2008 KeyBanc Capital Markets

Basic Materials and Packaging

Conference

Basic Materials and Packaging

Conference

Lamar M. Chambers

Senior Vice President and Chief Financial Officer

September 10, 2008

Forward-Looking Statements

This presentation contains forward-looking statements, within the meaning of Section 27A of the Securities Act of 1933

and Section 21E of the Securities Exchange Act of 1934. These statements include those made with respect to

Ashland’s operating performance and Ashland’s acquisition of Hercules Inc. These expectations are based upon a

number of assumptions, including those mentioned within this presentation. Performance estimates are also based

upon internal forecasts and analyses of current and future market conditions and trends, management plans and

strategies, weather, operating efficiencies and economic conditions, such as prices, supply and demand, cost of raw

materials, and legal proceedings and claims (including environmental and asbestos matters). These risks and

uncertainties may cause actual operating results to differ materially from those stated, projected or implied. Such risks

and uncertainties with respect to Ashland’s acquisition of Hercules include the possibility that the benefits anticipated

from the Hercules transaction will not be fully realized; the possibility the transaction may not close, including as a

result of failure to obtain the approval of Hercules stockholders; the possibility that financing may not be available on

the terms committed; and other risks that are described in filings made by Ashland with the Securities and Exchange

Commission (SEC) in connection with the proposed transaction. Although Ashland believes its expectations are based

on reasonable assumptions, it cannot assure the expectations reflected herein will be achieved. This forward-looking

information may prove to be inaccurate and actual results may differ significantly from those anticipated if one or more

of the underlying assumptions or expectations proves to be inaccurate or is unrealized or if other unexpected

conditions or events occur. Other factors, uncertainties and risks affecting Ashland are contained in Ashland's

periodic filings made with the SEC, including its Form 10-K for the fiscal year ended Sept. 30, 2007, and Forms 10-Q for

the quarters ended Dec. 31, 2007, and March 31 and June 30, 2008, which are available on Ashland’s Investor Relations

website at www.ashland.com/investors or the SEC’s website at www.sec.gov. Ashland undertakes no obligation to

subsequently update or revise the forward-looking statements made in this presentation to reflect events or

circumstances after the date of this presentation.

and Section 21E of the Securities Exchange Act of 1934. These statements include those made with respect to

Ashland’s operating performance and Ashland’s acquisition of Hercules Inc. These expectations are based upon a

number of assumptions, including those mentioned within this presentation. Performance estimates are also based

upon internal forecasts and analyses of current and future market conditions and trends, management plans and

strategies, weather, operating efficiencies and economic conditions, such as prices, supply and demand, cost of raw

materials, and legal proceedings and claims (including environmental and asbestos matters). These risks and

uncertainties may cause actual operating results to differ materially from those stated, projected or implied. Such risks

and uncertainties with respect to Ashland’s acquisition of Hercules include the possibility that the benefits anticipated

from the Hercules transaction will not be fully realized; the possibility the transaction may not close, including as a

result of failure to obtain the approval of Hercules stockholders; the possibility that financing may not be available on

the terms committed; and other risks that are described in filings made by Ashland with the Securities and Exchange

Commission (SEC) in connection with the proposed transaction. Although Ashland believes its expectations are based

on reasonable assumptions, it cannot assure the expectations reflected herein will be achieved. This forward-looking

information may prove to be inaccurate and actual results may differ significantly from those anticipated if one or more

of the underlying assumptions or expectations proves to be inaccurate or is unrealized or if other unexpected

conditions or events occur. Other factors, uncertainties and risks affecting Ashland are contained in Ashland's

periodic filings made with the SEC, including its Form 10-K for the fiscal year ended Sept. 30, 2007, and Forms 10-Q for

the quarters ended Dec. 31, 2007, and March 31 and June 30, 2008, which are available on Ashland’s Investor Relations

website at www.ashland.com/investors or the SEC’s website at www.sec.gov. Ashland undertakes no obligation to

subsequently update or revise the forward-looking statements made in this presentation to reflect events or

circumstances after the date of this presentation.

ADDITIONAL INFORMATION

In connection with the proposed transaction, Ashland filed a registration statement with the SEC on Form S-4 (File No.

333-152911) containing a preliminary proxy statement/prospectus and Ashland and Hercules expect to mail a definitive

proxy statement/prospectus to Hercules' shareholders containing information about the merger. Investors and security

holders are urged to read the registration statement on Form S-4 and the proxy statement/prospectus because they

contain important information about the proposed transaction. Investors and security holders may obtain free copies

of these documents and other documents filed with the SEC by contacting Ashland Investor Relations at (859) 815-

4454 or Hercules Investor Relations at (302) 594-7151, or free copies may also be obtained from Ashland's Investor

Relations website at www.ashland.com/investors or Hercules' website at www.herc.com or the SEC's website at

www.sec.gov.

333-152911) containing a preliminary proxy statement/prospectus and Ashland and Hercules expect to mail a definitive

proxy statement/prospectus to Hercules' shareholders containing information about the merger. Investors and security

holders are urged to read the registration statement on Form S-4 and the proxy statement/prospectus because they

contain important information about the proposed transaction. Investors and security holders may obtain free copies

of these documents and other documents filed with the SEC by contacting Ashland Investor Relations at (859) 815-

4454 or Hercules Investor Relations at (302) 594-7151, or free copies may also be obtained from Ashland's Investor

Relations website at www.ashland.com/investors or Hercules' website at www.herc.com or the SEC's website at

www.sec.gov.

Business Overview

• Founded in 1924; sales in 100 countries

• Number of employees: ~11,700

• A leading manufacturer of composite

polymers, adhesives, metal casting

consumables, and process and utility water

treatments

polymers, adhesives, metal casting

consumables, and process and utility water

treatments

• A leading North American distributor of

chemicals, plastics and composite materials

chemicals, plastics and composite materials

• Marketer of premium-branded lubricants,

automotive chemicals and quick-lube services

automotive chemicals and quick-lube services

Business Description

Ashland

Distribution

51%

Distribution

51%

Ashland

Distribution

51%

Distribution

51%

Performance

Materials

19%

Materials

19%

Performance

Materials

19%

Materials

19%

Valvoline

20%

20%

Sales & Operating Revenue*: $8.3 billion

Adjusted EBITDA*: $366 million

Adjusted EBITDA* Margin: 4.4%

Ashland

Distribution

19%

Distribution

19%

Ashland

Distribution

19%

Distribution

19%

Performance

Materials

29%

Materials

29%

Performance

Materials

29%

Materials

29%

Valvoline

37%

37%

10%

10%

15%

15%

* For the 12 months ended June 30, 2008. Sales & Operating Revenue includes intersegment sales. Adjusted

EBITDA in the pie chart graph excludes Unallocated and Other. See Appendix for Adjusted EBITDA reconciliation.

EBITDA in the pie chart graph excludes Unallocated and Other. See Appendix for Adjusted EBITDA reconciliation.

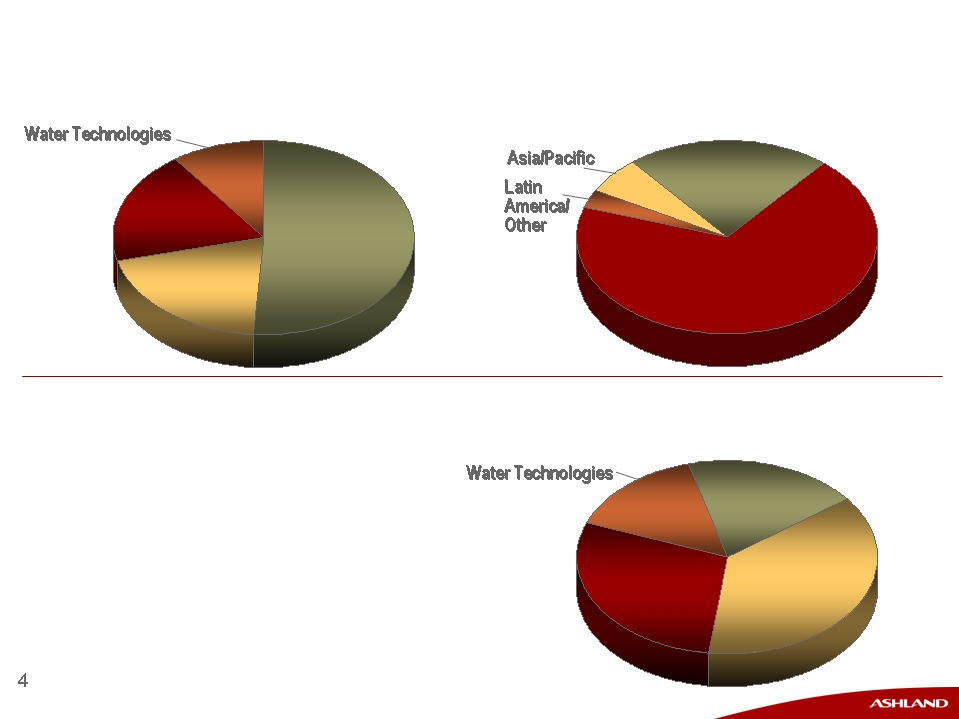

3%

3%

North

America

69%

America

69%

North

America

69%

America

69%

Europe

22%

22%

Europe

22%

22%

6%

6%

Ashland Overview

Pkg. &

Converting - -

9%

9%

North

America

America

North

America

America

47%

47%

Europe

36%

Latin

America/

Other - -

America/

Other - -

9%

Trans-

portation

portation

Trans-

portation

portation

24%

24%

Ind.

Constr.

Constr.

28%

Revenue

by Geography

by Geography

Revenue

by Market

by Market

For the 12 Months Ended June 30, 2008

Revenue: $1.6 billion

Adjusted EBITDA*: $95 million

Adjusted EBITDA* Margin: 5.8%

Res.

Constr.

Constr.

14%

Infra-

structure

structure

15%

Marine - - 10%

Asia/

Pacific - - 8%

Pacific - - 8%

* See Appendix for Adjusted EBITDA reconciliation.

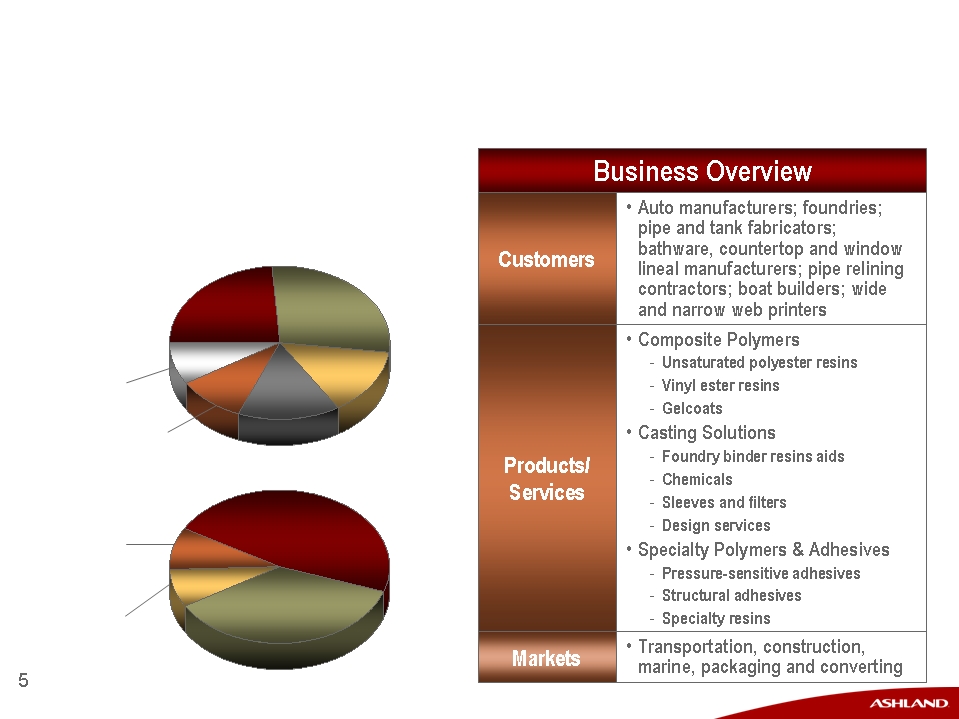

Ashland Performance Materials

A global leader in specialty chemicals

A global leader in specialty chemicals

Chemicals

Chemicals

45%

45%

Plastics

42%

Environmental

Service/Other - -

2%

Service/Other - -

2%

Construction

Construction

24%

24%

Other

15%

Revenue

by Product

Line

by Product

Line

Revenue

by Market

by Market

Trans-

portation

portation

15%

Paint & Coatings - 10%

Medical - - 6%

Marine - - 4%

Com-

posites

posites

11%

Chemical Mfg.

- 11%

- 11%

Retail

Consumer - - 8%

Consumer - - 8%

Personal

Care - - 7%

Care - - 7%

For the 12 Months Ended June 30, 2008

Revenue: $4.3 billion

Adjusted EBITDA*: $61 million

Adjusted EBITDA* Margin: 1.4%

* See Appendix for Adjusted EBITDA reconciliation.

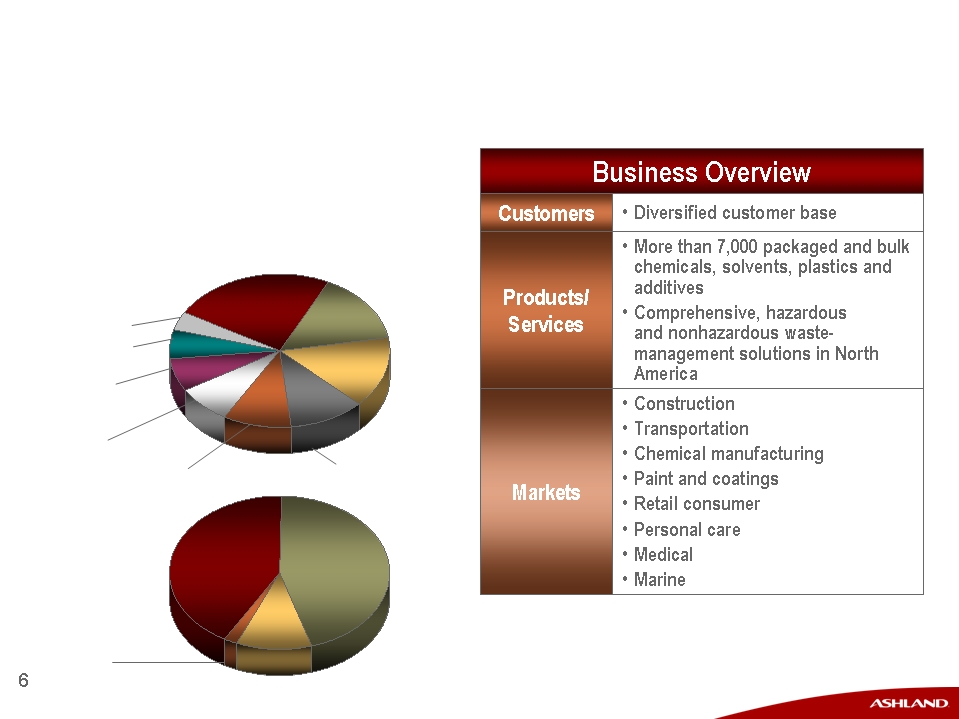

Ashland Distribution

A leading North American chemical and plastics distributor

A leading North American chemical and plastics distributor

Lubricants

84%

Filters - - 3%

Valvoline

Int'l - - 22%

Int'l - - 22%

Valvoline

Int'l - - 22%

Int'l - - 22%

Do-It-

Yourself

Yourself

35%

Revenue

by Product Line

by Product Line

Revenue

by Market Channel

by Market Channel

Do-It-

For-Me

36%

For-Me

36%

DIFM:

Installer channel

26%

Installer channel

26%

Specialty/

Other - - 7%

Other - - 7%

DIFM:

Valvoline Instant

Oil Change - 10%

Valvoline Instant

Oil Change - 10%

Chemicals - - 4%

Appearance

products - - 3%

products - - 3%

Antifreeze - - 6%

For the 12 Months Ended June 30, 2008

Revenue: $1.6 billion

Adjusted EBITDA*: $120 million

Adjusted EBITDA* Margin: 7.5%

* See Appendix for Adjusted EBITDA reconciliation.

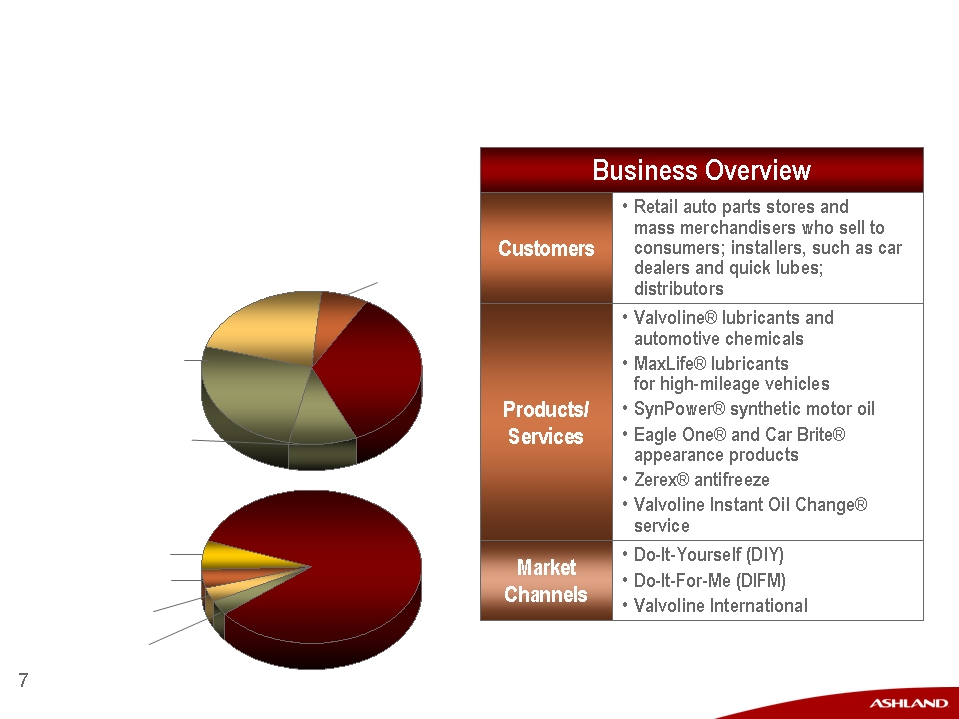

Valvoline: A leading worldwide marketer

of premium-branded automotive lubricants and chemicals

of premium-branded automotive lubricants and chemicals

North

America

America

27%

Latin America/

Other - 5%

Other - 5%

Marine

16%

16%

Marine

16%

16%

Industrial

41%

Revenue

by Geography

by Geography

Revenue

by Business Unit

by Business Unit

E&PS

43%

43%

Asia/

Pacific

17%

Pacific

17%

Europe

51%

51%

For the 12 Months Ended June 30, 2008

Revenue: $0.9 billion

Adjusted EBITDA*: $47 million

Adjusted EBITDA* Margin: 5.1%

* See Appendix for Adjusted EBITDA reconciliation.

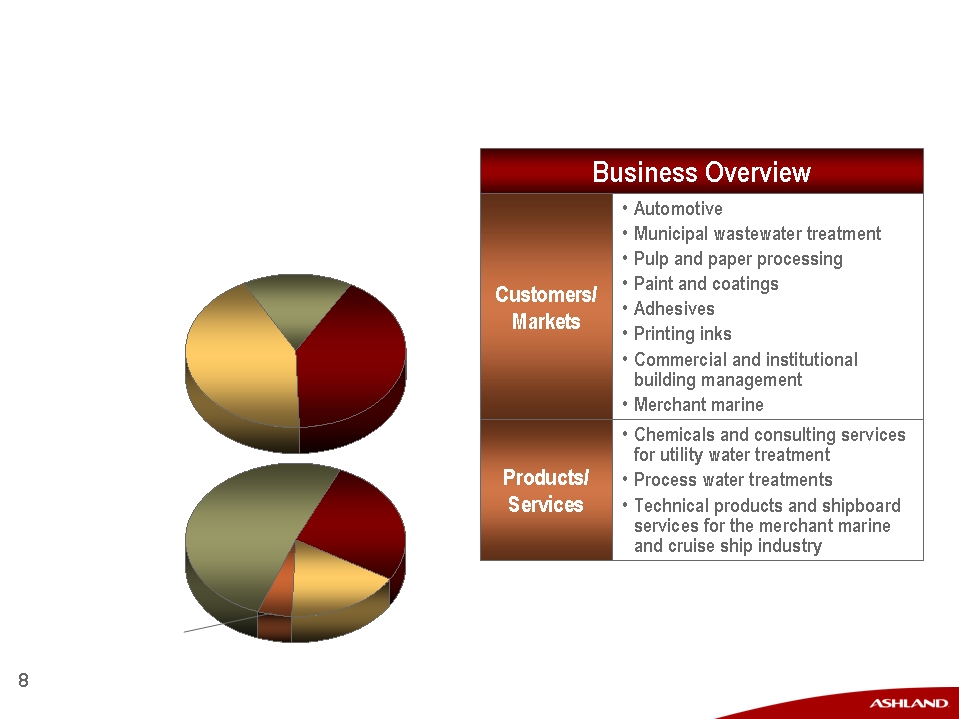

Ashland Water Technologies

A major global supplier to the water treatment industry

A major global supplier to the water treatment industry

Hercules Acquisition

Update

Update

• Creates a major, global specialty chemicals company

– ~75 percent of estimated pro forma adjusted EBITDA* derived from specialty

chemicals

chemicals

– More than $10 billion in pro forma revenue

– Boosts pro forma revenue from outside North America to approximately

$3.5 billion

$3.5 billion

• Significantly enhances focus and expands scale

in three specialty chemical businesses

in three specialty chemical businesses

– Specialty additives and ingredients, paper and water technologies,

and specialty resins

and specialty resins

• Creates leadership position in attractive and growing

renewable/sustainable chemistries

renewable/sustainable chemistries

– Derives approximately one-third of estimated pro forma EBITDA

from bio-based chemistries

from bio-based chemistries

* For the 12 months ended June 30, 2008. Sales & Operating Revenue includes intersegment sales.

EBITDA excludes Ashland Unallocated and Other and Hercules Corporate Items.

EBITDA excludes Ashland Unallocated and Other and Hercules Corporate Items.

Drives stronger, more profitable

and less cyclical earnings

and less cyclical earnings

Hercules Acquisition

Strategic Benefits

Strategic Benefits

• Founded in 1912 as a spinoff from DuPont

• Number of employees: ~4,700

• Leading supplier of functional, process

and water treatment chemical programs

for the pulp and paper industry

and water treatment chemical programs

for the pulp and paper industry

• World leader in products that manage

the flow characteristics of water-based

products

the flow characteristics of water-based

products

Business Description

Paper

Technologies

& Ventures

53%

Technologies

& Ventures

53%

Paper

Technologies

& Ventures

53%

Technologies

& Ventures

53%

Aqualon

47%

Sales & Operating Revenue*: $2.3 billion

Adjusted EBITDA*: $394 million

Adjusted EBITDA* Margin: 17.5%

Aqualon

61%

61%

EBITDA Margin

24%

24%

Paper

Technologies

& Ventures

39%

Technologies

& Ventures

39%

* For the 12 months ended June 30, 2008, as previously reported by Hercules. Adjusted EBITDA in the

pie chart graph excludes Corporate Items. See Appendix for Adjusted EBITDA reconciliation.

pie chart graph excludes Corporate Items. See Appendix for Adjusted EBITDA reconciliation.

Latin

America/

Other

America/

Other

6%

6%

Asia/Pacific

North

America

46%

America

46%

North

America

46%

America

46%

Europe

36%

36%

Europe

36%

36%

12%

12%

EBITDA

Margin

14%

Margin

14%

Hercules Overview

North

America

America

North

America

America

55%

55%

Asia-

Pacific

Pacific

Asia-

Pacific

Pacific

8%

8%

Europe

31%

Latin America/

Other - 6%

Other - 6%

Functional

Chemicals

Chemicals

Functional

Chemicals

Chemicals

55%

55%

Ventures

21%

Process

Chemicals

Chemicals

Process

Chemicals

Chemicals

24%

24%

Revenue

by Geography**

by Geography**

Revenue

by Product**

by Product**

For the 12 Months Ended June 30, 2008

Revenue: $1.2 billion

Revenue: $1.2 billion

Adjusted EBITDA*: $165 million

Adjusted EBITDA* Margin: 13.8%

* See Appendix for Adjusted EBITDA reconciliation. ** For the 12 months ended December 31, 2007.

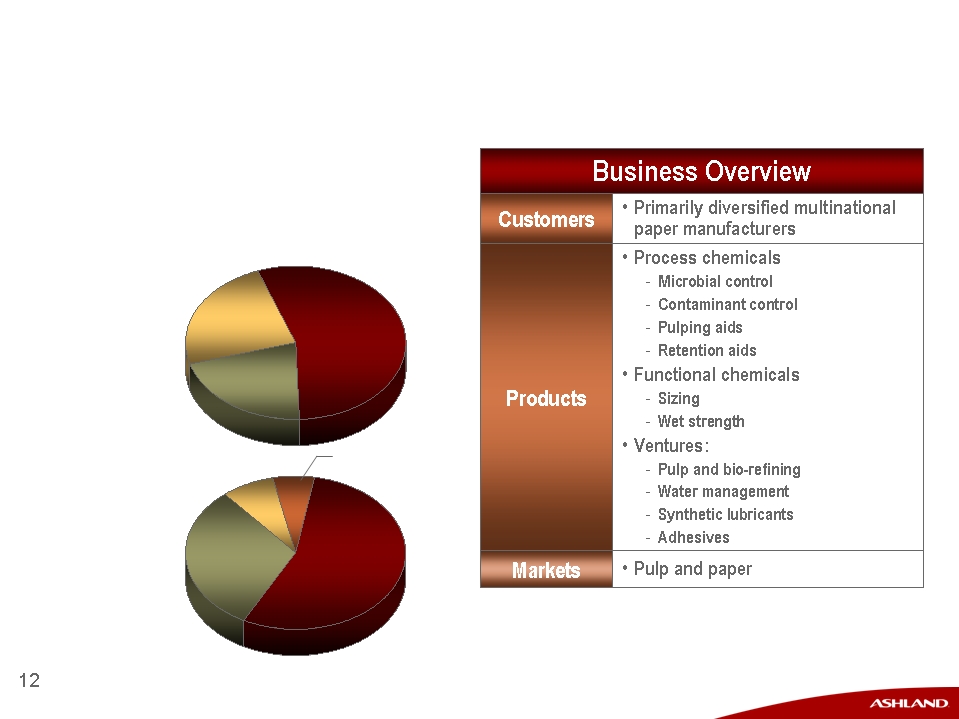

Paper Technologies and Ventures

A global leader in paper chemicals

A global leader in paper chemicals

North

America

America

North

America

America

38%

38%

Asia-

Pacific

Pacific

Asia-

Pacific

Pacific

15%

15%

Europe

41%

Latin America/

Other - - 6%

Coatings &

Construction

48%

Construction

48%

Coatings &

Construction

48%

Construction

48%

Energy &

Spec. Solutions

27%

Spec. Solutions

27%

Regulated

Industries

25%

Industries

25%

Regulated

Industries

25%

Industries

25%

Revenue

by Geography**

by Geography**

Revenue

by Product**

by Product**

For the 12 Months Ended June 30, 2008

Revenue: $1.1 billion

Revenue: $1.1 billion

Adjusted EBITDA*: $254 million

Adjusted EBITDA* Margin: 23.9%

* See Appendix for Adjusted EBITDA reconciliation. ** For the 12 months ended December 31, 2007.

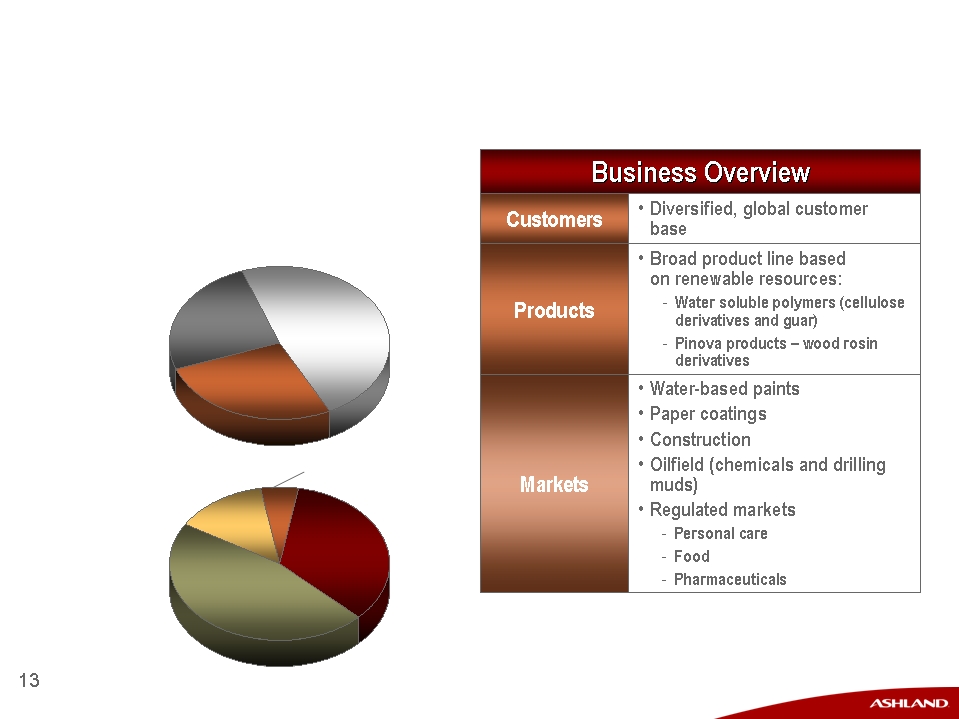

Aqualon Overview: A global leader

in managing rheology of water-based systems

in managing rheology of water-based systems

Sales/Mktg.

Manufacturing

Purchasing

~25%

Manufacturing

Purchasing

~25%

Sales/Mktg.

Manufacturing

Purchasing

~25%

Manufacturing

Purchasing

~25%

G&A

~75%

~75%

G&A

~75%

~75%

• Integration team to target

$30 million to $70 million

additional synergies, including:

$30 million to $70 million

additional synergies, including:

– Ashland Water

Technologies and Hercules

Paper Technologies &

Ventures commercial

efficiencies

Technologies and Hercules

Paper Technologies &

Ventures commercial

efficiencies

– Additional supply chain and

back office savings

back office savings

– Cross-selling of Ashland

Water products to paper

customers

Water products to paper

customers

Hercules Update

Synergies and Integration Costs

Synergies and Integration Costs

• $50 million initial estimate

– Basis for acquisition economics

– Run-rate savings by Year 3

– Estimated phasing (run rate)

• Year 1: 60 percent

• Year 2: 90 percent

• Year 3: 100 percent

• Estimated one-time integration costs

of $55 million to $60 million

of $55 million to $60 million

Hercules Acquisition

Update

Update

• Merger-control filings

- HSR early termination received

- EU merger-control filed, clearance expected early October

- All other foreign merger-control filings to be made

by mid-September

by mid-September

• SEC

- Form S-4 filed

- S-4 comments received

- Preparing responses; expect to resolve to meet closing schedule

• Financing

- Agent bank meeting

- Retail bank meeting scheduled next week

• Still expect closing in November

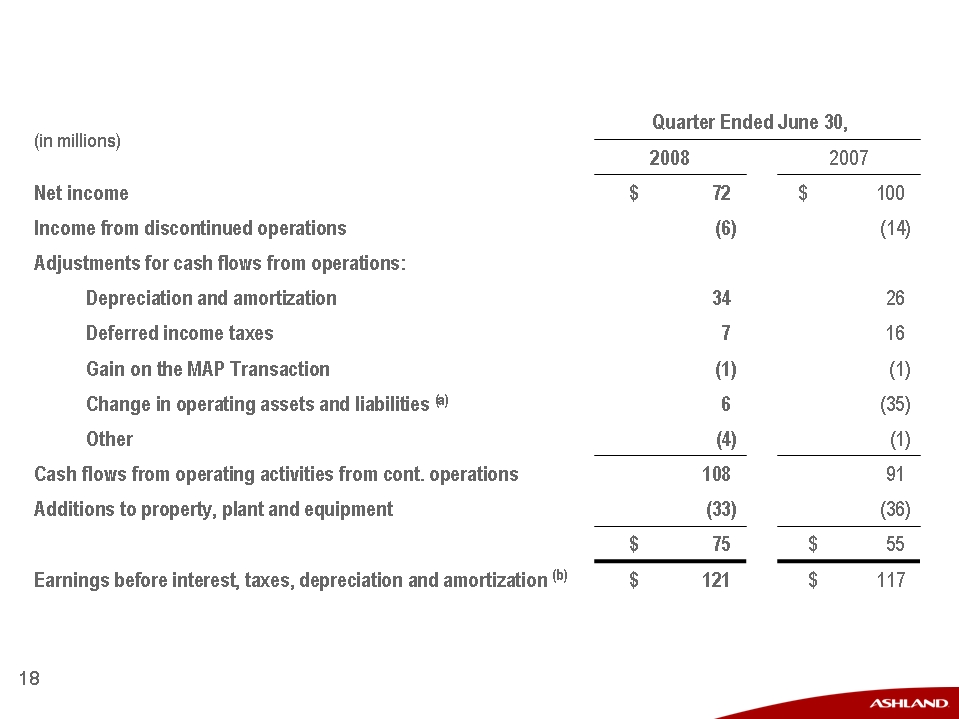

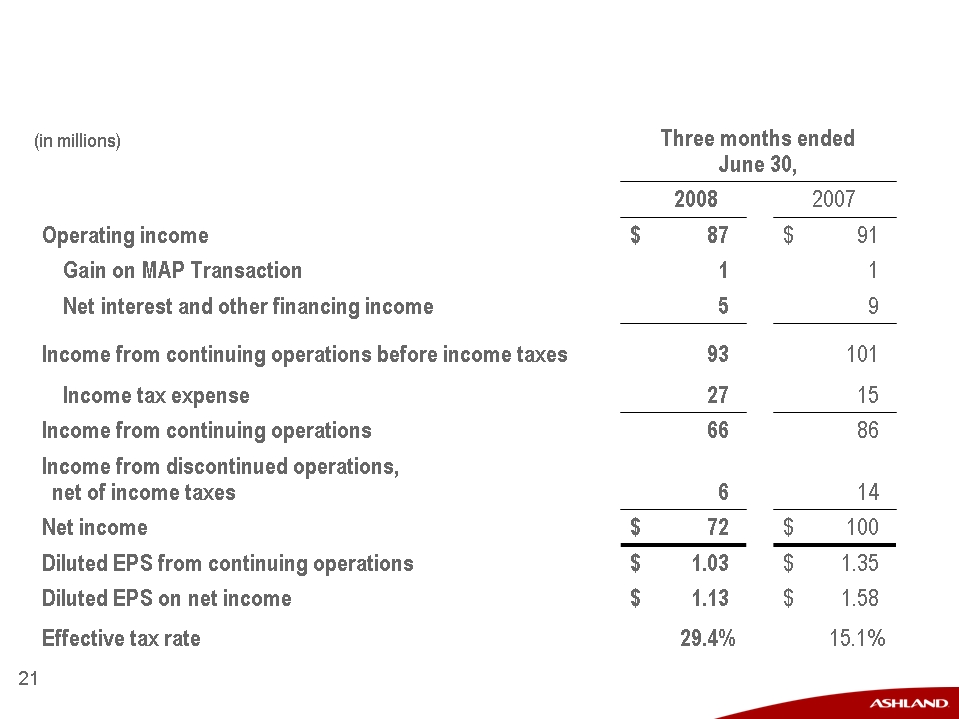

Fiscal Third-Quarter 2008

Earnings

Earnings

(a) When adjusted for key items in 2007 as noted in Appendix to this presentation.

(b) Operating income, plus depreciation and amortization.

Fiscal Third-Quarter 2008

Highlights

Highlights

• Operating income, excluding prior-year key items(a),

increased 19 percent over June 2007 quarter

increased 19 percent over June 2007 quarter

• Difficult demand and raw materials cost environment

• Operating income, as reported, compared

with June 2007 quarter:

with June 2007 quarter:

– Ashland Performance Materials down 44 percent

– Valvoline down 6 percent

– Ashland Water Technologies more than doubled

– Ashland Distribution up 70 percent

• EBITDA(b) increased by 3 percent to $121 million

• Continued reductions in operating-segment trade

working capital as a percent of sales

working capital as a percent of sales

(a) Excludes changes resulting from operations acquired or sold.

(b) Operating income, plus depreciation and amortization.

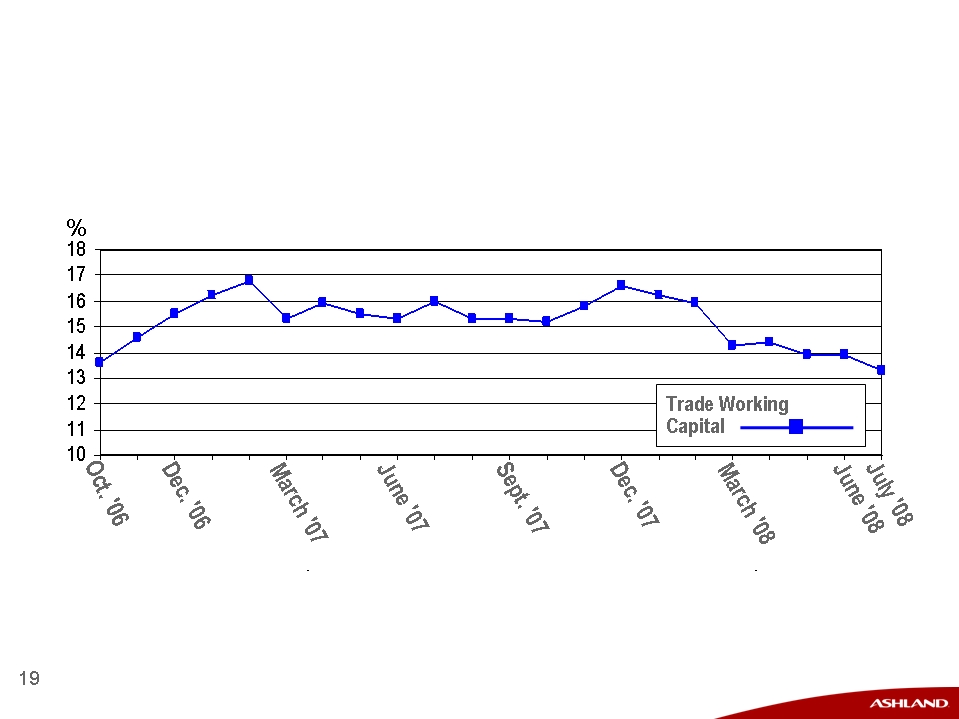

Fiscal Third-Quarter 2008

Operating Cash Flows

Operating Cash Flows

Operating-Segment

Trade Working Capital

Trade Working Capital

Operating Segments - Accounts Receivable, Inventories Excluding LIFO Reserve,

and Trade and Other Payables, Net, as a % of Trailing Three Months' Sales, Annualized*

* Excludes acquisitions made in June 2008 quarter.

(in millions, except change)

* When adjusted for key items in 2007 as noted in Appendix to this presentation, operating income

percentage for the June 2007 quarter was 3.7 percent.

percentage for the June 2007 quarter was 3.7 percent.

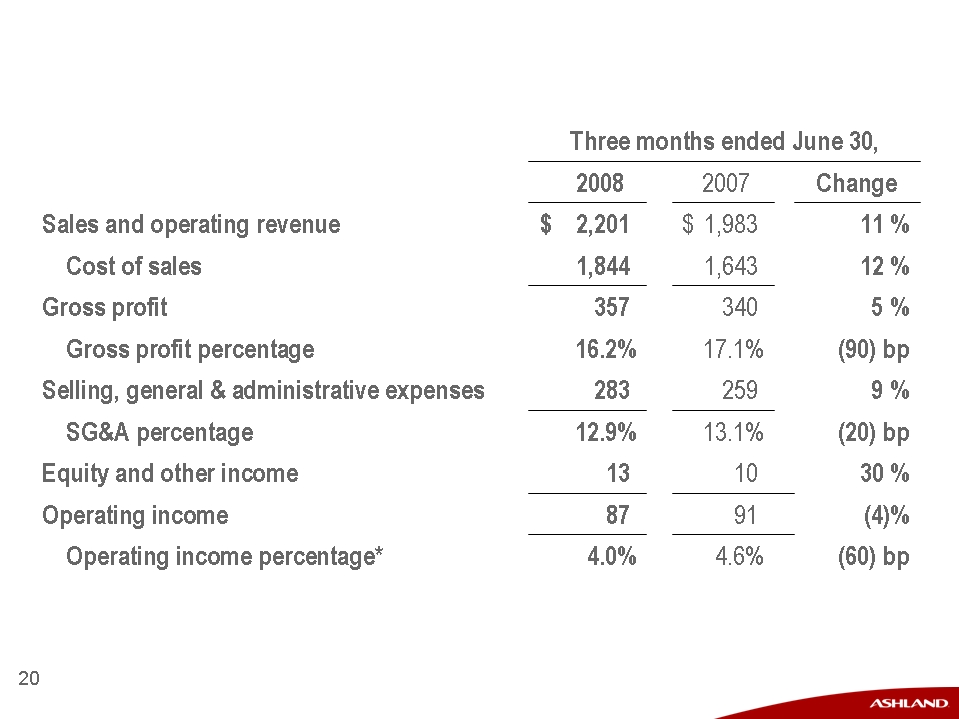

Fiscal Third-Quarter 2008

Financial Results

Financial Results

Fiscal Third-Quarter 2008

Diluted Earnings Per Share

Diluted Earnings Per Share

Fiscal Third-Quarter 2008

Progress on Cost Structure Efficiency

Progress on Cost Structure Efficiency

Appendix

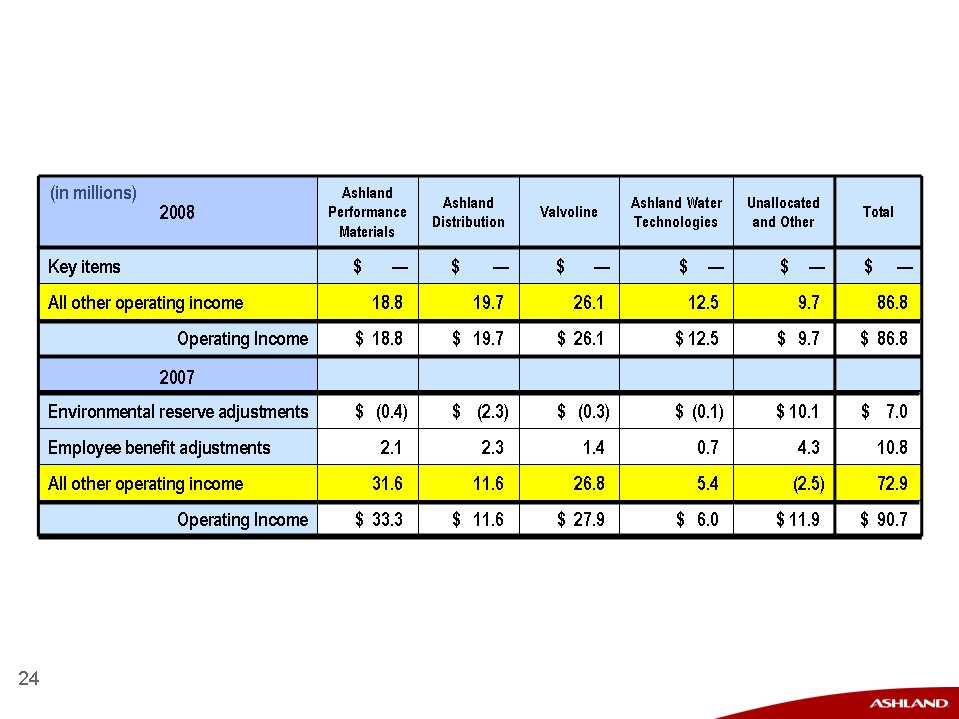

Fiscal Third Quarter

Key Items Affecting Operating

Income Comparisons

Key Items Affecting Operating

Income Comparisons

Regulation G: Reconciliation of

Operating Income to Adjusted EBITDA

Operating Income to Adjusted EBITDA

The information provided in this presentation

regarding adjusted earnings per share and earnings

before interest, taxes, depreciation, and amortization

(EBITDA) does not conform to generally accepted

accounting principles (GAAP) and should not be

construed as an alternative to the reported results

determined in accordance with GAAP. Management

has included this non-GAAP information to assist in

understanding the operating performance of the

Company and its operating segments. The non-GAAP

information provided may not be consistent with the

methodologies used by other companies. All non-

GAAP information is reconciled with reported GAAP

results in the financials that follow in this Appendix.

regarding adjusted earnings per share and earnings

before interest, taxes, depreciation, and amortization

(EBITDA) does not conform to generally accepted

accounting principles (GAAP) and should not be

construed as an alternative to the reported results

determined in accordance with GAAP. Management

has included this non-GAAP information to assist in

understanding the operating performance of the

Company and its operating segments. The non-GAAP

information provided may not be consistent with the

methodologies used by other companies. All non-

GAAP information is reconciled with reported GAAP

results in the financials that follow in this Appendix.

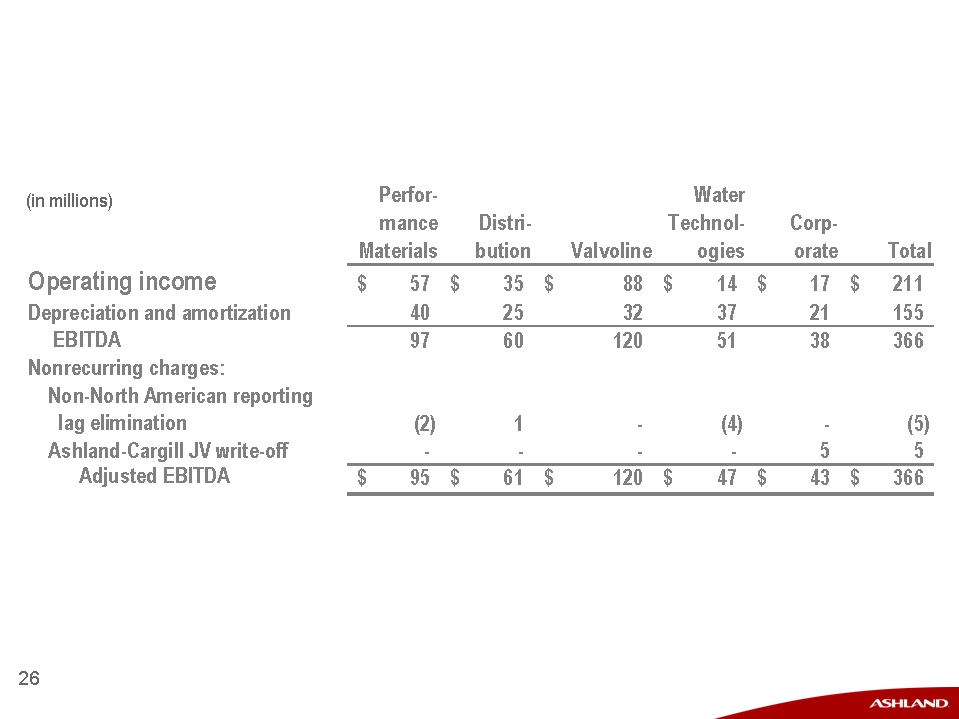

Ashland Inc.

Regulation G: Reconciliation of

Operating Income to Adjusted EBITDA

Regulation G: Reconciliation of

Operating Income to Adjusted EBITDA

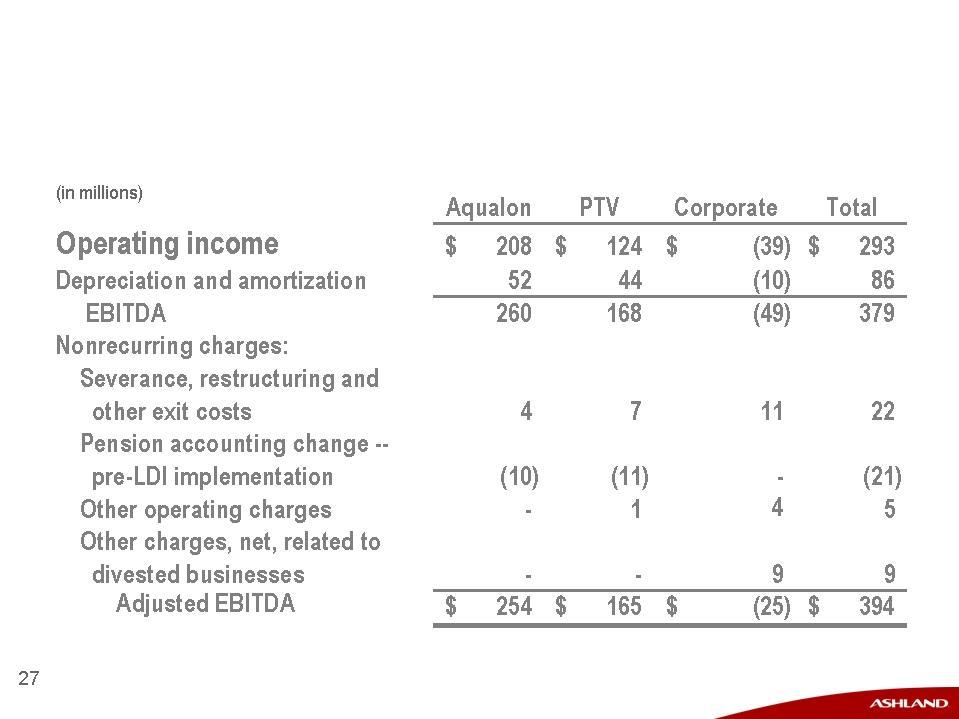

Hercules Inc.

Regulation G: Reconciliation of

Operating Income to Adjusted EBITDA

Regulation G: Reconciliation of

Operating Income to Adjusted EBITDA