American International Group, Inc. Fourth Quarter 2013 Results Conference Call Presentation February 14, 2014 Exhibit 99.1 |

2 Cautionary Statement Regarding Projections and Other Information About Future Events This document and the remarks made within this presentation may include, and officers and representatives of American International Group, Inc. (AIG) may from time to time make, projections, goals, assumptions and statements that may constitute “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. These projections, goals, assumptions and statements are not historical facts but instead represent only AIG’s belief regarding future events, many of which, by their nature, are inherently uncertain and outside AIG’s control. These projections, goals, assumptions and statements include statements preceded by, followed by or including words such as “believe,” “anticipate,” “expect,” “intend,” “plan,” “view,” “target” or “estimate”. It is possible that AIG’s actual results and financial condition will differ, possibly materially, from the results and financial condition indicated in these projections, goals, assumptions and statements. Factors that could cause AIG’s actual results to differ, possibly materially, from those in the specific projections, goals, assumptions and statements include: changes in market conditions; the occurrence of catastrophic events, both natural and man-made; significant legal proceedings; the timing and applicable requirements of any new regulatory framework to which AIG is subject as a savings and loan holding company, as a systemically important financial institution, and as a global systemically important insurer; concentrations in AIG’s investment portfolios; actions by credit rating agencies; judgments concerning casualty insurance underwriting and insurance liabilities; judgments concerning the recognition of deferred tax assets; and such other factors discussed in Part I, Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations (MD&A) in AIG’s Quarterly Report on Form 10-Q for the quarterly period ended September 30, 2013, Part II, Item 1A. Risk Factors in AIG’s Quarterly Report on Form 10-Q for the quarterly period ended June 30, 2013, Part I, Item 1A. Risk Factors and Part II, Item 7. MD&A in AIG’s Annual Report on Form 10-K for the fiscal year ended December 31, 2012 and Part I, Item 1A. Risk Factors and Part II, Item 7. MD&A in AIG’s Annual Report on Form 10-K for the fiscal year ended December 31, 2013 (which will be filed with the Securities and Exchange Commission). AIG is not under any obligation (and expressly disclaims any obligation) to update or alter any projections, goals, assumptions or other statements, whether written or oral, that may be made from time to time, whether as a result of new information, future events or otherwise. This document and the remarks made orally may also contain certain non-GAAP financial measures. The reconciliation of such measures to the most comparable GAAP measures in accordance with Regulation G is included in the Fourth Quarter 2013 Financial Supplement available in the Investor Information section of AIG's corporate website, www.aig.com, as well as this presentation. IRS Circular 230 Disclosure: To ensure compliance with requirements imposed by the IRS, we inform you that (i) any U.S. tax advice contained in this communication (including any attachments) is not intended or written to be used, and cannot be used, for the purpose of avoiding penalties under the Internal Revenue Code; (ii) any such tax advice is written in connection with the promotion or marketing of the matters addressed; and (iii) if you are not the original addressee of this communication, you should seek advice based on your particular circumstances from an independent advisor. |

3 Fourth Quarter 2013 Key Themes Highlights: Noteworthy Items Capital Management, Liquidity & Other In February 2014, $1 billion increase in share repurchase authorization; 25% increase in quarterly dividend to $0.125/sh. $4.1 billion of insurance company cash dividends ($8.7 billion in cash dividends and loan repayments in 2013) Issued $1.0 billion of 4.125% senior notes due 2024; repurchased and redeemed debt totaling $1.1 billion with an average coupon rate of approximately 7.5% Agreement to sell ILFC to AerCap Holdings N.V. for total consideration of approximately $5.4 billion* Severance charge of $265 million AIG Property Casualty Accident year loss ratio, as adjusted, increased 3.1 points to 66.4 from 4Q12 largely due to severe losses of $277 million Continued positive rate change in 4Q13, with Global Commercial rates up 2.6% (+5.0% in North America) Net premiums written grew 6% across all lines from 4Q12, excluding foreign exchange, timing of recognition of ceded premiums written on excess of loss reinsurance agreements and premium adjustments A low level of catastrophe losses of $208 million Net prior year adverse development of $266 million, largely from pre-2004 environmental and pollution products Net favorable change in discount of $325 million to reflect expected yields and future payout patterns Mortgage Guaranty New insurance written (NIW) of $10.9 billion in 4Q13. Record NIW of $49.4 billion in domestic 1 st lien for full-year 2013 59% of net premiums earned in 4Q13 were from new business written after 2008 Delinquency ratio declined 50 bps from 3Q13 to 5.9%, the lowest since 4Q07 AIG Life and Retirement Premiums and deposits of $8.0 billion driven by strong sales of investment products, including near record sales of variable annuities Significant increases in net flows and account balances resulted in higher fee income and contributed to the 10% increase in AUM from the year-ago period Continued initiatives to enhance profitability, including spread management actions Net investment income increase driven by higher returns on alternative investments and yield enhancements * Based on AerCap’s pre-announcement closing price per share of $24.93 on December 13, 2013. |

4 Fourth Quarter ($ in millions, except per share amounts) 2012 2013 Inc. (Dec.) Revenues $17,169 $17,346 1% Net income (loss) attributable to AIG (3,958) 1,978 NM Diluted earnings per common share ($2.68) $1.34 NM ROE, Ex. AOCI (1) NM 8.5% After-tax operating income attributable to AIG $290 $1,704 488% After-tax operating income attributable to AIG per common share $0.20 $1.15 475% ROE – After-tax operating income (2) 1.3% 7.3% Book value per common share $66.38 $68.62 3% Book value per common share - Ex. AOCI $57.87 $64.28 11% Financial Highlights 1) Computed as Annualized Net income (loss) attributable to AIG divided by Average AIG Shareholders' equity, excluding AOCI. 2) Computed as Annualized After-tax operating income divided by Average AIG Shareholders' equity, excluding AOCI. |

5 After-tax Operating Income Fourth Quarter ($ in millions, except per share amounts) 2012 2013 Insurance operations: AIG Property Casualty ($944) $1,090 AIG Life and Retirement 1,090 1,406 Mortgage Guaranty (45) 48 Total Insurance Operations 101 2,544 Other operations: Direct Investment book 509 418 Global Capital Markets 300 194 Interest expense (408) (328) Corporate expenses (337) (213) Change in fair value of AIA (including realized gain) 240 - Other (20) (92) Pre-tax operating income 385 2,523 Income tax expense (87) (815) Other noncontrolling interest (8) (4) After-tax operating income attributable to AIG $290 $1,704 After-tax operating income per diluted common share $0.20 $1.15 4Q13 results reflect strong growth in insurance operating earnings. (1) 1) 4Q13 included a severance charge of $265 million and real estate gains of $170 million. Note: In 4Q13, life settlement investments and associated income (loss) was transferred from AIG Property Casualty to AIG’s Other operations. Prior periods were reclassified to conform to the current period presentation. |

6 Deferred Tax Asset Overview AIG continues to have substantial deferred tax assets that are available to offset future tax obligations. 1) Foreign tax credits triggered in years 2013 have increased the amount of carryover. 2) Change during the period is primarily attributable to available for sale investment securities. As of 12/31/12 As of 12/31/13 ($ in billions) Type Gross Attributes Deferred Tax Asset Gross Attributes Deferred Tax Asset Utilization/Expiration Net Operating Loss Carryforwards Non-Life & Life $39.5 $13.8 $35.8 $12.5 Utilize against AIG PC, ILFC, UGC, AIG Parent and 35% of AIG L&R income 2028–2031 Expiration Capital Loss Carryforwards Valuation Allowance Life $16.6 $5.8 ($5.1) $1.4 $0.5 ($0.5) Utilize against capital gains from AIG L&R 2014 Expiration Foreign Tax Credits General $4.7 $5.3 (1) Utilize against 65% of AIG L&R income 2016–2023 Expiration Subtotal – U.S. Tax Attributes 19.2 17.8 Other Deferred Tax Assets/(Liabilities) (2.5) 3.4 (2) Net Deferred Tax Assets $16.7 $21.2 |

7 Strong Capital Position Book Value Per Share Capital Structure $66.38 ($ in billions, except per share data) $124.1 Leverage Ratios: Dec. 31, 2012 Dec. 31, 2013 Financial Debt + Hybrids / Capitalization 20.5% 17.3% Financial Debt / Capitalization 12.9% 12.8% $68.62 $122.3 Risk Based Capital Ratios (2) Year-end AIG U.S. Property Casualty AIG Life and Retirement 2012 443% (ACL) 532% (CAL) 2013 416% (ACL) 540% (CAL) 1) Includes AIG notes, bonds, loans and mortgages payable, and AIGLH notes and bonds payable and junior subordinated debt. 2) The inclusion of RBC measures is intended solely for the information of investors and is not intended for the purpose of ranking any insurance company or for use in connection with any marketing, advertising or promotional activities. ACL is defined as Authorized Control Level and CAL is defined as Company Action Level. RBC ratio for AIG Life and Retirement excludes holding company, AGC Life Insurance Company. Amounts for 2013 are estimated. |

8 Financial Flexibility – A Source of Strength Parent Cash, Short-Term Investments & Unencumbered Securities Insurance Company Distributions ($ in millions) ($ in billions) AIG Property Casualty distributions in 2013 included $1.8 billion resulting from legal entity restructurings and intercompany reinsurance optimization, including $1.5 billion in 4Q13. AIG Life and Retirement distributions in 2013 included approximately $800 million of legal settlement proceeds received. UGC remitted a $90 million dividend to AIG Parent in 4Q13, its first dividend since 2010. AIG Parent cash, short-term investments and unencumbered fixed maturity securities of $13.1 billion includes $5.9 billion allocated toward future maturities of liabilities and contingent liquidity stress needs of the Direct Investment book and Global Capital Markets as of December 31, 2013. AIG Parent also maintains available capacity of $4.4 billion under its syndicated credit facility plus its contingent liquidity facility. $12.7 $1,337 $1,933 FY 2013 - $8,893 $4,274 $13.1 * * Includes $222 million of non-cash distributions. $792 $716 $2,862 $545 $1,217 $1,322 $0 $1,000 $2,000 $3,000 $4,000 $5,000 1Q13 2Q13 3Q13 4Q13 AIG Property Casualty AIG Life and Retirement UGC $9.8 $10.2 $3.0 $3.0 Dec. 31, 2012 Sept. 30, 2013 Dec. 31, 2013 Unencumbered Fixed Maturity Securities Cash & Short-term Investments $1,349 $90 $12.6 |

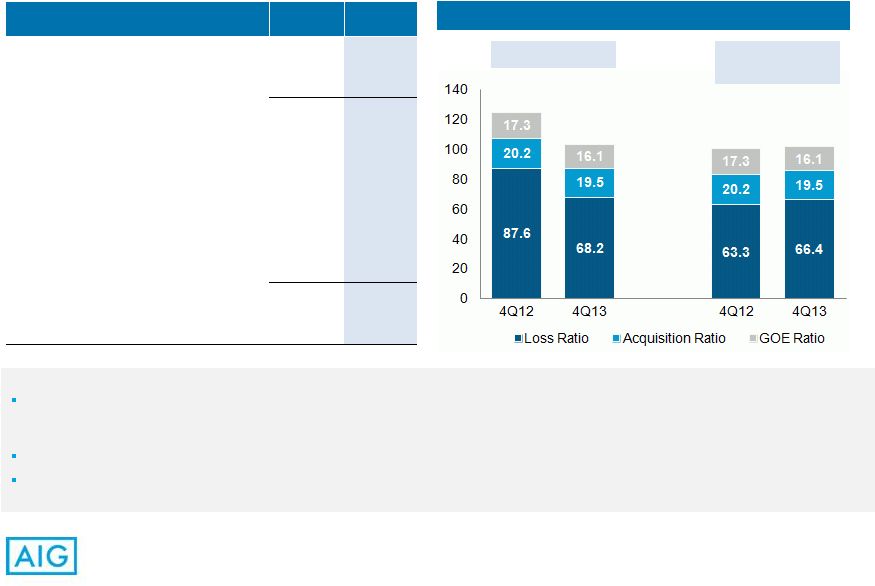

9 AIG Property Casualty – Financial Results Global Combined Ratios Calendar Year Accident Year, as adjusted (1) 1) Both the accident year combined ratio, as adjusted, and accident year loss ratio, as adjusted, exclude catastrophe losses and related reinstatement premiums, prior year development, net of premium adjustments, and the impact of reserve discounting. ($ in millions) 4Q12 4Q13 Net premiums written $7,809 $8,028 Net premiums earned 8,613 8,621 Underwriting loss (2,161) (330) Net investment income 1,217 1,420 Pre-tax operating income (loss) ($944) $1,090 Net premiums written, excluding foreign exchange, the timing of recognition of ceded premiums written on excess of loss reinsurance agreements and premium adjustments, grew 6% from 4Q12 reflecting growth of new business, rate increases and changes in reinsurance structure. Net premiums written on an as-reported basis grew 3% from 4Q12. The accident year loss ratio, as adjusted, increased 3.1 points from 4Q12, largely due to an increase in severe losses of $214 million. Net investment income growth was primarily driven by hedge fund performance and income from fair value option securities. Operating results demonstrate continued execution of strategic initiatives. 125.1 100.8 103.8 102.0 |

10 Commercial Insurance – Underwriting Results Calendar Year Accident Year, as adjusted (1) 130.3 Combined Ratios 95.8 Accident Year Loss Ratio, as adjusted (1) Net Premiums Written ($ in millions) $4,410 $4,841 107.7 97.1 1) Both the accident year combined ratio, as adjusted, and accident year loss ratio, as adjusted, exclude catastrophe losses and related reinstatement premiums, prior year development, net of premium adjustments, and the impact of reserve discounting. Commercial Insurance NPW, excluding foreign exchange, the timing of recognition of ceded premiums written on excess of loss reinsurance agreements and premium adjustments, grew 7% from 4Q12. This increase reflected growth of new business, rate increases and changes in our reinsurance structure. Net premiums written on an as-reported basis grew 10% from 4Q12. Commercial Insurance rates increased 2.6% (+5.0% for North America), led by Casualty at +5.0% and Financial Lines at +3.3%. The accident year loss ratio, as adjusted, in 2013 reflected volatility in the quarterly results due to the impact of severe losses which ranged from a low of 0.7 points in 2Q13 to 4.9 points in 4Q13. The 4Q13 combined ratio was negatively impacted by 6.1 pts due to a change in our discounting of workers’ compensation reserves. See page 13. |

11 Consumer Insurance – Underwriting Results Combined Ratios Accident Year Loss Ratio, as adjusted (1) Calendar Year Accident Year, as adjusted (1) 111.2 101.3 Net Premiums Written ($ in millions) $3,189 Consumer Insurance NPW, excluding foreign exchange and timing of recognition of ceded premiums written on excess of loss reinsurance agreements, grew 4% from 4Q12. On an as- reported basis NPW declined 6%. NPW growth was driven by increased Personal Lines premiums in EMEA and the U.S. as well as growth in Life premiums in Japan. The accident year loss ratio, as adjusted, increased in 4Q13 primarily due to higher A&H losses and severe loss activity in Private Client Group. 103.3 103.6 1) Both the accident year combined ratio, as adjusted, and accident year loss ratio, as adjusted, exclude catastrophe losses and related reinstatement premiums, prior year development, net of premium adjustments, and the impact of reserve discounting. $1,647 $1,532 $1,748 $1,657 $0 $1,000 $2,000 $3,000 $4,000 4Q12 4Q13 Accident & Health Personal Lines 67.9 60.4 58.0 60.7 26.9 25.2 26.9 25.2 16.4 17.7 16.4 17.7 0 20 40 60 80 100 120 4Q12 4Q13 4Q12 4Q13 Loss Ratio Acquisition Ratio GOE Ratio 58.4 59.1 57.7 58.0 58.8 60.2 58.5 60.7 40 45 50 55 60 65 1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13 4Q13 $3,395 |

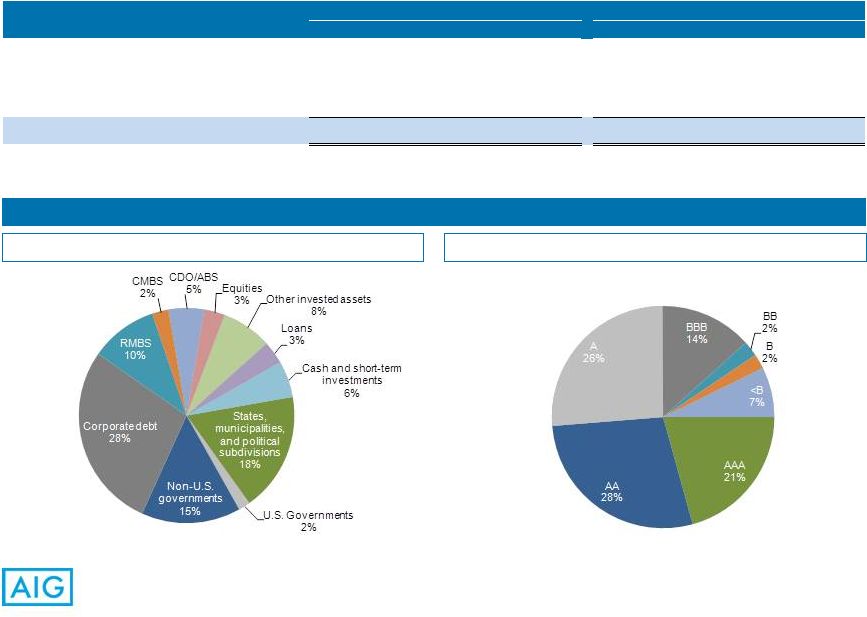

12 AIG Property Casualty – Investments 1) Includes income/loss from fair value option securities, investment real estate and mutual funds, net of investment expenses. 2) Includes intercompany invested assets that are eliminated in consolidation. Total Portfolio Composition Bond Portfolio - $99.0 billion - by Agency Credit Rating Total Cash & Invested Assets as of December 31, 2013 - $123.1 billion (2) Net investment income: ($ in millions) 2012 2013 Inc./(Dec.) 2012 2013 Inc./(Dec.) Interest and dividends 1,036 $ 1,041 $ 0% 4,215 $ 4,124 $ (2%) Alternative investments 157 303 93% 484 870 80% Other, net (1) 24 76 217% 81 273 237% Net investment income 1,217 $ 1,420 $ 17% 4,780 $ 5,267 $ 10% Yield 3.77% 4.59% 0.82% 3.79% 4.17% 0.38% Fourth Quarter Full Year |

13 AIG Property Casualty – Prior Year Development Unfavorable prior year development in the Other run-off lines in 4Q13 consisted primarily of charges associated with pre-2004 environmental business, reflecting changes in case reserves due to new developments such as the discovery of additional contamination in certain sites, legislative changes, court rulings, expansion of plaintiff damages and increased cost of remediation technologies. In 4Q13 we received permission from our Pennsylvania regulator to apply a consistent discount rate (U.S. Treasury rate plus liquidity premium) to our workers’ compensation reserves in our Pennsylvania-domiciled companies and to use payout patterns specific to our primary and excess workers’ compensation portfolios. Total discount benefit in the quarter was $325 million, including a charge of $322 million in Commercial Insurance from a lower discount rate on primary workers’ compensation reserves, and a benefit of $647 million in Other primarily from the use of payout patterns specific to excess workers’ compensation reserves. ($ in millions) 1Q13 2Q13 3Q13 4Q13 2012 2013 Product: Casualty 23 $ 89 $ 114 $ 68 $ 700 $ 294 $ Financial lines (9) 3 (9) (12) (250) (26) Specialty (46) 8 46 41 68 50 Property (29) 156 (46) (45) (228) 37 Total Commercial (61) 257 105 54 290 355 A&H (8) (5) (9) (7) (18) (30) Personal lines (34) (48) (21) (22) (2) (125) Total Consumer (42) (53) (30) (30) (20) (155) Other - run-off 61 20 (2) 248 229 327 Prior year loss reserve development (favorable) unfavorable, net of reinsurance (42) 224 73 272 499 527 Additional premium related to prior year development (10) (70) (6) (89) Net prior year development (favorable) unfavorable (52) $ 154 $ 70 $ 266 $ 445 $ 438 $ Net reserve discount benefit (charge) (5) $ (5) $ (6) $ 325 $ 63 $ 309 $ Quarterly Full Year (54) (3) |

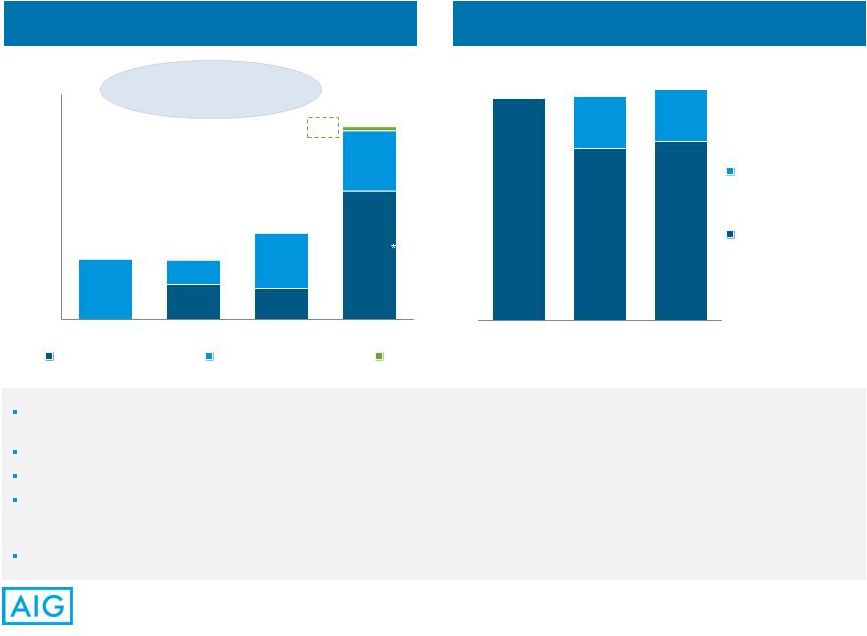

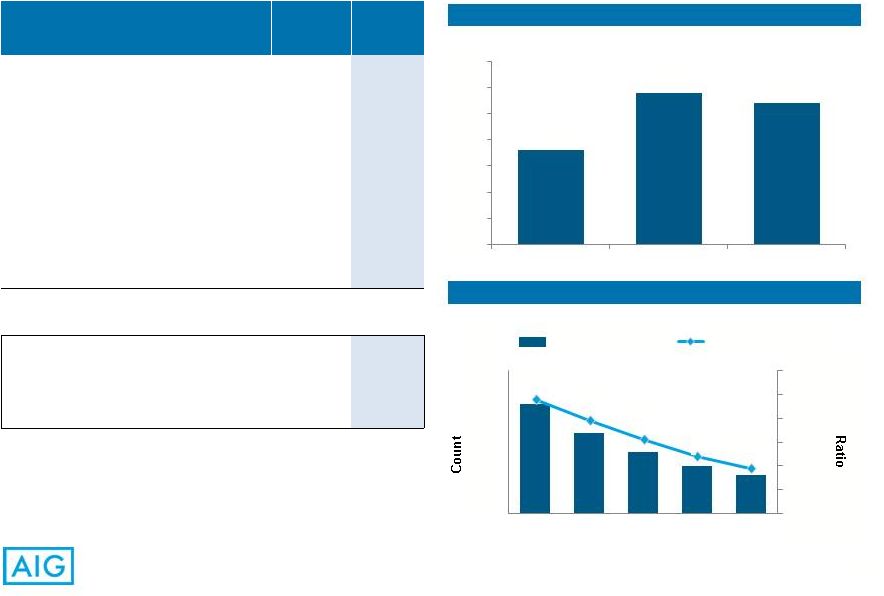

Mortgage Guaranty – Growing Profitability New business increasingly drives trend of improving operating results. 1) Domestic First-lien only. Primary Delinquency Trend (1) ($ in millions) 4Q12 4Q13 Net premiums written $236 $255 Net premiums earned 190 203 Underwriting income (loss) (82) 15 Net investment income 37 33 Pre-tax operating income (loss) ($45) $48 Net premiums earned from business written after 2008 44% 59% Loss ratio 118.4 63.1 New Insurance Written ($ in billions) $7.2 $11.6 $10.9 $0 $2 $4 $6 $8 $10 $12 $14 4Q11 4Q12 4Q13 63 57 53 50 48 8.8% 7.9% 7.1% 6.4% 5.9% 5.0% 6.0% 7.0% 8.0% 9.0% 10.0% 40 45 50 55 60 65 70 4Q12 1Q13 2Q13 3Q13 4Q13 14 DQ Ratio (%) DQ Count (000's) 4.0% |

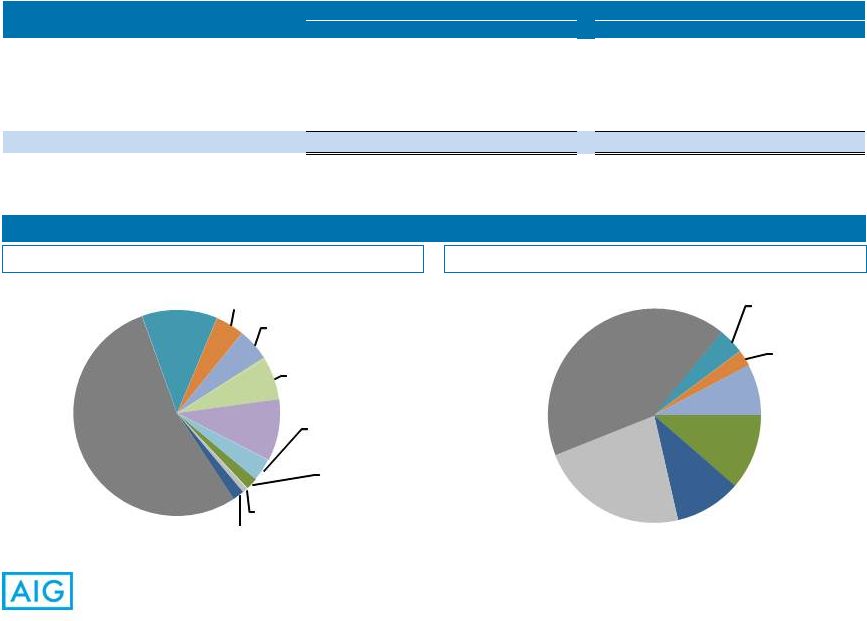

15 AIG Life and Retirement – Financial Results Increase in pre-tax operating income of 29% driven by effective spread management, higher net investment income and fee income growth. Ongoing strategy of actively managing profitability through crediting rate actions on existing spread business and disciplined new business pricing continued to enhance results. Net investment income benefited from higher returns on alternative investments, increased gains on calls and tenders, and appreciation of hybrid securities. Assets Under Management Strong sales and growth in pre-tax operating income. ($ in millions) 4Q12 4Q13 Premiums and deposits $5,215 $8,042 Premiums 634 606 Policy fees 618 652 Net investment income 2,715 2,873 Advisory fee and other income 358 454 Total revenues (1) 4,325 4,585 Benefits and expenses 3,235 3,179 Pre-tax operating income $1,090 $1,406 1) Excluding net realized capital gains (losses). Assets under management increased 10% from the year- ago period to $318 billion at December 31, 2013. Growth was driven by strong retail investment product net flows, higher separate account balances and greater institutional assets. These sources of AUM growth more than offset the impact of rising rates on our invested asset portfolio. Net inflows were $4.6 billion in 2013 compared to net outflows of $1.3 billion in 2012. The significant increase was driven by the strength of variable annuity and retail mutual fund sales and continued improvement in fixed annuities flows. Life Insurance and A&H 11% Fixed Annuities 22% Retirement Income Solutions 13% Retail Mutual Funds 4% Group Retirement 29% Institutional Markets 20% Group Benefits 1% |

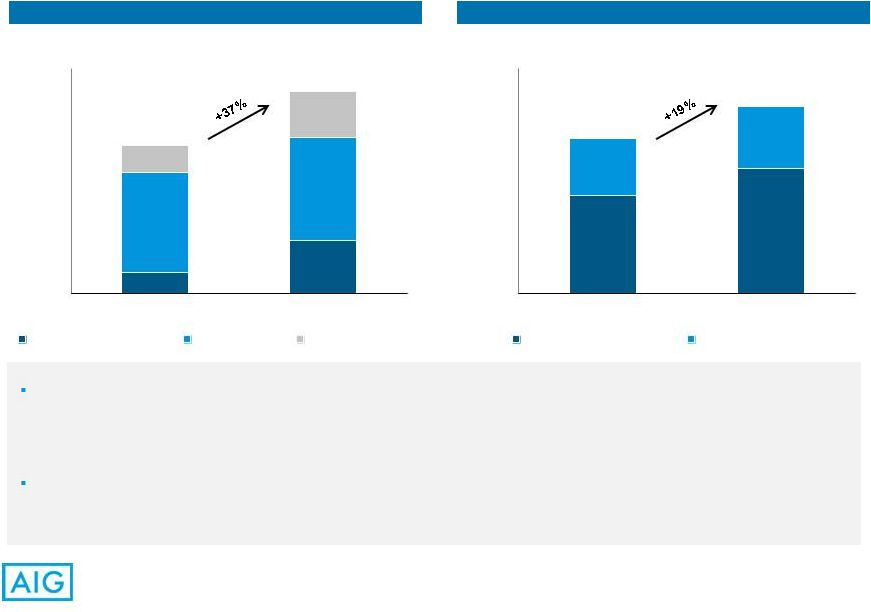

16 AIG Life and Retirement – Retail & Institutional Results Retail Pre-Tax Operating Income (1) Institutional Pre-Tax Operating Income (2) $598 $820 ($ in millions) $492 $586 ($ in millions) 1) Breakdown excludes operating income for Brokerage Services and Retail Mutual Funds which are included in the Retail operating segment total. 2) Breakdown excludes operating income for Group Benefits which is included in the Institutional operating segment total. $88 $213 $398 $413 $109 $186 $0 $100 $200 $300 $400 $500 $600 $700 $800 $900 4Q12 4Q13 Life Insurance and A&H Fixed Annuities Ret. Inc. Solutions $308 $392 $176 $191 $0 $100 $200 $300 $400 $500 $600 $700 4Q12 4Q13 Group Retirement Institutional Markets Retail pre-tax operating income increased 37% from 4Q12, driven by ongoing active spread management, higher net investment income, growth in fee income, and favorable mortality experience. Retirement Income Solutions benefited from increased assets under management and strong equity market performance. Fixed Annuities experienced improved spreads in the quarter; further, the prior-year period included a $76 million gain from DAC unlocking. Life Insurance and A&H benefited from better than expected mortality experience, and the prior-year period was impacted by charges for DAC unlocking and loss recognition. Institutional pre-tax operating income increased 19% from 4Q12, driven by active spread management, higher fee income on group separate account balances, and higher returns on alternative investments. Group Retirement earnings also benefited from a $35 million positive DAC unlocking in the quarter. |

17 AIG Life and Retirement – Investments Total Portfolio Composition Bond Portfolio - $157.2 billion - by Agency Credit Rating Total Cash & Invested Assets as of December 31, 2013 - $196.9 billion (4) Net investment income: ($ in millions) 2012 2013 Inc./(Dec.) 2012 2013 Inc./(Dec.) Interest and dividends 2,316 $ 2,291 $ (1%) 9,650 $ 9,173 $ (5%) Alternative investments 332 505 52% 954 1,567 64% Call and tender income 42 57 36% 146 196 34% Other, net (1) 25 20 (20%) (32) (82) 156% Net investment income 2,715 $ 2,873 $ 6% 10,718 $ 10,854 $ 1% Base Yield (2) 5.33% 5.29% (0.04%) 5.43% 5.30% (0.13%) Total Yield (3) 6.09% 6.27% 0.18% 6.04% 5.97% (0.07%) Fourth Quarter Full Year States, municipalities, and political subdivisions 2% U.S. Governments 1% Non -U.S. governments 2% Corporate debt 54% RMBS 12% CMBS 4% CDO/ABS 5% Other invested assets 7% Loans 10% Cash and short-term investments 3% AAA 11% AA 10% A 23% BBB 42% BB 4% B 2% <B 8% 1) Includes income/loss from mutual funds, real estate, equity method investments and mark-to-market gains and losses, net of investment expenses. 2) Includes the investment return other than alternative investment or yield enhancement activities. Quarterly results are annualized. 3) Represents the base yields and the incremental effect on base yield on investments in hedge funds, private equity funds, affordable housing partnerships, gains on Maiden Lane II (in 2012) and income from calls and prepayment fees. Quarterly results are annualized. 4) Includes intercompany invested assets that are eliminated in consolidation. |

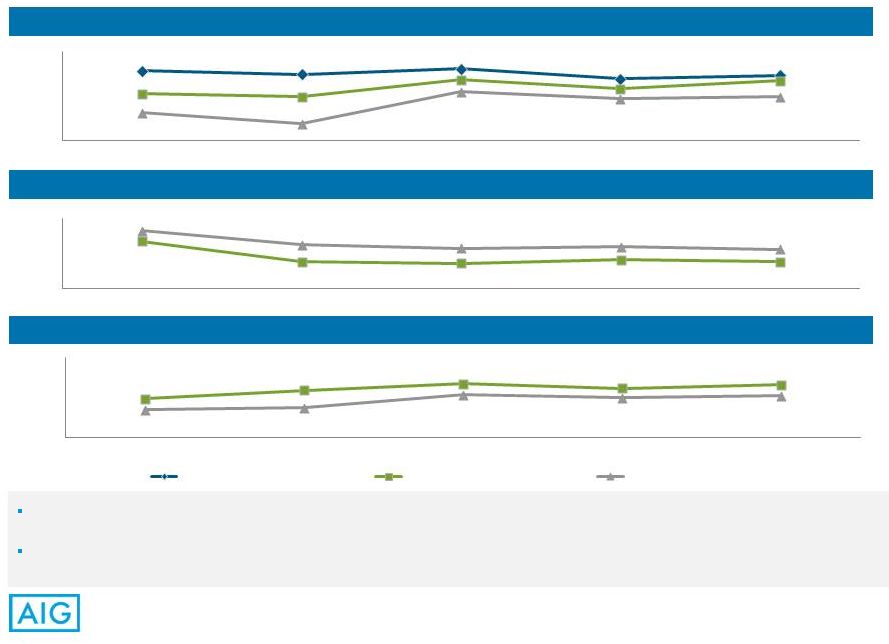

18 Base Yields (1) Base Net Investment Spreads (1) Cost of Funds (2) AIG Life and Retirement – Base Yields and Spreads Base net investment spreads expanded for both Fixed Annuities and Group Retirement from the year-ago period benefiting from higher base investment yields and active crediting rate management throughout the year. Overall portfolio base yield declined slightly from the year-ago period, due to the impact of reinvestment at lower rates than book yield and the sale of invested assets to generate taxable gains and monetize capital loss carryforwards. 5.33% 5.30% 5.35% 5.26% 5.29% 5.12% 5.10% 5.25% 5.17% 5.24% 4.95% 4.85% 5.14% 5.08% 5.10% 4.70% 4.90% 5.10% 5.30% 5.50% 4Q12 1Q13 2Q13 3Q13 4Q13 3.14% 2.91% 2.89% 2.93% 2.91% 3.26% 3.10% 3.06% 3.08% 3.05% 2.60% 2.80% 3.00% 3.20% 3.40% 4Q12 1Q13 2Q13 3Q13 4Q13 1.98% 2.19% 2.36% 2.24% 2.33% 1.69% 1.75% 2.08% 2.00% 2.05% 1.00% 1.50% 2.00% 2.50% 3.00% 4Q12 1Q13 2Q13 3Q13 4Q13 Total Base Yield Fixed Annuities Group Retirement 1) Includes the investment return on surplus other than alternative investment or yield enhancement activities. 2) Excludes the amortization of sales inducement assets. |

19 Q&A |

20 Appendix |

21 Non-GAAP Reconciliation – Pre-tax Operating Income (Loss) (1) 1) Includes results of ILFC. (1) Income (loss) from continuing operations, before tax $ (923) 1,252 (47) (6,321) (6,039) Adjustments to arrive at pre-tax operating income: Net (income) loss from divested businesses - - - 6,668 6,668 Legal reserves (settlements), net of related expenses (17) (154) - (29) (200) Changes in fair value of securities designated to hedge living benefit liabilities, net of interest expense - 11 - - 11 Change in benefit reserves and DAC, VOBA and SIA related to net realized capital gains (losses) - 81 - - 81 Other loss 4 - - (4) - Net realized capital (gains) losses (8) (100) 2 (30) (136) Pre-tax operating income (loss) $ (944) 1,090 (45) 284 385 Income (loss) from continuing operations, before tax $ 1,188 1,975 51 (1,064) 2,150 Adjustments to arrive at pre-tax operating income: Net (income) loss from divested businesses - - - 190 190 Legal reserves (settlements), net of related expenses (10) (553) - (52) (615) Changes in fair value of securities designated to hedge living benefit liabilities, net of interest expense - 33 - - 33 Change in benefit reserves and DAC, VOBA and SIA related to net realized capital gains (losses) - 4 - 98 102 AIG Property Casualty other income (expense), net 79 (7) 72 Loss on extinguishment of debt - - - 192 192 Net realized capital (gains) loss (167) (53) (3) 622 399 Pre-tax operating income (loss) 1,090 1,406 48 (21) 2,523 4Q12 Other Operations 4Q13 ($ in millions) AIG Property Casualty ($ in millions) AIG Property Casualty AIG Life and Retirement AIG Life and Retirement Mortgage Guaranty Other Operations Total Total Mortgage Guaranty $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ |

22 Non-GAAP Reconciliation – After-tax Operating Income (1) 1) Includes results of ILFC. 2012 2013 Net income (loss) attributable to AIG (3,958) 1,978 Adjustments to arrive at After-tax operating income attributable to AIG: (Income) loss from discontinued operations 8 (11) Net (income) loss from divested businesses 4,323 97 Uncertain tax positions and other tax adjustments 200 65 Legal reserves (settlements) related to legacy crisis matters (129) (399) Deferred income tax valuation allowance releases (116) (540) Changes in fair value of AIG Life and Retirement fixed maturity securities designated to hedge living benefit liabilities, net of interest expense 7 22 Changes in benefit reserves and DAC, VOBA and SIA related to net realized capital gains 52 67 AIG Property Casualty other income (expense), net - 47 Loss on extinguishment of debt - 125 Net realized capital (gains) losses (97) 253 After-tax operating income attributable to AIG 290 1,704 After-tax Operating Income Attributable to AIG ($ in millions) Fourth Quarter |

23 2012 2013 Annualized Net income attributable to AIG NM 7,912 $ Annualized After-tax operating income attributable to AIG 1,160 $ 6,816 Average AIG Shareholders' equity 99,834 99,632 Less: Average AOCI 12,394 6,435 Average AIG Shareholders' equity, excluding average AOCI 87,440 $ 93,197 $ ROE NM 7.9% ROE excluding AOCI NM 8.5% ROE - After-tax operating income 1.3% 7.3% Return On Equity Fourth Quarter Non-GAAP Reconciliation – Return On Equity 1) Includes net deferred tax asset. 2) Computed as Annualized Net income (loss) attributable to AIG divided by Average AIG Shareholders' equity. 3) Computed as Annualized Net income (loss) attributable to AIG divided by Average AIG Shareholders' equity, excluding AOCI. 4) Computed as Annualized After-tax operating income divided by Average AIG Shareholders' equity, excluding AOCI. (2) (3) (4) (1) (1) |

24 Non-GAAP Reconciliation – BVPS ex. AOCI and Premiums & Deposits 2012 2013 Total AIG shareholders’ equity 98,002 $ 100,470 $ Less: AOCI 12,574 6,360 Total AIG shareholders’ equity, excluding AOCI 85,428 $ 94,110 $ Total common shares outstanding 1,476,321,935 1,464,063,323 Book value per common share 66.38 $ 68.62 $ Book value per common share, excluding AOCI 57.87 $ 64.28 $ 2012 2013 Premiums and deposits 5,215 $ 8,042 $ Deposits (4,384) (7,238) Other (197) (198) Premiums 634 $ 606 $ December 31, AIG Life and Retirement Premiums and Deposits ($ in millions) Book Value Per Common Share - Ex. AOCI ($ in millions, except per share data) Fourth Quarter |

25 Non-GAAP Reconciliation – Accident Year Combined Ratio, As Adjusted 1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13 4Q13 Commercial Insurance Loss ratio 72.3 70.7 78.0 100.9 64.9 72.6 71.8 77.9 Catastrophe losses and reinstatement premiums (1.5) (5.4) (4.5) (32.8) (0.6) (6.0) (3.5) (3.6) Prior year development net of premium adjustments (0.5) 0.1 (2.7) (1.7) 1.1 (4.4) (2.1) (0.9) Net reserve discount benefit (charge) - 1.9 - - - - - (6.1) Accident year loss ratio, as adjusted 70.3 67.3 70.8 66.4 65.4 62.2 66.2 67.3 Acquisition ratio 18.0 17.2 15.6 15.5 16.3 16.3 15.8 16.1 General operating expense ratio 11.3 11.4 12.4 13.9 11.0 12.8 12.6 13.7 Expense ratio 29.3 28.6 28.0 29.4 27.3 29.1 28.4 29.8 Combined ratio 101.6 99.3 106.0 130.3 92.2 101.7 100.2 107.7 Catastrophe losses and reinstatement premiums (1.5) (5.4) (4.5) (32.8) (0.6) (6.0) (3.5) (3.6) Prior year development net of premium adjustments (0.5) 0.1 (2.7) (1.7) 1.1 (4.4) (2.1) (0.9) Net reserve discount benefit (charge) - 1.9 - - - - - (6.1) Accident year combined ratio, as adjusted 99.6 95.9 98.8 95.8 92.7 91.3 94.6 97.1 Consumer Insurance Loss ratio 58.1 59.2 58.3 67.9 57.8 58.9 58.8 60.4 Catastrophe losses and reinstatement premiums (0.1) (1.1) (0.6) (8.9) (0.3) (0.3) (1.2) (0.6) Prior year development net of premium adjustments 0.4 1.0 - (1.0) 1.3 1.6 0.9 0.9 Accident year loss ratio, as adjusted 58.4 59.1 57.7 58.0 58.8 60.2 58.5 60.7 Acquisition ratio 23.7 23.5 25.7 26.9 24.9 25.9 26.1 25.2 General operating expense ratio 14.9 15.0 14.8 16.4 15.7 15.3 15.0 17.7 Expense ratio 38.6 38.5 40.5 43.3 40.6 41.2 41.1 42.9 Combined ratio 96.7 97.7 98.8 111.2 98.4 100.1 99.9 103.3 Catastrophe losses and reinstatement premiums (0.1) (1.1) (0.6) (8.9) (0.3) (0.3) (1.2) (0.6) Prior year development net of premium adjustments 0.4 1.0 - (1.0) 1.3 1.6 0.9 0.9 Net reserve discount benefit (charge) - - - - - - - - Accident year combined ratio, as adjusted 97.0 97.6 98.2 101.3 99.4 101.4 99.6 103.6 Total AIG Property Casualty Loss ratio 68.0 68.9 71.4 87.6 63.3 68.0 67.3 68.2 Catastrophe losses and reinstatement premiums (0.9) (3.7) (2.9) (22.9) (0.5) (3.7) (2.7) (2.4) Prior year development net of premium adjustments (0.6) (1.5) (2.0) (1.4) 0.4 (2.3) (0.8) (3.1) Net reserve discount benefit (charge) (0.2) 1.1 - - - (0.1) (0.1) 3.7 Accident year loss ratio, as adjusted 66.3 64.8 66.5 63.3 63.2 61.9 63.7 66.4 Acquisition ratio 20.2 19.6 19.5 20.2 19.7 20.0 19.7 19.5 General operating expense ratio 13.7 13.9 14.1 17.3 14.3 14.6 14.6 16.1 Expense ratio 33.9 33.5 33.6 37.5 34.0 34.6 34.3 35.6 Combined ratio 101.9 102.4 105.0 125.1 97.3 102.6 101.6 103.8 Catastrophe losses and reinstatement premiums (0.9) (3.7) (2.9) (22.9) (0.5) (3.7) (2.7) (2.4) Prior year development net of premium adjustments (0.6) (1.5) (2.0) (1.4) 0.4 (2.3) (0.8) (3.1) Net reserve discount benefit (charge) (0.2) 1.1 - - - (0.1) (0.1) 3.7 Accident year combined ratio, as adjusted 100.2 98.3 100.1 100.8 97.2 96.5 98.0 102.0 AIG Property Casualty Accident year combined ratio, as adjusted Quarterly |

26 |