Additionally, general market and economic conditions or governmental actions generally may inhibit our successful integration of ClosetMaid.

Further, we will acquire the Business with the expectation that the ClosetMaid Acquisition will result in various benefits including, among other things, benefits relating to enhanced revenues, and increased earnings and cash flows. We believe that this acquisition will strengthen our Home & Building Products’ brand portfolio, expand our manufacturing, distribution and global sourcing capabilities and provide opportunities to leverage the segment. Additionally, we expect to derive potential benefits resulting from increased scale in our Home and Building Products segment which could result in cost savings from increased purchasing power, cross selling opportunities, internal sourcing opportunities, and technological and other operating efficiences. Achieving the anticipated benefits of this acquisition is subject to a number of uncertainties, including whether we can integrate ClosetMaid in an efficient and effective manner, whether or not the expected bases or sources of synergies produce the benefits anticipated and general competitive factors in the marketplace. While we believe that our expectations regarding the achievement of synergies and other benefits of the ClosetMaid Acquisition are reasonable, there can be no assurance that the integration of ClosetMaid’s operations, management and culture into ours will be timely or effectively accomplished. It is possible that the integration process could result in the loss of key employees, the disruption of ClosetMaid and our existing ongoing businesses, or inconsistencies in standards, controls, procedures and policies that adversely affect our ability to maintain relationships with customers.

In addition, our ability to realize the anticipated benefits are subject to significant business, economic and competitive uncertainties and contingencies, many of which are beyond our control, such as changes to government regulation governing or otherwise impacting our industry, reductions in service levels under our contracts, operating difficulties, customer preferences, changes in competition and general economic or industry conditions. Consequently, we may overestimate the synergies that will result from the Transactions or underestimate the cost of implementing such synergies.

Further, successful integration of our and ClosetMaid’s operations and personnel will place an additional burden on our management and our internal resources. The additional burden could lead to diversion of management attention, which could lead to a decrease in our future operating results and thereby negatively impact our financial condition.

Failure to achieve these anticipated benefits on the anticipated timeframe, or at all, could result in a reduction in the trading price of our shares as well as in increased costs, decreases in the amount of expected revenues and diversion of management’s time and energy and could materially and adversely affect our business, financial condition and operating results. Additionally, we will or have made fair value estimates of certain assets and liabilities in recording the ClosetMaid Acquisition. Actual values of these assets and liabilities could differ from our estimates, which could result in our not achieving the

anticipated benefits of the ClosetMaid Acquisition. Finally, any cost savings that are realized may be offset by losses in revenues or other charges to earnings.

Failure to successfully address these and other issues related to the ClosetMaid Acquisition or other expansion could have a material adverse effect on our financial condition and results of operations, and could adversely affect our ability to successfully implement our business strategy. Also, if our growth occurs more slowly than anticipated or declines, our operating results could be materially adversely affected.

The unaudited pro forma financial information included in this document is preliminary, and our actual financial position and operations after the ClosetMaid Acquisition may differ materially from the unaudited pro forma financial information included in this offering memorandum.

The unaudited pro forma condensed combined financial statements included in this offering memorandum are presented for illustrative purposes only and are not necessarily indicative of what our actual financial position or results of operations would have been had the ClosetMaid Acquisition been completed on the dates indicated. Our actual results and financial position after the consummation of the ClosetMaid Acquisition may differ materially and adversely from the unaudited pro forma financial information included in this offering memorandum.

If the ClosetMaid Acquisition does not close, we will have broad discretion as to the use of the proceeds from this offering, and we may not use the proceeds effectively.

The offering will be consummated prior to the closing of the ClosetMaid Acquisition and we expect to use all of the net proceeds from this offering to finance substantially all of the ClosetMaid Acquisition and to pay related fees and expenses. See “Use of Proceeds.” The ClosetMaid Acquisition is expected to close on or about October 2, 2017; the closing, however, is subject to the satisfaction or waiver of certain conditions, which make the completion and timing of the ClosetMaid Acquisition uncertain, and accordingly, there can be no assurance that all of these conditions will be satisfied, or, if they are, as to the timing of such satisfaction. As a result, the ClosetMaid Acquisition may be delayed or not occur at all.

This offering is not conditioned on the completion of the ClosetMaid Acquisition. Accordingly, if you decide to purchase New Notes in this offering, you should be willing to do so without the assumption that we will complete the ClosetMaid Acquisition. In the event that we fail to consummate the ClosetMaid Acquisition, we will have issued a significant amount of New Notes and we will not have acquired the revenue generating assets that would be required to produce the additional earnings, EBITDA and cash flow we anticipated. As a result, failure to consummate the ClosetMaid Acquisition could adversely affect our financial condition and results of operations.

In the event we do not consummate the ClosetMaid Acquisition for any reason, no mandatory redemption of the New Notes will be required and our management will have broad discretion as to the application of the net proceeds from this offering and could use them for purposes other than those contemplated at the time of this offering. The use of the net proceeds for the ClosetMaid Acquisition for other corporate purposes may not yield profitable results or increase our market value.

We intend to pursue strategic alternatives for PPC which may result in the use of a significant amount of our management resources or significant costs, and we may not be able to fully realize the potential benefit of such a transaction.

We are exploring strategic alternatives for PPC. Although we may devote significant time and resources in pursuit of such a transaction, we may struggle to successfully identify such an opportunity or to successfully consummate such a transaction. Should we be unable to identify or consummate a transaction involving a strategic alternative for PPC, our business

32

prospects and operations could be adversely affected as a result of the devotion of the significant managerial efforts required and the challenges of achieving our long-term objectives in the absence of the closing of such a transaction. In addition, we may incur significant costs in connection with seeking a strategic alternative for PPC, regardless of whether a transaction is completed. In the event that we consummate a strategic alternative for PPC in the future, we cannot assure you that we will fully realize the anticipated benefits of such a transaction.

Risks Related to the ClosetMaid Business

ClosetMaid is subject to intense competition in a marketplace dominated by large retailers and e-commerce companies.

ClosetMaid’s principal customers are large mass merchandisers, such as discount stores, home centers, warehouse clubs, office superstores, commercial distributors and e-commerce companies. The dominant share of the market represented by these large mass merchandisers, together with changes in consumer shopping patterns, has contributed to the formation of dominant multi-category retailers and e-commerce companies that have strong negotiating power with suppliers. Current trends among retailers and e-commerce companies include fostering high levels of competition among suppliers, demanding innovative new products and products tailored to each of their unique requirements, requiring suppliers to maintain or reduce product prices in response to competitive, economic or other factors, and requiring product delivery with shorter lead times. Other trends are for retailers and e-commerce companies to import products directly from foreign sources and to source and sell products under their own private label brands, typically at lower prices, that compete with the ClosetMaid’s products.

The combination of these market influences and retailer consolidation has created an intensely competitive environment in which the ClosetMaid’s principal customers continuously evaluate which product suppliers to use, resulting in downward pricing pressures and the need for big, consumer-meaningful brands, the ongoing introduction and commercialization of innovative new products, continuing improvements in category management and customer service, and the maintenance of strong relationships with large, high-volume purchasers. ClosetMaid also faces the risk of changes in the strategy or structure of its major customers, such as overall store and inventory reductions. The intense competition in the retail and e-commerce sectors, combined with the overall economic environment, may result in a number of customers experiencing financial difficulty, or failing in the future. In particular, a loss of, or a failure by, one of ClosetMaid’s large customers could adversely impact ClosetMaid’s sales and operating cash flows. To address these challenges, ClosetMaid must be able to respond to competitive factors, and the failure to respond effectively could result in a loss of sales, reduced profitability and a limited ability to recover cost increases through price increases.

If ClosetMaid is unable to effectively manage its proprietary online sales platform, its reputation and operating results may be harmed.

ClosetMaid sells merchandise over the Internet through its website, www.closetmaid.com, and through mobile applications for smart phones and tablets. ClosetMaid is vulnerable to certain risks and uncertainties associated with its e-commerce websites, including: changes in required technology interfaces; website downtime and other technical failures; costs and technical issues ClosetMaid may be required to upgrade its website software; computer viruses; changes in applicable federal and state regulations; security breaches; and consumer privacy concerns. The failure of ClosetMaid’s website or mobile applications to perform as expected could result in disruptions and costs to its operations and make it more difficult for customers to purchase merchandise online.

33

In addition, ClosetMaid must successfully respond to changing consumer preferences and buying trends relating to e-commerce usage, including the use of new or improved technology, creative user interfaces and other e-commerce marketing tools such as paid search and mobile applications, among others, which may increase its costs and which may not succeed in increasing sales or attracting customers. Many of ClosetMaid’s competitors, some of whom have greater resources than ClosetMaid, may also be able to benefit from changes in e-commerce technologies, which could harm the competitive position of ClosetMaid. ClosetMaid’s failure to successfully respond to these risks and uncertainties might adversely affect the sales in its e-commerce business, as well as damage its reputation and brands.

ClosetMaid faces risks related to the disruption of its primary manufacturing facilities

ClosetMaid’s manufacturing facilities are concentrated in just a few locations, some of which are located abroad in low-cost locations. These locations are subject to disruption for a variety of reasons, such as natural or man-made disasters, terrorist activities, disruptions of our information technology resources, and utility interruptions. Such disruptions may cause delays in shipping ClosetMaid’s products, which could result in the loss of business or customer trust, adversely affecting ClosetMaid’s business and operating results.

Manufacturing capacity constraints or increased manufacturing costs may have a material adverse effect on our business, results of operations, financial condition and cash flows.

ClosetMaid’s current manufacturing resources may be inadequate to meet significantly increased demand for some of its products. ClosetMaid’s ability to increase its manufacturing capacity depends on many factors, including the availability of capital, steadily increasing consumer demand, equipment delivery, construction lead-times, installation, qualification, regulatory permitting and regulatory requirements. Increasing capacity through the use of third party manufacturers may depend on ClosetMaid’s ability to develop and maintain such relationships and the ability of such third parties to devote additional capacity to fill its orders.

A lack of sufficient manufacturing capacity to meet demand could cause ClosetMaid’s customer service levels to decrease, which may negatively affect customer demand for its products and customer relations generally, which in turn could have a material adverse effect on ClosetMaid’s business, results of operations, financial condition and cash flows. In addition, operating facilities at or near capacity may also increase production and distribution costs and negatively affect relations with ClosetMaid’s employees or contractors, which could result in disruptions in our operations.

In addition, ClosetMaid’s manufacturing costs may increase significantly and ClosetMaid may not be able to successfully recover these cost increases with increased pricing to its customers. For example, subsequent to our entering into the Purchase Agreement, ClosetMaid management reported that the trend of increased manufacturing costs that occurred primarily during the quarter ended June 30, 2017 continued through the fourth quarter resulting in continued decreases in ClosetMaid’s operating results. ClosetMaid management also indicated that it expects this trend to impact future results. These increased manufacturing costs could have an adverse impact on our business, results of operations, financial condition and cash flows.

If ClosetMaid is unable to commercialize a continuing stream of new products that create demand, ClosetMaid’s ability to compete in the marketplace may be adversely impacted.

ClosetMaid’s strategy includes investment in new product development and a focus on innovation. Its long-term success in the competitive retail environment and the industrial and commercial markets depends on its ability to develop and commercialize a continuing stream of innovative new products and line extensions that create demand. New product

34

development and commercialization efforts, including efforts to enter markets or product categories in which ClosetMaid has limited or no prior experience, have inherent risks. These risks include the costs involved, such as development and commercialization, product development or launch delays, and the failure of new products and line extensions to achieve anticipated levels of market acceptance or growth in sales or operating income. ClosetMaid also faces the risk that its competitors will introduce innovative new products that compete with ClosetMaid products. In addition, sales generated by new products or line extensions could cause a decline in sales of ClosetMaid’s other existing products. If new product development and commercialization efforts are not successful, ClosetMaid’s financial results could be adversely affected.

If ClosetMaid does not continue to develop and maintain leading brands or realize the anticipated benefits of increased advertising and promotion spend, its operating results may suffer.

ClosetMaid’s ability to compete successfully also depends increasingly on its ability to develop and maintain leading brands so that ClosetMaid’s retail and other customers will need ClosetMaid’s products to meet consumer demand. Leading brands allow ClosetMaid to realize economies of scale in its operations. The development and maintenance of such brands require significant investment in brand-building and marketing initiatives. While ClosetMaid plans to continue to increase its expenditures for advertising and promotion and other brand-building and marketing initiatives over the long term, the initiatives may not deliver the anticipated results and the results of such initiatives may not cover the costs of the increased investment.

35

The loss of large customers can harm financial results.

A small number of customers account for, and are expected to continue to account for, a substantial portion of our consolidated revenue. Approximately 13% and 12% of consolidated revenue and 51% and 49% of the PPC segment revenue for the year ended September 30, 2016 and the nine months ended June 30, 2017 was generated from P&G. Home Depot, Lowe’s, Menards and Bunnings are significant customers of HBP with Home Depot accounting for approximately 13% of consolidated revenue and 24% of HBP’s revenue for the year ended September 30, 2016 and 13% of consolidated revenue and 23% of HBP’s revenue of the nine months ended June 30, 2017. This customer concentration will increase once we integrate ClosetMaid’s business into our Home and Building Products segment, as many of these businesses are large customers of ClosetMaid as well. ClosetMaid’s top ten customers accounted for approximately 74% of ClosetMaid’s total revenue for the nine months ended June 30, 2017. During such period, Home Depot accounted for approximately 48% of ClosetMaid’s sales while Target accounted for 10% of such sales. The U.S. Government and its agencies and subcontractors, including Lockheed Martin and Boeing, is a significant customer of Telephonics, and accounts for approximately 16% of consolidated revenue and 70% of Telephonics segment revenue for the year ended September 30, 2016 and 13% of consolidated revenue and 68% of Telephonics segment revenue for the nine months ended June 30, 2017. Future operating results will continue to substantially depend on the success of our largest customers, as well as our relationship with them. Orders from these customers are subject to fluctuation and may be reduced materially due to changes in customer needs or other factors. Any reduction or delay in sales of products to one or more of these customers could significantly reduce our revenue. Our operating results will also depend on successfully developing relationships with additional key customers. We cannot assure that our largest customers will be retained or that additional key customers will be recruited. Also, HBP and PPC extend credit to their customers, which exposes them to credit risk. HBP’s largest customer accounted for approximately 26% and 14% of HBP’s and our net accounts receivable as of September 30, 2016, respectively. PPC largest customer accounted for approximately 31% and 7% of PPC and our net accounts receivable as of September 30, 2016, respectively. If either of these customers were to become insolvent or otherwise unable to pay its debts, the financial condition, results of operations and cash flows of the respective segments and we could be adversely affected.

36

CAPITALIZATION

The following table sets forth our cash and capitalization as of June 30, 2017:

|

| | • | | on an actual basis; |

|

| | • | | on a pro forma basis to give effect to this offering and the application of the estimated net proceeds therefrom for the consummation of the ClosetMaid Acquisition as set forth under “Use of Proceeds”. |

The historical data in the table are derived from, and should be read in conjunction with “Use of Proceeds,” “Unaudited Pro Forma Condensed Combined Financial Statements” “Summary—Summary Historical Consolidated Financial Data of Griffon Corporation,” “Summary—Summary Historical Consolidated Financial Data of ClosetMaid Corporation,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” and the consolidated financial statements and the related notes thereto incorporated herein by reference or attached hereto.

| | | | |

| | Actual | | As Adjusted for this

Offering and application

of net proceeds

for the ClosetMaid Acquisition(5) |

| | (Dollars in thousands) |

Cash and Cash Equivalents | | | $ | | 69,448 | | | | $ | | 58,448 | |

| | | | |

Debt: | | | | |

Revolving Credit Facilty(1) | | | | 163,748 | | | | | 163,748 | |

Existing Notes Due 2022 | | | | 725,000 | | | | | 725,000 | |

New Notes Offered Hereby(2) | | | | — | | | | | 200,000 | |

Other Debt(3) | | | | 121,705 | | | | | 121,705 | |

| | | | |

Total Debt | | | $ | | 1,010,453 | | | | $ | | 1,210,453 | |

Total Equity(4) | | | | 394,088 | | | | | 388,088 | |

| | | | |

Total Capitalization | | | $ | | 1,404,541 | | | | $ | | 1,598,541 | |

| | | | |

|

| | (1) | | As of June 30, 2017, we had $163.7 million outstanding under our revolving credit facility. On an as adjusted basis as of June 30, 2017, there would have been $171.9 million of availability under the revolving credit facility and $14.4 million in letters of credit expected to be outstanding. Assuming the use of proceeds to temporarily repay amounts outstanding under our revolving credit facility and without giving effect to the ClosetMaid Acquisition, approximately $335.6 million under our revolving credit facility would be available for borrowing, subject to certain covenants, all of which would be secured. |

|

| | (2) | | Assumes New Notes are issued at par. |

|

| | (3) | | Amount consists of outstanding amounts under our ESOP loans, capital leases, real estate mortgages, foreign lines of credit and term loans and other long-term debt. |

|

| | (4) | | On August 2, 2017 the Board of Directors declared a quarterly cash dividend of $0.06 per share, payable on September 21, 2017 to shareholders of record as of the close of business on August 24, 2017. |

|

| | (5) | | The completion of this offering is not contingent on the completion of the ClosetMaid Acquisition, which, if completed, may occur subsequent to the closing of this offering. There can be no assurance that we will consummate the ClosetMaid Acquisition. In the event we do not consummate the ClosetMaid Acquisition for any reason, the net proceeds of this offering would be available for general corporate purposes, including to temporarily repay amounts outstanding under our revolving credit facility and the as adjusted capitalization would no longer be applicable. |

37

SELECTED HISTORICAL FINANCIAL DATA OF GRIFFON CORPORATION

The following table presents selected consolidated financial data. This information should only be read in conjunction with “Griffon Corporation’s Management’s Discussion and Analysis of Financial Condition and Results of Operations,” included elsewhere in this offering memorandum, and our consolidated financial statements and the notes related thereto, which are incorporated herein by reference. The selected consolidated financial data for the nine months ended June 30, 2016 and 2017 were derived from our unaudited consolidated financial statements, which are incorporated herein by reference. The unaudited financial statements have been prepared on the same basis as the audited financial statements and, in the opinion of our management, include all normal recurring adjustments necessary for a fair presentation of the information set forth herein. The consolidated financial data for the fiscal years ended September 30, 2012 and 2013 were derived from our audited consolidated financial statements that are not included, or incorporated by reference, in this offering memorandum. The consolidated financial data for the fiscal years ended September 30, 2014, 2015 and 2016 have been derived from our audited consolidated financial statements, which are incorporated herein by reference. Historical results are not necessarily indicative of the results to be expected in the future. In addition, our results for the nine months ended June 30, 2017 are not necessarily indicative of results expected for the full year ending September 30, 2017.

| | | | | | | | | | | | | | |

| | For the Years Ended September 30, | | Nine Months Ended

June 30, |

| | 2012(1) | | 2013(2) | | 2014(3) | | 2015(4) | | 2016(5) | | 2016 | | 2017 |

| | (Dollars in thousands) |

Statement of Operations Data: | | | | | | | | | | | | | | |

Revenue | | | $ | | 1,861,145 | | | | $ | | 1,871,327 | | | | $ | | 1,991,811 | | | | $ | | 2,016,032 | | | | $ | | 1,957,161 | | | | $ | | 1,456,456 | | | | $ | | 1,436,184 | |

Cost of goods and services | | | | 1,442,340 | | | | | 1,453,742 | | | | | 1,532,412 | | | | | 1,540,254 | | | | | 1,483,727 | | | | | 1,106,837 | | | | | 1,088,550 | |

| | | | | | | | | | | | | | |

Gross profit | | | | 418,805 | | | | | 417,585 | | | | | 459,399 | | | | | 475,778 | | | | | 473,434 | | | | | 349,619 | | | | | 347,634 | |

Selling, general and administrative expenses. | | | | 341,696 | | | | | 340,469 | | | | | 375,099 | | | | | 374,761 | | | | | 364,027 | | | | | 271,765 | | | | | 272,972 | |

Restructuring and other related charges | | | | 4,689 | | | | | 13,262 | | | | | 6,136 | | | | | — | | | | | 5,900 | | | | | 5,900 | | | | | — | |

| | | | | | | | | | | | | | |

Total operating expenses | | | | 346,385 | | | | | 353,731 | | | | | 381,235 | | | | | 374,761 | | | | | 369,927 | | | | | 277,665 | | | | | 272,972 | |

Income from operations | | | | 72,420 | | | | | 63,854 | | | | | 78,164 | | | | | 101,017 | | | | | 103,507 | | | | | 71,954 | | | | | 74,662 | |

Other income (expense) | | | | | | | | | | | | | | |

Interest expense | | | | (52,007 | ) | | | | | (52,520 | ) | | | | | (48,447 | ) | | | | | (48,173 | ) | | | | | (51,254 | ) | | | | | (37,454 | ) | | | | | (38,747 | ) | |

Interest income | | | | 292 | | | | | 353 | | | | | 303 | | | | | 301 | | | | | 143 | | | | | 134 | | | | | 46 | |

Loss from debt extinguishment | | | | — | | | | | — | | | | | (38,890 | ) | | | | | — | | | | | — | | | | | — | | | | | — | |

Other, net | | | | 1,236 | | | | | 2,646 | | | | | 3,154 | | | | | 491 | | | | | 768 | | | | | 312 | | | | | (1,176 | ) | |

| | | | | | | | | | | | | | |

Total other income (expense) | | | | (50,479 | ) | | | | | (49,521 | ) | | | | | (83,880 | ) | | | | | (47,381 | ) | | | | | (50,343 | ) | | | | | (37,008 | ) | | | | | (39,877 | ) | |

| | | | | | | | | | | | | | |

Income (loss) before taxes | | | | 21,941 | | | | | 14,333 | | | | | (5,716 | ) | | | | | 53,636 | | | | | 53,164 | | | | | 34,946 | | | | | 34,785 | |

Provision (benefit) for income taxes | | | | 4,930 | | | | | 7,543 | | | | | (5,539 | ) | | | | | 19,347 | | | | | 23,154 | | | | | 10,467 | | | | | 7,923 | |

| | | | | | | | | | | | | | |

Income (loss) from continuing operations | | | | 17,011 | | | | | 6,790 | | | | | (177 | ) | | | | | 34,289 | | | | | 30,010 | | | | | 24,479 | | | | | 26,862 | |

Discontinued operations: | | | | | | | | | | | | | | |

Loss from operations of discontinued businesses | | | | — | | | | | (4,651 | ) | | | | | — | | | | | — | | | | | — | | | | | — | | | | | — | |

Benefit from income taxes | | | | — | | | | | 1,628 | | | | | — | | | | | — | | | | | 2,193 | | | | | — | | | | | — | |

| | | | | | | | | | | | | | |

Loss from discontinued operations | | | | — | | | | | (3,023 | ) | | | | | — | | | | | — | | | | | — | | | | | — | | | | | — | |

| | | | | | | | | | | | | | |

Net Income (loss) | | | $ | | 17,011 | | | | $ | | 3,767 | | | | $ | | (177 | ) | | | | $ | | 34,289 | | | | $ | | 30,010 | | | | $ | | 24,479 | | | | $ | | 26,862 | |

| | | | | | | | | | | | | | |

38

| | | | | | | | | | | | | | |

| | For the Years Ended September 30, | | Nine Months Ended

June 30, |

| | 2012(1) | | 2013(2) | | 2014(3) | | 2015(4) | | 2016(5) | | 2016 | | 2017 |

| | (Dollars in thousands) |

Balance Sheet Data: | | | | | | | | | | | | | | |

Cash and equivalents | | | $ | | 209,654 | | | | $ | | 178,130 | | | | $ | | 92,405 | | | | $ | | 52,001 | | | | $ | | 72,553 | | | | $ | | 68,616 | | | | $ | | 69,448 | |

Property, plant and equipment, net | | | | 356,879 | | | | | 353,593 | | | | | 370,565 | | | | | 379,972 | | | | | 405,404 | | | | | 388,149 | | | | | 410,472 | |

Total assets | | | | 1,802,921 | | | | | 1,777,608 | | | | | 1,808,826 | | | | | 1,712,813 | | | | | 1,782,096 | | | | | 1,779,641 | | | | | 1,804,483 | |

Total debt, net of issuance costs | | | | 685,991 | | | | | 677,672 | | | | | 799,187 | | | | | 843,569 | | | | | 936,558 | | | | | 931,614 | | | | | 997,376 | |

Total liabilities | | | | 1,148,769 | | | | | 1,127,144 | | | | | 1,276,799 | | | | | 1,282,288 | | | | | 1,371,149 | | | | | 1,359,614 | | | | | 1,410,395 | |

Total shareholders’ equity | | | | 654,152 | | | | | 650,464 | | | | | 532,027 | | | | | 430,525 | | | | | 410,947 | | | | | 420,027 | | | | | 394,088 | |

Other Financial Data: | | | | | | | | | | | | | | |

Capital expenditures | | | $ | | 68,851 | | | | $ | | 64,441 | | | | $ | | 77,094 | | | | $ | | 73,620 | | | | $ | | 90,759 | | | | $ | | 63,247 | | | | $ | | 59,153 | |

Depreciation and amortization | | | | 66,264 | | | | | 70,748 | | | | | 67,396 | | | | | 69,800 | | | | | 70,208 | | | | | 51,879 | | | | | 56,380 | |

|

| | (1) | | 2012 includes $4,689 of restructuring charges ($3,048, net of tax), $477 of acquisition related costs ($310, net of tax) and discrete tax benefits, net, of $5,110. |

|

| | (2) | | 2013 includes $13,262 of restructuring charges ($8,266, net of tax), a loss on pension settlement of $2,142 ($1,392, net of tax) and discrete tax benefits, net, of $325. |

|

| | (3) | | 2014 includes $6,136 of restructuring charges ($3,804, net of tax), $3,161 of acquisition costs ($1,960, net of tax), $38,890 loss on debt extinguishment ($24,964, net of tax) and discrete tax benefits, net, of $4,674. |

|

| | (4) | | 2015 includes discrete tax benefits, net, of $62. |

|

| | (5) | | 2016 includes $5,900 of restructuring charges ($4,247, net of tax, or $0.10 per share), discrete tax provisions, net, of $2,658 or $0.06 per share. |

39

UNAUDITED PRO FORMA CONDENSED CONSOLIDATED FINANCIAL INFORMATION

On September 1, 2017, CMLLC entered into the Purchase Agreement with Emerson pursuant to which CMLLC will (subject to the satisfaction or waiver of the closing conditions in the Purchase Agreement) acquire, directly or indirectly, the Business and on September 25, 2017 CMLLC and Emerson entered into the Amendment.

The following unaudited pro forma condensed combined financial information is based on our historical consolidated financial statements and ClosetMaid’s and the Business’ historical consolidated financial statements and has been prepared and adjusted to give effect to the ClosetMaid Acquisition and related financing transactions. Concurrently and in connection with our entering into the Purchase Agreement, we entered into the Commitment Letter, pursuant to which the DB Commitment Parties have committed to provide 100% of the principal amount of the Bridge Facility, subject to the satisfaction or waiver of certain conditions set forth therein. Pursuant to the Commitment Letter, the commitment under the Bridge Facility will be reduced, on a dollar-for-dollar basis, by the amount of aggregate proceeds, if any, from this offering. The commitment under the Bridge Facility will terminate upon the consummation of this offering in full.

The unaudited pro forma condensed combined statements of operations for the nine months ended June 30, 2017 and the year ended September 30, 2016 give effect to the ClosetMaid Acquisition as if it had occurred on October 1, 2015. The unaudited pro forma condensed combined balance sheet as of June 30, 2017 gives effect to the ClosetMaid Acquisition as if it had occurred on June 30, 2017.

The pro forma condensed combined financial information contained herein are provided for information purposes only and do not necessarily reflect what the combined company’s financial condition or results of operations would have been had the ClosetMaid Acquisition occurred on the dates indicated. They also may not be useful in predicting, and are not intended to project, the future financial condition and results of operations of the combined company. The actual financial position and results of operations may differ significantly from the pro forma amounts reflected herein due to a variety of factors, and do not reflect all of the costs, benefits and synergies, or any anticipated tax benefits, that may be incurred or realized as a result of the ClosetMaid Acquisition.

The unaudited pro forma financial statements reflect adjustments to give effect to pro forma events that are directly attributable to the ClosetMaid Acquisition and this offering, factually supportable and, with respect to the pro forma statement of statement of operations, expected to have a continuing impact on the operating results of the combined company. The pro forma adjustments included herein are based upon currently available information and certain assumptions that we believe are reasonable under the circumstances and which are set forth in the notes below. The pro forma adjustments are more fully described in the notes to the unaudited pro forma condensed combined financial statements below. In addition, the unaudited pro forma condensed combined balance sheet includes pro forma purchase price allocations based upon preliminary estimates of the fair value of the assets acquired and liabilities assumed in connection with the ClosetMaid Acquisition. These allocations are preliminary and may be adjusted in the future upon finalization of these preliminary estimates.

The pro forma condensed combined financial statements should be read in conjunction with, and are qualified in their entirety by reference to, the following information: (i) the notes to the unaudited pro forma condensed combined financial information below; (ii) our audited financial statements as of and for the year ended September 30, 2016, which are included in our Annual Report on Form 10-K for the year then ended filed on November 17, 2016 and incorporated by reference into this offering memorandum; (iii) our unaudited financial statements as of and for the period ended June 30, 2017, which are included in our Quarterly Report on Form 10-Q for the period then ended filed on August 2, 2017 and incorporated by reference into this offering memorandum; (iv) ClosetMaid’s audited financial statements as of and for the year ended September 30, 2016, which are included in this offering memorandum; and (v) ClosetMaid’s unaudited financial statements as of and for the period ended June 30, 2017, which are included elsewhere in this offering memorandum.

40

GRIFFON CORPORATION AND SUBSIDIARIES

UNAUDITED PRO FORMA CONDENSED COMBINED STATEMENT OF OPERATIONS

FOR THE YEAR ENDED SEPTEMBER 30, 2016

(in thousands)

| | | | | | | | | | |

($ in thousands) | | Historical | | Adjustments | | | | Pro Forma

Combined |

| | Griffon | | Closet Maid |

Revenue | | | $ | | 1,957,161 | | | | $ | | 318,600 | | | | $ | | — | | | | | | $ | | 2,275,761 | |

Cost of goods and services | | | | 1,483,727 | | | | | 220,100 | | | | | — | | | | | | | 1,703,827 | |

| | | | | | | | | | |

Gross profit | | | | 473,434 | | | | | 98,500 | | | | | — | | | | | | | 571,934 | |

Selling, general and administrative expenses, other | | | | 364,027 | | | | | 69,800 | | | | | 2,176 | | | | | a | | | | | 436,003 | |

Restructuring and other related charges | | | | 5,900 | | | | | 600 | | | | | — | | | | | | | 6,500 | |

| | | | | | | | | | |

Total operating expenses | | | | 369,927 | | | | | 70,400 | | | | | 2,176 | | | | | | | 442,503 | |

Income from operations | | | | 103,507 | | | | | 28,100 | | | | | (2,176 | ) | | | | | | | 129,431 | |

Other income (expense) | | | | | | | | | | |

Interest expense | | | | (51,111 | ) | | | | | 2,500 | | | | | (14,000 | ) | | | | | b | | | | | (62,611 | ) | |

Other, net | | | | 768 | | | | | — | | | | | — | | | | | | | 768 | |

| | | | | | | | | | |

Total other income (expense) | | | | (50,343 | ) | | | | | 2,500 | | | | | (14,000 | ) | | | | | | | (61,843 | ) | |

Income before taxes | | | | 53,164 | | | | | 30,600 | | | | | (16,176 | ) | | | | | | | 67,588 | |

Provision for income taxes | | | | 23,154 | | | | | 12,000 | | | | | (6,519 | ) | | | | | c | | | | | 28,635 | |

| | | | | | | | | | |

Net income | | | $ | | 30,010 | | | | $ | | 18,600 | | | | $ | | (9,657 | ) | | | | | | $ | | 38,953 | |

| | | | | | | | | | |

See Notes to Unaudited Pro Forma Combined Condensed Financial Statements.

41

GRIFFON CORPORATION AND SUBSIDIARIES

UNAUDITED PRO FORMA CONDENSED COMBINED STATEMENT OF OPERATIONS

FOR THE NINE MONTH PERIOD ENDED JUNE 30, 2017

(in thousands)

| | | | | | | | | | |

($ in thousands) | | Historical | | Adjustments | | | | Pro Forma

Combined |

| | Griffon | | Closet Maid |

Revenue | | | $ | | 1,436,184 | | | | $ | | 227,900 | | | | $ | | — | | | | | | $ | | 1,664,084 | |

Cost of goods and services | | | | 1,088,550 | | | | | 160,700 | | | | | ��� | | | | | | | 1,249,250 | |

| | | | | | | | | | |

Gross profit | | | | 347,634 | | | | | 67,200 | | | | | — | | | | | | | 414,834 | |

Selling, general and administrative expenses, other | | | | 272,972 | | | | | 52,400 | | | | | 1,632 | | | | | a | | | | | 327,004 | |

| | | | | | | | | | |

Income from operations | | | | 74,662 | | | | | 14,800 | | | | | (1,632 | ) | | | | | | | 87,830 | |

Other income (expense) | | | | | | | | | | |

Interest expense, net | | | | (38,701 | ) | | | | | 2,900 | | | | | (11,525 | ) | | | | | b | | | | | (47,326 | ) | |

Other, net | | | | (1,176 | ) | | | | | — | | | | | — | | | | | | | (1,176 | ) | |

| | | | | | | | | | |

Total other income (expense) | | | | (39,877 | ) | | | | | 2,900 | | | | | (11,525 | ) | | | | | | | (48,502 | ) | |

Income before taxes | | | | 34,785 | | | | | 17,700 | | | | | (13,157 | ) | | | | | | | 39,328 | |

Provision for income taxes | | | | 7,923 | | | | | 6,700 | | | | | (4,974 | ) | | | | | c | | | | | 9,649 | |

| | | | | | | | | | |

Net income | | | $ | | 26,862 | | | | $ | | 11,000 | | | | $ | | (8,184 | ) | | | | | | $ | | 29,678 | |

| | | | | | | | | | |

See Notes to Unaudited Pro Forma Combined Condensed Financial Statements.

42

GRIFFON CORPORATION AND SUBSIDIARIES

UNAUDITED PRO FORMA CONDENSED COMBINED STATEMENT OF OPERATIONS

FOR THE TRAILING TWELVE MONTH PERIOD ENDED JUNE 30, 2017

(in thousands)

| | | | | | | | | | |

($ in thousands) | | TTM | | Adjustments | | | | Pro Forma

Combined |

| | Griffon | | Closet Maid |

Revenue | | | $ | | 1,936,889 | | | | $ | | 309,700 | | | | $ | | — | | | | | | $ | | 2,246,589 | |

Cost of goods and services | | | | 1,465,440 | | | | | 215,700 | | | | | — | | | | | | | 1,681,140 | |

| | | | | | | | | | |

Gross profit | | | | 471,449 | | | | | 94,000 | | | | | — | | | | | | | 565,449 | |

Selling, general and administrative expenses, other | | | | 365,234 | | | | | 69,200 | | | | | 2,176 | | | | | a | | | | | 436,610 | |

| | | | | | | | | | |

Income from operations | | | | 106,215 | | | | | 24,800 | | | | | (2,176 | ) | | | | | | | 128,839 | |

Other income (expense) | | | | | | | | | | |

Interest expense, net | | | | (52,492 | ) | | | | | 3,500 | | | | | (15,000 | ) | | | | | b | | | | | (63,992 | ) | |

Other, net | | | | (720 | ) | | | | | — | | | | | — | | | | | | | (720 | ) | |

| | | | | | | | | | |

Total other income (expense) | | | | (53,212 | ) | | | | | 3,500 | | | | | (15,000 | ) | | | | | | | (64,712 | ) | |

Income before taxes | | | | 53,003 | | | | | 28,300 | | | | | (17,176 | ) | | | | | | | 64,127 | |

Provision for income taxes | | | | 20,610 | | | | | 11,300 | | | | | (7,073 | ) | | | | | c | | | | | 24,837 | |

| | | | | | | | | | |

Net income | | | $ | | 32,393 | | | | $ | | 17,000 | | | | $ | | (10,103 | ) | | | | | | $ | | 39,290 | |

| | | | | | | | | | |

See Notes to Unaudited Pro Forma Combined Condensed Financial Statements.

43

GRIFFON CORPORATION AND SUBSIDIARIES

UNAUDITED PRO FORMA CONDENSED COMBINED BALANCE SHEET

AS OF JUNE 30, 2017

| | | | | | | | | | |

($ in thousands) | | Historical | | Adjustments | | | | Pro Forma

Combined |

| | Griffon | | Closet Maid |

CURRENT ASSETS | | | | | | | | | | |

Cash and equivalents | | | $ | | 69,448 | | | | $ | | 8,900 | | | | $ | | (19,900 | ) | | | d | | | $ | | 58,448 | |

Accounts receivable, net of allowances | | | | 227,813 | | | | | 39,400 | | | | | — | | | | | | | 267,213 | |

Contract costs and recognized income not yet billed, net of progress payments | | | | 119,367 | | | | | — | | | | | — | | | | | | | 119,367 | |

Inventories, net | | | | 339,393 | | | | | 33,700 | | | | | — | | | | | | | 373,093 | |

Prepaid and other current assets | | | | 43,622 | | | | | 10,600 | | | | | (3,700 | ) | | | e | | | | 50,522 | |

Assets of discontinued operations | | | | 479 | | | | | — | | | | | — | | | | | | | 479 | |

| | | | | | | | | | |

Total Current Assets | | | | 800,122 | | | | | 92,600 | | | | | (23,600 | ) | | | | | | | 869,122 | |

PROPERTY, PLANT AND EQUIPMENT, net | | | | 410,472 | | | | | 33,700 | | | | | 794 | | | e | | | | 444,966 | |

GOODWILL | | | | 361,405 | | | | | 139,900 | | | | | (23,900 | ) | | | f | | | | 477,405 | |

INTANGIBLE ASSETS, net | | | | 210,060 | | | | | 1,300 | | | | | 36,206 | | | e,f | | | | 247,566 | |

OTHER ASSETS | | | | 18,110 | | | | | 400 | | | | | 3,700 | | | e | | | | 22,210 | |

ASSETS OF DISCONTINUED OPERATIONS | | | | 4,314 | | | | | — | | | | | — | | | | | | | 4,314 | |

| | | | | | | | | | |

Total Assets | | | $ | | 1,804,483 | | | | $ | | 267,900 | | | | $ | | (6,800 | ) | | | | | | $ | | 2,065,583 | |

| | | | | | | | | | |

CURRENT LIABILITIES | | | | | | | | | | |

Notes payable and current portion of long-term debt | | | $ | | 16,656 | | | | $ | | 1,700 | | | | $ | | — | | | | | | $ | | 18,356 | |

Accounts payable | | | | 178,571 | | | | | 48,400 | | | | | — | | | | | | | 226,971 | |

Accrued liabilities | | | | 97,871 | | | | | 15,400 | | | | | (8,900 | ) | | | g | | | | 104,371 | |

Liabilities of discontinued operations | | | | 1,107 | | | | | — | | | | | — | | | | | | | 1,107 | |

| | | | | | | | | | |

Total Current Liabilities | | | | 294,205 | | | | | 65,500 | | | | | (8,900 | ) | | | | | | | 350,805 | |

LONG-TERM DEBT, net of issuance costs | | | | 980,720 | | | | | 3,800 | | | | | 195,000 | | | h | | | | 1,179,520 | |

OTHER LIABILITIES | | | | 131,149 | | | | | 11,700 | | | | | — | | | | | | | 142,849 | |

LIABILITIES OF DISCONTINUED OPERATIONS | | | | 4,321 | | | | | — | | | | | — | | | | | | | 4,321 | |

| | | | | | | | | | |

Total Liabilities | | | | 1,410,395 | | | | | 81,000 | | | | | 186,100 | | | | | | | 1,677,495 | |

SHAREHOLDERS’ EQUITY | | | | | | | | | | |

Total Shareholders’ Equity (Deficit) | | | | 394,088 | | | | | 186,900 | | | | | (192,900 | ) | | | i | | | | 388,088 | |

| | | | | | | | | | |

Total Liabilities and Shareholders’ Equity | | | $ | | 1,804,483 | | | | $ | | 267,900 | | | | $ | | (6,800 | ) | | | | | | $ | | 2,065,583 | |

| | | | | | | | | | |

See Notes to Unaudited Pro Forma Combined Condensed Financial Statements.

44

NOTES TO UNAUDITED PRO FORMA CONDENSED COMBINED FINANCIAL STATEMENTS

1. Description of ClosetMaid Acquisition

On September 1, 2017, ClosetMaid Acquisition Corp., our indirect, wholly-owned subsidiary (“CMAC”) entered into a Purchase Agreement with Emerson as the seller. On September 12, 2017, CMAC was converted into CMLLC. On September 25, 2017, CMLLC and Emerson entered into the Amendment. Under the Purchase Agreement, CMLLC will (subject to the satisfaction or waiver of the closing conditions in the Purchase Agreement) acquire, directly or indirectly, all of the outstanding equity interests in ClosetMaid and certain other of Emerson’s subsidiaries as well as certain assets owned, used or held for use in connection with Business. The purchase price for ClosetMaid is $200.0 million.

The ClosetMaid acquisition is expected to close on or about October 2, 2017, subject to the satisfaction or waiver of certain closing conditions. There can be no assurance that the ClosetMaid acquisition will close, or if it does, when the closing will occur.

2. Basis of Presentation

The unaudited pro forma condensed combined financial information was prepared to give effect to the completed ClosetMaid acquisition, which will be accounted for using the acquisition method of accounting. The unaudited pro forma condensed combined financial information was based on the historical financial statements of Griffon and ClosetMaid. All pro forma financial statements use Griffon’s period-end date.

The acquisition method of accounting under U.S. GAAP requires, among other things, that most assets acquired and liabilities assumed be recognized at their fair values at the acquisition date. Fair value is defined under U.S. GAAP as “the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date.” Market participants are assumed to be buyers and sellers in the principal (or most advantageous) market for the asset or liability. Fair value measurements for an asset assume the highest and best use by these market participants. Fair value measurements can be highly subjective and it is possible that other professionals, applying reasonable judgment to the same facts and circumstances, could develop and support a range of alternative estimated amounts.

We have not initiated a process to value the assets to be acquired and liabilities to be assumed and have made only an initial estimate of the intangible assets acquired from ClosetMaid for the purposes of presenting these unaudited pro forma condensed combined financial statements. Consequently, the recorded assets and liabilities on ClosetMaid’s financial statements, along with an initial estimate of the intangible assets to be acquired, were added to those of Griffon. Financial statements and reported results of operations of Griffon for periods following completion of the acquisition may reflect different values, and the related depreciation and amortization thereof, after Griffon completes the process of valuing the assets acquired and liabilities assumed. However, any adjustments will not be retroactively restated to reflect the historical financial position or results of operations of ClosetMaid for periods prior to the acquisition.

Acquisition-related transaction costs (e.g., advisory, legal, valuation, other professional fees) and certain acquisition-related restructuring charges impacting the acquired company are not included as a component of consideration transferred, but are accounted for as expenses in the periods in which the costs are incurred. The unaudited pro forma condensed combined statements of operations do not reflect acquisition-related transaction costs incurred by Griffon and ClosetMaid, however, the unaudited pro forma condensed combined balance sheets include the effect of expensing acquisition-related transaction costs as an adjustment to retained earnings and reduction to cash proceeds. The unaudited pro forma condensed combined financial statements reflect no restructuring and integration charges that may be incurred in connection with the acquisition.

45

Certain immaterial reclassifications were made to the overall presentation of the ClosetMaid’s financial statements to conform to Griffon’s presentation.

3. Accounting Policies

Griffon has not identified any differences in accounting policies that would have a material impact on the combined financial statements except as detailed below.

4. Assets Acquired and Liabilities Assumed

The estimated assets acquired and the liabilities assumed by Griffon in the acquisition of ClosetMaid, reconciled to the consideration transferred, are provided below (in thousands):

| | |

Accounts receivable, net | | | $ | | 39,400 | |

Inventories, net | | | | 33,700 | |

Other current assets | | | | 6,900 | |

Property, plant and equipment, net | | | | 34,494 | |

Intangible assets, net | | | | 37,506 | |

Goodwill | | | | 116,000 | |

Other assets | | | | 4,100 | |

| | |

Total assets acquired | | | | 272,100 | |

| | |

| | |

Notes payable and current portion of long-term debt | | | | 1,700 | |

Accounts payable and accrued liabilities | | | | 54,900 | |

Long-term debt | | | | 3,800 | |

Other liabilities | | | | 11,700 | |

| | |

Total liabilities assumed | | | | 72,100 | |

| | |

Total | | | $ | | 200,000 | |

| | |

Notes payable and current portion of long-term debt and Long-term debt reflect the assumption of capital leases. The above allocation is preliminary with the final allocation to be based upon the balance sheet as of the closing date of the ClosetMaid Acquisition. Griffon is expecting to finalize the above adjustments with the filing of its 10-K with the exception of certain purchase price adjustments required to be completed by the end of November, 2017.

5. Pro Forma Adjustments

This note should be read in conjunction withNote 1. Description of ClosetMaid Acquisition; Note 2. Basis of Presentation.

|

| | (a) | | To adjust for the amortization attributable to the estimated fair value of $37.5 million of intangible assets acquired (intellectual property and customer relationships); amortized over a fifteen year life. The $37.5 million is estimated to be approximately 20% of the $185 million attributed to the purchase of ClosetMaid ($200 million total purchase price less $15 million paid to acquire a 338(h)(10) tax benefit). |

|

| | (b) | | To eliminate interest income recorded by ClosetMaid, consisting of interest income on intercompany receivable from Emerson, and to recognize the cost of debt incurred by Griffon in connection with the acquisition of ClosetMaid as follows (in thousands) at an assumed rate of interest which would be higher if we are required to draw down on the Bridge Facility to pay for all or any portion of the ClosetMaid Acquisition: |

46

| | | | | | |

| | Fiscal Year 2016 | | Nine Months

Ended June 30,

2017 | | Trailing Twelve

Months Ended

June 30, 2017 |

Elimination of ClosetMaid interest income | | | $ | | 2,500 | | | | $ | | 2,900 | | | | $ | | 3,500 | |

Interest expense on New Notes | | | | 10,500 | | | | | 7,875 | | | | | 10,500 | |

Amortization of debt issuance costs | | | | 1,000 | | | | | 750 | | | | | 1,000 | |

| | | | | | |

Totals | | | $ | | 14,000 | | | | $ | | 11,525 | | | | $ | | 15,000 | |

| | | | | | |

|

| | (c) | | Griffon has estimated an incremental 38% tax rate in assessing the tax impact of the combination of ClosetMaid with Griffon. The effective tax rate and tax accounts in the balance sheet of the combined company could be significantly different (either higher or lower) depending on post-acquisition activities, including tax planning opportunities, cash repatriation decisions and geographic mix of income. |

|

| | (d) | | Represents cash paid for related advisory, legal and financing costs of $11 million and removal of ClosetMaid cash of $8.9 million. |

|

| | (e) | | The pro forma balance sheet adjustments included reclassifications of certain balances to conform to Griffon’s balance sheet presentation. ClosetMaid’s current deferred taxes of $3.7 million were reclassified from prepaid and other current assets to other assets as Griffon has already adopted Financial Accounting Standard Board ASU 2015-17 “Balance Sheet Classification of Deferred Taxes”. ClosetMaid’s capitalized software of $0.8 million was reclassified from intangible assets, net, to property, plant and equipment, net, to be consistent with Griffon’s balance sheet presentation. |

|

| | (f) | | Goodwill and intangible assets, net includes amounts to reflect the ClosetMaid acquisition as well as the reclassification of capitalized software discussed in note (e) above as follows (in thousands): |

| | | | |

| | Goodwill | | Acquired

Intangible Assets,

Net |

Remove ClosetMaid goodwill | | | $ | | (139,900 | ) | | | | $ | | — | |

Record goodwill from ClosetMaid acquisition | | | | 116,000 | | | | | — | |

Record intangible assets from ClosetMaid acquisition | | | | — | | | | | 37,000 | |

Reclassification of capitalized software | | | | — | | | | | (794 | ) | |

| | | | |

Totals | | | $ | | (23,900 | ) | | | | $ | | 36,206 | |

| | | | |

|

| | (g) | | To reflect the amount owed to Emerson for cash transferred upon the consummation of the ClosetMaid acquisition. |

|

| | (h) | | To record the debt related to the New Notes less estimated financing costs. |

|

| | (i) | | To eliminate ClosetMaid’s historical equity and reflect the impact of expensing certain advisory and legal costs associated with the acquisition of ClosetMaid and paid with the proceeds received from the New Notes. |

47

CLOSETMAID

Overview

ClosetMaid is a leader in the North American residential storage and organization solutions industry with leading positions across the major channels where it does business including retail, building and e-commerce. ClosetMaid designs, manufactures and sells a comprehensive portfolio of wire and laminate shelving, containers, storage cabinets and other closet and home organization accessories under the highly recognized ClosetMaid brand name and other private label brands. ClosetMaid currently operates as a business unit of Emerson’s Commercial & Residential Solutions segment. ClosetMaid was founded in 1965 in Delray Beach, Florida. In 1970, ClosetMaid moved its corporate headquarters to Ocala, Florida. In a 1990 joint venture, Emerson and Bosch each acquired 50% of ClosetMaid. Emerson purchased the remaining 50% of ClosetMaid from Bosch in 1997.

ClosetMaid offers a diversified and well-balanced mix of wood and wire storage and organizational solutions. ClosetMaid’s wood solutions include closet systems, cube storage, storage furniture and cabinets targeted at customers looking for functional storage with a strong aesthetic appeal and the look of quality furniture. Selected wood product brands include MasterSuite, Suite Symphony, Impressions, ExpressShelf, and SpaceCreations. In the twelve months ended September 30, 2016, wood solution products made up approximately 52% of total ClosetMaid sales.

ClosetMaid’s wire solutions include wire shelving and hardware, wire accessories and kitchen storage products that provide affordable, customizable, versatile and durable solutions for single and multi-family homes. Selected wire product brands include Maximum Load®, SuperSlide® and ShelfTrack®. In the twelve months ended September 30, 2016, wood solution products made up approximately 48% of total ClosetMaid sales.

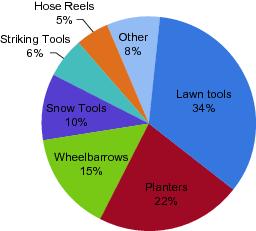

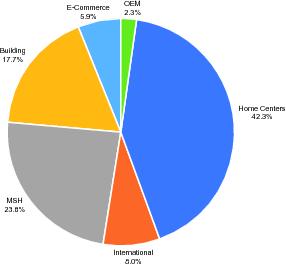

For the twelve months ended June 30, 2017 and September 30, 2016, ClosetMaid generated net sales of approximately $309.7 million and $318.6 million, respectively. After giving effect to the ClosetMaid Acquisition, Griffon’s pro forma revenue and Adjusted EBITDA for the trailing twelve month period ended June 30, 2017 would have been approximately $2.25 billion and approximately $221.2 million, respectively. See footnote 3 to Summary Unaudited Pro Forma Condensed Consolidated financial Information and Other Information for a reconciliation to Adjusted EBITDA. The pie chart below illustrates ClosetMaid’s Net Sales by business category for the twelve months ended June 30, 2017.

48

ClosetMaid’s Business Strengths

|

| | • | | Premier Brand.ClosetMaid is a leader in the North American residential storage and organization industry, with a highly recognizable brand and strong reputation among customers as demonstrated by its net promoter score of 51 and 85% of total sales in products with leading industry share positions. Do-it-yourself customers and professional installers choose the ClosetMaid brand due to its reputation for quality, high value, functionality, durability, versatility and ease of installation. These qualities, along with the Company’s sell through rates and supply chain reliability and support, have made ClosetMaid the supplier of choice for a number of leading retailers and homebuilders; |

|

| | • | | Strong Position in Served Channels.We believe that ClosetMaid held an aggregate total market share of 15% within its addressable industry in 2016, which we believe was twice as large as each of ClosetMaid’s two largest competitors. ClosetMaid has built leading positions in the retail, building and e-commerce channels it serves. The retail channel, including home centers, mass merchants, hardware and specialty stores, recognizes ClosetMaid as a dependable supply chain partner who can consistently provide a breadth of quality products when needed and offers sales support both before and after the sale. ClosetMaid has a presence in over 20,000 retail stores worldwide, with a presence in approximately 16,000 retail stores in North America. The building channel, which includes homebuilders, developers, contractors and dealers, is driven by installing dealers and builders who decide which products to use and select ClosetMaid products due to their quality, ease of installation, availability and value. The e-commerce channel is comprised of fragmented brick and mortar retailers offering a wide variety of brands, online retailers, and ClosetMaid’s own website, Closetmaid.com. ClosetMaid has built a strong online presence through its own website and through large key online retailers, that drives customer awareness and influences decision making; |

|

| | • | | Comprehensive and Innovative Product Portfolio. ClosetMaid offers a breadth of products, providing storage and organizational solutions for every room in the home. ClosetMaid has a broad and balanced portfolio of wood and wire storage and organizational solutions including closet systems, wire shelving, hardware and accessories, cube storage, storage furniture and cabinets and kitchen storage. ClosetMaid has a strong history of continuous innovation and was the first manufacturer to introduce ventilated wire closet shelving for use in new homes. Today, that tradition of innovation continues with approximately 35% of sales through June 30, 2017 coming from products introduced in the prior five years and numerous recent new product introductions that are expected to drive additional growth; |

|

| | • | | Deep Customer and Channel Relationships. ClosetMaid has built established, long-term relationships with key retailers such as Home Depot, Lowe’s, and Walmart, and leading homebuilders such as D.R. Horton, KB Home, Lennar and NVR. ClosetMaid maintains collaborative relationships with key customers with a focus on new product development, managing planograms, demand planning and online design which creates more entrenched partnerships; |

|

| | • | | Strong Momentum in E-Commerce.Digital commerce is a key pillar of growth and focus for ClosetMaid. Over the last five years, ClosetMaid has built a proactive and focused business model that offers ClosetMaid products where they are most likely to be identified when customers are researching and making buying decisions online and has invested in digital and social media advertising to continue to build brand awareness and drive traffic. Today, ClosetMaid receives over 7,000 visitors per day on its websites. Additionally, ClosetMaid’s fulfillment centers have been redesigned to include single function and multi-order picking (implemented across all facilities) to support growth of the e-commerce platform. As a result, ClosetMaid has driven growth of approximately 72% per year over the last five years in its e-commerce platform and |

49

|

| | | | we believe it is well positioned to recognize additional growth in the future as more customers’ storage solution decisions are made online; |

|

| | • | | Best-in-Class Manufacturing and Supply Chain. ClosetMaid has four strategically located manufacturing facilities (two of which are located in low-cost locations) with highly efficient production processes and a wide distribution footprint to meet consumer demand. ClosetMaid’s lean inventory model minimizes working capital (which was 6.7% of ClosetMaid’s net sales for 2016 and 8.7% for the twelve months ended June 30, 2017) and supports strong free cash flow. ClosetMaid’s multi-facility footprint optimizes direct fulfillment speed and minimizes freight costs. In addition to traditional manufacturing operations, ClosetMaid utilizes a lean manufacturing process known as cellular manufacturing in which small workcells are organized in an assembly line fashion enabling them to quickly respond to niche segments in the closet business, support small runs of unique wood specifications and react swiftly to meet customer delivery speed expectations; |

|

| | • | | Experienced Management Team. ClosetMaid’s seasoned and dedicated management team have a successful history working together and an average of 18 years of experience at ClosetMaid. The management team has strong industry experience providing valuable operational acumen and knowledge of industry dynamics with a proven track record of executing sustainable growth as well as operating efficiency initiatives and acquisitions. Additionally, the management team has deep and long-standing relationships with decision-makers at key customers. |

ClosetMaid’s Growth Strategy

ClosetMaid’s growth strategy includes the following:

|

| | • | | Product Mix Shift Upward.ClosetMaid seeks to shift away from products with lower margins and growth, and develop new product lines to maintain and expand its leadership position in its core closet segment and drive increased profitability. |

|

| | • | | Retail and Building Growth. ClosetMaid plans to grow its space and productivity within the retail channel and continue to grow in the building segment through the development of new products (i.e., ExpressShelf), dealer and pull-through sales initiatives and field sales development. |

|

| | • | | Leverage E-Commerce Platform. ClosetMaid seeks to continue to grow its e-commerce business and expand differentiated programs that leverage the e-commerce selling platform it has built over the last five years. |

|

| | • | | Grow International Sales.ClosetMaid plans to grow its international sales in over 23 countries and increase its market presence in underpenetrated markets. |

|

| | • | | Investment in New Products.ClosetMaid expects that its strength in traditional closet storage solutions and its focus on innovation can be leveraged to expand into new growth adjacencies including garage and kitchen organization. |

ClosetMaid’s Industry

ClosetMaid is a leader in the North American residential storage and organizational industry, which is driven by demand for home organization products and spans a range of material and product categories. ClosetMaid operates in the building products sector where demand for its products is heavily influenced by the repair and remodeling (“R&R”) of existing homes and the construction of new homes. Additionally, existing home sales and increasing home equity help drive R&R spending on storage and organizational solutions.

ClosetMaid primarily competes in the fragmented $9.7 billion U.S. home organization market. According to analysis from The Freedonia Group, U.S. sales of home organization products increased at an annual rate of 3.6% from 2006 to 2016 and are projected to grow at an annual rate of 3.8% through 2021.

50

Source: The Freedonia Group

The U.S. home storage and organization industry has been impacted by changing consumer preferences and demographics. Significant demand has shifted towards space-conscious living in smaller areas, particularly for consumers living in urban areas, which has driven demand for stackable and nestable products to maximize limited space. The market has seen increased demand for higher-end storage solutions driven by the perception that closets and garages are no longer simply utilitarian areas reserved for storage, but extensions of daily living spaces. Additionally, new homes are being built with larger closets, increasing homeowners’ need for storage and organizational products. Finally, The Freedonia Group has indicated that baby boomers and empty nesters tend to invest more in their closets which results in the rising demand of storage products.

Raw Materials and Suppliers

ClosetMaid’s primary raw materials are particleboard wood and wire rod. ClosetMaid purchases its wood supply primarily from three suppliers in the United States and Mexico (for its particleboard) and Asia (for its finished goods). Wire supply comes primarily from Jacksonville, Florida (for wire rod used in shelving) and Asia (for small wire). ClosetMaid has favorable pricing and payment terms with its suppliers of raw materials.

Manufacturing, Distribution and Operations

ClosetMaid has two manufacturing facilities in the United States; a 620,000 square foot facility in Ocala Florida used for manufacturing wire shelving, and a 155,000 square foot facility in Grantsville, Maryland used for wood manufacturing. ClosetMaid also has manufacturing facilities in two low-cost locations; a 102,000 square foot facility in Reynosa, Mexico used for wood manufacturing and a 157,000 square foot facility in Jiangmen, China used for small wire manufacturing.

Finished goods are transported by truck and rail to ClosetMaid’s distribution/warehousing centers, strategically located in Ocala, Florida, Chino, California, Belle Vernon, Pennsylvania and Pharr, Texas.

In response to its rapid growth in e-commerce, ClosetMaid has implemented wave picking at distribution centers. Orders are grouped into batches, or “waves”, enabling employees to collect items all at once for multiple orders (split order capability vs. pickers checking out individual orders as they come in). Order pickers gather items within the wave using a consolidated pick list, reducing travel time by allowing them to make picks for multiple orders in the same area. Warehouse Management System (WMS) tools support organizing the daily flow of work and enable fulfillment processing, picking efficiencies, improvements in product flow, and simplified/visible order pulls.

51

Competition

The home storage and organizational solutions industry is highly fragmented. ClosetMaid sells through retail, direct to consumer (e-commerce category) and direct to installer (building) channels and competes with a significant number of companies across these unique channels. ClosetMaid’s strengths are its highly recognized brand, broad portfolio of quality products and services, product differentiation, successful history of innovation, dependable supply-chain and high on-time delivery rates. ClosetMaid’s leading industry position and brand recognition are key to expanding its customer base, entering new adjacencies and driving continued growth. We believe that ClosetMaid held an aggregate total market share of 15% within its addressable industry in 2016, which we believe was twice as large as each of ClosetMaid’s two largest competitors.

Employees

As of June 2017, ClosetMaid had approximately 1,500 full-time employees. None of ClosetMaid’s employees in the U.S. are represented by a union or covered by a collective bargaining agreement.

Regulation

ClosetMaid’s operations are subject to various environmental, health, and employee safety laws and regulations. ClosetMaid believes that it is in material compliance with these laws and regulations. Historically, compliance with environmental laws has not materially affected, and is not expected to materially affect, ClosetMaid’s capital expenditures, earnings or competitive position in the future. Nevertheless, there can be no assurance that, in the future, it will not incur additional costs for compliance or that such costs will not be material.

Customers

ClosetMaid’s large customer base, which included approximately 718 customers for the nine months ended June 30, 2017, is diversified among various industries. Key retail customers of ClosetMaid include Home Depot, Target, Lowes, and Walmart and building customers include D.R. Horton, KB Home, Lennar and NVR. ClosetMaid’s top ten customers accounted for approximately 74% of ClosetMaid’s total revenues for the nine months ended June 30, 2017. During this period, Home Depot and Target accounted for approximately 48% and 10% of ClosetMaid’s sales, respectively. No other customer accounted for 10% of ClosetMaid’s sales during such period.

Seasonality

Historically, ClosetMaid’s revenue and income are lowest in its quarter ending March 31 and highest in its quarter ending December 31, primarily due to the holiday season.

Financial Information About Geographic Areas

In 2016, 92% of ClosetMaid’s revenue was from sales to customers in the United States. Of the remainder of ClosetMaid’s revenue, 64% was from sales to customers in Canada and 36% was from sales to customers in Australia and the rest of the world. For the nine months ended June 30, 2017, 92% of ClosetMaid’s revenue was from sales to customers in the United States. Of the remainder of ClosetMaid’s revenue, 68% was from sales to customers in Canada and 32% was from sales to customers in Australia and the rest of the world.

Research and Development

ClosetMaid strives to improve existing products as well as develop new products to satisfy consumer needs, expand revenue opportunities, maintain or extend competitive

52

advantages, increase market share and reduce production costs. R&D costs for ClosetMaid were $1.1 million for the nine months ended June 30, 2017, $1.4 million in 2016 and $1.4 million in 2015.

Intellectual Property

ClosetMaid follows a practice of actively protecting and enforcing its proprietary rights in the U.S. and throughout the world where ClosetMaid’s products are sold. All intellectual property information presented in this section is as of June 30, 2017.

Trademarks are of significant importance to ClosetMaid’s business. With over 50 years of experience and innovation in the storage and organization industry, ClosetMaid has a significant level of goodwill in its strong family of brands, including: ClosetMaid®, ShelfTrack®, Cubeicals®, Selectives® and MasterSuite®. ClosetMaid has approximately 87 registered trademarks and approximately 11 pending trademark applications around the world.

ClosetMaid constantly seeks to offer new and innovative products to its customers. ClosetMaid has 68 issued patents and 10 pending patent applications. ClosetMaid’s patents are in various stages of their terms of validity.

Properties

ClosetMaid occupies approximately 1.6 million total square feet of general office, factory and warehouse space throughout the U.S., Mexico and China. The following table sets forth certain information related to ClosetMaid’s major facilities:

| | | | | | | | | |

Location | | Primary Use | | Approx. Square

Footage | | Owned/Leased | | Lease End Year |

Ocala, FL | | Warehouse and manufacturing | | | | 620,000 | | | Leased | | | | 2020 | |

Grantsville, MD | | Manufacturing | | | | 155,000 | | | Owned | | |

Reynosa, MX | | Warehouse and manufacturing | | | | 133,000 | | | Manufacturing site owned; warehouse site leased | | | | 2020 | |

Jiangmen, China | | Manufacturing | | | | 157,000 | | | Leased | | | | 2019 | |

Chino, CA | | Warehouse | | | | 202,000 | | | Leased | | | | 2021 | |

Pharr, TX | | Warehouse | | | | 80,000 | | | Leased | | | | 2018 | |

Belle Vernon, PA | | Warehouse | | | | 233,000 | | | Leased | | | | 2022 | |

Mississauga, ON | | Sales Office for Mississauga | | | | 5,300 | | | Leased | | | | 2018 | |

Moresville, NC | | Sales Office for Lowes | | | | 3,300 | | | Leased | | | | 2018 | |

Atlanta, GA | | Sales Office for Home Depot | | | | 6,800 | | | Leased | | | | 2018 | |

All of ClosetMaid’s facilities are generally well maintained and suitable for the operations conducted.

Legal Proceedings

ClosetMaid is involved in litigation, investigations and claims arising out of the normal conduct of business, including those relating to commercial transactions, product liability and warranty claims, environmental, employment, and health and safety matters. ClosetMaid estimates and accrues liabilities resulting from such matters based on a variety of factors, including the stage of the proceeding; potential settlement value; assessments by internal

53

and external counsel; and assessments by environmental engineers and consultants of potential environmental liabilities and remediation costs. Such estimates are not discounted to reflect the time value of money due to the uncertainty in estimating the timing of the expenditures, which may extend over several years.

While it is impossible to ascertain the ultimate legal and financial liability with respect to certain contingent liabilities and claims, we believe, based upon examination of currently available information, experience to date, and advice from its legal counsel, that the individual and aggregate liabilities resulting from the ultimate resolution of these contingent matters, after taking into consideration ClosetMaid’s existing insurance coverage and amounts already accrued, will not have a material adverse impact on ClosetMaid’s combined results of operations, financial position or cash flows.

ClosetMaid Performance Overview

ClosetMaid’s fiscal year, like ours, ends on September 30. For the nine months ended June 30, 2017 and year ended September 30, 2016, ClosetMaid generated approximately $227.9 million and $318.6 million, respectively, in revenue, which represented 16% of Griffon’s net sales for such periods on a pro forma basis, after giving effect to the ClosetMaid Acquisition.

Results of Operations.ClosetMaid’s net sales for the nine months ended June 30, 2017 declined by approximately $8.9 million from the comparable prior year period due to lower revenue from a large customer of ClosetMaid managing inventory levels and a price decrease related to reduced steel costs, partially offset by increased building channel and e-commerce sales. ClosetMaid’s net earnings for the nine months ended June 30, 2017 decreased by approximately $1.6 million from the comparable period in the prior year. The decrease was primarily due to the decrease in revenue described above and unfavorable sales mix impacting gross margins. Subsequent to our entering into the Purchase Agreement, ClosetMaid management reported that the trend of increased manufacturing costs that occurred primarily during the quarter ended June 30, 2017 continued through the fourth quarter resulting in continued decreases in operating results. ClosetMaid management also indicated it expects this trend to impact future results. Further, ClosetMaid’s results of operations may be adversely effected as a result of decreases in sales in regions impacted by Hurricane Harvey and Hurricane Irma. As a result of the foregoing, we currently expect that ClosetMaid net sales, EBITDA and Adjusted EBITDA for the fiscal year ending September 30, 2017 will be approximately $298 million, $24 million and $24.9 million, respectively

Net sales for the fiscal year ended September 30, 2016 declined by approximately $15.4 million compared with the fiscal year ended September 30, 2015 due to implementation of a freight allowance in lieu of delivery to stores of a large customer of ClosetMaid, reduced cubical and fabric drawer sales, and decreased Russia and Australia sales, partially offset by increased e-commerce and building channel sales. Earnings improved by $2.9 million due to reduced restructuring costs and reduced steel costs.

Balance Sheet.ClosetMaid’s inventories increased as of June 30, 2017 by approximately $5.6 million as compared with the levels as of June 30, 2016 due to increased purchase of finished goods and wire inventory levels in order to improve customer service. ClosetMaid’s June 30, 2017 receivables increased $1.6 million from June 30, 2016, while cash and cash equivalents decreased by approximately $1 million due to timing of sales and customer mix. Current liabilities increased as of June 30, 2017, by approximately $2.8 million as compared to June 30, 2016, primarily due to purchase of finished goods, which have longer payment terms.