Dennis Glass

President and Chief Executive Officer

Lincoln Financial Group

Strategic Overview

AUM

+ $31 billion

+14%

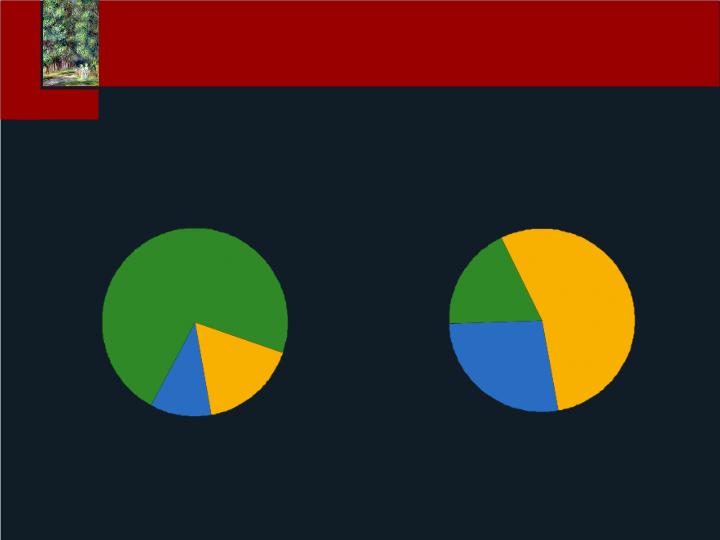

Life

Annuities

Defined Contribution

Delaware Retail Mutual Funds

Group Protection Premiums

+ 39%

+ 22%

+ 23%

+ 35%

+ 15%

Sales*

* Data represents 3Q06 YTD versus 3Q07 YTD sales and includes JP results prior to 2Q06; Life sales represent target premium plus 5% of excess premium (including adjustments for internal replacements at 50%), except whole life and term sales, which represent 100% of first year paid premium; Annuity sales represent deposits; Mutual fund sales represent deposits and reinvested dividends for new and existing accounts; Group Protection premiums represent annualized sales from new policies and include group life, disability and dental.

Strong Year-over-Year Asset and

Sales Growth

Focused on Top Line and

Bottom Line Growth

Change the growth trend line by over allocating

resources to high growth retirement businesses -

VA a good example

Invest in distribution expansion

Use acquisitions to accelerate growth in select

sub-scale businesses

Execute on the details

Innovate in the retirement income security space to

drive longer-term growth

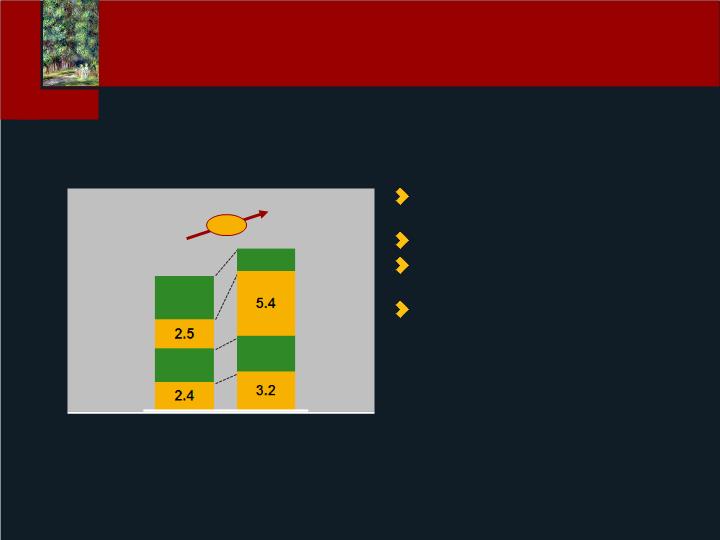

Year-end 2006

Headcount

2007

Growth

2008

Growth

530

37

6,576

120

+ 17%

+ 170%

3%

+ 19%

+ 22%

14%

Productivity Increases

Lincoln Financial

Distributors

Employer Markets -

Defined Contribution

Lincoln Financial

Network

Employer Markets -

Group Protection

Distribution Growth and

Productivity Driving Sales Results

Variable

annuities

Fixed

annuities

Channels

Independents/

FPs/IBDs

Banks

Stockbrokers

#1

18%

#10

4%

#9

3%

#5

9%

#7

9%

#14

2%

$28

$17

$4

Source: McKinsey Research, LIMRA 2006 Individual Annuities Sales Survey, LFG

$20

$30

$50

High potential

Market Size in

$ Billions

Opportunities for Further Market

Penetration - Annuities

2006 Lincoln rank and market share

#4

8%

#9

4%

#2

10%

#4

10%

#2

20%

#3

9%

$0.8

$0.9

$0.1

Career/

affiliated

PPGAs/IP

Life brokerage/

MGA

Stock-brokers/

Banks

Source: LIMRA 2006; LFD

VUL/VL

Universal life

High potential

Market Size in

$ Billions

Products

#8

4%

#7

5%

$0.2

$1.0

$3.3

$0.1

$0.8

Opportunities for Further Market

Penetration - Life

2006 Lincoln rank and market share

Career

agents

Advisors/

brokers

Size, 2006 ($ Billions)

$590

$181

$188

$769

Consultants/

institutional

direct

$376

$1552

Large/

mega

Micro/

small

Medium

Health

care

K-12

Higher

ed

403(b)

401(k)

High potential

#3

#3

#8

#11

Opportunities for Further Market

Penetration - DC

Product Development and

Innovation Driving Sales

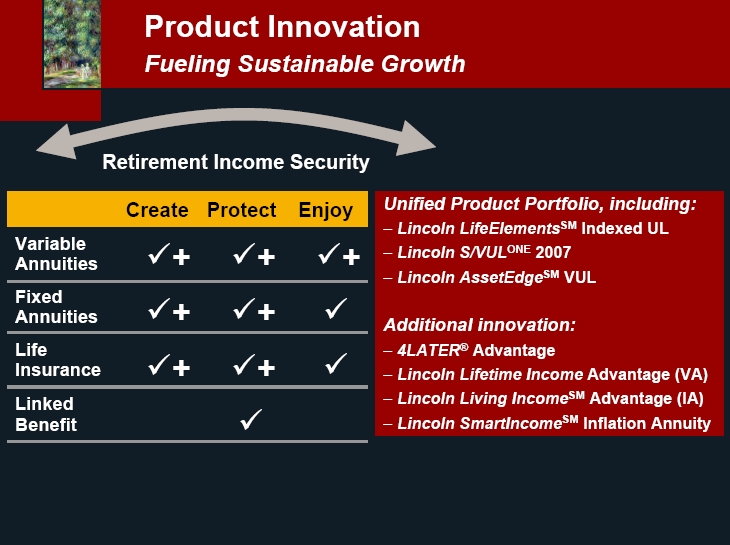

Unified Product Portfolio

MoneyGuard® Reserve NY

VULONE

Unified Product Portfolio

Lincoln Lifetime Income

Lincoln SmartIncomeSM Inflation Annuity

i4LIFE® Advantage

SmartFutureSM

Closed End Fund

Life

Annuity

DC

Asset

Management

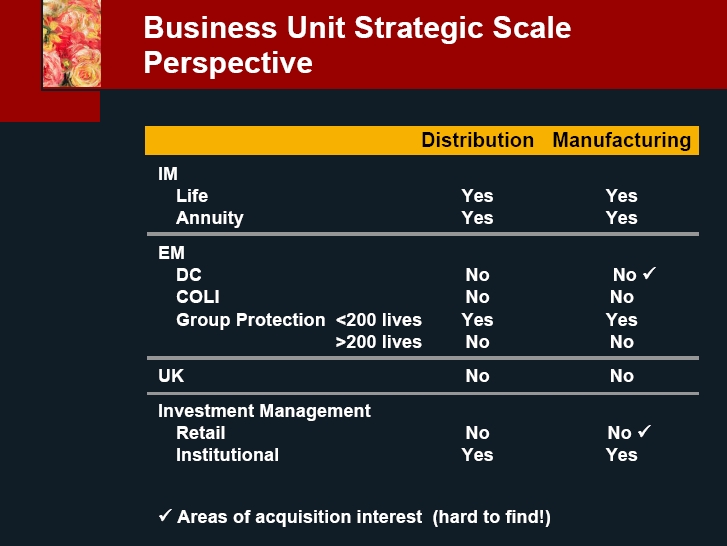

| Distribution | Manufacturing | |

| IM | ||

| Life | yes | yes |

| Annuity | yes | yes |

| EM | ||

| DC | no | no |

| COLI | no | no |

| Group Protection <200 lives | yes | yes |

| >200 lives | no | no |

| UK | ||

| Investment Management | ||

| Retail | no | no |

| Institutional | yes | yes |

“Operating effectiveness equals margin

improvement and increased earnings for

reinvesting in the business.”

Executing on Details -

Operating Effectiveness

Unit costs decreasing across the Company

Raising merger cost savings target by 10%

LFD and LFN are operating within allowables

(vs. a loss of ~$36 million in 2005)

Questions?

Patrick Coyne

President

Delaware Investments

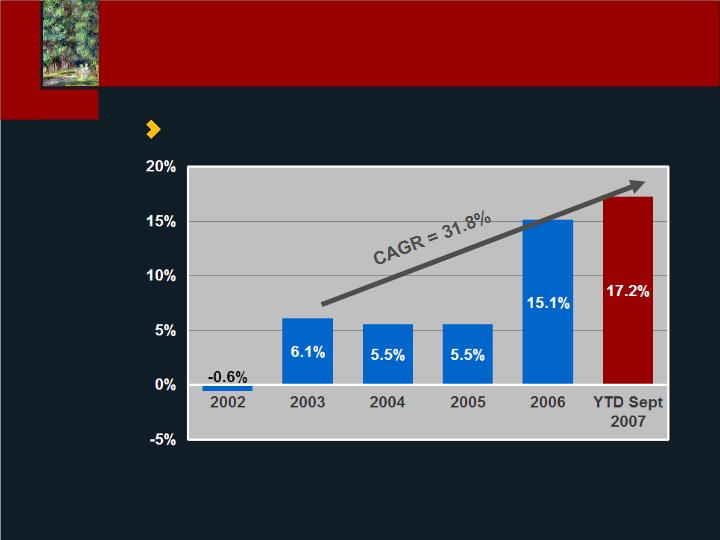

0

5

10

15

20

25

30

35

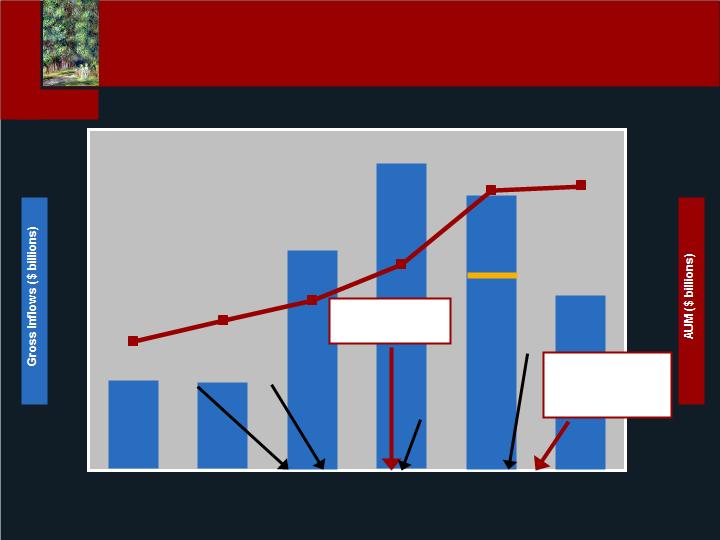

2002

2003

2004

2005

2006

YTD 9/30/07

0

40

80

120

160

200

Added

Large Cap

Value Team

Added

Emerging

Markets

Team

Added Focus

Growth Team

Added Int’l

Value Equity

Team

Sold

DIAL

Announcement

of LCP

discussions

As of

9/30/06

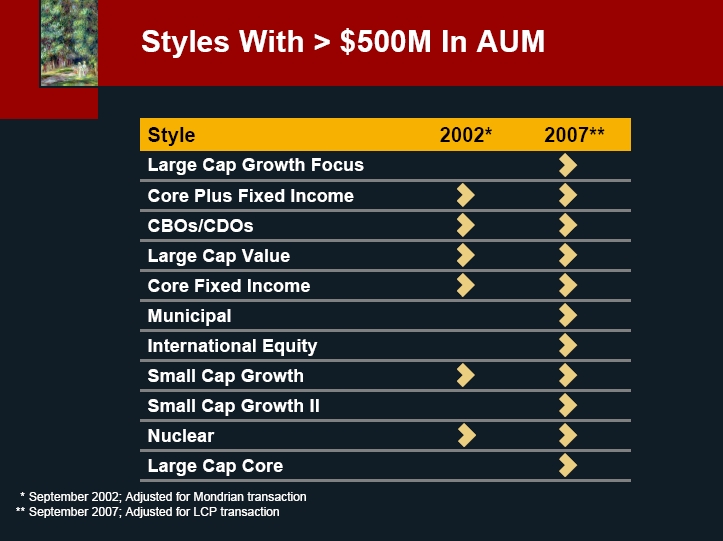

2002 and 2003 Sales and AUM excludes Mondrian

Asset & Gross Inflows

Fixed Income Update

Transaction Overview

Logan Circle Partners (LCP) transaction closed on

October 31, 2007

Delaware remains fully committed to the fixed income

business

• Since spring 2007, we have actively recruited and

hired seasoned individuals to replace departed

team members

• Delaware currently employs over 100 fixed income

investment professionals, including dedicated

insurance resources, that manage approximately

$93 billion in assets

Incremental impact to operating earnings in 4Q07

expected to be minimal relative to 3Q07

Incremental impact to operating earnings in 2008

expected to be $3 million / quarter, after tax

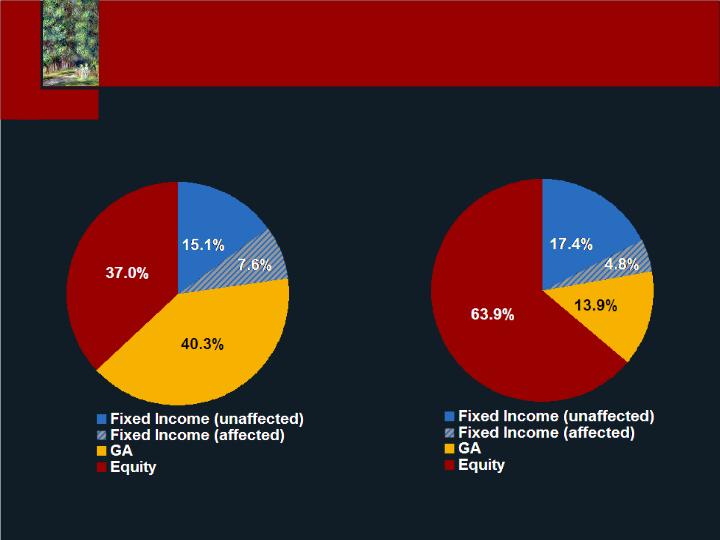

Total AUM

Advisory Revenues

Data pro-forma using September 30, 2007 assets and 3Q07 revenues

Fixed Income Update

Marginal Impact on Overall Business

Sales exclude 529, Optimum Funds, Closed End and Dividend Reinvestments

Mutual Fund Sales

Delaware Mutual Fund Family

• In February 2007 Barron’s, ranked #4 based on

– 2nd time in 4 years that Delaware achieved

Top 5 distinction

• Ranked one of the top fund families of 2007 by Lipper

– Won 7 Lipper Awards for 3-, 5-, and 10-year performance2

Individual Fund Distinctions

• Delaware Dividend Income Fund

– One of only 10 “stock-holding funds that have finished

each calendar year since 1997 with positive returns”3

• Delaware Diversified Income Fund

– Overall Morningstar rating of “5-stars”

– Largest fund, as well as best-selling fund in past two years

• Delaware Emerging Markets Fund

– One of the top funds in a 5-year performance period for ALL

Barron’s annual review of

fund families; February 2007

2 March 2007

3 10/9/07 Dow Jones article

4 10/4/07 Wall Street Journal articl

mutual fund

1 Gross Proceeds

Building On Our Momentum

Accelerating Organic Growth

Retail Scale

• Exploring opportunities, including M&A, to build

retail scale

Proprietary in-house international value equity

and emerging markets teams

• Internal products now offered as alternatives to

capacity-constrained Mondrian products

Closed-End Funds

• Launched $260 million1 fund in June; continuing to

explore future opportunities based on market

demand

CDOs

• $2.4 billion of CDO launches in 2007; opportunistic

and based on market conditions

Building On Our Momentum

Constant Rationalization of our Business

Transfer of certain investment accounting

administrative activities to our provider of

asset services

Exit of 529 business

Reducing sub advisory expenses by bringing new

teams on board to replace external managers

Natural leverage of business as asset base grows

Anticipate pre-tax operating margins for full-year

2008 in 19% - 20% range

* Pre-tax operating margin defined as

income (loss) from operations before

federal income taxes divided by

operating revenue

Improving Operating Results

Pre-Tax Operating Margins*

Questions?

Appendix

All data as of 9/30/07

Domestic Equity

International / Global Equity

Taxable Fixed Income

Tax-Free Fixed Income

Lipper Performance

Percent of Funds by Style in Top Half of

Lipper universes

Total Operating Revenue ($ million)

Total Operating Expenses ($ million)

Pre-Tax Operating Income ($ million)

Pre-Tax Operating Margin*

Indicates Sept. YTD 2006

Indicates Sept. YTD 2006

Indicates Sept. YTD 2006

* Pre-tax operating margin defined as income (loss) from operations before federal income taxes divided by operating revenue

Historical Financials

Wes Thompson

President, Lincoln Employer Markets

Employer Markets

Investing for

Long-Term Growth

Employer Markets’ Mission

Addressing the retirement income

security needs of employers and their

employees through:

• Defined Contribution Plans

• Group Protection Plans and

• Executive Benefits

Defined

Contribution

53%

Group

Protection

32%

Executive

Benefits &

Other

15%

23% of LFG Earnings

$43.7 billion in

Account Values

$262.9 million in

Income from

Operations

Employer Markets Business Today

Employer Markets Income from Operations*

| * As of September 30, 2007 YTD |

Healthcare Education 403(b) | Mid-Large Healthcare & Corporate 401(k) and 403(b) | Small Corporate 401(k) |

Advisor-based | Consultants Brokers | Independent Planners, Wirehouses, Banks, TPAs |

Multi-Fund® Alliance® DirectorSM

(Annuity) (Mutual Fund) (Group Variable

Annuity)

Market

Focus

Distribution

LFG’s DC Business

* As of September 30, 2007 YTD

** As of June 30, 2007 YTD

*** Alliance data throughout the presentation includes the fixed portion of the contract.

Earnings**

Account Value*

Deposits*

Alliance (Mid-Large Mutual Fund)***

Director/LALR (Small GVA)

Multi-Fund (403(b) Annuity)

Other

25%

22%

50%

3%

50%

29%

19%

2%

13%

70%

4%

13%

The Changing DC Business Mix

Historically, Lincoln’s DC business mix was

dominated by the annuity 403(b) block

* As of September 30, 2007 YTD

Net Flows*

in Millions

Director/LALR (Small GVA)

Alliance (Mid-Large Mutual Fund)

Multi-Fund (403(b) Annuity)

Other

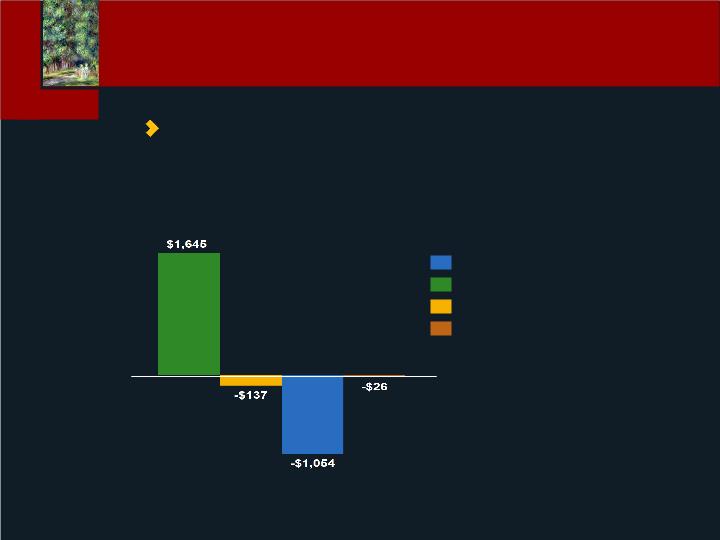

The Changing DC Business Mix

Positive Net Flows From “New” Products

Business Mix is Shifting to the Mid-Market Mutual Fund and

Small Market Group Variable Annuity Platforms

Annuity 403(b)

Net Flows

- $1,054 million

ROA (bps)

75

Earnings Implication

-$7.9 million

x

=

Mid-Large Mutual Fund

Net Flows

$3,000 million

ROA (bps)

25- 40

Earnings Implication

$7.5 - $12 million

x

=

The Changing DC Business Mix

Earnings Implications

However, the changing mix of Lincoln’s DC business

creates a short-term earnings gap…

To replace $8 million in earnings from Multi-Fund, we

need to generate $3 billion in additional assets in

Alliance and Director

Strategy to Replace and Grow Earnings

Building the Business

• Clear Focus on Growth Markets

• Invest in Distribution and New Channels

• Expand Product and Service Capabilities

• Improve Operating Effectiveness

2004

2007E

2012E

11%

9%

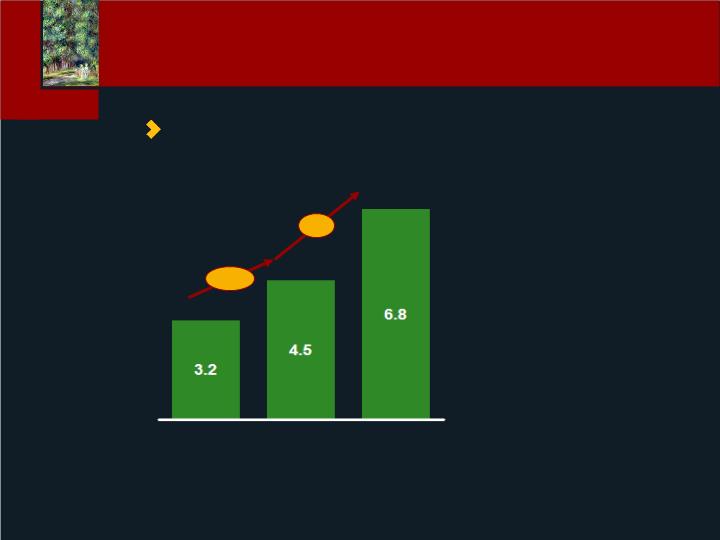

Clear Focus on Growth Markets

AUM Projections

Defined Contribution Market

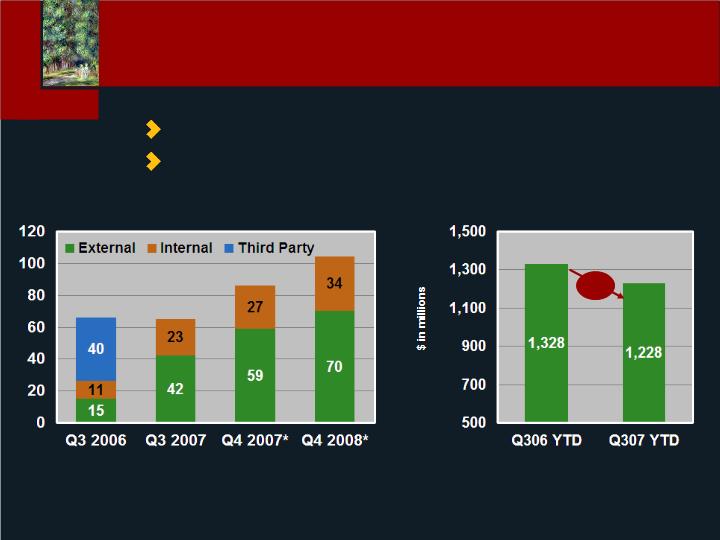

AUM, $ Trillions

* Includes 457 and 401(a), as well as money purchase plans, profit sharing plans, and deferred compensation plans

Source: ICI; Cerulli; EM internal projections of DC net flows (from Cerulli, 2006); McKinsey banking practice

*As of September 30, 2007 YTD

** DirectorSM deposits include $25 million of deposits from the LALR product.

Multi-Fund® | Alliance® | DirectorSM |

$948m | $2,161m | $1,228m** |

Healthcare Education 403(b) | Mid-Large Healthcare & Corporate 401(k) and 403(b) | Small Corporate 401(k) |

Advisor-based | Consultants Brokers | Independent Planners, Wirehouses, Banks, TPAs |

Market

Focus

Distribution

Deposits*

Clear Focus on Growth Markets

View of Today’s Deposits

Today, 79% of deposits come from our target markets*

* 2007 Wholesales as of YTD 3Q07, 2008 Wholesalers are projected**Internal and External Wholesaler counts include Sales Management

Number of Wholesalers**

Sales

99%

Investing In Distribution

Capacity and Productivity

Mid-Large Healthcare & Corporate 403(b) & 401(k) Market

Alliance®

8%

* 2007 Wholesales as of YTD 3Q07, 2008 Wholesalers are projected**Internal and External Wholesaler counts include Sales Management

Number of Wholesalers**

Sales

Investing In Distribution

Capacity and Productivity

Small Corporate 401(k) Market

DirectorSM and LALRSM

2+ Years

10%

<1 Year

73%

1-2 Years

17%

2+ Years

27%

1-2 Years

55%

Tenure

DirectorSM/LALRSM Wholesalers*:

Tenure

Alliance® Wholesalers*:

<1 Year

18%

Investing In Distribution

Capacity and Productivity

| * 2007 Wholesalers as of YTD September 30, 2007 |

Top Firms Serving Small to Mid Market

Wire

• Morgan

Stanley

• UBS

• AG Edwards

• Wachovia

• Smith Barney

• Merrill Lynch

Independent Planner

• LFN

• Edward Jones

• LPL

• Raymond James

• HD Vest

• AIG

Current market opportunity > $30-50 billion*

Investing In Distribution

Capitalizing on Strategic Partner Model

Strategic Partner Focus…Room to Grow

* Estimated Annual Sales

Expanding Product and Service Capabilities

The Customer Experience

Achieving Strategic Scale in Manufacturing

by Launching Innovative Product Solutions

• Lincoln American Legacy RetirementSM

• SmartFutureSM

• i4LIFE® Advantage

• Lincoln Ibbotson Insight Series

Investing in Service Improvements

• Lincoln Unifier (Multi-vendor Consolidation Services)

• Consolidated Platforms

• Customer Facing Enhancements

Defined Contribution

G & A expenses

Average Account Value

G & A as annualized % of AV

$165

$35,174

62 bps

2007

Sept. YTD

2006

Full Year

$210

$31,891

66 bps

$ in millions

Improving Operating Effectiveness

Disciplined Financial Management

What To Expect In 2008

Strong organic deposit growth in our

target markets

Improvement in net flows

Ongoing product enhancements

Additional platform improvements

Taking Market Share

Sources of Competitive Advantage*

• Scale and Brand

• Differentiated Service

• Distribution

• Education and Advice

• Product Innovation

* McKinsey Research

Questions?

Mark Konen

President

Individual Markets

Scale, Momentum, Opportunity

Product | Industry Ranking* |

Life Insurance | 1 |

Variable Annuities | 5 |

Fixed / Indexed Annuities | 10 |

$103 billion in account values**

$518 billion of life insurance in-force**

Annualized sales over $13 billion***

Over $1 billion in annualized operating earnings***

Strategic Scale

Enabling Investments in the Business

| * Based on 2Q07 YTD LIMRA, 3Q07 YTD VARDS rankings |

| **As of September 30, 2007 |

| ***Annualized numbers based on 9/30/07 year-to-date data; Fixed, indexed, and variable annuity sales represent deposits throughout the presentation; Life sales throughout the presentation represent target premium plus 5% of excess premium (including adjustments for internal replacements at 50%), except whole life and term sales, which represent 100% of first year paid premium. |

12th

3.3%

8th

5.5%

6th

6.4%

5th

6.6%

5th

6.9%

Industry Rank*

Market Share*

$6.7

3Q06

YTD

27% Growth YTD

3Q07 vs. 3Q06

Variable Annuity Growth

Taking Market Share

Lincoln Yearly Total VA Sales

* Industry and market share based on VARDS data through 3Q07 YTD

Sources: McKinsey Retirement Practice, ICI, Strategic Insight, Empirical Research Partners, SRI

3,608

3,813

1,154

Retirement assets - 2006

Expected net flows

2007-12E

Deposits

Mutual

funds

Annuities

2,556

731

351

Deposits

Mutual

funds

Annuities

Annuity Competitive Landscape

Significant Opportunity to Grow

Large share of assets in deposits and mutual funds

Significant money in motion

Longevity and investment risk management concerns should

enable insurers to capture share of money in motion

5th

5.6%

5th

6.0%

1st

7.0%

$405

3Q06

YTD

Industry Rank*

Market Share*

39% Growth YTD

3Q07 vs. 3Q06

Life Insurance Growth

Taking Market Share

Lincoln Life Insurance Sales

* Industry and market share based on VARDS data through 3Q07 YTD

Source: LIMRA

$ in Billions

Big companies taking market

share

Increased focus on protection

Flat VUL sales since 2003 present

potential opportunity

Lincoln well-positioned to

capitalize on industry trends

3.6

2.8

11.2

2001

1.9

3.0

13.5

2006

Total Industry - New Premiums

Whole

Term

VUL/VL

UL

CAGR

Percent

(12)

17

1

7

Top 10 CAGR =

6.5%

+4%

Life Insurance Competitive Landscape

Leveraging Critical Success Factors

Product Innovation and

Responsiveness

Retirement Income

Security

Operational Effectiveness

Comprehensive Risk

Management

Distribution Depth

and Breadth

Strategic Cornerstones

Blueprint for Profitable Growth

Unified Product Portfolio, including: – Lincoln LifeElementsSM Indexed UL – Lincoln S/VULONE 2007 – Lincoln AssetEdgeSM VUL Additional innovation:

– 4LATER® Advantage– Lincoln Lifetime Income Advantage (VA)– Lincoln Living IncomeSM Advantage (IA)– Lincoln SmartIncomeSM Inflation Annuity

Increasing Top Line While Decreasing Expenses

2006

Post Merger

(4/1/06 - 12/31/06)

Annuity

G & A expenses

Average Account Value

G & A as annualized % of AV

Life

G & A expenses

Collected Premiums

G & A as a % of premiums

$233

$62,046

50 bps

$336

$3,324

10.1%

$233

$70,511

44 bps

$331

$3,476

9.5%

2007

YTD

(1/1/07 - 9/30/07)

2005

Lincoln

(1/1/05 - 12/31/05)

$271

$43,498

62 bps

$297

$2,407

12.3%

Operational Effectiveness

Driving Down Expense Ratios

Customer-Centric, Scale-Enabled = Competitive Differentiator

Front Line Cross-Functional Team

Underwriting Account Executive

Dotted line to UW

Center of

Excellence

Operations Manager

Sr. NBA

NBA

NBA

NBA

NBA

Underwriting Director

Underwriter

Underwriter

Underwriter

Underwriter

Underwriting Team Structure

Operational Effectiveness

Industry Leading Underwriting

Manages New

Business staff

Business staff

Senior team member

Coaches and mentors

Accountable for team performance

Technical and process

training

training

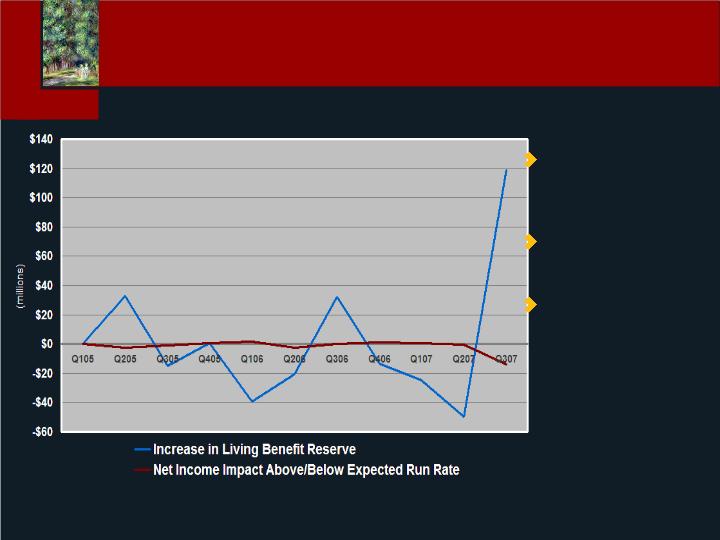

Expected run rate

cost of $2.0 - $3.0

million, after tax, after

DAC, per quarter

Q3 results driven by

volatile market

conditions

Would not expect

significant breakage

in more normal

environment

Comprehensive Risk Management

Variable Annuity Hedging Effectiveness

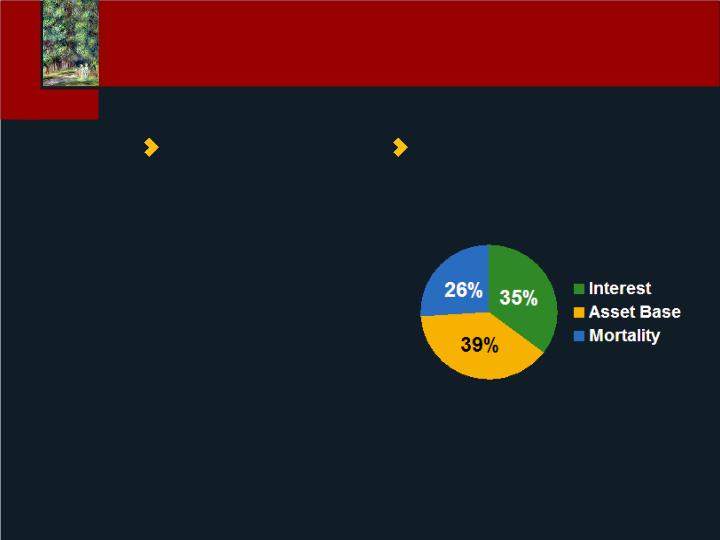

Macro:

•Balanced business mix:

$2,761M Total**

Margins

•Distribution diversification

Comprehensive Risk Management

Ensuring Stability of Results

Micro:

• Disciplined New

Business Pricing and

Monitoring

•YTD new business

expected returns:

–Annuity 18%, Life

13%*

•Equity Risk

Management

•Asset Liability

Management

•Risk Transfer

*Assumes capital solution

**Numbers reflect trailing 12 months as of 9/30/07

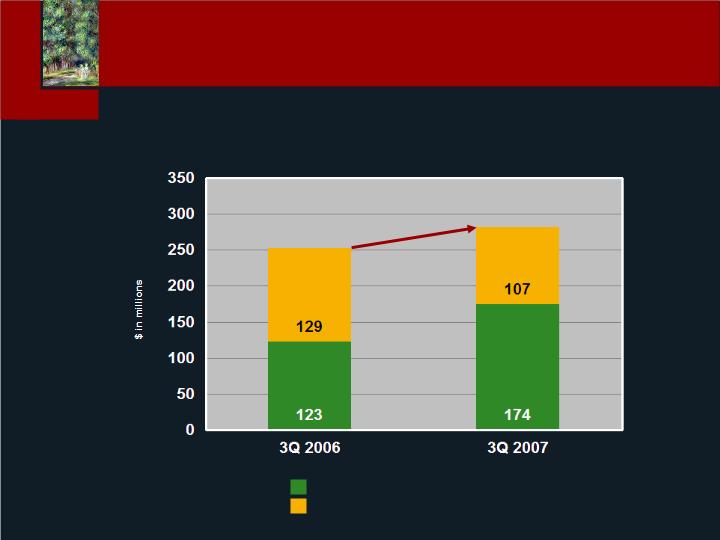

Life Income from Operations

Annuity Income from Operations

Total Individual Markets Income from Operations

11% growth

252

281

Annuity and Life Earnings

Driving Bottom Line Growth

Profitable Growth

Strategic scale

Momentum

Opportunity

Execution

Individual Markets

Questions?

Terry Mullen

President and CEO

Lincoln Financial Distributors

Lincoln

Financial

Distributors

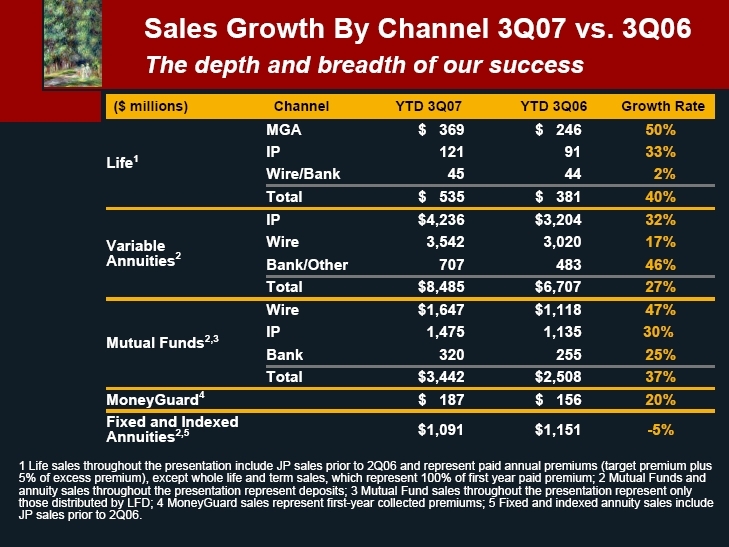

Sales Growth By Channel 3Q07 vs. 3Q06 The depth and breadth of our success ($ millions)Channel YTD 3Q07 YTD 3Q06Growth Rat Life1MGA$ 369$ 246 50% IP12191 33% Wire/Bank4544 2% Total$ 535$ 381 40% Variable Annuities2IP$4,236$3,204 32% Wire3,5423,020 17% Bank/Other707483 46% Total$8,485$6,707 27% Mutual Funds2,3Wire$1,647$1,118 47% IP1,4751,135 30% Bank320255 25% Total$3,442$2,508 37% MoneyGuard4$ 187$ 156 20% Fixed and Indexed Annuities2,5$1,091$1,151 -5% 1 Life sales throughout the presentation include JP sales prior to 2Q06 and represent paid annual premiums (target premium plus 5% of excess premium), except whole life and term sales, which represent 100% of first year paid premium; 2 Mutual Funds and annuity sales throughout the presentation represent deposits; 3 Mutual Fund sales throughout the presentation represent only those distributed by LFD; 4 MoneyGuard sales represent first-year collected premiums; 5 Fixed and indexed annuity sales include JP sales prior to 2Q06.

1 Includes term and JP sales prior to 2Q06

2 Source: LIMRA International, Inc., including term

3 Source: ICI Retail Long-Term New Sales

4 Source: VARDS Online by Morningstar New Sales

LFD | Industry | |

Life | 17%1 | 4%2 |

Mutual Funds | 17% | 6%3 |

Variable Annuity - ChoicePlus | 34% | 8%4 |

Variable Annuity - American Legacy | 25% | 8%4 |

LFD versus Industry:

Compound Annual Growth Rates 2001-2006

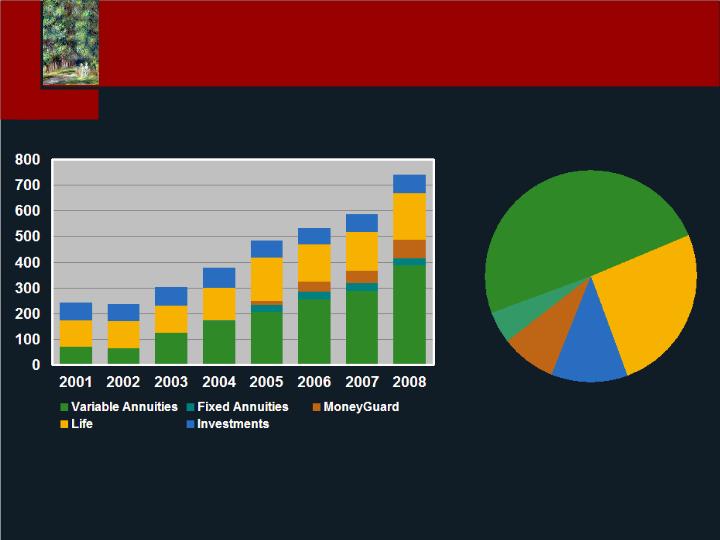

Sales Growth By Product 2001-2006

The sustainability of our success

The right business model,

the right strategy, the right people

Annuities

Investments

Wirehouse &

Regional B/Ds

Marketing

General

Agents

Independent

Planners

Banks

Wholesaling Scale and

Quality

Life

Strategic

Partnerships

Unique Solutions-Based Distribution Model

Variable

Annuities

49%

Life 26%

Investments3

12%

Number of Wholesalers1

MoneyGuard

8%

Fixed

Annuities

5%

Wholesalers by Product

As of September 30, 2007

2

2

1 Includes External Wholesalers, Internal Wholesalers and Sales Management

2 2007 Wholesalers as of YTD 3Q07, 2008 represents preliminary projections

3 Investments defined as Mutual Funds and Managed Accounts

Scale Of Wholesaling

Distribution Expansion

- Attracting top talent

Strategic Wholesaler Expansion

Redesigning territories and building deeper

relationships

Workforce Planning - Sample Analysis - IXI:

Wholesaler Tenure

As of September 30, 2007

2+ Years

52%

<1 Year

26%

1-2 Years

22%

2+ Years

43%

<1 Year

25%

1-2 Years

32%

As of September 30, 20051

1 Excludes Jefferson-Pilot wholesalers

Wholesaler Quality

Retention leading to increased productivity

Strategic Priorities

2008 - 2010

Attract and retain top wholesaling talent

Continue to surpass industry average variable

annuity, life and linked benefit sales

Develop current and new strategic partnerships

Continue to grow the population of financial advisors

selling multiple LFG products

Questions?

Bob Dineen

President and CEO

Lincoln Financial Network

Jefferson Pilot Securities Corp.

Lincoln Financial Advisors Corp.

Lincoln Financial

Network

Lincoln Financial Network Overview

LFN positioned for top & bottom-line growth

Multi-channel model is a competitive advantage

for recruiting and retaining top advisors

Retirement Income is a particularly compelling

opportunity for Retail Distribution

Independent

Full Service Support

JPSC GA ABGA / DAN LFA / Sagemark

Lincoln Financial Network Overview

6,950 affiliated producing advisors*

4 channels of independent distribution

2 broker dealers

$89B customer assets**

* Advisors as of September 30, 2007.** Aggregate customer assets for which an LFN planner as the representative of record. |

Year-to-Date September 30, 2007

Contribution to Lincoln Financial

22% life insurance PAP

•$122 million of life target premium

12% annuity premium*

•$1.4 billion of annuity and

retirement investments

~50% in-force permanent life

insurance block

* |

2006 & 2007 YTD show combined JP distribution and LFA/Sagemark

Prior periods reflect operating loss for LFA/Sagemark stand-alone

Operating results are allocated to Individual Markets and Employer Markets for external reporting

2003

2004

2005

2006

2007

YTD

Delivering Positive Results

Lincoln Financial Network

•Operating Income/Loss

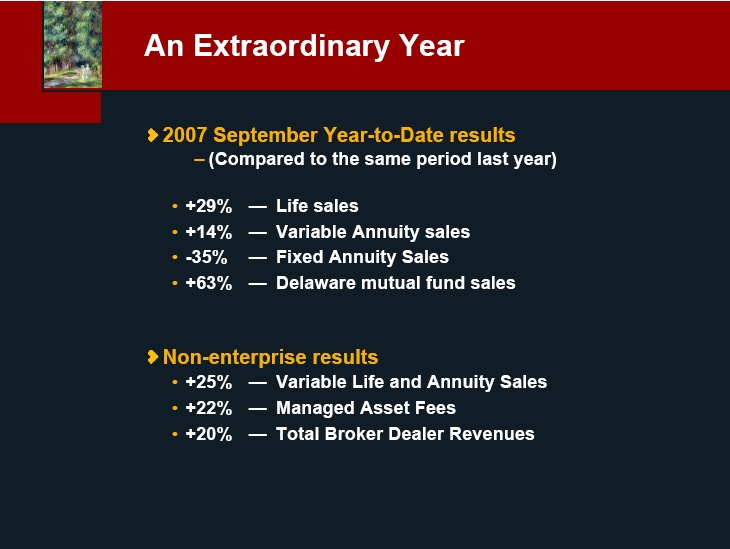

An Extraordinary Year 2007 September Year-to-Date results (Compared to the same period last year) +29% Life sales +14% Variable Annuity sales -35% Fixed Annuity Sales +63% Delaware mutual fund sales Non-enterprise results +25% Variable Life and Annuity Sales +22% Managed Asset Fees +20% Total Broker Dealer Revenues

2007 Growth Drivers

Multi-channel Model (flexibility and choice)

Investment build-out of our National

Recruiting Platform

Positive trends in GA / affiliated brokerage activations

Investment in a more competitive

compensation structure

•Fixed Life

•VA / Mutual Fund

“Distribution strategies with most success for end

consumers rely on face to face consultations and

personal referrals; independent financial advisors are

capturing greater share of the retirement market.”

- McKinsey Survey, October 2007

LFN Retirement Income Security

Our LFN Integrated Structure is positioned to serve

•Life & Legacy (Retirement Specialists)

–69 received CRPCSM certification as of 10/31/07

–25 graduated, awaiting final certification

–Additional 219 active participants

•RIS Planning Support

•Sagemark Private Wealth Services

Recruiting and Retention

From September 30, 2006 to September 30, 2007

LFN’s Recruiting Strategy

• Continue positive trend of Net Gross Dealer

Concession (GDC) Growth from Full-time Recruits

• Drive incremental GDC Growth from affiliated

brokerage activations

First full year national recruiting team

• Added 375 producing advisors

• Added 15 national recruiting professionals

• Positive net growth of GDC from Recruiting in 2007

• Current Recruiting Pipeline - 400+ experienced

advisors with average GDC of 245,000

Scale =

Growth

Outlook For An Even Better 2008

The power of Lincoln Financial Network

•Sustainable, attractive model

•Growing number of loyal, productive advisors

•Open architecture & affiliation choice

•Best-in-class products and wholesaling

•Deep financial planning expertise

•Forward-thinking retirement strategies

•The leverage of Lincoln Financial Group

Questions?

Fred Crawford

Chief Financial Officer

Lincoln Financial Group

Financial Outlook & Capital

Management

3 Year Rolling Plan - Sets Incentive Compensation

Currently In-Process - Approved by Board in February

A Look Inside Our Financial Plan

Earnings & Capital Plan

Budget Process

Sales Plan

Strategic Investments

Fundamentals

Heading for a record VA & Life

production year

Strong asset and in-force growth

Solid group protection dynamics

Investment Management expanding

margins

Defined Contribution in transition

Healthy capital position

Volatility impacts hedging

Pressure on alt. investments

Monitoring credit conditions

Markets

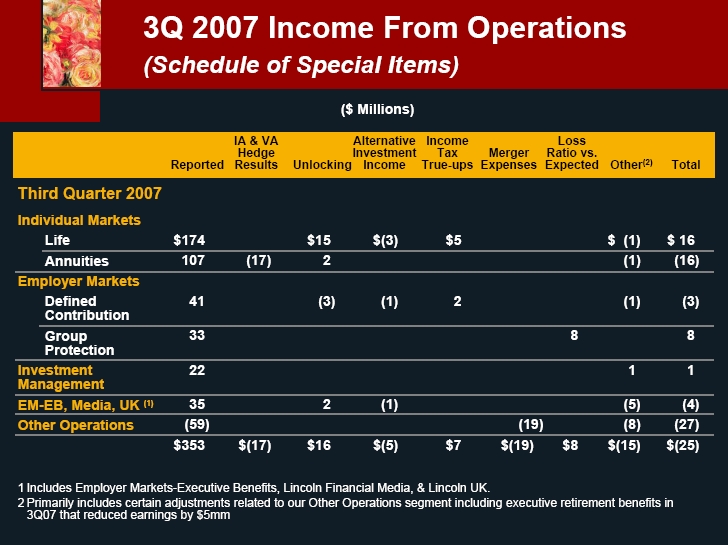

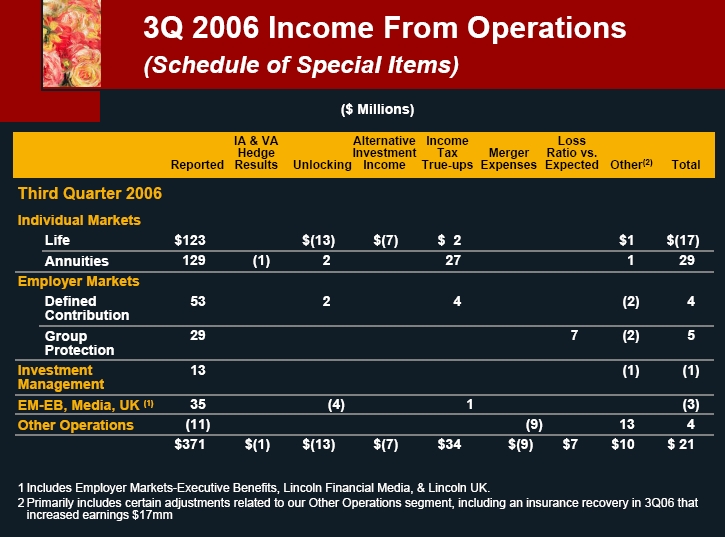

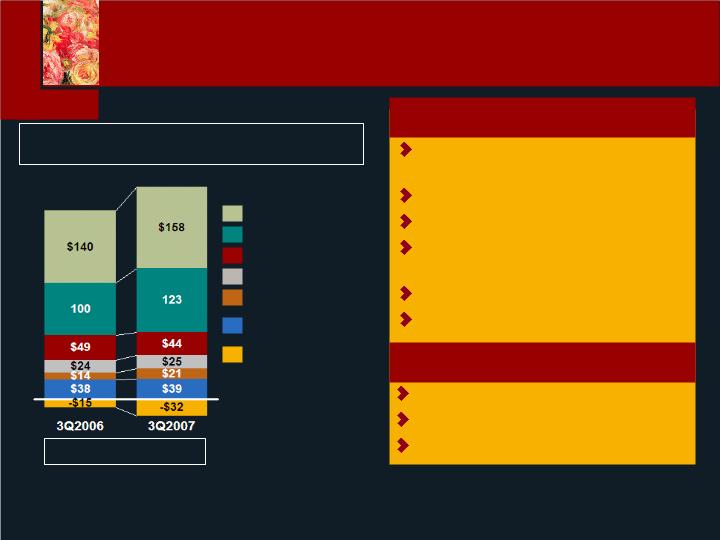

3Q Income from Operations Adjusted for Merger

Expenses & Schedule of Special Items

$350mm

$378mm

Life Insurance

Annuities

Defined Contrib.

Group Protection

Investment Mgmt.

UK, Media, Executive

Benefits**

Other Operations

Avg. diluted shares

282.4 272.5

Third Quarter: Strong Fundamentals

* See Appendix for definition of non-GAAP financial information and/or reconciliations, and schedule of special items. |

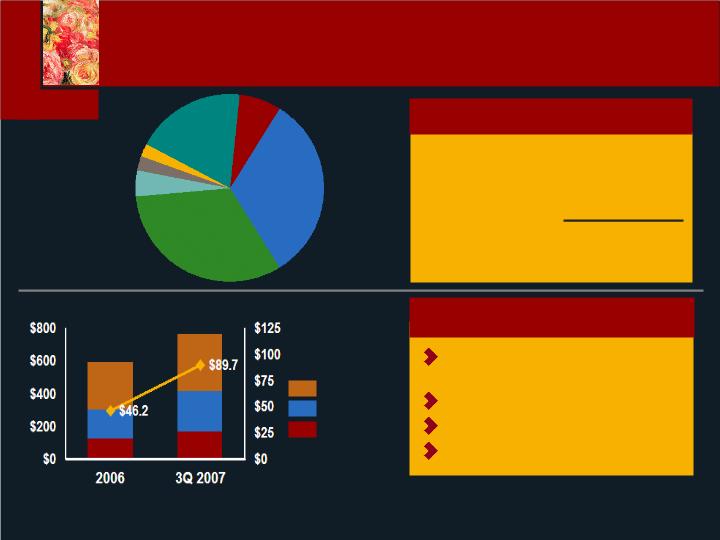

Total Average Variable Assets

($ billions)

Continued VA deposits and flow

strength

DC flows driven by Alliance

Delaware retail deposits

continue to build

2008 Outlook

Asset Fee Revenue*

($ millions)

$325

$420

S&P 50015.7%

Variable

Annuities40%

Defined

Contribution17%

Asset

Management12%

Growth Rates

Retirement Asset Gathering Engine

* VA & DC expense assessment income and asset management third-party advisory fee income. S&P represents daily average |

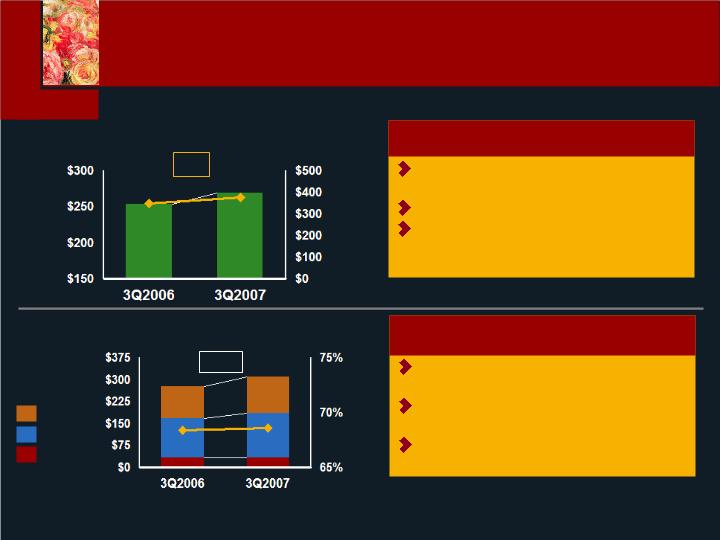

Annuity: Spreads of 200 bps. - negative flows diminish

Life: Spreads of 180 bps. - steady asset growth; securitization impact

DC: Spreads under pressure at 225 bps - with stable assets

Excess income pressured in 2008

2008 Outlook

Fixed Margin* ($ millions)

$271

$268

Defined

Contribution

Life

Annuities

($ Millions)

Fixed Margin - “A Mixed Story”

* Adjusted for FAS 113 Forward-Starting Option valuation of ($7mm) 3Q2006 and ($13mm) 3Q2007. |

Income** ($ mm)¨

Book Value* ($ mm)

Hedge Funds

Pvt. Equity

Energy/RE

$589

$761

A

28%

BBB

32%

AAA

23%

AA

10%

BB 3%

B & Lower 2%

Adj. Cash 2%

Alternative Investments

Target a 10-12% portfolio

return

Life = BV of $500mm

Annuities = BV of $121mm

DC = BV of $140mm

$60 Billion

Bond Portfolio

S-Prime Alt-A

AAA

AA & A

BBB & Lower

Total

Price / BV

$673

118

52

$843

94%

$1,137

317

30

$1,484

96%

Average Rating

“A”

General Account Conditions

* Book value at amortized cost** Pre-DAC and pre-tax |

Life - 2008 Outlook

Stable 6-8% growth in earnings

drivers

Growth in VUL and M-Guard

Settling into unified product

portfolio

Continued strength in core

small-case markets

Net earned premium growth

of 9-11%

Loss Ratios: low end of our range

71%-74%

Group - 2008 Outlook

Total Charges*

($ millions)¨

$253b

$269b

$348m

$375m

Interest-Sensitive

In-force ($ B)

8%

Non-Medical

Loss Ratio¨

Net Earned

Premium ($ mm)

11%

Life

Disability

Dental

Steady Mortality & Morbidity Margins

* Includes cost of insurance charges and expense assessments. Adjusted for prospective unlocking and related amortization of |

Integrating, Investing, and Growing ….all at the same time

Improving expense ratios in all major segments

Making significant technology & infrastructure investments

3-year save target increased to $195m-$205m range

Enterprise Expense Ratio

Expenses* to Total Revenue

3Q2006 3Q2007

Expenses* to Total Revenue

(Excluding Investment Income)

14.3% 13.3%

25.7% 22.1%

Merger Expenses

2006 2007(E) 2008-2009

$49m $100m $55m- $65m

Operating Effectiveness

* Gross G&A + Commissions (less) Deferred expenses. Adjusted for special expense items including incentive compensation |

Available Capital:

•Capital margin ~ $400 mm

•B of A stock ~ $150 mm

(A-T)

•Reserve relief ~ $300 mm

•FCF run-rate ~ $200 mm +/-

Capital Targets

“AA” capital ratios

RBC 350% to 400%

Leverage 20-25%

Capital structure (10/20/70)

EBIT coverage 8-10x

Repurchase range $300-$400mm

(ex-media)

Support Life & Annuity growth

Strategic investments

Volatile capital markets

2008 Outlook

RBC (%)** ¨

21.1%

21.6%

411%

400%

Leverage* (%)

“AA” Capital Conditions

* Leverage calculated by dividing debt adjusted for capital securities equity credit by total capital (debt plus equity adjusted for |

ROE Drivers

Growth in high-ROE segments

Capital management

Favorable capital conditions

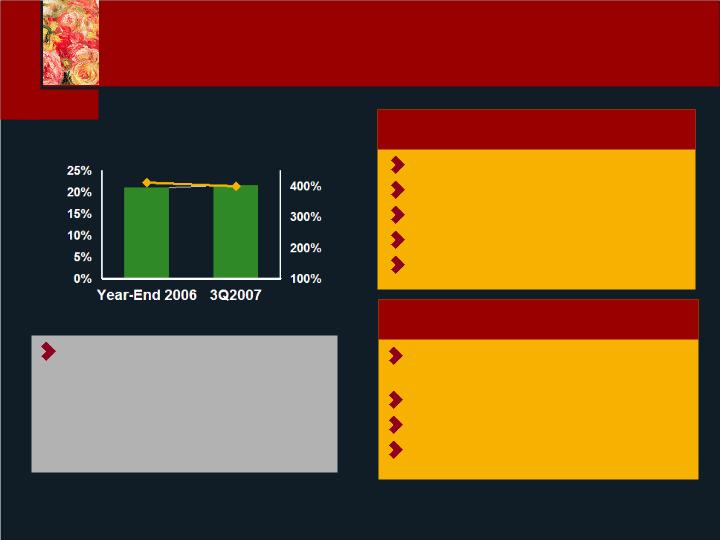

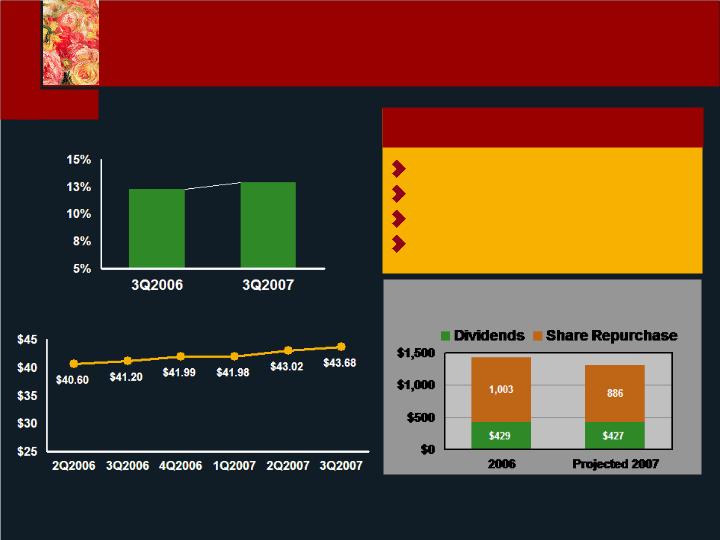

Progress towards 15% in 3 yrs

12.2%

12.9%

ROE* (%)

BVPS ($/share ex AOCI)

Capital Returned to

Shareholders ($ millions)

ROE & Book Value Progression

* ROE is based upon income from operations adjusted for special items and merger- related expenses. ROE is calculated by dividing |

Television

Charlotte Radio

Sports

Key

Takeaways

San Diego,

Denver,

Atlanta and

Miami Radio

Markets

Divested

Media

Businesses

Remaining

Media

Investment

Date Agreement

Signed

Purchase Price

($ mm)

2007 Broadcast

Cash Flow

Multiple

Strong offers reflected quality of Lincoln Financial

Media’s operations

Purchase multiples reflect acquisition levels competitive

with “normalized” credit and M&A market conditions

Concluding our strategic review

Deliberate approach in recognition of current market

environment

Continue to actively manage these investments to maximize

station performance and future valuation

Nov. 12th

$548

13.1x

Nov. 12th

100

13.8x

Nov. 12th

35

Residual

Valuation

Lincoln Media Update

Key Assumptions

Pro Forma Impact Calculations

“Leverage neutral” approach - 25% debt reduction & 75% stock repurchase

Assume 3Q adjusted earnings, diluted shares, BVPS, current share price,

and interest rates(2)

(1)Net of fees and expenses.

(2)Accretion/dilution and ROE impact is based upon annualized 3Q2007 income from operations adjusted for special items. See Appendix for non-GAAP financial

information and/or reconciliations. Other assumptions include LNC share price of $60 for repurchase, interest rate on debt of 6% and current book value per share of

$43.68.

Total Pre-tax proceeds$683

Total Net Proceeds(1)~ $450

EPS accretion/dilution (2)~.2%

Book Value Impact From Sale~($130)mm (1.1%)

ROE Impact(2)~0.3%

Media - Pro Forma Impact

3Q07 Results

Capital

Mid-point of the “AA” range

Executed on capital projects

General account well positioned

Earnings

$1.36 adjusted (ex merger exp.)

L&A, GP (80% of total) up 13% with

strong fundamentals

Market volatility

Production

Excellent retail growth - LFD/LFN

Institutional - “a mixed story”

2008 Outlook

Capital

Support growth & monitor capital

markets

Strong available capital position

$300-$400 million of repurchase

Earnings

L&A, GP continued strength in

fundamentals

“Headwinds” in DC & Inv. Mgt. with

plans in place

Markets?

Production

Retail momentum continues

Institutional - investment mode

Invest in retirement income

Financial Plan Roll-Forward

Appendix

Net Income

Less:

Net realized gains (losses) on investments

and derivatives

Net gain on reinsurance derivative/trading

account securities

Reserve development and related amortization

on business sold through reinsurance

Income from Operations

Earnings per share (diluted)

Net Income

Income from Operations

Average Equity

(Excluding accumulated other comprehensive income)

Return on Equity

Net Income

Income from Operations

($ in millions, except per share data)

For the Quarter Ended

September 30,

$329.60

-23.2

-0.5

0.4

$352.90

$1.21

$1.29

$11,726.30

11.20%

12.00%

$364.10

-4.1

-3.1

0.2

$371.10

$1.29

$1.31

$11,437.90

12.70%

13.00%

2007

2006

Net Income to Operating Earnings

Reconciliation

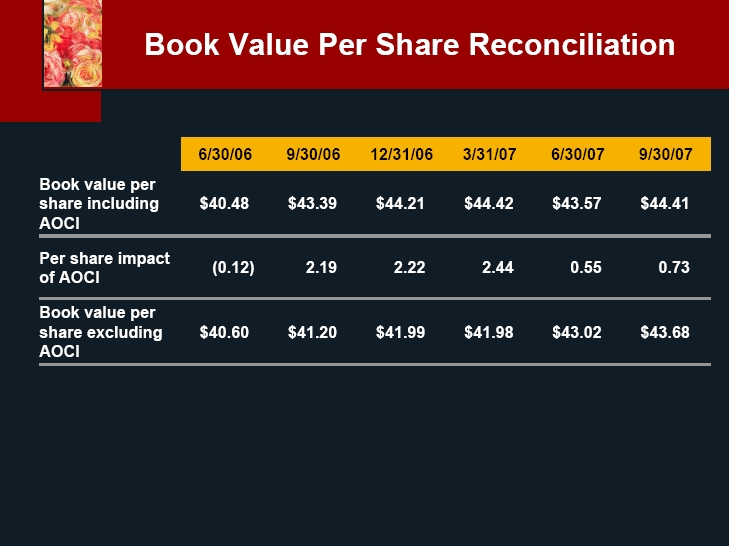

Book Value Per Share Reconciliation 6/30/06 9/30/06 12/31/06 3/31/07 6/30/07 9/30/07 Book value per share including AOCI $40.48 $43.39 $44.21 $44.42 $43.57 $44.41 Per share impact of AOCI (0.12) 2.19 2.22 2.44 0.5 50.73 Book value per share excluding AOCI $40.60 $41.20 $41.99 $41.98 $43.02 $43.68