Exhibit 99.1

| Arthur Bedrosian, CEO Marty Galvan, CFO May 2014 |

| 2 Forward-Looking Statements Except for historical facts, the statements in this presentation, as well as oral statements or other written statements made or to be made by Lannett Company, Inc. (the “Company”), are forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995 and involve risks and uncertainties. For example, statements about the expected positive FDA inspection results of the Company’s manufacturing facilities and product approvals, anticipated growth and future operations, the current or expected market size for its products, the success of current or future product offerings, continued relationships with the Company’s suppliers and customers, the research and development efforts, the Company’s ability to file for and obtain U.S. Food and Drug Administration (FDA) approvals for future products, and the Company’s ability to obtain and maintain necessary licenses and permits, are forward-looking statements. Forward-looking statements are merely the Company’s current prediction of future events. The statements are inherently uncertain and actual results could differ materially from the statements made herein. There is no assurance that the Company will achieve the sales levels that will keep its operations profitable or that FDA filings and approvals will be completed and obtained as anticipated. For a description of additional risks and uncertainties, please refer to the Company’s filings with the Securities and Exchange Commission, including its latest Annual Report on Form 10–K and its latest Quarterly Report on Form 10-Q. The Company assumes no obligation to update its forward-looking statements to reflect new information and developments. |

| 3 U.S. Generic Pharmaceutical Industry Strong drivers for continued growth Cost: Often 80-85% less than the brand Supply: $86 billion of brand drugs are coming off patent through 2017* Demand: Aging baby boomers will continue to fuel market growth Account for over 83% of prescriptions* Same active ingredient, dosage form and route of administration as brand Similar safety, efficacy and quality as brand, at a lower price * IMS June 2013 |

| 4 U.S. Generic Pharmaceutical Industry (con’t) Product approval process: Abbreviated New Drug Application (ANDA) Generally no preclinical/clinical data required; only need to demonstrate bioequivalence Less development time, money and risk compared to New Drug applications (NDA) for brands Distribution Model Brand products require marketing budgets and investment in sales reps to call directly on physicians / hospitals -- new products need detailing Generics are sold through 3rd party channels including: Wholesaler Distributors (McKesson, Cardinal, AmerisourceBergen) Chain Drug Stores (Walgreens, CVS, RiteAid) Mail-order Pharmacies (Express Scripts/Medco, OPTUMRx, Caremark) |

| 5 At a Glance 31 Marketed Products 19 ANDAs Pending Record of Regulatory Compliance 1 facility in Cody, WY 5 facilities in Philadelphia, PA |

| 6 Management Team Arthur Bedrosian President & CEO 45 years in industry; 12 at Lannett Trinity Labs, Pharmeral, Liquipharm, Zenith Labs, PurePac Martin Galvan CFO 34 years in industry; 2 at Lannett Viasys Healthcare, Rhone-Poulenc Rorer, Revlon Health Care William Schreck COO 44 years in industry; 11 at Lannett Nature’s Products, Ivax Pharmaceuticals, Zenith-Goldline, Rugby-Darby Kevin Smith VP Sales & Marketing 25 years in industry; 12 at Lannett Bi-Coastal Pharma, Mova Labs, Sidmak Labs, Purdue Ernest Sabo VP Regulatory Affairs, Chief Compliance Officer 30 years in industry; 9 at Lannett Wyeth Pharma, Delavau/Accucorp Robert Ehlinger VP Logistics, Chief Information Officer 20 years in industry; 7 at Lannett MedQuist, Kennedy Health Systems |

| Our Strengths Talented management across all functional areas: product development, regulatory, manufacturing, compliance, sales, finance Strong customer relationships fostered over many years - business is personal Track record of: Selecting products with high profit potential and manageable competition Getting products approved and maintaining regulatory compliance Stability plus growth: Base generics business represents a solid financial foundation Controlled substances represent area for higher profit margins and growth rates One of seven DEA-licensed importers of concentrated poppy straw (CPS) 7 |

| FY 2013 Sales Mix by Product Category 8 |

| 9 Deep Pipeline 14 ANALYSIS FDA PENDING STABILITY/ PREFILING DEVELOPMENT NUMBER OF PRODUCTS 11 13 28 19 2012 Sales (brand and generic) of $1.25 billion* * IMS 2012 |

| Top 5 Products in Pipeline Drug Product Product Category 2012 Brand & Generic Sales* (Millions) 2012 Generic Sales* (Millions) #1 Oncology $414 N/A #2 Pain Management $365 $281 #3 Anorexia $135 $120 #4 Glaucoma $76 $61 #5 Dialysis $65 $29 Total $1,055 $491 10 * IMS 2012 |

| Controlled Substance Market and Goal US market: $15 billion* Generic portion: $3.4 billion* High barrier to entry: DEA-required licenses and quotas 1 of 7 companies with DEA import license for CPS CPS = natural raw material from which APIs are manufactured Profitability and growth: Current gross margin on controlled substances: 60% 5-year goal: 50% of manufactured products to be controlled substances 11 * IMS 2012 |

| 1 Plant 4 Alkaloids 8 APIs 44 Products 132 Strengths Brand Names Avinza Dilaudid Exalgo Hycodan Kadian Lortab Opana Oxycontin Percocet Suboxone Vicodin Out of OneMany 12 |

| Vertical Integration => Higher Margins Vertically Integrated Today: Hydromorphone tablets (patented API process) Cocaine HCI topical solution (patented API process) Near-term Integration Goal: Morphine Sulfate (various dosage forms) Hydrocodone (tablet and oral solutions) Fentanyl (various dosage forms) Oxycodone HCI (various dosage forms) 13 Philadelphia: Finished Dosage Form Cody, Wyoming : API |

| Growth Strategy Base generic products: Commercialize products upon FDA approval Acquire ANDAs and products that meet our expectations for sales potential, barriers to entry, limited competition and gross margin Expand product development partnerships to enhance internal efforts Monitor market for opportunities to increase prices File Paragraph IV challenges for products which meet target metric thresholds Controlled substance products: Become a dominant player and one-stop shop in the U.S. Grow percent of manufactured products to 50% by 2018 Continue to invest in development of higher margin products Develop novel (proprietary) forms of API delivery 14 |

| Brand product: C-Topical® Cocaine HCl Requirements for commercialization: Clinical testing for FDA approval Marketing and dedicated sales force to call on surgeons Product Advantages: Increased number of procedures per day due to faster therapeutic onset Ease of use - one product versus current therapy of combining two products Potential to provide: Higher profit margins New Chemical Entity (NCE) designation = Market Exclusivity 15 Growth Strategy (cont’d) |

| 16 C-Topical® Sales Territories |

| Financial Discussion 17 |

| Strategic Goal: Stability Plus Growth 18 25% CAGR -- All Organic! Revenue: $460 Million Revenue: $151 Million |

| Fiscal 2013 Achievements Net sales increased 23% for FY 2013 Increased market share on Levothyroxine: the #2 most prescribed molecule in U.S.* Cardiovascular drugs increased almost 43% from FY2012 Gout drugs increased ten-fold from FY2012 Gross margin up 6 percentage points due to price increases and manufacturing efficiencies Strengthened Board of Directors Received $1.25 million from litigation settlement 19 * IMS June 2013 |

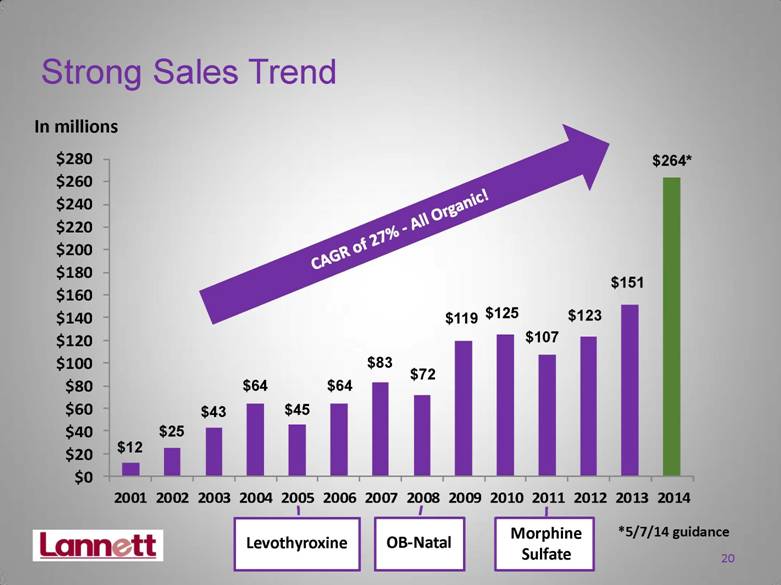

| Strong Sales Trend In millions $12 $25 $43 $64 $45 $64 $83 $72 $119 $125 $107 CAGR of 27% - All Organic! $123 $151 20 Levothyroxine OB-Natal Morphine Sulfate $264* *5/7/14 guidance $0 $20 $40 $60 $80 $100 $120 $140 $160 $180 $200 $220 $240 $260 $280 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 |

| Fiscal 2013 Full Year In millions Operating Income Net Sales Gross margin up 6 percentage points to 38% 21 Up 23% Up nearly 3x $123.0 $151.1 $60 $80 $100 $120 $140 $160 FY12 FY13 $6.9 $18.8 $0 $5 $10 $15 $20 FY12 FY13 |

| Operating Income Net Sales In millions Fiscal 2014 Third Quarter 22 Doubled Increase 7x Gross margin up 31 percentage points to 70% $4.7 $36.0 $0.0 $10.0 $20.0 $30.0 $40.0 Q3-FY13 Q3-FY14 $39.0 $80.0 $25 $45 $65 $85 Q3-FY13 Q3-FY14 |

| Operating Income Net Sales In millions Fiscal 2014 First Nine Months 23 Up 74% Increase 5x Gross margin up 23 percentage points to 61% *Excludes $20.1 M non-recurring charge for JSP contract renewal; GAAP operating income was $50.7 M $110.9 $193.2 $50 $100 $150 $200 9mos-FY13 9mos-FY14 $13.1 *$70.8 $0.0 $20.0 $40.0 $60.0 $80.0 9mos-FY13 9mos-FY14 |

| Strong Balance Sheet Cash & Investments Debt Stockholders’ Equity Total Assets Total Liabilities (In millions) As of March 31, 2014 $123.5 $307.3 $1.2 $38.3 $269.0 24 |

| Fiscal 2014 Guidance Net sales: $261 to $267 million Gross margin: *61.5% to 62.5% R&D: $30 to $31 million SG&A: $38 to $39 million FY effective tax rate: 36% to 38% Capital expenditures: $24 to $26 million Q1, non-recurring charge: $20 million JSP contract renewal As reported on May 7, 2014 *Excludes the impact of JSP contract renewal charge 25 |

| 26 Price Increase Guidance K.I.S.S. (Keep It Simple, Stupid!) |

| 27 Investment Highlights Generics: 83% of new Rxs in the US and growing* Sales Growth: LCI well-positioned for continued growth in multiple categories 23% top-line growth in FY 2013 and 75% guidance for FY 2014 5-year goal: 25% CAGR and FY 2018 sales of $460 million (all organic) Pipeline: 19 ANDAs pending at FDA Increased Profitability: favorable pricing and product mix and manufacturing efficiencies Gross margin up 6 percentage points in FY 2013; FY 2014 guidance of 61.5% to 62.5% Vertical Integration: just beginning to unleash value Barriers to entry and higher gross margins (~60%) to fuel sales and profits Strong Balance Sheet: cash to fund growth strategy: organically and through acquisitions * IMS June 2013 |

| Thank You It has been a pleasure. NYSE: LCI www.Lannett.com 28 |