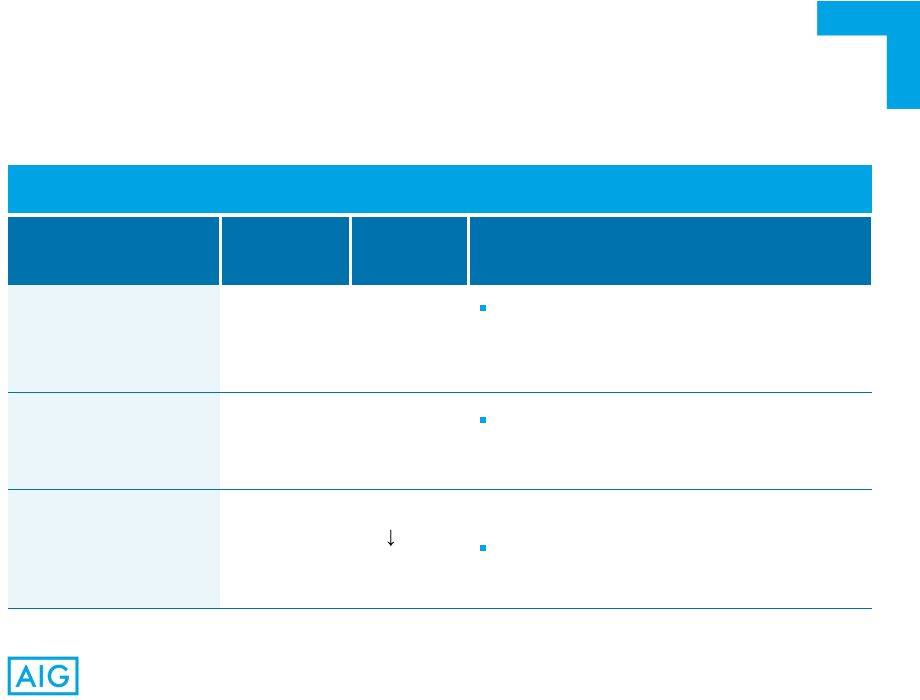

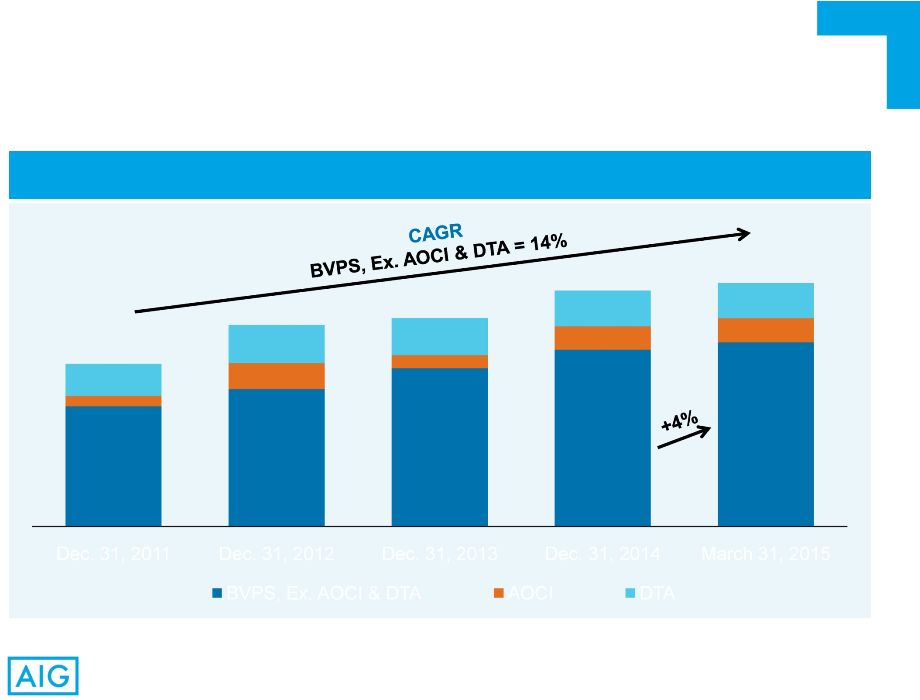

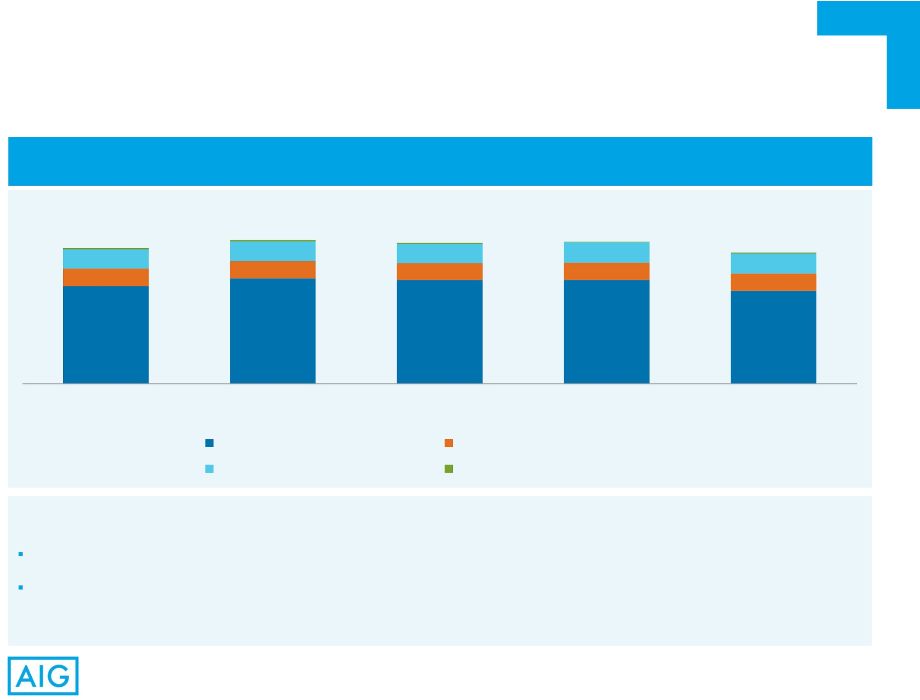

Glossary of Non-GAAP Financial Measures AIG – income and loss from divested businesses, including: • gain on the sale of International Lease Finance Corporation (ILFC); and • certain post-acquisition transaction expenses incurred by AerCap Holdings N.V. (AerCap) in connection with its acquisition of ILFC and the difference between expensing AerCap’s maintenance rights assets over the remaining lease term as compared to the remaining economic life of the related aircraft and related tax effects; – legacy tax adjustments primarily related to certain changes in uncertain tax positions and other tax adjustments; and – legal reserves and settlements related to legacy crisis matters, which include favorable and unfavorable settlements related to events leading up to and resulting from our September 2008 liquidity crisis and legal fees incurred as the plaintiff in connection with such legal matters. 41 We use the following operating performance measures because we believe they enhance the understanding of the underlying profitability of continuing operations and trends of our business segments. We believe they also allow for more meaningful comparisons with our insurance competitors. When we use these measures, reconciliations to the most comparable GAAP measure are provided, on a consolidated basis. Operating revenue excludes Net realized capital gains (losses), Aircraft leasing revenues, income from legal settlements (included in Other income for GAAP purposes) and changes in fair values of fixed maturity securities designated to hedge living benefit liabilities, net of interest expense (included in Net investment income for GAAP purposes). After-tax operating income attributable to AIG is derived by excluding the following items from net income attributable to AIG: – deferred income tax valuation allowance releases and charges; – changes in fair value of fixed maturity securities designated to hedge living benefit liabilities (net of interest expense); – changes in benefit reserves and deferred policy acquisition costs (DAC), value of business acquired (VOBA), and sales inducement assets (SIA) related to net realized capital gains and losses; – other income and expense — net, related to Corporate and Other run-off insurance lines; – loss on extinguishment of debt; – net realized capital gains and losses; – non-qualifying derivative hedging activities, excluding net realized capital gains and losses; – income or loss from discontinued operations; Return on Equity – After-tax Operating Income Excluding AOCI and Return on Equity – After-tax Operating Income Excluding AOCI and DTA are used to show the rate of return on shareholders’ equity. We believe these measures are useful to investors because they eliminate the effect of non-cash items that can fluctuate significantly from period to period, including changes in fair value of our available for sale securities portfolio, foreign currency translation adjustments and U.S. tax attribute deferred tax assets. Deferred tax assets represent U.S. tax attributes related to net operating loss carryforwards and foreign tax credits. Amounts are estimates based on projections of full year attribute utilization. Return on Equity – After-tax Operating Income Excluding AOCI is derived by dividing actual or annualized after-tax operating income attributable to AIG by average AIG shareholders’ equity, excluding average AOCI. Return on Equity – After-tax Operating Income Excluding AOCI and DTA is derived by dividing actual or annualized after-tax operating income attributable to AIG, by average AIG shareholders’ equity, excluding average AOCI and DTA. Book Value Per Share Excluding Accumulated Other Comprehensive Income (AOCI) and Book Value Per Share Excluding AOCI and Deferred Tax Assets (DTA) are used to show the amount of our net worth on a per-share basis. We believe these measures are useful to investors because they eliminate the effect of non-cash items that can fluctuate significantly from period to period, including changes in fair value of our available for sale securities portfolio, foreign currency translation adjustments and U.S. tax attribute deferred tax assets. Deferred tax assets represent U.S. tax attributes related to net operating loss carryforwards and foreign tax credits. Amounts are estimates based on projections of full year attribute utilization. Book Value Per Share Excluding AOCI is derived by dividing Total AIG shareholders’ equity, excluding AOCI, by Total common shares outstanding. Book Value Per Share Excluding AOCI and DTA is derived by dividing Total AIG shareholders’ equity, excluding AOCI and DTA, by Total common shares outstanding. |