UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

_________________________

FORM 10‑K

(Mark One)

| þ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2016

or

| o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from ______________ to __________

Commission File Number 1‑3473

TESORO CORPORATION

(Exact name of registrant as specified in its charter)

| Delaware |  | 95-0862768 |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |

| 19100 Ridgewood Pkwy, San Antonio, Texas 78259-1828 | ||

| (Address of principal executive offices) (Zip Code) | ||

| 210-626-6000 | ||

| (Registrant’s telephone number, including area code) | ||

Securities registered pursuant to Section 12(b) of the Act:

| Title of Each Class | Name of Each Exchange on Which Registered | |

Common Stock, $0.16 2/3 par value | New York Stock Exchange | |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes þ No o

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No þ

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes þ No o

Indicate by check mark if the disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of the registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. þ

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer | þ | Accelerated filer | o | |||

| Non-accelerated filer | o (Do not check if a smaller reporting company) | Smaller reporting company | o | |||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No þ

At June 30, 2016, the aggregate market value of the voting common stock held by non-affiliates of the registrant was approximately $8.8 billion based upon the closing price of its common stock on the New York Stock Exchange Composite tape. At February 15, 2017, there were 116,986,291 shares of the registrant’s common stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE:

Portions of the registrant’s Proxy Statement to be filed pursuant to Regulation 14A pertaining to the 2016 Annual Meeting of Stockholders are incorporated by reference into Part III hereof. The Company intends to file such Proxy Statement no later than 120 days after the end of the fiscal year covered by this Form 10-K.

| TABLE OF CONTENTS | ||

TESORO CORPORATION

ANNUAL REPORT ON FORM 10-K

This Annual Report on Form 10-K (including documents incorporated by reference herein) contains statements with respect to our expectations or beliefs as to future events. These types of statements are “forward-looking” and subject to uncertainties. See “Important Information Regarding Forward-Looking Statements.”

| IMPORTANT INFORMATION REGARDING FORWARD-LOOKING STATEMENTS | ||

IMPORTANT INFORMATION REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K (including information incorporated by reference) contains “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. All statements other than statements of historical fact, including without limitation statements regarding expectations regarding refining margins, revenues, cash flows, capital expenditures, turnaround expenses and other financial items, our business strategy, goals and expectations concerning our market position, future operations, margins and profitability, are forward-looking statements. Forward-looking statements may be identified by use of the words “anticipate,” “believe,” “could,” “estimate,” “expect,” “intend,” “may,” “plan,” “predict,” “project,” “will,” “would” and similar terms and phrases. Although we believe our assumptions concerning future events are reasonable, a number of risks, uncertainties and other factors could cause actual results and trends to differ materially from those projected, including, but not limited to:

| • | the constantly changing margin between the price we pay for crude oil and other refinery feedstocks as well as renewable identification numbers (“RINs”) and environmental credits, and the prices at which we are able to sell refined products; |

| • | changes in the expected value of and benefits derived from acquisitions and capital projects; |

| • | changes in global economic conditions on our business, especially in California, and the business of our suppliers, customers, business partners and credit lenders; |

| • | changes in fuel and utility costs for our facilities; |

| • | changes in the cost or availability of third-party vessels, pipelines and other means of transporting crude oil feedstocks and refined products; |

| • | regulatory and other requirements concerning the transportation of crude oil, particularly from the Bakken area; |

| • | changes in the carrying costs of our inventory; |

| • | the timing and extent of changes in commodity prices and underlying demand for our refined products, natural gas and natural gas liquids; |

| • | the availability and costs of crude oil, other refinery feedstocks, refined products and RINs; |

| • | changes in our cash flow from operations; |

| • | earthquakes or other natural disasters affecting operations; |

| • | direct or indirect effects on our business resulting from actual or threatened terrorist incidents, cyber-security breaches or acts of war; |

| • | weather conditions affecting our operations or the areas in which our refined products are marketed; |

| • | actions of customers and competitors; |

| • | state and federal environmental, economic, health and safety, energy and other policies and regulations, including those related to climate change and any changes therein, and any legal or regulatory investigations, delays, compliance costs or other factors beyond our control; |

| • | delays in obtaining necessary approvals and permits; |

| • | adverse rulings, judgments, or settlements in litigation or other legal or tax matters, including unexpected environmental remediation costs in excess of any reserves; |

| • | operational hazards inherent in refining operations and in transporting and storing crude oil and refined products; |

| • | changes in our credit profile; |

| • | changes in capital requirements or in execution of planned capital projects; |

| • | disruptions due to equipment interruption or failure at our facilities or third-party facilities; |

| • | seasonal variations in demand for refined products and natural gas; |

| • | risks related to labor relations and workplace safety; |

| • | political developments; and |

| • | the factors described in greater detail under “Competition” and “Risk Factors” in Items 1 and 1A, and our other filings with the SEC. |

All forward-looking statements included in this report are based on information available to us on the date of this report. We undertake no obligation to revise or update any forward-looking statements as a result of new information, future events or otherwise.

December 31, 2016 | 1 | ||

| GLOSSARY OF TERMS | ||

GLOSSARY OF TERMS

Alkylation - A process that chemically combines isobutane with other hydrocarbons through the control of temperature and pressure in the presence of an acid catalyst. This process produces alkylates, which have a high octane value and are blended into gasoline to improve octane values.

API - American Petroleum Institute - The main U.S. trade association for the oil and natural gas industry.

API Gravity - A scale for denoting the lightness or heaviness of crude oil and other liquid hydrocarbons. Calibrated in API degrees (or degrees API), it is used universally to express a crude oil’s relative density in an inverse measure - the lighter the crude, the higher the API gravity, and vice versa.

Blendstocks - Components used for blending or compounding into finished jet or gasoline (e.g., straight-run gasoline, alkylate, reformulate, benzene, toluene, and xylene). Excludes oxygenates (alcohols, ethers), butane and pentanes.

Calcining - A process whereby green or raw petroleum coke from the refining process is converted to a high grade coke by thermally treating it to remove moisture and volatile combustible matter. The upgraded high grade calcined coke is typically used by the aluminum industry.

CARB - California Air Resources Board - Gasoline and diesel fuel sold in the state of California are regulated by CARB and require stricter quality and emissions reduction performance than required by other states.

Cracking - The process of breaking down larger hydrocarbon molecules into smaller molecules using catalysts and/or elevated temperatures and pressures.

D&A - Depreciation and amortization expenses.

Deasphalting - A solvent extraction process of recovering higher-value oils from refining residues.

Delayed Coking - A process by which the heaviest crude oil fractions can be thermally cracked under conditions of elevated temperatures to produce both refined products and petroleum coke.

Exchange Arrangement - An agreement providing for the delivery of crude oil or refined products to/from a third party, in exchange for the delivery of crude oil or refined products to/from the third party.

FERC - Federal Energy Regulatory Commission.

Fluid Catalytic Cracking - A process that breaks down larger, heavier, and more complex hydrocarbon molecules into simpler and lighter molecules through the use of a catalytic agent and is used to increase the yield of gasoline. Fluid catalytic cracking uses a catalyst in the form of very fine particles, which behave as a fluid when aerated with a vapor.

Fractionation - The process of separating natural gas liquids into its component parts by heating the natural gas liquid stream and boiling off the various fractions in sequence from the lighter to the heavier hydrocarbon.

Fuel Margin - The margin on fuel products sold through our Marketing segment calculated as revenues less cost of sales. Cost of sales in fuel margin are based on purchases from our refining segment and third parties using average bulk market prices adjusted for transportation and other differentials.

Gas Processing - A complex industrial process designed to remove the heavier and more valuable natural gas liquids components from raw natural gas allowing the residue gas remaining after extraction to meet the quality specifications for long-haul pipeline transportation or commercial use.

Gross Refining Margin - The margin on products manufactured and purchased, including those sold to our Marketing segment. Gross refining margin is the difference between the prices of all manufactured refined products sold and the cost of crude oil and other feedstocks used to produce refined products, including the cost of transportation and distribution.

Heavy Crude Oil - Crude oil with an API gravity of 24 degrees or less. Heavy crude oil is typically sold at a discount to lighter crude oil.

Heavy Fuel Oils, Residual Products, Internally Produced Fuel and Other - Products other than gasoline, jet fuel and diesel fuel produced in the refining process. These products include residual fuels, gas oils, propane, petroleum coke, asphalt and internally produced fuel.

Hydrocracking - A process that uses a catalyst to crack heavy hydrocarbon molecules in the presence of hydrogen. Major products from hydrocracking are distillates, naphtha, propane and gasoline components such as butane.

Hydrotreating - A process that removes sulfur from refined products in the presence of catalysts and substantial quantities of hydrogen to reduce sulfur dioxide emissions that result from the use of the products.

Isomerization - A process that alters the fundamental arrangement of atoms in the molecule without adding or removing anything from the original material. The process is used to convert normal butane into isobutane and normal pentane into isopentane and hexane into isohexane.

2 | Tesoro Corporation | ||

| GLOSSARY OF TERMS | ||

Jobber/Dealer - Retail station owned by a third party that sells products purchased from or through us.

Light Crude Oil - Crude oil with an API gravity greater than 24 degrees. Light crude oil is typically sold at a premium to heavy crude oil.

Manufacturing Costs - Costs associated directly with the manufacturing process including cash operating expenses, but excluding depreciation and amortization.

Mbpd - Thousand barrels per day.

MMBtu - Million British thermal units.

MMMBtu - Billion British thermal units.

MMcf - Million cubic feet.

Multi-Site Operator (“MSO”) - Companies licensed to operate retail stations in which we have a fee or leasehold interest in the property and title to the fuel until sold to the consumer. MSOs operate the non-fuel business at the location and employ the operating personnel.

Naphtha - Refined product used as a gasoline blending component, a feedstock for reforming and as a petrochemical feedstock.

NGLs - Natural gas liquids.

OPEC - Organization of the Petroleum Exporting Countries

Other Feedstocks - Any non-crude raw or semi-finished material, which is further processed in various units of a refinery.

Refined Products - Hydrocarbon compounds, such as gasoline, diesel fuel, jet fuel and residual fuel that are produced by a refinery.

Refining Yield - Volumes of product produced from crude oil and feedstocks.

Reforming - A process that uses controlled heat and pressure with catalysts to rearrange certain hydrocarbon molecules into petrochemical feedstocks and higher octane stocks suitable for blending into finished gasoline.

Residual crude oil - The remainder of the crude oil after gasoline and distillate fuel oils have been extracted through distillation.

SG&A - Selling, general and administrative expenses.

Sweet crude oil - Crude oil containing less than 0.45% sulfur.

Sour crude oil - Crude oil containing greater than 0.45% sulfur.

Tesoro Index - A performance benchmark that uses several crude oils and approximately 8 to 10 products to provide a potentially closer representation of the trends in the available margin. Our actual gross refining margins differ from the Tesoro Index based on the actual slate of crude oil that is run at our refineries and the products we produce or yield. The published Tesoro Index, including a reconciliation of the included components, is available on our website at www.tsocorp.com.

Throughput - The quantity of crude oil and other feedstocks processed at a refinery measured in barrels per day.

Turnaround - The scheduled shutdown of a refinery processing unit for significant overhaul and refurbishment. Turnaround expenditures are capitalized and amortized over the period of time until the next planned turnaround of the unit.

Unit Train - A train consisting of approximately one hundred rail cars containing a single material (such as crude oil) that is transported by the railroad as a single unit from its origin point to the destination, enabling decreased transportation costs and faster deliveries.

Vacuum Distillation - Distillation under reduced pressure, which lowers the boiling temperature of crude oil in order to distill crude oil components that have high boiling points.

December 31, 2016 | 3 | ||

| BUSINESS | ||

As used in this Annual Report on Form 10-K, the terms “Tesoro,” the “Company,” “we,” “us” or “our” may refer to Tesoro Corporation, one or more of its consolidated subsidiaries or all of them taken as a whole. The words “we,” “us” or “our” generally include Tesoro Logistics LP (“TLLP”), a publicly traded limited partnership, and its subsidiaries as consolidated subsidiaries of Tesoro Corporation with certain exceptions where there are transactions or obligations between TLLP and Tesoro Corporation or its other subsidiaries. When used in descriptions of agreements and transactions, “TLLP” or the “Partnership” refers to TLLP and its consolidated subsidiaries.

PART I

ITEM 1. BUSINESS

Tesoro was incorporated in Delaware in 1968. Headquartered in San Antonio, Texas, we are one of the largest independent petroleum refining, logistics and marketing companies in the United States. Our common stock trades on the New York Stock Exchange under the symbol “TSO.”

Our business is organized into three operating segments:

REFINING. Our refining operating segment refines crude oil and other feedstocks into transportation fuels, such as gasoline and gasoline blendstocks, jet fuel and diesel fuel, as well as other products, including heavy fuel oils, liquefied petroleum gas and petroleum coke for sale in bulk markets to a wide variety of customers within our markets.

TLLP. Our logistics operating segment, which is comprised of TLLP’s assets and operations, includes certain crude oil and natural gas gathering assets, natural gas and

NGLs processing assets, and crude oil and refined products terminalling, transportation and storage assets acquired from Tesoro and third parties. The TLLP financial and operational data presented include the historical results of all assets acquired from Tesoro prior to the dates they were acquired by TLLP. The historical results of operations of these assets have been retrospectively adjusted to conform to the current presentation.

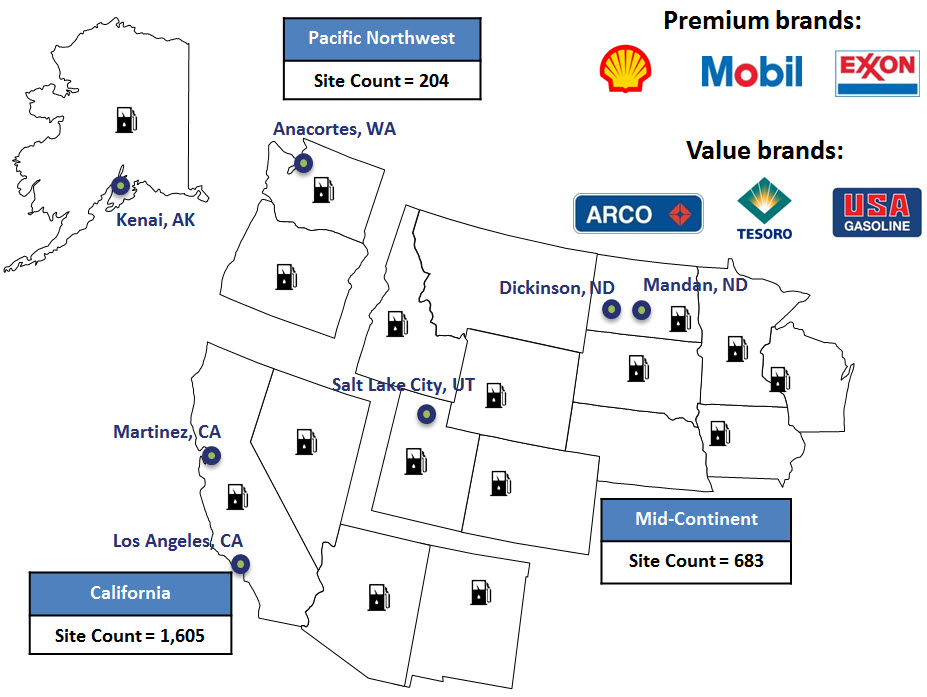

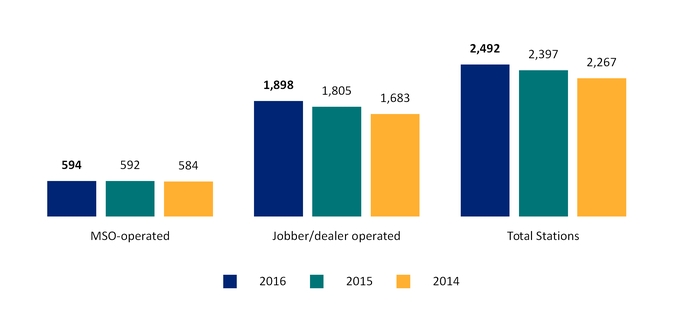

MARKETING. Our marketing segment sells transportation fuels through branded and unbranded channels. The branded business sells transportation fuels using a unique brand portfolio with the ARCO®, Shell®, Exxon®, Mobil®, USA GasolineTM, RebelTM, ThriftyTM and Tesoro® brands across a network of 2,492 retail stations.

See Notes 15 and 19 to our consolidated financial statements in Item 8 for additional information on our operating segments and properties.

REFINING

REFININGOVERVIEW. We currently own and operate seven petroleum refineries located in the western United States with a combined crude oil capacity of 895 Mbpd. Our Refining segment buys and refines crude oil and other feedstocks into transportation fuels that we sell to a wide variety of customers. Demand for gasoline is higher during the spring and summer months than during the fall and winter months in most of our markets due to seasonal changes in vehicle miles traveled. As a result, our operating results for both the Refining and Marketing segments for the first and fourth quarters are typically lower than the second and third quarters.

REGIONS. We currently operate the Refining segment in three separate regions: California, Pacific Northwest and Mid-Continent. Our geographic footprint and integrated logistics and marketing businesses enable our refineries to interact across these regions providing higher asset utilization and lower operating costs while maintaining well-balanced product supplies to better serve our customers.

CALIFORNIA REFINERIES

Crude Oil Capacity / 2016 Throughput (in Mbpd)

Los Angeles: 380 / 364

Martinez: 166 / 143

4 | Tesoro Corporation | ||

| BUSINESS | ||

LOS ANGELES. Our Los Angeles refinery is located on approximately 930 acres in the Carson-Wilmington area of California about 20 miles south of Los Angeles. The refinery’s major processing units include crude distillation, vacuum distillation, delayed coking, hydrocracking, naphtha reforming, hydrotreating, fluid catalytic cracking, butane isomerization and alkylation. The refinery produces a high proportion of transportation fuels, including CARB gasoline and CARB diesel fuel, conventional gasoline, diesel fuel and jet fuel. The refinery also produces heavy fuel oils, liquefied petroleum gas, petroleum coke, calcined coke and electricity.

MARTINEZ. Our Martinez refinery is located on approximately 2,200 acres in Martinez, California about 30 miles east of San Francisco. The refinery’s major processing units include crude distillation, vacuum distillation, delayed coking, hydrocracking, naphtha reforming, hydrotreating, fluid catalytic cracking and alkylation units. The refinery produces a high proportion of transportation fuels, including CARB gasoline and CARB diesel fuel, conventional gasoline and diesel fuel. The refinery also produces liquefied petroleum gas and petroleum coke.

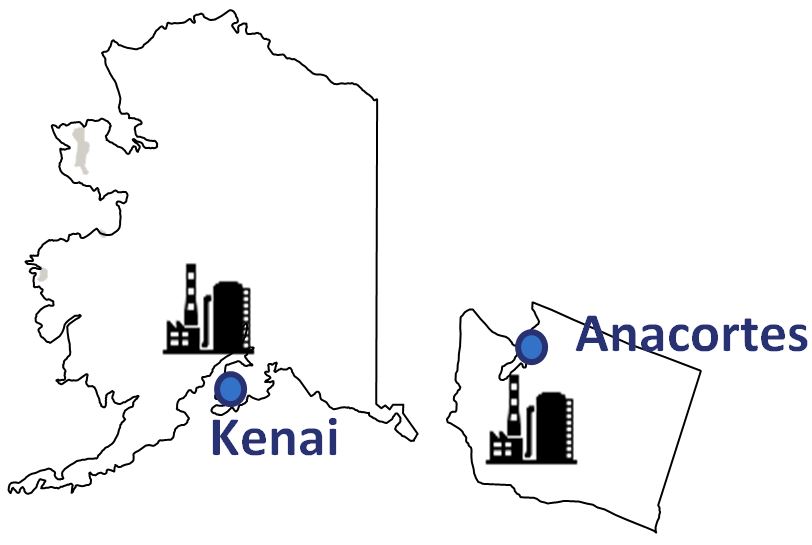

PACIFIC NORTHWEST REFINERIES

Crude Oil Capacity / 2016 Throughput (in Mbpd)

Anacortes: 120 / 124 (a)

Kenai: 72 / 57

(a) Throughput can exceed crude oil capacity due to the processing of other feedstocks in addition to crude oil.

ANACORTES. Our Anacortes refinery is located on approximately 950 acres in northwest Washington about 70 miles north of Seattle. The refinery’s major processing units include crude distillation, vacuum distillation, deasphalting, naphtha reforming, hydrotreating, fluid catalytic cracking, butane isomerization and alkylation units, which enable us to produce a high proportion of transportation fuels such as conventional gasoline, diesel fuel and jet fuel. The refinery also produces heavy fuel oils and liquefied petroleum gas.

KENAI. Our Kenai refinery is located on approximately 450 acres on the Cook Inlet near Kenai, Alaska about 60 miles southwest of Anchorage. The refinery’s major processing units include crude distillation, vacuum distillation, hydrocracking, hydrotreating, naphtha reforming, diesel desulfurizing and light naphtha isomerization units, which produce transportation fuels, including gasoline and gasoline blendstocks, jet fuel and diesel fuel, as well as other products, including heating oil, heavy fuel oils, liquefied petroleum gas and asphalt.

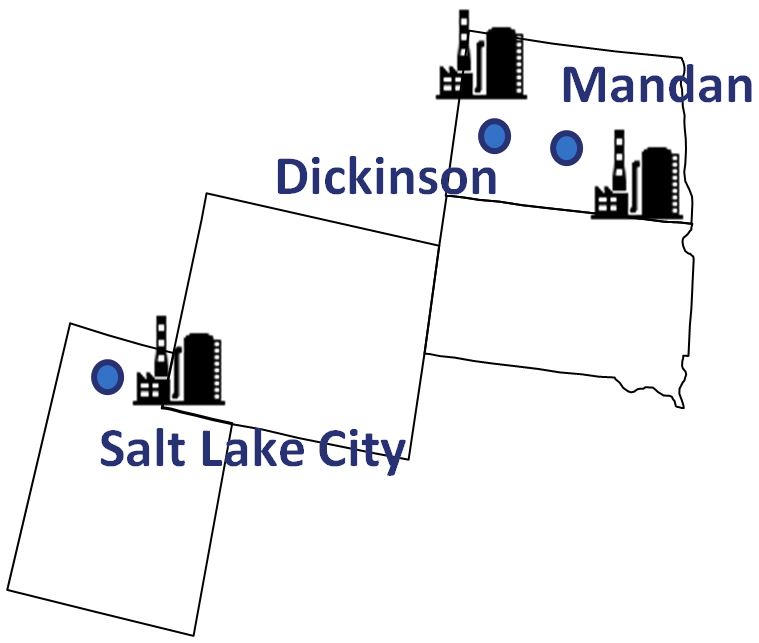

MID-CONTINENT REFINERIES

Crude Oil Capacity / 2016 Throughput (in Mbpd)

Salt Lake City: 63 / 58

Mandan: 74 / 71

Dickinson: 20 / 14 (b)

| (b) | Throughput for the 2016 period for Dickinson measured since our acquisition of the refinery on June 28, 2016. |

SALT LAKE CITY. Our Salt Lake City refinery is located on approximately 150 acres in Salt Lake City, Utah. The refinery’s major processing units include crude distillation, fluid catalytic cracking, naphtha reforming, hydrotreating and alkylation units, which produce transportation fuels, including gasoline, diesel fuel and jet fuel, as well as other products, including heavy fuel oils and liquefied petroleum gas.

MANDAN. Our Mandan refinery is located on approximately 950 acres along the Missouri River near Mandan, North Dakota. The refinery’s major processing units include crude distillation, fluid catalytic cracking, naphtha reforming, hydrotreating and alkylation units, which produce transportation fuels, including gasoline, diesel fuel and jet fuel, as well as other products, including heavy fuel oils and liquefied petroleum gas.

DICKINSON. Acquired during 2016, our Dickinson refinery is located on 318 acres approximately 100 miles west of the Mandan refinery near Dickinson, North Dakota. The refinery produces ultra-low sulfur diesel, naphtha and residuals.

December 31, 2016 | 5 | ||

| BUSINESS | ||

FEEDSTOCK PURCHASES. We purchase crude oil and other feedstocks from domestic and foreign sources either through the spot market or term agreements with renewal provisions and volume commitments. We purchase domestic crude oil produced primarily in North Dakota, Alaska, California, Utah and Wyoming. We purchase foreign crude oil produced in South America, the Middle East, Canada, western Africa and other locations. We lease access to the Trans-Panama pipeline (the “Panama Pipeline”) and several tanks in Panama through agreements expiring in April 2017 that allow us to deliver the crude oil acquired in Africa and the Atlantic region of South America to refineries on the West Coast. We also transport crude oil across the Panama Pipeline for third parties. At December 31, 2016, we held title to approximately 5.2 million barrels of crude oil in transit or in Panama for delivery to our refineries on the West Coast or to third parties.

SOURCES OF OUR CRUDE OIL PURCHASES BASED ON VOLUMES PURCHASED

Our refineries process both heavy and light crude oil. Light crude oil, when refined, produces a greater proportion of higher value transportation fuels such as gasoline, diesel and jet fuel, and as a result is typically more expensive than heavy crude oil. In contrast, heavy crude oil produces more low value by-products and heavy residual oils. These lower value products can be upgraded to higher value products through additional, more complex and expensive refining processes.

PRIMARY CRUDE OIL CHARACTERISTICS AND SOURCES OF CRUDE OIL FOR OUR REFINERIES

| Characteristics | Sources | |||||||||||||||||||||||||||||||

| Sweet | Sour | Residual | Other Feedstocks | Blendstocks | United States | Canada | South & Central America | Asia | Middle East & Africa | |||||||||||||||||||||||

| Los Angeles | ||||||||||||||||||||||||||||||||

| Martinez | ||||||||||||||||||||||||||||||||

| Anacortes | ||||||||||||||||||||||||||||||||

| Kenai | ||||||||||||||||||||||||||||||||

| Mandan | ||||||||||||||||||||||||||||||||

| Salt Lake City | ||||||||||||||||||||||||||||||||

| Dickinson | ||||||||||||||||||||||||||||||||

REFINED PRODUCTS. The total products produced in the refining process are referred to as the refining yield. The refining yield consists primarily of transportation fuels, including gasoline and gasoline blendstocks, jet fuel and diesel fuel, but may also include other products such as heavy fuel oils, liquefied petroleum gas, petroleum coke, calcined coke and asphalt.

6 | Tesoro Corporation | ||

| BUSINESS | ||

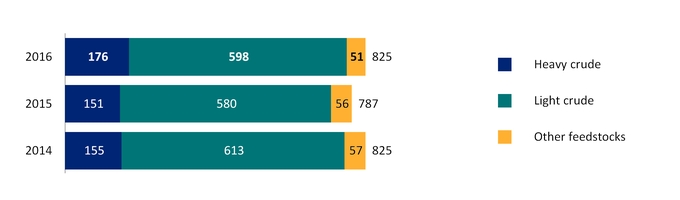

2016 THROUGHPUT VOLUMES AND REFINING YIELDS

| California | Pacific Northwest | Mid-Continent | Total Refining | |||||||||||||||||

| Volume | % | Volume | % | Volume | % | Volume | % | |||||||||||||

| Throughput | ||||||||||||||||||||

| Heavy crude | 170 | 34 | 6 | 3 | — | — | 176 | 21 | ||||||||||||

| Light crude | 304 | 60 | 162 | 90 | 132 | 96 | 598 | 73 | ||||||||||||

| Other feedstocks | 33 | 6 | 13 | 7 | 5 | 4 | 51 | 6 | ||||||||||||

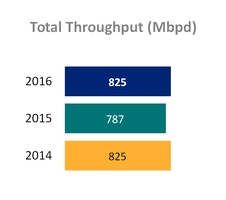

| Total | 507 | 100 | 181 | 100 | 137 | 100 | 825 | 100 | ||||||||||||

| Yield | ||||||||||||||||||||

| Gasoline and gasoline blendstocks | 294 | 53 | 80 | 42 | 77 | 55 | 451 | 51 | ||||||||||||

| Diesel fuel | 113 | 21 | 35 | 19 | 41 | 29 | 189 | 22 | ||||||||||||

| Jet fuel | 71 | 13 | 35 | 19 | 12 | 8 | 118 | 13 | ||||||||||||

| Heavy fuel oils, residual products, internally produced fuel and other (a) | 74 | 13 | 37 | 20 | 11 | 8 | 122 | 14 | ||||||||||||

| Total (b) | 552 | 100 | 187 | 100 | 141 | 100 | 880 | 100 | ||||||||||||

| (a) | The majority of internally produced fuel is consumed during the refining process. |

| (b) | Refined product sales may exceed our yield due to purchased refined products. |

LOGISTICS ASSETS

TERMINAL AND PIPELINES. We transport, store and distribute crude oil, feedstocks and refined products through our terminals and pipelines or terminals and pipelines owned by TLLP and third-parties in our market areas as well as through purchases and exchange arrangements with other refining and marketing companies. Our refineries are integrated with each other via pipelines, terminals and barges. The transportation links that connect our refineries allow for movement of intermediate and finished products, which permit us to optimize our value chain and maximize utilization.

MARINE. We charter tankers to optimize the transportation of crude oil, feedstocks, and refined products to support our refinery system and ensure adequate shipping capacity. Our current U.S.-flag and foreign-flag tanker time charters will expire with varying dates between 2017 and 2021, unless we exercise renewal options. We also time charter tug and barge units and a ship assist tug with varying expiration dates between 2017 through 2018, unless we exercise renewal options. We continually look to optimize our marine fleet and minimize costs, and from time to time we sub-charter vessels in our fleet to third-parties to maintain high utilization. All of our chartered tankers and barges are double-hulled.

RAIL. We maintain a fleet of leased rail cars to transport crude and refined products in support of our refining

operations. In 2016, Tesoro placed an order for 525 additional tank cars for crude oil service that exceed the U.S. Department of Transportation’s 117 standards that were announced in 2015 (“DOT120J200”). These cars started delivering in the second half of 2016 and will complement the 210 DOT120J200 tank cars currently in our fleet. We intend to continue ordering new rail cars that are among the safest available at the time of order and to comply with all relevant regulatory requirements.

REFINED PRODUCT SALES

Our Marketing segment provides a committed outlet for the majority of gasoline produced by our refineries; however, we also sell gasoline and gasoline blendstocks, jet fuel, diesel fuel, heavy fuel oils and residual products in bulk markets in the western U.S. We also opportunistically export gasoline and diesel fuel to certain foreign markets. Our bulk sales are primarily to independent unbranded distributors, other refining and marketing companies, utilities, railroads, airlines and marine and industrial end-users. Our sales include refined products that we manufacture, purchase or receive through exchange arrangements.

SALES OF PURCHASED PRODUCTS. In the normal course of business, we purchase refined products manufactured by others for resale through our marketing and bulk operations to our customers to meet local market demands and fulfill supply commitments. We purchase these refined products, primarily gasoline, jet fuel, diesel fuel and industrial and marine fuel blendstocks, mainly in the spot market.

December 31, 2016 | 7 | ||

| BUSINESS | ||

TLLP

TLLPOVERVIEW. TLLP is a fee-based, growth-oriented Delaware limited partnership formed by us to own, operate, develop and acquire logistics assets. TLLP is a publicly traded limited partnership that is traded on the New York Stock Exchange under the symbol “TLLP.” TLLP’s operations are organized into three businesses: Gathering, Processing, and Terminalling and Transportation. TLLP owns and operates a network of crude oil, refined products and natural gas pipelines, terminals with dedicated and non-dedicated storage capacity for crude oil and refined products, rail facilities with loading and off-loading capabilities, marine terminals and trucking fleets. In addition, TLLP owns and operates natural gas processing and fractionation complexes. TLLP generates revenues by charging fees for gathering crude oil and natural gas, for processing natural gas, and for terminalling, transporting and storing crude oil and refined products. TLLP’s customers experience modest seasonality due to regulatory restrictions, weather conditions and seasonal refined product demand, resulting in higher volumes during the summer months and lower volumes during the winter months. Many of the effects of

seasonality on TLLP’s operating results are mitigated through fee-based commercial agreements that include minimum volume commitments. On January 1, 2017, TLLP acquired crude oil, natural gas and produced water gathering systems and two natural gas processing facilities (“North Dakota Gathering and Processing Assets”). The North Dakota Gathering and Processing Assets include over 650 miles of crude oil, natural gas, and produced water gathering pipelines, 170 MMcf per day of natural gas processing capacity and 18,700 bpd of fractionation capacity in the Sanish and Pronghorn fields of the Williston Basin in North Dakota.

TLLP intends to continue expanding its business through organic growth, including the construction of new assets and increasing the utilization of existing assets, and by acquiring assets from us and third parties. TLLP’s continued expansion of the logistics business is expected to allow us to optimize the value of our assets within the midstream and downstream value chain. Below is a map of TLLP’s strategic assets in relation to our refineries.

8 | Tesoro Corporation | ||

| BUSINESS | ||

GATHERING. TLLP’s Gathering business consists of crude oil, natural gas and produced water gathering systems in the North Dakota Williston Basin/Bakken Shale area (the “Bakken Region”) and the Uinta, Vermillion and greater Green River basins. TLLP’s High Plains System, located in the Bakken Region, gathers and transports crude oil from various production locations in this area for transportation to Tesoro’s North Dakota refinery and other destinations in the Bakken Region, including export rail terminals and pipelines. In addition in the High Plains System, we own and operate a truck-based crude oil gathering operation and a pipeline regulated by the FERC. TLLP’s natural gas gathering systems include the Uinta Basin, Vermillion, Williston, Green River, and Three Rivers gathering systems, its equity method investments in Rendezvous Gas Services, L.L.C., Uintah Basin Field Services, L.L.C. and Three Rivers Gathering, LLC, and two pipelines regulated by the FERC through which it provides natural gas and crude oil transportation services.

TLLP GATHERING - VOLUMES TRANSPORTED IN 2016

| (a) | Also includes barrels that were gathered and delivered into TLLP’s High Plains System by truck. |

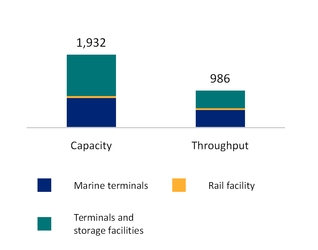

PROCESSING. TLLP’s Processing business consists of natural gas processing and fractionation complexes with a combined processing throughput capacity of approximately 1,600 MMcf/d and fractionation throughput capacity of approximately 34 Mbpd. TLLP processes gas for certain producers under keep-whole processing agreements. Under a keep-whole agreement, a producer transfers title to the NGLs produced during gas processing and the processor, in exchange, delivers to the producer natural gas with a BTU content equivalent to the NGLs removed. The operating margin for these agreements is determined by the spread between NGLs sales prices and the price paid to purchase the replacement natural gas (“Shrink Gas”). We are party to a five-year agreement, entered into in December 2014 and amended in February 2016, with TLLP that substantially transfers the commodity risk exposure associated with these keep-whole processing agreements from TLLP to us (the “Keep-Whole Commodity Agreement”). Under the Keep-Whole Commodity Agreement, we pay TLLP a fee to process NGLs related to keep-whole agreements and deliver Shrink Gas to the producers on behalf of TLLP. TLLP pays us a marketing fee in exchange for assuming the commodity risk.

As of 2016, pricing under this agreement is subject to a tiered pricing structure with pricing for a base level of NGLs production and pricing for incremental volumes over 315,000 gallons per day. The pricing for both the base and incremental volumes are subject to revision each year.

TERMINALLING AND TRANSPORTATION. TLLP’s Terminalling and Transportation business consists of: crude oil and refined products terminals and storage facilities in the western and midwestern U.S. that are supplied by Tesoro-owned and third-party pipelines, trucks and barges; marine terminals in California that load and unload vessels; pipelines that transport products and crude oil from our refineries to nearby facilities in Salt Lake City and Los Angeles; a 50% fee interest in a pipeline that transports jet fuel from our Los Angeles refinery to the Los Angeles International Airport; a regulated common carrier products pipeline running from Salt Lake City, Utah to Spokane, Washington and a jet fuel pipeline to the Salt Lake City International Airport (the “Northwest Products Pipeline”); a rail-car unloading facility in Washington that receives crude oil transported on unit trains we lease; a petroleum coke handling and storage facility in Los Angeles that handles and stores petroleum coke from our Los Angeles refinery; and a regulated common carrier refined products pipeline system connecting our Kenai refinery to Anchorage, Alaska.

TLLP TRANSPORTATION VOLUME (in Mbpd)

TLLP TERMINALLING THROUGHPUT (in Mbpd)

December 31, 2016 | 9 | ||

| BUSINESS | ||

MARKETING

MARKETINGOur Marketing segment sells gasoline and diesel fuel in the western U.S. through branded and unbranded channels. Our branded operations include transportation fuel sales through retail stations and agreements with third-party dealers and distributors. Our unbranded business includes volumes sold through agreements with third-party distributors/operators. Our branded and unbranded

channels provide a committed outlet for the majority of the gasoline produced by our refineries. The map below shows the approximate number of retail outlets by region included in our Marketing segment’s branded network of retail stations under the ARCO®, Shell®, Exxon®, Mobil®, USA GasolineTM, RebelTM, ThriftyTM and Tesoro® brands as of December 31, 2016.

COMPETITION

The refining industry is highly competitive and includes a diverse set of competitors. Our primary competitors are typically the other local refining, marketing and logistics companies within the regions we operate, but may include companies from across the globe depending on the market environment. The competitors range from small independently owned businesses to some of the largest integrated multi-national oil companies in the world.

We obtain all of our crude oil from third-party sources and compete in the world market for the crude oil and feedstocks we process, and for the customers who purchase refined products. The availability and cost of crude oil and other feedstocks, as well as the prices of the products we produce, are heavily influenced by global supply and demand dynamics.

10 | Tesoro Corporation | ||

| BUSINESS | ||

We compete with other refiners and with importers for customers in most of our market areas including sales of our distillate production through wholesale and bulk channels. Competition and concentrations specific to each of our refineries are:

| • | Our Martinez, Los Angeles and Anacortes refineries compete with several refiners in the U.S., Canada and throughout the Pacific Rim; |

| • | Our Kenai refinery competes with two other in-state refineries along with refineries on the West Coast and in Asia. Our jet fuel sales in Alaska are concentrated in Anchorage, where we are one of the principal suppliers at the Anchorage International Airport; and |

| • | Our mid-continent refineries in Mandan, Dickinson, and Salt Lake City compete with supplies provided from refineries in surrounding states and pipeline supply from the Midwest and Gulf Coast regions. |

We sell gasoline through our network of branded retail stations as well as on an unbranded, or wholesale, and bulk basis. Our marketing operations compete with other independent marketers, integrated oil companies and high-volume retailers. Competitive factors that affect Marketing include product price, location, convenience and brand appeal.

TLLP’s gathering business competes with a number of transportation, midstream, and trucking companies for the gathering and transportation of crude oil and natural gas, as applicable, in the areas in which they operate. TLLP’s gathering business competes for opportunities to build gathering lines from producers or other pipeline companies, to provide accessible and flexible service to producers, and facilitate the transportation of crude oil and natural gas to applicable markets. In processing, TLLP competes with midstream companies and producers primarily based on reputation, commercial terms, reliability, service levels, flexibility, access to markets, location, available capacity, capital expenditures and fuel efficiencies. TLLP’s terminalling and transportation business competes predominately with independent terminal and pipeline companies, integrated petroleum companies, refining and marketing companies and distribution companies with marketing and trading arms. Competition in particular geographic areas is affected primarily by the volumes of refined products produced by refineries located in those areas, the availability of refined products and the cost of transportation to those areas from refineries located in other areas.

HEALTH & SAFETY

Improving personal and process safety is a core value at Tesoro. We are committed to operating our refineries, pipelines, retail stations and other facilities in a manner that promotes the health and safety of our employees, our customers and the communities where we do business.

Our Environmental, Health & Safety (EH&S) policy in conjunction with our Operational Excellence Management System establish metrics, expectations and responsibilities for achieving our goals for these key areas:

PERSONAL SAFETY. At Tesoro, we consider the health and safety of our people a core value and an essential area of focus of our leadership. We strive to instill a culture of personal responsibility among our employees and contractors by setting clear expectations around our safety standards and policies. We conduct regular audits, assessments and program reviews to ensure these practices are being followed and to identify improvements to enhance our workplace safety.

PROCESS SAFETY. Our facilities are designed, constructed, operated and maintained to ensure safe work environments. To maintain the integrity of our operating systems, we enforce a disciplined framework that includes comprehensive design, engineering, operating and maintenance practices. We use industry-recognized methodologies to assure process safety and asset integrity and reduce the risk of incidents.

TRANSPORTATION SAFETY. We are committed to conducting business in a manner that promotes the safety of our employees and those living around us. This includes the operations of our pipelines, storage facilities, rail cars and trucking fleet, which transports crude oil and other feedstock, as well as fuel and other products. We proactively led the industry in the safe transport of crude oil via rail by working collaboratively with tank car manufacturers to develop enhanced rail cars (120J) that surpass regulatory standards.

December 31, 2016 | 11 | ||

| BUSINESS | ||

GOVERNMENT REGULATION AND LEGISLATION

REGULATORY CONTROLS AND EXPENDITURES. Like other companies engaged in similar businesses, we are subject to extensive and frequently changing federal, state, regional and local laws, regulations and ordinances relating to the environment, including those governing emissions or discharges to land, air and water, the handling and disposal of solid and hazardous wastes and the remediation of contamination. While we believe our facilities are in substantial compliance with current requirements, we will continue to engage in efforts to meet new legislative and regulatory requirements applicable to our operations. Compliance with these laws and regulations may require us to make significant expenditures.

For example:

| • | The U.S. Environmental Protection Agency (“EPA”) has promulgated multiple regulations to control greenhouse gas emissions under the Federal Clean Air Act. The first of these regulations, finalized on April 1, 2010, set standards for the control of greenhouse gas emissions from light trucks and cars. The U.S. Congress may also consider legislation regarding greenhouse gas emissions in the future. |

| • | The Energy Independence and Security Act of 2007 mandates the blending of increasing amounts of renewable fuels in the supply of transportation fuels used domestically. This use of renewable fuels is required of all manufacturers and importers of transportation fuels sold domestically. The EPA implemented the second renewable fuel standard (“RFS2”) through regulation and RFS2 requires transportation fuel manufacturers to provide proof of purchase of these renewable fuels. The costs associated with RFS2 compliance are uncertain and fluctuate with market dynamics. |

| • | The EPA finalized amendments to the Clean Air Act Risk Management Planning regulations in 2016 significantly expanding the regulatory requirements. |

| • | The Department of Transportation (“DOT”) issued new regulations in 2015 governing the design of rail cars used to transport petroleum and other materials. |

| • | In California, Senate Bill 32 (“SB 32”) set a new greenhouse gas emission reduction requirement of 40% below 1990 levels by 2030. Assembly Bill (“AB 197”) mandated direct emission reductions of greenhouse gases from large stationary sources such as our refineries. Assembly Bill 32 (“AB 32”), previously created a statewide cap on greenhouse gas emissions now replaced by SB 32 but also created a low carbon fuel standard, which requires a 10% reduction in the carbon intensity of fuels by 2020. |

| • | In California, the Board for the South Coast Air Quality Management District passed amendments to the Regional Clean Air Incentives Market (“RECLAIM”) on December 4, 2015. The RECLAIM Amendments became effective in 2016 and required a staged reduction of Nitrogen Oxides through 2022. |

| • | In California, new and expanded Process Safety Management and Refinery Safety and Prevention regulations were proposed in 2016 in response to recommendations made in 2014 by the Governor’s Interagency Refinery Safety Working Group. |

The impact of these and other regulatory and legislative developments is likely to result in increased compliance costs, additional operating restrictions on our business and an increase in the cost of the products we manufacture. Depending on market conditions, we may attempt to pass these costs on to consumers. If that is not possible, the changes could have an adverse impact on our financial position, results of operations, and liquidity. We cannot currently determine the amounts of such future impacts. For additional information regarding our environmental matters see “Environmental and Other Matters” in Item 7.

OIL SPILL PREVENTION AND RESPONSE. We operate in environmentally sensitive coastal waters, where tanker, pipeline, rail cars and other petroleum product transportation operations are regulated by federal, state and local agencies and monitored by environmental interest groups. The transportation of crude oil and refined products involves risk and subjects us to the provisions of the Federal Oil Pollution Act of 1990 and related state requirements, which require that most petroleum refining, transport and storage companies maintain and update various oil spill prevention and oil spill contingency plans. Our spill prevention plans and procedures are frequently reviewed and modified to prevent releases and to minimize potential impacts to land and water should a release occur. We have submitted these plans and received federal and state approvals necessary to comply with the Federal Oil Pollution Act of 1990 and related regulations. At our facilities adjacent to water, federally certified Oil Spill Response Organizations (“OSROs”) are available to respond to a spill on water from above ground storage tanks or pipelines. We have contracts in place to ensure support from the respective OSROs for spills in both open and inland waters, as well as on land.

We currently charter tankers to ship crude oil from foreign and domestic sources to our California, Washington and Alaska refineries. The tanker owners contract with OSROs to comply with federal, state and local requirements, except in Alaska where we contract with the OSROs. The OSROs are capable of responding to an oil spill equal to the greatest tanker volume delivering crude oil to our refineries. Those volumes range from 350,000 barrels to two million barrels.

12 | Tesoro Corporation | ||

| BUSINESS | ||

We have entered into spill-response contracts with various OSROs to provide spill-response services, if required, to respond to a spill of oil originating from our facilities. We have spill-response agreements in Alaska with Cook Inlet Spill Prevention and Response, Incorporated and with Alyeska Pipeline Service Company. We also have entered into contracts with Marine Spill Response Corporation for the San Francisco Bay, Puget Sound, the Port of Los Angeles and the Port of Long Beach, and the Clean Rivers Cooperative, Inc. for the Columbia River, and Bay West, Inc. in our Mid-Continent region. These OSROs are capable of responding to an oil spill on water equal to the greatest volume above ground storage tank at our facilities or pipelines. Those volumes range from 50,000 to 600,000 barrels. We also contract with one spill-response organization outside the U.S. to support our shipments in foreign waters. In addition, we contract with various spill-response specialists to ensure appropriate expertise is available for any contingency. We believe these contracts provide the additional services necessary to meet or exceed all regulatory spill-response requirements and support our commitment to environmental stewardship.

The OSROs we contract with have the highest available rating and certification from the U.S. Coast Guard and are required to annually demonstrate their response capability to the U.S. Coast Guard and state agencies. We maintain our own spill-response resources to mitigate the impact of a spill from a tanker at our refineries until an OSRO can deploy its resources. Our spill response capability meets the U.S. Coast Guard and state requirements to either deploy on-water containment equipment two and one-half times the length of a vessel at our dock or have smaller vessels available.

The services provided by the OSROs principally consist of operating response-related equipment, managing certain aspects of a response and providing technical expertise. The OSROs provide various resources in response to an oil spill. The resources include dedicated vessels that have skimming equipment to recover oil, storage barges to temporarily store recovered oil, containment boom to control the spread of oil on water and land and to protect shorelines, and various pumps and other equipment supporting oil recovery efforts and the protection of natural resources. The OSROs have full-time personnel and contract with third parties to provide additional personnel when needed.

As a general matter, our agreements with these organizations do not contain specific physical or financial limitations. General physical limitations of these organizations would include the geographical area for which services are available and the amount of resources available at the initiation of a request for services or the duration of response and recovery efforts.

Additionally, we require all tankers and barges engaged in moving crude oil, heavy and finished products to be double hulled. All vessels used by us to transport crude oil and refined products over water are examined or evaluated and subject to our approval prior to their use.

RAIL CAR SAFETY. Tesoro maintains a fleet of leased rail cars to transport crude and support our refining operations. Generally, rail operations are subject to federal, state and local regulations. Over the last year, Tesoro has added over 700 new DOT120J200 tank cars to its crude oil fleet. These cars exceed the new federal standards issued by the DOT during 2015. The new DOT regulations allow for an orderly phase out or retrofit of previous generation rail cars. In 2016, Tesoro retrofit 250 cars while phasing out 500 older CPC-1232 tank cars. Tesoro will continue to comply with all regulatory requirements and order only new rail cars that are among the safest and most robust available at the time of order. TLLP rail operations are limited to loading and unloading rail cars at its facilities. TLLP believes its entire rail car loading and unloading operations meet or exceed all applicable regulations.

PIPELINE SAFETY. Our pipelines, gathering systems and terminal operations, including those owned by TLLP, are subject to increasingly strict safety laws and regulations. The transportation and storage of refined products, natural gas and crude oil involve a risk that hazardous liquids may be released into the environment, potentially causing harm to the public or the environment. The DOT, through the Pipeline and Hazardous Materials Safety Administration and state agencies, enforce safety regulations with respect to the design, construction, operation, maintenance, inspection and management of our pipeline and storage facilities.

REGULATION OF PIPELINES. Operations on portions of our pipelines are regulated by state agencies in Alaska and California. In addition, TLLP owns and operates crude oil, refined product and natural gas pipelines, which are common carriers regulated by various federal, state and local agencies. The FERC regulates interstate transportation on TLLP’s High Plains System, Northwest Products Pipeline and natural gas pipeline under the Interstate Commerce Act, the Energy Policy Act of 1992 and the rules and regulations promulgated under those laws.

Federal regulation of interstate pipelines extends to such matters as rates, services, and terms and conditions of service; the types of services offered to customers; the certification and construction of new facilities; the acquisition, extension, disposition or abandonment of facilities; the maintenance of accounts and records; relationships between affiliated companies; the initiation and continuation of services; market manipulation in connection with interstate sales, purchases or transportation of commodities; and participation by interstate pipelines in cash management arrangements.

December 31, 2016 | 13 | ||

| BUSINESS | ||

The intrastate operation of TLLP’s Alaska pipeline is regulated by the Regulatory Commission of Alaska. The state regulatory authorities require that we notify shippers of proposed tariff increases to provide the shippers an opportunity to protest the increases. In addition to challenges to new or proposed rates, challenges to existing intrastate rates are permitted by complaint of an interested person or by independent action of the appropriate regulatory authority. The intrastate operations of TLLP’s High

Plains System in North Dakota are regulated by the North Dakota Public Service Commission. Applicable state law requires that pipelines operate as common carriers, that access to transportation services and pipeline rates be non-discriminatory, that if more crude oil is offered for transportation than can be transported immediately the crude oil volumes transported be apportioned equitably and that pipeline rates be just and reasonable.

WORKING CAPITAL

We fund our business operations through a combination of available cash and equivalents and cash flows generated from operations. In addition, our revolving lines of credit are available for additional working capital needs. For additional information regarding working capital see “Capital Resources and Liquidity” in Item 7.

EMPLOYEES

We had more than 6,300 full-time employees at December 31, 2016, approximately 2,090 of whom are full-time represented union employees covered by collective bargaining agreements. The agreements for approximately 1,750 of these employees will expire on February 1, 2019, the agreements for approximately 80 of these employees will expire on March 1, 2017, and the agreements for the remaining represented employees expire on May 1, 2019.

EXECUTIVE OFFICERS

The following is a list of our executive officers, their ages and their positions at Tesoro, effective as of February 21, 2017.

There are no family relationships among the officers listed, and there are no arrangements or understandings pursuant to which any of them were elected as officers. Officers are elected annually by our Board of Directors (the “Board”) in conjunction with the annual meeting of stockholders. The term of each office runs until the corresponding meeting of the Board in the next year or until a successor has been elected or qualified. Positions held for at least the past five years for each of our executive officers are described below (positions, unless otherwise specified, are with Tesoro).

Gregory J. Goff, 60, was named President and Chief Executive Officer in May 2010 and Chairman of our Board of Directors in December 2014. Mr. Goff also serves as Chief Executive Officer and Chairman of the Board of Directors of Tesoro Logistics GP, LLC (“TLGP”), the general partner of TLLP. Since March 2015, Mr. Goff has served as Chairman of the Board of the American Fuel & Petrochemical Manufacturers. Before joining Tesoro, he served as Senior Vice President, Commercial for ConocoPhillips Corporation (“ConocoPhillips”), an international, integrated energy company, from 2008 to 2010. Mr. Goff held various positions at ConocoPhillips from 1981 to 2008, including Managing Director and CEO of Conoco JET Nordic from 1998 to 2000; Chairman and Managing Director of Conoco Limited, a UK-based refining and marketing affiliate, from 2000 to 2002; President of ConocoPhillips Europe and Asia Pacific downstream operations from 2002 to 2004; President of ConocoPhillips specialty businesses and business development from 2006 to 2008; and President of ConocoPhillips specialty businesses and business development from 2006 to 2008. Mr. Goff serves as Chairman of the Board of the American Fuel and Petrochemical Manufacturers trade association and on the National Advisory Board of the University of Utah Business School. Previously, Mr. Goff served on the board of Chevron Phillips Chemical Company and was a member of the upstream and downstream committees of the American Petroleum Institute. In addition, Mr. Goff has public company experience from his prior service on the board of directors of DCP Midstream GP, LLC. Mr. Goff received a Bachelor’s degree in Science and Master’s degree in Business Administration from the University of Utah.

Keith M. Casey, 50, was named Executive Vice President, Marketing and Commercial in August 2016. Prior to his current role, Mr. Casey served as Executive Vice President, Operations, since May 2014. Prior to that, he served as Senior Vice President, Strategy and Business Development beginning in April 2013. Prior to joining Tesoro, Mr. Casey served as Vice President, BP Products North America, Texas City Refinery beginning in September 2006.

14 | Tesoro Corporation | ||

| BUSINESS | ||

Kim K.W. Rucker, 50, joined Tesoro in March 2016 as Executive Vice President, General Counsel and Secretary. Ms. Rucker also serves as Executive Vice President and General Counsel for TLGP. Before joining Tesoro, Ms. Rucker served as Executive Vice President, Corporate and Legal Affairs, General Counsel and Corporate Secretary of Kraft Food Groups, Inc., a food and beverage company (now The Kraft-Heinz Company), from October 2012 to July 2015. She joined Mondelēz International as Executive Vice President, Corporate & Legal Affairs, Kraft Foods North America in September 2012. Prior to that, she served as Senior Vice President, General Counsel and Chief Compliance Officer of Avon Products, Inc., a global manufacturer of beauty and related products, beginning in March 2008 and as Corporate Secretary in February 2009. Ms. Rucker also served as Senior Vice President, Secretary and Chief Governance Officer of Energy Future Holdings Corp. (formerly TXU Corp.), an energy company, from 2004 to 2008. She was Corporate Counsel for Kimberly-Clark Corporation and a Partner in the Corporate & Securities group at Sidley Austin LLP in Chicago. Ms. Rucker serves on the board of directors of Lennox International Inc. She holds a bachelor of business administration degree in economics from the University of Iowa, a law degree from the Harvard Law School and a master’s in public policy from the John F. Kennedy School of Government at Harvard University.

Steven M. Sterin, 45, was named Executive Vice President and Chief Financial Officer in August 2014. In August 2016, he also assumed leadership of corporate development in support of our growth plans. Mr. Sterin also serves as Executive Vice President and Chief Financial Officer of TLGP. Prior to joining Tesoro, Mr. Sterin served as the Senior Vice President and Chief Financial Officer of Celanese Corporation, a global technology and specialty material company, from July 2007 until May 2014 and continued to serve as an employee until August 2014. From December 2010 through January 2013, he was president of Celanese’s Advanced Fuel Technologies business. Mr. Sterin joined Celanese in 2003 as Director of Finance and Controller for the company’s chemical business and also served as Corporate Controller and Principal Accounting Officer before being appointed CFO. Before Celanese, Mr. Sterin spent six years with global chemicals company Reichhold, Inc. in a variety of financial positions, including Director of Tax and Treasury in the Netherlands, Global Treasurer and Vice President of Finance for one of the company’s divisions in North Carolina. Mr. Sterin holds a Master of Professional Accounting degree and a Bachelor of Business Administration degree in accounting, which he earned concurrently at the University of Texas at Austin. He is also a certified public accountant in Texas.

Cynthia J. Warner, 58, was named Executive Vice President, Operations in August 2016. Prior to her current role, Mrs. Warner served as Executive Vice President, Strategy and Business Development since October 2014. Before joining Tesoro, Mrs. Warner served as President, Chief Executive Officer, and Chairman of the Board of Sapphire Energy beginning in 2009.

Blane W. Peery, 50, was named Vice President and Controller of both Tesoro and TLGP in November 2016. Prior to that, he served as Vice President, Process Excellence and Chief Information Officer from February 2015 through October 2016. Mr. Peery has experience leading global accounting organizations, business planning and analysis functions, supply chain groups, global shared services including finance, human resources, information technology, and mergers and acquisitions integration. From March 2014 to February 2015, Mr. Peery served as VP, Global Business Services at Mylan N.V., a leading global pharmaceutical company. Prior to that he worked for Celanese Corporation, a global technology and specialty materials company, for over 20 years in roles with increasing responsibility, including positions as its Vice President, Global Business Services from October 2012 to March 2014, its Vice President, Supply Chain from October 2011 to October 2012 and its first-ever Global Accounting Director. Mr. Peery began his career as an auditor for PricewaterhouseCoopers and is a Certified Public Accountant (CPA). Mr. Peery holds a Bachelor of Business Administration degree in accounting, which he earned at the University of Texas at Austin.

Stephan E. Tompsett, 40, was named Vice President, Treasurer and Credit in August 2016. From May 2015 through August 2016, he served as Chief Financial Officer, Logistics of Tesoro Companies, Inc. Prior to joining Tesoro, Mr. Tompsett served in a variety of finance roles at Energy Transfer Partners from February 2011 to May 2015. From September 2008 to January 2011, he was Vice President, Corporate Development at Synthesis Energy Systems. He was an associate at JPMorgan from July 2005 to August 2008. Mr. Tompsett holds a Master of Business Administration degree from the University of Texas at Austin - Red McCombs School of Business and a Bachelors of Science degree in biology and mathematics from the University of Texas at Austin.

WEBSITE ACCESS TO REPORTS AND OTHER INFORMATION

Our Internet website address is http://www.tsocorp.com. Information contained on our Internet website is not part of this Annual Report on Form 10-K.

Our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and other public filings with the Securities and Exchange Commission (“SEC”) are available, free of charge, on our website as soon as reasonably practicable after we file them with, or furnish them to, the SEC. You may also access these reports on the SEC’s website at http://www.sec.gov.

December 31, 2016 | 15 | ||

| RISK FACTORS | ||

ITEM 1A. RISK FACTORS

Our proposed acquisition of Western Refining is subject to significant risks and uncertainties.

As described elsewhere in this Annual Report on Form 10-K, we have entered into a merger agreement, dated as of November 16, 2016, with Western Refining, Inc. (“Western Refining”) pursuant to which, on the terms and subject to the conditions included therein, we have agreed to acquire Western Refining. Our ability to complete the proposed acquisition on a timely basis or at all is subject to numerous risks and uncertainties, including, but not limited to, the following:

| • | we may not obtain required shareholder approval; |

| • | we may not obtain required regulatory approvals or receipt of regulatory approvals may take longer than expected or may impose conditions to the proposed acquisition that are not presently anticipated or cannot be met; |

| • | conditions to the proposed acquisition may not be fulfilled in a timely manner or at all; or |

| • | unforeseen events and those beyond our control. |

The proposed acquisition also subjects us to business uncertainties while it is pending and places other restrictions on our business, including, without limitation:

| • | our ability to attract, retain and motivate key personnel until the proposed acquisition is completed and for a period of time thereafter; |

| • | our ability to maintain our relationships with our customers and other third parties we transact with, who may seek to change their existing business relationships with us as a result of the proposed acquisition; and |

| • | restrictions imposed on us under the merger agreement that prohibit us from entering into certain corporate transactions and taking other specified actions without the consent of Western Refining, which may prevent us from pursuing attractive business opportunities that may arise prior to the completion of the acquisition. |

We have incurred and expect to continue to incur significant transaction and acquisition-related costs associated with the proposed acquisition. These, as well as other unanticipated costs and expenses could have a material adverse effect on our financial condition and operating results. Combining our businesses may be more difficult, costly or time consuming than expected. Integration involves numerous challenges, including our ability to integrate our businesses in an efficient and timely manner, integrate our systems and controls as well as integrate our relationships with our customers, suppliers, employees and other third parties. The integration process may, for us and Western Refining, result in the loss of key employees, the disruption of ongoing businesses or inconsistencies in standards, controls, procedures and policies.

The success of the proposed acquisition will depend on, among other things, our ability to realize the anticipated benefits and cost savings from combining our and Western Refining’s businesses in a manner that facilitates growth opportunities and realizes anticipated synergies and costs savings. These anticipated benefits and cost savings may not be realized fully or at all, or may take longer to realize than expected or could have other adverse effects that we do not currently foresee.

The volatility of crude oil prices, refined product prices and natural gas and electrical power prices may have a material adverse effect on our cash flow and results of operations.

Our refining margins are influenced by the price of our refining feedstocks-crude oil and other feedstocks-and the price of our refined products. These prices often move independently of each other, which can negatively impact our margins, earnings or cash flows. In recent years, prices have fluctuated significantly due to global and local factors that are beyond our control, including:

| • | production and availability of foreign and domestic crude oil and refined products; |

| • | production controls set and maintained by the members of the Organization of the Petroleum Exporting Countries; |

| • | transportation infrastructure availability, local market conditions, operation levels of other refineries in our markets, and the import or export of crude and refined products; |

| • | political instability, threatened or actual terrorist incidents, acts of war, and other global political conditions; |

| • | domestic and foreign governmental regulations and taxes; |

| • | the price, availability and efficiency of competing energy sources; |

| • | local, regional, national and worldwide economic conditions; and |

| • | weather conditions, hurricanes or other natural disasters. |

16 | Tesoro Corporation | ||

| RISK FACTORS | ||

Some of these factors can vary by region and may change quickly, adding to market volatility, while others may have longer-term effects. The long-term effects of these and other factors on prices for crude oil, refinery feedstocks and refined products are uncertain and could negatively impact our margins, earnings or financial condition.

The short-term effects of these fluctuations could affect our margins, earnings and cash flows. We purchase our refinery feedstocks weeks before manufacturing and selling the refined products. Price level changes during the period between purchasing feedstocks and selling the refined products could affect our margins, earnings or cash flows. In addition, we purchase refined products manufactured by others to sell to our customers. If we are unable to manage our commodity exposure risk, it could affect our business, financial condition and results of operations. Lower refining margins may reduce the amount of refined products we produce, which may reduce our revenues, income from operations or cash flows. Significant reductions in margins could require us to reduce our capital expenditures or impair the carrying value of our assets.

Volatile prices for natural gas and electricity used by our refineries and other operations affect manufacturing and operating costs. Natural gas and electricity prices have been, and will continue to be, affected by supply and demand for fuel and utility services in both local and regional markets. In addition, the volume of crude oil, refined products, natural gas and NGLs that TLLP distributes and stores at its terminals, transports and processes depends substantially on our and other customers’ profit margins, the market price of crude oil, natural gas, NGLs and other refinery feedstocks, and product demand.

A substantial change to fiscal or tax policies may adversely affect our business.

Recent events have given rise to a heightened possibility of a substantial change to fiscal and tax policies, which may include comprehensive tax reform. We cannot predict the impact these changes will have on our business; however, it is possible that these changes could adversely affect our business, our cash flows, our profitability, and our ability to compete domestically and internationally. Until we know what changes are enacted, we will not know the type or extent of the effects on our business.

We may be unsuccessful in integrating the operations of the assets we have acquired or may acquire in the future, or in realizing all or any part of the anticipated benefits of any such acquisition.

If we are unable to successfully integrate our acquisitions into our business, we may never realize their expected benefits. With each acquisition, we may discover unexpected costs, environmental liabilities, delays, or lower than expected cost savings or synergies. In addition, we may be unable to successfully integrate the diverse company cultures, retain key personnel, apply our expertise to new competencies, or react to adverse changes in commodity prices or industry conditions.

We cannot predict with certainty the benefits of these acquisitions, which often constitute multi-year endeavors. For example, our proposed acquisition of Western Refining is uncertain and, if completed, will require substantial capital during 2017 and later years. If we are unable to realize all or part of the projected benefits from this or other acquisitions within our expected timeframes, our business, results of operations and financial condition may suffer.

We are subject to interruptions of supply and increased costs as a result of our reliance on logistics assets for the transportation of crude oil, feedstocks and refined products within our business.

Our subsidiaries own and operate seven refineries in the western United States, which refine crude oil and other feedstocks into refined products for sale to a wide variety of markets. We rely on a variety of logistics assets to transport crude oil, feedstocks and refined products, including, but not limited to, marine vessels, marine terminals, rail, pipelines, product terminals, storage tanks and trucks. Some of these assets are owned and operated by third-parties. In particular, losing access to certain assets owned by TLLP could halt production at some of our refineries. Accidents, natural disasters, government regulation, third-party actions or other events outside of our control could impede our use or increase the cost of using these assets, which could have a material adverse effect on our financial condition and results of operations.

Adverse changes in global economic conditions and the demand for transportation fuels may impact our business and financial condition in ways that we currently cannot predict.

Our business is affected by the strength of the U.S. and global economies, and the risk of global economic downturn continues. Prolonged downturns could result in declines in consumer and business confidence and spending as well as increased unemployment and reduced demand for transportation fuels. These conditions may decrease the creditworthiness of our suppliers, customers and business partners, which could interrupt or delay our suppliers’ performance of our contracts, reduce or delay customer purchases, delay or prevent customers from obtaining financing to purchase our products, or result in bankruptcy of customers or business partners. Any of these events may adversely affect our cash flow, profitability and financial condition.

December 31, 2016 | 17 | ||

| RISK FACTORS | ||

Our business includes selling products in international markets, and we are subject to risks of doing business on a global level.

We sell some of our products internationally, primarily to markets in Mexico, South America and Asia. Our operating results or financial condition could be negatively impacted by disruptions in any of these markets, including economic instability, restrictions on the transfer of funds, duties and tariffs, transportation delays, import and export controls, changes in governmental policies, labor unrest and changing regulatory and political environments. In addition, if trade relationships deteriorate with these countries, if existing trade agreements are modified or terminated, or if taxes, border adjustments or tariffs make trading with these countries more costly, it could have a material adverse effect on our business.

The availability and cost of renewable identification numbers could have an adverse effect on our financial condition and results of operations.

The RFS2 requires refiners to add annually increasing amounts of “renewable fuels” to their petroleum products or to purchase credits, known as renewable identification numbers (“RINs”), in lieu of such blending. Due to regulatory uncertainty and in part due to the nation’s fuel supply approaching the “blend wall” (the 10% ethanol limit prescribed by most automobile warranties), the price and availability of RINs has been volatile.

While we generate RINs by blending renewable fuels manufactured by third parties, we purchase RINs on the open market to comply with the RFS2. We cannot predict the future prices of RINs, and the costs to obtain the necessary RINs could be material. Our financial condition and results of operations could be adversely affected if we are unable to pass the cost of compliance on to our customers, pay significantly higher prices for RINs, and generate or purchase RINs to meet RFS2 mandated standards.

Meeting the requirements of, including the cost to comply with evolving environmental, health and safety laws and regulations including those related to climate change could materially affect our performance, financial condition and results of operations.