Filed by Ashland Inc.

Pursuant to Rule 425

Under the Securities Act of 1933

Subject Company

Hercules Incorporated

Commission File Number 333-152911

Fourth-Quarter Fiscal 2008 Earnings

October 28, 2008

October 28, 2008

Fourth-Quarter Fiscal 2008 Earnings

October 28, 2008

October 28, 2008

James J. O'Brien

Chairman and Chief Executive Officer

Chairman and Chief Executive Officer

James J. O'Brien

Chairman and Chief Executive Officer

Chairman and Chief Executive Officer

Lamar M. Chambers

Sr. Vice President and Chief Financial Officer

Sr. Vice President and Chief Financial Officer

Lamar M. Chambers

Sr. Vice President and Chief Financial Officer

Sr. Vice President and Chief Financial Officer

Eric N. Boni

Director, Investor Relations

Director, Investor Relations

Eric N. Boni

Director, Investor Relations

Director, Investor Relations

2

Forward-Looking Statements

This presentation contains forward-looking statements, within the meaning of Section 27A of the

Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. These statements

include those made with respect to Ashland’s operating performance and Ashland’s acquisition of

Hercules Inc. These expectations are based upon a number of assumptions, including those mentioned

within this presentation. Performance estimates are also based upon internal forecasts and analyses of

current and future market conditions and trends, management plans and strategies, weather, operating

efficiencies and economic conditions, such as prices, supply and demand, cost of raw materials, and

legal proceedings and claims (including environmental and asbestos matters). These risks and

uncertainties may cause actual operating results to differ materially from those stated, projected or

implied. Such risks and uncertainties with respect to Ashland’s acquisition of Hercules include the

possibility that the benefits anticipated from the Hercules transaction will not be fully realized; the

possibility the transaction may not close, including as a result of failure to obtain the approval of

Hercules stockholders; the possibility that financing may not be available on the terms committed; and

other risks that are described in filings made by Ashland with the Securities and Exchange Commission

(SEC) in connection with the proposed transaction. Although Ashland believes its expectations are

based on reasonable assumptions, it cannot assure the expectations reflected herein will be achieved.

This forward-looking information may prove to be inaccurate and actual results may differ significantly

from those anticipated if one or more of the underlying assumptions or expectations proves to be

inaccurate or is unrealized or if other unexpected conditions or events occur. Other factors,

uncertainties and risks affecting Ashland are contained in Ashland's periodic filings made with the SEC,

including its Form 10-K for the fiscal year ended Sept. 30, 2007, and Forms 10-Q for the quarters ended

Dec. 31, 2007, and March 31 and June 30, 2008, which are available on Ashland’s Investor Relations

Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. These statements

include those made with respect to Ashland’s operating performance and Ashland’s acquisition of

Hercules Inc. These expectations are based upon a number of assumptions, including those mentioned

within this presentation. Performance estimates are also based upon internal forecasts and analyses of

current and future market conditions and trends, management plans and strategies, weather, operating

efficiencies and economic conditions, such as prices, supply and demand, cost of raw materials, and

legal proceedings and claims (including environmental and asbestos matters). These risks and

uncertainties may cause actual operating results to differ materially from those stated, projected or

implied. Such risks and uncertainties with respect to Ashland’s acquisition of Hercules include the

possibility that the benefits anticipated from the Hercules transaction will not be fully realized; the

possibility the transaction may not close, including as a result of failure to obtain the approval of

Hercules stockholders; the possibility that financing may not be available on the terms committed; and

other risks that are described in filings made by Ashland with the Securities and Exchange Commission

(SEC) in connection with the proposed transaction. Although Ashland believes its expectations are

based on reasonable assumptions, it cannot assure the expectations reflected herein will be achieved.

This forward-looking information may prove to be inaccurate and actual results may differ significantly

from those anticipated if one or more of the underlying assumptions or expectations proves to be

inaccurate or is unrealized or if other unexpected conditions or events occur. Other factors,

uncertainties and risks affecting Ashland are contained in Ashland's periodic filings made with the SEC,

including its Form 10-K for the fiscal year ended Sept. 30, 2007, and Forms 10-Q for the quarters ended

Dec. 31, 2007, and March 31 and June 30, 2008, which are available on Ashland’s Investor Relations

website at www.ashland.com/investors or the SEC’s website at www.sec.gov. Ashland undertakes no

obligation to subsequently update or revise the forward-looking statements made in this presentation to

reflect events or circumstances after the date of this presentation.

3

Additional Information

In connection with the proposed transaction, Ashland filed a registration statement

on Form S-4 (File No. 333-152911) with the SEC containing a proxy

statement/prospectus. On Oct. 6, 2008, Ashland and Hercules mailed a definitive

proxy statement/prospectus to Hercules’ shareholders containing information about

the merger. Investors and security holders are urged to read the registration

statement on Form S-4 and the proxy statement/prospectus because they contain

important information about the proposed transaction. Investors and security holders

may obtain free copies of these documents and other documents filed with the SEC

by contacting Ashland Investor Relations at (859) 815-4454 or Hercules Investor

Relations at (302) 594-7151. Free copies may also be obtained from Ashland's

Investor Relations website at www.ashland.com/investors, Hercules' website at

www.herc.com or the SEC's website at www.sec.gov.

on Form S-4 (File No. 333-152911) with the SEC containing a proxy

statement/prospectus. On Oct. 6, 2008, Ashland and Hercules mailed a definitive

proxy statement/prospectus to Hercules’ shareholders containing information about

the merger. Investors and security holders are urged to read the registration

statement on Form S-4 and the proxy statement/prospectus because they contain

important information about the proposed transaction. Investors and security holders

may obtain free copies of these documents and other documents filed with the SEC

by contacting Ashland Investor Relations at (859) 815-4454 or Hercules Investor

Relations at (302) 594-7151. Free copies may also be obtained from Ashland's

Investor Relations website at www.ashland.com/investors, Hercules' website at

www.herc.com or the SEC's website at www.sec.gov.

4

Agenda

· Fiscal fourth-quarter preliminary results

and business outlook

and business outlook

· Ashland full-year highlights

· Hercules update

· Questions

Appendices

- Appendix A: Full-year fiscal 2008 preliminary results

- Appendix B: Business profiles

- Appendix C: Regulation G reconciliation

5

Fiscal Fourth Quarter 2008

Highlights

Highlights

· Continued volatile raw materials cost environment and

declining demand

declining demand

· Operating income versus September 2007

- Increased 6 percent to $27.8 million, as reported

- Declined 41 percent to $23.8 million, excluding key items1

§ Declines in Ashland Performance Materials, Ashland Water

Technologies and Valvoline

Technologies and Valvoline

§ Significant improvement of $10.6 million at Ashland Distribution

· EBITDA2 decreased 11 percent to $68 million

· Tax provision adjustments unfavorably impacted

EPS by approximately 30 cents per share

EPS by approximately 30 cents per share

· Continued reductions in operating-segment trade

working capital as a percent of sales to 12.3 percent

working capital as a percent of sales to 12.3 percent

1 When adjusted for key items in both periods as noted on Slide 7 of this presentation.

2 Operating income, plus depreciation and amortization.

6

Fiscal Fourth Quarter 2008

Preliminary Financial Results

Preliminary Financial Results

(in millions, except change) | Three months ended Sept. 30, | ||||||||

2008 | 2007 | Fav./(Unfav.) | |||||||

Sales and operating revenue | 2,216) | 2,085) | 6 % | ||||||

Cost of sales | 1,898) | 1,740) | (9)% | ||||||

Gross profit | 318) | 345) | (8)% | ||||||

Gross profit percentage | 14.4% | 16.5% | (210) bp | ||||||

Selling, general & administrative expenses | 310) | 338) | 8)% | ||||||

SG&A percentage | 14.0% | 16.2% | 220) bp | ||||||

Equity and other income | 20) | 19) | 5 % | ||||||

Operating income | 28) | 26) | 8)% | ||||||

Operating income percentage | 1.3% | 1.2% | 10) bp | ||||||

Earnings before interest, taxes, depreciation and amortization (EBITDA) | $ | 68) | $ | 76) | (11)% | ||||

EBITDA as a percent of sales | 3.1% | 3.6% | (50) bp | ||||||

$

$

7

Key Items Affecting Operating Income

Comparisons

Comparisons

(in millions) | Three months ended Sept. 30, | |

Ashland Inc. | 2008 | 2007 |

Self-insurance reserve adjustment | $ 11.3) | $ 8.0) |

Severance costs | (7.3) | —) |

Non-North American entities reporting lag elimination | —) | 5.2) |

Litigation reserve adjustment | —) | (5.5) |

Asset impairment - PathGuard® equipment | —) | (10.6) |

Postretirement benefit obligation adjustment | —) | (11.3) |

All other income | 23.8) | 40.4) |

Total operating income | $ 27.8) | $ 26.2) |

8

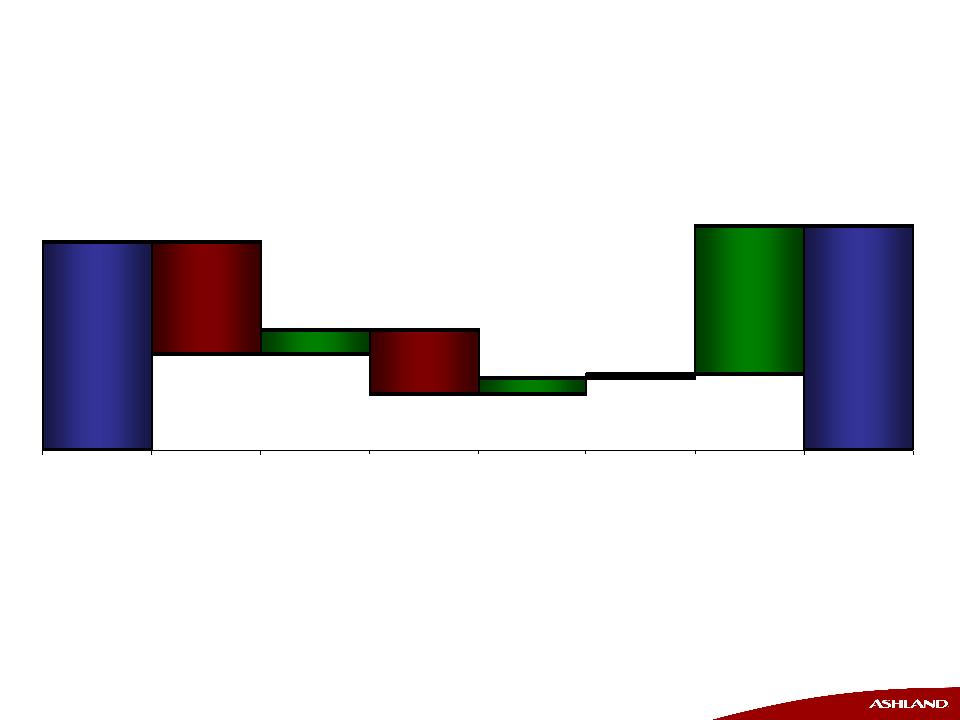

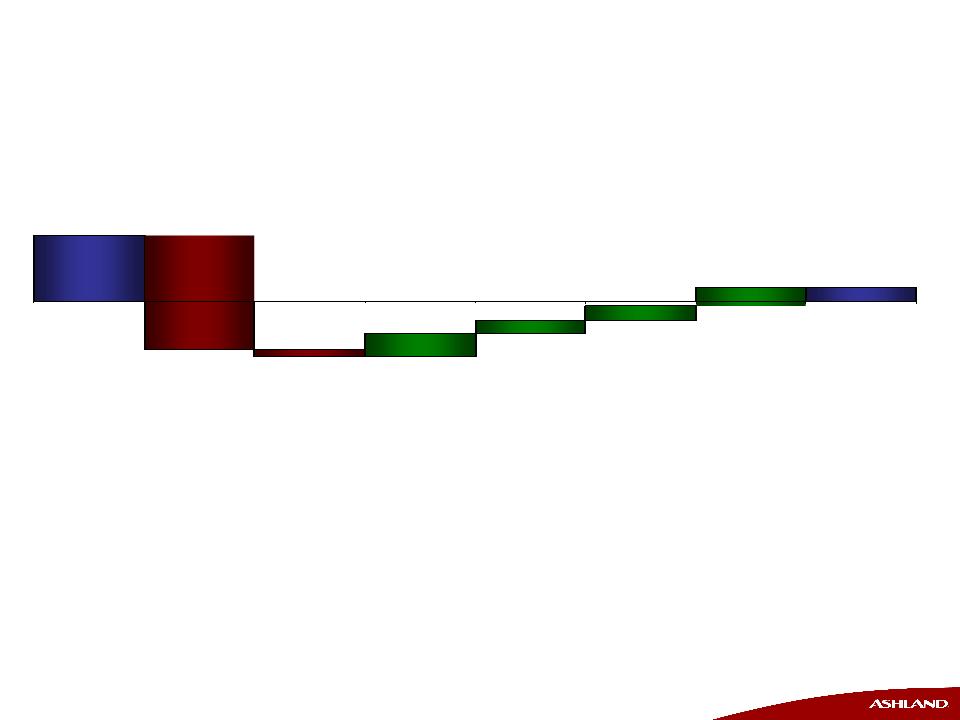

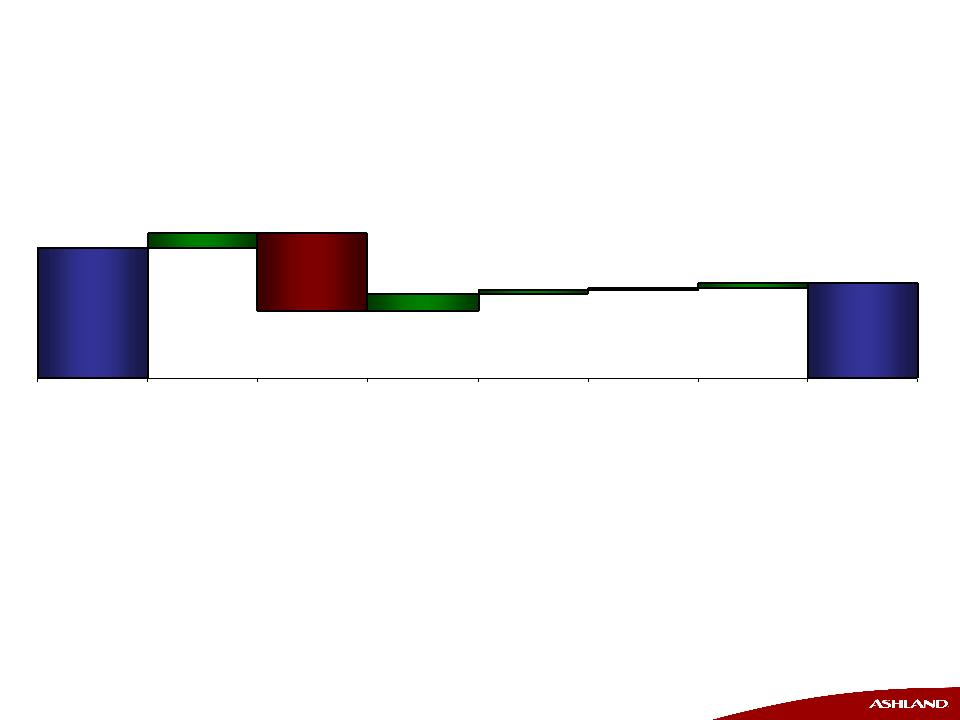

Q4 FY 2007 vs. Q4 FY 2008

Factors Impacting Operating Income

Factors Impacting Operating Income

($ millions)

(8.2)

(14.0)

Q4 2007

Volume/

Mix

Mix

Q4 2008

Currency

Translation

Translation

Margin

3.0

26.2

27.8

SG&A

Expenses

Expenses

2.2

0.4

Other

18.2

Key

Items

Items

9

Fiscal Fourth Quarter 2008

Preliminary Diluted Earnings Per Share

Preliminary Diluted Earnings Per Share

(in millions) | Three months ended Sept. 30, | |

2008 | 2007 | |

Operating income | $ 28) | $ 26) |

Loss on MAP Transaction | (3) | -) |

Net interest and other financing income | 2) | 12) |

Income from continuing operations before income taxes | 27) | 38) |

Income tax expense | (28) | (6) |

Income (loss) from continuing operations | (1) | 32) |

Loss from discontinued operations, net of income taxes | (9) | -) |

Net income (loss) | (10) | 32) |

Diluted EPS from continuing operations | (.01) | .51) |

Diluted EPS on net income | (.15) | .51) |

Q4 effective tax rate | 102.4% | 16.2% |

Full-year effective tax rate | 32.9% | 22.3% |

10

Fiscal Fourth Quarter 2008

Components of Preliminary EPS

Components of Preliminary EPS

Three months ended Sept. 30, | ||

Ashland Inc. | 2008 | 2007 |

Self-insurance reserve adjustment | $ .11) | $ .08) |

Severance costs | (.07) | —) |

Tax provision adjustment1 | (.30) | .04) |

Non-North American entities reporting-lag elimination | —) | .05) |

Litigation reserve adjustment | —) | (.05) |

Asset impairments | —) | (.10) |

Postretirement benefit obligation adjustment | —) | (.11) |

All other diluted EPS from continuing operations | .25) | .60) |

Diluted EPS from continuing operations | $ (.01) | $ .51) |

1Difference between quarterly and full-year effective tax rates.

11

Fiscal Fourth Quarter 2008

Operating Cash Flows

Operating Cash Flows

(in millions) | Three months ended Sept. 30, | |

2008 | 2007 | |

Net income (loss) | $ (10) | $ 32) |

Loss from discontinued operations | 9) | -) |

Adjustments for cash flows from operations: | ||

Depreciation and amortization | 40) | 50) |

Deferred income taxes | 24) | 7) |

Change in operating assets and liabilities1 | 68) | 81) |

Other | 13) | 11) |

Cash flows from operating activities from cont. operations | 144) | 181) |

Additions to property, plant and equipment | (87) | (52) |

$ 57) | $ 129) | |

1Excludes changes resulting from operations acquired or sold.

12

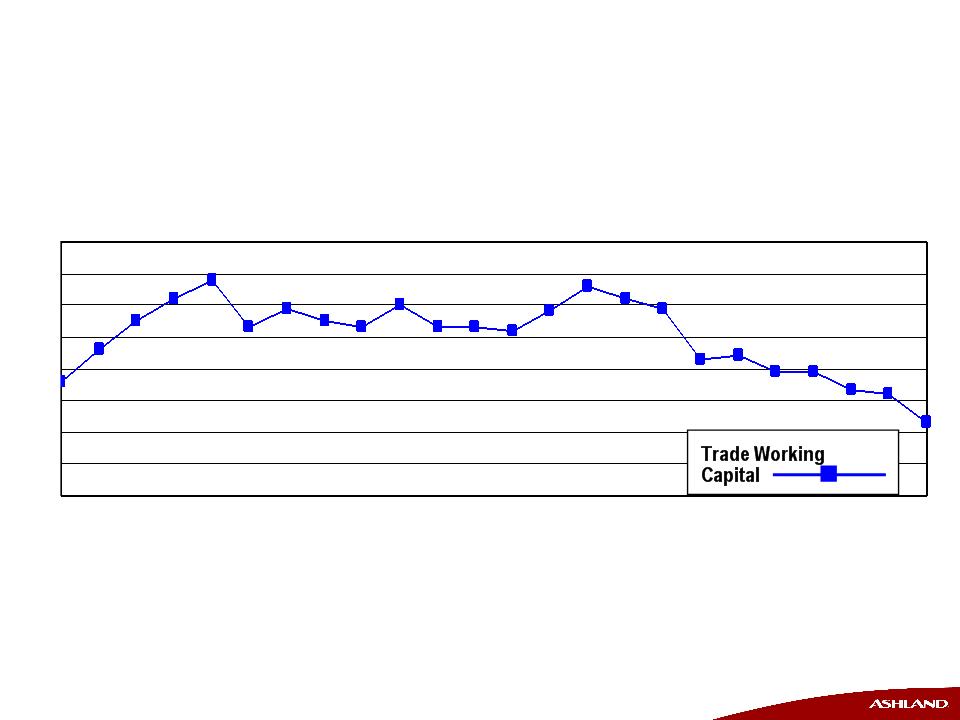

Operating Segments - Accounts Receivable, Inventories Excluding LIFO Reserve,

and Trade and Other Payables, Net, as a % of Trailing Three Months' Sales, Annualized*

* Excludes acquisitions made in June 2008 quarter.

Oct '06

Dec '06

Mar '07

Jun '07

Sep '07

Dec '07

Mar '08

Jun '08

Operating Segment

Trade Working Capital

Trade Working Capital

Sep '08

· Reduced trade working capital by 430 basis points

during last nine months of fiscal 2008

during last nine months of fiscal 2008

18

17

17

16

15

14

13

12

11

10

%

13

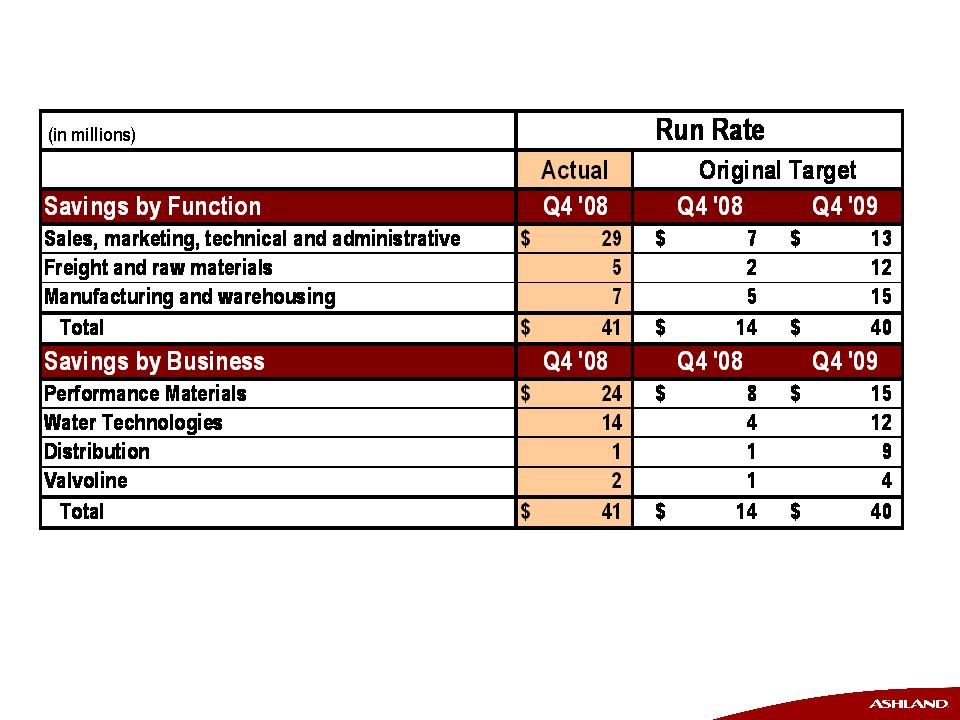

Progress on cost-structure efficiency

14

Fiscal Fourth Quarter 2008

Performance Summary

Performance Summary

· Operating income down 41 percent, excluding key items

· Generated $144 million of cash flows from operating

activities from continuing operations

activities from continuing operations

· Made substantial progress in reducing working capital

· Exceeding forecast for cost-structure efficiencies

15

Key Items Affecting Operating Income

Comparisons

Comparisons

(in millions) | Fiscal fourth quarter ended Sept. 30, | |

Ashland Performance Materials | 2008 | 2007 |

Severance costs | $ (4.7) | $ —) |

Non-North American entities reporting-lag elimination | —) | 2.1) |

Litigation reserve adjustment | —) | (5.5) |

Postretirement benefit obligation adjustment | —) | (3.3) |

All other income | 6.3) | 13.9) |

Total operating income | $ 1.6) | $ 7.2) |

16

Performance Materials

Fiscal Fourth Quarter Summary

Fiscal Fourth Quarter Summary

(in millions, except percentages) Preliminary | Three months ended Sept. 30, | ||

2008 | 2007 | Favor./ (Unfav.) | |

Pounds/day1 | 5.2) | 4.8) | 8)% |

Operating revenue2 | $ 427) | $ 438) | (3)% |

Gross profit as a % of sales1 | 14.6% | 18.4% | (380) bp |

Selling, general & admin. costs | $ 65) | $ 75) | 13)% |

Operating income | $ 1.6) | $ 7.2) | (78)% |

Operating income as a % of sales | 0.4% | 1.6% | (120) bp |

EBITDA | $ 15) | $ 18) | (17)% |

EBITDA as a % of sales | 3.5% | 4.1% | (60) bp |

1 Excludes effect of non-North American financial-reporting-lag elimination in 2007.

2 Includes $56 million of revenue from non-North American financial-reporting-lag elimination in 2007.

17

($ millions)

2.6

(12.4)

Q4 2007

Volume/

Mix

Mix

Q4 2008

Currency

Translation

Translation

Margin

(0.8)

7.2

1.6

SG&A

Expenses

Expenses

1.4

Other

2.0

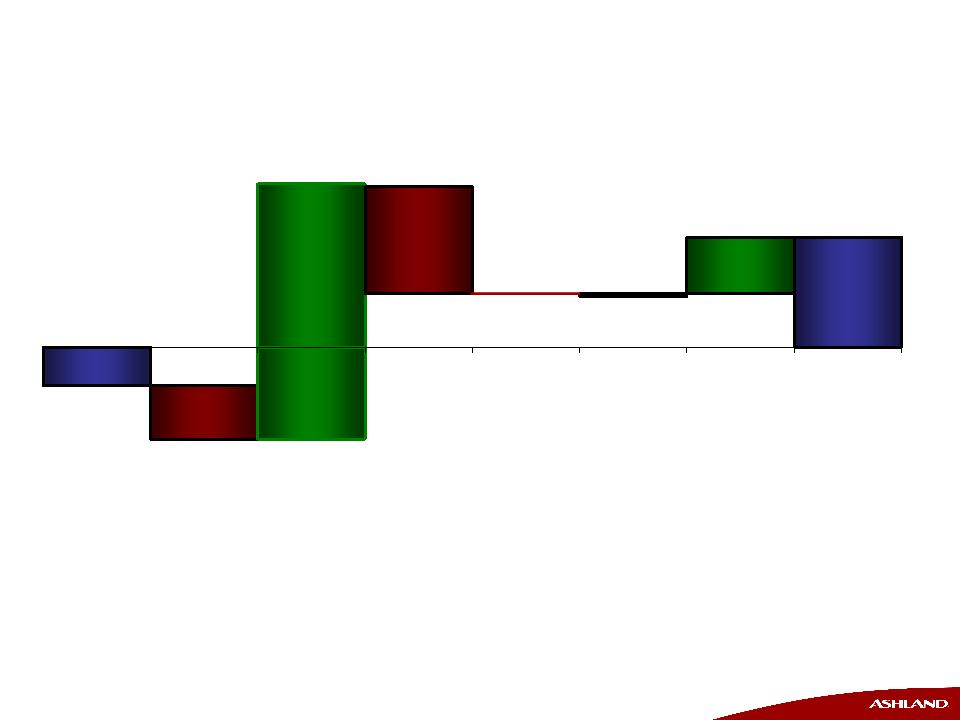

Q4 FY 2007 versus Q4 FY 2008

Performance Materials

Factors Impacting Operating Income

Factors Impacting Operating Income

· Continued significant weakness in North American

residential construction and transportation markets

residential construction and transportation markets

1.6

Key Items

18

Performance Materials

Outlook

Outlook

· Getting our costs right

- Should achieve approximately $8 million

in quarterly savings in Q1 '09 vs. Q1 '08

in quarterly savings in Q1 '09 vs. Q1 '08

· Mothballing certain North American manufacturing

capacity and reducing hours of operation in Europe

capacity and reducing hours of operation in Europe

· Strong potential for raw material cost reductions,

although little received to date

although little received to date

19

Key Items Affecting Operating Income

Comparisons

Comparisons

(in millions) | Fiscal fourth quarter ended Sept. 30, | |

Ashland Distribution | 2008 | 2007 |

Non-North American entities reporting-lag elimination | $ —) | $ (0.9) |

Postretirement benefit obligation adjustment | —) | (5.6) |

All other income | 12.6) | 2.0) |

Total operating income | $ 12.6) | $ (4.5) |

20

Distribution

Fiscal Fourth Quarter Summary

Fiscal Fourth Quarter Summary

(in millions, except percentages) Preliminary | Three months ended Sept. 30, | ||

2008 | 2007 | Favor./ (Unfav.) | |

Pounds/day1 | 18.2) | 19.6) | (7)% |

Operating revenue2 | $ 1,151) | $ 1,050) | 10 % |

Gross profit as a % of sales1 | 8.1% | 7.0% | 110 bp |

Selling, general & admin. costs | $ 82) | $ 79) | (4)% |

Operating income (loss) | $ 12.6) | $ (4.5) | N.D. |

Operating income (loss) as a % of sales | 1.1% | (0.4)% | 150)bp |

EBITDA | $ 19) | $ 3) | 533)% |

EBITDA as a % of sales | 1.7% | 0.3% | 130)bp |

1 Excludes effect of non-North American financial-reporting-lag elimination in 2007.

2 Includes $46 million of revenue from non-North American financial-reporting-lag elimination in 2007.

21

· Volume declined 7 percent, including 12-percent reduction in Europe

· Unit gross profit increased 17 percent due to continued focus on pricing

process improvement

process improvement

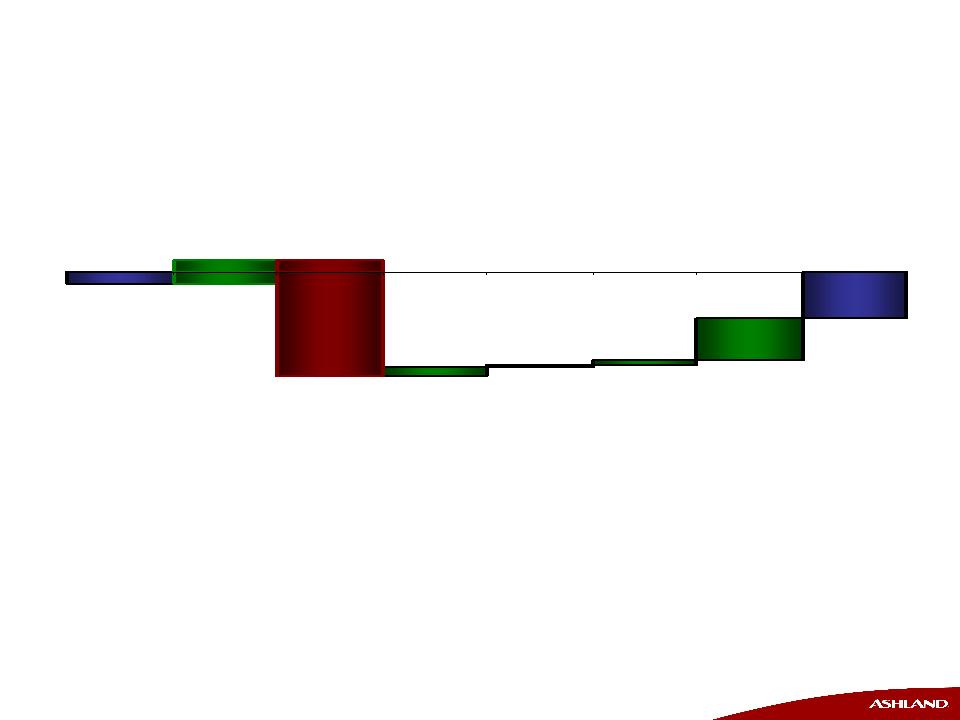

($ millions)

29.2

Q4 2007

Currency

Translation

Translation

Margin

Q4 2008

Volume/

Mix

Mix

SG&A

Expenses

Expenses

(6.2)

(4.5)

6.5

Other

(0.1)

(12.0)

12.6

Q4 FY 2007 versus Q4 FY 2008

Distribution

Factors Impacting Operating Income

Factors Impacting Operating Income

Key

Items

Items

(0.3)

22

Distribution

Selling Price, Cost and Gross Profit Trends

Selling Price, Cost and Gross Profit Trends

Gross

Profit

Profit

Price

& Cost

(cents/lb.)

23

Distribution

Outlook

Outlook

· Difficult market conditions likely to continue

- Severe product cost volatility, with select commodities

starting to decline

starting to decline

- Building and construction, automotive, and marine

markets remain challenging

markets remain challenging

· Demand will continue to soften

in our primary markets

in our primary markets

- Volume will be driven by overall U.S. industrial production

- European demand also starting to fall

- Credit crisis impacting small manufacturers

· Margins will be pressured by extreme cost volatility

and softening demand

and softening demand

- Improved pricing practices have enabled margin

expansion over last three quarters

expansion over last three quarters

24

Key Items Affecting Operating Income

Comparisons

Comparisons

(in millions) | Fiscal fourth quarter ended Sept. 30, | |

Valvoline | 2008 | 2007 |

Postretirement benefit obligation adjustment | $ —) | $ (0.9) |

All other income | 13.1) | 18.8) |

Total operating income | $ 13.1) | $ 17.9) |

25

Valvoline

Fiscal Fourth Quarter Summary

Fiscal Fourth Quarter Summary

(in millions, except percentages) Preliminary | Three months ended Sept. 30, | ||

2008 | 2007 | Favor./ (Unfav.) | |

Lubricant gallons1 | 43.5) | 43.3) | -)% |

Operating revenue1 | $ 454) | $ 384) | 18 % |

Gross profit as a % of sales1 | 19.2% | 24.6% | (540) bp |

Selling, general & admin. costs | $ 77) | $ 79) | 3)% |

Operating income | $ 13.1) | $ 17.9) | (27)% |

Operating income as a % of sales | 2.9% | 4.7% | (180) bp |

EBITDA | $ 21)) | $ 26) | (19)% |

EBITDA as a % of sales | 4.6% | 6.8% | (220) bp |

1 Non-North American financial-reporting-lag elimination had no significant impact in fourth-quarter 2007.

26

Valvoline

Operating Income Performance Factors

Operating Income Performance Factors

($ millions)

· Margin decrease driven by higher raw materials costs

· SG&A improvement due primarily to lower advertising

expenses

expenses

Q4 2007

Volume/

Mix

Mix

Q4 2008

Currency

Translation

Translation

Margin

SG&A

Expenses

Expenses

Q4 FY 2007 versus Q4 FY 2008

17.9

1.8

(10.6)

0.4

0.3

13.1

0.9

Other

2.4

Key Items

27

Valvoline

Outlook

Outlook

· Price increases through September should

enable gross profit to improve on a per-unit basis

to levels approximating Q1 - Q3 2008

enable gross profit to improve on a per-unit basis

to levels approximating Q1 - Q3 2008

· Base oil market expected to remain tight

into the second quarter with potential cost relief

later in 2009

into the second quarter with potential cost relief

later in 2009

· Soft market demand experienced in 2008 is likely

to persist in 2009 despite lower gasoline prices

to persist in 2009 despite lower gasoline prices

28

Key Items Affecting Operating Income

Comparisons

Comparisons

(in millions) | Fiscal fourth quarter ended Sept. 30, | |

Ashland Water Technologies | 2008 | 2007 |

Severance costs | $ (2.6) | $ —) |

Non-North American entities reporting-lag elimination | —) | 4.0) |

Asset impairments | —) | (10.6) |

Postretirement benefit obligation adjustment | —) | (1.5) |

All other income (loss) | (3.3) | 6.6) |

Total operating loss | $ (5.9) | $ (1.5) |

29

Water Technologies

Fiscal Fourth Quarter Summary

Fiscal Fourth Quarter Summary

(in millions, except percentages) Preliminary | Three months ended Sept. 30, | ||

2008 | 2007 | Favor./ (Unfav.) | |

Operating revenue1 | $ 226) | $ 249) | (9) % |

Gross profit as a % of sales2 | 32.9% | 39.7% | (680) bp |

Selling, general & admin. costs | $ 81) | $ 100) | 19)% |

Operating loss | $ (5.9) | $ (1.5) | N.D. |

Operating loss as a % of sales | (2.6)% | (0.6)% | (200) bp |

EBITDA | $ 1) | $ 17) | (94)% |

EBITDA as a % of sales | 0.4% | 6.8% | (640) bp |

1 Includes $42 million of revenue from non-North American financial-reporting-lag elimination in 2007.

2 Excludes effect of non-North American financial-reporting-lag elimination in 2007.

30

($ millions)

Q4 2007

Sales/Mix

Q4 2008

Currency

Translation

Translation

Margin

SG&A

Expenses

Expenses

Other

Q4 FY 2007 versus Q4 FY 2008

· Experiencing significant margin erosion

due to raw material increases

due to raw material increases

· Beginning to realize benefits of cost structure changes and

discipline in SG&A reductions

discipline in SG&A reductions

Water Technologies

Factors Impacting Operating Income

Factors Impacting Operating Income

(1.5)

2.8

(14.8)

1.2

0.4

0.5

5.5

(5.9)

Key Items

31

Water Technologies

Outlook

Outlook

· Getting our costs right

- Reduced sales, marketing, technical, administrative and

plant headcount

plant headcount

· Opportunity to renegotiate contract pricing in Q1 '09

- High percentage of contracts up for renewal

· Integration into Hercules Paper Technologies

- Reporting in Q1 will be on a combined basis

32

Fiscal 2008 Summary

(in millions, except percentages) Preliminary | 12 months ended Sept. 30, | ||

2008 | 2007 | Favor./ (Unfav.) | |

Operating revenue | $ 8,381) | $ 7,785) | 8 % |

Gross profit as a % of sales | 15.8% | 17.2% | (140) bp |

Operating income | $ 213) | $ 216) | (1)% |

Operating income as a % of sales | 2.5% | 2.8% | (30) bp |

EBITDA | $ 358) | $ 349) | 3)% |

EBITDA as a % of sales | 4.3% | 4.5% | (20) bp |

Return on investment | 6.1% | 8.0% | (190) bp |

33

Ashland Inc.

Fiscal 2008 EBITDA Summary

Fiscal 2008 EBITDA Summary

· EBITDA increased 3 percent over FY2007

- Performance Materials down 25 percent

- Distribution up 19 percent

- Valvoline just 2 percent below 2007 record

§ Record annual operating income for Valvoline Instant Oil

Change and Valvoline International

Change and Valvoline International

- Water Technologies down 16 percent

34

Ashland Inc.

Fiscal 2008 Highlights

Fiscal 2008 Highlights

· Initiated cost-structure efficiency program

· Generated cash flows from operating activities

from continuing operations in fiscal 2008 of $478

million versus $189 million in fiscal 2007

from continuing operations in fiscal 2008 of $478

million versus $189 million in fiscal 2007

· Operating-segment trade working capital

decrease of 300 basis points to 12.3 percent

of sales

decrease of 300 basis points to 12.3 percent

of sales

· Hercules Inc. transaction announced

35

Hercules Update

· All regulatory approvals received

- Hercules shareholder vote Nov. 5

- Anticipated close Nov. 13

· Continue to work with banks on structure and terms

of the committed financing

of the committed financing

· Synergies expected at high end of original estimates

- $120 million annually

- $80 million run-rate by 1-year anniversary

- Integration expenses still being determined

· Creates a major, global specialty chemicals company

with ~75 percent of EBITDA derived

from specialty chemicals

with ~75 percent of EBITDA derived

from specialty chemicals

– Reduces earnings volatility, improves profitability and

strengthens cash flow generation

strengthens cash flow generation

Appendix A

Fiscal 2008 Preliminary Results

Fiscal 2008 Preliminary Results

Appendix A

Fiscal 2008 Preliminary Results

Fiscal 2008 Preliminary Results

37

Fiscal 2008

Preliminary Financial Results

Preliminary Financial Results

(in millions, except change) | Three months ended Sept. 30, | ||||||||

2008 | 2007 | Fav./(Unfav.) | |||||||

Sales and operating revenue | 8,381) | 7,785) | 8 % | ||||||

Cost of sales | 7,056) | 6,447) | (9)% | ||||||

Gross profit | 1,325) | 1,338) | (1)% | ||||||

Gross profit percentage | 15.8% | 17.2% | (140) bp | ||||||

Selling, general & administrative expenses | 1,166) | 1,171) | -)% | ||||||

SG&A percentage | 13.9% | 15.0% | 110) bp | ||||||

Equity and other income | 54) | 49) | 10 % | ||||||

Operating income | 213) | 216) | (1)% | ||||||

Operating income percentage | 2.5% | 2.8% | (30) bp | ||||||

Earnings before interest, taxes, depreciation and amortization (EBITDA) | $ | 358) | $ | 349) | 3)% | ||||

EBITDA as a percent of sales | 4.3% | 4.5% | (20) bp | ||||||

$

$

38

Fiscal 2008

Preliminary Diluted Earnings Per Share

Preliminary Diluted Earnings Per Share

(in millions) | Twelve months ended Sept. 30, | |

2008 | 2007 | |

Operating income | $ 213) | $ 216) |

Gain (loss) on MAP Transaction | 20) | (3) |

Net interest and other financing income | 28) | 46) |

Income from continuing operations before income taxes | 261) | 259) |

Income tax expense | (86) | (58) |

Income from continuing operations | 175) | 201) |

Income (loss) from discontinued operations, net of income taxes | (8) | 29) |

Net income | 167) | 230) |

Diluted EPS from continuing operations | 2.76) | 3.15) |

Diluted EPS on net income | 2.63) | 3.60) |

Full-year effective tax rate | 32.9% | 22.3% |

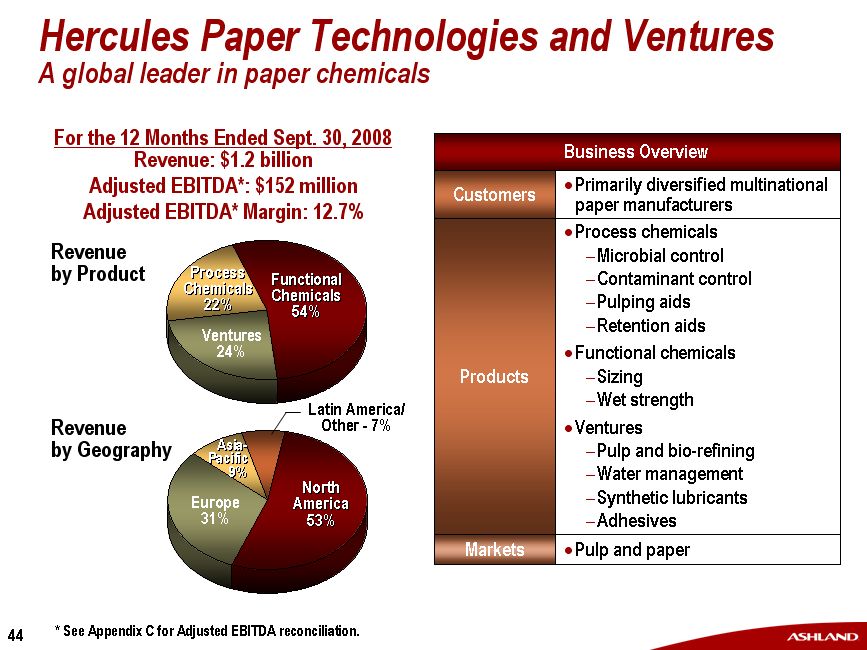

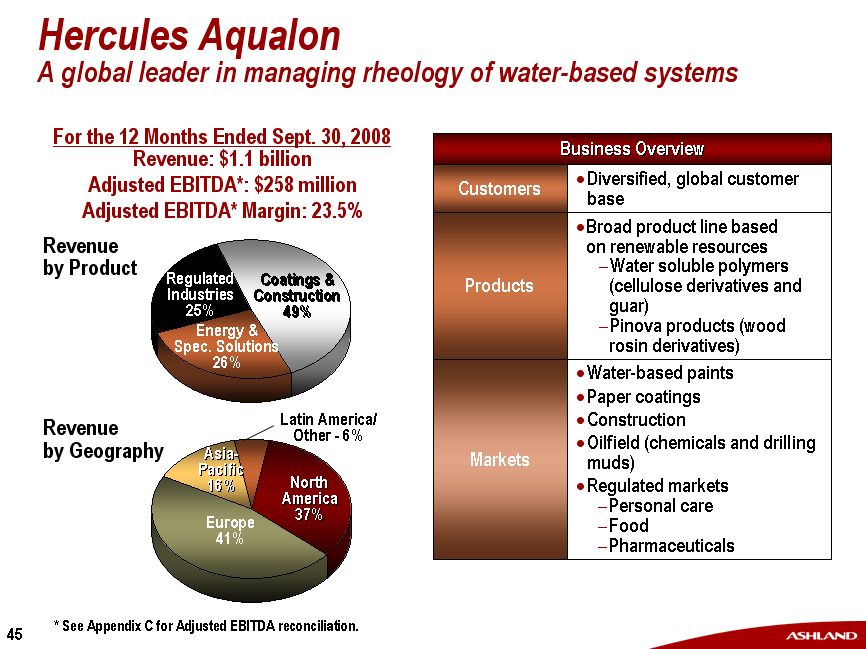

Appendix B

Business Profiles

Business Profiles

Appendix B

Business Profiles

Business Profiles

40

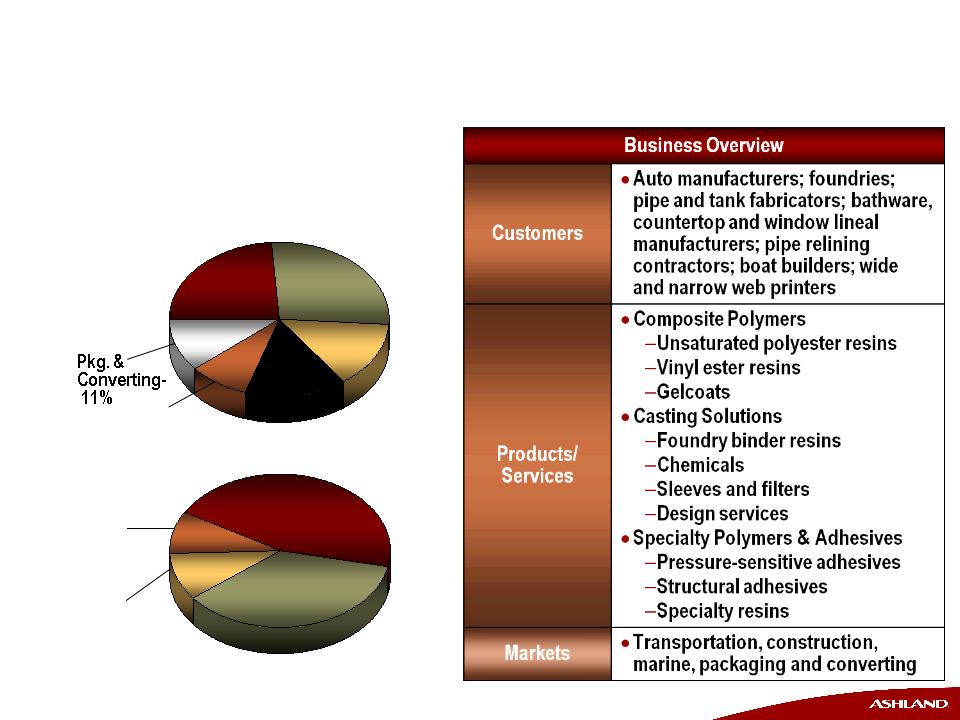

Ashland Performance Materials

A global leader in specialty chemicals

A global leader in specialty chemicals

North

America

America

North

America

America

45%

45%

Europe

36%

Latin

America/

Other - -

America/

Other - -

9%

Trans-

portation

portation

Trans-

portation

portation

24%

24%

Ind.

Constr.

Constr.

27%

Revenue

by Geography

by Geography

Revenue

by Market

by Market

For the Fiscal Year Ended Sept. 30, 2008

Revenue: $1.6 billion

EBITDA*: $94 million

EBITDA* Margin: 5.8%

Res.

Constr.

Constr.

14%

Infra-

structure

structure

15%

Marine - - 9%

Asia/

Pacific - - 10%

Pacific - - 10%

* See Appendix C for EBITDA reconciliation.

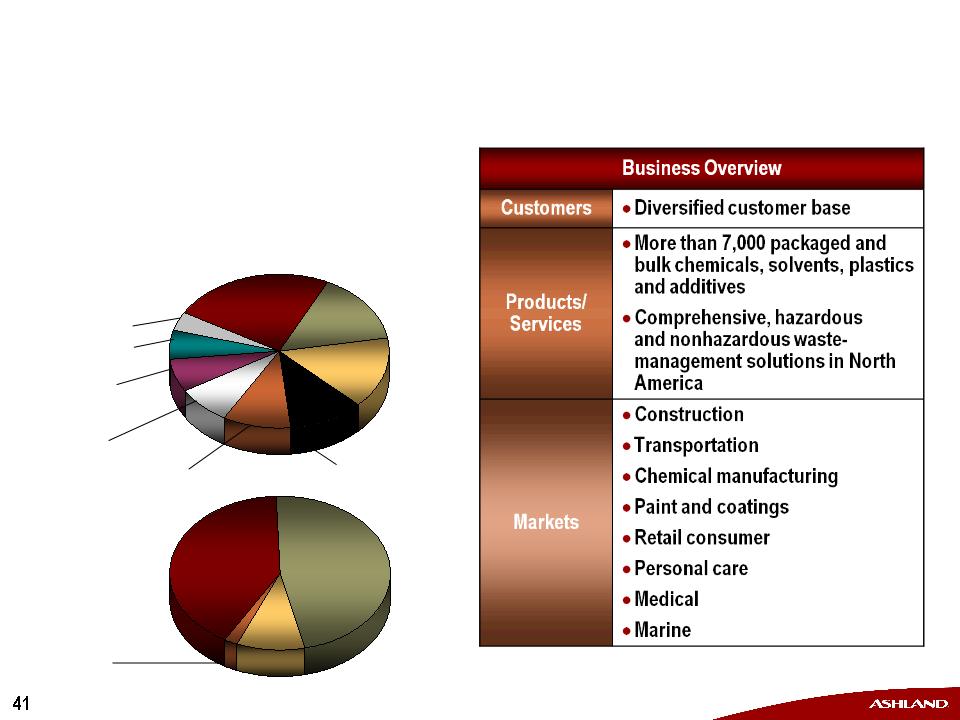

Ashland Distribution

A leading North American chemicals and plastics distributor

A leading North American chemicals and plastics distributor

Chemicals

Chemicals

47%

47%

Plastics

41%

Environmental

Service/Other - -

2%

Service/Other - -

2%

Construction

Construction

24%

24%

Other

15%

Revenue

by Product

Line

by Product

Line

Revenue

by Market

by Market

Trans-

portation

portation

15%

Paint & Coatings - 10%

Medical - - 6%

Marine - - 4%

Com-

posites

posites

10%

Chemical Mfg.

- 11%

- 11%

Retail

Consumer - - 8%

Consumer - - 8%

Personal

Care - - 7%

Care - - 7%

For the Fiscal Year Ended Sept. 30, 2008

Revenue: $4.4 billion

EBITDA*: $75 million

EBITDA* Margin: 1.7%

* See Appendix C for EBITDA reconciliation.

42

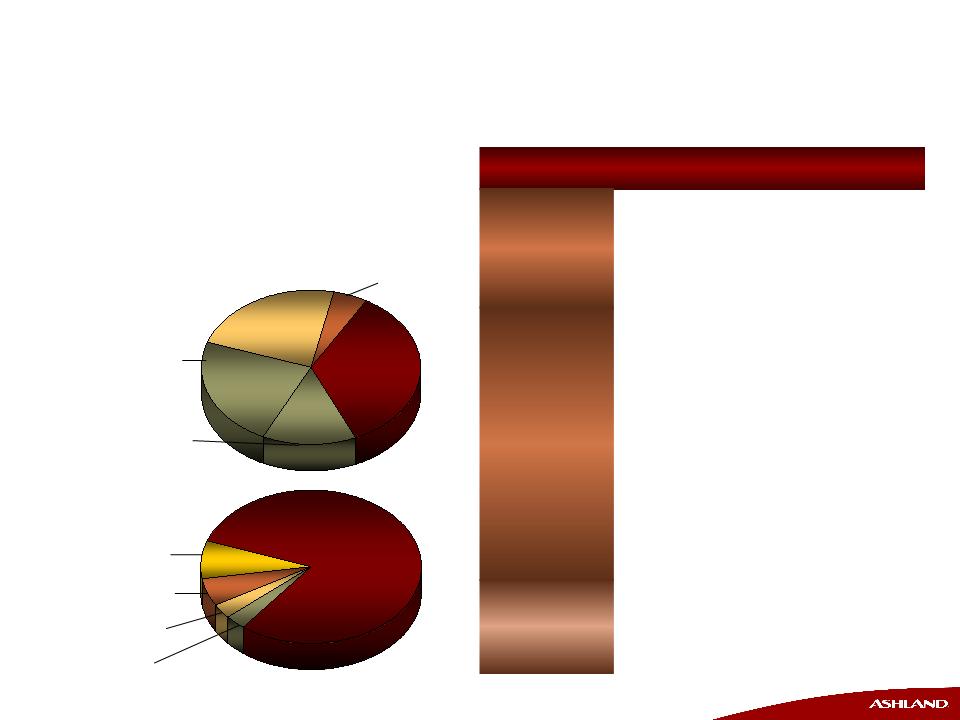

Valvoline: A leading worldwide marketer of premium-branded

automotive lubricants and chemicals

automotive lubricants and chemicals

Lubricants

80%

Filters - - 3%

Valvoline

Int'l - - 23%

Int'l - - 23%

Valvoline

Int'l - - 23%

Int'l - - 23%

Do-It-

Yourself

Yourself

35%

Business Overview | |

Customers | · Retail auto parts stores and mass merchandisers who sell to consumers; installers, such as car dealers and quick lubes; distributors |

Products/ Services | · Valvoline® lubricants and automotive chemicals · MaxLife® lubricants for high-mileage vehicles · SynPower® synthetic motor oil · Eagle One® and Car Brite® appearance products · Zerex® antifreeze · Valvoline Instant Oil Change�� service |

Market Channels | · Do-It-Yourself (DIY) · Do-It-For-Me (DIFM) · Valvoline International |

Revenue

by Product Line

by Product Line

Revenue

by Market Channel

by Market Channel

Do-It-

For-Me

37%

For-Me

37%

DIFM:

Installer channel

23%

Installer channel

23%

Specialty/

Other - - 5%

Other - - 5%

DIFM:

Valvoline Instant

Oil Change - 14%

Valvoline Instant

Oil Change - 14%

Chemicals - - 6%

Appearance

products - - 3%

products - - 3%

Antifreeze - - 8%

For the Fiscal Year Ended Sept. 30, 2008

Revenue: $1.7 billion

EBITDA*: $115 million

EBITDA* Margin: 6.9%

* See Appendix C for EBITDA reconciliation.

43

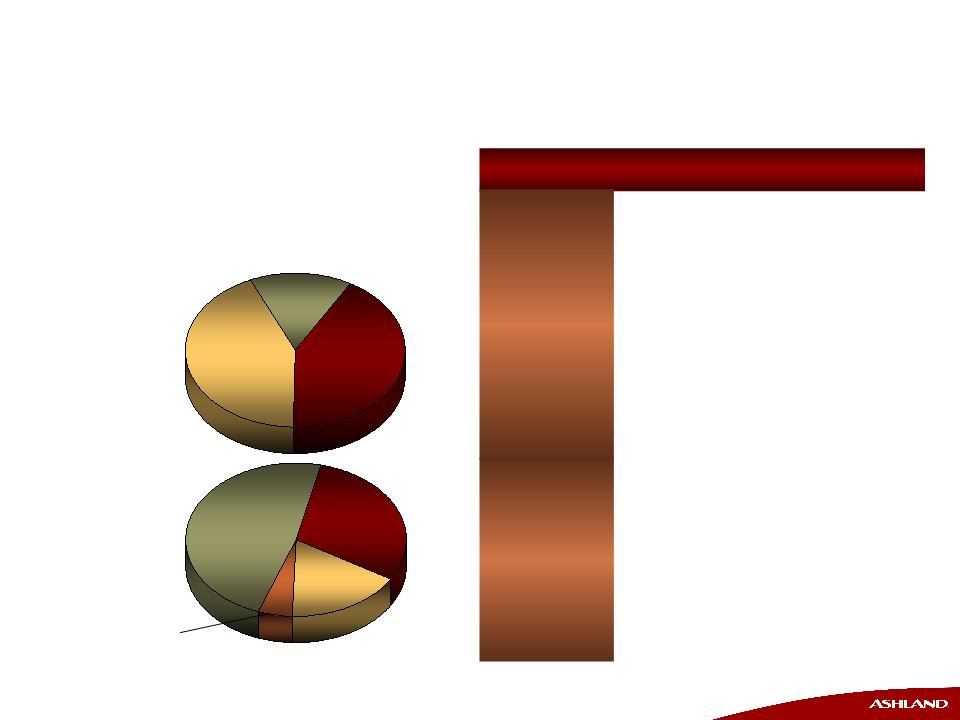

Ashland Water Technologies

A major global supplier to the water treatment industry

A major global supplier to the water treatment industry

North

America

America

30%

Latin America/

Other - 5%

Other - 5%

Marine

15%

15%

Marine

15%

15%

Industrial

42%

Business Overview | |

Customers/ Markets | · Automotive · Municipal wastewater treatment · Pulp and paper processing · Paint and coatings · Adhesives · Printing inks · Commercial and institutional building management · Merchant marine |

Products/ Services | · Chemicals and consulting services for utility water treatment · Process water treatments · Technical products and shipboard services for the merchant marine and cruise ship industry |

Revenue

by Geography

by Geography

Revenue

by Business Unit

by Business Unit

E&PS

43%

43%

Asia/

Pacific

17%

Pacific

17%

Europe

48%

48%

For the Fiscal Year Ended Sept.30, 2008

Revenue: $0.9 billion

EBITDA*: $36 million

EBITDA* Margin: 4.0%

* See Appendix C for EBITDA reconciliation.

Appendix C

Regulation G Reconciliations

Regulation G Reconciliations

Appendix C

Regulation G Reconciliations

Regulation G Reconciliations

47

Regulation G: Reconciliation of Operating

Income to Adjusted EBITDA

Income to Adjusted EBITDA

The information provided in this presentation regarding

adjusted earnings before interest, taxes, depreciation,

and amortization (EBITDA) does not conform to generally

accepted accounting principles (GAAP) and should not

be construed as an alternative to the reported results

determined in accordance with GAAP. Management has

included this non-GAAP information to assist in

understanding the operating performance of the

Company and its operating segments. The non-GAAP

information provided may not be consistent with the

methodologies used by other companies. All non-GAAP

information is reconciled with reported GAAP results in

the financials that follow in this Appendix.

adjusted earnings before interest, taxes, depreciation,

and amortization (EBITDA) does not conform to generally

accepted accounting principles (GAAP) and should not

be construed as an alternative to the reported results

determined in accordance with GAAP. Management has

included this non-GAAP information to assist in

understanding the operating performance of the

Company and its operating segments. The non-GAAP

information provided may not be consistent with the

methodologies used by other companies. All non-GAAP

information is reconciled with reported GAAP results in

the financials that follow in this Appendix.

48

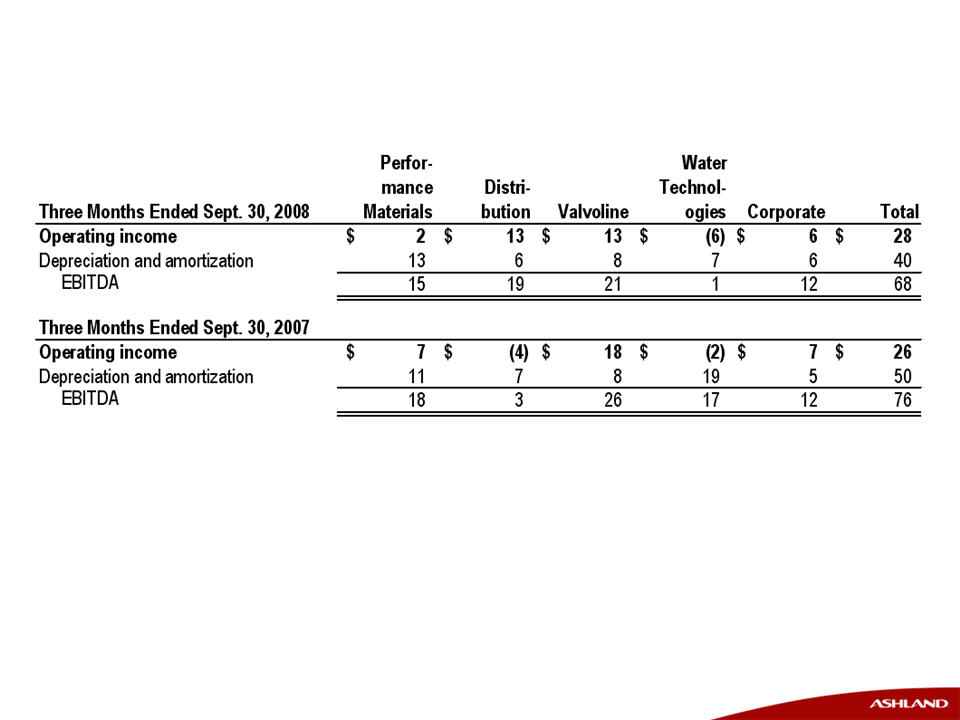

Ashland Inc. Fiscal Fourth Quarter

Regulation G: Reconciliation of Operating Income

to EBITDA

Regulation G: Reconciliation of Operating Income

to EBITDA

(in millions)

49

Ashland Inc. Fiscal Year Ended Sept. 30

Regulation G: Reconciliation of Operating Income

to EBITDA

Regulation G: Reconciliation of Operating Income

to EBITDA

(in millions)

50

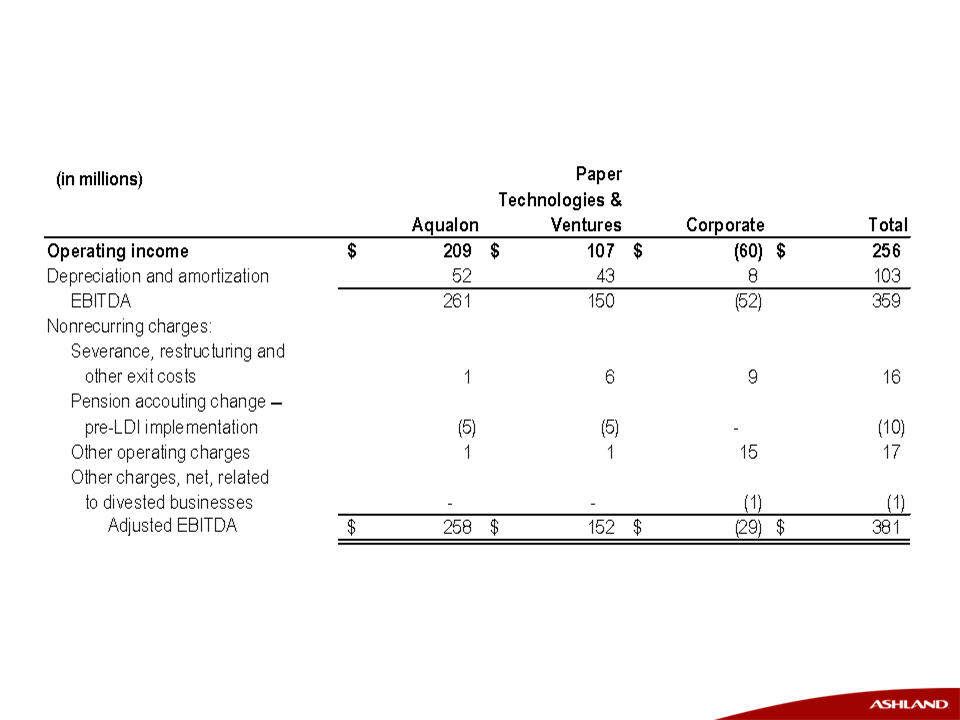

Hercules Inc. 12 Months Ended Sept. 30, 2008

Regulation G: Reconciliation of Operating

Income to Adjusted EBITDA

Regulation G: Reconciliation of Operating

Income to Adjusted EBITDA