Signatures on this Letter of Transmittal must be guaranteed by an Eligible Guarantor Institution, unless Restricted Notes are tendered: (i) by a holder who has not completed the box entitled “Special Issuance Instructions” or “Special Delivery Instructions” on this Letter of Transmittal; or (ii) for the account of an Eligible Guarantor Institution. In the event that the signatures in this Letter of Transmittal or a notice of withdrawal, as the case may be, are required to be guaranteed, such guarantees must be by an Eligible Guarantor Institution which is a member of a firm of a registered national securities exchange or of the Financial Industry Regulatory Authority, a commercial bank or trust company having an office or correspondent in the United States or another “eligible guarantor institution” within the meaning of Rule 17Ad-15 under the Securities Exchange Act of 1934, as amended (an “Eligible Guarantor Institution”). If Restricted Notes are registered in the name of a person other than the signer of this Letter of Transmittal, the Restricted Notes surrendered for exchange must be endorsed by, or be accompanied by a written instrument or instruments of transfer or exchange, in satisfactory form as determined by the Issuer, in its sole discretion, duly executed by the registered holder with the signature thereon guaranteed by an Eligible Guarantor Institution.

4. Special Issuance and Delivery Instructions.

Tendering holders should indicate, as applicable, the name and address to which the Restricted Notes not exchanged are to be issued or delivered, if different from the name or address of the person signing this Letter of Transmittal. In the case of issuance in a different name, the taxpayer identification number of the person named must also be indicated and, as described in Instruction 8, a duly completed IRS Form W-9 or IRS Form W-8, as applicable, must be provided. Holders tendering Restricted Notes by book-entry transfer may request that Restricted Notes not exchanged be credited to such account maintained at the book-entry transfer facility as such holder may designate.

5. Transfer Taxes.

If Restricted Notes for principal amounts not tendered or accepted for exchange are to be registered or issued in the name of any person other than the registered holder of the Restricted Notes tendered, or if tendered Restricted Notes or Registered Notes are to be registered in the name of any person other than the person signing this Letter of Transmittal, or if a transfer tax is imposed for any other reason, the amount of any such transfer taxes (whether imposed on the registered holder or any other person) will be payable by the applicable holder. If satisfactory evidence of payment of such taxes or exemption therefrom is not submitted herewith, the amount of such transfer taxes will be billed directly to such applicable holder.

6. Waiver of Conditions.

The Issuer reserves the absolute right to waive, in whole or in part, any of the conditions to the Exchange Offer set forth in the Prospectus.

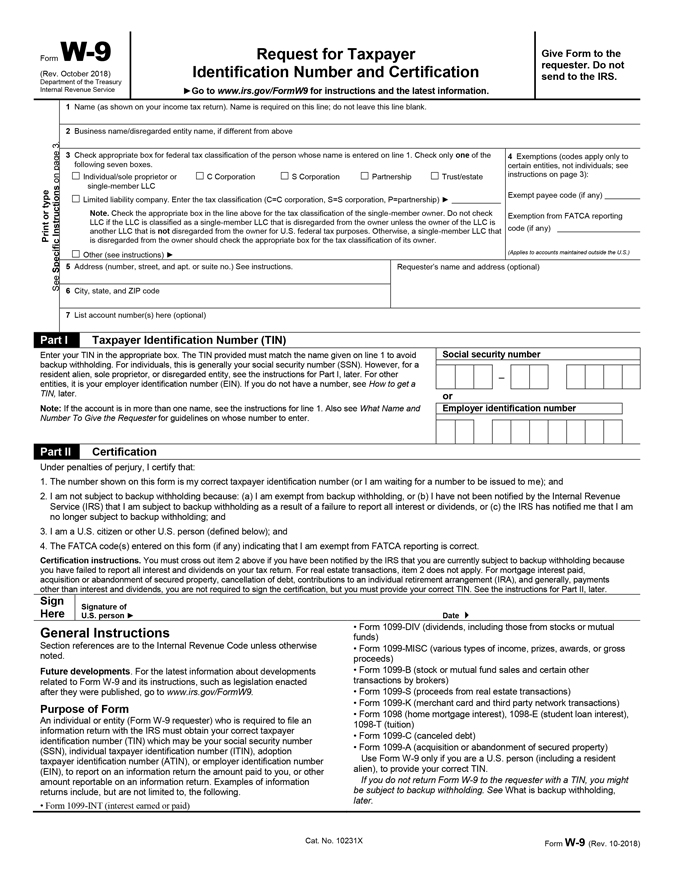

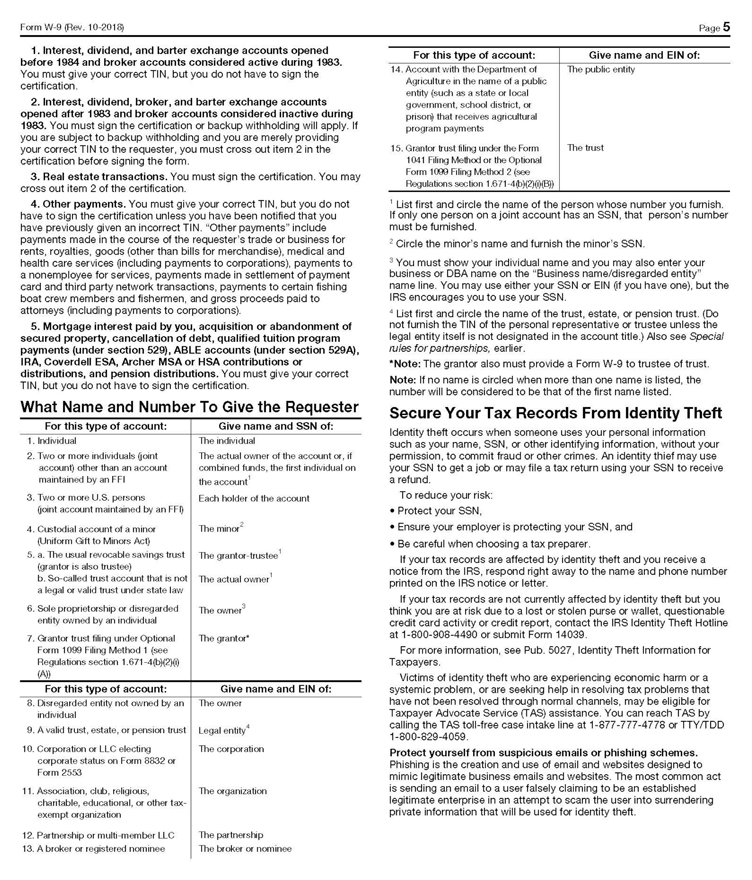

7. Taxpayer Information; IRS Form W-9; IRS Form W-8.

Under U.S. federal income tax law, a tendering holder whose Restricted Notes are accepted for exchange for Registered Notes may be subject to backup withholding on reportable payments made on the Registered Notes unless the holder provides the Exchange Agent, Issuer, or other payor with its correct taxpayer identification number (“TIN”) and certain other information on Internal Revenue Service (“IRS”) Form W-9, which is provided below, or otherwise establishes an exemption. If the Exchange Agent, Issuer or other payor is not provided with the correct TIN or an adequate basis for an exemption, a holder may be subject to a penalty imposed by the IRS, and backup withholding (currently, at a rate of 24%) may apply to any reportable payments on the Registered Notes made to such holder. Such reportable payments generally will be subject to information reporting, even if the Exchange Agent, Issuer or other payor is provided with a TIN. Backup withholding is not an additional tax. Rather, the U.S. federal income tax liability of a person subject to backup withholding will be reduced by the amount withheld. If withholding results in an overpayment of taxes, a refund may be obtained, provided that the required information is timely provided to the IRS.

To prevent backup withholding on reportable payments made on the Registered Notes, each holder that is a “United States person” for U.S. federal income tax purposes should provide a properly completed and executed IRS Form W-9. Please see the instructions to the enclosed IRS Form W-9 for further information.

Certain holders (including, among others, generally all corporations and certain non-U.S. persons) are not subject to backup withholding. Exempt U.S. holders may establish their exempt status on IRS Form W-9. A non-U.S. holder may qualify as an exempt recipient by submitting a properly completed IRS Form W-8BEN, Form W-8BEN-E, W-8ECI, W-8EXP or W-8IMY, as the case may be, signed under penalties of perjury, attesting to that holder’s exempt status. The applicable IRS Form W-8 can be obtained from the IRS website at www.irs.gov.

10