UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number811- 2402

John Hancock Sovereign Bond Fund

(Exact name of registrant as specified in charter)

200 Berkeley Street, Boston, Massachusetts 02116

(Address of principal executive offices) (Zip code)

Salvatore Schiavone

Treasurer

200 Berkeley Street

Boston, Massachusetts 02116

(Name and address of agent for service)

Registrant's telephone number, including area code:617-663-4497

| Date of fiscal year end: | May 31 | |

| Date of reporting period: | November 30, 2019 |

ITEM 1. REPORTS TO STOCKHOLDERS.

John Hancock

Bond Fund

Semiannual report 11/30/19

Beginning on January 1, 2021, as permitted by regulations adopted by the Securities and Exchange Commission, paper copies of the fund's shareholder reports like this one will no longer be sent by mail, unless you specifically request paper copies of the reports from the fund or from your financial intermediary. Instead, the reports will be made available on a website, and you will be notified by mail each time a report is posted and provided with a website link to access the report.

If you already elected to receive shareholder reports electronically, you will not be affected by this change, and you do not need to take any action. You may elect to receive shareholder reports and other communications electronically by calling John Hancock Investment Management at 800-225-5291 (Class A, Class B and Class C shares) or 888-972-8696 (Class I, Class R2, Class R4 and Class R6 shares) or by contacting your financial intermediary.

You may elect to receive all reports in paper, free of charge, at any time. You can inform John Hancock Investment Management or your financial intermediary that you wish to continue receiving paper copies of your shareholder reports by following the instructions listed above. Your election to receive reports in paper will apply to all funds held with John Hancock Investment Management or your financial intermediary.

A message to shareholders

Dear shareholder,

It was a volatile time for bond investors during the six months ended November 30, 2019, although most market segments delivered attractive absolute returns for the period. Uncertainty surrounding trade with China, the impeachment inquiry against President Trump, and the broader health of the global economy led to some dramatic swings in performance. The trend in longer-term yields was decidedly downward, leading to several periods where the U.S. Treasury yield curve was inverted. Three times in 2019—in July, September, and October—the U.S. Federal Reserve stepped in with reductions in short-term interest rates in an attempt to shore up the economy.

While the economic fundamentals in the United States appear fairly solid—with a strong labor market, low inflation and interest rates, and a confident consumer base—the outlook for the global economy is less certain. Subsequent to period end, President Trump was impeached by the House of Representatives; it remains to be seen how the Senate and financial markets will react. We feel confident in saying there are sure to be patches of market turbulence in the months ahead. As always, your best resource in unpredictable markets is your financial advisor, who can help position your portfolio so that it's sufficiently diversified to meet your long-term objectives and to withstand the inevitable bouts of market volatility along the way.

On behalf of everyone at John Hancock Investment Management, I'd like to take this opportunity to welcome new shareholders and thank existing shareholders for the continued trust you've placed in us.

Sincerely,

Andrew G. Arnott

President and CEO,

John Hancock Investment Management

Head of Wealth and Asset Management,

United States and Europe

This commentary reflects the CEO's views as of this report's period end and are subject to change at any time. Diversification does not guarantee investment returns and does not eliminate risk of loss. All investments entail risks, including the possible loss of principal. For more up-to-date information, you can visit our website at jhinvestments.com.

John Hancock

Bond Fund

INVESTMENT OBJECTIVE

The fund seeks a high level of current income consistent with prudent investment risk.

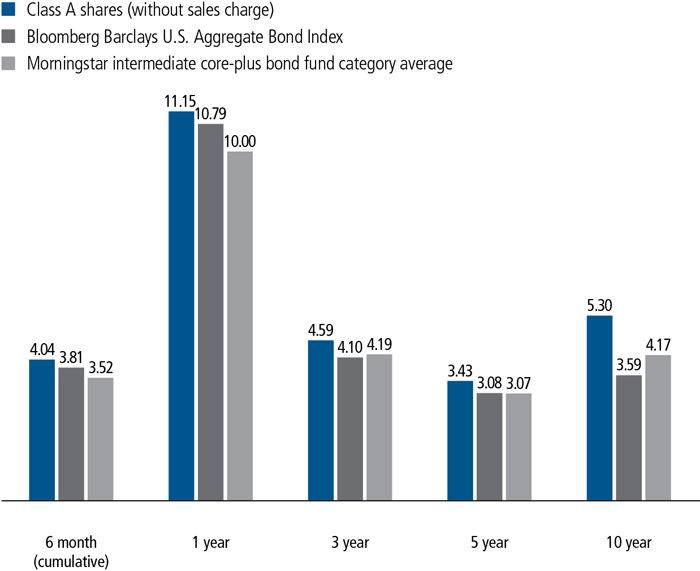

AVERAGE ANNUAL TOTAL RETURNS AS OF 11/30/19 (%)

The Bloomberg Barclays U.S. Aggregate Bond Index is an unmanaged index of dollar-denominated and non-convertible investment-grade debt issues.

It is not possible to invest directly in an index. Index figures do not reflect expenses or sales charges, which would result in lower returns.

Figures from Morningstar, Inc. include reinvested distributions and do not take into account sales charges. Actual load-adjusted performance is lower.

The past performance shown here reflects reinvested distributions and the beneficial effect of any expense reductions, and does not guarantee future results. Returns for periods shorter than one year are cumulative. Performance of the other share classes will vary based on the difference in the fees and expenses of those classes. Shares will fluctuate in value and, when redeemed, may be worth more or less than their original cost. Current month-end performance may be lower or higher than the performance cited, and can be found at jhinvestments.com or by calling 800-225-5291. For further information on the fund's objectives, risks, and strategy, see the fund's prospectus.

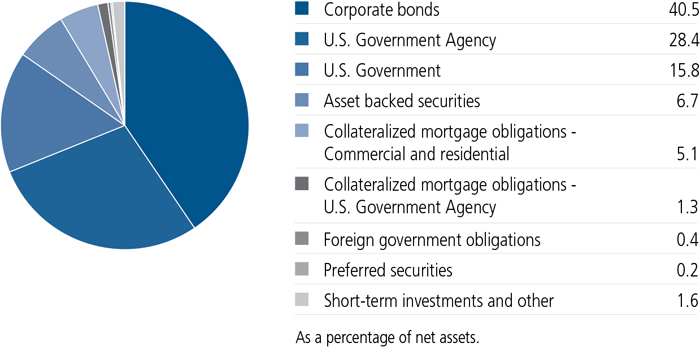

PORTFOLIO COMPOSITION AS OF 11/30/19 (%)

COUNTRY COMPOSITION AS OF 11/30/19 (%)

| United States | 89.8 |

| United Kingdom | 2.4 |

| Netherlands | 1.2 |

| Canada | 1.2 |

| Other countries | 5.4 |

| TOTAL | 100.0 |

| As a percentage of net assets. |

A note about risks

The fund is subject to various risks as described in the fund's prospectus. For more information, please refer to the "Principal risks" section of the prospectus.

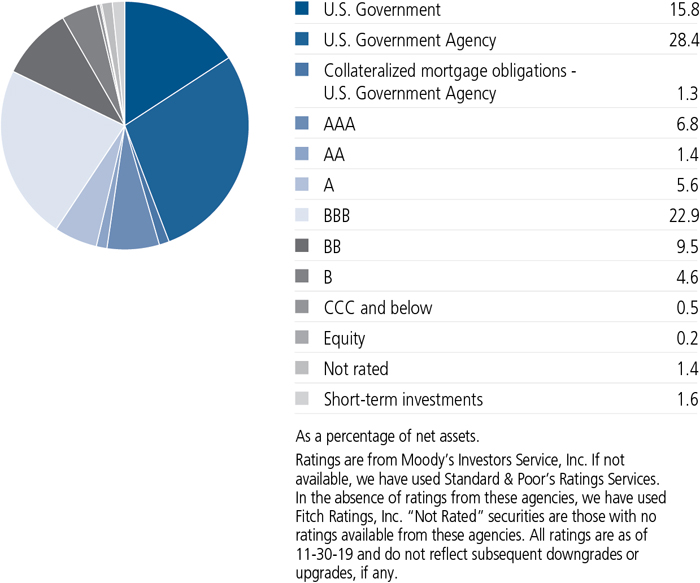

QUALITY COMPOSITION AS OF 11/30/19 (%)

TOTAL RETURNS FOR THE PERIOD ENDED NOVEMBER 30, 2019

| Average annual total returns (%) with maximum sales charge | Cumulative total returns (%) with maximum sales charge | SEC 30-day yield (%) subsidized | SEC 30-day yield (%) unsubsidized1 | ||||||||

| 1-year | 5-year | 10-year | 6-month | 5-year | 10-year | as of 11-30-19 | as of 11-30-19 | ||||

| Class A | 6.69 | 2.58 | 4.87 | -0.13 | 13.61 | 60.96 | 2.34 | 2.33 | |||

| Class B | 5.38 | 2.36 | 4.71 | -1.32 | 12.39 | 58.43 | 1.74 | 1.73 | |||

| Class C | 9.38 | 2.71 | 4.57 | 2.61 | 14.31 | 56.33 | 1.74 | 1.73 | |||

| Class I2 | 11.54 | 3.76 | 5.66 | 4.19 | 20.24 | 73.50 | 2.73 | 2.72 | |||

| Class R22,3 | 11.03 | 3.35 | 5.28 | 3.99 | 17.91 | 67.26 | 2.33 | 2.32 | |||

| Class R42,3 | 11.38 | 3.61 | 5.40 | 4.12 | 19.42 | 69.13 | 2.59 | 2.48 | |||

| Class R62,3 | 11.58 | 3.88 | 5.69 | 4.24 | 20.98 | 73.95 | 2.84 | 2.83 | |||

| Class NAV2,3 | 11.67 | 3.81 | 5.50 | 4.25 | 20.58 | 70.77 | 2.85 | 2.84 | |||

| Index† | 10.79 | 3.08 | 3.59 | 3.81 | 16.39 | 42.29 | — | — | |||

Performance figures assume all distributions have been reinvested. Figures reflect maximum sales charges on Class A shares of 4.0% and the applicable contingent deferred sales charge (CDSC) on Class B and Class C shares. The returns for Class A shares have been adjusted to reflect the reduction in the maximum sales charge from 4.5% to 4.0%, effective 2-3-14. The Class B shares' CDSC declines annually between years 1 to 6 according to the following schedule: 5%, 4%, 3%, 3%, 2%, 1%. No sales charge will be assessed after the sixth year. Class C shares sold within one year of purchase are subject to a 1% CDSC. Sales charges are not applicable to Class I, Class R2, Class R4, Class R6, and Class NAV shares.

The expense ratios of the fund, both net (including any fee waivers and/or expense limitations) and gross (excluding any fee waivers and/or expense limitations), are set forth according to the most recent publicly available prospectuses for the fund and may differ from those disclosed in the Financial highlights tables in this report. Net expenses reflect contractual expense limitations in effect until September 30, 2020 and are subject to change. Had the contractual fee waivers and expense limitations not been in place, gross expenses would apply. The expense ratios are as follows:

| Class A | Class B | Class C | Class I | Class R2 | Class R4 | Class R6 | Class NAV | |

| Gross (%) | 0.79 | 1.49 | 1.49 | 0.49 | 0.89 | 0.74 | 0.39 | 0.37 |

| Net (%) | 0.78 | 1.48 | 1.48 | 0.48 | 0.88 | 0.63 | 0.38 | 0.36 |

Please refer to the most recent prospectus and annual or semiannual report for more information on expenses and any expense limitation arrangements for each class.

The returns reflect past results and should not be considered indicative of future performance. The return and principal value of an investment will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Due to market volatility and other factors, the fund's current performance may be higher or lower than the performance shown. For current to the most recent month-end performance data, please call 800-225-5291 or visit the fund's website at jhinvestments.com.

The performance table above and the chart on the next page do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. The fund's performance results reflect any applicable fee waivers or expense reductions, without which the expenses would increase and results would have been less favorable.

| † | Index is the Bloomberg Barclays U.S. Aggregate Bond Index. |

See the following page for footnotes.

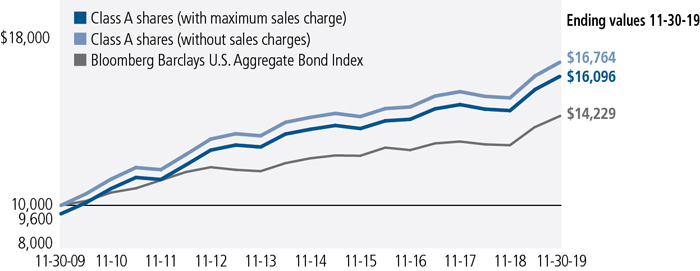

This chart and table show what happened to a hypothetical $10,000 investment in John Hancock Bond Fund for the share classes and periods indicated, assuming all distributions were reinvested. For comparison, we've shown the same investment in the Bloomberg Barclays U.S. Aggregate Bond Index.

| Start date | With maximum sales charge ($) | Without sales charge ($) | Index ($) | |

| Class B4 | 11-30-09 | 15,843 | 15,843 | 14,229 |

| Class C4 | 11-30-09 | 15,633 | 15,633 | 14,229 |

| Class I2,3 | 11-30-09 | 17,350 | 17,350 | 14,229 |

| Class R22,3 | 11-30-09 | 16,726 | 16,726 | 14,229 |

| Class R42,3 | 11-30-09 | 16,913 | 16,913 | 14,229 |

| Class R62,3 | 11-30-09 | 17,395 | 17,395 | 14,229 |

| Class NAV2,3 | 11-30-09 | 17,077 | 17,077 | 14,229 |

The values shown in the chart for Class A shares with maximum sales charge have been adjusted to reflect the reduction in the Class A shares' maximum sales charge from 4.5% to 4.0%, which became effective on 2-3-14.

The Bloomberg Barclays U.S. Aggregate Bond Index is an unmanaged index of dollar-denominated and non-convertible investment-grade debt issues.

It is not possible to invest directly in an index. Index figures do not reflect expenses or sales charges, which would result in lower returns.

Footnotes related to performance pages

| 1 | Unsubsidized yield reflects what the yield would have been without the effect of reimbursements and waivers. |

| 2 | For certain types of investors, as described in the fund's prospectuses. |

| 3 | Class R2 shares were first offered 3-1-12; Class R4 shares were first offered 3-27-15; Class R6 shares were first offered 9-1-11; Class NAV shares were first offered 8-31-15. Returns prior to these dates are those of Class A shares that have not been adjusted for class-specific expenses; otherwise, returns would vary. |

| 4 | The contingent deferred sales charge is not applicable. |

| Your expenses |

| SEMIANNUAL REPORT | JOHN HANCOCK BOND FUND | 7 |

| Account value on 6-1-2019 | Ending value on 11-30-2019 | Expenses paid during period ended 11-30-20191 | Annualized expense ratio | ||

| Class A | Actual expenses/actual returns | $1,000.00 | $1,040.40 | $3.98 | 0.78% |

| Hypothetical example | 1,000.00 | 1,021.10 | 3.94 | 0.78% | |

| Class B | Actual expenses/actual returns | 1,000.00 | 1,036.80 | 7.54 | 1.48% |

| Hypothetical example | 1,000.00 | 1,017.60 | 7.47 | 1.48% | |

| Class C | Actual expenses/actual returns | 1,000.00 | 1,036.10 | 7.53 | 1.48% |

| Hypothetical example | 1,000.00 | 1,017.60 | 7.47 | 1.48% | |

| Class I | Actual expenses/actual returns | 1,000.00 | 1,041.90 | 2.45 | 0.48% |

| Hypothetical example | 1,000.00 | 1,022.60 | 2.43 | 0.48% | |

| Class R2 | Actual expenses/actual returns | 1,000.00 | 1,039.90 | 4.44 | 0.87% |

| Hypothetical example | 1,000.00 | 1,020.70 | 4.40 | 0.87% | |

| Class R4 | Actual expenses/actual returns | 1,000.00 | 1,041.20 | 3.16 | 0.62% |

| Hypothetical example | 1,000.00 | 1,021.90 | 3.13 | 0.62% | |

| Class R6 | Actual expenses/actual returns | 1,000.00 | 1,042.40 | 1.89 | 0.37% |

| Hypothetical example | 1,000.00 | 1,023.20 | 1.87 | 0.37% | |

| Class NAV | Actual expenses/actual returns | 1,000.00 | 1,042.50 | 1.84 | 0.36% |

| Hypothetical example | 1,000.00 | 1,023.20 | 1.82 | 0.36% |

| 1 | Expenses are equal to the annualized expense ratio, multiplied by the average account value over the period, multiplied by 183/366 (to reflect the one-half year period). |

| 8 | JOHN HANCOCK BOND FUND | SEMIANNUAL REPORT |

| Fund’s investments |

| Rate (%) | Maturity date | Par value^ | Value | ||

| U.S. Government and Agency obligations 44.2% | $7,933,986,343 | ||||

| (Cost $7,747,338,579) | |||||

| U.S. Government 15.8% | 2,832,659,434 | ||||

| U.S. Treasury | |||||

| Bond | 2.250 | 08-15-49 | 872,308,000 | 880,622,186 | |

| Bond | 2.750 | 11-15-42 | 317,145,000 | 349,367,427 | |

| Bond | 3.000 | 02-15-47 | 197,535,000 | 229,981,667 | |

| Note (A) | 1.500 | 10-31-24 | 410,905,000 | 408,336,844 | |

| Note | 1.625 | 09-30-26 | 225,430,000 | 223,941,810 | |

| Note (A) | 1.750 | 11-15-29 | 653,766,000 | 652,054,970 | |

| Treasury Inflation Protected Security | 0.250 | 07-15-29 | 87,682,581 | 88,354,530 | |

| U.S. Government Agency 28.4% | 5,101,326,909 | ||||

| Federal Home Loan Mortgage Corp. | |||||

| 15 Yr Pass Thru | 3.000 | 07-01-32 | 75,995,839 | 78,402,893 | |

| 30 Yr Pass Thru | 3.000 | 03-01-43 | 5,633,545 | 5,832,288 | |

| 30 Yr Pass Thru | 3.000 | 04-01-43 | 6,682,358 | 6,882,602 | |

| 30 Yr Pass Thru | 3.000 | 06-01-43 | 2,244,929 | 2,316,410 | |

| 30 Yr Pass Thru | 3.000 | 12-01-45 | 23,234,251 | 23,959,534 | |

| 30 Yr Pass Thru | 3.000 | 05-01-46 | 4,246,080 | 4,379,953 | |

| 30 Yr Pass Thru | 3.000 | 10-01-46 | 7,917,476 | 8,157,206 | |

| 30 Yr Pass Thru | 3.000 | 10-01-46 | 8,225,309 | 8,433,233 | |

| 30 Yr Pass Thru | 3.000 | 10-01-46 | 13,995,987 | 14,389,150 | |

| 30 Yr Pass Thru | 3.000 | 10-01-46 | 96,392,827 | 99,341,590 | |

| 30 Yr Pass Thru | 3.000 | 10-01-46 | 23,859,126 | 24,426,157 | |

| 30 Yr Pass Thru | 3.000 | 11-01-46 | 17,493,283 | 17,984,689 | |

| 30 Yr Pass Thru | 3.000 | 12-01-46 | 82,204,941 | 84,437,101 | |

| 30 Yr Pass Thru | 3.000 | 12-01-46 | 16,828,229 | 17,353,541 | |

| 30 Yr Pass Thru | 3.000 | 04-01-47 | 48,339,836 | 49,667,543 | |

| 30 Yr Pass Thru | 3.000 | 09-01-49 | 32,352,253 | 33,030,139 | |

| 30 Yr Pass Thru | 3.000 | 10-01-49 | 37,438,792 | 38,213,315 | |

| 30 Yr Pass Thru | 3.500 | 02-01-41 | 14,759,688 | 15,574,710 | |

| 30 Yr Pass Thru | 3.500 | 01-01-42 | 1,517,176 | 1,602,851 | |

| 30 Yr Pass Thru | 3.500 | 05-01-42 | 1,361,134 | 1,432,042 | |

| 30 Yr Pass Thru | 3.500 | 06-01-42 | 5,632,664 | 5,926,094 | |

| 30 Yr Pass Thru | 3.500 | 08-01-42 | 1,468,135 | 1,544,616 | |

| 30 Yr Pass Thru | 3.500 | 09-01-42 | 1,844,292 | 1,939,793 | |

| 30 Yr Pass Thru | 3.500 | 04-01-44 | 6,560,978 | 6,943,775 | |

| 30 Yr Pass Thru | 3.500 | 05-01-45 | 14,932,013 | 15,686,558 | |

| 30 Yr Pass Thru | 3.500 | 01-01-46 | 1,858,253 | 1,951,573 | |

| 30 Yr Pass Thru | 3.500 | 08-01-46 | 78,089,479 | 82,303,929 | |

| 30 Yr Pass Thru | 3.500 | 09-01-46 | 20,621,962 | 21,593,143 | |

| 30 Yr Pass Thru | 3.500 | 09-01-46 | 10,802,565 | 11,273,497 | |

| 30 Yr Pass Thru | 3.500 | 10-01-46 | 4,525,951 | 4,723,258 | |

| SEE NOTES TO FINANCIAL STATEMENTS | SEMIANNUAL REPORT | JOHN HANCOCK BOND FUND | 9 |

| Rate (%) | Maturity date | Par value^ | Value | ||

| U.S. Government Agency (continued) | |||||

| 30 Yr Pass Thru | 3.500 | 10-01-46 | 29,151,237 | $30,742,734 | |

| 30 Yr Pass Thru | 3.500 | 11-01-46 | 9,990,272 | 10,460,759 | |

| 30 Yr Pass Thru | 3.500 | 11-01-46 | 9,576,019 | 10,050,937 | |

| 30 Yr Pass Thru | 3.500 | 12-01-46 | 16,144,915 | 16,950,659 | |

| 30 Yr Pass Thru | 3.500 | 01-01-47 | 9,328,544 | 9,826,171 | |

| 30 Yr Pass Thru | 3.500 | 02-01-47 | 15,724,133 | 16,406,671 | |

| 30 Yr Pass Thru | 3.500 | 04-01-47 | 17,195,777 | 18,118,451 | |

| 30 Yr Pass Thru | 3.500 | 09-01-47 | 52,985,577 | 55,613,370 | |

| 30 Yr Pass Thru | 3.500 | 11-01-47 | 44,504,167 | 46,419,270 | |

| 30 Yr Pass Thru | 3.500 | 11-01-47 | 15,484,116 | 16,159,138 | |

| 30 Yr Pass Thru | 3.500 | 11-01-47 | 24,676,256 | 25,583,898 | |

| 30 Yr Pass Thru | 3.500 | 06-01-49 | 55,372,724 | 57,514,824 | |

| 30 Yr Pass Thru | 4.000 | 01-01-41 | 14,845,749 | 15,882,037 | |

| 30 Yr Pass Thru | 4.000 | 03-01-42 | 7,416,773 | 7,927,538 | |

| 30 Yr Pass Thru | 4.000 | 11-01-43 | 4,752,578 | 5,106,603 | |

| 30 Yr Pass Thru | 4.000 | 02-01-44 | 1,876,503 | 2,009,249 | |

| 30 Yr Pass Thru | 4.000 | 07-01-45 | 21,752,808 | 23,339,212 | |

| 30 Yr Pass Thru | 4.000 | 01-01-47 | 13,871,197 | 14,865,467 | |

| 30 Yr Pass Thru | 4.000 | 03-01-47 | 56,416,873 | 59,878,962 | |

| 30 Yr Pass Thru | 4.000 | 03-01-47 | 16,096,301 | 16,883,872 | |

| 30 Yr Pass Thru | 4.000 | 04-01-47 | 24,541,632 | 25,817,007 | |

| 30 Yr Pass Thru | 4.000 | 05-01-47 | 18,673,194 | 19,641,263 | |

| 30 Yr Pass Thru | 4.000 | 10-01-47 | 31,845,532 | 33,455,442 | |

| 30 Yr Pass Thru | 4.000 | 11-01-47 | 24,805,328 | 25,955,457 | |

| 30 Yr Pass Thru | 4.000 | 03-01-48 | 12,711,203 | 13,323,612 | |

| 30 Yr Pass Thru | 4.000 | 07-01-48 | 56,587,682 | 60,060,253 | |

| 30 Yr Pass Thru | 4.000 | 08-01-48 | 34,728,778 | 36,773,129 | |

| 30 Yr Pass Thru | 4.500 | 11-01-39 | 2,040,655 | 2,210,873 | |

| 30 Yr Pass Thru | 4.500 | 02-01-41 | 3,357,297 | 3,633,145 | |

| 30 Yr Pass Thru | 4.500 | 03-01-41 | 2,196,732 | 2,385,461 | |

| 30 Yr Pass Thru | 4.500 | 09-01-41 | 1,370,440 | 1,482,183 | |

| 30 Yr Pass Thru | 4.500 | 10-01-41 | 1,628,843 | 1,761,656 | |

| 30 Yr Pass Thru | 4.500 | 06-01-47 | 19,331,545 | 20,536,285 | |

| 30 Yr Pass Thru | 5.500 | 11-01-39 | 4,258,539 | 4,794,833 | |

| Federal National Mortgage Association | |||||

| 15 Yr Pass Thru | 3.000 | 09-01-27 | 3,617,188 | 3,708,329 | |

| 15 Yr Pass Thru | 3.000 | 09-01-32 | 50,333,431 | 51,869,059 | |

| 15 Yr Pass Thru | 3.500 | 06-01-34 | 4,780,623 | 4,987,042 | |

| 15 Yr Pass Thru | 4.000 | 12-01-24 | 1,426,217 | 1,486,793 | |

| 30 Yr Pass Thru (B) | 3.000 | TBA | 263,405,000 | 267,129,705 | |

| 30 Yr Pass Thru | 3.000 | 07-01-42 | 4,344,644 | 4,489,987 | |

| 30 Yr Pass Thru | 3.000 | 10-01-42 | 8,550,980 | 8,788,940 | |

| 30 Yr Pass Thru | 3.000 | 10-01-42 | 4,327,281 | 4,447,702 | |

| 30 Yr Pass Thru | 3.000 | 12-01-42 | 1,998,932 | 2,062,055 | |

| 10 | JOHN HANCOCK BOND FUND | SEMIANNUAL REPORT | SEE NOTES TO FINANCIAL STATEMENTS |

| Rate (%) | Maturity date | Par value^ | Value | ||

| U.S. Government Agency (continued) | |||||

| 30 Yr Pass Thru | 3.000 | 01-01-43 | 1,503,435 | $1,546,682 | |

| 30 Yr Pass Thru | 3.000 | 03-01-43 | 1,591,087 | 1,646,303 | |

| 30 Yr Pass Thru | 3.000 | 04-01-43 | 2,593,809 | 2,674,907 | |

| 30 Yr Pass Thru | 3.000 | 05-01-43 | 2,253,496 | 2,330,995 | |

| 30 Yr Pass Thru | 3.000 | 06-01-43 | 2,258,011 | 2,324,376 | |

| 30 Yr Pass Thru | 3.000 | 07-01-43 | 25,074,765 | 25,905,762 | |

| 30 Yr Pass Thru | 3.000 | 12-01-45 | 51,294,203 | 52,561,339 | |

| 30 Yr Pass Thru | 3.000 | 08-01-46 | 55,194,113 | 56,712,823 | |

| 30 Yr Pass Thru | 3.000 | 08-01-46 | 40,879,163 | 42,003,985 | |

| 30 Yr Pass Thru | 3.000 | 09-01-46 | 5,300,776 | 5,431,723 | |

| 30 Yr Pass Thru | 3.000 | 10-01-46 | 4,167,239 | 4,270,183 | |

| 30 Yr Pass Thru | 3.000 | 10-01-46 | 36,006,350 | 36,862,069 | |

| 30 Yr Pass Thru | 3.000 | 01-01-47 | 32,625,840 | 33,503,175 | |

| 30 Yr Pass Thru | 3.000 | 02-01-47 | 17,279,902 | 17,809,372 | |

| 30 Yr Pass Thru | 3.000 | 04-01-47 | 175,484,559 | 179,655,090 | |

| 30 Yr Pass Thru | 3.000 | 10-01-47 | 38,357,449 | 39,412,885 | |

| 30 Yr Pass Thru | 3.000 | 11-01-47 | 44,656,954 | 45,885,726 | |

| 30 Yr Pass Thru | 3.000 | 11-01-48 | 153,437,533 | 157,084,099 | |

| 30 Yr Pass Thru | 3.000 | 11-01-48 | 38,048,304 | 38,988,222 | |

| 30 Yr Pass Thru | 3.000 | 12-01-48 | 23,394,794 | 23,936,168 | |

| 30 Yr Pass Thru | 3.000 | 07-01-49 | 53,592,919 | 54,364,164 | |

| 30 Yr Pass Thru | 3.000 | 09-01-49 | 44,498,996 | 45,431,397 | |

| 30 Yr Pass Thru | 3.000 | 09-01-49 | 50,795,699 | 52,066,394 | |

| 30 Yr Pass Thru | 3.000 | 10-01-49 | 33,241,115 | 33,802,584 | |

| 30 Yr Pass Thru | 3.000 | 10-01-49 | 64,183,046 | 65,267,149 | |

| 30 Yr Pass Thru | 3.000 | 10-01-49 | 64,229,146 | 65,815,818 | |

| 30 Yr Pass Thru | 3.000 | 11-01-49 | 130,612,009 | 133,389,578 | |

| 30 Yr Pass Thru | 3.000 | 11-01-49 | 35,239,920 | 36,165,525 | |

| 30 Yr Pass Thru | 3.000 | 11-01-49 | 44,165,139 | 45,228,560 | |

| 30 Yr Pass Thru | 3.000 | 11-01-49 | 38,562,279 | 39,382,337 | |

| 30 Yr Pass Thru | 3.500 | 11-01-40 | 3,166,418 | 3,339,376 | |

| 30 Yr Pass Thru | 3.500 | 06-01-42 | 3,162,063 | 3,324,902 | |

| 30 Yr Pass Thru | 3.500 | 06-01-42 | 277,558 | 291,852 | |

| 30 Yr Pass Thru | 3.500 | 08-01-42 | 5,525,966 | 5,810,540 | |

| 30 Yr Pass Thru | 3.500 | 01-01-43 | 2,543,773 | 2,672,386 | |

| 30 Yr Pass Thru | 3.500 | 02-01-43 | 794,946 | 840,853 | |

| 30 Yr Pass Thru | 3.500 | 05-01-43 | 1,456,705 | 1,539,006 | |

| 30 Yr Pass Thru | 3.500 | 06-01-43 | 19,130,368 | 20,199,232 | |

| 30 Yr Pass Thru | 3.500 | 07-01-43 | 1,479,390 | 1,564,821 | |

| 30 Yr Pass Thru | 3.500 | 07-01-43 | 5,473,092 | 5,778,888 | |

| 30 Yr Pass Thru | 3.500 | 07-01-43 | 5,689,106 | 6,006,972 | |

| 30 Yr Pass Thru | 3.500 | 01-01-45 | 4,551,757 | 4,804,653 | |

| 30 Yr Pass Thru | 3.500 | 04-01-45 | 15,115,340 | 15,879,573 | |

| 30 Yr Pass Thru | 3.500 | 04-01-45 | 4,005,519 | 4,208,038 | |

| SEE NOTES TO FINANCIAL STATEMENTS | SEMIANNUAL REPORT | JOHN HANCOCK BOND FUND | 11 |

| Rate (%) | Maturity date | Par value^ | Value | ||

| U.S. Government Agency (continued) | |||||

| 30 Yr Pass Thru | 3.500 | 04-01-45 | 16,365,675 | $17,193,125 | |

| 30 Yr Pass Thru | 3.500 | 08-01-45 | 20,508,424 | 21,532,514 | |

| 30 Yr Pass Thru | 3.500 | 01-01-46 | 38,804,892 | 40,924,516 | |

| 30 Yr Pass Thru | 3.500 | 02-01-46 | 28,585,569 | 29,861,132 | |

| 30 Yr Pass Thru | 3.500 | 07-01-46 | 34,399,499 | 35,805,496 | |

| 30 Yr Pass Thru | 3.500 | 07-01-46 | 10,770,715 | 11,278,260 | |

| 30 Yr Pass Thru | 3.500 | 08-01-46 | 39,528,707 | 41,465,519 | |

| 30 Yr Pass Thru | 3.500 | 02-01-47 | 45,614,365 | 47,835,105 | |

| 30 Yr Pass Thru | 3.500 | 03-01-47 | 50,119,523 | 52,763,208 | |

| 30 Yr Pass Thru | 3.500 | 05-01-47 | 33,329,772 | 35,119,084 | |

| 30 Yr Pass Thru | 3.500 | 07-01-47 | 63,686,744 | 67,065,969 | |

| 30 Yr Pass Thru | 3.500 | 08-01-47 | 48,730,015 | 51,148,125 | |

| 30 Yr Pass Thru | 3.500 | 09-01-47 | 12,852,897 | 13,313,963 | |

| 30 Yr Pass Thru | 3.500 | 11-01-47 | 61,069,309 | 64,061,558 | |

| 30 Yr Pass Thru | 3.500 | 11-01-47 | 8,807,782 | 9,123,740 | |

| 30 Yr Pass Thru | 3.500 | 12-01-47 | 30,909,628 | 32,337,192 | |

| 30 Yr Pass Thru | 3.500 | 01-01-48 | 52,264,368 | 54,678,203 | |

| 30 Yr Pass Thru | 3.500 | 03-01-48 | 10,179,801 | 10,723,123 | |

| 30 Yr Pass Thru | 3.500 | 03-01-48 | 42,937,317 | 44,410,500 | |

| 30 Yr Pass Thru | 3.500 | 06-01-48 | 25,738,117 | 26,999,223 | |

| 30 Yr Pass Thru | 3.500 | 03-01-49 | 8,066,389 | 8,438,936 | |

| 30 Yr Pass Thru | 3.500 | 06-01-49 | 56,529,575 | 59,016,740 | |

| 30 Yr Pass Thru | 3.500 | 06-01-49 | 27,856,931 | 28,595,073 | |

| 30 Yr Pass Thru | 3.500 | 06-01-49 | 43,177,369 | 44,645,296 | |

| 30 Yr Pass Thru | 3.500 | 07-01-49 | 26,886,639 | 27,666,287 | |

| 30 Yr Pass Thru | 3.500 | 07-01-49 | 102,880,770 | 105,864,065 | |

| 30 Yr Pass Thru | 3.500 | 09-01-49 | 21,185,878 | 21,760,494 | |

| 30 Yr Pass Thru | 4.000 | 09-01-40 | 7,176,935 | 7,677,914 | |

| 30 Yr Pass Thru | 4.000 | 09-01-40 | 10,768,634 | 11,520,328 | |

| 30 Yr Pass Thru | 4.000 | 11-01-40 | 2,627,241 | 2,808,990 | |

| 30 Yr Pass Thru | 4.000 | 12-01-40 | 1,473,124 | 1,575,033 | |

| 30 Yr Pass Thru | 4.000 | 12-01-40 | 4,144,608 | 4,431,328 | |

| 30 Yr Pass Thru | 4.000 | 01-01-41 | 4,532,983 | 4,846,570 | |

| 30 Yr Pass Thru | 4.000 | 01-01-41 | 1,755,668 | 1,881,513 | |

| 30 Yr Pass Thru | 4.000 | 02-01-41 | 1,942,376 | 2,081,604 | |

| 30 Yr Pass Thru | 4.000 | 09-01-41 | 8,423,931 | 9,006,690 | |

| 30 Yr Pass Thru | 4.000 | 09-01-41 | 2,187,393 | 2,351,019 | |

| 30 Yr Pass Thru | 4.000 | 09-01-41 | 3,714,997 | 3,992,894 | |

| 30 Yr Pass Thru | 4.000 | 10-01-41 | 2,009,684 | 2,160,016 | |

| 30 Yr Pass Thru | 4.000 | 10-01-41 | 1,533,498 | 1,639,584 | |

| 30 Yr Pass Thru | 4.000 | 10-01-41 | 2,576,345 | 2,764,235 | |

| 30 Yr Pass Thru | 4.000 | 01-01-42 | 3,330,752 | 3,578,865 | |

| 30 Yr Pass Thru | 4.000 | 03-01-42 | 1,742,660 | 1,869,206 | |

| 30 Yr Pass Thru | 4.000 | 05-01-42 | 6,323,494 | 6,755,019 | |

| 12 | JOHN HANCOCK BOND FUND | SEMIANNUAL REPORT | SEE NOTES TO FINANCIAL STATEMENTS |

| Rate (%) | Maturity date | Par value^ | Value | ||

| U.S. Government Agency (continued) | |||||

| 30 Yr Pass Thru | 4.000 | 07-01-42 | 411,005 | $441,493 | |

| 30 Yr Pass Thru | 4.000 | 09-01-43 | 7,912,086 | 8,545,975 | |

| 30 Yr Pass Thru | 4.000 | 10-01-43 | 8,833,107 | 9,504,900 | |

| 30 Yr Pass Thru | 4.000 | 10-01-43 | 3,596,007 | 3,858,260 | |

| 30 Yr Pass Thru | 4.000 | 01-01-44 | 6,157,610 | 6,625,921 | |

| 30 Yr Pass Thru | 4.000 | 12-01-45 | 20,284,275 | 21,649,487 | |

| 30 Yr Pass Thru | 4.000 | 02-01-46 | 13,010,397 | 13,707,155 | |

| 30 Yr Pass Thru | 4.000 | 04-01-46 | 13,526,421 | 14,250,814 | |

| 30 Yr Pass Thru | 4.000 | 06-01-46 | 9,217,722 | 9,711,368 | |

| 30 Yr Pass Thru | 4.000 | 07-01-46 | 22,617,380 | 23,828,631 | |

| 30 Yr Pass Thru | 4.000 | 10-01-46 | 5,219,646 | 5,492,655 | |

| 30 Yr Pass Thru | 4.000 | 01-01-47 | 17,328,874 | 18,230,912 | |

| 30 Yr Pass Thru | 4.000 | 03-01-47 | 27,286,476 | 28,943,898 | |

| 30 Yr Pass Thru | 4.000 | 04-01-47 | 23,655,707 | 24,887,081 | |

| 30 Yr Pass Thru | 4.000 | 08-01-47 | 35,288,740 | 36,980,094 | |

| 30 Yr Pass Thru | 4.000 | 11-01-47 | 8,384,077 | 8,783,821 | |

| 30 Yr Pass Thru | 4.000 | 12-01-47 | 15,215,580 | 16,192,101 | |

| 30 Yr Pass Thru | 4.000 | 12-01-47 | 13,526,740 | 14,170,836 | |

| 30 Yr Pass Thru | 4.000 | 04-01-48 | 78,926,169 | 83,942,243 | |

| 30 Yr Pass Thru | 4.000 | 07-01-48 | 27,437,645 | 28,569,215 | |

| 30 Yr Pass Thru | 4.000 | 09-01-48 | 50,142,404 | 53,172,460 | |

| 30 Yr Pass Thru | 4.000 | 10-01-48 | 48,650,506 | 51,499,188 | |

| 30 Yr Pass Thru | 4.000 | 10-01-48 | 29,040,401 | 30,722,683 | |

| 30 Yr Pass Thru | 4.000 | 10-01-48 | 34,327,540 | 36,401,919 | |

| 30 Yr Pass Thru | 4.000 | 01-01-49 | 23,927,611 | 25,022,096 | |

| 30 Yr Pass Thru | 4.000 | 02-01-49 | 32,455,003 | 33,939,543 | |

| 30 Yr Pass Thru | 4.500 | 11-01-39 | 4,180,901 | 4,529,506 | |

| 30 Yr Pass Thru | 4.500 | 08-01-40 | 3,141,715 | 3,400,727 | |

| 30 Yr Pass Thru | 4.500 | 08-01-40 | 1,893,822 | 2,049,954 | |

| 30 Yr Pass Thru | 4.500 | 02-01-41 | 7,119,421 | 7,704,140 | |

| 30 Yr Pass Thru | 4.500 | 05-01-41 | 4,099,979 | 4,436,711 | |

| 30 Yr Pass Thru | 4.500 | 05-01-41 | 4,856,422 | 5,258,316 | |

| 30 Yr Pass Thru | 4.500 | 06-01-41 | 6,048,038 | 6,540,985 | |

| 30 Yr Pass Thru | 4.500 | 07-01-41 | 4,498,371 | 4,865,012 | |

| 30 Yr Pass Thru | 4.500 | 08-01-41 | 2,951,244 | 3,191,785 | |

| 30 Yr Pass Thru | 4.500 | 05-01-42 | 6,768,455 | 7,320,119 | |

| 30 Yr Pass Thru | 4.500 | 11-01-42 | 4,532,822 | 4,917,852 | |

| 30 Yr Pass Thru | 4.500 | 01-01-43 | 1,341,800 | 1,451,164 | |

| 30 Yr Pass Thru | 4.500 | 10-01-45 | 15,686,497 | 16,916,007 | |

| 30 Yr Pass Thru | 4.500 | 05-01-46 | 9,044,266 | 9,634,451 | |

| 30 Yr Pass Thru | 4.500 | 04-01-48 | 1,644,410 | 1,755,827 | |

| 30 Yr Pass Thru | 4.500 | 04-01-48 | 16,380,918 | 17,378,192 | |

| 30 Yr Pass Thru | 4.500 | 05-01-48 | 45,297,438 | 48,366,575 | |

| 30 Yr Pass Thru | 4.500 | 06-01-48 | 50,322,184 | 53,731,774 | |

| SEE NOTES TO FINANCIAL STATEMENTS | SEMIANNUAL REPORT | JOHN HANCOCK BOND FUND | 13 |

| Rate (%) | Maturity date | Par value^ | Value | ||

| U.S. Government Agency (continued) | |||||

| 30 Yr Pass Thru | 4.500 | 06-01-48 | 41,243,879 | $44,205,920 | |

| 30 Yr Pass Thru (6 month LIBOR + 2.122%) (C) | 4.747 | 07-01-33 | 389 | 406 | |

| 30 Yr Pass Thru | 7.000 | 09-01-31 | 130 | 151 | |

| 30 Yr Pass Thru | 7.000 | 09-01-31 | 130 | 150 | |

| 30 Yr Pass Thru | 7.000 | 09-01-31 | 2,241 | 2,592 | |

| 30 Yr Pass Thru | 7.000 | 01-01-32 | 84 | 98 | |

| 30 Yr Pass Thru | 7.000 | 05-01-32 | 118 | 138 | |

| 30 Yr Pass Thru | 7.000 | 06-01-32 | 105 | 121 | |

| 30 Yr Pass Thru | 7.500 | 09-01-29 | 59 | 68 | |

| 30 Yr Pass Thru | 7.500 | 12-01-29 | 67 | 77 | |

| 30 Yr Pass Thru | 7.500 | 12-01-30 | 15 | 17 | |

| 30 Yr Pass Thru | 7.500 | 01-01-31 | 29 | 33 | |

| 30 Yr Pass Thru | 7.500 | 05-01-31 | 336 | 390 | |

| 30 Yr Pass Thru | 7.500 | 08-01-31 | 120 | 136 | |

| Government National Mortgage Association | |||||

| 30 Yr Pass Thru | 4.000 | 02-15-41 | 1,909,322 | 2,044,987 | |

| 30 Yr Pass Thru | 5.000 | 04-15-35 | 3,810 | 4,180 | |

| 30 Yr Pass Thru | 5.000 | 04-15-35 | 1,700 | 1,862 | |

| 30 Yr Pass Thru | 5.500 | 03-15-35 | 4,409 | 4,913 | |

| 30 Yr Pass Thru | 6.000 | 03-15-33 | 2,419 | 2,729 | |

| 30 Yr Pass Thru | 6.000 | 06-15-33 | 905 | 1,016 | |

| 30 Yr Pass Thru | 6.500 | 09-15-28 | 351 | 391 | |

| 30 Yr Pass Thru | 6.500 | 09-15-29 | 165 | 184 | |

| 30 Yr Pass Thru | 6.500 | 08-15-31 | 291 | 329 | |

| 30 Yr Pass Thru | 7.000 | 04-15-29 | 727 | 822 | |

| 30 Yr Pass Thru | 8.000 | 10-15-26 | 360 | 401 | |

| Foreign government obligations 0.4% | $79,082,762 | ||||

| (Cost $71,988,633) | |||||

| Qatar 0.2% | 43,801,586 | ||||

| State of Qatar | |||||

| Bond (D) | 3.375 | 03-14-24 | 23,339,000 | 24,377,586 | |

| Bond (D) | 5.103 | 04-23-48 | 15,175,000 | 19,424,000 | |

| Saudi Arabia 0.2% | 35,281,176 | ||||

| Kingdom of Saudi Arabia Bond (D) | 4.375 | 04-16-29 | 31,580,000 | 35,281,176 | |

| Corporate bonds 40.5% | $7,282,154,121 | ||||

| (Cost $6,993,539,540) | |||||

| Communication services 4.5% | 816,350,131 | ||||

| Diversified telecommunication services 1.7% | |||||

| AT&T, Inc. | 3.400 | 05-15-25 | 32,345,000 | 33,771,017 | |

| AT&T, Inc. | 3.800 | 02-15-27 | 17,626,000 | 18,739,758 | |

| 14 | JOHN HANCOCK BOND FUND | SEMIANNUAL REPORT | SEE NOTES TO FINANCIAL STATEMENTS |

| Rate (%) | Maturity date | Par value^ | Value | ||

| Communication services (continued) | |||||

| Diversified telecommunication services (continued) | |||||

| C&W Senior Financing DAC (A)(D) | 6.875 | 09-15-27 | 15,850,000 | $16,731,656 | |

| Cincinnati Bell, Inc. (A)(D) | 7.000 | 07-15-24 | 22,599,000 | 21,158,314 | |

| GCI LLC (D) | 6.625 | 06-15-24 | 7,997,000 | 8,656,753 | |

| GCI LLC | 6.875 | 04-15-25 | 10,150,000 | 10,594,063 | |

| Level 3 Financing, Inc. (D) | 3.400 | 03-01-27 | 21,423,000 | 21,441,210 | |

| Liquid Telecommunications Financing PLC (D) | 8.500 | 07-13-22 | 12,325,000 | 12,318,789 | |

| Radiate Holdco LLC (A)(D) | 6.625 | 02-15-25 | 13,365,000 | 13,498,650 | |

| Radiate Holdco LLC (D) | 6.875 | 02-15-23 | 4,594,000 | 4,685,880 | |

| Telecom Argentina SA (A)(D) | 6.500 | 06-15-21 | 9,120,000 | 8,641,200 | |

| Telecom Argentina SA (D) | 8.000 | 07-18-26 | 10,858,000 | 9,500,750 | |

| Telecom Italia Capital SA | 7.200 | 07-18-36 | 19,715,000 | 23,077,393 | |

| Telecom Italia SpA (D) | 5.303 | 05-30-24 | 14,870,000 | 15,989,265 | |

| UPCB Finance IV, Ltd. (D) | 5.375 | 01-15-25 | 11,781,000 | 12,104,978 | |

| Verizon Communications, Inc. | 4.400 | 11-01-34 | 16,224,000 | 18,828,779 | |

| Verizon Communications, Inc. | 4.862 | 08-21-46 | 39,929,000 | 49,938,814 | |

| Entertainment 0.4% | |||||

| Activision Blizzard, Inc. | 3.400 | 09-15-26 | 9,978,000 | 10,493,927 | |

| Lions Gate Capital Holdings LLC (A)(D) | 5.875 | 11-01-24 | 8,795,000 | 8,467,122 | |

| Netflix, Inc. | 4.875 | 04-15-28 | 14,130,000 | 14,473,076 | |

| Netflix, Inc. (A)(D) | 4.875 | 06-15-30 | 13,241,000 | 13,340,308 | |

| Netflix, Inc. (D) | 5.375 | 11-15-29 | 5,283,000 | 5,560,886 | |

| Netflix, Inc. | 5.875 | 11-15-28 | 23,170,000 | 25,313,225 | |

| Media 1.8% | |||||

| Altice Financing SA (D) | 6.625 | 02-15-23 | 11,370,000 | 11,625,825 | |

| Altice Luxembourg SA (D) | 10.500 | 05-15-27 | 4,417,000 | 5,008,878 | |

| Cablevision Systems Corp. | 5.875 | 09-15-22 | 11,420,000 | 12,305,050 | |

| CBS Corp. | 3.700 | 08-15-24 | 13,500,000 | 14,173,181 | |

| Charter Communications Operating LLC | 4.200 | 03-15-28 | 33,590,000 | 35,606,557 | |

| Charter Communications Operating LLC | 4.800 | 03-01-50 | 21,312,000 | 22,216,760 | |

| Charter Communications Operating LLC | 5.750 | 04-01-48 | 37,447,000 | 43,362,174 | |

| Charter Communications Operating LLC | 6.484 | 10-23-45 | 31,930,000 | 39,581,846 | |

| CSC Holdings LLC (D) | 5.375 | 02-01-28 | 7,545,000 | 7,978,838 | |

| CSC Holdings LLC (D) | 5.500 | 04-15-27 | 9,225,000 | 9,813,094 | |

| CSC Holdings LLC (D) | 5.750 | 01-15-30 | 11,119,000 | 11,716,646 | |

| CSC Holdings LLC (D) | 7.500 | 04-01-28 | 11,570,000 | 13,030,713 | |

| LCPR Senior Secured Financing DAC (D) | 6.750 | 10-15-27 | 9,115,000 | 9,399,844 | |

| MDC Partners, Inc. (D) | 6.500 | 05-01-24 | 22,212,000 | 20,212,920 | |

| National CineMedia LLC (D) | 5.875 | 04-15-28 | 8,680,000 | 9,048,900 | |

| Sirius XM Radio, Inc. (D) | 5.000 | 08-01-27 | 28,619,000 | 30,121,498 | |

| Sirius XM Radio, Inc. (D) | 5.375 | 07-15-26 | 15,345,000 | 16,208,156 | |

| WMG Acquisition Corp. (D) | 4.875 | 11-01-24 | 6,551,000 | 6,763,908 | |

| WMG Acquisition Corp. (D) | 5.500 | 04-15-26 | 9,627,000 | 10,156,485 | |

| SEE NOTES TO FINANCIAL STATEMENTS | SEMIANNUAL REPORT | JOHN HANCOCK BOND FUND | 15 |

| Rate (%) | Maturity date | Par value^ | Value | ||

| Communication services (continued) | |||||

| Wireless telecommunication services 0.6% | |||||

| CC Holdings GS V LLC | 3.849 | 04-15-23 | 15,526,000 | $16,291,805 | |

| Comunicaciones Celulares SA Via Comcel Trust (D) | 6.875 | 02-06-24 | 8,530,000 | 8,753,913 | |

| Millicom International Cellular SA (A)(D) | 5.125 | 01-15-28 | 4,100,000 | 4,187,125 | |

| MTN Mauritius Investments, Ltd. (D) | 4.755 | 11-11-24 | 12,421,000 | 12,722,997 | |

| Oztel Holdings SPC, Ltd. (D) | 6.625 | 04-24-28 | 12,515,000 | 13,081,036 | |

| Sprint Corp. | 7.875 | 09-15-23 | 15,206,000 | 16,717,096 | |

| Telefonica Celular del Paraguay SA (D) | 5.875 | 04-15-27 | 6,691,000 | 7,125,915 | |

| Vodafone Group PLC (7.000% to 1-4-29, then 5 Year U.S. Swap Rate + 4.873%) | 7.000 | 04-04-79 | 27,478,000 | 31,813,158 | |

| Consumer discretionary 4.0% | 723,935,227 | ||||

| Automobiles 1.6% | |||||

| Daimler Finance North America LLC (A)(D) | 2.700 | 06-14-24 | 13,695,000 | 13,824,118 | |

| Daimler Finance North America LLC (D) | 3.500 | 08-03-25 | 12,585,000 | 13,091,272 | |

| Ford Motor Credit Company LLC | 4.134 | 08-04-25 | 58,761,000 | 58,736,018 | |

| Ford Motor Credit Company LLC | 5.113 | 05-03-29 | 32,918,000 | 33,314,323 | |

| Ford Motor Credit Company LLC | 5.875 | 08-02-21 | 41,355,000 | 43,298,036 | |

| General Motors Company | 4.875 | 10-02-23 | 31,134,000 | 33,569,667 | |

| General Motors Financial Company, Inc. | 4.000 | 01-15-25 | 45,989,000 | 47,660,072 | |

| General Motors Financial Company, Inc. | 4.300 | 07-13-25 | 22,335,000 | 23,523,257 | |

| JB Poindexter & Company, Inc. (D) | 7.125 | 04-15-26 | 5,212,000 | 5,436,116 | |

| Mclaren Finance PLC (D) | 5.750 | 08-01-22 | 3,425,000 | 3,281,151 | |

| Nissan Motor Acceptance Corp. (D) | 3.450 | 03-15-23 | 13,440,000 | 13,810,182 | |

| Diversified consumer services 0.2% | |||||

| GEMS MENASA Cayman, Ltd. (D) | 7.125 | 07-31-26 | 6,680,000 | 7,030,700 | |

| Laureate Education, Inc. (D) | 8.250 | 05-01-25 | 8,575,000 | 9,261,000 | |

| Sotheby's (A)(D) | 7.375 | 10-15-27 | 15,799,000 | 15,423,774 | |

| Hotels, restaurants and leisure 0.7% | |||||

| CCM Merger, Inc. (D) | 6.000 | 03-15-22 | 10,710,000 | 10,924,200 | |

| Connect Finco Sarl (D) | 6.750 | 10-01-26 | 23,202,000 | 23,811,053 | |

| Eldorado Resorts, Inc. | 6.000 | 09-15-26 | 6,670,000 | 7,342,336 | |

| Eldorado Resorts, Inc. | 7.000 | 08-01-23 | 4,535,000 | 4,739,075 | |

| Hilton Domestic Operating Company, Inc. | 4.875 | 01-15-30 | 5,741,000 | 6,099,813 | |

| Hilton Domestic Operating Company, Inc. | 5.125 | 05-01-26 | 2,667,000 | 2,807,018 | |

| International Game Technology PLC (D) | 6.500 | 02-15-25 | 11,430,000 | 12,773,025 | |

| Jacobs Entertainment, Inc. (D) | 7.875 | 02-01-24 | 11,775,000 | 12,481,500 | |

| Resorts World Las Vegas LLC (D) | 4.625 | 04-16-29 | 16,090,000 | 16,762,769 | |

| Twin River Worldwide Holdings, Inc. (A)(D) | 6.750 | 06-01-27 | 13,773,000 | 14,186,190 | |

| Waterford Gaming LLC (D)(E)(F) | 8.625 | 09-15-14 | 440,015 | 0 | |

| Yum! Brands, Inc. (D) | 4.750 | 01-15-30 | 6,690,000 | 6,924,150 | |

| Internet and direct marketing retail 1.3% | |||||

| Amazon.com, Inc. | 3.150 | 08-22-27 | 38,826,000 | 41,255,383 | |

| 16 | JOHN HANCOCK BOND FUND | SEMIANNUAL REPORT | SEE NOTES TO FINANCIAL STATEMENTS |

| Rate (%) | Maturity date | Par value^ | Value | ||

| Consumer discretionary (continued) | |||||

| Internet and direct marketing retail (continued) | |||||

| Amazon.com, Inc. | 4.050 | 08-22-47 | 21,490,000 | $25,680,413 | |

| Expedia Group, Inc. (D) | 3.250 | 02-15-30 | 26,905,000 | 26,228,666 | |

| Expedia Group, Inc. | 3.800 | 02-15-28 | 38,185,000 | 39,503,023 | |

| Expedia Group, Inc. | 5.000 | 02-15-26 | 31,402,000 | 34,858,066 | |

| Prosus NV (D) | 4.850 | 07-06-27 | 4,575,000 | 4,989,037 | |

| Prosus NV (D) | 5.500 | 07-21-25 | 19,530,000 | 21,729,583 | |

| QVC, Inc. | 4.375 | 03-15-23 | 18,108,000 | 18,747,562 | |

| QVC, Inc. | 5.125 | 07-02-22 | 8,874,000 | 9,332,385 | |

| QVC, Inc. | 5.450 | 08-15-34 | 10,129,000 | 10,038,398 | |

| Leisure products 0.0% | |||||

| Diamond Sports Group LLC (A)(D) | 6.625 | 08-15-27 | 8,665,000 | 8,445,862 | |

| Multiline retail 0.2% | |||||

| Dollar Tree, Inc. | 4.200 | 05-15-28 | 40,219,000 | 43,016,034 | |

| Consumer staples 0.8% | 134,708,719 | ||||

| Beverages 0.2% | |||||

| Anheuser-Busch InBev Worldwide, Inc. | 4.600 | 04-15-48 | 21,469,000 | 24,909,500 | |

| Food and staples retailing 0.1% | |||||

| Alimentation Couche-Tard, Inc. (D) | 2.700 | 07-26-22 | 13,623,000 | 13,753,684 | |

| Simmons Foods, Inc. (A)(D) | 5.750 | 11-01-24 | 9,570,000 | 9,258,975 | |

| Food products 0.3% | |||||

| JBS Investments II GmbH (A)(D) | 5.750 | 01-15-28 | 25,669,000 | 27,016,623 | |

| Kraft Heinz Foods Company (D) | 4.875 | 02-15-25 | 13,957,000 | 14,352,336 | |

| NBM US Holdings, Inc. (D) | 6.625 | 08-06-29 | 8,240,000 | 8,675,072 | |

| Post Holdings, Inc. (D) | 5.500 | 12-15-29 | 8,311,000 | 8,705,773 | |

| Personal products 0.2% | |||||

| Natura Cosmeticos SA (A)(D) | 5.375 | 02-01-23 | 19,995,000 | 20,869,781 | |

| Walnut Bidco PLC (D) | 9.125 | 08-01-24 | 6,925,000 | 7,166,975 | |

| Energy 4.9% | 877,742,937 | ||||

| Energy equipment and services 0.4% | |||||

| Archrock Partners LP | 6.000 | 10-01-22 | 15,668,000 | 15,707,170 | |

| CSI Compressco LP (A) | 7.250 | 08-15-22 | 22,194,000 | 19,752,660 | |

| CSI Compressco LP (D) | 7.500 | 04-01-25 | 16,408,000 | 15,546,580 | |

| Inkia Energy, Ltd. (D) | 5.875 | 11-09-27 | 4,600,000 | 4,738,046 | |

| Tervita Corp. (D) | 7.625 | 12-01-21 | 11,842,000 | 11,840,697 | |

| Oil, gas and consumable fuels 4.5% | |||||

| Cheniere Corpus Christi Holdings LLC | 5.125 | 06-30-27 | 7,135,000 | 7,847,002 | |

| Cheniere Energy Partners LP (D) | 4.500 | 10-01-29 | 18,715,000 | 18,814,190 | |

| Cimarex Energy Company | 4.375 | 06-01-24 | 12,404,000 | 13,000,260 | |

| Colorado Interstate Gas Company LLC (D) | 4.150 | 08-15-26 | 9,460,000 | 9,871,488 | |

| Continental Resources, Inc. | 5.000 | 09-15-22 | 20,221,000 | 20,336,017 | |

| SEE NOTES TO FINANCIAL STATEMENTS | SEMIANNUAL REPORT | JOHN HANCOCK BOND FUND | 17 |

| Rate (%) | Maturity date | Par value^ | Value | ||

| Energy (continued) | |||||

| Oil, gas and consumable fuels (continued) | |||||

| DCP Midstream LP (7.375% to 12-15-22, then 3 month LIBOR + 5.148%) (A)(G) | 7.375 | 12-15-22 | 27,189,000 | $25,965,495 | |

| DCP Midstream Operating LP | 5.125 | 05-15-29 | 5,850,000 | 5,937,750 | |

| DCP Midstream Operating LP (5.850% to 5-21-23, then 3 month LIBOR + 3.850%) (D) | 5.850 | 05-21-43 | 27,700,000 | 25,484,000 | |

| Diamondback Energy, Inc. | 4.750 | 11-01-24 | 13,514,000 | 14,005,910 | |

| Enable Midstream Partners LP | 3.900 | 05-15-24 | 19,802,000 | 19,956,697 | |

| Enable Midstream Partners LP | 4.950 | 05-15-28 | 18,636,000 | 18,631,940 | |

| Enbridge, Inc. (5.500% to 7-15-27, then 3 month LIBOR + 3.418%) | 5.500 | 07-15-77 | 20,627,000 | 21,142,675 | |

| Enbridge, Inc. (6.250% to 3-1-28, then 3 month LIBOR + 3.641%) | 6.250 | 03-01-78 | 19,207,000 | 20,599,508 | |

| Energy Transfer Operating LP | 4.200 | 04-15-27 | 8,447,000 | 8,657,447 | |

| Energy Transfer Operating LP | 4.250 | 03-15-23 | 24,613,000 | 25,586,015 | |

| Energy Transfer Operating LP | 5.150 | 03-15-45 | 16,520,000 | 16,760,116 | |

| Energy Transfer Operating LP | 5.875 | 01-15-24 | 17,180,000 | 18,923,616 | |

| Enterprise Products Operating LLC (5.250% to 8-16-27, then 3 month LIBOR + 3.033%) | 5.250 | 08-16-77 | 34,782,000 | 34,955,910 | |

| Husky Energy, Inc. | 3.950 | 04-15-22 | 17,036,000 | 17,580,379 | |

| Kinder Morgan Energy Partners LP | 7.750 | 03-15-32 | 12,590,000 | 16,924,338 | |

| MPLX LP | 4.000 | 03-15-28 | 17,215,000 | 17,641,034 | |

| MPLX LP (D) | 4.250 | 12-01-27 | 7,928,000 | 8,312,827 | |

| MPLX LP (D) | 5.250 | 01-15-25 | 10,432,000 | 10,951,999 | |

| MPLX LP (D) | 6.375 | 05-01-24 | 13,574,000 | 14,199,109 | |

| MPLX LP (6.875% to 2-15-23, then 3 month LIBOR + 4.652%) (G) | 6.875 | 02-15-23 | 44,303,000 | 44,413,758 | |

| Murphy Oil Corp. | 5.750 | 08-15-25 | 9,531,000 | 9,757,171 | |

| Newfield Exploration Company | 5.625 | 07-01-24 | 16,774,000 | 18,296,859 | |

| ONEOK Partners LP | 4.900 | 03-15-25 | 8,673,000 | 9,478,597 | |

| Parsley Energy LLC (D) | 5.625 | 10-15-27 | 13,410,000 | 13,862,588 | |

| Petrobras Global Finance BV (D) | 5.093 | 01-15-30 | 27,279,000 | 28,561,113 | |

| Petrobras Global Finance BV | 6.900 | 03-19-49 | 10,625,000 | 12,151,813 | |

| Sabine Pass Liquefaction LLC | 4.200 | 03-15-28 | 13,415,000 | 14,123,302 | |

| Sabine Pass Liquefaction LLC | 5.000 | 03-15-27 | 15,534,000 | 17,005,417 | |

| Sabine Pass Liquefaction LLC | 5.875 | 06-30-26 | 26,740,000 | 30,587,027 | |

| Sunoco Logistics Partners Operations LP | 3.900 | 07-15-26 | 24,214,000 | 24,854,532 | |

| Sunoco Logistics Partners Operations LP | 5.400 | 10-01-47 | 15,951,000 | 16,796,699 | |

| Targa Resources Partners LP | 5.875 | 04-15-26 | 26,310,000 | 27,683,382 | |

| Teekay Offshore Partners LP (A)(D) | 8.500 | 07-15-23 | 17,445,000 | 17,445,000 | |

| The Williams Companies, Inc. | 3.750 | 06-15-27 | 21,304,000 | 21,811,274 | |

| The Williams Companies, Inc. | 4.550 | 06-24-24 | 43,752,000 | 46,836,229 | |

| The Williams Companies, Inc. | 5.750 | 06-24-44 | 7,401,000 | 8,482,580 | |

| TransCanada PipeLines, Ltd. | 4.250 | 05-15-28 | 13,565,000 | 14,929,075 | |

| 18 | JOHN HANCOCK BOND FUND | SEMIANNUAL REPORT | SEE NOTES TO FINANCIAL STATEMENTS |

| Rate (%) | Maturity date | Par value^ | Value | ||

| Energy (continued) | |||||

| Oil, gas and consumable fuels (continued) | |||||

| WPX Energy, Inc. | 5.250 | 09-15-24 | 5,040,000 | $5,150,729 | |

| WPX Energy, Inc. | 5.250 | 10-15-27 | 5,763,000 | 5,762,712 | |

| YPF SA (D) | 8.500 | 07-28-25 | 12,258,000 | 10,082,205 | |

| Financials 10.7% | 1,927,606,511 | ||||

| Banks 6.1% | |||||

| Australia & New Zealand Banking Group, Ltd. (6.750% to 6-15-26, then 5 Year U.S. ISDAFIX + 5.168%) (A)(D)(G) | 6.750 | 06-15-26 | 10,920,000 | 12,380,550 | |

| Banco Santander SA | 4.379 | 04-12-28 | 18,430,000 | 20,198,674 | |

| Bank of America Corp. | 3.950 | 04-21-25 | 23,346,000 | 24,820,794 | |

| Bank of America Corp. | 4.200 | 08-26-24 | 10,787,000 | 11,558,394 | |

| Bank of America Corp. | 4.450 | 03-03-26 | 29,257,000 | 32,118,930 | |

| Bank of America Corp. (6.300% to 3-10-26, then 3 month LIBOR + 4.553%) (G) | 6.300 | 03-10-26 | 32,565,000 | 37,286,925 | |

| Barclays Bank PLC (D) | 10.179 | 06-12-21 | 8,040,000 | 8,963,936 | |

| Barclays PLC | 4.375 | 01-12-26 | 15,935,000 | 17,087,016 | |

| BPCE SA (D) | 4.500 | 03-15-25 | 20,836,000 | 22,390,382 | |

| BPCE SA (D) | 5.700 | 10-22-23 | 23,245,000 | 25,639,154 | |

| Citigroup, Inc. | 3.200 | 10-21-26 | 29,535,000 | 30,646,998 | |

| Citigroup, Inc. | 4.600 | 03-09-26 | 34,598,000 | 38,079,616 | |

| Citigroup, Inc. | 5.500 | 09-13-25 | 10,611,000 | 12,130,962 | |

| Citigroup, Inc. (6.250% to 8-15-26, then 3 month LIBOR + 4.517%) (A)(G) | 6.250 | 08-15-26 | 24,848,000 | 28,202,480 | |

| Credit Agricole SA (7.875% to 1-23-24, then 5 Year U.S. Swap Rate + 4.898%) (D)(G) | 7.875 | 01-23-24 | 15,155,000 | 17,181,314 | |

| Danske Bank A/S (D) | 5.000 | 01-12-22 | 17,629,000 | 18,507,987 | |

| Discover Bank | 2.450 | 09-12-24 | 19,370,000 | 19,337,583 | |

| Fifth Third Bancorp (5.100% to 6-30-23, then 3 month LIBOR + 3.033%) (G) | 5.100 | 06-30-23 | 12,369,000 | 12,733,391 | |

| Freedom Mortgage Corp. (D) | 8.125 | 11-15-24 | 14,529,000 | 14,320,218 | |

| Freedom Mortgage Corp. (D) | 8.250 | 04-15-25 | 5,630,000 | 5,587,775 | |

| HSBC Holdings PLC (3.950% to 5-18-23, then 3 month LIBOR + 0.987%) | 3.950 | 05-18-24 | 30,775,000 | 32,219,976 | |

| HSBC Holdings PLC (6.375% to 9-17-24, then 5 Year U.S. ISDAFIX + 3.705%) (A)(G) | 6.375 | 09-17-24 | 6,870,000 | 7,307,963 | |

| HSBC Holdings PLC (6.875% to 6-1-21, then 5 Year U.S. ISDAFIX + 5.514%) (G) | 6.875 | 06-01-21 | 17,805,000 | 18,606,225 | |

| ING Bank NV (D) | 5.800 | 09-25-23 | 18,634,000 | 20,654,915 | |

| ING Groep NV | 3.550 | 04-09-24 | 17,692,000 | 18,445,628 | |

| ING Groep NV (6.500% to 4-16-25, then 5 Year U.S. Swap Rate + 4.446%) (G) | 6.500 | 04-16-25 | 7,245,000 | 7,752,150 | |

| JPMorgan Chase & Co. | 2.950 | 10-01-26 | 34,327,000 | 35,414,234 | |

| SEE NOTES TO FINANCIAL STATEMENTS | SEMIANNUAL REPORT | JOHN HANCOCK BOND FUND | 19 |

| Rate (%) | Maturity date | Par value^ | Value | ||

| Financials (continued) | |||||

| Banks (continued) | |||||

| JPMorgan Chase & Co. (3.960% to 1-29-26, then 3 month LIBOR + 1.245%) | 3.960 | 01-29-27 | 25,533,000 | $27,595,091 | |

| JPMorgan Chase & Co. (6.750% to 2-1-24, then 3 month LIBOR + 3.780%) (G) | 6.750 | 02-01-24 | 27,445,000 | 30,909,931 | |

| Lloyds Banking Group PLC | 4.450 | 05-08-25 | 47,565,000 | 51,784,152 | |

| Lloyds Banking Group PLC (7.500% to 6-27-24, then 5 Year U.S. Swap Rate + 4.760%) (G) | 7.500 | 06-27-24 | 18,190,000 | 20,077,213 | |

| M&T Bank Corp. (5.125% to 11-1-26, then 3 month LIBOR + 3.520%) (G) | 5.125 | 11-01-26 | 12,892,000 | 13,810,555 | |

| Manufacturers & Traders Trust Company (3 month LIBOR + 0.640%) (C) | 2.547 | 12-01-21 | 9,230,000 | 9,239,798 | |

| Santander Holdings USA, Inc. (D) | 3.244 | 10-05-26 | 39,550,000 | 39,726,800 | |

| Santander Holdings USA, Inc. | 3.400 | 01-18-23 | 18,107,000 | 18,555,915 | |

| Santander Holdings USA, Inc. | 3.500 | 06-07-24 | 38,050,000 | 39,068,060 | |

| Santander Holdings USA, Inc. | 4.400 | 07-13-27 | 9,667,000 | 10,382,242 | |

| Santander UK Group Holdings PLC (D) | 4.750 | 09-15-25 | 14,920,000 | 15,910,021 | |

| Societe Generale SA (7.375% to 9-13-21, then 5 Year U.S. Swap Rate + 6.238%) (A)(D)(G) | 7.375 | 09-13-21 | 17,145,000 | 18,127,409 | |

| The PNC Financial Services Group, Inc. | 2.200 | 11-01-24 | 30,950,000 | 30,870,024 | |

| The PNC Financial Services Group, Inc. | 3.500 | 01-23-24 | 14,603,000 | 15,375,885 | |

| The PNC Financial Services Group, Inc. (4.850% to 6-1-23, then 3 month LIBOR + 3.040%) (G) | 4.850 | 06-01-23 | 15,854,000 | 16,408,890 | |

| The PNC Financial Services Group, Inc. (6.750% to 8-1-21, then 3 month LIBOR + 3.678%) (G) | 6.750 | 08-01-21 | 29,319,000 | 30,922,749 | |

| The Royal Bank of Scotland Group PLC | 3.875 | 09-12-23 | 24,580,000 | 25,570,271 | |

| The Royal Bank of Scotland Group PLC (3.754% to 11-1-24, then 5 Year CMT + 2.100%) | 3.754 | 11-01-29 | 9,658,000 | 9,743,883 | |

| The Royal Bank of Scotland Group PLC (8.625% to 8-15-21, then 5 Year U.S. Swap Rate + 7.598%) (G) | 8.625 | 08-15-21 | 37,076,000 | 40,019,093 | |

| The Toronto-Dominion Bank | 3.250 | 03-11-24 | 22,739,000 | 23,723,352 | |

| Wells Fargo & Company (3 month LIBOR + 3.770%) (A)(C)(G) | 5.889 | 03-15-20 | 8,592,000 | 8,722,598 | |

| Wells Fargo & Company (5.875% to 6-15-25, then 3 month LIBOR + 3.990%) (G) | 5.875 | 06-15-25 | 54,681,000 | 60,739,096 | |

| Capital markets 1.2% | |||||

| Ares Capital Corp. | 3.625 | 01-19-22 | 18,302,000 | 18,588,525 | |

| Cantor Fitzgerald LP (D) | 4.875 | 05-01-24 | 25,325,000 | 26,943,794 | |

| 20 | JOHN HANCOCK BOND FUND | SEMIANNUAL REPORT | SEE NOTES TO FINANCIAL STATEMENTS |

| Rate (%) | Maturity date | Par value^ | Value | ||

| Financials (continued) | |||||

| Capital markets (continued) | |||||

| Credit Suisse Group AG (7.500% to 12-11-23, then 5 Year U.S. Swap Rate + 4.598%) (A)(D)(G) | 7.500 | 12-11-23 | 10,145,000 | $11,337,038 | |

| Credit Suisse Group AG (7.500% to 7-17-23, then 5 Year U.S. Swap Rate + 4.600%) (D)(G) | 7.500 | 07-17-23 | 17,955,000 | 19,554,791 | |

| Lazard Group LLC | 4.375 | 03-11-29 | 14,025,000 | 15,295,527 | |

| Macquarie Bank, Ltd. (D) | 4.875 | 06-10-25 | 20,345,000 | 21,924,307 | |

| Morgan Stanley | 3.875 | 01-27-26 | 19,031,000 | 20,508,251 | |

| Stearns Holdings LLC (D) | 5.000 | 11-05-24 | 63,051 | 43,505 | |

| Stifel Financial Corp. | 4.250 | 07-18-24 | 12,983,000 | 13,750,301 | |

| The Goldman Sachs Group, Inc. | 3.850 | 01-26-27 | 46,391,000 | 49,399,388 | |

| UBS Group AG (7.000% to 1-31-24, then 5 Year U.S. Swap Rate + 4.344%) (D)(G) | 7.000 | 01-31-24 | 16,288,000 | 17,652,120 | |

| Consumer finance 0.8% | |||||

| Ally Financial, Inc. | 5.125 | 09-30-24 | 27,788,000 | 30,532,065 | |

| Capital One Financial Corp. | 3.500 | 06-15-23 | 15,740,000 | 16,340,144 | |

| Capital One Financial Corp. | 3.900 | 01-29-24 | 15,290,000 | 16,146,516 | |

| Credit Acceptance Corp. | 6.125 | 02-15-21 | 11,504,000 | 11,561,520 | |

| Credito Real SAB de CV (9.125% to 11-29-22, then 5 Year CMT + 7.026%) (D)(G) | 9.125 | 11-29-22 | 9,375,000 | 9,808,594 | |

| Discover Financial Services | 3.950 | 11-06-24 | 28,628,000 | 30,390,405 | |

| Discover Financial Services | 4.100 | 02-09-27 | 6,489,000 | 6,956,898 | |

| Enova International, Inc. (D) | 8.500 | 09-01-24 | 3,051,000 | 2,837,430 | |

| Enova International, Inc. (D) | 8.500 | 09-15-25 | 15,597,000 | 14,466,218 | |

| Springleaf Finance Corp. | 6.875 | 03-15-25 | 5,750,000 | 6,566,673 | |

| Diversified financial services 0.9% | |||||

| Allied Universal Holdco LLC (D) | 6.625 | 07-15-26 | 3,713,000 | 3,926,498 | |

| GE Capital International Funding Company Unlimited Company | 4.418 | 11-15-35 | 33,592,000 | 36,158,208 | |

| Gogo Intermediate Holdings LLC (D) | 9.875 | 05-01-24 | 10,941,000 | 11,501,179 | |

| Jefferies Financial Group, Inc. | 5.500 | 10-18-23 | 15,716,000 | 17,151,973 | |

| Jefferies Group LLC | 4.150 | 01-23-30 | 21,760,000 | 22,421,025 | |

| Jefferies Group LLC | 4.850 | 01-15-27 | 22,235,000 | 24,139,944 | |

| Refinitiv US Holdings, Inc. (D) | 6.250 | 05-15-26 | 2,370,000 | 2,583,300 | |

| Refinitiv US Holdings, Inc. (D) | 8.250 | 11-15-26 | 3,750,000 | 4,195,313 | |

| Trident TPI Holdings, Inc. (D) | 6.625 | 11-01-25 | 4,032,000 | 3,608,640 | |

| Voya Financial, Inc. (5.650% to 5-15-23, then 3 month LIBOR + 3.580%) | 5.650 | 05-15-53 | 29,467,000 | 30,998,105 | |

| Insurance 1.2% | |||||

| AXA SA | 8.600 | 12-15-30 | 9,222,000 | 13,499,440 | |

| Brighthouse Financial, Inc. | 3.700 | 06-22-27 | 31,050,000 | 30,680,008 | |

| CNO Financial Group, Inc. | 5.250 | 05-30-25 | 17,855,000 | 19,777,269 | |

| SEE NOTES TO FINANCIAL STATEMENTS | SEMIANNUAL REPORT | JOHN HANCOCK BOND FUND | 21 |

| Rate (%) | Maturity date | Par value^ | Value | ||

| Financials (continued) | |||||

| Insurance (continued) | |||||

| CNO Financial Group, Inc. | 5.250 | 05-30-29 | 7,570,000 | $8,388,128 | |

| Liberty Mutual Group, Inc. (D) | 3.951 | 10-15-50 | 25,053,000 | 25,555,562 | |

| MetLife, Inc. (6.400% to 12-15-36, then 3 month LIBOR + 2.205%) | 6.400 | 12-15-66 | 12,368,000 | 15,148,326 | |

| MetLife, Inc. (9.250% to 4-8-33, then 3 month LIBOR + 5.540%) (D) | 9.250 | 04-08-68 | 5,570,000 | 8,187,900 | |

| Nippon Life Insurance Company (5.100% to 10-16-24, then 5 Year U.S. ISDAFIX + 3.650%) (D) | 5.100 | 10-16-44 | 18,215,000 | 19,990,963 | |

| Prudential Financial, Inc. (5.875% to 9-15-22, then 3 month LIBOR + 4.175%) | 5.875 | 09-15-42 | 39,321,000 | 42,418,315 | |

| Teachers Insurance & Annuity Association of America (D) | 4.270 | 05-15-47 | 21,655,000 | 25,141,495 | |

| Thrifts and mortgage finance 0.5% | |||||

| Ladder Capital Finance Holdings LLLP (D) | 5.250 | 03-15-22 | 3,415,000 | 3,543,063 | |

| Ladder Capital Finance Holdings LLLP (D) | 5.250 | 10-01-25 | 7,640,000 | 7,754,600 | |

| MGIC Investment Corp. | 5.750 | 08-15-23 | 7,286,000 | 8,051,030 | |

| Nationstar Mortgage Holdings, Inc. (D) | 8.125 | 07-15-23 | 8,821,000 | 9,438,470 | |

| Nationstar Mortgage Holdings, Inc. (D) | 9.125 | 07-15-26 | 7,037,000 | 7,775,885 | |

| Nationwide Building Society (3.622% to 4-26-22, then 3 month LIBOR + 1.181%) (D) | 3.622 | 04-26-23 | 18,230,000 | 18,702,617 | |

| Nationwide Building Society (3.960% to 7-18-29, then 3 month LIBOR + 1.855%) (A)(D) | 3.960 | 07-18-30 | 13,550,000 | 14,515,789 | |

| Quicken Loans, Inc. (D) | 5.750 | 05-01-25 | 15,960,000 | 16,576,455 | |

| Radian Group, Inc. | 4.500 | 10-01-24 | 7,901,000 | 8,315,803 | |

| Health care 2.4% | 426,808,625 | ||||

| Biotechnology 0.5% | |||||

| AbbVie, Inc. (D) | 3.200 | 11-21-29 | 44,511,000 | 45,163,219 | |

| AbbVie, Inc. (D) | 4.250 | 11-21-49 | 12,529,000 | 13,166,553 | |

| Shire Acquisitions Investments Ireland DAC | 3.200 | 09-23-26 | 30,074,000 | 31,101,565 | |

| Health care providers and services 1.3% | |||||

| Centene Corp. (D) | 4.250 | 12-15-27 | 5,858,000 | 6,026,418 | |

| Centene Corp. (D) | 4.625 | 12-15-29 | 6,105,000 | 6,402,619 | |

| Centene Corp. (D) | 5.375 | 06-01-26 | 14,365,000 | 15,244,856 | |

| CVS Health Corp. | 3.000 | 08-15-26 | 5,073,000 | 5,191,418 | |

| CVS Health Corp. | 4.100 | 03-25-25 | 24,300,000 | 26,094,251 | |

| CVS Health Corp. | 5.050 | 03-25-48 | 17,559,000 | 20,774,571 | |

| DaVita, Inc. (A) | 5.000 | 05-01-25 | 24,471,000 | 25,246,241 | |

| Encompass Health Corp. | 4.500 | 02-01-28 | 2,900,000 | 2,972,500 | |

| HCA, Inc. | 4.125 | 06-15-29 | 8,402,000 | 8,851,502 | |

| 22 | JOHN HANCOCK BOND FUND | SEMIANNUAL REPORT | SEE NOTES TO FINANCIAL STATEMENTS |

| Rate (%) | Maturity date | Par value^ | Value | ||

| Health care (continued) | |||||

| Health care providers and services (continued) | |||||

| HCA, Inc. | 5.250 | 04-15-25 | 15,959,000 | $17,768,139 | |

| HCA, Inc. | 5.250 | 06-15-26 | 18,243,000 | 20,383,614 | |

| MEDNAX, Inc. (D) | 5.250 | 12-01-23 | 13,806,000 | 14,116,635 | |

| MEDNAX, Inc. (A)(D) | 6.250 | 01-15-27 | 12,515,000 | 12,734,013 | |

| Select Medical Corp. (D) | 6.250 | 08-15-26 | 7,864,000 | 8,434,140 | |

| Team Health Holdings, Inc. (A)(D) | 6.375 | 02-01-25 | 3,197,000 | 1,694,410 | |

| Universal Health Services, Inc. (D) | 4.750 | 08-01-22 | 15,230,000 | 15,391,819 | |

| Universal Health Services, Inc. (D) | 5.000 | 06-01-26 | 13,991,000 | 14,760,505 | |

| Life sciences tools and services 0.0% | |||||

| Charles River Laboratories International, Inc. (D) | 4.250 | 05-01-28 | 3,981,000 | 4,010,858 | |

| Pharmaceuticals 0.6% | |||||

| Bausch Health Companies, Inc. (D) | 6.125 | 04-15-25 | 21,865,000 | 22,738,944 | |

| Bristol-Myers Squibb Company (D) | 2.900 | 07-26-24 | 40,990,000 | 42,273,426 | |

| Bristol-Myers Squibb Company (D) | 3.250 | 02-20-23 | 15,657,000 | 16,215,922 | |

| Catalent Pharma Solutions, Inc. (D) | 5.000 | 07-15-27 | 3,705,000 | 3,843,938 | |

| GlaxoSmithKline Capital PLC | 3.000 | 06-01-24 | 25,294,000 | 26,206,549 | |

| Industrials 4.9% | 880,195,389 | ||||

| Aerospace and defense 0.5% | |||||

| Arconic, Inc. (A) | 5.125 | 10-01-24 | 18,133,000 | 19,765,877 | |

| Huntington Ingalls Industries, Inc. (D) | 5.000 | 11-15-25 | 21,100,000 | 22,102,250 | |

| Kratos Defense & Security Solutions, Inc. (D) | 6.500 | 11-30-25 | 11,995,000 | 12,714,700 | |

| TransDigm, Inc. (D) | 5.500 | 11-15-27 | 34,786,000 | 34,786,000 | |

| Air freight and logistics 0.1% | |||||

| XPO Logistics, Inc. (D) | 6.500 | 06-15-22 | 11,266,000 | 11,529,174 | |

| Airlines 2.4% | |||||

| Air Canada 2013-1 Class A Pass Through Trust (D) | 4.125 | 11-15-26 | 10,711,079 | 11,306,793 | |

| Air Canada 2017-1 Class B Pass Through Trust (D) | 3.700 | 07-15-27 | 13,599,405 | 13,717,866 | |

| America West Airlines 2000-1 Pass Through Trust | 8.057 | 01-02-22 | 443,900 | 455,488 | |

| American Airlines 2001-01 Pass Through Trust | 6.977 | 11-23-22 | 2,000,882 | 2,025,750 | |

| American Airlines 2013-2 Class A Pass Through Trust | 4.950 | 07-15-24 | 19,804,277 | 20,725,562 | |

| American Airlines 2015-1 Class A Pass Through Trust | 3.375 | 11-01-28 | 20,216,862 | 20,924,962 | |

| American Airlines 2015-1 Class B Pass Through Trust | 3.700 | 11-01-24 | 6,701,616 | 6,759,093 | |

| American Airlines 2016-1 Class A Pass Through Trust (A) | 4.100 | 07-15-29 | 23,339,996 | 24,221,676 | |

| SEE NOTES TO FINANCIAL STATEMENTS | SEMIANNUAL REPORT | JOHN HANCOCK BOND FUND | 23 |

| Rate (%) | Maturity date | Par value^ | Value | ||

| Industrials (continued) | |||||

| Airlines (continued) | |||||

| American Airlines 2017-1 Class A Pass Through Trust | 4.000 | 08-15-30 | 7,811,769 | $8,310,099 | |

| American Airlines 2017-1 Class AA Pass Through Trust | 3.650 | 08-15-30 | 16,600,556 | 17,621,666 | |

| American Airlines 2017-2 Class A Pass Through Trust | 3.600 | 04-15-31 | 9,054,933 | 9,271,694 | |

| American Airlines 2019-1 Class A Pass Through Trust | 3.500 | 08-15-33 | 10,384,000 | 10,614,155 | |

| American Airlines 2019-1 Class AA Pass Through Trust | 3.150 | 08-15-33 | 15,568,000 | 16,341,524 | |

| Azul Investments LLP (A)(D) | 5.875 | 10-26-24 | 13,760,000 | 13,916,864 | |

| British Airways 2013-1 Class A Pass Through Trust (D) | 4.625 | 06-20-24 | 12,404,533 | 13,072,759 | |

| British Airways 2013-1 Class B Pass Through Trust (D) | 5.625 | 12-20-21 | 575,716 | 579,616 | |

| British Airways 2018-1 Class A Pass Through Trust (D) | 4.125 | 03-20-33 | 7,639,523 | 8,053,895 | |

| Continental Airlines 2007-1 Class A Pass Through Trust | 5.983 | 10-19-23 | 7,966,501 | 8,397,928 | |

| Continental Airlines 2012-1 Class B Pass Through Trust | 6.250 | 10-11-21 | 738,714 | 745,211 | |

| Delta Air Lines 2002-1 Class G-1 Pass Through Trust | 6.718 | 07-02-24 | 5,031,054 | 5,279,744 | |

| Delta Air Lines, Inc. | 2.900 | 10-28-24 | 32,491,000 | 32,119,949 | |

| Delta Air Lines, Inc. | 3.800 | 04-19-23 | 20,208,000 | 20,835,120 | |

| Delta Air Lines, Inc. | 4.375 | 04-19-28 | 22,850,000 | 23,689,709 | |

| JetBlue 2019-1 Class AA Pass Through Trust | 2.750 | 11-15-33 | 14,832,000 | 15,060,962 | |

| United Airlines 2014-2 Class A Pass Through Trust | 3.750 | 03-03-28 | 23,236,646 | 24,475,312 | |

| United Airlines 2014-2 Class B Pass Through Trust | 4.625 | 03-03-24 | 9,909,473 | 10,222,961 | |

| United Airlines 2016-1 Class A Pass Through Trust | 3.450 | 01-07-30 | 19,623,789 | 20,210,931 | |

| United Airlines 2016-1 Class B Pass Through Trust | 3.650 | 01-07-26 | 26,581,597 | 26,894,694 | |

| United Airlines 2018-1 Class B Pass Through Trust | 4.600 | 03-01-26 | 7,088,785 | 7,372,889 | |

| United Airlines 2019-1 Class A Pass Through Trust | 4.550 | 02-25-33 | 17,175,000 | 18,790,352 | |

| US Airways 2010-1 Class A Pass Through Trust | 6.250 | 10-22-24 | 4,198,855 | 4,554,398 | |

| US Airways 2012-1 Class A Pass Through Trust | 5.900 | 04-01-26 | 6,354,500 | 7,070,750 | |

| Building products 0.1% | |||||

| Owens Corning | 3.950 | 08-15-29 | 14,998,000 | 15,483,075 | |

| 24 | JOHN HANCOCK BOND FUND | SEMIANNUAL REPORT | SEE NOTES TO FINANCIAL STATEMENTS |

| Rate (%) | Maturity date | Par value^ | Value | ||

| Industrials (continued) | |||||

| Commercial services and supplies 0.1% | |||||

| Clean Harbors, Inc. (D) | 4.875 | 07-15-27 | 2,960,000 | $3,101,488 | |

| IAA, Inc. (D) | 5.500 | 06-15-27 | 835,000 | 878,090 | |

| LSC Communications, Inc. (D) | 8.750 | 10-15-23 | 19,591,000 | 9,893,455 | |

| Prime Security Services Borrower LLC (D) | 9.250 | 05-15-23 | 2,608,000 | 2,741,660 | |

| Construction and engineering 0.2% | |||||

| AECOM | 5.125 | 03-15-27 | 22,537,000 | 24,001,905 | |

| Tutor Perini Corp. (A)(D) | 6.875 | 05-01-25 | 3,182,000 | 3,106,428 | |

| Industrial conglomerates 0.3% | |||||

| 3M Company | 3.250 | 02-14-24 | 24,330,000 | 25,501,553 | |

| General Electric Company | 5.550 | 01-05-26 | 26,960,000 | 30,731,598 | |

| Machinery 0.0% | |||||

| Harsco Corp. (D) | 5.750 | 07-31-27 | 5,035,000 | 5,299,338 | |

| Professional services 0.2% | |||||

| IHS Markit, Ltd. (D) | 4.000 | 03-01-26 | 22,669,000 | 24,071,304 | |

| IHS Markit, Ltd. (A)(D) | 4.750 | 02-15-25 | 6,967,000 | 7,603,017 | |

| IHS Markit, Ltd. (A) | 4.750 | 08-01-28 | 11,465,000 | 12,758,997 | |

| Road and rail 0.1% | |||||

| Uber Technologies, Inc. (D) | 7.500 | 09-15-27 | 20,585,000 | 20,404,881 | |

| Trading companies and distributors 0.9% | |||||

| AerCap Ireland Capital DAC | 2.875 | 08-14-24 | 24,033,000 | 24,223,520 | |

| AerCap Ireland Capital DAC | 5.000 | 10-01-21 | 16,850,000 | 17,662,977 | |

| Ahern Rentals, Inc. (D) | 7.375 | 05-15-23 | 21,183,000 | 16,522,740 | |

| Air Lease Corp. | 3.625 | 12-01-27 | 10,511,000 | 10,880,056 | |

| Aircastle, Ltd. | 4.400 | 09-25-23 | 9,561,000 | 10,136,787 | |

| Aircastle, Ltd. | 5.500 | 02-15-22 | 13,545,000 | 14,408,898 | |

| Ashtead Capital, Inc. (D) | 4.250 | 11-01-29 | 8,614,000 | 8,700,140 | |

| Ashtead Capital, Inc. (D) | 4.375 | 08-15-27 | 14,640,000 | 15,097,500 | |

| Avolon Holdings Funding, Ltd. (D) | 5.125 | 10-01-23 | 12,797,000 | 13,755,495 | |

| H&E Equipment Services, Inc. | 5.625 | 09-01-25 | 7,015,000 | 7,374,519 | |

| United Rentals North America, Inc. | 3.875 | 11-15-27 | 10,861,000 | 10,956,034 | |

| United Rentals North America, Inc. | 4.875 | 01-15-28 | 19,515,000 | 20,361,561 | |

| Information technology 4.4% | 791,869,525 | ||||

| Communications equipment 0.5% | |||||

| CommScope, Inc. (D) | 8.250 | 03-01-27 | 22,112,000 | 22,221,454 | |

| Motorola Solutions, Inc. | 4.600 | 02-23-28 | 33,189,000 | 35,832,673 | |

| Telefonaktiebolaget LM Ericsson | 4.125 | 05-15-22 | 29,710,000 | 30,786,988 | |

| Electronic equipment, instruments and components 0.1% | |||||

| Tech Data Corp. | 3.700 | 02-15-22 | 10,760,000 | 10,959,087 | |

| IT services 0.8% | |||||

| Banff Merger Sub, Inc. (D) | 9.750 | 09-01-26 | 12,341,000 | 11,566,602 | |

| Fiserv, Inc. | 2.750 | 07-01-24 | 18,919,000 | 19,217,371 | |

| SEE NOTES TO FINANCIAL STATEMENTS | SEMIANNUAL REPORT | JOHN HANCOCK BOND FUND | 25 |

| Rate (%) | Maturity date | Par value^ | Value | ||

| Information technology (continued) | |||||

| IT services (continued) | |||||

| Fiserv, Inc. | 3.200 | 07-01-26 | 27,855,000 | $28,852,252 | |

| PayPal Holdings, Inc. | 2.400 | 10-01-24 | 25,619,000 | 25,678,814 | |

| PayPal Holdings, Inc. | 2.850 | 10-01-29 | 30,408,000 | 30,339,331 | |

| Tempo Acquisition LLC (D) | 6.750 | 06-01-25 | 6,270,000 | 6,458,100 | |

| VeriSign, Inc. | 4.750 | 07-15-27 | 7,792,000 | 8,282,896 | |

| VeriSign, Inc. | 5.250 | 04-01-25 | 9,210,000 | 10,133,763 | |

| Semiconductors and semiconductor equipment 2.2% | |||||

| Broadcom Corp. | 3.875 | 01-15-27 | 47,695,000 | 48,687,247 | |

| Broadcom, Inc. (D) | 4.750 | 04-15-29 | 19,150,000 | 20,477,612 | |

| KLA Corp. | 4.100 | 03-15-29 | 17,241,000 | 18,907,081 | |

| Lam Research Corp. | 3.750 | 03-15-26 | 19,502,000 | 20,919,758 | |

| Lam Research Corp. | 4.875 | 03-15-49 | 17,074,000 | 21,241,893 | |

| Marvell Technology Group, Ltd. | 4.875 | 06-22-28 | 23,499,000 | 26,359,447 | |

| Microchip Technology, Inc. | 4.333 | 06-01-23 | 47,401,000 | 49,875,307 | |

| Micron Technology, Inc. | 4.185 | 02-15-27 | 46,310,000 | 48,703,869 | |

| Micron Technology, Inc. | 4.975 | 02-06-26 | 11,033,000 | 12,121,644 | |

| Micron Technology, Inc. | 5.327 | 02-06-29 | 42,469,000 | 47,548,196 | |

| NXP BV (D) | 3.875 | 06-18-26 | 16,420,000 | 17,233,089 | |

| NXP BV (D) | 4.625 | 06-01-23 | 34,550,000 | 36,836,131 | |

| NXP BV (D) | 4.875 | 03-01-24 | 17,920,000 | 19,458,064 | |

| Qorvo, Inc. | 5.500 | 07-15-26 | 7,029,000 | 7,477,099 | |

| Software 0.1% | |||||

| Microsoft Corp. | 4.450 | 11-03-45 | 19,750,000 | 24,895,815 | |

| Technology hardware, storage and peripherals 0.7% | |||||

| Dell International LLC (D) | 4.900 | 10-01-26 | 29,030,000 | 31,569,888 | |

| Dell International LLC (A)(D) | 5.300 | 10-01-29 | 29,321,000 | 32,455,587 | |

| Dell International LLC (D) | 8.350 | 07-15-46 | 31,996,000 | 42,930,123 | |

| Seagate HDD Cayman (A) | 4.750 | 01-01-25 | 22,665,000 | 23,842,344 | |

| Materials 1.1% | 190,908,696 | ||||

| Chemicals 0.6% | |||||

| Braskem Netherlands Finance BV (D) | 4.500 | 01-10-28 | 13,909,000 | 13,639,896 | |

| Cydsa SAB de CV (A)(D) | 6.250 | 10-04-27 | 14,025,000 | 14,112,656 | |

| Methanex Corp. | 5.250 | 12-15-29 | 18,194,000 | 18,487,044 | |

| Orbia Advance Corp. SAB de CV (D) | 5.500 | 01-15-48 | 17,715,000 | 17,604,281 | |

| Syngenta Finance NV (D) | 4.441 | 04-24-23 | 25,935,000 | 27,037,686 | |

| Syngenta Finance NV (D) | 5.676 | 04-24-48 | 8,210,000 | 8,553,310 | |

| Construction materials 0.1% | |||||

| Cemex SAB de CV (D) | 6.125 | 05-05-25 | 15,185,000 | 15,716,475 | |

| Containers and packaging 0.1% | |||||

| Ardagh Packaging Finance PLC (D) | 6.000 | 02-15-25 | 14,410,000 | 15,130,500 | |

| Klabin Finance SA (D) | 4.875 | 09-19-27 | 1,453,000 | 1,494,774 | |

| 26 | JOHN HANCOCK BOND FUND | SEMIANNUAL REPORT | SEE NOTES TO FINANCIAL STATEMENTS |

| Rate (%) | Maturity date | Par value^ | Value | ||

| Materials (continued) | |||||

| Metals and mining 0.2% | |||||

| Anglo American Capital PLC (D) | 4.750 | 04-10-27 | 13,375,000 | $14,550,075 | |

| Commercial Metals Company | 5.375 | 07-15-27 | 5,017,000 | 5,192,595 | |

| First Quantum Minerals, Ltd. (D) | 6.875 | 03-01-26 | 9,625,000 | 9,360,313 | |

| First Quantum Minerals, Ltd. (A)(D) | 7.500 | 04-01-25 | 5,100,000 | 5,010,750 | |

| Newmont Goldcorp Corp. | 2.800 | 10-01-29 | 10,482,000 | 10,373,485 | |

| Paper and forest products 0.1% | |||||

| Norbord, Inc. (A)(D) | 6.250 | 04-15-23 | 7,025,000 | 7,490,406 | |

| Suzano Austria GmbH (A) | 6.000 | 01-15-29 | 6,460,000 | 7,154,450 | |

| Real estate 1.4% | 253,498,137 | ||||

| Equity real estate investment trusts 1.4% | |||||

| American Homes 4 Rent LP | 4.250 | 02-15-28 | 22,190,000 | 23,799,878 | |

| American Tower Corp. | 2.950 | 01-15-25 | 16,023,000 | 16,327,509 | |

| American Tower Corp. | 3.550 | 07-15-27 | 32,300,000 | 33,841,820 | |

| American Tower Corp. | 3.800 | 08-15-29 | 12,980,000 | 13,841,783 | |

| CyrusOne LP (B) | 3.450 | 11-15-29 | 14,081,000 | 14,108,317 | |

| Equinix, Inc. | 3.200 | 11-18-29 | 27,111,000 | 27,176,609 | |

| Equinix, Inc. | 5.375 | 05-15-27 | 12,381,000 | 13,417,909 | |

| GLP Capital LP | 5.375 | 04-15-26 | 16,732,000 | 18,437,530 | |

| SBA Tower Trust (D) | 2.836 | 01-15-25 | 22,481,000 | 22,739,023 | |

| SBA Tower Trust (D) | 3.722 | 04-09-48 | 26,799,000 | 27,527,952 | |

| The GEO Group, Inc. | 6.000 | 04-15-26 | 4,171,000 | 3,305,518 | |

| Ventas Realty LP | 3.500 | 02-01-25 | 16,239,000 | 16,912,989 | |

| VEREIT Operating Partnership LP | 4.600 | 02-06-24 | 17,864,000 | 19,241,105 | |

| VICI Properties LP (A)(D) | 4.625 | 12-01-29 | 2,735,000 | 2,820,195 | |

| Utilities 1.4% | 258,530,224 | ||||

| Electric utilities 0.7% | |||||

| ABY Transmision Sur SA (D) | 6.875 | 04-30-43 | 9,530,535 | 11,853,698 | |

| Electricite de France SA (5.250% to 1-29-23, then 10 Year U.S. Swap Rate + 3.709%) (D)(G) | 5.250 | 01-29-23 | 27,115,000 | 28,199,600 | |

| Emera US Finance LP | 3.550 | 06-15-26 | 11,506,000 | 11,999,100 | |

| Empresa Electrica Angamos SA (D) | 4.875 | 05-25-29 | 9,234,680 | 9,402,025 | |

| Instituto Costarricense de Electricidad (D) | 6.375 | 05-15-43 | 9,810,000 | 8,228,138 | |

| Israel Electric Corp., Ltd. (D) | 6.875 | 06-21-23 | 6,630,000 | 7,527,192 | |

| Vistra Operations Company LLC (D) | 3.700 | 01-30-27 | 27,272,000 | 26,973,120 | |

| Vistra Operations Company LLC (D) | 4.300 | 07-15-29 | 24,825,000 | 25,592,712 | |

| Gas utilities 0.1% | |||||

| AmeriGas Partners LP | 5.500 | 05-20-25 | 12,441,000 | 13,314,607 | |

| Independent power and renewable electricity producers 0.6% | |||||

| Clearway Energy Operating LLC | 5.375 | 08-15-24 | 13,749,000 | 14,092,725 | |

| Greenko Dutch BV (D) | 4.875 | 07-24-22 | 11,885,000 | 11,902,828 | |

| SEE NOTES TO FINANCIAL STATEMENTS | SEMIANNUAL REPORT | JOHN HANCOCK BOND FUND | 27 |

| Rate (%) | Maturity date | Par value^ | Value | ||

| Utilities (continued) | |||||

| Independent power and renewable electricity producers (continued) | |||||

| Greenko Dutch BV (D) | 5.250 | 07-24-24 | 7,105,000 | $7,190,971 | |

| LLPL Capital Pte, Ltd. (D) | 6.875 | 02-04-39 | 3,595,072 | 4,159,138 | |

| NextEra Energy Capital Holdings, Inc. | 3.550 | 05-01-27 | 32,227,000 | 34,418,088 | |

| NextEra Energy Operating Partners LP (D) | 3.875 | 10-15-26 | 15,359,000 | 15,267,614 | |

| NextEra Energy Operating Partners LP (A)(D) | 4.500 | 09-15-27 | 5,100,000 | 5,202,000 | |

| NRG Energy, Inc. (D) | 3.750 | 06-15-24 | 12,190,000 | 12,566,704 | |

| Multi-utilities 0.0% | |||||

| CenterPoint Energy, Inc. | 2.500 | 09-01-24 | 10,639,000 | 10,639,964 | |

| Term loans (H) 0.0% | $4,122,305 | ||||

| (Cost $4,463,017) | |||||

| Financials 0.0% | 4,122,305 | ||||

| Capital markets 0.0% | |||||

| LSF9 Atlantis Holdings LLC, 2017 Term Loan (1 month LIBOR + 6.000%) | 7.758 | 05-01-23 | 4,482,813 | 4,122,305 | |

| Collateralized mortgage obligations 6.4% | $1,152,968,720 | ||||

| (Cost $1,163,806,901) | |||||

| Commercial and residential 5.1% | 914,034,262 | ||||

| Americold LLC | |||||

| Series 2010-ARTA, Class C (D) | 6.811 | 01-14-29 | 2,150,000 | 2,211,380 | |

| Series 2010-ARTA, Class D (D) | 7.443 | 01-14-29 | 9,783,000 | 10,097,070 | |

| Angel Oak Mortgage Trust I LLC | |||||

| Series 2018-1, Class A1 (D)(I) | 3.258 | 04-27-48 | 2,469,323 | 2,477,299 | |

| Series 2018-3, Class A1 (D)(I) | 3.649 | 09-25-48 | 6,781,636 | 6,867,661 | |

| AOA Mortgage Trust Series 2015-1177, Class C (D)(I) | 3.110 | 12-13-29 | 6,896,000 | 6,942,915 | |

| Arroyo Mortgage Trust | |||||

| Series 2018-1, Class A1 (D)(I) | 3.763 | 04-25-48 | 28,168,452 | 28,633,716 | |

| Series 2019-2, Class A1 (D)(I) | 3.347 | 04-25-49 | 25,812,044 | 26,116,350 | |

| Series 2019-3, Class A1 (D)(I) | 2.962 | 10-25-48 | 14,778,002 | 14,837,859 | |

| BAMLL Commercial Mortgage Securities Trust Series 2019-BPR, Class ENM (D)(I) | 3.843 | 11-05-32 | 11,565,000 | 10,941,427 | |

| Barclays Commercial Mortgage Trust Series 2019-C5, Class A2 | 3.043 | 11-15-52 | 15,448,000 | 15,961,221 | |

| BBCMS Mortgage Trust Series 2018-TALL, Class E (1 month LIBOR + 2.437%) (C)(D) | 4.351 | 03-15-37 | 9,590,000 | 9,586,934 | |

| BBCMS Trust | |||||

| Series 2015-MSQ, Class D (D)(I) | 4.123 | 09-15-32 | 7,340,000 | 7,460,075 | |

| Series 2015-SRCH, Class D (D)(I) | 5.122 | 08-10-35 | 15,371,000 | 16,824,121 | |

| Bear Stearns Commercial Mortgage Securities Trust Series 2005-PWR8, Class X1 IO (D) | 0.798 | 06-11-41 | 310,076 | 806 | |

| BENCHMARK Mortgage Trust | |||||

| 28 | JOHN HANCOCK BOND FUND | SEMIANNUAL REPORT | SEE NOTES TO FINANCIAL STATEMENTS |

| Rate (%) | Maturity date | Par value^ | Value | ||

| Commercial and residential (continued) | |||||

| Series 2019-B10, Class A2 | 3.614 | 03-15-62 | 20,454,000 | $21,553,732 | |

| Series 2019-B11, Class A2 | 3.410 | 05-15-52 | 16,845,000 | 17,660,414 | |

| Series 2019-B12, Class A2 | 3.001 | 08-15-52 | 21,935,000 | 22,641,618 | |

| Series 2019-B13, Class A2 | 2.889 | 08-15-57 | 19,985,000 | 20,535,261 | |

| Series 2019-B14, Class A2 | 2.915 | 12-15-61 | 19,098,000 | 19,669,998 | |

| BRAVO Residential Funding Trust Series 2019-NQM1, Class A1 (D)(I) | 2.666 | 07-25-59 | 11,091,771 | 11,092,737 | |

| Bunker Hill Loan Depositary Trust Series 2019-1, Class A1 (D) | 3.613 | 10-26-48 | 3,059,667 | 3,095,641 | |

| BWAY Mortgage Trust | |||||

| Series 2013-1515, Class XB IO (D) | 0.534 | 03-10-33 | 46,410,000 | 944,861 | |

| Series 2015-1740, Class XA IO (D) | 1.023 | 01-10-35 | 123,773,000 | 2,385,898 | |

| BX Commercial Mortgage Trust Series 2018-BIOA, Class D (1 month LIBOR + 1.321%) (C)(D) | 3.235 | 03-15-37 | 12,620,000 | 12,627,884 | |

| CAMB Commercial Mortgage Trust Series 2019-LIFE, Class D (1 month LIBOR + 1.750%) (C)(D) | 3.671 | 12-15-37 | 6,315,000 | 6,336,650 | |

| CGBAM Commercial Mortgage Trust Series 2015-SMRT, Class F (D)(I) | 3.912 | 04-10-28 | 5,190,000 | 5,195,967 | |

| CGDBB Commercial Mortgage Trust Series 2017-BIOC, Class E (1 month LIBOR + 2.150%) (C)(D) | 4.064 | 07-15-32 | 9,287,082 | 9,287,058 | |

| CHT Mortgage Trust Series 2017-CSMO, Class D (1 month LIBOR + 2.250%) (C)(D) | 4.171 | 11-15-36 | 17,654,000 | 17,664,863 | |

| Citigroup Commercial Mortgage Trust | |||||

| Series 2017-1500, Class E (1 month LIBOR + 2.500%) (C)(D) | 4.414 | 07-15-32 | 4,667,000 | 4,686,744 | |

| Series 2019-PRM, Class A (D) | 3.341 | 05-10-36 | 8,060,000 | 8,396,527 | |

| Series 2019-SMRT, Class A (D) | 4.149 | 01-10-36 | 6,922,000 | 7,405,813 | |

| COLT Mortgage Loan Trust | |||||

| Series 2018-2, Class A1 (D)(I) | 3.470 | 07-27-48 | 1,782,323 | 1,788,597 | |

| Series 2019-2, Class A1 (D)(I) | 3.337 | 05-25-49 | 10,341,885 | 10,364,302 | |

| Commercial Mortgage Trust (Cantor Fitzgerald/Deutsche Bank AG) | |||||