UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act File Number: 811-02145

LORD ABBETT BOND-DEBENTURE FUND, INC.

(Exact name of Registrant as specified in charter)

90 Hudson Street, Jersey City, NJ 07302

(Address of principal executive offices) (Zip code)

John T. Fitzgerald, Esq., Vice President & Assistant Secretary

90 Hudson Street, Jersey City, NJ 07302

(Name and address of agent for service)

Registrant’s telephone number, including area code:(800) 201-6984

Date of fiscal year end: 12/31

Date of reporting period: 12/31/2018

| Item 1: | Report(s) to Shareholders. |

LORD ABBETT

ANNUAL REPORT

Lord Abbett

Bond Debenture Fund

For the fiscal year ended December 31, 2018

Important Information on Paperless Delivery

Beginning in February 2021, as permitted by regulations adopted by the Securities and Exchange Commission, paper copies of the Fund’s shareholder reports like this one will no longer be sent by mail, unless you specifically request paper copies of the reports from the Fund or from your financial intermediary, such as a broker-dealer, investment advisor or bank. Instead, the reports will be made available on Lord Abbett’s website and you will be notified by mail each time a report is posted and provided with a website link to access the report.

If you already elected to receive shareholder reports electronically, you will not be affected by this change and you need not take any action. Shareholders who hold accounts directly with the Fund may elect to receive shareholder reports and other communications from the Fund electronically by signing into your Lord Abbett online account at lordabbett.com and selecting “Log In.” For further information, you may also contact the Fund at (800) 821-5129. Shareholders who hold accounts through a financial intermediary should contact them directly.

You may elect to receive all future reports in paper free of charge by contacting the Fund at (800) 821-5129. Your election to receive reports in paper will apply to all funds held with Lord Abbett. If your fund shares are held through a financial intermediary please contact them directly. Your election applies to all funds held with that intermediary.

Table of Contents

Lord Abbett Bond Debenture Fund

Annual Report

For the fiscal year ended December 31, 2018

From left to right: James L.L. Tullis, Independent Chairman of the Lord Abbett Funds and Douglas B. Sieg, Director, President, and Chief Executive Officer of the Lord Abbett Funds.

Dear Shareholders:We are pleased to provide you with this overview of the performance of Lord Abbett Bond Debenture Fund for the fiscal year ended December 31, 2018. On this page and the following pages, we discuss the major factors that influenced fiscal year performance. For detailed and more timely information about the Fund, please visit our website at www.lordabbett.com, where you also can access quarterly commentaries that provide updates on the Fund’s performance and other portfolio related updates.

Thank you for investing in Lord Abbett mutual funds. We value the trust that you place in us and look forward to serving your investment needs in the years to come.

Best regards,

Douglas B. Sieg

Director, President and Chief Executive Officer

For the fiscal year ended December 31, 2018, the Fund returned -3.79%, reflecting performance at the net asset value (NAV) of Class A shares with all distributions reinvested, compared to its benchmark, the Bloomberg Barclays U.S. Aggregate Bond Index,1which returned 0.01% over the same period.

During the period, there were several market-moving events. In June 2018, the White House announced its intent to impose additional tariffs on $200 billion worth of Chinese goods, on top of the $50

billion previously announced. The aggressive U.S. trade posture continued into September with trade tensions mounting between the U.S. and China. While the impact has yet to fully be realized, many corporations anticipate that the retaliatory tariffs will weigh on profits. In 2018, the Fed raised its target for short-term interest rates by 0.25% at each of its March, June, September and December meetings, raising the target range to 2.25%-2.50%. As the Fed continued to raise rates, the U.S. Treasury yield curve

1

flattened throughout the year. The yield on 10-year U.S. Treasury securities (“Treasuries”) reached multi-year highs in November, and pulled back in December as risk averse sentiment roiled the markets and investors to flocked to safety. Amid rising concerns surrounding escalating trade tensions, slowing global growth, and increasing interest rates, the Nasdaq experienced the largest monthly drop since 2008 in October 2018. US equity markets were volatile to finish out the year, with the S&P 500® Index2suffering the largest December decline since the Great Depression, culminating in the worst year since the financial crisis. Additionally, leveraged credit segments of the market experienced a sharp sell-off, notably in December, due to concerns over slower growth, falling oil prices, year-end technical pressures and general risk averse sentiment. Despite the sell-off, the U.S. economy continued to expand by more than 2% during each quarter of the trailing 12-month period, with domestic GDP growth ranging between 2.2% to 4.2% from the third quarter of 2017 to the third quarter of 2018. The 4.2% GDP growth in the second quarter marked the strongest growth rate since the third quarter of 2014. Inflation, as measured by the Consumer Price Index (CPI), gained 1.9%, a decline of 0.1% year-over-year, mainly driven lower by falling energy prices. Oil prices suffered sharp declines due to oversupply concerns.

During the 12-month period the leveraged credit sectors of the U.S. fixed income market, including high yield bonds and loans, experienced mixed returns, with high yield bonds underperforming and bank loans outperforming investment grade bonds. High yield credit spreads widened during the period, most notably in December, as the fourth quarter risk averse sentiment took a toll on risk assets. Returns within the high yield market were driven lower primarily by the lower-rated issues, as ‘CCC’ rated bonds underperformed higher-rated issues over the 12-month period.

As it has in the past, the Fund maintained a significant allocation to high yield bonds, as we remained positive on the high yield market from a fundamental perspective. The Fund’s exposure to high yield bonds detracted from relative performance, as the high yield market significantly underperformed investment grade bonds, as represented by the Fund’s benchmark the Bloomberg Barclays US Aggregate Bond Index1.

The Fund maintained an allocation to equities throughout the period, which also detracted from relative performance, as the asset class came under pressure during the year, most notably in the fourth quarter, as general risk averse sentiment caused a broad-based sell-off.

The Fund’s modest allocation to bank loans contributed to relative performance during the period. Despite volatility late in the year, the asset class performed relatively well in relation to other risk assets.

2

The Fund’s portfolio is actively managed and, therefore, its holdings and the weightings of a particular issuer or

particular sector as a percentage of portfolio assets are subject to change. Sectors may include many industries.

1 The Bloomberg Barclays U.S. Aggregate Bond Index is an index of U.S dollar-denominated, investment-grade U.S. government and corporate securities, and mortgage pass-through securities, and asset-backed securities. Indexes are unmanaged, do not reflect the deduction of fees or expenses, and an investor cannot invest directly in an index.

2 The S&P 500®Index is widely regarded as the standard for measuring large cap U.S. stock market performance and includes a representative sample of leading companies in leading industries.

Unless otherwise specified, indexes reflect total return, with all dividends reinvested. Indexes are unmanaged, do not reflect the deduction of fees or expenses, and are not available for direct investment.

Important Performance and Other Information

Performance data quoted in the following pages reflect past performance and are no guarantee of future results. Current performance may be higher or lower than the performance quoted. The investment return and principal value of an investment in the Fund will fluctuate so that shares, on any given day or when redeemed, may be worth more or less than their original cost. You

can obtain performance data current to the most recent month end by calling Lord Abbett at 888-522-2388 or referring to www.lordabbett.com.

The annual commentary above discusses the views of the Fund’s management and various portfolio holdings of the Fund as of December 31, 2018. These views and portfolio holdings may have changed after this date. Information provided in the commentary is not a recommendation to buy or sell securities. Because the Fund’s portfolio is actively managed and may change significantly, the Fund may no longer own the securities described above or may have otherwise changed its position in the securities. For more recent information about the Fund’s portfolio holdings, please visit www.lordabbett.com.

A Note about Risk:See Notes to Financial Statements for a discussion of investment risks. For a more detailed discussion of the risks associated with the Fund, please see the Fund’s prospectus.

Mutual funds are not insured by the FDIC, are not deposits or other obligations of, or guaranteed by, banks, and are subject to investment risks including possible loss of principal amount invested.

3

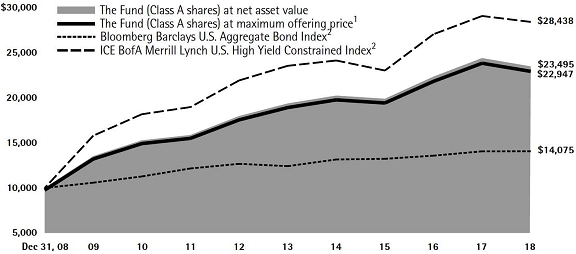

Investment Comparison

Below is a comparison of a $10,000 investment in Class A shares with the same investment in the Bloomberg Barclays U.S. Aggregate Bond Index and the ICE BofA Merrill Lynch U.S. High Yield Constrained Index, assuming reinvestment of all dividends and distributions. The performance of other classes will be greater than or less than the performance shown in the graph below due to different sales loads and expenses applicable to such classes. The graph and performance table below do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.Past performance is no guarantee of future results.

Average Annual Total Returns at Maximum Applicable

Sales Charge for the Periods Ended December 31, 2018

| | | 1 Year | | 5 Years | | | 10 Years | | | Life of Class | |

| Class A3 | | | –5.95% | | | 3.45% | | | | 8.66% | | | | – | |

| Class C4 | | | –5.28% | | | 3.28% | | | | 8.23% | | | | – | |

| Class F5 | | | –3.83% | | | 4.00% | | | | 9.10% | | | | – | |

| Class F36 | | | –3.57% | | | – | | | | – | | | | 1.56% | |

| Class I5 | | | –3.77% | | | 4.10% | | | | 9.21% | | | | – | |

| Class P5 | | | –4.00% | | | 3.85% | | | | 8.88% | | | | – | |

| Class R25 | | | –4.17% | | | 3.52% | | | | 8.59% | | | | – | |

| Class R35 | | | –4.21% | | | 3.60% | | | | 8.69% | | | | – | |

| Class R47 | | | –3.83% | | | – | | | | – | | | | 3.41% | |

| Class R57 | | | –3.63% | | | – | | | | – | | | | 3.66% | |

| Class R67 | | | –3.56% | | | – | | | | – | | | | 3.74% | |

1 Reflects the deduction of the maximum initial sales charge of 2.25%.

2 Performance of each unmanaged index does not reflect any fees or expenses. The performance of each index is not necessarily representative of the Fund’s performance.

3 Total return, which is the percentage change in net asset value, after deduction of the maximum initial sales charge of 2.25% applicable to Class A shares, with all dividends and distributions reinvested for the periods shown ended December 31, 2018 is calculated using the SEC-required uniform method to compute such return.

4 The 1% CDSC for Class C shares normally applies before the first anniversary of the purchase date. Performance for other periods is at net asset value.

5 Performance is at net asset value.

6 Commenced operations and performance for the Class began on April 4, 2017. Performance is at net asset value.

7 Commenced operations and performance for the Class began on June 30, 2015. Performance is at net asset value.

4

Expense Example

As a shareholder of the Fund, you incur two types of costs: (1) transaction costs, including sales charges (loads) on purchase payments (these charges vary among the share classes); and (2) ongoing costs, including management fees; distribution and service (12b-1) fees (these charges vary among the share classes); and other Fund expenses. This Example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The Example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period (July 1, 2018 through December 31, 2018).

Actual Expenses

For each class of the Fund, the first line of the table on the following page provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading titled “Expenses Paid During Period 7/1/18 – 12/31/18” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

For each class of the Fund, the second line of the table on the following page provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

| | See Notes to Financial Statements. | 5 |

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads). Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| | | Beginning

Account

Value | | Ending

Account

Value | | Expenses

Paid During

Period† |

| | | 7/1/18 | | 12/31/18 | | 7/1/18 – 12/31/18 |

| Class A | | | | | | |

| Actual | | $ | 1,000.00 | | | $ | 973.50 | | | $ | 3.98 | |

| Hypothetical (5% Return Before Expenses) | | $ | 1,000.00 | | | $ | 1,021.17 | | | $ | 4.08 | |

| Class C | | | | | | | | | | | | |

| Actual | | $ | 1,000.00 | | | $ | 969.20 | | | $ | 7.15 | |

| Hypothetical (5% Return Before Expenses) | | $ | 1,000.00 | | | $ | 1,017.95 | | | $ | 7.32 | |

| Class F | | | | | | | | | | | | |

| Actual | | $ | 1,000.00 | | | $ | 972.60 | | | $ | 3.48 | |

| Hypothetical (5% Return Before Expenses) | | $ | 1,000.00 | | | $ | 1,021.68 | | | $ | 3.57 | |

| Class F3 | | | | | | | | | | | | |

| Actual | | $ | 1,000.00 | | | $ | 973.30 | | | $ | 2.59 | |

| Hypothetical (5% Return Before Expenses) | | $ | 1,000.00 | | | $ | 1,022.58 | | | $ | 2.65 | |

| Class I | | | | | | | | | | | | |

| Actual | | $ | 1,000.00 | | | $ | 972.90 | | | $ | 2.98 | |

| Hypothetical (5% Return Before Expenses) | | $ | 1,000.00 | | | $ | 1,022.18 | | | $ | 3.06 | |

| Class P | | | | | | | | | | | | |

| Actual | | $ | 1,000.00 | | | $ | 970.90 | | | $ | 4.72 | |

| Hypothetical (5% Return Before Expenses) | | $ | 1,000.00 | | | $ | 1,019.91 | | | $ | 4.84 | |

| Class R2 | | | | | | | | | | | | |

| Actual | | $ | 1,000.00 | | | $ | 970.30 | | | $ | 5.96 | |

| Hypothetical (5% Return Before Expenses) | | $ | 1,000.00 | | | $ | 1,019.16 | | | $ | 6.11 | |

| Class R3 | | | | | | | | | | | | |

| Actual | | $ | 1,000.00 | | | $ | 970.70 | | | $ | 5.46 | |

| Hypothetical (5% Return Before Expenses) | | $ | 1,000.00 | | | $ | 1,019.66 | | | $ | 5.60 | |

| Class R4 | | | | | | | | | | | | |

| Actual | | $ | 1,000.00 | | | $ | 972.00 | | | $ | 4.22 | |

| Hypothetical (5% Return Before Expenses) | | $ | 1,000.00 | | | $ | 1,020.92 | | | $ | 4.33 | |

| Class R5 | | | | | | | | | | | | |

| Actual | | $ | 1,000.00 | | | $ | 973.00 | | | $ | 2.98 | |

| Hypothetical (5% Return Before Expenses) | | $ | 1,000.00 | | | $ | 1,022.18 | | | $ | 3.06 | |

| Class R6 | | | | | | | | | | | | |

| Actual | | $ | 1,000.00 | | | $ | 973.30 | | | $ | 2.59 | |

| Hypothetical (5% Return Before Expenses) | | $ | 1,000.00 | | | $ | 1,022.58 | | | $ | 2.65 | |

| † | For each class of the Fund, net expenses are equal to the annualized expense ratio for such class (0.80% for Class A, 1.44% for Class C, 0.70% for Class F, 0.52% for Class F3, 0.60% for Class I, 0.95% for Class P, 1.20% for Class R2, 1.10% for Class R3, 0.85% for Class R4, 0.60% for Class R5 and 0.52% for Class R6) multiplied by the average account value over the period, multiplied by 184/365 (to reflect one-half year period). |

| 6 | See Notes to Financial Statements. |

Portfolio Holdings Presented by Sector

December 31, 2018

| Sector* | | | %** | |

| Asset Backed | | | 1.23 | % |

| Automotive | | | 1.05 | % |

| Banking | | | 4.38 | % |

| Basic Industry | | | 5.12 | % |

| Capital Goods | | | 3.01 | % |

| Consumer Goods | | | 5.03 | % |

| Energy | | | 7.80 | % |

| Financial Services | | | 3.64 | % |

| Foreign Government | | | 6.50 | % |

| Healthcare | | | 8.59 | % |

| Insurance | | | 1.94 | % |

| Leisure | | | 3.67 | % |

| Media | | | 4.04 | % |

| Municipal | | | 3.54 | % |

| Real Estate | | | 1.18 | % |

| Retail | | | 7.69 | % |

| Services | | | 3.08 | % |

| Technology & Electronics | | | 5.64 | % |

| Telecommunications | | | 4.33 | % |

| Transportation | | | 3.04 | % |

| U.S. Government | | | 10.13 | % |

| Utility | | | 5.21 | % |

| Repurchase Agreement | | | 0.16 | % |

| Total | | | 100.00 | % |

| * | | A sector may comprise several industries. |

| ** | | Represents percent of total investments. |

| | See Notes to Financial Statements. | 7 |

Schedule of Investments

December 31, 2018

| Investments | | Interest

Rate | | Maturity

Date | | Principal

Amount

(000) | | | Fair

Value | |

| LONG-TERM INVESTMENTS 108.56% | | | | | | | | | | | | |

| | | | | | | | | | | | | |

| ASSET-BACKED SECURITIES 2.68% | | | | | | | | | | | | |

| | | | | | | | | | | | | |

| Automobiles 0.17% | | | | | | | | | | | | |

| ACC Trust 2018-1 B† | | 4.82% | | 5/20/2021 | | $ | 6,637 | | | $ | 6,656,851 | |

| ACC Trust 2018-1 C† | | 6.81% | | 2/21/2023 | | | 5,140 | | | | 5,160,437 | |

| TCF Auto Receivables Owner Trust 2016-1A B† | | 2.32% | | 6/15/2022 | | | 8,695 | | | | 8,556,775 | |

| Westlake Automobile Receivables Trust 2016-3A B† | | 2.07% | | 12/15/2021 | | | 416 | | | | 416,128 | |

| Total | | | | | | | | | | | 20,790,191 | |

| | | | | | | | | | | | | |

| Other 2.51% | | | | | | | | | | | | |

| ALM XIX Ltd. 2016-19A C† | | 6.786%

(3 Mo. LIBOR + 4.35% | )# | 7/15/2028 | | | 4,038 | | | | 4,045,420 | |

| AMMC CLO 15 Ltd. 2014-15A DRR† | | 5.727%

(3 Mo. LIBOR + 3.40% | )# | 1/15/2032 | | | 2,514 | | | | 2,454,889 | |

| AMMC CLO XII Ltd. 2013-12A DR† | | 5.318%

(3 Mo. LIBOR + 2.70% | )# | 11/10/2030 | | | 3,859 | | | | 3,515,593 | |

| Anchorage Capital CLO 9 Ltd. 2016-9A D† | | 6.436%

(3 Mo. LIBOR + 4.00% | )# | 1/15/2029 | | | 9,600 | | | | 9,469,286 | |

| Ascentium Equipment Receivables Trust 2016-2A B† | | 2.50% | | 9/12/2022 | | | 3,705 | | | | 3,684,796 | |

| Atrium XV-15A D† | | 5.776%

(3 Mo. LIBOR + 3.00% | )# | 1/23/2031 | | | 7,286 | | | | 6,802,358 | |

| Battalion CLO VII Ltd. 2014-7A CRR† | | 5.379%

(3 Mo. LIBOR + 2.93% | )# | 7/17/2028 | | | 1,831 | | | | 1,778,711 | |

| BlueMountain CLO XXIII Ltd. 2018-23A D† | | 5.365%

(3 Mo. LIBOR + 2.90% | )# | 10/20/2031 | | | 4,348 | | | | 4,076,922 | |

| Cedar Funding VI CLO Ltd. 2016-6A BR† | | 4.069%

(3 Mo. LIBOR + 1.60% | )# | 10/20/2028 | | | 2,600 | | | | 2,536,483 | |

| Cedar Funding VI CLO Ltd. 2016-6A DR† | | 5.469%

(3 Mo. LIBOR + 3.00% | )# | 10/20/2028 | | | 7,699 | | | | 7,211,757 | |

| Cent CLO 21 Ltd. 2014-21A CR2† | | 5.709%

(3 Mo. LIBOR + 3.20% | )# | 7/27/2030 | | | 4,936 | | | | 4,605,472 | |

| Conn’s Receivables Funding LLC 2017-B C† | | 5.95% | | 11/15/2022 | | | 23,832 | | | | 24,214,084 | |

| Galaxy XXI CLO Ltd. 2015-21A AR† | | 3.489%

(3 Mo. LIBOR + 1.02% | )# | 4/20/2031 | | | 5,311 | | | | 5,241,542 | |

| Halcyon Loan Advisors Funding Ltd. 2015-2A CR† | | 4.64%

(3 Mo. LIBOR + 2.15% | )# | 7/25/2027 | | | 5,476 | | | | 5,312,989 | |

| Harbor Park CLO 18-1 Ltd. 2018-1A D† | | 5.739%

(3 Mo. LIBOR + 2.90% | )# | 1/20/2031 | | | 4,560 | | | | 4,221,251 | |

| Hardee’s Funding LLC 2018-1A A2II† | | 4.959% | | 6/20/2048 | | | 38,186 | | | | 38,938,565 | |

| Jamestown CLO VII Ltd. 2015-7A BR† | | 4.14%

(3 Mo. LIBOR + 1.65% | )# | 7/25/2027 | | | 12,548 | | | | 11,893,323 | |

| KKR CLO 15 Ltd-15 DR† | | 5.592%

(3 Mo. LIBOR + 3.15% | )# | 1/18/2032 | | | 2,736 | | | | 2,615,473 | |

| 8 | See Notes to Financial Statements. | |

Schedule of Investments (continued)

December 31, 2018

| Investments | | Interest

Rate | | Maturity

Date | | Principal

Amount

(000) | | | Fair

Value | |

| Other (continued) | | | | | | | | | | | | |

| Madison Park Funding XIV Ltd. 2014-14A DRR† | | 5.419%

(3 Mo. LIBOR + 2.95% | )# | 10/22/2030 | | $ | 3,923 | | | $ | 3,693,748 | |

| Mariner CLO 2015-1 LLC 2015-1A DR† | | 6.119%

(3 Mo. LIBOR + 3.65% | )# | 4/20/2029 | | | 2,277 | | | | 2,218,896 | |

| Mariner CLO LLC 2017-4A D† | | 5.558%

(3 Mo. LIBOR + 3.05% | )# | 10/26/2029 | | | 6,254 | | | | 5,912,035 | |

| Mountain View CLO X Ltd. 2015-10A BR† | | 3.786%

(3 Mo. LIBOR + 1.35% | )# | 10/13/2027 | | | 13,725 | | | | 13,430,516 | |

| Octagon Investment Partners 39 Ltd. 2018-3A D† | | 5.415%

(3 Mo. LIBOR + 2.95% | )# | 10/20/2030 | | $ | 3,789 | | | $ | 3,566,070 | |

| Palmer Square Loan Funding Ltd. 2018-1A A1† | | 3.036%

(3 Mo. LIBOR + .60% | )# | 4/15/2026 | | | 25,600 | | | | 25,445,768 | |

| Palmer Square Loan Funding Ltd. 2018-1A A2† | | 3.486%

(3 Mo. LIBOR + 1.05% | )# | 4/15/2026 | | | 9,660 | | | | 9,250,845 | |

| Palmer Square Loan Funding Ltd. 2018-1A B† | | 3.836%

(3 Mo. LIBOR + 1.40% | )# | 4/15/2026 | | | 5,069 | | | | 4,745,568 | |

| Planet Fitness Master Issuer LLC 2018-1A A2I† | | 4.262% | | 9/5/2048 | | | 17,994 | | | | 18,111,901 | |

| Planet Fitness Master Issuer LLC 2018-1A A2II† | | 4.666% | | 9/5/2048 | | | 22,493 | | | | 22,821,515 | |

| Regatta VI Funding Ltd. 2016-1A DR† | | 5.169%

(3 Mo. LIBOR + 2.70% | )# | 7/20/2028 | | | 2,216 | | | | 2,086,252 | |

| Sound Point CLO XI Ltd. 2016-1A DR† | | 5.408%

(3 Mo. LIBOR + 2.95% | )# | 7/20/2028 | | | 6,840 | | | | 6,684,850 | |

| THL Credit Wind River CLO Ltd. 2018-3A D† | | 5.776%

(3 Mo. LIBOR + 2.95% | )# | 1/20/2031 | | | 7,164 | | | | 6,658,883 | |

| Voya CLO Ltd. 2016-2A C† | | 6.70%

(3 Mo. LIBOR + 4.25% | )# | 7/19/2028 | | | 5,250 | | | | 5,251,807 | |

| West CLO Ltd. 2014-2A BR† | | 4.186%

(3 Mo. LIBOR + 1.75% | )# | 1/16/2027 | | | 4,541 | | | | 4,420,961 | |

| Westcott Park CLO Ltd. 2016-1A D† | | 6.819%

(3 Mo. LIBOR + 4.35% | )# | 7/20/2028 | | | 8,150 | | | | 8,161,774 | |

| Wingstop Funding LLC 2018-1 A2† | | 4.97% | | 12/5/2048 | | | 19,747 | | | | 20,218,953 | |

| Total | | | | | | | | | | | 305,299,256 | |

| Total Asset-Backed Securities (cost $330,207,336) | | | | | | | | | | | 326,089,447 | |

| | | | | | | | | | | | | |

| | | | | | | Shares

(000) | | | | | |

| COMMON STOCKS 9.37% | | | | | | | | | | | | |

| | | | | | | | | | | | | |

| Aerospace/Defense 0.11% | | | | | | | | | | | | |

| HEICO Corp. | | | | | | | 170 | | | | 13,197,633 | |

| | | | | | | | | | | | | |

| Air Transportation 0.26% | | | | | | | | | | | | |

| Alaska Air Group, Inc. | | | | | | | 318 | | | | 19,346,527 | |

| Spirit Airlines, Inc.* | | | | | | | 217 | | | | 12,581,672 | |

| Total | | | | | | | | | | | 31,928,199 | |

| | See Notes to Financial Statements. | 9 |

Schedule of Investments (continued)

December 31, 2018

| Investments | | | | | | Shares

(000) | | | Fair

Value | |

| Auto Parts & Equipment 0.13% | | | | | | | | | | | | |

| Chassix Holdings, Inc. | | | | | | | 607 | | | $ | 15,176,425 | |

| | | | | | | | | | | | | |

| Banking 0.35% | | | | | | | | | | | | |

| American Express Co. | | | | | | | 249 | | | | 23,735,442 | |

| Western Alliance Bancorp* | | | | | | | 478 | | | | 18,863,544 | |

| Total | | | | | | | | | | | 42,598,986 | |

| | | | | | | | | | | | | |

| Beverages 0.10% | | | | | | | | | | | | |

| Pernod Ricard SA(a) | | | | | | EUR | 77 | | | | 12,577,204 | |

| | | | | | | | | | | | | |

| Building & Construction 0.10% | | | | | | | | | | | | |

| PulteGroup, Inc. | | | | | | | 478 | | | | 12,427,898 | |

| | | | | | | | | | | | | |

| Building Materials 0.21% | | | | | | | | | | | | |

| RPM International, Inc. | | | | | | | 210 | | | | 12,347,091 | |

| Vulcan Materials Co. | | | | | | | 134 | | | | 13,252,143 | |

| Total | | | | | | | | | | | 25,599,234 | |

| | | | | | | | | | | | | |

| Chemicals 0.10% | | | | | | | | | | | | |

| Ecolab, Inc. | | | | | | | 85 | | | | 12,473,030 | |

| | | | | | | | | | | | | |

| Discount Stores 0.12% | | | | | | | | | | | | |

| Amazon.com, Inc.* | | | | | | | 10 | | | | 14,893,535 | |

| | | | | | | | | | | | | |

| Diversified Capital Goods 0.11% | | | | | | | | | | | | |

| Dover Corp. | | | | | | | 183 | | | | 13,015,423 | |

| | | | | | | | | | | | | |

| Electric: Generation 0.10% | | | | | | | | | | | | |

| AES Corp. | | | | | | | 878 | | | | 12,691,976 | |

| | | | | | | | | | | | | |

| Electric: Integrated 0.52% | | | | | | | | | | | | |

| Ameren Corp. | | | | | | | 276 | | | | 18,007,263 | |

| Eneva SA*(a) | | | | | | BRL | 33 | | | | 117,832 | |

| OGE Energy Corp. | | | | | | | 628 | | | | 24,598,309 | |

| Portland General Electric Co. | | | | | | | 438 | | | | 20,073,267 | |

| Total | | | | | | | | | | | 62,796,671 | |

| | | | | | | | | | | | | |

| Electronics 0.17% | | | | | | | | | | | | |

| Zebra Technologies Corp. Class A* | | | | | | | 128 | | | | 20,398,955 | |

| | | | | | | | | | | | | |

| Energy: Exploration & Production 0.17% | | | | | | | | | | | | |

| Chaparral Energy, Inc. Class A* | | | | | | | 541 | | | | 2,662,350 | |

| MEG Energy Corp.*(a) | | | | | | CAD | 3,213 | | | | 18,143,050 | |

| Templar Energy LLC Class A Units | | | | | | | 417 | | | | 260,514 | |

| Total | | | | | | | | | | | 21,065,914 | |

| 10 | See Notes to Financial Statements. | |

Schedule of Investments (continued)

December 31, 2018

| Investments | | | | | | Shares

(000) | | | Fair

Value | |

| Food & Drug Retailers 0.16% | | | | | | | | | | |

| Kroger Co. (The) | | | | | | | 688 | | | $ | 18,926,298 | |

| | | | | | | | | | | | | |

| Food: Wholesale 0.35% | | | | | | | | | | | | |

| Lamb Weston Holdings, Inc. | | | | | | | 257 | | | | 18,940,155 | |

| McCormick & Co., Inc. | | | | | | | 172 | | | | 24,006,647 | |

| Total | | | | | | | | | | | 42,946,802 | |

| | | | | | | | | | | | | |

| Gas Distribution 0.15% | | | | | | | | | | | | |

| Dommo Energia SA*(a) | | | | | | BRL | 3,526 | | | | 757,898 | |

| ONE Gas, Inc. | | | | | | | 226 | | | | 18,024,385 | |

| Total | | | | | | | | | | | 18,782,283 | |

| | | | | | | | | | | | | |

| Health Facilities 0.25% | | | | | | | | | | | | |

| HCA Healthcare, Inc. | | | | | | | 242 | | | | 30,108,189 | |

| | | | | | | | | | | | | |

| Health Services 0.10% | | | | | | | | | | | | |

| PRA Health Sciences, Inc.* | | | | | | | 132 | | | | 12,162,446 | |

| | | | | | | | | | | | | |

| Insurance Brokerage 0.16% | | | | | | | | | | | | |

| Aon plc (United Kingdom)(b) | | | | | | | 133 | | | | 19,361,807 | |

| | | | | | | | | | | | | |

| Investments & Miscellaneous Financial Services 0.69% | | | | | | | | |

| Arthur J Gallagher & Co. | | | | | | | 342 | | | | 25,170,466 | |

| BlackRock, Inc. | | | | | | | 33 | | | | 13,002,342 | |

| CME Group, Inc. | | | | | | | 110 | | | | 20,738,349 | |

| FactSet Research Systems, Inc. | | | | | | | 65 | | | | 12,954,215 | |

| Thomson Reuters Corp. (Canada)(b) | | | | | | | 259 | | | | 12,515,623 | |

| Total | | | | | | | | | | | 84,380,995 | |

| | | | | | | | | | | | | |

| Machinery 0.11% | | | | | | | | | | | | |

| Roper Technologies, Inc. | | | | | | | 48 | | | | 12,766,841 | |

| | | | | | | | | | | | | |

| Media: Content 0.13% | | | | | | | | | | | | |

| AMC Networks, Inc. Class A* | | | | | | | 242 | | | | 13,304,613 | |

| ION Media Networks, Inc. | | | | | | | 4 | | | | 2,651,730 | (c) |

| Total | | | | | | | | | | | 15,956,343 | |

| | | | | | | | | | | | | |

| Media: Diversified 0.16% | | | | | | | | | | | | |

| Walt Disney Co. (The) | | | | | | | 182 | | | | 20,003,450 | |

| | | | | | | | | | | | | |

| Medical Products 0.16% | | | | | | | | | | | | |

| Edwards Lifesciences Corp.* | | | | | | | 127 | | | | 19,404,035 | |

| | See Notes to Financial Statements. | 11 |

Schedule of Investments (continued)

December 31, 2018

| Investments | | | | | | Shares

(000) | | | Fair

Value | |

| Packaging 0.20% | | | | | | | | | | | | |

| AptarGroup, Inc. | | | | | | | 265 | | | $ | 24,888,288 | |

| | | | | | | | | | | | | |

| Personal & Household Products 0.33% | | | | | | | | | | | | |

| Church & Dwight Co., Inc. | | | | | | | 226 | | | | 14,849,200 | |

| Gibson Brands, Inc. | | | | | | | 105 | | | | 10,527,700 | (d) |

| Procter & Gamble Co. (The) | | | | | | | 139 | | | | 12,811,809 | |

| Remington Outdoor Co., Inc.* | | | | | | | 164 | | | | 1,596,543 | |

| Total | | | | | | | | | | | 39,785,252 | |

| | | | | | | | | | | | | |

| Pharmaceuticals 0.36% | | | | | | | | | | | | |

| Amgen, Inc. | | | | | | | 67 | | | | 12,998,700 | |

| Canopy Growth Corp.*(a) | | | | | | CAD | 409 | | | | 10,974,204 | |

| Eli Lilly & Co. | | | | | | | 166 | | | | 19,196,212 | |

| Total | | | | | | | | | | | 43,169,116 | |

| | | | | | | | | | | | | |

| Real Estate Investment Trusts 0.26% | | | | | | | | | | | | |

| Americold Realty Trust | | | | | | | 733 | | | | 18,713,158 | |

| Medical Properties Trust, Inc. | | | | | | | 829 | | | | 13,337,427 | |

| Total | | | | | | | | | | | 32,050,585 | |

| | | | | | | | | | | | | |

| Restaurants 0.40% | | | | | | | | | | | | |

| Shake Shack, Inc. Class A* | | | | | | | 663 | | | | 30,122,272 | |

| Texas Roadhouse, Inc. | | | | | | | 320 | | | | 19,079,463 | |

| Total | | | | | | | | | | | 49,201,735 | |

| | | | | | | | | | | | | |

| Software/Services 0.77% | | | | | | | | | | | | |

| Atlassian Corp. plc Class A (Australia)*(b) | | | | | | | 388 | | | | 34,514,363 | |

| MongoDB, Inc.* | | | | | | | 172 | | | | 14,363,252 | |

| Tableau Software, Inc. Class A* | | | | | | | 164 | | | | 19,735,800 | |

| Trade Desk, Inc. (The) Class A* | | | | | | | 211 | | | | 24,481,929 | |

| Total | | | | | | | | | | | 93,095,344 | |

| | | | | | | | | | | | | |

| Specialty Retail 1.19% | | | | | | | | | | | | |

| Claires Holdings LLC | | | | | | | 15 | | | | 12,700,162 | |

| Columbia Sportswear Co. | | | | | | | 302 | | | | 25,415,194 | |

| Deckers Outdoor Corp.* | | | | | | | 256 | | | | 32,737,415 | |

| Etsy, Inc.* | | | | | | | 316 | | | | 15,053,003 | |

| Lululemon Athletica, Inc. (Canada)*(b) | | | | | | | 160 | | | | 19,398,011 | |

| NIKE, Inc. Class B | | | | | | | 358 | | | | 26,574,000 | |

| Ollie’s Bargain Outlet Holdings, Inc.* | | | | | | | 191 | | | | 12,688,179 | |

| Total | | | | | | | | | | | 144,565,964 | |

| 12 | See Notes to Financial Statements. | |

Schedule of Investments (continued)

December 31, 2018

| Investments | | | | | | Shares

(000) | | | Fair

Value | |

| Support: Services 0.26% | | | | | | | | | | | | |

| Bright Horizons Family Solutions, Inc.* | | | | | | | 174 | | | $ | 19,359,534 | |

| TripAdvisor, Inc.* | | | | | | | 234 | | | | 12,605,778 | |

| Total | | | | | | | | | | | 31,965,312 | |

| | | | | | | | | | | | | |

| Technology Hardware & Equipment 0.11% | | | | | | | | | | | | |

| Cisco Systems, Inc. | | | | | | | 298 | | | | 12,924,689 | |

| | | | | | | | | | | | | |

| Telecommunications: Wireless 0.25% | | | | | | | | | | | | |

| American Tower Corp. | | | | | | | 196 | | | | 30,955,094 | |

| | | | | | | | | | | | | |

| Theaters & Entertainment 0.27% | | | | | | | | | | | | |

| Live Nation Entertainment, Inc.* | | | | | | | 396 | | | | 19,515,460 | |

| Tencent Music Entertainment Group ADR* | | | | | | | 989 | | | | 13,072,624 | |

| Total | | | | | | | | | | | 32,588,084 | |

| Total Common Stocks (cost $1,207,813,193) | | | | | | | | | | | 1,140,830,035 | |

| | | | | | | | | | | | | |

| | | Interest

Rate | | Maturity

Date | | Principal

Amount

(000) | | | | | |

| CONVERTIBLE BONDS 0.49% | | | | | | | | | | | | |

| | | | | | | | | | | | | |

| Automakers 0.16% | | | | | | | | | | | | |

| Tesla, Inc. | | 1.25% | | 3/1/2021 | | $ | 17,223 | | | | 19,389,843 | |

| | | | | | | | | | | | | |

| Software/Services 0.33% | | | | | | | | | | | | |

| Twilio, Inc.† | | 0.25% | | 6/1/2023 | | | 14,414 | | | | 20,612,467 | |

| Weibo Corp. (China)†(b) | | 1.25% | | 11/15/2022 | | | 21,409 | | | | 19,559,904 | |

| Total | | | | | | | | | | | 40,172,371 | |

| Total Convertible Bonds (cost $59,167,563) | | | | | | | | | | | 59,562,214 | |

| | | | | | | | | | | | | |

| FLOATING RATE LOANS(e)6.61% | | | | | | | | | | | | |

| | | | | | | | | | | | | |

| Air Transportation 0.21% | | | | | | | | | | | | |

| American Airlines, Inc. 2018 Replacement Term Loan | 4.256%

(1 Mo. LIBOR + 1.75% | ) | 6/27/2025 | | | 27,044 | | | | 25,421,360 | |

| | | | | | | | | | | | | |

| Department Stores 0.25% | | | | | | | | | | | | |

| Belk, Inc. 1st Lien Closing Date Term Loan | 7.365%

(3 Mo. LIBOR + 4.75% | ) | 12/12/2022 | | | 15,577 | | | | 12,638,984 | |

| Neiman Marcus Group Ltd LLC Other Term Loan | 5.63%

(3 Mo. LIBOR + 3.25% | ) | 10/25/2020 | | | 21,160 | | | | 17,953,060 | |

| Total | | | | | | | | | | | 30,592,044 | |

| | See Notes to Financial Statements. | 13 |

Schedule of Investments (continued)

December 31, 2018

| Investments | | Interest

Rate | | Maturity

Date | | Principal

Amount

(000) | | | Fair

Value | |

| Diversified Capital Goods 0.07% | | | | | | | | | | | | |

| Graftech International Ltd. Initial Term Loan | | 6.022%

(1 Mo. LIBOR + 3.50% | ) | 2/12/2025 | | $ | 8,550 | | | $ | 8,111,344 | (f) |

| | | | | | | | | | | | | |

| Electric: Generation 0.71% | | | | | | | | | | | | |

| Astoria Energy LLC Advance Term Loan B | | 6.53%

(3 Mo. LIBOR + 4.00% | ) | 12/24/2021 | | | 16,262 | | | | 16,021,926 | |

| Frontera Generation Holdings LLC Initial Term Loan | | 6.629%

(3 Mo. LIBOR + 4.25% | ) | 5/2/2025 | | | 13,281 | | | | 12,816,085 | |

| Helix Gen Funding, LLC Term Loan | | – | (g) | 6/3/2024 | | | 2,762 | | | | 2,592,756 | |

| Lightstone Holdco LLC Refinancing Term Loan B | | 6.272%

(3 Mo. LIBOR + 3.75% | ) | 1/30/2024 | | | 23,196 | | | | 22,017,017 | |

| Lightstone Holdco LLC Refinancing Term Loan C | | 6.272%

(3 Mo. LIBOR + 3.75% | ) | 1/30/2024 | | | 1,246 | | | | 1,182,519 | |

| Longview Power, LLC Advance Term Loan B | | – | (g) | 4/13/2021 | | | 2,247 | | | | 1,904,484 | |

| Moxie Patriot LLC Construction Advances Term Loan B1 | | 8.553%

(3 Mo. LIBOR + 5.75% | ) | 12/19/2020 | | | 2,355 | | | | 2,311,223 | |

| Moxie Patriot LLC Construction Advances Term Loan B2 | | 8.553%

(3 Mo. LIBOR + 5.75% | ) | 12/19/2020 | | | 12,621 | | | | 12,384,578 | |

| Edgewater Generation, L.L.C. Term Loan | | 6.272%

(3 Mo. LIBOR + 3.75% | ) | 12/13/2025 | | | 15,043 | | | | 14,760,944 | |

| Total | | | | | | | | | | | 85,991,532 | |

| | | | | | | | | | | | | |

| Electronics 0.13% | | | | | | | | | | | | |

| EXC Holdings III Corp. 1st Lien Initial Dollar Term Loan | 6.303%

(3 Mo. LIBOR + 3.50% | ) | 12/2/2024 | | | 15,841 | | | | 15,326,361 | |

| | | | | | | | | | | | | |

| Food: Wholesale 0.39% | | | | | | | | | | | | |

| H-Food Holdings, LLC Initial Term Loan | | 6.21%

(3 Mo. LIBOR + 3.69% | ) | 5/23/2025 | | | 13,197 | | | | 12,695,223 | |

| Post Holdings, Inc. Incremental Term Loan | | – | (g) | 5/24/2024 | | | 36,053 | | | | 34,836,211 | |

| Total | | | | | | | | | | | 47,531,434 | |

| | | | | | | | | | | | | |

| Gaming 0.42% | | | | | | | | | | | | |

| MGM Growth Properties Operating Partnership LP Term Loan B | | – | (g) | 3/21/2025 | | | 26,975 | | | | 25,924,668 | |

| VICI Properties 1 LLC Term Loan B | | – | (g) | 12/20/2024 | | | 27,044 | | | | 25,915,859 | |

| Total | | | | | | | | | | | 51,840,527 | |

| | | | | | | | | | | | | |

| Gas Distribution 0.11% | | | | | | | | | | | | |

| NorthRiver Midstream Finance LP Initial Term Loan B (Canada) | | 5.646%

(3 Mo. LIBOR + 3.25% | ) | 10/1/2025 | | | 13,700 | | | | 13,408,886 | |

| 14 | See Notes to Financial Statements. | |

Schedule of Investments (continued)

December 31, 2018

| Investments | | Interest

Rate | | Maturity

Date | | Principal

Amount

(000) | | | Fair

Value | |

| Health Services 0.21% | | | | | | | | | | | | |

| Regionalcare Hospital Partners Holdings, Inc. 1st Lien Term Loan B | | 7.129%

(3 Mo. LIBOR + 4.50% | ) | 11/16/2025 | | $ | 27,086 | | | $ | 25,774,090 | |

| | | | | | | | | | | | | |

| Insurance Brokerage 0.14% | | | | | | | | | | | | |

| Hub International Limited Initial Term Loan | | 5.24%

(3 Mo. LIBOR + 3.00% | ) | 4/25/2025 | | | 18,164 | | | | 17,201,683 | |

| | | | | | | | | | | | | |

| Investments & Miscellaneous Financial Services 0.21% | | | | | | | | | | | | |

| Edelman Financial Center, LLC, (The) 1st Lien Initial Term Loan | | 5.686%

(3 Mo. LIBOR + 3.25% | ) | 7/21/2025 | | | 6,948 | | | | 6,714,721 | |

| Vertafore, Inc. 1st Lien Initial Term Loan | | 6.053%

(3 Mo. LIBOR + 3.25% | ) | 7/2/2025 | | | 19,457 | | | | 18,551,264 | |

| Total | | | | | | | | | | | 25,265,985 | |

| | | | | | | | | | | | | |

| Media: Content 0.02% | | | | | | | | | | | | |

| Univision Communications Inc. 2017 1st Lien Replacement Repriced Term Loan | | – | (g) | 3/15/2024 | | | 2,303 | | | | 2,095,659 | |

| | | | | | | | | | | | | |

| Oil Field Equipment & Services 0.13% | | | | | | | | | | | | |

| Apergy Corp. Initial Term Loan | | 5.063%

(1 Mo. LIBOR + 2.50% | ) | 5/9/2025 | | | 17,069 | | | | 16,087,616 | (f) |

| | | | | | | | | | | | | |

| Personal & Household Products 0.60% | | | | | | | | | | | | |

| Anastasia Parent, LLC Closing Date Term Loan | | 6.272%

(1 Mo. LIBOR + 3.75% | ) | 8/11/2025 | | | 26,412 | | | | 25,025,185 | (f) |

| Britax U.S. Holdings Inc. Initial Dollar Term Loan | 6.303%

(3 Mo. LIBOR + 3.50% | ) | 10/15/2020 | | | 15,264 | | | | 11,931,492 | |

| Energizer Holdings, Inc. Bridge Term Loan | | – | (g) | 6/30/2022 | | | 10,441 | | | | 10,441,000 | |

| FGI Operating Company, LLC Exit Term Loan | | 12.616%

(3 Mo. LIBOR + 10.00% | ) | 5/15/2022 | | | 1,005 | | | | 1,005,238 | (f) |

| Revlon Consumer Products Corp. Initial Term Loan B | | 6.207%

(3 Mo. LIBOR + 3.50% | ) | 9/7/2023 | | | 16,487 | | | | 11,805,922 | |

| TGP Holdings III LLC 1st Lien 2018 Refinancing Term Loan | | 7.053%

(3 Mo. LIBOR + 4.25% | ) | 9/25/2024 | | | 13,456 | | | | 12,934,566 | |

| Total | | | | | | | | | | | 73,143,403 | |

| | | | | | | | | | | | | |

| Recreation & Travel 0.42% | | | | | | | | | | | | |

| Intrawest Resorts Holdings, Inc. Initial Bluebird Term Loan | | 5.506%

(1 Mo. LIBOR + 3.00% | ) | 7/31/2024 | | | 27,486 | | | | 26,432,242 | |

| Kingpin Intermediate Holdings LLC 1st Lien Refinancing Term Loan | | 6.02%

(1 Mo. LIBOR + 3.50% | ) | 7/3/2024 | | | 12,746 | | | | 12,411,156 | |

| Silk Bidco AS Facility Term Loan B(a) | | 3.75%

(6 Mo. Euribor + 4.00% | ) | 2/22/2025 | | EUR | 10,916 | | | | 12,400,131 | |

| Total | | | | | | | | | | | 51,243,529 | |

| | See Notes to Financial Statements. | 15 |

Schedule of Investments (continued)

December 31, 2018

| Investments | | Interest

Rate | | Maturity

Date | | Principal

Amount

(000) | | | Fair

Value | |

| Restaurants 0.40% | | | | | | | | | | | | |

| CEC Entertainment, Inc. Term Loan B | | 5.772%

(1 Mo. LIBOR + 3.25% | ) | 2/12/2021 | | $ | 14,252 | | | $ | 13,230,178 | |

| IRB Holding Corp. Term Loan B | | 5.682%

(1 Mo. LIBOR + 3.25% | ) | 2/5/2025 | | | 19,501 | | | | 18,643,267 | |

| Panera Bread Co. Term Loan | | 4.25%

(1 Mo. LIBOR + 1.75% | ) | 7/18/2022 | | | 17,335 | | | | 16,749,687 | |

| Total | | | | | | | | | | | 48,623,132 | |

| | | | | | | | | | | | | |

| Specialty Retail 1.08% | | | | | | | | | | | | |

| Ascena Retail Group, Inc. Tranche B Term Loan | | 7.063%

(3 Mo. LIBOR + 4.50% | ) | 8/21/2022 | | | 12,286 | | | | 11,465,725 | |

| Bass Pro Group, LLC Initial Term Loan | | 7.522%

(1 Mo. LIBOR + 5.00% | ) | 9/25/2024 | | | 12,941 | | | | 12,436,530 | |

| BJ’s Wholesale Club, Inc. 1st Lien Tranche B Term Loan | | 5.432%

(1 Mo. LIBOR + 3.00% | ) | 2/3/2024 | | | 25,364 | | | | 24,726,542 | |

| Boardriders, Inc. Initial Term Loan | | 9.022%

(1 Mo. LIBOR + 6.50% | ) | 4/23/2024 | | | 15,604 | | | | 15,564,581 | |

| Claire’s Stores, Inc. Revolving Credit Term Loan | | – | (g) | 9/22/2022 | | | 720 | | | | 719,580 | (f) |

| Claire’s Stores, Inc. Term Loan | | 8.631%

(1 Mo. LIBOR + 6.25% | ) | 9/15/2038 | | | 2,399 | | | | 3,757,930 | |

| EG Group Limited Additional Facility Term Loan (United Kingdom)(b) | 6.813%

(3 Mo. LIBOR +4.00% | ) | 2/7/2025 | | | 9,932 | | | | 9,596,988 | |

| EG Group Limited Facility Term Loan B (United Kingdom)(b) | | 6.813%

(3 Mo. LIBOR + 4.00% | ) | 2/7/2025 | | | 7,916 | | | | 7,648,779 | |

| GOBP Holdings, Inc. 1st Lien Initial Term Loan | | – | (g) | 10/22/2025 | | | 15,812 | | | | 15,495,299 | |

| J. Crew Group, Inc. Amended Term Loan | | 5.742%

(3 Mo. LIBOR + 3.22%) - 6.023% | | 3/5/2021 | | | 16,873 | | | | 13,376,445 | |

| Mavis Tire Express Services Corp. 1st Lien Closing Date Term Loan | | 5.754%

(1 Mo. LIBOR + 3.25% | ) | 3/20/2025 | | | 14,975 | | | | 14,488,572 | |

| Mavis Tire Express Services Corp. 1st Lien Delayed Draw Term Loan | | 5.754%

(1 Mo. LIBOR + 3.25% | ) | 3/20/2025 | | | 2,413 | | | | 2,334,919 | |

| Total | | | | | | | | | | | 131,611,890 | |

| | | | | | | | | | | | | |

| Support: Services 0.55% | | | | | | | | | | | | |

| AVSC Holding Corp. 1st Lien Initial Term Loan | | 6.00%

(1 Mo. LIBOR +3.25%) - 6.053 | | 3/1/2025 | | | 12,815 | | | | 12,185,103 | |

| Pike Corp. Initial Term Loan | | 6.03%

(3 Mo. LIBOR + 3.50% | ) | 3/23/2025 | | | 18,633 | | | | 18,295,074 | |

| Southern Graphics Inc. 1st Lien Refinancing Term Loan | | 5.745%

(2 Mo. LIBOR + 3.25% | ) | 12/31/2022 | | | 18,187 | | | | 17,156,148 | |

| Trans Union LLC 2018 Incremental Term Loan B4 | | 4.522%

(1 Mo. LIBOR +2.00% | ) | 6/19/2025 | | | 19,749 | | | | 19,103,194 | |

| Total | | | | | | | | | | | 66,739,519 | |

| 16 | See Notes to Financial Statements. | |

Schedule of Investments (continued)

December 31, 2018

| Investments | | Interest

Rate | | Maturity

Date | | Principal

Amount

(000) | | | Fair

Value | |

| Telecommunications: Wireless 0.21% | | | | | | | | | | | | |

| Sprint Communications, Inc. Initial Term Loan | | 5.063%

(1 Mo. LIBOR + 2.50% | ) | 2/2/2024 | | $ | 26,975 | | | $ | 25,739,080 | |

| | | | | | | | | | | | | |

| Theaters & Entertainment 0.25% | | | | | | | | | | | | |

| SeaWorld Parks & Entertainment, Inc. Term Loan B5 | | 5.522%

(1 Mo. LIBOR + 3.00% | ) | 3/31/2024 | | | 32,247 | | | | 30,870,607 | |

| | | | | | | | | | | | | |

| Transportation: Infrastructure/Services 0.10% | | | | | | | | | | | | |

| Commercial Barge Line Co. Initial Term Loan | | 11.272%

(1 Mo. LIBOR + 8.75% | ) | 11/12/2020 | | | 16,686 | | | | 12,114,014 | |

| Total Floating Rate Loans (cost $832,075,829) | | | | | | | | | | | 804,733,695 | |

| | | | | | | | | | | | | |

| FOREIGN BONDS(a)0.20% | | | | | | | | | | | | |

| | | | | | | | | | | | | |

| France 0.10% | | | | | | | | | | | | |

| CMA CGM SA† | | 5.25% | | 1/15/2025 | | EUR | 13,210 | | | | 12,698,864 | |

| | | | | | | | | | | | | |

| Netherlands 0.10% | | | | | | | | | | | | |

| Hema Bondco I BV† | | 6.25%

(3 Mo. Euribor + 6.25% | )# | 7/15/2022 | | EUR | 12,774 | | | | 12,484,050 | |

| Total Foreign Bonds (cost $28,995,725) | | | | | | | | | | | 25,182,914 | |

| | | | | | | | | | | | | |

| FOREIGN GOVERNMENT OBLIGATIONS 7.18% | | | | | | | | | | | | |

| Abu Dhabi Government International†(b) | | 3.125% | | 5/3/2026 | | $ | 47,836 | | | | 46,341,843 | |

| Arab Republic of Egypt†(b) | | 5.577% | | 2/21/2023 | | | 39,734 | | | | 37,761,048 | |

| Australian Government(a) | | 4.25% | | 4/21/2026 | | AUD | 26,802 | | | | 21,479,956 | |

| Bahrain Government International Bond†(b) | | 6.75% | | 9/20/2029 | | $ | 21,000 | | | | 20,631,219 | |

| City of Buenos Aires†(b) | | 7.50% | | 6/1/2027 | | | 16,064 | | | | 13,694,560 | |

| Development Bank of Mongolia LLC†(b) | | 7.25% | | 10/23/2023 | | | 26,519 | | | | 26,069,238 | |

| Federal Republic of Brazil(b) | | 4.625% | | 1/13/2028 | | | 40,519 | | | | 39,030,332 | |

| Government of Bermuda† | | 4.138% | | 1/3/2023 | | | 14,720 | | | | 14,958,022 | |

| Government of Bermuda† | | 4.75% | | 2/15/2029 | | | 12,997 | | | | 13,256,940 | |

| Government of Bermuda† | | 4.854% | | 2/6/2024 | | | 6,410 | | | | 6,693,130 | |

| Government of Jamaica(b) | | 6.75% | | 4/28/2028 | | | 22,327 | | | | 23,889,890 | |

| Government of Jamaica(b) | | 8.00% | | 3/15/2039 | | | 23,326 | | | | 26,824,900 | |

| Hellenic Republic†(a) | | 4.375% | | 8/1/2022 | | EUR | 14,317 | | | | 17,080,597 | |

| Honduras Government†(b) | | 6.25% | | 1/19/2027 | | $ | 19,384 | | | | 19,240,558 | |

| Ivory Coast Bond†(b) | | 5.375% | | 7/23/2024 | | | 28,894 | | | | 26,572,945 | |

| Province of British Columbia Canada(a) | | 2.85% | | 6/18/2025 | | CAD | 44,800 | | | | 33,396,871 | |

| Province of Santa Fe†(b) | | 6.90% | | 11/1/2027 | | $ | 17,773 | | | | 13,196,452 | |

| Provincia de Cordoba†(b) | | 7.125% | | 6/10/2021 | | | 15,068 | | | | 13,335,180 | |

| Provincia de Cordoba†(b) | | 7.45% | | 9/1/2024 | | | 11,998 | | | | 9,838,360 | |

| Provincia de Mendoza†(b) | | 8.375% | | 5/19/2024 | | | 27,674 | | | | 22,554,310 | |

| | See Notes to Financial Statements. | 17 |

Schedule of Investments (continued)

December 31, 2018

| Investments | | Interest

Rate | | Maturity

Date | | Principal

Amount

(000) | | | Fair

Value | |

| Queensland Treasury Corp.†(a) | | 4.00% | | 6/21/2019 | | AUD | 22,400 | | | $ | 15,919,607 | |

| Republic of Ecuador†(b) | | 8.875% | | 10/23/2027 | | $ | 49,199 | | | | 42,495,636 | |

| Republic of Angola†(b) | | 8.25% | | 5/9/2028 | | | 12,699 | | | | 11,992,999 | |

| Republic of Argentina(b) | | 6.875% | | 4/22/2021 | | | 21,391 | | | | 19,407,199 | |

| Republic of Chile(b) | | 3.125% | | 1/21/2026 | | | 27,092 | | | | 26,211,104 | |

| Republic of EI Salvador†(b) | | 6.375% | | 1/18/2027 | | | 27,126 | | | | 24,949,138 | |

| Republic of Kenya†(b) | | 7.25% | | 2/28/2028 | | | 22,576 | | | | 20,239,881 | |

| Republic of Kenya†(b) | | 8.25% | | 2/28/2048 | | | 14,447 | | | | 12,352,416 | |

| Republic of Paraguay†(b) | | 5.60% | | 3/13/2048 | | | 27,485 | | | | 27,141,437 | |

| Republic of Senegal†(b) | | 6.25% | | 7/30/2024 | | | 18,776 | | | | 18,292,800 | |

| Republic of South Africa(b) | | 4.30% | | 10/12/2028 | | | 22,575 | | | | 20,159,475 | |

| Republic of Sri Lanka(b) | | 6.825% | | 7/18/2026 | | | 24,464 | | | | 22,694,103 | |

| Republic of Suriname†(b) | | 9.25% | | 10/26/2026 | | | 14,321 | | | | 13,855,567 | |

| Republic of Turkey(a) | | 3.25% | | 6/14/2025 | | EUR | 26,171 | | | | 27,413,056 | |

| Republic of Turkey(b) | | 7.25% | | 12/23/2023 | | $ | 39,978 | | | | 41,155,552 | |

| Republic of Uruguay†(a) | | 8.50% | | 3/15/2028 | | UYU | 472,059 | | | | 12,451,348 | |

| Socialist Republic of Vietnam†(b) | | 4.80% | | 11/19/2024 | | $ | 27,091 | | | | 27,387,186 | |

| State of Qatar†(b) | | 3.25% | | 6/2/2026 | | | 27,091 | | | | 26,233,624 | |

| Uruguay Monetary Regulation Bill(a) | | Zero Coupon | | 5/3/2019 | | UYU | 598,596 | | | | 17,916,441 | |

| Total Foreign Government Obligations (cost $896,287,046) | | | | | | | 874,114,920 | |

| | | | | | | | | | | | | |

| GOVERNMENT SPONSORED ENTERPRISES PASS-THROUGH 8.85% | | | | | | | | |

Federal National Mortgage Assoc.(h)

(cost $1,071,645,776) | | 4.50% | | TBA | | $ | 1,040,200 | | | | 1,077,800,203 | |

| | | | | | | | | | | | | |

| HIGH YIELD CORPORATE BONDS 66.23% | | | | | | | | | | | | |

| | | | | | | | | | | | | |

| Advertising 0.07% | | | | | | | | | | | | |

| Lamar Media Corp. | | 5.75% | | 2/1/2026 | | | 8,810 | | | | 8,953,163 | |

| | | | | | | | | | | | | |

| Aerospace/Defense 1.06% | | | | | | | | | | | | |

| BBA US Holdings, Inc.† | | 5.375% | | 5/1/2026 | | | 11,385 | | | | 10,815,636 | |

| Bombardier, Inc. (Canada)†(b) | | 7.50% | | 12/1/2024 | | | 23,093 | | | | 21,822,885 | |

| Bombardier, Inc.(Canada)†(b) | | 7.50% | | 3/15/2025 | | | 45,373 | | | | 42,934,201 | |

| Bombardier, Inc. (Canada)†(b) | | 8.75% | | 12/1/2021 | | | 10,395 | | | | 10,745,831 | |

| United Technologies Corp. | | 4.125% | | 11/16/2028 | | | 43,645 | | | | 43,425,133 | |

| Total | | | | | | | | | | | 129,743,686 | |

| | | | | | | | | | | | | |

| Air Transportation 0.58% | | | | | | | | | | | | |

| Air Canada (Canada)†(b) | | 7.75% | | 4/15/2021 | | | 10,183 | | | | 10,816,892 | |

| Air Canada 2013-1 Class A Pass Through Trust (Canada)†(b) | | 4.125% | | 11/15/2026 | | | 8,893 | | | | 8,831,854 | |

| 18 | See Notes to Financial Statements. | |

Schedule of Investments (continued)

December 31, 2018

| Investments | | Interest

Rate | | Maturity

Date | | Principal

Amount

(000) | | | Fair

Value | |

| Air Transportation (continued) | | | | | | | | | | | | |

| Azul Investments LLP† | | 5.875% | | 10/26/2024 | | $ | 35,600 | | | $ | 33,375,356 | |

| British Airways 2018-1 Class A Pass Through Trust (United Kingdom)†(b) | | 4.125% | | 3/20/2033 | | | 8,972 | | | | 8,880,038 | |

| British Airways 2018-1 Class AA Pass Through Trust (United Kingdom)†(b) | | 3.80% | | 3/20/2033 | | | 8,945 | | | | 8,794,427 | |

| Total | | | | | | | | | | | 70,698,567 | |

| | | | | | | | | | | | | |

| Auto Loans 0.10% | | | | | | | | | | | | |

| General Motors Financial Co., Inc. | | 3.85% | | 1/5/2028 | | | 14,047 | | | | 12,260,887 | |

| | | | | | | | | | | | | |

| Auto Parts & Equipment 0.11% | | | | | | | | | | | | |

| Allison Transmission, Inc.† | | 5.00% | | 10/1/2024 | | | 14,461 | | | | 13,936,789 | |

| | | | | | | | | | | | | |

| Automakers 0.77% | | | | | | | | | | | | |

| General Motors Co. | | 5.00% | | 10/1/2028 | | | 19,990 | | | | 18,987,954 | |

| General Motors Co. | | 8.375% | | 7/15/2049 | | | 15,000 | | | | 1,500 | (c) |

| Navistar International Corp.† | | 6.625% | | 11/1/2025 | | | 12,846 | | | | 12,460,620 | |

| Tesla, Inc.† | | 5.30% | | 8/15/2025 | | | 71,655 | | | | 62,518,987 | |

| Total | | | | | | | | | | | 93,969,061 | |

| | | | | | | | | | | | | |

| Banking 4.20% | | | | | | | | | | | | |

| ABN AMRO Bank NV (Netherlands)†(b) | | 4.75% | | 7/28/2025 | | | 31,461 | | | | 31,364,792 | |

| AIB Group plc (Ireland)†(b) | | 4.75% | | 10/12/2023 | | | 22,383 | | | | 22,183,496 | |

| Ally Financial, Inc. | | 4.625% | | 3/30/2025 | | | 22,002 | | | | 21,396,945 | |

| American Express Co. | | 3.40% | | 2/27/2023 | | | 17,804 | | | | 17,654,218 | |

| ANZ New Zealand Int’l Ltd. (United Kingdom)†(b) | | 2.125% | | 7/28/2021 | | | 14,890 | | | | 14,401,604 | |

| Associated Banc-Corp. | | 4.25% | | 1/15/2025 | | | 7,996 | | | | 8,051,343 | |

| Australia & New Zealand Banking Group Ltd. (United Kingdom)†(b) | | 6.75%

(USD Swap + 5.17% | )# | – | (i) | | 19,074 | | | | 18,764,047 | |

| Banco Mercantil del Norte SA† | 7.625%

(10 Yr Treasury CMT + 5.353% | )# | – | (i) | | 6,572 | | | | 6,391,336 | |

| Banco Safra SA† | | 4.125% | | 2/8/2023 | | | 19,821 | | | | 19,201,594 | |

| Bank of America Corp. | | 4.45% | | 3/3/2026 | | | 19,634 | | | | 19,455,776 | |

| Bank of Ireland Group plc (Ireland)†(b) | | 4.50% | | 11/25/2023 | | | 17,871 | | | | 17,526,036 | |

| BankUnited, Inc. | | 4.875% | | 11/17/2025 | | | 24,313 | | | | 24,834,023 | |

| BBVA Bancomer SA† | | 5.125% | #(j) | 1/18/2033 | | | 35,647 | | | | 31,057,805 | |

| CIT Group, Inc. | | 5.25% | | 3/7/2025 | | | 6,722 | | | | 6,587,560 | |

| CIT Group, Inc. | | 6.125% | | 3/9/2028 | | | 12,241 | | | | 12,210,398 | |

| Citigroup, Inc. | | 4.45% | | 9/29/2027 | | | 13,296 | | | | 12,834,297 | |

| Compass Bank | | 3.875% | | 4/10/2025 | | | 26,897 | | | | 25,830,579 | |

| Fifth Third Bancorp | | 8.25% | | 3/1/2038 | | | 8,042 | | | | 10,700,494 | |

| | See Notes to Financial Statements. | 19 |

Schedule of Investments (continued)

December 31, 2018

| Investments | | Interest

Rate | | Maturity

Date | | Principal

Amount

(000) | | | Fair

Value | |

| Banking (continued) | | | | | | | | | | | | |

| Goldman Sachs Group, Inc. (The) | | 3.50% | | 11/16/2026 | | $ | 13,667 | | | $ | 12,642,988 | |

| Goldman Sachs Group, Inc. (The) | | 3.618%

(3 Mo. LIBOR + 1.11% | )# | 4/26/2022 | | | 6,189 | | | | 6,122,211 | |

| Goldman Sachs Group, Inc. (The) | | 4.25% | | 10/21/2025 | | | 18,995 | | | | 18,214,209 | |

| Home BancShares, Inc. | | 5.625%

(3 Mo. LIBOR + 3.58% | )# | 4/15/2027 | | | 19,481 | | | | 19,914,778 | |

| Huntington Bancshares, Inc. | | 5.70% | #(j) | – | (i) | | 13,740 | | | | 12,220,013 | |

| JPMorgan Chase & Co. | | 3.54%

(3 Mo. LIBOR + 1.38% | )# | 5/1/2028 | | | 11,994 | | | | 11,454,966 | |

| JPMorgan Chase & Co. | | 3.90% | | 7/15/2025 | | | 17,386 | | | | 17,250,693 | |

| JPMorgan Chase & Co. | 6.10%

(3 Mo. LIBOR + 3.33% | )# | – | (i) | | 12,015 | | | | 11,954,925 | |

| Macquarie Bank Ltd. (United Kingdom)†(b) | 6.125%

(5 Yr Swap rate + 3.70% | )# | – | (i) | | 28,891 | | | | 24,737,919 | |

| Morgan Stanley | | 3.125% | | 7/27/2026 | | | 18,976 | | | | 17,531,932 | |

| Morgan Stanley | | 3.625% | | 1/20/2027 | | | 24,804 | | | | 23,610,672 | |

| Popular, Inc. | | 6.125% | | 9/14/2023 | | | 15,922 | | | | 15,832,518 | |

| Washington Mutual Bank(k) | | 6.875% | | 6/15/2011 | | | 22,500 | | | | 2,250 | (c) |

| Total | | | | | | | | | | | 511,936,417 | |

| | | | | | | | | | | | | |

| Beverages 1.06% | | | | | | | | | | | | |

| Bacardi Ltd.† | | 2.75% | | 7/15/2026 | | | 20,151 | | | | 17,357,711 | |

| Bacardi Ltd.† | | 4.70% | | 5/15/2028 | | | 28,786 | | | | 27,730,659 | |

| Becle SAB de CV (Mexico)†(b) | | 3.75% | | 5/13/2025 | | | 15,764 | | | | 15,060,444 | |

| Brown-Forman Corp. | | 3.50% | | 4/15/2025 | | | 8,956 | | | | 8,929,388 | |

| Brown-Forman Corp. | | 4.50% | | 7/15/2045 | | | 18,174 | | | | 19,179,448 | |

| Coca-Cola Icecek AS (Turkey)†(b) | | 4.215% | | 9/19/2024 | | | 28,540 | | | | 26,792,810 | |

| PepsiCo, Inc. | | 3.60% | | 3/1/2024 | | | 14,292 | | | | 14,516,492 | |

| Total | | | | | | | | | | | 129,566,952 | |

| | | | | | | | | | | | | |

| Building & Construction 1.16% | | | | | | | | | | | | |

| Ashton Woods USA LLC/Ashton Woods Finance Co.† | | 6.75% | | 8/1/2025 | | | 14,048 | | | | 12,292,000 | |

| Ashton Woods USA LLC/Ashton Woods Finance Co.† | | 6.875% | | 2/15/2021 | | | 9,653 | | | | 9,315,145 | |

| ITR Concession Co. LLC† | | 5.183% | | 7/15/2035 | | | 7,658 | | | | 7,443,342 | |

| Lennar Corp. | | 4.75% | | 11/15/2022 | | | 15,303 | | | | 14,901,296 | |

| Lennar Corp. | | 4.75% | | 5/30/2025 | | | 4,408 | | | | 4,149,030 | |

| Lennar Corp. | | 4.75% | | 11/29/2027 | | | 5,102 | | | | 4,623,688 | |

| PulteGroup, Inc. | | 5.00% | | 1/15/2027 | | | 17,108 | | | | 15,546,895 | |

| PulteGroup, Inc. | | 6.375% | | 5/15/2033 | | | 25,646 | | | | 23,530,205 | |

| Shea Homes LP/Shea Homes Funding Corp.† | | 6.125% | | 4/1/2025 | | | 14,448 | | | | 12,858,720 | |

| Toll Brothers Finance Corp. | | 5.625% | | 1/15/2024 | | | 14,213 | | | | 13,999,805 | |

| William Lyon Homes, Inc. | | 5.875% | | 1/31/2025 | | | 25,933 | | | | 22,172,715 | |

| Total | | | | | | | | | | | 140,832,841 | |

| 20 | See Notes to Financial Statements. |

Schedule of Investments (continued)

December 31, 2018

| Investments | | Interest

Rate | | Maturity

Date | | Principal

Amount

(000) | | | Fair

Value | |

| Building Materials 0.10% | | | | | | | | | | | | |

| Hillman Group, Inc. (The)† | | 6.375% | | 7/15/2022 | | $ | 14,608 | | | $ | 11,978,560 | |

| | | | | | | | | | | | | |

| Cable & Satellite Television 2.18% | | | | | | | | | | | | |

| Altice France SA (France)†(b) | | 7.375% | | 5/1/2026 | | | 46,103 | | | | 42,414,760 | |

| Altice France SA (France)†(b) | | 8.125% | | 2/1/2027 | | | 13,530 | | | | 12,785,850 | |

| CCO Holdings LLC/CCO Holdings Capital Corp.† | | 5.125% | | 5/1/2027 | | | 32,573 | | | | 30,419,925 | |

| CCO Holdings LLC/CCO Holdings Capital Corp.† | | 5.75% | | 2/15/2026 | | | 71,221 | | | | 69,974,632 | |

| CCO Holdings LLC/CCO Holdings Capital Corp.† | | 5.875% | | 4/1/2024 | | | 15,739 | | | | 15,699,653 | |

| CSC Holdings LLC† | | 10.875% | | 10/15/2025 | | | 16,727 | | | | 18,824,900 | |

| DISH DBS Corp. | | 7.75% | | 7/1/2026 | | | 41,950 | | | | 34,818,500 | |

| UPCB Finance IV Ltd.† | | 5.375% | | 1/15/2025 | | | 16,988 | | | | 15,928,289 | |

| Ziggo BV (Netherlands)†(b) | | 5.50% | | 1/15/2027 | | | 27,526 | | | | 24,704,585 | |

| Total | | | | | | | | | | | 265,571,094 | |

| | | | | | | | | | | | | |

| Chemicals 0.96% | | | | | | | | | | | | |

| CF Industries, Inc.† | | 4.50% | | 12/1/2026 | | | 26,420 | | | | 25,876,418 | |

| CF Industries, Inc. | | 4.95% | | 6/1/2043 | | | 3,074 | | | | 2,393,878 | |

| CF Industries, Inc. | | 5.15% | | 3/15/2034 | | | 5,096 | | | | 4,306,120 | |

| CNAC HK Finbridge Co. Ltd. (Hong Kong)(b) | | 4.125% | | 7/19/2027 | | | 2,784 | | | | 2,637,562 | |

| CVR Partners LP/CVR Nitrogen Finance Corp.† | | 9.25% | | 6/15/2023 | | | 13,118 | | | | 13,691,912 | |

| International Flavors & Fragrances, Inc. | | 5.00% | | 9/26/2048 | | | 21,585 | | | | 21,611,813 | |

| Mexichem SAB de CV (Mexico)†(b) | | 5.875% | | 9/17/2044 | | | 14,262 | | | | 12,897,840 | |

| OCI NV (Netherlands)†(b) | | 6.625% | | 4/15/2023 | | | 13,200 | | | | 13,035,000 | |

| Yingde Gases Investment Ltd. (Hong Kong)†(b) | | 6.25% | | 1/19/2023 | | | 21,196 | | | | 19,976,394 | |

| Total | | | | | | | | | | | 116,426,937 | |

| | | | | | | | | | | | | |

| Consumer/Commercial/Lease Financing 1.01% | | | | | | | | | | | | |

| Curo Group Holdings Corp.† | | 8.25% | | 9/1/2025 | | | 20,870 | | | | 16,487,300 | |

| Freedom Mortgage Corp.† | | 8.125% | | 11/15/2024 | | | 7,514 | | | | 6,480,825 | |

| Freedom Mortgage Corp.† | | 8.25% | | 4/15/2025 | | | 12,646 | | | | 10,875,560 | |

| Nationstar Mortgage Holdings, Inc.† | | 9.125% | | 7/15/2026 | | | 20,586 | | | | 20,071,350 | |

| Navient Corp. | | 6.125% | | 3/25/2024 | | | 22,447 | | | | 19,360,537 | |

| Navient Corp. | | 6.75% | | 6/25/2025 | | | 28,191 | | | | 24,103,305 | |

| Quicken Loans, Inc.† | | 5.25% | | 1/15/2028 | | | 28,288 | | | | 25,140,960 | |

| Total | | | | | | | | | | | 122,519,837 | |

| | | | | | | | | | | | | |

| Department Stores 0.36% | | | | | | | | | | | | |

| Kohl’s Corp. | | 5.55% | | 7/17/2045 | | | 27,768 | | | | 26,085,192 | |

| Seven & i Holdings Co. Ltd. (Japan)†(b) | | 3.35% | | 9/17/2021 | | | 17,869 | | | | 17,926,968 | |

| Total | | | | | | | | | | | 44,012,160 | |

| | See Notes to Financial Statements. | 21 |

Schedule of Investments (continued)

December 31, 2018

| Investments | | Interest

Rate | | Maturity

Date | | Principal

Amount

(000) | | | Fair

Value | |

| Discount Stores 1.03% | | | | | | | | | | | | |

| Amazon.com, Inc. | | 3.15% | | 8/22/2027 | | $ | 28,837 | | | $ | 27,871,510 | |

| Amazon.com, Inc. | | 4.25% | | 8/22/2057 | | | 20,632 | | | | 20,136,228 | |

| Amazon.com, Inc. | | 4.80% | | 12/5/2034 | | | 28,691 | | | | 30,812,905 | |

| Amazon.com, Inc. | | 5.20% | | 12/3/2025 | | | 41,869 | | | | 46,052,211 | |

| Total | | | | | | | | | | | 124,872,854 | |

| | | | | | | | | | | | | |

| Diversified Capital Goods 1.10% | | | | | | | | | | | | |

| BCD Acquisition, Inc.† | | 9.625% | | 9/15/2023 | | | 12,382 | | | | 12,784,415 | |

| General Electric Co. | | 2.70% | | 10/9/2022 | | | 39,891 | | | | 37,046,499 | |

| General Electric Co. | | 3.10% | | 1/9/2023 | | | 25,636 | | | | 23,941,986 | |

| Griffon Corp. | | 5.25% | | 3/1/2022 | | | 11,628 | | | | 10,566,945 | |

| KOC Holding AS (Turkey)†(b) | | 5.25% | | 3/15/2023 | | | 15,211 | | | | 14,268,724 | |

| Siemens Financieringsmaatschappij NV (Netherlands)†(b) | | 3.25% | | 5/27/2025 | | | 13,036 | | | | 12,791,990 | |

| SPX FLOW, Inc.† | | 5.625% | | 8/15/2024 | | | 8,609 | | | | 8,178,550 | |

| SPX FLOW, Inc.† | | 5.875% | | 8/15/2026 | | | 14,947 | | | | 13,975,445 | |

| Total | | | | | | | | | | | 133,554,554 | |

| | | | | | | | | | | | | |

| Electric: Distribution/Transportation 0.68% | | | | | | | | | | | | |

| Atlantic City Electric Co. | | 4.00% | | 10/15/2028 | | | 13,493 | | | | 13,903,824 | |

| Cemig Geracao e Transmissao SA (Brazil)†(b) | | 9.25% | | 12/5/2024 | | | 13,163 | | | | 14,058,084 | |

| Oklahoma Gas & Electric Co. | | 4.15% | | 4/1/2047 | | | 11,379 | | | | 11,069,163 | |

| State Grid Overseas Investment 2016 Ltd.† | | 3.50% | | 5/4/2027 | | | 45,150 | | | | 43,563,287 | |

| Total | | | | | | | | | | | 82,594,358 | |

| | | | | | | | | | | | | |

| Electric: Generation 1.32% | | | | | | | | | | | | |

| Acwa Power Management & Investments One Ltd. (Sounth Africa)†(b) | | 5.95% | | 12/15/2039 | | | 14,814 | | | | 13,967,084 | |

| Calpine Corp. | | 5.75% | | 1/15/2025 | | | 41,895 | | | | 38,438,662 | |

| Clearway Energy Operating LLC† | | 5.75% | | 10/15/2025 | | | 15,737 | | | | 15,087,849 | |

| NextEra Energy Operating Partners LP† | | 4.50% | | 9/15/2027 | | | 19,300 | | | | 17,249,375 | |

| NRG Energy, Inc. | | 5.75% | | 1/15/2028 | | | 32,817 | | | | 31,627,384 | |

| NSG Holdings LLC/NSG Holdings, Inc.† | | 7.75% | | 12/15/2025 | | | 14,893 | | | | 15,786,630 | |

| Rio Energy SA/UGEN SA/UENSA SA (Argentina)†(b) | | 6.875% | | 2/1/2025 | | | 17,545 | | | | 13,071,025 | |

| Talen Energy Supply LLC | | 4.60% | | 12/15/2021 | | | 198 | | | | 179,190 | |

| Vistra Operations Co. LLC† | | 5.50% | | 9/1/2026 | | | 15,758 | | | | 15,226,167 | |

| Total | | | | | | | | | | | 160,633,366 | |

| 22 | See Notes to Financial Statements. |

Schedule of Investments (continued)

December 31, 2018

| Investments | | Interest

Rate | | Maturity

Date | | Principal

Amount

(000) | | | Fair

Value | |

| Electric: Integrated 2.25% | | | | | | | | | | | | |

| Aegea Finance Sarl (Brazil)†(b) | | 5.75% | | 10/10/2024 | | $ | 20,480 | | | $ | 19,609,805 | |

| AES Corp. (The) | | 4.50% | | 3/15/2023 | | | 11,417 | | | | 11,174,389 | |

| AES Corp. (The) | | 5.125% | | 9/1/2027 | | | 802 | | | | 771,925 | |

| Arizona Public Service Co. | | 2.95% | | 9/15/2027 | | | 13,385 | | | | 12,697,180 | |

| Ausgrid Finance Pty Ltd. (Australia)†(b) | | 4.35% | | 8/1/2028 | | | 13,786 | | | | 13,775,547 | |

| Black Hills Corp. | | 4.35% | | 5/1/2033 | | | 13,491 | | | | 13,567,368 | |

| El Paso Electric Co. | | 5.00% | | 12/1/2044 | | | 20,062 | | | | 20,969,249 | |

| Entergy Arkansas LLC | | 4.00% | | 6/1/2028 | | | 18,151 | | | | 18,554,625 | |

| Entergy Arkansas LLC | | 4.95% | | 12/15/2044 | | | 16,883 | | | | 16,946,623 | |

| Entergy Louisiana LLC | | 4.00% | | 3/15/2033 | | | 10,745 | | | | 10,895,575 | |

| Entergy Mississippi LLC | | 2.85% | | 6/1/2028 | | | 19,150 | | | | 17,935,778 | |

| Indianapolis Power & Light Co.† | | 4.05% | | 5/1/2046 | | | 24,503 | | | | 22,464,482 | |

| Louisville Gas & Electric Co. | | 4.375% | | 10/1/2045 | | | 15,039 | | | | 15,095,873 | |

| Monongahela Power Co.† | | 3.55% | | 5/15/2027 | | | 13,657 | | | | 13,412,345 | |

| Ohio Power Co. | | 4.15% | | 4/1/2048 | | | 26,865 | | | | 26,616,398 | |

| Puget Sound Energy, Inc. | | 4.223% | | 6/15/2048 | | | 13,467 | | | | 13,521,462 | |

| Puget Sound Energy, Inc. | | 7.02% | | 12/1/2027 | | | 2,920 | | | | 3,592,888 | |

| Rochester Gas & Electric Corp.† | | 3.10% | | 6/1/2027 | | | 13,724 | | | | 13,114,589 | |

| Sierra Pacific Power Co. | | 2.60% | | 5/1/2026 | | | 9,730 | | | | 9,078,334 | |

| Total | | | | | | | | | | | 273,794,435 | |

| | | | | | | | | | | | | |

| Electronics 0.82% | | | | | | | | | | | | |

| Nokia OYJ (Finland)(b) | | 4.375% | | 6/12/2027 | | | 13,838 | | | | 12,903,935 | |

| NVIDIA Corp. | | 3.20% | | 9/16/2026 | | | 29,939 | | | | 28,474,191 | |

| QUALCOMM, Inc. | | 3.25% | | 5/20/2027 | | | 17,987 | | | | 16,827,335 | |

| Trimble, Inc. | | 4.75% | | 12/1/2024 | | | 27,261 | | | | 27,518,167 | |

| Xilinx, Inc. | | 2.95% | | 6/1/2024 | | | 15,096 | | | | 14,418,457 | |

| Total | | | | | | | | | | | 100,142,085 | |

| | | | | | | | | | | | | |

| Energy: Exploration & Production 3.01% | | | | | | | | | | | | |

| Alta Mesa Holdings LP/Alta Mesa Finance Services Corp. | | 7.875% | | 12/15/2024 | | | 15,686 | | | | 9,803,750 | |

| California Resources Corp.† | | 8.00% | | 12/15/2022 | | | 37,595 | | | | 25,564,600 | |

| Centennial Resource Production LLC† | | 5.375% | | 1/15/2026 | | | 12,041 | | | | 11,258,335 | |

| Chesapeake Energy Corp. | | 7.00% | | 10/1/2024 | | | 33,707 | | | | 29,325,090 | |

| Chesapeake Energy Corp. | | 7.50% | | 10/1/2026 | | | 13,490 | | | | 11,601,400 | |

| Denbury Resources, Inc.† | | 7.50% | | 2/15/2024 | | | 12,976 | | | | 10,510,560 | |

| Eclipse Resources Corp. | | 8.875% | | 7/15/2023 | | | 13,873 | | | | 11,965,462 | |

| Endeavor Energy Resources LP/EER Finance, Inc.† | | 5.50% | | 1/30/2026 | | | 12,585 | | | | 12,946,819 | |

| | See Notes to Financial Statements. | 23 |

Schedule of Investments (continued)

December 31, 2018

| Investments | | Interest

Rate | | Maturity

Date | | Principal

Amount

(000) | | | Fair

Value | |

| Energy: Exploration & Production (continued) | | | | | | | | | | | | |

| EP Energy LLC/Everest Acquisition Finance, Inc.† | | 8.00% | | 11/29/2024 | | $ | 11,547 | | | $ | 8,660,250 | |

| Gulfport Energy Corp. | | 6.375% | | 5/15/2025 | | | 6,742 | | | | 5,991,953 | |

| Gulfport Energy Corp. | | 6.375% | | 1/15/2026 | | | 6,913 | | | | 5,997,028 | |

| HighPoint Operating Corp. | | 7.00% | | 10/15/2022 | | | 9,822 | | | | 8,987,130 | |

| Hilcorp Energy I LP/Hilcorp Finance Co.† | | 5.00% | | 12/1/2024 | | | 19,212 | | | | 17,098,680 | |

| Hilcorp Energy I LP/Hilcorp Finance Co.† | | 5.75% | | 10/1/2025 | | | 8,125 | | | | 7,271,875 | |

| Hilcorp Energy I LP/Hilcorp Finance Co.† | | 6.25% | | 11/1/2028 | | | 12,846 | | | | 11,352,652 | |

| Hunt Oil Co. of Peru LLC Sucursal Del Peru (Peru)†(b) | | 6.375% | | 6/1/2028 | | | 26,408 | | | | 26,847,693 | |

| Indigo Natural Resources LLC† | | 6.875% | | 2/15/2026 | | | 13,837 | | | | 11,969,005 | |

| Jonah Energy LLC/Jonah Energy Finance Corp.† | | 7.25% | | 10/15/2025 | | | 21,795 | | | | 14,166,750 | |

| MEG Energy Corp. (Canada)†(b) | | 6.50% | | 1/15/2025 | | | 11,902 | | | | 12,125,162 | |

| MEG Energy Corp. (Canada)†(b) | | 7.00% | | 3/31/2024 | | | 23,708 | | | | 22,759,680 | |

| Murphy Oil Corp. | | 6.875% | | 8/15/2024 | | | 5,221 | | | | 5,205,481 | |

| OGX Austria GmbH (Brazil)†(b)(k) | | 8.50% | | 6/1/2018 | | | 20,000 | | | | 400 | |

| Range Resources Corp. | | 4.875% | | 5/15/2025 | | | 14,471 | | | | 11,938,575 | |

| SM Energy Co. | | 6.625% | | 1/15/2027 | | | 8,237 | | | | 7,372,115 | |

| SM Energy Co. | | 6.75% | | 9/15/2026 | | | 12,750 | | | | 11,475,000 | |

| Southwestern Energy Co. | | 7.75% | | 10/1/2027 | | | 12,722 | | | | 12,149,510 | |

| SRC Energy, Inc. | | 6.25% | | 12/1/2025 | | | 21,135 | | | | 17,647,725 | |

| Texaco Capital, Inc. | | 8.625% | | 11/15/2031 | | | 11,023 | | | | 16,215,042 | |

| WildHorse Resource Development Corp. | | 6.875% | | 2/1/2025 | | | 8,918 | | | | 8,472,100 | |

| Total | | | | | | | | | | | 366,679,822 | |

| | | | | | | | | | | | | |

| Environmental 0.27% | | | | | | | | | | | | |

| Darling Global Finance BV†(a) | | 3.625% | | 5/15/2026 | | EUR | 7,646 | | | | 8,698,860 | |

| Paprec Holding SA(a) | | 4.00% | | 3/31/2025 | | EUR | 12,427 | | | | 12,106,056 | |

| Waste Pro USA, Inc.† | | 5.50% | | 2/15/2026 | | $ | 13,660 | | | | 12,635,500 | |

| Total | | | | | | | | | | | 33,440,416 | |

| | | | | | | | | | | | | |

| Food & Drug Retailers 0.87% | | | | | | | | | | | | |

| Albertsons Cos LLC/Safeway, Inc./Albertsons LP/Albertson’s LLC | | 5.75% | | 3/15/2025 | | | 32,370 | | | | 28,485,600 | |

| Albertsons Cos LLC/Safeway, Inc./Albertsons LP/Albertson’s LLC | | 6.625% | | 6/15/2024 | | | 24,128 | | | | 22,499,360 | |

| CVS Health Corp. | | 4.30% | | 3/25/2028 | | | 25,242 | | | | 24,763,195 | |

| Ingles Markets, Inc. | | 5.75% | | 6/15/2023 | | | 19,550 | | | | 19,403,375 | |

| Kroger Co. (The) | | 2.65% | | 10/15/2026 | | | 8,094 | | | | 7,217,035 | |

| Kroger Co. (The) | | 4.65% | | 1/15/2048 | | | 4,496 | | | | 4,146,328 | |

| Total | | | | | | | | | | | 106,514,893 | |

| 24 | See Notes to Financial Statements. |

Schedule of Investments (continued)

December 31, 2018

| Investments | | Interest

Rate | | Maturity

Date | | Principal

Amount

(000) | | | Fair

Value | |

| Food: Wholesale 1.61% | | | | | | | | | | | | |

| Arcor SAIC (Argentina)†(b) | | 6.00% | | 7/6/2023 | | $ | 22,148 | | | $ | 20,484,685 | |

| B&G Foods, Inc. | | 5.25% | | 4/1/2025 | | | 14,068 | | | | 13,135,995 | |

| Campbell Soup Co. | | 4.15% | | 3/15/2028 | | | 23,370 | | | | 21,810,805 | |

| Chobani LLC/Chobani Finance Corp., Inc.† | | 7.50% | | 4/15/2025 | | | 15,174 | | | | 12,025,395 | |

| Conagra Brands, Inc. | | 4.60% | | 11/1/2025 | | | 16,978 | | | | 17,063,618 | |

| FAGE International SA/FAGE USA Dairy Industry, Inc. (Luxembourg)†(b) | | 5.625% | | 8/15/2026 | | | 13,976 | | | | 12,001,890 |

| JBS USA LUX SA/JBS USA Finance, Inc.† | | 5.875% | | 7/15/2024 | | | 13,559 | | | | 13,338,666 | |

| JBS USA LUX SA/JBS USA Finance, Inc.† | | 6.75% | | 2/15/2028 | | | 13,602 | | | | 13,312,957 | |

| Kernel Holding SA (Ukraine)†(b) | | 8.75% | | 1/31/2022 | | | 7,753 | | | | 7,455,192 | |

| Lamb Weston Holdings, Inc.† | | 4.625% | | 11/1/2024 | | | 12,447 | | | | 12,135,825 | |

| Lamb Weston Holdings, Inc.† | | 4.875% | | 11/1/2026 | | | 892 | | | | 860,780 | |

| McCormick & Co., Inc. | | 4.20% | | 8/15/2047 | | | 21,326 | | | | 20,024,424 | |

| MHP Lux SA (Luxembourg)†(b) | | 6.95% | | 4/3/2026 | | | 21,993 | | | | 19,015,148 | |

| Nvent Finance Sarl (Luxembourg)(b) | | 4.55% | | 4/15/2028 | | | 13,384 | | | | 13,145,373 | |

| Total | | | | | | | | | | | 195,810,753 | |

| | | | | | | | | | | | | |

| Forestry/Paper 0.56% | | | | | | | | | | | | |

| Norbord, Inc. (Canada)†(b) | | 6.25% | | 4/15/2023 | | | 18,438 | | | | 18,536,828 | |

| Rayonier AM Products, Inc.† | | 5.50% | | 6/1/2024 | | | 13,628 | | | | 12,060,780 | |

| Suzano Austria GmbH (Brazil)†(b) | | 5.75% | | 7/14/2026 | | | 14,057 | | | | 14,373,282 | |

| Suzano Austria GmbH (Brazil)†(b) | | 6.00% | | 1/15/2029 | | | 9,025 | | | | 9,232,575 | |

| West Fraser Timber Co. Ltd. (Canada)†(b) | | 4.35% | | 10/15/2024 | | | 14,594 | | | | 14,477,959 | |

| Total | | | | | | | | | | | 68,681,424 | |

| | | | | | | | | | | | | |

| Gaming 1.11% | | | | | | | | | | | | |

| Boyd Gaming Corp. | | 6.00% | | 8/15/2026 | | | 13,070 | | | | 12,269,463 | |

| Eldorado Resorts, Inc.† | | 6.00% | | 9/15/2026 | | | 13,521 | | | | 12,811,147 | |

| Eldorado Resorts, Inc. | | 6.00% | | 4/1/2025 | | | 5,376 | | | | 5,212,785 | |

| Everi Payments, Inc.† | | 7.50% | | 12/15/2025 | | | 13,419 | | | | 12,731,276 | |

| GLP Capital LP/GLP Financing II, Inc. | | 5.75% | | 6/1/2028 | | | 18,808 | | | | 19,066,610 | |

| Jacobs Entertainment, Inc.† | | 7.875% | | 2/1/2024 | | | 19,057 | | | | 19,676,352 | |

| Mohegan Gaming & Entertainment†(l) | | 7.875% | | 10/15/2024 | | | 13,557 | | | | 12,726,634 | |

| Penn National Gaming, Inc.† | | 5.625% | | 1/15/2027 | | | 20,104 | | | | 18,043,340 | |

| Stars Group Holdings BV/Stars Group US Co-Borrower LLC (Netherlands)†(b) | | 7.00% | | 7/15/2026 | | | 13,242 | | | | 12,910,950 | |

| Station Casinos LLC† | | 5.00% | | 10/1/2025 | | | 11,158 | | | | 10,125,885 | |

| Total | | | | | | | | | | | 135,574,442 | |

| | See Notes to Financial Statements. | 25 |

Schedule of Investments (continued)

December 31, 2018

| Investments | | Interest

Rate | | Maturity

Date | | Principal

Amount

(000) | | | Fair

Value | |

| Gas Distribution 2.32% | | | | | | | | | | | | |

| Cheniere Corpus Christi Holdings LLC | | 5.125% | | 6/30/2027 | | $ | 23,796 | | | $ | 22,553,849 | |

| Cheniere Corpus Christi Holdings LLC | | 5.875% | | 3/31/2025 | | | 14,002 | | | | 13,966,995 | |

| Cheniere Corpus Christi Holdings LLC | | 7.00% | | 6/30/2024 | | | 8,783 | | | | 9,288,022 | |

| Dominion Energy Gas Holdings LLC | | 3.60% | | 12/15/2024 | | | 12,050 | | | | 11,984,441 | |

| Florida Gas Transmission Co. LLC† | | 4.35% | | 7/15/2025 | | | 18,069 | | | | 18,478,952 | |

| IFM US Colonial Pipeline 2 LLC† | | 6.45% | | 5/1/2021 | | | 17,675 | | | | 18,463,243 | |

| LBC Tank Terminals Holding Netherlands BV (Belgium)†(b) | | 6.875% | | 5/15/2023 | | | 13,377 | | | | 12,039,300 | |

| NGPL PipeCo LLC† | | 4.875% | | 8/15/2027 | | | 31,233 | | | | 29,554,226 | |

| Northern Natural Gas Co.† | | 4.30% | | 1/15/2049 | | | 20,972 | | | | 20,520,266 | |

| ONE Gas, Inc. | | 4.50% | | 11/1/2048 | | | 13,497 | | | | 13,947,596 | |