and construction systems business is now reported in the Engineered Products and Solutions segment and the Russian forgings business was moved from the Engineered Products-and Solutions segment to the Flat-Rolled Products segment, where total Russian operations are now reported. Prior period amounts were reclassified to reflect the new segment structure. Also, the Engineered Solutions segment was renamed the Engineered Products and Solutions segment. |