Alcan+ Pechiney

Invest With Confidence

October 2003

©2003 ALCAN INC.

Alcan has filed a French prospectus (“note d’information”) with the FrenchCommission des opérations de bourse(“COB”) which has been registered under visa n° 03-858. A copy of thenote d’information may be obtained at no cost by contacting Morgan Stanley & Co. International Ltd. (25, rue Balzac - 75008 Paris, France), Lazard Frères (121, boulevard Hausmann – 75008 Paris), Société Générale (17, cours Valmy – 92972 Paris-La-Défense Cedex) and on the COB’s Internet web site at www.cob.fr.

This presentation and document are for information purposes only. They shall not and do not constitute either an offer to purchase or buy or a solicitation to purchase or buy or an offer to sell or exchange or a solicitation to sell or exchange any securities in any jurisdiction in which such offer or solicitation would be unlawful. You are urged to enquire as to the applicable local restrictions and to abide by them.

While the information contained in this presentation and document has been prepared in good faith, no representation or warranty, express or implied, is or will be made and no responsibility or liability is or will be accepted by Alcan or any of its subsidiaries or by any of their respective officers, employees or agents as to or in relation to the accuracy or completeness thereof and any such liability is expressly disclaimed (provided that the above does not exclude any liability for, or remedy in respect of, fraudulent misrepresentation).

This presentation may only be attended by, and this document may only be distributed to, persons who (i) are outside the United Kingdom, or (ii) have professional experience in matters relating to investments or (iii) are persons falling within article 49(2)(a) to (d) of The Financial Services and Markets Act 2000 (Financial Promotion) Order 2001 (all such persons together being referred to as "relevant persons"). This presentation and document must not be acted on or relied on by persons who are not relevant persons. Any investment or investment activity to which this presentation or document relate is available only to relevant persons and will be engaged in only with relevant persons.

Alcan will have no liability with respect to the violation of any of the restrictions contained in this disclaimer by any person or entity.

2

The French Commission des opérations de bourse draws the public’s attention on the two following points:

- Alcan Inc. is a Canadian company; an application for listing of its shares in France is made. On account of this specificity, applicable rules relating to information of the public and protection of investors as well as the company’s undertakings towards stock exchange authorities and the market, are described in the note d’information;

- Alcan Inc. will announce, before the opening in Paris of the fifth stock exchange trading day prior to the last day of the offer, the average value of the Alcan share, its decision to substitute, for Alcan shares -valued at the average value- an equivalent amount of cash as well as the exchange parity and the fraction paid in cash offered to shareholders of Pechiney as further described in section I.4.2 of the note d’information.

This document shall not be transmitted or distributed in the United States and in Canada.

FORWARD-LOOKING STATEMENTS

Certain statements made in this communication are forward-looking statements within the meaning of the United States Private Securities Litigation Reform Act of 1995. Although Alcan’s management believes that the expectations reflected in such forward-looking statements are reasonable, readers are cautioned that these forward-looking statements by their nature involve risk and uncertainty because they relate to events and depend on circumstances that will occur in the future. Many factors could cause actual results and developments to differ materially from those expressed or implied by these forward-looking statements, including those listed under “Cautionary Statement Concerning Forward-Looking Statements “ and “Risk Factors” in the preliminary prospectus included in the registration statement we intend to file with the SEC. See the previous paragraph for information about how you can obtain a free copy of the registration statement. We undertake no obligation to update forward-looking statements.

3

IMPORTANT ADDITIONAL INFORMATION

This presentation includes certain information concerning Pechiney and the combined business of Alcan and Pechiney. This information is subject to risks and uncertainties. We have based this information on publicly available information about Pechiney (primarily filings by Pechiney with the SEC and the French Commission des opérations de bourse). However, Pechiney has not yet granted Alcan access to Pechiney’s books and records or any other non-public information regarding Pechiney and Alcan has no means of compelling such access. In addition, Pechiney’s primary financial statements are prepared in accordance with generally accepted accounting principles (“GAAP”) in France while Alcan’s primary financial statements are prepared in accordance with Canadian GAAP. There are differences between Canadian and French GAAP. The unaudited pro forma information included herein is prepared based on the US GAAP information that Pechiney discloses pub licly. Alcan has not been in a position to verify the Pechiney information or the pro forma information about the combined entity included in this presentation. Some of the information about Pechiney in this presentation is based on good faith estimates by Alcan or industry sources that may be materially inaccurate. The pro forma information presented is not necessarily indicative of the operating results or financial condition that would have been achieved had Alcan’s offer for Pechiney been completed during the periods or at the times presented, nor is this information necessarily indicative of future results or conditions of Alcan after it has acquired Pechiney. The pro forma information does not reflect the impact of synergies that Alcan expects to realize over time or the costs associated with the integration of operations necessary to achieve such synergies nor does it reflect the impact of significant divestitures that Alcan must make as required by antitrust regulators. Some of the risks as sociated with the information about Pechiney and the combined Alcan and Pechiney will be discussed under “Risk Factors” in the preliminary prospectus included in the registration statement that we have filed with the SEC in connection with the proposed offer.

Certain terms used in this presentation are defined in the appendix.

4

Alcan + Pechiney

Invest With Confidence

- Alcan at a Glance

- Strategic Rationale

- The Combined Company

- Transaction Review

- Summary

5

Alcan at a Glance

Overview

Worldwide Leader

| Key Facts | Key Attributes |

| Second largest aluminum company | Diversified business mix |

| $12.3 billion revenues* | Low cost operations |

| 54,000 employees | Attractive growth platforms |

| 42 countries | Strong financial performance |

| 6 business segments | Robust earnings capacity |

* Fiscal year 2002

One Governing Objective – Maximize Value

6

Alcan at a Glance

Global Presence

Geographic Balance

| 2002 Alcan Capital Assets ($12.9 Billion) | 2002 Alcan Revenues ($12.3 Billion) |

|  |

2002 Western World Al Consumption (28.5 Mt)

7

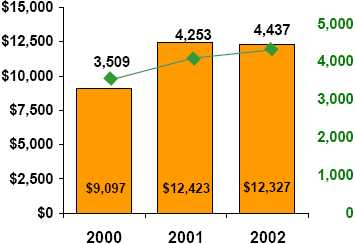

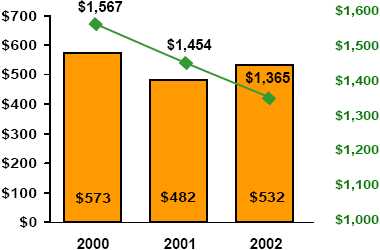

Alcan at a Glance

Strong Financial Performance

Delivering Despite Weak Economic Conditions

Revenues and Aluminum Volumes

![]() Sales & operating rev. (US$M)

Sales & operating rev. (US$M) ![]() Total aluminum volume (kt)

Total aluminum volume (kt)

Operating Income(1)

![]() Operating income (US$M)

Operating income (US$M) ![]() LME (US$/t)

LME (US$/t)

![]()

(1) Operating income: calculated by substracting foreign currency balance sheet translation effects and Other Specified Items from Net Income

8

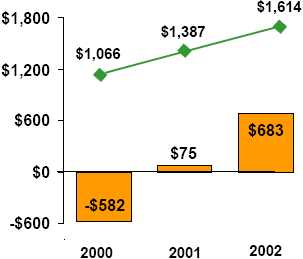

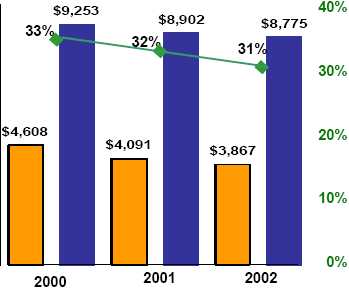

Alcan at a Glance

Strong Financial Performance

Demonstrated Financial Discipline

Cash Flow (in US$M)

![]() Free Cash Flow (US$M)

Free Cash Flow (US$M) ![]() Cash from Operations (US$M)

Cash from Operations (US$M)

Debt as a Percent of Total Capital

| $10,000 $8,000 $6,000 $4,000 $2,000 $0 |  |

![]() Borrowings (US$M)

Borrowings (US$M) ![]() Debt:Total Capital

Debt:Total Capital ![]() Equity (US$M)

Equity (US$M)

![]()

9

Alcan at a Glance

Q3 2003 Highlights*

Strong Cash Flow Underscores Business Performance

Earnings

Operating EPS up 5% over Q2 and stable year-over-year. Cost efficiencies and improved metal prices offset falling US$ and higher pension and energy costs.

Net income from continuing operations down $0.23 per share Y/Y due mainly to foreign currency balance sheet translation effects and Other Specified Items.

Cash Flow

- Record free cash flow of $266 M, up $60 M Y/Y

- Cash from operations of $560 M, up $140 M Y/Y

- Capex in line with depreciation

- Debt as a percentage of total capital at 31%

Maximizing Value Initiatives Continue

- Pechiney offer initiated and approved

- VAW integration on track

- Uniwood/Fome-Cor purchase announced

* For additional information about Q3 2003, see press release dated October 23, 2003 and Form 8-K of same date.

10

Alcan at a Glance

Financial Targets

Long Term Objective: Double Value Every Five Years

- Grow operating earnings per share by 15% per year

- Minimum of $400 million free cash flow per year

- EVA positive by 2006

11

Strategic Rationale

Compelling Strategic Rationale

Creates Substantial Value for Shareholders

- Consistent with strategy & value-maximizing objectives

- Solidifies Alcan as a world-leading aluminum company

- Broad technology leadership - core smelting technology

- Enhanced aluminum fabrication portfolio, e.g. aerospace

- US$6 billion packaging leader

- Accretive to EPS, free cash flow, ROCE from Year 1

- Timing is right

- Substantial future options created

12

Strategic Rationale

US$250 Million Annual Pre-Tax Cost Synergies

Synergies are Realistic and Achievable

100% percent of synergiesby year-end 2005

Costs

- Implementation: US$200 million

- CAPEX: US$50 million

13

Strategic Rationale

Competition Review

Clearance by MTF and DOJ Received

European Commission (MTF) | US Department of Justice (DOJ) |

| Divestiture of either | Divestiture of Pechiney's aluminumrolling mill located in Ravenswood (West Virginia) |

| The statutory waiting period under the US Hart-Scott Rodino Act expired on September 29. |

| |

| Continue licensing of alumina refining technology and aluminum smelter cell technology | |

| Divestiture of anode baking furnace designs | |

| Elimination of the overlap in aluminum aerosol cans and aluminum cartridges |

Total commitments amount to approximately 5% of pro-forma sales

(1) Alcan's Latchford casting operations can also be added to either the AluNorf or Neuf-Brisach packages at the purchaser’s option.

14

Strategic Rationale

Government Review

Clearance by French Treasury Department Received

Continuity of operations at industrial sites except those which Pechiney has, as of today, announced would be closed

Location in France of

- The global headquarters for packaging and aerospace operations

- The global headquarters of new cell technology for primary aluminum

- The European headquarters for primary aluminum operations

- The global headquarters for engineered products

15

Strategic Rationale

Integration Approach

Lessons Learned from algroup

- Maintain current operating focus

- Line leadership of integration process

- Jointly staffed integration teams

- Fill and announce key jobs as soon as possible

- Timeline to achieve full synergy run-rate within 2 years

Demonstrated track record in synergies

16

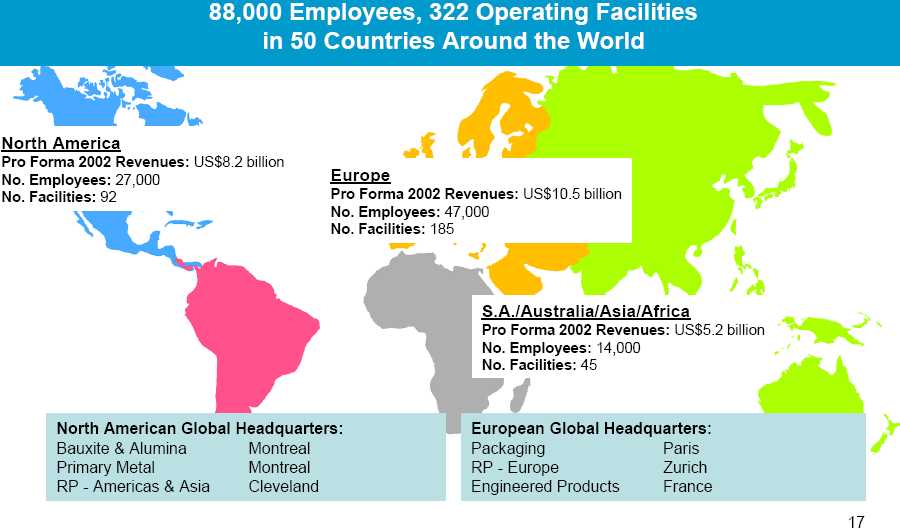

The Combined Company

Global Group - Balanced Presence

17

The Combined Company

Diversified Business Mix

Balanced Portfolio

2002 Revenue

Alcan: US$12.3 Bn

Pechiney: US$11.4 Bn(1),(2)

Pro Forma: US$23.7 Bn(1),(2)

27%

27%

- (1) Including Pechiney trading revenue of US$4.8 billion

- (2) On the basis of average US$/€ exchange rate during 2002 of .95

18

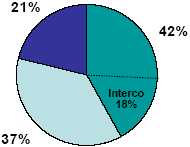

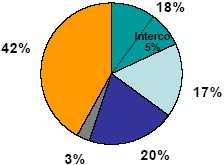

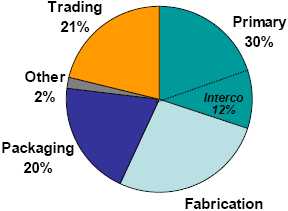

The Combined Company

Increased Core Market Presence

Strengthens Current Position

2002 Revenue By End-Use Market(1)(2)

| Alcan | Pechiney |

|  |

Pro Forma

(1) Excludes Pechiney trading revenues of US$4.8 billion

(2) On the basis of average US$/€ exchange rate during 2002 of .95

Source: Pechiney figures are based on estimates derived from publicly available documents

19

The Combined Company

Leading Position in Aluminum

A Leader in Primary Aluminum and Rolled Products

Primary

– Bauxite and alumina

- 2nd worldwide position in alumina production capacities(1)

- Complementary bauxite mines and alumina refineries

- Technology optimization

–Aluminum smelting

- Largest share of low-cost smelting capacity in the world

- Advanced high-amperage smelting technology

Rolled and fabricated products

- Large presence in value-added aerospace market

- Improved service of growing demand for automotive applications in North America and Europe

- Application of best manufacturing practices

(1)Source : CRU (Industry and Market Outdoor, January 2003)

20

The Combined Company

A Packaging Leader

Strength Across Key End-Use Markets

21

The Combined Company

Technological Excellence

Cutting-Edge Capabilities

| Alcan | Pechiney | Together |

| Alumina refining Smelter -Cell efficiency Automotive Rolling Packaging Composites | Alumina refining Smelter - High amperage Aerospace Packaging | Strong technological base Sharing best practices & More efficient investments |

22

The Combined Company

Customer Benefits

Meets Customers' Need for Full-Service Suppliers

Enhanced Scale and Regional Diversity

| Aluminum | Packaging |

| Diversified low-cost primary position Increased R&D and technological capabilities Capacity and reach to address Aerospace capability | Leading full-service supplier in most segments Global reach Integrated solutions |

23

Transaction Review

Summary of Terms

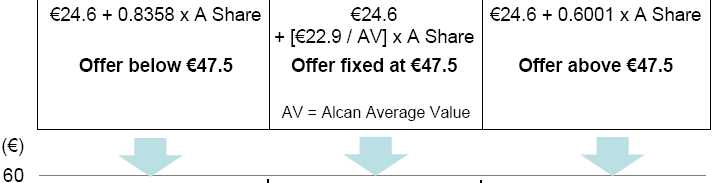

An Attractive Premium

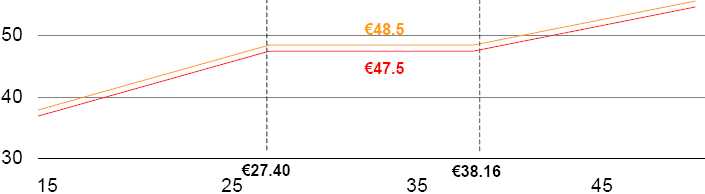

| Consideration | €47.5 per Pechiney share(1) €83.4 per OCEANE |

| Offer Structure | For each Pechiney share: €24.6 in cash plus Alcan shares equivalent to €22.9, based on the average value pricing formula Maximum number of Alcan shares: 0.8358 Minimum number of Alcan shares: 0.6001 |

| Substitution Option | Option to substitute an equivalent amount of cash for all or part of the stock component |

| Bonus | Additional €1 in cash if more than 95% of Pechiney capital and voting rights on a fully diluted basis are tendered €0.4 bonus per OCEANE |

| Minimum Condition | More than 50% shares tendered |

(1) If Alcan’s average value is between €27.40 and €38.16 as explained under “Pricing”.

24

Transaction Review

Pricing

A Fixed-Price Mechanism, with Potential Upside

Value of the Offer for 1 Pechiney share

(Excluding share for cash substitution option) Alcan Average Value (€)

25

Transaction Review

Pricing

Value-Protecting Structure

- Offer value fixed at €47.5 even if Alcan stock price in € decreases, down to a value of €27.4, contrary to usual fixed parity mixed offers

- Pechiney shareholders retain upside potential on Alcan stock

- Greater transparency and certainty for Pechiney shareholders:

- Average value of Alcan stock based on 10 trading days among 30 days

- Determination of the stock component consideration 5 trading days before the end of the offer period

- Average value of Alcan stock based on 10 trading days among 30 days

26

Transaction Review

Remaining Transaction Milestones

Alcan Committed to Successful Process

| Main Steps | Time Period | |

| Initial Offer filed | July 7 | |

| Pechiney Board recommends revised Offer | September 12 | |

| Revised Offer filed | September 15 | |

| Approval decision ("Avis de recevabilité") by the Conseil des Marchés Financiers (CMF) Receipt of competitive/anti-trust clearances in EU, US and Canada | September 29 | |

| Launch of the Offer in France | October 7 | |

| Launch of the Offer in US | October 27 | |

| Subject to CMF decision | Alcan to announce final terms of Offer | November 17 |

| Closing of the Offer | November 24 | |

| Publication of the Results of the Offer | December 1 |

27

Summary

Alcan: Committed to Maximizing Value

Invest With Confidence

- Creates industry leader

- Provides strong base for further value-creating opportunities

- Supports financial targets

- Enables potential for re-rating

- Leverages track record

28

Appendix

29

Western World Aluminum Balance

Primary Metal

(kt)

| 2001 | 2002 | 2003f | |

| Production | 16,670 | 17,230 | 17,730 |

| FSU/China/E. Europe | 2,700 | 2,750 | 3,150 |

| SUPPLY | 19,370 | 19,980 | 20,880 |

| % Change | -1.9% | +3.1% | +4.5% |

| DEMAND | 18,920 | 19,570 | 20,490 |

| % Change | -6.2% | +3.4% | +4.7% |

| INVENTORY CHANGE | +450 | +410 | +390 |

30

Aluminum – Primary

Bauxite & Alumina

2002 Alumina Production

| kt |

- Further 20% of Queensland

- Integrate complementary bauxite mines and alumina refineries

- Optimize technologyof the two companies

Source: CRU (Industry and Market Outlook, January 2003)

31

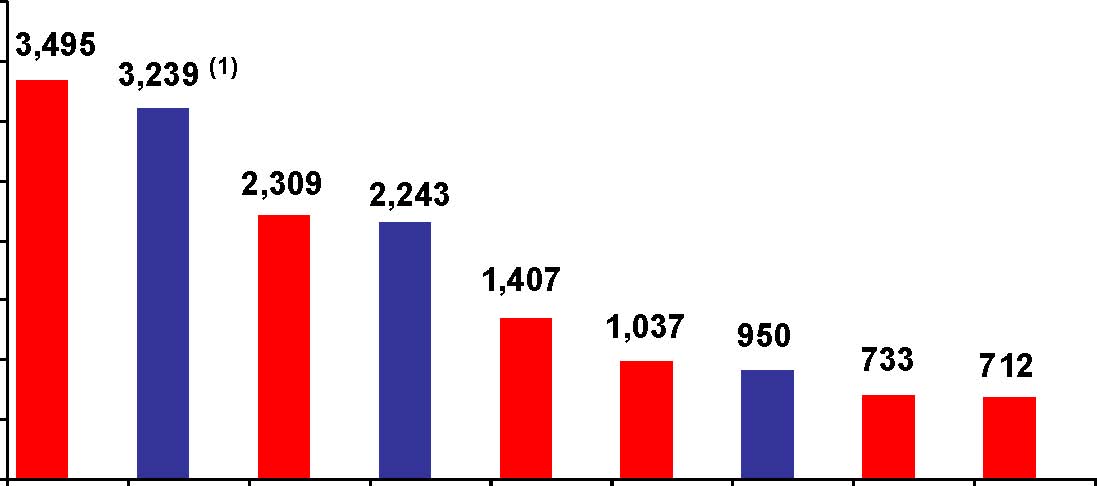

Aluminum - Primary

Aluminum Smelting

2002 Production as % of Global

16% 14% 12% 10% 8% 6% 4% 2% 0% |  |

Alcoa Pro forma Alcan RusAI Alcan VAW Billiton Pechiney Chinalco Comalco

- Largest share of low-cost smelting capacity in the world

- 50% in bottom third of global cost curve

- 50% in bottom third of global cost curve

- Advanced high-amperage smelting technology (AP30 & AP-50 cell)

- Alcan’s wholly owned hydroelectric power

(1) Adjusted to include Alouette for full year

Source: CRU (Industry and Market Outlook, January 2003)

32

Aluminum – Rolled & Fabricated Products

2002 Pro Forma Revenues by End Market

| World class aluminum rolling and Application of best manufacturing Improved service Synergy potential

|

Source: Pechiney figures based on estimates derived from publicly available documents.

33

Definitions

EVA® is a registered trademark of Stern Stewart & Co. and a key measure of financial performance. The term means the difference between the return on capital and the cost for using the capital over the same period.

Foreign currency balance sheet translation means gains and losses arising from translating balance sheet items mainly in Canada and Australia (principally accounts payable, deferred credits and other liabilities, and deferred income taxes) at period-end exchange rates.

Free Cash Flow is calculated by substracting dividends and capital expenditures from cash from operating activities.

Operating Income is calculated by substracting foreign currency balance sheet translation effects and Other Specified Items from net Income.

Other Specified Items include, for example: restructuring charges; asset impairment charges; unusual environmental charges; gains and losses on non-routine sales of assets, businesses or investments; gains and losses from legal claims; gains and losses on the redemption of debt; income tax adjustments related to prior years and the effects of changes in income tax rates; and other items that do not typify normal business activities.

ROCE (return on capital employed) is earnings before interest and tax divided by capital, which is equal to Total Capital.

Total Capital is the sum of short-term borrowings, debt maturing within one year, debt not maturing within one year, minority interest, redeemable non-retractable preference shares and common shareholders’ equity.

34

©2003 ALCAN INC.