UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-02090

Invesco Bond Fund

(Exact name of registrant as specified in charter)

1555 Peachtree Street, N.E., Suite 1800 Atlanta, Georgia 30309

(Address of principal executive offices) (Zip code)

Sheri Morris 1555 Peachtree Street, N.E., Suite 1800 Atlanta, Georgia 30309

(Name and address of agent for service)

Registrant’s telephone number, including area code: (713) 626-1919

Date of fiscal year end: 2/28

Date of reporting period: 2/28/21

| ITEM 1. | Report to Stockholders. |

| Annual Report to Shareholders | February 28, 2021 |

| Invesco Bond Fund |

| NYSE: VBF | |

| Management’s Discussion of Fund Performance |

Performance summary

For the year ended February 28, 2021, Invesco Bond Fund (the Fund), at net asset value (NAV), outperformed its style-specific benchmark, the Bloomberg Barclays Baa U.S. Corporate Bond Index. The Fund’s return can be calculated based on either the market price or the NAV of its shares. NAV per share is determined by dividing the value of the Fund’s portfolio securities, cash and other assets, less all liabilities, by the total number of shares outstanding. Market price reflects the supply and demand for Fund shares. As a result, the two returns can differ, as they did during the year. |

| Performance |

| Total returns, 2/29/20 to 2/28/21 |

| Fund at NAV | 6.17% |

| Fund at Market Value | 8.88 |

| Bloomberg Barclays Baa U.S. Corporate Bond Index▼ (Style-Specific Index) | 3.53 |

| Market Price Discount to NAV as of 2/28/21 | -4.95 |

| Source(s): ▼RIMES Technologies Corp. |

The performance data quoted represent past performance and cannot guarantee comparable future results; current performance may be lower or higher. Investment return, NAV and market price will fluctuate so that you may have a gain or loss when you sell shares. Please visit invesco.com/us for the most recent month-end performance. Performance figures reflect Fund expenses, the reinvestment of distributions (if any) and changes in NAV for performance based on NAV and changes in market price for performance based on market price. Since the Fund is a closed-end management investment company, shares of the Fund may trade at a discount or premium from the NAV. This characteristic is separate and distinct from the risk that NAV could decrease as a result of investment activities and may be a greater risk to investors expecting to sell their shares after a short time. The Fund cannot predict whether shares will trade at, above or below NAV. The Fund should not be viewed as a vehicle for trading purposes. It is designed primarily for risk-tolerant long-term investors. |

| | | |

Market conditions and your Fund Fixed income markets began 2020 buoyed by positive economic data and the signing of the phase one US-China trade deal. However, initial optimism was dampened by the outbreak of the new coronavirus (COVID-19) that swiftly spread from China to other global regions. Global markets fell sharply as the human and economic cost of the COVID-19 pandemic mounted. As fear of a worldwide recession increased, the US Federal Reserve (the Fed) took aggressive action to support both the domestic and global economy by slashing rates to a range of 0.00% to 0.25%.1 The unemployment rate reached a peak of 14.7%2 while real gross domestic product (GDP) decreased at an annual rate of 31.4%3 in the second quarter of 2020. Many economies received fiscal stimulus and very significant monetary stimulus due to the impact of COVID-19. The massive monetary policy response created an environment in which investors embraced risk, and stocks rose globally after a deep rout in the first half of the year. Consequently, some countries were able to achieve some success in controlling the spread of the virus and were able to slowly reopen their economies in the third quarter. With a potential vaccine in sight for the end of 2020 or early 2021 the broader bond market, both developed and emerging, ended the year in positive territory. The 10-year US Treasury yield continued to decline at the start of 2020, as the Fed | | adopted a more dovish stance and continued geopolitical uncertainty forced investors to seek higher quality fixed income instruments. Elevated volatility levels due to the COVID-19 pandemic and ensuing global recession led to a severe “risk-off” tone in the markets driving Treasury yields even lower. The 10-year US Treasury yield ended the year (2020) at 0.93%, 99 basis points lower than at the beginning of the year.4 (A basis point is one one-hundredth of a percentage point.) US corporate markets posted gains in the fourth quarter of 2020, as positive news on COVID-19 vaccines and strong corporate earnings outweighed investor concerns about political disagreement over a fiscal stimulus package and sharply rising coronavirus infections nationwide. Cyclical sectors like energy and financials led the way, while real estate and consumer staples lagged. While the US economy rebounded significantly since the pandemic began, the recovery appeared to slow in the fourth quarter with estimates for employment gains and GDP growth down from the third quarter. However, bonds were buoyed by the Fed’s pledge to maintain its accommodative stance and asset purchases, “until substantial further progress has been made” toward employment and inflation targets. In the first quarter of 2021, rising 10-year US Treasury yields increased significantly to 1.6%,4 its highest level since February 2020, reflecting higher inflation expectations. Consequently, yields have fallen further into |

negative territory as the Fed remains in its accommodative policy. As vaccine rollouts become more widespread and accessible across the country, along with the passing of another fiscal stimulus package, we believe there will be an economic rebound later in the year. The Fund, at NAV, generated positive absolute returns for the year and outperformed its style-specific benchmark, the Bloomberg Barclays Baa U.S. Corporate Bond Index. Security selection in investment-grade corporate bonds was the most notable contributor to the Fund’s relative performance. Security selection in the technology, media & telecom, financial institutions, and consumer non-cyclical sectors contributed significantly to the Fund’s relative performance, as did an out-of-index exposure to the high yield sector. The Fund’s duration relative to the style-specific benchmark contributed to the Fund’s relative performance, as interest rates fell meaningfully during the year. Additionally, securitized assets detracted slightly from the Fund’s relative performance as Commercial Mortgage-Backed Securities and Asset-Backed Securities gradually recovered. The Fund may use active duration and yield curve positioning for risk management and for generating returns. Duration measures a portfolio’s price sensitivity to interest rate changes, with a shorter duration tending to be less sensitive to these changes. Yield curve positioning refers to actively emphasizing particular points (maturities) along the yield curve with favorable risk-return expectations. During the year, duration of the portfolio was maintained near the Fund’s benchmark, on average, and the timing of changes and the degree of variance from the Fund’s benchmark detracted from relative Fund returns. Buying and selling US Treasury futures was an important tool used for the management of interest rate risk and to seek to maintain our targeted portfolio duration during the year. Part of the Fund’s strategy in seeking to manage currency risk in the portfolio during the year entailed purchasing and selling currency derivatives. Management of currency risk was carried out via currency forwards on an as-needed basis and we believe it was effective in managing the currency positioning within the Fund during the year. Derivatives can be a cost-effective way to gain exposure to asset classes. However, derivatives may amplify traditional investment risks through the creation of leverage and may be less liquid than traditional securities. We wish to remind you that the Fund is subject to interest rate risk, meaning when interest rates rise, the value of fixed-income securities tends to fall. The risk may be greater in the current market environment because interest rates are near historic lows. The degree to which the value of fixed income securities may decline due to rising interest rates may vary depending on the speed and |

magnitude of the increase in interest rates as well as individual security characteristics, such as price, maturity, duration and coupon and market forces, such as supply and demand for similar securities. We are monitoring interest rates and the market, economic and geopolitical factors that may impact the direction, speed and magnitude of changes to interest rates across the maturity spectrum, including the potential impact of monetary policy changes by the Fed and certain foreign central banks. If interest rates rise or fall faster than expected, markets may experience increased volatility, which may affect the value and/or liquidity of certain of the Fund’s investments. Thank you for investing in Invesco Bond Fund and for sharing our long-term investment horizon. 1 Source: US Federal Reserve 2 Source: US Bureau of Labor Statistics 3 Source: US Bureau of Economic Analysis 4 Source: US Department of the Treasury |

Portfolio manager(s): Matt Brill Chuck Burge Michael Hyman Todd Schomberg The views and opinions expressed in management’s discussion of Fund performance are those of Invesco Advisers, Inc. These views and opinions are subject to change at any time based on factors such as market and economic conditions. These views and opinions may not be relied upon as investment advice or recommendations, or as an offer for a particular security. The information is not a complete analysis of every aspect of any market, country, industry, security or the Fund. Statements of fact are from sources considered reliable, but Invesco Advisers, Inc. makes no representation or warranty as to their completeness or accuracy. Although historical performance is no guarantee of future results, these insights may help you understand our investment management philosophy. See important Fund and, if applicable, index disclosures later in this report. |

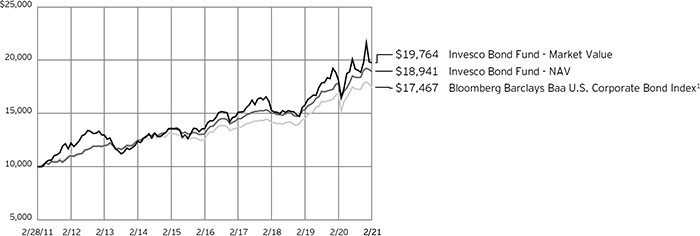

| Your Fund’s Long-Term Performance |

Results of a $10,000 Investment

Fund and index data from 2/28/11

1 Source: RIMES Technologies Corp. Past performance cannot guarantee future results. Performance shown in the chart does not reflect deduction of taxes a shareholder would pay on Fund distributions or sale of Fund shares. |

| Average Annual Total Returns |

| As of 2/28/21 |

| | NAV | Market |

| 10 Years | 6.60% | 7.05% |

| 5 Years | 7.70 | 7.85 |

| 1 Year | 6.17 | 8.88 |

The performance data quoted represent past performance and cannot guarantee future results; current performance may be lower or higher. Please visit invesco.com/ performance for the most recent month-end performance. Performance figures do not reflect deduction of taxes a shareholder would pay on Fund distributions or sale of Fund shares. Investment return and principal value will fluctuate so that you may have a gain or loss when you sell shares. |

Supplemental Information

| ■ | Unless otherwise stated, information presented in this report is as of February 28, 2021, and is based on total net assets. |

| ■ | Unless otherwise noted, all data provided by Invesco. |

| ■ | To access your Fund’s reports, visit invesco.com/fundreports. |

| About indexes used in this report |

| ■ | The Bloomberg Barclays Baa U.S. Corporate Bond Index measures the Baa-rated, fixed-rate, taxable corporate bond market. |

| ■ | The Fund is not managed to track the performance of any particular index, including the index(es) described here, and consequently, the performance of the Fund may deviate significantly from the performance of the index(es). |

| ■ | A direct investment cannot be made in an index. Unless otherwise indicated, index results include reinvested dividends, and they do not reflect sales charges. Performance of the peer group, if applicable, reflects fund expenses; performance of a market index does not. |

Changes to the Fund’s Governing Documents

On August 13, 2020, the Fund’s Board of Trustees (the “Board”) approved changes to the Fund’s Amended and Restated Agreement and Declaration of Trust (the “Declaration of Trust”) and the Fund’s Amended and Restated Bylaws (the “Bylaws”). The following is a summary of certain of these changes.

Declaration of Trust

The Fund’s Declaration of Trust was amended to provide as follows:

| ■ | A Majority Trustee Vote is required on all Board actions, including amendments to the Declaration of Trust. “Majority Trustee Vote” means (a) with respect to a vote of the Board, a vote of the majority of the Trustees then in office, and a separate vote of a majority of the Continuing Trustees; and (b) with respect to a vote of a committee or sub-committee of the Board, a vote of the majority of the members of such committee or sub-committee, and a separate vote of a majority of the Continuing Trustees that are members of such committee or sub-committee. “Continuing Trustee” means a Trustee who either (a) has been a member of the Board for a period of at least thirty-six months (or since the commencement of the Fund’s operations, if less than thirty-six months) or (b) was nominated to serve as a member of the Board by a majority of the Continuing Trustees then members of the Board. |

| ■ | Any Trustee may only be removed for cause, including but not limited to (i) willful misconduct, dishonesty, or fraud on the part of the Trustee in the conduct of his or her office; (ii) failing to meet, on a continuous basis, the Trustee Qualifications (as defined below); or (iii) being indicted for, pleading guilty to or being convicted of a felony, in each case only by a written instrument signed by at least 75% of the number of Trustees prior to such removal (not including the Trustee(s) for which removal is being sought), specifying the date when such removal shall become effective. |

| ■ | In the event of a vacancy on the Board, the size of the Board is automatically reduced by the number of vacancies (but not to less than two) until the Board maintains or increases the size of the Board. |

| ■ | The following Trustee Qualifications are imposed on all nominees and current Trustees, whether or not nominated by a third party: |

(a) An individual who is an Affiliated Person of any:

(1) Investment Adviser (other than the Fund’s Investment Adviser or any Investment Adviser affiliated with the Fund’s Investment Adviser);

(2) Pooled Vehicle (as defined below) (other than a Pooled Vehicle advised or managed by the Fund’s Investment Adviser or any Investment Adviser affiliated with the Fund’s Investment Adviser); or

(3) Entity Controlling, Controlled by, or under common Control with, any Investment Adviser (other than the Fund’s Investment Adviser or any Investment Adviser affiliated with the Fund’s Investment Adviser) or Pooled Vehicle (other than a Pooled Vehicle advised or managed by the Fund’s Investment Adviser or any Investment Adviser affiliated with the Fund’s Investment Adviser);

shall be disqualified from being nominated or serving as a Trustee, if the Board determines by Majority Trustee Vote (excluding the vote of any Trustee subject to such vote) that such relationship is reasonably likely to:

(1) Present undue conflicts of interest between (i) the Fund and its Shareholders, and (ii) such other Investment Adviser or Pooled Vehicle;

(2) Impede the ability of the individual to discharge the duties of a Trustee; and/or

(3) Impede the free flow of information (including proprietary, non-public or confidential information) between the Fund’s Investment Adviser and the Board.

(b) An individual who:

(1) Is a 12(d) Control Person (as defined below);

(2) Is an Affiliated Person of a 12(d) Holder (as defined below) or 12(d) Control Person; or

(3) Has accepted directly or indirectly any consulting, advisory, or other compensatory fee from any 12(d) Holder or 12(d) Control Person;

shall be disqualified from being nominated or serving as a Trustee.

(c) An individual who serves as a trustee or director of 5 or more issuers (including the Fund) having securities registered under the Securities Exchange Act of 1934 (the “Exchange Act”) (for these purposes, investment companies or individual series thereof having the same Investment Adviser as the Fund or any Investment Adviser affiliated with the Fund’s Investment Adviser shall be counted as a single issuer) shall be disqualified from being nominated or serving as a Trustee.

(d) An individual who has been subject to any censure, order, consent decree or adverse final action of any federal, state, or foreign governmental or regulatory authority barring or suspending such individual from participation in or association with any investment-related business or restricting such individual’s activities with respect to any investment-related business, been the subject of any investigation or proceeding that could reasonably be expected to result in an individual nominated or serving as a Trustee failing to satisfy the requirements of this paragraph, or is or has been engaged in any conduct which has resulted in, or could have reasonably been expected or would reasonably be expected to result in, the Securities and Exchange Commission (“SEC”) censuring, placing limitations on the activities, functions, or operation of, suspending, or revoking the registration of any Investment Adviser under Section 203(e) or (f) of the Investment Advisers Act of 1940 shall be disqualified from being nominated or serving as a Trustee.

(e) An individual who is or has been the subject of any of the ineligibility provisions contained in Section 9(b) of the Investment Company Act of 1940 (the “1940 Act”) that would permit, or could reasonably have been expected or would reasonably be expected to permit the SEC by order to prohibit, conditionally or unconditionally, either permanently or for a period of time, such individual from servicing or acting as an employee, officer, trustee, director, member of an advisory board, Investment Adviser or depositor of, or principal underwriter for, a registered investment company or Affiliated Person of such Investment Adviser, depositor, or principal underwriter shall be disqualified from being nominated or serving as a Trustee.

For purposes of the foregoing, the following definitions apply:

“12(d) Control Person” means any person who Controls, is Controlled by, or under common Control with, a 12(d) Holder (solely for purposes of this definition, an Investment Adviser shall be deemed to Control any investment company that it advises, including any collective investment vehicle that would be an investment company but for the exception provided by Section 3(c)(1) or (7) of the 1940 Act);

“12(d) Holder” is defined as an investment company (including, for purposes of (1) below, any collective investment vehicle that would be an investment company but for the exception provided by Section 3(c)(1) or (7) of the 1940 Act) that in the aggregate owns, directly or indirectly through any companies Controlled by the 12(d) Holder, of record or beneficially as defined in Rule 13d-3 and 13d-5 of the Securities Act of 1934:

(1) More than three percent (3%) of the outstanding voting Shares of the Fund;

(2) Securities issued by the Fund having an aggregate value in excess of five percent (5%) of the total assets of such investment company or of any company or companies Controlled by such investment company;

(3) Securities issued by the Fund and by all other investment companies having an aggregate value in excess of ten percent (10%) of the total assets of the investment company making such investment or any company or companies Controlled by the investment company making such investment;

(4) Together with other investment companies having the same Investment Adviser and companies Controlled by such investment companies, more than ten percent (10%) of the total outstanding Shares of the Fund; or

(5) For an investment company operating as a “fund of funds” pursuant to Section 12(d)(1)(F) of the 1940 Act, together with all Affiliated Persons of such investment company, more than three percent (3%) of the outstanding voting Shares of the Fund (solely for purposes of determining an “Affiliated Person” for purposes of this definition, an Investment Adviser shall be deemed to Control any investment company that it advises, including any collective investment vehicle that would be an investment company but for the exception provided by Section 3(c)(1) or 3(c)(7) of the 1940 Act).

“Pooled Vehicle” means (i) any issuer meeting the definition of an “investment company” in Section 3(a) of the 1940 Act, or (ii) any person that would meet the definition of an investment company but for the exceptions in Section 3(c) of the 1940 Act.

Bylaws

The Fund’s Bylaws were amended to provide as follows:

| ■ | At all meetings of the Board, one-half (50%) of the Trustees then in office, including one-half (50%) of the Continuing Trustees (but in no event fewer than two Trustees), shall constitute a quorum for the transaction of business. At all meetings of any committee or subcommittee, one-half (50%) of the committee members or sub-committee members, including one-half (50%) of the committee members or sub-committee members who are Continuing Trustees (but in no event fewer than two Trustees), shall constitute a quorum for the transaction of business. Business transacted at any meeting of Shareholders shall be limited to (a) the purpose stated in the notice, (b) the adjournment of such meeting in accordance with the relevant provisions of the Bylaws, and (c) solely with respect to annual meetings, such other matters as are permitted to be presented at the meeting in accordance with the relevant provisions of the Bylaws. |

| ■ | A majority of the outstanding Shares entitled to vote at a Shareholders’ meeting, which are present in person or represented by proxy, shall constitute a quorum at the Shareholders’ meeting, except when a larger quorum is required by applicable law or the requirements of any securities exchange on which Shares are listed for trading, in which case such quorum shall comply with such requirements. Quorum |

shall be determined with respect to the meeting as a whole regardless of whether particular matters have achieved the requisite vote for approval, but the presence or absence of a quorum shall not prevent any adjournment at the meeting pursuant to the relevant provisions of the Bylaws.

| ■ | When a quorum is present at any meeting, the vote of the shares as set forth in the Declaration of Trust shall decide any question brought before such meeting, unless a different vote is required by the express provision of applicable law, the Declaration of Trust, the Bylaws or other governing instrument of the Fund, in which case such express provision shall govern and control the decision of such question. Notwithstanding the foregoing, and whether or not a quorum is present, the vote of the holders of one-third (1/3) of the shares cast, or the chair of the meeting in his or her discretion, shall have the power to adjourn a meeting of the Shareholders with regard to a particular proposal scheduled to be voted on at such meeting or to adjourn such meeting entirely. |

| ■ | The matters to be considered and brought before any annual meeting of Shareholders of the Fund shall be limited to only such matters, including the nomination and election of Trustees, as shall be brought properly before such meeting in compliance with the procedures set forth in the Bylaws. For any matter to be properly brought before any annual meeting of Shareholders, the matter must be (among other requirements specified in the Bylaws), brought before the annual meeting in the manner specified in the Bylaws by a Record Owner at the time of the giving of notice, on the record date for such meeting and at the time of the meeting, or a Shareholder (a “Nominee Holder”) that holds voting securities entitled to vote at meetings of Shareholders through a nominee or “street name” holder of record and can demonstrate to the Fund such indirect ownership and such Nominee Holder’s entitlement to vote such securities, and is a Nominee Holder at the time of the giving of notice provided for in the Bylaws, on the record date for such meeting and at the time of the meeting, with proof of such ownership or holding reasonably satisfactory to the Fund to be provided by such Record Owner or Nominee Holder at each such aforementioned time. |

| ■ | Any Shareholder desiring to nominate any person(s) for election as a Trustee shall deliver, as part of such Shareholder Notice, a statement in writing with respect to the person(s) to be nominated, together with any persons to be designated as a proposed substitute nominee in the event that a proposed nominee is unwilling or unable to serve, including by reason of any disqualification (a “Proposed Nominee”) setting forth all information required by the Bylaws, including each Proposed Nominee’s written representation that he or she agrees to complete, execute, and return to the Fund within 5 business days of receipt the Fund’s form of trustee questionnaire and any supplemental information reasonably requested by the Fund. |

| ■ | Any Shareholder who gives a Shareholder Notice of any matter proposed to be brought before an annual meeting or to elect Proposed Nominees shall deliver, as part of such Shareholder Notice, all statements and representations required by the Bylaws, including: 1) a statement in writing with respect to the Shareholder and the beneficial owner, if any, on whose behalf the proposal is being made setting forth, among other requirements, the number and class of all Shares which the Shareholder has the right to acquire pursuant to any agreement or upon exercise of conversion rights or warrants, or otherwise (including any derivative or short positions, profit interests, options or similar rights, and borrowed or loaned shares); and 2) an agreement to return to the Fund within 5 business days of receipt such other information as the Board may reasonably request. |

| ■ | To be considered a qualified representative of the Shareholder, a Person must be a duly authorized officer, manager or partner of such Shareholder, as evidenced by an incumbency certificate executed by the corporate secretary (or other duly authorized officer) of the Shareholder, or must be authorized by a writing executed by such Shareholder delivered by such Shareholder to act for such Shareholder as proxy at the meeting of Shareholders, and such Person must deliver a copy of such incumbency certificate or writing to the secretary of the meeting. |

| ■ | Only such matters shall be conducted at a special meeting of Shareholders as shall have been brought before the meeting pursuant to the Fund’s notice of meeting. Nominations of individuals for election to the Board may be made at a special meeting of Shareholders at which Trustees are to be elected: 1) pursuant to the Fund’s notice of meeting; 2) by or at the direction of the Board; or 3) provided that the Board has determined that Trustees shall be elected at such special meeting, and such special meeting shall meet all of the requirements with respect to annual meetings as if such special meeting were an annual meeting. |

| ■ | Provisions in the Bylaws regarding advance notice of Shareholder Nominees for Trustee and other Shareholder proposals shall not apply to Shareholder proposals made pursuant to Rule 14a-8 under the Exchange Act. Notwithstanding the forgoing, no Shareholder proposal may be brought before an annual meeting, whether submitted pursuant to the applicable provisions of the Bylaws or Rule 14a-8 under the Exchange Act, unless Shareholders have power to vote on the Shareholder proposal, or the subject matter of the Shareholder proposal, pursuant to the Declaration of Trust, irrespective of whether such Shareholder proposal is submitted as a precatory recommendation to the Board. |

| ■ | No person shall be eligible for election as a Trustee of the Fund unless nominated in accordance with the procedures set forth in the Bylaws. |

The Fund’s Declaration of Trust and Bylaws contain other provisions, including all requirements for the conduct of shareholder meetings, and are available in their entirety upon request to the Fund’s Secretary, c/o Invesco Advisers, Inc.,

1555 Peachtree Street NE, Atlanta, GA 30309.

NOT FDIC INSURED | MAY LOSE VALUE | NO BANK GUARANTEE

Dividend Reinvestment Plan

The dividend reinvestment plan (the Plan) offers you a prompt and simple way to reinvest your dividends and capital gains distributions (Distributions) into additional shares of your Invesco closed-end Fund (the Fund). Under the Plan, the money you earn from Distributions will be reinvested automatically in more shares of the Fund, allowing you to potentially increase your investment over time. All shareholders in the Fund are automatically enrolled in the Plan when shares are purchased.

You may increase your shares in your Fund easily and automatically with the Plan.

Shareholders who participate in the Plan may be able to buy shares at below-market prices when the Fund is trading at a premium to its net asset value (NAV). In addition, transaction costs are low because when new shares are issued by the Fund, there is no brokerage fee, and when shares are bought in blocks on the open market, the per share fee is shared among all participants.

You will receive a detailed account statement from Computershare Trust Company, N.A. (the Agent), which administers the Plan. The statement shows your total Distributions, date of investment, shares acquired, and price per share, as well as the total number of shares in your reinvestment account. You can also access your account at invesco.com/closed-end.

The Agent will hold the shares it has acquired for you in safekeeping.

| Who can participate in the Plan |

| If you own shares in your own name, your purchase will automatically enroll you in the Plan. If your shares are held in “street name” – in the name of your brokerage firm, bank, or other financial institution – you must instruct that entity to participate on your behalf. If they are unable to participate on your behalf, you may request that they reregister your shares in your own name so that you may enroll in the Plan. |

| How to enroll |

| If you haven’t participated in the Plan in the past or chose to opt out, you are still eligible to participate. Enroll by visiting invesco.com/closed-end, by calling toll-free 800 341 2929 or by notifying us in writing at Invesco Closed-End Funds, Computer-share Trust Company, N.A., P.O. Box 505000, Louisville, KY 40233-5000. If you are writing to us, please include the Fund name and account number and ensure that all shareholders listed on the account sign these written instructions. Your participation in the Plan will begin with the next Distribution payable after the Agent receives your authorization, as long as they receive it before the “record date,” which is generally 10 business days before the Distribution is paid. If your authorization arrives after such record date, your participation in the Plan will begin with the following Distribution. |

| How the Plan works |

If you choose to participate in the Plan, your Distributions will be promptly reinvested for you, automatically increasing your shares. If the Fund is trading at a share price that is equal to its NAV, you’ll pay that amount for your reinvested shares. However, if the Fund is trading above or below NAV, the price is determined by one of two ways: |

| 1. | Premium: If the Fund is trading at a premium - a market price that is higher than its NAV -you’ll pay either the NAV or 95 percent of |

| the market price, whichever is greater. When the Fund trades at a premium, you may pay less for your reinvested shares than an investor purchasing shares on the stock exchange. Keep in mind, a portion of your price reduction may be taxable because you are receiving shares at less than market price. |

| 2. | Discount: If the Fund is trading at a discount - a market price that is lower than its NAV -you’ll pay the market price for your reinvested shares. |

| Costs of the Plan |

| There is no direct charge to you for reinvesting Distributions because the Plan’s fees are paid by the Fund. If the Fund is trading at or above its NAV, your new shares are issued directly by the Fund and there are no brokerage charges or fees. However, if the Fund is trading at a discount , the shares are purchased on the open market, and you will pay your portion of any per share fees. These per share fees are typically less than the standard brokerage charges for individual transactions because shares are purchased for all participants in blocks, resulting in lower fees for each individual participant. Any service or per share fees are added to the purchase price. Per share fees include any applicable brokerage commissions the Agent is required to pay. |

| Tax implications |

| The automatic reinvestment of Distributions does not relieve you of any income tax that may be due on Distributions. You will receive tax information annually to help you prepare your federal income tax return. |

| Invesco does not offer tax advice. The tax information contained herein is general and is not exhaustive by nature. It was not intended or written to be used, and it cannot be used, by any taxpayer for avoiding penalties that may be imposed on the taxpayer under US federal tax laws. Federal and state tax laws are complex and constantly changing. Shareholders should always consult a legal or tax adviser for information concerning their individual situation. |

| How to withdraw from the Plan |

You may withdraw from the Plan at any time by calling 800 341 2929, by visiting invesco.com/ closed-end or by writing to Invesco Closed-End Funds, Computershare Trust Company, N.A., P.O. Box 505000, Louisville, KY 40233-5000. Simply indicate that you would like to withdraw from the Plan, and be sure to include your Fund name and account number. Also, ensure that all shareholders listed on the account sign these written instructions. If you withdraw, you have three options with regard to the shares held in the Plan: |

| 1. | If you opt to continue to hold your non-certificated whole shares (Investment Plan Book Shares), they will be held by the Agent electronically as Direct Registration Book-Shares (Book-Entry Shares) and fractional shares will be sold at the then-current market price. Proceeds will be sent via check to your address of record after deducting applicable fees, including per share fees such as any applicable brokerage commissions the Agent is required to pay. |

| 2. | If you opt to sell your shares through the Agent, we will sell all full and fractional shares and send the proceeds via check to your address of record after deducting a $2.50 service fee and per share fees. Per share fees include any applicable brokerage commissions the Agent is required to pay. |

| 3. | You may sell your shares through your financial adviser through the Direct Registration System (DRS). DRS is a service within the securities industry that allows Fund shares to be held in your name in electronic format. You retain full ownership of your shares, without having to hold a share certificate. You should contact your financial adviser to learn more about any restrictions or fees that may apply. |

| The Fund and Computershare Trust Company, N.A. may amend or terminate the Plan at any time. Participants will receive at least 30 days written notice before the effective date of any amendment. In the case of termination, Participants will receive at least 30 days written notice before the record date for the payment of any such Distributions by the Fund. In the case of amendment or termination necessary or appropriate to comply with applicable law or the rules and policies of the Securities and Exchange Commission or any other regulatory authority, such written notice will not be required. |

| To obtain a complete copy of the current Dividend Reinvestment Plan, please call our Client Services department at 800 341 2929 or visit invesco.com/closed-end. |

Fund Information

| Portfolio Composition | |

| By security type | % of total net assets |

| U.S. Dollar Denominated Bonds & Notes | 87.47% |

| Preferred Stocks | 5.29 |

| U.S. Treasury Securities | 3.12 |

| Security Types Each Less Than 1% of Portfolio | 1.37 |

| Money Market Funds Plus Other Assets Less Liabilities | 2.75 |

Top Five Debt Issuers*

| | | % of total net assets |

| 1. | AT&T, Inc. | 2.53% |

| 2. | U.S. Treasury Bonds | 2.06 |

| 3. | Corning, Inc. | 1.72 |

| 4. | Citigroup, Inc. | 1.64 |

| 5. | Bank of America Corp. | 1.38 |

| The Fund’s holdings are subject to change, and there is no assurance that the Fund will continue to hold any particular security. |

* Excluding money market fund holdings, if any.

Data presented here are as of February 28, 2021.

Schedule of Investments(a)

February 28, 2021

| | | Principal

Amount | | Value | |

| U.S. Dollar Denominated Bonds & Notes–87.47% |

| Advertising–0.47% | | | | | | | |

| Interpublic Group of Cos., Inc. (The), | | | | | | | |

| 4.75%, 03/30/2030 | | $ | 530,000 | | $ | 632,192 | |

| Lamar Media Corp., | | | | | | | |

| 3.75%, 02/15/2028 | | | 374,000 | | | 379,376 | |

| 3.63%, 01/15/2031(b) | | | 100,000 | | | 98,938 | |

| | | | | | | 1,110,506 | |

| | | | | | | | |

| Aerospace & Defense–0.41% | | | | | | | |

| Boeing Co. (The), | | | | | | | |

| 2.75%, 02/01/2026 | | | 383,000 | | | 396,871 | |

| 2.20%, 02/04/2026 | | | 485,000 | | | 486,101 | |

| Howmet Aerospace, Inc., 6.88%, 05/01/2025 | | | 36,000 | | | 41,875 | |

| TransDigm, Inc., 6.38%, 06/15/2026 | | | 48,000 | | | 49,539 | |

| | | | | | | 974,386 | |

| | | | | | | | |

| Agricultural & Farm Machinery–0.02% | | | | | | | |

| Titan International, Inc., 6.50%, 11/30/2023 | | | 57,000 | | | 55,937 | |

| | | | | | | | |

| Agricultural Products–0.21% | | | | | | | |

| Cargill, Inc., | | | | | | | |

| 0.75%, 02/02/2026(b) | | | 191,000 | | | 187,948 | |

| 1.70%, 02/02/2031(b) | | | 325,000 | | | 316,135 | |

| | | | | | | 504,083 | |

| | | | | | | | |

| Airlines–2.65% | | | | | | | |

| American Airlines Pass-Through Trust, | | | | | | | |

| Series 2017-1, Class AA, 3.65%, 02/15/2029 | | | 451,605 | | | 458,072 | |

| Series 2017-2, Class AA, 3.35%, 10/15/2029 | | | 431,483 | | | 431,728 | |

| British Airways Pass-Through Trust (United Kingdom), Series 2019-1, Class AA, 3.30%, 12/15/2032(b) | | | 546,024 | | | 542,636 | |

| Delta Air Lines Pass-Through Trust, | | | | | | | |

| Series 2019-1, Class A, 3.40%, 04/25/2024 | | | 447,000 | | | 451,823 | |

| Series 2020-1, Class AA, 2.00%, 06/10/2028 | | | 334,686 | | | 339,897 | |

| Delta Air Lines, Inc., | | | | | | | |

| 7.00%, 05/01/2025(b) | | | 135,000 | | | 157,393 | |

| 7.38%, 01/15/2026 | | | 90,000 | | | 105,518 | |

| Delta Air Lines, Inc./SkyMiles IP Ltd., | | | | | | | |

| 4.50%, 10/20/2025(b) | | | 372,000 | | | 397,437 | |

| 4.75%, 10/20/2028(b) | | | 624,000 | | | 693,290 | |

| | | Principal

Amount | | Value | |

| Airlines–(continued) | | | | | | | |

| United Airlines Pass-Through Trust, | | | | | | | |

| Series 2014-2, Class B, 4.63%, 09/03/2022 | | $ | 333,489 | | $ | 337,839 | |

| Series 2016-1, Class B, 3.65%, 01/07/2026 | | | 295,736 | | | 291,692 | |

| Series 2020-1, Class A, 5.88%, 10/15/2027 | | | 616,721 | | | 694,224 | |

| Series 2018-1, Class AA, 3.50%, 03/01/2030 | | | 554,937 | | | 568,182 | |

| Series 2019-1, Class A, 4.55%, 08/25/2031 | | | 269,863 | | | 277,224 | |

| Series 2019-1, Class AA, 4.15%, 08/25/2031 | | | 524,928 | | | 550,405 | |

| | | | | | | 6,297,360 | |

| | | | | | | | |

| Aluminum–0.09% | | | | | | | |

| Alcoa Nederland Holding B.V., 6.75%, 09/30/2024(b) | | | 200,000 | | | 207,875 | |

| | | | | | | | |

| Apparel Retail–0.18% | | | | | | | |

| L Brands, Inc., | | | | | | | |

| 6.88%, 11/01/2035 | | | 26,000 | | | 31,582 | |

| 6.75%, 07/01/2036 | | | 119,000 | | | 143,321 | |

| Ross Stores, Inc., 0.88%, 04/15/2026 | | | 257,000 | | | 252,879 | |

| | | | | | | 427,782 | |

| | | | | | | | |

| Apparel, Accessories & Luxury Goods–0.03% |

| Hanesbrands, Inc., | | | | | | | |

| 4.63%, 05/15/2024(b) | | | 11,000 | | | 11,543 | |

| 4.88%, 05/15/2026(b) | | | 63,000 | | | 67,944 | |

| | | | | | | 79,487 | |

| Application Software–0.16% | | | | | | | |

| ZoomInfo Technologies LLC/ZoomInfo Finance Corp., 3.88%, 02/01/2029(b) | | | 380,000 | | | 378,100 | |

| | | | | | | | |

| Asset Management & Custody Banks–1.57% |

| Affiliated Managers Group, Inc., 4.25%, 02/15/2024 | | | 1,112,000 | | | 1,224,024 | |

| Ameriprise Financial, Inc., 3.00%, 04/02/2025 | | | 363,000 | | | 389,966 | |

| Apollo Management Holdings L.P., 4.95%, 01/14/2050(b)(c) | | | 50,000 | | | 51,458 | |

| Carlyle Holdings II Finance LLC, 5.63%, 03/30/2043(b) | | | 1,304,000 | | | 1,616,729 | |

| CI Financial Corp. (Canada), 3.20%, 12/17/2030 | | | 444,000 | | | 446,880 | |

| | | | | | | 3,729,057 | |

| | | | | | | | |

| Auto Parts & Equipment–0.04% | | | | | | | |

| Clarios Global L.P./Clarios US Finance Co., 8.50%, 05/15/2027(b) | | | 30,000 | | | 32,420 | |

| Dana Financing Luxembourg S.a.r.l., 5.75%, 04/15/2025(b) | | | 22,000 | | | 22,635 | |

| Dana, Inc., 5.38%, 11/15/2027 | | | 37,000 | | | 38,734 | |

| | | | | | | 93,789 | |

See accompanying Notes to Financial Statements which are an integral part of the financial statements.

| | | Principal

Amount | | Value | |

| Automobile Manufacturers–1.49% | | | | | | | |

| Allison Transmission, Inc., 3.75%, 01/30/2031(b) | | $ | 316,000 | | $ | 302,767 | |

| Ford Motor Co., | | | | | | | |

| 8.50%, 04/21/2023 | | | 88,000 | | | 98,450 | |

| 9.00%, 04/22/2025 | | | 169,000 | | | 204,669 | |

| 9.63%, 04/22/2030 | | | 38,000 | | | 53,819 | |

| 4.75%, 01/15/2043 | | | 71,000 | | | 72,076 | |

| Ford Motor Credit Co. LLC, 3.38%, 11/13/2025 | | | 206,000 | | | 209,628 | |

| Hyundai Capital America, | | | | | | | |

| 2.85%, 11/01/2022(b) | | | 364,000 | | | 376,638 | |

| 4.30%, 02/01/2024(b) | | | 1,788,000 | | | 1,957,667 | |

| J.B. Poindexter & Co., Inc., 7.13%, 04/15/2026(b) | | | 54,000 | | | 57,105 | |

| Volkswagen Group of America Finance LLC (Germany), 1.63%, 11/24/2027(b) | | | 200,000 | | | 198,209 | |

| | | | | | | 3,531,028 | |

| | | | | | | | |

| Automotive Retail–0.11% | | | | | | | |

| Advance Auto Parts, Inc., 3.90%, 04/15/2030 | | | 25,000 | | | 27,888 | |

| Group 1 Automotive, Inc., 4.00%, 08/15/2028(b) | | | 120,000 | | | 121,350 | |

| Lithia Motors, Inc., | | | | | | | |

| 5.25%, 08/01/2025(b) | | | 19,000 | | | 19,691 | |

| 4.63%, 12/15/2027(b) | | | 18,000 | | | 18,934 | |

| 4.38%, 01/15/2031(b) | | | 16,000 | | | 16,830 | |

| Penske Automotive Group, Inc., 5.50%, 05/15/2026 | | | 59,000 | | | 60,880 | |

| | | | | | | 265,573 | |

| | | | | | | | |

| Biotechnology–0.58% | | | | | | | |

| AbbVie, Inc., 4.05%, 11/21/2039 | | | 1,039,000 | | | 1,194,815 | |

| Amgen, Inc., 2.45%, 02/21/2030 | | | 169,000 | | | 174,207 | |

| | | | | | | 1,369,022 | |

| | | | | | | | |

| Brewers–0.24% | | | | | | | |

| Anheuser-Busch InBev Worldwide, Inc. | | | | | | | |

| (Belgium), 8.00%, 11/15/2039 | | | 343,000 | | | 559,008 | |

| | | | | | | | |

| Broadcasting–0.09% | | | | | | | |

| Fox Corp., 3.50%, 04/08/2030 | | | 120,000 | | | 130,786 | |

| Gray Television, Inc., 7.00%, 05/15/2027(b) | | | 75,000 | | | 82,031 | |

| | | | | | | 212,817 | |

| | | | | | | | |

| Building Products–0.13% | | | | | | | |

| Masco Corp., | | | | | | | |

| 2.00%, 02/15/2031 | | | 155,000 | | | 152,049 | |

| 3.13%, 02/15/2051 | | | 149,000 | | | 147,582 | |

| | | | | | | 299,631 | |

| | | | | | | | |

| Cable & Satellite–1.62% | | | | | | | |

| CCO Holdings LLC/CCO Holdings Capital Corp., | | | | | | | |

| 5.75%, 02/15/2026(b) | | | 149,000 | | | 154,185 | |

| 5.00%, 02/01/2028(b) | | | 31,000 | | | 32,503 | |

| 4.50%, 08/15/2030(b) | | | 99,000 | | | 102,639 | |

| 4.25%, 02/01/2031(b) | | | 140,000 | | | 141,925 | |

| | | Principal

Amount | | Value | |

| Cable & Satellite–(continued) | | | | | | | |

| Charter Communications Operating LLC/ | | | | | | | |

| Charter Communications Operating Capital Corp., | | | | | | | |

| 4.91%, 07/23/2025 | | $ | 40,000 | | $ | 45,680 | |

| 5.38%, 04/01/2038 | | | 42,000 | | | 50,329 | |

| 3.50%, 06/01/2041 | | | 322,000 | | | 311,822 | |

| 5.75%, 04/01/2048 | | | 316,000 | | | 390,149 | |

| 3.85%, 04/01/2061 | | | 446,000 | | | 413,324 | |

| Comcast Corp., | | | | | | | |

| 6.45%, 03/15/2037 | | | 531,000 | | | 773,350 | |

| 4.60%, 10/15/2038 | | | 326,000 | | | 406,592 | |

| 3.25%, 11/01/2039 | | | 115,000 | | | 122,624 | |

| 2.80%, 01/15/2051 | | | 357,000 | | | 334,992 | |

| Cox Communications, Inc., | | | | | | | |

| 1.80%, 10/01/2030(b) | | | 124,000 | | | 118,715 | |

| 2.95%, 10/01/2050(b) | | | 198,000 | | | 183,058 | |

| CSC Holdings LLC, | | | | | | | |

| 6.75%, 11/15/2021 | | | 67,000 | | | 69,303 | |

| 5.25%, 06/01/2024 | | | 94,000 | | | 101,344 | |

| DISH DBS Corp., | | | | | | | |

| 5.88%, 11/15/2024 | | | 40,000 | | | 41,915 | |

| 7.75%, 07/01/2026 | | | 22,000 | | | 24,239 | |

| Intelsat Jackson Holdings S.A. (Luxembourg), 8.50%, 10/15/2024(b)(d) | | | 43,000 | | | 28,053 | |

| | | | | | | 3,846,741 | |

| | | | | | | | |

| Casinos & Gaming–0.17% | | | | | | | |

| CCM Merger, Inc., 6.38%, 05/01/2026(b) | | | 81,000 | | | 86,062 | |

| MGM Resorts International, | | | | | | | |

| 7.75%, 03/15/2022 | | | 42,000 | | | 44,389 | |

| 6.00%, 03/15/2023 | | | 67,000 | | | 71,523 | |

| Mohegan Gaming & Entertainment, | | | | | | | |

| 8.00%, 02/01/2026(b) | | | 71,000 | | | 70,290 | |

| Scientific Games International, Inc., | | | | | | | |

| 8.25%, 03/15/2026(b) | | | 119,000 | | | 126,346 | |

| | | | | | | 398,610 | |

| | | | | | | | |

| Coal & Consumable Fuels–0.05% | | | | | | | |

| SunCoke Energy Partners L.P./SunCoke Energy Partners Finance Corp., 7.50%, 06/15/2025(b) | | | 105,000 | | | 109,166 | |

| | | | | | | | |

| Commodity Chemicals–0.18% | | | | | | | |

| Alpek S.A.B. de C.V. (Mexico), 3.25%, 02/25/2031(b) | | | 200,000 | | | 199,500 | |

| Axalta Coating Systems LLC, 3.38%, 02/15/2029(b) | | | 245,000 | | | 238,109 | |

| | | | | | | 437,609 | |

| | | | | | | | |

| Computer & Electronics Retail–0.02% | | | | | | | |

| Rent-A-Center, Inc., 6.38%, 02/15/2029(b) | | | 52,000 | | | 54,216 | |

| | | | | | | | |

| Construction & Engineering–0.04% | | | | | | | |

| AECOM, 5.13%, 03/15/2027 | | | 24,000 | | | 26,280 | |

| New Enterprise Stone & Lime Co., Inc., | | | | | | | |

| 6.25%, 03/15/2026(b) | | | 40,000 | | | 41,275 | |

| 9.75%, 07/15/2028(b) | | | 33,000 | | | 37,125 | |

| | | | | | | 104,680 | |

See accompanying Notes to Financial Statements which are an integral part of the financial statements.

| | | Principal

Amount | | Value | |

| Construction Materials–0.18% | | | | | | | |

| CRH America Finance, Inc. (Ireland), | | | | | | | |

| 3.95%, 04/04/2028(b) | | $ | 384,000 | | $ | 437,712 | |

| | | | | | | | |

| Consumer Finance–0.38% | | | | | | | |

| Ally Financial, Inc., | | | | | | | |

| 5.13%, 09/30/2024 | | | 34,000 | | | 38,828 | |

| 4.63%, 03/30/2025 | | | 223,000 | | | 251,154 | |

| Navient Corp., | | | | | | | |

| 7.25%, 01/25/2022 | | | 25,000 | | | 25,984 | |

| 7.25%, 09/25/2023 | | | 184,000 | | | 199,985 | |

| 5.00%, 03/15/2027 | | | 82,000 | | | 80,473 | |

| 5.63%, 08/01/2033 | | | 28,000 | | | 25,672 | |

| OneMain Finance Corp., | | | | | | | |

| 6.88%, 03/15/2025 | | | 50,000 | | | 56,488 | |

| 7.13%, 03/15/2026 | | | 120,000 | | | 138,751 | |

| 5.38%, 11/15/2029 | | | 90,000 | | | 95,175 | |

| | | | | | | 912,510 | |

| | | | | | | | |

| Copper–0.15% | | | | | | | |

| Freeport-McMoRan, Inc., | | | | | | | |

| 4.38%, 08/01/2028 | | | 161,000 | | | 171,910 | |

| 5.40%, 11/14/2034 | | | 139,000 | | | 172,447 | |

| | | | | | | 344,357 | |

| | | | | | | | |

| Data Processing & Outsourced Services–0.13% |

| Cardtronics, Inc./Cardtronics USA, Inc., | | | | | | | |

| 5.50%, 05/01/2025(b) | | | 115,000 | | | 119,025 | |

| Fidelity National Information Services, Inc., | | | | | | | |

| 2.25%, 03/01/2031 | | | 50,000 | | | 49,808 | |

| 3.10%, 03/01/2041 | | | 140,000 | | | 141,935 | |

| | | | | | | 310,768 | |

| | | | | | | | |

| Department Stores–0.20% | | | | | | | |

| 7-Eleven, Inc., 1.80%, 02/10/2031(b) | | | 223,000 | | | 214,696 | |

| Macy’s, Inc., 8.38%, 06/15/2025(b) | | | 236,000 | | | 261,120 | |

| | | | | | | 475,816 | |

| | | | | | | | |

| Diversified Banks–10.56% | | | | | | | |

| Africa Finance Corp. (Supranational), 4.38%, 04/17/2026(b) | | | 1,080,000 | | | 1,182,438 | |

| Australia & New Zealand Banking Group Ltd. (Australia), 2.57%, 11/25/2035(b)(c) | | | 229,000 | | | 223,720 | |

| 6.75%(b)(c)(e) | | | 765,000 | | | 905,894 | |

| Bank of America Corp., | | | | | | | |

| 7.75%, 05/14/2038 | | | 765,000 | | | 1,234,414 | |

| 2.68%, 06/19/2041(c) | | | 75,000 | | | 72,819 | |

| Series AA, 6.10%(e)(f) | | | 1,369,000 | | | 1,522,047 | |

| Series DD, 6.30%(c)(e) | | | 402,000 | | | 461,799 | |

| Bank of China Ltd. (China), 5.00%, 11/13/2024(b) | | | 540,000 | | | 608,412 | |

| BBVA Bancomer S.A. (Mexico), | | | | | | | |

| 4.38%, 04/10/2024(b) | | | 535,000 | | | 583,155 | |

| 1.88%, 09/18/2025(b) | | | 250,000 | | | 252,531 | |

| BNP Paribas S.A. (France), 2.82%, 01/26/2041(b) | | | 606,000 | | | 569,819 | |

| BPCE S.A. (France), 2.28%, 01/20/2032(b)(c) | | | 260,000 | | | 258,554 | |

| | | Principal

Amount | | Value | |

| Diversified Banks–(continued) | | | | | | | |

| Citigroup, Inc., | | | | | | | |

| 5.50%, 09/13/2025 | | $ | 1,116,000 | | $ | 1,321,013 | |

| 3.11%, 04/08/2026(c) | | | 414,000 | | | 445,487 | |

| 4.41%, 03/31/2031(c) | | | 335,000 | | | 390,000 | |

| 2.57%, 06/03/2031(c) | | | 60,000 | | | 61,522 | |

| 4.65%, 07/23/2048 | | | 249,000 | | | 317,991 | |

| 3.88%(e)(f) | | | 619,000 | | | 617,453 | |

| Series A, 5.95%(e)(f) | | | 108,000 | | | 112,631 | |

| Series Q, 4.29% (3 mo. USD LIBOR + 4.10%)(e)(f) | | | 350,000 | | | 349,125 | |

| Series V, 4.70%(c)(e) | | | 260,000 | | | 263,140 | |

| Credit Agricole S.A. (France), | | | | | | | |

| 1.91%, 06/16/2026(b)(c) | | | 250,000 | | | 256,777 | |

| 7.88%(b)(e)(f) | | | 200,000 | | | 224,577 | |

| Federation des Caisses Desjardins du Quebec (Canada), 2.05%, 02/10/2025(b) | | | 615,000 | | | 638,461 | |

| Global Bank Corp. (Panama), 4.50%, 10/20/2021(b) | | | 772,000 | | | 784,198 | |

| HSBC Holdings PLC (United Kingdom), | | | | | | | |

| 1.65%, 04/18/2026(c) | | | 202,000 | | | 204,396 | |

| 2.01%, 09/22/2028(c) | | | 575,000 | | | 578,244 | |

| 6.00%(c)(e) | | | 845,000 | | | 921,050 | |

| 6.25%(c)(e) | | | 200,000 | | | 212,500 | |

| 4.60%(c)(e) | | | 312,000 | | | 314,371 | |

| ING Groep N.V. (Netherlands), | | | | | | | |

| 6.88%(b)(c)(e) | | | 409,000 | | | 426,919 | |

| JPMorgan Chase & Co., 1.11% (3 mo. USD LIBOR + 0.89%), 07/23/2024(f) | | | 756,000 | | | 768,474 | |

| Series W, 1.19% (3 mo. USD LIBOR + 1.00%), 05/15/2047(f) | | | 790,000 | | | 675,450 | |

| Series V, 3.56% (3 mo. USD LIBOR + 3.32%)(e)(f) | | | 490,000 | | | 486,693 | |

| Mizuho Financial Group, Inc. (Japan), | | | | | | | |

| 2.17%, 05/22/2032(f) | | | 500,000 | | | 494,274 | |

| SMBC Aviation Capital Finance DAC (Ireland), | | | | | | | |

| 3.00%, 07/15/2022(b) | | | 474,000 | | | 485,819 | |

| 4.13%, 07/15/2023(b) | | | 552,000 | | | 590,521 | |

| Standard Chartered PLC (United Kingdom), 1.43% (3 mo. USD LIBOR + 1.20%), 09/10/2022(b)(f) | | | 442,000 | | | 444,268 | |

| 4.30%, 02/19/2027(b) | | | 300,000 | | | 330,065 | |

| 3.27%, 02/18/2036(b)(c) | | | 471,000 | | | 466,665 | |

| 7.75%(b)(c)(e) | | | 459,000 | | | 504,537 | |

| 7.50%(b)(c)(e) | | | 210,000 | | | 220,089 | |

| Sumitomo Mitsui Financial Group, Inc. | | | | | | | |

| (Japan), 2.14%, 09/23/2030 | | | 50,000 | | | 48,890 | |

| U.S. Bancorp, Series I, 3.73% (3 mo. USD LIBOR + 3.49%)(e)(f) | | | 296,000 | | | 294,890 | |

| Wells Fargo & Co., | | | | | | | |

| 5.38%, 11/02/2043 | | | 1,685,000 | | | 2,179,756 | |

| 4.75%, 12/07/2046 | | | 344,000 | | | 423,876 | |

| 3.90%(e)(f) | | | 372,000 | | | 370,800 | |

| | | | | | | 25,100,524 | |

See accompanying Notes to Financial Statements which are an integral part of the financial statements.

| | | Principal

Amount | | Value | |

| Diversified Capital Markets–1.64% | | | | | | | |

| Credit Suisse Group AG (Switzerland), | | | | | | | |

| 4.19%, 04/01/2031(b)(c) | | $ | 280,000 | | $ | 319,373 | |

| 7.13%(b)(c)(e) | | | 426,000 | | | 448,574 | |

| 7.50%(b)(c)(e) | | | 792,000 | | | 868,270 | |

| 5.10%(b)(c)(e) | | | 478,000 | | | 488,158 | |

| 5.25%(b)(c)(e) | | | 448,000 | | | 477,120 | |

| 4.50%(b)(c)(e) | | | 468,000 | | | 458,055 | |

| Macquarie Bank Ltd. (Australia), | | | | | | | |

| 6.13%(b)(c)(e) | | | 530,000 | | | 573,505 | |

| UBS Group AG (Switzerland), 4.38%(b)(e) | | | 258,000 | | | 254,852 | |

| | | | | | | 3,887,907 | |

| | | | | | | | |

| Diversified Metals & Mining–0.97% | | | | | | | |

| Anglo American Capital PLC (South Africa), 5.63%, 04/01/2030(b) | | | 404,000 | | | 501,405 | |

| Corp. Nacional del Cobre de Chile (Chile), | | | | | | | |

| 3.15%, 01/15/2051(b) | | | 200,000 | | | 182,542 | |

| Teck Resources Ltd. (Canada), | | | | | | | |

| 6.13%, 10/01/2035 | | | 492,000 | | | 629,976 | |

| 6.25%, 07/15/2041 | | | 762,000 | | | 996,930 | |

| | | | | | | 2,310,853 | |

| | | | | | | | |

| Diversified REITs–1.26% | | | | | | | |

| iStar, Inc., 4.75%, 10/01/2024 | | | 90,000 | | | 92,522 | |

| Trust Fibra Uno (Mexico), | | | | | | | |

| 5.25%, 12/15/2024(b) | | | 283,000 | | | 313,423 | |

| 5.25%, 01/30/2026(b) | | | 764,000 | | | 851,287 | |

| 4.87%, 01/15/2030(b) | | | 360,000 | | | 389,340 | |

| 6.39%, 01/15/2050(b) | | | 1,180,000 | | | 1,345,200 | |

| | | | | | | 2,991,772 | |

| | | | | | | | |

| Drug Retail–0.93% | | | | | | | |

| CVS Pass-Through Trust, | | | | | | | |

| 6.04%, 12/10/2028 | | | 723,727 | | | 838,379 | |

| 5.77%, 01/10/2033(b) | | | 1,166,449 | | | 1,366,289 | |

| | | | | | | 2,204,668 | |

| | | | | | | | |

| Electric Utilities–2.96% | | | | | | | |

| Consolidated Edison Co. of New York, Inc., Series C, 3.00%, 12/01/2060 | | | 436,000 | | | 404,531 | |

| Drax Finco PLC (United Kingdom), 6.63%, 11/01/2025(b) | | | 400,000 | | | 415,750 | |

| Duke Energy Progress LLC, 2.50%, 08/15/2050 | | | 587,000 | | | 532,827 | |

| Electricite de France S.A. (France), 6.00%, 01/22/2114(b) | | | 1,755,000 | | | 2,407,299 | |

| Eversource Energy, Series R, 1.65%, 08/15/2030 | | | 158,000 | | | 152,643 | |

| Georgia Power Co., | | | | | | | |

| 2.85%, 05/15/2022 | | | 275,000 | | | 283,201 | |

| Series A, 2.20%, 09/15/2024 | | | 1,285,000 | | | 1,347,444 | |

| NextEra Energy Operating Partners L.P., | | | | | | | |

| 3.88%, 10/15/2026(b) | | | 53,000 | | | 56,809 | |

| 4.50%, 09/15/2027(b) | | | 21,000 | | | 23,440 | |

| Southern Co. (The), | | | | | | | |

| Series B, | | | | | | | |

| 4.00%, 01/15/2051(c) | | | 437,000 | | | 456,557 | |

| 5.50%, 03/15/2057(c) | | | 734,000 | | | 758,421 | |

| Talen Energy Supply LLC, 7.63%, 06/01/2028(b) | | | 79,000 | | | 84,248 | |

| Virginia Electric & Power Co., 2.45%, 12/15/2050 | | | 61,000 | | | 54,998 | |

| | | Principal

Amount | | Value | |

| Electric Utilities–(continued) | | | | | | | |

| Vistra Operations Co. LLC, 5.00%, 07/31/2027(b) | | $ | 55,000 | | $ | 57,599 | |

| | | | | | | 7,035,767 | |

| | | | | | | | |

| Electrical Components & Equipment–0.20% | | | | | | | |

| Acuity Brands Lighting, Inc., 2.15%, 12/15/2030 | | | 376,000 | | | 368,468 | |

| EnerSys, | | | | | | | |

| 5.00%, 04/30/2023(b) | | | 76,000 | | | 79,899 | |

| 4.38%, 12/15/2027(b) | | | 18,000 | | | 19,035 | |

| | | | | | | 467,402 | |

| | | | | | | | |

| Electronic Components–1.76% | | | | | | | |

| Corning, Inc., 5.45%, 11/15/2079 | | | 3,134,000 | | | 4,077,083 | |

| Sensata Technologies, Inc., 3.75%, 02/15/2031(b) | | | 100,000 | | | 100,500 | |

| | | | | | | 4,177,583 | |

| | | | | | | | |

| Electronic Manufacturing Services–0.19% | | | | | | | |

| Jabil, Inc., 3.00%, 01/15/2031 | | | 450,000 | | | 460,535 | |

| | | | | | | | |

| Financial Exchanges & Data–0.53% | | | | | | | |

| Moody’s Corp., | | | | | | | |

| 5.25%, 07/15/2044 | | | 389,000 | | | 515,115 | |

| 3.25%, 05/20/2050 | | | 131,000 | | | 133,337 | |

| 2.55%, 08/18/2060 | | | 124,000 | | | 104,274 | |

| MSCI, Inc., 3.88%, 02/15/2031(b) | | | 257,000 | | | 270,171 | |

| S&P Global, Inc., 1.25%, 08/15/2030 | | | 247,000 | | | 233,621 | |

| | | | | | | 1,256,518 | |

| | | | | | | | |

| Food Retail–0.30% | | | | | | | |

| Albertsons Cos., Inc./Safeway, Inc./New | | | | | | | |

| Albertsons L.P./Albertson’s LLC, 3.50%, 02/15/2023(b) | | | 394,000 | | | 405,312 | |

| SEG Holding LLC/SEG Finance Corp., 5.63%, 10/15/2028(b) | | | 79,000 | | | 83,937 | |

| Simmons Foods, Inc., 5.75%, 11/01/2024(b) | | | 100,000 | | | 103,310 | |

| Simmons Foods, Inc./Simmons Prepared Foods, Inc./Simmons Pet Food, Inc., 4.63%, 03/01/2029(b) | | | 125,000 | | | 126,847 | |

| | | | | | | 719,406 | |

| | | | | | | | |

| Health Care Facilities–0.61% | | | | | | | |

| Acadia Healthcare Co., Inc., 5.00%, 04/15/2029(b) | | | 150,000 | | | 156,938 | |

| Encompass Health Corp., 4.75%, 02/01/2030 | | | 148,000 | | | 156,815 | |

| HCA, Inc., | | | | | | | |

| 5.00%, 03/15/2024 | | | 733,000 | | | 821,263 | |

| 5.38%, 02/01/2025 | | | 39,000 | | | 43,787 | |

| 5.25%, 04/15/2025 | | | 30,000 | | | 34,585 | |

| 5.88%, 02/15/2026 | | | 71,000 | | | 82,161 | |

| 5.38%, 09/01/2026 | | | 18,000 | | | 20,578 | |

| 7.50%, 11/06/2033 | | | 49,000 | | | 67,549 | |

| 5.50%, 06/15/2047 | | | 49,000 | | | 62,707 | |

| | | | | | | 1,446,383 | |

| | | | | | | | |

| Health Care REITs–0.95% | | | | | | | |

| Diversified Healthcare Trust, | | | | | | | |

| 6.75%, 12/15/2021 | | | 1,090,000 | | | 1,106,350 | |

| 9.75%, 06/15/2025 | | | 81,000 | | | 91,328 | |

| 4.38%, 03/01/2031 | | | 184,000 | | | 182,390 | |

See accompanying Notes to Financial Statements which are an integral part of the financial statements.

| | | Principal

Amount | | Value | |

| Health Care REITs–(continued) | | | | | | | |

| MPT Operating Partnership L.P./MPT Finance Corp., 4.63%, 08/01/2029 | | $ | 328,000 | | $ | 353,215 | |

| National Health Investors, Inc., 3.00%, 02/01/2031 | | | 205,000 | | | 199,450 | |

| Physicians Realty L.P., 4.30%, 03/15/2027 | | | 284,000 | | | 317,015 | |

| | | | | | | 2,249,748 | |

| | | | | | | | |

| Health Care Services–1.53% | | | | | | | |

| Akumin, Inc., 7.00%, 11/01/2025(b) | | | 163,000 | | | 170,742 | |

| Baylor Scott & White Holdings, Series 2021, 2.84%, 11/15/2050 | | | 252,000 | | | 248,299 | |

| Cigna Corp., | | | | | | | |

| 3.75%, 07/15/2023 | | | 523,000 | | | 562,874 | |

| 1.13% (3 mo. USD LIBOR + 0.89%), 07/15/2023(f) | | | 742,000 | | | 752,188 | |

| 3.00%, 07/15/2023 | | | 961,000 | | | 1,015,063 | |

| 4.80%, 08/15/2038 | | | 40,000 | | | 49,572 | |

| CommonSpirit Health, 1.55%, 10/01/2025 | | | 140,000 | | | 141,831 | |

| CVS Health Corp., 1.30%, 08/21/2027 | | | 278,000 | | | 272,196 | |

| DaVita, Inc., | | | | | | | |

| 4.63%, 06/01/2030(b) | | | 36,000 | | | 36,652 | |

| 3.75%, 02/15/2031(b) | | | 180,000 | | | 171,868 | |

| Hadrian Merger Sub, Inc., 8.50%, 05/01/2026(b) | | | 43,000 | | | 44,873 | |

| MEDNAX, Inc., 6.25%, 01/15/2027(b) | | | 83,000 | | | 87,771 | |

| RP Escrow Issuer LLC, 5.25%, 12/15/2025(b) | | | 84,000 | | | 87,045 | |

| | | | | | | 3,640,974 | |

| | | | | | | | |

| Homebuilding–0.89% | | | | | | | |

| Ashton Woods USA LLC/Ashton Woods Finance Co., 9.88%, 04/01/2027(b) | | | 55,000 | | | 62,071 | |

| Lennar Corp., | | | | | | | |

| 5.38%, 10/01/2022 | | | 56,000 | | | 59,965 | |

| 4.75%, 11/15/2022 | | | 31,000 | | | 32,619 | |

| M.D.C. Holdings, Inc., | | | | | | | |

| 3.85%, 01/15/2030 | | | 764,000 | | | 824,868 | |

| 6.00%, 01/15/2043 | | | 530,000 | | | 700,594 | |

| Mattamy Group Corp. (Canada), 4.63%, 03/01/2030(b) | | | 200,000 | | | 208,094 | |

| PulteGroup, Inc., | | | | | | | |

| 6.38%, 05/15/2033 | | | 2,000 | | | 2,650 | |

| 6.00%, 02/15/2035 | | | 66,000 | | | 87,120 | |

| Taylor Morrison Communities, Inc., | | | | | | | |

| 6.63%, 07/15/2027(b) | | | 113,000 | | | 121,334 | |

| Taylor Morrison Communities, Inc./Taylor | | | | | | | |

| Morrison Holdings II, Inc., 5.88%, 04/15/2023(b) | | | 10,000 | | | 10,636 | |

| | | | | | | 2,109,951 | |

| | | | | | | | |

| Hotels, Resorts & Cruise Lines–0.14% | | | | | | | |

| Carnival Corp., | | | | | | | |

| 11.50%, 04/01/2023(b) | | | 49,000 | | | 55,941 | |

| 10.50%, 02/01/2026(b) | | | 25,000 | | | 29,094 | |

| 5.75%, 03/01/2027(b) | | | 25,000 | | | 25,410 | |

| Hilton Domestic Operating Co., Inc., | | | | | | | |

| 3.63%, 02/15/2032(b) | | | 216,000 | | | 212,995 | |

| | | | | | | 323,440 | |

| | | Principal

Amount | | Value | |

| Household Products–0.05% | | | | | | | |

| Energizer Holdings, Inc., 4.38%, 03/31/2029(b) | | $ | 126,000 | | $ | 125,874 | |

| | | | | | | | |

| Independent Power Producers & Energy Traders–0.78% |

| AES Corp. (The), | | | | | | | |

| 1.38%, 01/15/2026(b) | | | 258,000 | | | 255,315 | |

| 2.45%, 01/15/2031(b) | | | 284,000 | | | 279,214 | |

| Calpine Corp., 3.75%, 03/01/2031(b) | | | 580,000 | | | 560,692 | |

| Clearway Energy Operating LLC, 4.75%, 03/15/2028(b) | | | 79,000 | | | 84,505 | |

| EnfraGen Energia Sur S.A./EnfraGen Spain S.A./Prime Energia S.p.A. (Spain), 5.38%, 12/30/2030(b) | | | 630,000 | | | 632,709 | |

| Enviva Partners L.P./Enviva Partners Finance Corp., 6.50%, 01/15/2026(b) | | | 35,000 | | | 36,684 | |

| | | | | | | 1,849,119 | |

| | | | | | | | |

| Industrial Conglomerates–0.87% | | | | | | | |

| GE Capital International Funding Co. Unlimited Co., 4.42%, 11/15/2035 | | | 630,000 | | | 720,281 | |

| General Electric Co., 5.55%, 01/05/2026 | | | 1,127,000 | | | 1,345,270 | |

| | | | | | | 2,065,551 | |

| | | | | | | | |

| Industrial Machinery–0.09% | | | | | | | |

| Cleaver-Brooks, Inc., 7.88%, 03/01/2023(b) | | | 42,000 | | | 41,418 | |

| EnPro Industries, Inc., 5.75%, 10/15/2026 | | | 79,000 | | | 83,725 | |

| Mueller Industries, Inc., 6.00%, 03/01/2027 | | | 80,000 | | | 81,848 | |

| | | | | | | 206,991 | |

| | | | | | | | |

| Industrial REITs–0.06% | | | | | | | |

| Lexington Realty Trust, | | | | | | | |

| 2.70%, 09/15/2030 | | | 151,000 | | | 152,264 | |

| | | | | | | | |

| Integrated Oil & Gas–1.37% | | | | | | | |

| BP Capital Markets America, Inc., | | | | | | | |

| 2.94%, 06/04/2051 | | | 321,000 | | | 293,957 | |

| BP Capital Markets PLC (United Kingdom), 4.38%(c)(e) | | | 272,000 | | | 287,441 | |

| Occidental Petroleum Corp., | | | | | | | |

| 2.70%, 02/15/2023 | | | 16,000 | | | 15,670 | |

| 2.90%, 08/15/2024 | | | 153,000 | | | 149,088 | |

| 8.50%, 07/15/2027 | | | 15,000 | | | 17,986 | |

| 6.38%, 09/01/2028 | | | 11,000 | | | 12,231 | |

| 6.13%, 01/01/2031 | | | 51,000 | | | 57,073 | |

| 6.45%, 09/15/2036 | | | 5,000 | | | 5,707 | |

| 6.20%, 03/15/2040 | | | 39,000 | | | 42,217 | |

| 4.10%, 02/15/2047 | | | 51,000 | | | 43,446 | |

| Saudi Arabian Oil Co. (Saudi Arabia), | | | | | | | |

| 2.88%, 04/16/2024(b) | | | 1,471,000 | | | 1,552,555 | |

| 2.25%, 11/24/2030(b) | | | 200,000 | | | 196,535 | |

| 4.38%, 04/16/2049(b) | | | 346,000 | | | 394,634 | |

| 3.50%, 11/24/2070(b) | | | 200,000 | | | 184,048 | |

| | | | | | | 3,252,588 | |

| | | | | | | | |

| Integrated Telecommunication Services–4.32% | | | | | | | |

| Altice France S.A. (France), | | | | | | | |

| 7.38%, 05/01/2026(b) | | | 200,000 | | | 208,790 | |

See accompanying Notes to Financial Statements which are an integral part of the financial statements.

| | | Principal

Amount | | Value | |

| Integrated Telecommunication Services–(continued) |

| AT&T, Inc., | | | | | | | |

| 1.40% (3 mo. USD LIBOR + 1.18%), | | | | | | | |

| 06/12/2024(f) | | $ | 393,000 | | $ | 403,584 | |

| 2.55%, 12/01/2033(b) | | | 137,000 | | | 132,494 | |

| 3.10%, 02/01/2043 | | | 499,000 | | | 469,191 | |

| 3.50%, 09/15/2053(b) | | | 1,174,000 | | | 1,078,954 | |

| 3.55%, 09/15/2055(b) | | | 3,939,000 | | | 3,623,484 | |

| 3.50%, 02/01/2061 | | | 320,000 | | | 288,023 | |

| Embarq Corp., 8.00%, 06/01/2036 | | | 71,000 | | | 84,490 | |

| Frontier Communications Corp., 10.50%, 09/15/2022(d) | | | 66,000 | | | 37,661 | |

| Level 3 Financing, Inc., 3.75%, 07/15/2029(b) | | | 130,000 | | | 129,838 | |

| Telecom Italia Capital S.A. (Italy), 7.20%, 07/18/2036 | | | 80,000 | | | 102,836 | |

| Telefonica Emisiones S.A. (Spain), 7.05%, 06/20/2036 | | | 1,066,000 | | | 1,533,198 | |

| Verizon Communications, Inc., | | | | | | | |

| 0.85%, 11/20/2025 | | | 420,000 | | | 414,172 | |

| 1.75%, 01/20/2031 | | | 328,000 | | | 312,882 | |

| 4.81%, 03/15/2039 | | | 377,000 | | | 466,387 | |

| 2.65%, 11/20/2040 | | | 232,000 | | | 217,133 | |

| 2.88%, 11/20/2050 | | | 216,000 | | | 196,643 | |

| 3.00%, 11/20/2060 | | | 636,000 | | | 571,231 | |

| | | | | | | 10,270,991 | |

| | | | | | | | |

| Interactive Home Entertainment–0.68% | | | | | | | |

| Activision Blizzard, Inc., 2.50%, 09/15/2050 | | | 471,000 | | | 416,072 | |

| Electronic Arts, Inc., | | | | | | | |

| 1.85%, 02/15/2031 | | | 453,000 | | | 442,432 | |

| 2.95%, 02/15/2051 | | | 431,000 | | | 414,000 | |

| WMG Acquisition Corp., 3.00%, 02/15/2031(b) | | | 357,000 | | | 344,059 | |

| | | | | | | 1,616,563 | |

| | | | | | | | |

| Interactive Media & Services–1.75% | | | | | | | |

| Alphabet, Inc., | | | | | | | |

| 1.90%, 08/15/2040 | | | 247,000 | | | 222,513 | |

| 2.25%, 08/15/2060 | | | 429,000 | | | 363,708 | |

| Baidu, Inc. (China), | | | | | | | |

| 3.08%, 04/07/2025 | | | 210,000 | | | 222,670 | |

| 1.72%, 04/09/2026 | | | 210,000 | | | 209,993 | |

| 2.38%, 10/09/2030 | | | 215,000 | | | 212,099 | |

| Cumulus Media New Holdings, Inc., | | | | | | | |

| 6.75%, 07/01/2026(b) | | | 34,000 | | | 34,781 | |

| Diamond Sports Group LLC/Diamond Sports Finance Co., 5.38%, 08/15/2026(b) | | | 96,000 | | | 68,011 | |

| Scripps Escrow II, Inc., 3.88%, 01/15/2029(b) | | | 86,000 | | | 84,624 | |

| Tencent Holdings Ltd. (China), | | | | | | | |

| 2.99%, 01/19/2023(b) | | | 298,000 | | | 310,600 | |

| 1.81%, 01/26/2026(b) | | | 200,000 | | | 201,662 | |

| 3.60%, 01/19/2028(b) | | | 620,000 | | | 675,102 | |

| 2.39%, 06/03/2030(b) | | | 381,000 | | | 378,956 | |

| 3.93%, 01/19/2038(b) | | | 448,000 | | | 487,739 | |

| 3.24%, 06/03/2050(b) | | | 200,000 | | | 194,256 | |

| 3.29%, 06/03/2060(b) | | | 200,000 | | | 195,387 | |

| Twitter, Inc., 3.88%, 12/15/2027(b) | | | 284,000 | | | 303,440 | |

| | | | | | | 4,165,541 | |

| | | Principal

Amount | | Value | |

| Internet & Direct Marketing Retail–1.87% | | | | | | | |

| Alibaba Group Holding Ltd. (China), | | | | | | | |

| 2.13%, 02/09/2031 | | $ | 239,000 | | $ | 233,232 | |

| 2.70%, 02/09/2041 | | | 272,000 | | | 257,905 | |

| 4.20%, 12/06/2047 | | | 295,000 | | | 334,898 | |

| 3.15%, 02/09/2051 | | | 336,000 | | | 322,445 | |

| 4.40%, 12/06/2057 | | | 290,000 | | | 346,025 | |

| 3.25%, 02/09/2061 | | | 382,000 | | | 366,682 | |

| Expedia Group, Inc., | | | | | | | |

| 4.63%, 08/01/2027(b) | | | 286,000 | | | 318,625 | |

| 2.95%, 03/15/2031(b) | | | 185,000 | | | 183,307 | |

| Meituan (China), | | | | | | | |

| 2.13%, 10/28/2025(b) | | | 400,000 | | | 405,125 | |

| 3.05%, 10/28/2030(b) | | | 500,000 | | | 503,700 | |

| Prosus N.V. (China), 3.83%, 02/08/2051(b) | | | 1,092,000 | | | 994,208 | |

| QVC, Inc., 5.45%, 08/15/2034 | | | 167,000 | | | 177,020 | |

| | | | | | | 4,443,172 | |

| | | | | | | | |

| Internet Services & Infrastructure–0.19% | | | | | | | |

| Leidos, Inc., 2.30%, 02/15/2031(b) | | | 470,000 | | | 458,219 | |

| | | | | | | | |

| Investment Banking & Brokerage–2.10% | | | | | | | |

| Cantor Fitzgerald L.P., 6.50%, 06/17/2022(b) | | | 516,000 | | | 553,734 | |

| Charles Schwab Corp. (The), Series E, 4.63%(c)(e) | | | 790,000 | | | 798,927 | |

| Goldman Sachs Group, Inc. (The), | | | | | | | |

| 3.50%, 04/01/2025 | | | 360,000 | | | 393,880 | |

| 0.85% (SOFR + 0.79%), 12/09/2026(f) | | | 659,000 | | | 665,075 | |

| 6.75%, 10/01/2037 | | | 284,000 | | | 414,787 | |

| 4.80%, 07/08/2044 | | | 970,000 | | | 1,256,595 | |

| Jefferies Group LLC/Jefferies Group Capital Finance, Inc., 4.15%, 01/23/2030 | | | 30,000 | | | 34,049 | |

| Morgan Stanley, | | | | | | | |

| 2.19%, 04/28/2026(c) | | | 279,000 | | | 290,696 | |

| 3.62%, 04/01/2031(c) | | | 345,000 | | | 384,684 | |

| Raymond James Financial, Inc., 4.65%, 04/01/2030 | | | 171,000 | | | 205,190 | |

| | | | | | | 4,997,617 | |

| | | | | | | | |

| IT Consulting & Other Services–0.18% | | | | | | | |

| DXC Technology Co., 4.45%, 09/18/2022 | | | 323,000 | | | 339,824 | |

| Gartner, Inc., 4.50%, 07/01/2028(b) | | | 79,000 | | | 83,049 | |

| | | | | | | 422,873 | |

| | | | | | | | |

| Leisure Facilities–0.02% | | | | | | | |

| Cedar Fair L.P./Canada’s Wonderland Co./Magnum Management Corp., 5.38%, 06/01/2024 | | | 44,000 | | | 44,220 | |

| | | | | | | | |

| Life & Health Insurance–3.77% | | | | | | | |

| AIA Group Ltd. (Hong Kong), 3.20%, 09/16/2040(b) | | | 200,000 | | | 200,611 | |

| American Equity Investment Life Holding Co., 5.00%, 06/15/2027 | | | 288,000 | | | 324,671 | |

| Athene Global Funding, | | | | | | | |

| 1.20%, 10/13/2023(b) | | | 489,000 | | | 494,982 | |

| 2.50%, 01/14/2025(b) | | | 362,000 | | | 379,366 | |

| 1.45%, 01/08/2026(b) | | | 226,000 | | | 225,191 | |

See accompanying Notes to Financial Statements which are an integral part of the financial statements.

| | | | Principal

Amount | | | Value | |

| Life & Health Insurance–(continued) |

| Athene Holding Ltd., | | | | | | | |

| 4.13%, 01/12/2028 | | $ | 887,000 | | $ | 983,567 | |

| 6.15%, 04/03/2030 | | | 384,000 | | | 475,079 | |

| 3.50%, 01/15/2031 | | | 136,000 | | | 141,871 | |

| Brighthouse Financial, Inc., 4.70%, 06/22/2047 | | | 370,000 | | | 391,854 | |

| GA Global Funding Trust, 1.63%, 01/15/2026(b) | | | 81,000 | | | 81,894 | |

Global Atlantic Fin Co.,

8.63%, 04/15/2021(b) | | | 950,000 | | | 959,091 | |

| 4.40%, 10/15/2029(b) | | | 1,167,000 | | | 1,271,920 | |

| MetLife, Inc., 4.13%, 08/13/2042 | | | 357,000 | | | 428,700 | |

| Nationwide Financial Services, Inc., | | | | | | | |

| 5.38%, 03/25/2021(b) | | | 1,645,000 | | | 1,650,310 | |

| 3.90%, 11/30/2049(b) | | | 339,000 | | | 367,047 | |

| Prudential Financial, Inc., 3.91%, 12/07/2047 | | | 503,000 | | | 574,333 | |

| | | | | | | 8,950,487 | |

| Life Sciences Tools & Services–0.03% |

| Charles River Laboratories International, Inc., 4.25%, 05/01/2028(b) | | | 60,000 | | | 62,726 | |

| Managed Health Care–0.72% |

| Centene Corp., | | | | | | | |

| 5.38%, 06/01/2026(b) | | | 86,000 | | | 89,968 | |

| 5.38%, 08/15/2026(b) | | | 26,000 | | | 27,430 | |

| 4.63%, 12/15/2029 | | | 88,000 | | | 95,066 | |

| 3.38%, 02/15/2030 | | | 154,000 | | | 158,507 | |

| 2.50%, 03/01/2031 | | | 649,000 | | | 628,524 | |

| Children’s Hospital, Series 2020, 2.93%, 07/15/2050 | | | 179,000 | | | 172,717 | |

| Community Health Network, Inc., Series 20-A, 3.10%, 05/01/2050 | | | 384,000 | | | 378,947 | |

| Hackensack Meridian Health, Inc., 2.88%, 09/01/2050 | | | 162,000 | | | 158,335 | |

| | | | | | | 1,709,494 | |

| Metal & Glass Containers–0.19% |

| Ardagh Metal Packaging Finance USA LLC/Ardagh Metal Packaging Finance PLC, 3.25%, 09/01/2028(b) | | | 200,000 | | | 200,000 | |

| Ball Corp., 5.25%, 07/01/2025 | | | 70,000 | | | 78,881 | |

| Silgan Holdings, Inc., 1.40%, 04/01/2026(b) | | | 178,000 | | | 175,911 | |

| | | | | | | 454,792 | |

| Movies & Entertainment–0.29% |

| Netflix, Inc., | | | | | | | |

| 5.88%, 11/15/2028 | | | 186,000 | | | 223,377 | |

| 5.38%, 11/15/2029(b) | | | 26,000 | | | 30,750 | |

| Tencent Music Entertainment Group (China), | | | | | | | |

| 1.38%, 09/03/2025 | | | 210,000 | | | 207,864 | |

| 2.00%, 09/03/2030 | | | 235,000 | | | 226,504 | |

| | | | | | | 688,495 | |

| Multi-line Insurance–1.84% |

| American International Group, Inc., | | | | | | | |

| 3.40%, 06/30/2030 | | | 520,000 | | | 570,585 | |

| 4.50%, 07/16/2044 | | | 1,359,000 | | | 1,632,252 | |

| Fairfax Financial Holdings Ltd. (Canada), | | | | | | | |

| 4.85%, 04/17/2028 | | | 379,000 | | | 423,942 | |

| 4.63%, 04/29/2030 | | | 362,000 | | | 400,438 | |

| | | | Principal

Amount | | | Value | |

| Multi-line Insurance–(continued) |

| Liberty Mutual Group, Inc., 4.30%, 02/01/2061(b) | | $ | 236,000 | | $ | 215,486 | |

| Massachusetts Mutual Life Insurance Co., 3.38%, 04/15/2050(b) | | | 186,000 | | | 190,806 | |

| Nationwide Mutual Insurance Co., 4.95%, 04/22/2044(b) | | | 830,000 | | | 938,038 | |

| | | | | | | 4,371,547 | |

| Multi-Utilities–0.21% |

| CMS Energy Corp., 4.75%, 06/01/2050(c) | | | 176,000 | | | 192,922 | |

| DTE Energy Co., Series F, 1.05%, 06/01/2025 | | | 170,000 | | | 169,511 | |

| WEC Energy Group, Inc., 1.38%, 10/15/2027 | | | 129,000 | | | 127,500 | |

| | | | | | | 489,933 | |

| Office REITs–0.52% |

| Alexandria Real Estate Equities, Inc., 3.95%, 01/15/2027 | | | 523,000 | | | 593,437 | |

| Highwoods Realty L.P., 2.60%, 02/01/2031 | | | 98,000 | | | 97,194 | |

| Office Properties Income Trust, 4.50%, 02/01/2025 | | | 521,000 | | | 556,082 | |

| | | | | | | 1,246,713 | |

| Oil & Gas Drilling–0.14% |

| Global Partners L.P./GLP Finance Corp., 6.88%, 01/15/2029 | | | 81,000 | | | 88,037 | |

| NGL Energy Operating LLC/NGL Energy Finance Corp., 7.50%, 02/01/2026(b) | | | 70,000 | | | 72,302 | |

| Precision Drilling Corp. (Canada), 5.25%, 11/15/2024 | | | 37,000 | | | 34,664 | |

| Rockies Express Pipeline LLC, | | | | | | | |

| 4.80%, 05/15/2030(b) | | | 70,000 | | | 72,809 | |

| 6.88%, 04/15/2040(b) | | | 57,000 | | | 63,270 | |

| | | | | | | 331,082 | |

| Oil & Gas Equipment & Services–0.04% |

| USA Compression Partners L.P./USA Compression Finance Corp., 6.88%, 09/01/2027 | | | 82,000 | | | 86,239 | |

| Oil & Gas Exploration & Production–1.53% |

| Aethon United BR L.P./Aethon United Finance Corp., 8.25%, 02/15/2026(b) | | | 176,000 | | | 183,480 | |

| Cameron LNG LLC, | | | | | | | |

| 3.30%, 01/15/2035(b) | | | 457,000 | | | 492,197 | |

| 3.40%, 01/15/2038(b) | | | 494,000 | | | 516,205 | |

| CNX Resources Corp., 7.25%, 03/14/2027(b) | | | 80,000 | | | 85,700 | |

| Comstock Resources, Inc., 9.75%, 08/15/2026 | | | 77,000 | | | 84,149 | |

| ConocoPhillips, 2.40%, 02/15/2031(b) | | | 115,000 | | | 117,027 | |

| Galaxy Pipeline Assets Bidco Ltd. (United Arab Emirates), | | | | | | | |