EXHIBIT D

Government of Jamaica

This description of the Government of Jamaica is dated as of June 2, 2017 and appears as Exhibit (D) to the Government of Jamaica’s Annual Report on Form 18-K to the US Securities and Exchange Commission for the fiscal year ended March 31, 2017.

D-1

EXCHANGE RATES

The following table shows exchange rate information for the selling of US dollars for the periods indicated. The Federal Reserve Bank of New York does not report a noon buying rate for the JA dollar. The official exchange rate published by the Bank of Jamaica for US dollars on April 12, 2017 was J$128.75 per US$1.00.

Foreign Exchange Rates(1)

| | | | | | | | | | | | |

Foreign Exchange Rates(1) Year | | Average for

Period(1) | | | End of Period | | | Percentage

Change(2)

(End of Period) | |

| | | (spot weighted average ask in J$ for US$) | |

2007 | | | 69.17 | | | | 70.62 | | | | 5.17 | |

2008 | | | 73.36 | | | | 80.47 | | | | 13.95 | |

2009 | | | 88.82 | | | | 89.60 | | | | 11.35 | |

2010 | | | 87.34 | | | | 85.86 | | | | (4.17 | ) |

2011 | | | 86.09 | | | | 86.60 | | | | 0.86 | |

2012 | | | 88.23 | | | | 92.98 | | | | 7.37 | |

2013 | | | 101.26 | | | | 106.38 | | | | 14.41 | |

2014 | | | 111.54 | | | | 114.66 | | | | 7.78 | |

2015 | | | 117.48 | | | | 120.42 | | | | 5.01 | |

2016 | | | 125.77 | | | | 128.44 | | | | 6.66 | |

| | | | | | | | | | | | |

Foreign Exchange Rates(1) Month/

Year | | Average for

Period(1) | | | End of Period | | | Percentage

Change

(End of Period)(3) | |

| | | (spot weighted average ask in J$ for US$) | |

January 2017 | | | 128.55 | | | | 128.35 | | | | (0.07 | ) |

February 2017 | | | 128.07 | | | | 128.11 | | | | (0.19 | ) |

March 2017 | | | 128.41 | | | | 128.67 | | | | 0.44 | |

April 2017 | | | 128.74 | | | | 128.75 | | | | 0.06 | |

| (1) | The weighted average of the exchange rates for annual periods is calculated as the simple average of end of month rates. |

| (2) | As compared to the prior year. |

| (3) | As compared to the prior month. |

Source: Bank of Jamaica

PRESENTATION OF CERTAIN INFORMATION

All references in the annual report on Form 18-K to “Jamaica” and the “Government” are to the Government of Jamaica, unless otherwise indicated. All references to “JA dollars” and “J$” are to Jamaica dollars, all references to “US dollars” and “US$” are to the lawful currency of the United States of America, or US, all references to “€” are to Euro all references to £ are to Great Britain Pounds. Historical amounts translated into JA dollars or US dollars have been converted at historical rates of exchange. References to annual periods (e.g., “2016”) refer to the calendar year ended December 31, and references to fiscal year or FY (e.g., “FY 2015/16” or “FY 2016/17”) refer to Jamaica’s fiscal year ended March 31. All references to “tonnes” are to metric tonnes. Jamaica publishes external economy information, such as external debt and goods and services exported, in US dollars. All international currencies, such as external debt denominated in Euro, are translated into US dollars. Domestic economy information is published by Jamaica in JA dollars. Components contained in tabular information in this annual report on Form 18-K may not add to totals due to rounding. The term “N/A” is used to identify economic or financial data that is not presented for a particular period because it is not applicable to such period and “n.a.” for economic or financial data that is not available.

Statistical information included in this report is the latest official data publicly available. Financial data provided may be subsequently revised in accordance with Jamaica’s ongoing maintenance of its economic data.

D-2

D-3

SUMMARY

The following is a summary of Jamaica’s economic information for the five years ended and as at December 31, 2016. This summary does not purport to be complete and is qualified by the more detailed information appearing elsewhere in this document.

Summary of Economic Information

| | | | | | | | | | | | | | | | | | | | |

| | | 2012 | | | 2013 | | | 2014 | | | 2015 | | | 2016 | |

DOMESTIC SECTOR(1) | | | | | | | | | | | | | | | | | | | | |

Nominal GDP (J$ millions) | | | 1,313,792.2 | | | | 1,431,097.7 | | | | 1,541,718.8 | | | | 1,667,193.4 | | | | 1,754,727.3 | |

Nominal GDP (US$ millions)(2) | | | 14,805.5 | | | | 14,268.7 | | | | 13,851.9 | | | | 14,211.9 | | | | 14,022.1 | |

Total Value Added (J$ millions) at basic price(1)(2) | | | 1,124,004.7 | | | | 1,213,715.5 | | | | 1,305,562.6 | | | | 1,401,692.9 | | | | 1,458,851.5 | |

Real GDP(J$ millions) at basic price(3) | | | 731,038.3 | | | | 732,543.7 | | | | 736,405.3 | | | | 743,289.2 | | | | 753,345.6 | |

Real GDP at basic price (US$ millions)(2)(3) | | | 10,631.5 | | | | 10,653.4 | | | | 10,709.6 | | | | 10,809.7 | | | | 10,956.0 | |

Percent Change in Real GDP(3) | | | (0.5 | ) | | | 0.2 | | | | 0.5 | | | | 0.9 | | | | 1.4 | |

Real GDP at basic price per capita (J$/person)(3) | | | 269,974.5 | | | | 269,846.4 | | | | 270,682.1 | | | | 272,737.8 | | | | 276,040.6 | |

Real GDP (J$ millions) at market price | | | 837,105.9 | | | | 841,322.3 | | | | 847,166.2 | | | | 855,607.7 | | | | 878,449.2 | |

Real GDP at market price (US$ millions)(2) | | | 12,174.1 | | | | 12,235.3 | | | | 12,320.4 | | | | 12,443.2 | | | | 6,984.6 | |

Percent change in Real GDP at market price | | | (0.6 | ) | | | 0.5 | | | | 0.7 | | | | 1.0 | | | | 2.7 | |

Real GDP at market price per capita (J$/person) | | | 309,145.6 | | | | 309,917.1 | | | | 311,394.7 | | | | 313,951.3 | | | | 321,411.3 | |

Inflation Consumer Price Index (Percent Change) | | | 8.0 | | | | 9.5 | | | | 6.4 | | | | 3.7 | | | | 1.7 | |

Interest Rates (%)(4) Weighted Average Loan Rate | | | 18.4 | | | | 17.5 | | | | 17.2 | | | | 17.1 | | | | 16.2 | |

Weighted Average Deposit Rate | | | 2.1 | | | | 2 | | | | 2 | | | | 1.5 | | | | 1.4 | |

Treasury Bill Yield(5) | | | 7.2 | | | | 8.3 | | | | 7.1 | | | | 7.0 | | | | 6.6 | |

Unemployment Rate (%)(6) | | | 13.9 | | | | 15.2 | | | | 13.7 | | | | 13.5 | | | | 13.2 | |

EXTERNAL SECTOR (US$ millions) | | | | | | | | | | | | | | | | | | | | |

Average Annual Nominal Exchange Rate (J$/US$) | | | 88.2 | | | | 101.2 | | | | 111.5 | | | | 117.5 | | | | 125.8 | |

Export of Goods (f.o.b) | | | 1,728.5 | | | | 1,580.5 | | | | 1,448.6 | | | | 1,254.9 | | | | 1,194.9 | |

Alumina | | | 508.3 | | | | 523.7 | | | | 529.4 | | | | 518.6 | | | | 444.0 | |

Sugar | | | 94.1 | | | | 53.2 | | | | 55.8 | | | | 53.9 | | | | 14.8 | |

Imports of Goods (c.i.f) | | | 6,298.3 | | | | 6,129.9 | | | | 5,847.3 | | | | 5,033.5 | | | | 4,751.3 | |

Goods Balance | | | (3,905.7 | ) | | | (3,877.7 | ) | | | (3,759.0 | ) | | | (3,194.5 | ) | | | (2,973.7 | ) |

Current Account Balance | | | (1,440.2 | ) | | | (1,356.8 | ) | | | (1,114.4 | ) | | | (430.1 | ) | | | (103.0 | ) |

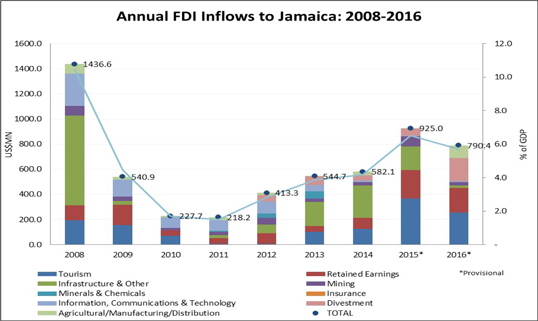

Gross Foreign Direct Investments | | | 413.3 | | | | 544.7 | | | | 582.1 | | | | 925.0 | | | | 790.4 | |

Net Foreign Direct Investments | | | 389.2 | | | | 471.9 | | | | 502.4 | | | | 920.7 | | | | 564.1 | |

Increase/(Decrease) in Reserves | | | (840.5 | ) | | | (77.8 | ) | | | 953.3 | | | | 435.9 | | | | 282.4 | |

Net International Reserves of the Bank of Jamaica | | | 1,125.6 | | | | 1,047.8 | | | | 2,001.1 | | | | 2,437.0 | | | | 2,719.4 | |

Weeks of Coverage of Goods Imports(7) | | | 18.1 | | | | 17.9 | | | | 25.5 | | | | 35.5 | | | | 40.1 | |

PUBLIC FINANCE (J$ millions)(8) | | | 344,677.7 | | | | 396,979.4 | | | | 411,715.9 | | | | 455,835.8 | | | | 499,879.9 | |

Revenue and Grants | | | | | | | | | | | | | | | | | | | | |

Expenditure | | | 399,278.9 | | | | 395,241.8 | | | | 418,986.8 | | | | 460,719.4 | | | | 503,356.0 | |

Fiscal Surplus (Deficit) | | | (54,601.1 | ) | | | 1,737.6 | | | | (7,270.9 | ) | | | (4,883.7 | ) | | | (3,476.1 | ) |

Fiscal Surplus (Deficit) as a % of Nominal GDP | | | (4.1 | ) | | | 0.1 | | | | (0.5 | ) | | | (0.4 | ) | | | (0.2 | ) |

Primary Surplus | | | 72,336.5 | | | | 111,657.1 | | | | 117,241.8 | | | | 120,795.9 | | | | 135,880.1 | |

Primary Surplus as a % of Nominal GDP | | | 5.4 | | | | 7.6 | | | | 7.5 | | | | 7.1 | | | | 7.7 | (13) |

Loan Receipts | | | 144,347.1 | | | | 93,527.5 | | | | 168,705.9 | | | | 298,600.5 | | | | 89,826.8 | |

D-4

| | | | | | | | | | | | | | | | | | | | |

| | | 2012 | | | 2013 | | | 2014 | | | 2015 | | | 2016 | |

Amortization | | | 88,329.8 | | | | 106,640.2 | | | | 87,794.4 | | | | 342,725.9 | | | | 75,389.7 | |

Overall Surplus (Deficit) | | | 1,161.2 | | | | (11,375.0 | ) | | | 73,640.6 | | | | (42,937.9 | ) | | | 25,565.7 | |

Overall Public Sector Surplus (Deficit)(9) | | | (62,142.7 | ) | | | (1,888.7 | ) | | | 7,374.1 | | | | 28,695.1 | | | | 13,515.1 | |

Overall Public Sector Surplus (Deficit) as a % of Nominal GDP | | | (4.6 | ) | | | (0.1 | ) | | | 0.5 | | | | 1.7 | | | | 0.8 | |

PUBLIC DEBT | | | 995,230.9 | | | | 1,054,174.0 | | | | 1,046,850.3 | | | | 860,262.6 | | | | 834,319.9 | |

Domestic Debt (J$ millions)(10) | | | | | | | | | | | | | | | | | | | | |

Percent of Nominal GDP | | | 75.8 | | | | 74.2 | | | | 68.5 | | | | 52.4 | | | | 48.3 | |

Public Sector External Debt (US$ millions) | | | 8,255.5 | | | | 8,310.0 | | | | 8,658.6 | | | | 10,314.0 | | | | 10,244.2 | |

Percent of Nominal GDP | | | 56.0 | | | | 59.0 | | | | 64.9 | | | | 75.6 | | | | 74.5 | |

Total Public Sector Debt (J$ millions) | | | 1,762,811.2 | | | | 1,938,176.2 | | | | 2,039,650.3 | | | | 2,102,220.0 | | | | 2,150,062.67 | |

Percent of Nominal GDP | | | 134.3 | | | | 136.4 | | | | 133.4 | | | | 128.0 | | | | 122.8 | |

External Debt Service Ratio | | | 15.6 | | | | 15.1 | | | | 19.4 | | | | 18.4 | | | | 14.1 | |

TOURISM | | | | | | | | | | | | | | | | | | | | |

Total Visitor Arrivals | | | 3,306,168 | | | | 3,273,677 | | | | 3,503,978 | | | | 3,691,744 | | | | 3,837,243 | |

Occupancy Rate (% Hotel Rooms) | | | 60.5 | | | | 62.3 | | | | 67.9 | | | | 68.0 | | | | 69.0 | |

Visitor Expenditures(11) (US$ millions) | | | 2,069.6 | | | | 2,112.7 | | | | 2,244.4 | | | | 2,402.3 | | | | 2,538.9 | (13) |

| (1) | The gross domestic product series has been revised. This revision was made in order to capture the changing structure of industries in the manufacturing, financial and insurance services, business services and the miscellaneous services sectors. In addition, the base year has been changed from 1996 to 2003. |

| (2) | Calculated using the average annual nominal exchange rate. |

| (3) | At constant 2007 prices. |

| (4) | Loans are in domestic currency. |

| (5) | Tenors of Treasury Bills are approximately 182 days. |

| (6) | Includes all persons without jobs, whether actively seeking employment or not. |

| (7) | Calculated on the basis of gross international reserves. |

| (8) | Fiscal year data from April 1 to March 31. For example, 2016 refers to the period April 1, 2016 to March 31, 2017. |

| (9) | Overall Public Sector comprises the central government, the Bank of Jamaica, governmental statutory bodies and authorities and government-owned companies. |

| (10) | Does not include contingent liabilities in the form of guarantees of certain obligations of public entities. |

| (11) | Estimate. 2015 Revised. Updated data is as at March 2016. |

| (13) | Provisional estimate. |

Source: Bank of Jamaica, Statistical Institute of Jamaica, Ministry of Finance and the Public Service and Jamaica Tourist Board

D-5

JAMAICA

History

Originally settled by the Arawak Indians, Jamaica was first visited by Christopher Columbus in 1494 on his second voyage to the New World. Jamaica’s name derives from the Arawak word “Xaymaca,” which means “Land of Wood and Water.” In 1655 Admiral William Penn and General Robert Venables led a British force that conquered the island, ousting the Spaniards. Over the next 40 years, Jamaica became the stronghold of the Caribbean buccaneers who transformed Port Royal, then the island’s commercial center, into the richest city in the New World. The sugar industry, supported to a great extent by slaves transported from Africa until the abolition of slavery in 1834, formed the basis of the island’s economy. During its three centuries as a British colony, Jamaica was variously administered by a governor and a planter-controlled legislature, by British Crown Colony rule from London, England, and by limited representative government in the late 19th and early 20th centuries. The Government granted universal adult suffrage in 1944. From 1958 to 1961, Jamaica was a member of the now-defunct West Indies Federation, which encompassed all of Britain’s Caribbean colonies. Although plans for independence first appeared in the 1940s, internal self-government did not begin until 1959. On August 6, 1962, Jamaica became an independent country within the British Commonwealth.

The historical development of the island has influenced Jamaican national symbols. Jamaica’s flag, a diagonal cross of gold on a green and black background, represents the statement, “The sun shineth, the land is green and the people are strong and creative.” The national crest incorporates the original Arawak inhabitants with the legend “Out of Many, One People,” which reflects the country’s multiracial heritage. Jamaica’s reggae music enjoys international renown.

Territory and Population

Jamaica, the third largest island in the Caribbean Sea, is located 558 miles (898 kilometers) southeast of Miami, Florida, 90 miles (144.8 kilometers) south of Cuba and 100 miles (160.9 kilometers) southwest of Haiti. The island has an area of 4,411 square miles (11,420 square kilometers), and its highest point is the Blue Mountain Peak, which rises 7,402 feet (2,256 meters) above sea level. The capital city, Kingston, located on the island’s southeast coast, also serves as Jamaica’s major commercial center. The natural harbor in Kingston is the seventh largest in the world. The country’s second-largest city, Montego Bay, located on the island’s northwest coast, is Jamaica’s main center for tourism. See “The Jamaican Economy—Principal Sectors of the Economy—Tourism.”

From 2010 to 2016, Jamaica’s population grew at an annual growth rate of approximately 0.22% per year. At December 31, 2016, Jamaica’s population was estimated at 2,730,894, a 0.20% increase over the December 31, 2015 population of 2,727,328. This low rate of population growth is primarily due to declining birth rates, a trend which the Government believes will continue. The most recent 2011 population and housing census reported that 46% of Jamaica’s population lives in rural areas while 54% lives in urban areas. Jamaica’s official language is English, and the majority of the population speaks a dialect.

Society

Jamaica’s educational system is based on the British system. The school system consists of a pre-primary cycle of two years, followed by a primary cycle of six years, a secondary cycle of seven years, post-secondary and tertiary education. The education and training sector focuses on the development of the population, from early childhood through to the tertiary level and beyond. One focus is being placed on increasing the Government’s involvement at the early childhood education level for an increased access to better quality education.

The Government has embarked on a new learner-center curriculum (National Standards Curriculum) geared at fostering the development of critical thinking and higher order skills at the primary level. Students will access their secondary education based on their aptitude, interests and ability.

The HEART Trust/NTA is the facilitating and coordinating body for technical and vocational workforce development in Jamaica. The HEART Trust/NTA provides access to training, development of competence,

D-6

assessment and certification to working age Jamaicans. It also facilitates career development and employment services island-wide. Training is provided both in the workplace (enterprise-based), as well as through formal Technical, Vocational and Educational Training (“TVET”) institutions and TVET special programs. Programs have also been implemented to increase access to all, especially unattached youths. As at March 2016, the HEART Trust/NTA directly administered training in over 29 institutions island-wide and over 356 secondary schools and special church-based and community-based training institutions.

The educational system accommodates a variety of public and private schools. Post-secondary education is available to qualified candidates at community colleges, the University of Technology, University of the Commonwealth Caribbean, Northern Caribbean University, International University of the Caribbean, the Jamaica campus of the University of the West Indies and several private off shore universities.

In addition to the formal school system, Jamaica has an adult literacy program – the Jamaican Foundation of Lifelong Learning. According to the 2008 Jamaica Survey of Living Condition Survey Literacy Module 91.7% of the population was “Literate,” with 78.3% being “Functionally Literate” and 13.4% having only “Basic Literacy,” while 8.3% were “Illiterate.” Data provided by UNESCO Institute for Statistics estimates the 2017 adult literacy rate at 90.0% (85.5% male and 94.2% female).

Recent macro- and micro-economic developments have generally caused the unemployment rate to decrease. In 2016, the average number of unemployed persons was 178,500, an increase of 0.4% from 177,900 in 2015. The average unemployment rate was 13.2% in 2016, a decrease from 13.5% in 2015. See “The Jamaican Economy—Employment and Labor.” The unemployment rate in Jamaica during the past six years has decreased from a high of 15.2% in 2013 to a low of 13.2% in 2016. Unemployment was 12.7% as at January 31, 2017, as compared to 13.3% as at January 31, 2016 and 12.9% as at March 31, 2017.

The Government remains committed to prioritizing the social protection program in an effort to minimize any potentially adverse impact on the most vulnerable within the population. To this end, the Government is providing a budgetary increase of 47% to the Programme of Advancement Through Health and Education (“PATH”) in a move to strengthen the country’s social safety net. This addition of J$3.68 billion in the FY 2017/18 budget, brings the total budget for PATH to J$11.47 billion.

The following table shows selected social indicators applicable to Jamaica for the five years ended December 31, 2016:

Social Indicators

| | | | | | | | | | | | | | | | | | | | |

| | | 2012 | | | 2013 | | | 2014 | | | 2015 | | | 2016* | |

Real GDP at market price per capita(1) | | J$ | 309,145.6 | | | J$ | 309,917.1 | | | J$ | 311,394.7 | | | J$ | 313,951.3 | | | J$ | 321,411.3 | |

Real GDP at basic price per capita | | J$ | 269,974.5 | | | J$ | 269,846.4 | | | J$ | 270,682.1 | | | J$ | 272,737.8 | | | J$ | 276,040.6 | |

Perinatal Mortality Rate (per thousand)(2) | | | 30.2 | | | | 29.2 | | | | 29.4 | | | | 30.8 | | | | 29.0 | |

| (1) | In constant 2007 prices. |

| (2) | Defined as deaths in government hospitals occurring anytime from 28 weeks of pregnancy until seven days after birth |

Please note that the statistics for Perinatal Mortality Rate are only reflective of the public secondary and tertiary health care facilities; no inference should be made of the primary health care facilities or Jamaica as a whole. Data marked by an * should be used provisionally.

Source: Statistical Institute of Jamaica, Planning Institute of Jamaica and Ministry of Health—Planning and Evaluation Branch.

Governmental Structure and Political Parties

The Jamaica Order in Council 1962 (the “Constitution”) is the supreme law of Jamaica and sets forth the basic framework and legal underpinnings for governmental activity in Jamaica. The Constitution came into effect when Jamaica became an independent country on August 6, 1962, and includes provisions that safeguard the fundamental freedoms of the individual. While a simple majority of Parliament can enact amendments to the Constitution, certain amendments require ratification by a two-thirds majority in both houses of Parliament, and amendments altering fundamental rights and freedoms require the additional approval of a national referendum.

D-7

Jamaica is a parliamentary democracy based upon the British Westminster model and is a member of the British Commonwealth. The Head of State is the British Monarch, who is represented locally by the Governor-General of Jamaica. Traditionally, the British Monarch appoints the Governor-General upon the recommendation of Jamaica’s Prime Minister. The actions of the Governor-General are, in most cases, of a purely formal and ceremonial nature. General elections are constitutionally due every five years, at which time all seats in the House of Representatives will be up for election. The Constitution permits the Prime Minister to call elections at any time within or shortly beyond the five-year period, consistent with the Westminster model.

National legislative power is vested in a bicameral Parliament composed of a House of Representatives and a Senate. The House of Representatives comprises 63 members elected by the people in the general elections. The Senate comprises 21 members appointed by the Governor-General, 13 of whom are appointed on the advice of the Prime Minister and eight of whom are appointed on the advice of the Leader of the Opposition. The President of the Senate is elected by its members. The members of the House of Representatives select their own chairman, known as the Speaker. The Prime Minister, usually the member most likely to command the support of the majority of the members of the House of Representatives, is appointed by the Governor-General.

In addition to the national governing bodies, local government is administered through 13 municipal corporations (12 parish councils and the Kingston and St Andrew Corporation) and the Municipality of Portmore. The results of the last local government election, which took place on November 28, 2016, accorded the Jamaica Labour Party (“JLP”), 8 of the 12 municipal corporations (that is including the KSAC). The People’s National Party (“PNP”) and JLP shared the St Thomas Municipal Corporation. The PNP won the Municipality of Portmore.

The principal policy-making body of the Government is the Cabinet, which is responsible for the general direction and control of Jamaica and whose members are collectively accountable to Parliament. The Cabinet consists of the Prime Minister and no fewer than 11 other members of the two Houses of Parliament. No fewer than two, and no more than four members must be selected from the Senate. The Governor-General appoints members of the Cabinet upon the recommendation of the Prime Minister.

The Jamaican judicial system is based on English common law and practice and consists of a Supreme Court, a Court of Appeal and local courts. Final appeals are made to the Judicial Committee of the Privy Council in the United Kingdom (“UK”). A number of Caribbean nations, including Jamaica, are currently discussing the establishment of a Caribbean Court of Justice to replace the Judicial Committee of the Privy Council for those nations. Jamaica has signed an agreement to establish the Caribbean Court of Justice. In April 2005, Jamaica passed the Caribbean Court of Justice (Original Jurisdiction) Act 2005. The Act provides for the implementation of the provisions of the agreement establishing the Caribbean Court of Justice in its original jurisdiction. The Caribbean Court of Justice, in its original jurisdiction, will hear and determine matters relating to the interpretation and application of the Revised Treaty of Chaguaramas (“Revised Treaty”) establishing the Caribbean Community and Common Market.

Two major political parties dominate Jamaica’s political system, the JLP and the PNP. From Jamaica’s independence on August 6, 1962, until 1972, the JLP formed the government; then the PNP assumed power in 1972. In late 1980, the JLP returned to power until February 1989, when Michael Manley led the PNP to victory and became Prime Minister. In 1992, Prime Minister Manley resigned as Prime Minister and leader of the PNP and was succeeded by Percival James (“P.J.”) Patterson. The PNP won the 1993 general election and P.J. Patterson returned as Prime Minister. In 1995, a former Chairman of the JLP formed a third political party, the National Democratic Movement. In the 1997 general election, the PNP won 51.7% of the votes cast, and P. J. Patterson returned to the office of Prime Minister. In March 2006, Prime Minister P.J. Patterson resigned as Prime Minister and leader of the PNP and was succeeded by Portia Simpson-Miller.

Jamaica held its most recent general election on February 25, 2016. As a result of that election, the JLP won 50.1% of the valid votes cast, and Andrew Holness became Prime Minister. The Constitution requires that a general election be held every five years, at which time all seats in the House of Representatives are up for election. Given that the last general election was February 25, 2016, an election is to be constitutionally held by February 2021. However, the Prime Minister, as constitutionally permitted, can decide to call an election before this date. Parliament may consider legislation to create fixed election dates and term limits for the Prime Minister.

D-8

The following table shows the parliamentary electoral results for the past six general elections:

Parliamentary Electoral Results

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | 1993 | | | 1997 | | | 2002 | | | 2007 | | | 2011(1) | | | 2016 | |

People’s National Party | | | 52 | | | | 51 | | | | 34 | | | | 28 | | | | 42 | | | | 31 | |

Jamaica Labour Party | | | 8 | | | | 9 | | | | 26 | | | | 32 | | | | 21 | | | | 32 | |

| (1) | Following a Boundaries Revision exercise conducted between April 2008 and March 2010, the number of constituencies (parliamentary seats) was increased from sixty to sixty-three. |

Source: Office of the Prime Minister.

As part of the legislative agenda for FY 2016/17, the Government announced its intention to table a Constitutional (Amendment) Bill to replace Her Majesty The Queen with a non-executive President as Head of State. The Administration also intends to broaden and deepen Jamaican input into the regional integration movement. See “—International Relationships—Caribbean Community (CARICOM).”

International Relationships

Jamaica maintains diplomatic relations with almost every nation in the world. Jamaica is a member of the United Nations and its affiliated institutions, including the Food and Agriculture Organization, the International Monetary Fund (“IMF”), the World Bank Group, the World Health Organization, the World Tourism Organization, the World Intellectual Property Organization, the International Seabed Authority, the United Nations Environment Program and the United Nations Conference on Trade and Development (“UNCTAD”). It is also a member of several other regional and international bodies, including the World Trade Organization (“WTO”), the African, Caribbean and Pacific Group of States (“ACP”), the Association of Caribbean States, the Caribbean Community (“CARICOM”), the Commonwealth; the Latin American and Caribbean Economic System, the Organization of American States, and the Community of Latin American and Caribbean States.

Jamaica is a signatory to the Cotonou Partnership Agreement (“CPA”); party to the CARIFORUM-EU Economic Partnership Agreement (“EPA”) and CARICOM Bilateral Trade Agreements with Colombia, Costa Rica, Cuba, Dominican Republic and Venezuela. It is also a beneficiary of the Caribbean Basin Economic Recovery Act and the Caribbean-Canada Trade Agreement (“CARIBCAN”). In addition, as a member of the United Nations bloc of developing countries known as the Group of 77, Jamaica is eligible for the Generalized System of Preferences.

Jamaica receives preferential tariff treatment on most of its products pursuant to, among others, the trade agreements described below.

The WTO Agreements

Jamaica currently trades with the 164 members of the WTO on the basis of the Most Favoured Nation (“MFN”) and National Treatment principles, except in specific cases where it trades with members under regional trade agreements provided for in Article 24 of the General Agreement on Tariffs and Trade/WTO or where it benefits from preferences under the Enabling Clause, some of which are non-reciprocal and unilateral, such as the Generalised System of Preferences. Jamaica also benefits from other non-reciprocal preferential market access schemes provided by WTO members under the legal cover of waivers obtained within the context of Article 9 of the Marrakesh Agreement.

The WTO provides a forum for exchanging liberalization commitments through successive rounds of multilateral trade negotiations. The current round, called the Doha Development Agenda (“DDA”), was launched in 2001 and should have ended in 2005. Limited progress has been made in the DDA to further reform multilateral trade rules. Deep divisions among WTO members, including on the draft modalities for liberalizing trade in agriculture, non-agricultural market access and services and modalities for strengthening WTO rules, have contributed to the delayed progress.

D-9

A breakthrough in the round was reached at the ninth WTO Ministerial Conference held in Bali, Indonesia, in December 2013, with the adoption of the WTO Agreement on Trade Facilitation (“TF”). The TF Agreement entered into force on February 22, 2017, when two-thirds of the current WTO membership (108 Members out of 162) ratified the agreement. Jamaica ratified the agreement on January 19, 2016.

A further breakthrough in the round was reached at the tenth WTO Ministerial Conference held in Nairobi, Kenya, from December 15 – 19, 2015. Ministers adopted the historic decision to establish disciplines on export competition. This decision establishes disciplines on export subsidies and other types of export support instruments that can distort competition i.e. export credits, export credit guarantees and other types of export financing; exporting state trading enterprises; and food aid. This will see the elimination of export subsidies in the area of agriculture, a practice that was prohibited for non-agricultural products decades ago.

Work is ongoing on other outstanding issues of the DDA. WTO members are preparing for the eleventh WTO Ministerial Conference to be held from December 11 – 14, 2017, in Buenos Aires, Argentina.

Caribbean Community (CARICOM)

The Treaty of Chaguaramas (the “Treaty”) establishing CARICOM was signed in 1973 by four English-speaking Caribbean countries.

Between 1997 and 2001, Member States negotiated a revision of the Treaty to expand the scope of the Common Market by establishing a single market and economy. Consequently, the Revised Treaty of Chaguaramas (the “Revised Treaty”) establishing the Caribbean Community, including the CARICOM Single Market and Economy (“CSME”), was signed by the following Caribbean countries in July 2001: Antigua and Barbuda, The Bahamas, Barbados, Belize, Dominica, Grenada, Guyana, Jamaica, Montserrat, St. Kitts and Nevis, St. Lucia, St. Vincent and the Grenadines, Suriname, and Trinidad and Tobago. Haiti later signed the Revised Treaty on July 2, 2002.

The Revised Treaty seeks to establish a common economic space among CARICOM Member States that would provide for the free movement of goods, services, people and capital, and would give CSME nationals the right to establish businesses and to provide a service in any CARICOM Member State participating in the CSME. In January 2006, the implementation of the provisions of the CARICOM Single Market (“CSM”) was initiated by Jamaica, Barbados, Belize, Guyana, Suriname and Trinidad and Tobago, that is, the provisions enabling the free movement of goods, services, people and capital. Other Member States started the CSM implementation process in July 2006. The Bahamas and Montserrat are members of the Caribbean Community, but are not yet participating in the CSME. A 2009 audit conducted by the CARICOM Secretariat indicates that Jamaica is far advanced in implementing its obligations under the Revised Treaty.

Additionally, the Revised Treaty provides for the establishment of the single economy, which would include the harmonization of fiscal and monetary policies and the establishment of a common currency. The single economy requires a great degree of legislative and economic policy harmonization among Member States, and covers areas in which the region has not yet been able to find policy convergence. At a CARICOM Heads of Government retreat held in May 2011, Heads of the Government agreed to consolidate the gains of the CSM and to put on hold the single economy.

At the regional level, a number of instruments – draft protocols, model legislation and draft sectoral and regional policies – relating to the CSM are being negotiated. Jamaica is participating actively in these negotiations. They relate to, inter alia, the Draft Protocol on Contingent Rights, the CARICOM Financial Services Agreement, the Draft Protocol on Public Procurement, the Model Bill on Consumer Protection, the Draft Framework Policy on the Single Jurisdiction and the Draft Policy Framework on Mergers and Acquisitions.

D-10

Efforts are also underway to put in place the CARICOM Administrative Processing System (“CAPS”) at the regional level. The CAPS is a fully automated system being implemented to enable CARICOM nationals to secure online their Skilled Certificates and Service Providers Certificates.

Trade with Latin America

Jamaica, as part of CARICOM, has concluded bilateral trade agreements with Venezuela, Colombia, Cuba, the Dominican Republic and Costa Rica. These agreements were negotiated pursuant to Article 80 – Coordination of External Trade Policy of the Revised Treaty. Jamaica has only recently formally ratified the Agreements with the Dominican Republic, Costa Rica and Cuba.

Caribbean-Canada Trade Agreement (CARIBCAN)

The 1986 CARIBCAN is an agreement between Canada and all CARICOM countries, except Haiti and Suriname. This agreement establishes a program for trade, investment and industrial cooperation, and features the unilateral extension by Canada of duty-free access to the Canadian market for a range of eligible imports from beneficiary CARICOM countries. CARIBCAN’s basic objectives are to enhance the Caribbean region’s existing trade and export earnings, improve its trade and economic development prospects, promote new investment opportunities, and encourage enhanced economic integration and cooperation within the region. After more than twenty years of CARIBCAN’s existence, the Parties commenced negotiations in 2009 for a CARICOM-Canada Trade and Development Agreement that would allow reciprocal access for Canadian companies to the Caribbean market in a range of areas, including goods as well as services and investment. The negotiations on the new reciprocal trade agreement were suspended in May 2015. However, the CARIBCAN arrangement remains in force, and Canada applied for and received a new WTO MFN waiver in July 2015 which extends to 2023.

The Caribbean Basin Initiative

The Caribbean Basin Initiative (“CBI”), which was initially launched in 1983 with the enactment of the Caribbean Basin Economic Recovery Act (“CBERA”), was amended in 1990 to increase market access to the United States. In 2000, the United States further expanded the CBI with the enactment of the Caribbean Basin Trade Partnership Act (“CBTPA”). The CBTPA provides preferential access for a number of products previously excluded from the CBI. The CBTPA will expire on September 30, 2020. The United States applied for and received a new WTO waiver for CBERA/CBTPA in May 2015. The waiver will expire on December 31, 2019.

Generalized System of Preferences

Under the aegis of the UNCTAD, the Generalized System of Preferences (“GSP”) was designed to afford developing countries preferential access for a wide range of their exports to the markets of developed countries. The GSP is an export-promotion tool with the objectives of increasing the export earnings of developing countries, promoting industrialization in developing countries and accelerating the rate of economic growth in developing countries. Jamaica continues to benefit from preferences extended unilaterally under the GSP schemes of Australia, Japan, New Zealand, Norway and Switzerland.

ACP/European Union Cotonou Partnership Agreement

In February 2000, the European Union and the ACP, concluded negotiations for a new 20-year trade, industrial, financial and technical cooperation agreement. Jamaica ratified the new agreement, known as the CPA, in February 2001 and, following ratification by 75% of ACP Member States and all European Union members, the agreement formally entered into force on April 1, 2003. The agreement was reviewed in 2005 and 2010. The trade provisions of the CPA have been replaced by the EPA, as described below.

The CPA will expire in 2020. Article 95 (4) stipulates that eighteen (18) months before the expiry of the agreement, the parties shall enter into negotiations in order to examine what provisions shall subsequently govern their relationship. As such, consultations are now underway within both groupings (the ACP and the European Union) to prepare for the negotiations, which will formally commence in August 2018 on the successor arrangement to the CPA.

D-11

The CARIFORUM-EU Economic Partnership Agreement

The EPA between the Caribbean Forum of ACP States (CARIFORUM, i.e., CARICOM and the Dominican Republic) and the European Union is a reciprocal trade agreement, which was signed in October 2008 by the European Union and fourteen (14) CARIFORUM States, with the exception of Haiti, which signed the agreement in December 2009.

The EPA is a comprehensive and development-orientated trading arrangement which replaced the previous non-reciprocal trading arrangement between the European Union and the ACP countries.

Under the EPA, the European Union committed to remove immediately all tariffs and quotas on exports from CARIFORUM, with the exception of rice and sugar. In the case of rice, full liberalization took place in 2010; for sugar it took place in 2015. Under the EPA, exporters of CARIFORUM-originated goods are accorded duty-free and quota-free access to the European Union market.

Unlike the European Union, CARIFORUM States will reduce tariffs on a phased basis. The European Union’s exports into CARIFORUM are to be liberalized over a period of 25 years with exclusions and long phase—in periods for sensitive products. Seventy-five percent (75%) of all CARIFORUM’s imports of agricultural and fisheries products have been excluded from liberalization under the EPA. These sensitive products will continue to be protected by tariffs applied by CARIFORUM States. The tariff liberalization process under the EPA must be completed by January 1, 2033. The first reduction in tariffs began in January 2011. Jamaica implemented the first and second phases of tariff reductions under the EPA in January 2011 and January 2013 respectively. Jamaica commenced the third phase of tariff reductions on goods imported from the European Union in January 2015. The tariff reductions are now being made automatically.

The EPA goes beyond trade in goods to include trade in services. The agreement requires the European Union to remove restrictions on CARIFORUM’s services exports, beginning with the liberalization of 29 sectors and sub-sectors.

The EPA establishes provisions to administer trade-related issues between the parties. These trade-related issues are primarily in relation to agriculture and fisheries, sanitary and phyto-sanitary standards, customs and trade facilitation, investment facilitation, intellectual property rights, competition, electronic commerce and personal data protection. The agreement goes further to provide for parties to undertake development cooperation in a number of areas, ranging from the development of supply-side capacity, including the development of trade-related infrastructure, to the enhancement of the tourism sector and cultural cooperation.

There are several institutions established under the EPA to oversee its implementation, monitoring and review. These bodies are (i) the Joint CARIFORUM-EU Council convened at the ministerial level; (ii) the CARIFORUM-EU Trade and Development Committee convened at the level of senior officials; (iii) the CARIFORUM-EU Parliamentary Committee involving the parliamentarians; and (iv) the CARIFORUM-EU Consultative Committee to promote dialogue among civil society. Jamaica is currently applying the EPA provisionally, pending ratification.

D-12

THE JAMAICAN ECONOMY

General

Jamaica operates as a mixed, free market economy with state enterprises as well as private sector businesses. Major sectors of the Jamaican economy include agriculture, mining, manufacturing, tourism, and financial and insurance services. As an open economy, Jamaica is well integrated into the global economy with intraregional trade contributing prominently to overall economic activity.

Since the early 1980s, successive governments have implemented structural reforms aimed at fostering private sector activity and increasing the role of market forces in resource allocation. During this period, a large share of the economy has been returned to private sector ownership through divestment and privatization programs in areas such as agriculture, tourism, transportation, banking, manufacturing and communications. See “—The Jamaican Economy—Privatization.” Deregulation of markets, the elimination of price subsidies and price controls and the reduction and removal of trade barriers have reduced or eliminated production disincentives and anti-export biases.

In the early 1990s, the reform process in Jamaica gained momentum with, among other developments, the liberalization of the foreign exchange market and the overhaul and simplification of the tax system. In addition to changes in personal income tax and corporate tax regimes, taxes have been streamlined and simplified to facilitate compliance and greater efficiency in tax collection, and a number of tax exemptions have also been eliminated. The Government is continuously assessing its current tax legislation and has been implementing a series of tax reforms. See “Public Finance—Taxes and Tax Reform.”

In 2009, Jamaica introduced a new strategic plan to achieve developed country status by 2030 called Vision 2030 Jamaica. The plan is based on the following seven guiding principles: transformational leadership, partnership, transparency and accountability, social cohesion, equity, sustainability, and urban and rural development. Vision 2030 Jamaica seeks to redefine the strategic direction of Jamaica by moving from dependence on lower forms of capital, such as tourism and basic agricultural commodities, to higher forms of capital, such as cultural, human, knowledge, institutional and services capital stocks. Jamaican business owners face challenges that primarily stem from global factors that include high energy prices, including the price of oil, and, in some sectors, high commodity prices. See “—The Jamaican Economy—Principal Sectors of the Economy.”

D-13

During FY 2016/17, the Government continued on its comprehensive Economic Reform Program (“ERP”) which it began in FY 2012/13, while continuing to tighten fiscal policy. The main pillars of the ERP were:

| | • | | structural reforms to boost economic growth and employment; |

| | • | | actions to improve price and non-price competitiveness; |

| | • | | upfront fiscal adjustment, supported by extensive fiscal reforms; |

| | • | | debt reduction, including active debt management, to place public debt on a sustainable path, while protecting financial system stability; and |

| | • | | improved social protection programs. |

The ERP included a heavy and front-loaded reform agenda to support a prompt economic recovery, maintain social cohesion, build labor capacity and improve productivity. Accordingly, measures were implemented to improve access to credit, reduce bureaucracy and other limiting factors in the business environment, and to improve labor market flexibility. This reform agenda was focused on actions to strengthen public financial management, introduce a fiscal rule, reform the tax system, improve the business climate, move towards inflation targeting and reform of the securities dealers sector. See “The Monetary System—Legislation and Regulation” and “Public Finance—Taxes and Tax Reform.” These fiscal reforms were essential to a sustained fiscal consolidation effort to promote debt reduction. Structural reforms to achieve higher and sustained growth were pivotal to long-term economic stability and increased welfare of the population.

To alleviate the possible adverse impact of fiscal adjustment on the most vulnerable, the program included a floor on social spending for the most vulnerable in the population. The Government also recognized that safeguarding the financial sector was critical, and consequently had established a Financial Sector Support Fund to offer assistance, if needed, to financial institutions that participated in the debt exchange of 2013. See “The Monetary System—Legislation and Regulation.”

A key part of the ERP was a growth strategy that would focus on investment in:

| | • | | the consolidation of Jamaica as a logistics hub for shipment; |

| | • | | information technology; |

| | • | | infrastructure development; |

| | • | | diversification of the tourism product; |

| | • | | sustainable energy; and |

| | • | | the promotion of a more business-friendly environment with respect to government agency administration, workforce and access to credit for smaller to medium-sized businesses. |

Some of the impact of the ERP was reflected in the improvement in Jamaica’s ranking in the ‘Ease of Doing Business’ report, published by the World Bank. Specifically, based on the Ease of Doing Business 2017 report, Jamaica ranked 67th for the year 2016 relative to 85th in 2014. This progress was mainly based on improvements in access to financing, and ease of access to electricity as well as reductions in impediments to starting a business. This improvement also reflected the efforts towards implementing key structural reforms which augur well for a sustainable medium-term growth path for Jamaica.

D-14

IMF Arrangements

Stand-By-Arrangement

In February 2010, the Government entered into a 27-month Stand-by-Arrangement (“SBA”), with the IMF in the amount of 820.5 million (approximately US$1.27 billion) special drawing rights (“SDR”). Prior to the execution of the SBA, the Government had to take several actions, including adopting a tax policy package yielding approximately 2% of GDP; completing the Jamaica Debt Exchange (“JDX”); and reaching an agreement regarding the divestment of Air Jamaica, all of which the Government completed. The SBA supported the Government’s economic program aimed at restoring macroeconomic stability and creating conditions for improved growth. This program included critical steps and policy reforms to tackle fiscal and debt imbalances and other underlying vulnerabilities. The program was designed to assist the country in the establishment of fiscal and debt sustainability over the medium term. As such, the program focused on facilitating tax reform, rationalization of the public sector and reform of public financial systems. See “—Public Sector Indebtedness—The Jamaica Debt Exchange,” “—Public Finance—Taxes and Tax Reform” and “—The Jamaican Economy—Privatization.”

To achieve these goals, the program focused on a three-pronged strategy of:

| | • | | comprehensive debt management; and |

| | • | | reforms to further strengthen the financial system. |

As part of the SBA, the Government undertook a structural reform agenda, which included reforms to fiscal institutions, public entities, debt management, and the financial sector. As part of these reforms the Government passed the Fiscal Responsibility Framework (“FRF”), launched its strategic and comprehensive domestic liability management program, and implemented a variety of reforms impacting the financial system. The SBA approved by the IMF Board in February 2010 went off-track within a year, as the program’s targets for improving the government’s budget position were missed, which in turn eroded confidence, lowered economic growth, and resulted in acute balance of payments pressures. In the absence of the scheduled reviews under the SBA, no further performance targets were established to form the basis for further drawdowns. This also resulted in the Government not receiving SDR 285.7 million (US$420 million) from the IMF as well as multilateral funding of approximately US$550 million and grants of approximately $59.19 million. See “Public Sector Indebtedness—External Debt.”

Extended Fund Facility

On May 1, 2013, the Executive Board of the IMF approved a request by the Government for a four-year extended arrangement extended fund facility (“EFF”) in an amount of SDR 615.38 million (approximately US$932.3 million) based on exchange rates published by the IMF on January 31, 2013, the equivalent of 225% of the Government’s quota in the IMF. This EFF is the successor to and supersedes the SBA. The purpose of the EFF is to support the Government’s comprehensive ERP described above. See below for a description of the disbursements made to date under the EFF.

Pursuant to the terms of the EFF, its implementation and progress is monitored through the quarterly review quantitative performance criteria, indicative targets and structural benchmarks. See “—General.” The quantitative performance criteria establishes targets relating to, among other things: the primary balance of the Central Government; tax revenues; the overall balance of the public sector, the aggregate amount of Government direct debt, the aggregate amount of Government guaranteed debt; the aggregate amount of Government accumulation of domestic arrears, the aggregate amount of Government accumulation of tax refund arrears, the consolidated Government accumulation of external debt payment arrears, the amount of Government social spending, the cumulative change in the Government’s net international reserves and the cumulative change in the Government’s net domestic assets.

D-15

Progress under the Extended Fund Facility

The first review of performance criteria was completed by the end of September 2013, the Government met all required criteria, targets and benchmarks and the IMF made a second disbursement in the amount of approximately SDR 19.97 million on October 2, 2013. On each of the following dates, the IMF Board completed its review, found the Government to have met all criteria, and disbursed the corresponding funds:

| | • | | On December 18, 2013, with a disbursement of SDR 19.97 million (approximately US$30.8 million). |

| | • | | On March 19, 2014 with a disbursement of SDR 46.0 million (approximately US$71.4 million). |

| | • | | On September 24, 2014, with a disbursement of SDR 45.95 million (approximately US$68.6 million). |

| | • | | On December 19, 2014, with a disbursement of SDR 45.95 million (approximately US$67.0 million). |

| | • | | On March 30, 2015, the completion of that review resulted in disbursement of SDR 28.32 million (approximately US$40.0 million). |

| | • | | On June 16, 2015, permitting the disbursement of SDR 28.32 million (approximately US$39.7 million). |

| | • | | On September 23, 2015, with a disbursement of SDR 28.32 million (approximately US$39.7 million). |

| | • | | On December 17, 2015, with a disbursement of SDR 28.32 million (approximately US$39.3 million). |

| | • | | On June 21, 2016, with a disbursement of SDR 56.64 million (approximately US$80.34 million). |

| | • | | On September 20, 2016, with a disbursement of SDR 28.32 million (approximately US$38.87 million). |

D-16

The following table reflects Jamaica’s quantitative performance criteria and indicative targets, for the periods presented, under the PSBA, as applicable:

IMF Performance Criteria

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | 2016 | | | 2017 | | | 2018 | |

| | | Performance

Criteria | | | Adjusted

PC | | | Actual | | | Indicative

Target | | | Performance

Criteria | | | Proposed

Revised

Performance

Criteria | | | Indicative

Target | | | Proposed

Performance

Criteria | | | Indicative

Target | |

| | | End-Dec | | | End-Mar | | | End-June | | | End-June | | | End-Sep | | | End-Dec | | | End-Mar | |

| | | (in billions of Jamaican dollars unless otherwise stated) | |

Fiscal targets | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Performance Criteria | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Primary balance of the central government (floor)(3) | | | 54.0 | | | | | | | | 76.6 | | | | 123.0 | | | | 13.4 | | | | 15.0 | | | | 37.0 | | | | 59.0 | | | | 130.5 | |

Overall balance of the public sector (floor)(3) | | | (51.5 | ) | | | (47.7 | ) | | | 10.7 | | | | (17.2 | ) | | | (41.4 | ) | | | (39.2 | ) | | | (46.9 | ) | | | (59.3 | ) | | | (14.8 | ) |

Net increase in the central government guaranteed debt (ceiling)(3) | | | 0.0 | | | | | | | | (4.1 | ) | | | 0.0 | | | | 0.0 | | | | 0.0 | | | | 0.0 | | | | 0.0 | | | | 0.0 | |

Central government accumulation of domestic arrears (ceiling)(4)(10) | | | 0.0 | | | | | | | | 0.0 | | | | 0.0 | | | | 0.0 | | | | 0.0 | | | | 0.0 | | | | 0.0 | | | | 0.0 | |

Central government accumulation of tax refund arrears (ceiling)(5)(10) | | | 0.0 | | | | | | | | (4.4 | ) | | | 0.0 | | | | 0.0 | | | | 0.0 | | | | 0.0 | | | | 0.0 | | | | 0.0 | |

Accumulation of external debt payment arrears (ceiling)(4)(9) | | | 0.0 | | | | | | | | 0.3 | | | | 0.0 | | | | 0.0 | | | | 0.0 | | | | 0.0 | | | | 0.0 | | | | 0.0 | |

Indicative targets | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Tax revenues of the central government (floor)(3) | | | 300.0 | | | | | | | | 322.1 | | | | 440.0 | | | | 100.0 | | | | 100.0 | | | | 215.0 | | | | 328.0 | | | | 473.0 | |

Change in the stock of public bodies non-guaranteed debt (ceiling)(11) | | | (1.0 | ) | | | 2.8 | | | | (1.3 | ) | | | 3.3 | | | | 7.6 | | | | 2.5 | | | | 2.0 | | | | 3.5 | | | | 11.5 | |

Central government spending on social programs (floor)(3)(7) | | | 16.4 | | | | | | | | 23.2 | | | | 24.3 | | | | 5.0 | | | | 6.1 | | | | 11.2 | | | | 18.3 | | | | 26.6 | |

Total loan value of all user funded PPPs (ceiling, percent of GDP) | | | 3.0 | | | | | | | | 0.4 | | | | 3.0 | | | | 3.0 | | | | 3.0 | | | | 3.0 | | | | 3.0 | | | | 3.0 | |

Monetary targets | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Stock of non-borrowed net international reserves (floor)(6)(8) | | | 1,428 | | | | 1,419 | | | | 1,671 | | | | 1,475 | | | | 1,521 | | | | 1,521 | | | | 1,637 | | | | 1,777 | | | | 1,917 | |

Monetary policy consultation clause (in percent | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Upper band | | | 9.0 | | | | | | | | | | | | 9.0 | | | | 9.0 | | | | 9.0 | | | | 9.0 | | | | 9.0 | | | | 8.0 | |

Center inflation target | | | 5.5 | | | | | | | | 1.7 | | | | 5.5 | | | | 5.5 | | | | 5.5 | | | | 5.5 | | | | 5.5 | | | | 5.5 | |

Lower band | | | 1.0 | | | | | | | | | | | | 2.0 | | | | 2.0 | | | | 2.0 | | | | 2.0 | | | | 2.0 | | | | 3.0 | |

| (1) | Targets as defined in the Technical Memorandum of Understanding (“TMU”). |

| (2) | Based on program exchange rates defined in the TMU. |

| (3) | Cumulative flows from April 1 through March 31. |

| (4) | Includes debt payments, supplies and other committed spending as per contractual obligations; full definition in TMU. |

| (5) | Includes tax refund arrears as stipulated by law. |

| (6) | In millions of US dollars. |

| (7) | Defined as a minimum annual expenditure on specified social protection initiatives and programs (defined in TMU). |

| (8) | Stock of BOJ NIR minus all foreign currency CDs to domestic residents; full definition in TMU. |

| (9) | Continuous performance criterion. |

| (10) | The accumulation is measured against the stock at end-March 2016, which is J$21.0 billion for domestic arrears and J$17.3 billion for tax arrears. |

| (11) | For end-Dec 2016 and end-Mar 2017, these are cumulative flows from October 1, 2016. For subsequent dates, these are cumulative flows from April 1, 2017. |

Source: Bank of Jamaica.

Precautionary Stand-By-Arrangement

A Memorandum of Understanding (“MOU”), which was submitted to the IMF on October 21, 2016, embodied the tenets of the Government’s economic reform agenda. Coupled with other measures and prior actions, the board of the IMF approved a three-year precautionary Stand-By-Arrangement (“PSBA”) on November 11, 2016 for FY 2016/17 through to FY 2019/20 in an amount of SDR 1,195.3 million (approximately US$1,640.76 million), the equivalent of 312% of Jamaica’s quota in the IMF. Following this approval, SDR 300.1 million (approximately US$411.94 million) was made available for the country to access immediately and the remaining funds will become accessible to Jamaica in six tranches upon successful completion of the semi-annual program reviews.

The new SBA replaced the EFF in the penultimate quarter of FY2016/17 and it is treated as a precautionary arrangement. The Government does not intend to draw on the new SBA unless exogenous shocks generate a balance

D-17

of payments need. In addition to the commitment to maintaining macroeconomic stability, reducing public debt and addressing a wide range of structural issues, initially raised under the EFF, the SBA incorporates a renewed focus on unlocking Jamaica’s growth potential through structural reforms and combating crime and national security challenges.

The aims of the PSBA include:

| | • | | Boosting employment and GDP growth; |

| | • | | Raising the living standards of the Jamaican people; |

| | • | | Progressively reducing a poverty level that remains too high; |

| | • | | Strengthening the social safety net for the poor; |

| | • | | Improving public sector efficiency; |

| | • | | Reallocating public resources to growth-enhancing capital spending; |

| | • | | Rebalancing taxes from direct to indirect taxes; |

| | • | | Bolstering the resilience of the financial system; and |

| | • | | Modernizing the monetary policy framework and building the foundation for an eventual move to inflation targeting, while maintaining exchange rate flexibility and continuing to build precautionary foreign reserves. |

The first IMF-Staff Review mission under the SBA was conducted between February 20 and March 3, 2017 and was followed by a successful review by the Executive Board of the IMF on April 18, 2017. All structural benchmarks for the first review were met. The approval of the first review provides Jamaica with access to an additional SDR 126 million (approximately US$170 million).

Fiscal Responsibility Framework

As part of its economic reform agenda, Jamaica is committed to strengthening its fiscal discipline by adopting a number of programs, the main one being the FRF. The FRF requires the Government to adopt a number of initiatives including the following:

| | • | | preparing medium-term goals and explaining deviations, should there be any; |

| | • | | more comprehensive reporting in several areas and empowering the Financial Secretary to obtain fiscal information from all public sector entities; |

| | • | | strengthening accountability to Parliament in areas such as corporate plans and budgets of public bodies and increasing oversight of overall fiscal policy; |

| | • | | establishing quantitative ceilings on debt stock, fiscal balance and wages within a specific time frame; |

| | • | | requiring the Ministry of Finance and the Public Service to present to Parliament, at the time of the annual budget, a medium-term fiscal policy paper with plans and policies for developing the country; and |

| | • | | establishing a revised budget calendar, which includes the simultaneous tabling of the Estimates of Revenue and Expenditure in a timely manner to effect approval no later than March 31, commencing with the FY 2015/16 Budget. |

D-18

The FRF is the centerpiece of a number of other initiatives aimed at achieving fiscal consolidation. These other initiatives include a medium-term expenditure framework, the establishment of a centralized treasury management system and the enhancement and consolidation of legislation governing debt management generally. See “Public Finance—Central Government Budget.”

Comprehensive Debt Management

On January 14, 2010, the Government of Jamaica launched its strategic and comprehensive domestic liability management program, marketed as the JDX for domestic securities only. The results of the JDX revealed a participation rate of approximately 99.2% with a 100% participation rate from financial institutions. This level of success represented an exchange of approximately J$695.6 billion in eligible bonds.

In addition to implementing the JDX, the Government has an on-going debt management strategy that includes the following:

| | • | | promoting the development of the domestic securities market; |

| | • | | improving the maturity profile of the debt; |

| | • | | increasing the fixed-rate proportion of the domestic debt stock; |

| | • | | mitigating foreign currency and interest rate risks; |

| | • | | continuing to engage multilateral institutions and bilateral creditors; and |

| | • | | continuing to execute market friendly liability management operations including buy backs and debt swaps. |

In November 2012, the House of Parliament approved the Public Debt Management Act, 2012, to make provision for the better management of the public debt. See “Public Sector Indebtedness—General.”

In February 2013, the Government of Jamaica executed a second liability management program marketed as the National Debt Exchange (“NDX”). The NDX had a participation rate of approximately 99%, which translated to a nominal amount of J$845.5 billion tendered for exchange. See “Public Sector Indebtedness—Comprehensive Debt Management.”

During 2015 and thereafter, the Government has successfully and strategically used debt management tools to rebalance the debt portfolio through the execution of buybacks, switches and other liability management tools. For example, on July 28, 2015, Jamaica, through the Central Government, purchased US$3.25 billion of Jamaica’s Petrocaribe Energy Cooperation debt from the Government of Venezuela, acting through PDVSA Petroleo, S.A. The outstanding debt as at December 31, 2015 was purchased for US$1.5 billion. Additionally, on August 30, 2016, the Government settled a tender of US$317.8 million of its 10.625% Notes due 2017 and US$467.4 million of its 8.000% Amortizing Notes due 2019 in exchange for US$743.2 million of its 8.000% Amortizing Notes due 2039. The transaction resulted in the extension of maturities, debt stock reduction and mitigation of refinancing risk in the external debt portfolio.

D-19

Legal Reforms to Financial System

As part of the MOU with the ERP and EFF, the Government passed the Banking Services Act (omnibus banking law), which includes provisions for the qualification of auditors. Additionally, the Bank of Jamaica Act was amended, giving the Bank of Jamaica responsibility for overall financial stability. In keeping with the policy direction of the Government, the Jamaican Securities Act was also amended to enhance the legislative framework for the regulation of the securities industry in order to (i) combat the establishment and proliferation of unlawful financial operations; (2) correct other deficiencies in the regulatory framework of the securities industry; and (3) strengthen the FSC’s investigative powers. The Government has also implemented a variety of reforms impacting the financial system, in particular the securities sector. These reforms include the following:

| | • | | Continuing to strengthen the regulatory and supervisory framework of securities dealers to enhance capitalization and strengthen their ability to withstand shocks. The Securities (Licensing & Registration) Regulations were amended to increase the minimum capital requirements for securities industry dealers and investment advisors. In addition, the Securities (Prudential) Regulations were enacted with a view to improving the soundness of the industry. The Securities (Prudential) Regulations stipulates standards for (i) minimum risk based capital adequacy ratios covering exposures to market, credit, foreign exchange and operational risks; (ii) stress testing; (iii) large exposures limits; (iv) restrictions on the withdrawal of capital and (v) liquidity management. |

| | • | | Reforming the securities dealers’ primary business model, which was retail repo, aimed at reducing the risks associated with the business model. The Securities (Retail Repurchase Agreement) Regulations were enacted to enhance the legal and regulatory framework for the retail repo market, by establishing a distinct treatment for investors in order to protect their interest in the event of insolvency of any securities dealer. In addition, the Collective Investment Scheme (“CIS”) regulations were promulgated to replace the Unit Trust Act and Mutual Fund regulations. These regulations were aimed at expanding the legal form in which the fund could be established as well as enhance the FSC’s authority to regulate all facets of the CIS industry. CIS product was recognized as a viable alternative to the retail repo product as it would reduce the balance sheet risks associated with the retail repo, thus, strengthening their ability to withstand interest rate and liquidity shocks. |

For further details on certain laws and regulations governing the financial sector, see “—Monetary System— Legislation and Regulation.”

Energy Policy

The Government has made the energy policy an essential component of its conscious growth agenda demonstrated through several initiatives and programs being pursued. To this end, Jamaica continues to implement the National Energy Policy 2009-2030 to reduce energy costs, develop additional generating capacity and to facilitate investments in renewable and alternative resources, as a strategy to diversify its source of energy and decrease its reliance on crude oil. Renewable sources of energy and natural gas are more financially viable and environmentally sustainable when compared to crude oil. Natural gas as an alternative source of energy acts as a transitional fuel to help the country increase its electricity generation from renewable sources. The increase in electricity generation will be informed by the Integrated Resource Plan (“IRP”) currently being undertaken by the Government of Jamaica. This IRP will provide a comprehensive assessment and projection of existing and new generation capacities within the country and outline the mechanisms that will help to determine the exact scale of investment in infrastructure to improve quality, stability and efficiency of the grid, and the transmission and distribution systems. Jamaica aims to increase renewable generation to 20% of the grid by 2030, as outlined in the National Energy Policy 2009-2030. Furthermore, in promoting energy efficiency and conservation, a new Electricity Act was passed, which takes into consideration the use and implementation of renewable energy technologies, replacing the 1890 Electric Lighting Act.

D-20

Business Process Outsourcing

Business Process Outsourcing (“BPO”) is presently making a noticeable contribution to employment generation and is augmenting economic growth in Jamaica. Jamaica provides for a number of advantages for BPO, including:

| | • | | ideal time-zone and proximity to the US, the world’s biggest originator of outsourcing; |

| | • | | sophisticated telecommunications infrastructure; |

| | • | | a large and educated English speaking workforce with low attrition rates; and |

| | • | | competitive business costs. |

The following are some recent developments in the BPO sector:

| | • | | Currently, in excess of 40 BPO firms operate in Jamaica, employing approximately 22,000 full-time workers. |

| | • | | Sutherland Global Services has expanded, increasing the headcount in that location from 2,000 to 3,000 individuals. Other BPO facilities are currently underway, including a US$6 million, 75,000 square-foot facility in Montego Freeport. |

| | • | | The PetroCaribe Development Fund has lent a total of US$46 million to BPO ventures, which are engaged in developing a total of 670,000 square feet of operating space. Employment from these ventures, is expected to be 12,000. |

| | • | | A 5-year national strategy to support further development and expansion of the industry and to create an additional 18,000 jobs has been significantly enhanced to drive the workforce in this industry to 50,000 by 2020. |

Moving forward, the objective is to move Jamaica up the value chain in the BPO industry from simple call centers to knowledge processing centers. The aim is for outsourcing more professional services such as legal, medical and accounting support, software development and technical support services.

Gross Domestic Product

The Jamaican economy expanded by 1.4% in 2016 compared to 2015, expanded by 0.9% in 2015 compared to 2014 and expanded by 0.5% in 2014 when compared to 2013. The increase in 2016 was mainly the result of improvement in all industries with the exception of Mining & Quarrying and Producers of Government Services. Industries reflecting growth in 2016 over 2015 included Agriculture, Forestry & Fishing (13.5%), Construction (0.4%), Manufacturing (0.2%), Hotels & Restaurants (2.1%), Transport, Storage & Communication (0.5%), Finance & Insurance Services (1.2%), Real Estate, Renting & Business Activities (0.4%) and Other Services (0.5%).

Real Gross Domestic Product (“GDP”) is expected to expand and strengthen over the medium term against the background of lower consumer prices, improving consumer confidence and continued improvements in Jamaica’s external competitiveness.

D-21

Sectoral Origin of Gross Domestic Product

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | 2012 | | | 2013 | | | 2014 | | | 2015 | | | 2016(1) | |

| | | Amount | | | % of

Total | | | Amount | | | % of

Total | | | Amount | | | % of

Total | | | Amount | | | % of

Total | | | Amount | | | % of

Total | |

| | | (in millions of J$ at constant 2007 prices, except percentages) | |

Agriculture, Forestry and Fishing: | | | 49,371 | | | | 6.8 | | | | 49,018 | | | | 6.7 | | | | 48,782 | | | | 6.6 | | | | 48,757 | | | | 6.6 | | | | 55,333 | | | | 7.3 | |

Traditional Export Agriculture | | | 7,302 | | | | 1.0 | | | | 6,129 | | | | 0.8 | | | | 7,987 | | | | 1.1 | | | | 8,132 | | | | 1.1 | | | | n.a. | | | | n.a. | |

Other Agricultural Crops and Post-Harvest Crop Activities | | | 33,019 | | | | 4.5 | | | | 33,842 | | | | 4.6 | | | | 31,331 | | | | 4.3 | | | | 30,848 | | | | 4.2 | | | | n.a. | | | | n.a. | |

Animal Farming, Forestry and Fishing | | | 9,051 | | | | 1.2 | | | | 9,047 | | | | 1.2 | | | | 9,464 | | | | 1.3 | | | | 9,777 | | | | 1.3 | | | | n.a. | | | | n.a. | |

Construction | | | 51,252 | | | | 7.0 | | | | 52,208 | | | | 7.1 | | | | 53,084 | | | | 7.2 | | | | 53,686 | | | | 7.2 | | | | 53,917 | | | | 7.2 | |

Manufacture | | | 62,522 | | | | 8.6 | | | | 62,226 | | | | 8.5 | | | | 61,706 | | | | 8.4 | | | | 63,901 | | | | 8.6 | | | | 64,049 | | | | 8.5 | |

Mining and Quarrying: | | | 16,273 | | | | 2.2 | | | | 16,716 | | | | 2.3 | | | | 16,861 | | | | 2.3 | | | | 17,022 | | | | 2.3 | | | | 16,476 | | | | 2.2 | |

Bauxite and Alumina | | | 15,087 | | | | 2.1 | | | | 15,698 | | | | 2.1 | | | | 15,772 | | | | 2.1 | | | | 15,843 | | | | 2.1 | | | | n.a. | | | | n.a. | |

Quarrying incl. Gypsum | | | 1,186 | | | | 0.2 | | | | 1,018 | | | | 0.1 | | | | 1,089 | | | | 0.1 | | | | 1,179 | | | | 0.2 | | | | n.a. | | | | n.a. | |

Total Goods | | | 179,418 | | | | 24.5 | | | | 180,167 | | | | 24.6 | | | | 180,434 | | | | 24.5 | | | | 183,366 | | | | 24.7 | | | | 189,776 | | | | 25.2 | |

Wholesale & Retail Trade; Repairs; Installation of Machinery and Equipment | | | 129,559 | | | | 17.7 | | | | 129,400 | | | | 17.7 | | | | 129,838 | | | | 17.6 | | | | 130,586 | | | | 17.6 | | | | 131,144 | | | | 17.4 | |

Electricity and Water Supply | | | 23,705 | | | | 3.2 | | | | 23,242 | | | | 3.2 | | | | 22,973 | | | | 3.1 | | | | 23,293 | | | | 3.1 | | | | 24,152 | | | | 3.2 | |

Finance & Insurance Services | | | 81,130 | | | | 11.1 | | | | 81,216 | | | | 11.1 | | | | 81,606 | | | | 11.1 | | | | 82,000 | | | | 11.0 | | | | 83,020 | | | | 11.0 | |

Producers of Government Services | | | 96,891 | | | | 13.3 | | | | 96,739 | | | | 13.2 | | | | 96,561 | | | | 13.1 | | | | 96,460 | | | | 13.0 | | | | 96,406 | | | | 12.8 | |

Hotels & Restaurants | | | 40,322 | | | | 5.5 | | | | 40,787 | | | | 5.6 | | | | 42,005 | | | | 5.7 | | | | 42,821 | | | | 5.8 | | | | 43,713 | | | | 5.8 | |

Real Estate, Renting & Business Activities | | | 78,950 | | | | 10.8 | | | | 79,291 | | | | 10.8 | | | | 79,680 | | | | 10.8 | | | | 80,097 | | | | 10.8 | | | | 80,426 | | | | 10.7 | |

Transport, Storage & Communication | | | 80,393 | | | | 11.0 | | | | 80,743 | | | | 11.0 | | | | 81,379 | | | | 11.1 | | | | 82,187 | | | | 11.1 | | | | 82,621 | | | | 11.0 | |

Other Services | | | 50,482 | | | | 6.9 | | | | 50,603 | | | | 6.9 | | | | 51,301 | | | | 7.0 | | | | 51,948 | | | | 7.0 | | | | 52,228 | | | | 6.9 | |

Total Services | | | 581,432 | | | | 79.5 | | | | 582,023 | | | | 79.5 | | | | 585,345 | | | | 79.5 | | | | 589,392 | | | | 79.3 | | | | 593,710 | | | | 78.8 | |

Less: Financial Intermediation Services Indirectly Measured (FISIM) | | | 29,812 | | | | 4.1 | | | | 29,647 | | | | 4.0 | | | | 29,373 | | | | 4.0 | | | | 29,469 | | | | 4.0 | | | | 30,140 | | | | 4.0 | |

Real GDP at Basic Prices | | | 731,038 | | | | 100.0 | | | | 732,544 | | | | 100.0 | | | | 736,405 | | | | 100.0 | | | | 743,289 | | | | 100.0 | | | | 753,346 | | | | 100.0 | |

| (1) | Data for 2016 are preliminary. |

Source: Statistical Institute of Jamaica.

D-22

The following table shows the rate of growth of real GDP by economic sectors at constant 2007 prices for the five years ended December 31, 2016:

Rate of Growth of Real GDP by Sector

| | | | | | | | | | | | | | | | | | | | |

| | | 2012 | | | 2013 | | | 2014 | | | 2015 | | | 2016(1) | |

| | | (%) | |

Agriculture, Forestry and Fishing: | | | 2.3 | | | | (0.7 | ) | | | (0.5 | ) | | | (0.1 | ) | | | 13.5 | |

Traditional Export Agriculture | | | 2.0 | | | | (16.1 | ) | | | 30.3 | | | | 1.8 | | | | n.a. | |

Other Agricultural Crops and Post-Harvest Crop Activities | | | 4.9 | | | | 2.5 | | | | (7.4 | ) | | | (1.5 | ) | | | n.a. | |

Animal Farming, Forestry and Fishing | | | (5.8 | ) | | | 0.0 | | | | 4.6 | | | | 3.3 | | | | n.a. | |

Construction | | | (4.4 | ) | | | 1.9 | | | | 1.7 | | | | 1.1 | | | | 0.4 | |

Manufacture | | | (0.3 | ) | | | (0.5 | ) | | | (0.8 | ) | | | 3.6 | | | | 0.2 | |

Mining and Quarrying: | | | (8.7 | ) | | | 2.7 | | | | 0.9 | | | | 1.0 | | | | (3.2 | ) |

Bauxite and Alumina | | | (9.6 | ) | | | 4.0 | | | | 0.5 | | | | 0.5 | | | | n.a. | |

Quarrying incl. Gypsum | | | 4.3 | | | | (14.2 | ) | | | 7.5 | | | | 8.2 | | | | n.a. | |

| | | | | | | | | | | | | | | | | | | | |

Total Goods | | | (1.6 | ) | | | 0.4 | | | | 0.1 | | | | 1.6 | | | | 3.5 | |

| | | | | | | | | | | | | | | | | | | | |

Wholesale & Retail Trade; Repairs and Installation of Machinery | | | (1.4 | ) | | | (0.1 | ) | | | 0.3 | | | | 0.6 | | | | 0.4 | |

Electricity and Water Supply | | | (2.2 | ) | | | (2.0 | ) | | | (1.2 | ) | | | 1.4 | | | | 3.7 | |

Finance & Insurance Services | | | (0.1 | ) | | | 0.1 | | | | 0.5 | | | | 0.5 | | | | 1.2 | |

Producers of Government Services | | | (0.2 | ) | | | (0.2 | ) | | | (0.2 | ) | | | (0.1 | ) | | | (0.1 | ) |

Hotels & Restaurants | | | 1.8 | | | | 1.2 | | | | 3.0 | | | | 1.9 | | | | 2.1 | |

Real Estate, Renting & Business Activities | | | (0.2 | ) | | | 0.4 | | | | 0.5 | | | | 0.5 | | | | 0.4 | |

Transport, Storage & Communication | | | (0.1 | ) | | | 0.4 | | | | 0.8 | | | | 1.0 | | | | 0.5 | |

Other Services | | | 1.2 | | | | 0.2 | | | | 1.4 | | | | 1.3 | | | | 0.5 | |

| | | | | | | | | | | | | | | | | | | | |

Total Services | | | (0.3 | ) | | | 0.1 | | | | 0.6 | | | | 0.7 | | | | 0.7 | |

| | | | | | | | | | | | | | | | | | | | |

Less: Financial Intermediation Services Indirectly Measured (FISIM) | | | (2.6 | ) | | | (0.6 | ) | | | (0.9 | ) | | | 0.3 | | | | 2.3 | |

| | | | | | | | | | | | | | | | | | | | |

Real GDP at Basic Prices | | | (0.5 | ) | | | 0.2 | | | | 0.5 | | | | 0.9 | | | | 1.4 | |

| | | | | | | | | | | | | | | | | | | | |

| (1) | Data for 2016 are preliminary. |

Source: Statistical Institute of Jamaica.

The Petrocaribe Agreement