Table of Contents

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE

SECURITIES EXCHANGE ACT OF 1934

For The Fiscal Year Ended September 26, 2021

OR

☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE

SECURITIES EXCHANGE ACT OF 1934

Commission File Number 1-6227

LEE ENTERPRISES, INCORPORATED

(Exact name of Registrant as specified in its Charter)

Delaware | 42-0823980 |

(State of incorporation) | (I.R.S. Employer Identification No.) |

4600 E 53rd Street, Davenport, Iowa 52807

(Address of principal executive offices)

(563) 383-2100

Registrant's telephone number, including area code

| |

Securities registered pursuant to Section 12(b) of the Act: |

| | | |

Title of Each Class | Trading Symbol(s) | Name of Each Exchange On Which Registered |

Common Stock - $0.01 par value | LEE | The Nasdaq Global Select Market |

| Preferred Share Purchase Rights | LEE | The Nasdaq Global Select Market |

Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ��

Indicate by check mark whether the Registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this Chapter) during the preceding 12 months (or such shorter period that the Registrant was required to submit). Yes ☒ No ☐

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer," "accelerated filer," "smaller reporting company,” and "emerging growth company" in Rule 12b-2 of the Exchange Act.

Large accelerated filer ☐ Accelerated filer ☐ Non-accelerated filer ☒ Smaller Reporting Company ☒ Emerging growth company ☐

If an emerging growth company, indicate by check mark if the Registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management's assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registrant's public accounting firm that prepared or issued its audit report. ☒

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No ☒

As of March 31, 2021, the aggregate market value of the Registrant's common stock held by non-affiliates of the registrant was $141,804,818 based on the closing sale price as reported on the New York Stock Exchange. As of November 30, 2021, 5,889,159 shares of Common Stock $0.01 par value were outstanding on Nasdaq Global Select Market.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Lee Enterprises, Incorporated Definitive Proxy Statement to be filed in January 2022 are incorporated by reference in Part III of this Form 10-K. Except as expressly incorporated by reference, the Registrant's Definitive Proxy Statement shall not be deemed to be a part of this report.

References to “we”, “our”, “us” and the like throughout this document refer to Lee Enterprises, Incorporated and subsidiaries (the "Company"). References to "2021", "2020", "2019" and the like refer to the fiscal years ended the last Sunday in September.

PART I

ITEM 1. BUSINESS

Lee Enterprises, Incorporated was founded in 1890, incorporated in 1950 and serves 77 mid-sized local communities (including TNI Partners ("TNI") and Madison Newspapers, Inc. ("MNI") in 26 states) as the leading provider of valuable, intensely local, original news and information through our traditional print and digital subscriptions, and innovative, digitally focused marketing solutions to local advertisers. On March 16, 2020, we completed the acquisition of BH Media Group, Inc. ("BH Media") and The Buffalo News, Inc. ("Buffalo News"), adding 31 local media operations and nearly doubling our audience size and total operating revenue.

Our asset portfolio includes digital subscription platforms, daily, weekly and monthly newspapers and niche publications, all delivering original local news and information. Our products offer print and digital editions, and our content and advertising is available in real time through our websites and mobile apps. We operate in predominately mid-sized communities with products ranging from large daily newspapers and associated digital products, such as the St. Louis Post-Dispatch and The Buffalo News, to non-daily newspapers with news websites and digital platforms serving smaller communities.

As the leading provider of local news and information in our local markets and an innovative marketing solutions company, we aim to grow our business through three main categories: subscriptions to our product offerings, advertising and marketing solutions to local advertisers, and digital services to a diverse set of customers. The execution of this strategy is expected to enable the Company to continue its transformation from a more traditional print media business to a digitally focused subscription platform and digital marketing solutions company.

| | • | Our digital subscription platforms are some of the fastest growing digital subscription platforms in local media. At the end of 2021, we had more than 400,000 subscribers to our digital platforms, up 65% over 2020. |

| | • | Our digital marketing services agency, Amplified Agency ("Amplified") offers a full suite of digital marketing solutions to local advertisers both in and outside of the markets in which we operate a subscription platform. Revenue at Amplified totaled almost $42 million in 2021, up 43% over 2020. |

| | • | Our software as a service (SaaS) content platform, TownNews, is one of the largest web-hosting and content management SaaS providers in North America. TownNews represents a powerful opportunity to drive additional digital revenue by providing state-of-the-art web hosting and content management services to more than 2,000 customers who rely on TownNews for their web, over-the-top display ("OTT"), mobile, video and social media products. Revenue at TownNews, including intercompany revenue, totaled more than $27 million in 2021, and has achieved a compound annual growth rate of 10.5% over the last ten years. |

We generate revenue primarily through advertising and marketing services, subscriptions to our digital and print products, and digital services, primarily through our majority owned subsidiary, TownNews. Our operations also provide printing and distribution of third party publications.

Advertising and Marketing Services - In 2021, advertising and marketing services of $369.3 million comprised 46% of total operating revenue, down from 47% in the prior year.

| | • | Local advertising revenue is earned from top local accounts and small to medium businesses (SMBs) in but not limited to our markets. Advertising takes the form of display advertising in daily and non-daily publications, preprinted advertising inserted in the publication, display advertising delivered on our owned and operated websites, and a full suite of digital marketing services through Amplified, including targeted display, video, OTT, custom content, web development, social media management, search, email marketing and other tactics. |

| | • | National advertising is revenue earned from the sale of print or digital display advertising space, or from preprint advertising inserted in the publication, from national accounts that do not have a local retailer representing the account in the market. |

Our primary strategy is a data-driven, multi-channel sales approach that enables our sales force to put the right marketing solution that maximizes audience reach for our advertisers by tailoring advertising and marketing solutions based on the size, scale, and needs of the advertiser. Through Amplified we create sophisticated digital campaigns on our owned and operated sites and on third-party sites that give advertisers the ability to target their message. We collaborate with Google and other ad tech companies to provide key metrics and analytics to measure campaign effectiveness.

Our advertising revenues are subject to seasonality due primarily to fluctuations in advertising spend. Advertising revenue is typically highest in our first quarter due to holiday and seasonal advertising and lowest in the second quarter following the holiday season. The volume of advertising sales in any period is also impacted by other external factors such as competitors' pricing, advertisers' decisions to increase or decrease their advertising expenditures in response to anticipated consumer demand, and general economic conditions.

Subscription Revenue - In 2021, subscription revenue of $357.7 million comprised 45% of our total operating revenue, up from 43% in the prior year. Subscription revenue is earned primarily from our full access subscription model, whereby subscribers receive complete access to our content on all platforms, both print and digital, and from subscriptions to our digital-only products. We also generate revenue from the sale of single copy editions.

| | • | Our printed newspapers reach almost 1 million households daily and more than 1.2 million on Sunday, and more than 265,000 users access our digital e-edition. |

| | • | Our web and mobile sites are the number one digital source of local news in most of our markets, reaching more than 50 million unique visitors, at the end of September 2021, with almost 1 million "known-users". |

| | • | As of September 26, 2021, we have 402,000 digital-only subscribers, a 65% increase over 2020. Growing our digital only subscribers remains a key strategic priority as we make the digital transformation. |

Digital Services Revenue – In 2021, digital services revenue of $19 million comprised 2.4% of our total operating revenue, compared to 3% in the prior year. Almost all of our digital services revenue is from TownNews. TownNews, operated through our 82.5% owned subsidiary INN Partners, L.C. and is one of the largest web-hosting and content management SaaS providers in North America and offers state of the art integrated digital publishing and content management solutions for creating, distributing, and monetizing multimedia content.

| | • | TownNews is the engine that powers our digital products. In addition, TownNews services nearly 2,000 daily customers, including legacy media publications, universities, television stations and niche publications. |

| | • | Including intercompany revenue generated from our markets, revenue at TownNews grew almost 9% in 2021 and totaled $27 million. |

| | • | With strong product offerings, investments in video and streaming technology and diversifying the customer base into broadcast, TownNews is positioned to continue to be a key component to our growth strategy. |

Other Revenue - In 2021, Other Revenue of $67.7 million comprised 8.5% of total operating revenue, down from 9.7% the prior year. Excluding digital services revenue, other revenue is comprised mainly of commercial printing and delivery of third party products and until March 16, 2020 revenue from our Management Agreement with BH Media. In 2021, other revenue excluding digital services of $19 million, comprised 6.1% of our total operating revenue, down from 6.8% in the prior year.

We compete with other media and digital companies for advertising and marketing spend as well as other news and information outlets for subscription spend. The market for local digital marketing solutions is highly competitive and evolving allowing opportunities for new competitors to enter the market. Amplified competes with other digital marketing solutions agencies as well as other media companies who have a similar strategy for digital marketing solutions. While some of our competitors enjoy competitive advantages such as greater name recognition, longer histories as well as greater financial resources, we believe we compete favorably and our product capabilities meet customer requirements due to our data-driven, multichannel sales approach, our experienced digital sales force and our overall customer satisfaction.

While very few of our local media operations have similar daily print competitors that are published in the same city, our local media operations compete with other media including magazines, radio, television, outdoor/billboard advertising, other classified and specialty publications, other print publications both free and paid, direct mail, directories, and national, regional and local advertising websites and content providers.

The number of competitors in any given market varies, however all of the forms of competition noted above exist to some degree in all of our markets.

STRATEGIC INITIATIVES

We are a major subscription platform providing trusted, local information, news, and an innovative, digitally focused marketing solutions company. Our focus is the local market - including local news and information, marketing solutions for local advertisers, and digital services for local content curators. To align with the core strength of our company, our digital transformation strategy is locally focused and revolves around three pillars:

To align with customer expectations, we will transform the way we present local news, information, and viewpoints, both in digital and print. We seek to maintain our position as the leading provider of news and information by providing best-in-class digital experiences to improve consumer engagement and grow our audiences. We aim to achieve this by delivering relevant, useful, and engaging content to the consumer using a multi-media approach with a heavy emphasis on video and audio.

In 2022, we look to create new content and video channels by growing our multimedia capabilities leveraging the high quality, trusted, engaging content we produce locally to tap into these growing market segments. Through strategic investments in talent and technology, we aim to continuously improve the user experience with our digital products and to expand our digital product offerings where we have niche expertise.

We believe that our proprietary local content displayed in best-in-class multimedia platforms combined with new and engaging content and video channels will grow our audiences and increase our audience monetization capabilities.

We will accelerate subscription growth, transforming our print-centric audience model to a robust digital subscription model. We are one of the fastest growing digital subscription platforms in local media. In 2021, our total paid audiences (including print and digital) increased for the first time in several years. Digital only subscriber growth accelerated in 2021, offsetting the declines in our traditional full access (print and digital) subscribers. In 2021, we reached 50 million unique visitors across all of our digital platforms, with 393 million page views in September. Our digital audiences are comprised of full access subscribers, digital-only subscribers and non-subscribers who access our sites subject to our paywalls. More than 60% of our full access subscribers have activated their digital access and digital-only subscribers increased 65% in 2021, reaching 402,000 digital-only subscribers.

Our acquisition and retention tactics are focused on growing our digital subscription base by using data and analytics to direct our huge addressable market of 50 million unique visitors toward obtaining a digital subscription. In 2022, we expect to implement an ongoing, comprehensive marketing campaign focused on aggressively promoting dynamic video and graphic content that drives consumption, engagement and ultimately feeds consumers down our digital subscription funnel.

Using these techniques, we expect digital-only subscribers to continue to grow substantially, reaching more than 900,000 digital-only subscribers by 2026.

We believe our digital transformation will have a favorable impact on the environment. A key component to our digital growth strategy is to accelerate the pace of digital subscriber growth. Growing our digital business as the legacy business wanes will have a favorable impact on the environment as our production hubs will consume less energy, we will consume less newsprint and there will be less environmental impact from our distribution channels that largely operate on fossil-fuel powered transportation.

We will diversify and transform the services and products we offer advertisers and dramatically expand our local advertiser base. According to eMarketer, local advertising spending is expected to reach nearly $115 billion in 2022. Our vast array of rapidly growing digital products, our large, digitally adept salesforce and Amplified, our high powered full service digital agency, creates a powerful opportunity to gain scale both in and outside of our local markets.

| | • | Our local sales forces are larger than any local competitor, and we believe they are the most highly trained and proficient sales force in our markets. |

| | • | We have strong relationships with businesses in our markets and offer a wide array of products to deliver our advertisers' message. |

| | • | Our sales executives pitch the power of our audiences directly to local decision makers. |

We have a world-class sales force, managed and supported centrally to ensure the highest digital talent is recruited, developed and retained to meet our clients' needs. Amplified is the backbone of our sales force and supports our local operators by providing lead generation, developing highly sophisticated proposals and provides all of the essential digital marketing services including web development, social media management, email marketing, fulfillment and search that most sophisticated advertisers are looking for. Amplified also provides our advertisers with the best data and metrics in order for them to maximize their advertising ROI. Amplified is a powerful organization that will help us improve our advertising revenue trends in 2022 and beyond.

TownNews represents a powerful opportunity for us to drive additional digital revenue through their SaaS content platform. In 2021, revenue at TownNews, including intercompany revenue, totaled more than $27,197,000 and since 2011 the compounded annual growth rate of TownNews revenue has been 10.5%. Through continuous investment in product development and gaining essential technology, like world-class video and streaming technology, TownNews is the leading CMS provider in the publishing CMS segment and is growing its market share in the broadcast CMS segment. In 2022, we believe we can grow revenue at TownNews through modest market share gains in our core markets, increasing our average revenue per customer.

DAILY NEWSPAPERS AND MARKETS

The Company, TNI and MNI, defined in Note 4, publish the following daily newspapers and maintain the following primary digital sites:

| | | | | Average Units (1) | | | 2021 Monthly Average ('000s) (5)(6) | |

Newspaper | Primary Website | Location | | Daily (2) | | | Sunday (2) | | | Unique Visitors | | | Page Views | |

| | | | | | | | | | | | | | | | | | | |

| St. Louis Post-Dispatch | stltoday.com | St. Louis, MO | | | 97,634 | | | | 127,802 | | | | 5,256 | | | | 51,311 | |

Buffalo News | buffalonews.com | Buffalo, NY | | | 68,989 | | | | 102,969 | | | | 2,683 | | | | 12,374 | |

Arizona Daily Star (4) | azstarnet.com | Tucson, AZ | | | 48,391 | | | | 80,657 | | | | 1,903 | | | | 16,663 | |

Omaha World Herald | omaha.com | Omaha, NE | | | 69,945 | | | | 78,528 | | | | 3,660 | | | | 26,779 | |

Richmond Times-Dispatch | richmond.com | Richmond, VA | | | 60,552 | | | | 68,124 | | | | 2,691 | | | | 16,869 | |

Wisconsin State Journal (3) | madison.com | Madison, WI | | | 58,406 | | | | 66,308 | | | | 3,155 | | | | 22,121 | |

The Times | nwitimes.com | Munster, Valparaiso, and Crown Point, IN | | | 35,364 | | | | 44,392 | | | | 1,905 | | | | 25,277 | |

Lincoln Journal Star | journalstar.com | Lincoln, NE | | | 38,653 | | | | 43,319 | | | | 2,128 | | | | 19,558 | |

Tulsa World | tulsaworld.com | Tulsa, OK | | | 35,608 | | | | 41,118 | | | | 2,581 | | | | 14,499 | |

Roanoke Times | roanoke.com | Roanoke, VA | | | 27,850 | | | | 29,253 | | | | 1,574 | | | | 8,267 | |

Winston Salem Journal | journalnow.com | Winston-Salem, NC | | | 25,471 | | | | 28,186 | | | | 1,335 | | | | 7,524 | |

The Press of Atlantic City | pressofatlanticcity.com | Atlantic City, NJ | | | 22,039 | | | | 25,759 | | | | 1,533 | | | | 9,234 | |

Greensboro News-Record | greensboro.com | Greensboro, NC | | | 21,510 | | | | 25,207 | | | | 1,241 | | | | 5,809 | |

The Post-Star | poststar.com | Glens Falls, NY | | | 23,580 | | | | 24,248 | | | | 626 | | | | 6,755 | |

Billings Gazette (5) | billingsgazette.com | Billings, MT | | | 17,323 | | | | 23,054 | | | | 1,245 | | | | 12,578 | |

Quad-City Times | qctimes.com | Davenport, IA | | | 18,370 | | | | 22,637 | | | | 842 | | | | 7,251 | |

The Pantagraph | pantagraph.com | Bloomington, IL | | | 20,376 | | | | 21,866 | | | | 555 | | | | 9,475 | |

The Courier | wcfcourier.com | Waterloo and Cedar Falls, IA | | | 11,946 | | | | 20,574 | | | | 556 | | | | 5,095 | |

The Free-Lance-Star | fredericksburg.com | Fredericksburg, VA | | | 17,942 | | | | 20,195 | | | | 979 | | | | 5,851 | |

The Bismarck Tribune | bismarcktribune.com | Bismarck, ND | | | 17,298 | | | | 18,122 | | | | 549 | | | | 6,412 | |

Casper Star-Tribune | trib.com | Casper, WY | | | 14,272 | | | | 17,660 | | | | 644 | | | | 3,972 | |

Missoulian (5) | missoulian.com | Missoula, MT | | | 12,151 | | | | 17,536 | | | | 648 | | | | 6,183 | |

Statesville Record & Landmark | statesville.com | Statesville, NC | | | 14,757 | | | | 15,713 | | | | 294 | | | | 1,611 | |

La Crosse Tribune | lacrossetribune.com | La Crosse, WI | | | 13,423 | | | | 15,352 | | | | 564 | | | | 6,244 | |

Dispatch-Argus | qconline.com | Moline, IL | | | 50,261 | | | | 15,214 | | | | 359 | | | | 4,167 | |

Sioux City Journal (5) | siouxcityjournal.com | Sioux City, IA | | | 11,798 | | | | 14,531 | | | | 607 | | | | 4,293 | |

Waco Tribune-Herald | wacotrib.com | Waco, TX | | | 12,947 | | | | 14,388 | | | | 838 | | | | 4,589 | |

Charlottesville Daily Progress | dailyprogress.com | Charlottesville, VA | | | 11,381 | | | | 12,274 | | | | 636 | | | | 3,374 | |

Lynchburg News & Advance | newsadvance.com | Lynchburg, VA | | | 11,077 | | | | 12,657 | | | | 721 | | | | 3,927 | |

Bristol Herald Courier | heraldcourier.com | Bristol,VA | | | 10,722 | | | | 11,668 | | | | 622 | | | | 2,848 | |

Independent Record (5) | helenair.com | Helena, MT | | | 7,946 | | | | 11,380 | | | | 489 | | | | 4,986 | |

Dothan Eagle | dothaneagle.com | Dothan, AL | | | 10,841 | | | | 11,351 | | | | 480 | | | | 2,082 | |

Kenosha News | kenoshanews.com | Kenosha, WI | | | 9,658 | | | | 11,117 | | | | 719 | | | | 5,738 | |

The Journal Times | journaltimes.com | Racine, WI | | | 9,993 | | | | 11,116 | | | | 611 | | | | 6,611 | |

Grand Island Independent | theindependent.com | Grand Island, NE | | | 10,823 | | | | 10,979 | | | | 507 | | | | 3,176 | |

The Daily News (5) | tdn.com | Longview, WA | | | 7,443 | | | | 10,377 | | | | 295 | | | | 2,307 | |

Napa Valley Register | napavalleyregister.com | Napa, CA | | | 10,120 | | | | 10,212 | | | | 551 | | | | 4,150 | |

The Times-News | magicvalley.com | Twin Falls, ID | | | 10,698 | | | | 9,725 | | | | 408 | | | | 3,545 | |

| | | | | Average Units (1) | | | 2021 Monthly Average ('000s) (5)(6) | |

Newspaper | Primary Website | Location | | Daily (2) | | | Sunday (2) | | | Unique Visitors | | | Page Views | |

Florence Morning News | scnow.com | Florence, SC | | | 7,960 | | | | 9,181 | | | | 429 | | | | 2,239 | |

The Citizen (5) | auburnpub.com | Auburn, NY | | | 5,390 | | | | 8,949 | | | | 386 | | | | 3,527 | |

Hickory Daily Record | hickoryrecord.com | Hickory, NC | | | 7,585 | | | | 8,689 | | | | 1,022 | | | | 5,868 | |

Montana Standard (5) | mtstandard.com | Butte, MT | | | 6,540 | | | | 8,623 | | | | 331 | | | | 3,686 | |

Globe Gazette | globegazette.com | Mason City, IA | | | 5,808 | | | | 8,531 | | | | 328 | | | | 3,143 | |

Corvallis Gazette-Times | gazettetimes.com | Corvallis, OR | | | 5,844 | | | | 8,172 | | | | 106 | | | | 192 | |

Bryan-College Station Eagle | theeagle.com | Bryan, TX | | | 8,094 | | | | 8,153 | | | | 532 | | | | 2,826 | |

Arizona Daily Sun (5) | azdailysun.com | Flagstaff, AZ | | | 5,259 | | | | 7,467 | | | | 305 | | | | 1,812 | |

Albany Democrat-Herald | democratherald.com | Albany, OR | | | 5,687 | | | | 6,962 | | | | 462 | | | | 4,054 | |

Martinsville Bulletin | martinsvillebulletin.com | Martinsville, VA | | | 6,144 | | | | 6,747 | | | | 315 | | | | 1,655 | |

Danville Register & Bee | godanriver.com | Danville, VA | | | 5,212 | | | | 6,377 | | | | 310 | | | | 1,649 | |

Opelika Auburn News | oanow.com | Opelika, AL | | | 6,639 | | | | 6,629 | | | | 460 | | | | 2,389 | |

The Times and Democrat (5) | thetandd.com | Orangeburg, SC | | | 5,012 | | | | 6,627 | | | | 347 | | | | 2,671 | |

Scottsbluff Star-Herald | starherald.com | Scottsbluff, NE | | | 6,109 | | | | 6,092 | | | | 318 | | | | 1,544 | |

Kearney Hub | kearneyhub.com | Kearney, NE | | | 5,938 | | | | 6,013 | | | | 460 | | | | 2,318 | |

The Daily Nonpareil | nonpareilonline.com | Council Bluffs, IA | | | 5,121 | | | | 5,133 | | | | 335 | | | | 1,540 | |

The News Herald | morganton.com | Morganton, NC | | | 4,306 | | | | 4,561 | | | | 368 | | | | 1,962 | |

North Platte Telegraph | nptelegraph.com | North Platte, NE | | | 4,509 | | | | 4,527 | | | | 225 | | | | 1,081 | |

Winona Daily News | winonadailynews.com | Winona, MN | | | 2,925 | | | | 3,063 | | | | 129 | | | | 1,192 | |

Culpeper Star-Exponent | starexponent.com | Culpeper, VA | | | 2,620 | | | | 2,790 | | | | 215 | | | | 856 | |

The News Virginian | newsvirginian.com | Waynesboro, VA | | | 2,432 | | | | 2,579 | | | | 111 | | | | 540 | |

The McDowell News | mcdowellnews.com | Marion, NC | | | 2,288 | | | | 2,456 | | | | 144 | | | | 602 | |

Ravalli Republic (5) | ravallinews.com | Hamilton, MT | | | 2,136 | | | | 2,000 | | | | 90 | | | | 434 | |

Herald & Review | herald-review.com | Decatur, IL | | | 16,427 | | | | | | | | 819 | | | | 5,543 | |

Rapid City Journal (5) | rapidcityjournal.com | Rapid City, SD | | | 10,888 | | | | | | | | 1,047 | | | | 6,611 | |

The Southern Illinoisan | thesouthern.com | Carbondale, IL | | | 9,515 | | | | | | | | 360 | | | | 2,118 | |

The Sentinel (5) | cumberlink.com | Carlisle, PA | | | 5,654 | | | | | | | | 291 | | | | 2,213 | |

Journal Gazette & Times-Courier | jg-tc.com | Mattoon/Charleston, IL | | | 4,190 | | | | | | | | 178 | | | | 1,874 | |

Daily Citizen | wiscnews.com/bdc | Beaver Dam, WI | | | 3,293 | | | | | | | | | | | | | |

Columbus Telegram (5) | columbustelegram.com | Columbus, NE | | | 3,274 | | | | | | | | 122 | | | | 1,266 | |

Baraboo News Republic | wiscnews.com/bnr | Baraboo, WI | | | 2,891 | | | | | | | | | | | | | |

Elko Daily Free Press (5) | elkodaily.com | Elko, NV | | | 2,849 | | | | | | | | 180 | | | | 1,629 | |

Daily Journal (5) | dailyjournalonline.com | Park Hills, MO | | | 2,810 | | | | | | | | 250 | | | | 1,875 | |

Fremont Tribune (5) | fremonttribune.com | Fremont, NE | | | 2,533 | | | | | | | | 131 | | | | 1,266 | |

Beatrice Daily Sun (5) | beatricedailysun.com | Beatrice, NE | | | 2,112 | | | | | | | | 76 | | | | 687 | |

Muscatine Journal | muscatinejournal.com | Muscatine, IA | | | 1,996 | | | | | | | | 92 | | | | 695 | |

Portage Daily Register | wiscnews.com/pdr | Portage, WI | | | 1,870 | | | | | | | | | | | | | |

York News-Times (5) | yorknewstimes.com | York, NE | | | 1,801 | | | | | | | | 134 | | | | 732 | |

The Chippewa Herald (5) | chippewa.com | Chippewa Falls, WI | | | 1,414 | | | | | | | | 154 | | | | 992 | |

| | (1) | Source: AAM: March 2021 Quarterly Executive Summary Data Report, unless otherwise noted. More recent data is not available. |

| | (2) | Not all newspapers are published Monday through Saturday or have a Sunday edition |

| | (3) | Owned by MNI |

| | (4) | Owned by Star Publishing and published through TNI |

| | (5) | Source: Company statistics. |

| | (6) | Excludes Agri-Media sites |

NEWSPRINT

The raw material of newspapers, and our other print publications, is newsprint. We purchase newsprint from U.S. and Canadian producers. We believe we will continue to receive a supply of newsprint adequate for our needs and consider our relationships with newsprint producers to be good. Newsprint purchase prices can be volatile and fluctuate based upon factors that include foreign currency exchange rates, tariffs and both foreign and domestic production capacity and consumption. Price fluctuations can affect our results of operations. We have not entered into derivative contracts for newsprint. For the quantitative impacts of these fluctuations, see Item 7A, “Quantitative and Qualitative Disclosures about Market Risk”, included herein.

EMPLOYEES AND HUMAN CAPITAL RESOURCES

We believe the foundation of our business is the people and employees who carry out the various tactics that support our business strategy. A major focus in 2021 was our integration of BH Media Group and the Buffalo News into common platforms and operating structures that manage all aspects of the employee experience including communication, performance management and benefits. This integration allows us to provide a unified approach to our digital transformation efforts.

At September 26, 2021, we had approximately 5,130 employees, including approximately 915 part-time employees, exclusive of TNI and MNI. Full-time equivalent employees in 2021 totaled approximately 4,793 of which 805 are represented by unions. We consider our relationships with our employees to be good. We are committed to an equitable and inclusive workplace that also reflects the diversity of our local readers and communities in which we serve. This past year, we hired a Director of News and Talent Development who is charged with improving diversity in our newsrooms and hiring practices that promote a more complete and inclusive news coverage of the communities in which we serve.

We continue to demonstrate our commitment to diversity, equity, and inclusion by assessing our hiring practices, extending our hiring reach, providing skill-building opportunities on diverse storytelling, and developing business strategies that include historically marginalized communities. These efforts and initiatives will help us reach our goal of a more diverse workforce at all levels of our company.

CORPORATE GOVERNANCE AND PUBLIC INFORMATION

We have a long history of sound corporate governance practices. Currently, our Board of Directors has affirmatively determined that six of its eight members are independent, including all members of the Board's Audit, Executive Compensation and Nominating and Corporate Governance committees. The Audit Committee approves all services to be provided by our independent registered public accounting firm and its affiliates.

At www.lee.net, one may access a wide variety of information, including news releases, SEC filings, financial statistics, annual reports, investor presentations, governance documents, newspaper profiles and digital links. We make available via our website all filings made by the Company under the Securities Exchange Act of 1934 ("Exchange Act"), including Forms 10-K, 10-Q and 8-K, and related amendments, as soon as reasonably practicable after they are filed with, or furnished to, the SEC. All such filings are available free of charge. The content of any website referred to in this Annual Report on Form 10-K ("Annual Report") is not incorporated by reference unless expressly noted.

FORWARD-LOOKING STATEMENTS

The Private Securities Litigation Reform Act of 1995 provides a “safe harbor” for forward-looking statements. This Annual Report contains information that may be deemed forward-looking that is based largely on our current expectations, and is subject to certain risks, trends and uncertainties that could cause actual results to differ materially from those anticipated. Among such risks, trends and other uncertainties, which in some instances are beyond our control, are:

| | • | Revenues may continue to diminish or declines in revenue could accelerate as a result of the COVID-19 pandemic; |

| | • | Revenues may continue to be diminished longer than anticipated as a result of the COVID-19 pandemic; |

| | • | The COVID-19 pandemic may result in material long-term changes to the publishing industry which may result in permanent revenue reductions for the Company and other risks and uncertainties; |

| | • | We may experience increased costs, inefficiencies and other disruptions as a result of the COVID-19 pandemic; |

| | • | We may be required to indemnify the previous owners of the BH Media Newspaper Business or Buffalo News for unknown legal and other matters that may arise; |

| | • | Our ability to manage declining print revenue; |

| | • | The warrants issued in our 2014 refinancing will not be exercised; |

| | • | The impact and duration of adverse conditions in certain aspects of the economy affecting our business; |

| | • | Change in advertising and subscription demand; |

| | • | Changes in technology that impact our ability to deliver digital advertising; |

| | • | Potential changes in newsprint, other commodities and energy costs; |

| | • | Labor costs; |

| | • | Significant cyber security breaches or failure of our information technology systems; |

| | • | Our ability to achieve planned expense reductions and realize the expected benefit of our acquisitions; |

| | • | Our ability to maintain employee and customer relationships; |

| | • | Our ability to manage increased capital costs; |

| | • | Our ability to maintain our listing status on NASDAQ; |

| | • | Other risks detailed from time to time in our publicly filed documents, including this Annual Report and particularly in "Risk Factors", Part I, Item 1A herein. |

Any statements that are not statements of historical fact (including statements containing the words “may”, “will”, “would”, “could”, “believes”, “expects”, “anticipates”, “intends”, “plans”, “projects”, “considers” and similar expressions) generally should be considered forward-looking statements. Readers are cautioned not to place undue reliance on such forward-looking statements, which are made as of the date of this Annual Report. We do not undertake to publicly update or revise our forward-looking statements, except as required by law.

ITEM 1A. RISK FACTORS

The risks described below could materially and adversely affect our business, financial condition and results of operations. We could also be affected by additional risks that apply to all companies operating in the U.S., as well as other risks that are not presently known to us or that we currently consider to be immaterial. These Risk Factors should be carefully reviewed in conjunction with Management's Discussion and Analysis of Financial Condition and Results of Operations in Item 7 and our Financial Statements and Supplementary Data in Item 8 of this Report. For ease of review, the risk factors generally have been grouped into categories, but many of the risks described in a given category relate to multiple categories.

Risks Related to General Economic Factors

The Company has incurred a material drop in advertising revenues as COVID-19 continues.

The COVID-19 pandemic and subsequent government restrictions caused and continue to cause significant declines in demand for certain products and services of ours, which ultimately affects advertising revenue. As such, certain aspects of our operating results have experienced lower revenue and profitability over 2021 and 2020 and these trends are expected to continue in the future.

Our advertising revenues may decline due to weakness in the brick and mortar retail sector.

A significant portion of our revenue is derived from advertising. The demand for advertising is sensitive to the overall level of economic strength, both in the markets in which we operate and nationally. Also, the decline in the financial or economic conditions of our advertisers could alter discretionary spending by advertisers. Certain segments of the economy have been challenged in recent years, particularly in the brick and mortar retail sector, and total advertising revenues have declined as a result. Advertising revenues may worsen if advertisers reduce their budgets, shift their spending priorities, are forced to consolidate, or cease operations.

Our ability to generate revenue is highly sensitive to the strength of the economies in which we operate and the demographics of the local communities that we serve.

Our advertising and marketing services revenues and subscription revenues depend upon a number of factors, including the size and demographic characteristics of the local population; the general local economic conditions; and the economic condition of the retail segments in the communities that our publications serve. In the case of an economic downturn in a market, our publications, revenues, and profitability in that market could be adversely affected. Our advertising and marketing services revenues could also be affected by negative trends in the general economy that affect consumer spending. The advertisers in our newspapers, other publications, and related websites are primarily retail businesses that can be significantly affected by regional or national economic downturns and other developments. Declines in the U.S. economy could also significantly affect key advertising revenue categories, such as help wanted, real estate, and automotive.

Uncertainty and adverse changes in the general economic conditions of markets in which we participate may negatively affect our business.

Current and future economic conditions are inherently uncertain. It is difficult to estimate the level of growth or contraction for the economy as a whole, and even more difficult to estimate growth or contraction in various parts, sectors, and regions of the economy, including the markets our publications serve. Adverse changes may occur as a result of weak global economic conditions, declining oil prices, wavering consumer confidence, unemployment, declines in stock markets, contraction of credit availability, declines in real estate values, natural disasters, or other factors affecting economic conditions in general. These changes may negatively affect the sales of our products, increase exposure to losses from bad debts, increase the cost and decrease the availability of financing, or increase costs associated with publishing and distributing our publications.

The collectability of accounts receivable under adverse economic conditions could deteriorate to a greater extent than provided for in our financial statements and in our projections of future results.

Adverse economic conditions in the U.S. may increase our exposure to losses resulting from financial distress, insolvency, and the potential bankruptcy of our advertising and marketing services customers. Our accounts receivable is stated at net estimated realizable value, and our allowance for credit losses has been determined based on several factors, including receivable agings, significant individual credit risk accounts, and historical experience. If such collectability estimates prove inaccurate, adjustments to future operating results could occur.

The value of our intangible assets may become impaired, depending upon future operating results.

At September 26, 2021, the carrying value of our goodwill was $330,204,000, the carrying value of mastheads was $39,672,000, and the carrying value of our amortizable intangible assets was $116,999,000. The indefinite-lived assets (goodwill and mastheads) are subject to annual impairment testing and more frequent testing upon the occurrence of certain events or significant changes in our circumstances that indicate all or a portion of their carrying values may no longer be recoverable, in which case a non-cash charge to earnings may be necessary in the relevant period. We may subsequently experience market pressures which could cause future cash flows to decline below our current expectations, or volatile equity markets could negatively impact market factors used in the impairment analysis, including earnings multiples, discount rates, and long-term growth rates. Any future evaluations requiring an asset impairment charge for goodwill or other intangible assets would adversely affect future reported results of operations and stockholders’ equity.

For further information on goodwill and intangible assets, see Note 5 — Goodwill and other intangible assets.

Risk Related to Competition from Digital Media

Our operating revenue may be materially adversely affected if we do not successfully respond to the shift in newspaper readership and advertising expenditures away from traditional print media and towards digital media. Significant capital investments may be needed to respond to this shift.

Currently, a primary source of revenue is from advertising and marketing services, which accounts for 46% of our revenue. Subscription revenue accounts for 45% of our revenue. The media publishing industry has experienced rapid evolution in consumer demands and expectations due to advances in technology, which have led to a proliferation of delivery methods for news and information. The number of consumers who access online services through devices other than personal computers, such as tablets and mobile devices, has increased dramatically in recent years and likely will continue to increase. The media publishing industry also continues to be affected by demographic shifts, with older generations preferring more traditional print newspaper delivery and younger generations consuming news through digital media. Also, the revenues generated by media publishing companies have been affected significantly by the shift in advertising expenditures towards digital media.

The future revenue performance of our digital business depends to a significant degree upon the growth development and management of our subscriber and advertising audiences. The growth of our digital business over the long term depends on various factors, including, among other things, the ability to:

| | • | Continue to increase digital audiences; |

| | • | Attract advertisers to our digital platforms; |

| | • | Tailor our products to efficiently and effectively deliver content and advertising on mobile devices; |

| | • | Maintain or increase the advertising rates on our digital platforms; |

| | • | Exploit new and existing technologies to distinguish our products and services from those of competitors and develop new content, products and services; |

| | • | Invest funds and resources in digital opportunities; |

| | • | Partner with, or use services from, providers that can assist us in effectively growing our digital business; and |

| | • | Create digital content and platforms that attract and engage audiences in our markets. |

If we are unable to grow our digital audience, distinguish our products and services from those of our competitors or develop compelling new products and services that engage users across multiple platforms, then our business, financial condition, and results of operations may be adversely affected. Responding to the changes described above may require us to make significant capital investments and incur significant research and development costs related to building, maintaining, and evolving our technology infrastructure, and our ability to make the level of investments required may be limited.

See “Audiences” in Item 1, included herein, for additional information on about our print and digital audiences.

Risks Related to Takeover Attempts

Alden’s unsolicited proposal to acquire us may divert management’s attention and resources, cause us to incur substantial costs, and have an adverse effect on our business.

On November 22, 2021, we received an unsolicited proposal from Alden Global Capital, LLC (with its affiliates, “Alden”) to acquire the Company for $24.00 per share in cash (the “Unsolicited Proposal”). On December 9, 2021, we announced that our Board of Directors, in consultation with its independent financial and legal advisors, unanimously determined to reject the Unsolicited Proposal, as it significantly undervalues the Company and is not in the best interests of the Company and its stockholders.

The events surrounding the Unsolicited Proposal and related circumstances and our response have required, and may continue to require, significant time and attention by management and our Board of Directors and have required us, and may continue to require us, to incur significant legal and advisory fees and expenses. Further, actions taken by Alden or other third parties as a result of the Unsolicited Proposal, including a proxy contest, could disrupt our business, distract us from efforts to improve our business, cause us to incur substantial additional expense, create perceived uncertainties among current and potential employees, customers, clients, suppliers, and other constituencies as to our future direction as a consequence thereof that may result in lost sales or other business arrangements and the loss of potential business opportunities, and make it more difficult to attract and retain qualified personnel and business partners. Actions that our Board of Directors has taken, and may take in the future, in response to any offer or other related actions by Alden, including the Unsolicited Proposal and Alden’s purported notice of nominations in connection with our 2022 annual meeting of stockholders (which our Board of Directors determined was invalid under our by-laws for failing to comply with requirements of our by-laws), or any other offer or proposal may result in litigation against us. These lawsuits may be a significant distraction for our management and employees and may require us to incur significant costs. If determined adversely to us, these lawsuits could harm our business and have a material adverse effect on our results of operations. We also believe the future trading price of our Common Stock could be subject to wide price fluctuations based on uncertainty associated with the Unsolicited Proposal.

The stockholder rights plan adopted by our Board of Directors may impair a takeover attempt.

On November 24, 2021, our Board of Directors adopted a stockholder rights plan (the “Rights Agreement”). Pursuant to the Rights Agreement, on November 24, 2021, our Board of Directors declared a dividend of one preferred share purchase right (a “Right”), payable on December 6, 2021, for each share of our Common Stock outstanding to the stockholders of record on that date. Each Right entitles the registered holder to purchase from the Company one-thousandth of a share of Series B Participating Convertible Preferred Stock, without par value (the “Preferred Shares”), of the Company at a price of $120.00 per one one-thousandth of a Preferred Share represented by a Right, subject to adjustment.

The Rights will initially trade with our Common Stock and will generally become exercisable only if any person or group, other than certain exempt persons, acquires beneficial ownership of 10% (or 20% in the case of certain passive investors) or more of our Common Stock outstanding. In the event the Rights become exercisable, each holder of a Right, other than the triggering person(s), will be entitled to purchase additional shares of our Common Stock at a 50% discount or the Company may exchange each Right held by such holders for one share of our Common Stock. The Rights Agreement will continue in effect until November 23, 2022, or unless earlier redeemed or terminated by the Company, as provided in the Rights Agreement. The Rights have no voting or dividend privileges, and, unless and until they become exercisable, have no dilutive effect on the earnings of the Company.

The Rights Agreement applies equally to all current and future stockholders and is not intended to deter offers or preclude our Board of Directors from considering acquisition proposals that are fair and otherwise in the best interest of our stockholders. However, the overall effect of the Rights Agreement may render it more difficult or discourage a merger, tender offer, or other business combination involving us that is not supported by our Board of Directors.

Additional details about the Rights Agreement are contained in the Current Report on Form 8-K filed by the Company with the SEC on November 24, 2021.

Risks Related to our Acquisitions of BH Media and Buffalo News

On March 16, 2020, the Company completed the purchase of certain assets and the assumption of certain liabilities of the newspaper and related community publications business of BH Media and the purchase of all of the issued and outstanding capital stock of Buffalo News (collectively, the “Transactions”). Under the terms of the Asset and Stock Purchase Agreement, dated January 29, 2020, with Berkshire Hathaway, Inc. (“Berkshire”), and BH Media (the “Purchase Agreement”), the aggregate purchase price for the Transactions was $140 million, which excluded $12 million in cash at closing of the Transactions. BH Finance, LLC (“BH Finance”), an affiliate of Berkshire, financed the Purchase Agreement through the Credit Agreement, dated January 29, 2020 (the “Credit Agreement”).

The Company borrowed $576 million from BH Finance under the Credit Agreement in order to finance the Transactions and refinance its outstanding indebtedness.

We may not achieve the intended benefits of the BH Media acquisition.

We completed the BH Media acquisition in March 2020, and there can be no assurance that we will be able to realize the expected benefits of the transaction.

There are many challenges associated with integrating a material acquisition, such as our acquisition of BH Media and Buffalo News, including the integration of executive and other employee teams with historically different cultures and priorities; the coordination of personnel located across multiple geographic locations; retaining key management and other employees; consolidating corporate and administrative infrastructures and eliminating duplicative operations; the diversion of management’s attention from ongoing business concerns; retaining existing business and operational relationships, including customers, suppliers and other counterparties, and attracting new business and operational relationships; unanticipated issues in integrating information technology, communications and other systems; as well as unforeseen expenses associated with the acquisition. These and other challenges could result in unanticipated operational challenges and the failure to realize anticipated synergies in the expected timeframe or at all.

If we fail to realize anticipated synergies in the amount and within the timeframe expected, our actual financial condition and results of operations may differ materially from the illustrative financial information disclosed in connection with the acquisition, which was based on various assumptions and estimates that may prove to be incorrect. Such illustrative financial information did not constitute management’s projections of future financial performance or results of operations; however, any material variance from such illustrative financial information could result in negative investor reactions that materially and adversely affect the market price of our Common Stock.

Our actual financial condition and results of operations may differ materially even if synergies are realized, due to macroeconomic factors or a variety of other risks to our business that are independent of the acquisition.

Our future results will suffer if we do not effectively manage our expanded operations.

With completion of the BH Media acquisition, the size of our business has increased significantly. Our continued success depends, in part, upon our ability to manage this expanded business, which poses substantial challenges for management, including challenges related to the management and monitoring of new operations and associated increased costs and complexity. We cannot assure that we will be successful or that we will realize the expected operating efficiencies, cost savings, and other benefits from the combination that we currently anticipate.

Risks Related to Cybersecurity

Our business, operating results, and reputation may be negatively impacted, and we may be subject to legal and regulatory claims if there is a loss, destruction, disclosure, misappropriation, or alteration of or unauthorized access to data owned or maintained by us, or if we are the subject of a significant data breach or cyberattack.

We rely on our information technology and communications systems to manage our business data, including communications, news and advertising content, digital products, order entry, fulfillment and other business processes. These technologies and systems also help us manage many of our internal controls over financial reporting, disclosure controls and procedures and financial systems. Attempts to compromise information technology and communications systems occur regularly across many industries and sectors, and we may be vulnerable to security breaches resulting from accidental events (such as human error) or deliberate attacks. Moreover, the techniques used to attempt attacks and the perpetrators of such attacks are constantly expanding. We face threats both from use of malicious code (such as malware, viruses and ransomware), employee theft or misuse, advanced persistent threats, and phishing and denial-of-service attacks. The Company has complied with all applicable legal requirements relating to this activity. As cyberattacks become increasingly sophisticated, and as tools and resources become more readily available to malicious third parties, the Company will incur increased costs to secure its technology environment and there can be no guarantee that the Company’s and our third-party vendors’ actions, security measures and controls designed to prevent, detect or respond to security breaches, to limit access to data, to prevent destruction, alteration, or exfiltration of data, or to limit the negative impact from such attacks, can provide absolute security against compromise. As a result, our business data, communications, news and advertising content, digital products, order entry, fulfillment and other business processes may be lost, destroyed, disclosed, misappropriated, altered or accessed without consent and various controls, automated procedures and financial systems could be compromised.

A significant security breach or other successful attack could result in significant remediation costs, including repairing system damage, engaging third-party experts, deploying additional personnel or vendor support, training employees, and compensation or incentives offered to third parties whose data has been compromised. These incidents may also lead to lost revenues resulting from a loss in competitive advantage due to the unauthorized disclosure, alteration, destruction or use of business data, the failure to retain or attract customers, the disruption of critical business processes or systems, and the diversion of management’s attention and resources. Moreover, such incidents may result in adverse media coverage, which may harm our reputation. These incidents may also lead to legal claims or proceedings, including regulatory investigations and actions and private lawsuits, and related legal fees, as well as potential settlements, judgments and fines. We maintain insurance, but the coverage and limits of our insurance policies may not be adequate to reimburse us for losses caused by security breaches.

Our possession and use of personal information and the use of payment cards by our customers present risks and expenses that could harm our business. Unauthorized access to or disclosure or manipulation of such data, whether through breach of our network security or otherwise, could expose us to liabilities and costly litigation and damage our reputation.

Our online systems store and process confidential subscriber and other sensitive data, such as names, email addresses, addresses, and other personal information. Therefore, maintaining our network security is critical. Additionally, we depend on the security of our third-party service providers. Unauthorized use of or inappropriate access to our, or our third-party service providers’ networks, computer systems and services could potentially jeopardize the security of confidential information, including payment card (credit or debit) information, of our customers. Because the techniques used to obtain unauthorized access, disable or degrade service, or sabotage systems change frequently and often are not recognized until launched against a target, we or our third-party service providers may be unable to anticipate these techniques or to implement adequate preventative measures. Non-technical means, for example, actions by an employee, can also result in a data breach. A party that is able to circumvent our security measures could misappropriate our proprietary information or the information of our customers or users, cause interruption in our operations, or damage our computers or those of our customers or users. As a result of any such breaches, customers or users may assert claims of liability against us and these activities may subject us to legal claims, adversely impact our reputation, and interfere with our ability to provide our products and services, all of which may have an adverse effect on our business, financial condition and results of operations. The coverage and limits of our insurance policies may not be adequate to reimburse us for losses caused by security breaches.

A significant number of our customers authorize us to bill their payment card accounts directly for all amounts charged by us. These customers provide payment card information and other personally identifiable information which, depending on the particular payment plan, may be maintained to facilitate future payment card transactions. Under payment card rules and our contracts with our card processors, if there is a breach of payment card information that we store, we could be liable to the banks that issue the payment cards for their related expenses and penalties. In addition, if we fail to follow payment card industry data security standards, even if there is no compromise of customer information, we could incur significant fines or lose our ability to give our customers the option of using payment cards. If we were unable to accept payment cards, our business would be seriously harmed.

There can be no assurance that any security measures we, or our third-party service providers, take will be effective in preventing a data breach. We may need to expend significant resources to protect against security breaches or to address problems caused by breaches. If an actual or perceived breach of our security occurs, the perception of the effectiveness of our security measures could be harmed and we could lose customers or users. Failure to protect confidential customer data or to provide customers with adequate notice of our privacy policies could also subject us to liabilities imposed by United States federal and state regulatory agencies or courts. We could also be subject to evolving state laws that impose data breach notification requirements, specific data security obligations, or other consumer privacy-related requirements. Our failure to comply with any of these laws or regulations may have an adverse effect on our business, financial condition and results of operations.

Risks Related to Catastrophic and Other External Events

The COVID-19 pandemic is affecting our business, financial condition and results of operations in many respects.

The impacts of the COVID-19 pandemic remain unpredictable and volatile. The COVID-19 pandemic continues to adversely impact portions of the United States economy as well as our employees, advertisers, customers, suppliers and other people and entities with whom and which we do business. There is considerable uncertainty regarding the extent to which COVID-19 will continue to spread and the extent and duration of measures to try to contain the virus, such as travel bans and restrictions, quarantines, the use of social distancing, masks and other safety measures, shelter-in-place orders and business and government shutdowns and vaccines. We are taking precautionary measures intended to help minimize the risk of the virus to our employees, including temporarily requiring some employees to work remotely.

Other factors and uncertainties include:

| | • | the severity and duration of the pandemic, including whether there are future waves or spikes in the number of COVID-19 cases caused by future mutations or related variants of the virus; |

| | • | the long-term impact of the pandemic on our business, including customer behaviors; |

| | • | general economic uncertainty, unemployment rates, and recessionary pressures; |

| | • | unknown consequences on our business performance and initiatives stemming from the substantial investment of time and other resources to the pandemic response; and |

| | • | the pace of recovery when the pandemic subsides. |

The persistence of the COVID-19 pandemic may have a material impact on our digital and print advertising and subscriptions for an unknown length of time.

We expect the COVID-19 pandemic to continue to have a negative impact in the near term. The long-term impact will depend on the length, severity, and reoccurrence of the pandemic, as well as changes in consumer behavior. The COVID-19 pandemic may accelerate, hasten or worsen the other Risk Factors described in this Item 1A.

Government-imposed COVID-19 vaccine mandates could have a material adverse impact on our business.

The United States Department of Labor’s Occupational Safety and Health Administration recently issued an Emergency Temporary Standard (“ETS”) requiring that most employers with at least 100 employees ensure their employees become fully vaccinated against COVID-19 or require those employees who do not become fully vaccinated to obtain a negative COVID-19 test weekly. While the ETS is currently subject to a judicial stay, because we have over 100 employees the ETS applies to us if and when it becomes enforceable. Mandating the vaccination or weekly testing of all of our employees could be logistically difficult and costly, both economically and operationally, including possible labor disruptions, employee attrition, and a reduced ability to replace departing employees. Such issues could have a material adverse effect on our business operations, potentially reducing revenues and increasing costs

Natural disasters, extreme weather conditions, public health emergencies or other catastrophic events could negatively affect our business, financial condition, and results of operations.

Natural disasters and extreme weather conditions, such as hurricanes, derecho windstorms, floods, earthquakes, wildfires; acts of terrorism or violence, including active-shooter situations; and public health issues, including pandemics and quarantines, could negatively affect our operations and financial performance. Such events could result in physical damage to our properties, disruptions to our IT systems, temporary or long-term disruption in the supply of products from our suppliers, and delays in the delivery of goods to our printing facilities. Public health issues, whether occurring in the U.S. or Canada, could disrupt our operations, the operations of suppliers, or have an adverse impact on consumer spending and confidence levels.

Risks Related to Competition

We compete with a large number of companies in the local media industry, including digital media businesses and, if we are unable to compete effectively, our advertising and subscription revenues may decline.

We compete for audiences and advertising revenue with newspapers and other media such as the internet, magazines, broadcast, cable and satellite television, radio, direct mail, outdoor billboards and yellow pages. As the use of the internet and mobile devices has increased, we have lost some classified advertising and subscribers to online advertising businesses and our free Internet sites that contain abbreviated versions of our publications. Some of our current and potential competitors have greater financial and other resources than we do. If we fail to compete effectively with competing newspapers and other media, our results of operations may be materially adversely affected.

Risks Related to Pension Liabilities

Sustained increases in funding requirements of our pension and postretirement obligations may reduce the cash available for our business.

Pension plans were in a net overfunded position of $13.4 million at September 26, 2021, compared to an underfunded position of $71.5 million at September 27, 2020.

Our pension and postretirement plans invest in a variety of equity and debt securities. Future volatility and disruption in the securities markets could cause declines in the asset values of our pension and postretirement plans. In addition, a decrease in the discount rates or changes to mortality estimates and other assumptions used to determine the liability could increase the benefit obligation of the plans. Unfavorable changes to the plan assets and/or the benefit obligations could increase the level of required contributions above what is currently estimated, which could reduce the cash available for our business and debt service.

We expect to be subject to additional withdrawal liabilities in connection with multiemployer pension plans, which may reduce the cash available for our business.

We contributed to various multiemployer defined benefit pension plans during 2021 under the terms of collective-bargaining agreements (“CBAs”). For plans that are in critical status, benefit reductions may apply/or we could be required to make additional contributions.

ITEM 1B. UNRESOLVED STAFF COMMENTS

None.

ITEM 2. PROPERTIES

Our executive offices are located in leased facilities at 4600 E. 53rd Street, Davenport, Iowa. The initial lease term expires August 1, 2029.

We have 23 print sites which print most of our dailies with the exception of 14 that are printed at third party printers.

Our newspapers and other publications have formal or informal backup arrangements for printing in the event of a disruption in production capability.

ITEM 3. LEGAL PROCEEDINGS

We are involved in a variety of legal actions that arise in the normal course of business. Insurance coverage mitigates potential loss for certain of these matters. While we are unable to predict the ultimate outcome of these legal actions, it is our opinion that the disposition of these matters will not have a material adverse effect on our Consolidated Financial Statements, taken as a whole.

ITEM 4. MINE SAFETY DISCLOSURES

Not applicable.

PART II

ITEM 5. MARKET FOR THE REGISTRANT'S COMMON EQUITY,

RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

Our Common Stock is listed on the NASDAQ.

At November 30, 2021, we had 5,268 registered holders of record of our Common Stock.

Our Credit Agreement restricts us from paying dividends on our Common Stock. This restriction does not apply to dividends issued with the Company's Equity Interests or from the proceeds of a sale of the Company's Equity Interest. See Note 6 of the Notes to Consolidated Financial Statements, included herein.

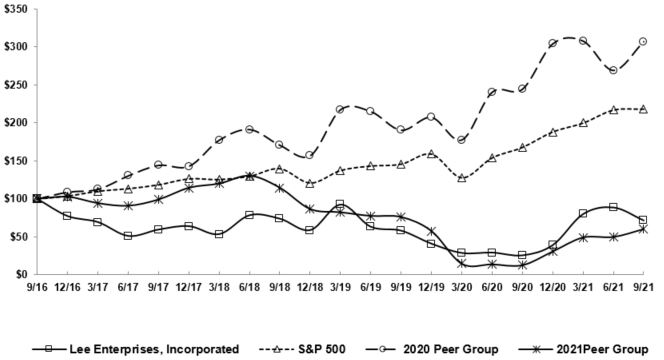

PERFORMANCE PRESENTATION

The following graph compares the percentage change in the cumulative total return of the Company, the Standard & Poor's ("S&P") 500 Stock Index, and a peer group index, in each case for the five years ended September 26, 2021 (with September 25, 2016, as the measurement point). Total return is measured by dividing (a) the sum of (i) the cumulative amount of dividends declared for the measurement period, assuming dividend reinvestment and (ii) the difference between the issuer's share price at the end and the beginning of the measurement period, by (b) the share price at the beginning of the measurement period.

Copyright© 2021 Standard & Poor's, a division of S&P Global. All rights reserved.

ITEM 6. SELECTED FINANCIAL DATA

The company has adopted the removal of the disclosure required by this item, as permitted by SEC rule changes effective February 10, 2021.

ITEM 7. MANAGEMENT'S DISCUSSION AND ANALYSIS OF

FINANCIAL CONDITION AND RESULTS OF OPERATIONS

The following discussion includes comments and analysis relating to our results of operations and financial condition as of September 26, 2021 and for fiscal years 2020 and 2019. This discussion should be read in conjunction with the Consolidated Financial Statements and related Notes thereto, included herein.

NON-GAAP FINANCIAL MEASURES

We use non-GAAP financial performance measures to supplement the financial information presented on a GAAP basis. These non-GAAP financial measures should not be considered in isolation or as a substitute for the relevant GAAP measures and should be read in conjunction with information presented on a GAAP basis.

In this report, we present Adjusted EBITDA, cash costs and margin, which are non-GAAP financial performance measures that exclude from our reported GAAP results the impact of certain items consisting primarily of restructuring charges and non-cash charges. We believe such expenses, charges, and gains are not indicative of normal, ongoing operations, and their inclusion in results makes for more difficult comparisons between years and with peer group companies. In the future, however, we are likely to incur expenses, charges, and gains similar to the items for which the applicable GAAP financial measures have been adjusted and to report non-GAAP financial measures excluding such items. Accordingly, exclusion of those or similar items in our non-GAAP presentations should not be interpreted as implying the items are non-recurring, infrequent, or unusual.

We define our non-GAAP measures, which may not be comparable to similarly titled measures reported by other companies, as follows:

Adjusted EBITDA is a non-GAAP financial performance measure that enhances financial statement users overall understanding of the operating performance of the Company. The measure isolates unusual, infrequent or non-cash transactions from the operating performance of the business. This allows users to easily compare operating performance among various fiscal periods and how management measures the performance of the business. This measure also provides users with a benchmark that can be used when forecasting future operating performance of the Company that excludes unusual, nonrecurring or one time transactions. Adjusted EBITDA is also a component of the calculation used by stockholders and analysts to determine the value of our business when using the market approach, which applies a market multiple to financial metrics. It is also a measure used to calculate the leverage ratio of the Company, which is a key financial ratio monitored and used by the Company and its investors. Adjusted EBITDA is defined as net income (loss), plus non-operating expenses, income tax expense (benefit), depreciation and amortization, assets loss (gain) on sales, impairments and other, restructuring costs and other, stock compensation and our 50% share of EBITDA from TNI and MNI, minus equity in earnings of TNI and MNI and curtailment gains.

Cash Costs represent a non-GAAP financial performance measure of operating expenses which are measured on an accrual basis and settled in cash. This measure is useful to investors in understanding the components of the Company’s cash-settled operating costs. Cash Costs can be used by financial statement users to assess the Company's ability to manage and control its operating structure. Cash Costs are defined as compensation, newsprint and ink and other operating expenses. Depreciation and amortization, assets loss (gain) on sales, impairments and other, other non-cash operating expenses and other non-operating expenses are excluded. Cash Costs also exclude restructuring costs and other, which are typically settled in cash.

Total Operating Revenue Less Cash Costs, or “margin”, represents a non-GAAP financial performance measure of revenue less total cash costs, also a non-GAAP financial measure. This measure is useful to investors in understanding the profitability of the Company after direct cash costs related to the production and delivery of products are paid. Margin is also useful in developing opinions and expectations about the Company’s ability to manage and control its operating cost structure in relation to its peers.

A table reconciling Adjusted EBITDA to net income, the most directly comparable measure under GAAP, is set forth below under the caption "Reconciliation of Non-GAAP Financial Measures".

The subtotals of operating expenses representing cash costs and total operating revenue less cash costs can be found in tables in Item 7, included herein, under the caption “Continuing Operations”.

RECONCILIATION OF NON-GAAP FINANCIAL MEASURES

(UNAUDITED)

The table below reconciles the non-GAAP financial performance measure of Adjusted EBITDA to net income, the most directly comparable GAAP measure:

(Thousands of Dollars) | | 2021 | | | 2020 | | | 2019 | |

| | | | | | | | | | | | | |

Net Income (loss) | | | 24,832 | | | | (1,261 | ) | | | 15,909 | |

Adjusted to exclude | | | | | | | | | | | | |

Income tax expense | | | 7,215 | | | | 4,104 | | | | 7,931 | |

Non-operating expenses, net | | | 24,509 | | | | 47,435 | | | | 50,889 | |

Equity in earnings of TNI and MNI | | | (6,412 | ) | | | (3,403 | ) | | | (7,121 | ) |

Assets loss (gain) on sales, impairments and other | | | 8,214 | | | | (5,403 | ) | | | 2,464 | |

Depreciation and amortization | | | 42,841 | | | | 36,133 | | | | 29,332 | |

Restructuring costs and other | | | 7,182 | | | | 13,751 | | | | 11,635 | |

Stock compensation | | | 854 | | | | 1,051 | | | | 1,638 | |

Add: | | | | | | | | | | | | |

Ownership share of TNI and MNI EBITDA (50%) | | | 7,317 | | | | 4,764 | | | | 8,811 | |

Adjusted EBITDA | | | 116,552 | | | | 97,171 | | | | 121,488 | |

CRITICAL ACCOUNTING POLICIES

The preparation of financial statements in conformity with generally accepted accounting principles requires management to make estimates and assumptions about future events that affect the amounts reported in the financial statements and accompanying notes. Actual results could differ significantly from those estimates. We believe the following discussion addresses our most critical accounting policies, which are those that are important to the presentation of our financial condition and results of operations and require management's most subjective and complex judgments.

Intangible Assets, Other Than Goodwill

Local mastheads (e.g., publishing periodical titles and web site domain names) are not subject to amortization. Non-amortized intangible assets are tested for impairment annually on the first day of the fourth fiscal quarter or more frequently if events or changes in circumstances suggest the asset might be impaired.

The quantitative impairment test consists of comparing the fair value of each masthead or domain name with its carrying amount. We use a relief from royalty approach which utilizes a discounted cash flow model to determine the fair value of each masthead, domain name, or trade name. Management's judgments and estimates of future operating results in determining the intangibles fair values are consistently applied to each underlying business in determining the fair value of each intangible asset. In 2021 and 2020, we recognized impairment charges of $787,000 and $972,000, respectively. No impairment was recorded in 2019. Of our various mastheads, several have fair values that have headroom under 20% over their carrying value and could experience impairment in the future if we do not achieve our revenue projections.

Our amortizable intangible assets consist mainly of customer relationships including subscriber lists and advertiser relationships. These asset values are amortized systematically over their estimated useful lives. Intangible assets subject to amortization are tested for recoverability whenever events or changes in circumstances indicate that their carrying amounts may not be recoverable. The carrying amount of each asset group is not recoverable if it exceeds the sum of the undiscounted cash flows expected to result from the use of such asset group. In 2021, we recognized $190,000 of impairment on intangible assets subject to amortization. There were no indicators of impairment on intangible assets subject to amortization in 2020 or 2019.