UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2007

Commission File No. 0-1093

KAMAN CORPORATION

(Exact name of registrant as specified in its charter)

| | |

| Connecticut | | 06-0613548 |

(State or other jurisdiction of incorporation or organization) | | (I.R.S. Employer Identification No.) |

1332 Blue Hills Avenue

Bloomfield, Connecticut 06002

(Address of principal executive offices)

Registrant’s telephone number, including area code: (860) 243-7100

Securities registered pursuant to Section 12(b) of the Act:

| | | | |

| Title of each class | | | | Name of each exchange on which registered |

Common Stock ($1 par value) | | | | The NASDAQ Stock Market, Inc. |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes x No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (Section 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated herein by reference in Part III of this Form 10-K or any amendment to this Form 10-K ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See definitions of “large accelerated filer”, “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer x Accelerated filer ¨ Non-accelerated filer ¨ Smaller reporting company ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

The aggregate market value on June 29, 2007 (the last business day of the Company’s most recently completed second quarter) of the voting common stock held by non-affiliates of the registrant, computed by reference to the closing price of the stock, was approximately $744,806,447.

At February 1, 2008, there were 25,178,586 shares of Common Stock outstanding.

Documents Incorporated Herein By Reference

Portions of our definitive proxy statement for our 2008 Annual Meeting of Shareholders are incorporated by reference into Part III of this Report.

Kaman Corporation

Index to Form 10-K

Year Ended December 31, 2007

2

PART I

ITEM 1. BUSINESS

Kaman Corporation, headquartered in Bloomfield, Connecticut, was incorporated in 1945. We are a diversified company that conducts business in the aerospace and industrial distribution markets. The company reports information for itself and its subsidiaries (collectively, the “company”) in five business segments. They are Industrial Distribution and four reporting segments within the aerospace industry: Aerostructures, Fuzing, Helicopters, and Specialty Bearings (collectively, the “Aerospace Segments”).

The combined Aerospace Segments consist primarily of the following operating subsidiaries: Kaman Aerospace Corporation (KAC), Kamatics Corporation, Kaman Dayron, Inc. (Dayron), Plastic Fabricating Company, Inc. (PlasticFab), and RWG Frankenjura-Industrie Flugwerklager GmbH (RWG). Kaman Aerospace Corporation is our principal business unit. Kamatics was established in 1966 as a maker of specialty aircraft bearings. PlasticFab was acquired in 2001, while Kaman Dayron and RWG Bearings were acquired in 2002. In 2005, we realigned KAC and created separate divisions to provide a more focused organizational structure, separating the operating units that were subject to larger prime contractor overheads from the other operating units. The divisions of Kaman Aerospace Corporation are Aerostructures, Fuzing and Helicopters.

A discussion of 2007 developments is included in Item 7, Management’s Discussion and Analysis of Financial Condition and Results of Operations.

Aerostructures Segment

The Aerostructures segment has been a supplier of commercial and military aircraft structures and subsystems for over 50 years. Our product portfolio currently consists of metallic and composite detail parts, minor and major subassemblies, flight control surfaces, composite interiors and fuselage and wing structures. Our service offerings range from build-to-print manufacturing, to major structural assembly, to full production integration, including procurement and installation of wiring and sub-systems. We currently perform work on many major commercial and military platforms including the Boeing 767, 777 & 787, the Boeing C-17 and the Sikorsky UH-60. Work for Boeing and Sikorsky comprised 87.8% of total segment sales in 2007. Other customers include Bell Helicopter, Spirit AeroSystems and Shenyang Aircraft Corporation. Operations are conducted in Jacksonville, FL and at our PlasticFab facility in Wichita, KS.

We have made, and continue to make, strategic investments in composite technology and machining capabilities. This combined with the expansion of our supply chain and program management organizations as well as a commitment to achieving operational excellence allows us to offer our customers an integrated solution offering for their aerostructures needs.

Fuzing Segment

The Fuzing segment, which includes Dayron’s operations, manufactures products for military and commercial markets, primarily related to military safe, arm and fuzing devices for several missile and bomb programs; as well as precision non-contact measuring systems for industrial and scientific use; and high reliability memory systems for airborne, shipboard, and ground-based programs. One of the key programs of the Fuzing segment is the Joint Programmable Fuze (FMU-152 A/B) used in the MK80 series bombs, BLU-109 and in conjunction with JDAM and Paveway weapon kits.

Our capabilities include the design, development, test and manufacture of fuzing products. Our year round test facility is equipped with projectile velocity measurement equipment, projectile impact media, high-speed photographic equipment and lighting for night firing and tests. We are forward-looking and growth-oriented,

3

pursuing and applying innovations in development and manufacturing technology. Our vision to grow employs organic resources, teaming, co-development and co-production relationships with other qualified companies and government and university research agencies.

Principal customers include the U.S. military, Boeing, Lockheed Martin and Raytheon. Operations are conducted at the Middletown, Connecticut; Orlando, Florida; and Tucson, Arizona facilities.

Helicopters Segment

The Helicopters segment, with our manufacturing capabilities and highly experienced people, markets our helicopter engineering expertise and performs subcontract work for other prime aerospace manufacturers. This includes the designing, testing, certifying, and delivery of major assemblies, complex components, subassemblies, and detail parts. We also refurbish, provide upgrades for and otherwise support Kaman SH-2G maritime helicopters operating with foreign militaries. Our K-MAX® “aerial truck” helicopter is used to perform repetitive external lifting and is operated by commercial customers in several countries. The SH-2G aircraft is currently in service with the Egyptian Air Force and the New Zealand and Polish navies. Operations are primarily conducted at the Bloomfield, Connecticut facility.

Our two largest programs currently are for the Royal Australian Navy and the Egyptian Air Force. These programs constituted approx 47.6% of total 2007 segment sales.

Specialty Bearings Segment

The Specialty Bearings segment, which includes Kamatics’ and RWG’s operations, manufactures high-performance mechanical products used in aviation, marine, hydropower, and other industrial applications. These products are used as original equipment and/or specified as replacement parts by the manufacturers of nearly every military and commercial aircraft manufactured in North and South America and Europe. Our engineering services are available for unique high performance applications requiring innovation and advanced technology. We operate in highly automated manufacturing facilities that allow us to produce our products reliably and efficiently. These products are primarily proprietary self-lubricated bearings for aircraft flight controls, turbine engines, and landing gear; driveline couplings for helicopters; self-lubricated bearings for hydropower installations, ships and submarines; and composite “flyer bows” used in the wire industry. The range of Specialty Bearings’ products includes:

| | • | | KAron® Bearings - self-lubricating bearings for aircraft and marine use; |

| | • | | FraSlip® Bearings - self-lubricating bearings for aircraft and industrial use; |

| | • | | KAron® Hydropower Bearings - ideally suited for demanding hydropower applications; |

| | • | | KAflex® Couplings - driveshafts and couplings used in helicopters; and |

| | • | | Composite Flyer Bows - high-strength processing devices for the wire making industry including the Back Bone Bow®. |

The Specialty Bearings segment also manufactures proprietary custom designed and manufactured rolling element and plain bearings for aerospace applications.

Operations for the Specialty Bearings segment are conducted at the Bloomfield, Connecticut and Dachsbach, Germany facilities.

Industrial Distribution Segment

Kaman Industrial Technologies brings our commitment to technological leadership and value-added services to the Industrial Distribution business. The Industrial Distribution segment is the third largest power transmission/motion control industrial distributor in North America. We provide products including bearings, mechanical and electrical power transmission, fluid power, motion control and materials handling components to a broad

4

spectrum of industrial markets throughout North America. Locations consist of nearly 200 branches, distribution centers and call centers across the United States and in Canada and Mexico. We offer approximately three million items, as well as value-added services, to a base of approximately 50,000 customers representing a highly diversified cross-section of North American industry.

Divestiture of the Music Segment

On December 31, 2007, we completed the previously announced sale of all of the capital stock of our wholly owned subsidiary, Kaman Music Corporation, to Fender Musical Instruments Corporation (“FMIC” or “Fender”). Pursuant to the terms of the stock purchase agreement, as amended, we received $119.5 million in cash, which includes the purchase price of $117.0 million and certain working capital and cash adjustments made at closing as set forth in the stock purchase agreement. The purchase price is subject to additional specified post closing purchase price adjustments. As of our third quarter 2007 Form 10-Q, the segment qualified for discontinued operations presentation. As a result, in this report we have presented the results of operations and consolidated financial position of this segment as discontinued operations within the consolidated financial statements for all periods presented.

FINANCIAL INFORMATION ABOUT OUR SEGMENTS

Financial information about our segments is included in Item 7, Management’s Discussion and Analysis of Financial Condition and Results of Operations, and Note 19, Segment and Geographic Information, of the Notes to Consolidated Financial Statements, included in Item 8, Financial Statements and Supplementary Data, of this Annual Report on Form 10-K.

PRINCIPAL PRODUCTS AND SERVICES

The following is information for the three preceding years concerning the percentage contribution of each business segment’s products and services to the company’s consolidated net sales:

| | | | | | |

| | | Years Ended December 31, |

| | | 2007 | | 2006 | | 2005 |

Aerostructures | | 9.4% | | 7.9% | | 6.1% |

Fuzing | | 8.1% | | 7.2% | | 7.0% |

Helicopters | | 6.6% | | 7.1% | | 8.4% |

Specialty Bearings | | 11.4% | | 10.7% | | 10.1% |

| | | | | | |

Subtotal Aerospace | | 35.5% | | 32.9% | | 31.6% |

Industrial Distribution | | 64.5% | | 67.1% | | 68.4% |

| | | | | | |

Total | | 100.0% | | 100.0% | | 100.0% |

| | | | | | |

AVAILABILITY OF RAW MATERIALS

While we believe we have sufficient sources for the materials, components, services and supplies used in our manufacturing, we are highly dependent on the availability of essential materials, parts and subassemblies from our suppliers and subcontractors. The most important raw materials required for our aerospace products are aluminum (sheet, plate, forgings and extrusions), titanium, nickel, copper and composites. Many major components and product equipment items are procured or subcontracted on a sole-source basis with a number of domestic and non-U.S. companies. Although alternative sources generally exist for these raw materials, qualification of the sources could take a year or more. We are dependent upon the ability of a large number of suppliers and subcontractors to meet performance specifications, quality standards and delivery schedules at anticipated costs. While we maintain an extensive qualification system to control risk associated with such

5

reliance on third parties, failure of suppliers or subcontractors to meet commitments could adversely affect production schedules and contract profitability, while jeopardizing our ability to fulfill commitments to our customers. Although recent high prices for some raw materials important to some of our businesses (steel, copper, aluminum, titanium and nickel) have caused margin and cost pressures, we do not foresee any near term unavailability of materials, components or supplies that would have an adverse effect on our business, or on any of our business segments. For further discussion of the possible effects of changes in the cost or availability of raw materials on our business, see Item 1A, “Risk Factors” in this Form 10-K.

PATENTS AND TRADEMARKS

We hold patents and trademarks reflecting functional, design and technical accomplishments in a wide range of areas covering both basic production of certain aerospace products as well as highly specialized devices and advanced technology products in defense related and commercial fields.

Although the company’s patents and trademarks enhance our competitive position, we believe that none of such patents or trademarks is singularly or as a group essential to our business as a whole. We hold or have applied for U.S. and foreign patents with expiration dates that range through the year 2025.

Registered trademarks of Kaman Corporation include KAflex, KAron, and K-MAX. In all, we maintain 24 U.S. and foreign trademarks.

BACKLOG

Our entire backlog is attributable to the Aerospace Segments. We anticipate that approximately 66.1% of our backlog at the end of 2007 will be performed in 2008. Approximately 57.0% of the backlog at the end of 2007 is related to U.S. Government contracts or subcontracts, which are included in backlog to the extent that the government orders are firm but not yet funded or contracts that are awarded but not yet signed. Virtually all of these government contracts or subcontracts have been signed.

Total backlog, the portion of the backlog we expect to complete in 2008, and the portion of the backlog represented by U.S. Government contracts for each of the Aerospace Segments, are as follows:

| | | | | | | | | | | | | | | |

| In thousands | | Total Backlog at

December 31,

2007 | | 2007 Backlog to

be completed in

2008 | | % U.S.

Government | | | Total Backlog at

December 31,

2006 | | Total Backlog at

December 31,

2005 |

Aerostructures | | $ | 130,598 | | $ | 100,404 | | 83.3 | % | | $ | 84,178 | | $ | 109,347 |

Fuzing | | | 140,872 | | | 89,641 | | 98.6 | % | | | 169,742 | | | 91,717 |

Helicopters | | | 106,269 | | | 40,595 | | 10.0 | % | | | 116,028 | | | 103,605 |

Specialty Bearings | | | 96,790 | | | 83,234 | | 12.6 | % | | | 80,646 | | | 69,217 |

| | | | | | | | | | | | | | | |

Total | | $ | 474,529 | | $ | 313,874 | | 57.0 | % | | $ | 450,594 | | $ | 373,886 |

| | | | | | | | | | | | | | | |

GOVERNMENT CONTRACTS

During 2007, approximately 92.2% of the work performed by the company directly or indirectly for the U.S. government was performed on a fixed-price basis and the balance was performed on a cost-reimbursement basis. Under a fixed-price contract, the price paid to the contractor is negotiated at the outset of the contract and is not generally subject to adjustment to reflect the actual costs incurred by the contractor in the performance of the contract. Cost reimbursement contracts provide for the reimbursement of allowable costs and an additional negotiated fee.

The company’s U.S. government contracts and subcontracts contain the usual required provisions permitting termination at any time for the convenience of the government with payment for work completed and associated profit at the time of termination.

6

COMPETITION

The reporting segments within the aerospace industry operate in a competitive environment with many other domestic and foreign organizations and are also affected by the political and economic circumstances of their potential foreign customers.

The Aerostructures segment competes for aircraft structures and components business on the basis of price, product quality, and our past performance. Competitors for this business range from small machine shops, to Tier I suppliers such as Spirit Aerosystems, and offshore competitors.

The Fuzing segment competes for its business primarily on the basis of technical competence, product quality, price, its experience as a developer and manufacturer of such products for particular applications and the availability of facilities, equipment and personnel.

The Helicopters segment competes on the basis of price, performance, its experience as a manufacturer of helicopters, the quality of its products and services, and the availability of facilities and equipment to perform subcontract services.

The Specialty Bearings segment competes for its specialty aircraft bearing business based on quality and proprietary knowledge, product endurance, delivery lead-time, and special performance characteristics.

The Industrial Distribution segment competes for business with several other national distributors, two of which are substantially larger, and with many regional and local organizations. In addition, we compete with low-cost industrial products manufactured off shore and introduced into the U.S. market from a number of sources. Competitive forces have intensified due to the increasing importance of large national accounts and the increasing consolidation in supplier relationships. We compete for business on the basis of price, performance and value added services that we are able to provide as one of the largest national distributors in the North America.

RESEARCH AND DEVELOPMENT EXPENDITURES

Government sponsored research expenditures (which are included in cost of sales) were $2.6 million in 2007, $4.4 million in 2006, and $7.0 million in 2005. Independent research and development expenditures (which are included in selling, general and administrative expenses) were $3.3 million in 2007, $3.3 million in 2006, and $2.6 million in 2005.

COMPLIANCE WITH ENVIRONMENTAL PROTECTION LAWS

We are subject to the usual reviews, inspections and enforcement actions by various federal and state environmental and enforcement agencies and have entered into agreements and consent decrees at various times in connection with such reviews. In addition, we engage in various environmental studies and investigations and, where legally required to do so, undertake appropriate remedial actions at facilities we own or control, either voluntarily or in connection with the acquisition, disposal or operation of such facilities.

Such studies and investigations are ongoing at the company’s Bloomfield, and Moosup, Connecticut facilities with voluntary remediation activities also being undertaken at the Moosup facility. We have cooperated with the U.S. Government in the environmental studies required to be undertaken by the Government in connection with the Government’s proposed sale of its Bloomfield facility to the company. As a result of such studies, we are in the process of identifying various voluntary remediation activities that we would agree to undertake in connection with a completed purchase of the facility, which relate principally to items that are required under the Connecticut Transfer Act (the Act) upon a legal transfer of the property’s ownership. This item is discussed in more detail in Item 7, Management’s Discussion and Analysis of Financial Condition and Results of Operations (Helicopters Segment) and in Item 2 (Properties).

7

Also, in preparation for disposition of the Moosup facility, we have sought and obtained the conditional approval of the State of Connecticut Department of Environmental Protection (CTDEP) to a reclassification of the groundwater in the vicinity to be consistent with the industrial character of the area. The company has substantially completed work related to such ground water reclassification (including connection of certain neighboring properties to public drinking water) in coordination with CTDEP and local authorities. We anticipate that the project will be completed in 2008.

In connection with our sale of the Music segment, we assumed responsibility for meeting certain requirements of the Act that apply to the leased guitar manufacturing facility (Ovation) located in New Hartford, Connecticut, which was transferred as part of the sale. Under the Act, we are required to assess the environmental conditions of the site and remediate environmental impairments, if any, caused by Ovation’s operations. The site consists of a multi-tenant industrial park, in which Ovation and other unrelated entities lease space. We are in the process of assessing the environmental conditions at the site and determining our share of the cost of whatever environmental remediation may be required, if any. We currently estimate our share of the cost to assess the environmental conditions and remediate this property will be approximately $2.2 million, and this amount has been included in the determination of the net gain on the sale of Music.

With respect to all other matters that may currently be pending, in the opinion of management, based on our analysis of relevant facts and circumstances, compliance with relevant environmental protection laws is not likely to have a material adverse effect upon our capital expenditures, earnings or competitive position. In arriving at this conclusion, we have taken into consideration site-specific information available regarding total costs of any work to be performed, and the extent of work previously performed. Where we have been identified as a “potentially responsible party” (PRP) by environmental authorities at a particular site, we, using information available to us, also have reviewed and considered a number of other factors, including: (i) the financial resources of other PRPs involved in each site, and their proportionate share of the total volume of waste at the site; (ii) the existence of insurance, if any, and the financial viability of the insurers; and (iii) the success others have had in receiving reimbursement for similar costs under similar insurance policies issued during the periods applicable to each site. No such matters were outstanding at the end of 2007.

EMPLOYEES

As of December 31, 2007, the company employed 3,618 individuals throughout its business segments and corporate headquarters.

FINANCIAL INFORMATION ABOUT GEOGRAPHIC AREAS

Financial information about geographic areas is included in Note 19, Segment and Geographic Information, of the Notes to Consolidated Financial Statements, included in Item 8, Financial Statements and Supplementary Data, of this Annual Report on Form 10-K.

AVAILABLE INFORMATION

We are subject to the reporting requirements of the Exchange Act and its rules and regulations. The Exchange Act requires us to file reports, proxy statements and other information with the U.S. Securities and Exchange Commission (“SEC”). Copies of these reports, proxy statements and other information can be read and copied at:

SEC Public Reference Room

100 F Street NE

Washington, D.C. 20549

8

Information on the operation of the Public Reference Room may be obtained by calling the SEC at 1-800-SEC-0330.

The SEC maintains a website that contains reports, proxy statements and other information regarding issuers that file electronically with the SEC. These materials may be obtained electronically by accessing the SEC’s website at http://www.sec.gov.

We make available, free of charge on our website, our annual report on Form 10-K, quarterly reports on Form 10-Q, proxy statements, and current reports on Form 8-K as well as amendments to those reports filed or furnished pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934, together with Section 16 insider beneficial stock ownership reports, as soon as reasonably practicable after we electronically file these documents with, or furnish them to, the SEC. These documents are posted on our website at www.kaman.com — select the “Investors & Media” link and then the “SEC Documents” link. The information contained in the company’s website is not intended to be incorporated into this Form 10-K.

We also make available, free of charge on our website, the Certificate of Incorporation, Bylaws, Governance Principles and all Board of Directors’ standing Committee Charters (including Audit, Corporate Governance, Personnel & Compensation and Finance). These documents are posted on our website at www.kaman.com — select the “Corporate Governance” link.

ITEM 1A. RISK FACTORS

Our business, financial condition, operating results and cash flows can be impacted by a number of factors, including, but not limited to, those set forth below, any one of which could cause our actual results to vary materially from recent results or anticipated future results. For a discussion identifying additional risk factors and important factors that could cause actual results to differ materially from those anticipated, see the discussion in “Forward Looking Statements” in Part 1 of this Form 10-K.

Our financial performance is dependent on the conditions of the aerospace industry.

The combined Aerospace Segments’ results are directly tied to the economic conditions in the commercial aviation and defense industries. As a result, changes in economic conditions may cause customers to request that firm orders be rescheduled or canceled, which could put a portion of our backlog at risk. Additionally, a significant amount of work that we perform under contract tends to be for a few large customers.

The aviation industry tends to be cyclical, and capital spending by airlines and aircraft manufacturers may be influenced by a variety of factors including current and future traffic levels, aircraft fuel pricing, labor issues, competition, the retirement of older aircraft, regulatory changes, terrorism and related safety concerns, general economic conditions, worldwide airline profits and backlog levels.

The defense industry is also affected by a changing global political environment, continued pressure on U.S. and global defense spending, U.S. foreign policy and the level of activity in military flight operations. Changes to the defense industry could have a material impact on several of our current aerospace programs, which would adversely affect our operating results. To mitigate these risks, we have worked to expand our customer and product base to include both commercial and military markets.

Furthermore, because of the lengthy research and development cycle involved in bringing new products to market, we cannot predict the economic conditions that will exist when a new product is introduced. A reduction in capital spending in the aviation or defense industries could have a significant effect on the demand for our products, which could have an adverse effect on our financial performance or results of operations.

9

Competition from domestic and foreign manufacturers may result in the loss of potential contracts and opportunities.

The aerospace markets in which we participate are highly competitive and we often compete for work not only with large OEMs but also sometimes with our own customers and suppliers. Many of our large customers may choose not to outsource production due to, among other things, their own direct labor and overhead considerations and capacity utilization at their own facilities. This would result in these customers supplying their own products or services and competing directly with us for sales of these products or services, all of which could significantly reduce our revenues.

Our competitors may have more extensive or more specialized engineering, manufacturing and marketing capabilities than we do in some areas and we may not have the technology, cost structure, or available resources to effectively compete in the market. We believe that developing and maintaining a competitive advantage will require continued investment in product development, engineering, supply chain management and sales and marketing, and we may not have enough resources to make the necessary investments to do so.

We are also facing increased international competition. Further, our significant customers have in the past used, and may attempt in the future to use, their position to negotiate a reduction in price of a particular product regardless of the terms of an existing contract.

For these reasons, we may not be able to compete successfully in this market or against such competitors. Our strategies for our aerospace segments allow us to continue to effectively compete for key contracts and customers. For additional information on this topic, see Item 1 “Business — Competition” of this Form 10-K.

Estimates of future costs for long-term contracts impact our current operating results and profits.

For long-term contracts we generally recognize sales and gross margin based on the percentage-of-completion method of accounting. This method allows for revenue recognition as our work progresses on a contract.

The percentage-of-completion method requires that we estimate future revenues and costs over the life of a contract. Revenues are estimated based upon the original contract price, with consideration being given to exercised contract options, change orders and, in some cases, projected customer requirements. Contract costs may be incurred over a period of several years, and the estimation of these costs requires significant judgment based upon the acquired knowledge and experience of program managers, engineers, and financial professionals. Estimated costs are based primarily on anticipated purchase contract terms, historical performance trends, business base and other economic projections. The complexity of certain programs as well as technical risks and the availability of materials and labor resources could affect the company’s ability to estimate future contract costs. Additional factors that could affect recognition of revenue under the percentage-of-completion method include:

| | • | | Accounting for start-up costs; |

| | • | | The effect of non-recurring work; |

| | • | | Delayed contract start-up; |

| | • | | Transition of work from the customer or other vendors; |

| | • | | Claims or unapproved change orders; |

| | • | | Product warranty issues; |

| | • | | Delayed completion of certain programs for which inventory has been built up; and, |

| | • | | Accrual of contract losses. |

Because of the significance of the judgments and estimation processes, it is likely that materially different sales and profit amounts could be recorded if we used different assumptions or if the underlying circumstances were to

10

change. Changes in underlying assumptions, circumstances or estimates may adversely affect future period financial performance. We perform quarterly reviews of our long-term contracts to help us to address and lessen the effects of these risks.

The cost and effort to start-up new programs could negatively impact our current operating results and profits.

In recent years, the company has been ramping up several new programs. These include, but are not limited to, a contract for production of the composite flight deck floor, as well as metal and composite bonded panels for the vertical stabilizer, for the Boeing 787 Dreamliner, and a contract to manufacture and assemble composite tail rotor pylons for Sikorsky MH-92 helicopters.

The time required and cost incurred to get a new program underway can be significant and includes non-recurring costs for tooling, first article testing, finalizing drawings and engineering specifications and hiring new employees able to perform the technical work required. New programs typically involve greater volume of scrap, higher overhead rates due to inefficiencies, delays in production, and learning curves that are more extended than anticipated, all of which can impact current period results. We have been working with our customers and leveraging off of our years of experience to effectively ramp up these new programs.

We are continuing to work on the Australian SH-2G(A) program for the Royal Australian Navy but thus far have not delivered the first fully capable aircraft.

Work continued on the SH-2G(A) program for Australia during 2007. This program involves the remanufacture of eleven helicopters with support, including a support services facility, for the Royal Australian Navy. Following a review of the program and possible alternatives initiated by the Commonwealth’s Minister of Defence in mid-2006, the Minister announced in May 2007 that the Commonwealth would proceed with the program, “subject to satisfactory contract arrangements.” Since that time, in addition to ongoing program activities, the parties have been engaged in discussions aimed at developing a mutually acceptable path forward to complete the program.

The contract dispute resolution process initiated by the Commonwealth in January 2007, which the parties subsequently agreed to suspend with a mutual waiver of applicable statutes of limitation periods, continues to be outstanding. The Commonwealth’s principal assertions are that the helicopters have not been delivered in a timely manner and the design of the helicopter, particularly the automatic flight control system, is inadequate from a safety perspective. Management believes that its obligations to the Commonwealth under the program are being performed and the design of the SH-2G(A) is safe and proper as demonstrated by the significant operational history of this aircraft type with several countries, including the United States, Egypt, New Zealand, and Poland.

This matter is more fully discussed in “Management’s Discussion and Analysis of Financial Condition and Results of Operations”, in Item 7 of this Form 10-K and in “Notes to Consolidated Financial Statements” in Item 8 of this Form 10-K.

The final delivery of a fully capable aircraft has been delayed for several years initially due to the complexities of the Integrated Tactical Avionics System (ITAS) software and due to the Commonwealth’s concerns regarding the program. Through 2007, we have recorded a significant amount of contract loss charges and any further delay could result in additional charges in the future.

11

Our U.S. Government programs are subject to unique risks.

The company has several significant long-term contracts either directly with the U.S. government or where it is the ultimate customer, including the Sikorsky BLACK HAWK cockpit program, the JPF program, and the Boeing C-17 program. These contracts are subject to unique risks, some of which are beyond our control. Examples of such risks would include:

| | • | | The U.S. Government may modify, curtail or terminate our contracts. The U.S. Government may modify, curtail or terminate its contracts and subcontracts at its convenience without prior notice, upon payment for work done and commitments made at the time of termination. Modification, curtailment or termination of our major programs or contracts could have a material adverse effect on our future results of operations and financial condition. |

| | • | | Our U.S. Government business is subject to specific procurement regulations and other requirements. These requirements, although customary in U.S. Government contracts, increase our performance and compliance costs. These costs might increase in the future, reducing our margins, which could have a negative effect on our financial condition. Failure to comply with these regulations and requirements could lead to suspension or debarment, for cause, from U.S. Government contracting or subcontracting for a period of time and could have a negative effect on our reputation and ability to procure other U.S. Government contracts in the future. |

| | • | | Our contract costs are subject to audits by U.S. Government agencies. The costs we incur on our U.S. Government contracts, including allocated indirect costs, may be audited by U.S. Government representatives. These audits may result in adjustments to our contract costs. Any costs found to be improperly allocated to a specific contract will not be reimbursed, and such costs already reimbursed must be refunded. We normally negotiate with the U.S. Government representatives before settling on final adjustments to our contract costs. We have recorded contract revenues based upon costs we expect to realize upon final audit. However, we do not know the outcome of any future audits and adjustments and we may be required to reduce our revenues or profits upon completion and final negotiation of these audits. If any audit shows improper or illegal activities, we may be subject to civil and criminal penalties and administrative sanctions, including termination of contracts, forfeiture of profits, suspension of payments, fines and suspension or prohibition from doing business with the U.S. Government. |

| | • | | Our business is subject to potential U.S. Government inquiries and investigations. We are from time to time subject to certain routine U.S. Government inquiries and investigations of our business practices due to our participation in government contracts. Any adverse finding associated with such an inquiry or investigation could have a material adverse effect on our results of operations and financial condition. |

The price volatility and availability of raw material could increase our operating costs and adversely impact our profits.

We rely on foreign and domestic suppliers and commodity markets to secure raw materials used in many of the products we manufacture within the combined Aerospace Segments or sell within our Industrial Distribution segment. This exposes us to volatility in the price and availability of raw materials. In some instances, we depend upon a single source of supply. A disruption in deliveries from our suppliers, price increases, or decreased availability of raw materials or commodities could adversely affect our ability to meet our commitments to customers. This could also have an impact on our operating costs as well as our operating income. We try to base our supply management process on an appropriate balancing of the foreseeable risks and the costs of alternative

12

practices. We also try to pass on increases in our costs but our ability to do so depends on contract terms and market conditions. Raising our prices could result in decreased sales volume, which could significantly reduce our profitability. All of these factors may have an adverse effect on our results of operations or financial condition. To mitigate these risks, we negotiate long-term agreements for materials, when possible.

We may make acquisitions or investments in new businesses, products or technologies that involve additional risks, which could disrupt our business or harm our financial condition or results of operations.

As part of our business strategy, we have made, and expect to continue to make, acquisitions of businesses or investments in companies that offer complementary products, services and technologies. Such acquisitions or investments involve a number of risks, including:

| | • | | Assimilating operations and products may be unexpectedly difficult; |

| | • | | Management’s attention may be diverted from other business concerns; |

| | • | | The company may enter markets in which it has limited or no direct experience; |

| | • | | The company may lose key employees of an acquired business; and |

| | • | | The company may not realize the value of the acquired assets relative to the price paid. |

These factors could have a material adverse effect on our business, financial condition and operating results. Consideration paid for any future acquisitions could include our stock or require that we incur additional debt and contingent liabilities. As a result, future acquisitions could cause dilution of existing equity interests and earnings per share. Before we enter into any acquisition, we perform significant due diligence to ensure the potential acquisition fits with our strategic objectives. In addition, we ensure that we have adequate resources to transition the newly acquired company efficiently.

We rely on the experience and expertise of our skilled employees, and must continue to attract and retain qualified technical, marketing and managerial personnel in order to succeed.

Our future success will depend largely upon our ability to attract and retain highly skilled technical, managerial and marketing personnel. There is significant competition for such personnel in the aerospace and industrial distribution industries. We try to ensure that we offer competitive compensation and benefits as well as opportunities for continued development. There can be no assurance that we will continue to be successful in attracting and retaining the personnel we require to develop new and enhanced products and to continue to grow and operate profitably. We continue to work to recruit and train new personnel as well as maintain our existing employee base.

We are subject to litigation that could adversely affect our operating results.

Our financial results may be affected by the outcome of legal proceedings and other contingencies that cannot be predicted. In accordance with generally accepted accounting principles, if a liability is deemed probable and reasonably estimable in light of the facts and circumstances known to us at a particular point in time, we will make an estimate of material loss contingencies and establish reserves based on our assessment. Subsequent developments in legal proceedings may affect our assessment. The estimates of a loss contingency recorded in our financial statements could adversely affect our results of operations in the period in which a liability would be recognized. This could also have an adverse impact on our cash flows in the period during which damages would be paid. As of December 31, 2007, the company does not have any loss contingency recorded with respect to any pending litigation, as we do not believe that we have met the criteria to establish such a liability for any pending litigation matter.

13

We rely upon growth in our Industrial Distribution segment through development of national account relationships.

Over the past several years, more companies have begun to consolidate their purchases of industrial products, resulting in their doing such business with only a few major distributors rather than a large number of vendors. Through our national accounts strategy we have worked hard to develop the relationships necessary to be one of those major suppliers. Competition relative to these types of arrangements is significant. If we are not awarded additional national accounts in the future, our sales volume would be negatively impacted which may result in lower gross margins and weaker operating results. Additionally, national accounts typically require an increased level of customer service as well as investments in the form of opening of new branches to meet our customers’ needs. The cost and time associated with these activities could be significant and if the relationship is not maintained we could ultimately not make a return on these investments. One of our key strategies has been to increase our national account presence. Thus far, we have been successful with our strategy with the addition of several new large national accounts since late 2006. We will continue to focus on this endeavor through 2008.

We could be negatively impacted by the loss of key suppliers, lack of product availability, or changes in supplier programs that could adversely affect our operating results.

Our Industrial Distribution business depends on maintaining sufficient supply of various products to meet our customers’ demands. We have several long-standing relationships with key product suppliers but these relationships are non-exclusive and could be terminated by either party. If we lost a key supplier, or were unable to obtain the same levels of deliveries from these suppliers and were unable to supplement those purchases with products obtained from other suppliers, it could have a material adverse effect on our business. Supply interruptions could arise from shortages of raw materials, labor disputes or weather conditions affecting suppliers’ production, transportation disruptions, or other reasons beyond our control. Even if we continue with our current supplier relationships, high demand for certain products may result in us being unable to meet our customers’ demand, which could put us at a competitive disadvantage. Additionally our key suppliers could also increase pricing of their products, which would negatively affect our operating results if we were not able to pass these price increases through to our customers. We engage in strategic inventory purchases during the year, negotiate long-term vendor supply agreements and monitor our inventory levels to ensure that we have the appropriate inventory on hand to meet our customers’ requirements.

Our revenue and quarterly results may fluctuate, which could adversely affect our stock price.

We have experienced, and may in the future experience, significant fluctuations in our quarterly operating results that may be caused by many factors. These factors include but are not limited to:

| | • | | Changes in demand for our products; |

| | • | | Introduction, enhancement or announcement of products by us or our competitors; |

| | • | | Market acceptance of our new products; |

| | ��� | | The growth rates of certain market segments in which we compete; |

| | • | | Size and timing of significant orders; |

| | • | | Budgeting cycles of customers; |

| | • | | Mix of distribution channels; |

| | • | | Mix of products and services sold; |

| | • | | Mix of international and North American revenues; |

| | • | | Fluctuations in currency exchange rates; |

| | • | | Changes in the level of operating expenses; |

| | • | | Changes in our sales incentive plans; |

| | • | | Inventory obsolescence; |

14

| | • | | Additional contract losses; |

| | • | | Completion or announcement of acquisitions by us or our competitors; and |

| | • | | General economic conditions in regions in which we conduct business. |

Most of our expenses are relatively fixed, including costs of personnel and facilities, and are not easily reduced. Thus, an unexpected reduction in our revenue, or failure to achieve the anticipated rate of growth, could have a material adverse effect on our profitability. If our operating results do not meet the expectations of investors, our stock price may decline.

Changes in global economic and political conditions could adversely affect our foreign operations and results of operations.

During 2007, foreign sales were 14.0 percent of our total revenues. If our customers’ buying patterns, including decision-making processes, timing of expected deliveries and timing of new projects, unfavorably change due to economic or political conditions, there could be an adverse effect on our business. Other potential risks inherent in our foreign business include:

| | • | | Greater difficulties in accounts receivable collection; |

| | • | | Unexpected changes in regulatory requirements; |

| | • | | Export restrictions, tariffs and other trade barriers; |

| | • | | Difficulties in staffing and managing foreign operations; |

| | • | | Seasonal reductions in business activity during the summer months in Europe and certain other parts of the world; |

| | • | | Economic instability in emerging markets; |

| | • | | Potentially adverse tax consequences; and |

| | • | | Cultural and legal differences in the conduct of business. |

Any one or more of such factors could have a material adverse effect on our international operations, and, consequently, on our business, financial condition and operating results.

FORWARD-LOOKING STATEMENTS

This report may contain forward-looking information relating to the company’s business and prospects, including the Aerospace and Industrial Distribution businesses, operating cash flow, and other matters that involve a number of uncertainties that may cause actual results to differ materially from expectations. Those uncertainties include, but are not limited to: 1) the successful conclusion of competitions for government programs and thereafter contract negotiations with government authorities, both foreign and domestic; 2) political conditions in countries where the company does or intends to do business; 3) standard government contract provisions permitting renegotiation of terms and termination for the convenience of the government; 4) domestic and foreign economic and competitive conditions in markets served by the company, particularly the defense, commercial aviation and industrial production markets; 5) risks associated with successful implementation and ramp up of significant new programs; 6) satisfactory completion of the Australian SH-2G(A) program, including negotiation of payment and performance terms for the balance of the program as well as any additional work scope requested by the Commonwealth; 7) receipt and successful execution of production orders for the JPF U.S. government contract including the exercise of all contract options and receipt of orders from allied militaries, as both have been assumed in connection with goodwill impairment evaluations; 8) the University of Arizona’s continued failure to succeed in its appeals efforts to overturn the jury verdict that rejected the University’s breach of contract claim against the company; 9) satisfactory resolution of the company’s contract dispute with the U.S. Army procurement agency relating to the FMU-143 program; 10) continued support of the existing K-MAX helicopter fleet, including sale of existing K-MAX spare parts inventory; 11) cost growth in connection with

15

environmental remediation activities at the Moosup, CT and New Hartford, CT facilities and such potential activities at the Bloomfield, CT facility; 12) profitable integration of acquired businesses into the company’s operations; 13) changes in supplier sales or vendor incentive policies; 14) the effect of price increases or decreases; 15) pension plan assumptions and future contributions; 16) future levels of indebtedness and capital expenditures; 17) continued availability of raw materials in adequate supplies; 18) the effects of currency exchange rates and foreign competition on future operations; 19) changes in laws and regulations, taxes, interest rates, inflation rates, general business conditions and other factors; and 20) other risks and uncertainties set forth in the company’s annual, quarterly and current reports, and proxy statements. Any forward-looking information provided in this report should be considered with these factors in mind. The company assumes no obligation to update any forward-looking statements contained in this report.

ITEM 1B. UNRESOLVED STAFF COMMENTS

None.

ITEM 2. PROPERTIES

Our facilities are generally suitable for, and adequate to serve, their intended uses. At December 31, 2007, our business segments occupied major facilities at the following principal locations:

| | | | |

| Segment | | Location | | Property Type |

Aerostructures | | Jacksonville, Florida; Wichita, Kansas | | Manufacturing & Office |

| | |

Fuzing | | Middletown, Connecticut; Orlando, Florida; Tuscon, Arizona | | Manufacturing & Office |

| | |

Helicopters | | Bloomfield, Connecticut; New South Wales, Australia | | Manufacturing, Office & Service Center |

| | |

Specialty Bearings | | Bloomfield, Connecticut; Dachsbach, Germany | | Manufacturing & Office |

| | |

Industrial Distribution (1) | | Windsor, Connecticut; Ontario, California; Albany, New York; Salt Lake City, Utah; Louisville, Kentucky; Mexico City, Mexico; Ontario, Canada; British Columbia, Canada | | Distribution Centers & Office |

| | |

Corporate | | Bloomfield, Connecticut | | Office |

| | |

| Square Feet in thousands | | Total |

Aerostructures segment | | 338,335 |

Fuzing segment | | 342,848 |

Helicopters segment (2) | | 463,713 |

Specialty Bearings segment | | 201,481 |

Subtotal Aerospace Segments | | 1,346,377 |

Industrial Distribution segment | | 1,509,772 |

Corporate Headquarters (3,4) | | 619,556 |

Total | | 3,475,705 |

| |

| (1) | Branches for the Industrial Distribution segment are located across the United States, Canada and Mexico. |

| (2) | The U.S. Government owns 154 thousand square feet of the space occupied by Kaman Aerospace Corporation in Bloomfield, Connecticut in accordance with a Facilities Lease Agreement. The company continues to work with NAVAIR and the General Services Administration toward completing an agreement |

16

| | for the company’s purchase of the facility. Additional information relative to this matter is included in Item 7,Management’s Discussion and Analysis of Financial Condition and Results of Operations, and Note 16, Commitments and Contingencies, of the Notes to Consolidated Financial Statements, included in Item 8, Financial Statements and Supplementary Data, of this Annual Report on Form 10-K. |

| (3) | We occupy a 40 thousand square foot corporate headquarters building in Bloomfield, Connecticut and own another 76 thousand square foot mixed use building that is currently leased to Fender in connection with their acquisition of the Music segment on December 31, 2007. The maximum lease term is 2 years. |

| (4) | Approximately 500 thousand square feet of space included in the corporate square footage is attributable to a facility located in Moosup, Connecticut, that was closed in 2003 and is being held for disposition. |

ITEM 3. LEGAL PROCEEDINGS

From time to time, the company is subject to various claims and suits arising out of the ordinary course of business, including commercial, employment and environmental matters. We do not expect that the resolution of these matters would have a material adverse effect on our consolidated financial position. Although not material, certain legal proceedings that relate to specific segments of our company are discussed in Item 7,Management’s Discussion and Analysis of Financial Condition and Results of Operations, and Note 16, Commitments and Contingencies, of the Notes to Consolidated Financial Statements, included in Item 8, Financial Statements and Supplementary Data, of this Annual Report on Form 10-K. Other legal proceedings or enforcement actions relating to environmental matters, if any, are discussed in the section of Item 1 entitled Compliance with Environmental Protection Laws.

ITEM 4. SUBMISSION OF MATTERS TO A VOTE OF SECURITY HOLDERS

There were no matters submitted to a vote of security holders during the fourth quarter of 2007.

17

PART II

ITEM 5. MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER

MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

MARKET FOR COMMON STOCK

Our Common Stock is traded on the NASDAQ Global Market under the symbol “KAMN”.

HOLDERS OF COMMON STOCK

As of February 1, 2008, there were 4,186 registered holders of our Common Stock.

INVESTOR SERVICES PROGRAM

Holders of the company’s Common Stock are eligible to participate in the Mellon Investor Services Program administered by Mellon Bank, N.A. The program offers a variety of services including dividend reinvestment. A booklet describing the program may be obtained by contacting Mellon at (800) 227-0291 or via the web atwww.melloninvestor.com.

| | | | | | | | | | | | |

QUARTERLY COMMON STOCK INFORMATION |

| | | High | | Low | | Close | | Dividend

Declared |

2007 | | | | | | | | | | | | |

First | | $ | 24.41 | | $ | 21.38 | | $ | 23.31 | | $ | 0.125 |

Second | | | 32.59 | | | 22.89 | | | 31.19 | | | 0.125 |

Third | | | 37.64 | | | 29.54 | | | 34.56 | | | 0.140 |

Fourth | | | 39.31 | | | 30.08 | | | 36.81 | | | 0.140 |

2006 | | | | | | | | | | | | |

First | | $ | 25.45 | | $ | 18.91 | | $ | 25.16 | | $ | 0.125 |

Second | | | 25.69 | | | 15.52 | | | 18.20 | | | 0.125 |

Third | | | 19.00 | | | 17.25 | | | 18.01 | | | 0.125 |

Fourth | | | 24.50 | | | 17.70 | | | 22.39 | | | 0.125 |

NASDAQ market quotations reflect inter-dealer prices, without retail mark-up, mark-down, or commission and may not necessarily represent actual transactions.

ISSUER PURCHASES OF EQUITY SECURITIES

(a) Sales of Equity Securities; Conversion of Convertible Debentures

On November 26, 2007 we issued a redemption notice calling for the full redemption on December 20, 2007, of all $11.2 million of the outstanding 6% Convertible Subordinated Debentures due 2012 at a redemption price of 100% of principal amount plus accrued interest to December 20, 2007. The Debentures were convertible until the close of business on December 17, 2007, into shares of the company’s Common Stock at the conversion price of $23.36 per share.

From the date of the announcement to December 17, 2007, holders converted a total of 10,985 debentures, with a value of $11.0 million, into an aggregate of 470,226 shares of the company’s common stock. There were additional conversions during the fourth quarter of 2007 prior to the redemption announcement of 1,342 debentures for a total of 57,445 shares of common stock. Total conversions for the fourth quarter of 2007 were

18

12,327 debentures into an aggregate of 527,671 of the company’s common stock. We received no cash consideration for the issued shares, which were issued pursuant to an exemption from registration under the Securities Act of 1933, as amended, contained in Section 3(a)(9) of such Act. On December 20, 2007, we paid $0.2 million for the redemption of the remaining 179 debentures outstanding.

(b) In November 2000, our board of directors approved a replenishment of the company’s stock repurchase program providing for repurchase of an aggregate of 1.4 million shares of Common Stock for use in the administration of our stock plans and for general corporate purposes. The following table provides information about purchases of Common Stock by the company during the three months ended December 31, 2007:

| | | | | | | | |

Period | | Total Number of

Shares Purchased | | Average Price

Paid per Share | | Total Number of Shares

Purchased as Part of a

Publically Announced Plan | | Maximum Number of

Shares That May Yet Be

Purchased Under the Plan |

9/29/07- | | | | | | | | |

10/26/2007 | | - | | - | | 269,611 | | 1,130,389 |

| | | | |

10/27/2007- | | | | | | | | |

11/23/2007 | | - | | - | | 269,611 | | 1,130,389 |

| | | | |

11/24/07- | | | | | | | | |

12/31/2007 | | - | | - | | 269,611 | | 1,130,389 |

19

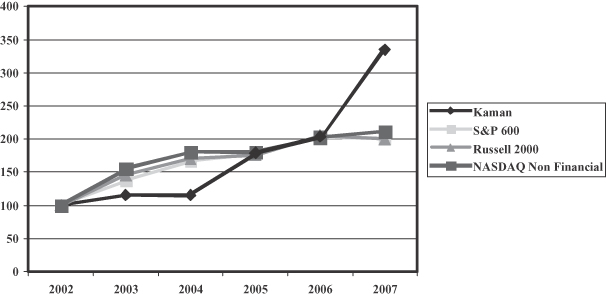

PERFORMANCE GRAPH

Following is a comparison of our total shareholder return for the period 2002 – 2007 compared to the S&P 600 Small Cap Index, the Russell 2000 Small Cap Index, and the NASDAQ Non-Financial Composite Index. The performance graph does not include a published industry or line-of-business index or peer group of similar issuers because during the performance period the company was conducting operations in three lines of business and we do not believe a meaningful industry index or peer group can be reasonably identified. Accordingly, as permitted by regulation, the graph includes the S&P 600 Small Cap Index, the Russell 2000 Small Cap Index, both of which are comprised of issuers with generally similar market capitalizations to that of the company, and the NASDAQ Non-Financial index calculated by the exchange on which company shares are traded.

| | | | | | | | | | | | |

| | | 2002 | | 2003 | | 2004 | | 2005 | | 2006 | | 2007 |

Kaman | | 100.0 | | 115.7 | | 115.0 | | 179.0 | | 203.6 | | 334.6 |

S&P 600 | | 100.0 | | 137.5 | | 167.3 | | 178.4 | | 203.5 | | 201.0 |

Russell 2000 | | 100.0 | | 145.4 | | 170.5 | | 175.7 | | 205.6 | | 200.0 |

NASDAQ Non Financial | | 100.0 | | 155.7 | | 180.8 | | 180.6 | | 203.0 | | 211.6 |

20

ITEM 6. SELECTED FINANCIAL DATA

FIVE-YEAR SELECTED FINANCIAL DATA

(in thousands except per share amounts, shareholders and employees)

| | | | | | | | | | | | | | | | | | | | |

| | | 20071,7 | | | 20061 | | | 2005 1,2,3,4 | | | 20041,5 | | | 20031,6 | |

OPERATIONS | | | | | | | | | | | | | | | | | | | | |

Net sales from continuing operations | | $ | 1,086,031 | | | $ | 991,422 | | | $ | 909,878 | | | $ | 834,191 | | | $ | 749,057 | |

Net gain (loss) on sale of product lines and other assets | | | 2,579 | | | | (52 | ) | | | (27 | ) | | | 199 | | | | 18,163 | |

Operating income (loss) from continuing operations | | | 64,728 | | | | 47,822 | | | | 19,741 | | | | (23,615 | ) | | | 26,593 | |

Earnings (loss) before income taxes from continuing operations | | | 57,527 | | | | 40,660 | | | | 15,817 | | | | (28,225 | ) | | | 22,345 | |

Income tax benefit (expense) | | | (21,036 | ) | | | (16,017 | ) | | | (10,743 | ) | | | 9,599 | | | | (8,819 | ) |

Net earnings (loss) from continuing operations | | | 36,491 | | | | 24,643 | | | | 5,074 | | | | (18,626 | ) | | | 13,526 | |

Net earnings from discontinued operations, net of taxes | | | 7,890 | | | | 7,143 | | | | 7,954 | | | | 6,804 | | | | 5,879 | |

Gain on disposal of discontinued operations, net of taxes | | | 11,538 | | | | - | | | | - | | | | - | | | | - | |

Net earnings (loss) | | $ | 55,919 | | | $ | 31,786 | | | $ | 13,028 | | | $ | (11,822 | ) | | $ | 19,405 | |

| | | | | |

FINANCIAL POSITION | | | | | | | | | | | | | | | | | | | | |

Current assets | | $ | 491,629 | | | $ | 513,231 | | | $ | 496,403 | | | $ | 468,406 | | | $ | 436,894 | |

Current liabilities | | | 182,631 | | | | 199,126 | | | | 223,722 | | | | 226,297 | | | | 160,681 | |

Working capital | | | 308,998 | | | | 314,105 | | | | 272,681 | | | | 242,109 | | | | 276,213 | |

Property, plant and equipment, net | | | 53,645 | | | | 49,954 | | | | 46,895 | | | | 46,538 | | | | 48,877 | |

Total assets | | | 634,863 | | | | 630,413 | | | | 598,497 | | | | 562,331 | | | | 528,311 | |

Long-term debt | | | 11,194 | | | | 72,872 | | | | 62,235 | | | | 18,522 | | | | 36,624 | |

Shareholders’ equity | | | 394,526 | | | | 296,561 | | | | 269,754 | | | | 284,170 | | | | 303,183 | |

| | | | | |

PER SHARE AMOUNTS | | | | | | | | | | | | | | | | | | | | |

Net earnings (loss) per share – basic from continuing operations | | | 1.50 | | | | 1.02 | | | | 0.22 | | | | (0.82 | ) | | | 0.60 | |

Net earnings (loss) per share – basic from discontinued operations | | | 0.32 | | | | 0.30 | | | | 0.35 | | | | 0.30 | | | | 0.26 | |

Net earnings (loss) per share – basic from disposal of disco ops | | | 0.47 | | | | - | | | | - | | | | - | | | | - | |

| | | | |

Net earnings (loss) per share – basic | | $ | 2.29 | | | $ | 1.32 | | | $ | 0.57 | | | $ | (0.52 | ) | | $ | 0.86 | |

| | | | |

| | | | | | | | | | | | | | | | | | | | |

Net earnings (loss) per share – diluted from continuing operations | | | 1.46 | | | | 1.01 | | | | 0.22 | | | | (0.82 | ) | | | 0.60 | |

Net earnings (loss) per share – diluted from discontinued operations | | | 0.31 | | | | 0.29 | | | | 0.35 | | | | 0.30 | | | | 0.26 | |

Net earnings (loss) per share – diluted from disposal of disco ops | | | 0.46 | | | | - | | | | - | | | | - | | | | - | |

| | | | |

Net earnings (loss) per share – diluted | | $ | 2.23 | | | $ | 1.30 | | | $ | 0.57 | | | $ | (0.52 | ) | | $ | 0.86 | |

| | | | |

| | | | | | | | | | | | | | | | | | | | |

Dividends declared | | | 0.530 | | | | 0.500 | | | | 0.485 | | | | 0.440 | | | | 0.440 | |

Shareholders’ equity | | | 15.69 | | | | 12.28 | | | | 11.28 | | | | 12.48 | | | | 13.40 | |

| | | | | |

Market price range – High | | | 39.31 | | | | 25.69 | | | | 24.48 | | | | 15.49 | | | | 14.91 | |

Market price range – Low | | | 21.38 | | | | 15.52 | | | | 10.95 | | | | 10.71 | | | | 9.40 | |

| | | | | |

AVERAGE SHARES OUTSTANDING | | | | | | | | | | | | | | | | | | | | |

Basic | | | 24,375 | | | | 24,036 | | | | 23,038 | | | | 22,700 | | | | 22,561 | |

Diluted | | | 25,261 | | | | 24,869 | | | | 23,969 | | | | 22,700 | | | | 23,542 | |

| | | | | |

GENERAL STATISTICS | | | | | | | | | | | | | | | | | | | | |

Registered shareholders | | | 4,186 | | | | 4,468 | | | | 4,779 | | | | 5,192 | | | | 5,509 | |

Employees | | | 3,618 | | | | 3,906 | | | | 3,712 | | | | 3,581 | | | | 3,499 | |

21

Included within certain annual results are a variety of unusual or significant items that may affect comparability. The most significant of such items are described below as well as within Management’s Discussion and Analysis and the Notes to Consolidated Financial Statements.

| 1. | Cost of sales includes charges for the Australian SH-2G(A) helicopter program as follows: 2007 — $6,413; 2006 — $9,701; 2005 — $16,810; 2004 — $5,474; 2003 — $0. |

| 2. | Results for 2005 include $8,265 of expense for the company’s stock appreciation rights, $3,339 for legal and financial advisory fees associated with the recapitalization and $6,754 recovery of previously written off amounts for MD Helicopters, Inc. (MDHI). |

| 3. | The effective tax rate for 2005 was 67.9 percent, which was high principally due to the non-deductibility of expenses associated with stock appreciation rights and the company’s recapitalization. |

| 4. | Average shares outstanding increased principally due to the completion of the recapitalization in November 2005. |

| 5. | Results for 2004 include the following adjustments: $20,083 (including $18,211 negative sales adjustments and $1,872 increase in bad debt reserve) related to the company’s investment in MDHI programs; $7,086 non-cash adjustment for the Boeing Harbour Point program; $3,507 warranty reserve for two product warranty related issues and $3,471 non-cash adjustment related to the University of Arizona matter. |

| 6. | The company sold its Electromagnetics Development Center during 2003, which resulted in a pre-tax gain of $17,415. |

| 7. | The company sold Kaman Music Corporation on December 31, 2007, which resulted in a pre-tax gain of $18,065, and the Fuzing segment’s 40mm product line assets, which resulted in a pre-tax gain of $2,570. |

22

| ITEM 7. | MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND |

Management’s Discussion and Analysis of Financial Condition and Results of Operations (MD&A) is intended to provide readers of our consolidated financial statements with the perspectives of management. The MD&A presents in a narrative form information regarding our financial condition, results of operations, liquidity and certain other factors that may affect our future results. This will allow our shareholders to obtain a comprehensive understanding of our businesses, strategies, current trends and future prospects. Our MD&A is presented in seven sections:

| | III. | Results of Operations |

| | IV. | Liquidity and Capital Resources |

| | V. | Critical Accounting Estimates |

| | VI. | Contractual Obligations and Off-Balance Sheet Arrangements |

| | VII. | Recent Accounting Standards |

Our MD&A should be read in conjunction with the Consolidated Financial Statements and related Notes included in this Form 10-K. Unless otherwise noted, this MD&A relates only to results from continuing operations. All years presented reflect the classification of Kaman Music’s financial results as discontinued operations.

I. OVERVIEW OF BUSINESS

Kaman Corporation is composed of five business segments:

| | • | | Aerostructures, a provider of subassemblies for commercial and military aircraft; |

| | • | | Fuzing, a producer of fuzing devices and memory and measuring systems for a variety of applications; |

| | • | | Helicopters, a provider of upgrades and support for its existing fleet as well as a subcontractor for other aerospace manufacturers; |

| | • | | Specialty Bearings, a manufacturer of high-performance mechanical products used in aviation, marine, hydropower, and other industrial applications; and |

| | • | | Industrial Distribution, the third largest power transmission/motion control industrial distributor in North America. |

Our long-term strategy is specific to each segment. For our aerospace businesses, we seek to maintain leadership in product technical performance, take advantage of opportunities arising from the prime and Tier 1 producers as they increasingly seek to outsource aircraft production tasks, and build on our strengths in areas targeted for growth through internal product development and acquisitions. For our industrial distribution business our long-term strategy involves acquisitions and internal means to expand our geographical footprint in major industrial markets and broaden our product lines to enhance our competitive position for national accounts. An overall strategy is to further enhance operating and asset utilization efficiencies throughout the enterprise.

II. EXECUTIVE SUMMARY

The following is a summary of key events that occurred during 2007:

| | • | | On September 17, 2007, Neal J. Keating joined the company as President and Chief Operating Officer and a member of the Board of Directors. Mr. Keating assumed the position of President and Chief Executive Officer on January 1, 2008. Mr. Paul Kuhn, the retiring President and CEO, is expected to continue to serve as Chairman until his scheduled retirement on February 29, 2008. |

23

| | • | | We sold our Music segment on December 31, 2007 for $119.5 million to Fender and recorded a pre-tax gain of $18.1 million. |

| | • | | We also sold the assets of our Fuzing segment’s 40mm product line on December 31, 2007 to DSE, Inc. and recorded a pre-tax gain of $2.6 million. |

| | • | | In December 2007, we redeemed the last of our outstanding 6% convertible subordinated debentures. |

| | • | | We increased our quarterly dividend by 12 percent to $0.14 per share, reflecting the continuing progress we have made over the past several years and our confidence in the company’s competitive position in the principal markets we serve. |

| | • | | The Aerostructures, Fuzing and Specialty Bearings segments continued to improve profitability through operating efficiencies and further developing relationships with many key customers including Sikorsky, Boeing and Airbus, which resulted in the broadening of our business base. |

| | • | | Our Industrial Distribution segment continued to win new national account contracts that have allowed us to increase our business base and further diversify our broad array of products. |

| | • | | Our net sales from continuing operations for 2007 were $1.1 billion, an increase of 9.5 percent over 2006, with our Specialty Bearings segment and the Industrial Distribution segment generating record sales for 2007. |

| | • | | Net earnings from continuing operations were $36.5 million, or $1.46 per share diluted, compared to net earnings from continuing operations for 2006 of $24.6 million, or $1.01 per share diluted. The increase was due in significant part to higher sales volume, increased gross profit and continued focus on controlling operating expenses. |

III. RESULTS OF CONTINUING OPERATIONS

CONSOLIDATED RESULTS

Net Sales

| | | | | | | | | | | | |

| In thousands | | 2007 | | | 2006 | | | 2005 | |

Aerostructures | | $ | 102,362 | | | $ | 78,742 | | | $ | 54,983 | |

Fuzing | | | 87,455 | | | | 71,068 | | | | 64,069 | |

Helicopters | | | 72,031 | | | | 69,914 | | | | 76,652 | |

Specialty Bearings | | | 124,009 | | | | 106,278 | | | | 92,241 | |

Subtotal Aerospace Segments | | $ | 385,857 | | | $ | 326,002 | | | $ | 287,945 | |

Industrial Distribution | | | 700,174 | | | | 665,420 | | | | 621,933 | |

Total | | $ | 1,086,031 | | | $ | 991,422 | | | $ | 909,878 | |

| | |

$ change | | $ | 94,609 | | | $ | 81,544 | | | $ | 75,687 | |

% change | | | 9.5 | % | | | 9.0 | % | | | 9.1 | % |

2007 vs. 2006

The growth in consolidated net sales for 2007 compared to 2006 was primarily due to increased shipments on several key product lines in our Aerostructures, Fuzing and Specialty Bearing segments, which was driven by the currently strong commercial and military aerospace markets. Our Industrial Distribution segment experienced sales growth during 2007 as a result of several new national accounts and continued strength in the Central and West regions.

2006 vs. 2005

The increase in sales was mainly due to higher organic sales, attributable to a variety of factors including an improved economic environment in the aerospace industry as well as stability in most of the markets in which the Industrial Distribution segment participated.

24

Gross Profit

| | | | | | | | | | | | |

| In thousands | | 2007 | | | 2006 | | | 2005 | |

Gross Profit | | $ | 300,945 | | | $ | 271,423 | | | $ | 231,451 | |

$ change | | | 29,522 | | | $ | 39,972 | | | | 54,170 | |

% change | | | 10.9 | % | | | 17.3 | % | | | 30.6 | % |

% of net sales | | | 27.7 | % | | | 27.4 | % | | | 25.4 | % |

2007 vs. 2006

The increase in the consolidated gross profit for 2007 was primarily attributable to sales growth in the Industrial Distribution and Specialty Bearings segments. In addition, the accrued contract loss charge related to additional anticipated cost growth on our Helicopters segment’s Australia program was $6.4 million for 2007 as compared to $9.7 million in 2006. Gross profit as a percentage of sales (gross margin) has improved slightly due to higher sales volume, increased efficiencies and a growing business base at all of our aerospace reporting segments.

2006 vs. 2005

The 2006 gross profit included $9.7 million in charges for our Helicopters segment’s Australia helicopter program as compared to $16.8 million in 2005. Both the 2006 and 2005 charges were offset by an increase in overall gross profit, primarily due to higher sales volume, at the other Aerospace Segments and the Industrial Distribution segment. The 2005 gross profit includes a recovery of $4.6 million related to certain amounts due from MD Helicopters, Inc. (MDHI) that were previously written off. Gross profit as a percentage of sales (gross margin) improved during 2006 primarily as a result of increased efficiencies, higher sales volume and a growing business base at our Aerostructures, Fuzing and Specialty Bearings segments as well as continued focus on gross margin improvement in our Industrial Distribution segment.

Selling, General & Administrative Expenses (S,G&A)

| | | | | | | | | | | | |

| In thousands | | 2007 | | | 2006 | | | 2005 | |

S,G&A | | $ | 238,796 | | | $ | 223,549 | | | $ | 211,683 | |

$ change | | | 15,247 | | | | 11,866 | | | | 10,588 | |

% change | | | 6.8 | % | | | 5.6 | % | | | 5.3 | % |

% of net sales | | | 22.0 | % | | | 22.5 | % | | | 23.3 | % |

2007 vs. 2006

The increase in S,G&A for 2007 compared to 2006 was primarily driven by our Industrial Distribution segment and corporate expenses. Our Industrial Distribution segment experienced higher operating expenses due to additional costs incurred for new branch openings and overall increased personnel costs. Corporate expense increased primarily as a result of an increase in stock compensation expense and higher group insurance expense. Total selling, general and administrative expenses as a percent of net sales decreased 0.5 percentage points in 2007 compared to 2006. This was primarily due to greater sales volume as well as continued cost control efforts.

2006 vs. 2005