Exhibit 99.1

| Helmerich & Payne, Inc. 4th Annual Johnson Rice Energy Conference October 2-3, 2012 |

| Statements within this presentation are “forward-looking statements” within the meaning of the Securities Act of 1933 and the Securities Exchange Act of 1934, and are based on current expectations and assumptions that are subject to risks and uncertainties. All statements other than statements of historical facts included in this release, including, without limitation, statements regarding the registrant’s future financial position, business strategy, budgets, projected costs, rig performance and plans and objectives of management for future operations, are forward looking statements. For information regarding risks and uncertainties associated with the Company’s business, please refer to the “Risk Factors” and “Management’s Discussion & Analysis of Financial Condition and Results of Operations” sections of the Company’s SEC filings, including but not limited to, its annual report on Form 10-K and quarterly reports on Form 10-Q. As a result of these factors, Helmerich & Payne, Inc.’s actual results may differ materially from those indicated or implied by such forward-looking statements. We undertake no duty to update or revise our forward-looking statements based on changes in internal estimates, expectations or otherwise, except as required by law. Forward-looking Statements |

| * Includes 16 announced new FlexRigs under construction with customer commitments as of September 28, 2012 that are scheduled for completion during fiscal 2012 and fiscal 2013. |

| Comments on U.S. land market conditions Growing shareholder value through FlexRig® innovation Market share leader in AC drive rigs and active rigs Unconventional plays shape the drilling landscape The rig replacement cycle continues Topics Today |

| U.S. Land Industry Rig Count |

| Comments on Today’s U.S. Land Market AC drive rigs are still experiencing strong utilization levels 98% of H&P’s active rigs are AC drive rigs H&P’s rig count and spot pricing continue to slightly soften Our position is strengthened by: Long-term contract coverage Spot rigs are high quality and liquids oriented Our operational outlook for the fourth fiscal quarter remains unchanged (not only for U.S. Land, but also for Offshore and International Land) |

| Growing Shareholder Value |

| Innovation & Applied Technology AC Driven Systems & Integrated Top Drive Mechanized Tubular Handling Computerized Controls BOP Handling Driller’s Cabin Satellite Communications Rig Move Capabilities |

| The FlexRig Difference: Key Advantages Increased drilling productivity and reliability Variable frequency (AC) drives with increased precision and measurability Computerized electronic driller that more precisely controls weight on bit, rotation and pressure Designed to move quickly from well to well Accelerated well programs and NPV gains An enhanced and significantly safer workplace Minimized impact to the environment Total well cost savings even at premium dayrates H&P’s FlexRig Advantage |

| A Value Proposition Example – H&P vs. Competitors Estimated Estimated Peer H&P FlexRig3 Conventional Fit-for-purpose Average Average Average 2012 (Spot Market) (Spot Market) (Spot Market) 1. Drilling days 20 13 9 Other days 3 3 3 Moving days 7 4 3 Total rig revenue days per well 30 20 15 2. Drilling contractor dayrate $17,500 $23,000 $28,000 Operator’s other intangible $25,000 $25,000 $25,000 cost per day estimate Total daily cost estimate $42,500 $48,000 $53,000 Total cost per well (daily services) $1,275,000 $960,000 $795,000 3. Total well savings with H&P – per well $480,000 $165,000 per year $11.7MM $4.0MM increased wells per rig per year versus conventional average: 12 wells Increased wells per rig per year versus peer fit-for-purpose: 6 wells |

| Organic U.S. Land Fleet Growth * Estimates include existing rigs and announced new build commitments. 304 49 |

| H&P’s New Build Advantages We have been improving and honing the process for over 10 years, prompting our assertion that we build a better rig for less Safety is our first priority, followed by a relentless focus on strong execution and performance in the field Exceptional fleet uniformity Extensive collaboration with customers and suppliers A strong organizational orientation to consistent, repeatable, field execution |

| Lean Manufacturing New Electrical Systems Test Assembly and Outfitting Unitizing Packages Fabricating New Structures Processing Raw Materials Building a New FlexRig® Commissioning / Delivery |

| Technology & Quality Service Make a Difference (1) Does not include the impact of early contract termination revenue. (2) Represents weighted-average rig margin per day for PTEN, NBR and UNT. (3) Utilization is herein calculated to be average active rigs divided by estimated available marketable rigs. (4) Represents estimated average combined utilization for PTEN, NBR, and UNT in the Lower 48 land market. H&P’s Margin Premium H&P’s Utilization Premium (1) (2) (3) (4) |

| Most Profitable Driller in U.S. Land Business (2) PTEN’s operating income includes drilling operations in Canada. (1) NBR’s operating income corresponds to its U.S. Lower 48 Land Drilling segment. (2) (1) |

| Five-Year Relative Shareholder Return Source: Thomson Financial as of September 25, 2012 |

| H&P’s Lead in U.S. Land AC Drive Rigs Note: The above estimates corresponding to U.S. lower 48 AC Drive fleets and new build commitments are derived from Rig Data and corporate filings. |

| AC Drive U.S. Rig Market Share (~600 Rigs) Note: The above estimates corresponding to market share are derived from multiple sources including Rig Data, Smith Bits, and corporate filings. |

| Our FlexRig New Build Efforts We are the most active driller in the U.S. land market as a result of our very significant lead in the growing segment of advanced technology AC drive rigs. We have continued to make new build deliveries on time and on budget, including nine new FlexRigs since our last webcast. We have 16 FlexRigs under construction with long-term contracts that are scheduled to continue to deploy at the rate of four per month through early calendar 2013. |

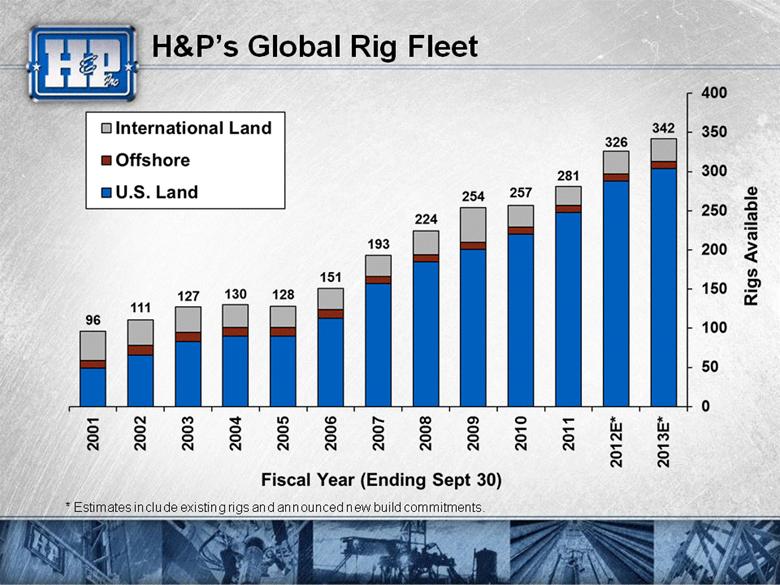

| H&P Activity as of September 28, 2012 Rigs Working/ Contracted 230 8 26 264 16 280 Rigs Available 288 9 29 326 16 342 % Contracted 80% 89% 90% 81% U.S. Land Offshore International Land Total FlexRig Construction Total Fleet Includes announced new build commitments. (1) |

| H&P U.S. Land Fleet by Power Type SCR Rigs 2% (230 Active Rigs in the U.S. By Power Type) |

| H&P’s U.S. Land Fleet Activity Active rigs on term (in blue) generated both revenue and revenue days. Includes completed new builds that were waiting on operators and which generated revenue but did not generate revenue days. (1) (2) |

| H&P’s Advanced Technology Footprint (230 Active Rigs in the U.S. By Power Type) |

| H&P Global Fleet Under Term Contract |

| H&P vs. Industry U.S. Land Customer Base Note: The above estimates corresponding to the active rig fleet in the U.S. are derived from multiple sources including Rig Data, Smith Bits, and corporate filings. |

| Lower 48 U.S. Land Market Share Active Rig Market Share - Ten Years Ago Note: The above estimates are derived from Smith Bits As of September 20, 2002 |

| Lower 48 U.S. Land Market Share Organically Growing Active Rig Market Share Note: The above estimates are derived from Smith Bits As of September 21, 2012 |

| Unconventional Plays Shaping Landscape Well complexity is increasing: Technology solutions that provide safe, environmentally sound and efficient operations are required by contractors to be competitive Extended reach laterals progressively longer Multi-well pad drilling gaining acceptance in more areas A factory approach to drilling wells is required This all creates an expanding level of demand for FlexRigs |

| Increasing Focus on More Difficult Drilling |

| The Ongoing Gas to Oil Transition... |

| (246 H&P Contracted Land Rigs as of 9/28/12*) Leading U.S. Unconventional Driller * Includes announced new FlexRigs with customer commitments scheduled for completion in fiscal 2012 and fiscal 2013. |

| Dry Gas (Long-term Contracts) 4% H&P’s Growing Exposure to Oil & Liquids Estimated proportion of H&P’s active U.S. Land rigs by primary hydrocarbon target as of 9/28/12 Includes one rig with a contract expiring during the quarter ending 12/31/12. Approximately one-fourth of rigs in this category are primarily drilling for liquids-rich gas. Dry Gas (Spot Market) 1% (1) (2) |

| The Replacement Cycle Continues AC drive rigs are best positioned to make the transition. Older, underperforming rigs are more likely to be sidelined. Since the 2008-2009 downturn, approximately 300 rigs have permanently stacked, and about 70% of these were mechanical rigs. Advanced technology AC drive rigs continue to displace mechanical and SCR rigs. |

| An Undersupply of AC Drive Rigs (~1,750 Active Rigs in the U.S. By Power Type) Note: The above estimates corresponding to rig activity are derived from multiple sources including Rig Data, Smith Bits, and corporate filings. Additionally, the drawworks capacity of each land rig included in the above analysis was greater than 600 horsepower. Certain assumptions were made on approximately 8% of the active rigs that were not readily identified. |

| Week Ended October 4, 2008 By Power Type 2008 Peak Rig Count (~1,925) - U.S. Land Note: The above estimates corresponding to rig activity are derived from multiple sources including Rig Data, Smith Bits, and corporate filings. Additionally, the drawworks capacity of each land rig included in the above analysis was greater than 600 horsepower. Certain assumptions were made on approximately 10% of the active rigs that were not readily identified. |

| Week Ended September 21, 2012 By Power Type Current Rig Count (~1,750) - U.S. Land Note: The above estimates corresponding to rig activity are derived from multiple sources including Rig Data, Smith Bits, and corporate filings. Additionally, the drawworks capacity of each land rig included in the above analysis was greater than 600 horsepower. Certain assumptions were made on approximately 8% of the active rigs that were not readily identified. |

| Our New Build Opportunities We do not believe that the replacement cycle is over, and our approach will be to make sure that our supply chain is ready to respond to incremental demand on a timely basis. Commodity price volatility and our customers’ desire to stay within 2012 budgets has resulted in fewer conversations regarding new build orders. Our integrated FlexRig manufacturing effort affords us an important flexibility that should serve us well. |

| Performance is Not Only About Better Rigs It’s also about: People Safety Experience Training Culture Support Structure Processes Organizational Network Maintenance Supply Chain |

| Note: Injury data taken from IADC ASP Program. Footage data taken from Land Rig Newsletter. 11.7 9.1 5.2 2.2 Recordable Injuries per 1-MM Feet Drilled in 2011 by the Largest U.S. Land Drilling Contractors |

| Performance is Not Only About Better Rigs It’s also about: People Safety Experience Training Culture Support Structure Processes Organizational Network Maintenance Supply Chain |

| H&P Competitive Advantages Our people, processes and FlexRig technology create a very important competitive advantage for the Company. Our value proposition will continue to be directed toward delivering compelling performance for our customers and shareholders. The shift to drilling more complex unconventional resource plays that require the drilling of horizontal and directional wells only magnifies our competitive advantage. |

| End of Presentation |

| Additional References |

| Changes in Lower 48 U.S. Land Rig Count * PDS’ active rig count includes both PDS and GW rigs. |

| H&P’s Global Rig Fleet * Estimates include existing rigs and announced new build commitments. |

| Active Contracted Idle Total Long-term Contracts Argentina 6 3 9 5 Bahrain 4 4 4 Colombia 7 7 2 Ecuador 5 5 Tunisia 2 2 U.A.E. 2 2 2 Total 26 3 29 13 H&P’s International Land Operations Rig Fleet Status (as of September 28, 2012) (1) 13 of 16 FlexRigs, included in the international fleet of 29 rigs, are under long-term contracts. (1) |

| End of Document |