Great Plains Energy

Merrill Lynch

Power and Gas Conference

September 23-24, 2008

Exhibit 99.1

Terry Bassham, CFO

Executive Vice President

Finance & Strategic Development

Executive Vice President

Finance & Strategic Development

1

Statements made in this presentation that are not based on historical facts are forward-looking, may involve

risks and uncertainties, and are intended to be as of the date when made. Forward-looking statements include,

but are not limited to, the outcome of regulatory proceedings, cost estimates of the Comprehensive Energy Plan

and other matters affecting future operations. In connection with the safe harbor provisions of the Private

Securities Litigation Reform Act of 1995, the registrants are providing a number of important factors that could

cause actual results to differ materially from the provided forward-looking information. These important factors

include: future economic conditions in the regional, national and international markets, including but not limited

to regional and national wholesale electricity markets; market perception of the energy industry, Great Plains

Energy, Kansas City Power & Light Company (KCP&L) and Aquila, which is doing business as KCP&L Greater

Missouri Operations Company (KCP&L GMO); changes in business strategy, operations or development plans;

effects of current or proposed state and federal legislative and regulatory actions or developments, including, but

not limited to, deregulation, re-regulation and restructuring of the electric utility industry; decisions of regulators

regarding rates KCP&L and KCP&L GMO can charge for electricity; adverse changes in applicable laws,

regulations, rules, principles or practices governing tax, accounting and environmental matters including, but not

limited to, air and water quality; financial market conditions and performance including, but not limited to,

changes in interest rates and credit spreads and in availability and cost of capital and the effects on pension plan

assets and costs; credit ratings; inflation rates; effectiveness of risk management policies and procedures and

the ability of counterparties to satisfy their contractual commitments; impact of terrorist acts; increased

competition including, but not limited to, retail choice in the electric utility industry and the entry of new

competitors; ability to carry out marketing and sales plans; weather conditions including weather-related

damage; cost, availability, quality and deliverability of fuel; ability to achieve generation planning goals and the

occurrence and duration of planned and unplanned generation outages; delays in the anticipated in-service dates

and cost increases of additional generating capacity and environmental projects; nuclear operations; workforce

risks, including retirement compensation and benefits costs; the ability to successfully integrate KCP&L and

KCP&L GMO operations and the timing and amount of resulting synergy savings; and other risks and

uncertainties. Other risk factors are detailed from time to time in Great Plains Energy’s and KCP&L’s most recent

quarterly reports on Form 10-Q or Annual Reports on Form 10-K filed with the Securities and Exchange

Commission. This list of factors is not all-inclusive because it is not possible to predict all factors.

risks and uncertainties, and are intended to be as of the date when made. Forward-looking statements include,

but are not limited to, the outcome of regulatory proceedings, cost estimates of the Comprehensive Energy Plan

and other matters affecting future operations. In connection with the safe harbor provisions of the Private

Securities Litigation Reform Act of 1995, the registrants are providing a number of important factors that could

cause actual results to differ materially from the provided forward-looking information. These important factors

include: future economic conditions in the regional, national and international markets, including but not limited

to regional and national wholesale electricity markets; market perception of the energy industry, Great Plains

Energy, Kansas City Power & Light Company (KCP&L) and Aquila, which is doing business as KCP&L Greater

Missouri Operations Company (KCP&L GMO); changes in business strategy, operations or development plans;

effects of current or proposed state and federal legislative and regulatory actions or developments, including, but

not limited to, deregulation, re-regulation and restructuring of the electric utility industry; decisions of regulators

regarding rates KCP&L and KCP&L GMO can charge for electricity; adverse changes in applicable laws,

regulations, rules, principles or practices governing tax, accounting and environmental matters including, but not

limited to, air and water quality; financial market conditions and performance including, but not limited to,

changes in interest rates and credit spreads and in availability and cost of capital and the effects on pension plan

assets and costs; credit ratings; inflation rates; effectiveness of risk management policies and procedures and

the ability of counterparties to satisfy their contractual commitments; impact of terrorist acts; increased

competition including, but not limited to, retail choice in the electric utility industry and the entry of new

competitors; ability to carry out marketing and sales plans; weather conditions including weather-related

damage; cost, availability, quality and deliverability of fuel; ability to achieve generation planning goals and the

occurrence and duration of planned and unplanned generation outages; delays in the anticipated in-service dates

and cost increases of additional generating capacity and environmental projects; nuclear operations; workforce

risks, including retirement compensation and benefits costs; the ability to successfully integrate KCP&L and

KCP&L GMO operations and the timing and amount of resulting synergy savings; and other risks and

uncertainties. Other risk factors are detailed from time to time in Great Plains Energy’s and KCP&L’s most recent

quarterly reports on Form 10-Q or Annual Reports on Form 10-K filed with the Securities and Exchange

Commission. This list of factors is not all-inclusive because it is not possible to predict all factors.

Forward Looking Statement

2

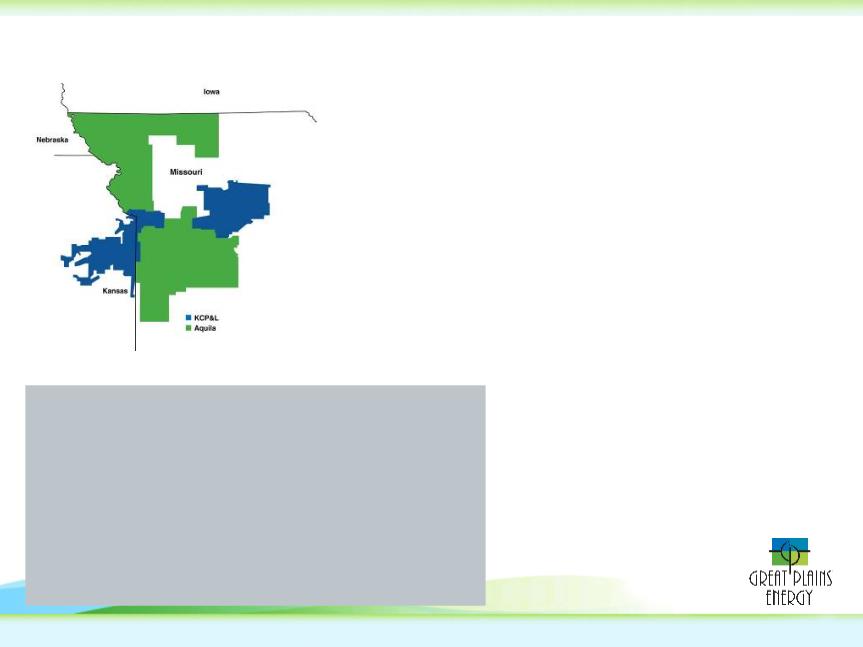

Regulated vertically integrated electric utility

operations:

operations:

• $7.7 billion in assets*

• $1.9 billion in revenues*

• $2.7 billion market cap - NYSE:GXP

• Approx. 800,000 customers in KS and MO

• Low retail utility rates

• Total generation capacity of over 5,700 MWs

Solid Midwest electric utility - KCP&L Brand

Capable, experienced management team

Investment grade credit rating

Building a platform for long-term earnings

growth:

growth:

Additions to rate base

Synergies from Aquila transaction

Annualized dividend of $1.66/share

* Based on unaudited proforma financial statements filed in 8K dated August 13, 2008

Great Plains Energy Business Overview

3

• Rate base growth through KCP&L’s Comprehensive

Energy Plan and plant investments by KCP&L GMO

(Aquila)

Energy Plan and plant investments by KCP&L GMO

(Aquila)

• Aquila integration and synergy target attainment

• Rate case filings to include investments in rate

base and to share synergies with customers

base and to share synergies with customers

Three Key Initiatives

4

Mike Chesser - CEO

37 years experience

Terry Bassham - CFO

22 years experience

Bill Downey - COO

37 years experience

John Marshall - EVP

Utility Operations

32 years experience

•Accounting

•Finance and IR

•Risk Management

•Strategic Planning

•Internal Audit

•Construction

•Regulatory

•Public Affairs

•Business Planning

•Utility Operations

•Supply - Generation

•Delivery - T&D

•Corporate Services

Leadership Team members have an average of

23 years of industry experience

Direct Reports’ Average

Years of Industry Experience

17 years

23 years

20 years

Current Key

Responsibilities

Experienced Management Team

Aligned to Succeed

Aligned to Succeed

Comprehensive Energy Plan

& KCP&L GMO Plant Investments

6

Spearville Wind Energy Facility

ü 100MW completed on schedule and under budget

LaCygne

ü Phase 1: Unit 1 SCR - Completed on schedule, under budget, and

performing per specification

performing per specification

• Phase 2: Unit 1 - bag house and scrubber environmental upgrades:

>Project Definition Report completed in Q3 2007

>Evaluating upgrade of Unit 2 at the same time

Iatan Unit 1

• Expected to be in-service early 2009

Iatan Unit 2 Construction

• Expected to be in-service summer 2010

Comprehensive Energy Plan

7

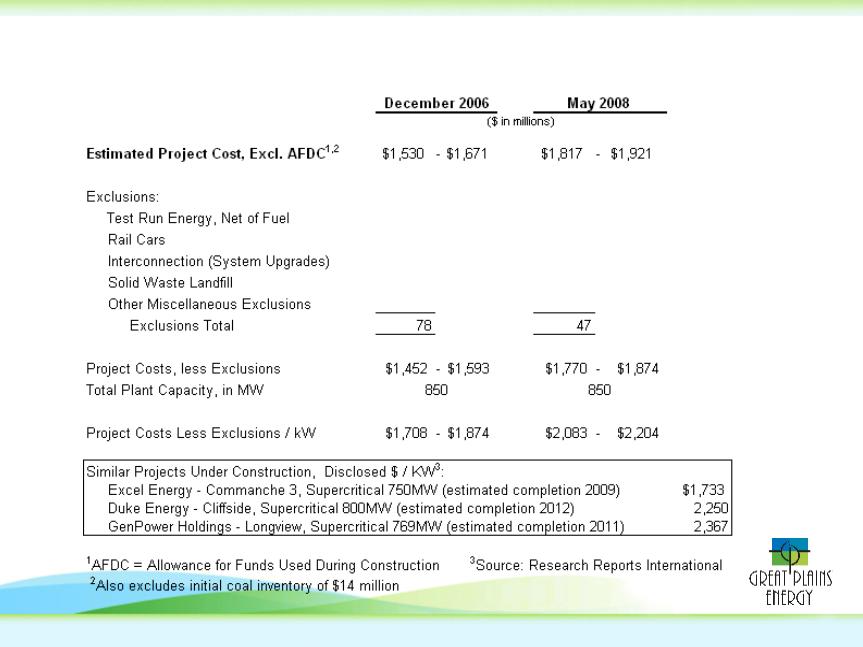

Total Iatan 2 Cost per KW

Combined Company

Integration of the Aquila Transaction &

Synergy Attainment

9

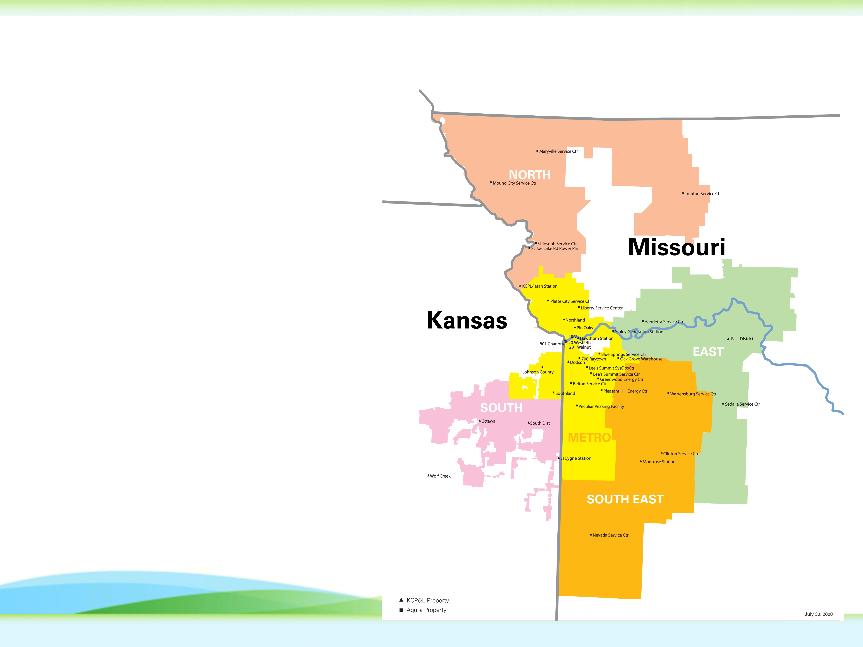

Integration Coordination

Scope of the effort

• 805,100 customers across

47 counties in MO and KS

covering 17,934 sq. miles

47 counties in MO and KS

covering 17,934 sq. miles

• 3,170 employees - - including

920 new hires

920 new hires

• 30 office/service center

locations

locations

• 9 generation plant sites and

10 peaking facilities

10 peaking facilities

• 3,309 miles transmission,

24,466 miles distribution,

and 322 substations

24,466 miles distribution,

and 322 substations

• Gas and electric assets

purchased by Black Hills that

support more than 800,000

customers in 4 other states

purchased by Black Hills that

support more than 800,000

customers in 4 other states

11

Early Integration Successes

Infrastructure

• Combined several key systems (billing, accounting, HR) as well as telecom and

network platforms into a single KCP&L version for each

network platforms into a single KCP&L version for each

Operations

• Two Aquila unions consolidated into the three existing KCP&L unions

• Training initiated to align work rules, safety rules, and construction specs

• Integrated T&D

• Work management system up and running

• Supply team actively procuring fuel and purchased power

• Expanded generating fleet is meeting its operational requirements

Customer Service

• Call Center operations integrated

• Accomplished two complete billing cycles

11

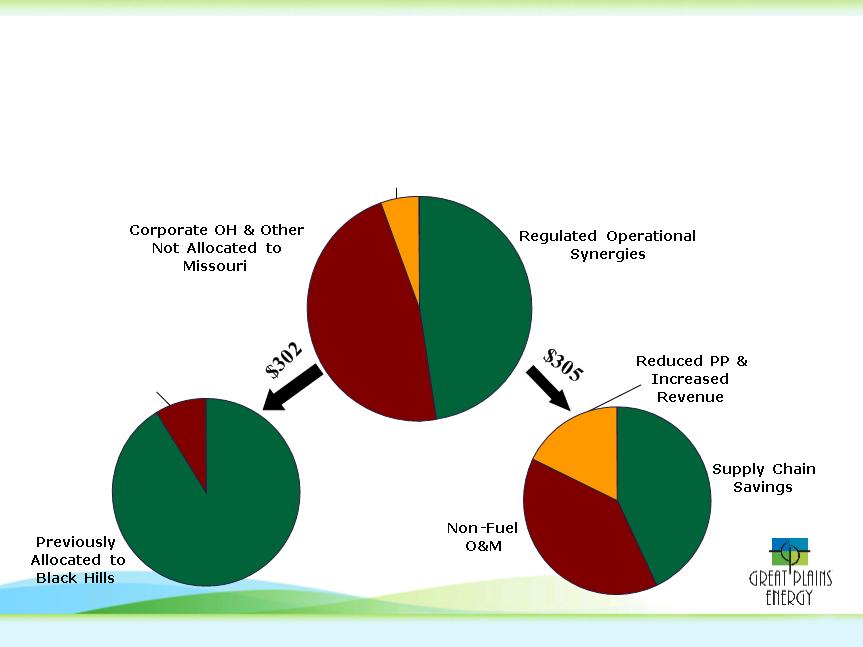

Great Plains expects to realize $675 million of total savings and

synergies over five years

synergies over five years

Interest Savings

Corporate Retained

& Merchant Savings

& Merchant Savings

$302

$305

$68

$120

$131

$54

$27

$275

Significant Synergies Expected

12

Missouri Hearings, Approval

and Close

and Close

Shareholders

receive benefits of

synergies

receive benefits of

synergies

File Rate Case

File Rate Case

Shareholders

receive benefits of

new synergies

receive benefits of

new synergies

Rates Effective

Rates Effective

Path to Synergy Sharing

Recent Rate Case Filings

for Recovery of Investments

& Sharing of Synergies

14

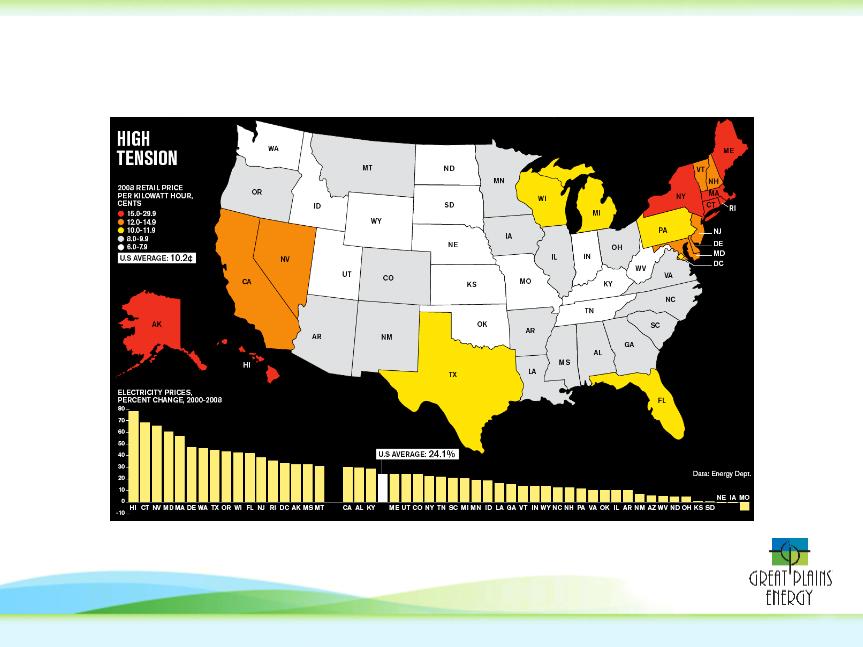

Business Week July 24, 2008

Missouri and Kansas Rates Below

National Average

National Average

15

• Requested ROE reasonable based on extensive cost of capital analysis

• Capital structure based on Great Plains Energy consolidated capital structure

>Excludes short-term debt

>Per the Aquila transaction approval, Kansas filing excludes Aquila cap structure

impact and synergies

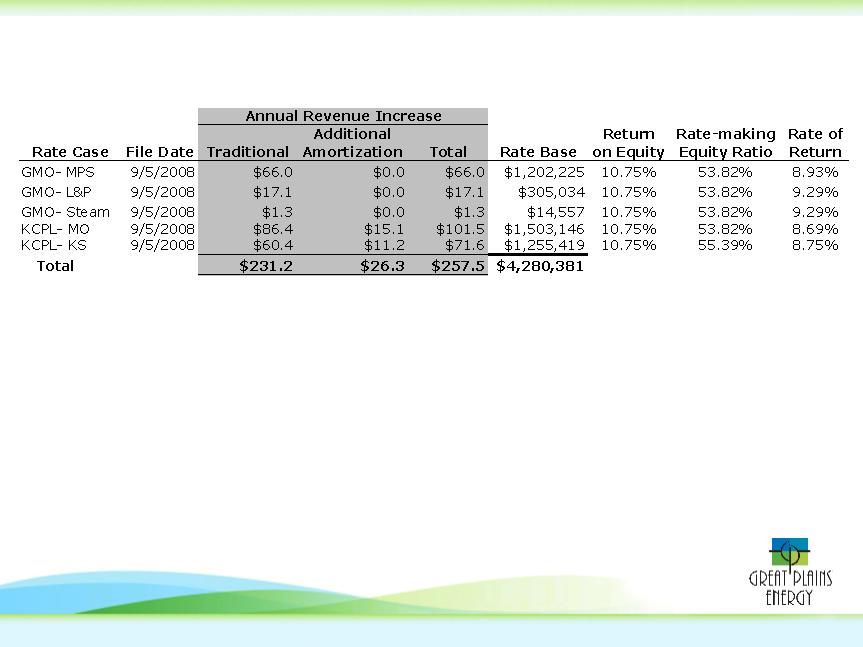

Summary of Rate Cases

16

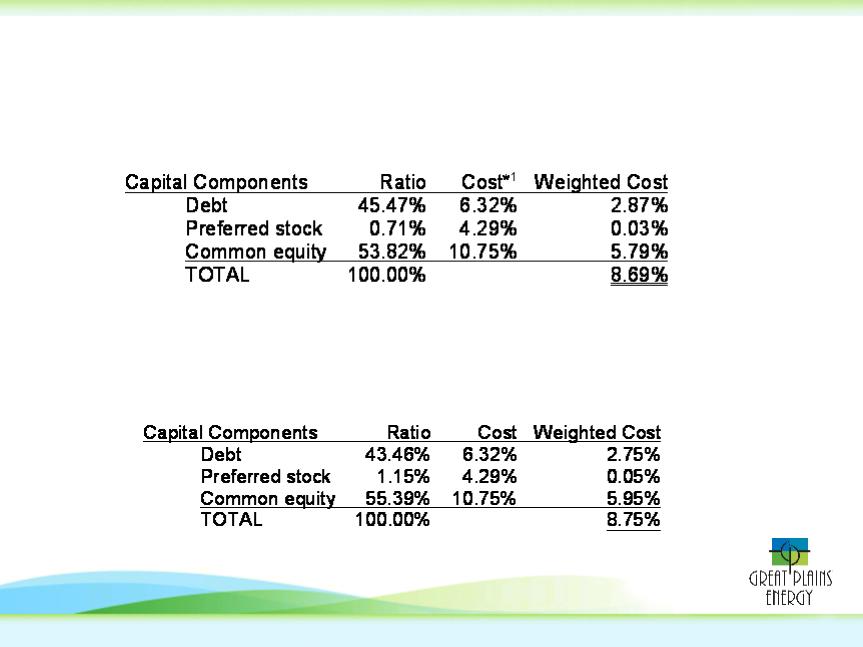

Requested Capital Structure - Missouri

Requested Capital Structure - Kansas

Note *1: Cost of debt varies by case as follows:

KCPL MO- 6.32%, GMO MPS- 6.851%, GMO L&P (electric and steam)- 7.634%

Requested Capital Structure

17

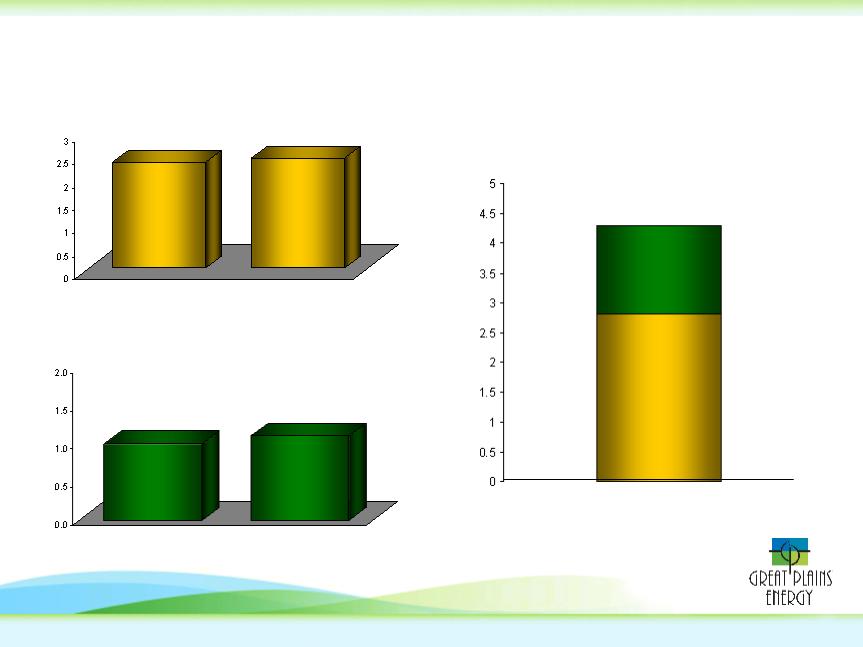

$1.0

$4.3

$1.5

KCP&L GMO

$2.8

KCP&L

$2.4

$1.1

$2.3

Rate Cases Filed

8/5/2008

KCP&L Historical Rate Base

Aquila (KCP&L GMO)

Historical Rate Base

Rates Effective

1/1/2007

Rates Effective

1/1/2008

Rates Effective

5/31/2007

Rates Effective

3/1/2006

Projected Combined Rate Base

March 31, 2009

(in billions)

• Iatan 2 CWIP at 6/30/08 is approximately $500 million

Rate Base Growth

18

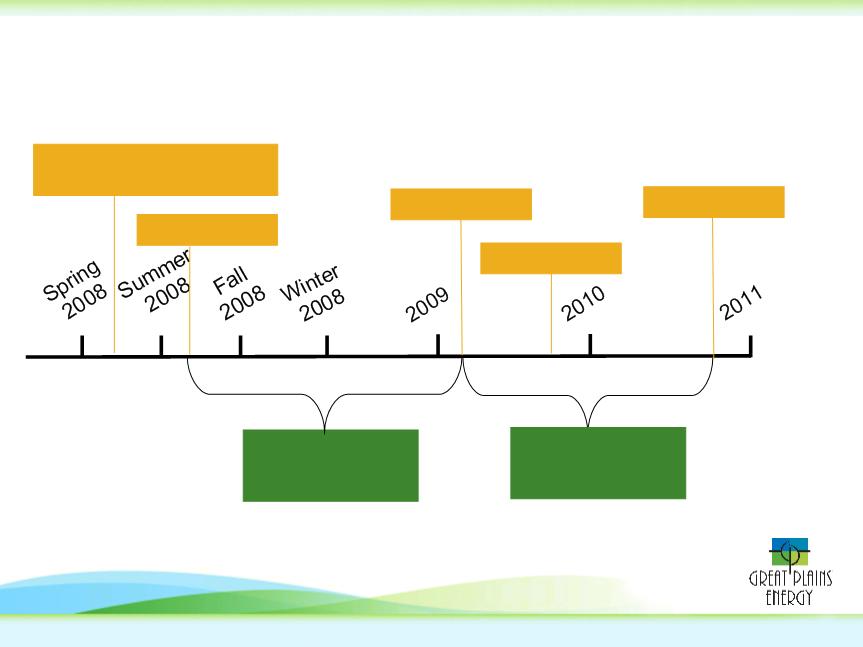

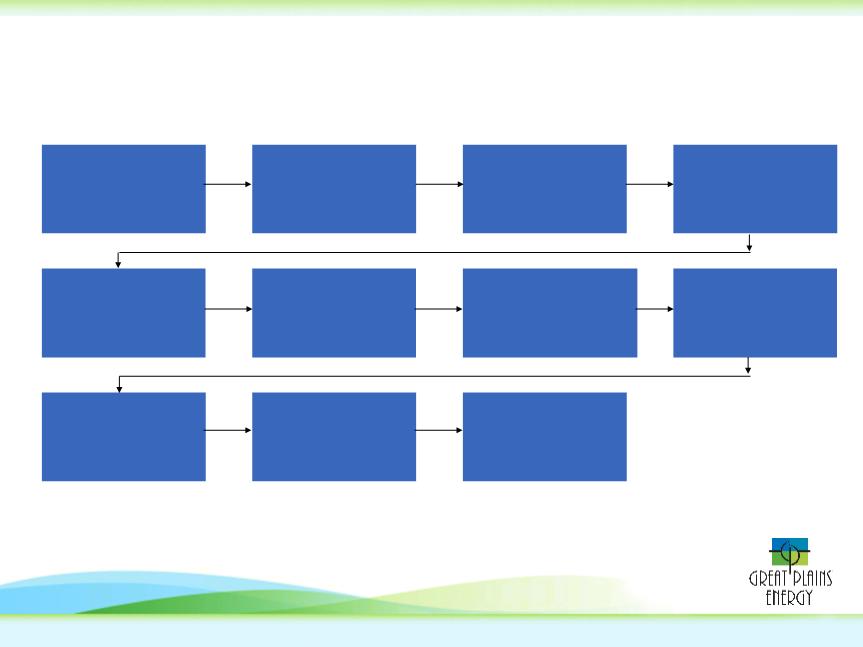

Applications filed

with MPSC

with MPSC

Sept. 5, 2008

Staff conducts audit

of entire operations

of entire operations

Now - - March 2009

Update of revenue

requirement model

based on Oct. 31,

2008. Submitted

approx. Jan. 1, 2009

requirement model

based on Oct. 31,

2008. Submitted

approx. Jan. 1, 2009

Staff and interveners

file

file

March 2009

Rebuttal testimony

March 2009

Pre-hearing

conference

conference

April 2009

True-up of revenue

requirement model

based on April 30,

2009 & submitted

early June 2009

requirement model

based on April 30,

2009 & submitted

early June 2009

Hearings

May 2009

Briefs

June 2009

Decision

July 2009

Rates implemented

August 5, 2009

Projected Missouri Regulatory Timeline

19

2009 and beyond: Extend the platform

• Complete and include Iatan 1 AQCS and Sibley environmental work in

rates effective in 2009

rates effective in 2009

• Include Crossroads plant in rates effective 2009

• Integrate Aquila and deliver synergies

• Evaluate 400 MW of additional wind

• Complete and include Iatan 2 in rates effective 2010

• Additional environmental spending at LaCygne 1 and potentially LaCygne 2

and Montrose

and Montrose

• Continue with sound strategic planning to effectively meet future

generation requirements and as an industry leader in energy efficiency

generation requirements and as an industry leader in energy efficiency

• Increase earnings driven by investments, synergies, and enhanced by

opportunities for organic service territory growth

opportunities for organic service territory growth

• Expected dividend growth, with a traditional target payout ratio, to follow

A Path to Growth