| For further information: Paula Waters, VP, Investor Relations Phone 504/576-4380, Fax 504/576-2897 pwater1@entergy.com |

INVESTOR NEWS

November 4, 2011

ENTERGY ISSUES FORWARD LOOKING FINANCIAL UPDATE

NEW ORLEANS – Entergy Corporation today issued 2012 earnings guidance and outlined its preliminary three-year capital expenditure plan for the period 2012 through 2014. In addition, Entergy affirmed its long-term financial outlook.

“The Utility continues to work toward its long-term outlook of a 6 to 8 percent compound annual net income growth rate over the 2010 – 2014 horizon,” said J. Wayne Leonard, Entergy’s chairman and chief executive officer. “Several portfolio transformation projects are in progress, including two power plant acquisitions and the Ninemile new build project. Efforts for the operating companies to join the Midwest Independent System Operator regional transmission organization, which will provide significant savings for our Utility customers, will be a key area of focus over the short term. Our Entergy Wholesale Commodities segment continues to be affected by depressed gas and power prices. Work to preserve the value of that business is ongoing through operational excellence and license renewal efforts as well as continuously enhancing opportunities to capture additional value in that business, such as the planned acquisition of the Rhode Island State Energy Center power plant.”

Members of Entergy’s senior management, including Leonard and Leo Denault, executive vice president and chief financial officer, will attend the 46th Edison Electric Institute (EEI) Financial Conference, hold stakeholder meetings on November 7 through November 8, 2011, and take questions on the information included in this release and accompanying handout material. This release and the handout material can also be accessed via Entergy’s website at www.entergy.com. As previously announced, Leonard will also provide a presentation on Tuesday, November 8 starting at approximately 7:30 a.m. ET. A live audio webcast and copy of the presentation slides will be available on Tuesday on Entergy’s website.

Earnings Guidance

Entergy is initiating 2012 earnings guidance in the range of $5.40 to $6.20 per share on both as-reported and operational bases. Year-over-year changes are shown as point estimates and are applied to an adjusted 2011 starting point to compute the 2012 guidance midpoint. While Entergy affirms its updated 2011 earnings guidance range of $7.15 to $7.65 per share on as-reported and operational bases, the 2011 starting point by business segment was adjusted consistent with current indications. Drivers for the 2012 guidance range are listed separately. Because there is a range of possible outcomes associated with each earnings driver, a range is applied to the guidance midpoint to produce Entergy’s guidance range. Entergy’s 2012 earnings guidance is detailed in Table 1 below.

| Table 1: 2012 Earnings Per Share Guidance – As-Reported and Operational |

| (Per share in U.S. $) – Prepared November 2011 |

| Segment | Description of Drivers | 2011 Adjusted Starting Point (a) | Expected Change | 2012 Guidance Midpoint | 2012 Guidance Range |

| | | | | | |

| Utility | Revised 2011 Operational Earnings per Share | 6.10 | | | |

| Adjustment to normalize weather | | (0.57) | | |

| Increased net revenue due to absence of sharing 2011 tax benefit with Entergy Louisiana customers | | 1.11 | | |

| Increased net revenue due to sales growth and rate actions | | 0.85 | | |

| Increased non-fuel operation and maintenance expense | | (0.05) | | |

| Increased other operating expenses | | (0.10) | | |

| Increased depreciation expense | | (0.20) | | |

| Increased interest and other charges | | (0.10) | | |

| Higher effective income tax rate | | (2.30) | | |

| Other | | 0.06 | | |

| Subtotal | 6.10 | (1.30) | 4.80 | |

| | | | | | |

| Entergy Wholesale Commodities | Revised 2011 Operational Earnings per Share | 2.40 | | | |

| Decreased net revenue from nuclear assets due primarily to lower pricing | | (0.60) | | |

| Increased non-fuel operation and maintenance expense for nuclear operations | | (0.05) | | |

| Increased other operating expenses for nuclear operations | | (0.05) | | |

| Increased depreciation expense on nuclear assets | | (0.05) | | |

| Increased after-tax operating income for EWC non-nuclear operations, including RISEC acquisition | | 0.10 | | |

| Increased interest and dividend income | | 0.05 | | |

| Higher effective income tax rate | | (0.05) | | |

| Other | | 0.05 | | |

| Subtotal | 2.40 | (0.60) | 1.80 | |

| | | | | | |

| Parent & Other | Revised 2011 Operational Earnings per Share | (1.10) | | | |

| Increased Parent non-fuel operation and maintenance expense | | (0.05) | | |

| Increased Parent interest expense | | (0.15) | | |

| Lower income tax expense | | 0.45 | | |

| Other | | 0.05 | | |

| Subtotal | (1.10) | 0.30 | (0.80) | |

| | | | | | |

| Consolidated | 2012 As-Reported and Operational Earnings per Share Guidance Range | 7.40 | (1.60) | 5.80 | 5.40 – 6.20 |

| | | | | | |

| (a) | The current 2011 as-reported and operational earnings guidance range is $7.15 to $7.65 per share, which was revised in October 2011. |

Key assumptions supporting 2012 earnings guidance are as follows:

Utility

| · | Retail sales growth of around 1.6% on a weather-adjusted basis, including the effects of industrial expansion and cogen loss |

| · | Increased revenue from rate actions |

| · | Increased net revenue due to the absence of the third quarter 2011 regulatory charge to reflect an agreement to share a portion of tax benefits with Entergy Louisiana customers that resulted from an IRS tax settlement |

| · | Increased non-fuel operation and maintenance expense due to plant acquisitions and general expense increases (including lower expense associated with employee stock options, which is offset in Parent & Other) |

| · | Increased depreciation expense associated with capital spending at the Utility |

| · | Increased other operating expense due primarily to higher taxes other than income taxes, resulting largely from new plant acquisitions as well as expiration of property tax exemptions |

| · | Increased interest expense due to higher debt outstanding |

| · | Higher effective income tax rate in 2012, due largely to the absence of the August 2011 IRS settlement, a portion of which was partially offset in net revenue as noted above |

| Other primarily driven by the effect of 2011 share repurchases |

Entergy Wholesale Commodities

| · | 41 TWh of total output for the non-utility nuclear fleet, reflecting an approximate 93 percent capacity factor, including 30-day scheduled refueling outages at Indian Point 2 and Palisades in Spring 2012 and FitzPatrick in Fall 2012 |

| · | Assumes full year operations for Vermont Yankee and Pilgrim |

| · | 89 percent of energy sold under existing contracts and 11 percent sold into the spot market for EWC-nuclear fleet |

| · | $49/MWh average energy contract price and $46/MWh average unsold energy price based on published market prices at the end of September 2011 for EWC-nuclear fleet |

| · | 50 percent of capacity sold under existing contracts (including 32 percent sold as capacity contracts and 18 percent sold bundled with energy) for EWC-nuclear fleet |

| · | $2.8/kW-month average sold capacity contract price and $0.5/kW-month average unsold capacity price based on published market prices at the end of September 2011 for EWC-nuclear fleet |

| · | Palisades PPA revenue amortization of $17 million in 2012, down from $43 million in 2011 |

| · | Increased nuclear fuel expense reflected in net revenue |

| · | Non-fuel operation and maintenance expense for nuclear operations, including refueling outage expense and purchased power, around $25.5/MWh reflecting general expense increases |

| · | Increased other operating expense due to higher decommissioning expense and higher taxes other than income taxes for nuclear operations |

| · | Increased depreciation expense on nuclear assets due to higher depreciable plant balances as well as declining useful life of nuclear assets |

| · | Improved year-over-year operating income for the balance of EWC’s business, including the assumed Rhode Island State Energy Center (RISEC) acquisition by year-end 2011 and market prices at the end of September 2011 |

| · | Higher effective income tax rate in 2012 |

Parent & Other

| · | Increased Parent non-fuel operation and maintenance expense due primarily to the offset of lower intercompany employee stock option expense at Utility |

| · | Higher Parent interest expense due to the refinancing of low-cost debt (current credit facility expires August 2012) |

| · | Lower income tax expense in 2012 |

Share Repurchase Program

| · | 2012 average fully diluted shares outstanding of approximately 177 million; does not assume any repurchases under the $500 million share repurchase authority, $350 million of which remained as of September 30, 2011 |

Other

| · | Overall effective income tax rate of 34 percent in 2012 |

| · | Pension discount rate of 5.6 percent |

Earnings guidance for 2012 should be considered in association with earnings sensitivities as shown in Table 2. These sensitivities illustrate the estimated change in operational earnings resulting from changes in various revenue and expense drivers. Traditionally, the most significant variables for earnings drivers are utility sales for Utility and energy prices for Entergy Wholesale Commodities. The broader earnings guidance range for 2012 also takes into consideration the following:

| · | A number of regulatory initiatives (rate actions) underway across the Utility jurisdictions |

| · | Potential outcomes for projected pension plan discount rate (guidance assumes 5.6 percent) |

Estimated annual impacts shown in Table 2 are intended to be indicative rather than precise guidance.

| Table 2: 2012 Earnings Sensitivities |

| (Per share in U.S. $) – Prepared November 2011 |

Variable | 2012 Guidance Assumption | Description of Change | Estimated Annual Impact (b) |

| Utility | | | |

Sales growth Residential Commercial / Governmental Industrial | Around 1.6% total sales growth on a weather adjusted basis | 1% change in Residential MWh sold 1% change in Comm / Govt MWh sold 1% change in Industrial MWh sold | - / + 0.05 - / + 0.04 - / + 0.02 |

| Rate base | Growing rate base | $100 million change in rate base | - / + 0.03 |

| Return on equity | Authorized regulatory ROEs | 1% change in allowed ROE | - / + 0.37 |

Entergy Wholesale Commodities (c) | | |

| Capacity factor | 93% capacity factor | 1% change in capacity factor | - / + 0.06 |

| Energy revenues | 89% energy sold at $49/MWh in 2012; 11% unsold at $46/MWh in 2012 | $10/MWh market price change | - 0.16 / + 0.20 |

| Non-fuel operation and maintenance expense | $25.5/MWh non-fuel operation and maintenance expense/purchased power | $1/MWh change | + / - 0.14 |

| Outage (lost revenue only) | 93% capacity factor, including refueling outages for three non-utility nuclear units | 1,000 MW plant for 10 days at average portfolio energy price of $49/MWh for sold and $46/MWh for unsold volumes in 2012 | - 0.03 / n/a |

| |

(b) Based on 2011 projected average fully diluted shares outstanding of approximately 178 million. (c) Based on Entergy Wholesale Commodities’ nuclear portfolio. Assumes successful license renewal and uninterrupted normal operation at all plants. |

Overarching Financial Aspiration

Entergy continues to aspire to deliver superior value to owners as measured by total shareholder return. The company believes top-quartile total shareholder return is achieved by:

| · | Operating the business with the highest expectations and standards; |

| · | Executing on earnings growth opportunities while managing commodity and other business risks; |

| · | Delivering returns at or above the risk-adjusted cost of capital for each initiative, project, business, etc.; |

| · | Maintaining credit quality and flexibility; |

| · | Deploying capital in a disciplined manner, whether for new investments, share repurchases, dividends or debt retirements; and |

| · | Being disciplined as either a buyer or a seller consistent with the market or Entergy’s proprietary point of view. |

Long-term Financial Outlook

Entergy believes it offers a long-term, competitive utility investment opportunity combined with a valuable option represented by a unique, clean, non-utility generation business located in attractive power markets. Table 3 summarizes the current long-term financial outlook for 2010 through 2014.

Table 3: Long-term Financial Outlook |

| Prepared November 2011 |

| | | |

| Category | Long-term Outlook | Assumption |

| | | |

| Earnings | Utility net income | 6 to 8 percent compound annual net income growth rate over the 2010 – 2014 horizon (2009 base year). |

| | | |

| | Entergy Wholesale Commodities results | Revenue projections through 2014 will experience increased volatility due to commodity market activities – one of the most important fundamental drivers for this business. At current sold and forward prices with its existing asset portfolio and in-the-money hedges that will roll off in the coming few years, EWC is expected to deliver declining adjusted EBITDA for the period through 2014 compared to 2010, with a 2013 inflection point (i.e., declining through 2013; 2014 trend turns to increasing). However, Entergy Wholesale Commodities offers a valuable long-term option from the potential positive effects of ongoing economic growth (driving increased load, market heat rates, capacity prices and natural gas prices), new environmental legislation and/or enforcement of additional environmental regulation. |

| | | |

| | Corporate results | Results will vary depending upon factors including future effective income tax and interest rates and the amount / timing of share repurchases. |

| | | |

| Capital Deployment | A balanced capital investment / return program | Entergy continues to see value-added investment opportunities at the Utility in the coming years, as well as an investment outlook at Entergy Wholesale Commodities that supports continued safe, secure and reliable operations and opportunistic investments. Entergy aspires to fund this capital program without issuing traditional common equity, while maintaining a competitive capital return program. Given the company’s financial profile with a mix of utility and non-utility businesses, return of capital is expected to be provided similar to the past through a combination of common stock dividends and share repurchases. Absent other attractive investment opportunities, capital deployment through dividends and share repurchases could total as much as $4 – $5 billion from 2010 – 2014 under the current long-term business outlook. The amount of share repurchases may vary as a result of material changes in business results, capital spending or new investment opportunities. |

| | | |

| Credit Quality | | Strong liquidity. |

| |

| Solid credit metrics that support ready access to capital on reasonable terms. |

| | | |

The long-term financial outlook should be considered in association with 2014 financial sensitivities as shown in Table 4. These sensitivities illustrate the estimated change in earnings or adjusted EBITDA resulting from changes in business drivers. Estimated impacts shown in Table 4 are intended to be illustrative.

Table 4: 2014 Financial Sensitivities – Illustrative |

| Prepared November 2011 |

Long-term Outlook | Assumption | Drivers | Estimated Annual Impact |

| Utility | | | (Per share in U.S. $) (d) |

| | | | |

Earnings growth | 6 – 8% compound annual net income growth rate from 2010 through 2014 (2009 base) | 1% retail sales growth $100 million/year investment in service 1% change in allowed ROE 1% change in non-fuel operation and maintenance expense $100 million change in debt | - / + 0.14 - / + 0.03 - / + 0.45 + / - 0.07 + / - 0.02 |

Entergy Wholesale Commodities (e) | | | (Adjusted EBITDA in U.S. $; millions) (f) |

| | | | |

| Adjusted EBITDA (f) | Decline in adjusted EBITDA at current sold and forward power prices compared to 2010, plus option value | +0 – 1,500 Btu/kWh heat rate expansion +$0 – 30/ton CO2 +$0 – 4/kW-mo capacity price - / + $0 – 1/MMBtu change in Henry Hub natural gas price $1/MWh EBITDA expense | Up to 240 Up to 440 Up to 150 Down / Up to 300 +/- 40 |

Corporate | | | (Per share in U.S. $) (d) |

| | | | |

| Balanced capital investment / return / credit quality | | 1% change in interest rate on $1 billion debt 1% change in overall effective income tax rate $500 million share repurchase (share accretion effect only) | + / - 0.03 + / - 0.09 + 0.20 – 0.25 |

(d) Based on estimated 2012 average fully diluted shares outstanding of approximately 177 million. (e) Based on Entergy Wholesale Commodities’ nuclear portfolio. Assumes successful license renewal and uninterrupted normal operation at all plants. (f) Adjusted EBITDA is defined as earnings before interest, income taxes, depreciation and amortization and interest and investment income excluding decommissioning expense, other than temporary impairment losses on decommissioning trust fund assets and special items. |

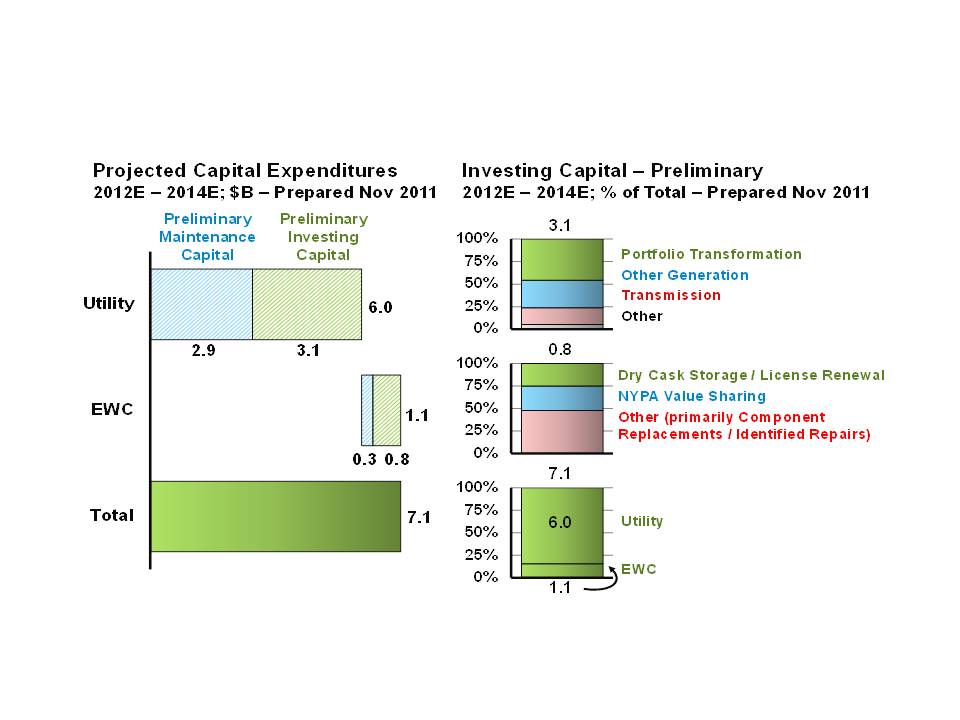

Planned Capital Expenditures – Preliminary

The preliminary capital plan for 2012 through 2014 anticipates $7.1 billion for investment, including $3.2 billion of maintenance capital, as shown in Figure 1. The remaining $3.9 billion is for specific investments and other initiatives such as:

| · | Utility: the Utility’s portfolio transformation strategy including the 620 MW Hot Spring and 450 MW Hinds power plant acquisitions (including planned plant upgrades, transaction costs, and contingencies), an approximate 178 MW uprate project at Grand Gulf nuclear plant, Entergy Louisiana’s Ninemile 6 new CCGT project, as well as the associated transmission investment; the steam generator replacement at Entergy Louisiana’s Waterford 3 nuclear unit; transmission upgrades and spending to support the Utility’s plan to join the MISO RTO by December 2013. |

| · | Entergy Wholesale Commodities: dry cask storage, nuclear license renewal efforts, component replacement and identified repairs across the fleet, NYPA value sharing, the Indian Point Independent Safety Evaluation, and wedgewire screens at the Indian Point site. |

Figure 1: 2012 – 2014 Preliminary Capital Expenditure Plan |

| Prepared November 2011 |

Entergy Corporation’s common stock is listed on the New York and Chicago exchanges under the symbol “ETR”.

Additional investor information can be accessed on-line at

www.entergy.com/investor_relations

**********************************************************************************************************************************

In this news release, and from time to time, Entergy Corporation makes certain “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. Except to the extent required by the federal securities laws, Entergy undertakes no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events, or otherwise.

Forward-looking statements involve a number of risks and uncertainties. There are factors that could cause actual results to differ materially from those expressed or implied in the forward-looking statements, including (a) those factors discussed in: (i) Entergy’s Form 10-K for the year ended December 31, 2010; (ii) Entergy’s Form 10-Q for the quarters ended March 31, 2011 and June 30, 2011; and (iii) Entergy’s other reports and filings made under the Securities Exchange Act of 1934; (b) uncertainties associated with rate proceedings, formula rate plans and other cost recovery mechanisms; (c) uncertainties associated with efforts to remediate the effects of major storms and recover related restoration costs; (d) nuclear plant relicensing, operating and regulatory risks, including any changes resulting from the nuclear crisis in Japan following its catastrophic earthquake and tsunami; (e) legislative and regulatory actions and risks and uncertainties associated with claims or litigation by or against Entergy and its subsidiaries; and (f) conditions in commodity and capital markets during the periods covered by the forward-looking statements, in addition to other factors described elsewhere in this release and in subsequent securities filings.