As filed with the Securities and Exchange Commission on January 19, 2006

Registration No. 333-

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form S-4

REGISTRATION STATEMENT

UNDER THE SECURITIES ACT OF 1933

Hawaiian Telcom Communications, Inc.

Hawaiian Telcom, Inc.

Hawaiian Telcom Services Company, Inc.

(Exact names of registrants as specified in their charters)

| | | | |

| Hawaiian Telcom Communications, Inc. Delaware | | Hawaiian Telcom, Inc. Hawaii | | Hawaiian Telcom Services Company, Inc. Delaware |

(State or other jurisdiction of incorporation or organization) 16-1710376 | | (State or other jurisdiction of incorporation or organization) 49-0049500 | | (State or other jurisdiction of incorporation or organization) 20-2045722 |

(I.R.S. Employer Identification No.) 4813 | | (I.R.S. Employer Identification No.) 4813 | | (I.R.S. Employer Identification No.) 2741 |

(Primary Standard Industrial Classification Code Number) | | (Primary Standard Industrial Classification Code Number) | | (Primary Standard Industrial Classification Code Number) |

1177 Bishop Street

Honolulu, Hawaii 96813

(808) 546-4511

(Address, including zip code, and telephone number, including area code, of each of the registrants’ principal executive offices)

Daniel P. O’Brien

Senior Vice President and Chief Financial Officer

Hawaiian Telcom Communications, Inc.

1177 Bishop Street

Honolulu, Hawaii 96813

(808) 546-4511

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

Gregory A. Ezring, Esq.

Joshua A. Tinkelman, Esq.

Latham & Watkins LLP

885 Third Avenue

Suite 1000

New York, New York 10022

(212) 906-1200

Approximate date of commencement of proposed exchange offer: As soon as practicable after the effective date of this registration statement.

If the securities being registered on this Form are being offered in connection with the formation of a holding company and there is compliance with General Instruction G, check the following box. ¨

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

CALCULATION OF REGISTRATION FEE

| | | | | | | | | | | | | |

Title of Each Class of Securities to be Registered | | Amount to be Registered | | Proposed Maximum Offering Price Per Note(1) | | | Proposed Maximum Aggregate Offering Price(1) | | Amount of Registration Fee | |

Senior Floating Rate Notes due 2013 | | $ | 150,000,000 | | 100 | % | | $ | 150,000,000 | | $ | 16,050.00 | |

Guarantees of the Senior Floating Rate Notes due 2013 | | $ | 150,000,000 | | N/A | | | | N/A | | | (2) | |

9 3/4% Senior Fixed Rate Notes due 2013 | | $ | 200,000,000 | | 100 | % | | $ | 200,000,000 | | $ | 21,400.00 | |

Guarantees of the 9 3/4% Senior Fixed Rate Notes due 2013 | | $ | 200,000,000 | | N/A | | | | N/A | | | (2) | |

12 1/2% Senior Subordinated Notes due 2015 | | $ | 150,000,000 | | 100 | % | | $ | 150,000,000 | | $ | 16,050.00 | |

Guarantees of the 12 1/2% Senior Subordinated Notes due 2015 | | $ | 150,000,000 | | N/A | | | | N/A | | | (2) | |

| (1) | Estimated solely for the purpose of calculating the registration fee pursuant to Rule 457(f) under the Securities Act. |

| (2) | No additional registration fee is due for guarantees pursuant to Rule 457(n) under the Securities Act. |

The registrants hereby amend this registration statement on such date or dates as may be necessary to delay its effective date until the registrants shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until this registration statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and we are not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED JANUARY 19, 2006.

PROSPECTUS

HAWAIIAN TELCOM COMMUNICATIONS, INC.

Offer to Exchange

$150,000,000 aggregate principal amount of its Series B Senior Floating Rate Notes due 2013, which have been registered under the Securities Act, for any and all of its outstanding Series A Senior Floating Rate Notes due 2013

and

$200,000,000 aggregate principal amount of its 9 3/4% Series B Senior Fixed Rate Notes due 2013, which have been registered under the Securities Act, for any and all of its outstanding 9 3/4% Series A Senior Fixed Rate Notes due 2013

and

$150,000,000 aggregate principal amount of its 12 1/2% Series B Senior Subordinated Notes due 2015, which have been registered under the Securities Act, for any and all of its outstanding 12 1/2% Series A Senior Subordinated Notes due 2015.

We are offering to exchange our Series B Senior Floating Rate Notes due 2013, or the “senior floating rate exchange notes,” for our currently outstanding Series A Senior Floating Rate Notes due 2013, or the “outstanding senior floating rate notes,” our 9 3/4% Series B Senior Fixed Rate Notes due 2013, or the “senior fixed rate exchange notes,” and collectively with the senior floating rate exchange notes, the “senior exchange notes,” for our currently outstanding 9 3/4% Series A Senior Fixed Rate Notes due 2013, or the “outstanding senior fixed rate notes,” and collectively with the outstanding senior floating rate notes, the “outstanding senior notes,” and our 12 1/2% Series B Senior Subordinated Notes due 2015, or the “senior subordinated exchange notes,” and collectively with the senior exchange notes, the “exchange notes,” for our currently outstanding 12 1/2% Series A Senior Subordinated Notes due 2015, or the “outstanding senior subordinated notes” and collectively with the outstanding senior notes, the “outstanding notes.” Each series of the exchange notes are substantially identical to the applicable outstanding notes, except that the exchange notes have been registered under the federal securities laws and will not bear any legend restricting their transfer. The exchange notes will represent the same debt as the outstanding notes, and we will issue the exchange notes under the same indentures.

The senior exchange notes will be guaranteed on a senior unsecured basis, and the senior subordinated exchange notes will be guaranteed on a senior subordinated unsecured basis, by Hawaiian Telcom, Inc. and Hawaiian Telcom Services Company, Inc., both of which are currently our only direct subsidiaries, and each of our future subsidiaries that is a guarantor under our senior credit facilities. Our indirect subsidiary, Hawaiian Telcom Insurance Company, Incorporated, will not guarantee the exchange notes or our senior credit facilities.

The principal features of the exchange offer are as follows:

| | • | | The exchange offer expires at 12:00 midnight, New York City time, on , 2006, unless extended. |

| | • | | We will exchange all outstanding notes that are validly tendered and not validly withdrawn prior to the expiration of the exchange offer. |

| | • | | You may withdraw tendered outstanding notes at any time prior to the expiration of the exchange offer. |

| | • | | The exchange of outstanding notes for exchange notes pursuant to the exchange offer will not be a taxable event for U.S. federal income tax purposes. |

| | • | | We will not receive any proceeds from the exchange offer. |

| | • | | We do not intend to apply for listing of the exchange notes on any securities exchange or automated quotation system. |

Each broker-dealer that receives exchange notes for its own account pursuant to the exchange offer must acknowledge that it will deliver a prospectus in connection with any resale of such exchange notes. The letter of transmittal delivered with this prospectus states that by so acknowledging and by delivering a prospectus, a broker-dealer will not be deemed to admit that it is an “underwriter” within the meaning of the Securities Act of 1933. This prospectus, as it may be amended or supplemented from time to time, may be used by a broker-dealer in connection with resales of exchange notes received in exchange for outstanding notes where such outstanding notes were acquired by such broker-dealer as a result of market-making activities or other trading activities. We have agreed that, for a period of 90 days after the completion of the exchange offer, we will make this prospectus available to any broker-dealer for use in connection with any such resale. See “Plan of Distribution.”

Investing in the exchange notes involves risks.

See “Risk Factors” beginning on page 19.

Neither the U.S. Securities and Exchange Commission nor any other federal or state agency has approved or disapproved of these securities to be distributed in the exchange offer, nor have any of these organizations determined that this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The date of this prospectus is , 2006.

TABLE OF CONTENTS

Until , 2006, all dealers that effect transactions in these securities, whether or not participating in this offering, may be required to deliver a prospectus. This is in addition to the dealers’ obligation to deliver a prospectus when acting as underwriters and with respect to their unsold allotments or subscriptions.

We have not authorized any dealer, salesman or other person to give any information or to make any representation other than those contained in this prospectus. You must not rely upon any information or representation not contained in this prospectus as if we had authorized it. This prospectus does not constitute an offer to sell or a solicitation of an offer to buy any securities other than the registered securities to which it relates, nor does this prospectus constitute an offer to sell or a solicitation of an offer to buy securities in any jurisdiction to any person to whom it is unlawful to make such offer or solicitation in such jurisdiction.

i

Prospectus Summary

This summary highlights information contained elsewhere in this prospectus. Because this is only a summary, it does not contain all of the information that may be important to you. This prospectus includes specific terms of the exchange offer, as well as information regarding our business and detailed financial information. The information regarding our business and the detailed financial information, while important to an understanding of our cost structure, results of operations, financial position and cash flows, does not directly impact your decision as to whether or not to participate in the exchange offer. Information directly relating to the exchange offer can be found in this summary under the subheadings “—The Offering,” “—The Exchange Offer,” “—Terms of the Exchange Notes,” and elsewhere in this prospectus under the headings “The Exchange Offer,” “Description of Senior Exchange Notes” and “Description of Senior Subordinated Exchange Notes.” You should read this entire prospectus and should consider, among other things, the matters set forth in this summary under the subheading “—Summary Historical and Pro Forma Financial Information,” under the headings “Risk Factors,” “Unaudited Pro Forma Financial Information,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our consolidated and combined financial statements and related notes thereto appearing elsewhere in this prospectus.

In this prospectus:

| | • | | “We,” “our” or “us” refers to our predecessor, Verizon’s Hawaii Business, for periods prior to May 2, 2005, and refers, collectively, to Hawaiian Telcom Communications, Inc., wholly-owned by Hawaiian Telcom Holdco, Inc., and its subsidiaries, for periods after May 2, 2005. In addition, where the context so requires, “we,” “our” or “us” refers, collectively, to Verizon’s Hawaii Business, Hawaiian Telcom Communications, Inc. and its subsidiaries; |

| | • | | “Company” refers, collectively, to Hawaiian Telcom Communications, Inc. from its inception on May 21, 2004 and its subsidiaries acquired on May 2, 2005; |

| | • | | “Issuer” refers only to Hawaiian Telcom Communications, Inc., the issuer of the notes, and not to any of its subsidiaries; |

| | • | | “Holdings” refers to Hawaiian Telcom Holdco, Inc., a corporation controlled by affiliates of The Carlyle Group; |

| | • | | “Verizon” refers to Verizon Communications Inc.; |

| | • | | “GTE” refers to GTE Corporation; |

| | • | | “Verizon Hawaii” refers to the historical operations of Verizon Hawaii Inc. (formerly known as GTE Hawaiian Telephone Company Incorporated) prior to May 2, 2005, the date that the Issuer acquired Verizon’s Hawaii Business; |

| | • | | “Verizon’s Hawaii Business” or “Predecessor” refers, collectively, to the historical operations of Verizon Hawaii Inc. and the carved-out components of Verizon Information Services Inc., GTE.NET LLC (d/b/a Verizon Online), Bell Atlantic Communications Inc. (d/b/a Verizon Long Distance) and Verizon Select Services Inc. that the Issuer acquired, prior to May 2, 2005; |

| | • | | “Successor Period” refers to the period from May 2, 2005 through September 30, 2005; |

| | • | | “outstanding senior floating rate notes” refers to the Series A Senior Floating Rate Notes due 2013 issued on May 2, 2005; |

| | • | | “outstanding senior fixed rate notes” refers to the 9 3/4% Series A Senior Fixed Rate Notes due 2013 issued on May 2, 2005; |

| | • | | “outstanding senior notes” refers collectively to the outstanding senior floating rate notes and the outstanding senior fixed rate notes; |

1

| | • | | “outstanding senior subordinated notes” refers to the 12 1/2% Series A Senior Subordinated Notes due 2015 issued on May 2, 2005; |

| | • | | “outstanding notes” refers collectively to the outstanding senior notes and the outstanding senior subordinated notes; |

| | • | | “senior floating rate exchange notes” refers to the Series B Senior Floating Rate Notes due 2013 offered pursuant to this prospectus; |

| | • | | “senior fixed rate exchange notes” refers to the 9 3/4% Series B Senior Fixed Rate Notes due 2013 offered pursuant to this prospectus; |

| | • | | “senior exchange notes” refers collectively to the senior floating rate exchange notes and the senior fixed rate exchange notes; |

| | • | | “senior subordinated exchange notes” refers to the 12 1/2% Series B Senior Subordinated Notes due 2015 offered pursuant to this prospectus; |

| | • | | “exchange notes” refers collectively to the senior exchange notes and the senior subordinated exchange notes; and |

| | • | | “notes” refers collectively to the outstanding notes and the exchange notes. |

Background Information

On May 21, 2004, the Issuer and its parent company, Holdings, entered into a merger agreement, which was subsequently amended and restated on April 8, 2005, with GTE and Verizon HoldCo LLC, to acquire Verizon’s local exchange carrier, long distance, Internet and directories businesses in Hawaii, or Verizon’s Hawaii Business. Pursuant to the merger agreement, prior to May 2, 2005, GTE contributed all of the outstanding stock of Verizon Hawaii Inc., which operates our local exchange carrier business, to Verizon HoldCo LLC and caused certain of its affiliates to contribute assets and liabilities related to our long distance, Internet and directories businesses to a newly-formed subsidiary of Verizon HoldCo LLC. The Issuer consummated the acquisition on May 2, 2005, when Verizon HoldCo LLC merged with and into the Issuer, with the Issuer as the surviving entity. We refer to the acquisition of Verizon’s Hawaii Business as the “Hawaii Business Acquisition.”

Our Business

We are a full-service telecommunications provider in Hawaii, operating two businesses: our telecommunications business, which includes our local exchange carrier, long distance, wireless and Internet services businesses, and our directories publishing business. Our services are offered on all of Hawaii’s major islands. As of September 30, 2005, we served 651,325 local access lines. We also served 289,521 long distance lines and had 76,028 retail digital subscriber line, or DSL, connections as of such date. For the year ended December 31, 2004, we generated revenues of $595.6 million. For the nine months ended September 30, 2005, we generated revenues of $201.8 million (reflecting revenues generated since the Hawaii Business Acquisition on May 2, 2005 and impacted by certain purchase accounting adjustments discussed in “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Results of Operations for the Nine Months Ended September 30, 2005 and Nine Months Ended September 30, 2004”).

Originally incorporated in 1883 as Mutual Telephone Company, we have a strong heritage of over 120 years as Hawaii’s incumbent local exchange carrier, or ILEC. From 1967 to May 1, 2005, we operated as a division of Verizon or its predecessors. On May 2, 2005, we became a stand-alone provider of telecommunications services and were renamed Hawaiian Telcom Communications, Inc. with subsidiaries Hawaiian Telcom, Inc. and Hawaiian Telcom Services Company, Inc.

2

Our Products and Services

We offer a full complement of state-of-the-art telecommunications and data products and services to our customers, including the following:

Telecommunications

We provide our telecommunications services to a broad and diverse base of residential and business customers. We generated $529.5 million in telecommunication operations revenues for the year ended December 31, 2004 and $201.8 million in revenues for the nine months ended September 30, 2005 (reflecting revenues generated since the Hawaii Business Acquisition on May 2, 2005).

Local Exchange and Related Services

Our primary source of revenue is our local exchange and related services. Of our 651,325 local access lines, 63% served residential customers and 36% served business customers, with the remaining 1% serving other customers. Our primary residential lines represent a market share of approximately 85% of the total households in Hawaii. Our local exchange carrier, or LEC, business provides a broad range of products, including (1) traditional local telephone and value-added services, such as caller ID, call waiting, voice messaging, three-way calling, call forwarding and speed dialing services for residential and business customers, (2) dedicated voice and high-end data services for business customers, and (3) wholesale network services for other telecommunications carriers. We also provide other regulated services, such as operator services and pay phones, and network access to long distance carriers, competing local carriers and end-user subscribers. We provide non-regulated services, such as customer premises equipment sales, installation and maintenance services to business customers, and billing and collections services to long distance carriers.

Long Distance Services

We provide domestic and international long distance services, utilizing our local exchange facilities for call origination and termination and our own inter-island network for toll calls among Hawaii’s islands. As of September 30, 2005, we served 289,521 long distance lines, of which 74% served residential customers and 26% served business customers.

Internet Services

We provide DSL and dial-up Internet access to our residential and business customers. Our data network enables us to provide extensive high-speed network access. We have DSL available in 74 of our 86 central offices. As of September 30, 2005, we served 67,485 retail residential DSL lines and 8,543 retail business DSL lines. We also provided dial-up Internet access to approximately 5,000 subscribers as of the same date. We believe that our Internet services business is a strong area of growth for us.

Wireless Services

Upon consummation of the Hawaii Business Acquisition, we launched a wireless service under ourHawaiian TelcomTM brand. We believe that there are significant opportunities to grow our revenues, create new product bundles and reduce landline disconnects by offering a wireless product that leverages our local phone company brand as well as integrated wireless/wireline services. In January 2005, we entered into a mobile virtual network operator, or MVNO, services agreement with a subsidiary of Sprint Corporation that allows us to resell Sprint wireless services, including access to Sprint’s nationwide personal communications service wireless network, under theHawaiian TelcomTM brand name. Initially, a subsidiary of InPhonic, Inc. will operate the back-office functions of our wireless business under a month-to-month mobile virtual network enabler, or MVNE, services agreement. We believe that our eight existing retail stores, our distribution partners, our residential and business customer service call centers and our business-to-business sales forces serve as important distribution channels for acquiring new wireless customers.

3

Publishing

We publish and sell directory advertising in yellow page directories and white page directories. Our seven yellow page directories are published annually on the islands of Oahu, Maui, Hawaii and Kauai and had total circulation exceeding 1.3 million copies for the year ended December 31, 2005. Our directories business has historically generated consistent revenues through relationships with over 21,000 advertisers for the year ended December 31, 2004. We also distributed approximately 1.3 million white page directories in 2005. Upon consummation of the Hawaii Business Acquisition, we launched an online directories business to complement the existing print directories business. We generated directory advertising revenues of $66.1 million for the year ended December 31, 2004. We began recognizing revenue in the fourth quarter of 2005 with the publication of the Oahu directories.

Our Competitive Strengths

Favorable Market Characteristics

Hawaii compares favorably to national averages in median household income ($56,454 vs. $44,389 in 2004) In addition, we believe that Hawaii’s gross state product composition is indicative of a stable demand for our services, with 23% of 2004 gross state product derived from federal and state government, 8% from the hospitality industry and 5% from financial institutions. Our market is characterized by high population density, with over 70% of Hawaii’s population located on the island of Oahu, where the population density is 1,461 persons per square mile versus an average of 80 persons per square mile for the United States as a whole. As a result, our network also has a high density rate, with approximately 69% of our access lines located on Oahu as of September 30, 2005. We believe that the demographics of our customer base allows for increased profitability and reduced capital expenditure requirements per access line compared to other ILECs. A locally concentrated population also allows us to offer new products, such as higher speed DSL, at a lower cost to us and at accelerated availability to our customers. We believe that Hawaii’s remoteness leads to a strong preference for advanced telecommunication services and that this preference drives demand for our products, particularly for our fast-growing DSL and our long distance businesses.

Strong Market Position

We have been a telecommunications provider in Hawaii for more than 120 years. We own the state’s most extensive local telecommunications network, which has 651,325 local access lines covering all of Hawaii’s major islands. Our primary residential lines represent a market share of approximately 85% of the total households in Hawaii. We attribute our leading market position to our historical incumbent position as a telecommunications provider, our commitment to customer service and our extensive network infrastructure. In addition, we believe that remoteness from the United States mainland and difficult geological terrain represent significant barriers to entry. We believe that these factors have historically led to muted competition from competitive local exchange carriers, or CLECs. Management believes that the ratio of unbundled network element—platform (or UNE-P), unbundled network element—loop (or UNE-L) and resale lines to total access lines compares favorably to the national average (less than 1% vs. 14% as of June 2004). We believe that our broad and diversified customer base affords us a superior understanding of the marketplace relative to our competitors.

Advanced Network Infrastructure

Our intra- and inter-island network consists of 100% digital switches, more than 13,100 sheath miles of metallic and fiber-optic cable, a microwave communications system and 86 central offices. For the five years ended December 31, 2004, our Predecessor invested $423.5 million in capital expenditures, primarily to upgrade and modernize our network facilities. As a result of our modernization efforts, we are able to offer a full complement of value-added services such as caller ID, call waiting and voicemail to all of our customers and

4

DSL availability in 74 of our 86 central offices. We believe that we are well positioned to offer new products and services that will generate growth in our business and allow us to compete more effectively in the marketplace.

Strong Local Heritage

With the separation from Verizon and the reintroduction of a locally focused brand, we believe that we benefit from Hawaii residents’ preference for locally managed and operated businesses. Based on our internal market research, we believe that our new brand name,Hawaiian TelcomTM, will leverage the strength of our strong local heritage and the name recognition of theHawaiian TelTM brand established by our predecessors and which we acquired as part of the Hawaii Business Acquisition. We are also one of Hawaii’s largest private employers, which enhances our local stature and community support. In addition, approximately $30.0 million of Holdings’ equity is held by prominent Hawaii business leaders, which we believe strengthens our ties to the local business community.

Experienced Management Team

We have assembled a strong and experienced executive management team to lead our workforce in the execution of our business plan. Led by our Chief Executive Officer, Michael S. Ruley, the former Chief Executive Officer of NextiraOne, our executive management team has extensive experience in both the incumbent and competitive segments of the telecommunications sector, with an average of over 25 years in the industry. We believe that the combination of our new management’s expertise with our organization’s extensive knowledge of our local market will be a critical driver of our success going forward.

Our Strategy

Our goal is to be among the best local telecommunications companies in the United States. The key elements of our strategy are as follows:

Reposition Our Business as a “Local” Hawaii Company

As a stand-alone telecommunications provider, we are repositioning ourselves as a “local” Hawaii company and introducing a locally-focused brand across all our product offerings. We have developed a branding campaign that is designed to position us as a technologically-advanced, full-service telecommunications provider that is locally branded, managed and operated. We have implemented a strategy of partnership with Hawaii’s business leaders and of high visibility in the community, where we believe residents have strong local pride and support the success of local companies. We believe that these efforts will sharpen our local profile and strengthen our customers’ allegiance across all our product offerings.

Develop and Execute a Focused Sales and Marketing Effort

We plan to complement our renewed local brand and presence with products and services and content customized for the Hawaii marketplace. Our Predecessor was managed remotely from the mainland United States with product offerings and marketing plans designed for Verizon’s nationwide network rather than for the unique characteristics of the Hawaii market, such as its distinctive ethnic composition and calling patterns. Our marketing department is introducing new products, services and bundles that we believe meet our market’s specific needs, including those arising from Hawaii’s unique geographic location and the prevalence of specific local industries, such as tourism and government. We believe that our transition to a stand-alone telecommunications provider also presents us with an opportunity to reinvigorate our sales force, increase our sales channel performance and improve coverage of sales opportunities.

5

Pursue Strategic Product Growth Opportunities

Our strategy is to leverage the breadth of our product offering by marketing more comprehensive bundles of our services, which we believe will increase our revenues per customer. We plan to leverage our local, customized sales and marketing plans and our advanced network infrastructure to increase sales of products and services. We plan to continue to grow our DSL business by capitalizing on our modern network to offer increased bandwidth and new products and services such as video over our core network. We also believe that significant opportunity exists in the long distance market, given penetration rates for our long distance services that we believe are low compared to other ILECs.

Upon consummation of the Hawaii Business Acquisition, we expanded our product line with a new wireless service under theHawaiian TelcomTM brand name. This wireless product allows us to increase the scope of our bundled offerings. Over time, we believe that by providing more of our customers’ telecommunications needs at increased convenience to them, on a single monthly bill, our product bundles will increase our customers’ loyalty and reduce churn.

Establish Highly Efficient Stand-Alone Operations

As part of our transition to a stand-alone telecommunications provider, we expect to increase the efficiency of our business operations. We have begun to provide through internal operations a significant portion of the services that have historically been provided from the United States mainland by Verizon and its affiliates. We have also begun to outsource a portion of such services.

Pursuant to our Transition Services Agreement with Verizon, Verizon and its affiliates are providing us with back-office services during a transition period following the Hawaii Business Acquisition. During this transition period, we are putting in place, and making a substantial investment in, a new back-office and information technology, or IT, infrastructure that will, among other things, integrate certain core operations support systems purchased from Verizon as part of the Hawaii Business Acquisition with customized, off-the-shelf commercial systems. Our new integrated back-office and IT infrastructure and related personnel will allow us to perform functions historically provided by Verizon and its affiliates, such as network management and monitoring, billing, customer relationship management, corporate finance, human resource and payroll. We believe that our new back-office and IT infrastructure will also allow us to improve and expand our customer services and streamline our operations. Enhanced data management and billing capabilities will allow us to broaden our bundled product offering and replace multiple existing customer service systems with one central system that will improve our efficiency and response time. In addition, our new back-office and IT infrastructure will provide us with a more comprehensive customer information tracking system, which we believe will enhance our market intelligence. We believe that the enhanced functionality of our new IT infrastructure will allow us to sell more products and bundles, operate more efficiently and reduce our costs.

Our Sponsor

The Carlyle Group, or Carlyle, is a global private equity firm with $31.0 billion under management. Carlyle invests in buyouts, venture capital, real estate and leveraged finance in North America, Europe and Asia, focusing on aerospace & defense, automotive & transportation, consumer & retail, energy & power, healthcare, industrial, information technology & business services and telecommunications & media. Since 1987, the firm has invested $14 billion of equity in 414 transactions. Carlyle employs over 300 investment professionals in 14 countries. In the aggregate, Carlyle portfolio companies have more than $30.0 billion in revenue and employ more than 131,000 people around the world.

Carlyle is an experienced telecommunications and media investor, and the Carlyle representatives on the Board of Directors of the Issuer have in-depth knowledge of and experience in the telecommunications industry.

6

The Hawaii Business Transactions

The transactions summarized below, pursuant to which we became a stand-alone company, include the Hawaii Business Acquisition, the issuance of our outstanding senior floating rate notes, outstanding senior fixed rate notes and outstanding senior subordinated notes, borrowings under our senior credit facilities, the assumption of existing debentures by Hawaiian Telcom, Inc. and the equity contribution by Carlyle and its assignees and designees. We refer to these transactions in this prospectus as the “Hawaii Business Transactions.” While an understanding of the Hawaii Business Transactions is important to your understanding of our future cost structure, results of operations, financial position and cash flows, the transactions do not directly impact your decision as to whether or not to participate in the exchange offer.

On May 21, 2004, the Issuer and its parent company, Holdings, which is controlled by affiliates of Carlyle, entered into a merger agreement, which was subsequently amended and restated on April 8, 2005, with GTE and Verizon HoldCo LLC, to acquire Verizon’s local exchange carrier, long distance, Internet and directories businesses in Hawaii, or Verizon’s Hawaii Business. Pursuant to the merger agreement, prior to May 2, 2005, GTE contributed all of the outstanding stock of Verizon Hawaii Inc., which operates our local exchange carrier business, to Verizon HoldCo LLC and caused certain of its affiliates to contribute assets and liabilities related to our long distance, Internet and directories businesses to a newly-formed subsidiary of Verizon HoldCo LLC. On May 2, 2005, Verizon HoldCo LLC merged with and into the Issuer, with the Issuer as the surviving entity. The Issuer currently has two direct subsidiaries—Hawaiian Telcom, Inc. (f/k/a Verizon Hawaii Inc.) and Hawaiian Telcom Services Company, Inc.—and one indirect subsidiary—Hawaiian Telcom Insurance Company, Incorporated (f/k/a GTE Hawaiian Tel Insurance Company Incorporated). Hawaiian Telcom, Inc. operates our regulated local exchange carrier business and Hawaiian Telcom Services Company, Inc. operates all of our other businesses, including our long distance, Internet, wireless and directories businesses. Hawaiian Telcom Insurance Company, Incorporated is a captive insurance subsidiary. Until December 31, 2003, it provided auto liability, general liability and worker’s compensation insurance to Verizon Hawaii Inc. on a direct basis. The captive subsidiary continues to settle claims related to incidents which occurred prior to January 1, 2004. We insure current incidents with external carriers.

Pursuant to the Transition Services Agreement, during a transition period following the Hawaii Business Acquisition, Verizon and its affiliates continue to provide us with services that are critical to the ongoing operation of our business. The transition period has an initial nine-month term, which by amendment dated December 15, 2005, was extended to April 1, 2006. If needed, we can elect to have Verizon continue to provide certain services after the extension period, but at prices that are double the prices charged during the extension period. During the transition period, Verizon and its affiliates are providing us with services that, among other things:

| | • | | provide us with access to certain existing IT systems and applications; |

| | • | | provide us with maintenance and support of certain IT applications and systems; |

| | • | | provide support for our residential and business customers; |

| | • | | provide us with accounting, payroll, accounts payable and transaction tax preparation services; |

| | • | | provide customer billing operation services; |

| | • | | provide network surveillance, maintenance and technical support of switches, relays, DSL and other Internet operations; |

| | • | | provide call center support, systems and related services; |

| | • | | perform infrastructure maintenance work for inside and outside plant engineering; and |

| | • | | provide and support Internet operations. |

7

Verizon is also providing us with long distance voice and data services following the Hawaii Business Acquisition pursuant to the Verizon Master Services Agreement. See “The Hawaii Business Transactions—The Transition.” Verizon is providing these services for a transition period following the Hawaii Business Acquisition, which period has also been extended to April 1, 2006. After Verizon ceases to provide services to us under the Transition Services Agreement or the Verizon Master Services Agreement, we intend to provide such services ourselves or receive such services from third-party service providers. See “The Hawaii Business Transactions—Transition Services Agreement.”

The total consideration that the Issuer paid for Verizon’s Hawaii Business was $1,605.1 million (excluding fees and expenses and subject to adjustments relating to working capital levels). In connection with the Hawaii Business Acquisition, Carlyle (including its assignees and designees) contributed $428.0 million in cash to Holdings, which, in turn, was contributed to the Issuer’s common equity. This equity contribution represented 25% of the purchase price of the Hawaii Business Acquisition (including fees and expenses). The consideration was also funded with:

| | • | | borrowings of $35.0 million under our revolving credit facility and $450.0 million under the Tranche B term loan portion of our senior credit facilities; |

| | • | | the proceeds from the issuance of the outstanding notes, which was consummated on May 2, 2005; and |

| | • | | the assumption of $300.0 million in aggregate principal amount of the 7% Debentures, Series A, due 2006 and 7 3/8% Debentures, Series B, due 2006, which were issued by Verizon Hawaii Inc. and which we refer to as the “Existing Debentures.” |

For federal income tax purposes, the Hawaii Business Acquisition was treated as a purchase of the assets of Verizon HoldCo LLC. An election under section 338(h)(10) of the Internal Revenue Code of 1986, as amended, was made with respect to the purchase and sale of the stock of Verizon HoldCo LLC’s subsidiaries and indirect subsidiary and as a result, we have a tax basis in the assets of such subsidiaries equal to the purchase price for the Hawaii Business Acquisition adjusted by the amount of liabilities assumed.

The following table sets forth the sources and uses of funds for the Hawaii Business Transactions.

| | | | | | | | |

(Dollars in millions)

| | | | | | |

Sources of Funds | | | | | Uses of Funds | | | |

Senior Credit Facilities: | | | | | Cash Purchase Price | | $ | 1,305.1 |

Revolving Credit Facility(1) | | $ | 35.0 | | Existing Debentures(2) | | | 300.0 |

Tranche A Term Loan Facility(2) | | | — | | Fees and Expenses | | | 26.0 |

Tranche B Term Loan Facility | | | 450.0 | | Working Capital Funds | | | 81.9 |

Outstanding senior notes | | | 350.0 | | | | | |

Outstanding senior subordinated notes | | | 150.0 | | | | | |

Existing Debentures(2) | | | 300.0 | | | | | |

Cash Contribution(3) | | | 428.0 | | | | | |

| | |

|

| | | |

|

|

Total Sources | | $ | 1,713.0 | | Total Uses | | $ | 1,713.0 |

| (1) | Our revolving credit facility has total availability of $200.0 million, of which $35.0 million was drawn to fund the Hawaii Business Acquisition and an additional $11.1 million was drawn in connection with a working capital purchase price adjustment two days after closing of the Hawaii Business Acquisition. As of September 30, 2005, we had approximately $71.5 million drawn under our revolving credit facility and approximately $128.5 million available for borrowing, subject to covenant restrictions. |

| (2) | $300.0 million is available for borrowing under the Tranche A term loan facility. We intend to draw such amount in full in connection with repayment of the Existing Debentures on their respective maturity dates in |

8

| | 2006. See “Description of Other Indebtedness—The Senior Credit Facilities,” “—7% Debentures, Series A, due 2006” and “—7 3/8% Debentures, Series B, due 2006.” |

| (3) | Represents the equity contribution from Carlyle (including its assignees and designees). |

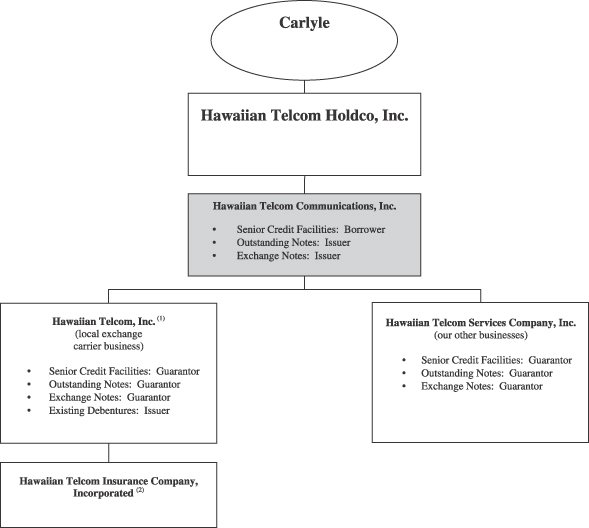

Corporate Structure

Our corporate structure is as follows.

| (1) | Substantially all of the assets of Hawaiian Telcom, Inc. secure the Existing Debentures and our senior credit facilities on a pari passu basis until the Existing Debentures are repaid. See “Description of Other Indebtedness.” |

| (2) | Hawaiian Telcom Insurance Company, Incorporated does not guarantee the outstanding notes, our senior credit facilities or the Existing Debentures and will not guarantee the exchange notes. |

9

The Offering

On May 2, 2005, we completed an offering of $150.0 million in aggregate principal amount of Series A Senior Floating Rate Notes due 2013, $200.0 million in aggregate principal amount of 9 3/4% Series A Senior Fixed Rate Notes due 2013 and $150.0 million in aggregate principal amount of 12 1/2% Series A Senior Subordinated Notes due 2015, each of which was exempt from registration under the Securities Act of 1933 (the “Securities Act”).

Outstanding Notes | We sold the outstanding notes to Goldman, Sachs & Co., J.P. Morgan Securities Inc., Lehman Brothers Inc., ABN AMRO Incorporated and Wachovia Capital Markets, LLC, the initial purchasers, on May 2, 2005. The initial purchasers subsequently resold the outstanding notes to qualified institutional buyers pursuant to Rule 144A under the Securities Act and to non-U.S. persons outside the United States in reliance on Regulation S under the Securities Act. |

Registration Rights Agreement | In connection with the sale of the outstanding notes, we entered into a registration rights agreement with the initial purchasers. Under the terms of that agreement, we agreed to: |

| | • | | use all commercially reasonable efforts to file a registration statement for the exchange offer and to consummate the exchange offer within 365 days after the initial issuance of the outstanding notes; and |

| | • | | file a shelf registration statement for the sale of the outstanding notes under certain circumstances and use all commercially reasonable efforts to cause such shelf registration statement to become effective under the Securities Act. |

| | If we do not meet one of these requirements, we must pay additional interest on the outstanding notes at a rate of 0.25% per annum for the first 90-day period, increasing by an additional 0.25% per annum with respect to each 90-day period until the exchange offer is completed or the shelf registration statement is declared effective, up to a maximum of 1.0% per annum of the principal amount of the notes. The exchange offer is being made pursuant to the registration rights agreement and is intended to satisfy the rights granted under the registration rights agreement, which rights terminate upon completion of the exchange offer. |

10

The Exchange Offer

The following is a brief summary of terms of the exchange offer. For a more complete description of the exchange offer, see “The Exchange Offer.”

Securities Offered | $150.0 million in aggregate principal amount of Series B Senior Floating Rate Notes due 2013, $200.0 million in aggregate principal amount of 9 3/4% Series B Senior Fixed Rate Notes due 2013 and $150.0 million in aggregate principal amount of 12 1/2% Series B Senior Subordinated Notes due 2015. |

Exchange Offer | The exchange notes are being offered in exchange for a like principal amount of outstanding notes. We will accept any and all outstanding notes validly tendered and not withdrawn prior to 12:00 midnight, New York City time, on , 2006. Holders may tender some or all of their outstanding notes pursuant to the exchange offer. However, outstanding notes may be tendered only in integral multiples of $1,000 in principal amount. The form and terms of the exchange notes are the same as the form and terms of the outstanding notes except that: |

| | • | | the exchange notes have been registered under the federal securities laws and will not bear any legend restricting their transfer; |

| | • | | the exchange notes bear a series B designation and a different CUSIP number than the outstanding notes; and |

| | • | | the holders of the exchange notes will not be entitled to certain rights under the registration rights agreement, including the provisions for an increase in the interest rate on the outstanding notes in some circumstances relating to the timing of the exchange offer. See “The Exchange Offer.” |

Expiration Date | The exchange offer will expire at 12:00 midnight, New York City time, on , 2006, unless we decide to extend the exchange offer. |

Conditions to the Exchange Offer | The exchange offer is subject to certain customary conditions, some of which may be waived by us. See “The Exchange Offer—Conditions to the Exchange Offer.” |

Procedures for Tendering Outstanding Notes | If you wish to accept the exchange offer, you must complete, sign and date the letter of transmittal, or a facsimile of the letter of transmittal, in accordance with the instructions contained in this prospectus and in the letter of transmittal. You should then mail or otherwise deliver the letter of transmittal, or facsimile, together with the outstanding notes to be exchanged and any other required documentation, to the exchange agent at the address set forth in this prospectus and in the letter of transmittal. |

11

| | By executing the letter of transmittal, you will represent to us that, among other things: |

| | • | | any exchange notes to be received by you will be acquired in the ordinary course of business; |

| | • | | you have no arrangement or understanding with any person to participate in the distribution (within the meaning of the Securities Act) of the exchange notes in violation of the provisions of the Securities Act; |

| | • | | you are not an “affiliate” (within the meaning of Rule 405 under Securities Act) of ours; and |

| | • | | if you are a broker-dealer that will receive exchange notes for your own account in exchange for outstanding notes that were acquired as a result of market-making or other trading activities, then you will deliver a prospectus in connection with any resale of such exchange notes. See “The Exchange Offer—Procedures for Tendering Outstanding Notes” and “Plan of Distribution.” |

Effect of Not Tendering | Any outstanding notes that are not tendered or that are tendered but not accepted will remain subject to the restrictions on transfer. Since the outstanding notes have not been registered under the federal securities laws, they bear a legend restricting their transfer absent registration or the availability of a specific exemption from registration. Upon the completion of the exchange offer, we will have no further obligations, except under limited circumstances, to provide for registration of the outstanding notes under the federal securities laws. See “The Exchange Offer—Purpose and Effect.” |

Interest on the Exchange Notes and the Outstanding Notes | The exchange notes will bear interest from the most recent interest payment date to which interest has been paid on the notes or, if no interest has been paid, from May 2, 2005. Interest on the outstanding notes accepted for exchange will cease to accrue upon the issuance of the exchange notes. |

Withdrawal Rights | Tenders of outstanding notes may be withdrawn at any time prior to 12:00 midnight, New York City time, on the expiration date. |

Federal Tax Consequences | There will be no federal income tax consequences to you if you exchange your outstanding notes for exchange notes in the exchange offer. See “Material Federal Income Tax Consequences.” |

Use of Proceeds | We will not receive any proceeds from the issuance of exchange notes pursuant to the exchange offer. |

Exchange Agent | U.S. Bank National Association, the trustee under the indentures, is serving as exchange agent in connection with the exchange offer. |

12

Terms of the Exchange Notes

The following is a brief summary of the terms of the exchange notes. The financial terms and covenants of the exchange notes are the same as the outstanding notes. For a more complete description of the terms of the exchange notes, see “Description of Senior Exchange Notes” and “Description of Senior Subordinated Exchange Notes.”

Issuer | Hawaiian Telcom Communications, Inc. |

Securities Offered | $150.0 million in aggregate principal amount of Series B Senior Floating Rate Notes due 2013. |

| | $200.0 million in aggregate principal amount of 9 3/4% Series B Senior Fixed Rate Notes due 2013. |

| | $150.0 million in aggregate principal amount of 12 1/2% Series B Senior Subordinated Notes due 2015. |

Maturity Dates | The senior exchange notes will mature on May 1, 2013. |

| | The senior subordinated exchange notes will mature on May 1, 2015. |

Interest Payment Dates | May 1 and November 1 of each year, commencing November 1, 2005. |

Guarantees | The payment of principal, premium, if any, and interest on each of the senior exchange notes and the senior subordinated exchange notes is unconditionally guaranteed, jointly and severally, by our current direct subsidiaries—Hawaiian Telcom, Inc. and Hawaiian Telcom Services Company, Inc.—and each of our future subsidiaries that guarantees our obligations under our senior credit facilities. The guarantees constitute a guarantee of payment for each of the senior exchange notes and senior subordinated exchange notes by each of the guarantors, which will be unsecured. The guarantees of the senior exchange notes will rank equally with all other senior unsecured indebtedness of the guarantors. The guarantees of the senior subordinated exchange notes will rank subordinate to all senior indebtedness of the guarantors. |

Ranking | The senior exchange notes will be our general unsecured obligations and will: |

| | • | | rank equal in right of payment to all of our existing and future unsecured indebtedness and other obligations that are not, by their terms, expressly subordinated in right of payment to the senior exchange notes; |

| | • | | rank senior in right of payment to any of our future indebtedness and other obligations that are, by their terms, expressly subordinated in right of payment to the senior exchange notes; |

13

| | • | | be effectively subordinated to all of our secured indebtedness and other secured obligations to the extent of the value of the assets securing such indebtedness and other obligations; and |

| | • | | be effectively subordinated to all indebtedness and other liabilities (including trade payables) of our subsidiaries that are not guarantors. |

| | The senior subordinated exchange notes will be our general unsecured obligations and will: |

| | • | | rank junior in right of payment to all of our existing and future unsecured indebtedness and other obligations that are not, by their terms, expressly subordinated in right of payment to the senior subordinated exchange notes; |

| | • | | rank equal in right of payment to any of our future indebtedness and other obligations that are, by their terms, expressly subordinated in right of payment to our senior debt; |

| | • | | be effectively subordinated to all of our secured indebtedness and other secured obligations to the extent of the value of the assets securing such indebtedness and other obligations; and |

| | • | | be effectively subordinated to all indebtedness and other liabilities (including trade payables) of our subsidiaries that are not guarantors. |

| | As of September 30, 2005, we had $1,321.5 million of indebtedness, of which $821.5 million was secured, and an additional $128.5 million of indebtedness was available for borrowing under the revolving portion of our senior credit facilities, subject to covenant restrictions, all of which, if borrowed, would be secured indebtedness. In addition, Hawaiian Telcom Insurance Company, Incorporated, our non-guarantor subsidiary, had no indebtedness and other liabilities of approximately $3.9 million. |

Optional Redemption | We may redeem some or all of the senior floating rate exchange notes on or after May 1, 2007, some or all of the senior fixed rate exchange notes on or after May 1, 2009 and some or all of the senior subordinated exchange notes on or after May 1, 2010 at the redemption prices set forth herein, plus accrued and unpaid interest and special interest, if any. In addition, prior to May 1, 2007 with respect to the senior floating rate exchange notes and prior to May 1, 2008 with respect to the senior fixed rate exchange notes and the senior subordinated exchange notes, we may also redeem up to 35% of each series of exchange notes with the proceeds of certain qualified equity offerings at the prices set forth herein, plus accrued and unpaid interest. We may also redeem some or all of the senior fixed rate exchange notes prior to May 1, 2009 and some or all of the senior subordinated exchange notes prior to May 1, 2010 at a price equal to 100% of such series of exchange notes redeemed plus a “make-whole” premium and accrued and unpaid interest and additional |

14

| | interest, if any. See “Description of Senior Exchange Notes—Optional Redemption” and “Description of Senior Subordinated Exchange Notes—Optional Redemption.” |

Change of Control | Upon the occurrence of a change of control, unless we have exercised our right to redeem all of the exchange notes of an issue as described above, you will have the right to require us to purchase all or a portion of your exchange notes at a purchase price in cash equal to 101% of the principal amount, plus accrued and unpaid interest (including additional interest), if any, to the date of purchase. See “Description of Senior Exchange Notes—Change of Control” and “Description of Senior Subordinated Exchange Notes—Change of Control.” |

Covenants | The indentures governing the exchange notes contain certain covenants that will, among other things, limit our ability and the ability of our restricted subsidiaries (which include Hawaiian Telcom, Inc., Hawaiian Telcom Services Company, Inc. and any future subsidiary that we form or acquire and do not subsequently designate as an unrestricted subsidiary in accordance with the provisions set forth in the indentures (see “Description of Senior Exchange Notes—Certain Definitions—Unrestricted Subsidiary” and “Description of Senior Subordinated Exchange Notes—Certain Definitions—Unrestricted Subsidiary”)) to: |

| | • | | declare or pay dividends, redeem stock or make other distributions to stockholders; |

| | • | | enter into transactions with affiliates; |

| | • | | sell or transfer assets; and |

| | These covenants are subject to a number of important qualifications and limitations. See “Description of Senior Exchange Notes—Certain Covenants” and “Description of Senior Subordinated Exchange Notes—Certain Covenants.” |

No Public Market for the Exchange Notes | The exchange notes are new issues of securities and will not be listed on any securities exchange or included in any automated quotation system. The initial purchasers of the outstanding notes have advised us that they intend to make a market in the exchange notes. The initial purchasers are not obligated, however, to make a market in the exchange notes, and any such market-making may be discontinued by the initial purchasers in their discretion at any time without notice. See “Plan of Distribution.” |

15

Risk Factors

You should carefully consider all the information in this prospectus prior to participating in the exchange offer. In particular, we urge you to consider carefully the factors set forth under “Risk Factors” beginning immediately after this “Prospectus Summary.”

Additional Information

Our principal executive offices are located at 1177 Bishop Street, Honolulu, Hawaii 96813. Our telephone number is (808) 546-4511. Our Internet address is http://www.hawaiiantel.com. The contents of our website are not part of this prospectus.

16

Summary Historical and Pro Forma Financial Information

The following table sets forth our summary historical and pro forma financial information as of the dates and periods indicated.

The Company’s historical balance sheet data as of December 31, 2004 and the statements of operations and cash flow data for the period from May 21, 2004 (date of inception) to December 31, 2004 have been derived from the financial statements of the Company, included elsewhere in this prospectus. The Company’s selected historical balance sheet data as of September 30, 2005 and 2004 and the statements of operations and cash flow data for the nine months ended September 30, 2005 and for the period from May 21, 2004 to September 30, 2004 have been derived from the unaudited consolidated financial statements of the Company, included elsewhere in this prospectus.

Predecessor historical balance sheet data as of December 31, 2004 and 2003 and the statements of operations and cash flow data for each of the years in the three-year period ended December 31, 2004 have been derived from the special-purpose combined statements of selected assets, selected liabilities and parent funding of our Predecessor, included elsewhere in this prospectus. The Predecessor historical balance sheet data as of May 1, 2005, September 30, 2004 and December 31, 2002 and the statements of operations and cash flow data for the period from January 1 to May 1, 2005 and nine months ended September 30, 2004 have been derived from the unaudited special-purpose combined statements of selected assets, selected liabilities and parent funding of our Predecessor.

The comparability of our summary historical financial information has been affected by the Hawaii Business Acquisition. The historical financial information includes periods prior to and subsequent to our consummation of the Hawaii Business Acquisition. Our Predecessor has historically operated as the local exchange carrier, directories business, and long distance and Internet service provider of Verizon in the State of Hawaii and not as a stand-alone telecommunications provider. The historical Predecessor financial statements in this prospectus, including the selected historical Predecessor financial information set forth below, reflect expenses related to services that were provided to our Predecessor by Verizon and its affiliates. After a transition period following the Hawaii Business Acquisition, we anticipate receiving such services from our internal operations or from third-party service providers, and not Verizon. Accordingly, we believe that the historical and pro forma financial statements in this prospectus are not indicative of our future performance and do not reflect what our cost structure would have been had we operated as a stand-alone telecommunications provider during the periods presented.

Our summary unaudited pro forma financial information for the year ended December 31, 2004 and for the nine months ended September 30, 2005 gives effect, in the manner described under “Unaudited Pro Forma Financial Information” and the notes thereto, to the Hawaii Business Acquisition and the related financing as if they had occurred on January 1, 2004. The summary pro forma financial information is presented for informational purposes only and is not necessarily indicative of our results of operations that would have occurred had the transactions been consummated as of the dates indicated. In addition, the summary pro forma combined financial information is not necessarily indicative of our future financial operating results.

The following data should be read in conjunction with “Unaudited Pro Forma Financial Information,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our audited and unaudited financial statements and related notes thereto included elsewhere in this prospectus.

17

Selected Financial Information (dollars in thousands)

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | Predecessor

| | | Company

| | | Pro Forma

| |

| | | Year Ended December 31,

| | | Nine Months Ended September 30, 2004

| | | Period from January 1

to May 1, 2005

| | | Period from May 21 to December 31, 2004

| | | Period

from

May 21 to

September

30, 2004

| | | Nine

Months

Ended

September

30, 2005

| | | Year Ended December 31, 2004

| | | Nine Months Ended September 30, 2005

| |

| | | 2002

| | | 2003

| | | 2004

| | | | | | | | |

Statement of operations data: | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Revenues(1) | | $ | 635,400 | | | $ | 612,300 | | | $ | 595,600 | | | $ | 445,200 | | | $ | 200,700 | | | $ | — | | | $ | — | | | $ | 201,779 | | | $ | 544,155 | | | $ | 410,053 | |

Depreciation and

amortization (2) | | | 107,900 | | | | 109,400 | | | | 114,800 | | | | 87,100 | | | | 39,600 | | | | — | | | | — | | | | 66,643 | | | | 159,632 | | | | 119,854 | |

Operating income (loss) (3) | | | 113,300 | | | | 59,200 | | | | 90,900 | | | | 70,500 | | | | 35,900 | | | | (17,373 | ) | | | (3,430 | ) | | | (77,397 | ) | | | (16,870 | ) | | | (51,048 | ) |

Interest expense | | | 37,400 | | | | 33,700 | | | | 36,800 | | | | 27,000 | | | | 11,700 | | | | — | | | | — | | | | 51,604 | | | | 111,200 | | | | 88,671 | |

Provision for income tax | | | 27,800 | | | | 8,800 | | | | 20,500 | | | | 15,500 | | | | 8,700 | | | | — | | | | — | | | | 2,600 | | | | 6,000 | | | | 4,600 | |

Net income (loss) | | | 50,900 | | | | 65,500 | | | | 36,900 | | | | 29,700 | | | | 16,100 | | | | (17,373 | ) | | | (3,430 | ) | | | (131,434 | ) | | | (130,770 | ) | | | (143,552 | ) |

Statement of cash data—net cash provided by (used in): | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Operating activities | | $ | 161,600 | | | $ | 125,300 | | | $ | 107,700 | | | $ | 63,000 | | | $ | 36,200 | | | $ | — | | | $ | — | | | $ | (19,506 | ) | | | NA | | | | NA | |

Investing activities(4) | | | (84,500 | ) | | | (144,100 | ) | | | 3,300 | | | | 26,100 | | | | (11,700 | ) | | | — | | | | — | | | | (1,383,941 | ) | | | NA | | | | NA | |

Financing activities(4) | | | (77,100 | ) | | | 18,900 | | | | (110,200 | ) | | | (89,400 | ) | | | (24,000 | ) | | | — | | | | — | | | | 1,411,737 | | | | NA | | | | NA | |

Other financial data: | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Ratio of earnings to fixed

charges(5) | | | 2.9 | | | | 1.7 | | | | 2.5 | | | | 2.6 | | | | 3.0 | | | | NA | | | | NA | | | | NA | | | | NA | | | | NA | |

EBITDA— | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Net income (loss) | | $ | 50,900 | | | $ | 65,500 | | | $ | 36,900 | | | $ | 29,700 | | | $ | 16,100 | | | $ | (17,373 | ) | | $ | (3,430 | ) | | $ | (131,434 | ) | | $ | (130,770 | ) | | $ | (143,552 | ) |

Interest expense | | | 37,400 | | | | 33,700 | | | | 36,800 | | | | 27,000 | | | | 11,700 | | | | — | | | | — | | | | 51,604 | | | | 111,200 | | | | 88,671 | |

Provision for income tax | | | 27,800 | | | | 8,800 | | | | 20,500 | | | | 15,500 | | | | 8,700 | | | | — | | | | — | | | | 2,600 | | | | 6,000 | | | | 4,600 | |

Depreciation and amortization | | | 107,900 | | | | 109,400 | | | | 114,800 | | | | 87,100 | | | | 39,600 | | | | — | | | | — | | | | 66,643 | | | | 159,632 | | | | 119,854 | |

| | |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

|

EBITDA(6) | | $ | 224,000 | | | $ | 217,400 | | | $ | 209,000 | | | $ | 159,300 | | | $ | 76,100 | | | $ | (17,373 | ) | | $ | (3,430 | ) | | $ | (10,587 | ) | | $ | 146,062 | | | $ | 69,573 | |

| | |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

|

Balance Sheet data (as of end of period): | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Cash | | $ | 300 | | | $ | 400 | | | $ | 1,200 | | | $ | 100 | | | $ | 1,700 | | | $ | — | | | $ | — | | | $ | 8,290 | | | | NA | | | | NA | |

Property, plant and equipment, net | | | 685,300 | | | | 786,400 | | | | 734,000 | | | | 740,900 | | | | 717,800 | | | | 962 | | | | — | | | | 793,236 | | | | NA | | | | NA | |

Total assets | | | 1,510,600 | | | | 1,607,700 | | | | 1,489,000 | | | | 1,502,000 | | | | 1,459,800 | | | | 6,734 | | | | 5,017 | | | | 1,756,563 | | | | NA | | | | NA | |

Long-term debt | | | 428,000 | | | | 427,400 | | | | 301,700 | | | | 301,800 | | | | 151,300 | | | | — | | | | — | | | | 1,319,500 | | | | NA | | | | NA | |

Stockholder’s equity/(deficiency) parent funding | | | 380,700 | | | | 419,200 | | | | 410,000 | | | | 414,100 | | | | 685,800 | | | | (17,373 | ) | | | (3,430 | ) | | | 286,197 | | | | NA | | | | NA | |

| (1) | The consolidated financial information for the Company includes the consolidated financial position, results of operations and cash flows of the Company from inception on May 21, 2004 and also includes the results of Verizon’s Hawaii Business from the May 2, 2005 acquisition date. |

| (2) | Depreciation and amortization for the Company reflects the depreciation of acquired property and equipment and amortization of acquired amortizable intangibles based on the estimated fair value and useful lives as of the May 2, 2005 acquisition date. |

| (3) | The operating loss for the Company is, in part, due to the transition costs the Company is incurring to become a stand-alone provider of telecommunications services. |

| (4) | The Company’s investing and financing activities during the nine months ended September 30, 2005 include the Hawaii Business Transactions. |

| (5) | For purposes of this computation, “earnings” consist of pre-tax income from continuing operations before adjustment for income or loss from equity investees, plus dividends from equity investees, plus fixed charges and amortization of capitalized interest less capitalized interest. “Fixed charges” consist of interest expense on all indebtedness plus amortization of debt issuance fees, the interest component of lease rental expense and capitalized interest. There were no fixed charges for the Company for the nine months ended September 30, 2004 and year ended December 31, 2004. For the nine months ended September 30, 2005, the Company’s deficiency of earnings to fixed charges amounted to $129,538. On a pro forma basis, the deficiency of earnings to fixed charges amounted to $130,760 and $144,336 for the year ended December 31, 2004 and nine months ended September 30, 2005, respectively. |

| (6) | EBITDA is defined as net income (loss) plus interest expense (net of interest income), income taxes, depreciation and amortization. We believe that GAAP-based financial information for highly leveraged businesses, such as ours, should be supplemented by EBITDA so that investors better understand our financial information in connection with their analysis of our business. The following demonstrates and forms the basis for such belief: (i) EBITDA is a component of the measure used by our board of directors and management team to evaluate our operating performance, (ii) our senior credit facilities contain covenants that require us to maintain certain interest expense coverage and leverage ratios, which contain EBITDA as a component, and restrict upstream cash payments if certain ratios are not met, subject to certain exclusions, and our management team uses EBITDA to monitor compliance with such covenants, (iii) EBITDA is a component of the measure used by our management team to make day-to-day operating decisions, (iv) EBITDA is a component of the measure used by our management to facilitate internal comparisons to competitors’ results and the telecommunications industry in general and (v) the payment of discretionary bonuses to certain members of our management is contingent upon, among other things, the satisfaction of certain targets, which contain EBITDA as a component. We acknowledge that there are limitations when using EBITDA. EBITDA is not a recognized term under GAAP and does not purport to be an alternative to net income (loss) as a measure of operating performance or to cash flows from operating activities as a measure of liquidity. Additionally, EBITDA is not intended to be a measure of free cash flow for management’s discretionary use, as it does not consider certain cash requirements such as tax payments and debt service requirements. Because all companies do not use identical calculations, this presentation of EBITDA may not be comparable to other similarly titled measures of other companies. |

18

Risk Factors

You should carefully consider the risk factors set forth below as well as the other information contained in this prospectus before making a decision to participate in the exchange offer. The risks described below are not the only risks facing us. Additional risks and uncertainties not currently known to us or that we currently deem to be immaterial may also materially and adversely affect our business operations. Any of the following risks could materially adversely affect our business, financial condition or results of operations. In such case, you may lose all or part of your original investment.

Risks Relating to our Business

We do not believe that our historical and pro forma financial information reflect our anticipated cost structure or are indicative of what our results of operations would have been as a stand-alone telecommunications provider.

We do not believe that the historical and pro forma financial information included in this prospectus reflect what our results of operations, financial position or cash flow would have been had we been a stand-alone telecommunications provider during the periods presented, what our cost structure will be as a stand-alone telecommunications provider, or what our results of operations, financial position or cash flows will be in the future.

The audited combined financial statements of our Predecessor included in this prospectus have been derived from the books and records of Verizon Hawaii, a wholly-owned subsidiary of GTE prior to the Hawaii Business Acquisition, and certain affiliates of Verizon. Preparing such audited combined financial statements required management of Verizon and GTE to assign certain assets, liabilities, revenues and expenses, including expenses for services provided to us by Verizon and its affiliates. These assignments are based on certain assumptions, and, as a result, such audited financial statements may not reflect what our results of operations, financial position or cash flow would have been if we had operated as a stand-alone provider of telecommunications services for the periods presented. In addition, the historical and pro forma financial statements included in this prospectus reflect expenses for services provided to us by Verizon and its affiliates. In connection with a transition period following the Hawaii Business Acquisition, we continue to receive certain services from Verizon and its affiliates at the prices set forth in our Transition Services Agreement and the Verizon Master Services Agreement. The expenses we are incurring under the Transition Services Agreement and the Verizon Master Services Agreement do not equal the expenses we have incurred for the same services provided by Verizon and its affiliates prior to the Hawaii Business Acquisition. After the dates on which Verizon ceases to provide services to us, we expect services previously provided by Verizon to be provided by our internal operations or from third-party service providers. It is unlikely that the expenses we will incur for such services in the future will reflect the historical expenses for such services included in the audited and pro forma financial statements included in this prospectus. Accordingly, we do not believe that the historical information included in the financial statements and the pro forma financial information contained in this prospectus are indicative of our future performance or reflect what our cost structure would have been had we operated as a stand-alone telecommunications provider during the periods presented.

We have limited experience operating as a stand-alone provider of telecommunications services. We may be materially and adversely affected by the separation of our business from that of Verizon.

We have limited experience operating as a stand-alone provider of telecommunications services. The separation from Verizon and our transition to a stand-alone provider of telecommunications services present several material risks and uncertainties that you should consider before making a decision to participate in the exchange offer. These risks include the following:

19

During the transition period, we are relying on Verizon to provide us with services that are critical to the ongoing operation of our business.

Verizon and its affiliates have historically provided us with services that are critical to the ongoing operation of our business. Among other things, Verizon and its affiliates have provided:

| | • | | proprietary software that enables us to operate our local telecommunications network; |

| | • | | a connection to the Internet backbone; and |

| | • | | critical back-office, network management, logistical and procurement services, including billing, customer relationship management, corporate finance, human resource, payroll and IT services. |

Pursuant to a Transition Services Agreement, which details Verizon’s obligations to provide the services described above during the transition period, we continue to rely on Verizon and its affiliates to provide us with such software and services, as well as other critical services. See “The Hawaii Business Transactions—Transition Services Agreement.” Pursuant to the Verizon Master Services Agreement, Verizon and its affiliates are also providing us with long distance voice and data services for a transition period following the Hawaii Business Acquisition. See “The Hawaii Business Transactions—The Transition.” If, notwithstanding the Transition Services Agreement and Verizon Master Services Agreement, Verizon or its affiliates fail or are unable to continue to provide such services to us, our business, financial condition and results of operations could be materially and adversely affected.

We also rely on Verizon for certain accounting services and related account reconciliations. This significant dependency on Verizon, in combination with our initial development of processes, procedures and controls as a stand-alone provider, increase the risk of material internal control deficiencies and the related probability of a restatement of our operating results. Any deficiency in Verizon’s internal controls will affect our reported financial information. Furthermore, Verizon’s internal processes may create deficiencies for us because certain processes deemed by Verizon not to be part of their key control environment may be material to our key control environment.

After the dates on which Verizon is no longer required to provide services to us, we expect to receive such services from our internal operations or third-party service providers. We may not be able to obtain such services on commercially reasonable terms.

After the dates on which Verizon is no longer required to provide services to us, we expect that such services will be provided by our internal operations or third-party service providers. We cannot assure you that we will be able to develop the ability to provide any of these services ourselves on a cost efficient basis.