FOIA Confidential Treatment Request

Certain confidential information in this letter has been omitted and provided separately in an unredacted version to the Securities and Exchange Commission. Confidential treatment has been requested under 17 C.F.R. § 200.83 with respect to the omitted portions, which are identified in this letter by the mark “[*].”

June 9, 2023

VIA EDGAR

Securities and Exchange Commission

Division of Corporation Finance

Office of Manufacturing

100 F Street, N.E.

Washington, D.C. 20549

Attention: Beverly Singleton and Andrew Blume

Re: Kulicke and Soffa Industries, Inc.

Form 10-K for the fiscal year ended October 1, 2022

Filed November 17, 2022

Form 10-Q for the quarterly period ended December 31, 2022

Filed February 2, 2023

File No. 000-00121

Response dated April 12, 2023

File No. 000-00121

Dear Beverly Singleton and Andrew Blume:

We are writing in response to the comment letter of the Staff (the “Staff”) of the Securities and Exchange Commission (the “Commission”), dated April 25, 2023, to Lester Wong, Chief Financial Officer of Kulicke and Soffa Industries, Inc. (the “Company”), related to the above referenced filings made by the Company.

For your convenience, the Staff’s comments are reproduced below in italics, followed by the Company’s responses.

***

CONFIDENTIAL TREATMENT REQUESTED BY KULICKE AND SOFFA INDUSTRIES, INC.

Form 10-K for the Fiscal Year Ended October 1, 2022

Notes to Consolidated Financial Statements

Note 16: Segment Information, page 68

1. We note your response to comment 2 and have the following comments:

•Please expand on how the aggregation of your operating segments is consistent with the objective and basic principles of ASC 280-10-10-1. In doing so, explain in greater detail how the aggregated operating segments are so similar that presenting the information separately would not significantly benefit an investor's understanding of your performance and future prospects. As part of your response, specifically address the aggregation within your Aftermarket Product and Services ("APS") reportable segment of your non-machine business, including Blades, Wedge Bonder Consumables, and Capillaries, with your customer support organization, Spares and Services.

Response:

The Company has determined that it was appropriate to perform a fresh review of its segment reporting and analysis of ASC 280, Segment Reporting (“ASC 280”). The Company considered the Staff’s comments and re-evaluated the overall process of its segment reporting analysis. Based on all the information gathered in connection with this review, the Company has reassessed its view on the determination of operating segments in both its APS and Capital Equipment (“CE”) reportable segments as outlined below.

Aftermarket Product and Services (“APS”)

In the Company’s previous response, the Company highlighted that discrete financial information for the six different components within APS is available to the Company’s chief operating decision maker (the “CODM”) for his review during various financial and business updates throughout the financial year. However, the Company has since performed a more detailed review of its processes, and notes that there are multiple sets of financial data provided to the CODM as listed below:

a.Quarterly Business Unit Financial Review (“QFR”). The QFR is presented to the CODM and the rest of the senior management team during the Company’s quarterly business update meeting. The QFR presents a detailed analysis of actual results achieved by the Company such as revenue, gross margin, operating expense, operating profit, and operating margin compared to budgeted results for the following business units: Ball Bonder, Wedge Bonder, Electronic Assembly / Advanced Packaging Mass Reflow, Advanced Packaging, Lithography and APS. The Company’s financial planning and analysis director and team present the QFR in a detailed manner for each of the aforementioned business units, and discussions are carried out during the meeting regarding the performance of each business unit. The Company would like to highlight that in the QFR, APS is presented as a single business unit, showing the profit and loss statement of APS as a whole, not at the individual component level. In addition to the QFR, the Company holds a Quarterly Business Review (“QBR”) whereby the operations and strategy of the various business units mentioned above are discussed with the CODM and the senior management team, including details on new product roadmaps, operational risks, sales targets and key strategies affecting those business units. While the QBR provides more detailed information to the CODM than the QFR, the QFR presentation is the primary document that the CODM reviews on a quarterly basis in order to make decisions on the allocation of resources.

CONFIDENTIAL TREATMENT REQUESTED BY KULICKE AND SOFFA INDUSTRIES, INC.

b.Executive Summary Review. The executive summary is a monthly financial snapshot that is provided to the senior management via email. There are no meetings or discussions held on a monthly basis in relation to the Executive Summary Review; instead, discussions are held during the QFR on a quarterly basis. The summary contains: (1) a year-to-date revenue compared to budget (broken down by Ball Bonder, Wedge Bonder, Electronic Assembly / Advanced Packaging Mass Reflow, Advanced Packaging, Lithography and APS); and (2) business unit performance measures such as revenue, gross margin, operating expense, and direct operating margin, which are broken down by Ball Bonder, Wedge Bonder, Electronic Assembly / Advanced Packaging Mass Reflow, Advanced Packaging, Lithography and APS. Within this snapshot, APS is further broken down by Capillaries, Blades, Wedge Bonder Consumables, Ball Bonder & Wedge Bonder Spares and Services, and Electronic Assembly / Advanced Packaging Mass Reflow Spares and Services.

ASC 280-10-50-6 states that “for many public entities, the three characteristics of operating segments described in paragraph 280-10-50-1 clearly identify a single set of operating segments. However, a public entity may produce reports in which its business activities are presented in a variety of different ways. If the [CODM] uses more than one set of segment information, other factors may identify a single set of components as constituting a public entity's operating segments, including the nature of the business activities of each component, the existence of managers responsible for them, and information presented to the board of directors.”

Given the framework of the management approach under ASC 280, there may be more than one way to provide discrete information to the CODM. Although the QFR presentation is the primary document that the CODM reviews on a quarterly basis in order to make decisions on the allocation of resources, the Company has also assessed the four factors discussed below to further support its aforementioned position on identifying operating segments for APS.

1.The nature of the business activities of each component. In addition to the similarities noted in the Company’s response to the Staff on April 12, 2023 (the “Prior Response Letter”), where the Company highlighted that the various business units within APS have similar economic characteristics due to similar competitive and operating risks, similar customer profiles and similar types of distributors, the Company would like to further highlight to the Staff that the Company has a consistent go-to-market strategy for each of the business units within APS. The strategy is to [*]. For example, [*]. Such [*] strategy creates [*].

CONFIDENTIAL TREATMENT REQUESTED BY KULICKE AND SOFFA INDUSTRIES, INC.

2.Organizational structure (existence of segment manager and compensation structure). ASC 280-10-50-7 states that “Generally, an operating segment has a segment manager who is directly accountable to and maintains regular contact with the [CODM] to discuss operating activities, financial results, forecasts, or plans for the segment.” In addition, ASC 280-10-50-8 states that “A single manager may be the segment manager for more than one operating segment. If the characteristics in paragraphs ASC 280-10-50-1 and 280-10-50-3 apply to more than one set of components of a public entity but there is only one set for which segment managers are held responsible, that set of components constitute the operating segments.” In assessing the organizational structure of APS with regard to the ASC guidance referred to in the preceding sentences, the Company highlighted in the Prior Response Letter that in 2017, the six business units in APS were brought under the leadership of the Company’s Vice President for APS, Meng Kwong Han, in order to synergize and accelerate the Company’s momentum in aftersales product and services. The Company would like to further highlight that Mr. Han directly reports to the CODM in his capacity as the segment manager. On a regular basis, Mr. Han discusses the operating activities, financial results, and strategy of APS with the CODM which is done at the consolidated APS level. Similarly, other segment managers for CE present the QFR to the CODM on a quarterly basis with regard to their respective operating segments. [*]. This provides further insight into how the CODM allocates resources and assesses performance. This conclusion is consistent with the guidance in ASC 280-10-50-7, which notes that operating segments will generally have “a segment manager who is directly accountable to and maintains regular contact with the [CODM]”.

3.Information presented to the board of directors. The Company also further assessed the information provided to the board of directors. In this regard, paragraph 70 of the Background Information and Basis of Conclusions of FASB Statement 131 states that in many enterprises, “only one set of data is provided to the board of directors. That set of data generally is indicative of how management views the enterprise’s activities”. The Company would like to highlight that during the quarterly meeting of its board of directors, the Company’s Chief Financial Officer presents the business update to the board of directors. The business update includes actual revenue achieved for the fiscal quarter as well as forecasted revenue for the next fiscal quarter. Beginning in fiscal year 2020, management decided to align the business update to the board of directors with how management views the company’s segment structure. As such, since fiscal year 2020, the revenue information presented has been broken down by Ball Bonder, Wedge Bonder, Electronic Assembly / Advanced Packaging Mass Reflow, Advanced Packaging, and APS. The Company would like to highlight that revenue for APS is presented as a single business unit to the board of directors. There is no further breakdown of financial information for APS that is presented to the board of directors. In addition to the quarterly revenue by business unit, the Company’s Chief Financial Officer presents the Company’s total profit & loss statement in the presentation to the board of directors.

4.Budgeting process. The Company would further like to highlight that during the annual budget approval process, the APS segment manager, Mr. Han, presents the budget to the CODM, highlighting operating expenses, headcount, and revenue for APS as a whole. When seeking approval for the budget, Mr. Han seeks that approval for the entire APS segment and has discretion to manage the overall APS budget to meet performance objectives at the APS segment level.

Based on the four additional factors above, and consistent with the management approach described in ASC 280, the Company has reassessed and concluded that APS is one operating segment rather than six operating segments. This is also consistent with how the CODM assesses performance and makes decisions about resources to be allocated.

CONFIDENTIAL TREATMENT REQUESTED BY KULICKE AND SOFFA INDUSTRIES, INC.

Since APS is one operating segment, no aggregation is required. The Company has concluded that the APS operating segment is also the reportable segment which is consistent with the Company’s prior segment reporting.

Capital Equipment (“CE”)

In the Prior Response Letter, the Company highlighted that there are six operating segments in CE,: Ball Bonder, Wedge Bonder, Wafer Level Bonder, Electronic Assembly / Advanced Packaging Mass Reflow, Advanced Packaging and Lithography.

Upon further review of financial information provided in the Executive Summary, QFR presentation and board of directors presentation, the Company would like to highlight to the Staff that financial information for CE was consistently broken down and presented as five business units, namely: Ball Bonder, Wedge Bonder, Electronic Assembly / Advanced Packaging Mass Reflow, Advanced Packaging and Lithography. Financial information for Wafer Level Bonder is included as part of Ball Bonder, rather than as a standalone business unit. Given the consistent level of granularity within the various sets of financial information being presented to the CODM, it is evident that the CODM reviews and allocates resources based on these five business units. As such, the Company has reassessed and concluded that, in accordance with the framework of the management approach described in ASC 280, CE has five operating segments. These five operating segments are: Ball Bonder, Wedge Bonder, Electronic Assembly / Advanced Packaging Mass Reflow, Advanced Packaging and Lithography.

The Company has also further reassessed the quantitative aggregation criteria for the five operating segments in CE. Please refer to the Company’s detailed assessment in the response to the Staff’s second comment below.

CONFIDENTIAL TREATMENT REQUESTED BY KULICKE AND SOFFA INDUSTRIES, INC.

•You indicate that the operating segments in your Capital Equipment ("CE") and APS reportable segments have long-term 5-year average gross margins within a range of approximately +/- 5% and +/-10%, respectively. You further indicate that the APS operating segments "have similar trends in sales growth" for the 5-year period from 2017 to 2022. Please provide us with the 5-year average gross margins and 5-year sales growth figures for each operating segment, as well as gross margins and sales by year within such periods.

Response:

Capital Equipment

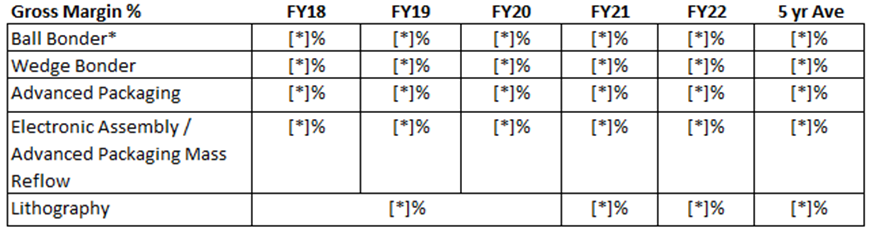

The following table shows the Company’s five-year average gross margins for the respective operating segments in CE from fiscal year 2018 to fiscal year 2022 and gross margins for the respective operating segments in CE by year within that five-year period.

* Gross Margin for Ball Bonder includes Wafer Level Bonder

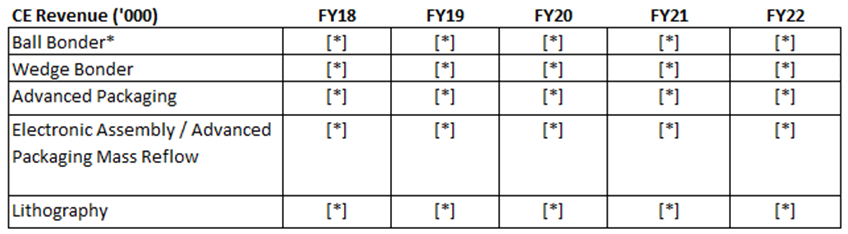

The following table shows the Company’s five-year sales growth for the respective operating segments in CE from fiscal year 2018 to fiscal year 2022 and sales by year for the respective operating segments in CE within that five-year period.

* Revenue for Ball Bonder includes Wafer Level Bonder

The following graph also shows the Company’s five-year sales growth for the respective operating segments in CE from fiscal year 2018 to fiscal year 2022:

[*]

CONFIDENTIAL TREATMENT REQUESTED BY KULICKE AND SOFFA INDUSTRIES, INC.

The Company views Ball Bonder and Wedge Bonder as the key drivers of the Company’s gross margin, given the significant amount of revenue that they contribute to the Company’s total revenue. These two operating segments represent the Company’s wire bonding business. These two operating segments are economically similar as defined in ASC 280, both from a quantitative perspective, as evidenced by the long-term average gross margin, long-term average operating margin (as further elaborated in the response below), and from a qualitative perspective, as highlighted by the Company in the Prior Response Letter. The Company is of the view that the five-year sales growth trend for Ball Bonder and Wedge Bonder supplements the Company’s quantitative assessment that they are economically similar; however, the Company has placed more emphasis on the gross margins and operating margins in performing the assessment.

Advanced Packaging, Electronic Assembly / Advanced Packaging Mass Reflow and Lithography together represent only a small percentage of the Company’s total revenue. For fiscal year 2022 and fiscal year 2021, these three operating segments, in the aggregate represented [*]% and [*]%, respectively, of the Company’s total revenue. The Company has reassessed its view on the economic similarity of these three operating segments and has concluded that these three operating segments do not meet the quantitative criteria for aggregation with the Ball Bonder and Wedge Bonder operating segments. The [*] gross margin for Advanced Packaging in fiscal year 2022 and fiscal year 2021 compared to the other operating segments in CE was due to [*]. Lithography is a relatively new business unit with [*] in fiscal year 2018 to fiscal year 2020, as the Company was focused on researching and developing a new lithography machine. The revenue recognized in fiscal year 2022 and fiscal year 2021 was for a prototype lithography machine, which contributed to [*] compared to the other operating segments in CE, as most of the cost was previously expensed as incurred in research and development. With respect to Electronic Assembly / Advanced Packaging Mass Reflow, although the gross margin and sales growth are similar to that of Ball Bonder and Wedge Bonder, when the Company considered additional financial measures such as operating margin, the Company noted that the operating margin is not economically similar with Ball Bonder and Wedge Bonder. The Company has further elaborated on this in its response to the Staff’s comment below.

In addition, the Company has performed the quantitative assessment for the three operating segments (Advanced Packaging, Electronic Assembly / Advanced Packaging Mass Reflow and Lithography) in accordance with ASC 280-10-50-12 and noted that none of these three operating segments meet the quantitative threshold (10% test) for fiscal year 2022 and the immediately preceding fiscal year, being fiscal year 2021 and, accordingly, the Company would not be required to report separately information about these three operating segments as reportable segments.

Since the Company has assessed that these three operating segments do not have similar economic characteristics, these three operating segments will not be aggregated to form a new reportable segment. However, the Company notes that when immaterial operating segments are not aggregated because they do not meet these criteria, the immaterial operating segments should be combined and disclosed in an “all other” category in accordance with ASC 280-10-50-15 (assuming that the 75% revenue test is met).

The Company performed the 75% revenue test in accordance with ASC 280-10-50-14 and concluded that total revenue reported by operating segments – Ball Bonder, Wedge Bonder and APS - constitute [*]% and [*]% of the Company’s total revenue for fiscal year 2022 and fiscal year 2021 respectively.

CONFIDENTIAL TREATMENT REQUESTED BY KULICKE AND SOFFA INDUSTRIES, INC.

In conclusion, Advanced Packaging, Electronic Assembly / Advanced Packaging Mass Reflow and Lithography are non-reportable operating segments that the Company will disclose in an “all other” category in the segment reporting footnote. Ball Bonder and Wedge Bonder meet the quantitative aggregation criteria according to ASC 280 as both operating segments have similar economic characteristics such as gross margin, sales growth trend and operating margin; please refer to the Company’s response below for a detailed analysis on operating margin. The Company will aggregate the Ball Bonder and Wedge Bonder operating segments and disclose as one reportable segment in the segment reporting footnote.

Aftermarket Product and Services

As discussed in the Company’s response to the Staff’s first comment above, the Company is of the view that the QFR information presented to the CODM, coupled with the four additional factors discussed above, demonstrates that APS is viewed by the CODM as a single operating segment. The Company has reassessed and concluded that APS is one operating segment according to the framework of the management approach under ASC 280, and this is how the CODM makes decisions regarding the allocation of resources. Since APS is one operating segment, no aggregation is required. The Company has concluded that the APS operating segment is also the reportable segment.

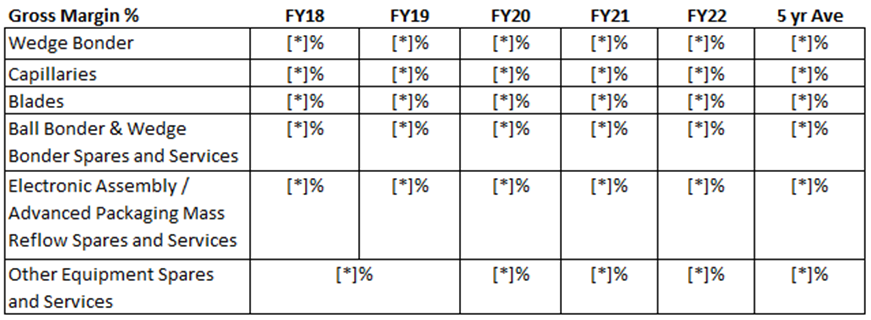

The Company did consider an alternative view for the purpose of its response to the Staff, where the performance measures relating to the six components in APS are presented at a more granular level. On the basis of such granularity, please refer to tables below showing the five-year average gross margins and five-year sales figures for the six components in APS for fiscal year 2018 to fiscal year 2022. Although the information for the six components in APS are available, the Company is of the view that the six components should not be viewed as six individual operating segments. As discussed in the Company’s first response above, this is inconsistent with the way the Company operates and manages the business and is not how the CODM reviews the financial information to assess performance and make decisions regarding the allocation of resources.

The table below shows the Company’s five-year average gross margins of the six components in APS from fiscal year 2018 to fiscal year 2022 and gross margins of the six components in APS by year within that five-year period.

CONFIDENTIAL TREATMENT REQUESTED BY KULICKE AND SOFFA INDUSTRIES, INC.

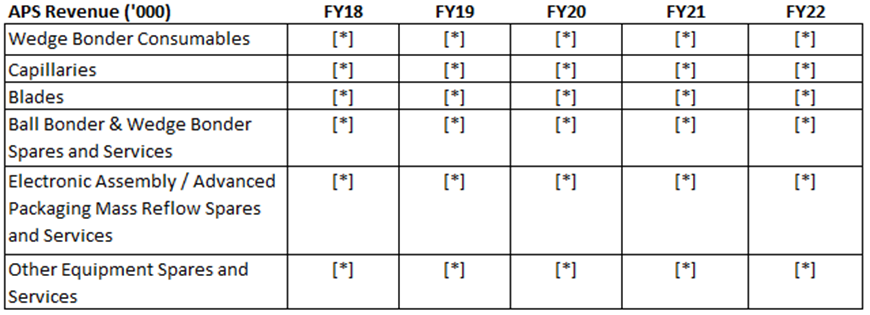

The table below shows the Company’s five-year sales growth of the six components in APS from fiscal year 2018 to fiscal year 2022 and sales by year within that five-year period.

The following graph also shows the Company’s five-year sales growth of the six components in APS from fiscal year 2018 to fiscal year 2022:

[*]

CONFIDENTIAL TREATMENT REQUESTED BY KULICKE AND SOFFA INDUSTRIES, INC.

•Tell us if you considered any other measures in assessing whether aggregated operating segments had similar economic characteristics and, if so, provide us with your analysis and the related supporting data. In doing so, tell us how you considered segmental income from operations, the measure of segment profitability used by your CODM, in assessing whether or not your operating segments had similar economic characteristics. Provide us with a 5-year historical quantification of each operating segment's income from operations.

Response:

Capital Equipment

The tables below show the Company’s operating income and operating margin of each operating segment in CE for each year between fiscal year 2018 and fiscal year 2022.

* Operating income for Ball Bonder includes Wafer Level Bonder

* Operating margin for Ball Bonder includes Wafer Level Bonder

CONFIDENTIAL TREATMENT REQUESTED BY KULICKE AND SOFFA INDUSTRIES, INC.

The Company focused on the long-term average operating margin for the five operating segments in CE as opposed to operating income, as the operating margins provide a more representative insight of the economic characteristics. The Company would like to highlight that the five-year average operating margin for Wedge Bonder is [*] than that of Ball Bonder by [*]%, mainly due to [*]. This had a [*] impact on the operating margin. Since the Company is looking at the long-term average operating margin, the Company re-calculated the long-term operating margin for Wedge Bonder based on the four-year average, ignoring the anomaly in fiscal year 2020. This provides a long-term average margin of [*]%. Consistent with the Company’s response above, Ball Bonder and Wedge Bonder share economic similarities from a quantitative perspective, where both operating segments have similar long-term gross margin, operating margin, and sales growth trend. As such, the Company has aggregated Ball Bonder and Wedge Bonder as one reportable segment.

Similar to the Company’s response above regarding gross margin, the long-term operating margins for Advanced Packaging, Electronic Assembly / Advanced Packaging Mass Reflow and Lithography are not similar. The Company concluded in the response above that these three are non-reportable operating segments that the Company will disclose in an “all other” category in the segment reporting footnote.

Aftermarket Product and Services

As highlighted above, APS is one operating segment. The Company has concluded that the APS operating segment is also the reportable segment. The Company did not consider the long-term operating margin for the various business units in APS, as no aggregation is required.

•To the extent not addressed above, provide us with quantitative information that helps us assess which operating segments materially contribute to your operating results.

Response:

The Company does not have any further information to provide in addition to the Company’s responses above. To conclude the Company’s response to the Staff, the Company has reassessed its operating segments from its previous response of twelve to a revised total of six, consisting of Ball Bonder, Wedge Bonder, Advanced Packaging, Electronic Assembly / Advanced Packaging Mass Reflow, Lithography and APS. The Company then determined it will have the following reportable segments: one reportable segment for Ball Bonder and Wedge Bonder, and another reportable segment for APS. The remaining operating segments (Advanced Packaging, Electronic Assembly/Advanced Packaging Mass Reflow and Lithography), which are immaterial, will be disclosed in an “all other” category in the segment reporting footnote. The Company will present the updated segment reporting footnote in its next Form 10-Q filing for the period ending July 1, 2023. Consistent with ASC 280-10-50-4, the Company will present the recast segment reporting disclosure for prior interim periods presented in its upcoming Form 10-Q for the fiscal quarter ending July 1, 2023, for comparative purposes.

***

If you have any questions relating to the foregoing, please do not hesitate to contact me.

Sincerely,

/s/ Lester Wong

Lester Wong

Chief Financial Officer

Kulicke and Soffa Industries, Inc.

CONFIDENTIAL TREATMENT REQUESTED BY KULICKE AND SOFFA INDUSTRIES, INC.