FORWARD LOOKING STATEMENT

Certain statements set forth in this presentation consist of forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. These forward-looking statements involve known and unknown risks, uncertainties, and other factors that may cause the actual results, performance, or achievements of the Company to be different from any future results, performance, and achievements expressed or implied by these statements. They should be read in conjunction with the company’s most recent annual report, as well as the company’s Form 10-K and other reports filed with the Securities and Exchange Commission containing a discussion of the company’s business and of various factors that may affect it. Statements in this presentation may include adjusted financial measures governed by Regulation G. For a reconciliation of these measures, please visit the Investor Relations page at www.hughessupply.com

1

Company Overview

2

Company Overview

75-year history as a leading diversified distributor of construction, repair and maintenance products with approximately $3.5 billion in sales and $150 million in operating income

– 489 branches in 38 states

Strong market share position in high growth end markets

– #1 or #2 market position in high growth product segments

– 70% of revenues in 10 fastest growing states in the U.S.

Comprehensive product offering, highly knowledgeable sales force and loyal customer base developed over long history

– Over 350,000 products and 100,000 customers

Transformational leadership initiating significant operational and financial changes

3

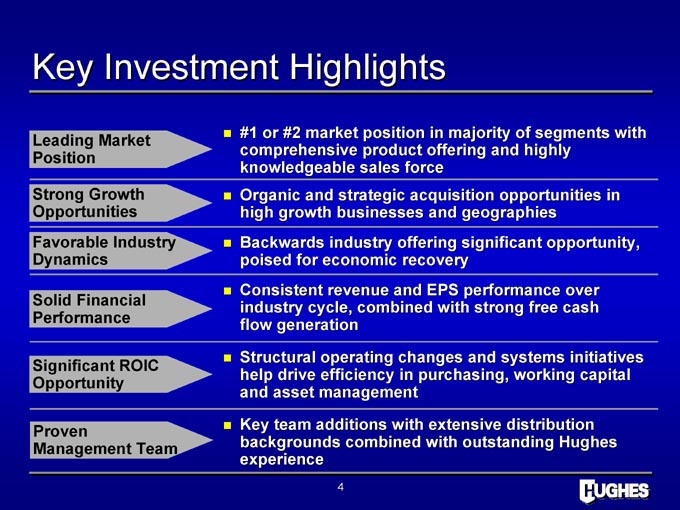

Key Investment Highlights

#1 or #2 market position in majority of segments with

Leading Market

comprehensive product offering and highly

Position

knowledgeable sales force

Strong Growth Organic and strategic acquisition opportunities in

Opportunities high growth businesses and geographies

Favorable Industry Backwards industry offering significant opportunity,

Dynamics poised for economic recovery

Consistent revenue and EPS performance over

Solid Financial industry cycle, combined with strong free cash

Performance flow generation

Structural operating changes and systems initiatives change

Significant ROIC

help drive efficiency in purchasing, working capital

Opportunity

and asset management

Proven Key team additions with extensive distribution

Management Team backgrounds combined with outstanding Hughes

experience

4

Transformational Leadership

Name Position Background

Tom Morgan President and CEO Genuine Parts – 22 years

US Office Products

David Bearman EVP and CFO General Electric – 20 years; CFO at

4 subsidiaries

Cardinal Health CFO – 1989–1998

NCR CFO

Tom Starnes President MRO HBS, P&G, Frito Lay

John Steele Operations Genuine Parts – 15 years,

Information Technology/Internet

Gradie Winstead

Skip Hughes Group Presidents

Mike Stanwood

118 Years of Hughes Service

Bob Machaby Vendor Development

Tom Ward Information Technology Industry Competitor – Ferguson

Steve Zepf Mergers & Acquisitions Hughes CFO – 18 years

5

Industry & Business Overview

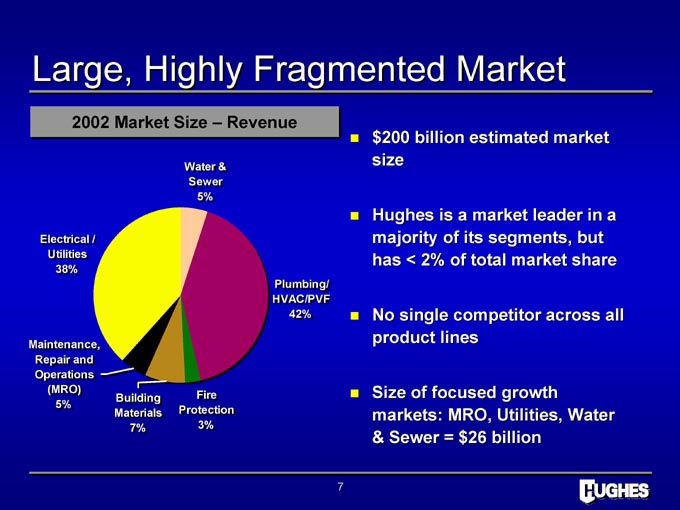

Large, Highly Fragmented Market

2002 Market Size – Revenue

Water & size

&

Sewer

5%

Hughes is a market leader in a

Electrical / / majority of its segments, but

Utilities has < 2% of total market share

38%

Plumbing/

HVAC/PVF

42% No single competitor across all

product lines

Maintenance,

Repair and

Operations

(MRO) Size of focused growth

Building Fire

5%

Materials Protection markets: MRO, Utilities, Water

7% 3%

& Sewer = $26 billion

7

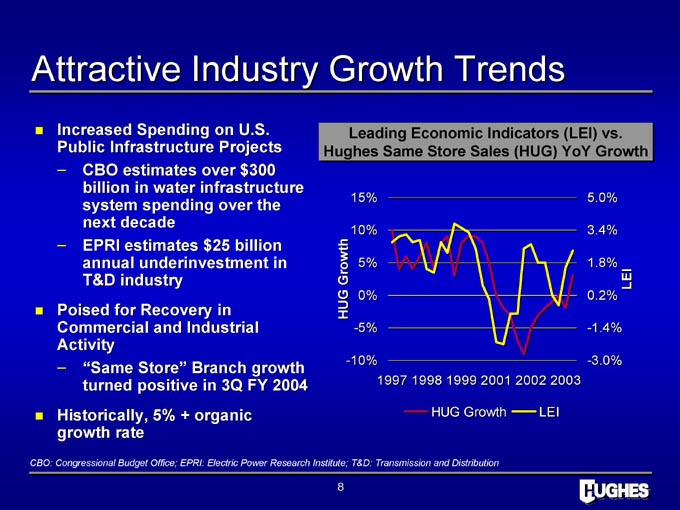

Attractive Industry Growth Trends

Increased Spending on U.S. Public Infrastructure Projects

– CBO estimates over $300 billion in water infrastructure system spending over the next decade

– EPRI estimates $25 billion annual underinvestment in T&D industry

Poised for Recovery in Commercial and Industrial Activity

– “Same Store” Branch growth turned positive in 3Q FY 2004

Historically, 5% + organic growth rate

Leading Economic Indicators (LEI) vs. Hughes Same Store Sales (HUG) YoY Growth

CBO: Congressional Budget Office; EPRI: Electric Power Research Institute; T&D: Transmission and Distribution

8

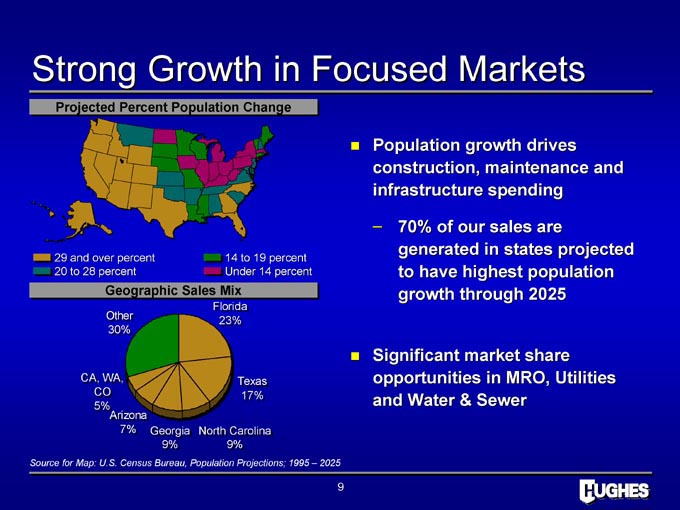

Strong Growth in Focused Markets

Projected Percent Population Change

29 and over percent 14 to 19 percent 20 to 28 percent Under 14 percent

Geographic Sales Mix

Population growth drives construction, maintenance and infrastructure spending

– 70% of our sales are generated in states projected to have highest population growth through 2025

Significant market share opportunities in MRO, Utilities and Water & Sewer

Source for Map: U.S. Census Bureau, Population Projections; 1995 – 2025

9

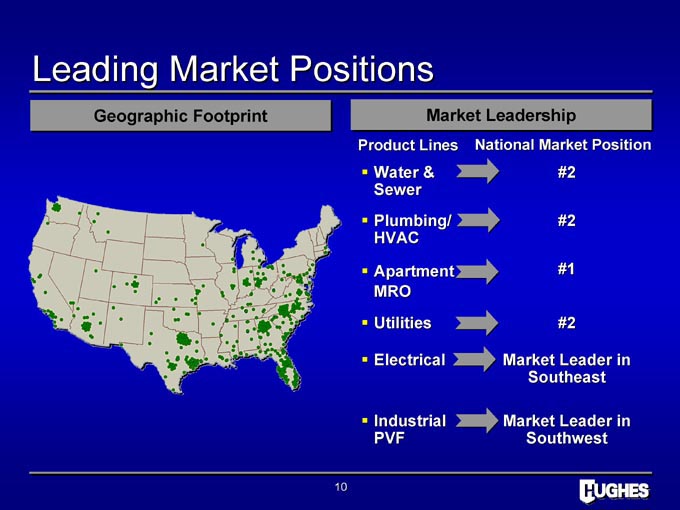

Leading Market Positions

Geographic Footprint

Market Leadership

Product Lines National Market Position

Water & #2

Sewer

Plumbing/ #2

HVAC

Apartment #1

MRO

Utilities #2

Electrical Market Leader in

Southeast

Industrial Market Leader in

PVF Southwest

10

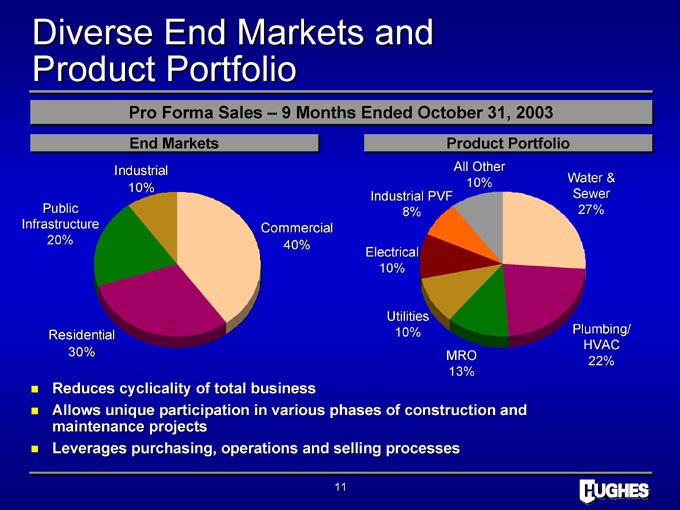

Diverse End Markets and Product Portfolio

Pro Forma Sales – 9 Months Ended October 31, 2003

End Markets Product Portfolio

Industrial All Other

10% Water &

10%

Industrial PVF Sewer

Public 8% 27%

Infrastructure Commercial

20% 40%

Electrical

10%

Utilities

Residential 10% Plumbing/

HVAC

30% MRO

22%

13%

Reduces cyclicality of total business

Allows unique participation in various phases of construction and maintenance projects

Leverages purchasing, operations and selling processes

11

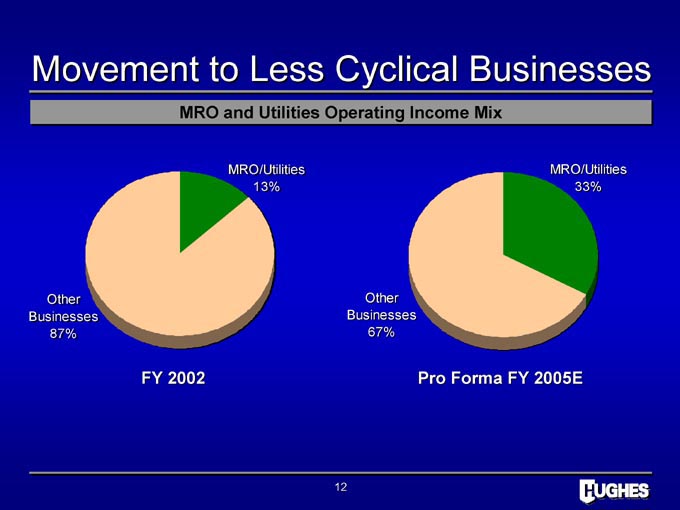

Movement to Less Cyclical Businesses

MRO and Utilities Operating Income Mix

MRO/Utilities MRO/Utilities

13% 33%

Other Other

Businesses Businesses

87% 67%

FY 2002 Pro Forma FY 2005E

12

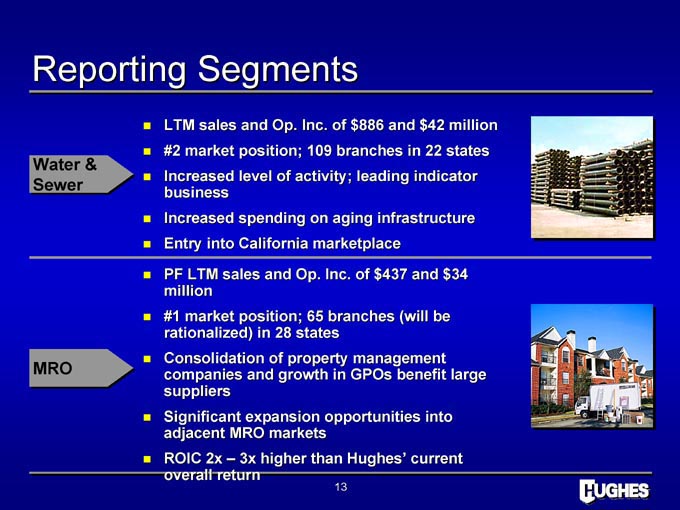

Reporting Segments

LTM sales and EBIT of $886 and $42 million

#2 market position; 109 branches in 22 states

Water &

Increased level of activity; leading indicator

Sewer

business

Increased spending on aging infrastructure

Entry into California marketplace

PF LTM sales and EBIT of $437 and $34 million

#1 market position; 65 branches (will be

rationalized) in 28 states

Consolidation of property management

companies and growth in GPOs benefit large

MRO suppliers

Significant expansion opportunities into

adjacent MRO markets

ROIC 2x – 3x higher than Hughes’ current

overall return

13

Century Acquisition

$ 360 million acquisition closed on December 19, 2003

Large, fast-growing participant in MRO market complements Hughes business

Opportunities to expand into adjacent markets – lodging / hospitality, healthcare / assisted living, education, government / military

– From a $2.5 billion market opportunity to atunity $10 billion market opportunity

Good management, superior business model – superior margins, costs, capital efficiency, annuity characteristics

Significant net synergies over next two years – facilities/distribution model, transportation, purchasing, marketing, corporate services, less amortization of intangibles

Accretive to EPS and strengthens overall financial equation

Strong step in the transformation of Hughes

14

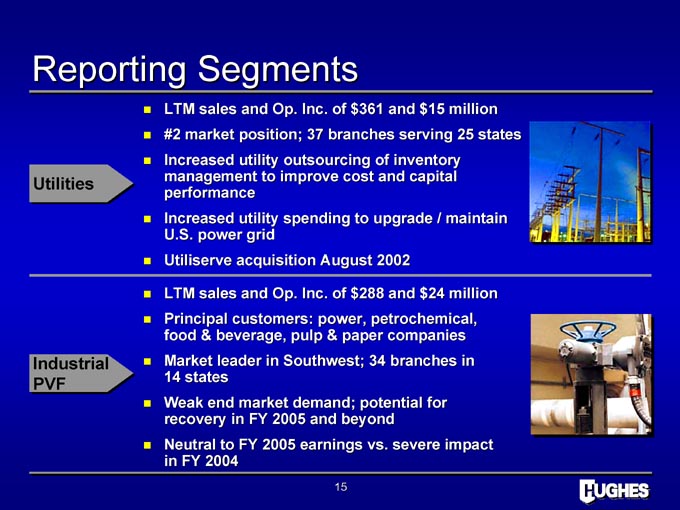

Reporting Segments

LTM sales and EBIT of $361 and $15 million

#2 market position; 37 branches serving 25 states

Increased utility outsourcing of inventory

Utilities management to improve cost and capital

performance

Increased utility spending to upgrade / maintain

U.S. power grid

Utiliserve acquisition August 2002

LTM sales and EBIT of $288 and $24 million

Principal customers: power, petrochemical,

food & beverage, pulp & paper companies

Industrial Market leader in Southwest; 34 branches in

PVF 14 states

Weak end market demand; potential for

recovery in FY 2005 and beyond

Neutral to FY 2005 earnings vs. severe impact

in FY 2004

15

Reporting Segments

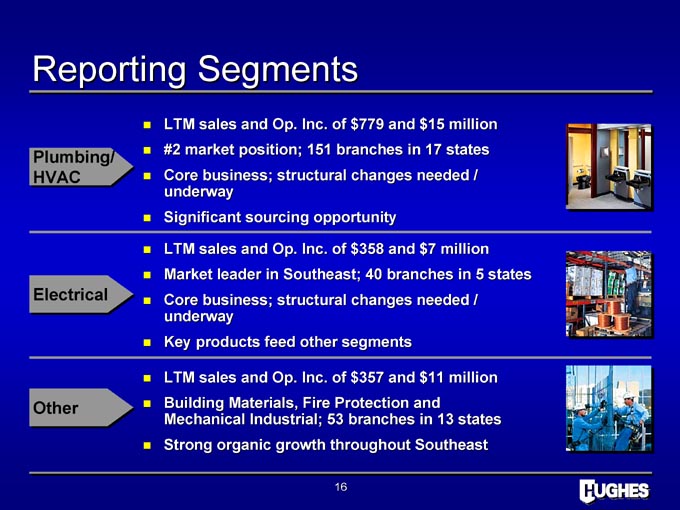

LTM sales and EBIT of $779 and $15 million

Plumbing/ #2 market position; 151 branches in 17 states

HVAC Core business; structural changes needed /

underway

Significant sourcing opportunity

LTM sales and EBIT of $358 and $7 million

Market leader in Southeast; 40 branches in 5 states

Electrical Core business; structural changes needed /

underway

Key products feed other segments

LTM sales and EBIT of $357 and $11 million

Other Building Materials, Fire Protection and

Mechanical Industrial; 53 branches in 13 states

Strong organic growth throughout Southeast

16

Business Strategy

17

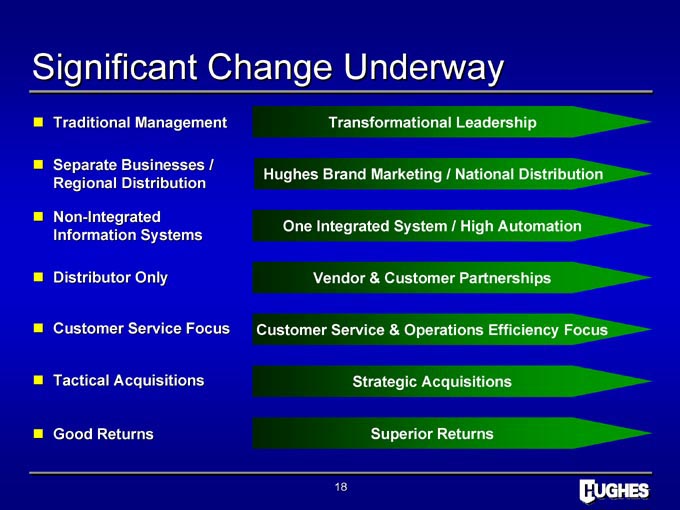

Significant Change Underway

Traditional Management Transformational Leadership

Separate Businesses /

Hughes Brand Marketing / National Distribution

Regional Distribution

Non-Integrated

One Integrated System / High Automation

Information Systems

Distributor Only Vendor & Customer Partnerships

Customer Service Focus Customer Service & Operations Efficiency Focus

Tactical Acquisitions Strategic Acquisitions

Good Returns Superior Returns

18

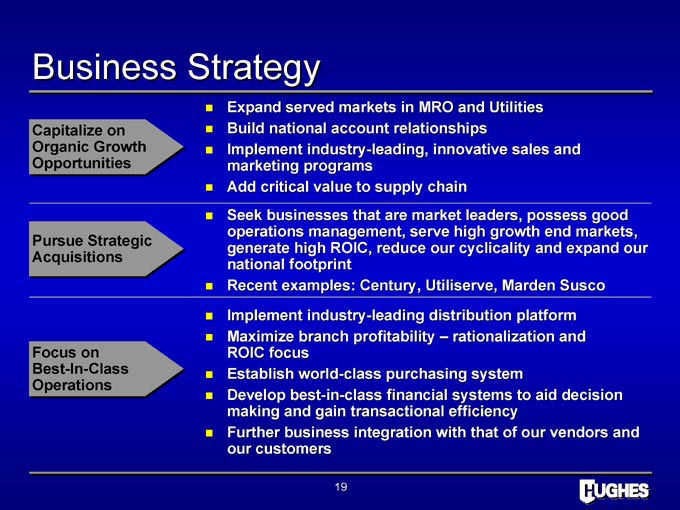

Business Strategy

Expand served markets in MRO and Utilities

Capitalize on Build national account relationships

Organic Growth Implement industry-leading, innovative sales and

Opportunities marketing programs

Add critical value to supply chain

Seek businesses that are market leaders, possess good

operations management, serve high growth end markets,

Pursue Strategic

generate high ROIC, reduce our cyclicality and expand our

Acquisitions

national footprint

Recent examples: Century, Utiliserve, Marden Susco

Implement industry-leading distribution platform

Maximize branch profitability – rationalization and

Focus on ROIC focus

Best-In-Class—- Establish world-class purchasing system

Operations

Develop best-in-class financial systems to aid decision

making and gain transactional efficiency

Further business integration with that of our vendors and

our customers

19

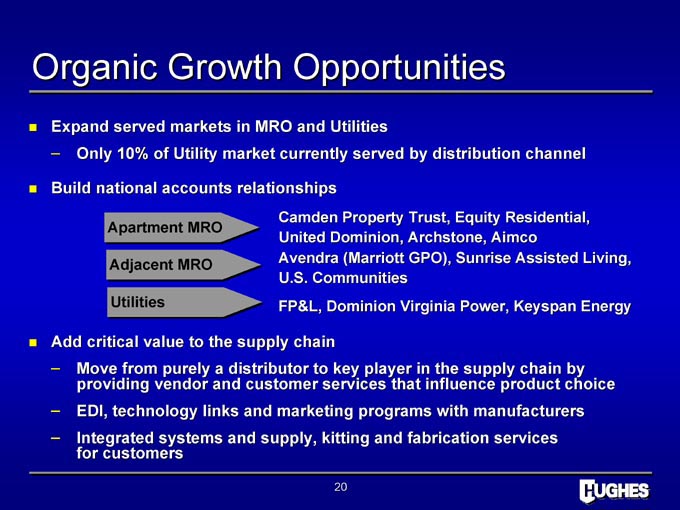

Organic Growth Opportunities

Expand served markets in MRO and Utilities

– Only 10% of Utility market currently served by distribution channel curren

Build national accounts relationships

Camden Property Trust, Equity Residential,

Apartment MRO

United Dominion, Archstone, Aimco

Adjacent MRO Avendra (Marriott GPO), Sunrise Assisted Living,

U.S. Communities

Utilities FP&L, Dominion Virginia Power, Keyspan Energy

Add critical value to the supply chain

– Move from purely a distributor to key player in the supply chain by providing vendor and customer services that influence product choice

– EDI, technology links and marketing programs with manufacturers ing

– Integrated systems and supply, kitting and fabrication services for customers

20

Innovative Sales and Marketing Programs

Hughes Branding

Promotional Product Brochures

Product Line Catalogs

Awards Programs

Major Marketing Events

21

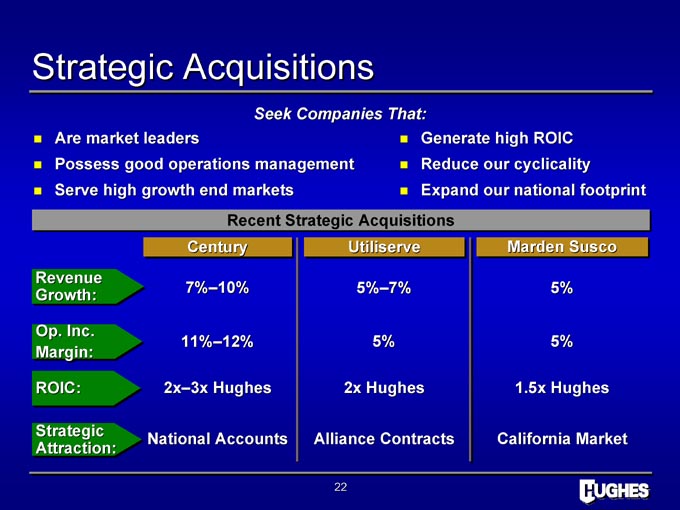

Strategic Acquisitions

Seek Companies That:

Are market leaders Generate high ROIC

Possess good operations management Reduce our cyclicality

Serve high growth end markets Expand our national footprint

Recent Strategic Acquisitions

Century Utiliserve Marden Susco

Revenue

7%–10% 5%–7% 5%

Growth:

EBIT

11%–12% 5% 5%

Margin:

ROIC: 2x–3x Hughes 2x Hughes 1.5x Hughes

Strategic

National Accounts Alliance Contracts California Market

Attraction:

22

Operations Strategy

23

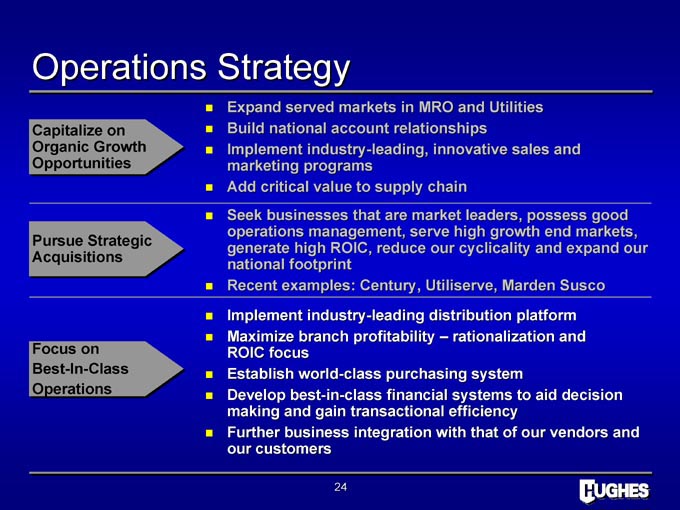

Operations Strategy

Expand served markets in MRO and Utilities

Capitalize on Build national account relationships

Organic Growth Implement industry-leading, innovative sales and

Opportunities marketing programs

Add critical value to supply chain

Seek businesses that are market leaders, possess good

operations management, serve high growth end markets,

Pursue Strategic

generate high ROIC, reduce our cyclicality and expand our

Acquisitions

national footprint

Recent examples: Century, Utiliserve, Marden Susco

Implement industry-leading distribution platform

Maximize branch profitability – rationalization and

Focus on ROIC focus

Best-In-Class—- Establish world-class purchasing system

Operations Develop best-in-class financial systems to aid decision

making and gain transactional efficiency

Further business integration with that of our vendors and

our customers

24

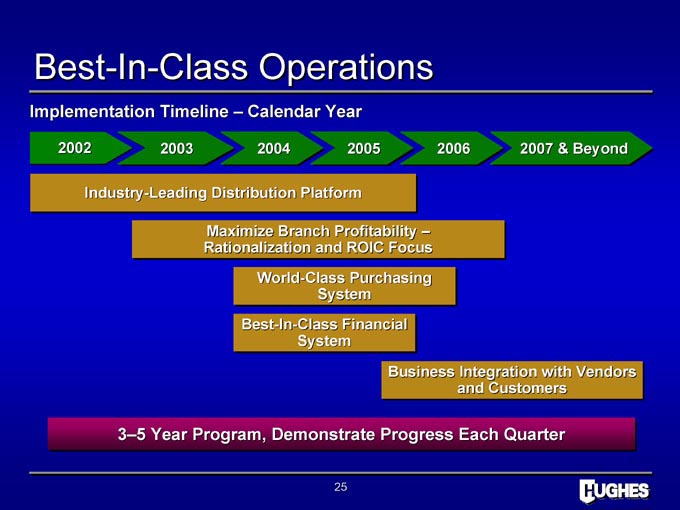

Best-In-Class Operations

Implementation Timeline – Calendar Year

2002 2003 2004 2005 2006 2007 & Beyond

Industry-Leading Distribution Platform

Maximize Branch Profitability –Rationalization and ROIC Focus World-Class Purchasing System Best-In-Class Financial System

Business Integration with Vendors and Customers

3–5 Year Program, Demonstrate Progress Each Quarter

25

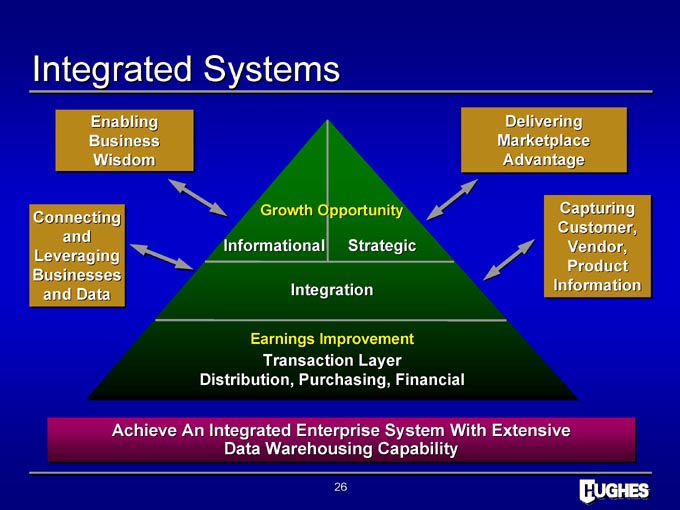

Integrated Systems

Enabling Delivering

Business Marketplace

Wisdom Advantage

Growth Opportunity Capturing

Connecting

Customer,

and

Informational Strategic Vendor,

Leveraging

Product

Businesses

Integration Information

and Data

Earnings Improvement

Transaction Layer

Distribution, Purchasing, Financial

Achieve An Integrated Enterprise System With Extensive Data Warehousing Capability

26

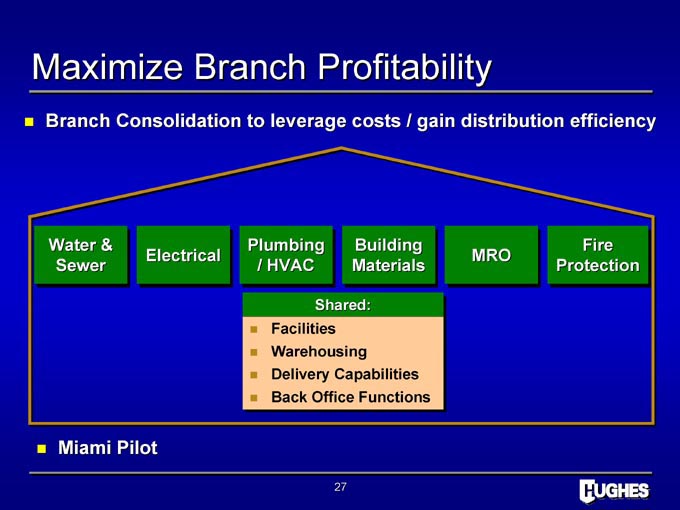

Maximize Branch Profitability

Branch Consolidation to leverage costs / gain distribution efficiency

Water & Plumbing Building Fire

Electrical MRO

Sewer / HVAC Materials Protection

Shared:

Facilities

Warehousing

Delivery Capabilities

Back Office Functions

Miami Pilot

27

Financial Review

28

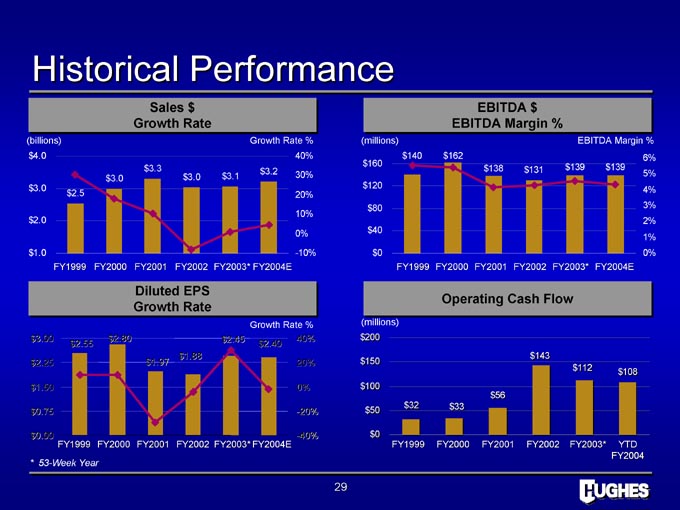

Historical Performance

Sales $ EBITDA $

Growth Rate EBITDA Margin %

(billions) Growth Rate % (millions) EBITDA Margin %

Diluted EPS

Operating Cash Flow

Growth Rate

Growth Rate % (millions)

* 53-Week Year

29

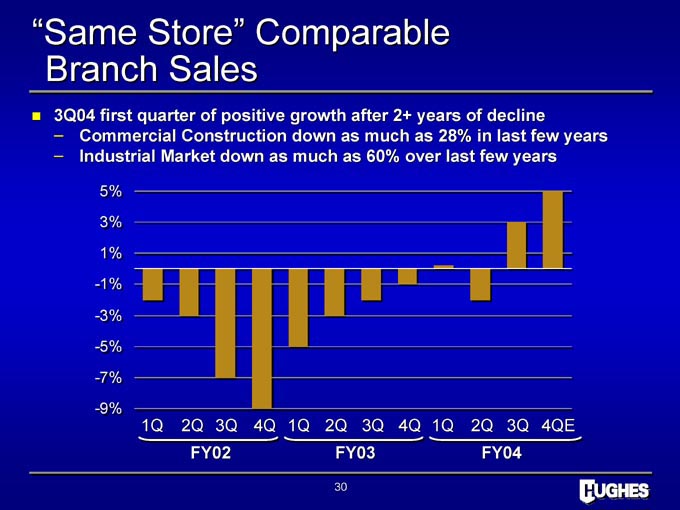

“Same Store” Comparable Branch Sales

3Q04 first quarter of positive growth after 2+ years of decline

– Commercial Construction down as much as 28% in last few years

– Industrial Market down as much as 60% over last few years

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4QE

FY02 FY03 FY04

30

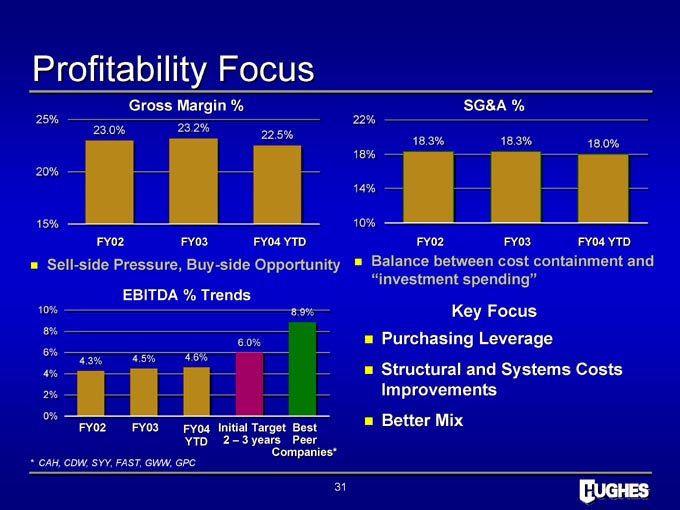

Profitability Focus

Gross Margin % SG&A %

Sell-side Pressure, Buy-side Opportunity Balance between cost containment and

“investment spending”

EBITDA % Trends

FY02 FY03 FY04 Initial Target Best

YTD 2 – 3 years Peer

Companies*

* CAH, CDW, SYY, FAST, GWW, GPC

Key Focus

Purchasing Leverage

Structural and Systems Costs Improvements

Better Mix

31

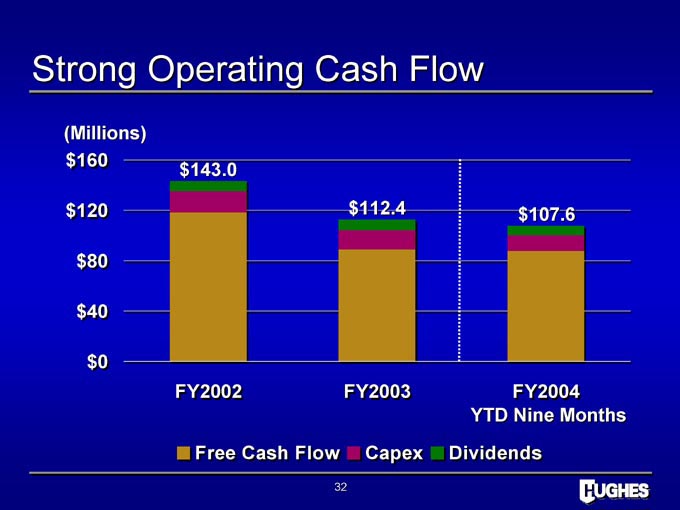

Strong Operating Cash Flow

(Millions)

FY2002 FY2003 FY2004

YTD Nine Months

Free Cash Flow Capex Dividends

32

Return on Invested Capital

Portfolio of nine businesses with significantly differentiated earnings and capital equations

Identify (1) most attractive growth areas and (2) businesses where equations require improvement

Structural changes at core businesses that provide buying power and feed growth businesses

Four businesses have superior returns:

–MRO – Water & Sewer

–Utilities – Industrial

33

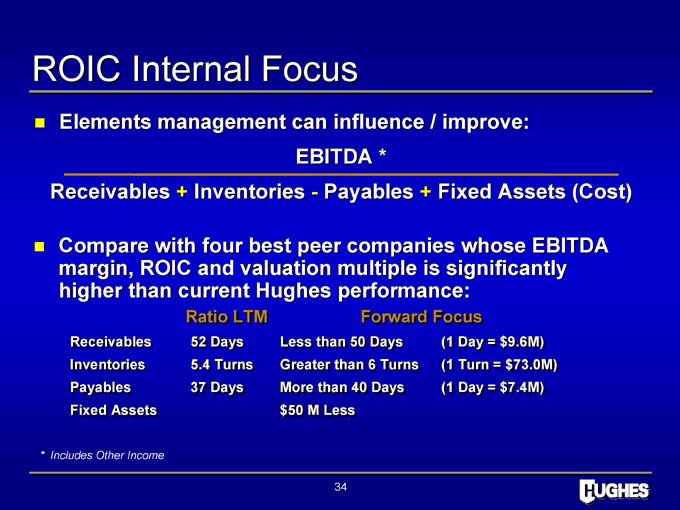

ROIC Internal Focus

Elements management can influence / improve: EBITDA *

Receivables + Inventories—Payables + Fixed Assets (Cost)

Compare with four best peer companies whose EBITDA margin, ROIC and valuation multiple is significantly higher than current Hughes performance:

Ratio LTM Forward Focus

Receivables 52 Days Less than 50 Days (1 Day = $ $9. 9.6M)

Inventories 5.4 Turns 5.4 Greater than 6 Turns 6 (1 Turn = $ $73.0M) .

Payables 37 Days More than 40 Days (1 Day = $ $7. 7.4M)

Fixed Assets $ $ 50 M Less

* Includes Other Income

34

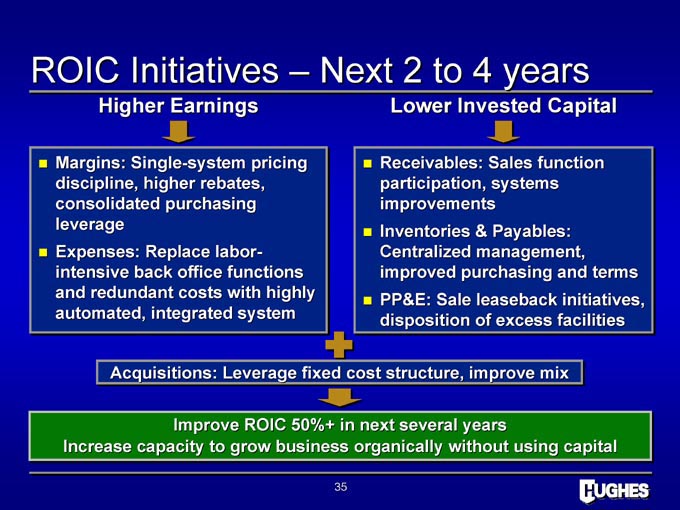

ROIC Initiatives – Next 2 to 4 years

Higher Earnings

Margins: Single-system pricing

discipline, higher rebates,

consolidated purchasing

leverage

Expenses: Replace labor-

intensive back office functions

and redundant costs with highly

automated, integrated system

Lower Invested Capital

Receivables: Sales function

participation, systems

improvements

Inventories & Payables:

Centralized management,

improved purchasing and terms

PP&E: Sale leaseback initiatives,

disposition of excess facilities

Acquisitions: Leverage fixed cost structure, improve mix

Improve ROIC 50%+ in next several years

Increase capacity to grow business organically without using capital

35

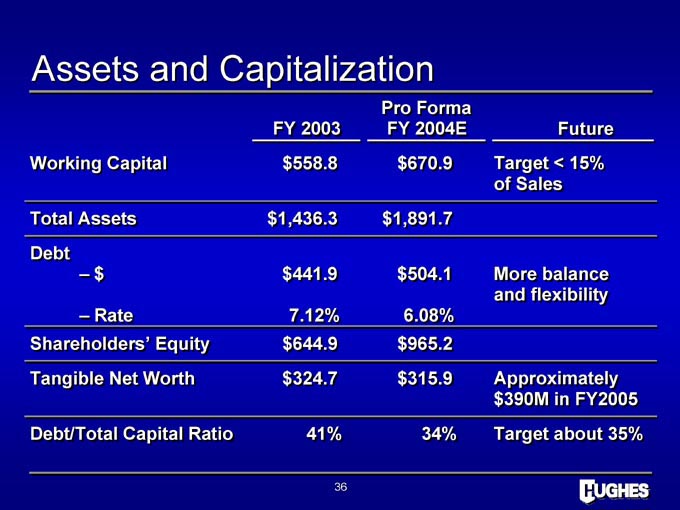

Assets and Capitalization

Pro Forma

FY 2003 FY 2004E Future

Working Capital $558.8 $670.9 Target < 15% of Sales

Total Assets $1,436.3 $1,891.7

Debt

– $ $441.9 $504.1 More balance and flexibility

– Rate 7.12% 6.08%

Shareholders’ Equity $644.9 $965.2

Tangible Net Worth $324.7 $315.9 Approximately $390M in FY2005

Debt/Total Capital Ratio 41% 34% Target about 35%

36

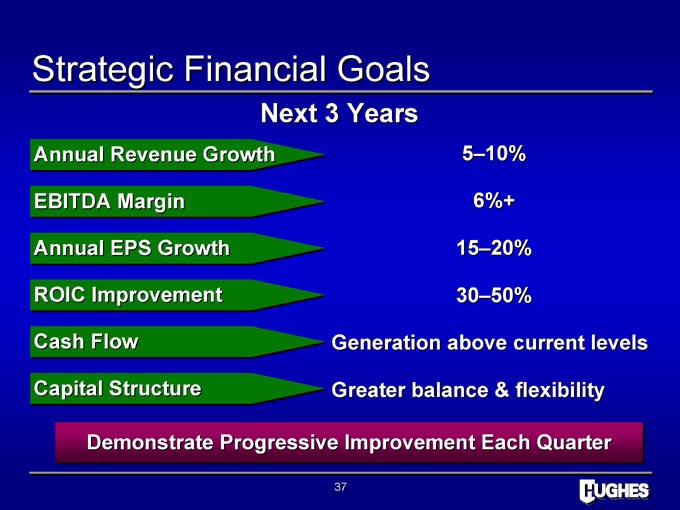

Strategic Financial Goals

Next 3 Years

Annual Revenue Growth 5–10%

EBITDA Margin 6%+

Annual EPS Growth 15–20%

ROIC Improvement 30–50%

Cash Flow Generation above current levels

Capital Structure Greater balance & flexibility

Demonstrate Progressive Improvement Each Quarter

37

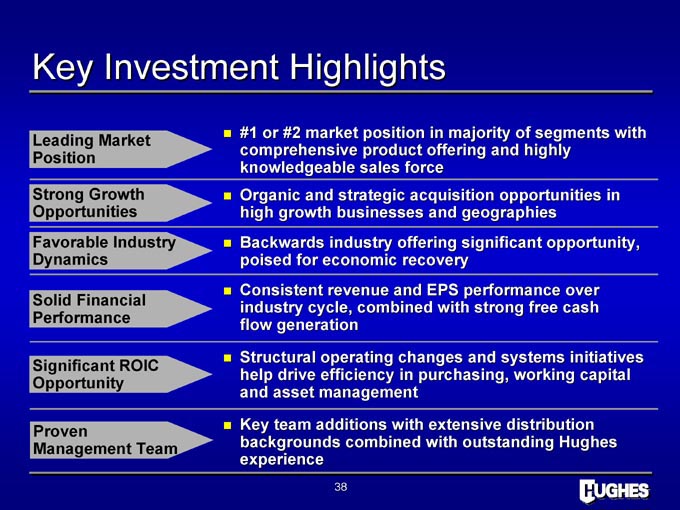

Key Investment Highlights

#1 or #2 market position in majority of segments with

Leading Market comprehensive product offering and highly

Position knowledgeable sales force

Strong Growth Organic and strategic acquisition opportunities in

Opportunities high growth businesses and geographies

Favorable Industry Backwards industry offering significant opportunity,

Dynamics poised for economic recovery

Consistent revenue and EPS performance over

Solid Financial industry cycle, combined with strong free cash

Performance flow generation

Significant ROIC Structural operating changes and systems initiatives change

Opportunity help drive efficiency in purchasing, working capital

and asset management

Proven Key team additions with extensive distribution

Management Team backgrounds combined with outstanding Hughes

experience

38