1 st Quarter 2011 Earnings Conference April 11, 2011 Exhibit 99.2 |

Alcoa Logo Cautionary Statement 2 |

Chuck McLane Executive Vice President and Chief Financial Officer |

Alcoa Logo 1 st Quarter 2011 Financial Overview Income from Continuing Operations of $309 million, or $0.27 per share; Restructuring and other special items totaled an unfavorable $8 million, or $0.01 per share Revenue up 22% versus first quarter 2010 and 5% sequentially Adjusted EBITDA of $955 million, up 22% from the fourth quarter 2010 and up 60% from first quarter 2010 Alumina: $71 Adjusted EBITDA/metric ton, 8% better than ten-year average of $66/mt Primary Metals: $438 Adjusted EBITDA/metric ton, 12% better than ten-year average of $390/mt Flat-Rolled Products: $173 million Adjusted EBITDA was record first quarter result Engineered Products: 18.4% Adjusted EBITDA margin was record result Days Working Capital two days lower than first quarter 2010 Debt to Capital of 33.6%, 130 basis points lower sequentially Completed acquisition of aerospace fastener business 4 See appendix for Adjusted EBITDA reconciliations |

Alcoa Logo Income Statement Summary $ Millions 1Q’10 4Q’10 1Q’11 Year Change Sequential Change Sales $4,887 $5,652 $5,958 $1,071 $306 Cost of Goods Sold $4,013 $4,538 $4,715 $702 $177 COGS % Sales 82.1% 80.3% 79.1% (3.0 % pts.) (1.2 % pts.) Selling, General Administrative, Other $239 $282 $245 $6 ($37) SGA % Sales 4.9% 5.0% 4.1% (0.8 % pts.) (0.9 % pts.) Restructuring and Other Charges $187 ($12) $6 ($181) $18 Effective Tax Rate -95.5% 16.1% 27.4% 122.9 % pts. 11.3 % pts. Income from Continuing Operations ($194) $258 $309 $503 $51 Income Per Diluted Share ($0.19) $0.24 $0.27 $0.46 $0.03 5 See appendix for Adjusted Income reconciliation |

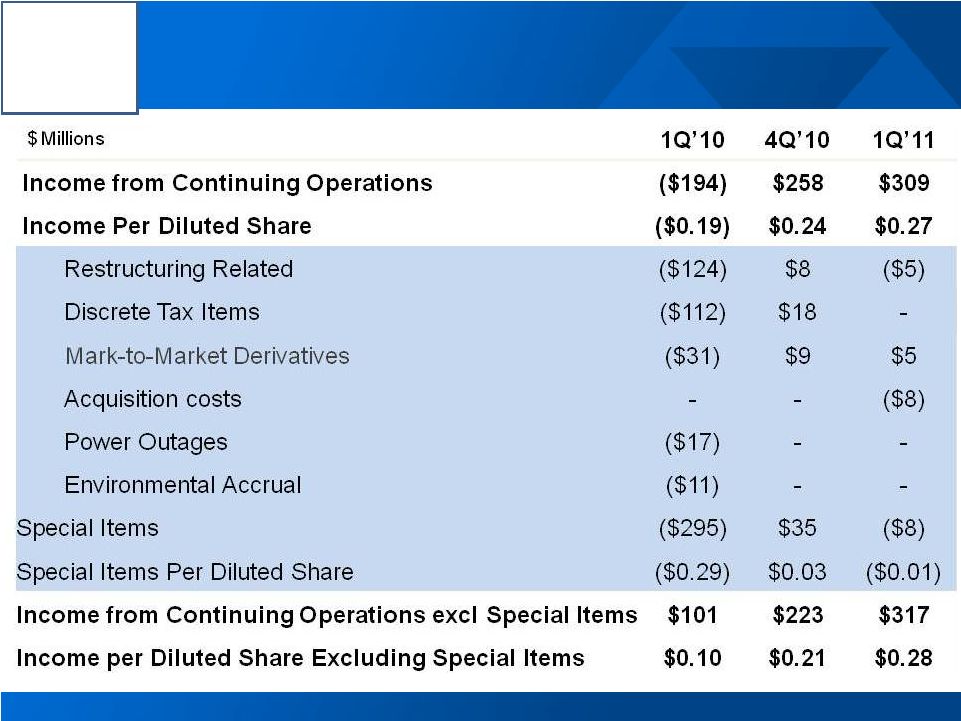

Alcoa Logo Restructuring and Other Special Items 6 See appendix for Adjusted Income reconciliation |

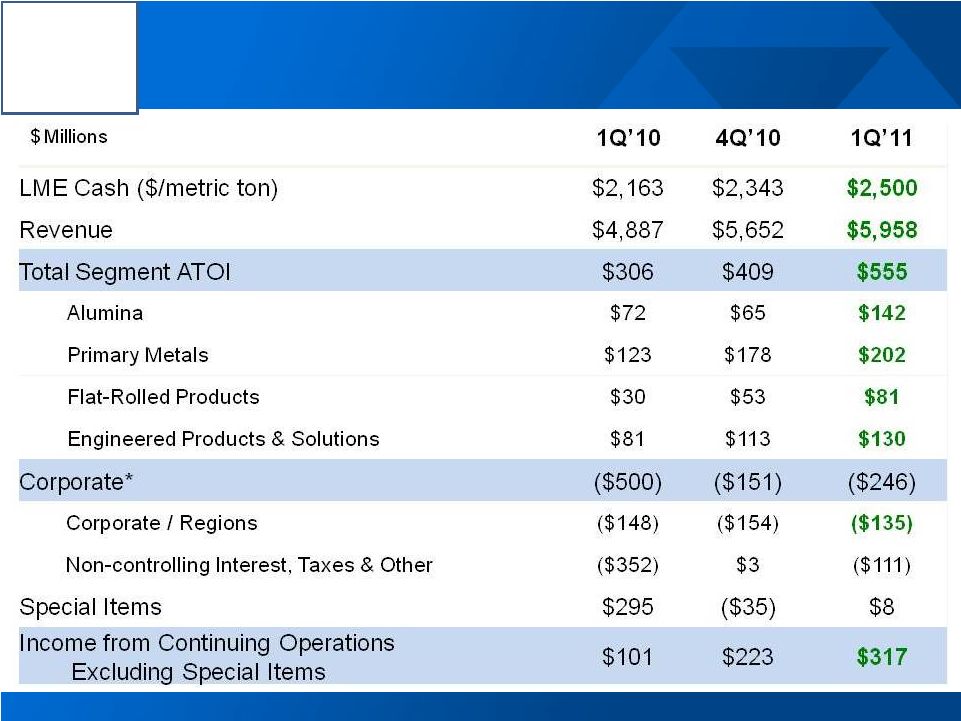

Alcoa Logo Sequential and Prior Year Improvements in All Segments 7 * These amounts represent the sum of all reconciling items (excluding discontinued operations) within the Reconciliation of ATOI included in the appendix |

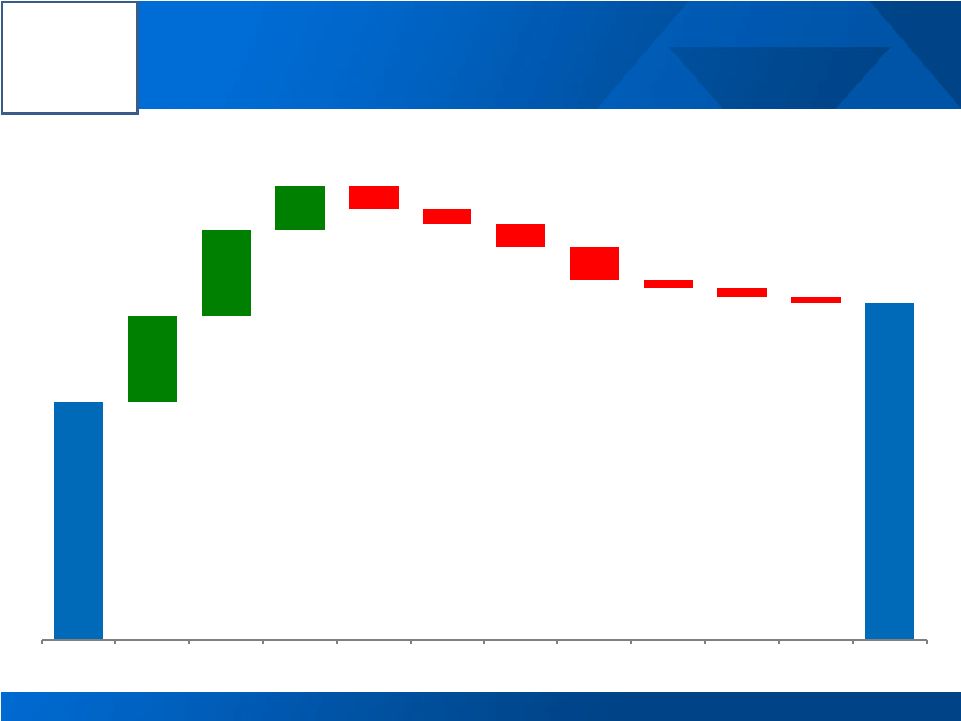

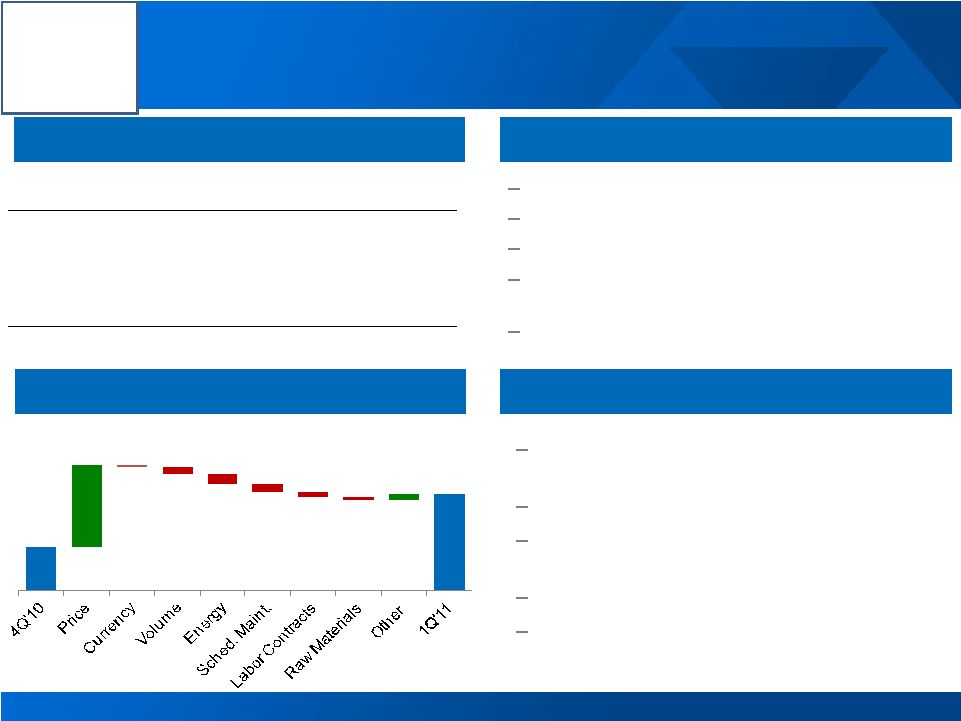

Alcoa Logo 1 st Quarter 2011 vs. 4 th Quarter 2010 Earnings Bridge Income from Continuing Operations excluding Restructuring & Other Special Items ($ millions) 8 See appendix for reconciliation $223 $81 $81 $41 ($21) ($14) ($22) ($31) ($7) ($9) ($5) $317 4Q10 LME Price/ Mix Productivity Energy Currency Raw Materials Taxes Alumina Mtce Restarts Other 1Q11 |

Alcoa Logo 1Q 10 4Q 10 1Q 11 Production (kmt) 3,866 4,119 4,024 3 rd Party Shipments (kmt) 2,126 2,433 2,206 3 rd Party Revenue ($ Millions) 638 759 810 ATOI ($ Millions) 72 65 142 Alumina 1 st Quarter Highlights 2 nd Quarter Outlook 1 st Quarter Business Conditions 9 Realized third-party alumina price up 15% Higher natural gas, fuel oil, and caustic prices Higher scheduled maintenance of $12 million Achieved $71 Adjusted EBITDA/tonne, better than ten-year average of $66 Impact of labor contract settlement in Australia of $7 million 20% of 3 rd party shipments on spot or prior- month indexed basis Other pricing to follow two-month lag on LME Maintenance costs continue in Australia with similar cost to Q1 Production projected to increase 125 kmt Higher energy and caustic costs to persist 1 st Quarter Performance Bridge $ Millions See appendix for Adjusted EBITDA reconciliation $65 $142 $120 ($3) ($10) ($15) ($12) ($7) ($5) $9 |

Alcoa Logo 1Q 10 4Q 10 1Q 11 Production (kmt) 889 913 904 3 rd Party Shipments (kmt) 695 743 698 3 rd Party Revenue ($ Millions) 1,702 1,970 1,980 3 rd Party Price ($/MT) 2,331 2,512 2,682 ATOI ($ Millions) 123 178 202 Primary Metals 1 st Quarter Highlights 1 st Quarter Business Conditions 2 nd Quarter Outlook 10 Realized pricing up 7% sequentially Achieved $438 Adjusted EBITDA/tonne, better than ten-year average of $390 Productivity benefits continue Restarts at US locations with cost of $9m Higher energy and energy-derivative costs Increasing cost of other raw materials Pricing to follow 15-day lag to LME US restarts will turn profitable, with no further cost expected 50 kmt higher production with restarts Higher energy and raw materials costs to persist 1 st Quarter Performance Bridge $ Millions ($13) See appendix for Adjusted EBITDA reconciliation $178 ($5) $202 $66 ($4) $9 ($20) ($9) |

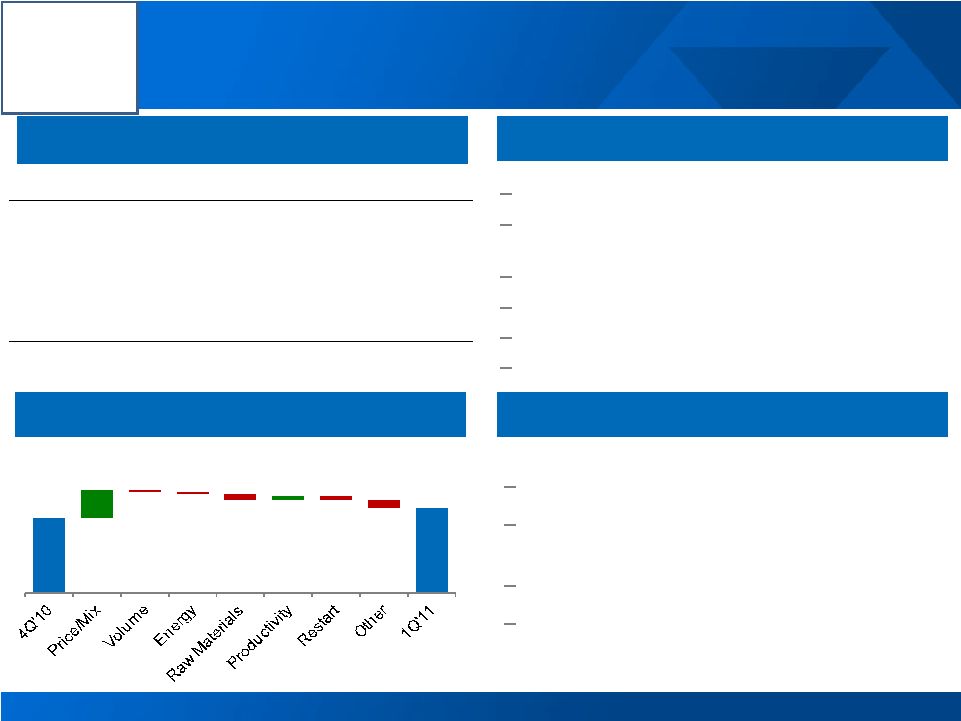

Alcoa Logo $29 $17 ($2) ($2) ($7) ($7) $53 $81 11 2 nd Quarter Outlook 1 st Quarter Business Conditions 1 st Quarter Highlights ATOI $ Millions 1Q 10 4Q 10 1Q 11 Flat-Rolled Products, excl Russia, China & Other 47 55 84 Russia, China & Other (17) (2) (3) Total ATOI 30 53 81 32% revenue growth from Q1 2010 Record 1 st Quarter ATOI and Adjusted EBITDA performance Strengthened demand in most end markets, and Improved pricing and mix Increased cost pressures Seasonal demand increases Improving productivity Cost pressures to continue Improvement in Russia and China as shipments increase 1 st Quarter Performance Bridge $ Millions Flat-Rolled Products 17% increase from 2010 241% increase from 2008 Adjusted EBITDA/mt 11 See appendix for Adjusted EBITDA reconciliation |

Alcoa Logo $ Millions 1Q 10 4Q 10 1Q 11 3 rd Party Revenue 1,074 1,215 1,247 ATOI 81 113 130 Adjusted EBITDA Margin 14% 17% 18% Engineered Products and Solutions 12 1 st Quarter Performance Bridge $ Millions 1 st Quarter Business Conditions 1 st Quarter Highlights 2 nd Quarter Outlook Building and construction market with continued weakness Markets showing incremental improvements in line with end market forecasts Increasing market share in several core businesses Product innovations continue to support aggressive 2011 and 2013 revenue targets Productivity improvements to continue See appendix for Adjusted EBITDA reconciliation $113 ($2) $11 $11 ($3) $130 |

Alcoa Logo 1 st Quarter 2011 Cash Flow Overview 13 See appendix for Free Cash Flow reconciliation 1Q’11 FCF ($0.4) billion $0.9 billion of cash Debt-to-Cap in target range at 33.6% DWC better by two Days from Q1 2010 ($ Millions) 1Q'10 4Q'10 1Q'11 Net Income ($179) $292 $366 DD&A 358 371 361 Change in Working Capital (336) 564 (646) Pension Contributions (22) (43) (31) Taxes / Other Adjustments 378 186 ($286) Cash From Operations $199 $1,370 ($236) Dividends to Shareholders (32) (31) (33) Change in Debt (42) (113) 101 Distributions to Noncontrolling Interest (72) (102) (97) Contributions from Noncontrolling Interest 27 41 121 Other Financing Activities (61) 4 33 Cash From Financing Activities ($180) ($201) $125 Capital Expenditures (221) (365) (204) Other Investing Activities 13 (109) (348) Cash From Investing Activities ($208) ($474) ($552) |

Alcoa Logo Sustainable Reductions in Days Working Capital 14 1Q 2009 1Q 2010 1Q 2011 Sustained historically low days working capital performance 1Q 2009 1Q 2010 1Q 2011 1Q 2009 1Q 2010 1Q 2011 1Q 2009 1Q 2010 1Q 2011 See appendix for Free Cash Flow reconciliation 67 71 81 54 38 47 69 40 33 46 70 38 GPP GRP EPS Alcoa |

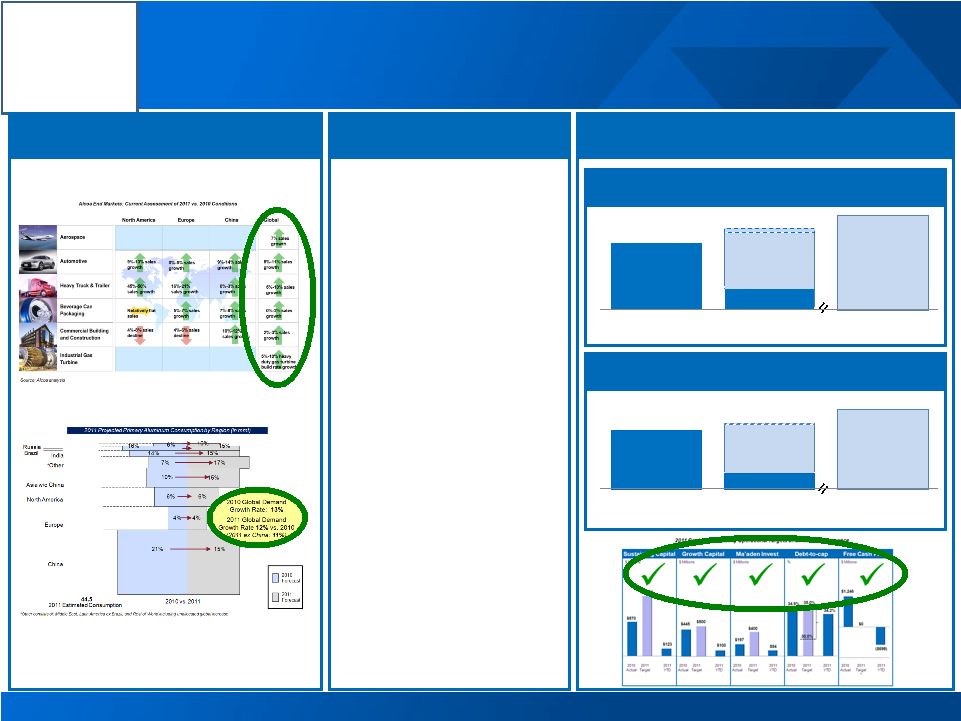

Alcoa Logo 2011 Cash Sustainability Operational Targets and Actual Performance 15 Sustaining Capital Growth Capital Ma’aden Invest $400 Debt-to-cap $ Millions $197 $ Millions $ Millions % 2010 Actual 2011 Target 2011 YTD $85 35.0% 34.9% 2010 Actual 2011 Target 2011 YTD 33.6% $500 $445 2010 Actual 2011 Target 2011 YTD $85 $1,000 $570 2010 Actual 2011 Target 2011 YTD $119 Free Cash Flow $ Millions $0 $1,246 ($440) 2010 Actual 2011 Target * 2011 YTD 30.0% •Target is to be free cash flow positive. See appendix for Free Cash Flow reconciliation We Are Focused on Achieving Our 2011 Goals |

Alcoa Logo A 16 |

Klaus Kleinfeld Chairman and Chief Executive Officer 17 |

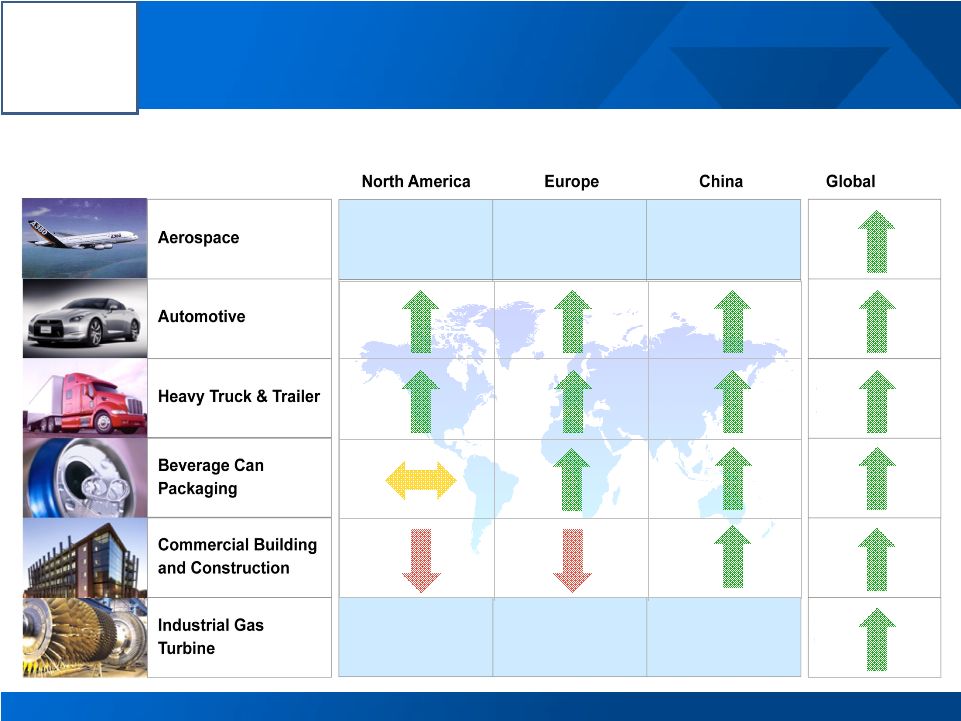

Alcoa Logo Market Conditions in 2011 Continue to Strengthen 18 Alcoa End Markets: Current Assessment of 2011 vs. 2010 Conditions Source: Alcoa analysis 9%-13% sales growth 0%-5% sales growth 9%-14% sales growth 5%-11% sales growth 45%-50% sales growth 16%-21% sales growth 0%-3% sales growth 5%-10% sales growth Relatively flat sales 5%-7% sales growth 7%-8% sales growth 0%-2% sales growth 10%-12% sales growth 2%-3% sales growth 4%-8% sales decline 4%-6% sales decline 5%-10% heavy duty gas turbine build rate growth 7% sales growth |

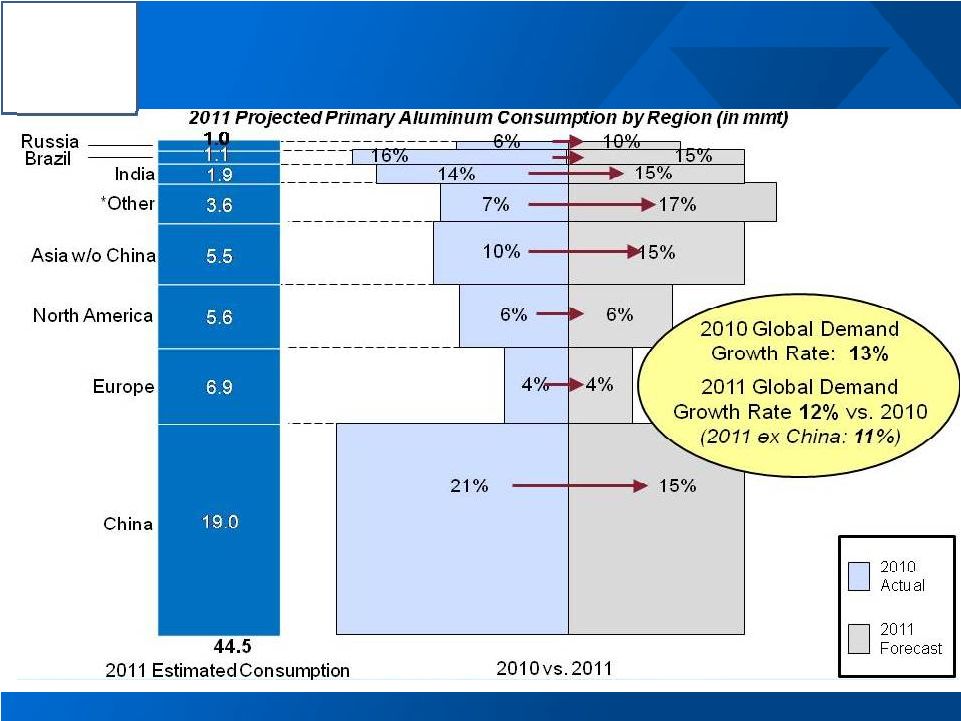

Alcoa Logo 19 *Other consists of: Middle East, Latin America ex Brazil, and Rest of World including unallocated global increase End Market Developments Support Strong Demand Growth |

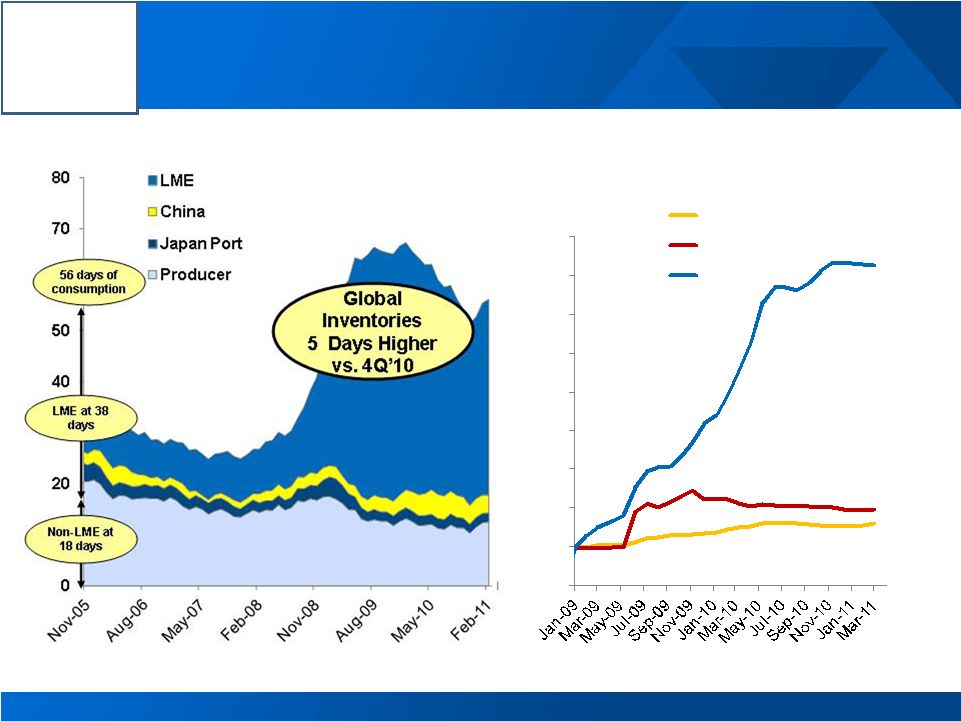

Alcoa Logo Inventories Increase, but Premiums Attest Physical Tightness 20 Regional Premiums Near All-Time Highs Global Inventories Increase in Q1 2011 $114 / MT $204 / MT $145 / MT Source: Alcoa estimates, LME, SHFE, IAI, Marubeni, Platt’s Metals Week and Metal Bulletin 0% 100% 200% 300% 400% 500% 600% 700% 800% 900% Midwest Japan Europe |

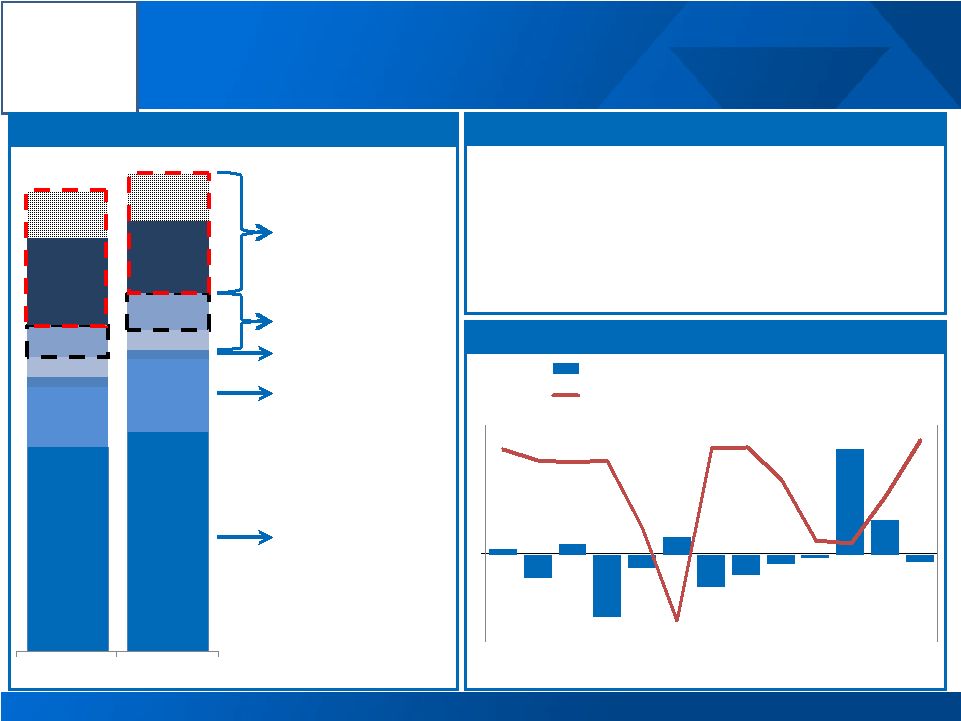

Alcoa Logo 4.3 4.6 1.2 1.5 0.2 0.2 0.4 0.4 0.7 0.8 1.8 1.5 1.0 1.0 Q4 2010 Q1 2011 Inventory: Driven by End Markets and Financing Structure 21 Off-warrant estimate range (1.5 to 2.5mmt) China Visible Japan Port Producer-held LME on-warrant Total Global Inventories (mmt) Source: Alcoa analysis Mar-10 May-10 Jul-10 Sep-10 Nov-10 Jan-11 •Improving end-market demand drives work-in- process and distribution inventories •Four additional reporting smelters in the Middle East & India Growing demand in All Regions Competing Financing Deals 13 (53) 26 (145) (32) 42 (75) (46) (21) (8) 248 82 (16) $31 $30 $29 $30 $19 $3 $32 $32 $26 $16 $16 $24 $33 $0 $5 $10 $15 $20 $25 $30 $35 (200) (150) (100) (50) 0 50 100 150 200 250 300 LME Stock Change (kmt) Contango (cash to 3 months) ($/mt) |

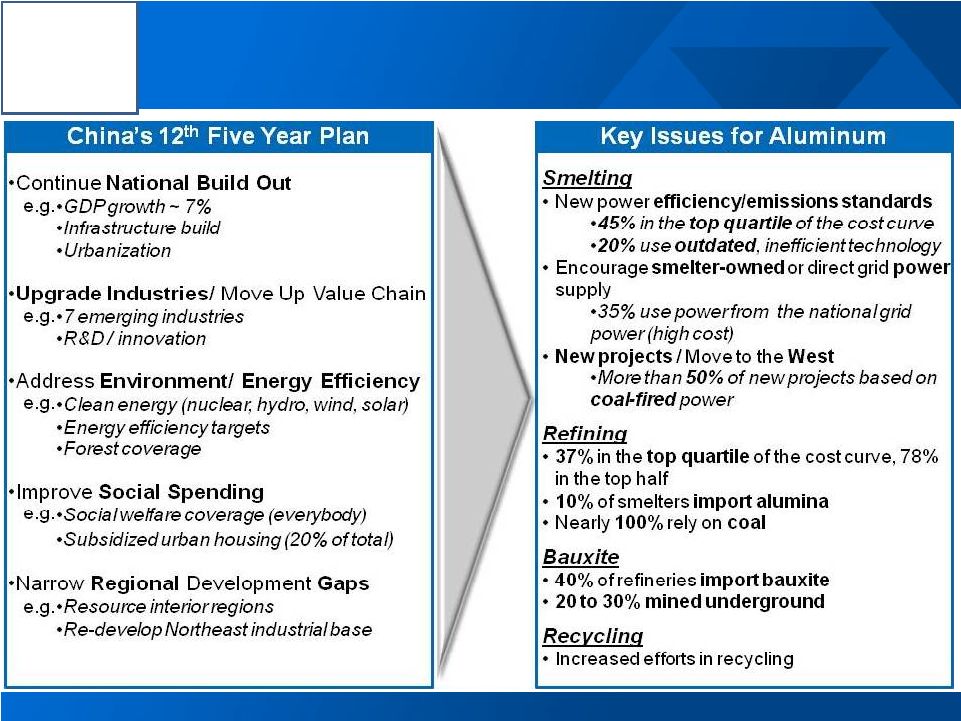

Alcoa Logo 12 th Five Year Plan Accelerates Change in Aluminum Industry 22 |

Alcoa Logo Western World Annualized Production (Feb 2011) 25,385 Restarts and Expanded Capacity 1,100 Total Supply 26,485 Western World Consumption (25,540) (Deficit) Surplus 945 China Annualized Production (Feb 2011) 15,865 Restarted and Expanded Capacity 2,410 Total Supply 18,275 Consumption (18,975) (Deficit) Surplus (700) 2011 Primary Aluminum Balances Unchanged 23 China Western World Production Demand Surplus Source: Alcoa estimates, Brook Hunt, CRU, CNIA, IAI Deficit Production Demand 2011E Aluminum Supply / Demand Balance (in kmt) |

Alcoa Logo 2011 Global Alumina Balance Unchanged 24 Source: Alcoa estimates, Brook Hunt, CRU, CNIA, IAI China Western World 2011 Annualized Production 31,500 Imports from Western World 3,500 Supply 35,000 Demand (35,000) (Deficit) / Surplus 0 2011 Annualized Production 55,900 Exports to China (3,500) Supply 52,400 Demand (52,400) (Deficit) / Surplus 0 Production Demand Balanced 2011E Alumina Supply / Demand Balance (in kmt) |

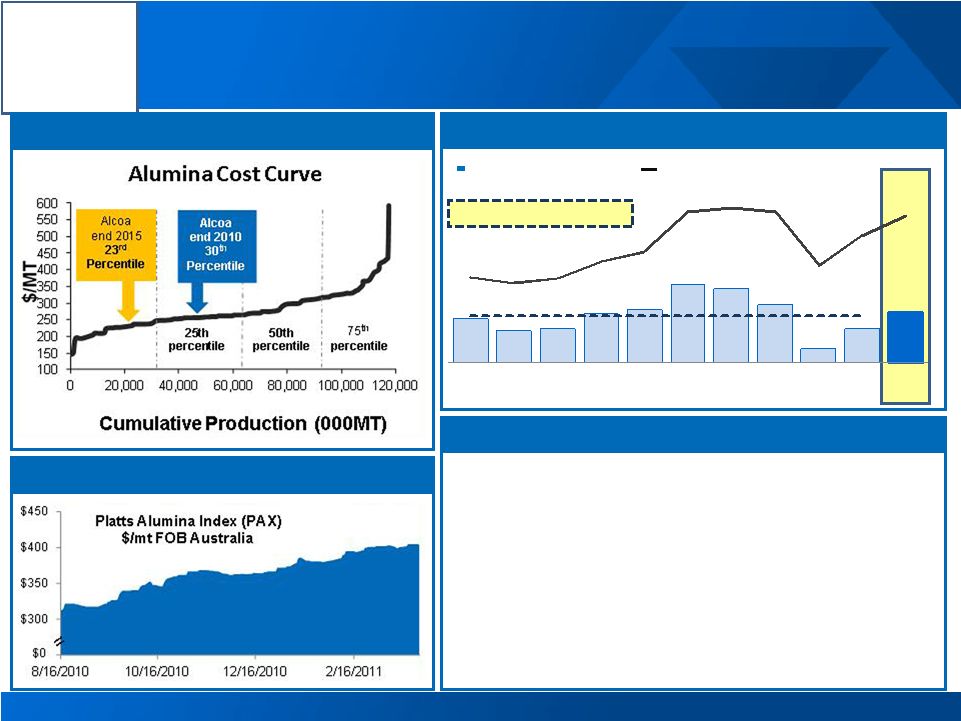

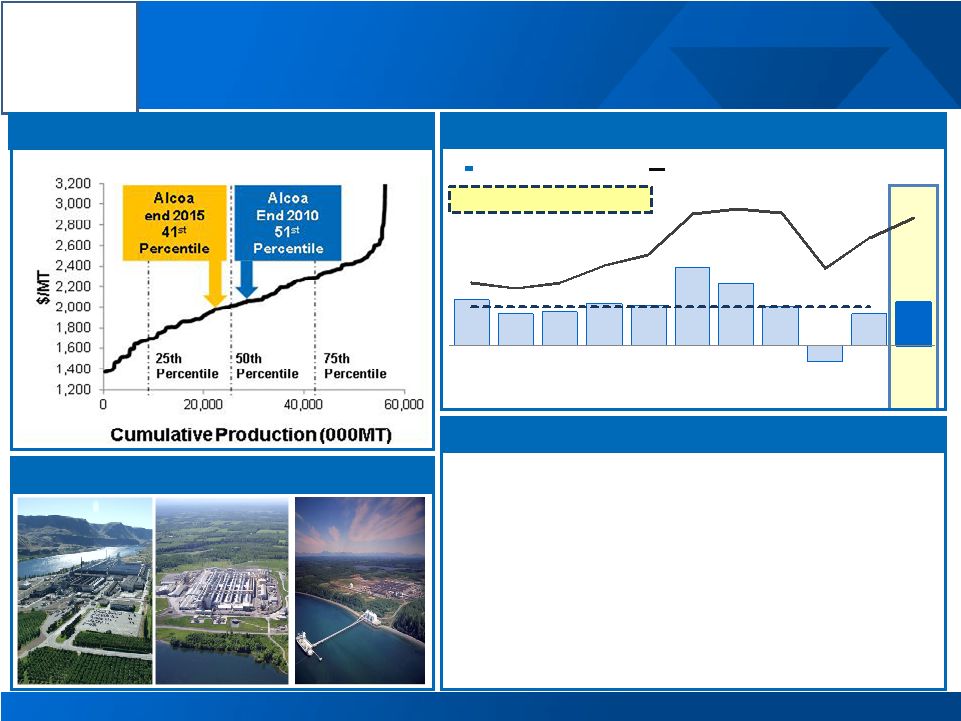

Alcoa Logo Alumina: Strong Performance and Strengthening Pricing 25 2015 Cost Curve Targets Source: CRU; Platt’s Index Adjusted EBITDA per Metric Ton – Sao Luis and Juruti continue to break production records – Volume increases at Suriname and Point Comfort will provide additional exposure to rising spot prices – Ma’aden, lowest cost refinery online in 2014 – 20% of our customers now priced on an alumina- indexed or spot basis Global Capacity: 18,100 kmt per year 10 Yr Average ~ $66/MT LME Adjusted EBITDA/MT Strengthening Alumina Index Prices See appendix for Adjusted EBITDA reconciliations 62 44 48 68 75 110 104 81 20 47 71 1,447 1,350 1,433 1,719 1,900 2,570 2,641 2,572 1,664 2,173 2,500 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 YTD |

Alcoa Logo 2015 Cost Curve Targets Aluminum: Continued Strength but Looking to the Future 26 Source: CRU Aluminum Cost Curve – Driving down the cost curve – US restarts on-track, increasing US-based production and capturing full LME increase – Ma’aden, lowest cost smelter online in 2013 – Sustainable cost reductions – Repowered asset base – Capturing optimal value from global casthouses Global Capacity: 4,500 kmt Adjusted EBITDA per Metric Ton LME Adjusted EBITDA/MT US Production Captures LME Increase See appendix for Adjusted EBITDA reconciliations 460 321 336 418 398 784 626 392 (159) 320 438 1,447 1,350 1,433 1,719 1,900 2,570 2,641 2,572 1,664 2,173 2,500 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 YTD 10 YR Average ~ $390/MT |

Alcoa Logo 27 Ma’aden Project is progressing very well Potline #1 Electrical Switch Building Cathode Sealing Plant Paste Plant Port Rail |

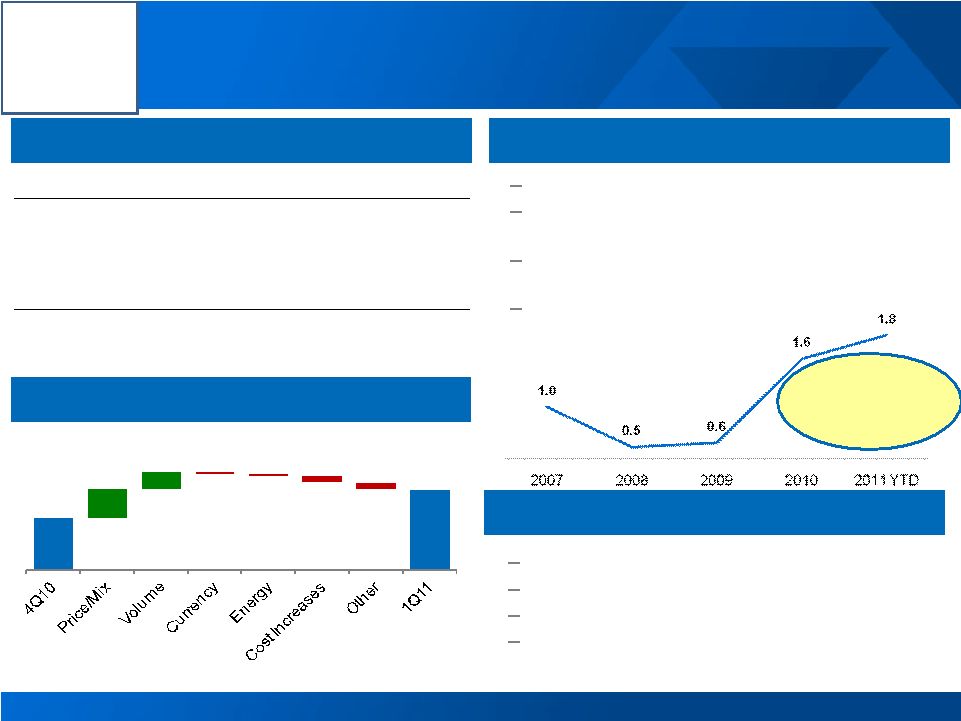

Alcoa Logo Distribution 15% Automotive 7% B&C 6% Commercial Transport 5% Industrial /Other 12% Packaging 44% Aerospace 11% Rolled Products: Strong Start to Targeted Revenues & Margin Adjusted EBITDA & Adjusted EBITDA Margin 28 541 495 479 531 620 536 498 254 224 551 173 Adjusted EBITDA $Millions Adjusted EBITDA % Sales 2011 YTD 3 rd Party Sales by Market 80% Utilization – 32% revenue growth from Q1 2010 – 2011 potential of at least 35 to 50% of $2.5b 2013 revenue growth target – Aerospace growth: robust build rates – Russia and China to capture growth in emerging markets – Ma’aden, lowest cost rolling mill in 2013 Leveraging our strategic asset base Strong Growth in Adjusted EBITDA per Tonne 240% increase from 2008 See appendix for Adjusted EBITDA reconciliations 11% 11% 10% 9% 9% 6% 5% 3% 4% 9% 9% 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 YTD 1.0 0.5 0.6 1.6 1.8 2007 2008 2009 2010 2011 YTD |

Alcoa Logo Russia Profitable Since Q2 2010 Solid Growth in all segments, especially can stock 60% volume growth from Q1 2010 Improving mix of products and customers drives higher realized conversion revenue Focus on increasing aluminum consumption and recycling in Russia 29 Solid Progress on GRP Growth Projects in Russia and China China Ramping Up by 2012 End & Tab Line, Samara Capacity utilization targeted to reach 100% by 2012 Key domestic supplier of lithographic sheet, brazing material and can sheet and supplier for consumer electronics 90% volume growth versus Q1 2010 Bohai ramp-up continues Bohai Flat Rolled Products |

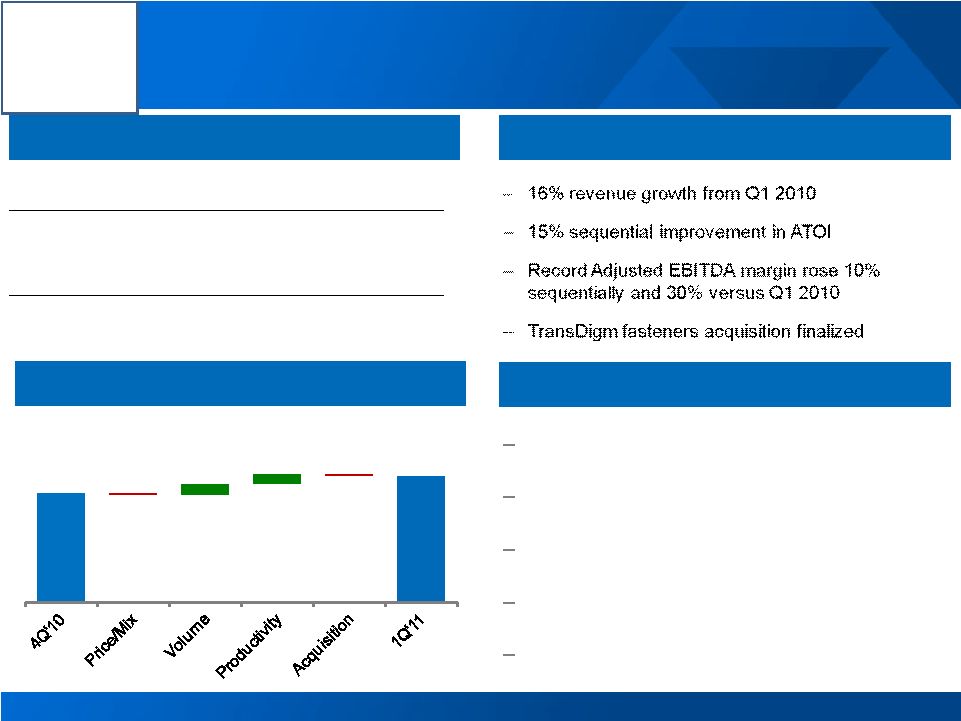

Alcoa Logo Aerospace 48% IGT 10% B&C 18% Commercial Transport 15% Automotive 3% Other 6% Engineered Products: Record Margins and Focus on Growth Adjusted EBITDA & Adjusted EBITDA Margin 30 436 287 356 495 536 676 783 922 630 762 229 Adjusted EBITDA $Millions Adjusted EBITDA % Sales 2011 YTD 3 rd Party Sales by Market 76% Utilization 67% Utilization Strong Platform for Profitable Growth – 16% revenue growth from Q1 2010 – 2011 potential of 25 to 30% of $1.6b 2013 revenue growth target – TransDigm fastener acquisition integration on track with accretive earnings in 2011 – Product innovations and share gains accelerate growth Continued Innovation in All of our Businesses Building & Construction Forgings & Extrusions Fastening Systems Power & Propulsion Commercial Wheels See appendix for Adjusted EBITDA reconciliations 11% 8% 9% 12% 11% 12% 13% 15% 13% 17% 18% 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 YTD |

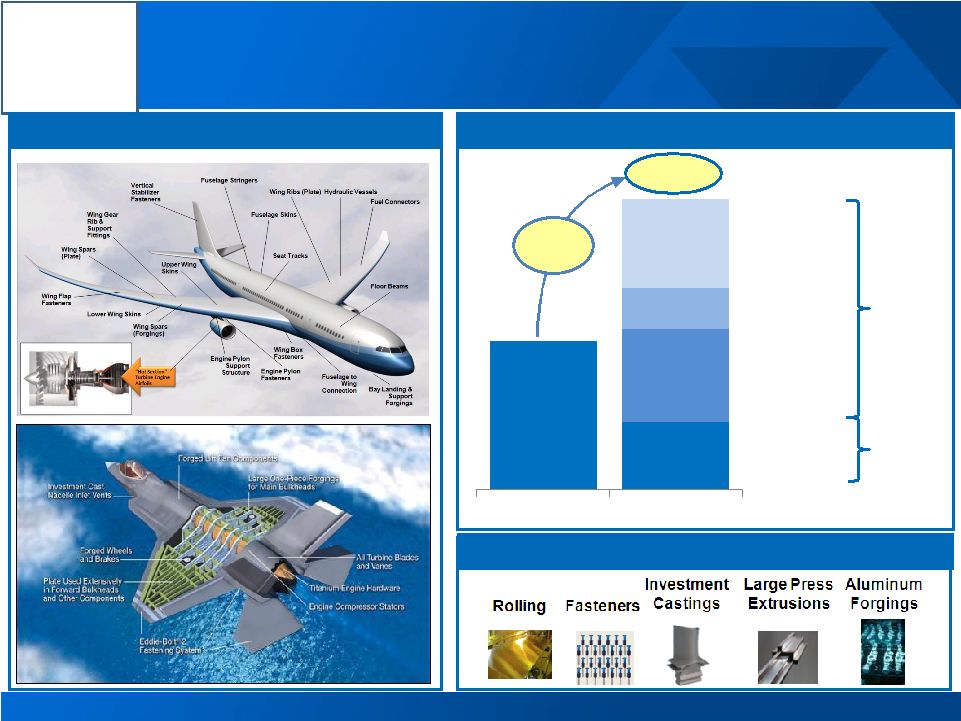

Alcoa Logo Alcoa Aerospace: A History of Growth and Innovation 31 Growth in Aerospace Revenue ($b) Deep Product Breadth $2.9 Alcoa Content: Tip to Tail – Wing to Wing 2X EPS Fastening Systems Forgings & Extrusions Power & Propulsion Rolled Products 1 Aerospace revenues are 48% of overall EPS; 2 Aerospace revenues are 11% of overall GRP GRP $1.5 $0.7 $0.9 $0.4 $0.9 2002 2010 1 2 |

Alcoa Logo Strong Start to 2011 is Just the Beginning Strengthening Markets Strong Performance 32 Meeting our Aggressive Targets EPS: $1.6b in Revenue Growth by 2013 ($b) GRP: $2.5b in Revenue Growth by 2013 ($b) Sales •22% revenue growth from Q1 2010 Alumina •$71 Adjusted EBITDA/mt, 8% better than ten-year average of $66/mt Primary Metals •$438 Adjusted EBITDA/mt, 12% better than ten-year average of $390/mt Flat-Rolled Products •$173 million Adjusted EBITDA was record first quarter result Engineered Products & Solutions •18% Adjusted EBITDA Margin was record result See appendix for Adjusted EBITDA reconciliations $6.3 $1.9 $8.8 $5.3 to $5.7 2010 2011 YTD 2013 Target $4.6 $1.2 $6.2 $3.8 to $3.9 2010 2011 YTD 2013 Target |

That's why … That's why … Alcoa can't wait Alcoa can't wait …for tomorrow …for tomorrow Alcoa Logo |

Alcoa Logo Roy Harvey Director, Investor Relations A 390 Park Avenue New York, NY 10022-4608 Telephone: (212) 836-2674 www.alcoa.com Additional Information 34 |

Alcoa Logo Annual Sensitivity Summary 35 Currency Annual Net Income Sensitivity +/- $0.01 versus USD Australian $ (USD to AUD) +/- $10 million Brazilian $ (BRL to USD) +/- $ 3 million Euro € (USD to EUR) +/- $ 2 million Canadian $ (CAD to USD) +/- $ 4 million +/- $100/MT = +/- $200 Million LME Aluminum Annual Net Income Sensitivity |

Alcoa Logo Revenue Change by Market 7% 30% 2% 12% 13% (12%) 14% (1%) 7% 1% 20% 5% 26% 37% (2%) 8% 45% 25% 27% 16% 1Q’11 Third Party Revenue Sequential Change Year-Over-Year Change 36 13% 3% 7% 5% 4% 2% 14% 5% 14% 33% Aerospace Automotive B&C Comm. Transport Industrial Products IGT Packaging Distribution/Other Alumina Primary Metals |

Alcoa Logo Reconciliation of ATOI to Consolidated Net (Loss) Income Attributable to Alcoa 37 (in millions) 1Q10 2Q10 3Q10 4Q10 2010 1Q11 Total segment ATOI $ 306 $ 381 $ 328 $ 409 $ 1,424 $ 555 Unallocated amounts (net of tax): Impact of LIFO (14) (3) (2) 3 (16) (24) Interest expense (77) (77) (91) (76) (321) (72) Noncontrolling interests (22) (34) (48) (34) (138) (58) Corporate expense (67) (59) (71) (94) (291) (67) Restructuring and other charges (122) (21) 1 8 (134) (6) Discontinued operations (7) (1) – – (8) (1) Other (198) (50) (56) 42 (262) (19) Consolidated net (loss) income attributable to Alcoa $ (201) $ 136 $ 61 $ 258 $ 254 $ 308 |

Alcoa Logo Reconciliation of Adjusted Income 38 (in millions, except per- share amounts) Income Diluted EPS Quarter ended March 31, 2010 December 31, 2010 March 31, 2011 March 31, 2010 December 31, 2010 March 31, 2011 Net (loss) income attributable to Alcoa $ (201) $ 258 $ 308 $ (0.20) $ 0.24 $ 0.27 Loss from discontinued operations (7) – (1) (Loss) income from continuing operations attributable to Alcoa (194) 258 309 (0.19) 0.24 0.27 Restructuring and other charges 119 (8) 5 Discrete tax items* 112 (18) – Other special items** 64 (9) 3 Income from continuing operations attributable to Alcoa – as adjusted $ 101 $ 223 $ 317 0.10 0.21 0.28 Income from continuing operations attributable to Alcoa – as adjusted is a non-GAAP financial measure. Management believes that this measure is meaningful to investors because management reviews the operating results of Alcoa excluding the impacts of restructuring and other charges, discrete tax items, and other special items. There can be no assurances that additional restructuring and other charges, discrete tax items, and other special items will not occur in future periods. To compensate for this limitation, management believes that it is appropriate to consider both Income from continuing operations attributable to Alcoa determined under GAAP as well as Income from continuing operations attributable to Alcoa – as adjusted. * Discrete tax items include the following: for the quarter ended December 31, 2010, a benefit for the reversal of the remaining valuation allowance related to net operating losses of an international subsidiary ($16) (a portion was initially reversed in the quarter ended September 30, 2010) and a net benefit for other small items ($2); and for the quarter ended March 31, 2010, charges for a change in the tax treatment of federal subsidies received related to prescription drug benefits provided under certain retiree health benefit plans ($79), unbenefitted losses in Russia, China, and Italy ($22), interest due to the IRS related to a previously deferred gain associated with the 2007 formation of the former soft alloy extrusions joint venture ($6), and a change in the anticipated sale structure of the Transportation Products Europe business ($5). ** Other special items include the following: for the quarter ended March 31, 2011, costs related to acquisitions of the aerospace fastener business of TransDigm Group Inc. and full ownership of carbothermic smelting technology from ORKLA ASA ($8) and favorable mark-to-market changes in certain power derivative contracts ($5); for the quarter ended December 31, 2010, favorable mark-to-market changes in certain power derivative contracts; and for the quarter ended March 31, 2010, charges related to unfavorable mark-to-market changes in certain power derivative contracts ($31), power outages at the Rockdale, TX and São Luís, Brazil facilities ($17), an additional environmental accrual for the Grasse River remediation in Massena, NY ($11), and the write off of inventory related to the permanent closures of certain U.S. facilities ($5). |

Alcoa Logo Reconciliation of Free Cash Flow 39 (in millions) Quarter ended Year ended March 31, 2011 December 31, 2010 Cash provided from operations $ (236) $ 2,261 Capital expenditures (204) (1,015) Free cash flow $ (440) $ 1,246 Free Cash Flow is a non-GAAP financial measure. Management believes that this measure is meaningful to investors because management reviews cash flows generated from operations after taking into consideration capital expenditures due to the fact that these expenditures are considered necessary to maintain and expand Alcoa’s asset base and are expected to generate future cash flows from operations. It is important to note that Free Cash Flow does not represent the residual cash flow available for discretionary expenditures since other non- discretionary expenditures, such as mandatory debt service requirements, are not deducted from the measure. |

Alcoa Logo Reconciliation of Alcoa Adjusted EBITDA 40 ($ in millions) 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 1Q10 4Q10 1Q11 Net income (loss) attributable to Alcoa $ 908 $ 420 $ 938 $ 1,310 $ 1,233 $ 2,248 $ 2,564 $ (74) $ (1,151) $ 254 $ (201) $ 258 $ 308 Add: Net income attributable to noncontrolling interests 205 181 212 233 259 436 365 221 61 138 22 34 58 Cumulative effect of accounting changes – (34) 47 – 2 – – – – – – – – Loss (income) from discontinued operations 5 101 – 27 50 (22) 250 303 166 8 7 – 1 Provision (benefit) for income taxes 524 307 367 546 464 853 1,623 342 (574) 148 84 56 138 Other (income) expenses, net (295) (175) (278) (266) (478) (236) (1,920) (59) (161) 5 21 (43) (28) Interest expense 371 350 314 271 339 384 401 407 470 494 118 118 111 Restructuring and other charges 530 398 (28) (29) 266 507 268 939 237 207 187 (12) 6 Provision for depreciation, depletion, and amortization 1,144 1,037 1,110 1,142 1,227 1,252 1,244 1,234 1,311 1,450 358 371 361 Adjusted EBITDA $ 3,392 $ 2,585 $ 2,682 $ 3,234 $ 3,362 $ 5,422 $ 4,795 $ 3,313 $ 359 $ 2,704 $ 596 $ 782 $ 955 Sales $19,906 $17,691 $18,879 $21,370 $24,149 $28,950 $29,280 $26,901 $18,439 $21,013 $ 4,887 $ 5,652 $ 5,958 Adjusted EBITDA Margin 17% 15% 14% 15% 14% 19% 16% 12% 2% 13% 12% 14% 16% Alcoa’s definition of Adjusted EBITDA (Earnings before interest, taxes, depreciation, and amortization) is net margin plus an add-back for depreciation, depletion, and amortization. Net margin is equivalent to Sales minus the following items: Cost of goods sold; Selling, general administrative, and other expenses; Research and development expenses; and Provision for depreciation, depletion, and amortization. Adjusted EBITDA is a non-GAAP financial measure. Management believes that this measure is meaningful to investors because Adjusted EBITDA provides additional information with respect to Alcoa’s operating performance and the Company’s ability to meet its financial obligations. The Adjusted EBITDA presented may not be comparable to similarly titled measures of other companies. |

Alcoa Logo Reconciliation of Alumina Adjusted EBITDA 41 ($ in millions, except per metric ton amounts) 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 4Q10 1Q11 After-tax operating income (ATOI) $ 471 $ 315 $ 415 $ 632 $ 682 $ 1,050 $ 956 $ 727 $ 112 $ 301 $ 65 $ 142 Add: Depreciation, depletion, and amortization 144 139 147 153 172 192 267 268 292 406 107 103 Equity (income) loss (1) (1) – (1) – 2 (1) (7) (8) (10) (3) (3) Income taxes 184 130 161 240 246 428 340 277 (22) 60 14 44 Other (17) (14) (55) (46) (8) (6) 2 (26) (92) (5) (3) – Adjusted EBITDA $ 781 $ 569 $ 668 $ 978 $ 1,092 $ 1,666 $ 1,564 $ 1,239 $ 282 $ 752 $ 180 $ 286 Production (thousand metric tons) (kmt) 12,527 13,027 13,841 14,343 14,598 15,128 15,084 15,256 14,265 15,922 4,119 4,024 Adjusted EBITDA/Production ($ per metric ton) $ 62 $ 44 $ 48 $ 68 $ 75 $ 110 $ 104 $ 81 $ 20 $ 47 $ 44 $ 71 Alcoa’s definition of Adjusted EBITDA (Earnings before interest, taxes, depreciation, and amortization) is net margin plus an add-back for depreciation, depletion, and amortization. Net margin is equivalent to Sales minus the following items: Cost of goods sold; Selling, general administrative, and other expenses; Research and development expenses; and Provision for depreciation, depletion, and amortization. The Other line in the table above includes gains/losses on asset sales and other nonoperating items. Adjusted EBITDA is a non-GAAP financial measure. Management believes that this measure is meaningful to investors because Adjusted EBITDA provides additional information with respect to Alcoa’s operating performance and the Company’s ability to meet its financial obligations. The Adjusted EBITDA presented may not be comparable to similarly titled measures of other companies. |

Alcoa Logo Reconciliation of Primary Metals Adjusted EBITDA 42 ($ in millions, except per metric ton amounts) 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 1Q11 After-tax operating income (ATOI) $ 905 $ 650 $ 657 $ 808 $ 822 $ 1,760 $ 1,445 $ 931 $ (612) $ 488 $ 202 Add: Depreciation, depletion, and amortization 327 300 310 326 368 395 410 503 560 571 141 Equity (income) loss (52) (44) (55) (58) 12 (82) (57) (2) 26 (1) (1) Income taxes 434 266 256 314 307 726 542 172 (365) 96 53 Other (8) (47) 12 20 (96) (13) (27) (32) (176) (7) 1 Adjusted EBITDA $ 1,606 $ 1,125 $ 1,180 $ 1,410 $ 1,413 $ 2,786 $ 2,313 $ 1,572 $ (567) $ 1,147 $ 396 Production (thousand metric tons) (kmt) 3,488 3,500 3,508 3,376 3,554 3,552 3,693 4,007 3,564 3,586 904 Adjusted EBITDA/Production ($ per metric ton) $ 460 $ 321 $ 336 $ 418 $ 398 $ 784 $ 626 $ 392 $ (159) $ 320 $ 438 Alcoa’s definition of Adjusted EBITDA (Earnings before interest, taxes, depreciation, and amortization) is net margin plus an add-back for depreciation, depletion, and amortization. Net margin is equivalent to Sales minus the following items: Cost of goods sold; Selling, general administrative, and other expenses; Research and development expenses; and Provision for depreciation, depletion, and amortization. The Other line in the table above includes gains/losses on asset sales and other nonoperating items. Adjusted EBITDA is a non-GAAP financial measure. Management believes that this measure is meaningful to investors because Adjusted EBITDA provides additional information with respect to Alcoa’s operating performance and the Company’s ability to meet its financial obligations. The Adjusted EBITDA presented may not be comparable to similarly titled measures of other companies. |

Alcoa Logo Reconciliation of Flat-Rolled Products Adjusted EBITDA 43 ($ in millions, except per metric ton amounts) 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 1Q11 After-tax operating income (ATOI) $ 253 $ 225 $ 222 $ 254 $ 278 $ 233 $ 178 $ (3) $ (49) $ 220 $ 81 Add: Depreciation, depletion, and amortization 167 184 190 200 220 223 227 216 227 238 58 Equity loss 2 4 1 1 – 2 – – – – – Income taxes 124 90 71 75 121 58 92 35 48 92 33 Other (5) (8) (5) 1 1 20 1 6 (2) 1 1 Adjusted EBITDA $ 541 $ 495 $ 479 $ 531 $ 620 $ 536 $ 498 $ 254 $ 224 $ 551 $ 173 Total sales $ 4,868 $ 4,571 $ 4,768 $ 6,042 $ 7,081 $ 8,610 $ 9,597 $ 9,184 $ 6,182 $ 6,457 $ 1,961 Adjusted EBITDA Margin 11% 11% 10% 9% 9% 6% 5% 3% 4% 9% 9% Total shipments (thousand metric tons) (kmt) 2,482 2,361 1,888 1,755 470 Adjusted EBITDA/Total shipments ($ per metric ton) $ 201 $ 108 $ 119 $ 314 $ 368 Alcoa’s definition of Adjusted EBITDA (Earnings before interest, taxes, depreciation, and amortization) is net margin plus an add-back for depreciation, depletion, and amortization. Net margin is equivalent to Sales minus the following items: Cost of goods sold; Selling, general administrative, and other expenses; Research and development expenses; and Provision for depreciation, depletion, and amortization. The Other line in the table above includes gains/losses on asset sales and other nonoperating items. Adjusted EBITDA is a non-GAAP financial measure. Management believes that this measure is meaningful to investors because Adjusted EBITDA provides additional information with respect to Alcoa’s operating performance and the Company’s ability to meet its financial obligations. The Adjusted EBITDA presented may not be comparable to similarly titled measures of other companies. |

Alcoa Logo Reconciliation of Engineered Products and Solutions Adjusted EBITDA 44 Alcoa’s definition of Adjusted EBITDA (Earnings before interest, taxes, depreciation, and amortization) is net margin plus an add-back for depreciation, depletion, and amortization. Net margin is equivalent to Sales minus the following items: Cost of goods sold; Selling, general administrative, and other expenses; Research and development expenses; and Provision for depreciation, depletion, and amortization. The Other line in the table above includes gains/losses on asset sales and other nonoperating items. Adjusted EBITDA is a non-GAAP financial measure. Management believes that this measure is meaningful to investors because Adjusted EBITDA provides additional information with respect to Alcoa’s operating performance and the Company’s ability to meet its financial obligations. The Adjusted EBITDA presented may not be comparable to similarly titled measures of other companies. |