Great Plains Energy

Wall Street Access and

Berenson & Company

Midwest Utilities Seminar

April 10, 2008

William Downey, CEO

Kansas City Power & Light

Michael Cline, VP - Investor Relations and Treasurer

Great Plains Energy

Exhibit 99.1

2

FORWARD-LOOKING STATEMENTS

Statements made in this release that are not based on historical facts are forward-looking, may involve risks and

uncertainties, and are intended to be as of the date when made. Forward-looking statements include, but are not limited to,

statements regarding projected delivered volumes and margins, the outcome of regulatory proceedings, cost estimates of

the comprehensive energy plan and other matters affecting future operations. In connection with the safe harbor provisions

of the Private Securities Litigation Reform Act of 1995, the registrants are providing a number of important factors that could

cause actual results to differ materially from the provided forward-looking information. These important factors include:

future economic conditions in the regional, national and international markets, including but not limited to regional and

national wholesale electricity markets; market perception of the energy industry, Great Plains Energy and KCP&L; changes in

business strategy, operations or development plans; effects of current or proposed state and federal legislative and

regulatory actions or developments, including, but not limited to, deregulation, re-regulation and restructuring of the electric

utility industry; decisions of regulators regarding rates KCP&L can charge for electricity; adverse changes in applicable laws,

regulations, rules, principles or practices governing tax, accounting and environmental matters including, but not limited to,

air and water quality; financial market conditions and performance including, but not limited to, changes in interest rates and

in availability and cost of capital and the effects on pension plan assets and costs; credit ratings; inflation rates;

effectiveness of risk management policies and procedures and the ability of counterparties to satisfy their contractual

commitments; impact of terrorist acts; increased competition including, but not limited to, retail choice in the electric utility

industry and the entry of new competitors; ability to carry out marketing and sales plans; weather conditions including

weather-related damage; cost, availability, quality and deliverability of fuel; ability to achieve generation planning goals and

the occurrence and duration of unplanned generation outages; delays in the anticipated in-service dates and cost increases

of additional generating capacity; nuclear operations; ability to enter new markets successfully and capitalize on growth

opportunities in non-regulated businesses and the effects of competition; workforce risks including compensation and

benefits costs; performance of projects undertaken by non-regulated businesses and the success of efforts to invest in and

develop new opportunities; the ability to successfully complete merger, acquisition or divestiture plans (including the

acquisition of Aquila, Inc., and Aquila’s sale of assets to Black Hills Corporation); risks that the transaction for Strategic

Energy, L.L.C. may not close and other risks and uncertainties. Other risk factors are detailed from time to time in Great

Plains Energy’s most recent quarterly report on Form 10-Q or annual report on Form 10-K filed with the Securities and

Exchange Commission. This list of factors is not all-inclusive because it is not possible to predict all factors.

uncertainties, and are intended to be as of the date when made. Forward-looking statements include, but are not limited to,

statements regarding projected delivered volumes and margins, the outcome of regulatory proceedings, cost estimates of

the comprehensive energy plan and other matters affecting future operations. In connection with the safe harbor provisions

of the Private Securities Litigation Reform Act of 1995, the registrants are providing a number of important factors that could

cause actual results to differ materially from the provided forward-looking information. These important factors include:

future economic conditions in the regional, national and international markets, including but not limited to regional and

national wholesale electricity markets; market perception of the energy industry, Great Plains Energy and KCP&L; changes in

business strategy, operations or development plans; effects of current or proposed state and federal legislative and

regulatory actions or developments, including, but not limited to, deregulation, re-regulation and restructuring of the electric

utility industry; decisions of regulators regarding rates KCP&L can charge for electricity; adverse changes in applicable laws,

regulations, rules, principles or practices governing tax, accounting and environmental matters including, but not limited to,

air and water quality; financial market conditions and performance including, but not limited to, changes in interest rates and

in availability and cost of capital and the effects on pension plan assets and costs; credit ratings; inflation rates;

effectiveness of risk management policies and procedures and the ability of counterparties to satisfy their contractual

commitments; impact of terrorist acts; increased competition including, but not limited to, retail choice in the electric utility

industry and the entry of new competitors; ability to carry out marketing and sales plans; weather conditions including

weather-related damage; cost, availability, quality and deliverability of fuel; ability to achieve generation planning goals and

the occurrence and duration of unplanned generation outages; delays in the anticipated in-service dates and cost increases

of additional generating capacity; nuclear operations; ability to enter new markets successfully and capitalize on growth

opportunities in non-regulated businesses and the effects of competition; workforce risks including compensation and

benefits costs; performance of projects undertaken by non-regulated businesses and the success of efforts to invest in and

develop new opportunities; the ability to successfully complete merger, acquisition or divestiture plans (including the

acquisition of Aquila, Inc., and Aquila’s sale of assets to Black Hills Corporation); risks that the transaction for Strategic

Energy, L.L.C. may not close and other risks and uncertainties. Other risk factors are detailed from time to time in Great

Plains Energy’s most recent quarterly report on Form 10-Q or annual report on Form 10-K filed with the Securities and

Exchange Commission. This list of factors is not all-inclusive because it is not possible to predict all factors.

Forward Looking Statement

3

¾ $2.1 billion market capitalization

¾ $4.8 billion in total assets as of 12/31/07

¾ $3.3 billion in revenues as of 12/31/07

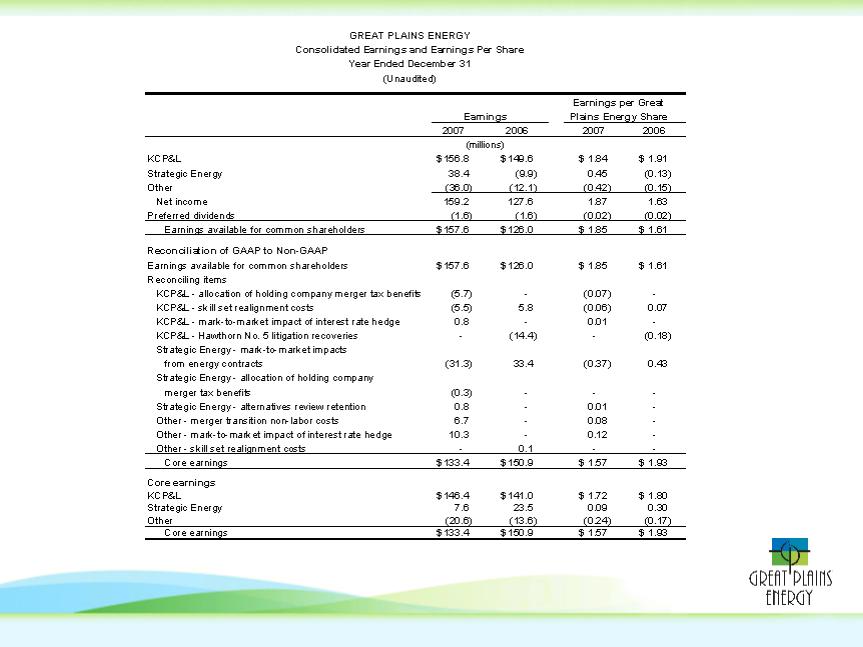

¾ $133.4 million of core earnings or $1.57/share in 2007*

Regulated electric utility:

• $146.4 million in core earnings or

$1.72/share in 2007

$1.72/share in 2007

• 506,000 customers in KS and MO

• Total generation capacity: 4,048 MWs

Comprehensive Energy Plan

GXP is expanding its regulated platform with

the proposed Aquila transaction

the proposed Aquila transaction

Competitive retail electricity provider:

• $7.6 million in core earnings or

$0.09/share in 2007

$0.09/share in 2007

• Serving approximately 109,000

accounts & 25,700 customers

accounts & 25,700 customers

GXP announced sale of business

*Also includes $(20.6) million of other earnings that includes the company’s investments in

affordable housing and unallocated corporate charges.

Note: All numbers as of year-end 2007

Great Plains Energy Overview

4

GXP - - A Compelling Investment Thesis

• Realizable growth in regulated business:

¾ Focused strategy with anticipated sale of Strategic Energy in Q2 2008

¾ Aquila transaction complements KCP&L and adds scale and scope

¾ Rate base growth at KCP&L driven by Comprehensive Energy Plan

• Low-cost generating platform; high reliability and customer satisfaction

levels in our distribution business

levels in our distribution business

• Attractive investment profile:

¾ Solid dividend with future growth potential - current dividend yield

approximately 6.6%

approximately 6.6%

¾ Solid investment grade rating

¾ Executing our growth plan

5

üNovember 2007, GXP announced intent to evaluate strategic

alternatives for Strategic Energy

alternatives for Strategic Energy

üApril 2008, announced definitive agreement for sale of the

business to Direct Energy, a subsidiary of Centrica, plc

business to Direct Energy, a subsidiary of Centrica, plc

¾ Price - $300 million in cash including working capital (approximately

$120 million at 12/31/07); to be adjusted for working capital and

severance adjustments at close

$120 million at 12/31/07); to be adjusted for working capital and

severance adjustments at close

• Expect to complete sale in late Q2 2008

• Cash will be used to offset some of Great Plains Energy’s 2008

anticipated financing needs

anticipated financing needs

Strategic Energy Update

6

Impact on Great Plains Energy

Expected Cash Proceeds

Additional Benefits

• In addition to the cash proceeds from

the transaction, there are also several

additional benefits to Great Plains

Energy from the sale of Strategic

Energy:

the transaction, there are also several

additional benefits to Great Plains

Energy from the sale of Strategic

Energy:

¾ Reduction in overall Company

credit support due to fewer letters

of credit and guarantees

outstanding

credit support due to fewer letters

of credit and guarantees

outstanding

¾ Reduced volatility in the GAAP

income statement due to the

elimination of Strategic Energy’s

mark-to-market accounting

income statement due to the

elimination of Strategic Energy’s

mark-to-market accounting

¾ A reduction in imputed debt from

the rating agencies

the rating agencies

¾ Great Plains Energy’s management

team’s sole focus will be the core

utility business

team’s sole focus will be the core

utility business

• The purchase price of $300 million is

subject to various closing adjustments

including working capital (as defined in

the agreement) and severance

adjustments

subject to various closing adjustments

including working capital (as defined in

the agreement) and severance

adjustments

After Tax Cash Proceeds to Great Plains

$269.2

$287.8

Amount ($mm) | |

Purchase Price from Direct Energy* | $300.0 |

Approx. Tax Basis in Strategic** | $225.0 |

Difference | $ 75.0 |

Taxes Due at 38% | $ 29.0 |

Approximate after tax cash proceeds to Great Plains Energy | $271.0* |

* Subject to adjustments for working capital and severance

** As of 12/31/07

Aquila Acquisition

Update

8

+

FORGING A STRONGER

REGIONAL UTILITY

ü Strong support for transaction from

shareholders of both companies

shareholders of both companies

ü FERC approval received

ü Nebraska, Iowa, & Colorado approval of Black

Hills transaction

Hills transaction

ü Kansas approval for Black Hills and Great

Plains Energy transactions

Plains Energy transactions

• Missouri hearings to begin April 21

• Transaction currently anticipated to close in

Q2 2008

Q2 2008

Aquila Transaction Update

9

• Allowed recovery of $10 million of transition costs as five-year

amortization starting with rates effective for Iatan 2 case

(anticipated in Fall 2010)

amortization starting with rates effective for Iatan 2 case

(anticipated in Fall 2010)

• Due to regulatory lag, no material synergy give-back until rates

set in the Iatan 2 rate case

set in the Iatan 2 rate case

• No tracking of synergies

• No litigation of merger costs or synergies

Kansas Agreement

10

Previous “ask” | Current “ask” |

•Immediate approval for retention of 50% of utility operational synergies ($260 million net of transition costs) over 5 years | •Recovery of utility operational synergies through traditional ratemaking process •Regulatory lag expected to provide opportunity for the retention of approximately 50% of the synergies |

•Recovery of 50% of transition costs ($45 million) over 5 years | •Recovery of 100% of updated transition cost ($58.9 million) over five years |

•Recovery of 100% of the transaction costs ($95 million) over 5 years | •Recovery of 100% of the revised transaction costs ($64.9 million) over 5 years •Company no longer requesting recovery of CIC and Rabbi Trust for Senior Aquila officers |

•Recovery requested of actual interest costs in Aquila customer rates | •No recovery of Aquila actual interest costs in excess of equivalent investment grade costs |

•Authorization to use additional amortizations in Aquila rate cases to meet credit metrics, consistent with KCP&L’s treatment | •Will include as a component in a future regulatory plan for Aquila |

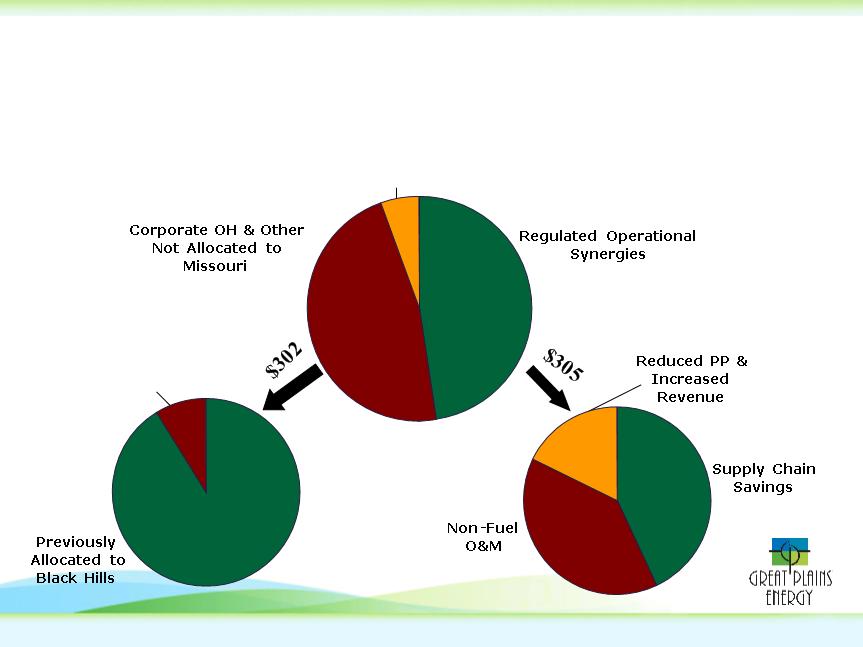

Amounts shown are total amounts before allocations between Missouri and Kansas jurisdictions.

11

Great Plains Energy expects to realize $675 million of total savings

and synergies over five years

and synergies over five years

Interest Savings

Corporate Retained

& Merchant Savings

& Merchant Savings

$302

$305

$68

$120

$131

$54

$27

$275

Significant Synergies Expected

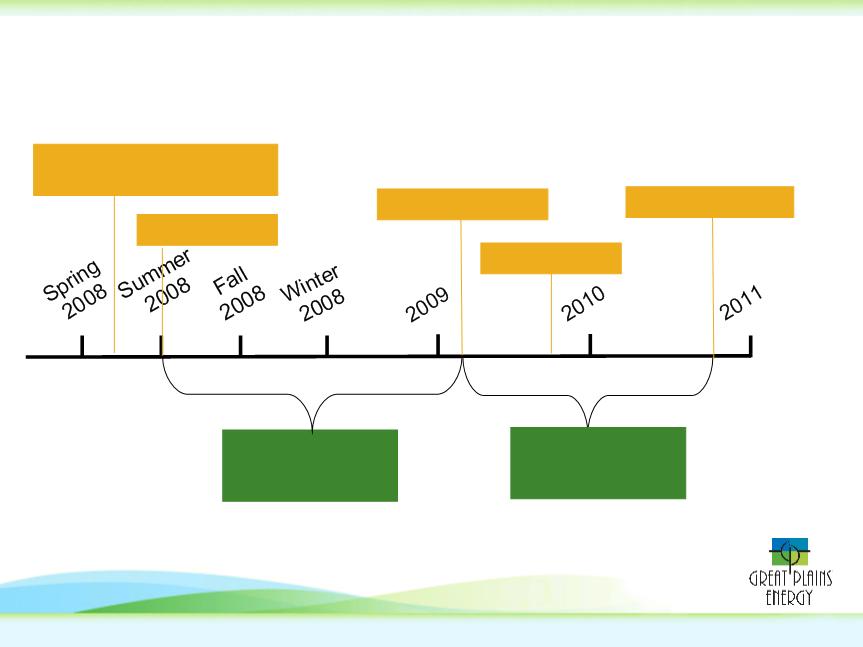

12

Missouri Hearings,

Approval and Close

Approval and Close

Shareholders

receive benefits

of synergies

receive benefits

of synergies

File rate case

File rate case

Shareholders

receive benefits

of new synergies

receive benefits

of new synergies

Rates effective

Rates effective

Path to Synergy Sharing

13

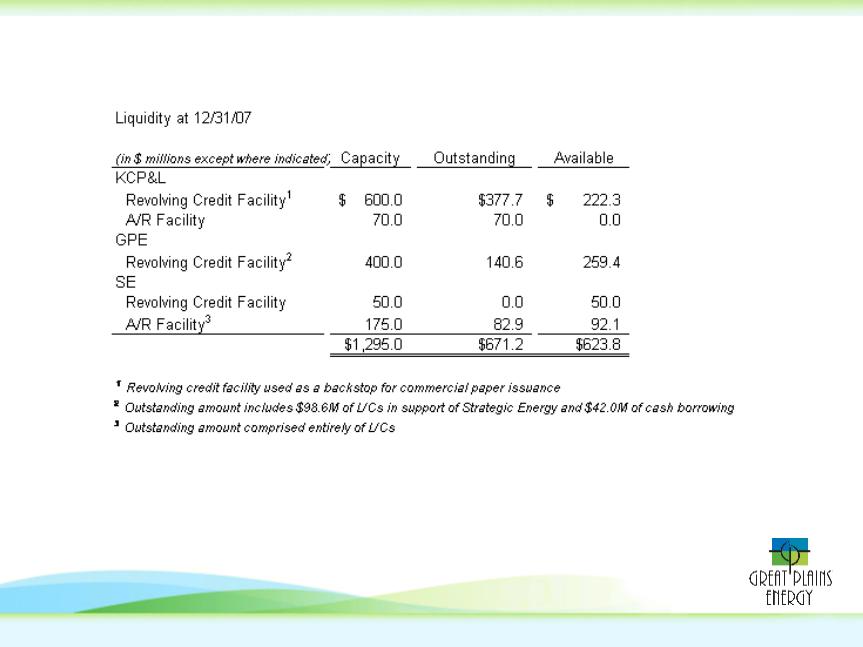

• KCP&L is weathering turbulent markets effectively:

¾ Converted entire auction rate debt portfolio to fixed rate

¾ Issued $350 million of new 10-year bonds at 6.375%

• Proceeds from sale of Strategic Energy to partially offset 2008

financing needs

financing needs

Strong Liquidity and Capital Markets

Access

Access

William Downey, CEO

Kansas City Power & Light

15

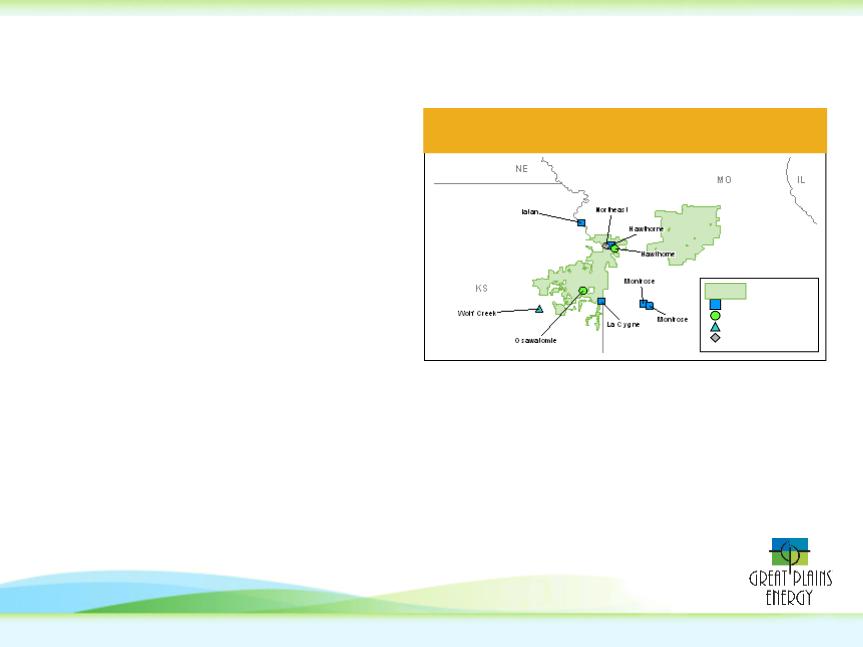

• Headquartered in Kansas City,

Missouri

Missouri

• Engage in the generation,

transmission, distribution and sale of

electricity

transmission, distribution and sale of

electricity

• $4.3 billion in assets at year-end 2007

• Serve approximately 506,000

customers located in western Missouri

and eastern Kansas

customers located in western Missouri

and eastern Kansas

• Total generation capacity: 4,048 MWs

• Regulated by commissions in two

states:

states:

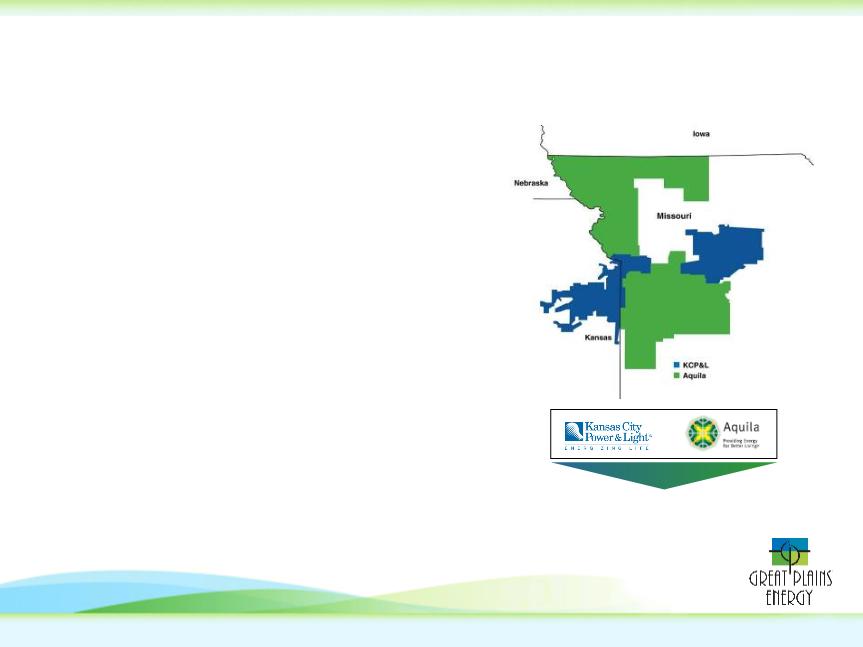

KCP&L Service Territory

Coal

Gas

Nuclear

Oil

KCP&L

Missouri:

¾ Public Service Commission of the State of Missouri (MPSC)

¾ KCP&L’s MO jurisdictional revenues averaged 57% over the last 3 years

Kansas:

¾ The State Corporation Commission of the State of Kansas (KCC)

¾ KCP&L’s KS jurisdictional revenues averaged 43% over the

last 3 years

KCP&L Overview

16

EEI Edison Award - - Kansas City Power & Light was recognized for distinguished leadership,

innovation and contribution to the advancement of the electric industry for its Comprehensive

Energy Plan collaboration. (June 2007)

innovation and contribution to the advancement of the electric industry for its Comprehensive

Energy Plan collaboration. (June 2007)

EEI Outstanding Customer Service Award voted Kansas City Power & Light the winner of

this award for medium-sized utility. (May 2007)

this award for medium-sized utility. (May 2007)

J.D. Power and Associates recognizes Tier 1 performance. In the Midwest, KCP&L

ranks No. 1 on Communications; No. 2 on Power Quality and Reliability, and Billing and

Payment; and No. 3 in Overall Satisfaction. (February 2007)

ranks No. 1 on Communications; No. 2 on Power Quality and Reliability, and Billing and

Payment; and No. 3 in Overall Satisfaction. (February 2007)

2007 ReliabilityOne™ National Reliability Excellence Award presented by PA Consulting

Group to Kansas City Power & Light as the most reliable electric utility nationwide. (October

2007)

Group to Kansas City Power & Light as the most reliable electric utility nationwide. (October

2007)

EEI Emergency Assistance Award for outstanding efforts to assist fellow utilities in power

restoration during 2007. (January 2008)

restoration during 2007. (January 2008)

2007 Mid-America Regional Council’s Regional Leadership Award presented to Kansas

City Power & Light for its outstanding environmental initiatives in metropolitan Kansas City.

(June 2007)

City Power & Light for its outstanding environmental initiatives in metropolitan Kansas City.

(June 2007)

David Garcia Award for Environmental Excellence presented by Bridging the Gap for the

groundbreaking Collaborative Agreement with Sierra Club and Concerned Citizens of

Platte County. (October 2007)

groundbreaking Collaborative Agreement with Sierra Club and Concerned Citizens of

Platte County. (October 2007)

Recognized Excellence in 2007

17

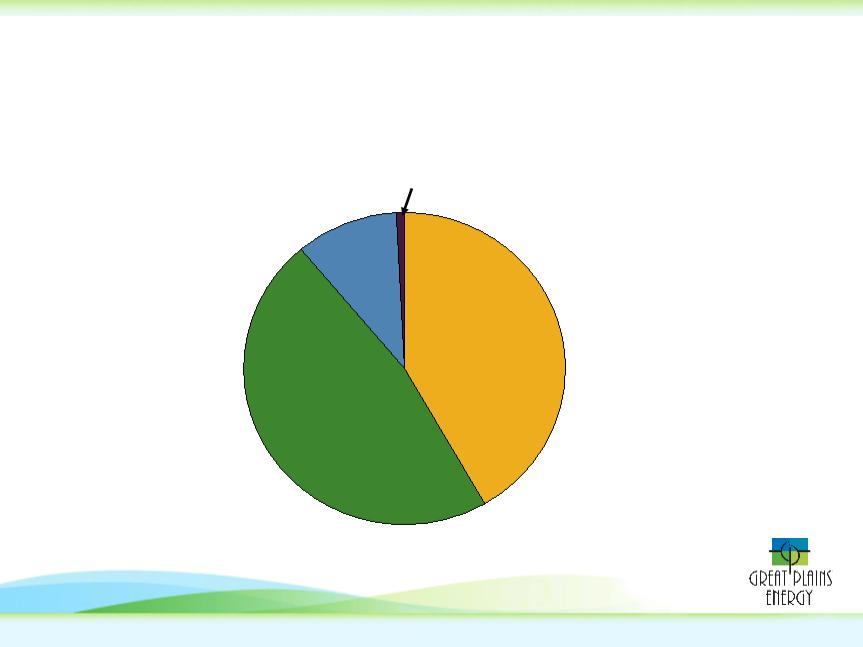

Other

Residential:

• 446,100 customers

• Revenues: $433.8 million

• 5,597 MWh sales

Commercial:

• 57,600 customers

• Revenues: $492.1 million

• 7,737 MWh sales

Industrial:

• 2,300 industrial customers,

• Revenues: $106.8 million

• 2,161 MWh sales

Customer Mix Based on 2007 Revenues

Note: All numbers as of year-end 2007

KCP&L - A Steady Retail Customer Base

18

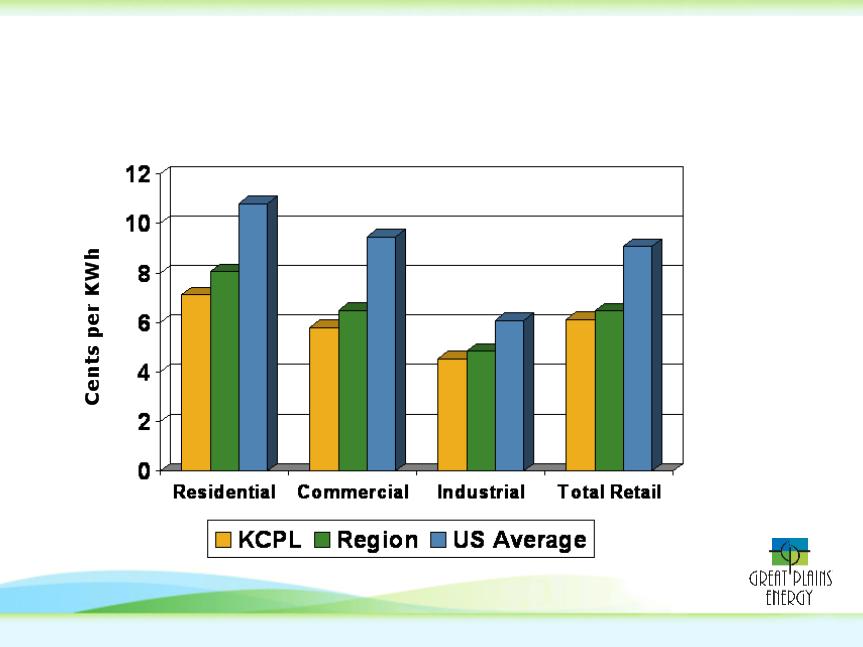

Source: “EEI Typical Bill Rankings Report and Typical Bill/Avg Rates Report for 12 month ended June

2007” Note: all rate actions after June 30, 2007 are not reflected in this chart including KCP&L’s new

annual rate increases in MO and KS that were implemented January 1, 2008

2007” Note: all rate actions after June 30, 2007 are not reflected in this chart including KCP&L’s new

annual rate increases in MO and KS that were implemented January 1, 2008

*

KCP&L Prices Compare Favorably on

National & Regional Basis

National & Regional Basis

19

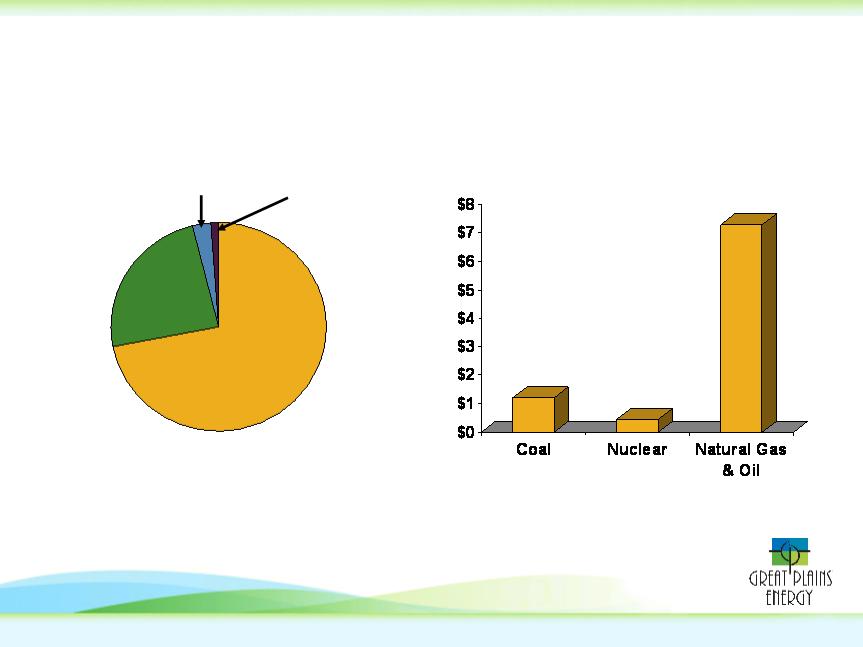

Wind 1%

Natural Gas & Oil - 3%

Nuclear - - 24%

Coal - - 72%

$1.23

$0.45

$7.30

Fuel costs in cents per

Net KWh generated

Fuel Mix

Fuel Costs

Strong, low cost coal and nuclear generation provides KCP&L stable,

competitive generation fleet in a volatile market

Note: All numbers as of year-end 2007

Low-Cost Diverse Generating Fleet

20

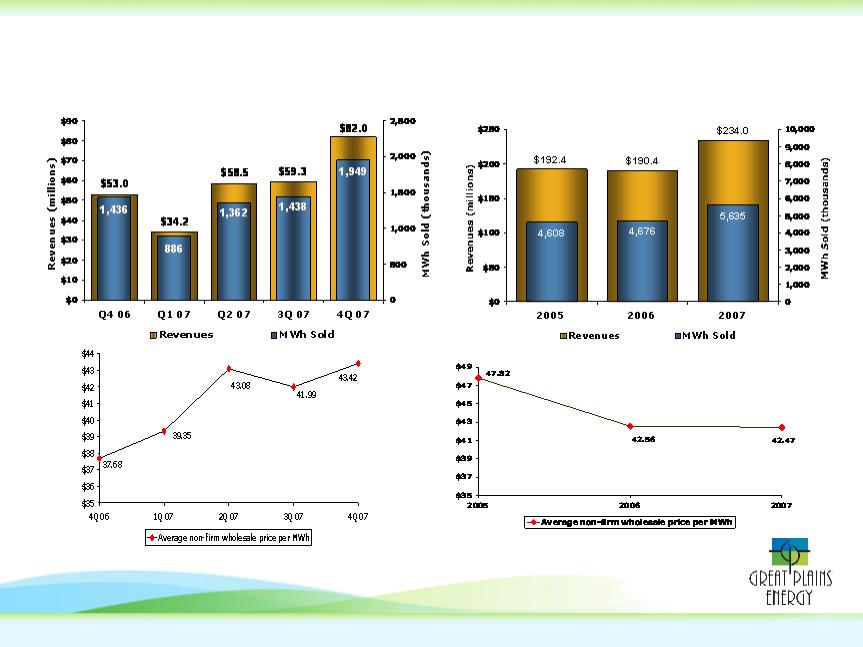

Q4 2006 - Q4 2007

2005 - - 2007

KCP&L Wholesale Power Performance

21

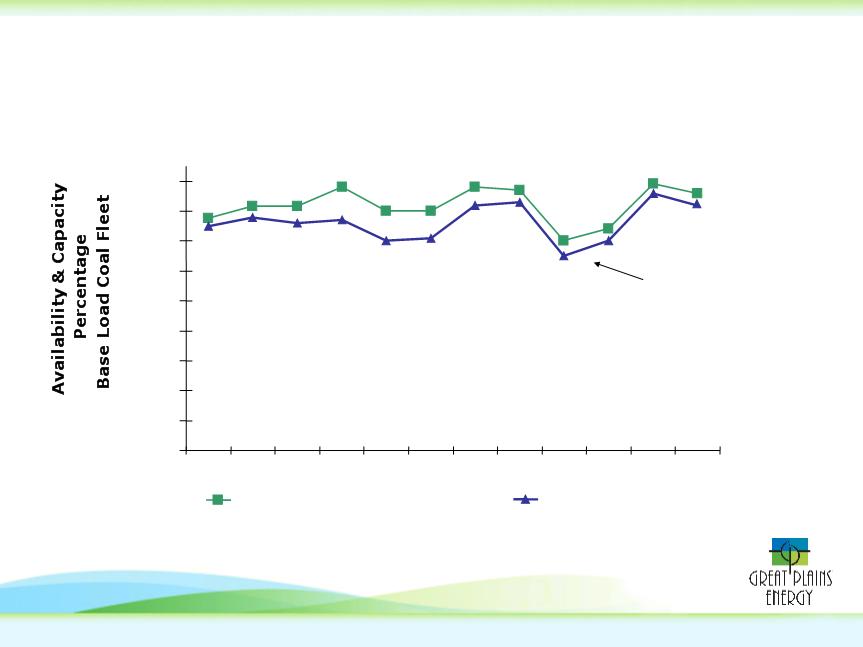

Impact of unplanned

outages in Q1 &Q2

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Q1 05

Q2 05

Q3 05

Q4 05

Q1 06

Q2 06

Q3 06

Q4 06

Q1 07

Q2 07

Q3 07

Q4 07

Equivalent Availability Factor

Capacity Factor

Base Load Coal Fleet

Equivalent Availability / Capacity

22

Spearville Wind Energy Facility

ü 100MW completed on schedule and on budget

LaCygne

ü Phase 1: Unit 1 SCR - Completed on schedule, under budget, and

performing per specification

performing per specification

• Phase 2: Unit 1 - bag house and scrubber environmental upgrades:

¾ Project Definition Report completed in Q3 2007

¾ Revised cost estimates higher than initial estimates

Iatan Unit 1

• AQCS Environmental Project to be completed late 2008 - early 2009

Iatan Unit 2 Construction

• Cost / schedule re-assessment underway; results available in Q2

Comprehensive Energy Plan Progress

23

• Develop long range resource plan and file Integrated Resource Plan in

Missouri in August 2008

Missouri in August 2008

• Continue to engage community and regulators to develop energy

efficiency and demand response as resource alternatives:

efficiency and demand response as resource alternatives:

¾ Potential energy efficiency projects designed to reduce annual

electricity demand 100MW by 2010; additional 200MW by 2012

• Continue development of environmental and renewable generation

alternatives

alternatives

• Potential to pursue an additional 400MW wind generation:

¾ 100MW by 2010 and additional 300MW by 2012

• Expected future Phase 3 environmental upgrades at LaCygne Unit 2 for

BART

BART

Developing Collaborative Resource

Strategy

Strategy

24

Annual Revenue Increase | ||||||||

Rate Case | Order Date | Traditional | Additional Amortization | Total | Rate Base | Return on Equity | Rate- making Equity Ratio | Rate of Return |

MO | 12/6/07 | $24.6 | $10.7 | $35.3 | $1,298 | 10.75% | 58% | 8.68% |

KS | 11/20/07 | $17.0 | $11.0 | $28.0 | n/a | n/a | n/a | n/a |

$ in millions

•Primary driver of 2007 rate cases was La Cygne Unit 1 SCR

•2007 Kansas rate case:

¾ Negotiated settlement

¾ Energy cost adjustment implemented

¾ Energy efficiency rider implemented

•Missouri and Kansas rate cases expected to be filed in summer 2008;

primary driver will be Iatan Unit 1 AQCS

Regulatory Update

25

2009 and beyond: Extend the platform

• Include Iatan 1 AQCS in rates effective in 2009

• Complete Iatan 2 and incorporate into rates in 2010

• Fully integrate Aquila and demonstrate ability to deliver on

synergies

synergies

• Pursue Collaborative Resource Strategy initiatives

A Path to Growth

Great Plains Energy

Wall Street Access and

Berenson & Company

Midwest Utilities Seminar

April 10, 2008

27

Core earnings is a non-GAAP financial measure that differs from GAAP earnings because it excludes the effects of certain unusual items and mark-to-market gains and losses on energy

contracts. Great Plains Energy believes core earnings provides to investors a meaningful indicator of its results that is comparable among periods because it excludes the effects of items that

may not be indicative of Great Plains Energy’s prospective earnings potential. Core earnings is used internally to measure performance against budget and in reports for management and the

Board of Directors and are a component, subject to adjustment, of employee and executive incentive compensation plans. Investors should note that this non-GAAP measure involves

judgments by management, including whether an item is classified as an unusual item, and Great Plains Energy’s definition of core earnings may differ from similar terms used by other

companies. The impact of these items could be material to operating results presented in accordance with GAAP. Great Plains Energy is unable to reconcile core earnings guidance to GAAP

earnings per share because it does not predict the future impact of unusual items and mark-to-market gains or losses on energy contracts.

contracts. Great Plains Energy believes core earnings provides to investors a meaningful indicator of its results that is comparable among periods because it excludes the effects of items that

may not be indicative of Great Plains Energy’s prospective earnings potential. Core earnings is used internally to measure performance against budget and in reports for management and the

Board of Directors and are a component, subject to adjustment, of employee and executive incentive compensation plans. Investors should note that this non-GAAP measure involves

judgments by management, including whether an item is classified as an unusual item, and Great Plains Energy’s definition of core earnings may differ from similar terms used by other

companies. The impact of these items could be material to operating results presented in accordance with GAAP. Great Plains Energy is unable to reconcile core earnings guidance to GAAP

earnings per share because it does not predict the future impact of unusual items and mark-to-market gains or losses on energy contracts.