2:00 – 2:05 | Welcome and Introductions |

2:05 – 2:30 | U.S. Inland Waterways |

2:30 – 3:00 | Kirby Overview |

3:00 – 3:15 | Kirby Inland Marine · Kirby and Industry Fleet Profile |

3:15 – 3:30 | Break 15 minutes |

3:30 – 3:50 | Kirby Engine Systems Overview |

3:50 – 4:35 | Outlook for the Petrochemical Industry · Chemical Market Associates, Inc. |

4:35 – 5:20 | Refined Products Supply & Demand Drivers · Purvin & Gertz, Inc. |

5:20 – 5:25 | Closing Remarks |

Agenda

Kirby Analyst/Investor Meeting

2:00 – 2:05 | Welcome and Introductions |

2:05 – 2:30 | U.S. Inland Waterways |

2:30 – 3:00 | Kirby Overview |

3:00 – 3:15 | Kirby Inland Marine · Kirby and Industry Fleet Profile |

3:15 – 3:30 | Break 15 minutes |

3:30 – 3:50 | Kirby Engine Systems Overview |

3:50 – 4:35 | Outlook for the Petrochemical Industry · Chemical Market Associates, Inc. |

4:35 – 5:20 | Refined Products Supply & Demand Drivers · Purvin & Gertz, Inc. |

5:20 – 5:25 | Closing Remarks |

Agenda

Kirby Analyst/Investor Meeting

The State of the Waterways

Kirby Corporation Analysts’ Briefing

Berdon Lawrence, Chairman

Kirby Corporation

John Doyle, Vice President

Waterways Council, Inc. &

Special Counsel, Jones Walker LLP

The waterways are an

American success story:

American success story:

| • | They helped make America great |

| • | They create and maintain good agricultural and manufacturing jobs |

| • | But, our leaders in Washington began to take them for granted |

| • | So, industry and agriculture organized to defend and improve the waterways |

| • | We have been successful so far |

| • | The outlook is positive |

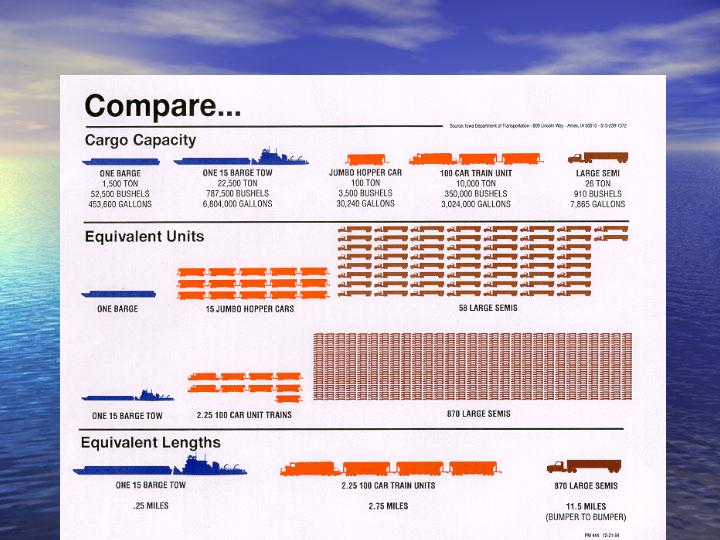

Canals

Dams

Locks

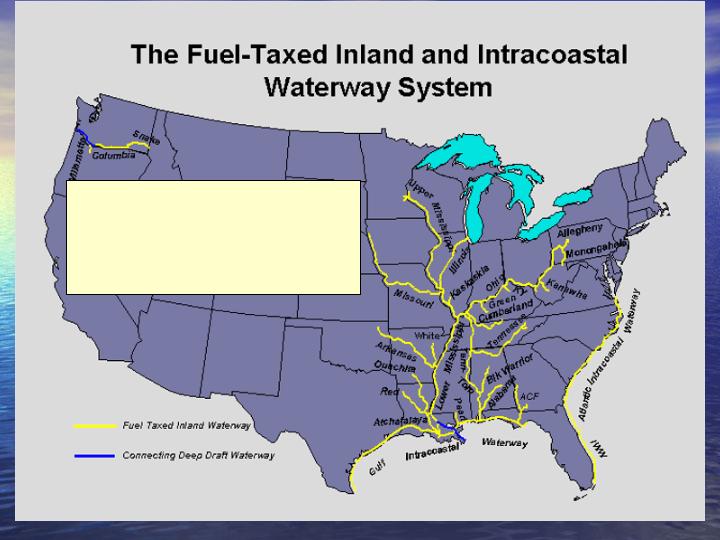

The System

Rivers

-Nearly 12,000 Miles 9 ft & Over

-192 Lock Sites / 238 Chambers

-About 2/3rds Cost of Rail and

1/10 Cost of Truck

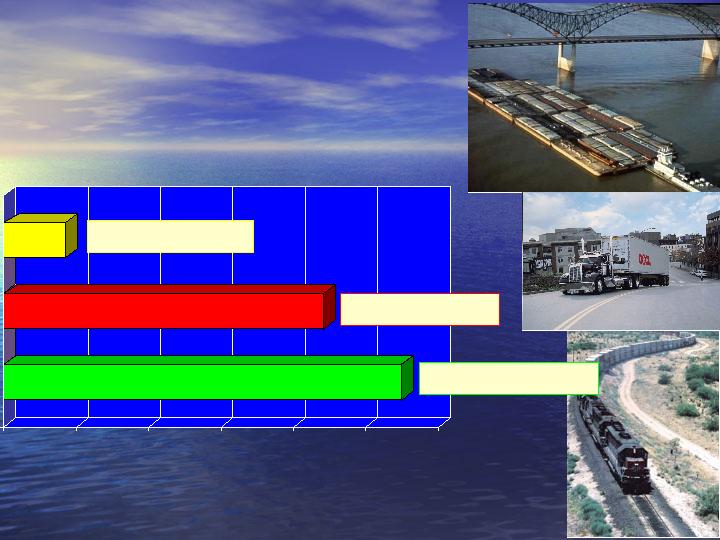

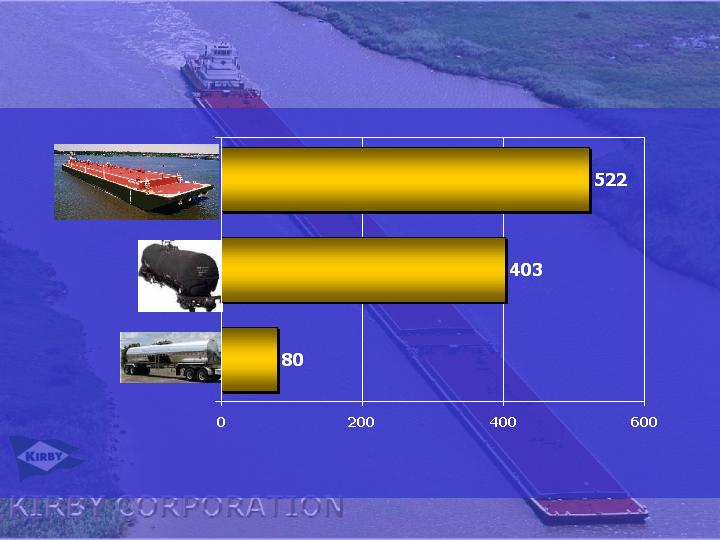

How farone gallon of fuel

movesone ton of freight, average by mode…

Truck: 70 miles

Rail: 420 miles

Barge: 530 miles

0

100

200

300

400

500

600

Miles

Barge transportation enjoys similar efficiencies in air

emissions per ton mile.

emissions per ton mile.

We Conserve Fuel & Reduce

Air Emissions

Air Emissions

We offer a solution to Congestion:

The waterways

serve key future

transportation corridors

serve key future

transportation corridors

The waterways serve many

traffic growth corridors.

America’s Waterways Advantage

| • | American farmers and industries compete in a tough global marketplace |

| – | If you get the goods to the customer cheaper, you get the sale |

| – | Efficient, low cost waterways transportation reduces total costs and allows us to compete |

| • | The Result: American exports win and vital, high paying jobs stay here! |

Over $10

Billion

Billion

$2 - 10

Billion

Billion

$1 - 2

Billion

Billion

$100 Million to

$1 Billion

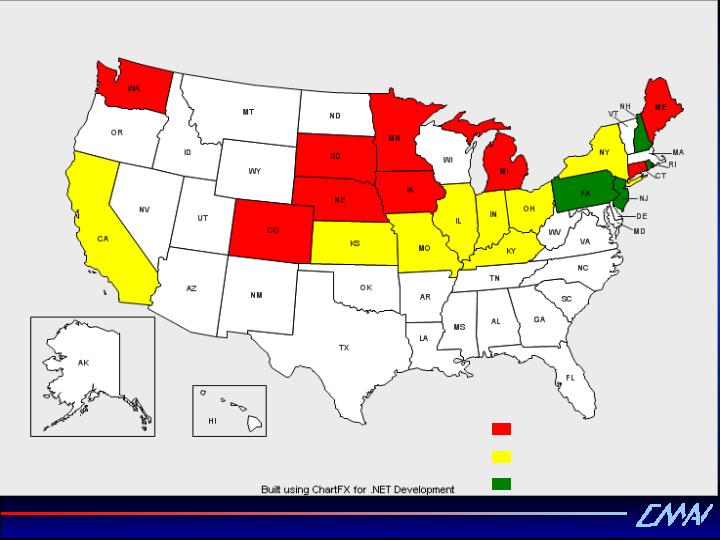

Lock Construction

or Rehabilitation

Under $100

Million

Based on data developed by TVA and USACE.

Value of Inland and Intracoastal

Waterborne Cargo

Waterborne Cargo

by State of Origin

| • | Over $112 billion in cargo |

| • | Shipped from 31 states |

| • | At average savings of $11 / ton over competing modes |

Waterways Role in Nation’s

Economic Prosperity

Economic Prosperity

| • | Grain Exports |

| – | 90 million tons annually |

| – | 70% of soybean and 62% of corn exports move by barge |

Waterways Role in Nation’s

Economic Prosperity

Economic Prosperity

| • | Coal for power plants |

| – | 227 million tons annually – inland, Lakes, coastal |

| – | 20 % of utility coal supplied by waterway |

Waterways Role in Nation’s

Economic Prosperity

Economic Prosperity

| • | Petrochemicals & Petroleum Products |

| – | 350 million tons annually between domestic points |

We are having success…

…because we have a good story to tell

…because we have a good story to tell

| • | Keeping our industries and farmers competitive in a very tough global marketplace preserves U.S. jobs |

| • | Reduces congestion on our highways |

This is an easy story to understand, but

somebody has to tell it to the Washington

lawmakers.

somebody has to tell it to the Washington

lawmakers.

Traditionally, the industry did not take a proactive

role in telling this story. Over time, this resulted in:

The 90’s

| • | Declining support in the Administration and Congress |

| • | Corps spending on waterways diverted elsewhere |

| • | Trust fund balance starts to rise |

| • | “Environmentalists” mount attack on the Corps |

| • | Media & editorial campaigns against the Corps and water resources development |

Waterways Work! was formed

in 2001 to counter negative

publicity about the industry

In 2003, Waterways Work

merged with DINAMO, the

Association for the Ohio

Valley, and formed the

Waterways Council, Inc.

The Waterways Council, Inc.:

| • | Professional staff based in Washington, DC |

| • | Media relations team |

| • | Annual budget now over $1 million |

| • | Active member involvement |

| • | Dedicated lobbying team – Jones Walker/Livingston Group |

The waterway community response:

Who are WCI

Members?

Members?

| • | All waterway business interests: |

| – | Carriers |

| – | Shippers |

| – | Waterways Service Providers |

| – | Port Authorities & Governmental Entities |

| – | Regional Associations |

| • | Geographically Diverse |

| • | All major commodity groups: |

| – | Oil, chemical and petrochemical |

| – | Grain |

| – | Coal |

| – | Building Materials |

| – | Steel, Aluminum and Ore |

| – | Containers |

The Objectives:

| • | Get the President to propose adequate budgets |

| • | Get Congress to pass laws that authorize projects and appropriate the money needed each year to build and maintain them |

| • | Ensure the Corps of Engineers actually spends the money as intended by Congress |

New Construction

Major Rehabilitation

Olmsted

Inner

Harbor

Marmet

McAlpine

Kentucky

L&D 11 Rehab

L&D 19 Rehab

L&D 24 Rehab

Lower Mon 2-4

Myers

Chickamauga

Active new lock

construction and major

rehabilitation program

underway in FY ‘05:

construction and major

rehabilitation program

underway in FY ‘05:

| • | 8 new or replacement |

locks(receiving IWTF funds)

| • | 3 major rehabs |

| • | $332 million in funding |

New Construction and Modernization:

Major Navigation Projects Underway

Major Navigation Projects Underway

Based on FY 2005 Appropriations

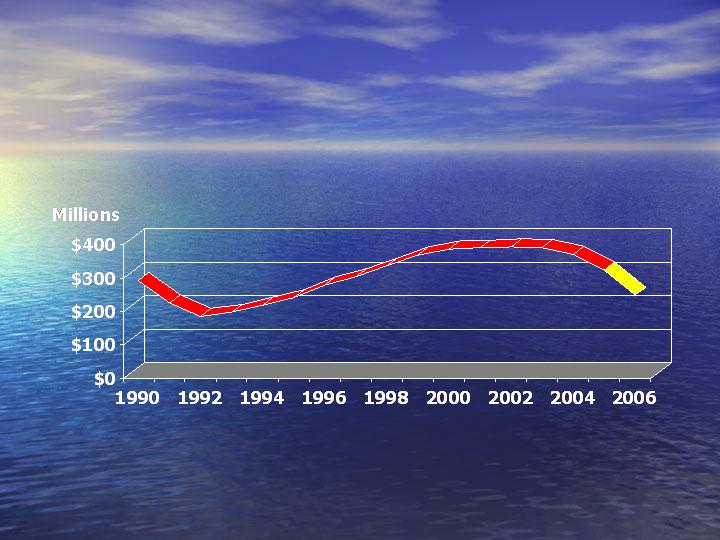

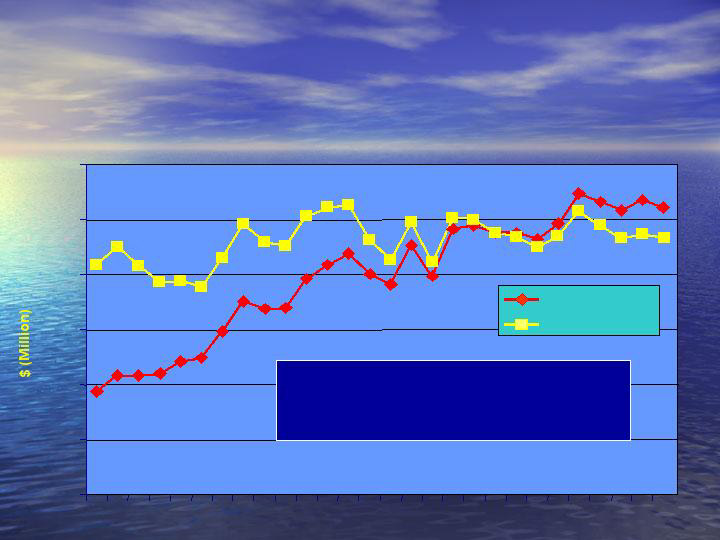

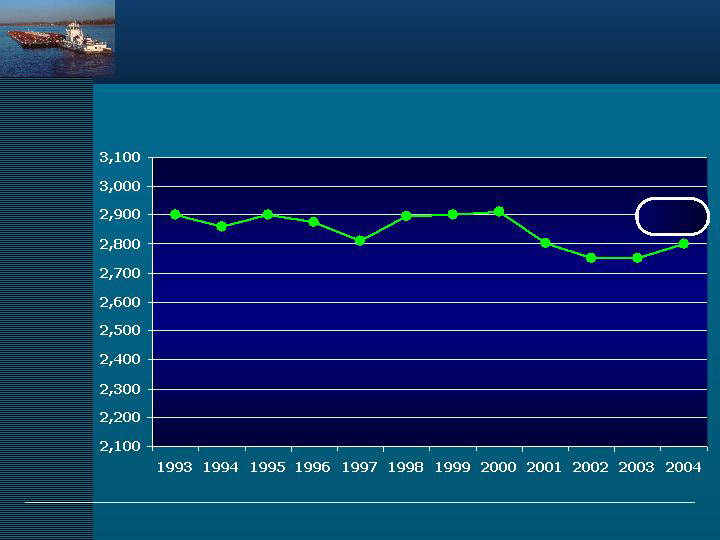

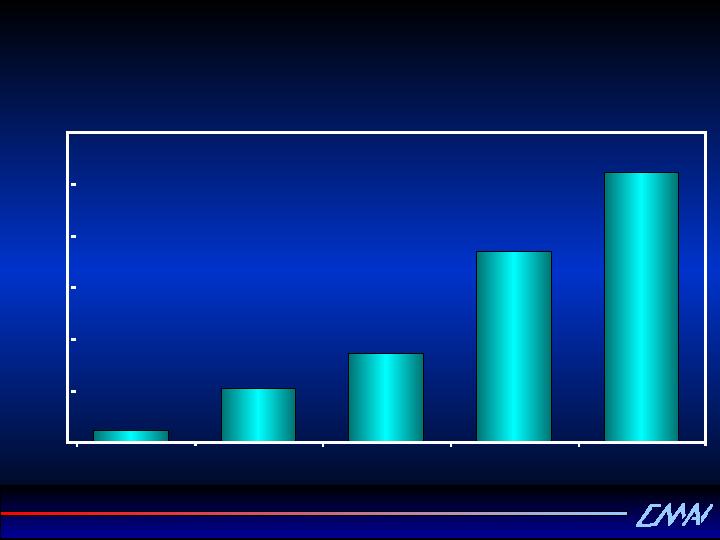

Year | Estimated Outlays | Tax Revenues | Interest Earnings | Year-End Balances |

| ($Millions) | ||||

1990 | 117.3 | 62.8 | 26.2 | 292.8 |

1991 | 148.6 | 60.5 | 21.2 | 225.9 |

1992 | 122.7 | 69.9 | 13.7 | 186.7 |

1993 | 74.5 | 78.6 | 7.5 | 198.3 |

1994 | 75.7 | 88.4 | 9.3 | 220.2 |

1995 | 94.8 | 103.4 | 13.3 | 242.1 |

1996 | 85.5 | 108.4 | 15.6 | 280.6 |

1997 | 89.5 | 96.4 | 17.0 | 304.6 |

1998 | 76.9 | 91.1 | 18.3 | 337.1 |

1999 | 88.2 | 104.4 | 16.0 | 369.2 |

2000 | 102.4 | 99.6 | 20.0 | 387.8 |

2001 | 120.3 | 102.6 | 20.9 | 390.9 |

2002 | 104.5 | 95.3 | 12.4 | 394.1 |

2003 | 101.6 | 89.5 | 9.5 | 391.6 |

2004 | 117.3 | 90.8 | 6.9 | 372.0 |

*2005 | 146.0 | 92.0 | 7.0 | 325.0 |

Inland Waterways Trust Fund

Trust Fund Balances

Money from 20 cent per gallon fuel tax. This is matched with an

equal sum from the Treasury. Actual spending is double this amount.

50

70

90

110

130

150

170

190

210

96

97

98

99

OO

O1

O2

O3

O4

O5

O6

Fiscal Year

$184 Mil.

in Bush

Budget.

Appropriations

bill pending.

Waterways Work /

Waterways Council

Formed

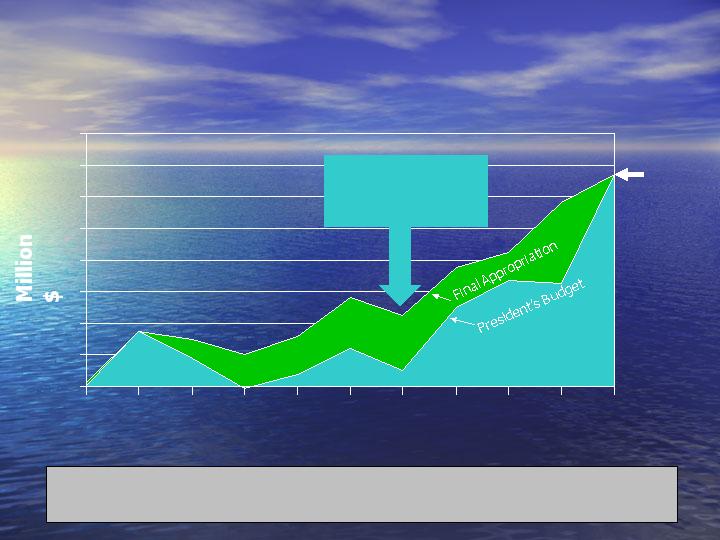

Trust Fund Spending:

New Construction and Major Rehab

New Construction and Major Rehab

Millions of dollars

from trust fund.

Matched with

general revenues.

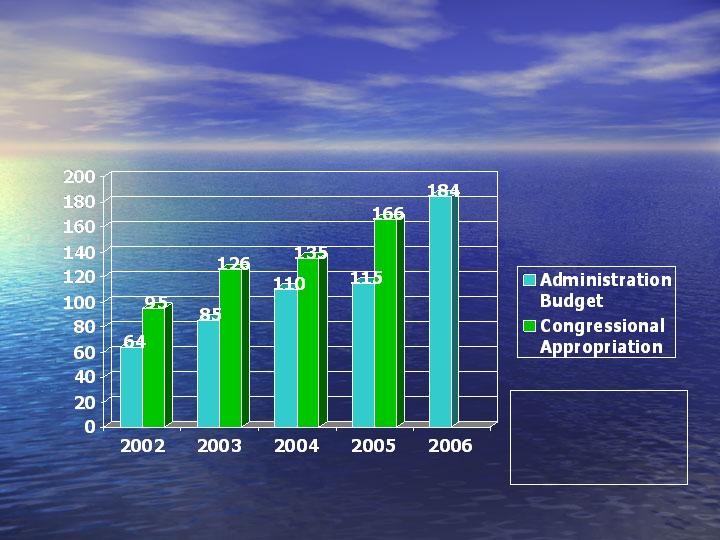

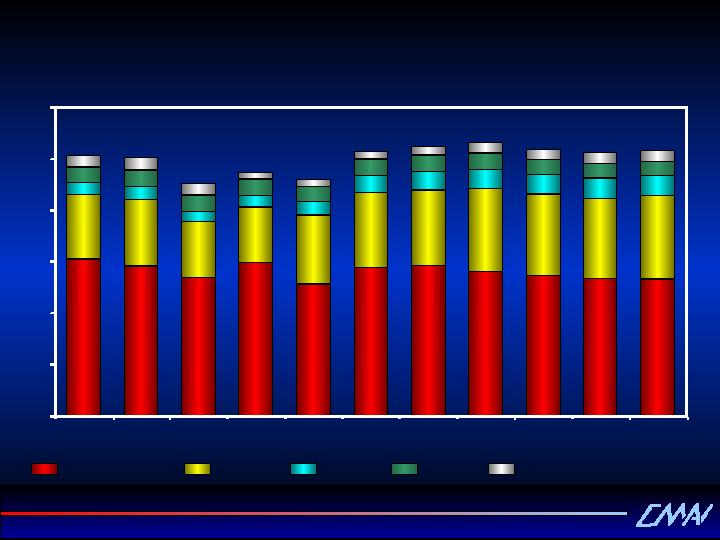

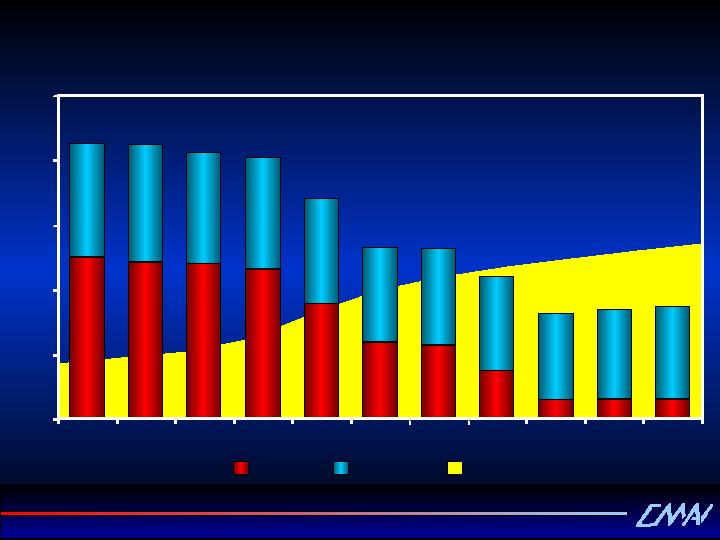

Recent Trust Fund Spending

| FY 2002 Enacted | FY 2003 Enacted | FY 2004 Enacted | FY 2005 Enacted | FY 2006 Request | % Difference (05 vs. 02) | % Difference (06 vs. 02) | |

| Construction General | 1,712 | 1,745 | 1,731 | 1,782 | 1,637 | 4.1 | (-4.4) |

| Inland Waterways Trust Fund | 189 | 253 | 270 | 332 | 368 | 75.7 | 94.7 |

| Corps Civil Works Total | 4,650 | 4,699 | 4,563 | 4,668 | 4,513 | 0.4 | (-2.9) |

Inland Waterways Trust Fund

Appropriations Comparison

Appropriations Comparison

($ in millions)

Goals for Fiscal Year 2006

Appropriations:

Appropriations:

| • | At least $300 million ($150 million from the Inland Waterways Trust Fund) for Building Priority Projects |

| • | An additional $100 million above the President’s budget for inland navigation Operations and Maintenance priority needs |

0

100

200

300

400

500

600

1977

1980

1983

1986

1989

1992

1995

1998

2001

Current $ and 1996 Constant $,

Fuel-Taxed Waterways Only

Fuel-Taxed Waterways Only

2004

Real O&M funding remains flat even

as project portfolio grows and

ages…

as project portfolio grows and

ages…

Current $

Constant

$

$

Operations & Maintenance (O&M)

funding is our next major challenge

funding is our next major challenge

The O&M Challenge

| • | Intensified Focus in 2005 |

| • | System-Wide Examination |

| • | Joint Industry/Corps Initiative |

| • | Maintain and Improve System Reliability |

| • | Secure Adequate Resources and Invest to Maximize Results |

| – | Reduce Risk and Increase Reliability |

Industry/Corps O&M Workshops in 2005

| • | Conducted |

| – | January Cincinnati, OH Ohio River System |

| – | January St. Louis, MO Upper Miss./Illinois |

| – | February Tampa, FL Integration |

| – | April New Orleans, LA Gulf Intracoastal |

| • | Being Planned |

| – | TBD TBD Lower Miss. & Tribs. |

| – | TBD TBD Columbia/Snake |

Industry/Corps O&M Workshops

| • | Identify most pressing problems from perspective of Corps and industry |

| • | Allocate resources to address most pressing needs |

| • | We are committed to both short term and long term solutions to navigational issues |

Also Where We Are Going…

| • | Passage of Water Resources Development Act (WRDA) |

| – | Authorize Lock Modernization on the Upper Mississippi and Illinois Rivers |

| – | Reasonable, Non-Damaging “Corps Reform” Provisions |

Kirby is a leader in efforts to

maintain and improve our

waterways infrastructure.

| • | Kirby supports national efforts: |

| – | Berdon Lawrence, Chair, Waterways Works/Waterways Council 2001- March, 2005 |

| – | Steve Valerius, Incoming Chair, American Waterways Operators |

| – | Joe Pyne, Chair, National Waterways Foundation |

Kirby is a leader in efforts to

maintain and improve our

waterways infrastructure.

| • | Kirby also supports regional efforts. Examples: |

| – | *Gulf Intracoastal Canal Association (GICA) |

| – | Midwest Area River Coalition (MARC 2000) |

| – | *Louisiana Association of Waterways Operators and Shipyards (LAWS) |

| – | *Texas Waterway Operators Association (TWOA) |

| – | *Warrior Tombigbee Waterway Association |

*Kirby employee is officer or director

Thingsare getting better

…yet we still have much work to do.

Some of the images in this presentation are courtesy of the

U.S. Army Corps of Engineers

2:00 – 2:05 | Welcome and Introductions |

2:05 – 2:30 | U.S. Inland Waterways |

2:30 – 3:00 | Kirby Overview |

3:00 – 3:15 | Kirby Inland Marine · Kirby and Industry Fleet Profile |

3:15 – 3:30 | Break 15 minutes |

3:30 – 3:50 | Kirby Engine Systems Overview |

3:50 – 4:35 | Outlook for the Petrochemical Industry · Chemical Market Associates, Inc. |

4:35 – 5:20 | Refined Products Supply & Demand Drivers · Purvin & Gertz, Inc. |

5:20 – 5:25 | Closing Remarks |

Agenda

Kirby Analyst/Investor Meeting

Kirby Corporation

Putting America’s Waterways to Work

NYSE: KEX

May 2005

Statements contained in this presentation with respect to the future are

forward-looking statements. These statements reflect management’s

reasonable judgement with respect to future events. Forward-looking

statements involve risks and uncertainties. Actual results could differ

materially from those anticipated as a result of various factors, including cyclical or other downturns in demand, significant pricing competition, unanticipated additions to industry capacity, changes in the Jones Act or in U.S. maritime policy and practice, fuel costs, interest rates, weather conditions and the timing, magnitude and the number of acquisitions made by Kirby. A list of additional risk factors can be found in Kirby’s annual report on Form 10-K for the year ended December 31, 2004, filed with the Securities and Exchange Commission.

forward-looking statements. These statements reflect management’s

reasonable judgement with respect to future events. Forward-looking

statements involve risks and uncertainties. Actual results could differ

materially from those anticipated as a result of various factors, including cyclical or other downturns in demand, significant pricing competition, unanticipated additions to industry capacity, changes in the Jones Act or in U.S. maritime policy and practice, fuel costs, interest rates, weather conditions and the timing, magnitude and the number of acquisitions made by Kirby. A list of additional risk factors can be found in Kirby’s annual report on Form 10-K for the year ended December 31, 2004, filed with the Securities and Exchange Commission.

Kirby reports its financial results in accordance with generally accepted

financial principles (GAAP). However, Kirby believes that certain

Non-GAAP financial measures are useful in managing Kirby’s businesses and evaluating Kirby’s performance. This presentation contains two Non-GAAP financial measures, adjusted net earnings and EBITDA. Please see the Appendix for a reconciliation of GAAP to Non-GAAP financial measures.

financial principles (GAAP). However, Kirby believes that certain

Non-GAAP financial measures are useful in managing Kirby’s businesses and evaluating Kirby’s performance. This presentation contains two Non-GAAP financial measures, adjusted net earnings and EBITDA. Please see the Appendix for a reconciliation of GAAP to Non-GAAP financial measures.

Kirby Forward Looking Statement

Marine Transportation

87% of 2004 Revenue - $588.8 million

Largest U.S. Inland Tank Barge Operator

Diesel Engine Services

13% of 2004 Revenue - $86.5 million

Largest Domestic EMD Diesel Services Company

Kirby... Business Operations

Kirby Facts

| • | Largest inland tank barge operator |

| • | Operates 878 barges and 239 towing vessels |

| • | Sustainable competitive advantages: |

| – | Lowest cost due to economies of scale |

| – | Best positioned for growth opportunities |

| – | “One Stop Shop” for customers |

| • | 70% of Kirby’s business is under contract, 30% spot market |

| • | Successful integration of 23 acquisitions |

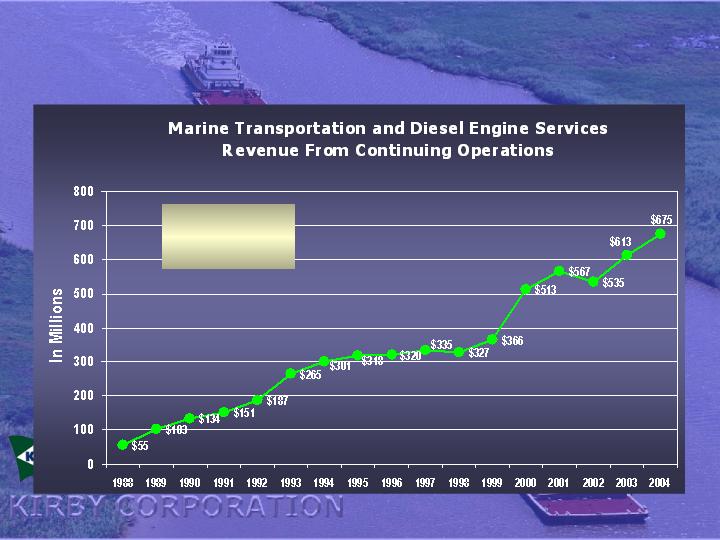

17% growth

rate from

1988-2004

rate from

1988-2004

Revenue... Business Operations

1994-2001 adjusted to exclude goodwill amortization expense

2002 adjusted to exclude impairment charges of $12.5 million, net of taxes, or $.51 per share

See Appendix for reconciliation of GAAP to Non-GAAP earnings per share

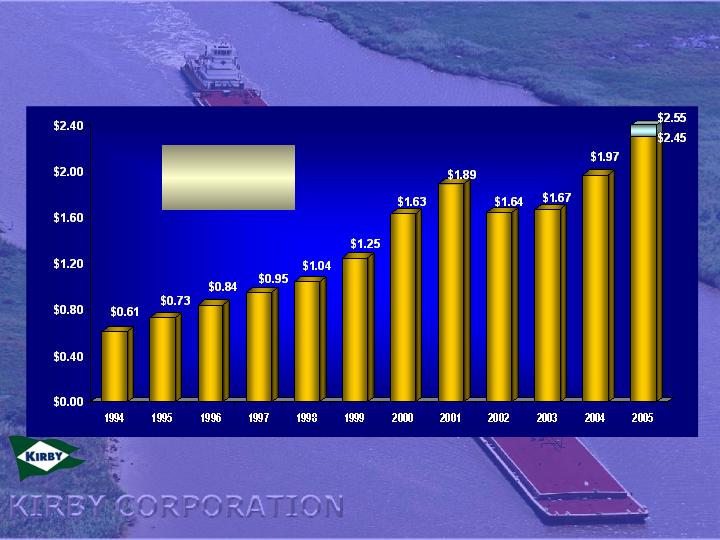

12.4% growth

rate from

1994 - 2004

rate from

1994 - 2004

Earnings Per Share From Continuing Operations Before Adjustments

Guidance

Earnings Per Share…

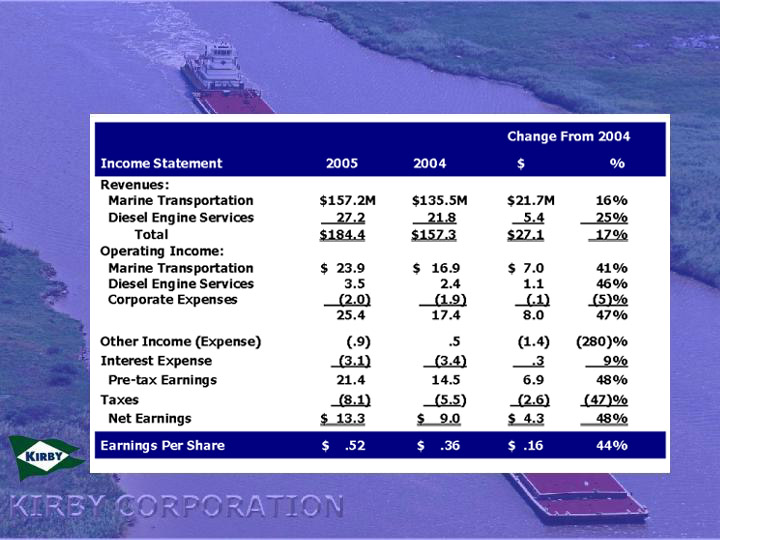

| • | Record 1st quarter 2005 earnings of $.52, 44% increase over 1st quarter 2004 earnings of $.36 |

| • | Raised 2005 annual forecast to $2.45 - $2.55, 24% to 29% above 2004 |

| • | 1st quarter 2005 spot and contract rates increased 4% to 5% |

| • | 2004 chemical volumes up 4% to 5%; 2005 chemical volumes expected to improve but at a slower rate |

| • | Diesel engine business during 1st quarter 2005 increased prices on both parts and labor |

Recent Demands and Pricing Trends

| • | 70% Contract, 30% Spot |

| – | Reduces volatility and improves predictability |

| – | Allows Kirby to service peak demand from contract customers |

| – | Long-term approach to business |

| • | Ideally would want higher spot exposure when spot rates were higher than contract rates |

| – | Short-term approach to business |

| – | More risk |

| – | Difficult to achieve |

Contract to Spot Market Mix

| • | Why has Kirby not benefited more from the problems that rail and trucks are having with their infrastructure? |

Issues

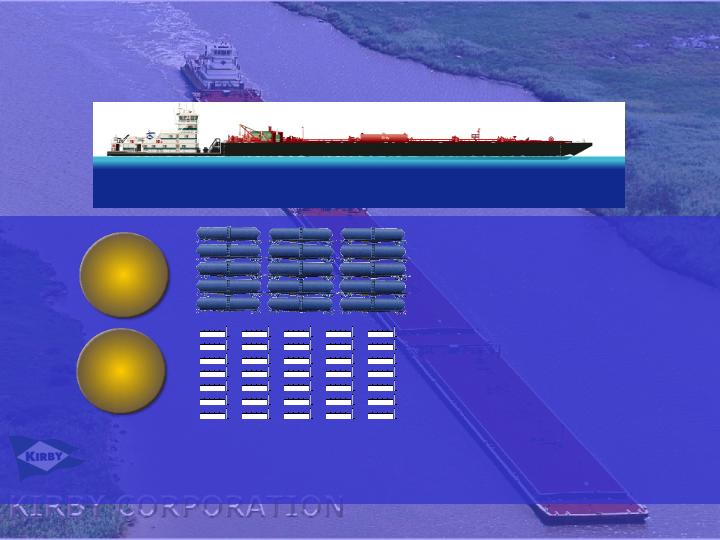

60,000 bbl. two-barge tow is equivalent to:

Kirby’s fleet capacity of 16.4 million bbls. equates

to82,000 trucks, or21,900 rail cars

to82,000 trucks, or21,900 rail cars

Rail Cars

80

Trucks

300

Barges Compete SuccessfullyWith Rails and Trucks

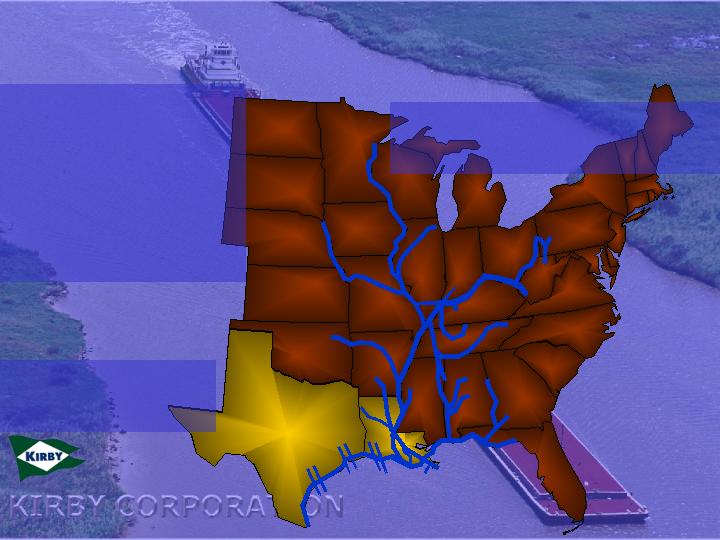

St. Paul

Sioux City

Chicago

Pittsburgh

Charleston

St. Marks

Tulsa

Brownsville

Corpus Christi

Houston

New Orleans

St. Louis

Cincinnati

Mobile

Kirby is one of the fewoperators offering distribution

throughout the

MississippiRiver System and Gulf

MississippiRiver System and Gulf

Intracoastal

Waterway

Waterway

12,000 miles of navigable waterways

linking America’s heartland to the world

linking America’s heartland to the world

Texas and Louisiana account for 80% of the total U.S. production of chemicals and petrochemicals

Putting America’s Waterways to Work

Inland Waterway System

Inland Waterway System

One gallon of fuel in a barge can move one ton of freight 522 miles, compared

to 403 miles by rail and only 80 miles for a truck.

to 403 miles by rail and only 80 miles for a truck.

Barge

Rail

Truck

Barges…

Efficient

Efficient

While moving one ton of freight 1,000 miles:

| • | Smog is a major problem in most major cities |

| • | Oxides of nitrogen are the chemicals that produce smog |

Trains produce 3.5times as much oxides of

nitrogen as barges

nitrogen as barges

Trucks produce 19times as much oxides of

nitrogen as barges

nitrogen as barges

Barges…

Environmentally Friendly

Environmentally Friendly

| • | Why has Kirby not benefited more from the problems that rail and trucks are having with their infrastructure? |

| • | What has been the cost of security measures required by the Homeland Security Act? |

| • | What are the prospects for an acquisition this year? |

Issues

Shipper Owned Independent | Tank Barges Operated | Dry Cargo Barges Operated |

Kirby Corporation | 878 | - |

American Commercial Lines LLC | 379 | 2,861 |

Marathon Ashland Petroleum | 167 | - |

Ingram Barge Company | 165 | 3,468 |

Canal Barge Company, Inc. | 150 | 226 |

Florida Marine | 103 | - |

American River Transportation Co | 84 | 1,892 |

Blessey Enterprises | 83 | - |

Higman Barge Lines, Inc. | 77 | - |

Cenac Towing Company, Inc. | 69 | - |

Magnolia Marine Transport Co | 60 | - |

PPG Industries, Inc. | 59 | - |

Martin Midstream Partners | 55 | - |

Southern Towing Company | 53 | - |

Settoon Towing, LLC | 49 | - |

LeBeouf Brothers Towing Co | 43 | - |

John W. Stone Oil | 31 | - |

Dupont | 30 | - |

Olin Corporation | 26 | - |

Buffalo Marine Service, Inc. | 22 | - |

River City Towing Services | 19 | - |

Rhodia, Inc. | 19 | - |

Lyondell Chemical Company | 17 | - |

Shipper Owned Independent | Tank Barges Operated | Dry Cargo Barges Operated |

Dynegy Midstream Services | 16 | - |

Waxler Towing Company, Inc. | 15 | - |

Highland Towing | 15 | - |

ConocoPhillips Company | 15 | - |

Plaquemine Towing Corp. | 13 | - |

Houston Marine Services, Inc. | 13 | - |

Devall Towing | 12 | - |

Chem Carriers, Inc. | 11 | - |

Westlake/GA&O Corporation | 10 | - |

Merichem Company | 8 | - |

Grifco | 8 | - |

Apex Towing | 7 | - |

Golding Barge Lines, Inc. | 6 | - |

Republic of Texas | 6 | - |

American Milling | 5 | 17 |

Barge Management, Inc. | 5 | - |

Mon River Towing, Inc. | 4 | 142 |

Reilly Industries | 4 | - |

Memphis Barge Lines | 2 | - |

Cytec Industries | 2 | - |

Jantran, Inc. | 1 | 3 |

Other dry cargo carriers | - | 9, 670 |

TOTAL | 2,816 | 18,279 |

Sparks Companies, March 2005

Kirby Outpaces the Competition

Tank Barge Owners By Number of Tank Barges

| • | Why has Kirby not benefited more from the problems that rail and trucks are having with their infrastructure? |

| • | What has been the cost of security measures required by the Homeland Security Act? |

| • | What are the prospects for an acquisition this year? |

| • | How is Osprey doing? |

Issues

Osprey

| • | Container on barge operation |

| – | Developing a new market |

| – | Challenge is to divert traffic from other modes and routes |

| – | Shorebased infrastructure more important than actual movement |

| • | Inland service shows great potential |

| – | Developing infrastructure |

| – | Building volume |

| – | Testing pricing |

| • | Coastal service using small ship struggling |

| – | Cost of vessel |

| – | Volume |

| • | Significant long term potential but short term development will be slow and uneven |

| – | 5 to 10 year play |

Observations About Market

| • | Bear Sterns Conference |

| – | Disconnect between Wall Street’s perception and what transportation companies are seeing |

| • | Kirby’s current business conditions |

| – | Saw no February/March soft patch |

| – | Remain very busy |

| – | Customers are not telling us they are worried about their volumes |

| • | Best fundamentals Kirby has seen in 25 years |

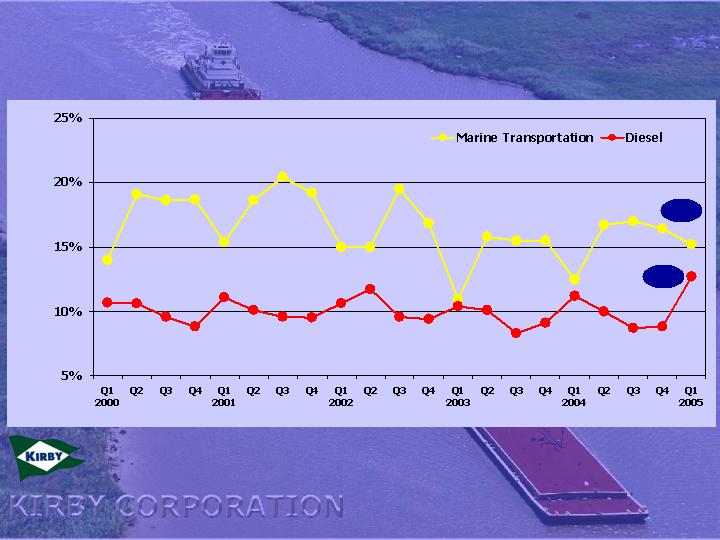

Financial Highlights

For Three Months Ended March 31

12.7%

15.2%

Operating Margins

11.2% growth

rate from

1994 - 2004

rate from

1994 - 2004

See Appendix for reconciliation of GAAP net earnings to Non-GAAP EBITDA

EBITDA Per Share Growth

* Excluding acquisitions

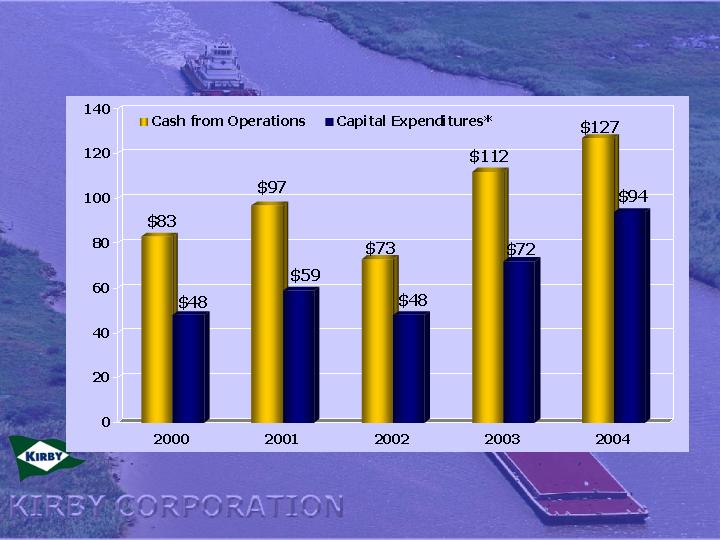

Cash Flows

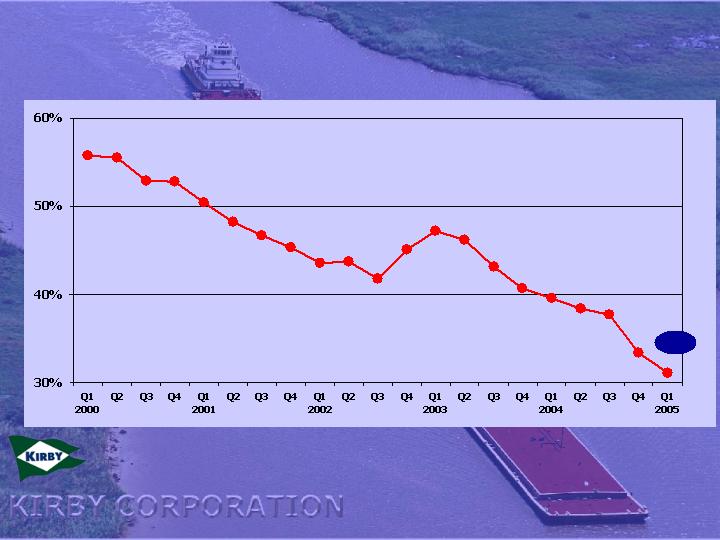

31.1%

Debt / Capitalization

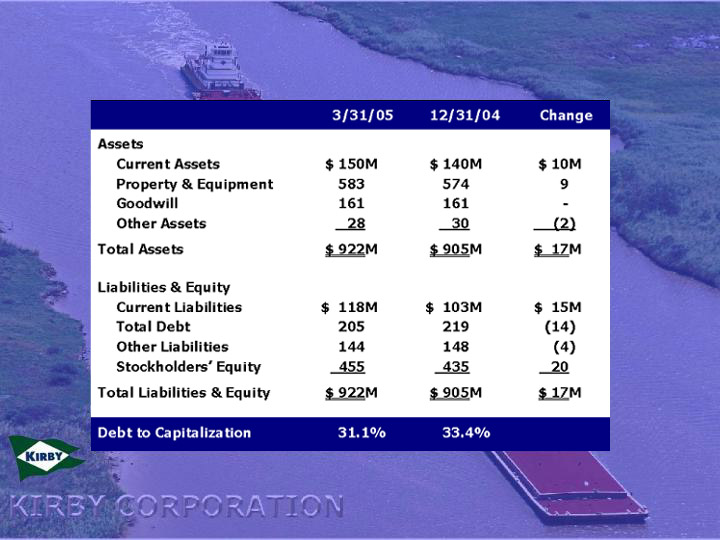

Balance Sheet

| • | Investment grade public debt |

| – | Standard & Poor’s – BBB |

| – | Moody’s – Baa3 |

| • | 10-year unsecured Private Placement due 2013 |

| – | $200 million outstanding |

| – | Floating rate of LIBOR +1.2% |

| – | Callable at par after one year without penalty |

| – | No required principal payments until maturity |

| • | $150 Million Revolving Credit Facility – December 2003 |

| – | Maturity extended three years to December 2007 |

| – | Accordion feature added to allow maximum amount to increase to $225 million without amendment |

Financial Strength

| • | Approximately $200 million of outstanding debt |

| – | Floating rate private placement maturing 2013 |

| – | $150 million bank revolving credit maturing December 2007 (expandable to $225 million) |

| • | $150 million hedged against interest rate movements |

| – | $50 million hedged until May 2009 |

| – | $100 million hedged until February 2013 |

| • | Total cost of debt in Q1 2005 averaged 6.0% |

Interest Rate Risk

| • | Completed first annual assessment of internal controls over financial reporting |

| – | No material weaknesses |

| – | No significant deficiencies |

| – | Clean opinion from KPMG |

| • | Total cost for 2004 compliance - $1 million plus |

| • | 2005 Compliance |

| – | Minimal effort to update controls |

| – | Testing of controls |

| • | PCAOB and SEC rule changes expected to reduce projected time and cost |

Section 404

Sarbanes-Oxley Act of 2002

| • | Covers only vessel employees |

| • | Kirby’s policy is to fund 100% of Accumulated Benefit Obligation (ABO) |

| – | Plan assets: $76.4 million at 12/31/04 |

| – | ABO: $75.6 million at 12/31/04 |

| • | Pension expense |

| – | 2003: $4.0 million |

| – | 2004: $5.2 million |

| – | 2005 Projected: $5.2 million |

| • | Contribution |

| – | 2003: $5.6 million |

| – | 2004: $4.6 million |

| – | 2005 Projected: $4 - $8 million |

Defined Benefit Pension Plan

2:00 – 2:05 | Welcome and Introductions |

2:05 – 2:30 | U.S. Inland Waterways |

2:30 – 3:00 | Kirby Overview |

3:00 – 3:15 | Kirby Inland Marine · Kirby and Industry Fleet Profile |

3:15 – 3:30 | Break 15 minutes |

3:30 – 3:50 | Kirby Engine Systems Overview |

3:50 – 4:35 | Outlook for the Petrochemical Industry · Chemical Market Associates, Inc. |

4:35 – 5:20 | Refined Products Supply & Demand Drivers · Purvin & Gertz, Inc. |

5:20 – 5:25 | Closing Remarks |

Agenda

Kirby Analyst/Investor Meeting

Kirby Inland Marine

May 2005

| • | Industry Fleet Profile |

| • | Logistics Management |

| • | Marine Workforce |

Focus

Industry Fleet Profile

Refined Products

10%

Black Oil

20%

Agricultural Chemicals

5%

Petrochemicals

65%

Market Segments

878 Active Tank Barges

Petrochemical

Refined

Products

Refined

Products

High Capacity

pumps –

Specialty coated

tanks

pumps –

Specialty coated

tanks

694

105

63

13

3

Pressure

Pressurized

tanks

tanks

Black Oil

Self-contained

heating systems

heating systems

Anhydrous

Ammonia

Ammonia

Refrigeration

tanks

tanks

Specialty

Stainless steel

tanks

tanks

High Tech and Diverse Fleet

Shipper Owned Independent | Tank Barges Operated | Dry Cargo Barges Operated |

Kirby Corporation | 878 | - |

American Commercial Lines LLC | 379 | 2,861 |

Marathon Ashland Petroleum | 167 | - |

Ingram Barge Company | 165 | 3,468 |

Canal Barge Company, Inc. | 150 | 226 |

Florida Marine | 103 | - |

American River Transportation Co | 84 | 1,892 |

Blessey Enterprises | 83 | - |

Higman Barge Lines, Inc. | 77 | - |

Cenac Towing Company, Inc. | 69 | - |

Magnolia Marine Transport Co | 60 | - |

PPG Industries, Inc. | 59 | - |

Martin Midstream Partners | 55 | - |

Southern Towing Company | 53 | - |

Settoon Towing, LLC | 49 | - |

LeBeouf Brothers Towing Co | 43 | - |

John W. Stone Oil | 31 | - |

Dupont | 30 | - |

Olin Corporation | 26 | - |

Buffalo Marine Service, Inc. | 22 | - |

River City Towing Services | 19 | - |

Rhodia, Inc. | 19 | - |

Lyondell Chemical Company | 17 | - |

Shipper Owned Independent | Tank Barges Operated | Dry Cargo Barges Operated |

Dynegy Midstream Services | 16 | - |

Waxler Towing Company, Inc. | 15 | - |

Highland Towing | 15 | - |

ConocoPhillips Company | 15 | - |

Plaquemine Towing Corp. | 13 | - |

Houston Marine Services, Inc. | 13 | - |

Devall Towing | 12 | - |

Chem Carriers, Inc. | 11 | - |

Westlake/GA&O Corporation | 10 | - |

Merichem Company | 8 | - |

Grifco | 8 | - |

Apex Towing | 7 | - |

Golding Barge Lines, Inc. | 6 | - |

Republic of Texas | 6 | - |

American Milling | 5 | 17 |

Barge Management, Inc. | 5 | - |

Mon River Towing, Inc. | 4 | 142 |

Reilly Industries | 4 | - |

Memphis Barge Lines | 2 | - |

Cytec Industries | 2 | - |

Jantran, Inc. | 1 | 3 |

Other dry cargo carriers | - | 9, 670 |

TOTAL | 2,816 | 18,279 |

Tank Barge Owners By Number of Tank Barges

Sparks Companies, March 2005

6

Fleet Size and Diversity

Total Tank Barges

2,816

Inland Tank Barge Industry

| 1,205 | Double Skin 30K barges |

| 1,292 | Double Skin 10K barges |

| 124 | Double Skin < 10K barges |

| 195 | Single Skin barges |

2,816 | Total |

Industry Fleet Hull Profile

Source: Sparks Companies, March 2005

Inland Tank Barge Fleet

2005 |

2006 |

113

29

Total Industry

New Construction on Order

31 Clean

8 Black Oil

39 Total

7 Clean

8 Black Oil

15 Total

2005

2006

Kirby New Construction Plan

New Construction | 23 | 39 | 15 | 6 | 9 | 11 | 18 |

Number of Barges

Barrel Capacity (mm)

Kirby Fleet Status

10,000 bbl – Clean | $1.0M |

30,000 bbl – Clean | $2.1M |

30,000 bbl – Heated Black Oil | $2.7M |

New Construction Prices

Construction labor | 38% |

Steel, steel products | 37% |

Components | 17% |

Engineering | 8% |

100% |

New Construction Cost

Components

Components

Logistics Management System

Logistics Management System

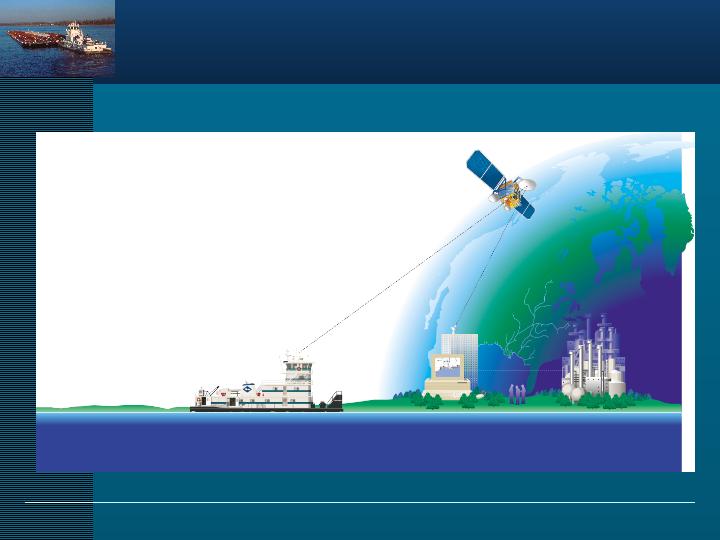

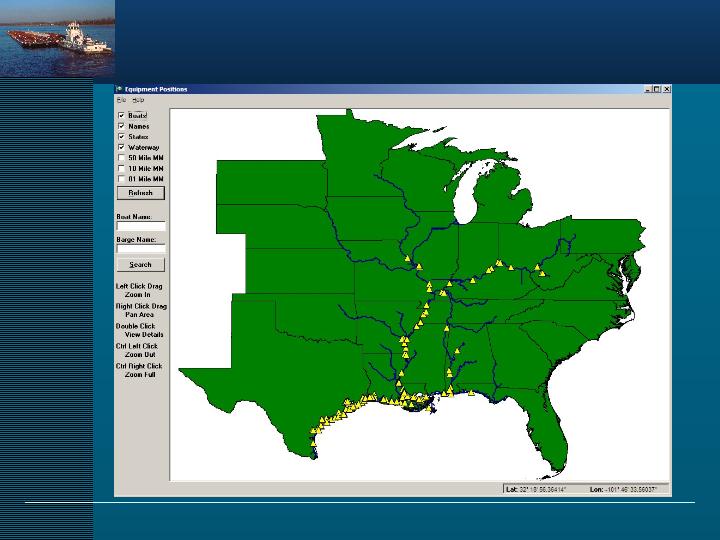

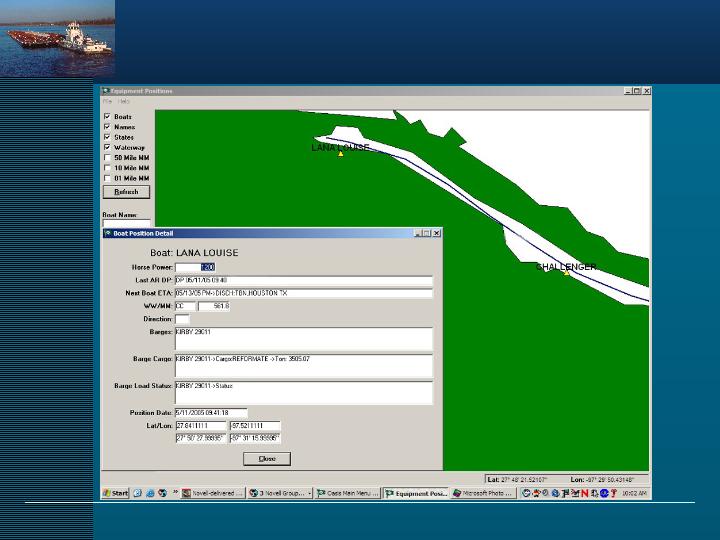

State-of-the-Art Communication and Positioning

Kirby Leads Industry

| • | All equipment locations instantly available to customer |

| – | Current position |

| – | ETA to customer’s dock |

| – | Information available from booking to final invoice |

Logistics Management

Equipment Positioning

Equipment Positioning

Kirby Leads Industry

| • | All equipment locations instantly available to customers |

| – | Current position |

| – | ETA to customer’s dock |

| – | Information available from booking to final invoice |

Logistics Management

| • | Advanced logistics system enables higher equipment utilization and increased efficiency |

| • | Kirby’s software automatically selects least cost communications route |

| • | Communication system allows Kirby to effortlessly comply with new security regulations |

Marine Workforce

| • | Focus on Safety |

| • | Recruit |

| • | Train to be the best |

| • | Retain skilled personnel |

| • | Offer excellent pay and benefits |

| • | Provide advancement opportunity |

| • | Foster community environment |

Recruit, Train and Retain

Captains / Pilots

Tankermen

Deckhands / Tankerman Trainees

Engineers

1,295 Marine Employees

468

424

307

96

Vessel Personnel Profile

Average Years of Service

Captains / Pilots

Tankermen

Engineers

12

5

13

Vessel Personnel Profile

| • | Recruit |

| – | Hirethe right people |

| – | Provide opportunity in rural areas with weak job markets |

| – | Comprehensive screening |

| • | Training and Development |

| – | Only company-owned and operated Training Center in industry |

| – | U.S. Coast Guard-approved programs |

| – | Provide safety and job skill training |

| – | Steersmen Training Program ensures lower turnover |

Recruit, Train and Retain

| • | Retain skilled personnel |

| – | Retain 30% we hire licensed from the outside |

| – | Retain 90% of the personnel we train in our program from deckhand to pilot |

Recruit, Train and Retain

Deckhand

Tankerman

Steersman

Pilot

Relief Captain

Captain

Starting salary

$29,000

As soon as 6 mos.

$31,200 to $44,300

In 2-3 years

$46,900

In 3-5 years

$71,900

In 5-10 years

$76,500

In 10 years

$82,000* Up to

$100,000 plus

bonus

$100,000 plus

bonus

Kirby Offers Excellent Benefits

| Highly competitive wages | 401(k) |

| Insurance | Disability coverage |

| Pension plan | Annual incentive bonus |

| Free training | Longevity pay* |

| Paid salary while training | Holiday pay* |

Provide Advancement

Opportunity

Opportunity

2:00 – 2:05 | Welcome and Introductions |

2:05 – 2:30 | U.S. Inland Waterways |

2:30 – 3:00 | Kirby Overview |

3:00 – 3:15 | Kirby Inland Marine · Kirby and Industry Fleet Profile |

3:15 – 3:30 | Break 15 minutes |

3:30 – 3:50 | Kirby Engine Systems Overview |

3:50 – 4:35 | Outlook for the Petrochemical Industry · Chemical Market Associates, Inc. |

4:35 – 5:20 | Refined Products Supply & Demand Drivers · Purvin & Gertz, Inc. |

5:20 – 5:25 | Closing Remarks |

Agenda

Kirby Analyst/Investor Meeting

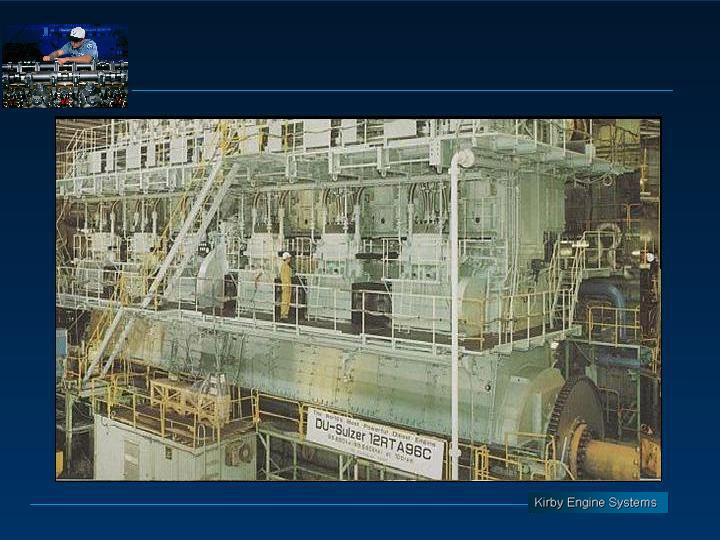

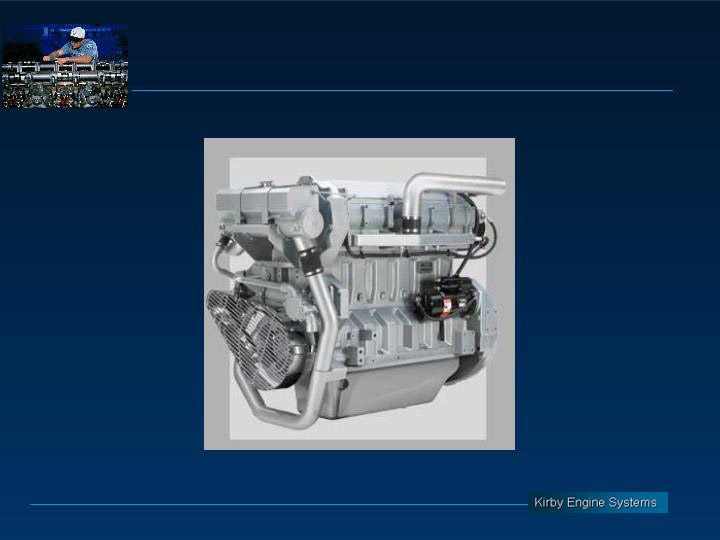

The Diesel Engine

Service Market

Service Market

Engine Speed | Horsepower Range | Applications | Manufacturers | |

Slow Speed | Less than 400 RPM | 7,000 – 108,000 hp | Large diesel-powered ocean going tankers, cruise ships, container ships and cargo carriers | Man B&W, Sulzer, Wartsila |

Medium Speed | 400 – 1,000 RPM | 800 – 32,000 hp | Locomotives, inland towing, ocean towing, oil services, harbor towing, fishing, power generation | EMD, GE, Caterpillar/MAK, MAN B&W, Colt-Pielstick, Wartsila |

High Speed | Over 1,000 RPM | 50 – 8,375 hp | On- and off-road trucks and equipment, oil services, inland towing, power generation, locomotives | Caterpillar, Cummins, MTU, Mitsubishi, Volvo, John Deere |

Basic Diesel Engine Types

Slow Speed Diesel Engine

Medium Speed Diesel Engine

High Speed Diesel Engine

No. of Engines* | % of Outstanding Population | |

EMD | 4,500 | 39% |

Detroit Diesel | 3,300 | 29% |

Caterpillar | 2,400 | 21% |

Cummins | 1,200 | 11% |

Marine Engines

*Estimated marine engines

What We Do

| • | Sell new & remanufactured OEM parts |

| – | EMD and Alco medium speed diesel engines |

| – | Caterpillar, Cummins and Detroit Diesel high speed diesel engines in Midwest market |

| • | Provide skilled labor & specialty services |

| – | Diesel engine repairs, overhauls & rebuilding |

| – | Marine reduction gear repairs & overhauls |

Seattle

Paducah

Houma

Chesapeake

Rocky Mount

Tampa

Miami

Facility Locations

2004 Revenue

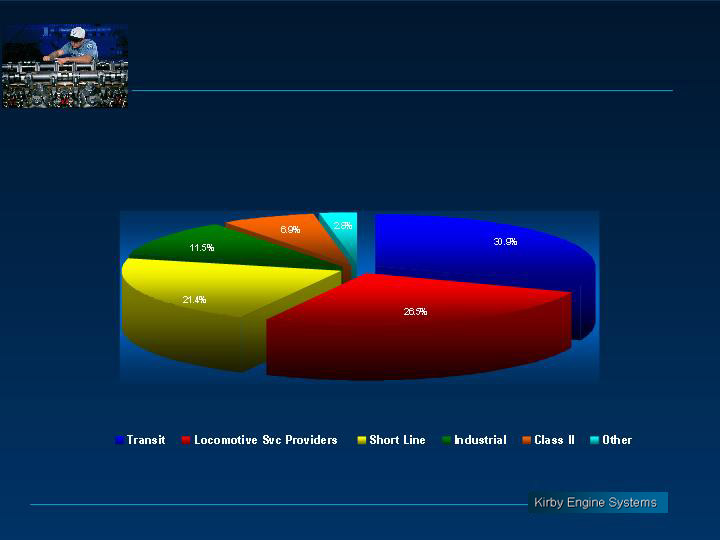

Rail

21%

Marine

59%

Power

Generation

20%

KES Primary Markets

Revenue Sources

| • | Part Sales (51%) |

| – | New parts |

| – | Nuclear parts dedication |

| – | Rebuilt parts |

| • | Services (49%) |

| – | Complete overhauls to OEM specifications |

| – | ABS certified block welding |

| – | In-place machining |

| – | Laser alignment |

| – | Troubleshooting |

| – | Preventive maintenance |

| – | Engine controls modifications |

Top Ten Customers

| • | America Electric Power (AEP) |

| • | Amtrak |

| • | Crowley |

| • | ENSCO (ESV) |

| • | Exelon (EXC) |

| • | Ingram Barge Company |

| • | Maritrans (TUG) |

| • | Moran Towing |

| • | New Jersey Transit |

| • | Tidewater, Inc. (TDW) |

59% of Total Revenue

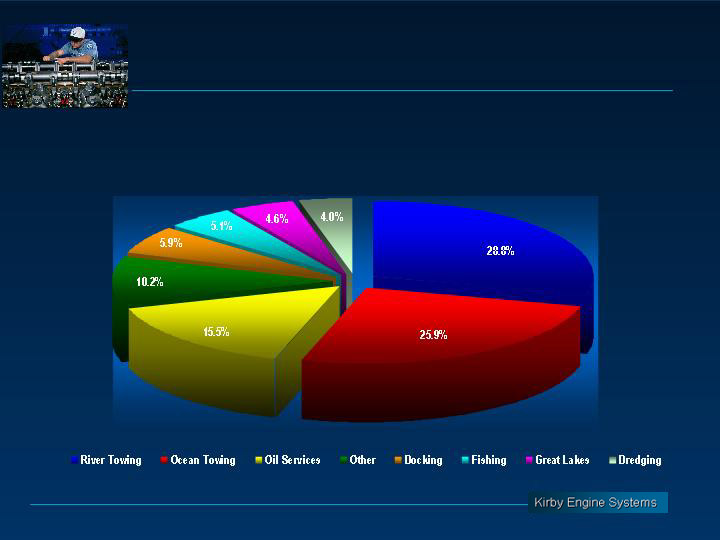

Marine Markets

Marine Market Drivers

| • | Market Drivers |

| – | Chemicals, petrochemicals, fertilizer, black oil, refined products, grain, coal, cement & steel |

| – | General import/export activity |

| • | Containers |

| • | Break bulk |

| – | Exploration and drilling |

21% of Total Revenue

Rail Markets

Rail Market Drivers

| • | Market Drivers |

| – | Commuter demand |

| – | Chemicals, petrochemicals, fertilizer, black oil, grain, coal, cement, automotive and steel |

| – | Containers |

20% of Total Revenue

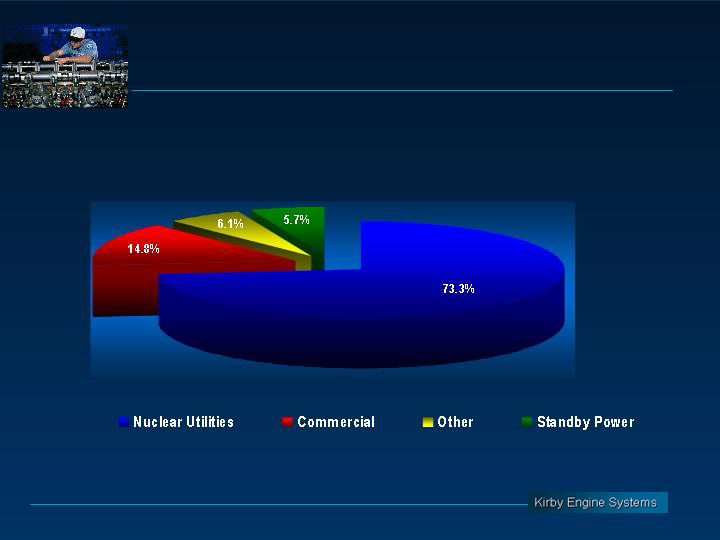

Power Generation Markets

Power Generation Market

Drivers

Drivers

| • | Market Drivers |

| – | Increasing electrical demand |

| – | Nuclear license renewals |

| – | Technology upgrades/modifications |

| – | Maintenance outsourcing |

Growth Opportunities

| • | Organic |

| – | Emissions Reduction Programs - new services to existing customers |

| – | Term Maintenance Contracts |

| • | Acquisition |

| – | Competitors |

| • | High Speed Diesel Engine Services |

| – | Engine Populations |

| • | New product lines for existing customers |

| • | New product lines for new customers |

2:00 – 2:05 | Welcome and Introductions |

2:05 – 2:30 | U.S. Inland Waterways |

2:30 – 3:00 | Kirby Overview |

3:00 – 3:15 | Kirby Inland Marine · Kirby and Industry Fleet Profile |

3:15 – 3:30 | Break 15 minutes |

3:30 – 3:50 | Kirby Engine Systems Overview |

3:50 – 4:35 | Outlook for the Petrochemical Industry · Chemical Market Associates, Inc. |

4:35 – 5:20 | Refined Products Supply & Demand Drivers · Purvin & Gertz, Inc. |

5:20 – 5:25 | Closing Remarks |

Agenda

Kirby Analyst/Investor Meeting

Outlook for Commodity

Chemicals in the United States

May 19, 2005

Presentedto:

Transportation Analyst Group

Outline

| • | 40,000 ft - Global Economic view, petrochemical cycle, new investment |

| • | 10,000 ft– Changing role of U.S. olefins industry, impact on feedstocks & derivatives |

| • | River Level– Bottom line, things are changing, but liquid movements expected to trend higher |

Chemicals & plastics markets

are in a full revival mode

Economic recovery firmly

entrenched – especially in

Asia & Americas.

The rate of new capacity

additions increasing but

remaining measured

Hyper natural gas & oil markets

maintaining high price levels

Producers leveraged their position of market strength,

improved profitability regardless of cost changes

improved profitability regardless of cost changes

Current Global Market Conditions…

Short-term Outlook Is Somewhat Tempered

Developing world healthy, Japan and Europe slowing

Geopolitical Uncertainties & High Energy are a big negative

Services Sector still very strong. Can China moderate?

Sustained by Longer-term Supporting Strengths

Monetary and Fiscal policies imply continuation

Moderately higher interest rates are still simulative

Banking Systems supportive and functioning well

International trade still gaining momentum (WTO)

Global Expansion Remains Firmly Entrenched

Recovery still responding to several stimuli

Developed Country consumption remains strong

The Economic Outlook

Next Two Years

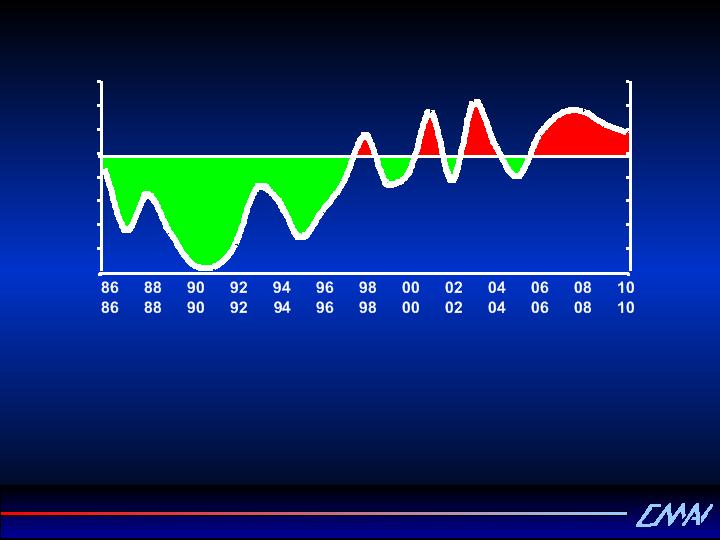

Global GDP Growth Rates

Constant 2000 Dollars

-2

-1

0

1

2

3

4

5

6

7

8

81

83

85

87

89

91

93

95

97

99

01

03

05

07

09

Percent Change

Global

U.S.

Demand Is Robust!

Petrochemicals

Health Care

Household Goods

Rubber & Plastics

Transportation

Construction

Food &

Beverage

Beverage

Textiles

Electronics

Impact of High Energy Prices

| • | Economies have underperformed by about 0.75 points |

| • | Extreme volatility |

| • | Declining energy prices will be supportive of economic growth in 2007 - - 2009 |

Feedstock Cost: Impacts all Regions

(well, some more than others…)

(well, some more than others…)

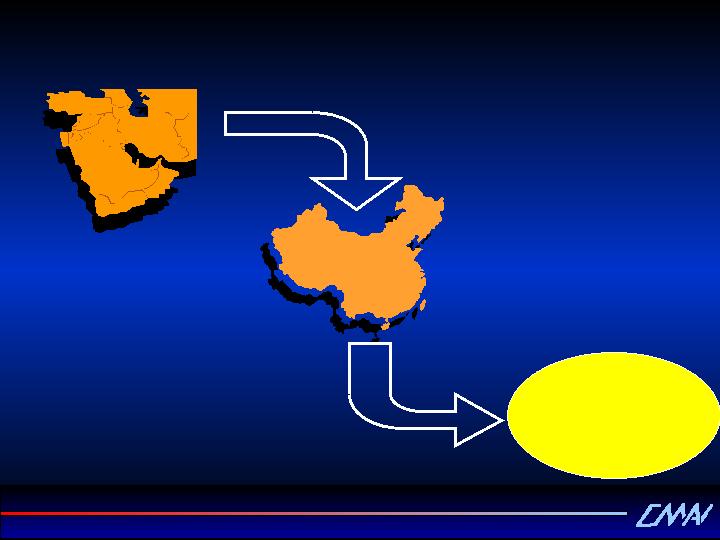

| • | Dramatic Increase in North America with higher natural gas prices |

| • | Up in West Europe, Latin America & Asia with $50+ per barrel crude oil |

| • | Middle East remains the lowest |

Middle East Advantage is All Natural Gas

Based

Based

$7.50/$50

$5.50/$47

$1.00/$45

$4.50

/$49

/$49

Nat Gas $/MMbtu /Crude Oil $/bbl

Ratio of Natural Gas vs. Crude Oil Price in the U.S.

40%

50%

60%

70%

80%

90%

100%

110%

120%

Environmental emphasis was not offset with sufficient supply incentives

Drilling (replacement) rates have not maintained pace - steady demand growth

Market will produce sufficient supply/demand reaction – at best, back to parity

(Conservation – Demand Switching – LNG Terminals – Northern Gas)

(Conservation – Demand Switching – LNG Terminals – Northern Gas)

Btu basis using 6 million per bbl for oil

40%

50%

60%

70%

80%

90%

100%

110%

120%

U.S. petchem industry was built on natural gas - an abundant and low cost fuel

Current Crude Oil

Current Nat Gas

U.S. Energy

Values

Values

10

15

20

25

30

35

40

45

50

55

86

87

88

89

90

91

92

93

94

95

96

97

98

99

00

01

02

03

04

05

06

07

08

09

10

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

9.00

($ per barrel)

($ per mmBtu)

Market Forces Will Eventually Return Energy

Prices To Fundamental Levels(Greenspan April-05)

Prices To Fundamental Levels(Greenspan April-05)

Rising crude oil prices impact

chemicals sector earnings

most severely in periods of

oversupply

chemicals sector earnings

most severely in periods of

oversupply

Strong market conditions

allow producers to pass

through rising costs (and

more), building up margins

allow producers to pass

through rising costs (and

more), building up margins

Cost push supported price

increases facilitate higher

earnings when cost fall – but

tight conditions must persist

increases facilitate higher

earnings when cost fall – but

tight conditions must persist

Sector Leverages High Energy Prices...

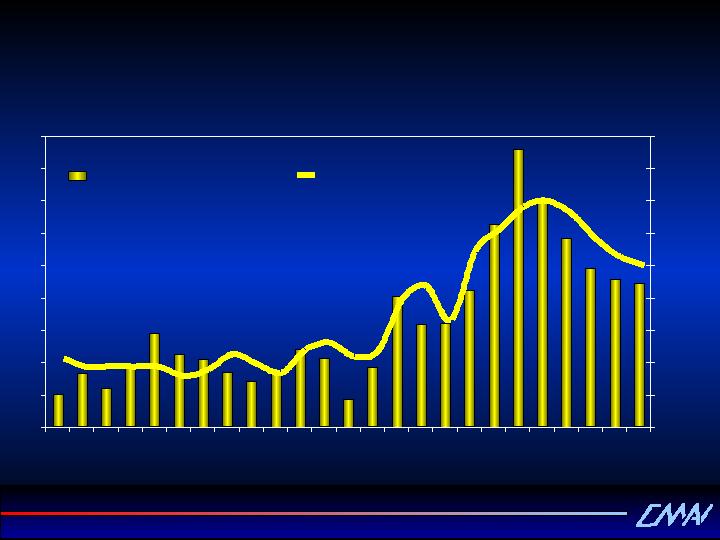

Basic Chemicals and Plastics

Annual Demand Growth

0

5

10

15

20

25

30

90

91

92

93

94

95

96

97

98

99

00

01

02

03

04

Million Metric Tons

Timing &

Duration

Duration

Ethylene

Glycol

Glycol

There now or

may not get

there

may not get

there

Remain above

for several

more years

for several

more years

From a Re-Investment Perspective

From a

Historical

Perspective

Historical

Perspective

Lower than

before

before

Higher than

previous

peaks

previous

peaks

PET

Resins

Resins

PE

Resins

Resins

PP

Resins

Resins

Ethylene

Propylene

Benzene

ECUs

Methanol

Paraxylene

Styrene

PS

Resins

Resins

PVC

Resins

Resins

Quality of

the

Earnings

the

Earnings

From a non-integrated

vantage

vantage

Up Cycle Peak Earnings Profile

Americas

Europe

Middle East/Africa

Asia Pacific

-2

0

2

4

6

8

10

Million Tons

00

01

02

03

04

05

06

07

08

09

10

Global Ethylene Capacity Growth

Global Assembly Line

Commodities to Converted Products to Retail Goods…

Growth In Chemicals

Demand Will Continue

To Outpace That Of

The World Economies

Demand Will Continue

To Outpace That Of

The World Economies

Extremely Efficient

Supply Chains Have

Been Developed -

Internationals and WTO

Very Supportive

Supply Chains Have

Been Developed -

Internationals and WTO

Very Supportive

Improving Standard Of

Living In China Has

Significantly Increase

Internal Consumption

Living In China Has

Significantly Increase

Internal Consumption

Implies That Current

Pace Of Additions Can

Be Absorbed As Long As

Restraint Continues

Pace Of Additions Can

Be Absorbed As Long As

Restraint Continues

Hydrocarbon

Value

Labor Cost

Consumer

Demand

Demand

Largest Deleterious

Impact on PE

Impact on PE

World

0.0

20.0

40.0

60.0

80.0

100.0

120.0

140.0

160.0

99

00

01

02

03

04

05

06

07

08

09

PE 3.6 / 4.9*

Ethylene Oxide 4.0 / 5.3*

EDC 2.4 / 3.2*

EBZ 3.4 / 4.1*

Others 1.2 / 3.0*

Capacity 3.6 / 4.8*

Million Metric Tons

*%AAGR 99-04 / %AAGR 04-09

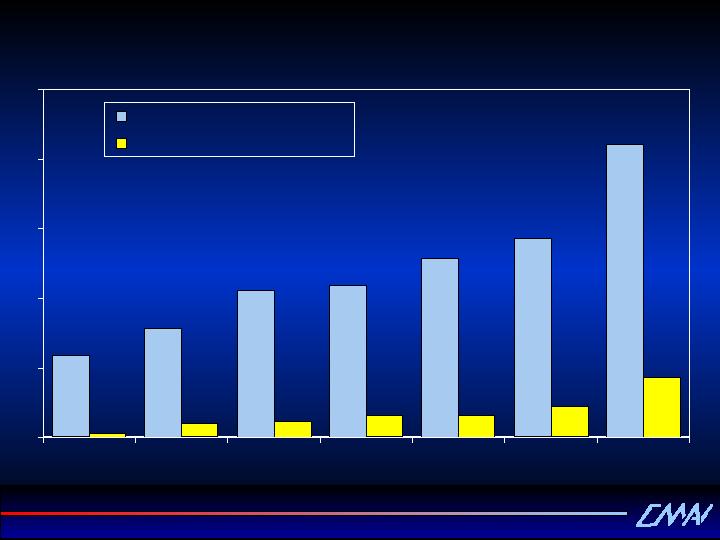

Ethylene Demand Forecast

Total Demand Growth = 4.4% AAGR 2004-09

0

100

200

300

400

500

600

700

800

00

01

02

03

04

05

06

07

08

09

Dollars Per Ton

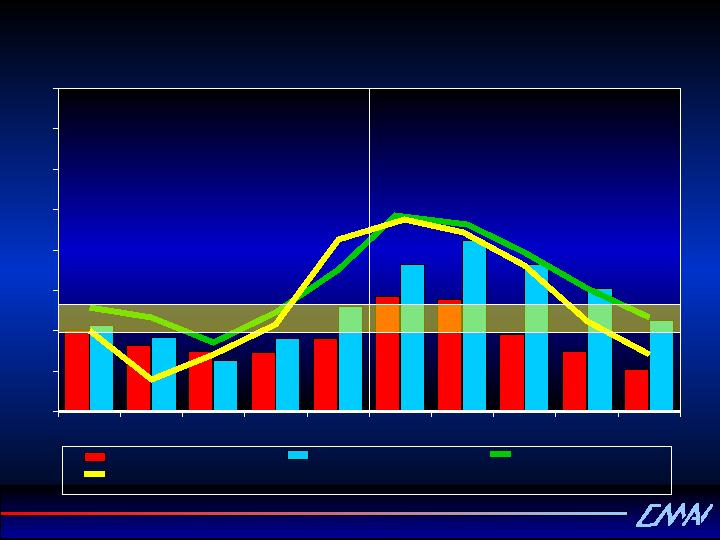

U.S. Ethane

U.S. Light Naphtha

WEP Naphtha

NEA Naphtha

Global Ethylene Cash Margins

Ethylene Margin Outlook Very Positive

U.S. Producers Respond

by Closing or Revamping E/PUnits

Feedstock Required Per Ton of Ethylene

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

Ethane

Propane

Butane

Light Naphtha

Gasoil

Tons

0

0.5

1.0

1.5

2.0

2.5

3.0

Ethane

Propane

Butane

Light

Naphtha

Naphtha

Gasoil

Volume of Liquid Co-products

per Ton of Ethylene

Tons

0

5

10

15

20

25

30

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

Million Tons

Ethane/Propane

Naphtha

Gas Oil

Others

Butane

U.S. Ethylene Production by Feedstock

(trend is flat to declining)

0

10

20

30

40

50

60

70

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

Million Tons

Naphtha

Gas Oil

Butane

Ethane/Propane (pipeline)

U.S. Ethylene Feedstock Requirements

(heavier feedslate will require increased liquid movements)

Co-Product Yield

Avg 2.7 million

tons/yr more than

2004 baseline

tons/yr more than

2004 baseline

0

2

4

6

8

10

12

14

16

18

20

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

Million Tons

Propylene

Butadiene

U.S. Propylene & Butadiene

Domestic Demand Forecast

Avg 1.0 million

tons/yr more than

2004 baseline

tons/yr more than

2004 baseline

Regional Refining & Reforming

0

5

10

15

20

25

SAM

ISC/SEA

AFR/MDE

CEP/FSU

NEA

WEP

NAM

Crude Refining Capacity

Reforming Capacity

MMBPCD

Sources: PGI/CMAI

0

5

10

15

20

25

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

Million Tons

Benzene

Styrene

Cumene

Phenol

Cyclohexane

U.S. Benzene & Derivative

Domestic Demand Forecast

Avg 500 thousand

tons/yr more than

2004 baseline

tons/yr more than

2004 baseline

0

2

4

6

8

10

12

14

16

18

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

Million Tons

Mixed Xylene

Paraxylene

Toluene

U.S. Xylene & Toluene

Domestic Demand Forecast

Avg 600 thousand

tons/yr more than

2004 baseline

tons/yr more than

2004 baseline

U.S. MTBE Federal Actions – Will it Pass?

| • | Federal Ban to pass eventually, but tough negotiation still required. |

| • | Energy Bill has been stalled in Congress since 2000, high priority for 2005. |

| – | Oxygen Mandate removed effective 270 days after the bill is signed |

| – | MTBE banned explicitly beginning 2015, but individual states can override and production for export expressly permitted |

| – | Renewable Fuels Standard (RFS) in 2007 (?) |

NAM

49.3%

SAM

1.6%

WEP

16.7%

CEP

6.4%

NEA

13.4

%

%

SEA

3.8%

MDE

7.7%

ISC

0.4%

AFR

0.8%

Total Demand =

16.1 Million Tons

16.1 Million Tons

2004

2009

NAM

26%

SAM

2%

WEP

12%

CEP

12%

NEA

23%

SEA

6%

AFR

1%

MDE

17%

ISC

1%

Total Demand =

10.8 Million Tons

10.8 Million Tons

Global MTBE Demand

- adopted ban prior to 2004

- adopted ban in/after 2004

- pending

States with MTBE Ban

3.1%

States with MTBE Ban

% consumption

- adopted ban prior to 2004

- adopted ban in/after 2004

- pending

31.7%

0.8%

1.1%

7.5%

States with MTBE Ban

% consumption

- adopted ban prior to 2004

- adopted ban in/after 2004

- pending

States with MTBE Ban

- adopted ban prior to 2004

- adopted ban in/after 2004

- pending

0

5

10

15

20

25

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

Million Tons

MTBE

Methanol

U.S. MTBE, Methanol & Ethanol

Domestic Demand Forecast

Ethanol

Mitigating Factors Around MTBE

| • | Vast Majority of MTBE moves via pipeline |

| • | States retaining MTBE are in Gulf Coast region |

| • | MTBE ban requires greater movement of other octane components |

| • | RFS will ultimately lead to longer mid-west to coast and inter-coastal barge movement of ethanol (all forms of ethanol are prohibited in pipeline system) |

| • | Japan evaluating large ETBE requirement for Kyoto Agreement that would require several U.S. units to convert |

| • | Isobutane dehydro units will be retrofitted to iso-octane swapping out MTBE movements |

Conclusions

| • | Global petrochemical markets are enjoying a significant up-cycle |

| • | Naphtha/gas oil based ethylene production remains competitive in the industrialized regions |

| • | U.S. producers have moved towards cracking more liquids that increase both feedstock and co-product volumes and traffic |

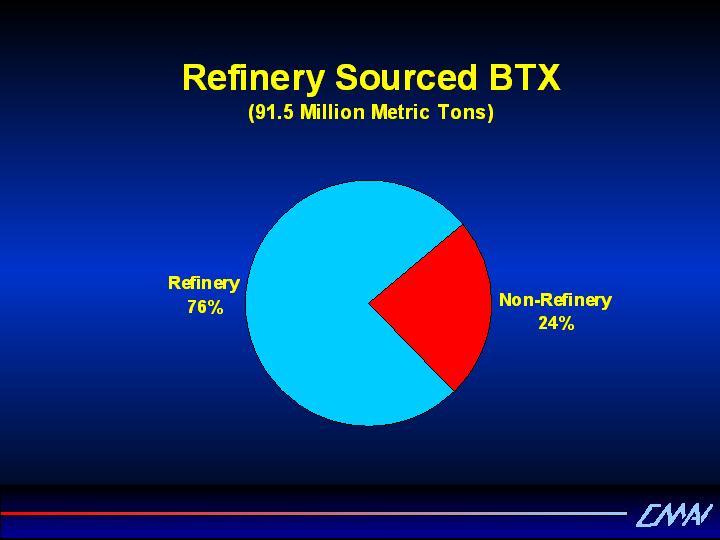

| • | Basic aromatics production is dominated by refinery sources and the U.S. remains the clear leader in supply |

| • | MTBE reductions will be largely off-set by ethanol opportunities |

2:00 – 2:05 | Welcome and Introductions |

2:05 – 2:30 | U.S. Inland Waterways |

2:30 – 3:00 | Kirby Overview |

3:00 – 3:15 | Kirby Inland Marine · Kirby and Industry Fleet Profile |

3:15 – 3:30 | Break 15 minutes |

3:30 – 3:50 | Kirby Engine Systems Overview |

3:50 – 4:35 | Outlook for the Petrochemical Industry · Chemical Market Associates, Inc. |

4:35 – 5:20 | Refined Products Supply & Demand Drivers · Purvin & Gertz, Inc. |

5:20 – 5:25 | Closing Remarks |

Agenda

Kirby Analyst/Investor Meeting

U.S. Refining Industry Outlook

Bill Sanderson

May 19, 2005

Agenda

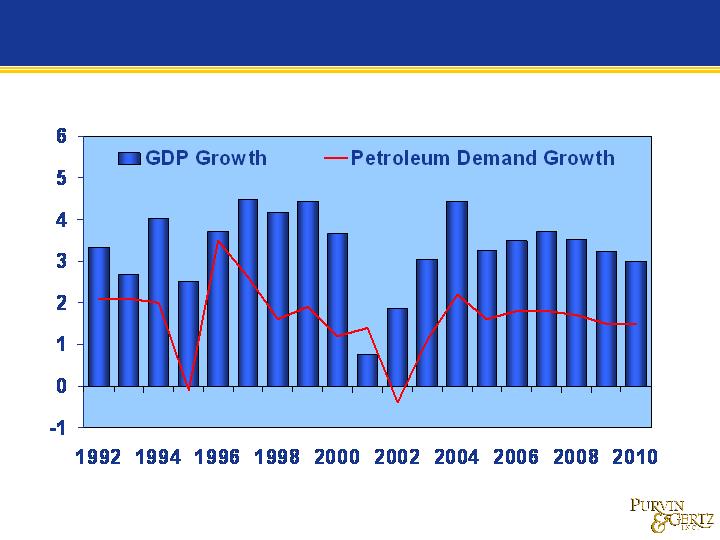

| Ø | U.S. Economic and Product Demand Outlook |

| Ø | Refining Industry Outlook |

| Ø | Regional Product Movements |

Percent Annual Growth

Note: GDP forecast provided by CMAI.

U.S. GDP and petroleum demand growth are

expected to remain strong short-term . . ..

expected to remain strong short-term . . ..

2005 – 2010

Year-to-Year Change, Thousand B/D

U.S. refined product demand is expected to

stay strong through this economic cycle . . ..

stay strong through this economic cycle . . ..

Will gasoline demand growth slow down

longer term?

longer term?

| Ø | Higher prices are beginning to affect consumer choices |

| § | Large SUV sales are beginning to fall |

| § | Hybrid sales are beginning to gain acceptance |

| Ø | In our view, policy and market factors are likely to increase vehicle efficiency after 2010 |

| Ø | Greenhouse Gas control may eventually become a U.S. regulatory goal, but not yet |

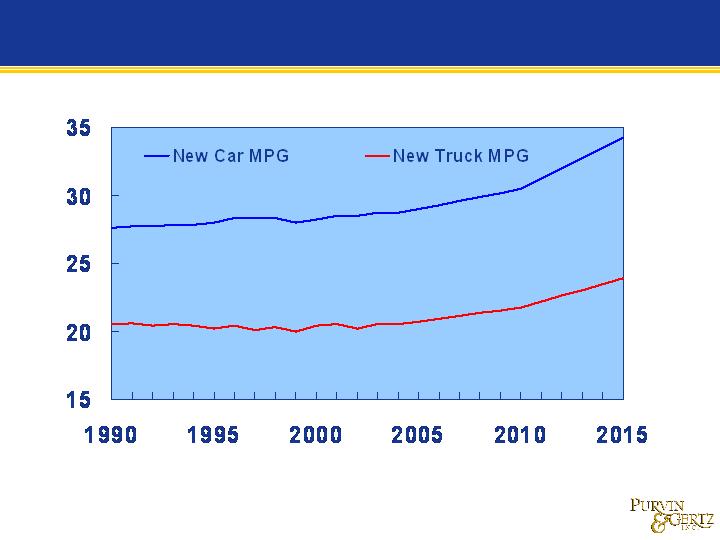

Note: Average U.S. new car efficiency

Miles per Gallon

Technology, policy and market factors expected

to increase new vehicle efficiency long-term ...

to increase new vehicle efficiency long-term ...

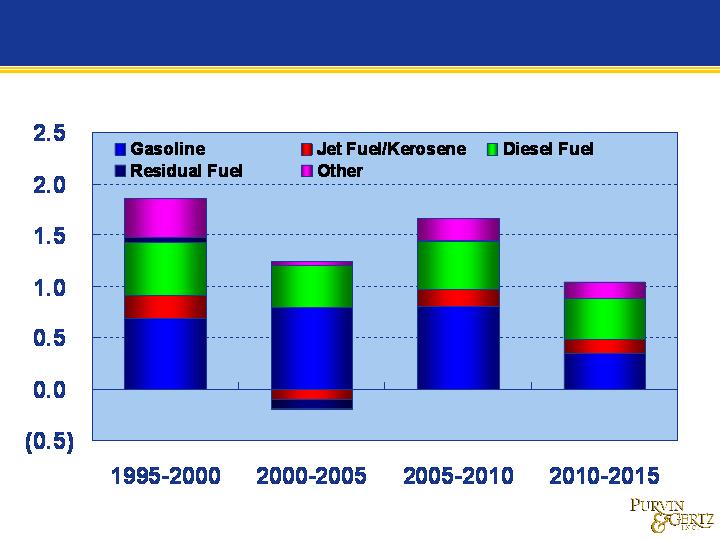

Five-Year Demand Change (Millions of B/D)

Gasoline demand to stay strong through 2010.

Diesel/jet fuel demand will remain strong . . .

Diesel/jet fuel demand will remain strong . . .

MTBE

Ban

(Cal.

and NY)

Low

Sulfur

Diesel

(15 ppm)

Low

Sulfur

Gasoline

(30 ppm)

(Tier 2)

Carbon taxes or

emissions controls?

2000-2006

2006-2010

Regulatory changes will continue to strongly

influence U.S. refining and distribution . .. .

influence U.S. refining and distribution . .. .

Renewable Fuel Requirements

MTBE Phaseouts

Increasing Vehicle Efficiency

Zero-sulfur fuels?

2010 +

Gasoline quality will continue improving . . .

| Ø | Sulfur is being reduced to 30 ppm |

| § | Sulfur poisons automobile emissions catalysts |

| § | Sulfur reductions provide … |

| • | Immediate emissions reduction impact on entire fleet |

| • | NOx trap capability |

| Ø | MTBE and Ethanol use will change |

| § | Nationwide MTBE ban expected, with many states moving more quickly |

| § | RFG oxygen mandate expected to disappear |

| § | Renewable mandate expected to boost ethanol |

| § | Current Energy Bill contains all these elements |

Both programs will affect the refining and

distribution industries . . ..

distribution industries . . ..

Gasoline Supply and Cost Impacts

Diesel Supply and Cost Impacts

| Ø | Upgrading of existing desulfurization capacity most common |

| Ø | May tighten international low-sulfur markets |

| Ø | Distribution, contamination issues remain unresolved |

| Ø | Recovery of ULSD costs of 5.0-6.0 cpg (vs 0.2%) expected |

| Ø | Refining investment to offset octane loss |

| Ø | Potential import reductions from non-complying suppliers |

| Ø | Increased domestic gasoline trade |

| Ø | Reduction in finished product distribution flexibility |

| Ø | Strong U.S. petroleum demand growth should continue through 2010 |

| Ø | Vehicle efficiency gains expected to reduce growth after the turn of the decade |

| Ø | Diesel growth will be stronger than gasoline |

| Ø | Refining capacity should remain tight for several years, due to investment lag times and focus on clean fuels compliance |

| Ø | Strong demand for U.S. product trade expected to continue in the near-term |

Supply/Demand Conclusions

Agenda

| Ø | U.S. Economic and Product Demand Outlook |

| Ø | Refining Industry Outlook |

| Ø | Regional Product Movements |

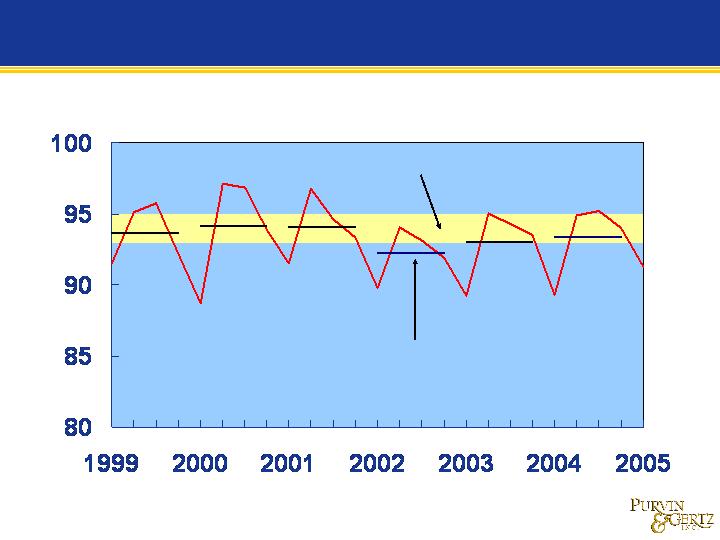

U.S. Refinery Utilization of Operating Capacity, %

Maximum Sustainable Capacity

Annual Average

Note: Figures are distillation capacity utilization for operating refineries.

U.S. refinery utilization has been operating at

or near capacity since the late 1990s . . .

or near capacity since the late 1990s . . .

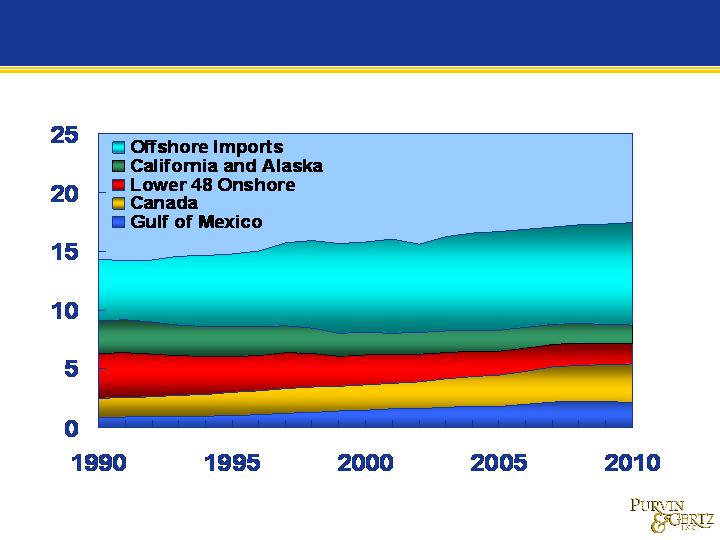

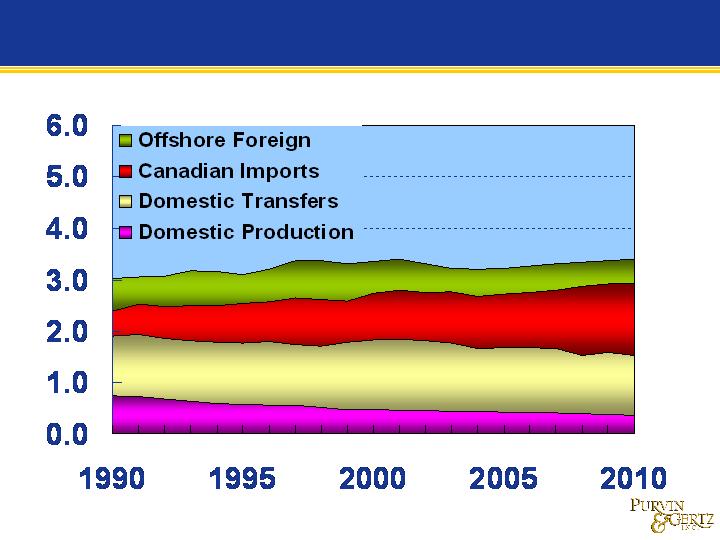

U.S. Crude Supplies by Source – Million B/D

Growth in crude oil supplies will be sourced by

offshore imports and Canadian supplies .. . .

offshore imports and Canadian supplies .. . .

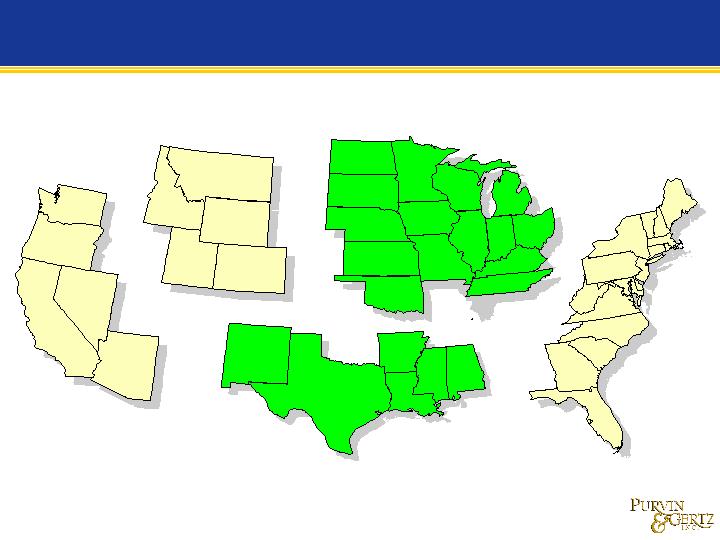

V

IV

III

II

I

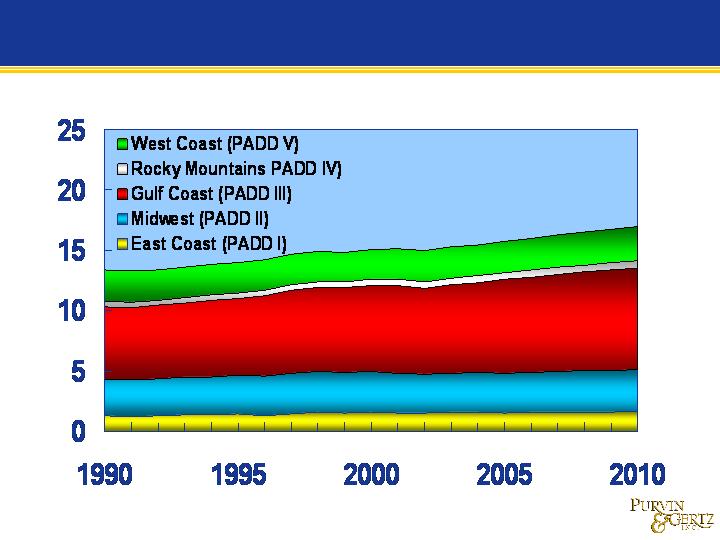

The U.S. market is divided into five Petroleum

Administration for Defense Districts (PADDs) . . .

Administration for Defense Districts (PADDs) . . .

PADD III includes the U.S. Gulf Coast which is

the largest refining region in the U.S. .. . .

the largest refining region in the U.S. .. . .

740

2,270

1,770

2,130

Total PADD III Distillation Capacity = 8.2 Million B/D

590

Note: Figures are distillation capacity for operating refineries in ‘000 B/D.

570

120

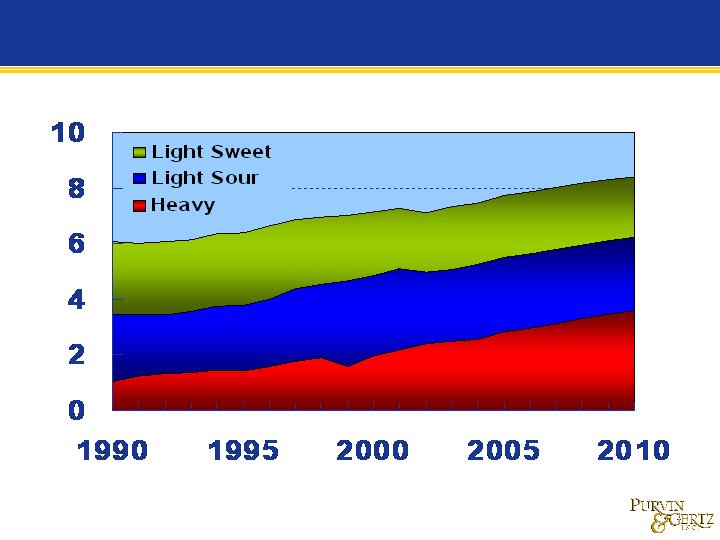

Crude Runs by Region - Million Barrels per Day

The Gulf Coast (PADD III) is the largest refining

region, at roughly 50% of the U.S. total . . .

region, at roughly 50% of the U.S. total . . .

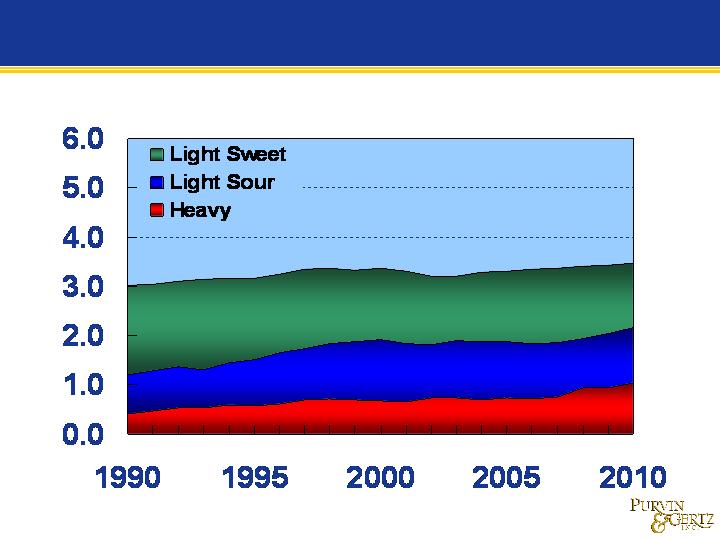

Gulf Coast Crude Oil Runs by Source, Million B/D

Gulf Coast (PADD III) crude runs will continue to

become heavier, driving refining investment ...

become heavier, driving refining investment ...

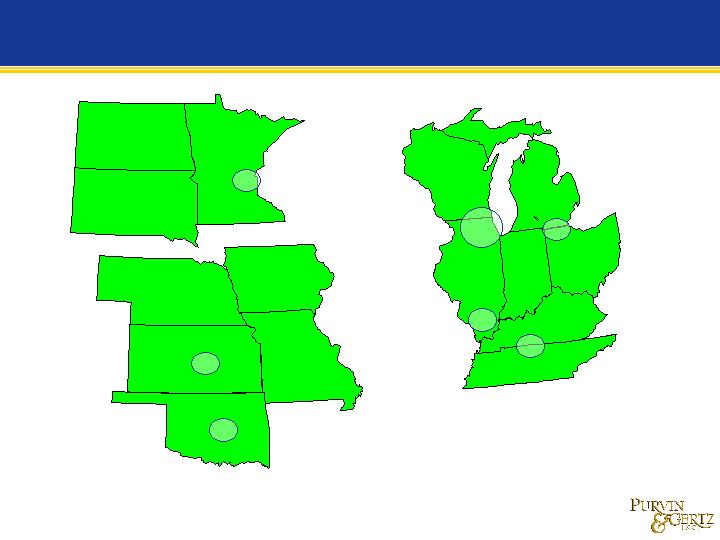

Midcontinent

Upper Midwest

Midwest

PADD II includes a number of sub-regions

comprised of smaller, local refining centers .. . .

comprised of smaller, local refining centers .. . .

Note: Figures are distillation capacity for operating refineries in ‘000 B/D.

Total PADD II Distillation Capacity = 3.6 Million B/D

400

420

870

500

600

300

490

Midwest Crude Oil Runs, Million B/D

Midwest (PADD II) crude supply balance

reflects growth of Canadian production . . ..

reflects growth of Canadian production . . ..

Midwest Crude Oil Runs, Million B/D

Midwest crude runs become heavier requiring

conversion capacity investment . . ..

conversion capacity investment . . ..

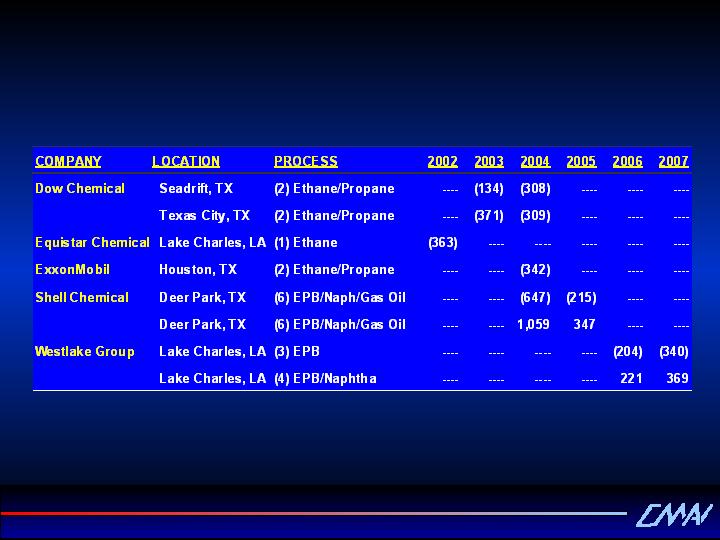

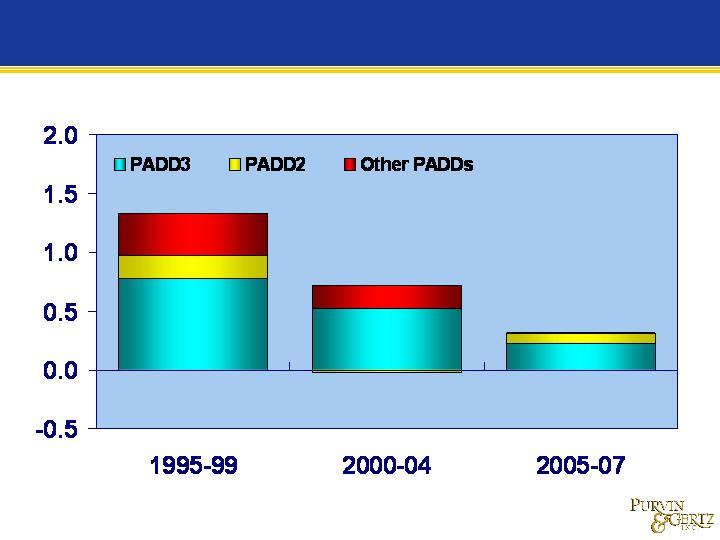

U.S. Refinery Distillation Capacity Changes

Thousand B/D of Capacity (Announced projects, excludes creep)

Million Barrels per Day

U.S. gasoline imports are expected to increase

until demand begins to slow late in decade . . .

until demand begins to slow late in decade . . .

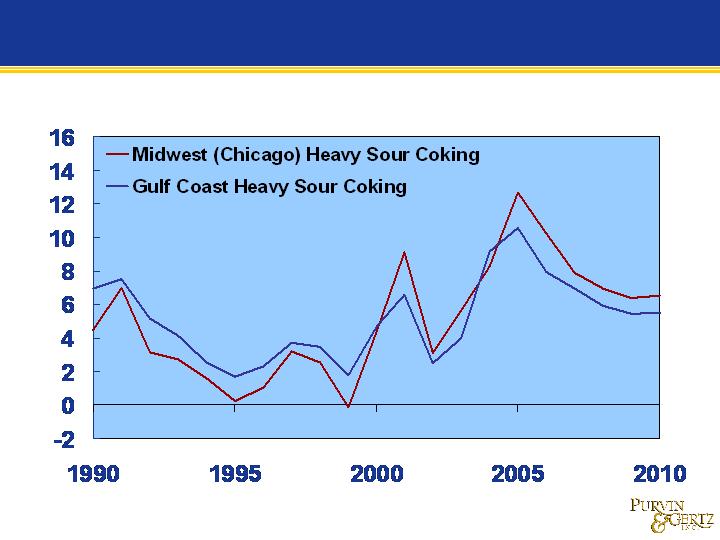

Forecast in Constant 2005 Dollars per Barrel

Comparable Gulf Coast and Midwest margins

track relatively well due to market factors . .. .

track relatively well due to market factors . .. .

Agenda

| Ø | U.S. Economic and Product Demand Outlook |

| Ø | Refining Industry Outlook |

| Ø | Regional Refined Product Movements |

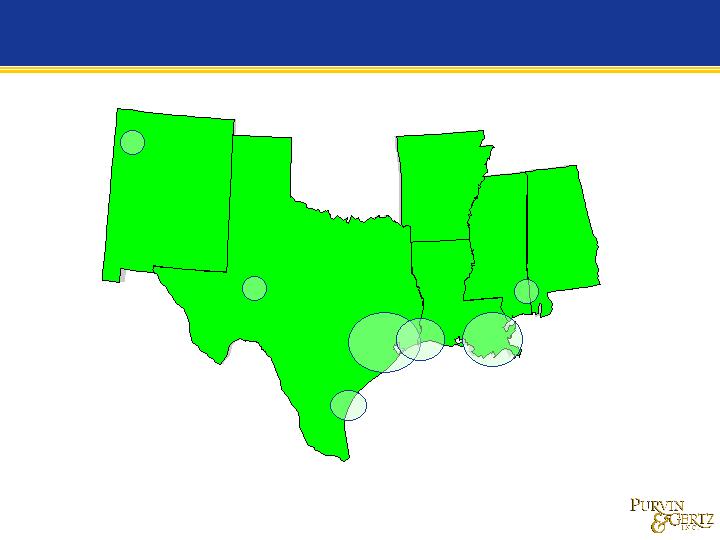

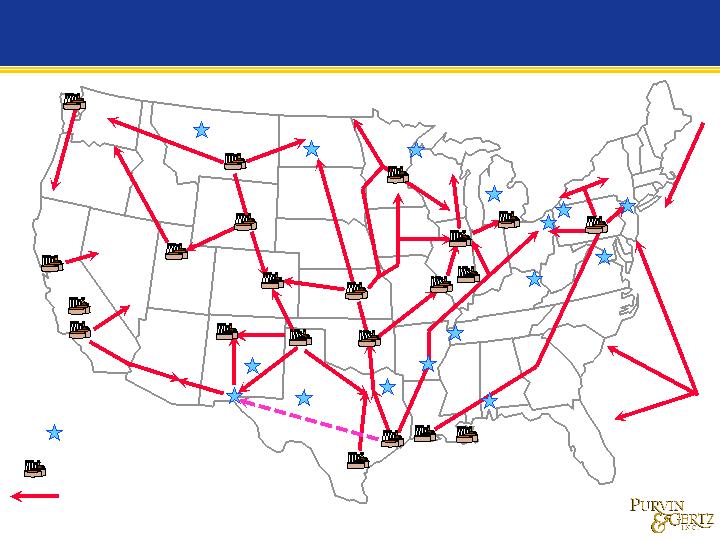

Refinery

Refining Centers

Refined product pipelines help integrate the

U.S. market . . .

U.S. market . . .

Refined Product Transportation

Routes

Routes

Refinery

Refining Centers

But the inland waterway system remains

crucial in supplying certain markets . . ..

crucial in supplying certain markets . . ..

Inland Waterways

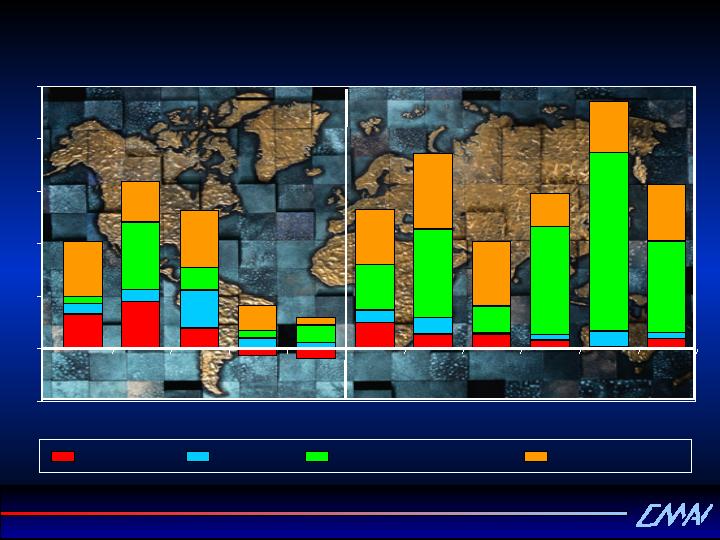

About 65% of PADD III products move to

consumers in PADDS I and II . . ..

consumers in PADDS I and II . . ..

PADD III Production

Major Light Products - Million B/D

Note: Major light products include gasoline, jet fuel and diesel fuels.

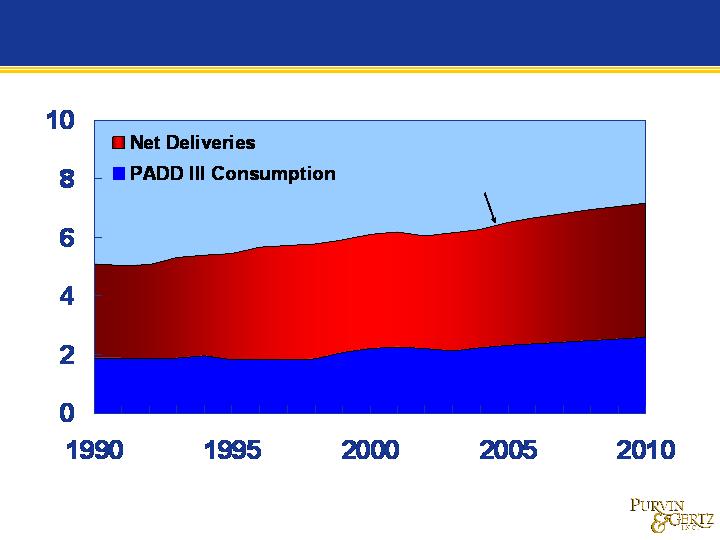

PADD II depends on PADD III for over 20% of

the total light product supply . . ..

the total light product supply . . ..

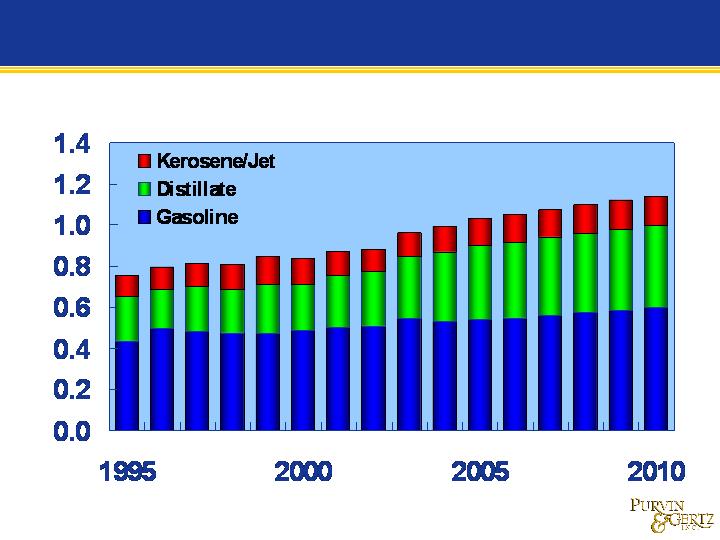

Major Light Products - Million B/D

PADD II Consumption

Note: Major light products include gasoline, jet fuel and diesel fuels.

PADD II receives large volumes of all light

refined products from PADD III . . ..

refined products from PADD III . . ..

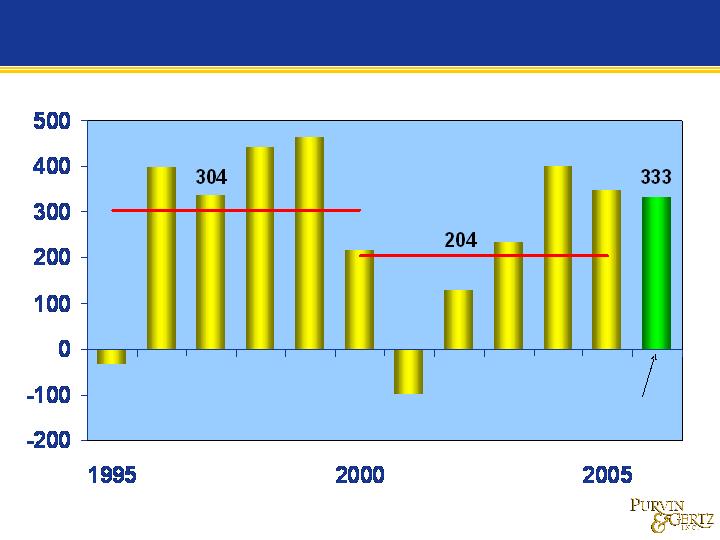

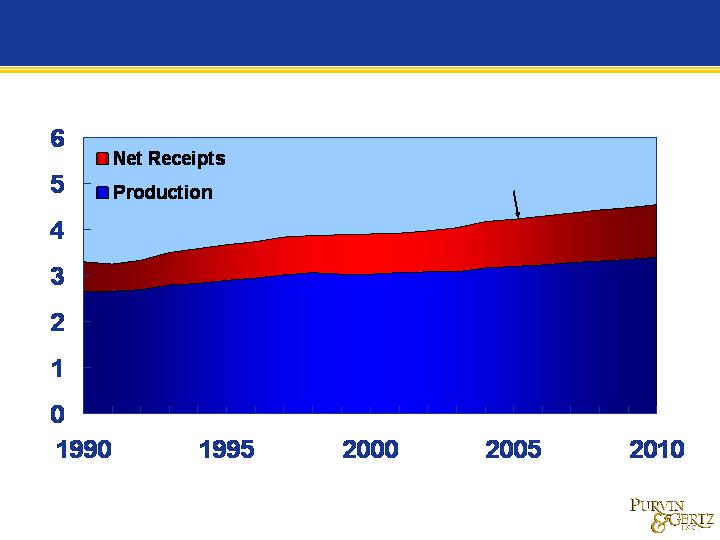

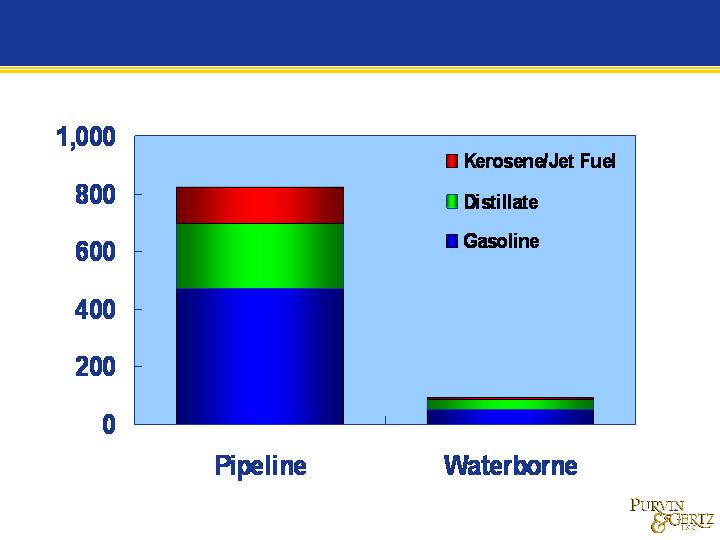

PADD II Net Receipts - Million B/D

Most light products move to PADD II by

pipeline . . .

pipeline . . .

Thousand B/D

Note: Product movements from PADD III to PADD II in 2004.

Thousand B/D

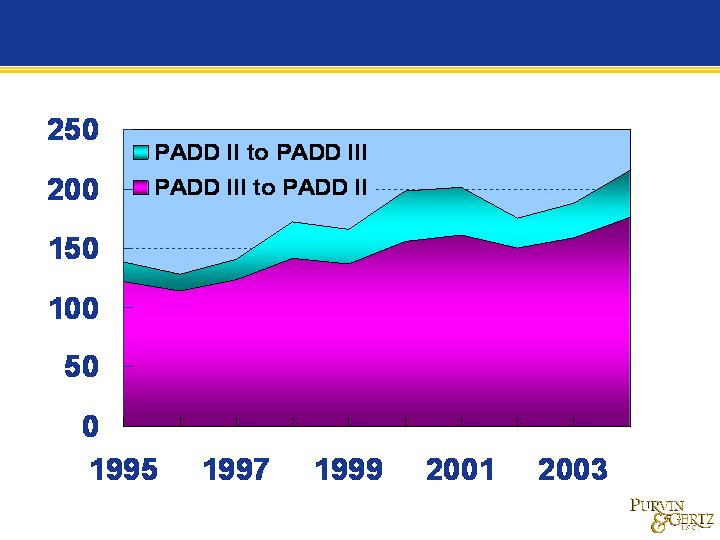

Waterborne commerce between PADD III and

PADD II has increased steadily . . ..

PADD II has increased steadily . . ..

Note: Waterborne product movements from PADD III to PADD II.

Thousand B/D

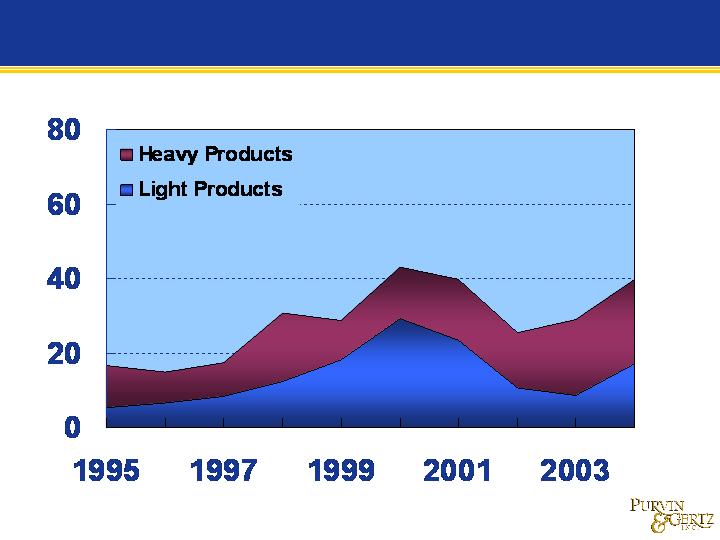

Movements from PADD III are primarily light

products . . ..

products . . ..

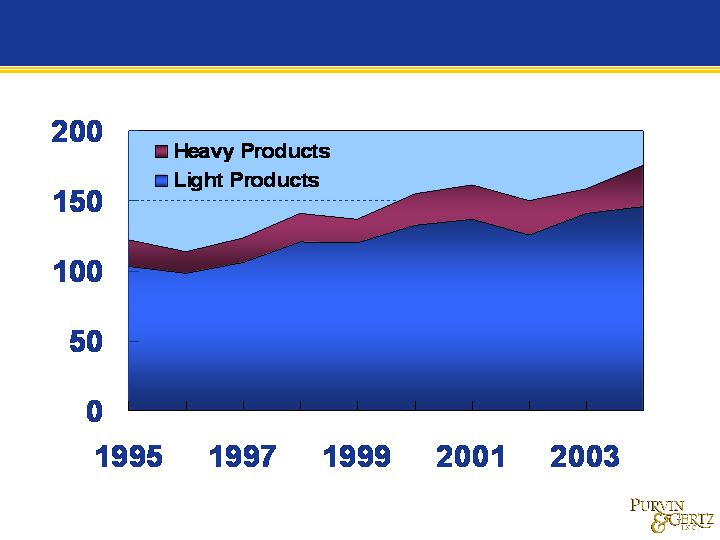

Note: Waterborne product movements from PADD II to PADD III.

Thousand B/D

PADD II generally moves out surplus heavy

products by water, some light products move .. . .

products by water, some light products move .. . .

Thousand B/D

Note: Waterborne movements from PADD II to PADD III. Figures for 2004

are estimated.

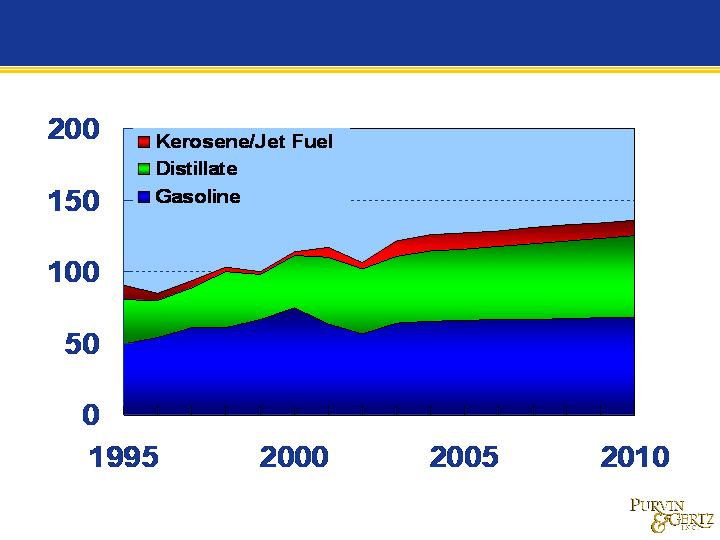

Waterborne light product movements from

PADD III to PADD II are projected to grow . . ..

PADD III to PADD II are projected to grow . . ..

Note: Waterborne movements from PADD II to PADD III. Figures for 2004

are estimated.

Thousand B/D

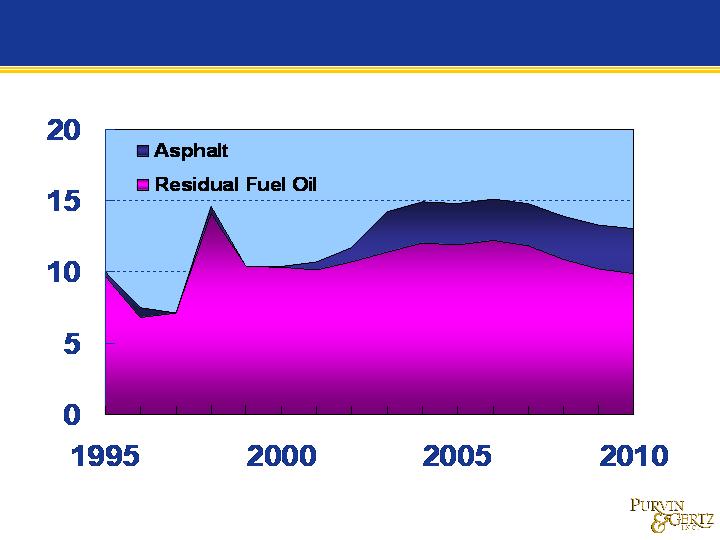

PADD II will remain in surplus for residual fuel

and asphalt . . ..

and asphalt . . ..

Conclusions

| Ø | Continued demand growth in PADD II will require additional movements to markets served by the inland waterway system |

| Ø | Growing heavy crude processing in PADD II will increase the local surplus of asphalt and residual fuel |

This analysis has been prepared for the sole benefit of Kirby Corporation. Neither the analysis nor any part of the analysis shall be provided to third parties without the written consent of Purvin & Gertz. Any third party in possession of the analysis may not rely upon its conclusions without the written consent of Purvin & Gertz. Possession of the analysis does not carry with it the right of publication.

Purvin & Gertz conducted this analysis utilizing reasonable care and skill in applying methods of analysis consistent with normal industry practice. All results are based on information available at the time of review. Changes in factors upon which the review is based could affect the results. Forecasts are inherently uncertain because of events or combinations of events that cannot reasonably be foreseen including the actions of government, individuals, third parties and competitors. NO IMPLIED WARRANTY OF MERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE SHALL APPLY.

Some of the information on which this analysis is based has been provided by others. Purvin & Gertz has utilized such information without verification unless specifically noted otherwise. Purvin & Gertz accepts no liability for errors or inaccuracies in information provided by others.

Terms and Conditions

U.S. Refining Industry Outlook

Bill Sanderson

May 19, 2005

2:00 – 2:05 | Welcome and Introductions |

2:05 – 2:30 | U.S. Inland Waterways |

2:30 – 3:00 | Kirby Overview |

3:00 – 3:15 | Kirby Inland Marine · Kirby and Industry Fleet Profile |

3:15 – 3:30 | Break 15 minutes |

3:30 – 3:50 | Kirby Engine Systems Overview |

3:50 – 4:35 | Outlook for the Petrochemical Industry · Chemical Market Associates, Inc. |

4:35 – 5:20 | Refined Products Supply & Demand Drivers · Purvin & Gertz, Inc. |

5:20 – 5:25 | Closing Remarks |

Agenda

Kirby Analyst/Investor Meeting

| • | Fundamentals have not been this good in 25 years |

| • | Business will continue to consolidate. Kirby is best positioned company to be the consolidator. |

| • | Strong free cash flow |

| • | Great operating leverage |

| • | Age profile of fleet provides hedge against over building |

| • | Best transportation franchise around |

Why is Kirby a Good

Investment?

Investment?