UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

_________________

FORM 6-K

Report of Foreign Private Issuer

Pursuant to Rule 13a-16 or 15d-16

of the Securities Exchange Act of 1934

For the Month of March 2011

_________________

HADERA PAPER LTD.

(Translation of Registrant’s Name into English)

P.O. Box 142, Hadera, Israel

(Address of Principal Corporate Offices)

Indicate by check mark whether the registrant files or will file annual reports under cover of Form 20-F or Form 40-F:

x Form 20-F oForm 40-F

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(1): o

Note: Regulation S-T Rule 101(b)(1) only permits the submission in paper of a Form 6-K if submitted solely to provide an attached annual report to security holders.

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(7): o

Note: Regulation S-T Rule 101(b)(7) only permits the submission in paper of a Form 6-K submitted to furnish a report or other document that the registrant foreign private issuer must furnish and make public under the laws of the jurisdiction in which the registrant is incorporated, domiciled or legally organized (the registrant’s “home country”), or under the rules of the home country exchange on which the registrant’s securities are traded, as long as the report or other document is not a press release, is not required to be and has not been distributed to the registrant’s security holders, and, if discussing a material event, has already been the subject of a Form 6-K submission or other Commission filing on EDGAR.

Indicate by check mark whether the registrant by furnishing the information contained in this form is also thereby furnishing the information to the Commission pursuant to Rule 12g3-2(b) under the Securities Exchange Act of 1934:

o Yes x No

If “Yes” is marked, indicate below the file number assigned to the registrant in connection with Rule 12g3-2(b): 82-______________

Attached hereto as Exhibit 1 and incorporated herein by reference is the Registrant’s press release dated March 7, 2011 with respect to the Registrant’s results of operations for the year ended December 31, 2010.

Attached hereto as Exhibit 2 and incorporated herein by reference is the Registrant’s Management Discussion with respect to the Registrant’s results of operations for the year ended December 31, 2010.

Attached hereto as Exhibit 3 and incorporated herein by reference is the Registrant’s periodical report for the year ended December 31, 2010.

Attached hereto as Exhibit 4 and incorporated herein by reference are the Registrant’s consolidated financial statements for the year ended December 31, 2010.

Attached hereto as Exhibit 5 and incorporated herein by reference are the consolidated financial statements of Hadera Paper- Printing and Writing Paper Ltd. and subsidiaries with respect to the year ended December 31, 2010.

Attached hereto as Exhibit 6 and incorporated herein by reference are the consolidated financial statements of Hogla-Kimberly Ltd. and subsidiaries with respect to the year ended December 31, 2010.

SIGNATURE

Pursuant to the requirements of the Securities Exchange Act of 1934, the Registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

HADERA PAPER LTD. (Registrant) By: /s/ Yael Nevo Name: Yael Nevo Title: Corporate Secretary |

Dated: March 8, 2011

EXHIBIT INDEX

Exhibit No. 1. 2. 3. 4. 5. 6. | Description Press release dated March 7, 2011. Registrant's management discussion. Registrant's periodical report. Registrant's consolidated financial statements. Consolidated financial statements of Hadera Paper- Printing and Writing Paper Ltd. and subsidiaries. Consolidated financial statements of Hogla- Kimberly Ltd. and subsidiaries. |

Exhibit 1

| NEWS | |

| For Release: IMMEDIATE |

Hadera Paper Ltd.

Reports Financial Results for Fiscal Year Ended December 31, 2010

Hadera, Israel, March 7, 2011 - Hadera Paper Ltd. (AMEX:AIP) (the “Company”) today reported financial results for the year ended December 31, 2010 ("the Reported Period") and for the fourth quarter of the year ("Fourth Quarter"). The Company, its subsidiaries and associated companies – are referred to hereinafter as the "Group".

The Consolidated Data set forth below excludes the results of operation of the associated companies: Hadera Paper- Printing and Writing Paper Ltd. ("Hadera Paper Printing") and Hogla-Kimberly Ltd. ("H-K").

It should be noted, that following an acquisition transaction, as at December 31, 2010, the Company holds approximately 75% of the shares of Hadera Paper Printing that was consolidated within the financial statements of the Company.

Consolidated sales in 2010 amounted to NIS 1,121.0 million, as compared with NIS 892.0 million last year, representing an increase of 25.7% originating primarily from growth in the packaging paper and recycling sector in relation to last year.

Consolidated sales in the Fourth Quarter of the year totaled NIS 336.4 million, as compared with NIS 237.6 million in the corresponding quarter last year, representing growth of approximately 41.6%, originating primarily as a result of an increase in the sales of the packaging paper and recycling sector in relation to the corresponding quarter last year and as compared with Fourth Quarter sales of NIS 295.4 million this year, representing growth of approximately 13.9%.

The operating profit totaled NIS 61.3 million in 2010, 5.5% of sales, as compared with NIS 15.6 million, 1.7% of sales, last year. The increase in operating profit in 2010 as compared with the corresponding year is primarily attributed to the increase in gross profit as a result of the increase in sales. In 2010 and in 2009 the operating profit included non-recurring revenues.

The operating profit in the Fourth Quarter of the year amounted to NIS 28.6 million in relation to operating profit of NIS 0.4 million in the corresponding quarter last year and as compared with operating profit of NIS 20.2 million in the third quarter of the year. The increase in operating profit this quarter is primarily attributed to the sharp rise in gross profit of paper and recycling sector, as a result of the increase in sales and the manufacturing efficiency of the sector as a result of the operation of Machine 8.

The net profit attributed to the Company's shareholders in 2010 amounted to NIS 100.7 million, as compared with net profit of NIS 91.2 million in 2009, representing an increase of 10.4%. The net profit, net of non-recurring revenues and expenditures during the Reported Period, amounted to approximately NIS 76.7 million, as compared with net profit, net of non-recurring revenues and expenditures in 2009 that amounted to NIS 59.2 million, representing an increase of 29.6%.

The net profit attributed to the Company's shareholders during the Reported Period was affected by the improvement in the operating margin of most Group companies in Israel as a result of the growth in operations that brought about an improvement in the operating profit.

Basic earnings per share amounted to NIS 19.84 per share ($5.59 per share) in 2010, as compared with basic earnings per share of NIS 18.03 per share ($4.78 per share) in 2009.

The exchange rate of the NIS in relation to the dollar was revaluated during 2010 by approximately 6.0%, as compared with a revaluation of approximately 0.7% last year (the average exchange rate of the NIS vis-à-vis the dollar was revaluated in 2010 by a rate of approximately 5.1% in relation to last year). The changes in exchange rates, affected the results of the various sectors, although the Group's business portfolio, including the investee companies, is practically at equilibrium in terms of foreign currency and consequently, the exposure of the group to sharp fluctuations in currency exchange rates is low.

The inflation rate in 2010 amounted to 2.7%, as compared with an inflation rate of 3.9% in 2009.

In the global packaging paper market, the Company estimates that as a result of the continuing rise in global pulp prices during the Reported Period, the demand for recycled packaging paper has increased, as an alternative to virgin packaging paper. The trend of rising prices of recycled products in the global packaging paper market continued consistently throughout the Reported Period, at an average rate of approximately 28% (according to publications by PPI Germany), and grew more moderate only toward the end of 2010 until its stabilization.

The Group manages a wide and diverse portfolio of companies and businesses focused on consumer goods and basic commodities. As part of the trend of consumption in the Israeli economy during the Reported Period, this trend led to an increase in demand at most Group companies for a wide range of products, while continuing to place an emphasis on the implementation of efficiency and cost-cutting measures across all sectors of operation.

The aforementioned revaluation of the NIS in relation to the average dollar and the euro, in relation to last year, by approximately 5.1% and 9.4%, respectively, led to savings in terms of inputs and imported products denominated in dollars or euro, in the principal sectors of operation of the Company, whose prices track import prices in the said currencies. As a result of the said revaluation, the relative price of natural gas denominated in dollars, decreased by approximately 6% in relation to last year and also contributed to savings. Moreover, the price of electricity also decreased by approximately 10% in 2010, in relation to last year. These savings were partially offset by the rising prices of water during the year, by an average rate of 42%, along with the sharp rise in the price of fibers by approximately 43%, in relation to last year.

Net financial expenses amounted to NIS 44.8 million in 2010, as compared with NIS 18.3 million in 2009. The growth in financial expenses originated primarily as a result of the growth in financial expenses on account of long-term liabilities, that increased by approximately NIS 30.6 million relation to last year, mostly due to the cost of financing Series 3 and 4, whose discounting of financing costs for Machine 8 ended at the end of May, coupled with the issuing of bond series 5 (new series) in May. Moreover, an increase was recorded in financial expenses as a result of long-term loans assumed by a subsidiary for financing an investment in a corrugator.

2

The Company’s share in the earnings of associated companies totaled NIS 81.1 million in 2010, as compared with NIS 87.4 million last year.

The following principal changes were recorded in the Company’s share in the earnings of associated companies, in relation to the corresponding period last year:

| - | The Company's share in the net profit of Hadera Paper Printing (49.9%) in 2010 amounted to NIS 11.1 million as compared with NIS 14.1 million in 2009, a decrease of NIS 3.0 million. The decrease in the profit originated primarily from the decrease in the operating profit of Hadera Paper Printing, that decreased from NIS 40.5 million last year, to NIS 31.1 million this year. The decrease in operating profit in 2010 originated primarily from the sharp rise in the prices of raw materials in relation to last year, despite measures to raise prices in the course of the year and the improved gross margin of part of the product range. The decrease in net income was also affected by the growth in tax expenditures in the amount of NIS 6.7 million in 2010, as compared with last year, primarily as a result of recording tax revenues of approximately NIS 6 million last year as a result of the change in the tax rate, that were offset as a result of the reduction in financial expenses in the amount of NIS 9.7 million. |

| - | The Company's share in the net profit of H-K in Israel (49.9%) in 2010 amount to NIS 75.0 million as compared with NIS 83.0 million in 2009. The decrease in the sum of NIS 8.0 million, originated primarily from the decrease in operating profit that fell from NIS 210.0 million to NIS 193.8 million this year. The decrease in the operating profit is primarily attributed to the erosion of the selling prices in some sectors of operation, coupled with the rise in the prices of some principal inputs at the company, that were offset by far-reaching efficiency measures that were implemented across the company, continuing savings in purchasing and the strengthening of the company brands, led to a reduction in the erosion of earnings in 2010. |

| - | The Company's share in the losses of KCTR Turkey (49.9%) in 2010, amounted to NIS 2.7 million, as compared with NIS 7.6 million in 2009, representing a decrease of NIS 4.9 million. This reduction in loss, despite the slight decrease in the volumes of operation, is primarily attributed to the sale of the PEDO brand to a local chain, that generated non-recurring revenues of NIS 3.1 million in 2010, that brought about the continuing reduction in the net loss from NIS 15.1 million last year, to NIS 5.4 million in 2010. In addition, the loss was reduced as a result of recording of financial revenues from the valuation of operational balances. |

The Company also announced that the Board of Directors has approved the convening of an annual general shareholders meeting to discuss the financial reports and management discussion for 2010, and to approve, the election of directors (other than external directors), the nomination of the auditing CPA's for 2011 and the approval of a lease agreement between the Company and Clal PV Projects Ltd. (a private company held and indirectly controlled by Clal Industries and Investments Ltd., the Company's controlling shareholder) for the Company’s leasing roof area to Clal P.V. for construction of installations for the production of electricity using photovoltaic technology. At such time as the Company fixes the record date and meeting date for the shareholders meeting, it will distribute a proxy statement describing the proposals to be considered at the meeting.

3

This report contains various forward-looking statements based upon the Board of Directors’ present expectations and estimates regarding the operations and plans of the Group and its business environment. The Company does not guarantee that the future results of operations will coincide with the forward-looking statements and these may in fact differ considerably from the present forecasts as a result of factors that may change in the future, such as changes in costs and market conditions, failure to achieve projected goals, failure to achieve anticipated efficiencies and other factors which lie outside the control of the Company as well as certain other risks detailed from time to time in the Company's filings with the Securities and Exchange Commission. The Company undertakes no obligation for publicly updating the said forward-looking statements, regardless of whether these updates originate from new information, future events or any other reason.

Hadera PAPER LTD.

SUMMARY OF RESULTS

(AUDITED)

except per share amounts

NIS IN THOUSANDS (1)

| 2010 | 2009 | |||||||

| Net sales | 1,121,008 | 891,995 | ||||||

| Net earnings attributed to the Company's shareholders | 100,728 | 91,230 | ||||||

| Basic net earnings per share attributed to the Company's shareholders | 19.84 | 18.03 | ||||||

| Fully diluted earnings per share attributed to the Company's shareholders | 19.68 | 18.03 | ||||||

(1) The representative exchange rate at December 31, 2011 was NIS 3.549=$1.00.

Contact:

Yael Nevo, Adv.

Corporate Secretary and Chief of Legal Department

Hadera Paper Ltd. Group

Yaeln@hadera-paper.co.il

4

Exhibit 2

-Translation from Hebrew-

March 6, 2011

MANAGEMENT DISCUSSION

The Board of Directors of Hadera Paper Ltd. ("The Company" or "Hadera Paper"", the Company, its consolidated subsidiaries and its associated companies – hereinafter: “The Group”)) is hereby honored to present the Management Discussion as at December 31, 2010, reviewing the principal changes in the operations of the company for the months January to December 2010 ("The Period of the Report" or "The Reported Period"). The report was formulated in accordance with the Securities Regulations (Periodic and Immediate Reports), 1970. The results of the company that are presented in the management discussion relate to the share of the shareholders of the company in the results, unless stated otherwise.

A. | Description of the Corporation’s Business |

| 1. | Company Description |

Hadera Paper Group deals in the manufacture and sale of packaging paper, corrugated board packaging, consumer product packaging and unique packaging for industry, recycling of paper and plastic waste, manufacture and marketing of fine paper and in the marketing of office supplies – through subsidiaries. The Company also holds associated companies that deal in the manufacture and marketing of household paper products, hygiene products, disposable diapers and complementary kitchen products.

The company’s securities are traded on the Tel Aviv Stock Exchange and on the New York Stock Exchange (NYSE).

| 2. | General |

Principal Current Operations

| 1. | Business Environment |

The economic recovery in most world financial and real markets continued during 2010, especially in awakening markets, including Israel. At the same time, the effects of the financial crisis which began in 2008 are still evident, including in the fluctuation of rates of securities and currencies, in light of the uncertainty regarding the capacities of some of the European countries to service their debts, the United States’ ability to bring down unemployment rates, the slow recovery of the US real estate market and the handling of increasing inflation in developing countries (China, in particular), following the sharp rise in commodity prices throughout the world.

In Israel, 2010 was a year of recovery from the global crisis. Starting in the second half of 2009, a gradual recovery was noted in GDP. This trend continued in 2010 as well, as 4.5% growth was recorded,1 as compared with 0.8% growth in 2009. Exports of goods and services grew by 12.6%2 in 2010, as compared with a decrease of 12.5% in 2009. In parallel to the recovery in exports in 2010, local demand bounced back, the industry’s sales in the local market grew at a cumulative rate of approximately 5% from the last quarter of 2009 until the second quarter of 2010. In 2010, a rise in private consumption per capita was noted, of some 2.9%3. The growth in local demand stemmed from households, in light of the drop in unemployment rates, as well as from the real increase in average wages in the market, as well as in light of the rise in economic activity in general.

The local capital market showed a positive trend in 2010, and at the same time, capital raising in the corporate debt market gradually increased. The obvious recovery of the Israeli market, on the one hand, and concerns regarding development of a bubble in the local residential real estate market, on the other hand, caused the Bank of Israel to slowly and gradually increase the monetary interest rate, and at the same time to continue be involved in the foreign currency market, and lately, in cooperation with the Ministry of Finance, also to pressure the short term movements of foreign capital. 2011 opened with a continued growth trend for the Israeli market and recovery in the financial markets, together with the development of a trend of geo-political instability in a number of countries in the Middle East.

The continued trend of geopolitical instability in the Middle East could, under certain scenarios, negatively impact the status of the Israeli market and also on the Company’s option of engaging under an agreement with gas provider EMG, one of the gas providers the Company has been negotiating with, in connection with gas supply. As of the date of this report, the Company cannot assess the impact the situation in the region will have on the option of said engagement with EMG, or said impact on possible conditions of engagement with other gas suppliers.

In September 2010 Israel formally joined the OECD (Organization for Economic Cooperation and Development) as a full member. The OECD is a forum of countries committed to democracy and free-market economics, serving as a platform formulate policy and actual practice in economics, society and the environment. Membership in the OECD serves as an indication that Israel is considered to be a "developed nation" and meets the economic and regulatory standards set by the organization. Moreover, Israel's membership in the OECD may hold a positive influence on foreign investors who are considering an investment in Israel and may also serve to influence the credit rating of the State of Israel.

1 Growth data from the Central Bureau of Statistics, December 29, 2010, "Preliminary Assessments for National Accounts for 2010".

2 The data regarding the export of goods and services originating from Central Bureau of Statistics publication, December 29, 2010, "Preliminary Assessments for National Accounts for 2010".

3 Data regarding consumption per capita from the Central Bureau of Statistics, December 29, 2010, "Preliminary Assessments for National Accounts for 2010".

2

In the global packaging paper market, the company estimates that as a result of the continuing rise in global pulp prices during the reported period, the demand for recycled packaging paper has increased, as an alternative to virgin packaging paper. The trend of rising prices of recycled products in the global packaging paper market continued consistently throughout the reported period, at an average rate of approximately 28% (according to publications by PPI Germany), and grew more moderate only toward the end of 2010 until its stabilization. At the beginning of 2011, the rising trend in global recycled paper prices is expected to continue according to indications in the publications of several recycled paper manufacturers in Europe. An additional increase in prices is expected starting in February 2011, a rate of approximately 10%. The said increase in prices and demand, in addition to the prevailing high level of prices, may support the continued growth and expansion in the volumes of operation of the packaging paper sector, in Israel and worldwide.

The above information regarding the impact of Israel having joined the OECD and pertaining to future trends in the paper market and input prices constitutes forward-looking information as defined in the Securities Law, based on the company's estimates at the date of this report. These estimates may not materialize - in whole or in part - or may materialize in a different manner, inter alia on account of factors that lie outside the control of the company, such as business opportunities the company may have, dependence on external factors and changes in regulation, changes in global raw material prices and changes in the supply and demand of global paper products as well as changes in the geopolitical situation in the Middle East.

| 2. | Impact of the Business Environment on Company Operations |

General

The Hadera Paper Group manages a wide and diverse portfolio of companies and businesses focused on consumer goods and basic commodities. As part of the trend of consumption in the Israeli economy during the reported period, this trend led to an increase in demand at most Group companies for a wide range of products, while continuing to place an emphasis on the implementation of efficiency and cost-cutting measures across all sectors of operation.

Sector Operations

In the packaging paper and recycling sector, Machine 8(the new packaging paper manufacturing array) entered into operation during the reported period. This manufacturing array is expected to lead to the doubling of operations in the sector. The running-in of the machine was completed in May and the results of operations have been included as part of the profits of the packaging paper and recycling sector since June. In parallel, the gradual improvement in the learning curve of the machine is continuing. Following the operation of the new manufacturing array, the sales turnover of the packaging paper and recycling sector has increased, both to the domestic market and in export sales. Selling prices in the packaging paper sector are currently on an upward trend globally and locally. This trend is apparently expected to continue in the near future. These factors and others are expected to assist in the continuing improvement in the profitability and results of the sector. Regarding the capitalization of the net costs of the running-in period, see Note 6g to the financial statements.

3

Paper waste, which constitutes the main raw material for the manufacture of packaging paper is collected by Amnir from various sources throughout Israel. On January 19, 2001, the Formalization of Treatment of Packaging Law – 2011 (hereinafter: the Packaging Law), with the goal of regulating arrangements in the matter of treatment of packaging waste. Inter alia, the Packaging Law establishes responsibility for recycling packaging waste and goals for recycling types of packaging waste. The Packaging Law will enter into effect on March 1, 2011, and certain provisions regarding the start of collection by the recognized body will enter into effect on July 1, 2011. In light of the provisions of the Packaging Law, an adjustment will be required in the set-up of the Company’s collection of paper. However, the Company cannot at this stage estimate the impact the law will have on operations, and this is dependent, inter alia, on regulations that will be enacted by power of the law in the matter of separation at source, removal and collection of waste, and on the method of operation to be used by the recognized body to be established by power of the law. The company is examining its preparations in anticipation of the potential setup of collection. For additional details regarding the packaging law, seen a detailed explanation in the periodical report in Section 24.1.24.5.

The impact of the packaging law on the company constitutes forward-looking information as defined in the Securities Law, based on the company's estimates at the date of this report. These estimates may not materialize - in whole or in part - or may materialize in a different manner, inter alia on account of factors that lie outside the control of the company, such as arrangements that will be determined by virtue of the law, changes in global raw material prices and changes in the supply and demand of global paper products.

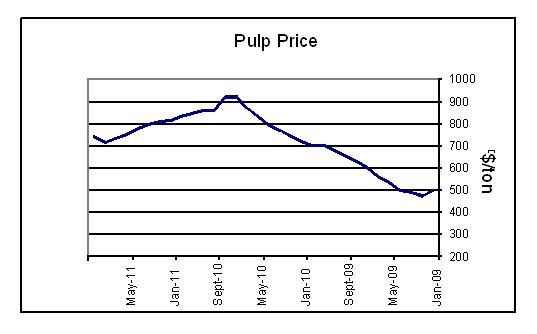

In the fine paper sector, pulp prices continued to soar during the reported period in relation to the corresponding period last year, inter alia as a result of the damage of the earthquake in Chile, that harmed three production plants of large pulp suppliers, thereby leading to delays in the provision of pulp to the global market. In order to compensate for this cost increase, prices were raised in this sector starting in the second quarter. This rise in prices served to compensate for the decrease in the sold quantities, among others. Additionally, Hadera Paper Printing successfully expanded its exports to the United States in 2010, thereby contributing to its improved profitability. The relocation to the logistics center in Modi'in is expected to improve the Company’s logistic capacities and to support the Company’s continued growth and development.

On December 31, 2010, the company acquired from a subsidiary of Mondi Business Paper Group, 25.1% of the issued and outstanding share capital of Hadera Paper Printing, (hereinafter in this section: "The Acquisition Transaction"). The total consideration of the acquisition transaction amounted to €10.364 million, that were paid from the company's own resources. Following the closing of the transaction, true to the date of the report, the company holds approximately 75% of the shares of Hadera Paper Printing, that was consolidated within the financial statements of the company, with a subsidiary of Mondi Group holding the remaining shares of Hadera Paper Printing. As to the accounting implications, see Note 17 to the Company's financial statements dated December 31, 2010, attached to this report.

4

On October 4, 2010, the Company completed a full tender offer for the acquisition of all of the holdings of the public in Carmel, at a price of $22.5 per share in cash, at a total consideration of approximately $4.4 million. As of October 4, 2010, the Company holds 100% of the issued and outstanding share capital and voting rights of Carmel, that has become a privately held company.

In the household paper and absorbent market (through the Hogla Kimberly sector - an associated company), the level of profitability has decreased somewhat in relation to the corresponding period, due to the fierce competition in certain areas of activity. Moreover, the collapse of a significant supplier overseas has created shortages and has led to a temporary increase in costs, that was partially offset by significant efficiency measures. Operations in this sector during the reported period were characterized by price competition and by a preference of consumers for attractively-priced products. The company is therefore continuing to promote special sales campaigns in order to preserve customers and market share. Additionally, the revaluation of the NIS in relation to the average dollar exchange rate during the reported period, as compared with the corresponding period last year, has reduced the damage associated with the higher purchasing costs in some of the sectors. Efforts were also made to distribute purchasing among a wider selection of suppliers, in order to reduce costs. These measures provided the company with the necessary flexibility in order to protect market share and preserve optimized profitability in a competitive business environment.

Raw Materials

In the course of 2010, the NIS was revaluated in relation to the average dollar and the euro, in relation to last year, by a rate of approximately 5.1% and 9.4%, respectively. This revaluation led to savings in terms of inputs and imported products denominated in dollars or euro, in the principal sectors of operation of the company, whose prices track import prices in the said currencies. As a result of the said revaluation, the relative price of natural gas denominated in dollars, decreased by approximately 6% in relation to last year and also contributed to savings. Moreover, the price of electricity also decreased by approximately 10% in 2010, in relation to last year. These savings were partially offset by the rising prices of water during the year, by an average rate of 42%, along with the sharp rise in the price of fibers by approximately 43%, in relation to last year.

Impact of Developments in Financial Markets

The developments in global markets, and especially in the euro bloc and in the United States, that also include volatility in global exchange rates, have and may continue to affect the business results of the Company and its investees, their liquidity, shareholders' equity and assets and the ability to realize these assets, the state of their business (including the demand for the products of the Company's investees), their financial benchmarks and covenants, credit ratings, ability to distribute dividends and even their ability to raise financing for operating activities and long-term activities as well as the financing terms.

5

All of the above, in relation to trends in the global market, in the paper market, in selling prices and in the prices of inputs and their impact on the company, the influence of the completion of the running-in period of the new manufacturing array - all constitute forward-looking information as defined in the securities law, based on the company's estimates at the date of this report. These estimates may not materialize - in whole or in part - or may materialize in a different manner, inter alia on account of factors that lie outside the control of the company, such as the crisis in global credit and banking markets, changes in global raw material prices and changes in the supply and demand of global paper products.

As at the date of publication of these financial statements, no material changes have occurred to the Company's risk management policy.

The exchange rate of the NIS in relation to the dollar was revaluated during 2010 by approximately 6.0%, as compared with a revaluation of approximately 0.7% last year (the average exchange rate of the NIS vis-à-vis the dollar was revaluated in 2010 by a rate of approximately 5.1% in relation to last year).

The changes in exchange rates as mentioned above, affected the results of the various sectors, although the group's business portfolio, including the investee companies, is practically at equilibrium in terms of foreign currency and consequently, the exposure of the group to sharp fluctuations in currency exchange rates is low.

The inflation rate in 2010 amounted to 2.7%, as compared with an inflation rate of 3.9% in 2009. As regards hedging transactions conducted by the company in 2010 on account of its index-linked liabilities, see Section E2, below.

B. | Explanation of the Results of Operation |

| 1. | Analysis of Operations and Profitability |

Commencing January 1, 2009, the company applies International Financial Reporting Standard (IFRS) No. 8, “Operating Segments”, and has accordingly recognized the packaging products and board segment, which includes the operations of Carmel Container Systems and Frenkel C.D., as a separate segment. The associated companies Hogla Kimberly and Hadera Paper - Printing and Writing Paper Ltd. ("Hadera Paper Printing") - formerly Mondi Hadera Paper (a consolidated company as of December 31, 2010) were also recognized as independent segments (for further details, see Note 21 to the financial statements dated December 31, 2010). Please note that the following analysis of financial results relates to the companies that are consolidated in the results of Hadera Paper and is affected by the adoption of the Standard mentioned above.

6

| a. | Sales |

Consolidated sales in 2010 amounted to NIS 1,121.0 million, as compared with NIS 892.0 million last year, representing an increase of 25.7% originating primarily from growth in the packaging paper and recycling sector in relation to last year.

The sales of the packaging paper and recycling sector amounted to NIS 511.4 million in 2010, or NIS 442.7 million net of inter-company sales, as compared with NIS 339.3 million, or NIS 264.2 million net of inter-company sales last year, representing an increase of 67.6%.

The growth in the sales turnover of the packaging paper and recycling sector originates from quantitative growth in the sales of packaging and recycling as a result of the operation of Machine 8, as mentioned above. The growth in the output of Machine 8 served to increase exports to Europe and offered a response for the growth in demand from the local market. The growth in sales is also attributed to the rise in selling prices in relation to last year.

The sales of the packaging products and cardboard sector in 2010 amounted to NIS 509.7 million, and NIS 500.8 million net of inter-company sales, as compared with NIS 484.3 million, and NIS 477.8 million net of inter-company sales, last year, representing an increase of approximately 4.8%, originating primarily as a result of the increase in the volume of operations of the companies in this sector.

The sales of the office supplies marketing sector in 2010 amounted to NIS 178.8 million, or NIS 177.5 million net of inter-company sales, as compared with NIS 151.0 million last year, or NIS 150.0 million net of inter-company sales, representing an increase of 18.3% that originated from the quantitative growth in sales, primarily due to having secured institutional tenders that have expanded the volume of customers and activity in this sector.

The consolidated sales in the fourth quarter of the year totaled NIS 336.4 million, as compared with NIS 237.6 million in the corresponding quarter last year, representing growth of approximately 41.6%, originating primarily as a result of an increase in the sales of the packaging paper and recycling sector in relation to the corresponding quarter last year and as compared with fourth quarter sales of NIS 295.4 million this year, representing growth of approximately 13.9%.

| b. | Cost of Sales |

The cost of sales amounted to NIS 945.4 million in 2010 – or 84.3% of sales – as compared with NIS 765.7 million – or 85.8% of sales – last year. The improvement in the ratio of cost of sales to sales is primarily attributed to the manufacturing efficiency of Machine 8 and a reduction in the rate of consumption of raw materials, despite the sharp rise in output. The increase in the cost of sales originated primarily from an increase in manufacturing costs, (especially energy costs and the use of raw materials, as a result of the operation of Machine 8).

The gross profit totaled NIS 175.6 million in 2010 (15.7% of sales), as compared with NIS 126.3 million, 14.2% of sales, last year, representing growth of approximately 39.0% in relation to last year.

The higher gross profit in relation to last year originated primarily as a result of a quantitative growth in sales in light of the initial recognition of revenues from the sales of Machine 8 in June, coupled with the expansion of operations at the entire range of companies as a result of the market recovery, as stated above. The growth in gross profit is also attributed to the lower prices of some of the raw materials, see Section A2, above.

7

Labor Wages

The labor wages within the cost of sales amounted to NIS 215.1 million in 2010,19.2% of sales, as compared with NIS 206.9 million last year,23.2% of sales. The growth in the labor wages in relation to last year is primarily attributed to the rise in the number of employees as a result of the growth in the volume of operations, both in the office supplies sector and in the packaging paper and recycling sector, that were offset as a result of the discounting of labor expenses in the sum of NIS 8.5 million in the running-in period of Machine 8. (See Note 6f to the financial statements dated December 31, 2010).

The labor wages within the general and administrative expenses amounted to NIS 95.7 million in 2010, 8.5% of sales, as compared with the sum of NIS 87.5 million last year, 9.8% of sales.

The growth in the cost of labor wages in relation to 2009 originated primarily from the recording of labor wages on account of a special bonus to the retiring CEO, according to the decision of the Board of Directors dated March 23, 2010.

The relatively sharp drop in the cost of labor wages as a proportion of sales is primarily attributed to the growth in the volume of operations and sales.

| c. | Selling, General and Administrative and other Expenses |

The growth in selling, general and administrative and other expenses is primarily attributed to the wage bonus granted to the retiring CEO, as mentioned above, that was offset by the recording of proceeds from the sale of real estate in the amount of NIS 18.5 million, a refund of approximately NIS 8.5 million from Hadadit fund for employers and earnings from the devaluation of an investment in a subsidiary that was consolidated on December 31, 2010, in the amount of NIS 5.8 million. The general and administrative expenses also included an amortization of excess cost in the sum of NIS 2.7 million, on account of excess cost recorded during the acquisition of Carmel and Frenkel CD in 2008. Net of the non-recurring labor expenses and net of non-recurring revenues, the Selling General, Administrative and Other expenses increased by approximately NIS 20.0 million, in relation to last year. The increase in expenses originates primarily from an increase in the selling and transportation expenses as a result of the growth in the volumes of operation on the local market in various sectors as well as opposite export markets of the packaging and recycling sector, coupled with the recording of an expenditure related to the valuation of a Hadera Paper Printing Put option in the amount of NIS 0.9 million in 2010, as compared with a revenue of NIS 1.9 million last year.

8

The selling, general and administrative expenses (including wages) and other expenses amounted to NIS 114.3 million in 2010 or 10. 2% of sales – as compared with NIS 110.7 million, 12.4% of sales, last year. Net of non-recurring revenues during the reported period, as a result of the sale of assets in the amount of approximately NIS 18.5 million, a refund from Hadadit fund for employers, valuation of an investment in an investee company and a non-recurring labor expenditure, as mentioned above, the selling, general and administrative expenses amounted to NIS 147.1 million, or approximately 13.1% of sales, as compared with last year, when the selling, general and administrative and other expenses, net of non-recurring revenues as a result of the distribution of a unilateral dividend on account of a preferred share that was allocated by a consolidated subsidiary in the amount of NIS 16.4 million, amounted to NIS 127.1 million, or approximately 14.2% of sales.

| d. | Operating Profit |

The operating profit totaled NIS 61.3 million in 2010, 5.5% of sales, as compared with NIS 15.6 million, 1.7% of sales, last year. The increase in operating profit in 2010 as compared with the corresponding year, is primarily attributed to the increase in gross profit as a result of the increase in sales, as mentioned above. In 2010 and in 2009 the operating profit included non-recurring revenues, as mentioned in Section 1.3, above.

The operating profit of the paper and recycling sector amounted to NIS 50.1 million in 2010, as compared with an operating loss of NIS 2.8 million last year, that included non-recurring profits, as mentioned above. It should be noted that the expenses allocated in 2010 to the packaging sector included non-recurring labor expenses of NIS 5.0 million, as detailed in Section 1.2, above.

The operating profit of the packaging products and board segment amounted to NIS 7.1 million in 2010, as compared with an operating profit of NIS 14.7 million last year. The decrease in operating profit in this sector is primarily attributed to the rise in raw material prices and the increase in other manufacturing expenses, as compared with last year.

The operating profit of the office supplies sector amounted to NIS 5.1 million in 2010, as compared with NIS 4.0 million last year.

The operating profit in the fourth quarter of the year amounted to NIS 28.6 million in relation to operating profit of NIS 0.4 million in the corresponding quarter last year and as compared with operating profit of NIS 20.2 million in the third quarter of the year. The increase in operating profit this quarter is primarily attributed to the sharp rise in gross profit of paper and recycling sector, as a result of the increase in sales and the manufacturing efficiency of the sector as a result of the operation of Machine 8, as mentioned above.

| e. | Financial Expenses |

Net financial expenses amounted to NIS 44.8 million in 2010, as compared with NIS 18.3 million in 2009.

The growth in financial expenses originated primarily as a result of the growth in financial expenses on account of long-term liabilities, that increased by approximately NIS 30.6 million relation to last year, mostly due to the cost of financing Series 3 and 4, whose discounting of financing costs for Machine 8 ended at the end of May, coupled with the issuing of bond series 5 (new series) in May. Moreover, an increase was recorded in financial expenses as a result of long-term loans assumed by a subsidiary for financing an investment in a corrugator.

9

| f. | Taxes on Income |

Tax revenues of NIS 3.0 million were recorded in 2010, as compared with tax revenues totaling NIS 7.1 million in 2009. The decrease in tax revenues this year, originating from a loss for tax purposes in the current operations, by comparison with the tax revenues last year, is primarily attributed to non-recurring tax revenues in the amount of NIS 8.6 million that were included in 2009, as a result of the decrease in the tax rate over the next several years.

| g. | Company’s Share in Earnings of Associated Companies |

The companies whose earnings are reported under this item (according to Hadera Paper’s holdings therein), include primarily: Hadera Paper Printing, Hogla Kimberly.

The company’s share in the earnings of associated companies totaled NIS 81.1 million in 2010, as compared with NIS 87.4 million last year.

The following principal changes were recorded in the Company’s share in the earnings of associated companies, in relation to the corresponding period last year:

| - | The Company's share in the net profit of Hadera Paper Printing (49.9%) in 2010 amounted to NIS 11.1 million as compared with NIS 14.1 million in 2009, a decrease of NIS 3.0 million. The decrease in the profit originated primarily from the decrease in the operating profit of Hadera Paper Printing, that decreased from NIS 40.5 million last year, to NIS 31.1 million this year. The decrease in operating profit in 2010 originated primarily from the sharp rise in the prices of raw materials in relation to last year, despite measures to raise prices in the course of the year and the improved gross margin of part of the product range. The decrease in net income was also affected by the growth in tax expenditures in the amount of NIS 6.7 million in 2010, as compared with last year, primarily as a result of recording tax revenues of approximately NIS 6 million last year as a result of the change in the tax rate, that were offset as a result of the reduction in financial expenses in the amount of NIS 9.7 million. |

| - | The Company's share in the net profit of Hogla Kimberly in Israel (49.9%) in 2010 amount to NIS 75.0 million as compared with NIS 83.0 million in 2009. The decrease in the sum of NIS 8.0 million, originated primarily from the decrease in operating profit from NIS 210.0 million to NIS 193.8 million this year. The decrease in the operating income is primarily attributed to the erosion of the selling prices in some sectors of operation, coupled with the rise in the prices of some principal inputs at the company, that were offset by far-reaching efficiency measures that were implemented across the company, continuing savings in purchasing and the strengthening of the company brands, led to a reduction in the erosion of earnings in 2010. |

10

| - | The Company's share in the losses of KCTR Turkey (49.9%) in 2010, amounted to NIS 2.7 million, as compared with NIS 7.6 million in 2009, representing a decrease of NIS 4.9 million. This reduction in loss, despite the slight decrease in the volumes of operation, is primarily attributed to the sale of the PEDO brand to a local chain, that generated non-recurring revenues of NIS 3.1 million in 2010, that brought about the continuing reduction in the net loss from NIS 15.1 million last year, to NIS 5.4 million in 2010. In addition, the loss was reduced as a result of recording of financial revenues from the valuation of operational balances. |

| h. | The Net Profit and the Earnings Per Share Attributed to the Company's Shareholders |

The net profit attributed to the Company's shareholders in 2010 amounted to NIS 100.7 million, as compared with net profit of NIS 91.2 million in 2009, representing an increase of 10.4%. The net profit, net of non-recurring revenues and expenditures during the reported period, amounted to approximately NIS 76.7 million, as compared with net profit, net of non-recurring revenues and expenditures in 2009, that amounted to NIS 59.2 million, representing an increase of 29.6%.

The net profit attributed to the Company's shareholders during the reported period was affected by the improvement in the operating margin of most Group companies in Israel as a result of the growth in operations that brought about an improvement in the operating profit, as mentioned above.

Basic earnings per share amounted to NIS 19.84 per share ($5.59 per share) in 2010, as compared with basic earnings per share of NIS 18.03 per share ($4.78 per share) in 2009.

Diluted earnings per share amounted to NIS 19.68 per share ($5.55 per share) in 2010, as compared with diluted earnings per share of NIS 18.03 per share ($4.78 per share) in 2009.

| 2. | Analysis of the Company's Financial Situation |

| · | The cash and cash equivalents item rose from NIS 26.3 million on December 31, 2009 to NIS 121.0 million on December 31, 2010. The increase in cash and cash equivalents originates primarily from the issuing of bond series 5 in the second quarter, that was invested in NIS deposits and is serving to finance the company's current operations. |

| · | The designated deposits in the sum of NIS 127.6 million on December 31, 2009 were utilized entirely in the course of 2010. The decrease in deposits originates as a result of the use of the designated deposit funds for the construction of Machine 8, between the reported years. |

| · | The increase in the accounts receivable item originates from the consolidation of the Hadera Paper Printing customers on December 31, 2010, in the amount of approximately NIS 175.6 million. In the packaging paper and recycling sector, an increase was recorded from NIS 81.2 million on December 31, 2009, to NIS 124.7 million on December 31, 2010. This increase is attributed to quantitative growth in activity in both local and export markets. In the packaging products and cardboard sector, a decrease was recorded in trade receivables, from NIS 199.4 million on December 31, 2009, to NIS 190.2 million on December 31, 2010, as a result of an increase in sales in this sector, coupled with an increase in the days of credit in some of the segments of operation in the sector. Trade receivables for the office supplies marketing sector rose from NIS 53.1 million as at December 31, 2009, to NIS 65.2 million, as at December 31, 2010, as a result of growth in the volume of operations. |

11

| · | Other receivables relating to the packaging paper and recycling segment decreased from NIS 92.1 million as at December 31, 2009, to NIS 43 million as at December 31, 2010. The decrease originates primarily from a reduction in credit/debit of inter-company balances as a result of the consolidation of Hadera Paper Printing on December 31, 2010 and the accounts payable balance that was consolidated and amounted to NIS 6.0 million. Other receivables relating to the packaging products and board sector decreased from NIS 5.1 million as at December 31, 2009, to NIS 4.5 million as at December 31, 2010. In the office supplies marketing segment, the other accounts receivable item increased from NIS 1.7 million on December 31, 2009, to NIS 3.6 million on December 31, 2010, primarily as a result of the increase in supplier advances. |

| · | The increase in the inventories item originates from the consolidation of the Hadera Paper Printing inventories on December 31, 2010, in the amount of approximately NIS 161.6 million. Inventories in the packaging paper and recycling sector decreased from NIS 91.1 million as at December 31, 2009, to NIS 76.2 million as at December 31, 2010. This increase is primarily attributed to utilizing the paper waste inventory as a result of the full operation of the new packaging paper manufacturing machine, following the completion of its running-in period. Inventories of the packaging products and board sector increased from NIS 68.5 million as at December 31, 2009, to NIS 79.1 million as at December 31, 2010. The increase is primarily attributed to the 7% rise in prices of raw materials in relation to last year. Inventories in the office supplies marketing sector rose from NIS 20.6 million as at December 31, 2009, to NIS 26.6 million, as at December 31, 2010, primarily as a result of growth in the inventories imported from the Far East. |

| · | The investment in associated companies decreased from NIS 340.1 million on December 31, 2009, to a sum of NIS 237.5 million on December 31, 2010. The principal components of the said decrease, include the consolidation of Hadera Paper Printing for the first time on December 31, 2010, which led to a decrease in investments of NIS 117.7 million, coupled with the company share in the dividend in distributed in the amount of NIS 47.4 million from associated companies and the company share in the declared dividend in the sum of NIS 2.5 million by an associated company, that were offset by the company share in the earnings of associated companies in the sum of NIS 70.1 million, between the reported years, that led to a decrease in investment between the reported years. |

| · | Short-term credit increased from NIS 131.6 million on December 31, 2009 to NIS 144.6 million on December 31, 2010. The growth in this item originates primarily as a result of the consolidation of the credit balances of Hadera Paper Printing on December 31, 2010, in the amount of NIS 92.9 million, that were offset as a result of the repayment of credit. |

12

| · | The growth in the other payables item originates primarily from the consolidation of the Hadera Paper Printing balances in the amount of NIS 23.7 million. In the packaging paper and recycling sector, growth was recorded from NIS 88.5 million as at December 31, 2009, to NIS 129 million as at December 31, 2010. The growth originated primarily as a result of a payable debt in the sum of NIS 49.4 million, on account of the purchase of Hadera Paper Printing. Other accounts payable of the packaging products and board sector increased from NIS 13.8 million as at December 31, 2009, to NIS 14.6 million as at December 31, 2010, primarily as a result of growth in debts to institutions on account of employees. Other accounts payable for the office supplies marketing sector decreased from NIS 5.8 million on December 31, 2009 to NIS 5.0 million on December 31, 2010. |

| · | The company’s shareholders' equity increased from NIS 858.4 million as at December 31, 2009 to NIS 953.6 million as at December 31, 2010. This change originated primarily from the net profit attributed to the company's shareholders between the periods, in the sum of NIS 100.7 million. |

| 3. | Investments in Fixed Assets |

| Investments in fixed assets amounted to NIS 219.1 million in 2010, as compared with NIS 352.5 million in 2009. The investments this year consisted primarily of payments on account of purchasing from equipment vendors for the new packaging paper manufacturing network (Machine 8), in the sum of NIS 96.3 million (including a decrease of NIS 43.8 million in supplier credit). The outstanding investment in Machine 8, true to December 31, 2010, amounts to NIS 702.3 million. Additional investments included were related to environmental protection (wastewater treatment) and current investments in equipment renewal, means of transportation and building maintenance at the Hadera site. |

| Regarding the examination of the need for impairment during the reported period, see Note 4c4 of the financial statements dated December 31, 2010, as well as the highly significant devaluation attached to the financial statements dated December 31, 2010. |

| 4. | Financial Liabilities The long-term liabilities (including current maturities) amounted to NIS 989.6 million as at December 31, 2010, as compared with NIS 847.6 million as at December 31, 2009. The long-term liabilities have increased in relation to last year primarily as a result of the issuing of a NIS-denominated bond series (Series 5) in the amount of NIS 181.5 million in the second quarter (see Note 10a(4) to the financial statements dated December 31, 2010), coupled with the assumption of long-term loans intended to finance the payments for Machine 8, as well as the consolidation of the long-term loans of Hadera Paper Printing in the amount of NIS 13.0 million. This increase was offset as a result of the repayment of the older debenture series, coupled with the cash flows from operating activities. The long-term liabilities include primarily four series of debentures and the following long-term bank loans: Series 2 – NIS 101.0 million, for repayment until 2013. Series 3 – NIS 179.8 million, for repayment until 2018. Series 4 – NIS 196.3 million, for repayment until 2015. Series 5 – NIS 181.5 million, for repayment until 2017. Long-term loans – NIS 331.8 million. |

13

| · | The balance of short-term credit, as at December 31, 2010, amounted to NIS 144.6 million, as compared with NIS 131.6 million as at December 31, 2009. |

| · | The net debt, as at December 31, 2010, net of the deposits and cash balance, amounted to NIS 1,013.2 million, as compared with net debt of NIS 825.3 million as at December 31, 2009. |

In July 2010 the Supervisor of the Capital Market, Insurance and Savings at the Ministry of Finance ("the Supervisor") published a circular which sets forth the Committee's recommendations for establishing parameters for institutional bodies' investments in non-government bonds. The circular, inter alia, includes provisions regarding the formulation of internal policies by institutional bodies prior to investing in bonds, the information required by such bodies to review and monitor investment in bonds, the mechanisms for cooperation between institutional bodies on certain matters relating to investment in bonds, the provisions that should be included in the bond documents as a condition for institutional bodies' investment therein and the requirement of institutional bodies to establish an investment policy (including with respect to rights to call in loans which would be included in the bonds), which addresses contractual criteria for the bonds and their various issuers. Most of the directives entered into force in October 2010. The memorandum of the Supervisor and the manner by which the recommendations are adopted as they appear in the report of the Committee, may hold implications on the ability to raise capital from institutional entities by way of bonds, including the terms and the price of raising such capital. As at the date of the reports the company is yet unable to identify these influences. |

| 5. | Financial liabilities at fair value through the statement of income Put Option to a Shareholder at an Associated Company For information pertaining to the Put option, see Note 17a to the annual financial statements dated December 31, 2010. Liability on account of the Put option to a shareholder at an associated company (investee until December 31, 2010), as at December 31, 2010 and as at December 31, 2009, is presented in the sum of NIS 31.5 million, and NIS 12.0 million, respectively. On account of the Put option, the associated company - until its consolidation on December 31, 2010 - other expenses of NIS 0.9 million were recorded in 2010, as compared with other expenses of NIS 1.9 million in 2009. The principal factors responsible for the change originated as a result of an agreement signed by the company for the acquisition of 25.1% of the shares of the associated companies ("Transaction Agreement") determining economic calculation of the value of the option and its blocking for three years. Regarding additional agreements arising from the transaction agreement and their potential impact on the terms of the option, see Note 17 to the financial statements dated December 31, 2010. |

14

C. | Liquidity |

| Cash Flows |

| The cash flows from operating activities in 2010 amounted to NIS 193.1 million, as compared with NIS 179.2 million in 2009. The growth in the cash flows from operating activities in 2010 in relation to last year, originated primarily from the growth in the earnings from operating activities, coupled with the company share in the dividends of associated companies, that was offset as a result of an increase in working capital this year in relation to last year, amounting to NIS 9.4 million, as compared with a decrease of approximately NIS 39.6 million last year. The increase in working capital this year originated primarily from an increase in the accounts receivable balances, an increase that was partially offset by the growth in the payable balances on account of a payable debt in the sum of NIS 49.4 million on account of the acquisition of control over Hadera Paper Printing. |

| The company possesses positive cash flows from operating activities, according to its interim consolidated financial statements dated December 31, 2010. However, the company's ongoing cash flows from operating activities in its separate financial statements, according to Regulation 38D of the Reporting Regulations ("Separate Financial Statements"), are negative. In light of the above, the company's Board of Directors conducted a discussion during its meeting on November 7, 2010, of Regulation 10(b)(14) to the Securities Regulations (Periodical and Immediate Reports) - 1970 ("Reporting Regulations") and determined that the ongoing negative cash flows from operating activities in the separate financial statements as at December 31, 2010, does not indicate a liquidity problem on the part of the company. This determination is based on an examination of the expected cash flows of the company and on the company's ability to raise additional credit, on the basis of an economic calculation performed by the company, and after having been presented to the Board of Directors and having the report of cash flows that is included in the company's separate financial statements discussed by the Board. |

| The data that served the Board of Directors as a basis for its estimation included the expected cash flows of the company for the next two years, based on the balance of cash and deposits as at the date of the report, totaling NIS 43.8 million held by the company, cash flows from operating activities in the sum of NIS 105 million in the coming year (approximately NIS 89.5 million in the following year), originating from company estimates regarding cash flows from revenues from operating activities, cash flows from dividends and the repayment of loans from investee companies. Cash flows created from investment activities totaling approximately NIS 9.9 million (net) in the coming year (approximately NIS 5 million that will serve for investment activities the following year), originating from the realization of real estate assets and an increase in holdings in investee and associated companies. The cash flows that will serve for financing activities, totaling approximately NIS 155 million in the coming year (approximately NIS 83.5 million in the following year), originating from the utilization of short-term credit, to serve for the repayment of loans plus interest, net. In addition to the above, the company is able to raise additional credit in the total sum of approximately NIS 280 million, also by way of recycling existing bank credit, for its continued operating activities and for making investments. |

15

| The information appearing above, including the expected cash flows, is based on the estimates, forecasts and plans of the company, according to the best of its knowledge and understanding regarding its operations and according to the data at its disposal as at the date of this report and which constitutes forward-looking information as defined in the Securities Law - 1968, whose materialization is not certain and whose realization is not exclusively under the control of the company. Consequently, there is no certainty that the data and/or estimates and/or forecasts and/or plans will materialize, in whole or in part, and they may materialize in a manner that is materially different than anticipated, inter alia, on account of the dependence upon external and macro-economic factors that are not subject to the control of the company, including changes in the business and defense environment, coupled with the materialization of any of the risk factors affecting the company. |

| D. | Details of Operations in the Various Sectors |

| 1. | Hogla-Kimberly (Household Products) |

The sales turnover of Hogla-Kimberly Israel amounted to approximately NIS 1,229.1 million in 2010, as compared with approximately NIS 1,237.6 million in 2009, representing a decrease of 0.7%.

The decrease in sales in relation to the corresponding period last year is primarily attributed to the erosion of prices as a result of escalating competition in the market.

The operating profit of Hogla-Kimberly Israel amounted to approximately NIS 193.8 million in 2010, as compared with approximately NIS 210.0 million in 2009.

The decrease in the operating profit in relation to the preceding year is attributed to the erosion of prices as a result of the escalating competition in the market, coupled with the rise in the prices of the principal raw materials, that was partially offset by efficiency measures that were implemented by the company, as well as of the decrease in the average US dollar exchange rate vis-à-vis the NIS, by a rate of approximately 5.1%, in relation to 2009.

The sales turnover of KCTR, Hogla-Kimberly’s subsidiary operating in Turkey, amounted to approximately NIS 498.2 million (approximately $132.6 million) in 2010, as compared with approximately NIS 493.6 million (approximately $127.7 million) last year, representing an increase of 0.9%.

KCTR’s strategic cooperation agreement with Unilever, under which Unilever carries out the selling, distribution and collection activities nationwide, with the exception of retail chains to which KCTR continues to sell independently, continues to expand the customer base in the reported period and to bring about the enhancement of the Huggies and Kotex brands.

In addition, it should be noted that toward the end of 2009, the Turkish tax authorities addressed KCTR as part of the examination of its financial statements for the years 2004-2008, conducted at KCTR on account of the taxation of the influx of capital from Hogla Kimberly Ltd. to KCTR. KCTR estimates, on the basis of the opinion of its legal and tax consultants, that the probability that it will be liable for an additional tax payment is low (See also Note 14.11 to the financial statements dated December 31, 2010).

The necessary funds for financing the strategic program in Turkey and for financing the current operations and investments, originate primarily from internal resources of Hogla Kimberly. (No investment was made in KCTR in 2010). The financial expenses this year were reduced as a result of an increase in financial incom as a result of the devaluation of operational balances, which contributed to an additional reduction in the net loss.

16

| 2. | Hadera Paper - Printing and Writing Paper (Formerly Mondi Hadera Paper) |

The sales turnover of Hadera Paper Printing amounted to NIS 728.7 million in 2010, as compared with NIS 669.2 million in 2009, representing an increase of 8.9%. The sales turnover of Hadera Paper Printing amounted to NIS 175.2 million in the fourth quarter of the year, as compared with NIS 157.3 million in the corresponding quarter last year, representing an increase of 11.4%.

The growth in the sales turnover, despite the quantitative decrease in sales, is primarily attributed to the raising of prices that was made in 2010. Prices in the local market grew by 11% in NIS terms in relation to last year. The course of the fourth quarter of 2010, the selling prices were eroded. Selling prices decreased by 5.5% in the fourth quarter, in relation to the third quarter of 2010, following escalating competition due to the widespread importing of paper into Israel.

The operating profit of Hadera Paper Printing amounted to NIS 31.1 million in 2010, as compared with NIS 40.5 million in 2009, representing a decrease of 23.2%. In the fourth quarter of 2010, the operating profit amounted to NIS 0.5 million, as compared with an operating profit of NIS 11.6 million in the fourth quarter of 2009 and as compared with operating profit of NIS 7.2 million in the third quarter of 2010.

The decrease in operating profit this year in relation to 2009, despite the rise in prices mentioned above, originated primarily as a result of the increase in the average pulp prices in 2010 in relation to 2009, in NIS terms, by a rate of approximately 43%. The decrease in the operating profit in the fourth quarter of 2010, in relation to the fourth quarter of 2009, originated from the increase in the average pulp prices as mentioned above, coupled with low operational efficiency in the fourth quarter of 2010, the relocation to the new logistics center in Modi'in and the decrease in the gross margin of the sale of purchase paper by Hadera Paper Printing.

A moderate decrease in pulp prices was recorded in the fourth quarter of 2010. Average pulp prices decreased by approximately 8.5% in NIS terms in the fourth quarter of the year, in relation to the third quarter of the year. This decrease did not result in an improved operating profit in the fourth quarter of 2010 in relation to the third quarter of the year, due to a greater erosion of selling prices as mentioned above, low operational efficiency, the relocation to the new logistics center in Modi'in and the decrease in the gross margin of the sale of purchase paper by Hadera Paper Printing.

| 3. | Carmel Container Systems - Packaging and Board Products |

The aggregate sales turnover of Carmel (including Frenkel CD) amounted to NIS 509.7 million in 2010, as compared with NIS 484.3 million last year, an increase of 5.2%.

In 2010, the consolidated sales turnover of Carmel Container Systems Ltd. amounted to NIS 397.3 million, as compared with NIS 383.0 million last year, an increase of 3.7%.

17

The consolidated sales turnover of Carmel Container Systems Ltd. amounted to NIS 113.9 million in the fourth quarter this year, as compared with NIS 99.7 million in the corresponding quarter last year, representing an increase of 14.2% and as compared with NIS 94.4 million in the third quarter this year.

The growth in sales turnover in 2010 as compared with 2009 originated primarily from a quantitative increase in sales of the corrugated board market, while maintaining a stable level of selling prices by comparison with 2009.

The consolidated operating profit of Carmel amounted to NIS 3.6 million in 2010, as compared with an operating profit of NIS 12.8 million last year. The decrease in the operating profit of Carmel is primarily attributed to the sharp rise of 7% in input prices, coupled with the eroded profitability of the Tri-Wall subsidiary. These influences were partially offset by the operational efficiency that was gained as a result of the reduction in stoppages and the greater output capacity. Moreover, in 2010, Carmel acquired a new processing machine that will serve to improve its output capacity and printing capability. These moves are expected to bring about an improvement in the profitability of Carmel over the next several quarters.

The consolidated operating profit of Carmel in the fourth quarter of 2010 amounted to NIS 2.4 million, as compared with an operating profit of NIS 5.9 million in the corresponding quarter in 2009 and as compared with an operating loss of NIS 0.4 million in the third quarter this year.

The aggregate operating profit of Carmel (including Frenkel CD) amounted to NIS 7.1 million in 2010, as compared with an operating profit of NIS 14.7 million last year.

Regarding the need to examine the impairment of the Carmel cash generating unit, see Note 8 to the financial statements dated September 30, 2010.

The above information pertaining to the output capacity and improved profitability of Carmel constitutes forward-looking information as defined in the Securities Law, based on the company's estimates at the date of this report. These estimates may not materialize - in whole or in part - or may materialize in a different manner, inter alia on account of factors that lie outside the control of the company, such as changes in local and global raw material prices and changes in the supply and demand of local and global cardboard packaging products.

| 4. | Packaging Paper and Recycling |

The sales turnover of the Packaging Paper and Recycling Division amounted to NIS 511.4 million in the reported period (NIS 581.4 million, net of the sales of Machine 8 totaling NIS 70 million that were discounted during its running in, until May 31, 2010), as compared with NIS 339.3 million last year, representing an increase of approximately 50.7%. The division’s sales turnover in the fourth quarter totaled NIS 170.0 million, as compared with NIS 88.3 million in the corresponding quarter last year, representing an increase of 92.5%, and as compared with NIS 152.0 million in the third quarter of the year.

The quantitative sales of packaging paper amounted to 214.3 thousand tons in 2010 (264.3 thousand tons net of sales totaling 50,000 tons that were discounted during the running-in of Machine 8), as compared with 141.9 thousand tons last year.

The sales of paper and cardboard waste by Amnir amounted to 355.5 thousand tons in 2010, as compared with 194.9 thousand tons last year.

18

The growth in the sales turnover originated primarily from the activation of Machine 8, starting in June this year. Moreover, as a result of the emergence from the economic crisis, an increase was recorded in the quantitative demand and in the selling prices, both of packaging paper and of paper waste at Amnir. The company also increased its export sales, as well as the sales of its new products, recycled paper that serves as a substitute for virgin paper.

The division ended 2010 with an operating profit of NIS 43.8 million, as compared with an operating loss of NIS 20.9 million last year. The cost of operating Machine 8, through to May 31, 2010, were discounted as part of the running-in expenses. The division’s operating profit in the fourth quarter of the year amounted to NIS 12.4 million, as compared with an operating loss of NIS 6.4 million in the corresponding quarter last year and an operating profits of NIS 21.1 million in the third quarter of the year, that included a non-recurring revenue of NIS 17.2 million. Net of the non-recurring revenue, the operating profits from current activities in the third quarter amounted to NIS 3.9 million.

The considerable improvement in operating profit in 2010, in relation to last year, is primarily attributed to the quantitative increase in sales as a result of the entry of Machine 8 into current operation, starting in June of this year, coupled with the raising of selling prices. The operating profit also included non-recurring earnings of approximately NIS 17.2 million from the sale of real estate in Bnei-Brak, in light of preparations being made by Amnir for the relocation into the logistic center at Modi'in.

| 5. | Graffiti - Office Supplies Marketing |

Graffiti's sales turnover during the reported period amounted to NIS 178.9 million, as compared with NIS 151.0 million in the corresponding period last year, representing an increase of 18.5%.

In 2010, Graffiti recorded an operating profit of NIS 5.1 million, as compared with an operating profit of NIS 4.0 million last year. The growth in the operating profit in 2010 is primarily attributed to the growth in sales that was offset as a result of the sharp rise in the cost of fine paper, at a rate of 14.1%.

Graffiti continues to implement its plan for growth in the marketing of office supplies to businesses and institutional clients and is taking several principal courses of action in order to establish its position as a leader in this market:

Graffiti is constantly working to improve the procurement network, with an emphasis on imports from the Far-East that will serve to significantly reduce purchasing costs, aiming to improve the gross and operating profitability.

Graffiti plans to relocate to a modern and efficient distribution center in Modi'in, that has already been occupied by Hadera Paper Printing and by Amnir in 2010, which will allow for realizing considerable savings in operational costs, while continuing to record growth in both sales and profitability. The relocation is planned for April 2011 and should last approximately 3 months. Graffiti will continue to operate its existing logistic centers during the transitional period, until the complete stabilization of the new logistic center at Modi'in.

Graffiti has completed the detailed specification of the computerized management systems of the logistic center and is currently working on constructing a detailed transition plan covering the various aspects, including: Planning the transfer of merchandise, recruiting supplier assistance for the move and communicating the relocation to the company customers.

Graffiti has successfully assimilated and implemented the Hadera Paper information systems during the reported period. This will allow the company to record accelerated growth and earnings while improving customer service, as modern systems and infrastructure are implemented at the new distribution center.

19

E. | Exposure and Management of Market Risks |

| 1. | General |

The Company conducts periodical discussions regarding market risks and exposure to exchange rate and interest rate fluctuations, with the participation of the relevant elements, so as to reach decisions in this matter. The individual responsible for the implementation of market risk management policy at the Company is Shaul Glicksberg, the Group's VP of Finance and Business Development.

| 2. | Market Risks to which the Company is Exposed |

Description of Market Risks

The market risks reflect the risk of changes in the value of financial instruments affected by changes in the interest rate, in the Consumer Price Index and in foreign currency exchange rates.

Exchange Rate Risks