Exhibit 14

| UPDATE OF THE | ||

| Economic | ||

| and Financial Document | ||

| 2020 | ||

| Submitted by the Prime Minister | ||

| Giuseppe Conte | ||

| and the Minister of the Economy and Finance | ||

| Roberto Gualtieri | ||

| Approved by the Cabinet on 5 October 2020 |

introduction

In recent months, the covid-19 pandemic has severely affected our country from a health point of view as well as in the economic and social system. The economic indicators show even too briefly the enormous difficulties that Italian families, workers and companies have had to endure.

The difficult context in which the Government found itself to operate has required to adopt a strategy based on different levels. In the first few months, the containment of the spread of contagion and the protection of health required the adoption of progressively more stringent precautionary measures, which have changed the lives of Italians in a sudden way. These measures have had a heavy repercussion on the economic system that has experienced, in a few months, the worst fall of the gross domestic product in Republican history.

The crisis has produced and is producing markedly heterogeneous economic, social and health effects from the point of view of territories, economic sectors, income levels, gender and generations. Several provinces of Lombardy and other Northern areas have been the epicenter of the spread of the contagion to which they paid a particularly hard price in terms of human lives; tourism and transport, trade and restaurants, sport, entertainment and the event sector and, more generally, sectors requiring human gathering have suffered above average turnovers falls and are still affected by the economic effects of the pandemic and persistent uncertainty; low-income households have been severely affected as well as women for whom it has been even heavier and unfair than usual to reconcile work and childcare needs; the latter faced a particularly complicated second semester of the school year which, among other things, showed significant digital inequalities within the population.

To address this situation, the Government has adopted major economic interventions, totaling 100 billion in terms of the impact on the general government net borrowing in 2020 (over 6 percent of GDP), to which must be added the unprecedented amount of public guarantees on liquidity.

These resources financed measures to limit the effects of the pandemic on household incomes, employment levels and the maintenance of the production system, along with providing the healthcare system the resources needed to contain the pandemic. In international comparison, the combination of healthcare policy and economic policy measures has proved to be, nowadays, among the best, succeeding in ensuring an effective fight against the spread of the virus and, at the same time, the greatest possible protection of incomes and production capacity. For example, and in particular, in the face of an estimated fall in GDP of 9 percent in 2020, employment is projected to fall by less than 2 percent. Overall, the measures introduced by the Government have significantly limited the increase in poverty and inequalities.

| Ministry of Economy and Finance | III |

UPDATE OF THE Economic and Financial Document 2020

Due to the collapse in gross domestic product, the consequent fall in tax revenues and expansionary fiscal policy, the public debt-to-GDP ratio is projected to increase up to 158 percent. Nevertheless, the Italian Republic has continued to finance itself on the capital markets at historically low prices, because of the solidity of our fundamentals but also thanks to the response of the European institutions. The monetary policy put in place by the European Central Bank, the new approach to budgetary and State aid rules and the decision to finally introduce common budgetary instruments financed with European bonds have proved essential for Italy and the euro area overall. The Government made a non-marginal contribution to this change of European strategy, which was decidedly different from that adopted in the last decade.

Starting in May, the economy began to recover, surprising most of the forecasters upwards. For the third quarter, it is now estimated a higher rebound than that assumed in the Stability Programme. The latest available indicators show, in fact, a growth trend in the summer months for industrial production, the construction sector and the turnover of services. Although future prospects continue to be characterised by considerable uncertainty, which suffers from the unpredictability of the evolution of the pandemic in Italy and abroad, as well as the effective availability of effective vaccines and possible therapies, economic policy must gradually move from the phase of protection of the economic and social system to that of the revamp of growth in the short term as well as in the medium and long term.

The next budget law and funds from the Recovery and Resilience Facility (RRF) will have a total value of about 2 percent of GDP in 2021. Economic growth will significantly benefit, reaching 6 percent. Over the next two years, the expansion of fiscal policy will gradually slow down to a primary surplus of 0.1 percentage points and a net borrowing over GDP of 3 percent. The level of GDP recorded in the year preceding the pandemic will therefore be recovered in 2022. Over the next three years, the public debt-to-GDP ratio will be placed on a significant and credible downward path.

The macroeconomic and public finance scenario outlined in this Update to the Stability Programme incorporates the substantial European resources that will be made available to our country by the Next Generation EU (NGEU), in particular, by the RRF. This is undoubtedly an unrepeatable opportunity for our country, which will allow us to overcome the unprecedented crisis triggered by the pandemic and a prolonged period of stagnation that has been going on for over twenty years. The resources deployed by the European Union will be used to achieve the objectives of innovation and environmental and social sustainability that characterise the programme of the new European Commission, fully consistent with the approach that the Government has taken since its settlement.

As soon as the agreement is finalised within the European institutions, the Government will present the National Recovery and Resilience Plan (NRRP). The NRRP’s interventions will help to boost public and private investment and implement important reforms within a plan of relaunch and transition to a more innovative and environmentally sustainable economy and more socially inclusive. This will make it possible to invest in the future to provide new job opportunities

| IV | Ministry of Economy and Finance |

introduction

to young people and, more generally, to create conditions that make the country more modern, fair and sustainable.

In addition to actions aimed at accelerating the ecological and digital transition and increasing the competitiveness and resilience of Italian companies, particular attention will be paid to territorial cohesion, through tax cuts, infrastructure investments and strengthening the enabling factors for growth. Particular efforts and resources will also be directed towards investment in education and research, with the aim of making a significant leap in the amount of resources and the quality of policies, and the strengthening and modernisation of the healthcare system.

A crucial role in the NRRP will be played by public investment, which will be significantly increased in the coming years with the aim of bringing them back to levels both above those prior to the 2008 crisis and above the European average. The increased availability of financial resources, combined with the improvement of design, implementation and expenditure ability by the general government, will be fundamental to achieve a qualitative leap in infrastructure, material and intangible, of the country. Improving the ability of administrations to make investments in ex-ante fixed times and ways is an essential and strategic objective as, together with other structural reforms, it will ensure a higher rate of growth for the country even when European resources will be exhausted.

The economic policy strategy also includes a broad programme of reforms to address bottlenecks in different sectors – from justice to public administration – and to increase the potential growth of our economy. Some of these actions will be financed with the European resources of the RRF, which will stimulate their rapid implementation.

With the resources of the public budget, the Government also intends to introduce over the next three years a reform of the tax system aimed at simplification and transparency, improving fairness and efficiency of the tax burden and reducing the fiscal pressure. The reform will be designed in a manner consistent with the enabling law on the single grant, also to promote participation of women in the labour market and increase population growth.

In the taxation field, a new fund will be introduced, to be financed with the higher revenues linked to the increase in tax compliance that will then be returned, in whole or in part, to taxpayers in the form of a reduction of the tax levy. The Government intends to establish a tax pact with Italian citizens that rewards the tax and contribution loyalty of companies and workers.

To show consistency between public finance trends and the resources made available by the RRF, this Update presents a broader horizon than usual, reaching up 2026. The NRRP and its resources will have a significant positive impact on the growth forecasts of the Italian economy and on the projections regarding the public debt to GDP ratio. Indeed, the scenario shows significant economic growth, which is steadily higher than in the last twenty years, which will allow the debt ratio to be reduced to its pre-covid level over a decade. This perspective is made reliable by the trend of the deficit in the unchanged legislation scenario over the

| Ministry of Economy and Finance | V |

UPDATE OF THE Economic and Financial Document 2020

next three years and by the absence of safeguard clauses, which, for the first time in several years, give us a realistic picture of the state of public finances.

We therefore have the opportunity to relaunch our country’s growth in terms of environmental and social sustainability, as well as to dissolve structural knots, social and territorial disparities that have been dragging on for a long time. This requires a change of pace and mentality on the part of the institutions and the components of the Italian economy and society. All together, we are called to a great challenge of responsibility in the selection of projects, which must be assessed in their capacity to relaunch in a structural way the growth and employment of this country, to heal its territorial and social fractures, to make it more innovative, stronger and fairer. This is a unique and unrepeatable opportunity, not only to overcome the consequences of the pandemic, but also to improve and relaunch our country and make it the protagonist of the challenges of the future.

Roberto Gualtieri

Minister for Economy and Finance |

| VI | Ministry of Economy and Finance |

INDEX

| I. | OVERALL FRAMEWORK AND fiscal POLICY |

| I.1 | Recent trends in the economy |

| I.2 | Macroeconomic scenario under unchanged legislation 2020-2023 |

| I.3 | Public finance forecast: scenario under unchanged legislation |

| I.4 | Macroeconomic framework and public finance under policy scenario |

| II. | MACROECONOMIC FRAMEWORK |

| II.1 | The international economy |

| II.2 | Italian economy: recent trends |

| II.3 | Italian economy: prospects |

| II.4 | Policy scenario |

| III. | NET BORROWING AND PUBLIC DEBT |

| III.1 | Summary data and forecasts under unchanged legislation |

| III.2 | Public finance: policy scenario |

| III.3 | The evolution of the debt-to-GDP ratio |

| III.4 | The debt rule and other relevant factors |

| III.5 | Medium-term public debt projection scenarios |

| III.6 | Main public finance measures adopted |

| III.7 | Valorisation of public property |

| IV. | THE REFORMS AND THE RECOMMENDATIONS OF THE COUNCIL OF THE EUROPEAN UNION |

| IV.1 | The National Recovery and Resilience Plan |

| IV.2 | Council Recommendations to the Country |

| IV.3 | Main actions in line with the Country-Specific Recommendations for 2020 |

ANNEXES

Explanatory note on multi-year laws on non-permanent capital expenditure

Policy report on fiscal expenditure

Report on the results achieved in the field of measures to fight tax and social security evasion - year 2020

| Ministero dell’economia e delle finanze | VII |

UPDATE OF THE ECONOMIC AND FINANCIAL DOCUMENT 2020

LIST OF TABLES

| Table I.1 | Synthetic macroeconomic framework under unchanged legislation |

| Table I.2 | Provisional summary framework of Recovery Plan Resources utilisation |

| Table I.3 | Macroeconomic framework based on the policy scenario |

| Table I.4 | Public finance indicators |

| Table II 1 | International exogenous variables |

| Table II.2 | Macroeconomic framework under unchanged legislation |

| Table II.3 | Effects on the GDP of the policy scenario with respect to the unchanged legislation scenario (impact on growth rates) |

| Table II.4 | Policy scenario macroeconomic framework |

| Table III.1.a | General government account at unchanged legislation |

| Table III.1.b | General government account at unchanged legislation |

| Table III.1.c | General government account at unchanged legislation |

| Table III.2 | Summary of public finance under the policy scenario |

| Table III.3 | Cyclically adjusted public finance |

| Table III.4 | Significant deviations |

| Table III.5 | Flexibility granted to Italy in the Stability Pact |

| Table III.6 | One-off measures under unchanged legislation |

| Table III.7 | General government debt by sub-sector |

| Table III.8 | Compliance with the debt rule: forward looking and cyclically adjusted debt |

| Table III.9 | Parameters affecting dynamic of debt-to GDP ratio |

| Table III.10 | Cumulative effects of the last measures approved in 2020 on the general government net borrowing |

| Table III.11 | Cumulative net effects of the last measures approved in 2020 on the general government net borrowing by sub-sector |

| Table III.12 | Net effects of the last measures approved in 2020 on the general government net borrowing |

| Table IV.1 | Country’s specific recommendations for 2019 and 2020 |

| Ministero dell’economia e delle finanze | VIII |

UPDATE OF THE ECONOMIC AND FINANCIAL DOCUMENT 2020

FIGURES

| Figure I.1 | Gross domestic product and industrial production |

| Figure I.2 | Confidence climate of Italian businesses |

| Figure I.3 | Recorded cases of Coronavirus infections in Italy |

| Figure I.4 | Real GDP forecast under unchanged legislation and under policy scenario |

| Figure I.5 | Deficit and public debt as ratio to GDP – policy scenario 2020-2023 |

| Figure I.6 | Debt-to-GDP ratio path under policy scenario to 2026 and extrapolation to 2031, maintaining the 2026 structural primary balance unchanged |

| Figure II.1 | Number of Covid-19 recorded cases by region and world deaths (weekly data, updated at 21 September) |

| Figure II.2 | Positivity rate at Covid-19 (%, share of positive tests on the number of performed tests, rolling 7 days average, data updated at 29 September) |

| Figure II.3 | Trend of the world trade (volume, data, index, 2010=100) |

| Figure II.4 | Global composite PMI and by Country |

| Figure II.5 | Price of Brent and Futures |

| Figure II.6 | Contributions to GDP growth |

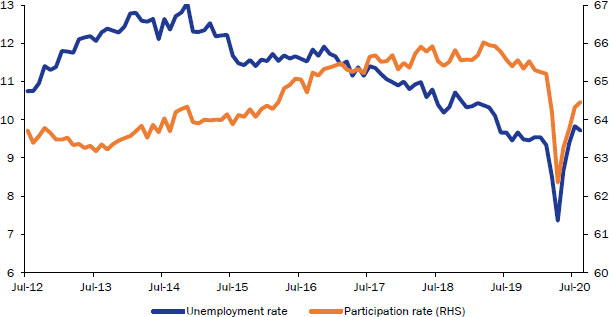

| Figure II.7 | Unemployment rate and participation rate |

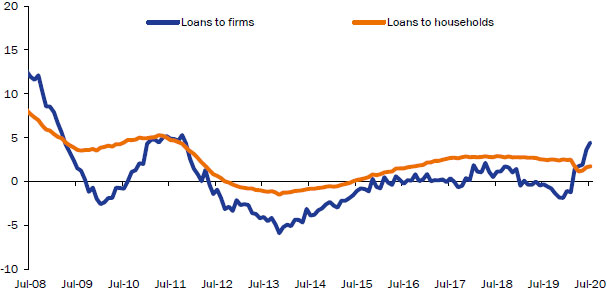

| Figure II.8 | Loans to the private sector |

| Figure II.9 | Real GDP forecast under unchanged legislation scenario |

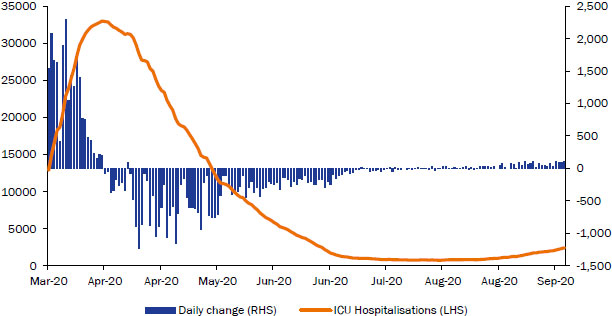

| Figure II.10 | Coronavirus patients in Italian hospitals (number of presences) |

| Figure III.1 | Trend of the debt-to-GDP ratio, gross and net of Euro Area supports |

| Figure III.2 | GDP and debt-to-GDP ratio projections, 2020-2031 |

BOX INDEX

| Chapter II | Recent initiatives of the Italian Government in response to the covid-19 health emergency |

| The revision of the forecasts for 2020 and 2021 | |

| A risk (or sensitivity) analysis of exogenous variables | |

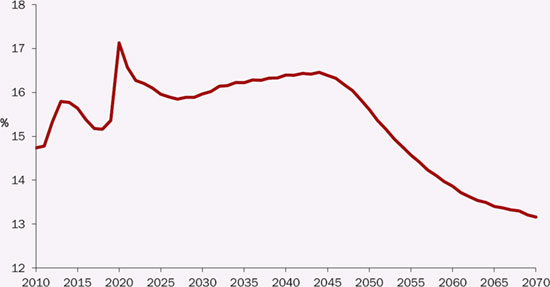

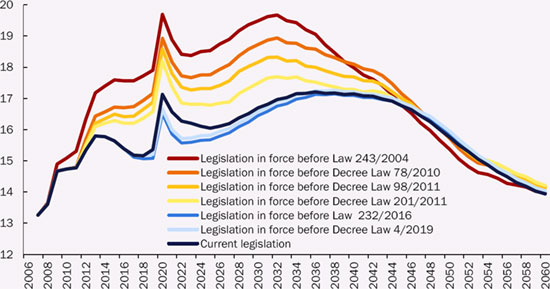

| Chapter III | Medium to long-term trends in the Italian pension system and public expenditure related to ageing |

| The activation of the general escape clause of the Stability and Growth Pact | |

| Estimating potential GDP at the time of the pandemic | |

| Assessment of revenues arising from the fight against tax evasion |

| Ministero dell’economia e delle finanze | IX |

UPDATE OF THE ECONOMIC AND FINANCIAL DOCUMENT 2020

Ministero dell’economia e delle finanze

| X |

I. overall framework and FISCAL policy

I.1 recent trends in the economy

The measures of social distancing and closure of productive sectors implemented from mid-March to early May in response to the covid-19 epidemic have caused an unprecedented fall in economic activity. Since May, economic indicators have recovered, thanks to the gradual easing of measures to prevent infection and a series of powerful economic policy measures to support employment, incomes and the liquidity of households and businesses. Overall, these interventions amounted to 100 billion (6.1 percentage points of GDP) in terms of the expected impact on the general government net borrowing.

Although economic activity is recovering, it remains well below the 2019 levels. Some restrictions remain in force, for example in relation to major sporting and artistic events; schools and universities have only recently restarted teaching on site. In addition, the virus has continued to spread globally, making precautionary measures necessary in all major countries of the world, resulting in a fall in international trade. Despite a strong recovery from May onwards, Italian exports continue to suffer from the global crisis, as well as the presence of foreign tourists remains much lower than in normal times.

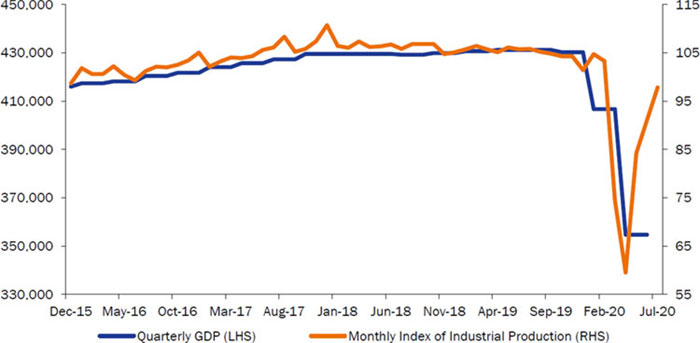

According to Istat’s latest estimates, GDP fell by 5.5 percent in the first quarter and 13.0 percent in the second quarter in quarter-on-quarter terms. The current Istat figure for the first quarter is equal to the Stability Programme forecast, while the fall in the second quarter is higher (in the Stability Programme it was expected to be -10.5 percent).

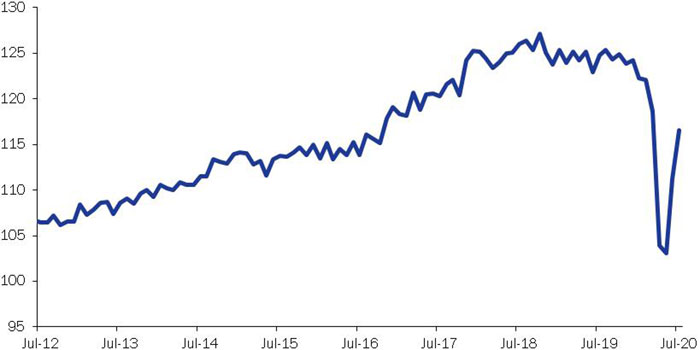

| FIGURE I.1: gross domestic product and industrial production |

|

| Source: Istat. |

MINISTRY OF ECONOMY AND FINANCE

| 1 |

UPDATE OF THE Economic and Financial Document 2020 |

For the third quarter, it is now estimated a significant rebound, higher than assumed in the Stability Programme (9.6 percent), which would bring the level of GDP estimated for this period slightly above the forecast in the Stability Programme. The latest available indicators show, in fact, a growth trend in the summer months.

As regards July, the index of industrial production increased by 7.4 percent over the previous month, resulting in an acquired growth of 25 percentage points in the quarter. In the same month, also the production of the construction sector continued to recover (+3.5 percent on June, with a carry-over on the third quarter of 41 percentage points). In addition, data on digital invoices indicate a marked recovery of service turnover compared to previous months1. On the demand side, with regard to consumption, retail sales in July show a slight setback, but this follows the sharp increase in May and June; instead, the registrations of new cars increase compared to the previous month on a seasonally adjusted basis. There are also positive indications from exports, with a monthly growth of 5.7 percent in nominal terms and a y-o-y contraction that falls to -7.3 percent, from -12.1 percent in June.

The indicators available so far for August are also positive. According to the Istat survey, business confidence has increased in all sectors of activity: the synthetic business confidence index in August reached a level of 81.4, still well below 98.2 in January, but well above the minimum in May, 53.8 (the survey was not published in April). In August, electricity production and consumption, road traffic and car registrations also rise.

| FIGURE I.2: confidence climate of Italian businesses |

|

| Source: Istat and MEF estimates for April 2020, in which the survey was not published. |

1 To be precise, since the historical series of monthly data starts in January 2019, it is not possible to seasonally adjust the series. The data show that the y-o-y contraction in the taxable amount of e-invoicing (corrected for working days) shrank considerably in July compared to June, which is likely to result in a cyclical increase in turnover and value added.

| 2 | MINISTRY OF ECONOMY AND FINANCE

|

I. overall framework and fiscal policy |

Economic developments in September should have benefited from the resumption of work on site and the reopening of schools and universities. As covid-19 infections resume, citizens’ behaviour appears to be more cautious, with possible repercussions on consumption expenditure. However, the monthly Istat survey shows a further increase in consumer and business confidence. The sentiment rises in all productive sectors; in particular, the confidence of manufacturing companies producing capital goods and of companies active in building and specialised works is rising. There is also a marked increase in confidence in services, in particular in tourism. Overall, all this indicates that the rebound of GDP in the third quarter could also exceed that underlying the new quarterly forecast.

Regarding the foreign trade balance, in the first seven months of the year, the trade surplus rose by EUR 3 billion compared with the same period in 2019, to 32.7 billion, while the current account surplus fell slightly, mainly due to a higher deficit in services2. The latter was affected by the fall of the presence and expenditure of foreign tourists in Italy3.

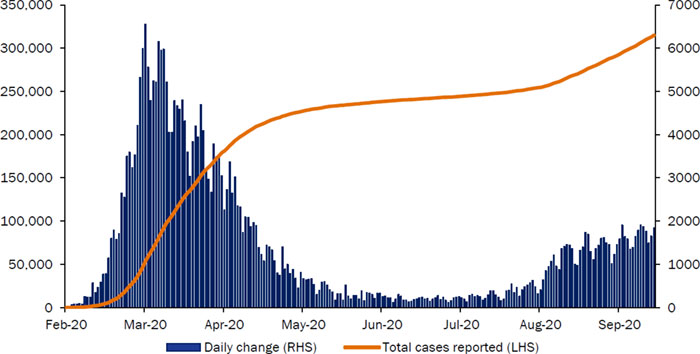

Inflation trend reflected the weakness of demand and the fall in oil and commodity prices during the most acute global crisis period. In the last two months (August and September), the consumer price index has fallen by 0.5 percentage points compared to a year earlier, approaching the historical low previously recorded in January 20154.

| FIGURE I.3: recorded cases OF CORONAVIRUS Infections in Italy |

|

| Source: Refinitiv. |

2 The current account surplus in the first seven months of the year amounted to 20.6 billion, down from 25.4 billion in the same period of 2019. However, the July figure improved compared to the corresponding month of 2019 (9.3 billion versus 8.7 billion) thanks to the commodity component (with a surplus of 9.8 billion versus 8.0 billion in 2019).

3 For example, in July the surplus for the ‘travel’ component of the services balance recorded a surplus of 1.1 billion, compared with 3.0 billion in July 2019. Credits (i.e. foreign spending in Italy) fell from 6.0 billion in July 2019 to 2.4 billion in July 2020.

4 Inflation measured on the basis of the consumer price index for the whole nation, including tobacco, marked a minimum of -0.6 percent in January 2015.

MINISTRY OF ECONOMY AND FINANCE

| 3 |

UPDATE OF THE Economic and Financial Document 2020 |

In addition to the mentioned cyclical factors, a further downward pressure in prices has been added since June, due to the significant appreciation of the euro exchange rate of almost 8 percentage points vis-à-vis the dollar compared to the average trend during the first five months of the year. On average for the first eight months of the year, the average inflation rate according to the consumer price index for the whole nation was -0.1 percent. The trend of the GDP deflator was more favourable, as it grew, on average for the first two quarters, by 1.4 percent in annual terms.

On the labour market side, the fall in worked hours in industry and market services (-26.5 percent in the second quarter compared to the fourth quarter of 2019) was even dipper than that of value added (-20.4 percent). However, thanks also to the measures taken by the Government, such as the introduction of the Extended Supplementary Income Scheme (Cassa Integrazione Guadagni in Deroga), the number of employees fell much less than labour input (-2.4 percent in the second quarter compared to the fourth quarter of 2019) and recovered part of the lost ground already in the third quarter. The Istat monthly labour force survey shows that employment increased in both July and August, with month-on-month increases of 0.4 percent in both months and an acquired growth of 0.5 percentage points in the quarter.

I.2 macroeconomic scenario under unchanged legislation 2020-2023

The official forecast of real GDP in 2020 is lowered to -9.0 percent (-9.1 percent on quarterly data), from -8.0 percent of the Stability Programme forecast (-8.1 percent on quarterly data). The main reason for the downward revision is the sharpest contraction of GDP in the second quarter, explained by the length of the period of partial closure of production activities in Italy and by the higher than assumed in April spread of the epidemic on global scale. In addition, a much more cautious forecast of GDP growth in the fourth quarter (now indicated at 0.4 percent, compared with 3.8 percent foreseen in the Stability Programme) was adopted.

Caution about the increase in GDP in the fourth quarter reflects, on the one hand, the strong rebound estimated for the summer quarter and, on the other hand, the recent resurgence of covid-19 infections, in both absolute terms and as a ratio of daily swab tests. Compared to the minimum achieved in the second half of July, the number of hospitalized covid-19 patients in Italian hospitals and deaths also rose. The recovery of new infections in Italy is moderate, but outside our country, the pandemic continues to expand and in some European countries social distancing measures have been reintroduced, albeit less drastic compared to last spring. All this could slow down the recovery of Italian exports observed in recent months.

The availability of increasingly reliable rapid tests and the high number of daily swabs will make it possible to monitor the epidemic more and more effectively. However, to be able to detect and circumscribe new local outbreaks, it is necessary to contain the number of new infections. The forecast for the next two quarters therefore takes into account the need to maintain prudential rules of

| 4 | MINISTRY OF ECONOMY AND FINANCE

|

I. overall framework and fiscal policy |

behaviour and the high probability that inflows of foreign tourists will remain far below pre-crisis levels.

Meanwhile, the development of covid-19 vaccines by numerous pharmaceutical companies is continuing and major advances are being made in the development of monoclonal antibodies therapies. The European Commission has already signed two agreements on the supply of vaccines and is discussing four more ones with as many pharmaceutical companies5. The production of some vaccines is already in progress while third stage clinical trials are being carried out. At the end of this phase, vaccines will have to be approved by the European Medicines Agency (EMA), which assesses their efficacy and safety.

The basic assumption adopted for the macroeconomic forecast remains unchanged with respect to the Stability Programme, i.e. that the distribution of one or more vaccines begins by the first quarter of 2021 and that in mid-year the availability of new therapies and vaccines is such that the Government can relax most, if not all, restrictive measures. As a result, the recovery of the economy is expected to regain momentum during 2021, also giving rise to a significant carry-over effect on 2022.

GDP growth rates in the new forecast under unchanged legislation are 5.1 percent for 2021, 3.0 percent for 2022 and 1.8 percent in 2023. These increases seem to be high if compared to the results of the last twenty years, but it should be borne in mind that the starting point is an unprecedented fall in GDP. Moreover, in this scenario, quarterly GDP would not return to end-2019 levels until the second quarter of 2023; indeed, on year average, the level of real GDP in 2023 would be higher than in 2019 by only 0.3 percentage points.

TABLE I.1: Synthetic MACROECONOMIC framework under unchanged legislation (1) (percentage changes unless otherwise indicated) | |||||

| 2019 | 2020 | 2021 | 2022 | 2023 | |

| GDP | 0.3 | -9.0 | 5.1 | 3.0 | 1.8 |

| GDP deflator | 0.7 | 1.1 | 0.7 | 1.1 | 1.0 |

| Consumption deflator | 0.5 | 0.0 | 0.6 | 1.1 | 1.0 |

| Nominal GDP | 1.1 | -8.0 | 5.8 | 4.2 | 2.8 |

| FTE Employment (2) | 0.2 | -9.5 | 5.0 | 2.6 | 1.7 |

| LF Employment (3) | 0.6 | -1.9 | -0.2 | 0.9 | 0.9 |

| Unemployment rate | 10.0 | 9.5 | 10.7 | 10.3 | 9.8 |

| Current account balance (% of GDP) | 3.0 | 2.4 | 2.7 | 2.8 | 2.8 |

| (1) Any inaccuracies result from rounding. | |||||

| (2) Employment expressed in terms of full time equivalent units (FTE). | |||||

| (3) Number of persons employed based on the Continuing Labour Forces Survey (LFS). | |||||

Compared to the Stability Programme forecast, the update of the exogenous variables in the forecast only marginally affects the estimate of real GDP for 2020

5 Coronavirus: the Commission signs second contract to ensure access to a potential vaccine, Press release, Brussels, 18 September 2020. The agreement signed by the European Commission and AstraZeneca states the possibility for the EU to acquire up to 300 million doses of the anti-covid-19 vaccine, with an option on an additional 100 million doses. The agreement between the Commission and Sanofi-GSK provides for further 300 million one. The Commission is negotiating further agreements with other vaccine manufacturers, Johnson & Johnson, CureVac, Moderna and BioNTech.

MINISTRY OF ECONOMY AND FINANCE

| 5 |

UPDATE OF THE Economic and Financial Document 2020 |

(0.1 percentage points). The effect on the forecast for 2021 is however significant and of negative sign (-1.2 percentage points) due to a lowering of the projection of growth of the imports of the countries of destination of Italian exports, as well as the strengthening of the exchange rate of the euro and the recovery of the oil price. However, the expected growth for 2021 rises from 4.7 percent of the Stability Programme to 5.1 percent in view of the huge measures of support and stimulus to the economy introduced in May with the decree-law ‘Relaunch’ and in August with the decree-law ’Support and Relaunch’. Simulations carried out with the ITEM econometric model indicate that the impact of the two decrees on GDP growth is evaluated at 0.8 percentage points in 2020 and 2.5 p.p. in 2021. It should be recalled that the D.L. Relaunch also included the repeal of the VAT increases planned for 2021 and 2022, which - again according to estimates obtained with the ITEM model - alone improves the growth by 0.3 p.p. in 2021, 0.71 p.p. in 2022 and 0.23 p.p. in 2023.

Focusing on the main components of aggregate demand, the fall in GDP this year affects all components with the exception of the general government consumption (although it should be noted that the Istat data are decreasing in the first half of the year). The fall in household consumption would be in line with that of GDP, while gross fixed capital formation would fall much more strongly. Exports of goods and services are expected to drop more than imports on average in the year, which would result in a negative net contribution to the growth of foreign trade.

Over the next three years, the recovery of the economy will be supported both by domestic demand and by foreign trade and, to a lesser extent, by the rise in inventories. The expected increases in household consumption are consistent with a gradual decline in the savings rate in the three-year period 2021-2023 after the marked increase estimated for this year. The expected recovery in investment, foreseen in the unchanged legislation scenario, is characterised by higher growth rates over the next three years than in consumption, but their recovery in 2021 would be lower and would gain more momentum (relating to the overall performance of the economy) over the following two years. The projection of growth in exports follows broadly the expected evolution of international trade, while the trend of imports is consistent with that of domestic demand and production. In line with the recovery in exports of goods and services, a rise of the current account surplus is expected, being the first signals, as mentioned, already pointed out by the figures for July 2020.

Regarding inflation, a moderate recovery is expected after the average flat trend estimated for this year. The forecast is mainly explained by the cyclical rebound and the ongoing recovery of commodity and oil prices.

Finally, with regard to employment, labour units are expected to grow only slightly less than GDP, resulting in a moderate increase in productivity. The number of employees will increase significantly less and the resumption of working hours will mainly take place through the reabsorption of the workers for whom in 2020 the companies have benefited from the Supplementary Income Schemes.

| 6 | MINISTRY OF ECONOMY AND FINANCE

|

I. overall framework and fiscal policy |

The 2020-2021 macroeconomic forecast under unchanged legislation was endorsed by the Parliamentary Budget Office (PBO) on 21 September 2020.6 Endorsement of the 2022-2023 forecast is not required at this stage.

I.3 public finance forecast: scenario under Unchanged legislation

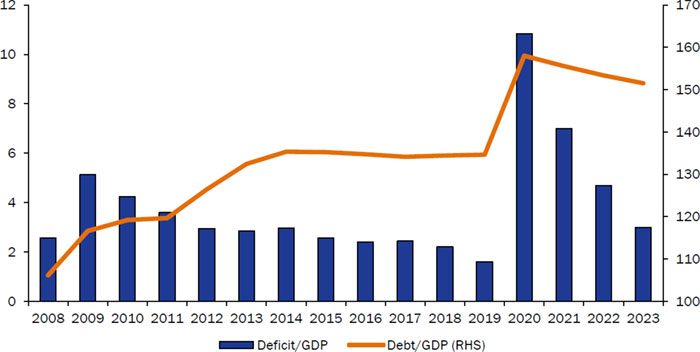

The forecasts updated based on the new macroeconomic framework, previously outlined, call for a general government net borrowing at 10.8 percent of GDP in 2020, with a marked increase from the 1.6 percent estimate of 2019. The increase in the deficit would be the result of a deterioration in the primary balance equivalent to more than 9 percentage points of GDP (from + 1.8 percent to -7.3 percent of GDP) and an increase in interest expenditure from 3.4 percent of GDP in 2019 to 3.5 percent in 2020 - an increase only due to the very strong fall in GDP, since in nominal terms interest payments are estimated to decrease by almost 2 billion compared to last year.

In turn, the deterioration in the primary balance is due to both cyclical factors and discretionary fiscal policy measures. As mentioned above, the expected ex-ante impact of all support measures introduced in response to the pandemic crisis was 6.1 percentage points of GDP. However, the new estimate of net borrowing is approximately 1.3 p.p. of GDP lower than the level deducible from the estimate of the Stability Programme by considering the downward revision of the estimate of GDP and the amounts of interventions carried out in May and August. This is due not only to a lesser use of some measures, but also to a better than expected revenue performance also due to a number of technical factors (e.g. the share of taxpayers who preferred to continue to make payments on the basis of the ‘historic’ rather than ‘forecast’ method).

Looking forward, the deficit based on current legislation is projected to fall to 5.7 percent of GDP in 2021 and then to 4.1 percent in 2022 and 3.3 percent in 2023. The primary balance would significantly improve in 2021 to -2.4 percent of GDP, then it would further converge towards the balance over the following two years, reaching -0.1 percent of GDP in 2023.

Due to the low level of current and expected government bond yields (according to the methodology usually used in official projections), interest expenditure would slightly decrease in absolute terms in 2021-2022 and then slightly increase in 2023. In relation to GDP, it would fall from 3.5 percent this year, to 3.3 percent in 2021 and 3.2 percent in 2022 and 2023.

On the primary expenditure side, the general government account under unchanged legislation set out in more detail in paragraph III.1 of this document is characterised by an increase in wage expenditure in 2020-2021, followed by a slight decrease in 2022-2023, as well as a sharp rise in intermediate consumption this year and then a fall in 2021 confirmed in 2022-2023. Conversely, pension

6 Parliamentary Budget Office, Letter of validation of the macroeconomic scenario under unchanged legislation of the Update of the DEF 2020, www.upbilancio.it.

MINISTRY OF ECONOMY AND FINANCE

| 7 |

UPDATE OF THE Economic and Financial Document 2020 |

expenditure under unchanged legislation would continue to grow throughout the forecast period, at a rate of 2.6 percent in 2020, 2.3 percent in 2021 and 2022, and 2.4 percent in 2023. Concerning the investment expenditure, nominal growth of 8.4 percent this year is expected to be around 6.5 percent in 2021 and 2022, followed by a slight decrease in 2023 (-1.8 percent). Nevertheless, in 2023 the ratio of public investment to GDP would be 2.7 percent, a level that is 0.4 p.p. higher than in 2019.

On the revenue side, the forecast based on current legislation reflects the ceasing of the emergency measures introduced this year and the recovery in nominal GDP. In 2021-2023, tax and contribution revenues grow at a pace consistent with nominal GDP growth. The other revenues are conservatively projected as roughly stationary.

In structural terms (i.e. net of the cyclical component and budgetary impacts of temporary measures) the government balance, after having improved by 0.4 percentage points of GDP in 2019, would worsen by 4.5 p.p. this year, and then improve by 2.4 p.p. in 2021, 0.4 p.p. in 2022 and 0.5 p.p. in 2023.

Moving on to public debt, the updated projection is based on the new annual national accounts data published by Istat on 22 September, which resulted in a moderate upward revision of nominal GDP in the years 2018 and 2019. In light of these new data, the public debt-to-GDP ratio was 134.4 percent in 2018 and 134.6 percent in 2019. In 2020, the strong fiscal expansion, the unprecedented fall in nominal GDP and the impact of some financial operations will push the debt-to-GDP ratio to 158.0 percent7. For the coming years, the scenario under unchanged legislation foresees an average decline in the public debt-to-GDP ratio of almost two percentage points per year in 2021 and 2022, and then a more moderate reduction in 2023, when this ratio would fall to 154.1 percent. The reduction in the debt-to-GDP ratio, although significant in the first two years of the period, would not be sufficient to meet the debt reduction rule in any of its configurations8.

Adverse scenario of resurgence of the epidemic

In line with a similar exercise carried out in the Stability Programme2020, Chapter II of this Update illustrates not only the usual risk scenarios linked to the exogenous variables (euro exchange rate, oil price, BTP spread and financial conditions), but also a more unfavourable scenario regarding the current covid-19 epidemic. This alternative scenario has been formulated in terms of the evolution of the disease, the effectiveness of the new rapid diagnostic tools, medicines and vaccines, as well as the timing of the mass distribution of the vaccines.

In the risk scenario, unlike what was assumed in the baseline scenario under unchanged legislation, the recovery of infections observed from August would

7 Among the above-mentioned financial transactions are the uses of the assigned assets, the instrument provided for in the DL Relaunch of 19 May 2020 to strengthen the capitalisation of companies.

8 The Debt Reduction Rule was introduced in 2011 by the Six Pack, which amended, among other things, Regulation 1467/97 of the European Council containing the rules of the corrective arm of the Stability and Growth Pact.

| 8 | MINISTRY OF ECONOMY AND FINANCE

|

I. overall framework and fiscal policy |

increase significantly in the final months of 2020, also leading to a significant increase in hospitalisations. This would lead the Government to reintroduce precautionary measures, albeit less drastic than last spring. After the rebound of the summer period, the GDP would suffer another fall in the fourth quarter. Assuming the continuation of some restrictive measures in the first few months of next year, the GDP would continue to fall, even if to a much lower extent than in the first half of 2020 (also thanks to the know-how and protective instruments acquired in the meantime). The trend of the epidemic would improve in the spring months, but the mass distribution of vaccines would take place later than assumed in the baseline scenario. Economic activity would resume in the second quarter. Nevertheless, the return towards the pre-crisis situation would be slower than in the baseline scenario and in the last quarter of 2021 real GDP would be more than one percentage point lower the baseline.

The upsurge of the covid-19 crisis would be accompanied by similar if not worse developments in other countries. The Italian economy would therefore also be impacted by lower exports of goods and services. This effect is modeled separately based on the assessments for the global economy made by Oxford Economics. The overall impact of domestic and international factors related to the pandemic risk scenario is given in Table R3 of Chapter II of this document. Based on these impacts, the annual GDP fall in 2020 would widen from -9.0 percent of the baseline scenario to -10.5 percent. GDP growth in 2021 would stop at 1.8 percent, compared with 5.1 percent of the baseline. Conversely, following a recovery path (although partial and delayed), the GDP would then grow by 6.5 percent in 2022 (compared to 3.0 percent of the baseline) and by 2.3 percent in 2023 (compared to 1.8 percent).

From the point of view of public finance, it can be estimated that, ceteris paribus (e.g. given the level of government bond yields), the government deficit would be around 11.5 percent of GDP in 2020 and 7.8 percent of GDP in 2021. The subsequent rebound of GDP would result in a marked decline in the deficit in 2022 and 2023. However, the final point would be a ratio of the public deficit to GDP higher by about half a percentage point in 2023 and a decreasing public debt-to-GDP ratio, but at a level more than 4 percentage points higher than the baseline.

These assessments do not include the possible impact on the budget balance and on the debt of any additional interventions that might be needed in the scenario of strong resurgence of the epidemic in Italy. However, the policy scenario discussed in the following paragraph provides additional resources to support the economy in 2021.

I.4 macroeconomic framework and public finance under policy scenario

The policy scenario is built in the light of the important novelty of the European Recovery Plan, called Next Generation EU (NGEU), a package of tools for the relaunch and resilience of the economies of the European Union that will be equipped with 750 billion resources in the period 2021-2026.

As explained in more detail in the following Chapter IV, the Government has assumed the leading role for the drafting of the National Recovery and Resilience

MINISTRY OF ECONOMY AND FINANCE

| 9 |

UPDATE OF THE Economic and Financial Document 2020 |

Plan (NRRP) provided for by the decision of the European Council of last 21 July9 through the Interministerial Committee for European Affairs (Comitato Interministeriale per gli Affari Europei, CIAE). In turn, the CIAE has entrusted the carrying out of activities to its Subcommittee, the Technical Evaluation Committee (TEC). In August, the latter launched an intensive collection activity of proposals, for projects to be financed through the Recovery and Resilience Facility (RRF), which is the most relevant component of the NGEU. On 9 September, the CIAE approved and subsequently sent to Parliament the Guidelines for the definition of Italy’s NRRP.

Following the outcome of the parliamentary examination and taking into account the policy advice that Parliament will want to formulate, as well as the Guidelines for the compilation of NRRP in the meantime published by the European Commission, in October the Government will draw up a Scheme of the Italian NRRP. In the following months, the latter will be the subject of interlocutions with the European Commission, which in turn will provide further elements for the final drafting of the NRRP. The final version of the Plan is to be presented at the beginning of 2021 and in any case no later than the end of April as scheduled by the European Semester.

As it is known, the RRF provides for a package of grants and loans. Budgetary planning will incorporate both components and is therefore more complex than in the past. The exploitation of the grant component is particularly important as it makes it possible to significantly increase the tangible and intangible public investments, increase expenditure on research, education and training, and stimulate more private investment, without this leading to additional government borrowing.

The NRRP and the financial programming should therefore be fully consistent to each other. To this end, although this Update refers to the three-year period 2021-2023, the Government has also developed six-year macroeconomic and public finance projections, which will form the basis for assessing both the impacts of the investment programme and other NGEU-funded interventions, as well as for achieving public finance targets.

The main objectives of budgetary policy for 2021-2023 can be summarised as follows:

| • | In the short term, support workers and productive sectors most affected by the pandemic as long as the covid-19 crisis continues; |

| • | In line with public finance objectives, fully exploit the resources made available by the NGEU to implement a comprehensive programme of investments and reforms of unprecedented scope and depth and bring the Italian economy on a sustained and balanced growth path; |

| • | Strengthen interventions to support the recovery of the Southern regions and disadvantaged areas, to improve territorial cohesion and to prevent that the covid-19 crisis could accentuate disparities between the different areas of the country. |

9 This decision also approved the Multiannual Financial Framework (MFF) 2021-2027.

| 10 | MINISTRY OF ECONOMY AND FINANCE

|

I. overall framework and fiscal policy |

| • | Implement a comprehensive tax reform that improves the fairness, efficiency and transparency of the tax system by also reducing the tax burden on middle and low incomes, coordinating it with the introduction of a single and universal child allowance (unified family support scheme); |

| • | Ensure a qualitative improvement in public finance, shifting resources towards the most appropriate uses to ensure an improvement in the well-being of the citizens, and in the fairness and the productivity of the economy; |

| • | Assuming that the crisis is gradually overcome over the next two years, the government net borrowing should be reduced to levels compatible with a continuous and significant reduction in the public debt-to-GDP ratio. |

Starting from the public finance scenario under unchanged legislation, the 2021-2023 manoeuvre of the next Budget Law will aim to support the recovery of the economy with a further fiscal boost in 2021, which will be reduced in 2022 and then aim at a significant improvement in the budget balance in 2023. As a result, government net borrowing objectives are set at 7.0 percent in 2021, 4.7 percent in 2022 and 3.0 percent in 2023. For the following years, a further significant improvement in the budget balance is expected to ensure a reduction in the public debt-to-GDP ratio throughout the forecast years.

Net borrowing objectives are also based on the fall in the primary deficit, which is expected to fall from 7.3 percent of GDP this year to 3.7 percent in 2021 and 1.6 percent in 2022, and then turn into a slight surplus (0.1 percent of GDP) in 2023. Under the policy scenario, interest expenditure (calculated on the basis of the same assumption on the implicit cost of debt financing used in the unchanged legislation framework) would fall from 3.5 percent this year to 3.1 percent in 2023.

In terms of the main fields of the manoeuvre, it provides for the refinancing of the so-called unchanged policies not covered by existing legislation (peace missions, refinancing of certain investment funds, business crisis fund, etc.). Secondly, significant resources are provided for to support workers’ employment and incomes, particularly in the sectors most affected by the covid-19 emergency and with particular reference to the first programming year, the 2021. Thirdly, the financing of the cut of the tax wedge on employees (the so-called EUR 100 measure) is completed and the social contributions cut to the South already introduced by the decree-law of August is financed only for the second half of 2020.

A major component of the three-year planning is the introduction of a comprehensive tax reform, which the Government intends to implement based on an enabling law that will be an integral part of the NRRP and its intermediate objectives. The reform will be in line with the introduction of a single and universal child allowance.

A further, important component of budgetary policy for 2021-2023 will be, as already mentioned, the full use of NGEU grants and loans to increase public investment in a never seen magnitude and increase resources for research, training, digitalisation and the conversion of the economy in terms of environmental sustainability.

The 2021-2023 policy scenario assumes the full use of grants under the first phase of the European Recovery Plan, representing 70 percent of the total amount

MINISTRY OF ECONOMY AND FINANCE

| 11 |

UPDATE OF THE Economic and Financial Document 2020 |

estimated for Italy, and of a first part of the remaining 30 percent (limited to 2023). In addition, it assumes a partial recourse to RRF’s loans in deficit. The remaining part of the RRF and the other components of the NGEU will be used in the period 2024-2026, as illustrated in Table I.2 below. It should be reiterated that grants will increase expenditure on public investment, support for private investment and expenditure on research, innovation, digitalisation, training and education according to the ‘Missions’ identified by the NRRP for an equal amount. Loans will play the same role, but will not result in an equivalent increase in net borrowing as they can partly replace existing expenditure programmes (even current expenditure) and partly be offset by deficit-reducing measures. The share of loans that translates into higher deficit is determined for each year according to the net borrowing objectives shown below.

The budgetary policy scenario for 2021-2023 foresees, on the expenditure side, the launch of a programme to review and redevelop the current general government expenditure and the revision of some environmentally harmful subsidies; on the revenue side, the most significant component is the additional revenue deriving from the higher GDP growth generated by the investment programme previously described. This second-round fiscal effect, however, has been prudently included in the estimates only from 2022 onwards, also in order to take into account the time lags with which revenues respond to increases in economic activity.

| TABLE I.2: Provisional Summary framework of RECOVERY PLAN RESOURCES utilisation (billion at 2018 values)* | |||||||||

| Recovery and Resilience Facility | ReactEU | Total RRF and ReactEU | Rural Development | Just Transition Fund | Other programmes | Total NGEU | |||

| Subsidies | Loans | Total | |||||||

| 2021 | 10.0 | 11.0 | 21.0 | 4.0 | 25.0 | .. | .. | .. | .. |

| 2022 | 16.0 | 17.5 | 33.5 | 4.0 | 37.5 | .. | .. | .. | .. |

| 2023 | 26.0 | 15.0 | 41.0 | 2.0 | 43.0 | .. | .. | .. | .. |

| 2024 | 9.5 | 29.9 | 39.4 | 0.0 | 39.4 | .. | .. | .. | .. |

| 2025 | 3.9 | 26.7 | 30.6 | 0.0 | 30.6 | .. | .. | .. | .. |

| 2026 | 0.0 | 27.5 | 27.5 | 0.0 | 27.5 | .. | .. | .. | .. |

| Total | 65.4 | 127.6 | 193.0 | 10.0 | 203.0 | 0.85 | 0.54 | 0.60 | 205.0 |

| (*) Preliminary assessment. The amounts may vary as a result of ongoing negotiations. | |||||||||

Moreover, the Government will continue to pursue policies to combat fraud and tax evasion and, in general, to improve tax compliance, which in recent years have achieved remarkable and exceeding expectations results. In a conservative view, the policy-scenario projections do not include further increases in revenue from tax evasion fight activity. On the other hand, a new fund will be set up financed with the revenue actually generated by this activity, which will be earmarked for the financing of fiscal reform measures and the reduction of public debt.

The main areas of the manoeuvre for 2021-2023 and its impacts are summarised in Table II.3 (Chapter II). The table confirms that, excluding the Recovery Plan, the fiscal impulse will be high in 2021 and will then be reduced in order to allow a gradual reduction of the deficit. On the other hand, the Recovery Plan will have a positive and increasing impact on GDP over the three-year period, because of both the increased resources deployed and composition effects

| 12 | MINISTRY OF ECONOMY AND FINANCE

|

I. overall framework and fiscal policy |

(increasing the share of public investment on the share of used resources) and time lags in the impact on GDP.

The real GDP path consistent with these estimates predicts a growth rate of 6.0 percent in 2021, 3.8 percent in 2022 and 2.5 percent in 2023. Quarterly GDP in the policy scenario recovers the level of the last pre-crisis quarter (fourth in 2019) in the third quarter of 2022.

| TABLE I.3: MACROECONOMIC Framework based on the policy scenario (1) (percentage changes unless otherwise indicated) | |||||

| 2019 | 2020 | 2021 | 2022 | 2023 | |

| GDP | 0.3 | -9.0 | 6.0 | 3.8 | 2.5 |

| GDP deflator | 0.7 | 1.1 | 0.8 | 1.3 | 1.2 |

| Consumption deflator | 0.5 | 0.0 | 0.7 | 1.2 | 1.2 |

| Nominal GDP | 1.1 | -8.0 | 6.8 | 5.1 | 3.7 |

| FTE employment (2) | 0.2 | -9.5 | 5.4 | 3.4 | 2.2 |

| LF Employment (3) | 0.6 | -1.9 | 0.3 | 1.7 | 1.5 |

| Unemployment rate | 10.0 | 9.5 | 10.3 | 9.5 | 8.7 |

| Current account balance (% of GDP) | 3.0 | 2.4 | 2.5 | 2.3 | 2.2 |

| (1) Any inaccuracies result from rounding. | |||||

| (2) Employment expressed in terms of full time equivalent units (FTE). | |||||

| (3) Number of persons employed based on the Continuing Labour Forces Survey (LFS). | |||||

The highest growth compared to the unchanged legislation scenario is mainly driven by gross fixed capital formation. The latter, in turn, have a multiplier effect on production and increase the households’ disposable income, resulting in higher private sector investment and household consumption expenditure. Exports are slightly affected by the impact of domestic growth on costs and prices, but over time, they benefit from the enhanced competitiveness of the economy achieved through higher investment.

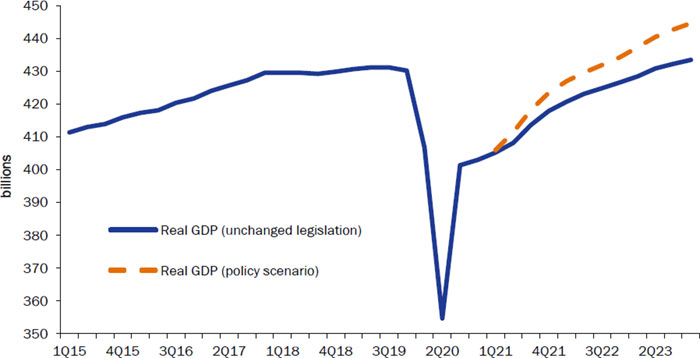

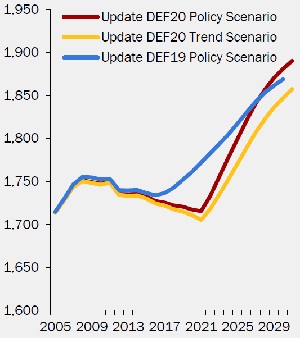

| Figure I.4: REAL gdp forecast under unchanged legislation and under policy scenario (billion, chain linked values) |

|

| Source: Istat and MEF computations. |

MINISTRY OF ECONOMY AND FINANCE

| 13 |

UPDATE OF THE Economic and Financial Document 2020 |

In view of these forecasts, it should be reiterated that, in the first part of the three-year period, the growth differential compared to the unchanged legislation scenario is ensured by the more expansive approach of fiscal policy, also motivated by the need to support incomes and employment at a time when the covid-19 epidemic will still adversely affect economic activity. In the second part of the period, however, the most significant boost to growth will come from the NRRP and in particular the grants component. Therefore, the forecasts are based to a significant extent on the success of the NRRP itself. Less growth fueled by the NRRP would also affect the performance of the public finance, even without jeopardising its sustainability.

On the other hand, the policy scenario forecast was set on the basis of conservative impact estimates. Furthermore, the forecast does not take into account neither the favourable impact on growth of the broad reforms programme, which will be an integral part of the NRRP, nor the favourable impact of the Recovery Plan on the average debt financing cost10. Overall, therefore, the forecast appears balanced although the level of economic uncertainty remains very high and there is a risk of implementation in relation to the NRRP (also considering that the relevant regulations still have to be approved).

In the light of the macroeconomic policy framework, although the trend of potential GDP is more favourable, the output gap closes more rapidly over the three-year forecast. Nevertheless, the structural balance significantly improves in each year. In particular, also thanks to the lower nominal deficit, the improvement in the structural balance is more marked in 2023 compared to the unchanged legislation scenario.

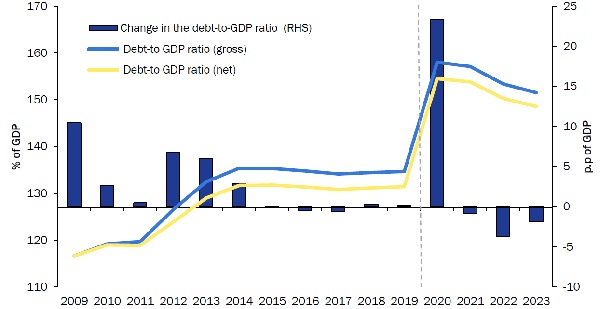

| FIGURE I.5: deficit and public debt As ratio to GDP – policy scenario 2020-2023 (%) |

|

| Source: Istat and MEF computations. |

10 The decrease in the public debt financing cost would result both from the lower yield paid on loans under the RRF compared to government bonds, and from the reduction in the spread on government bonds induced by the success of the programme in terms of increasing potential growth and improving debt sustainability.

| 14 | MINISTRY OF ECONOMY AND FINANCE

|

I. overall framework and fiscal policy |

As regards the development of the general government debt-to-GDP ratio, the policy scenario foresees a significant decline. From 158.0 percent estimated for this year, in fact, it would fall to 151.5 percent in 2023, a reduction that is 2.6 percentage points higher than in the unchanged legislation scenario.

| table i.4: public finance Indicators (% of GDP) (1) | ||||||

| 2018 | 2019 | 2020 | 2021 | 2022 | 2023 | |

| POLICY SCENARIO | ||||||

| Net borrowing | -2.2 | -1.6 | -10.8 | -7.0 | -4.7 | -3.0 |

| Primary balance | 1.5 | 1.8 | -7.3 | -3.7 | -1.6 | 0.1 |

| Interest expenditure | 3.6 | 3.4 | 3.5 | 3.3 | 3.1 | 3.1 |

| Structural net borrowing (2) | -2.3 | -1.9 | -6.4 | -5.7 | -4.7 | -3.5 |

| Structural change | -0.5 | 0.4 | -4.5 | 0.7 | 0.9 | 1.2 |

| Public debt (gross of support) (3) | 134.4 | 134.6 | 158.0 | 155.6 | 153.4 | 151.5 |

| Public debt (net of support) (3) | 131.1 | 131.4 | 154.5 | 152.3 | 150.3 | 148.6 |

| TREND SCENARIO AT UNCHANGED LEGISLATION | ||||||

| Net borrowing | -2.2 | -1.6 | -10.8 | -5.7 | -4.1 | -3.3 |

| Primary balance | 1.5 | 1.8 | -7.3 | -2.4 | -0.9 | -0.1 |

| Interest expenditure | 3.6 | 3.4 | 3.5 | 3.3 | 3.2 | 3.2 |

| Structural net borrowing (2) | -2.4 | -2.0 | -6.6 | -4.2 | -3.8 | -3.2 |

| Structural change | -0.5 | 0.4 | -4.5 | 2.4 | 0.4 | 0.5 |

| Public debt (gross of support) (3) | 134.4 | 134.6 | 158.0 | 155.8 | 154.3 | 154.1 |

| Public debt (net of support) (3) | 131.1 | 131.4 | 154.5 | 152.5 | 151.2 | 151.1 |

| MEMO: DEF 2020, NEW POLICIES SCENARIO | ||||||

| Net borrowing | -2.2 | -1.6 | -10.4 | -5.7 | ||

| Primary balance | 1.5 | 1.7 | -6.8 | -2.0 | ||

| Interest expenditure | 3.7 | 3.4 | 3.7 | 3.7 | ||

| Public debt (gross of support) (4) | 134.8 | 134.8 | 155.7 | 152.7 | ||

| Public debt (net of support) (4) | 131.5 | 131.6 | 152.3 | 149.4 | ||

| Nominal GDP at unchanged legislation (absolute values x 1,000) | 1771,1 | 1789,7 | 1647,2 | 1742,0 | 1814,8 | 1865,2 |

| Nominal GDP under policy scenario (absolute values x 1,000) | 1771,1 | 1789,7 | 1647,2 | 1759,2 | 1848,9 | 1916,6 |

(1) Any inaccuracies result from rounding. (2) Net of one-off and cyclical component. (3) Gross or net of Italy’s shares of loans to EMU Member States, bilateral or through the EFSF, and the contribution to the capital of the ESM. At the end of 2019, the amount of these shares amounted to approximately 57.8 billion, of which 43.5 billion for bilateral loans and through the EFSF and 14.3 billion for the ESM programme (see Bank of Italy, ’Statistical Bulletin of Public Finance, Needs and Debt’ of 15 September 2020). The MEF’s liquidity stocks are expected to be reduced by 0.2 percent of GDP in 2020 and 0.1 percent of GDP in 2021; in addition, estimates take into account the repurchase of SACE, the uses of the assets allocated and the EIB and SURE guarantees. The scenario of the interest rates used for the estimates is based on the implicit forecasts arising from the forward rates on Italian government bonds during the period of compilation of this document. (4) Gross or net of Italy’s shares of loans to EMU Member States, bilateral or through the EFSF, and the contribution to ESM capital. Estimates consider a reduction in MEF’s liquidity stocks of 0.8 percent of GDP in 2020 and an increase of 0.4 percent of GDP in 2021. | ||||||

MINISTRY OF ECONOMY AND FINANCE

| 15 |

UPDATE OF THE Economic and Financial Document 2020 |

Objectives for 2024-2026 and debt sustainability

The longer-term objective is to bring again the general government debt below the pre-covid-19 level by the end of the decade through a further improvement in the primary balance and the maintenance of an economic growth trend significantly higher than that of the past decade. As already mentioned, although the forecast horizon of the Update of the Stability Programme is three years, in light of the fact that the NRRP and the resources made available by the European Recovery Plan cover the period 2021-2026, the Government has also drawn up a preliminary scenario for the period 2024-2026. This ensures consistency between the assumptions made by the NRRP, the 2021-2023 budget and the public debt-to-GDP reduction strategy.

The starting point for the construction of the 2020-2026 policy scenario was to extend the unchanged legislation macroeconomic framework and the related public finance projections to 2024-2026. It has been postulated that GDP growth converges towards the estimated potential growth rate with the “T+10” methodology traditionally adopted by the European Commission11. With this growth rate of 1.1 percent, the effective growth rate is set equal to 1.5 percent in 2024 (decreasing from 1.8 percent in 2023) and then 1.1 percent in 2025 and 2026.

In the light of the public finance estimates based on unchanged legislation, the so-called unchanged policies have been projected to reach balances under the no-policy change assumption. On this baseline, the assumptions for the NRRP have been included and its net impact on GDP is estimated. This impact is positive throughout the period, but slightly decreasing, as the differential of increased expenditure for public investment and other policies financed by the RRF peaks between 2023 and 2024 and therefore its marginal impact on GDP is reduced in the final two years of the forecast scenario (although distributed lags of impacts soften this effect).

In view of these results, the general government primary balance objectives have been set. The policy scenario primary surplus rose from 0.1 percent of GDP in 2023 to 0.6 percent in 2024, 1.7 percent in 2025 and 2.5 percent in 2026. These objectives make emerge the scale of the manoeuvre required to achieve them; the manoeuvre second-round effect on the budget are calculated too. Real GDP growth in the 2024-2026 policy scenario is equal to 1.8 percent in 2024, 1.5 percent in 2025 and 1.4 percent in 2026.

The primary surplus for the final year of the projection, given the estimated interest expenditure, corresponds to a general government net borrowing (deficit) of 0.5 percent of GDP. The scale of the manoeuvre required is just over 0.4 percent of GDP in 2024 and a further tenth of a percentage point of GDP in 2025. The fiscal tightening required to achieve the net borrowing objective of 0.5 percent of GDP in 2026 is therefore relatively low, confirming that the

11The estimate mentioned in the text starts from the macroeconomic framework under unchanged legislation for 2021-2023 of this Update; it extrapolates potential growth until 2031 and results in real growth in line with the mechanical closure of the output gap. For the years 2024-2026, the estimated growth is about 1.1 percent per year and in subsequent years, it decreases to 0.6 percent in 2030-2031.

| 16 | MINISTRY OF ECONOMY AND FINANCE

|

I. overall framework and fiscal policy |

proposed scenario is reliable, as it does not require a markedly restrictive fiscal policy, which in the past has proved either unsustainable or counterproductive for the country’s economic and social stability. It should also be noted that if some of the new policies were not to be introduced, the proposed manoeuvre for 2024-2025 would not be necessary.

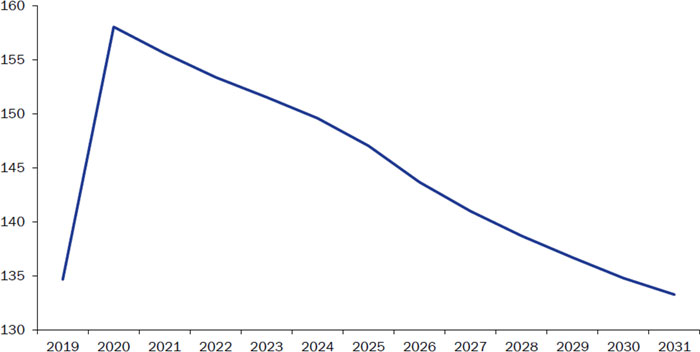

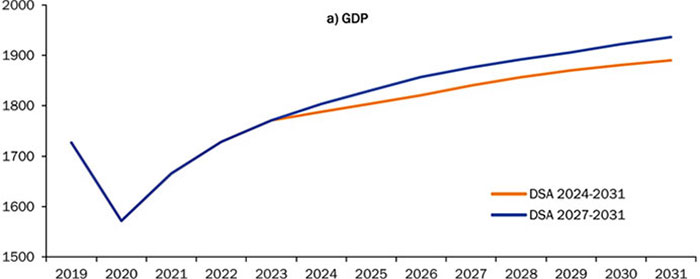

A Debt Sustainability Analysis (DSA) extended until 2031 was also carried out in light of the 2021-2026 policy scenario. This analysis is normally conducted starting from the primary balance of the final three-year forecast year (in this case 2023). Starting from this balance, the structural primary balance (i.e. net of temporary measures and cyclical component) is calculated and projected over a ten-year horizon, by assuming that: i) the economy follows the path of potential growth; ii) the deflator converges towards the ECB’s target inflation rate; iii) and that the debt financing cost follows an evolution consistent with the forward yields calculated by recent market levels. These extrapolations are discussed in detail in Section III.5 of this Update.

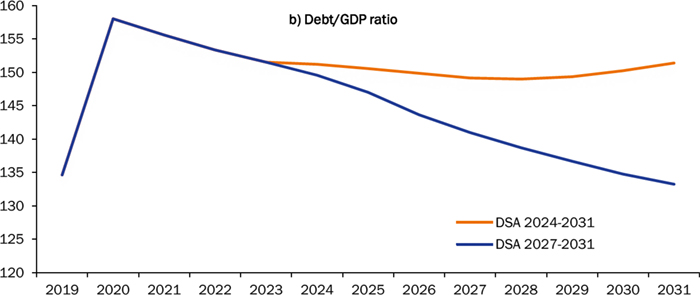

In the modified DSA variant summarised here, it is assumed, instead, that the primary balance follows the policy-scenario path until 2026 and then remains at this level in structural terms in the following five years. Based on this assumption, by applying the rest of the DSA methodology, it is obtained the path of the debt-to-GDP ratio represented in Figure I.6. The debt ratio steadily declines and falls below the level recorded last year by 2031.

| FIGURE I.6: debt-to-GDP ratio path under policy scenario to 2026 and extrapolation to 2031, maintaining the 2026 structural primary balance unchanged |

Source: MEF computations. |

Reabsorbing an increase in the debt-to-GDP ratio such as that expected for this year (over 23 percentage points) over a decade would be a great result. However, it could be argued that in order to protect public finance from other risks that could emerge in the coming years, it would be appropriate to plan a quicker adjustment, also in view of the fact that the debt reduction rule would not be fully met during the forecast period. Given that the European fiscal rules

MINISTRY OF ECONOMY AND FINANCE

| 17 |

UPDATE OF THE Economic and Financial Document 2020 |

will be reconsidered again once the pandemic emergency has been overcome, it is clear that if the recovery of the economy in the coming years will exceed expectations, then it would be possible to consider a path of even greater improvement in the primary balance, which would, under the same conditions, speed up the decline of public debt-to-GDP ratio.

In any case, the projection shown here confirms that an effective use of the Recovery Plan and a wise but non-restrictive management of public finance will allow to attain a high degree of debt sustainability. In the next future, the Government’s efforts will focus on the preparation of a wide-ranging and effective NRRP. On a longer-term horizon, it will be important to keep a constant focus on improving public finance, whose resilience is crucial to respond to unexpected shocks such as that caused by the current pandemic.

Net balance to be financed

In accordance with the rules of the Law on Public Accounting and Finance on the mandatory contents of the Update of the Stability Programme, the net balance to be financed of the State budget in accrual terms may increase to EUR 196 billion in 2021, 157 billion in 2022 and EUR 138.5 billion in 2023. The corresponding net balance to be financed in cash terms may increase to EUR 279 billion in 2021, 208.5 billion in 2022 and EUR 198 billion in 2023. These amounts shall include the necessary financial resources, to be allocated in anticipation, to implement the NRRP.

| 18 | MINISTRY OF ECONOMY AND FINANCE

|

I. overall framework and fiscal policy |

Draft laws related to the budget decision

To complete the 2021-2023 budgetary manoeuvre, the Government declares the following as the draft laws linked to the budgetary decision:

| • | Draft Law in the field of university qualifications (so-called Draft Law ‘qualifying degrees’); |

| • | Draft Law of reorganisation of the sector of artistic, musical and choreutical high education (so-called Draft Law ‘AFAM’); |

| • | Draft Law with provisions relating to entertainment, cultural and creative industries and tourism; |

| • | Draft Law for the reorganisation of environmental legislation, the promotion of the green economy and the circular economy (Green Generation); |

| • | Draft Law on the reform of social safety nets; |

| • | Draft Law for updating and reorganising the legislation on health and safety at workplaces; |

| • | Draft Law on minimum wages and representation of the social parties in collective bargaining; |

| • | Draft Law on tax reform; |

| • | Draft Law on tax justice reform; |

| • | Draft Law to reorganise the game sector; |

| • | Draft Law on “Reordering the rules on prevention of corruption, publicity obligations, transparency and information release by general government”; |

| • | Draft Law on “Provisions on smart working in public offices”; |

| • | Draft Law on “Simplification of administrative procedures for the containment of hydrogeological risk” |

| • | Draft Law with regard to the support and exploitation of agriculture and fisheries; |

| • | Draft Law “Provisions for the implementation of differentiated autonomy referred to in Article 116, 3 paragraph, Cost.”; |

| • | Draft Law “Implementation of the forms of coordination between central and regional governments, including the end of the reduction of constitutional litigation”; |

| • | Draft Law on simplification and reorganisation in the fields of start-ups and innovative SMEs; |

| • | Draft Law on the companies’ statute; |

| • | Draft Law on comprehensive review of incentives in favour of firms; |

| • | Draft Law on provisions for the development of the supply chains and to encourage the aggregation between firms; |

| • | Draft Law on the reform of the framework law for craftsmanship; |

| • | Draft Law on the revision of the Consolidated Text of Law on Local Authorities. |

MINISTRY OF ECONOMY AND FINANCE

| 19 |

UPDATE OF THE Economic and Financial Document 2020 |

| 20 | MINISTRY OF ECONOMY AND FINANCE

|

II.1 The International Economy

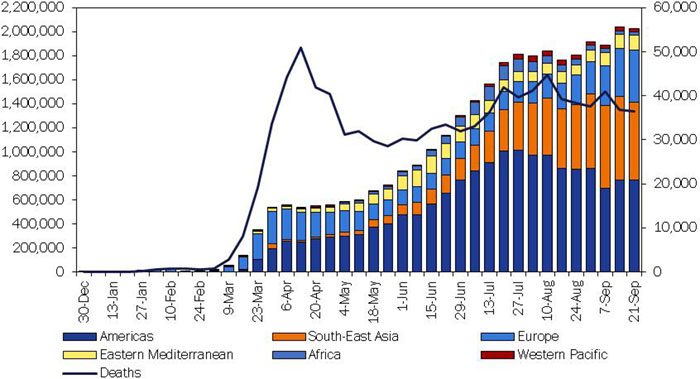

In the first half of 2020, the world economy faced the deepest setback since World War II, due to the spread of the covid-19 pandemic. Although with different durations, starting from March, the halt of non-essential activities and social distancing to contain the health emergency have been adopted in the various geo-economic areas.1 The economic activity of the major countries was gradually restarted in May thanks to the decline of the infection.

| Figure II.1: Number of covid-19 recorded cases by REGION AND world deaths (weekly data, updated at 21 September) |

|

| Source: World Health Organisation (WHO). |

1 As it was the first country where the epidemic occurred, the lockdown in China began on 23 January, ending on April 8. Remaining in the Asian area, the Japanese government adopted lockdown on April 16 throughout the country, while in India it was introduced on 25 March. In Europe, Italy started lockdown on 9 March, followed by Spain and France a few days later (14 and 17 March respectively); on 23 March the lockdown was declared by Germany and the United Kingdom. In the Americas, the United States introduced lockdown measure between 19 and 24 March, with different timing and intensity between the various States. Among the largest countries in Latin America, the lockdown began in the second half of March in Argentina, while Brazil did not introduce it at national level. (Source: For advanced countries, CER, Report n.1/2020, August 2020; for other countries, https://www.thinkglobalhealth.org/article/updated-timeline-coronavirus).

MINISTRY OF ECONOMY AND FINANCE

| 21 |

UPDATE OF THE Economic and Financial Document 2020

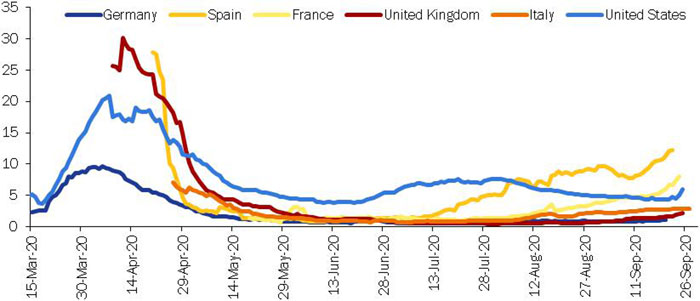

| Figure II.2: Positivity rate at covid-19 (%, share of positive tests on the number of performed tests, rolling 7 days average, data updated at 29 September) |

|

| Source: Our World in Data (OWD). |

Governments and central banks have introduced extraordinary fiscal and monetary policy measures to support workers’ incomes and the productive system, providing support on a much larger scale, and more quickly, than in the 2008 crisis. Despite these interventions, the lockdown led to a contraction of GDP and world trade by 3.5 percent and 2.7 percent q/q in the first quarter of the year, and an even sharper decline in the following quarter (by more than 5 percent and 12.5 percent respectively).

| Figure II.3: Trend OF THE WORLD trade (volume data, index, 2010=100) |

|

| Source: CPB. |

In the main advanced economies, the largest contraction in GDP occurred during the second quarter. In the United States and in Japan, the output decreased by about 8 percent q/q, while in the Eurozone there was a deeper drop (-11.8 percent q/q); the reduction in the United Kingdom was even more marked

| 22 | MINISTRY OF ECONOMY AND FINANCE

|

II. MACROECONOMIC FRAMEWORK

(-19.8 percent q/q). In contrast, China – having been the first country to be hit by covid-19 – reactivated the economy at the beginning of April, recording a y-o-y growth of 3.2 percent in the second quarter.

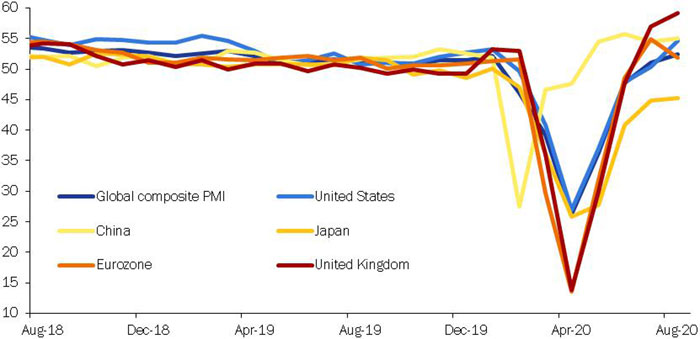

Following the restart of production, in May and June the recovery was more sustained than expected, although with a lower intensity and uneven trend in the various countries. The most recent business surveys show that the Global Composite Purchasing Managers’ Index (PMI),2 having reached its lowest level ever for the last ten years in April (equal to 26.2 points) has returned above the expansion threshold in August, reaching 52.4 points, the highest level since March 2019.

| Figure II.4: global COMPOSITE pmi and BY COUNTRY |

|

| Source: Markit, Refinitiv. |

As a result of social distancing measures, in the second quarter of the year the US economy contracted due to the sharp reduction in households consumption and investment, delayed by firms owing to uncertainty and weak demand. Industrial production reached its lowest level since the beginning of the year in April (-12.9 percent over the previous month), gradually recovering in the following months (+4.8 percent on average in June and July), but slowing down in August (+0.4 percent). The effects on the labour market have been significant, with the unemployment rate reaching the historic peak of the last fifty years (at 14.7 percent in April, from 4.4 percent in March) and then falling to 8.4 percent in August.

To contain the impact of the pandemic, federal spending has been expanded to finance programmes to support families, businesses, central and local levels of government. According to estimates provided by the Congressional Budget Office (CBO), such policies would result in additional expenditure and missed revenues for the 2020 federal budget of more than 2 trillion dollars (approximately 10

2 The purchasing managers index (PMI) is a spread index constructed in such a way that a value greater than 50.0 is consistent with an expansion of economic activity, in this case global.

MINISTRY OF ECONOMY AND FINANCE

| 23 |

UPDATE OF THE Economic and Financial Document 2020

percent of nominal GDP).3 These instruments have been accompanied by the FED’s financing programmes to assure lending to the economy and financial stability4. On the price side, core consumer inflation (excluding energy and food) gradually increased (to 1.7 percent in August from a minimum of 1.2 percent in May and June), remaining below the FED target. In this regard, the US Central Bank confirmed the new monetary policy strategy during its September meeting, announced at the end of August by Chair Jerome Powell, which foresees5 low policy rates (currently between 0.0 and 0.25 percent) until the economy returns to full employment and the inflation rate reaches at least 2 percent, being ready to tolerate moderately higher inflation for a reasonable period of time.

On the Asian continent, according to the International Monetary Fund, GDP6 is expected to contract by 1.6 percent, involving most countries, in relation to the need to contain infections, to dependence on global value chains, on the tourism sector and on foreign remittances.