INVESTOR PRESENTATION

June

Kaman Corporation

(Nasdaq: KAMNA)

2005

0

FORWARD-LOOKING STATEMENTS

This presentation may contain forward-looking information relating to the corporation's business and prospects, including aerostructures and helicopter

subcontract programs and components, advanced technology products, the SH-2G and K-MAX helicopter programs, the industrial distribution and

music businesses, operating cash flow, the benefits of the recapitalization transaction, and other matters that involve a number of uncertainties that may

cause actual results to differ materially from expectations. Those uncertainties include, but are not limited to: 1) the successful conclusion of

competitions for government programs and thereafter contract negotiations with government authorities, both foreign and domestic; 2) political

conditions in countries where the corporation does or intends to do business; 3) standard government contract provisions permitting renegotiation of

terms and termination for the convenience of the government; 4) economic and competitive conditions in markets served by the corporation,

particularly defense, commercial aviation, industrial production and consumer market for music products, as well as global economic conditions; 5)

satisfactory completion of the Australian SH-2G(A)program, including successful completion and integration of the full ITAS software; 6) receipt and

successful execution of production orders for the JPF U.S. government contract including the exercise of all contract options and receipt of orders from

allied militaries, as both have been assumed in connection with goodwill impairment evaluations; 7) satisfactory resolution of the EODC/University of

Arizona litigation; 8) achievement of enhanced business base in the Aerospace segment in order to better absorb overhead and general and

administrative expenses, including successful execution of the contract with Sikorsky for the BLACK HAWK Helicopter program; 9) satisfactory

results of negotiations with NAVAIR concerning the corporation's leased facility in Bloomfield, Conn.; 10) profitable integration of acquired businesses

into the corporation's operations; 11) changes in supplier sales or vendor incentive policies; 12) the effect of price increases or decreases; 13) pension

plan assumptions and future contributions; 14) continued availability of raw materials in adequate supplies; 15) satisfactory resolution of the supplier

switch and incorrect part issues at Dayron and the DCIS investigation; 16) cost growth in connection with potential environmental remediation activities

related to the Bloomfield and Moosup facilities; 17) successful replacement of the Corporation’s revolving credit facility upon its expiration in

November 2005; 18) risks associated with the course of litigation; 19) changes in laws and regulations, taxes, interest rates, inflation rates, general

business conditions and other factors; 20) the effects of currency exchange rates and foreign competition on future operations; and 21) other risks and

uncertainties set forth in Kaman's annual, quarterly and current reports, and proxy statements. Any forward-looking information provided in this release

should be considered with these factors in mind. The corporation assumes no obligation to update any forward-looking statements contained i

n this presentation.

Slide 1

1

Kaman intends to file with the Securities and Exchange Commission a Registration Statement on Form S-4, which will

contain a proxy statement/prospectus in connection with the proposed recapitalization. The proxy statement/prospectus will

be mailed to the stockholders of Kaman when it is finalized. STOCKHOLDERS OF KAMAN ARE ADVISED TO READ

THE PROXY STATEMENT/PROSPECTUS WHEN IT BECOMES AVAILABLE, BECAUSE IT WILL CONTAIN

IMPORTANT INFORMATION. Such proxy statement/prospectus (when available) and other relevant documents may also

be obtained, free of charge, on the Securities and Exchange Commission's website (http://www.sec.gov) or from Kaman by

contacting Russell H. Jones, SVP, Chief Investment Officer & Treasurer, by telephone at (860) 243-6307 or by email at rhj-

corp@kaman.com.

Kaman and certain persons may be deemed to be participants in the solicitation of proxies relating to the proposed

recapitalization. The participants in such solicitation may include Kaman's executive officers and directors. Further

information regarding persons who may be deemed participants will be available in Kaman's proxy statement/prospectus to

be filed with the Securities and Exchange Commission in connection with the proposed recapitalization.

FORWARD-LOOKING STATEMENTS, continued

Slide 2

2

Corporate Profile

Aerostructures: Produces aircraft structures and components for commercial

and military aircraft

Fuzing: Produces specialized missile and bomb fuzing for U.S. and allied militaries

Helicopters: Markets and supports the SH-2G Super Seasprite maritime helicopter

and K-MAX medium to heavy lift helicopter

Kamatics Bearings: Produces widely used proprietary aircraft bearings and

components for commercial and military programs

Kaman is one of the nation’s larger distributors of power transmission, motion control, material handling

and electrical components and a wide range of bearings.

Products and value-added services are offered to a customer base of more than 50,000 companies

Representing a highly diversified cross-section of North American industry.

Kaman is the largest independent distributor of musical instruments and accessories,

offering more than 17,500 products for amateurs and professionals.

Proprietary products include Adamas ®, Ovation ®, Takamine ®, and Hamer® guitars;

and Latin Percussion® and Toca® hand percussion instruments, Gibraltar® percussion hardware and

Gretsch ® professional drum sets.

AEROSPACE

INDUSTRIAL

DISTRIBUTION

MUSIC

Slide 3

3

Corporate Profile

2004 SALES

Slide 4

Percent Millions $

4

Aerospace

25%

$252.2

Industrial Distribution

59%

581.9

Music

16%

161.0

100.0%

$995.2

KEY INVESTMENT CONSIDERATIONS

Diversified revenue stream with mix of industrial, consumer

and military business

Strong and diverse customer base across each segment

Strong management team with extensive management experience

Industrial Distribution and Music segments follow well-established

economic models

Solid financial position

Unbroken dividend stream for over 30 years, with a 13.6% increase

announced recently

Proposed one share/one vote recapitalization

Kaman Corporation

Slide 5

5

STRATEGIES

Aerospace

SEGMENT OVERVIEW

Slide 6

6

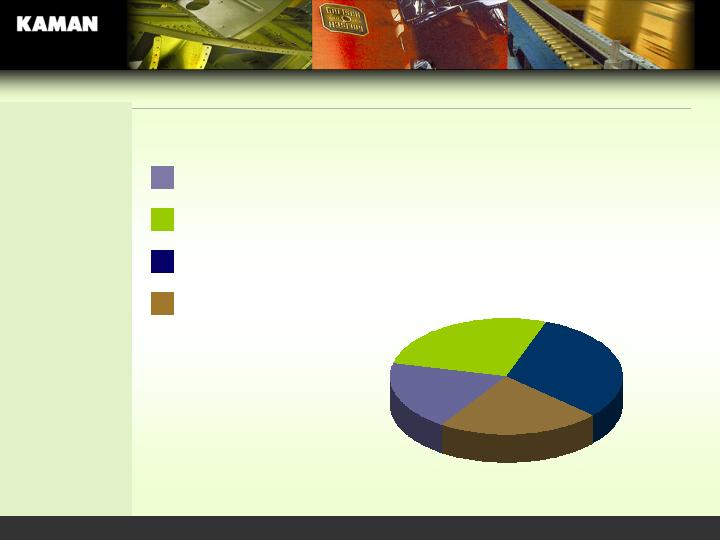

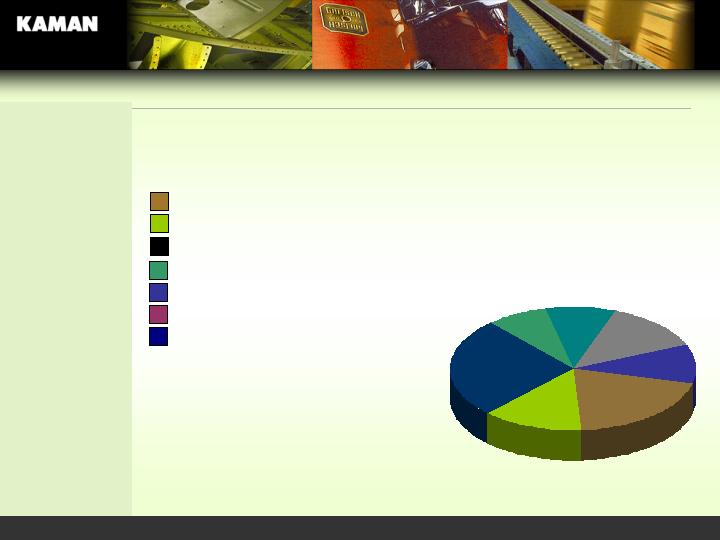

AEROSPACE OPERATING UNITS

Aerospace

Slide 7

t

t

t

t

18%

22%

29%

31%

Aerostructures

Fuzing

Helicopters

Kamatics

7

AEROSTRUCTURES DIVISION

Operations in Jacksonville, FL and Wichita, KS

Area of strategic emphasis for the Company, particularly in military assembly

and detail work

Transition of production facilities from Moosup, CT to Jacksonville, FL

in its later stages, and the plant has shifted from losses to beginnings of

profitability with significant new contract for production of Sikorsky

BLACKHAWK helicopter cockpits

Market conditions have improved: industry aircraft orders have increased

Domestic competitors include Vought, GKN, Ducommun and Middle River

Aerospace

Slide 8

Produces parts and subassemblies for various

customers, including:

Military programs such as the Boeing C-17

military transport (approx. $1.1 million per

shipset) and Sikorsky BLACKHAWK

helicopter cockpits (approximately $300

thousand per ship set)

Commercial programs such as the Boeing 737 (approximately $1.5

million annually, and 767 and 777 (approx. $170 and $190

thousand/ship set)

8

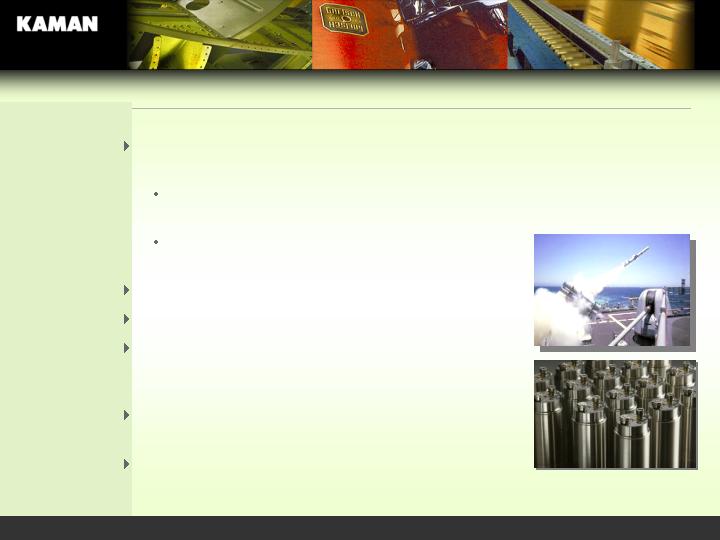

FUZING DIVISION

Manufactures safe, arm and fuzing devices for a number of

major missile and bomb programs

Missile programs include: AMRAAM, ATACMS, Brimstone, M-100 Hawk,

Harpoon, JASSM, Maverick, SLAM-ER, Standard and Tactical Tomahawk

Bomb programs include: Joint Programmable Fuze

FMU143, FMU139, 40mm and others

$500 million market

Operations in Middletown, CT and Orlando, FL

Principal customers the U.S. Army,

U.S. Air Force, U.S. Navy, Boeing,

General Dynamics, Lockheed Martin and Raytheon

Ramping up capabilities for production of the

152 A/B Joint Programmable Fuze

Competitors include ATK, L-3 and others

Aerospace

Slide 9

9

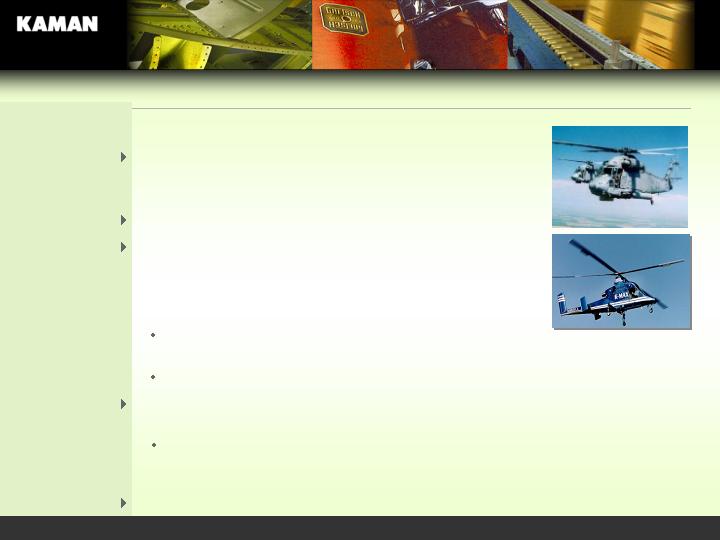

HELICOPTERS DIVISION

The majors are moving away from manufacturing to final assembly and

systems integration, providing opportunities for Kaman

Kaman is on the winning team for the US101 presidential helicopter

Principals customers include the governments of Australia, Egypt, New

Zealand and Poland; the U.S. Department of State and others

Helicopters are expected to return at 10-year service intervals for standard depot level

maintenance. Five-year program of approx. $30 million expected with Egypt. First

aircraft has arrived.

Program for Australia, in loss position, is moving toward completion

Aerospace

Slide 10

Markets and supports Kaman-made SH-2G(A)

Super Seasprite maritime helicopter and K-MAX

“Aerial Truck” helicopter

Primary operations in Bloomfield, CT

The domestic market has consolidated into

three large players: Boeing, Sikorsky and

Bell. The international market is dominated

by Agusta Westland and Eurocopter

10

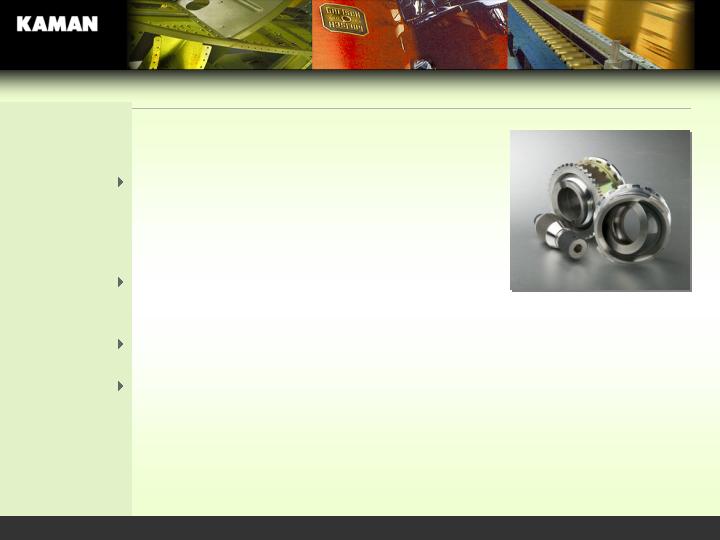

KAMATICS SUBSIDIARY

Manufactures proprietary self-lubricating

bearings for OEM and MRO use in nearly all

military and commercial aircraft produced

in North and South America and Europe.

Leader in product performance and

applications engineering support

Operations are in Bloomfield, CT and Dachsbach Germany

Key customers include: U.S. and allied militaries (32% of 2004 sales), and

commercial accounts with Boeing, Airbus, Embraer, Bombardier and others

(68% of sales). Largest customer represents 18% of 2004 sales, down from

43% in 1998.

Aerospace

Slide 11

11

STRATEGIES

Expand the aerostructures subcontract, fuzing products, and proprietary

aircraft bearings businesses through increased sales and marketing efforts and

strategic acquisitions

Pursue additional SH-2G opportunities in the international niche market for

intermediate-size maritime helicopters

Further deploy ‘lean thinking’ to improve manufacturing performance and

reduce costs

Aerospace

Slide 12

12

STRATEGIES

Industrial Distribution

SEGMENT OVERVIEW

Slide 13

13

Third largest player in highly fragmented $12 billion market

Provides more than one million products to more than 50,000 MRO and

OEM customers

Serves a broad cross section of North American Industry in 70 of the top

100 U.S. industrial markets

Nearly 200 locations in the U.S., Canada and Mexico

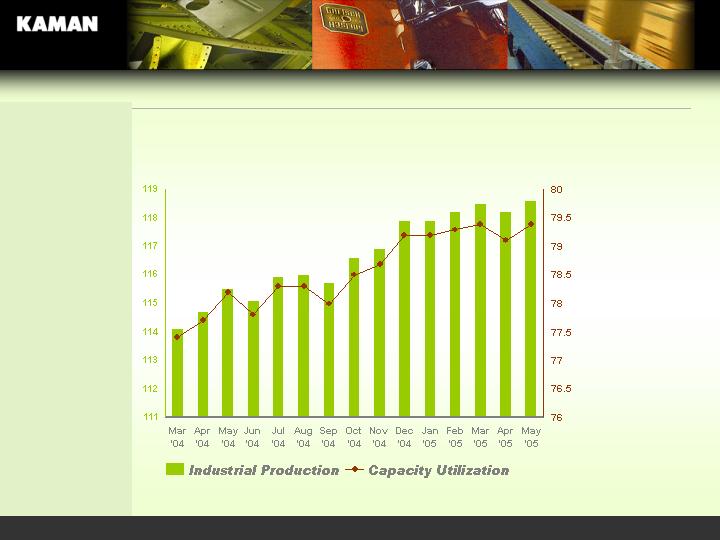

The business tends to closely track the U.S. Industrial Production and

Capacity Utilization Indices

Industrial Distribution

Slide 14

14

Industrial Distribution

$12 BILLION ESTIMATED DISTRIBUTION MARKET:

U.S. POWER TRANSMISSION/MOTION CONTROL DISTRIBUTION

BY PRODUCT LINE

Slide 15

Industry Kaman

Industry by Product Line

15

Fluid Power

Bearings

Power Transmission

Accessories

Material Handling

Electrical

Linear

20%

8%

13%

29%

27%

26%

8%

9%

9%

11%

13%

12%

10%

5%

Industrial Distribution

PORTFOLIO OF RECOGNIZED BRANDS

Slide 16

16

Industrial Machinery

Food & Kindred Products

Stone, Aggregate & Cement

Paper & Allied Products

Primary Metal Industries

Fabricated Metal Products

Chemicals (incl. Pharmaceuticals)

Electronic & Electric Products

Nonmetallic Minerals, except Fuel

Instruments & Related Products

Industrial Distribution

PERCENT SALES TO TOP 10 CUSTOMER INDUSTRIES

Slide 17

18%

10%

6%

5%

4%

3%

3%

3%

3%

3%

58%

17

FRB INDICES OF INDUSTRIAL PRODUCTION

AND CAPACITY UTILIZATION

Industrial Distribution

Source: Federal Reserve Board

Slide 18

18

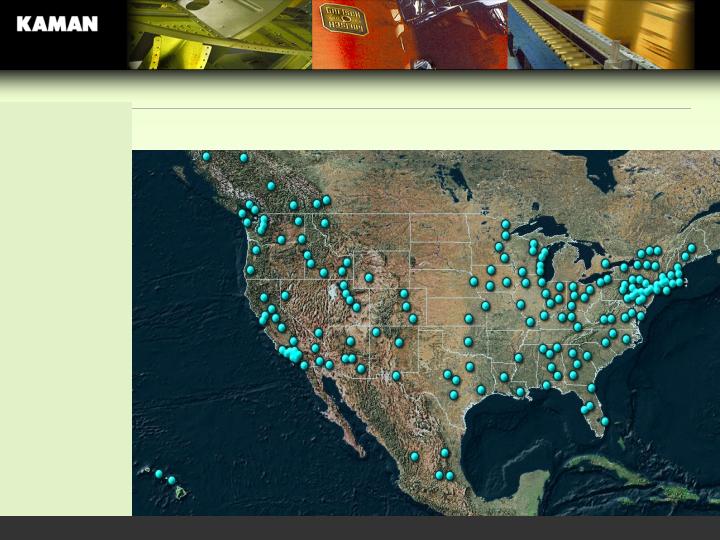

Insert Updated Map

GEOGRAPHICAL COVERAGE

Industrial Distribution

Slide 19

19

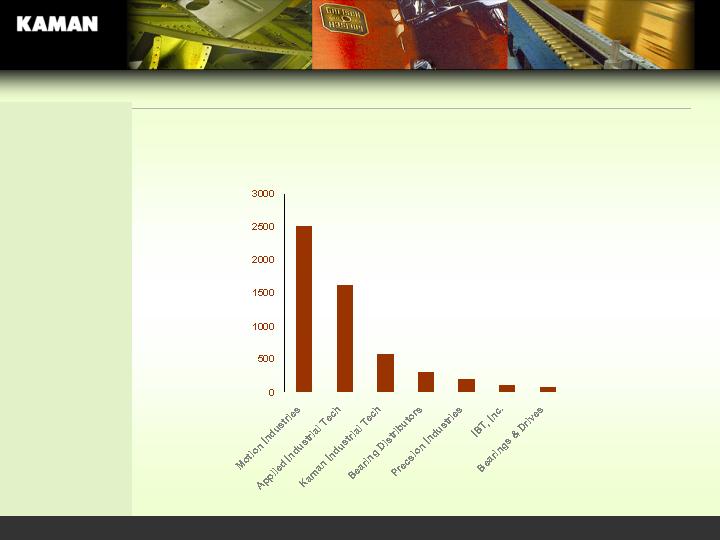

Industrial Distribution

2004 ACTUAL OR ESTIMATED SALES OF TOP DISTRIBUTORS

(AMOUNTS IN $MILLIONS)

Slide 20

Source: Public filings and Industrial

Distribution Magazine

20

STRATEGIES

Expand geographic coverage in major industrial markets

that increase Kaman’s ability to compete for regional and

national accounts

Provide industry leadership in e-commerce initiatives

Further enhance operating and asset utilization efficiencies throughout the

enterprise

Industrial Distribution

Slide 21

21

STRATEGIES

Music

SEGMENT OVERVIEW

Slide 22

22

Largest independent distributor of musical

instruments and accessories in the $7.0 billion

U.S. musical instrument market

Provides over 17,500 products: Proprietary

lines to the large retail chains, and the full

catalogue to the smaller regional and local

stores

Strategically located distribution centers cover the

U.S. and Canadian markets

U.S. and Asian manufacturing supports our

proprietary and licensed brands of premium products

Leads the market in use of technology, providing systems to service customers at all

levels

Market is driven by consumer sentiment with the “Back-to-School” and Christmas

seasons being important indicators

Music

Slide 23

23

Music

PORTFOLIO OF PREMIER BRANDED PRODUCTS

Slide 24

24

Accessories

Percussion

Fretted

t

t

t

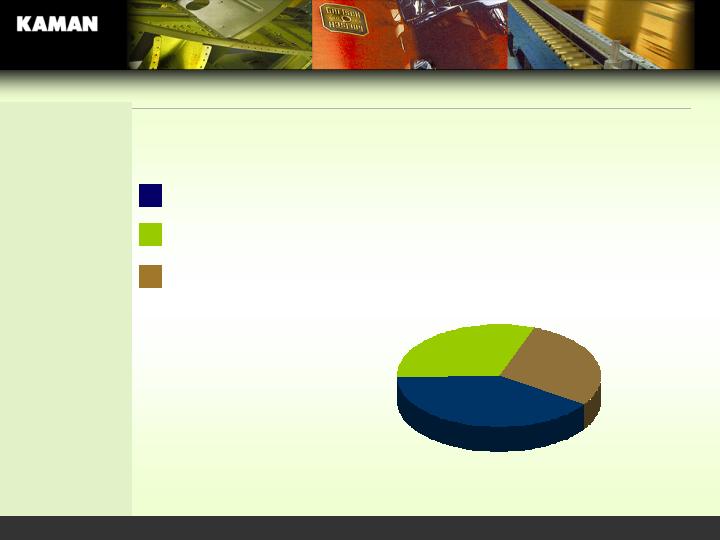

MUSIC BUSINESS MIX:

DIVERSIFICATION BY MAJOR PRODUCT TYPE

Music

Slide 25

40%

31%

29%

25

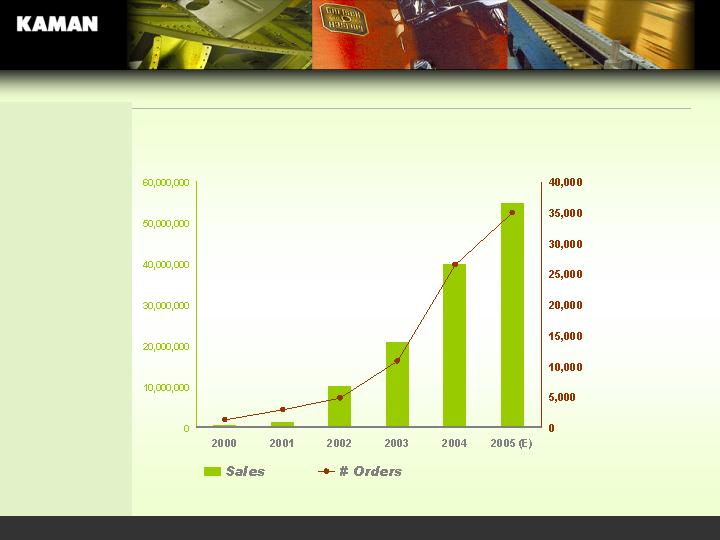

E-COMMERCE SALES HISTORY

Source: Federal Reserve Board

Slide 26

$

Music

26

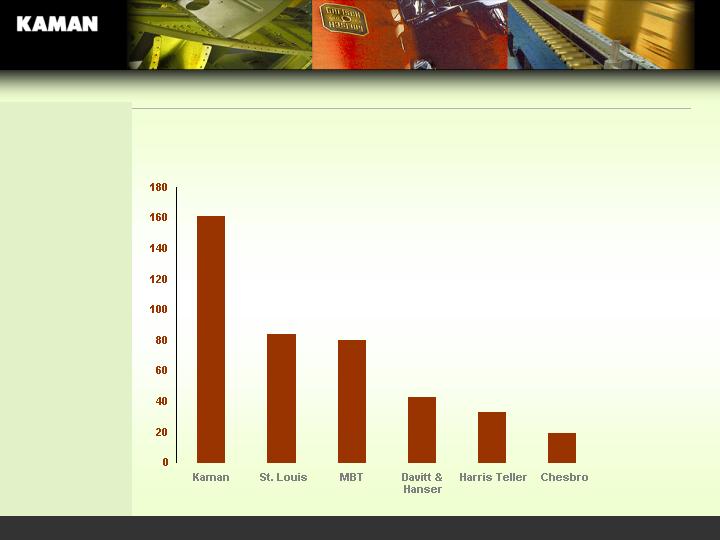

KAMAN MUSIC 2004 ESTIMATED SALES OF

TOP INDEPENDENT DISTRIBUTORS

(AMOUNTS IN MILLIONS)

Slide 27

Source: Music Trades Magazine

Music

27

STRATEGIES

Preserve Kaman’s leadership position as the largest

independent distributor of musical instruments and accessories

Build on Kaman’s strong brand identity while adding

new market-leading names to the Corporation’s offering

of proprietary products

Lead the market with distribution systems and technologies

that add value and reduce costs for customer, supplier and

the Corporation

Music

Slide 28

28

Financial Review

Slide 29

29

KAMAN CORPORATION AND SUBSIDIARIES NET SALES

Financial Overview

2005

$12.9

$12.7

17.1

23.0

$65.7

156.0

41.6

$263.3

2004

$10.7

8.9

19.9

19.8

$59.3

145.6

40.3

$245.2

2004

$45.3

56.7

73.2

77.1

$252.2

581.9

161.0

$995.2

2003

$43.1

45.1

97.1

65.9

$251.2

497.9

145.4

$894.5

NET SALES ($ in Millions)

Aerospace

Aerostructures

Fuzing

Helicopters (incl. EODC)

Kamatics/RWG

Industrial Distribution

Music

Total

YEAR ENDED FIRST QUARTER

Slide 30

30

KAMAN CORPORATION AND SUBSIDIARIES EBIT/EBITDA

Financial Overview

Q1 ’05

$7.6

8.5

2.6

18.7

—

(9.5)

9.2

11.2

Q1 ’04

$3.0

5.0

2.0

10.0

—

(6.7)

3.3

5.1

2004

(14.3)

19.3

11.1

16.1

0.2

(28.8)

(12.5)

(4.6)

2003

$ 14.8

12.7

9.5

37.0

18.2

(19.1)

$ 36.1

$ 44.9

EBIT/EBITDA ($ in Millions)

Aerospace

Industrial Distribution

Music

Total Segment Operating Profit

Net Gain on Sale of Product Lines and

Other Assets

Corporate Expense

Total Operating Profit/Loss

EBITDA

Slide 31

31

2004 EARNINGS ADJUSTMENTS - AEROSPACE

$20.1 million

7.1 million

2.0 million

5.5 million

3.5 million

3.4 million

$41.6 million Total

Financial Overview

Slide 32

Elimination of investment in contracts with MD Helicopters

Adjustment to Boeing Harbour Pointe contract

Severance in connection with realignment of Aerospace

management team

Increased accrued contract costs associated with completion

of Australia SH-2G (A) program

Product warranty issues at Dayron

Adjustment to EODC contract

32

KAMAN CORPORATION

13.3%

$7,539

$9,979

18.4%

$1,098

$2,504

Debt as % of capital

Capital Expenditures

Dividends

$284,170

$287,320

Shareholders’ equity

$43,405

$64,604

Bank Debt & Debentures

$224,230

$228,381

Working capital

226,105

236,619

Current liabilities

$450,335

$465,000

Current assets

As of December 31, 2004

As of April 1, 2005

Financial Overview

Slide 33

33

KEY INVESTMENT CONSIDERATIONS

Diversified revenue stream with mix of industrial, consumer

and military business

Strong and diverse customer base across each segment

Strong management team with extensive management experience

Industrial Distribution and Music segments follow well-established

economic models

Solid financial position

Unbroken dividend stream for over 30 years, with a 13.6% increase

announced recently

Proposed one share/one vote recapitalization

Kaman Corporation

Slide 34

34