SCHEDULE 14A

(RULE 14a-101)

INFORMATION REQUIRED IN PROXY STATEMENT

SCHEDULE 14A INFORMATION

Proxy Statement Pursuant to Section 14(a) of the Securities

Exchange Act of 1934 (Amendment No. ______)

Filed by the Registrantx

Filed by Party other than the Registrant¨

Check the appropriate box:

| ¨ | Preliminary Proxy Statement |

| ¨ | Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) |

| x | Definitive Proxy Statement |

| ¨ | Definitive Additional Materials |

| ¨ | Soliciting Material Pursuant to §240.14a-12 |

JOHN HANCOCK CAPITAL SERIES

(Name of Registrant as Specified in Its Charter)

Payment of Filing Fee (Check the appropriate box):

| x | No fee required. | |

| ¨ | Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11. | |

| (1) | Title of each class of securities to which transaction applies: | |

| (2) | Aggregate number of securities to which transaction applies: | |

| (3) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (Set forth the amount on which the filing fee is calculated and state how it was determined): | |

| (4) | Proposed maximum aggregate value of transaction: | |

| (5) | Total fee paid: | |

| ¨ | Fee paid previously with preliminary materials. | |

| ¨ | Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. | |

| (1) | Amount Previously Paid: | |

| (2) | Form, Schedule or Registration Statement No.: | |

| (3) | Filing Party: | |

| (4) | Date Filed: | |

April 6, 2018

Your action is required. Please vote today.

Dear shareholder:

I am writing to ask you to approve three proposals that affect John Hancock U.S. Global Leaders Growth Fund. As a registered shareholder, you would be voting on behalf of the fund shares you own.

Approve a new subadvisory agreement with Sustainable Growth Advisors

As the fund’s subadvisor, Sustainable Growth Advisers, LP (SGA) is responsible for the day-to-day management of your fund’s portfolio. In February 2018, SGA announced they had agreed to sell a majority ownership stake to Virtus Investment Partners, a multi-boutique asset manager based in Hartford, Connecticut, in a transaction that is expected to close by June 30, 2018. While there are no changes to your fund’s portfolio team or SGA’s operations, under the Investment Company Act of 1940 (the 1940 Act), the change in ownership structure necessitates a new subadvisory agreement.Your fund’s Trustees unanimously approved the agreement, but the 1940 Act also requires shareholder approval. Approval of the new agreement is necessary to ensure continuity of fund management.

Approve “manager of managers” oversight authority for the fund’s advisor

The multimanager investment approach we have employed at John Hancock Investments since 1988 involves finding the best specialized manager for every fund we offer and providing stringent oversight to ensure they continue to meet expectations. We are asking the fund’s shareholders to allow the fund’s advisor to hire and replace managers under a “manager of managers” structure without having to incur the cost and delay of holding a shareholder meeting and soliciting shareholder votes. Any change in the fund’s subadvisory agreement would be subject to Board approval and require shareholder notification.

Approve greater flexibility in the fund’s future investment management

Finally, we are asking shareholders to approve an update of the fund’s investment restrictions. The update would not substantively change the fund’s investment policies, but rather would provide the flexibility to accommodate potential future legal and regulatory developments. We recommended this change to your fund’s Trustees, and they agreed it was in the best interests of shareholders.

How to vote

A special shareholder meeting to vote on these proposals has been scheduled for June 15, 2018, at the offices of John Hancock Investments, 601 Congress Street, Boston, Massachusetts. Please read the enclosed proxy statement, and vote your shares as described below. While you may attend the meeting in person,voting today will save on the potential cost of future mailings required to obtain shareholder votes.You may vote your shares by proxy in one of three ways:

Online:www.proxyvote.com

Phone:1-800-690-6903

Mail:by returning the enclosed proxy card(s)

Sincerely,

/s/ Andrew G. Arnott

Andrew G. Arnott

President and CEO

John Hancock Investments

April 6, 2018

Your action is required. Please vote today.

Dear shareholder:

I am writing to ask you to approve three proposals that affect John Hancock U.S. Global Leaders Growth Fund. As a registered shareholder, you would be voting on behalf of the fund shares you own.

Approve a new subadvisory agreement with Sustainable Growth Advisors

As the fund’s subadvisor, Sustainable Growth Advisers, LP (SGA) is responsible for the day-to-day management of your fund’s portfolio. In February 2018, SGA announced they had agreed to sell a majority ownership stake to Virtus Investment Partners, a multi-boutique asset manager based in Hartford, Connecticut, in a transaction that is expected to close by June 30, 2018. While there are no changes to your fund’s portfolio team or SGA’s operations, under the Investment Company Act of 1940 (the 1940 Act), the change in ownership structure necessitates a new subadvisory agreement.Your fund’s Trustees unanimously approved the agreement, but the 1940 Act also requires shareholder approval. Approval of the new agreement is necessary to ensure continuity of fund management.

Approve “manager of managers” oversight authority for the fund’s advisor

The multimanager investment approach we have employed at John Hancock Investments since 1988 involves finding the best specialized manager for every fund we offer and providing stringent oversight to ensure they continue to meet expectations. We are asking the fund’s shareholders to allow the fund’s advisor to hire and replace managers under a “manager of managers” structure without having to incur the cost and delay of holding a shareholder meeting and soliciting shareholder votes. Any change in the fund’s subadvisory agreement would be subject to Board approval and require shareholder notification.

Approve greater flexibility in the fund’s future investment management

Finally, we are asking shareholders to approve an update of the fund’s investment restrictions. The update would not substantively change the fund’s investment policies, but rather would provide the flexibility to accommodate potential future legal and regulatory developments. We recommended this change to your fund’s Trustees, and they agreed it was in the best interests of shareholders.

How to vote

A special shareholder meeting to vote on these proposals has been scheduled for June 15, 2018, at the offices of John Hancock Investments, 601 Congress Street, Boston, Massachusetts. Please read the enclosed proxy statement, and vote your shares as described below. While you may attend the meeting in person,voting today will save on the potential cost of future mailings required to obtain shareholder votes.You may vote your shares by proxy in one of three ways:

Online:by visiting the website on your proxy card(s) and entering your control number

Phone:by calling the number listed on your proxy card(s)

Mail:by returning the enclosed proxy card(s)

Sincerely,

/s/ Andrew G. Arnott

Andrew G. Arnott

President and CEO

John Hancock Investments

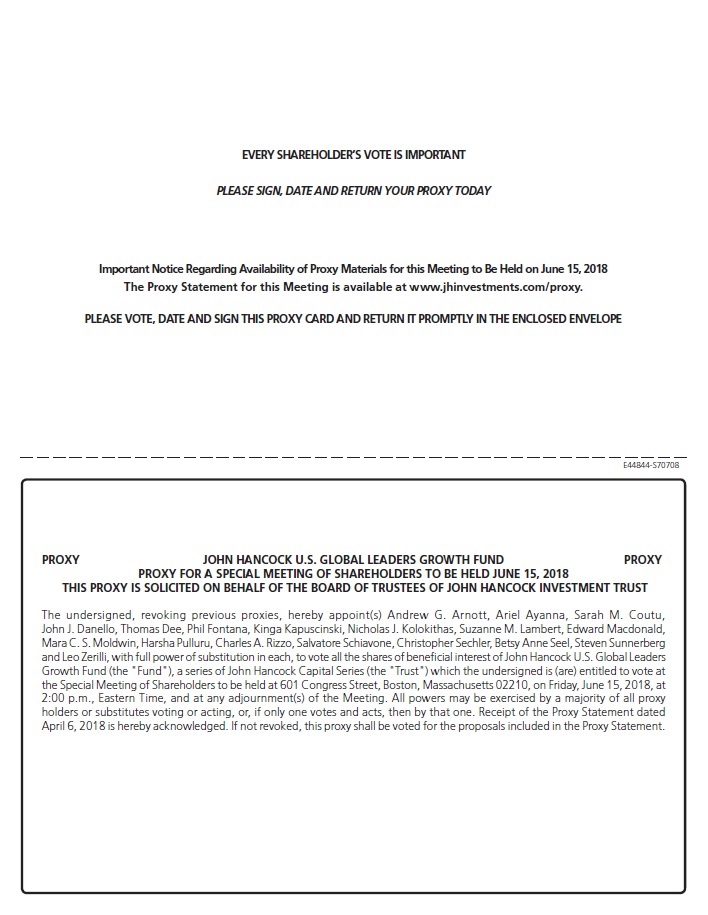

JOHN HANCOCK U.S. GLOBAL LEADERS GROWTH FUND

a series of JOHN HANCOCK CAPITAL SERIES

601 Congress Street

Boston, Massachusetts 02210

NOTICE OF SPECIAL MEETING OF SHAREHOLDERS

To the shareholders of John Hancock U.S. Global Leaders Growth Fund (the “Fund”):

Notice is hereby given that a special meeting of shareholders of the Fund will be held at 601 Congress Street, Boston, Massachusetts 02210, onFriday, June 15, 2018, at 2:00 P.M., Eastern Time (the “Meeting”).A Proxy Statement, which provides information about the purposes of the Meeting, is included with this notice. The Meeting will be held for the following purposes:

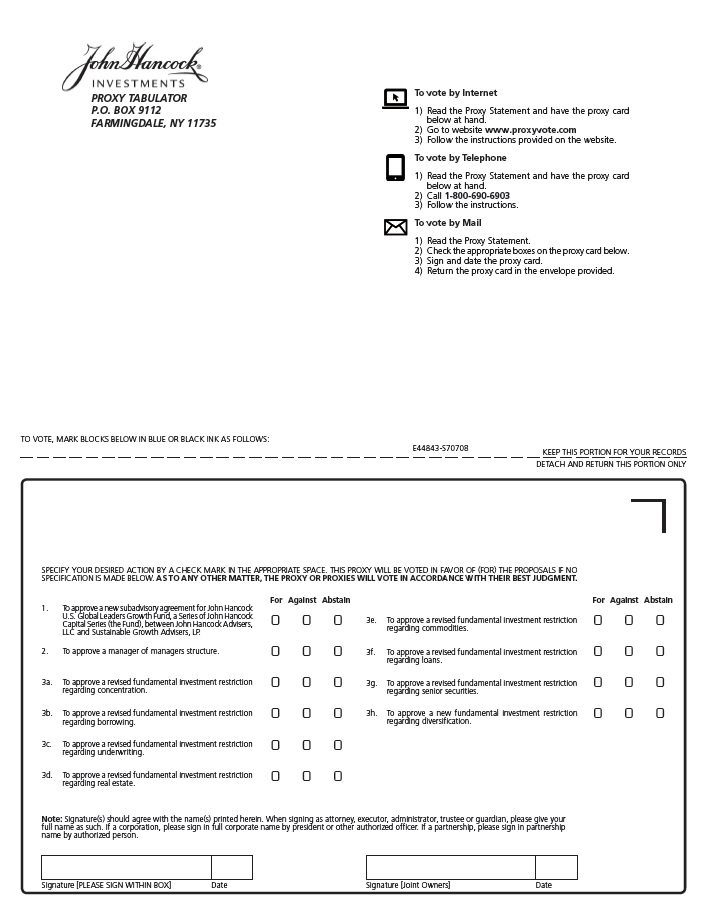

| Proposal 1 | To approve a new subadvisory agreement for the Fund between John Hancock Advisers, LLC and Sustainable Growth Advisers, LP. |

| Shareholdersofthe FundwillvoteseparatelyonProposal 1. | |

| Proposal 2 | To approve a manager of managers structure for the Fund. |

| Shareholdersofthe FundwillvoteseparatelyonProposal 2. | |

| Proposal 3 | To approve revised or new fundamental investment restrictions regarding: |

| (a) | Concentration | |

| (b) | Borrowing | |

| (c) | Underwriting | |

| (d) | Real Estate | |

| (e) | Commodities | |

| (f) | Loans | |

| (g) | Senior Securities | |

| (h) | Diversification |

| Shareholders of the Fund will vote separately on each of Proposals 3(a) through (h). |

Any other business that may properly come before the Meeting or any adjournment of the Meeting.

The Board of Trustees recommends that you vote FOR Proposals 1, 2, and 3(a) through (h).

Each shareholder of record of the Fund as of the close of business on April 3, 2018, is entitled to receive notice of, and to vote at, the Meeting and at any adjournment thereof.

Whether or not you expect to attend the Meeting, please complete and return the enclosed proxy card in the accompanying envelope. No postage is necessary if mailed in the United States.

Important Notice Regarding the Availability of Proxy Materials for

the Shareholder Meeting to Be Held on June 15, 2018:

The Proxy Statement is available at: www.jhinvestments.com/proxy.

By order of the Board of Trustees,

John J. Danello

Secretary

April 6, 2018

Boston, Massachusetts

Your vote is important - Please vote your shares promptly.

Shareholders are invited to attend the Meeting in person. Valid photo identification may be required to attend the Meeting in person. Any shareholder who does not expect to attend the Meeting is urged to vote by:

| (i) | completing the enclosed proxy card(s), dating and signing it, and returning it in the envelope provided, which needs no postage if mailed in the United States; |

| (ii) | following the touch-tone telephone voting instructions found below; or |

| (iii) | following the Internet voting instructions found below. |

In order to avoid unnecessary expense, we ask your cooperation in responding promptly, no matter how large or small your holdings may be.

INSTRUCTIONS FOR EXECUTING PROXY CARDS

The following general rules for executing proxy cards may be of assistance to you and help avoid the time and expense involved in validating your vote if you fail to execute your proxy card(s) properly.

Individual Accounts: Your name should be signed exactly as it appears on the proxy card(s).

Joint Accounts:Either party may sign, but the name of the party signing should conform exactly to a name shown on the proxy card(s).

All other accounts should show the capacity of the individual signing. This can be shown either in the form of the account registration itself or by the individual executing the proxy card(s).

INSTRUCTIONS FOR VOTING BY TOUCH-TONE TELEPHONE

Read the enclosed Proxy Statement, and have your proxy card(s) handy.

Call the toll-free number indicated on your proxy card(s).

Enter the control number found on the front of your proxy card(s).

Follow the recorded instructions to cast your vote.

INSTRUCTIONS FOR VOTING BY INTERNET

Read the enclosed Proxy Statement, and have your proxy card(s) handy.

Go to the Web site on the proxy card(s).

Enter the control number found on the front of your proxy card(s).

Follow the instructions on the Web site.

TABLE OF CONTENTS

JOHN HANCOCK U.S. GLOBAL LEADERS GROWTH FUND,

a series of JOHN HANCOCK CAPITAL SERIES

PROXY STATEMENT

SPECIAL MEETING OF SHAREHOLDERS

TO BE HELD ON JUNE 15, 2018

This Proxy Statement contains the information that a shareholder should know before voting on the proposals described in the notice.The Fund will furnish, without charge, a copy of its Annual Report to any shareholder upon request by writing to the Fund at 601 Congress Street, Boston, Massachusetts 02210 or by calling 1-800-225-5291.

This Proxy Statement is being furnished in connection with the solicitation of proxies by the Board of Trustees (the “Board”) of John Hancock Capital Series (the “Trust”) for use at the special meeting of shareholders of John Hancock U.S. Global Leaders Growth Fund (the “Fund”), a series of the Trust. The special meeting will be held at 601 Congress Street, Boston, Massachusetts 02210, on Friday, June 15, 2018, at 2:00 P.M., Eastern Time (the “Meeting”). The Board is soliciting proxies from shareholders with respect to the proposals set forth in the accompanying notice.

The following table summarizes the proposals.

| Proposal Number | Description of Proposal |

| Proposal 1 | To approve a new subadvisory agreement for the Fund between John Hancock Advisers, LLC and Sustainable Growth Advisers, LP. |

| Proposal 2 | To approve a manager of managers structure. |

| Proposal 3(a) | To approve a revised fundamental investment restriction regarding concentration. |

| Proposal 3(b) | To approve a revised fundamental investment restriction regarding borrowing. |

| Proposal 3(c) | To approve a revised fundamental investment restriction regarding underwriting. |

| Proposal 3(d) | To approve a revised fundamental investment restriction regarding real estate. |

| Proposal 3(e) | To approve a revised fundamental investment restriction regarding commodities. |

| Proposal 3(f) | To approve a revised fundamental investment restriction regarding loans. |

| Proposal 3(g) | To approve a revised fundamental investment restriction regarding senior securities. |

| Proposal 3(h) | To approve a new fundamental investment restriction regarding diversification. |

The definitive Proxy Statement and proxy card are intended to be first mailed to shareholders on or about April 16, 2018.

The Fund’s Advisor, Administrator, Distributor, and Subadvisor

John Hancock Advisers, LLC (the “Advisor”), 601 Congress Street, Boston, Massachusetts, 02210, serves as the Fund’s investment advisor and administrator. An affiliate of the Advisor, John Hancock Funds, LLC, 601 Congress Street, Boston, Massachusetts 02210, serves as the Fund’s distributor. Sustainable Growth Advisers, LP (the “Subadvisor”), 3 Stamford Plaza, Suite 1310, 301 Tresser Blvd., Stamford, Connecticut 06901, serves as the Fund’s subadvisor.

Record Ownership

The Board has fixed the close of business on April 3, 2018 as the record datefor determining shareholders eligible to vote at the Meeting (the “Record Date”).All shareholders of record at the close of business on the Record Date are entitled to one vote for each share (and fractional votes for fractional shares)on all business of the Meeting or any adjournment of the Meeting. On the Record Date, 31,159,932,626 shares of beneficial interest of the Fund were outstanding.

As of the Record Date, none of the Trustees beneficially owned individually, and the Trustees and executive officers of theFund as a group did not beneficially own, in excess of one percent of the outstanding shares of the Fund. Information regarding shareholders that hold 5% or more of the Fund’s shares as of the Record Date is set forth in Appendix A to this Proxy Statement (“Outstanding Shares and Share Ownership”).

Proposal 1 - Approval of New Subadvisory Agreement

On February 2, 2018, it was announced that the subadvisor had agreed to sell a majority ownership stake to Virtus Investment Partners (“Virtus”), a multi-boutique asset manager, based in Hartford, Connecticut (the “Virtus Transaction”). The Virtus Transaction is expected to close by June 30, 2018. The Virtus Transaction, when it closes, will constitute a “change of control” of the Subadvisor under the Investment Company Act of 1940, as amended (the “1940 Act”), but it is not expected to result in a change on the personnel or operations of the Subadvisor, any changes in the Subadvisor’s investment approach with respect to the Fund’s portfolio management, or any changes in the subadvisory fee paid to the Subadvisor by the Advisor.

Section 15(a)(4) of the 1940 Act requires all investment advisory agreements, including subadvisory agreements, to provide for their automatic termination in the event that they are assigned. Because the Virtus Transaction will result in a change in control of the Subadvisor, the current subadvisory agreement between and among the Trust, the Advisor, and the Subadvisor dated February 16, 2004, as amended on March 31, 2008, March 11, 2013, and June 1, 2013 (collectively, the “Current Subadvisory Agreement”) will be deemed to have been assigned, thereby triggering the automatic termination provision of Section 15(a)(4).

Due to the termination of the Current Subadvisory Agreement, the Fund’s shareholders are being asked to approve a new subadvisory agreement between the Advisor and the Subadvisor (the “New Subadvisory Agreement”). The New Subadvisory Agreement will not affect the Fund’s investment approach or the individuals providing subadvisory services to the Fund.Approval of the New Subadvisory Agreement will not change the annual advisory fee rates payable by the Fund to the Advisor. The subadvisory fees are payable by the Advisor and not the Fund and will not be changed by approval of the New Subadvisory Agreement.

At its in-person meeting held on March 19-22, 2018, the Board approved the New Subadvisory Agreement. The Board recommends that the Fund’s shareholders approve the New Subadvisory Agreement.

The Subadvisor is responsible for formulating the Fund’s investment program. The Subadvisor was founded in 2003 and manages approximately $11.6 billion as of December 31, 2017, of which approximately $10.0 billion is regulatory assets under management and $1.6 billion is model/emulation assets under contract. Currently, George P. Fraise, Gordon M. Marchand, and Robert L. Rohn each owns approximately 15% of the Subadvisor.

The Fund is the successor to U.S. Global Leaders Growth Fund (the “Predecessor Fund”), a series of Professionally Managed Portfolios, a Massachusetts business trust, which merged with the Fund on May 17, 2002. The Fund was subadvised by Yeager, Wood & Marshall, Inc. (“YWM”) until July 16, 2003. Thereafter, the Advisor directly managed the Fund’s assets until February 16, 2004, when the Fund’s shareholders approved a subadvisory agreement with Sustainable Growth Advisers, LP, the Fund’s current Subadvisor.

As the Fund’s portfolio managers, Messrs. Fraise, Marchand, and Rohn are jointly and primarily responsible for the day-to-day management of the Fund’s portfolio. Messrs. Fraise, Marchand, and Rohn have managed the Fund (including service on the Predecessor Fund) since 2000, 1995, and 2003, respectively, and are expected to continue to manage the Fund under the New Subadvisory Agreement. During the period between the termination of the

| 2 |

subadvisory agreement with YWM and the effective date of the Current Subadvisory Agreement, Messrs. Fraise, Marchand, and Rohn managed the Fund’s assets under a dual-employment arrangement between the Advisor and Sustainable Growth Advisers, LP.

The Subadvisor serves as the Fund’s subadvisor pursuant to the Current Subadvisory Agreement. The Board most recently approved the Current Subadvisory Agreement at its June 19-22, 2017 meeting.

If Proposal 1 is approved by the Fund’s shareholders, the New Subadvisory Agreement is expected to become effective promptly thereafter.

If the Fund’s shareholders do not approve Proposal 1, the New Subadvisory Agreement will not take effectand the Board will consider what other action to take.

Comparison of the Current and New Subadvisory Agreements

The material terms of the New Subadvisory Agreement, are substantially the same as those of the Current Subadvisory Agreement, and the subadvisory fee payable to the Subadvisor is the same under each Agreement. Other than the effective date of the New Subadvisory Agreement, which will be on or shortly after the date that shareholder approval is obtained, the only significant difference from the Current Subadvisory Agreement is that the Trust is not a party to the New Subadvisory Agreement, consistent with more recent subadvisory agreements for the John Hancock funds. The New Subadvisory Agreement will have an initial two-year term, and thereafter, as is the case with the Current Subadvisory Agreement, must be specifically approved at least annually either by: (a) the Board; or (b) a Majority of the Outstanding Voting Securities of the Fund (as defined below). Any such continuance also requires the approval of a majority of the Trustees of the Trust who are not “interested persons” (as defined in the 1940 Act) of the Trust, the Advisor, or the Subadvisor (the “Independent Trustees”).

A copy of the form of New Subadvisory Agreement is included in Appendix B to this proxy statement.

Duties. The Subadvisor will manage the Fund’s investment program, subject to the supervision of the Board and the Advisor. The Subadvisor will, at its own expense, furnish all necessary investment and management facilities, including salaries of personnel required for it to execute its duties, as well as administrative facilities, including bookkeeping, clerical personnel, and equipment necessary for the conduct of the Fund’s investment affairs.

The Subadvisor’s duties under the New Subadvisory Agreement are the same as under the Current Subadvisory Agreement.

Compensation. As compensation for its services to the Fund, the Subadvisor will receive from the Advisor a management fee that is stated as an annual percentage of the aggregate net assets of the Fund determined in accordance with the following schedule.

| Average daily net assets ($) | Annual rate (%) |

| First 500 million | 0.2625% |

| Next 500 million | 0.2425% |

| Next 1 billion | 0.2225% |

| Next 3 billion | 0.2125% |

| Excess over 5 billion | 0.1625% |

The compensation payable to the Subadvisor under the New Subadvisory Agreement is the same as under the Current Subadvisory Agreement.

The aggregate amount of subadvisory fees that the Advisor paid to the Subadvisor during the fiscal year ended October 31, 2017 pursuant to the Current Subadvisory Agreement was $3,192,498.92. If the New Subadvisory Agreement had been in effect during that period, the amount paid to the Subadvisor would have been the same. As noted above, the Advisor, and not the Fund, is responsible for payment of these fees to the Subadvisor.

| 3 |

Liability.Each Agreement provides that neither the Subadvisor nor any of its directors, officers, employees, shareholders, partners, or agents will be liable to the Advisor or the funds for any error of judgment or mistake of law or for any loss suffered by the Advisor or the Fund in connection with the matters to which the Agreement relates, except for losses resulting from willful misfeasance, bad faith or gross negligence in the performance of, or from the reckless disregard of, the duties of the Subadvisor under the Agreement or its directors, officers, employees, shareholders, partners, or agents.

Term. The New Subadvisory Agreement has an initial two-year term, and its continuance must be specifically approved thereafter at least annually either by: (a) the Board; or (b) a Majority of the Outstanding Voting Securities (as defined below) of the Fund. Any such continuance also requires the approval of a majority of the Independent Trustees.

In this Proxy Statement, the term “Majority of the Outstanding Voting Securities” of the Fund means the affirmative vote of the lesser of:

| (1) | 67% or more of the voting securities of the Fund, present at the Meeting, if the holders of more than 50% of the outstanding voting securities of the Fund are present in person or by proxy; or | |

| (2) | more than 50% of the outstanding voting securities of the Fund. |

Termination. The Current Subadvisory Agreement may be terminated at any time, without payment or penalty: (a) by the Board, by vote of a Majority of the Outstanding Voting Securities of the Fund, or by the Advisor on 30 days’ written notice to the Subadvisor; or (b) by the Subadvisor on 90 days' written notice to the Fund and the Advisor. The New Subadvisory Agreement may be terminated at any time, without payment or penalty: (a) by the Board or by vote of a Majority of the Outstanding Voting Securities of the Fund, on 60 days’ written notice to the Advisor and the Subadvisor; or (b) by the Advisor or Subadvisor on 60 days' written notice to the Fund and the other party.

Each Agreement will automatically terminate in the event of its assignment.

Amendments.Each Agreement may be amended by the parties thereto, provided the amendment is approved by the vote of a majority of the Trustees of the fund, including a majority of the Independent Trustees. Any required shareholder approval shall be effective with respect to the Fund if a Majority of the Outstanding Voting Securities of the Fund vote to approve the amendment.

Insurance. The Current Subadvisory Agreement requires the Subadvisor to maintain at all times insurance coverage for errors and omissions of not less than $1 million (including a deductible not in excess of $100,000). Such coverage includes an endorsement providing at least thirty days’ advance notice of any amendment or cancelation of such insurance coverage to be provided by the insurance company directly to the Advisor. Although the New Subadvisory Agreement is silent on this topic, the Advisor has evaluated the Subadvisor’s financial condition, including any customary or legally required insurance arrangements related to the Subadvisor’s activities, and has concluded that such arrangements are appropriate to cover the Subadvisor’s potential liability for errors and omissions. As a practical matter, the Advisor believes that there is no additional risk to the Fund as a result of this difference in contractual provisions.

Information About the Subadvisor

The Subadvisor is a Delaware limited partnership having its principal offices at 3 Stamford Plaza, Suite 1310, 301 Tresser Blvd., Stamford, Connecticut 06901. The Subadvisor is registered as an investment advisor under the Investment Advisers Act of 1940, as amended. Currently, George P. Fraise, Gordon M. Marchand, and Robert L. Rohn each owns approximately 15% of the Subadvisor.

The following table sets forth the principal executive officers and managers of the Subadvisor. No principal executive officer or manager of the Subadvisor has a position with the Trust. The business address of each such person is 3 Stamford Plaza, Suite 1310, 301 Tresser Blvd., Stamford, Connecticut 06901.

| 4 |

| Name | Position with the Subadvisor and Principal Occupation |

| Gordon M. Marchand | Principal of the Subadvisor; Portfolio Manager of the Fund and other accounts managed by the Subadvisor |

| George P. Fraise | Principal of the Subadvisor; Portfolio Manager of the Fund and other accounts managed by the Subadvisor |

| Robert L. Rohn | Principal of the Subadvisor; Portfolio Manager of the Fund and other accounts managed by the Subadvisor |

| Alexandra S. Lee | Research Principal of the Subadvisor; investment analyst of accounts managed by the Subadvisor |

| Kishore D. Rao | Research Principal of the Subadvisor; investment analyst of accounts managed by the Subadvisor |

| Michael T. Brown | Research Principal of the Subadvisor; investment analyst of accounts managed by the Subadvisor |

| Peter J. Seuffert | Chief Operating Officer of the Subadvisor |

| Daniel C. Callaway | Chief Compliance Officer of the Subadvisor |

During the fiscal year ended October 31, 2017, the Fund did not pay brokerage commissions to any affiliated broker-dealer.

The Subadvisor manages other investment companies with an investment objective similar to that of the Fund. The following table identifies each such other investment company, its assets as of December 31, 2017, the rate of advisory or subadvisory fees payable to the Subadvisor, and whether the Subadvisor has waived or reduced its fees during such investment company’s last fiscal year, or has contractually agreed to reduce its fees.

| Other Investment Company | Assets as of 12/31/17 | Advisory or Subadvisory Fee Schedule | Has Subadvisor Waived Fees in Last FYE? | Has Subadvisor Contractually Agreed to Waive Fees? |

| Bridge Builder Large Cap Growth Fund | $1,820,545,662 | 0.25% on First $500 million 0.2125% on Next $1.5 billion 0.2% in Excess of $2.0 billion | No | No |

Hirtle Callaghan

Hirtle Callaghan Trust

| $295,714,898

$248,939,449

| 0.35% on First $200 million 0.3% on Next $200 million 0.25% on Next $200 million 0.22% on Next $400 million 0.2% in Excess of $1 billion | No | No |

| Liberty All-Star Equity Fund | $264,085,014 | 0.4% on First $400 million 0.36% on Next $400 million 0.324% on Next $400 million

| No | No |

| 5 |

| Other Investment Company | Assets as of 12/31/17 | Advisory or Subadvisory Fee Schedule | Has Subadvisor Waived Fees in Last FYE? | Has Subadvisor Contractually Agreed to Waive Fees? |

0.292% in Excess of $1.2 billion | ||||

| Liberty All-Star Growth Fund | $50,279,116 | 0.4% on First $300 million

0.36% in Excess of $300 million

| No | No |

Board’s Evaluation and Recommendation

At an in-person meeting held on March 19-22, 2018, the Board, including all the Independent Trustees, approved the New Subadvisory Agreement.In considering the approval of the New Subadvisory Agreement, the Board took into account certain information and materials relating to the Subadvisor that the Board had received and considered in connection with the annual evaluation of the Current Subadvisory Agreement between and among the Trust, on behalf of the Fund, the Advisor, and the Subadvisor at the in-person meetings held on May 22-24, 2017 and June 19-22, 2017. A discussion of the bases of the Board’s approval of the Current Subadvisory Agreement is included in Appendix C to this Proxy Statement.

At the March 19-22, 2018 meeting, the Board revisited the factors it previously considered at theMay 22-24, 2017 and June 19-22, 2017meetings to the extent relevant to the New Subadvisory Agreement and reached the same conclusions with respect to those factors, as set forth in Appendix C to this Proxy Statement. The Board also took into account additional information that it considered relevant in its evaluation of the New Subadvisory Agreement and in connection therewith reviewed materials provided by the Advisor comparing the Current and New Subadvisory Agreement, and materials provided by the Subadvisor regarding the Virtus Transaction.

The Board reviewed with respect to the Fund the nature, extent and quality of services provided by the Subadvisor, including the quality and depth of the investment professionals having principal investment responsibility for managing the Fund’s investments and the performance record of those professionals. The Board considered the Subadvisor’s history and experience providing services to the Fund, including the Fund’s performance record.

In addition to evaluating the nature, extent and quality of services provided by the Subadvisor, the Board reviewed the contractual subadvisory fee rates payable to the Subadvisor with respect to the Fund. The Board noted that the subadvisory fees are paid by the Advisor and not by the Fund and that the Board relies on the ability of the Advisor to negotiate the subadvisory fees at arm’s-length. The Board further noted that neither the advisory fees paid by the Fund nor the subadvisory fees paid by the Advisor will change under the New Subadvisory Agreement.

In evaluating the impact of the Virtus Transaction, the Board noted that no changes were planned to the Fund’s current portfolio management team or investment approach after the closing of the Virtus Transaction. In addition, the Board considered the Subadvisor’s representations that the Virtus Transaction would provide the Subadvisor with an opportunity to take advantage of full autonomy regarding its business, such as greater latitude to hire and reward investment and research staff and more freedom to pursue market opportunities.

Based on its review, the Board, including the Independent Trustees, determined that the terms of the New Subadvisory Agreement, including the fee rates, were fair and reasonable and in the best interests of the Fund and its shareholders, and unanimously approved the New Subadvisory Agreement.

| 6 |

The Board, including all the Independent Trustees, recommends that the Fund’s shareholders vote “FOR” Proposal 1.

Proposal 2 - Approval of Manager of Managers Structure

The Advisor serves as the Fund’s investment manager, subject to the supervision of the Board, pursuant to an Advisory Agreement between the Trust, on behalf of the Fund, and the Advisor. The Advisor is permitted under the Advisory Agreement, at its own expense, to select and contract with one or more investment subadvisors to perform some or all of the investment advisory services for which the Advisor is responsible under the Advisory Agreement.

If the Advisor delegates portfolio management duties to a subadvisor with respect to the Fund, the 1940 Act requires that the subadvisory agreement must be approved by the Fund’s shareholders. Specifically, Section 15 of the 1940 Act makes it unlawful for any person to act as an investment manager (including as a subadvisor) to a registered investment company, except pursuant to a written contract that has been approved by shareholders. Therefore, to comply with Section 15 of the 1940 Act, the Fund must obtain shareholder approval of a subadvisory agreement in order to employ a subadvisor, replace an existing subadvisor with a new subadvisor, materially change the terms of a subadvisory agreement, or continue the employment of an existing subadvisor whose subadvisory agreement terminates because of an assignment (as such term is defined under the 1940 Act). Proposal 1, relating to the approval of the New Subadvisory Agreement, illustrates this last situation.

Because of the expense and delay associated with obtaining shareholder approval of subadvisors and related subadvisory agreements, many mutual fund investment managers have requested and obtained orders from the SEC exempting them and the mutual funds they manage from certain requirements of Section 15 of the 1940 Act and the rules thereunder. Subject to certain specified conditions, these orders permit the covered mutual funds and their respective managers to employ a “manager of managers” structure with respect to the funds, whereby the investment managers may retain unaffiliated subadvisors for the funds and change the terms of a subadvisory agreement without obtaining shareholder approval.

On January 27, 2000, the SEC issued an exemptive order pursuant to Section 6(c) of the 1940 Act that allows the Advisor to enter into and materially amend subadvisory agreements without shareholder approval. This order does not extend to a subadvisor that is an “affiliated person,” as defined in Section 2(a)(3) of the 1940 Act, of the Trust or the Advisor, other than by reason of serving as a subadvisor to an investment company managed by the Advisor or its affiliates. Before a fund relies on this order, the fund’s shareholders must approve the fund’s operation under the manager of managers structure described in the order. A John Hancock mutual fund that commenced operations after the order was granted has obtained such approval by consent of such fund’s initial shareholder prior to the fund’s public offering. However, because the Fund commenced operations prior to the granting of the order, it is necessary for the Fund’s current shareholders to approve the Fund’s operation under the manager of managers structure. (Other John Hancock mutual funds that commenced operations after the order was granted have obtained such approval by consent of each such fund’s initial shareholder prior to the fund’s public offering). This order will become effective with respect to the Fund, and the Fund will commence operations under the manager of manager structure, only upon shareholder approval of Proposal 2 and upon disclosure of the structure in the Fund’s prospectus.

The proposed manager of managers structure would permit the Advisor, as the Fund’s investment manager, to make changes to the Fund’s subadvisors and materially amend subadvisory agreements without shareholder approval. This would allow the Advisor, subject to the Board’s approval, to select new or additional subadvisors for the Fund and terminate and replace existing subadvisors to the Fund. The manager of managers structure is intended to enable the Fund to operate with greater efficiency and help the Fund enhance performance by allowing the Board and the Advisor to employ subadvisors best suited to the needs of the Fund without incurring the expense and delay associated with obtaining shareholder approval of a new subadvisor and its subadvisory agreement. The Board believes that it is in the best interests of the Fund and its shareholders to adopt a manager of managers structure. A discussion of the factors considered by the Board is set forth in the section below entitled “Board Approval of Manager of Managers Structure.”

| 7 |

The process of seeking shareholder approval can be administratively expensive to the Fund and may cause delays in executing changes that the Board and the Advisor have determined are necessary or desirable. These costs are often borne by the Fund (and therefore indirectly by the Fund’s shareholders). Further, if a subadvisor of the Fund is involved in a corporate transaction that could be deemed to result in an assignment of its subadvisory agreement (such as is described in Proposal 1 with respect to the Subadvisor), the Fund currently must seek shareholder approval of a new subadvisory agreement, even where there will be no change in the individuals managing the Fund or the subadvisory fee paid to the subadvisor. If the Fund’s shareholders approve the policy authorizing a manager of managers structure for the Fund, the Board would be able to act more quickly, and with less expense to the Fund, to appoint an unaffiliated subadvisor, in instances in which the Board and the Advisor believe that the appointment would be in the best interests of the Fund and its shareholders.

The Board, including the Independent Trustees, would continue to oversee the subadvisor selection process under the manager of managers structure to help ensure that the interests of shareholders are protected whenever the Advisor would seek to select a subadvisor or modify a subadvisory agreement. Specifically, the Board, including the Independent Trustees, would evaluate and approve each subadvisory agreement as well as any modification to an existing subadvisory agreement. The Board, including a majority of the Independent Trustees, will continue to be required to review and consider the continuance of each subadvisory agreement at least annually, after the expiration of the initial term. In reviewing new or existing subadvisory agreements or modifications to existing subadvisory agreements, the Board will analyze all factors that it considers to be relevant to its determination, including the subadvisory fees, the nature, quality and scope of services to be provided by the subadvisor, the investment performance of the assets managed by the subadvisor in the particular style for which a subadvisor is sought, as well as the subadvisor’s compliance with federal securities laws and regulations. The Advisor and each subadvisor will continue to have a legal duty to provide the Board with information on all factors pertinent to the Board’s decision regarding the subadvisory arrangement.

Furthermore, operation of the Fund under the proposed manager of managers structure would not: (1) permit investment management fees paid by the Fund to the Advisor to be increased without shareholder approval, or (2) diminish the Advisor’s responsibilities to the Fund, including the Advisor’s overall responsibility for the portfolio management services furnished by a subadvisor. Under the structure, the Advisor would continue to supervise and oversee the activities of the subadvisors to the Fund, monitor each subadvisor’s performance and make recommendations to the Board about whether its subadvisory agreement should be continued, modified or terminated. The Advisor will only enter into new or materially amended subadvisory agreements with shareholder approval, to the extent required by applicable law.

Under the manager of managers structure, the Fund’s shareholders would receive notice of, and information pertaining to, any new subadvisory agreement or any material change to an existing subadvisory agreement for the Fund. In particular, shareholders would receive the same information about a new subadvisory agreement and a new subadvisor that they would have received in a proxy statement related to their approval of a new subadvisory agreement in the absence of a manager of managers structure.

If Proposal 2 is approved by the Fund’s shareholders,the adoption of a manager of managers structure is expected to become effective immediately upon approval and upon disclosure of the structure in the Fund’s prospectus.

If the Fund’s shareholders do not approve Proposal 2,the proposed manager of managers structure will not take effect.

Board Approval of Manager of Managers Structure

At its in-person meeting held on March 19-22, 2018, the Board, including the Independent Trustees, unanimously approved the use of the manager of managers structure and determined: (1) that it would be in the best interests of the Fund and its shareholders; and (2) to obtain shareholder approval of the structure. In evaluating this structure, the Board, including the Independent Trustees, considered various factors and other information, including the following:

| 1. | A manager of managers structure will enable the Board to act more quickly, with less expense to the Fund, in employing an unaffiliated subadvisor, replacing an existing subadvisor with a new |

| 8 |

unaffiliated subadvisor, materially changing the terms of an agreement with an unaffiliated subadvisor, or continuing the employment of an existing unaffiliated subadvisor whose agreement terminates because of its assignment when the Board and the Advisor believe that any such actions would be in the best interests of the Fund and its shareholders. For example, if a manager of managers structure had been in place for the Fund, the approval of the New Subadvisory Agreement necessitated by the Virtus Transaction could have been approved by the Board without incurring the time and expense involved in holding a special shareholder meeting and issuing a proxy statement to solicit shareholder approval;

| 2. | The Advisor would continue to be directly responsible for monitoring a subadvisor’s compliance with the Fund’s investment objectives and investment strategies and analyzing the performance of the subadvisor; |

| 3. | The management fees paid by the Fund to the Advisor would remain the same and any increase in management fees would require shareholder approval; and |

| 4. | No unaffiliated subadvisor could be appointed, removed or replaced without the Board’s approval and involvement. |

The Board, including all the Independent Trustees, recommends that the Fund’s shareholders vote “FOR” Proposal 2.

Proposal 3 ─ Approval of REVISion or establishment of FUNDAMENTAL RESTRICTIONS

The Fund has adopted investment policies. Investment policies that can only be changed by a vote of shareholders are considered “fundamental.” The 1940 Act requires that certain policies, including those dealing with industry concentration, diversification, borrowing money, underwriting securities of other issuers, purchasing or selling real estate or commodities, making loans and the issuance of senior securities be fundamental. The Board may elect to designate other policies as fundamental. The fundamental policies described in Proposal 3(a) through (h) are referred to as “investment restrictions.” The Fund’s current fundamental investment restrictions are set forth in the Fund’s registration statement in the Statement of Additional Information (the “SAI”).

Shareholders of the Fund are being asked to approve amendments and restatements of the current fundamental investment restrictions that apply to the Fund, and a new fundamental restriction relating to the Fund’s classification as a diversified investment company under the 1940 Act. The amendment to each current investment restriction is set forth in a separate proposal below (Proposals 3(a) through (g)), and the new investment restriction relating to diversification is set forth in a separate Proposal 3(h). The Advisor has reviewed each of the current investment restrictions and has recommended to the Board that they be amended and restated, and has recommended that a formal investment restriction be established regarding diversification.

The primary purpose of the proposed amendments and new restriction is to conform and standardize the investment restrictions that apply to the Fund and to other John Hancock funds. Standardizing the investment restrictions across the John Hancock funds is expected to facilitate more effective management of the Fund by the Advisor and the subadvisor, enhance monitoring compliance with applicable restrictions, and eliminate conflicts among comparable restrictions resulting from minor variations in their terms. In addition, to reflect changes over time in industry practices and regulatory requirements, the proposed amendments are intended to update those fundamental restrictions that are more restrictive than are required under the federal securities laws. The proposed amendments and new diversification restriction are also intended to simplify the Fund’s fundamental restrictions and to incorporate maximum flexibility that will permit the investment restrictions to accommodate future regulatory changes without the need for further shareholder action. The proposed amendments and new diversification restriction are substantially similar to the current corresponding fundamental restrictions and current classification, respectively, and are not

| 9 |

expected to have any material effect on the manner in which the Fund is managed or on its current investment objective.

The Board has concluded that the proposed amendments to the investment restrictions and new diversification restriction are appropriate and will benefit the Fund and its shareholders.TheBoardunanimouslyrecommendsthatshareholdersof the Fundapprovetheproposedamendments and new diversification restriction.

If approved by the Fund’s shareholders, each amended investment restriction and the new diversification restriction will become effective when the Fund’s SAI is revised or supplemented to reflect the amendment. Assuming that one or more of the proposed amendments is approved at the Meeting, the Fund expects to file a revision or supplement to its SAI on or about June 30, 2018.

If a proposed amendment is not approved by the Fund’s shareholders, the current investment restriction will remain in effect. If the new diversification restriction is not approved by the Fund’s shareholders, the Fund will continue to operate as a diversified fund, but will not state this classification as a fundamental investment restriction.

Proposal 3(a) — Amended Fundamental Restriction Relating to Concentration

Under the 1940 Act, the Fund’s policy regarding concentration of investments in the securities of companies in any particular industry must be fundamental. While the 1940 Act does not define what constitutes “concentration” in an industry, the staff of the Securities and Exchange Commission (the “SEC”) takes the position that any fund that invests more than 25% of its total assets in a particular industry (excluding the U.S. Government, its agencies or instrumentalities) is deemed to be “concentrated” in that industry.

The following table sets forth the statement of the Fund’s current investment restriction relating to concentration and the proposed revision.

| Current Fundamental Restriction Relating to Concentration | Proposed Revision |

| The Fund may not purchase the securities of issuers conducting their principal activity in the same industry if, immediately after such purchase, the value of its investments in such industry would exceed 25% of its total assets taken at market value at the time of such investment. This limitation does not apply to investments in obligations of the U.S. Government or any of its agencies, instrumentalities or authorities. | The Fund may not concentrate its investments in a particular industry, as that term is used in the 1940 Act, as amended, and as interpreted or modified by regulatory authority having jurisdiction, from time to time. |

Discussion of Proposal.The proposed amendment permits investment in an industry up to the most recently prescribed limits under the 1940 Act and related regulatory interpretations. In addition, the proposed amendment is expected to reduce administrative and compliance burdens by simplifying and making uniform the fundamental investment restriction with respect to concentration. As noted, the 1940 Act does not define what constitutes “concentration” in an industry, but the SEC has taken the position that investment of 25% or more of a fund’s total assets in one or more issuers conducting their principal business activities in the same industry (excluding the U.S. Government, its agencies or instrumentalities) constitutes concentration. The Fund’s proposed fundamental restriction is consistent with this interpretation.

The Board, including all the Independent Trustees, recommends that the Fund’s shareholders vote “FOR” Proposal 3(a).

* * *

| 10 |

Proposal 3(b) — Amended Fundamental Restriction Relating to Borrowing

Under Section 18(f)(1) of the 1940 Act, a fund may not borrow money, except as expressly permitted by Section 18. Sections 8(b)(1)(B) and 13(a)(2) of the 1940 Act together require the Fund to have a fundamental investment restriction addressing borrowing.

The 1940 Act permits the Fund to borrow money in amounts of up to one-third of its total assets, at the time of borrowing, from banks for any purpose (the Fund’s total assets include the amounts being borrowed). To limit the risks attendant to borrowing, the 1940 Act requires the Fund to maintain at all times an “asset coverage” of at least 300% of the amount of its borrowings, not including borrowings for temporary purposes in an amount not exceeding 5% of the value of its total assets. “Asset coverage” means the ratio that the value of the Fund’s total assets (including amounts borrowed), minus liabilities other than borrowings, bears to the aggregate amount of all borrowings.

The following table sets forth the statement of the Fund’s current investment restriction relating to borrowing and the proposed revision.

| Current Fundamental Restriction Relating to Borrowing | Proposed Revision |

| The Fund may not borrow money, except: (i) for temporary or short-term purposes or for the clearance of transactions in amounts not to exceed 33⅓% of the value of the Fund’s total assets (including the amount borrowed) taken at market value; (ii) in connection with the redemption of Fund shares or to finance failed settlements of portfolio trades without immediately liquidating portfolio securities or other assets, (iii) in order to fulfill commitments or plans to purchase additional securities pending the anticipated sale of other portfolio securities or assets; (iv) in connection with entering into reverse repurchase agreements and dollar rolls, but only if after each such borrowing there is asset coverage of at least 300% as defined in the 1940 Act; and (v) as otherwise permitted under the 1940 Act. For purposes of this investment restriction, the deferral of trustees’ fees and transactions in short sales, futures contracts, options on futures contracts, securities or indices and forward commitment transactions shall not constitute borrowing. | The Fund may not borrow money, except as permitted under the 1940 Act, as amended, and as interpreted or modified by regulatory authority having jurisdiction, from time to time. |

Discussion of Proposal. Under the proposed amendment, the Fund’s ability to borrow money is not subject to the limitation included in the current investment restriction that the Fund may borrow only for temporary or emergency purposes (not for leverage). To the extent that the Fund borrows money, positive or negative performance by the Fund’s investments may be magnified. Therefore, borrowed money creates an opportunity for greater capital gain but at the same time increases exposure to capital risk.

In the same manner as the current investment restriction, the proposed borrowing restriction would provide the Fund with borrowing flexibility by permitting it to engage in transactions that technically could constitute borrowings, such as reverse repurchase agreements and mortgage dollar rolls, but that have been permitted by the SEC and its staff, subject to the satisfaction of certain conditions designed to reduce or eliminate the leveraging effects of such transactions. However, under the proposed amendment, the Fund would not have to determine whether a particular transaction is “similar” to a reverse repurchase agreement or mortgage dollar roll. To the extent that the Fund uses such flexibility in the future, the Fund may be subject to some additional costs and risks inherent in borrowing, such as reduced total return and increased volatility. The proposed amendment also conforms the Fund’s investment restriction relating to borrowing to a format that has become standard for the John Hancock fund complex.

| 11 |

The Fund does not have a present intention to borrow for leveraging purposes, although the Fund may do so in the future, with Board approval.

The Board, including all the Independent Trustees, recommends that the Fund’s shareholders vote “FOR” Proposal 3(b).

* * *

Proposal 3(c) — Amended Fundamental Restriction Relating to Underwriting

Sections 8(b)(1)(D) and 13(a)(2) of the 1940 Act together require that the Fund have an investment restriction addressing the underwriting of securities. Section 12(c) of the 1940 Act prohibits a fund that is a diversified investment company from making any underwriting commitments in excess of limits set forth in that Section. The Fund does not intend to enter into formal underwriting commitments. The Fund may acquire restricted securities (i.e., securities that may be sold only if registered under the Securities Act of 1933, as amended, or pursuant to an exemption from registration such as that provided by Rule 144A). These acquisitions, however, are not deemed to be underwriting commitments within the meaning of Section 12(c).

The following table sets forth the statement of the Fund’s current investment restriction relating to underwriting and the proposed revision.

| Current Fundamental Restriction Relating to Underwriting | Proposed Revision |

| The Fund may not act as an underwriter, except to the extent that in connection with the disposition of portfolio securities, the Fund may be deemed to be an underwriter for purposes of the Securities Act of 1933. | The Fund may not engage in the business of underwriting securities issued by others, except to the extent that the Fund may be deemed to be an underwriter in connection with the disposition of portfolio securities |

Discussion of Proposal. The amendment revises the current investment restriction without making any material change and will conform the Fund’s restriction relating to underwriting to a format that has become standard for the John Hancock fund complex.

The Board, including all the Independent Trustees, recommends that the Fund’s shareholders vote “FOR” Proposal 3(c).

* * *

Proposal 3(d) — Amended Fundamental Restriction Relating to Real Estate

Sections 8(b)(1)(F) and 13(a)(2) of the 1940 Act together require the Fund to have an investment restriction governing the purchase or sale of real estate. The 1940 Act does not prohibit an investment company from investing in real estate, either directly or indirectly.

| 12 |

The following table sets forth the statement of the Fund’s current investment restriction relating to real estate and the proposed revision.

| Current Fundamental Restriction Relating to Real Estate | Proposed Revision |

| The Fund may not purchase, sell or invest in real estate, but subject to its other investment policies and restrictions may invest in securities of companies that deal in real estate or are engaged in the real estate business. These companies include real estate investment trusts and securities secured by real estate or interests in real estate. The Fund may hold and sell real estate acquired through default, liquidation or other distributions of an interest in real estate as a result of the Fund’s ownership of securities. | The Fund may not purchase or sell real estate, which term does not include securities of companies which deal in real estate or mortgages or investments secured by real estate or interests therein, except that the Fund reserves freedom of action to hold and to sell real estate acquired as a result of the Fund’s ownership of securities. |

Discussion of Proposal. The proposed restriction permits the Fund to invest directly in securities issued by companies investing in real estate and interests in real estate as well as in mortgages and mortgage-backed securities. The proposal also permits the Fund to hold and to sell real estate acquired as a result of the Fund’s ownership of securities. The amendment will conform the Fund’s investment restriction with respect to real estate to a format that has become standard for the John Hancock fund complex.

The Board, including all the Independent Trustees, recommends that the Fund’s shareholders vote “FOR” Proposal 3(d).

* * *

Proposal 3(e) — Amended Fundamental Restriction Relating to Commodities

Sections 8(b)(1)(F) and 13(a)(2) of the 1940 Act together require that the Fund have an investment restriction dealing with the purchase or sale of commodities. Under the federal securities and commodities laws, certain financial instruments such as futures contracts and options thereon, including currency futures, stock index futures or interest rate futures, may, under certain circumstances, also be considered to be commodities. Mutual funds typically invest in futures contracts and related options on these and other types of commodity contracts for hedging purposes, to implement tax or cash management strategies, or to enhance returns.

The following table sets forth the statement of the Fund’s current investment restriction relating to commodities and the proposed revision.

| Current Fundamental Restriction Relating to Commodities | Proposed Revision |

| The Fund may not invest in commodities or commodity futures contracts, other than financial derivative contracts. Financial derivatives include forward currency contracts; financial futures contracts and options on financial futures contracts; options and warrants on securities, currencies and financial indices; swaps, caps, floors, collars and swaptions; and repurchase agreements entered into in accordance with the Fund’s investment policies. | The Fund may not purchase or sell commodities, except as permitted under the 1940 Act, as amended, and as interpreted or modified by regulatory authority having jurisdiction, from time to time. |

Discussion of Proposal. The present restriction does not permit the Fund to purchase physical commodities. Under the proposed amendment, the Fund would be permitted to purchase or sell commodities as permitted by the 1940 Act and as interpreted or modified by regulatory authority having jurisdiction. Currently, the 1940 Act does not prohibit

| 13 |

investments in physical commodities or contracts related to physical commodities. As a result, if this proposal is approved by the Fund’s shareholders, the Fund would have the flexibility to invest in physical commodities and contracts related to physical commodities to the extent the Advisor and the Board determine such investments could assist the Fund in achieving its investment objective and are consistent with the best interests of the Fund’s shareholders.

If the Fund were to invest in a physical commodity or a contract related to a physical commodity, it would be subject to the additional risks of such an investment. These may include price volatility, relative illiquidity, and market speculation by other investors in such commodity or related contracts. The proposed amendment also permits the Fund to invest in securities, derivatives and other instruments backed by or linked to commodities of all types including physical commodities, other investment companies and other investment vehicles that invest in commodities or commodity linked investments. Under certain market conditions, derivatives could become harder to value and may become illiquid. Also, the Fund would bear underlying fund fees and expenses indirectly. Thus, the Fund would have additional flexibility to invest in all types of financial instruments that are considered to be commodities. In addition, the proposed amendment is intended to reduce administrative burdens by simplifying and making uniform the investment restriction with respect to commodities that applies to the Fund.

The Board, including all the Independent Trustees, recommends that the Fund’s shareholders vote “FOR” Proposal 3(e).

* * *

Proposal 3(f) — Amended Fundamental Restriction Relating to Loans

Sections 8(b)(1)(G) and 13(a)(2) of the 1940 Act together require that the Fund have an investment restriction governing the making of loans to other persons. In addition to a loan of cash, a loan may include certain transactions and investment-related practices under certain circumstances (e.g., lending portfolio securities, purchasing certain debt instruments and entering into repurchase agreements). Although the 1940 Act does not prohibit the Fund from making loans, SEC staff interpretations currently prohibit funds from lending more than one-third of their total assets, except through the purchase of debt obligations or the use of repurchase agreements. A repurchase agreement is an agreement to purchase a security, coupled with an agreement to sell that security back to the original seller on an agreed-upon date at a price that reflects current interest rates. The SEC frequently treats repurchase agreements as loans.

The following table sets forth the statement of the Fund’s current investment restriction relating to loans and the proposed revision.

| Current Fundamental Restriction Relating to Loans | Proposed Revision |

| The Fund may not make loans, except that the Fund may (i) lend portfolio securities in accordance with the Fund’s investment policies up to 33⅓% of the Fund’s total assets taken at market value, (ii) enter into repurchase agreements, and (iii) purchase all or a portion of an issue of publicly distributed debt securities, bank loan participation interests, bank certificates of deposit, bankers’ acceptances, debentures or other securities, whether or not the purchase is made upon the original issuance of the securities. | The Fund may not make loans except as permitted under the 1940 Act, as amended, and as interpreted or modified by regulatory authority having jurisdiction, from time to time. |

Discussion of Proposal.The proposed amendment would allow the Fund to lend money and other assets — thus becoming a creditor — to the full extent permitted under the 1940 Act. Thus, the Fund would continue to be able to engage in the types of transactions presently permitted by the current restriction, such as securities loans and repurchase agreements, as well as to engage in other activities that could be deemed to be lending, such as the acquisition of loans, loan participations, and other forms of debt instruments. Loans and debt instruments involve the

| 14 |

risk that the party responsible for repaying a loan or paying the principal and interest on a debt instrument will not meet its obligation. The proposed amendment is also intended to conform the Fund’s fundamental restriction with respect to loans to a format that has become standard for the John Hancock fund complex.

The Board, including all the Independent Trustees, recommends that the Fund’s shareholders vote “FOR” Proposal 3(f).

* * *

Proposal 3(g) — Amended Fundamental Restriction Relating to Senior Securities

Under Section 18(f)(1) of the 1940 Act, a fund may not issue “senior securities,” a term that is defined, generally, to refer to obligations that have a priority over shares of the fund with respect to the distribution of its assets or the payment of dividends. Sections 8(b)(1)(C) and 13(a)(2) of the 1940 Act together require that the Fund have a fundamental restriction addressing senior securities. SEC staff interpretations permit a fund, under certain conditions, to engage in a number of types of transactions that might otherwise be considered to create senior securities, including short sales, certain options and futures transactions, reverse repurchase agreements and securities transactions that obligate the fund to pay money at a future date (such as when-issued, forward commitment or delayed delivery transactions).

The following table sets forth the statement of the Fund’s current investment restriction relating to senior securities and the proposed revision.

| Current Fundamental Restriction Relating to Senior Securities | Proposed Revision |

| The Fund may not issue senior securities, except as permitted by the Fund’s fundamental investment restrictions on borrowing, lending and investing in commodities, and as otherwise permitted under the 1940 Act. For purposes of this restriction, the issuance of shares of beneficial interest in multiple classes or series, the deferral of trustees’ fees, the purchase or sale of options, futures contracts and options on futures contracts, forward commitments, forward foreign exchange contracts and repurchase agreements entered into in accordance with the Fund’s investment policies are not deemed to be senior securities. | The Fund may not issue senior securities, except as permitted under the 1940 Act, as amended, and as interpreted or modified by regulatory authority having jurisdiction, from time to time.

(For purposes of this fundamental restriction, purchasing securities on a when-issued, forward commitment or delayed delivery basis and engaging in hedging and other strategic transactions will not be deemed to constitute the issuance of a senior security.)

|

Discussion of Proposal. “Senior securities” are defined as Fund obligations that have a priority over the Fund’s shares with respect to the payment of dividends or the distribution of Fund assets. The 1940 Act prohibits the Fund from issuing any class of senior securities or selling any senior securities of which it is the issuer, except that the Fund is permitted to borrow from a bank so long as, immediately after such borrowings, there is an asset coverage of at least 300% for all borrowings of the Fund (not including borrowings for temporary purposes in an amount not exceeding 5% of the value of the Fund’s total assets). In the event that such asset coverage falls below this percentage, the Fund must reduce the amount of its borrowings within three days (not including Sundays and holidays) so that the asset coverage is restored to at least 300%.

The proposed amendment permits the Fund to issue senior securities in accordance with the most recent regulatory requirements, or, provided certain conditions are met, to engage in the types of transactions that have been interpreted by the SEC staff as not constituting the issuance of senior securities. Such transactions include covered reverse repurchase transactions, futures, permitted borrowings, short sales, swaps and other strategies. The fundamental investment restriction regarding senior securities will be interpreted so as to permit collateral arrangements with respect to swaps, options, forward or futures contracts or other derivatives, or the posting of initial or variation margin.

| 15 |

The proposed amendment is also intended to conform the Fund’s fundamental restriction with respect to senior securities to a format that has become standard for the John Hancock fund complex.

The Board, including all the Independent Trustees, recommends that the Fund’s shareholders vote “FOR” Proposal 3(g).

* * *

Proposal 3(h) — New Fundamental Restriction Relating to Diversification

Section 5(b)(1) of the 1940 Act sets forth the requirements that must be met for an investment company to be diversified. Section 13(a)(1) of the 1940 Act provides that an investment company may not change its classification from diversified to non-diversified unless authorized by the vote of a Majority of the Outstanding Voting Securities of the investment company.

A diversified fund is limited as to the amount it may invest in any single issuer. Specifically, with respect to 75% of its total assets, a diversified fund currently may not invest in a security if, as a result of such investment, more than 5% of its total assets (calculated at the time of purchase) would be invested in securities of any one issuer. In addition, with respect to 75% of its total assets, a diversified fund may not hold more than 10% of the outstanding voting securities of any one issuer. In determining the issuer of a municipal security, each state, each political subdivision, agency, and instrumentality of each state and each multi-state agency of which such state is a member is considered a separate issuer. In the event that securities are backed only by assets and revenues of a particular instrumentality, facility or subdivision, such entity is considered the issuer. Under the 1940 Act, these restrictions do not apply to U.S. government securities, securities of other investment companies, cash and cash items.

The following table sets forth a statement of the Fund’s current classification as a diversified investment company and the proposed new fundamental investment restriction regarding diversification.

| Statement of the Fund’s Current Classification as a Diversified Investment Company | Proposed New Fundamental Restriction |

| Although not stated as a fundamental investment restriction, the Fund is classified as a diversified investment company in accordance with Section 5(b)(1) of the 1940 Act. | The Fund has elected to be treated as a diversified investment company, as that term is used in the 1940 Act, as amended, and as interpreted or modified by regulatory authority having jurisdiction, from time to time. |

Discussion of Proposal. Proposal 3(h) states as a fundamental investment restriction the Fund’s classification as a “diversified” fund under the 1940 Act by relying on the definition of the term “diversified” in the 1940 Act rather than stating the relevant limitations expressed under current law. By relying on the definition of the term “diversified,” the proposed fundamental restriction also effectively clarifies that securities issued by other investment companies are not subject to the fundamental restriction regarding portfolio diversification. In addition, the proposed fundamental restriction is intended to conform the Fund’s statement regarding its classification as a diversified fund in a format that has become standard for the John Hancock fund complex.

The Board, including all the Independent Trustees, recommends that the Fund’s shareholders vote “FOR” Proposal 3(h).

* * *

| 16 |

Required Vote for Proposals 1, 2, and 3(a) through (h)

Approval of each of Proposals 1, 2, and each of Proposals 3(a) through (h) will require the affirmative vote of a Majority of the Outstanding Voting Securities of the Fund, as defined below.

In this Proxy Statement, the term “Majority of the Outstanding Voting Securities” of the Fund means the affirmative vote of the lesser of:

| (1) | 67% or more of the voting securities of the Fund, present at the Meeting, if the holders of more than 50% of the outstanding voting securities of the Fund are present in person or by proxy; or |

| (2) | more than 50% of the outstanding voting securities of the Fund. |

Proposals 1, 2, and 3(a) through (h) are separate and independent proposals, and approval and implementation of one is not contingent on approval and implementation of any of the others. Any required shareholder approval of a Proposal shall be effective if a Majority of the Outstanding Voting Securities of the Fund votes to approve such Proposal, even if one or more of the other Proposals may not have been approved by a Majority of the Outstanding Voting Securities of the Fund. Shareholders do not have appraisal rights in connection with the Proposals in this Proxy Statement.

Directions to attend the Meeting where you may vote in person can be found on our website atwww.jhinvestments.com/proxy. Valid photo identification may be required to attend the Meeting in person.All properly executed andtimely received proxieswillbevotedinaccordancewithspecificationsthereon,orintheabsenceofspecifications,forapprovalofthe proposals. A proxy that is not timely received will not be voted.

Revocation of Proxies.Proxies may be revoked at any time before the Meeting either: (i) by a written revocation received by the Secretary of the Trust; (ii) by a properly executed later-dated proxy received by the Secretary of the Trust; or (iii) by an in-person vote at the Meeting. Attendance at the Meeting will not in and of itself revoke a proxy. Shareholders may revoke a proxy as often as they wish before the Meeting. Only the latest dated, properly executed proxy card received prior to or at the Meeting will be counted.

Quorum.Shareholders of record at the close of business on the Record Date will be entitled to vote at the Meeting or any adjournment of the Meeting. The holders of a simple majority of the outstanding shares of the Fund at the close of business on that date present in person or by proxy will constitute a quorum for the Meeting.

Shareholders are entitled to one vote for each share held and proportionate fractional votes for fractional shares held. No shares have cumulative voting rights.

In the event the necessary quorum to transact business or the vote required to approve a proposal is not obtained at the Meeting, the persons named as proxies may propose one or more adjournments of the Meeting with respect to any proposal in accordance with applicable law to permit further solicitation of proxies. Any adjournment of the Meeting will require the affirmative vote of the holders of a simple majority of the Fund’s shares cast at the Meeting, and any adjournment with respect to any proposal will require the affirmative vote of the holders of a simple majority of the shares entitled to vote on the proposal cast at the Meeting. The persons named as proxies will vote for or against any adjournment in their discretion.

AbstentionsandBroker“Non-Votes.” Abstentions and broker non-votes (i.e., shares held by brokers or nominees as to which: (i) instructions have not been received from the beneficial owners or the persons entitled to vote; and (ii) the broker ornominee indicates on the proxy that it does not have discretionary voting power on a particular matter) are counted as shares entitled to vote at the Meeting in determining whether a quorum is present, but do not count as votes cast for a proposal. Therefore, abstentions and broker non-votes have the same effect as a vote “against” a proposal.

| 17 |

CostofPreparationandDistributionofProxyMaterials.The costs of the preparation of these proxy materials and their distribution will be borne by Sustainable Growth Advisers, LP.

Solicitation of Proxies. In addition to the mailing of these proxy materials, proxies may be solicited by telephone, by fax, by email, or in person by the Trustees, officers and employees of the Trust; by personnel of the Advisor, its affiliates, or by broker-dealer firms. Broadridge, an investor communications firm,has been retained to assist in the solicitation of proxies at a cost of approximately $602,726. The costs of any proxy solicitation will be borne by the Fund.

In addition to soliciting proxies by mail, by fax, by email or in person, the Trust may also arrange to have votes recorded by telephone by officers and employees of the Trust or by the personnel of the Advisor, the transfer agent or solicitor. The telephone voting procedure is designed to verify a shareholder’s identity, to allow a shareholder to authorize the voting of shares in accordance with the shareholder’s instructions and to confirm that the voting instructions have been properly recorded.

A shareholder will be called on a recorded line at the telephone number in the Fund’s account records and will be asked to provide certain identifying information.

The shareholder will then be given an opportunity to authorize proxies to vote his or her shares at the Meeting in accordance with the shareholder’s instructions.

Alternatively, a shareholder may call the Fund’s Voice Response Unit to vote by taking the following steps:

| § | Read the Proxy Statement and have your proxy card(s) at hand. |

| § | Call the toll-free-number located on your proxy card(s). |

| § | Enter the “control number” found on the front of your proxy card(s). |