Alcoa Logo Alcoa Logo 1 st Quarter 2010 Earnings Conference April 12, 2010 1 Exhibit 99.2 |

Alcoa Logo Forward-Looking Statements Today’s discussion may include “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. Such statements relate to future events and expectations and involve known and unknown risks and uncertainties. Alcoa’s actual results or actions may differ materially from those projected in the forward-looking statements. For a summary of the specific risk factors that could cause results to differ materially from those expressed in the forward-looking statements, please refer to Alcoa’s Form 10-K for the year ended December 31, 2009, and other reports filed with the Securities and Exchange Commission. 2 |

Alcoa Logo Alcoa Logo Chuck McLane Executive Vice President and Chief Financial Officer 3 |

Alcoa Logo 1 st Quarter 2010 Financial Overview Continued benefits from Cash Sustainability Initiatives COGS % Sales of 82.1%, SGA % Sales of 4.9% EBITDA of $596 million – highest since Q3’08 Loss from continuing operations of $194 million, or $0.19 per share – Restructuring and special items total $295 million, or $0.29 per share – Net loss of $201 million, or $0.20 per share Realized aluminum price up 8%; realized alumina price up 13% Debt to Capital of 38.1%, down 60 basis points – Total debt reduced to $9.75 billion; Cash on hand of $1.3 billion 4 |

Alcoa Logo Revenue Change by Market 0% 5% (6%) 39% 34% (21%) (32%) 1% (16%) (10%) (22%) 40% (6%) 18% 58% (36%) (24%) (18%) 48% 102% 1Q’10 Third Party Revenue Sequential Change Year-Over-Year Change 5 14% 5% 6% 2% 6% 2% 12% 5% 13% 35% Aerospace Automotive B&C Comm. Transport Industrial Products IGT Packaging Distribution/Other Alumina Primary Metals |

Alcoa Logo Sequential Income Statement Summary 6 $ Millions 4Q’09 1Q’10 Change Sales $5,433 $4,887 ($546) Cost of Goods Sold $4,905 $4,013 ($892) COGS % Sales 90.3% 82.1% (8.2 % pts.) Selling, General Administrative, Other $291 $239 ($52) SGA % Sales 5.4% 4.9% (0.5 % pts.) Restructuring and Other Charges $69 $187 $118 Effective Tax Rate 34.8% (95.5%) N/A Income (Loss) from Continuing Operations ($266) ($194) $72 Income (Loss) from Discontinued Operations ($11) ($7) $4 |

Alcoa Logo 7 1 st Quarter Restructuring and Special Items *Restructuring Related includes ($119) million of restructuring in the corporate segment and ($5) million of closure related inventory in COGS in the Alumina and Primary metal segments $ Millions After-Tax & Non- Controlling Interests Earnings Per Share Income Statement Classification Segment Restructuring Related* ($124) ($0.12) -- -- Discrete Tax Items ($112) ($0.11) Taxes Corporate Special Items: ($59) ($0.06) -- -- Mark -to-Market Power Contracts ($31) ($0.03) Other Income/Expense Corporate Power Outages ($17) ($0.02) Revenue & Cost of Goods Sold Alumina/Primary Environmental Accrual ($11) ($0.01) Cost of Goods Sold Corporate Total ($295) ($0.29) |

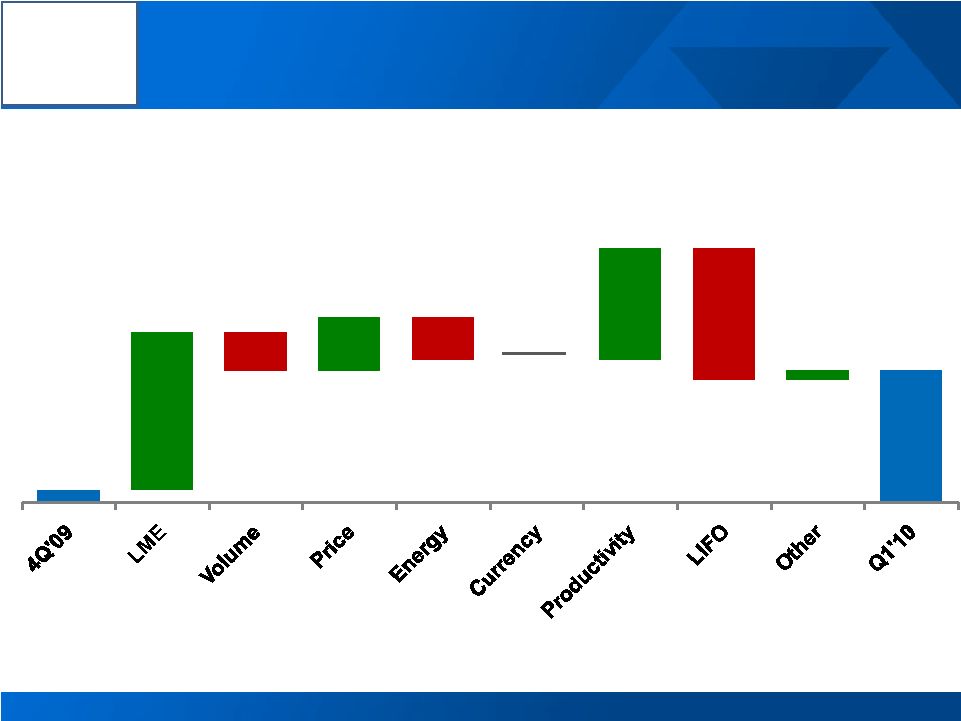

Alcoa Logo 1 st Quarter 2010 vs. 4th Quarter 2009 Earnings Bridge 8 See appendix for reconciliation $9 $121 ($30) $41 ($33) $0 $86 ($101) $8 $101 Income (Loss) from Continuing Operations excluding Restructuring & Other Special Items ($ millions) |

Alcoa Logo Sensitivity Summary 9 +/- $100/MT = +/- $200 million LME Aluminum Annual Net Income Sensitivity Currency Annual Net Income Sensitivity +/- 10% versus USD Australian $ +/- $75 million Brazilian $ +/- $50 million Euro € +/- $40 million Canadian $ +/- $35 million |

Alcoa Logo Alumina 1 st Quarter Highlights 2 nd Quarter Outlook 1 st Quarter Business Conditions 10 1Q 09 4Q 09 1Q 10 Production (kmt) 3,445 3,897 3,866 3 rd Party Shipments (kmt) 1,737 2,716 2,126 3 rd Party Revenue ($MM) 430 760 638 ATOI ($MM) 35 19 72 Realized 3rd party Alumina price up 13% Cash sustainability initiative benefits Sao Luis power outage negatively impacted cost by $10 million Higher Juruti costs of $20 million Pricing to follow two month lag on LME Continued benefits from cash sustainability initiatives Potential labor disruptions in Australia Production projected to increase by 100 KMT 1 st Quarter Performance Bridge $ Millions |

Alcoa Logo Primary Metals 1 st Quarter Highlights 1 st Quarter Business Conditions 2 nd Quarter Outlook 11 1Q 09 4Q 09 1Q 10 Production (kmt) 880 897 889 3 rd Party Shipments (kmt) 683 878 695 3 rd Party Revenue ($MM) 844 1,900 1,702 3 rd Party Price ($/MT) 1,567 2,155 2,331 ATOI ($MM) (212) (214) 123 Realized pricing up 8% Positive currency impact of $14 million Non-recurrence of Q4 ‘09 non-cash charge related to Italy power decision Productivity improvement of $15 million Higher power costs, particularly in Italy Rockdale outage negatively affected quarter by $ 11 million Pricing to follow 15-day lag Continued benefits from cash sustainability initiatives Rockdale power station running below capacity US labor negotiations Production equal to first quarter 1 st Quarter Performance Bridge $ Millions |

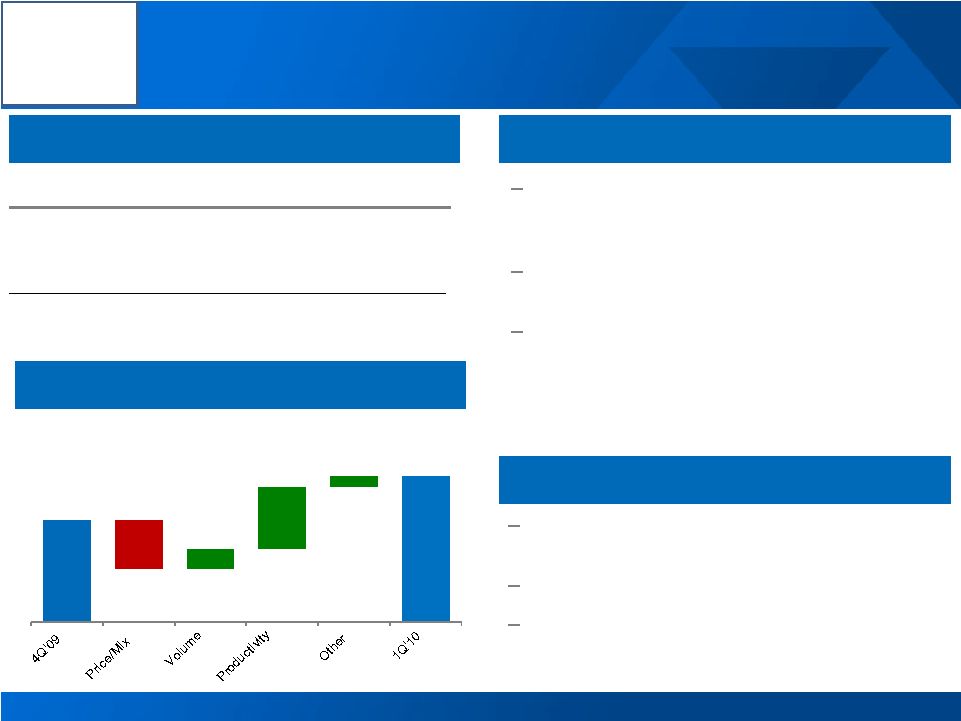

Alcoa Logo Flat Rolled Products 12 2 Quarter Outlook 1 Quarter Business Conditions 1 Quarter Highlights ATOI $ Millions 1Q 09 4Q 09 1Q 10 Global Rolled Products, excl Russia, China & Other 3 63 47 Russia, China & Other (64) (26) (17) Total ATOI (61) 37 30 Improved mix and pricing across every region Decision to curtail sales in RPD drove lower volumes Gains from cash sustainability initiatives – overhead reduction of 8% sequentially Higher energy costs in North America and Russia Continued benefits from cash sustainability initiatives Modest improvement in aerospace and industrial markets North American RPD volumes remain at low levels 1 Quarter Performance Bridge $ Millions st st st nd $37 $50 ( $41) ($2) ( $6) $3 ($11) $30 |

Alcoa Logo Engineered Products and Solutions 1 st Quarter Business Conditions 2 nd Quarter Outlook 1 st Quarter Highlights 13 ATOI % Sales equal to year ago quarter despite $200M decline in sales driven by strong performance in cash sustainability initiatives Volume improvements in Commercial Transport and Industrial Products markets Continued downward pressure in IGT and Building and Construction markets Continued benefits from cash sustainability initiatives Market conditions show slight improvement Aerospace destocking slowly coming to an end $ Millions 1Q 09 4Q 09 1Q 10 3 rd Party Revenue 1,270 1,097 1,074 ATOI 95 57 81 ATOI % of Revenue 7.5% 5.2% 7.5% 1 st Quarter Performance Bridge $ Millions $57 ($26) $12 $34 $6 $81 |

Alcoa Logo 1 st Quarter 2010 Cash Flow Overview 14 See appendix for free cash flow reconciliation ($ Millions) 1Q'09 4Q'09 1Q'10 Net Loss (487) ($268) ($179) DD&A 283 369 358 Change in Working Capital 351 522 (336) Pension Contributions (34) (26) (22) Taxes / Other Adjustments (384) 527 378 Cash From Operations (271) $1,124 $199 Dividends to Shareholders (137) (30) (32) Change in Debt (305) (286) (42) Dividends to Noncontrolling Interest (77) (47) (72) Contributions from Noncontrolling Interest 159 153 27 Other Financing Activities 863 0 (61) Cash From Financing Activities 503 ($210) ($180) Capital Expenditures (471) (363) (221) Other Investing Activities 607 (137) 13 Cash From Investing Activities 136 (500) (208) |

We Are Focused on Achieving Our 2010 Goals 15 Procurement reduction of $2.5 billion Overhead reduction of $500 million Capital expenditures of $1.25 billion Days Working Capital reduction of 2 days Driving Positive Free Cash Flow |

Alcoa Logo Alcoa Logo Klaus Kleinfeld President and Chief Executive Officer 16 |

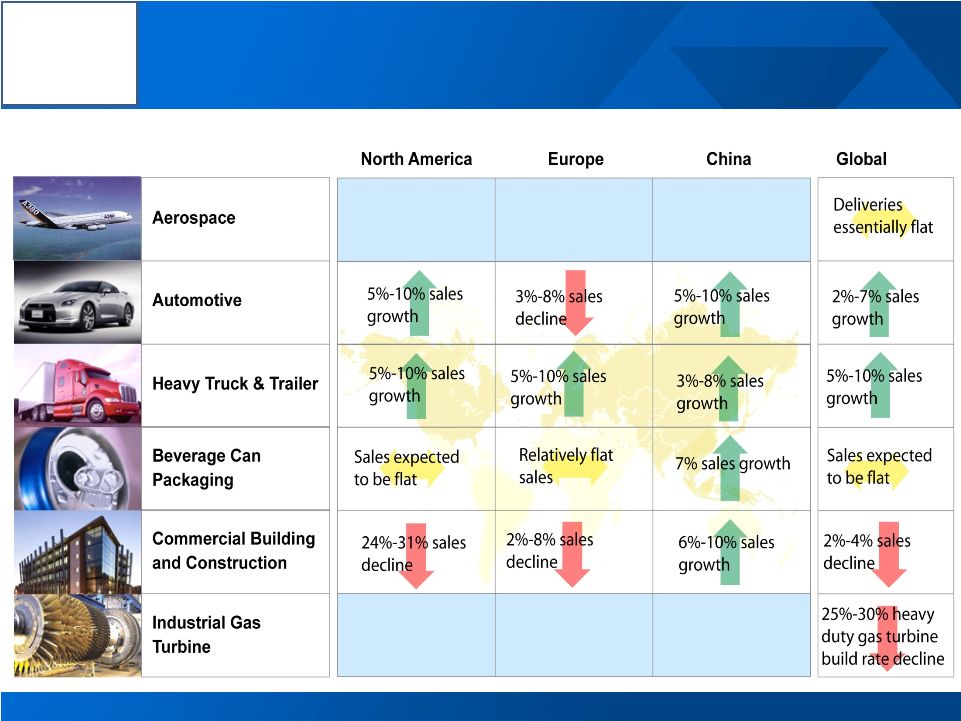

Alcoa Logo Market Conditions in 2010 Alcoa End Markets: Current Assessment of 2010 vs. 2009 Conditions Source: Alcoa analysis 17 |

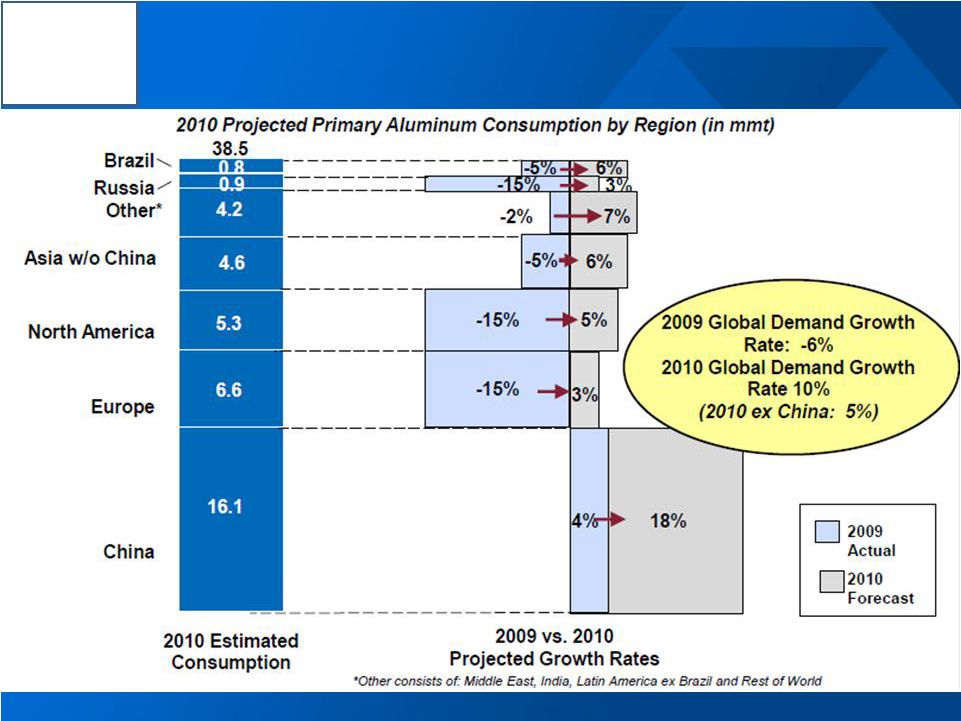

Alcoa Logo Global Physical Demand to Rise 10% in 2010 18 |

Alcoa Logo Inventories Flat As Stable Demand Drives Premiums Higher Source: Bloomberg, IAI Global inventory days of consumption and regional premiums 45% 118% 266% 66 days of consumption LME at 47 days Non-LME at 19 days $135 / MT $136 / MT $124 / MT 19 0 10 20 30 40 50 60 70 80 LME Shanghai Japan Port Producer 0% 50% 100% 150% 200% 250% 300% 350% 400% Midwest Japan Europe Regional Premium (1-Year Change) |

Alcoa Logo 2010 Annualized Run Rate 23,150 2010 Restarts or Curtailments (365) 2010 Brown/Greenfield Expansion 745 Total Supply 23,530 Demand (22,500) Exports to China, Net (200) Net Surplus 830 China Western World 2010 Primary Aluminum Surplus Is Manageable (in kmt) 2010 Annualized Run Rate 16,100 2010 Restarts or Curtailments 0 2010 Brown//Greenfield Expansion 200 Total Supply 16,300 Demand (16,100) Imports from West, Net 200 Net Surplus 400 Source: Alcoa estimates, Brook Hunt, CRU, CNIA, IAI 20 Surplus Surplus |

Alcoa Logo 2010E Alumina Supply / Demand Balance (in kmt) Source: Alcoa estimates, CRU, CNIA, IAI 2010 Global Alumina in Balance China Western World 21 2010 Annualized Run Rate 27,000 Imports from Western World 5,400 Supply 32,400 Demand (32,400) (Deficit) / Surplus 0 2010 Annualized Run Rate 51,000 Exports to China (5,400) Supply 45,600 Demand (45,400) (Deficit) / Surplus 200 Balanced |

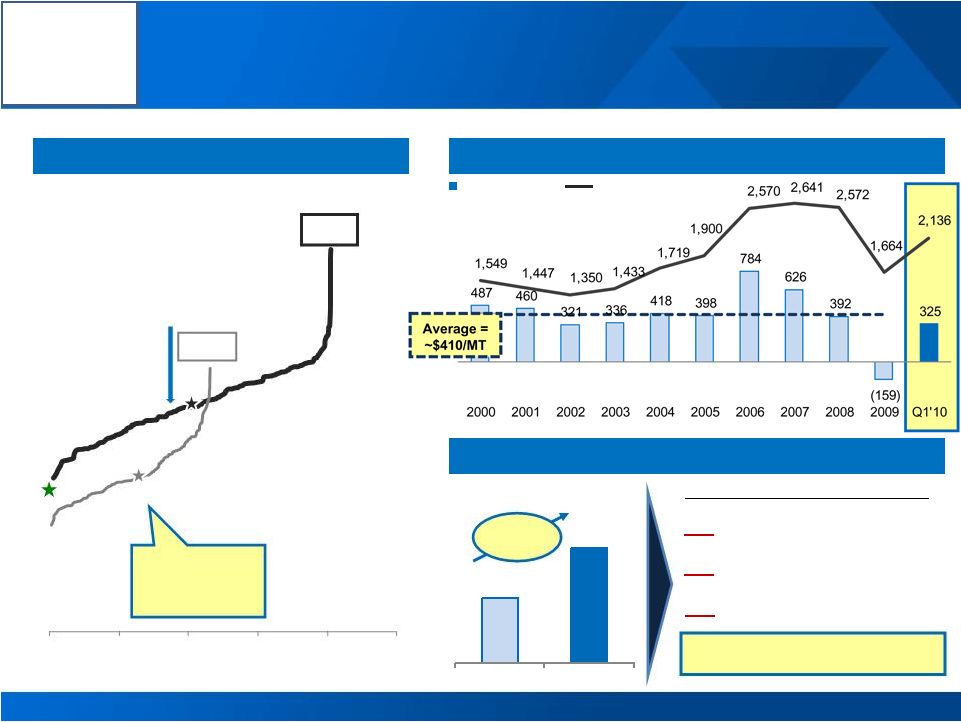

Alcoa Logo 72 62 44 48 68 75 110 104 81 20 49 1,549 1,447 1,350 1,433 1,719 1,900 2,570 2,641 2,572 1,664 2,136 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 Q1'10 0 20,000 40,000 60,000 80,000 100,000 Cumulative Production KMT Significant Value Creation From The Alumina Leader Alumina financial and strategic overview Global Refining Cost Curve LME EBITDA/MT Ma’aden 1st Percentile Online 2014 EBITDA per Metric Ton 22 Source : CRU; Alcoa Analysis 50 th Percentile = $232/MT ~50% increase in midpoint since 2000 Average = ~$70/MT 50 th Percentile = $140MT [Alcoa Logo] Alcoa 25 th Percentile 2000 2009 Tight Market, Rising Cost = Higher Alumina % LME Alcoa 3 rd Party Alumina Sales % LME 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 |

Streamlined Primary Metals Poised to Drive EBITDA Primary Metals financial and strategic overview Global Primary Cost Curve EBITDA per Metric Ton LME EBITDA/MT 23 Future Capacity Growth Challenged Aluminum Demand (MMT) Requires 2.3 MMT per Year 3x Ma’aden Smelters per Year 4x Sao Luis Expansions per Year 20 New Gas Turbines per Year 50 Percentile = $1,755/MT 50 Percentile = $1,183/MT 2009 Ma’aden 1st Percentile Online 2013 45 Percentile Source : CRU; Alcoa Analysis 0 10,000 20,000 30,000 40,000 50,000 Cumulative Production KMT 38.5 68.0 2010 2018 ~50% increase in midpoint since 2000 6% CAGR ~$30 Billion per Year 2000 Alcoa Logo th th th [Alcoa Logo] Alcoa |

Alcoa Logo Rolled Products Positioned to Substantially Improve Returns – Russian can sheet mill fully operational in 2010 – China Bohai mill on schedule for full ramp-up by 2011 – Lowest conversion cost Ma’aden mill on-line in 2013 – Strengthened positions in aerospace, can sheet, lithographic sheet – Exited global foil business – Headcount reduced by 5,000 FTEs since 2008 – Overhead $140 million lower than 2008 Global Flat Rolled Products financial and strategic overview 2009 3 rd Party Sales by Market Segment EBITDA & EBITDA % Sales Strategic Position 24 573 541 495 479 531 620 536 498 254 224 107 EBITDA $Millions EBITDA % Sales 11% 11% 11% 10% 9% 9% 6% 5% 3% 4% 7% 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 Q1'10 Distribution 10% Automotive 4% B&C 5% Commercial Transport 3% Industrial /Other 13% Aerospace 12% Packaging 53% 75% Utilization |

Alcoa Logo EPS Strong Platform for Profitable Growth – Focused the portfolio on strategic segments – 85% of sales are from #1 or #2 market leaders – $440 million of productivity improvement in 2009 – Aerospace destocking is improving – Significant profit accelerators for the future – 787/A380 – Joint Strike Fighter – Heavy Truck market recovery – Rapidly integrated 2 fastener acquisitions Engineered Products & Solutions financial and strategic overview 2009 3 rd Party Sales by Market Segment EBITDA & EBITDA % Sales Strategic Position 25 368 436 287 356 495 536 676 783 922 630 152 EBITDA $Millions EBITDA % Sales 11% 11% 8% 9% 12% 11% 12% 13% 15% 13% 14% 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 Q1'10 Aerospace 47% IGT 14% B&C 20% Commercial Transport 4% Automotive 10% Other 5% 70% Utilization 65% Utilization |

Alcoa Logo Aggressively Pursuing 2010 Operational Targets 26 Procurement Overhead $500 Total Capex* $1,250 Working Capital 35 2010 Cash Sustainability Operational Targets and Actual Performance $ Millions $127 $281 42 $ Millions $ Millions Days Working Capital $2,500 $505 2010 YTD 2010 Target 2010 YTD 2010 Target 2010 YTD 2010 Target 2010 YTD 2010 Target *Total Capex includes investments in Ma’aden project |

Alcoa Logo Alcoa Driving Near-term and Long-term Shareholder Value 27 – End-markets improving – Aluminum demand to rise 10% in 2010 – Global alumina supply/demand in balance – Global primary metal surplus of 12 days – Overhead cost reduction target of $500 million – Procurement cost reduction target of $2.5 billion – Divested underperforming businesses – Strengthened balance sheet Environment Stabilized Exceeding Goals Growing Profitably – Global alumina leader leveraging lowest cost production base – Global aluminum leader reducing cost position – Alcoa Rolled Products leading profitability revitalization – EPS expanding market leadership and competitive distance Momentum Execution Growth |

Alcoa Logo Matthew E. Garth Director, Investor Relations A 390 Park Avenue New York, NY 10022-4608 Telephone: (212) 836-2674 www.alcoa.com Additional Information 28 |

Alcoa Logo A Alcoa Logo |

Alcoa Logo Effective Tax Rate Effective tax rate, excluding discrete tax items is a non-GAAP financial measure. Management believes that the Effective tax rate, excluding discrete tax items is meaningful to investors because it provides a view of Alcoa’s operational tax rate. 30 $ Millions 1Q’09 (Loss) income from continuing operations before income taxes ($88) Provision for income taxes $84 Effective tax rate as reported (95.5%) Discrete tax provisions: Medicare Part D - $79 Transaction-related and other items - $33 Subtotal - Discrete tax (benefits) provisions $112 (Benefit) Provision for income taxes excluding discrete tax (benefits) provisions ($28) Effective tax rate excluding discrete tax (benefits) provisions 31.8% |

Alcoa Logo Reconciliation of ATOI to Consolidated Net (Loss) Income Attributable to Alcoa 31 (in millions) 1Q09 2Q09 3Q09 4Q09 2009 1Q10 Total segment ATOI $ (143) $ (132) $ 142 $ (101) $ (234) $ 306 Unallocated amounts (net of tax): Impact of LIFO 29 39 80 87 235 (14) Interest income 1 8 (1) 4 12 3 Interest expense (74) (75) (78) (79) (306) (77) Noncontrolling interests (10) 5 (47) (9) (61) (22) Corporate expense (71) (70) (71) (92) (304) (67) Restructuring and other charges (46) (56) (3) (50) (155) (122) Discontinued operations (17) (142) 4 (11) (166) (7) Other (166) (31) 51 (26) (172) (201) Consolidated net (loss) income attributable to Alcoa $ (497) $ (454) $ 77 $ (277) $ (1,151) $ (201) |

Alcoa Logo Reconciliation of Alcoa EBITDA 32 (in millions) Quarter ended March 31, 2010 Net loss attributable to Alcoa $ (201) Add: Net income attributable to noncontrolling interests 22 Loss from discontinued operations 7 Provision for income taxes 84 Other expenses, net 21 Interest expense 118 Restructuring and other charges 187 Provision for depreciation, depletion, and amortization 358 Earnings before interest, taxes, and depreciation and amortization (EBITDA) $ 596 Alcoa’s definition of EBITDA is net margin plus an add-back for depreciation, depletion, and amortization. Net margin is equivalent to Sales minus the following items: Cost of goods sold; Selling, general administrative, and other expenses; Research and development expenses; and Provision for depreciation, depletion, and amortization. EBITDA is a non- GAAP financial measure. Management believes that this measure is meaningful to investors because EBITDA provides additional information with respect to Alcoa’s operating performance and the Company’s ability to meet its financial obligations. The EBITDA presented may not be comparable to similarly titled measures of other companies. |

Alcoa Logo Reconciliation of Adjusted Income 33 (in millions) Quarter ended December 31, 2009 March 31, 2010 Net loss attributable to Alcoa $ (277) $ (201) Loss from discontinued operations (11) (7) Loss from continuing operations attributable to Alcoa (266) (194) Restructuring and other charges 49 119 Discrete tax items* (82) 112 Special items** 308 64 Income from continuing operations attributable to Alcoa – as adjusted $ 9 $ 101 Income from continuing operations attributable to Alcoa – as adjusted is a non-GAAP financial measure. Management believes that this measure is meaningful to investors because management reviews the operating results of Alcoa excluding the impacts of restructuring and other charges, discrete tax items, and special items. There can be no assurances that additional restructuring and other charges, discrete tax items, and special items will not occur in future periods. To compensate for this limitation, management believes that it is appropriate to consider both Loss from continuing operations attributable to Alcoa determined under GAAP as well as Income from continuing operations attributable to Alcoa – as adjusted. * Discrete tax items include the following: charges for a change in the tax treatment of federal subsidies received related to prescription drug benefits provided under certain retiree health benefit plans ($79), unbenefitted losses in Russia, China, and Italy ($22) (will be offset in future 2010 quarters), interest due to the IRS related to a previously deferred gain associated with the 2007 formation of the former soft alloy extrusions joint venture ($6), and a change in the anticipated sale structure of the Transportation Products Europe business ($5) for the quarter ended March 31, 2010; and a benefit for the reorganization of an equity investment in Canada (-$71), a charge for the write-off of deferred tax assets related to operations in Italy ($41), a benefit for a tax rate change in Iceland (-$31), and a benefit for the reversal of a valuation allowance on net operating losses in Norway (-$21) for the quarter ended December 31, 2009. ** Special items include the following: charges related to unfavorable mark-to-market changes in derivative contracts ($31), power outages at the Rockdale, TX and São Luís, Brazil facilities ($17), an additional environmental accrual for the Grasse River remediation in Massena, NY ($11), and the write off of inventory related to the permanent closures of certain U.S. facilities ($5) for the quarter ended March 31, 2010; and charges related to a recent European Commission’s ruling on electricity pricing for smelters in Italy ($250), a tax settlement related to an equity investment in Brazil ($24), an estimated loss on excess power at our Intalco smelter ($19), and an environmental accrual for smelters in Italy ($15) for the quarter ended December 31, 2009. |

Alcoa Logo Reconciliation of Alumina EBITDA 34 ($ in millions) 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 1Q10 Alumina After-tax operating income (ATOI) $ 585 $ 471 $ 315 $ 415 $ 632 $ 682 $ 1,050 $ 956 $ 727 $ 112 $ 72 Add: Depreciation, depletion, and amortization 163 144 139 147 153 172 192 267 268 292 92 Equity (income) loss (3) (1) (1) – (1) – 2 (1) (7) (8) (2) Income taxes 279 184 130 161 240 246 428 340 277 (22) 27 Other (12) (17) (14) (55) (46) (8) (6) 2 (26) (92) 1 Earnings before interest, taxes, depreciation, and amortization (EBITDA) $ 1,012 $ 781 $ 569 $ 668 $ 978 $ 1,092 $ 1,666 $ 1,564 $ 1,239 $ 282 $ 190 Production (thousand metric tons) (kmt) 13,968 12,527 13,027 13,841 14,343 14,598 15,128 15,084 15,256 14,265 3,866 EBITDA/Production ($ per metric ton) 72 62 44 48 68 75 110 104 81 20 49 Alcoa’s definition of EBITDA is net margin plus an add-back for depreciation, depletion, and amortization. Net margin is equivalent to Sales minus the following items: Cost of goods sold; Selling, general administrative, and other expenses; Research and development expenses; and Provision for depreciation, depletion, and amortization. The Other line in the table above includes gains/losses on asset sales and other nonoperating items. EBITDA is a non-GAAP financial measure. Management believes that this measure is meaningful to investors because EBITDA provides additional information with respect to Alcoa’s operating performance and the Company’s ability to meet its financial obligations. The EBITDA presented may not be comparable to similarly titled measures of other companies. |

Alcoa Logo Reconciliation of Primary Metals EBITDA 35 ($ in millions) 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 1Q10 Primary Metals After-tax operating income (ATOI) $ 1,000 $ 905 $ 650 $ 657 $ 808 $ 822 $ 1,760 $ 1,445 $ 931 $ (612) $ 123 Add: Depreciation, depletion, and amortization 311 327 300 310 326 368 395 410 503 560 147 Equity (income) loss (50) (52) (44) (55) (58) 12 (82) (57) (2) 26 – Income taxes 505 434 266 256 314 307 726 542 172 (365) 18 Other (41) (8) (47) 12 20 (96) (13) (27) (32) (176) 1 Earnings before interest, taxes, depreciation, and amortization (EBITDA) $ 1,725 $ 1,606 $ 1,125 $ 1,180 $ 1,410 $ 1,413 $ 2,786 $ 2,313 $ 1,572 $ (567) $ 289 Production (thousand metric tons) (kmt) 3,539 3,488 3,500 3,508 3,376 3,554 3,552 3,693 4,007 3,564 889 EBITDA/Production ($ per metric ton) 487 460 321 336 418 398 784 626 392 (159) 325 Alcoa’s definition of EBITDA is net margin plus an add-back for depreciation, depletion, and amortization. Net margin is equivalent to Sales minus the following items: Cost of goods sold; Selling, general administrative, and other expenses; Research and development expenses; and Provision for depreciation, depletion, and amortization. The Other line in the table above includes gains/losses on asset sales and other nonoperating items. EBITDA is a non-GAAP financial measure. Management believes that this measure is meaningful to investors because EBITDA provides additional information with respect to Alcoa’s operating performance and the Company’s ability to meet its financial obligations. The EBITDA presented may not be comparable to similarly titled measures of other companies. |

Alcoa Logo Reconciliation of Flat-Rolled Products EBITDA 36 ($ in millions) 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 1Q10 Flat-Rolled Products After-tax operating income (ATOI) $ 296 $ 253 $ 225 $ 222 $ 254 $ 278 $ 233 $ 178 $ (3) $ (49) $ 30 Add: Depreciation, depletion, and amortization 153 167 184 190 200 220 223 227 216 227 59 Equity (income) loss (3) 2 4 1 1 – 2 – – – – Income taxes 126 124 90 71 75 121 58 92 35 48 18 Other 1 (5) (8) (5) 1 1 20 1 6 (2) – Earnings before interest, taxes, depreciation, and amortization (EBITDA) $ 573 $ 541 $ 495 $ 479 $ 531 $ 620 $ 536 $ 498 $ 254 $ 224 $ 107 Total sales $ 5,167 $ 4,868 $ 4,571 $ 4,768 $ 6,042 $ 7,081 $ 8,610 $ 9,597 $ 9,184 $ 6,182 $ 1,481 EBITDA/Total sales 11% 11% 11% 10% 9% 9% 6% 5% 3% 4% 7% Alcoa’s definition of EBITDA is net margin plus an add-back for depreciation, depletion, and amortization. Net margin is equivalent to Sales minus the following items: Cost of goods sold; Selling, general administrative, and other expenses; Research and development expenses; and Provision for depreciation, depletion, and amortization. The Other line in the table above includes gains/losses on asset sales and other nonoperating items. EBITDA is a non-GAAP financial measure. Management believes that this measure is meaningful to investors because EBITDA provides additional information with respect to Alcoa’s operating performance and the Company’s ability to meet its financial obligations. The EBITDA presented may not be comparable to similarly titled measures of other companies. |

Alcoa Logo Reconciliation of Engineered Products and Solutions EBITDA 37 ($ in millions) 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 1Q10 Engineered Products and Solutions After-tax operating income (ATOI) $ 125 $ 189 $ 63 $ 124 $ 156 $ 271 $ 365 $ 435 $ 533 $ 315 $ 81 Add: Depreciation, depletion, and amortization 165 186 150 166 168 160 152 163 165 177 41 Equity (income) loss (1) – – – – – 6 – – (2) (1) Income taxes 79 61 39 55 65 116 155 192 222 139 31 Other – – 35 11 106 (11) (2) (7) 2 1 – Earnings before interest, taxes, depreciation, and amortization (EBITDA) $ 368 $ 436 $ 287 $ 356 $ 495 $ 536 $ 676 $ 783 $ 922 $ 630 $ 152 Total sales $ 3,386 $ 4,141 $ 3,492 $ 3,905 $ 4,283 $ 4,773 $ 5,428 $ 5,834 $ 6,199 $ 4,689 $ 1,074 EBITDA/Total sales 11% 11% 8% 9% 12% 11% 12% 13% 15% 13% 14% Alcoa’s definition of EBITDA is net margin plus an add-back for depreciation, depletion, and amortization. Net margin is equivalent to Sales minus the following items: Cost of goods sold; Selling, general administrative, and other expenses; Research and development expenses; and Provision for depreciation, depletion, and amortization. The Other line in the table above includes gains/losses on asset sales and other nonoperating items. EBITDA is a non-GAAP financial measure. Management believes that this measure is meaningful to investors because EBITDA provides additional information with respect to Alcoa’s operating performance and the Company’s ability to meet its financial obligations. The EBITDA presented may not be comparable to similarly titled measures of other companies. |