QuickLinks -- Click here to rapidly navigate through this document

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 14A

Proxy Statement Pursuant to Section 14(a) of

the Securities Exchange Act of 1934 (Amendment No. )

| Filed by the Registrantý | ||

Filed by a Party other than the Registranto | ||

Check the appropriate box: | ||

o | Preliminary Proxy Statement | |

o | Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) | |

ý | Definitive Proxy Statement | |

o | Definitive Additional Materials | |

o | Soliciting Material Pursuant to §240.14a-12 | |

Louisville Gas and Electric Company | ||||

(Name of Registrant as Specified In Its Charter) | ||||

(Name of Person(s) Filing Proxy Statement, if other than the Registrant) | ||||

| Payment of Filing Fee (Check the appropriate box): | ||||

ý | No fee required. | |||

o | Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11. | |||

| (1) | Title of each class of securities to which transaction applies: | |||

| (2) | Aggregate number of securities to which transaction applies: | |||

| (3) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined): | |||

| (4) | Proposed maximum aggregate value of transaction: | |||

| (5) | Total fee paid: | |||

o | Fee paid previously with preliminary materials. | |||

o | Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. | |||

(1) | Amount Previously Paid: | |||

| (2) | Form, Schedule or Registration Statement No.: | |||

| (3) | Filing Party: | |||

| (4) | Date Filed: | |||

Persons who are to respond to the collection of information contained in this form are not required to respond unless the form displays a currently valid OMB control number. | ||||

![]()

June 25, 2004

Dear Louisville Gas and Electric Company Shareholder:

You are cordially invited to attend the Annual Meeting of Shareholders of Louisville Gas and Electric Company ("LG&E") to be held on Thursday, July 8, 2004 at 3:00 p.m., local time in the Twelfth Floor Assembly Room at the LG&E Building, Third and Main Streets, Louisville, Kentucky.

Business items to be acted upon at the Annual Meeting are (i) the election of three directors, (ii) the approval of PricewaterhouseCoopers LLP as independent auditors of the Company for 2004 and (iii) the transaction of any other business properly brought before the meeting. Additionally, we will report on the progress of LG&E and shareholders will have the opportunity to present questions of general interest.

We encourage you to read the proxy statement carefully and complete, sign and return your proxy in the envelope provided, even if you plan to attend the meeting. Returning your proxy to us will not prevent you from voting in person at the meeting, or from revoking your proxy and changing your vote at the meeting, if you are present and choose to do so.

If you plan to attend the Annual Meeting, please check the box on the proxy card indicating that you plan to attend the meeting. Please bring the Admission Ticket, which forms the top portion of the form of proxy, to the meeting with you. If you wish to attend the meeting but do not have an Admission Ticket, you will be admitted to the meeting after presenting personal identification and evidence of ownership.

The directors and officers of LG&E appreciate your continuing interest in the business of LG&E. We hope you can join us at the meeting.

Victor A. Staffieri

Chairman of the Board, President and

Chief Executive Officer

![]()

NOTICE OF ANNUAL MEETING OF SHAREHOLDERS

The Annual Meeting of Shareholders of Louisville Gas and Electric Company ("LG&E"), a Kentucky corporation, will be held in the Twelfth Floor Assembly Room at the LG&E Building, Third and Main Streets, Louisville, Kentucky, on Thursday July 8, 2004, at 3:00 p.m., local time. At the Annual Meeting, shareholders will be asked to consider and vote upon the following matters, which are more fully described in the accompanying proxy statement:

- 1.

- A proposal to elect three directors for terms expiring in 2005;

- 2.

- A proposal to approve and ratify the appointment of PricewaterhouseCoopers LLP as independent auditors of LG&E for 2004; and

- 3.

- Such other business as may properly come before the meeting.

The close of business on May 3, 2004 has been fixed by the Board of Directors as the record date for determination of shareholders entitled to notice of and to vote at the Annual Meeting or any adjournment thereof.

You are cordially invited to attend the annual meeting.WHETHER OR NOT YOU PLAN TO ATTEND THE ANNUAL MEETING, PLEASE COMPLETE, SIGN, DATE AND RETURN YOUR PROXY IN THE REPLY ENVELOPE AS SOON AS POSSIBLE. Your cooperation in signing and promptly returning your proxy is greatly appreciated.

By Order of the Board of Directors,

John R. McCall, Secretary

Louisville Gas and Electric Company

220 West Main Street

Louisville, Kentucky 40202

June 25, 2004

ANNUAL MEETING OF SHAREHOLDERS TO BE HELD JULY 8, 2004

The Board of Directors of Louisville Gas and Electric Company ("LG&E" or the "Company") hereby solicits your proxy, and asks that you vote, sign, date and promptly mail the enclosed proxy card for use at the Annual Meeting of Shareholders to be held July 8, 2004, and at any adjournment of such meeting. The meeting will be held in the Twelfth Floor Assembly Room of the LG&E Building, Third and Main Streets, Louisville, Kentucky. This proxy statement and the accompanying proxy were first mailed to shareholders on or about June 25, 2004.

If you plan to attend the meeting, please check the box on the proxy card indicating that you plan to attend the meeting. Also, please bring the Admission Ticket, which forms the top portion of the form of proxy, to the meeting with you. Shareholders who do not have an Admission Ticket, including beneficial owners whose accounts are held by brokers or other institutions, will be admitted to the meeting upon presentation of personal identification and, in the case of beneficial owners, proof of ownership.

The outstanding stock of LG&E is divided into three classes: Common Stock, Preferred Stock (without par value), and Preferred Stock, par value $25 per share. At the close of business on May 3, 2004, the record date for the Annual Meeting, the following shares of four series of such classes were outstanding:

| Common Stock, without par value | 21,294,223 shares | |

| Preferred Stock, par value $25 per share, 5% Series | 860,287 shares | |

| Preferred Stock, without par value $5.875 Series | 237,500 shares | |

| Auction Series A (stated value $100 per share) | 500,000 shares |

All of the outstanding LG&E Common Stock is owned by LG&E Energy LLC ("LG&E Energy"). Based on information contained in a Schedule 13G originally filed with the Securities and Exchange Commission in October 1998, AMVESCAP PLC, a parent holding company, reported certain holdings in excess of five percent of LG&E's Preferred Stock. AMVESCAP PLC, with offices at 1315 Peachtree Street, N.W., Atlanta, Georgia 30309, and certain of its subsidiaries reported sole voting and dispositive power as to no shares and shared voting and dispositive power as to 43,000 shares of LG&E Preferred Stock, without par value, $5.875 Series, representing 17.2% of that class of Preferred Stock. The reporting companies indicated that they hold the shares on behalf of other persons who have the right to receive or the power to direct the receipt of dividends or the proceeds of sales of the shares. No other persons or groups are known by management to be beneficial owners of more than five percent of LG&E's Preferred Stock.

As of May 3, 2004, all directors, nominees for director and executive officers of LG&E as a group beneficially owned no shares of LG&E Preferred Stock and less than 1% of E.ON AG shares, the ultimate parent company of LG&E.

On December 11, 2000, Powergen plc, a public limited company with registered offices in England and Wales ("Powergen") completed its acquisition of LG&E Energy Corp., then the parent corporation of LG&E and Kentucky Utilities Company ("KU" and, collectively with LG&E, the "Companies"), for cash of approximately$3.2 billion, or$24.85 per share of LG&E Energy Corp. common stock. In connection with such transaction, certain officers and directors of Powergen were appointed to fill vacancies in the Board of Directors of LG&E occurring by resignation of prior directors. In January 2003, Powergen was reregistered as Powergen Limited.

1

On July 1, 2002, E.ON AG, a German corporation ("E.ON"), completed the acquisition of Powergen. In connection with such transaction, certain officers or directors of E.ON and Powergen were appointed to fill vacancies in the Board of Directors of LG&E occurring by resignation of prior directors.

On December 30, 2003, LG&E Energy LLC became the successor, by assignment and subsequent merger, to the assets and liabilities of LG&E Energy Corp.

Required Vote

Owners of record at the close of business on May 3, 2004 of LG&E Common Stock and the 5% Cumulative Preferred Stock, par value $25 per share (the "5% Preferred Stock") are entitled to one vote per share for each matter presented at the Annual Meeting or any adjournment thereof. In addition, each shareholder has cumulative voting rights with respect to the election of directors. Accordingly, in electing directors, each shareholder is entitled to as many votes as the number of shares of stock owned multiplied by the number of directors to be elected. All such votes may be cast for a single nominee or may be distributed among two or more nominees. The persons named as proxies reserve the right to cumulate votes represented by proxies that they receive and to distribute such votes among one or more of the nominees at their discretion.

You may revoke your proxy at any time before it is voted by giving written notice of its revocation to the Secretary of LG&E, by delivery of a later dated proxy, or by attending the Annual Meeting and voting in person. Signing a proxy does not preclude you from attending the meeting in person.

Directors are elected by a plurality of the votes cast by the holders of LG&E's Common Stock and 5% Preferred Stock at a meeting at which a quorum is present. "Plurality" means that the individuals who receive the largest number of votes cast are elected as directors up to the maximum number of directors to be chosen at the meeting. Consequently, any shares not voted (whether by withholding authority, broker non-vote or otherwise) have no impact on the election of directors except to the extent the failure to vote for an individual results in another individual receiving a larger percentage of votes.

The affirmative vote of a majority of the shares of LG&E Common Stock and 5% Preferred Stock represented at the Annual Meeting is required for the approval of the independent auditors and any other matters that may properly come before the meeting. Abstentions from voting on any such matter are treated as votes against, while broker non-votes are treated as shares not voted.

LG&E Energy owns all of the outstanding LG&E Common Stock (representing approximately 96% of the LG&E shares entitled to vote on these proposals), and intends to vote this stock for the nominees for directors as set forth below, thereby ensuring their election to the Board. LG&E Energy also intends to vote all of the outstanding LG&E Common Stock in favor of the appointment of PricewaterhouseCoopers LLP as the independent auditors for LG&E. Nonetheless, the Board encourages you to vote on each of these matters, and appreciates your interest.

The Louisville Gas and Electric Company 2003 Financial Report, containing audited financial statements of LG&E and management's discussion of such financial statements, is included with this proxy statement (the "Financial Report"), and is incorporated by reference herein. All shareholders are urged to read the accompanying Financial Report.

2

PROPOSAL NO. 1

The number of members of the Board of Directors of LG&E is currently fixed at three, pursuant to the Company's By-Laws and resolutions adopted by the Board of Directors. Generally, directors are elected at each year's Annual Meeting to serve for one-year terms and to continue in office until their successors are elected and qualified.

Effective July 1, 2002, in connection with the completion of the E.ON-Powergen acquisition, Sir Frederick Crawford, Dr. David K-P Li and Messrs. Nicholas P. Baldwin, Sydney Gillibrand and David J. Jackson resigned as directors of LG&E. Messrs. Victor A. Staffieri and Edmund A. Wallis continued as directors and Mr. Michael Söhlke was appointed to fill a vacancy. Effective June 18, 2003, Edmund A. Wallis tendered his resignation, resulting in a Board of two persons. On November 3, 2003, Dr. Hans Michael Gaul was appointed to fill this vacancy and Messrs. John R. McCall and S. Bradford Rives were also appointed directors. Messrs. McCall and Rives tendered their resignations in November 2003. At the 2003 Annual Meeting held on December 16, 2003, LG&E's shareholders approved amendments previously recommended by the Board which reduced the required number of directors from nine to three and eliminated staggered terms for directors.

Effective January 31, 2004, Dr. Gaul and Mr. Söhlke resigned from the Board of LG&E and Messrs. McCall and Rives were appointed to fill the vacancies created thereby.

At this Annual Meeting, the following three persons are proposed for election to the Board of Directors:

For one-year terms expiring at the 2005 Annual Meeting: Victor A. Staffieri, John R. McCall and S. Bradford Rives.

Messrs. Staffieri, McCall and Rives are presently also directors of LG&E Energy and KU.

The Board of Directors does not know of any nominee who will be unable to stand for election or otherwise serve as a director. If for any reason any nominee becomes unavailable for election, the Board of Directors may designate a substitute nominee, in which event the shares represented on the proxy cards returned to LG&E will be voted for such substitute nominee, unless an instruction to the contrary is indicated on the proxy card.

THE BOARD OF DIRECTORS RECOMMENDS THAT YOU VOTE "FOR" THE ELECTION OF THE THREE NOMINEES FOR DIRECTOR.

3

INFORMATION ABOUT DIRECTORS AND NOMINEES

The following contains certain information concerning the nominees for director:

Nominees for Directors with Terms Expiring at the 2005 Annual Meeting of Shareholders

Victor A. Staffieri(Age 49): Mr. Staffieri is Chairman, President and Chief Executive Officer of LG&E Energy, LG&E and KU, serving from April 2001 to the present. He served as President and Chief Operating Officer of LG&E Energy, LG&E and KU from February 1999 to April 2001; Chief Financial Officer of LG&E Energy and LG&E, May 1997 to February 2000; Chief Financial Officer of KU, May 1998 to February 2000. President, Distribution Services Division of LG&E Energy, December 1995 to May 1997; Senior Vice President, General Counsel and Public Policy of LG&E Energy and LG&E from November 1992 to December 1993. Mr. Staffieri has been a director of LG&E Energy, LG&E and KU since April 2001 and of Powergen from April 2001 until January 2004.

John R. McCall(Age 60): Mr. McCall is Executive Vice President, General Counsel and Secretary of LG&E Energy and Executive Vice President, General Counsel and Corporate Secretary of LG&E and KU. Mr. McCall has held these positions at LG&E Energy and LG&E since July 1994 and at KU since May 1998. Mr. McCall has been a director of LG&E and KU since January 2004.

S. Bradford Rives(Age 45): Mr. Rives is Chief Financial Officer of LG&E Energy, LG&E and KU, serving from September 2003 until the present. He served as Senior Vice President—Finance and Controller of LG&E Energy, LG&E and KU from December 2000 until September 2003; Senior Vice President—Finance and Business Development of LG&E Energy and LG&E from February 1999 to December 2000; and Vice President—Finance and Controller of LG&E Energy and LG&E from March 1996 to February 1999. Mr. Rives has been a director of LG&E and KU since January 2004.

INFORMATION CONCERNING THE BOARD OF DIRECTORS

Each member of the Board of Directors of LG&E is also a director of LG&E Energy and KU, as described above.

During 2003, there were a total of 18 meetings or consents of the LG&E and KU Boards. All directors attended 75% or more of the total number of meetings or consents of the Board of Directors and committees of the Board on which they served.

Compensation of Directors

Directors who are also officers or employees of E.ON, Powergen, LG&E Energy or their subsidiaries receive no compensation in their capacities as directors of LG&E or KU.

Committees

There are currently no committees of the Board of Directors of LG&E. Due to the small Board size of three members, the Board as a whole performs the functions related to audit or nominating committees.

In July 2002, upon completion of the E.ON-Powergen acquisition, the structures of the LG&E and KU Boards were changed to recognize practical and administrative efficiencies. The LG&E and KU Boards and LG&E Energy Board, respectively, adopted resolutions providing that (i) the functions of the former Audit Committee would be performed by the LG&E and KU Boards as a whole and (ii) certain functions of the former Remuneration Committee under certain LG&E Energy executive compensation plans would be performed by the Senior Vice President—Corporate Executive Human Resources of E.ON, currently Dr. Stefan Vogg.

4

Audit and Auditor Matters

Due to the small size of the LG&E Board, the Board as a whole performs the functions associated with an audit committee. The Board has determined that each of Victor A. Staffieri and S. Bradford Rives is an audit committee financial expert as defined by Item 401(h) of Regulation S-K. All members of the Board are officers or employees of LG&E and therefore are not independent within the meaning of Item 7(d)(3)(iv) of Schedule 14A of the Securities Exchange Act of 1934.

During 2003, the Board maintained direct and indirect contact with the independent auditors and LG&E's internal Audit Services to review the following matters pertaining to LG&E: the adequacy of accounting and financial reporting procedures; the adequacy and effectiveness of internal accounting controls; the scope and results of the annual audit and any other matters relative to the audit of LG&E's accounts and financial affairs that the Board, Audit Services or the independent auditors deemed necessary. A report of the Board acting as Audit Committee is included in the "Report of 2003 Audit Committee" section of this document. A copy of the charter applicable to the Board acting as Audit Committee is attached as Appendix A hereto.

The Board is responsible for approving all audit and permissible non-audit services to be provided by the independent auditors in accordance with LG&E's Pre-Approval Policy. Under the policy, the Board annually reviews and pre-approves the services that may be provided by the independent auditor. These include audit services, audit-related services, tax services and some permissible non-audit services, up to designated fee or budget levels. New services or services exceeding these levels will require separate pre-approval by the Board. Under the policy, the Board may delegate pre-approval authority to one or more of its members, subject to reporting of any decisions by such member to the Board, or may rely upon certain annual or other pre-approvals by the E.ON AG Audit Committee under its policy, subject to certain reporting to the Board.

Nominations

Due to the small size of the Board and the fact that LG&E Energy owns all of LG&E's common stock and approximately 96% of its voting stock, the Board has determined that it is appropriate not to have a standing nominating committee, nominating committee charter or policy regarding consideration of candidates for director, including shareholder nominees. The full Board, with input from E.ON officers, selects director nominees. All members of the Board are officers or employees of LG&E and therefore are not independent within the meaning of Item 7(d)(2)(ii)(D) of Schedule 14A of the Securities Exchange Act of 1934.

Nominations for the election of directors may be made by the Board, a committee thereof or by shareholders entitled to vote in the election of directors generally. Shareholder nominations must provide timely written notice in writing to LG&E's Secretary in accordance with the procedures set forth in the section "Shareholder Proposals and Nominations" of this document. The Board's chairman may void the nomination of any candidate for election which was not made in compliance with applicable procedures.

5

PROPOSAL NO. 2

APPROVAL OF INDEPENDENT AUDITORS FOR 2004

The Board of Directors, subject to ratification by shareholders, has selected PricewaterhouseCoopers LLP as independent auditors to audit the accounts of LG&E for the fiscal year ending December 31, 2004. The firm was originally selected as independent auditors for the Company effective April 30, 2001, following the completion of the Powergen-LG&E Energy merger in December 2000. PricewaterhouseCoopers has audited the accounts of E.ON and Powergen for many years. PricewaterhouseCoopers has audited the accounts of E.ON and Powergen for many years.

Representatives of PricewaterhouseCoopers LLP are expected to be present at the annual meeting and available to respond to questions and will be given the opportunity to make a statement, if they so desire.

As previously stated, LG&E Energy intends to vote all of the outstanding shares of common stock of the Company in favor of approval of the appointment of PricewaterhouseCoopers LLP as independent auditors, and since LG&E Energy's ownership of such common stock represents over 96% of the voting power of the Company, the approval of such independent auditors is assured.

THE BOARD OF DIRECTORS RECOMMENDS THAT YOU VOTE "FOR" THE APPROVAL OF THE APPOINTMENT OF THE INDEPENDENT AUDITORS.

6

Following the July 1, 2002 completion of E.ON's acquisition of Powergen, the Remuneration Committee of the Boards of Directors of LG&E and KU was terminated. As stated above, the LG&E Energy, LG&E and KU Boards adopted resolutions providing that certain functions of the former Remuneration Committee under certain executive compensation plans would be performed by the Senior Vice President—Corporate Executive Human Resources of E.ON, currently Dr. Stefan Vogg. This report describes the compensation policies applicable to LG&E's executive officers for the last completed fiscal year.

Prior to 2003, Dr. Vogg, in consultation with certain officers of E.ON, Powergen, LG&E Energy, LG&E and KU, including members of LG&E's Board of Directors (collectively, the "Compensation Group"), arrived at decisions regarding the compensation of LG&E's executive officers, including the setting of base pay levels for 2003, and the administration and determination of awards under the E.ON Group Stock Option Program (the "E.ON SAR Plan") and the LG&E Energy Corp. Performance Unit Plan (the "Long-Term Plan") and of payments under the Short-Term Incentive Plan (the "Short-Term Plan") as applicable to LG&E.

LG&E's executive compensation program and the target awards and opportunities for executives are designed to be competitive with the compensation and pay programs of comparable companies, including utilities, utility holding companies and companies in general industry, where appropriate. The executive compensation program has been developed and implemented over time through consultation with, and upon the recommendations of, recognized executive compensation consultants. The Compensation Group and the Board of Directors have continued access to such consultants as desired, and are provided with independent compensation data for their review.

Set forth below is a report addressing LG&E's compensation policies during 2003 for its officers, including the executive officers named in the following tables. In many cases, the executive officers also serve in similar capacities for affiliates of LG&E, including LG&E Energy and KU. For each of the executive officers of LG&E, the policies and amounts discussed below are for all services to LG&E, KU and their affiliates, during the relevant period.

Compensation Philosophy

During 2003, LG&E's executive compensation program had three major components: (1) base salary; (2) short-term or annual incentives; and (3) long-term incentives. This executive compensation program was developed to focus on both short-term and long-term business objectives that are designed to enhance overall shareholder value. The short-term and long-term incentives were premised on the belief that the interests of executives should be closely aligned with those of shareholders. Based on this philosophy, these two portions of each executive's total compensation package were linked to the accomplishment of specific results that were designed to benefit shareholders in both the short-term and long-term.

The executive compensation program also recognized that compensation practices must be competitive not only with utilities and utility holding companies, but also with companies in general industry to ensure that a stable and successful management team can be recruited and retained.

Pursuant to this competitive market positioning philosophy, in establishing compensation levels for all executive positions for 2003, the Compensation Group reviewed competitive compensation information for United States general industry companies with revenue of approximately $3 billion (the "Survey Group") and established targeted total direct compensation (base salary plus short-term incentives and long-term incentives) for each executive for 2003 to generally approach the 50th percentile of the competitive range from the Survey Group. Salaries, short-term incentives and long-term incentives for 2003 are described below. (The utilities and utility holding companies that

7

were in the Survey Group were not necessarily the same as those in the Dow Jones Utility Average used in the Company Performance Graph in this proxy statement.)

The 2003 compensation information set forth in other sections of this document, particularly with respect to the tabular information presented, reflects the considerations set forth in this report. The Base Salary, Short-Term Incentives, and Long-Term Incentives sections that follow address the compensation philosophy for 2003 for all executive officers except those serving as Chief Executive Officer. The compensation of the Chief Executive Officer is discussed below under the heading "Chief Executive Officer Compensation."

Base Salary

The base salaries for LG&E's executive officers for 2003 were designed to be competitive with the Survey Group at approximately the 50th percentile of the base salary range for executives in similar positions with companies in the Survey Group. Actual base salaries were determined based on a combination of market position, individual performance and experience.

Short-Term Incentives

The Short-Term Plan provided for Company Performance Awards and Individual Performance Awards, each of which is expressed as a percentage of base salary and each of which is determined independent of the other. The Compensation Group established the performance goals for the Company Performance Awards and Individual Performance Awards at the beginning of the 2003 performance year. Payment of Company Performance Awards for executive officers was based on varying performance measures tied to each officer's responsible areas. These measures and goals included, among others, LG&E Energy internal operating profit targets and LG&E/KU internal operating profit targets. The Compensation Group retains discretion to adjust the measures and goals as deemed appropriate. Payment of Individual Performance Awards was based 100% on management effectiveness. As stated, the awards varied within the executive officer group based upon the nature of each individual's functional responsibilities.

For 2003, the Company Performance Award targets for named executive officers ranged from 29% to 42% of base salary, and the Individual Performance Award targets ranged from 20% to 28% of base salary. Both awards were established to be competitive with the 50th percentile of such awards granted to comparable executives employed by companies in the Survey Group. The individual officers were eligible to receive from 0% to 175% of their targeted Company Performance Award amounts, dependent upon Company performance as measured by the relevant performance goals, and were eligible to receive from 0% to 175% of their targeted Individual Performance Award amounts dependent upon individual performance as measured by management effectiveness.

Using the relevant E.ON, Powergen, LG&E Energy, LG&E/KU and other subsidiaries' performance against goals in 2003 and making adjustments for certain foreign currency rate effects, the Compensation Group determined relative annual performance against targets for Company Performance Awards. Based upon this determination, Company Performance Awards for 2003 to the named executive officers were paid ranging from 119% to 159% of target and 36% to 67% of base salary. Based on determinations of management effectiveness, payouts for Individual Performance Awards to the named executive officers ranged from 150% to 165% of target and 30% to 48% of base salary.

Long-Term Incentives

The Compensation Group determines the competitive long-term grants under the Long-Term Plan and the E.ON SAR Plan to be awarded for each executive based on the long-term awards for the 50th percentile of the Survey Group. The aggregate expected value of the awards is intended to approach

8

the expected value of long-term incentives payable to executives in similar positions with companies in the 50th percentile of the Survey Group, depending upon achievement of targeted Company performance.

In 2003, the Compensation Group granted performance units under the Long-Term Plan to executive officers and senior management and stock appreciation rights ("SAR's") under the E.ON SAR Plan to executive officers. The amounts of the executive's long-term award to be delivered in SAR's and performance units were 25% and 75% respectively. Under the Long-Term Plan, the future value of grants of performance units is dependent upon company performance against a value-added target. The ultimate value of the performance unit can range from 0% to 150% of grant. Under the E.ON SAR Plan, the amount paid to executives when they exercise their SAR's, after satisfaction of vesting and performance criteria, is the difference between E.ON's stock price at the time of exercise and the stock price at the time of issuance, multiplied by the number of SAR's exercised. The price at issuance is the average of the XETRA closing quotations for E.ON stock during the December prior to issuance. The future value of the 2003 grants of SAR's was substantially dependent upon the changing value of E.ON shares in the marketplace.

No SAR's were exercisable during 2003 as the two year vesting requirements had not been completed. No regular payouts of performance units under the Long-Term Plan occurred during 2003 as the three-year performance periods had not been completed.

Other

In connection with the E.ON-Powergen merger, Messrs. Staffieri and McCall entered into amendments to their employment and severance agreements and the other named officers entered into new retention and severance agreements.

Chief Executive Officer Compensation

Mr. Victor A. Staffieri was appointed Chief Executive Officer of LG&E and KU effective May 1, 2001. Mr. Staffieri's compensation was governed by the terms of an Employment and Severance Agreement entered into on February 25, 2000 as amended (including upon his appointment as Chief Executive Officer) (the "2000 Agreement"). The 2000 Agreement was for an initial term of two years commencing on December 11, 2000, with automatic annual extensions thereafter unless the Companies or Mr. Staffieri give notice of non-renewal.

The 2000 Agreement established the minimum levels of Mr. Staffieri's base compensation, although the Chairman of E.ON retains discretion to increase such compensation. In the first quarter of 2003, the Compensation Group established Mr. Staffieri's compensation and long-term awards using comparisons to relevant officers of companies in the Survey Group, including utilities, and survey data from various compensation consulting firms. Mr. Staffieri also received Company contributions to the savings plan, similar to those of other officers and employees. Details of Mr. Staffieri's 2003 compensation are set forth below.

Base Salary. Mr. Staffieri was paid a total base salary of$648,902 during 2003, pursuant to the 2000 Agreement, as amended. The Compensation Group, in determining Mr. Staffieri's 2003 annual salary, including the minimum, considered his individual performance in the prior growth of LG&E Energy and the comparative compensation data described above.

Short-Term Incentives. Mr. Staffieri's short-term incentive target award as Chief Executive Officer was 70% of his 2003 base salary. As with other executive officers receiving short-term incentive awards, Mr. Staffieri was eligible to receive more or less than the targeted amount, based on Company performance and individual performance. His 2003 short-term incentive payouts were based 60% on

9

achievement of Company Performance Award targets and 40% on achievement of Individual Performance Award targets.

For 2003, the Company Performance Award payout for Mr. Staffieri was 158% of target and 67% of his 2003 base salary and the Individual Performance Award payout was 170% of target and 48% of his 2003 base salary. Mr. Staffieri's Company Performance Award was based on LG&E Energy internal operating profit. His Company Performance Award was calculated based upon annual Company performance as described under the heading "Short-Term Incentives." In determining the Individual Performance Award, the Compensation Group considered Mr. Staffieri's effectiveness in several areas, including the financial and operational performance of LG&E Energy, LG&E, KU and other subsidiaries, Company growth and other measures.

Long-Term Incentive Grant. In 2003, Mr. Staffieri received 851,681 performance units for the 2003-2005 performance period under the Long-Term Plan and 25,282 SAR's under the E.ON SAR Plan. These amounts were determined pursuant to the terms of his 2000 Agreement, as amended, with an aggregate expected value representing approximately 175% of his base salary. The terms of the performance units and SAR's for Mr. Staffieri are the same as for other executive officers, as described under the heading "Long-Term Incentives."

Long-Term Incentive Payout. As with other executive officers, no SAR's were exercisable by Mr. Staffieri during 2003 as the two year vesting requirements had not been completed. As with other executive officers, no regular payouts of performance units under the Long-Term Plan occurred during 2003 as the three-year performance periods had not been completed.

Other. In 2003, Mr. Staffieri also received a bonus in connection with a 2002 amendment to his employment and severance agreement in the amount of $837,375, including interest.

Members of LG&E's Board of Directors

Victor A. Staffieri

John R. McCall

S. Bradford Rives

10

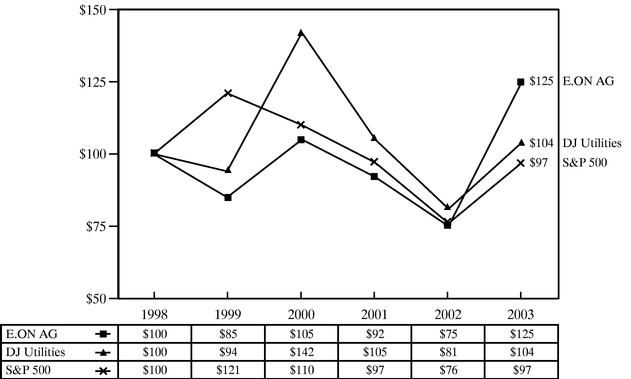

All of the outstanding Common Stock of LG&E is owned by LG&E Energy and, accordingly, there are no trading prices for LG&E's Common Stock. During 2003, all of the common stock or membership interests of LG&E Energy were indirectly owned by E.ON. The following graph reflects a comparison of the cumulative total return (change in stock price plus reinvested dividends) to holders of American Depositary Shares ("ADS's") of E.ON from December 31, 1998, through December 31, 2003, with the Standard & Poor's 500 Composite Index and the Dow Jones' Utility Average. The comparisons in this table are required by the Securities and Exchange Commission and, therefore, are not intended to forecast or be indicative of possible future performance.

COMPARISON OF FIVE YEAR CUMULATIVE

TOTAL SHAREHOLDER RETURN (1)

DATA POINTS (IN $)

- (1)

- Total Shareholder Return assumes $100 invested on December 31, 1998, with reinvestment of dividends.

- 1

- While similar, the utilities and holding companies that were in the Survey Group were not necessarily the same as those in the Dow Jones' Utility Average used in the Company Performance Graph.

11

EXECUTIVE COMPENSATION AND OTHER INFORMATION

The following table shows the cash compensation paid or to be paid by LG&E, KU or LG&E Energy, as well as certain other compensation paid or accrued for those years, to the Chief Executive Officer and the next four highest compensated executive officers of LG&E who were serving as such at December 31, 2003, as required, in all capacities in which they served LG&E, KU, LG&E Energy or its subsidiaries during 2001, 2002 and 2003:

| | | | | | Long-Term Compensation | | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | Annual Compensation | Awards | | | | ||||||||||||

| | Payouts | | |||||||||||||||

| | | | | Other Annual Comp. ($) | Restricted Stock Awards ($) | All Other Compen- sation ($) | |||||||||||

| Name and Principal Position | Year | Salary ($) | Bonus ($) | Securities Underlying Options/SAR (#)(1) | LTIP Payouts ($)(2) | ||||||||||||

Victor A. Staffieri Chairman of the Board, President and Chief Executive Officer | 2003 2002 2001 | 648,902 630,001 555,769 | 741,340 650,101 529,330 | 39,461 24,282 45,704 | — — — | 25,282 6,250 51,011 | 0 1,483,377 0 | 902,945 2,433,735 1,811,703 | (3) (4) (5) | ||||||||

John R. McCall Executive Vice President, General Counsel and Corporate Secretary | 2003 2002 2001 | 389,475 363,975 383,365 | 313,933 251,543 242,104 | 198,681 144,756 8,732 | (6) (6) | — — — | 8,671 3,611 14,786 | 0 401,580 0 | 47,529 1,390,557 463,793 | (3) (4) (5) | |||||||

S. Bradford Rives Chief Financial Officer | 2003 2002 2001 | 305,495 280,019 235,000 | 243,607 180,145 131,342 | 6,880 6,616 6,595 | — — — | 5,345 2,877 7,554 | 0 204,450 0 | 423,923 486,491 390,335 | (3) (4) (5) | ||||||||

Paul W. Thompson Senior Vice President— Energy Services | 2003 2002 2001 | 269,071 262,497 245,193 | 187,526 147,944 142,650 | 7,232 8,106 9,970 | — — — | 4,792 2,604 10,714 | 0 290,000 0 | 10,151 440,486 436,152 | (3) (4) (5) | ||||||||

Chris Hermann Senior Vice President Energy Delivery | 2003 2002 2001 | 252,928 246,748 234,999 | 166,267 129,505 131,342 | 4,905 7,892 12,122 | — — — | 3,378 2,448 7,554 | 0 204,450 0 | 22,463 228,722 13,996 | (3) (4) (5) | ||||||||

- (1)

- Amounts for years 2003 and 2002 reflect E.ON SAR Plan grants. Amounts for year 2001 reflect options for Powergen ADS's.

- (2)

- No payouts were made under the Long-Term Plan during years 2003 or 2002 as the three-year performance periods had not been completed. Amounts for year 2002 reflect acceleration of open performance periods upon the change in control event resulting from the Powergen shareholders' approval of the E.ON transaction.

- (3)

- Includes employer contributions to 401(k) plan, nonqualified thrift plan, employer paid life insurance premiums, vacation sell back, and retention payments in 2003 as follows: Mr. Staffieri $6,000, $32,970, $26,600, $0 and $837,375, respectively; Mr. McCall $5,775, $13,680, $20,583, $7,491 and $0, respectively; Mr. Rives $3,229, $11,478, $1,042, $4,618 and $403,556, respectively; Mr. Thompson, $2,688, $5,384, $2,078, $0 and $0, respectively; and Mr. Hermann, $5,732, $5,886, 5,981, $4,864 and $0, respectively. The retention payments above are discussed in the "Report Regarding Remuneration" and "Employment Contracts and Termination of Employment Arrangements and Change in Control Provisions".

12

- (4)

- Includes retention payments in 2002 as follows: Mr. Staffieri, $2,349,170; Mr. McCall, $1,346,416; Mr. Rives, $87,746; Mr. Thompson, $425,926; and Mr. Hermann, $211,342, respectively.

- (5)

- Includes retention payments in 2001 as follows: Mr. Staffieri, $1,719,884; Mr. McCall, $423,524; Mr. Rives, $382,393; Mr. Thompson, $405,860; and Mr. Hermann, $0, respectively.

- (6)

- Includes financial planning, automobile, spouse travel, dues, overseas compensation and tax payments in 2003 ($1,500, $4,000, $7,202, $0, $0 and $178,445) and 2002 ($2,000, $7,586, $50,589, $240, $36,398 and $48,143) respectively.

OPTION/SAR GRANTS TABLE

Option/SAR Grants in 2003 Fiscal Year

The following table contains information at December 31, 2003, with respect to grants of E.ON AG stock appreciation rights ("SAR's") to the named executive officers:

| | Individual Grants | | | | | | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | Number of Securities Underlying Options/SARs Granted (#)(1) | Percent of Total Options/SARs Granted to Employees in Fiscal Year(2) | | Potential Realizable Value At Assumed Annual Rates of Stock Price Appreciation For Option Term | ||||||||||

| | Exercise Or Base Price ($/Share) | |||||||||||||

| Name | Expiration Date | 0%($) | 5%($) | 10%($) | ||||||||||

| Victor A. Staffieri | 25,282 | 36.1 | % | 43.99 | 12/31/2009 | 0 | 452,759 | 1,055,121 | ||||||

| John R. McCall | 8,671 | 12.4 | % | 43.99 | 12/31/2009 | 0 | 155,283 | 361,876 | ||||||

| S. Bradford Rives | 5,345 | 7.6 | % | 43.99 | 12/31/2009 | 0 | 95,720 | 223,069 | ||||||

| Paul W. Thompson | 4,792 | 6.9 | % | 43.99 | 12/31/2009 | 0 | 85,817 | 199,990 | ||||||

| Chris Hermann | 3,378 | 4.8 | % | 43.99 | 12/31/2009 | 0 | 60,494 | 140,978 | ||||||

- (1)

- E.ON SAR's were awarded with an exercise price at issuance equal to the average XETRA closing quotations for E.ON stock during the December prior to issuance. The SAR's are exercisable over a seven-year period from their issuance date.

- (2)

- Represents percentage grants to LG&E Energy, LG&E and KU employees only.

13

OPTION/SAR EXERCISES AND YEAR-END VALUE TABLE

Aggregated Option/SAR Exercises in 2003 Fiscal Year

And FY-End Option/SAR Values

The following table sets forth information with respect to the named executive officers concerning the value of unexercised E.ON SAR's held by them as of December 31, 2003:

| Name | Shares Acquired On Exercise (#)(1) | Value Realized ($) | Number of Securities Underlying Unexercised Options/SARs at FY-End (#)(2) Exercisable/Unexercisable | Value of Unexercised In-The-Money Options/SARs at FY-End ($) Exercisable/Unexercisable | |||||

|---|---|---|---|---|---|---|---|---|---|

| Victor A. Staffieri | 0 | 0 | 0/31,532 | 0/$ | 640,924 | ||||

| John R. McCall | 0 | 0 | 0/12,282 | 0/$ | 242,975 | ||||

| S. Bradford Rives | 0 | 0 | 0/8,222 | 0/$ | 160,049 | ||||

| Paul W. Thompson | 0 | 0 | 0/7,396 | 0/$ | 143,880 | ||||

| Chris Hermann | 0 | 0 | 0/5,826 | 0/$ | 111,088 | ||||

- (1)

- Amounts shown are E.ON SAR's. At December 31, 2003, no E.ON SAR's were exercisable due to the two year vesting period from their 2002 or 2003 grant dates.

LONG-TERM INCENTIVE PLAN AWARDS TABLE

Long-Term Incentive Plan Awards in 2003 Fiscal Year

The following table provides information concerning awards of performance units made in 2003 to the named executive officers under the Powergen Long-Term Plan.

| | Number of Shares, Units or Other Rights(1) | Performance or Other Period Until Maturation Or Payout | Estimated Future Payouts Under Non-Stock Price Based Plans (number of shares)(1) | |||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Name | Threshold(#) | Target(#) | Maximum(#) | |||||||

| Victor A. Staffieri | 851,681 | 12/31/2005 | 425,841 | 851,681 | 1,277,522 | |||||

| John R. McCall | 292,106 | 12/31/2005 | 146,053 | 292,106 | 438,159 | |||||

| S. Bradford Rives | 180,090 | 12/31/2005 | 90,045 | 180,090 | 270,135 | |||||

| Paul W. Thompson | 161,445 | 12/31/2005 | 80,723 | 161,445 | 242,168 | |||||

| Chris Hermann | 113,816 | 12/31/2005 | 56,908 | 113,816 | 170,724 | |||||

- (1)

- Amounts shown are awards of performance units under the Long-Term Plan during 2003.

Each performance unit awarded under the Long-Term Plan represented the right to receive an amount payable in cash on the date of payout. The amount of the payout is determined by the company performance over a three year cycle. For awards made in 2003, the Long-Term Plan awards were intended to reward executives on a three-year rolling basis dependent upon the achievement of a value-added target by LG&E Energy.

Pension Plans

The following table shows the estimated pension benefits payable to a covered participant at normal retirement age under LG&E Energy's qualified defined benefit pension plans, as well as non-qualified supplemental pension plans that provide benefits that would otherwise be denied participants by reason of certain Internal Revenue Code limitations for qualified plan benefits, based on the remuneration that is covered under the plan and years of service with LG&E Energy and its subsidiaries:

14

2003 PENSION PLAN TABLE

| | | Years of Service | | ||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | Remuneration | 15 | 20 | 25 | 30 or more | | |||||||||||

| $ | 100,000 | $ | 43,348 | $ | 43,348 | $ | 43,348 | $ | 43,348 | ||||||||

| $ | 200,000 | $ | 107,348 | $ | 107,348 | $ | 107,348 | $ | 107,348 | ||||||||

| $ | 300,000 | $ | 171,348 | $ | 171,348 | $ | 171,348 | $ | 171,348 | ||||||||

| $ | 400,000 | $ | 235,348 | $ | 235,348 | $ | 235,348 | $ | 235,348 | ||||||||

| $ | 500,000 | $ | 299,348 | $ | 299,348 | $ | 299,348 | $ | 299,348 | ||||||||

| $ | 600,000 | $ | 363,348 | $ | 363,348 | $ | 363,348 | $ | 363,348 | ||||||||

| $ | 700,000 | $ | 427,348 | $ | 427,348 | $ | 427,348 | $ | 427,348 | ||||||||

| $ | 800,000 | $ | 491,348 | $ | 491,348 | $ | 491,348 | $ | 491,348 | ||||||||

| $ | 900,000 | $ | 555,348 | $ | 555,348 | $ | 555,348 | $ | 555,348 | ||||||||

| $ | 1,000,000 | $ | 619,348 | $ | 619,348 | $ | 619,348 | $ | 619,348 | ||||||||

| $ | 1,100,000 | $ | 683,348 | $ | 683,348 | $ | 683,348 | $ | 683,348 | ||||||||

| $ | 1,200,000 | $ | 747,348 | $ | 747,348 | $ | 747,348 | $ | 747,348 | ||||||||

| $ | 1,300,000 | $ | 811,348 | $ | 811,348 | $ | 811,348 | $ | 811,348 | ||||||||

| $ | 1,400,000 | $ | 875,348 | $ | 875,348 | $ | 875,348 | $ | 875,348 | ||||||||

| $ | 1,500,000 | $ | 939,348 | $ | 939,348 | $ | 939,348 | $ | 939,348 | ||||||||

| $ | 1,600,000 | $ | 1,003,348 | $ | 1,003,348 | $ | 1,003,348 | $ | 1,003,348 | ||||||||

| $ | 1,700,000 | $ | 1,067,348 | $ | 1,067,348 | $ | 1,067,348 | $ | 1,067,348 | ||||||||

| $ | 1,800,000 | $ | 1,131,348 | $ | 1,131,348 | $ | 1,131,348 | $ | 1,131,348 | ||||||||

| $ | 1,900,000 | $ | 1,195,348 | $ | 1,195,348 | $ | 1,195,348 | $ | 1,195,348 | ||||||||

A participant's remuneration covered by the Retirement Income Plan (the "Retirement Income Plan") is his or her average base salary and short-term incentive payment (as reported in the Summary Compensation Table) for the five calendar plan years during the last ten years of the participant's career for which such average is the highest. The years of service for each named executive employed by LG&E Energy at December 31, 2003 was as follows: 11 years for Mr. Staffieri; 9 years for Mr. McCall; 20 years for Mr. Rives; 12 years for Mr. Thompson; and 33 years for Mr. Hermann. Benefits shown are computed as a straight life single annuity beginning at age 65.

Current Federal law prohibits paying benefits under the Retirement Income Plan in excess of$160,000 per year. Officers of LG&E Energy, LG&E and KU with at least one year of service with an affiliated company are eligible to participate in LG&E Energy's Supplemental Executive Retirement Plan (the "Supplemental Executive Retirement Plan"), which is an unfunded supplemental plan that is not subject to the$160,000 limit. Presently, participants in the Supplemental Executive Retirement Plan consist of all of the eligible officers of LG&E Energy, LG&E and KU. This plan provides generally for retirement benefits equal to 64% of average current earnings during the highest 36 consecutive months prior to retirement, reduced by Social Security benefits, by amounts received under the Retirement Income Plan and by benefits from other employers. As with all other officers, Mr. Staffieri participates in the Supplemental Executive Retirement Plan described above.

Estimated annual benefits to be received under the Retirement Income Plan and the Supplemental Executive Retirement Plan upon normal retirement at age 65 and after deduction of Social Security benefits will be $702,523 for Mr. Staffieri; $344,984 for Mr. McCall; $251,425 for Mr. Rives; $241,419 for Mr. Thompson; and $208,324 for Mr. Hermann.

15

EMPLOYMENT CONTRACTS AND TERMINATION OF EMPLOYMENT

ARRANGEMENTS AND CHANGE IN CONTROL PROVISIONS

In connection with the E.ON-Powergen merger, Messrs. Staffieri and McCall entered into amendments to their employment and severance agreements. The original agreements, effective upon the LG&E Energy-Powergen merger for two year terms, contained change in control provisions and the benefits described below. Pursuant to the amended agreements, Mr. Staffieri received certain retention payments in 2003, as described in the Report Regarding Remuneration and the Summary Compensation Table.

Under the terms of his revised employment and severance agreement, Mr. Staffieri is entitled to additional retention payments of $800,570, plus interest, on each of July 1, 2004 and January 1, 2005, (the two year and thirty month anniversaries of the E.ON-Powergen merger), which will initially be credited into a deferred compensation account and which will then be payable in a lump sum in cash, if Mr. Staffieri elects, upon (i) a termination of employment (other than by Mr. Staffieri without good reason), (ii) a change in control within 30 months of the E.ON-Powergen merger, or (iii) the respective first year, second year and thirty month anniversaries of the E.ON-Powergen merger, if Mr. Staffieri is still employed. If during the term of his agreement, which is automatically extended for subsequent one year terms unless terminated upon 90 days notice, and within twenty four months following a change in control, Mr. Staffieri's employment is terminated for reasons other than cause, disability or death, or for good reason, Mr. Staffieri shall be entitled to a severance amount equal to 2.99 times the sum of (1) his annual base salary and (2) his bonus or "target" award paid or payable. If during the term of his agreement but prior to a change in control, Mr. Staffieri's employment is terminated for reasons other than cause, disability or death, or for good reason, Mr. Staffieri will be entitled an amount equal to two times his annual base salary and target annual bonus.

Under the terms of his revised employment and severance agreement, if Mr. McCall is (a) employed by LG&E Energy or LG&E or any of their affiliates on July 1, 2004 or (b) terminated prior to July 1, 2004 for any reason other than by the employer for cause or by Mr. McCall without good reason; then in each case Mr. McCall is entitled to receive a lump sum cash payment equal to his annual salary plus target annual bonus. If during the term of his agreement, which is automatically extended for subsequent one year terms unless terminated upon 90 days notice, and within twenty four months following a change in control or within forty-eight months of the E.ON- Powergen merger, Mr. McCall's employment is terminated for reasons other than cause, disability or death, or for good reason, Mr. McCall shall be entitled to a severance amount equal to 2.99 times the sum of (1) his annual base salary and (2) his bonus or "target" award paid or payable, or, if within 48 months of the date of the E.ON-Powergen merger, 2.99 times the sum of (1) and (2).

In 2003, Mr. Rives became entitled to receive a scheduled retention payment of $355,078, plus interest, pursuant to the terms his retention agreement entered into at the time of the Powergen-LG&E Energy merger. During 2002, in connection with the E.ON-Powergen merger, Messrs. Thompson, Rives and Hermann entered into new retention agreements under which these officers will be entitled to a payment equal to the sum of (1) his annual base salary and (2) his annual bonus or "target" award, in the event of their continued employment through the second anniversary of the E.ON-Powergen merger. Messrs. Thompson, Rives and Hermann have also entered into change of control agreements with terms of 24 months, which provide that, in the event of termination of employment for reasons other than cause, disability or death, or for good reason within the 24 months following a change in control, these officers shall be entitled to a severance amount equal to 2.99 times the sum of (1) his annual base salary and (2) his bonus or "target" award paid or payable.

Pursuant to the employment and other agreements described above, payments may be made to executives which would equal or exceed an amount which would constitute a nondeductible payment pursuant to Section 280G of the Code, if any. Additionally, executives receive continuation of certain

16

welfare benefits and payments in respect of accrued but unused vacation days and for out-placement assistance. A change in control encompasses certain merger and acquisition events, changes in board membership and acquisitions of voting securities.

EQUITY COMPENSATION PLAN INFORMATION

The executive officers of LG&E and KU do not participate in any compensation plans under which equity securities of LG&E, KU or any affiliate are authorized for issuance.

REPORT ON 2003 AUDIT COMMITTEE MATTERS

The Board of Directors, consisting of three members, performed the functions of an Audit Committee ("Audit Committee"). The Audit Committee is governed by a charter adopted by the Board of Directors, which sets forth the responsibilities of the Audit Committee members. The Audit Committee held one meeting during 2003.

The financial statements of Louisville Gas and Electric Company and Subsidiary are prepared by management, which is responsible for their objectivity and integrity. With respect to the financial statements for the calendar year ended December 31, 2003, the Audit Committee reviewed and discussed the audited financial statements and the quality of the financial reporting with management and the independent accountants. It also discussed with the independent accountants the matters required to be discussed by Statement on Auditing Standards No. 61,Communication with Audit Committees, as amended, and received and discussed with the independent accountants the matters in the written disclosures required by Independence Standards Board Standard No. 1,Independence Discussions with Audit Committees.

Based upon the reviews and discussions referred to above, the Audit Committee recommended to the Board of Directors the inclusion of the audited financial statements in Louisville Gas and Electric Company's Annual Report on Form 10-K for the year ended December 31, 2003, for filing with the Securities and Exchange Commission.

The following information on independent audit fees and services is being provided in compliance with the Securities and Exchange Commission rules on auditor independence.

1. PricewaterhouseCoopers LLP fees for the periods ended December 31, 2002 and December 31, 2003 are as follows: (Certain amounts for 2002 have been reclassified to conform to 2003 presentation.)

| | LG&E | ||||||

|---|---|---|---|---|---|---|---|

| | 2003 | 2002 | |||||

| • Audit Fees | |||||||

| • Audit Fees | $ | 128,862 | $ | 47,500 | |||

| • Regulatory Work | $ | 4,665 | — | ||||

| • Total Audit Fees | $ | 131,527 | $ | 47,500 | |||

| • Audit Related Fees | |||||||

| • Pension Plan Audits | $ | 17,200 | $ | 17,000 | |||

| • Comfort Letter Procedures | $ | 51,154 | $ | 69,270 | |||

| • Total Audit Related Fees | $ | 68,354 | $ | 86,270 | |||

| • Tax Fees | — | — | |||||

• All Other Fees | — | — | |||||

2. The Audit Committee considered whether the independent accountant's provision of non-audit services is compatible with maintaining the accountant's independence.

17

3. The Audit Committee has been advised by PricewaterhouseCoopers LLP that hours expended on the audit engagement were entirely performed by PricewaterhouseCoopers' personnel.

This report has been provided by the Board of Directors performing the functions of the Audit Committee.

Victor A. Staffieri, Chairman

John R. McCall

S. Bradford Rives

SECTION 16(A) BENEFICIAL OWNERSHIP REPORTING

LG&E has in place procedures to assist its directors and officers in complying with Section 16(a) of the Exchange Act of 1934, which includes assisting the director or officer in preparing forms for filing. However, due to administrative errors arising from the transition from overseas directors to US-based directors, two reports were filed late or omitted regarding personnel changes in November 2003 and January 2004. All such errors related solely to entry or exit filings for individuals who had no holdings of or transactions in LG&E securities. Except as set forth above, based upon information provided to LG&E and KU by individual directors and officers, LG&E believes that during the year ended December 31, 2003, all filing requirements have otherwise been complied with.

SHAREHOLDER PROPOSALS AND NOMINATIONS

Any shareholder may submit a proposal for consideration at the 2005 Annual Meeting. Any shareholder desiring to submit a proposal for inclusion in the proxy statement for consideration at the 2005 Annual Meeting should forward the proposal so that it will be received at LG&E's principal executive offices no later than February 26, 2005. Proposals received by that date that are proper for consideration at the Annual Meeting and otherwise conform to the rules of the Securities and Exchange Commission will be included in the 2005 proxy statement.

Under LG&E's By-laws, shareholders intending to nominate a director for election or submit a proposal in person at the annual meeting must provide advance written notice along with other prescribed information. In general, such notice must be received by the Secretary of LG&E (a) not less than 90 days prior to the meeting date or (b) if the meeting date is not publicly announced more than 100 days prior to the meeting, by the tenth day following such announcement.

To be proper, written notice for a director nominee must generally include (a) the name and address of the shareholder and of each nominee, (b) a representation that the shareholder is a holder of record entitled to vote at such meeting and intends to appear in person or by proxy, (c) a description of all arrangements between the shareholder and each nominee, (d) such other information regarding each nominee as would be required to be included in a proxy statement under the Securities and Exchange Commission rules had the nominee been nominated by the Board and (e) the consent of the each nominee to serve if elected. Proposals not properly submitted will be considered untimely.

Shareholders can communicate with our Board by submitting a letter or writing addressed to a director care of: John R. McCall, Secretary, Louisville Gas and Electric Company, P.O. Box 32102, 220 West Main Street, Louisville, KY 40232. The Secretary may initially review communications with directors and transmit a summary to the directors, but has discretion to exclude from transmittal any communications that are commercial advertisements or other forms of solicitation or individual service or billing complaints (although all communications are available to the directors upon request). The Secretary will forward to the directors any communications raising substantial issues.

18

We encourage all directors to attend our annual meeting. Two of our three directors were in attendance at the annual meeting in 2003.

At the annual meeting, it is intended that the first two items set forth in the accompanying notice and described in this proxy statement will be presented. Should any other matter be properly presented at the Annual Meeting, the persons named in the accompanying proxy will vote upon them in accordance with their best judgment. Any such matter must comply with those provisions of LG&E's Articles of Incorporation requiring advance notice for new business to be acted upon at the meeting. The Board of Directors knows of no other matters that may be presented at the meeting.

LG&E will bear the costs of printing and preparing this proxy solicitation. LG&E will provide copies of this proxy statement, the accompanying proxy and the Financial Report to brokers, dealers, banks and voting trustees, and their nominees, for mailing to beneficial owners, and upon request therefore, will reimburse such record holders for their reasonable expenses in forwarding solicitation materials. In addition to using the mails, proxies may be solicited by directors, officers and regular employees of LG&E, in person or by telephone.

Any shareholder may obtain without charge a copy of LG&E's Annual Report on Form 10-K, as filed with the Securities and Exchange Commission for the year 2003 by submitting a request in writing to: John R. McCall, Secretary, Louisville Gas and Electric Company, P.O. Box 32010, 220 West Main Street, Louisville, Kentucky 40232.

19

LOUISVILLE GAS AND ELECTRIC COMPANY

AND

KENTUCKY UTILITIES COMPANY

AUDIT COMMITTEE CHARTER

Mission Statement

The Audit Committee (the "Committee") is a Committee, respectively, of the Boards of Directors (each, separately, the "Board") of Louisville Gas and Electric Company and of Kentucky Utilities Company (each, separately, the "Company"). Its primary function is to assist the Board in fulfilling its oversight responsibilities by reviewing the financial information provided to shareholders and others, the systems of internal controls which management and the Board of Directors have established and the audit process. Although operating as a combined Committee, actions of the Committee related to an individual Company only are applicable to such Company only, as appropriate.

Composition

The Committee will be composed of at least three members of the Board of Directors who shall serve at the pleasure of the Board. In the event that the Board of Directors does not appoint a Committee, the functions of the Committee shall be performed by the Board of Directors or its members.

Audit Committee members will be appointed by the Board of Directors. One of the members will be designated as the Committee's Chairman. The Chairman will preside over the Committee meetings and report Committee actions to the Board of Directors.

Meetings

The Committee will meet on a regular basis and will call special meetings as circumstances require. It will meet privately with the Director of Audit Services and the independent public accountant in separate executive sessions to discuss any matters that the Committee, the Director of Audit Services, or the independent accountant believes should be discussed privately. The Committee may ask members of management or others to attend meetings and provide pertinent information, as necessary.

Responsibilities

- 1.

- Provide an open avenue of communication between the internal auditors, the independent accountant, and the Board of Directors.

- 2.

- Review and update, where appropriate, the Committee's charter annually.

- 3.

- Recommend to the Board of Directors on an annual basis the independent accountant to be nominated, approve the compensation of the independent accountant, and review and approve the discharge of the independent accountant. The independent accountant is ultimately responsible to the Board of Directors and the Audit Committee.

- 4.

- Pre-approve the audit and non-audit services performed by the independent accountant as prescribed under the Sarbanes-Oxley Act of 2002, and related regulations of the Securities and Exchange Commission.

- 5.

- Review and concur in the appointment, replacement, reassignment or dismissal of the Director of Audit Services.

A-1

- 6.

- Require the independent accountant to submit to the Committee on a periodic basis a formal written statement regarding independence of such independent accountant and all facts and circumstances relevant thereto; discuss with the independent accountant its independence; confirm and assure the independence of the Audit Services Department and the independent accountant, including a review of management consulting services and related fees provided by the independent accountant; and recommend to the Board of Directors actions necessary to ensure independence of the Audit Services Department and the independent accountant.

- 7.

- Inquire of management, the Director of Audit Services, and the independent accountant about significant risks or exposures and assess the steps management has taken to minimize such risk to the Company.

- 8.

- Approve the annual audit plan and review the three-year plan of the internal auditing function. Review the independent accountant's proposed audit plan, including coordination with Audit Services' annual audit plan.

- 9.

- Review with the Director of Audit Services and the independent accountant the coordination of audit effort to assure completeness of coverage, reduction of redundant efforts, and the effective use of audit resources.

- 10.

- Consider with management and the independent accountant the rationale for employing audit firms other than the principal independent accountant.

- 11.

- Consider and review with the independent accountant and the Director of Audit Services:

- a.

- The adequacy of the Company's internal controls, including computerized information system controls and security, and

- b.

- Any related significant issues identified by the independent accountant and Audit Services, together with management's responses thereto.

- 12.

- Review with management and the independent accountant at the completion of the annual audit:

- a.

- The Company's annual financial statements and related footnotes;

- b.

- The independent accountant's audit of the financial statements and the report thereon;

- c.

- The independent accountant's judgment about the quality and appropriateness of the Company's accounting principals as applied to its financial reporting;

- d.

- Any significant changes required in the independent accountant's audit plan and scope;

- e.

- Any serious difficulties or disputes with management encountered during the course of the audit; and

- f.

- Other matters related to the conduct of the audit which are to be communicated to the Committee under generally accepted auditing standards.

- 13.

- Review with management such appropriate notices or reports as may be required to be filed on behalf of the Committee with the regulatory authorities, exchanges or included in the Company's proxy materials or otherwise, pursuant to law or exchange regulations.

- 14.

- Consider and review with management and the Director of Audit Services:

- a.

- Any difficulties encountered in the course of their audits, including any restrictions on the scope of their work or access to required information;

- b.

- Any significant changes required in their audit plan;

- c.

- Any significant audit findings and management's responses thereto;

A-2

- d.

- The Audit Services Department staffing and staff qualifications; and

- e.

- The Audit Services Department charter.

- 15.

- Review with the Director of Audit Services the results of the annual Code of Business Conduct questionnaire.

- 16.

- Review legal and regulatory matters that may have a material impact on the financial statements, related Company compliance policies and programs, and reports received from regulators.

- 17.

- Report Committee actions to the Board of Directors with such recommendations as the Committee may deem appropriate.

- 18.

- Conduct or authorize investigations into any matters within the Committee's scope of responsibilities, and retain independent counsel, accountants or others to assist it in the conduct of any investigation.

- 19.

- Assume such other duties and considerations as may be delegated to the Committee by the Board of Directors, or required of the Committee upon the request of the Board of Directors from time to time pursuant to a duly adopted resolution of the Board of Directors.

A-3

LOUISVILLE GAS AND ELECTRIC COMPANY

LOUISVILLE GAS AND ELECTRIC COMPANY

2003 FINANCIAL REPORT

| Index of Abbreviations | 2 | |

Selected Financial Data | 4 | |

Management's Discussion and Analysis | 5 | |

Market for the Registrant's Common Equity and Related Stockholder Matters | 25 | |

Consolidated Statements of Income | 26 | |

Consolidated Statements of Retained Earnings | 26 | |

Consolidated Statements of Comprehensive Income | 27 | |

Consolidated Balance Sheets | 28 | |

Consolidated Statements of Cash Flows | 29 | |

Consolidated Statements of Capitalization | 30 | |

Notes to Consolidated Financial Statements | 31 | |

Report of Management | 62 | |

Report of Independent Auditors | 63 |

1

| AFUDC | Allowance for Funds Used During Construction | |

| ARO | Asset Retirement Obligation | |

| Capital Corp. | LG&E Capital Corp. | |

| Clean Air Act | The Clean Air Act, as amended in 1990 | |

| CCN | Certificate of Public Convenience and Necessity | |

| CT | Combustion Turbines | |

| CWIP | Construction Work in Progress | |

| DSM | Demand Side Management | |

| ECR | Environmental Cost Recovery | |

| EEI | Electric Energy, Inc. | |

| EITF | Emerging Issues Task Force Issue | |

| E.ON | E.ON AG | |

| EPA | U.S. Environmental Protection Agency | |

| ESM | Earnings Sharing Mechanism | |

| F | Fahrenheit | |

| FAC | Fuel Adjustment Clause | |

| FERC | Federal Energy Regulatory Commission | |

| FGD | Flue Gas Desulfurization | |

| FPA | Federal Power Act | |

| FT and FT-A | Firm Transportation | |

| GSC | Gas Supply Clause | |

| IBEW | International Brotherhood of Electrical Workers | |

| IMEA | Illinois Municipal Electric Agency | |

| IMPA | Indiana Municipal Power Agency | |

| Kentucky Commission | Kentucky Public Service Commission | |

| KIUC | Kentucky Industrial Utility Consumers, Inc. | |

| KU | Kentucky Utilities Company | |

| KU Energy | KU Energy Corporation | |

| KU R | KU Receivables LLC | |

| kV | Kilovolts | |

| Kva | Kilovolt-ampere | |

| KW | Kilowatts | |

| Kwh | Kilowatt hours | |

| LEM | LG&E Energy Marketing Inc. | |

| LG&E | Louisville Gas and Electric Company | |

| LG&E Energy | LG&E Energy LLC (as successor to LG&E Energy Corp.) | |

| LG&E R | LG&E Receivables LLC | |

| LG&E Services | LG&E Energy Services Inc. | |

| Mcf | Thousand Cubic Feet | |

| MGP | Manufactured Gas Plant | |

| MISO | Midwest Independent Transmission System Operator | |

| Mmbtu | Million British thermal units | |

| Moody's | Moody's Investor Services, Inc. | |

| Mw | Megawatts | |

| Mwh | Megawatt hours | |

| NNS | No-Notice Service | |

| NOPR | Notice of Proposed Rulemaking | |

| NOx | Nitrogen Oxide | |

| OATT | Open Access Transmission Tariff | |

| OMU | Owensboro Municipal Utilities | |

| OVEC | Ohio Valley Electric Corporation | |

| PBR | Performance-Based Ratemaking | |

| PJM | Pennsylvania, New Jersey, Maryland Interconnection | |

| Powergen | Powergen Limited (formerly Powergen plc) | |

| PUHCA | Public Utility Holding Company Act of 1935 | |

2

| ROE | Return on Equity | |

| RTO | Regional Transmission Organization | |

| S&P | Standard & Poor's Rating Services | |

| SCR | Selective Catalytic Reduction | |

| SEC | Securities and Exchange Commission | |

| SERP | Supplemental Employee Retirement Plan | |

| SFAS | Statement of Financial Accounting Standards | |

| SIP | State Implementation Plan | |

| SMD | Standard Market Design | |

| SO2 | Sulfur Dioxide | |

| Tennessee Gas | Tennessee Gas Pipeline Company | |

| Texas Gas | Texas Gas Transmission LLC | |

| TRA | Tennessee Regulatory Authority | |

| Trimble County | LG&E's Trimble County Unit 1 | |

| USWA | United Steelworkers of America | |

| Utility Operations | Operations of LG&E and KU | |

| VDT | Value Delivery Team Process | |

| Virginia Commission | Virginia State Corporation Commission | |

| Virginia Staff | Virginia State Corporation Commission Staff | |

| WNA | Weather Normalization Adjustment |

3

Louisville Gas and Electric Company and Subsidiary

Selected Financial Data

The 1999 and 2000 consolidated financial data were derived from financial statements audited by Arthur Andersen LLP, independent accountants, who expressed an unqualified opinion on those financial statements in their report dated January 26, 2001, before the revisions required by EITF 02-03. Arthur Andersen LLP has ceased operations. The amounts shown below for such periods, reclassified pursuant to the adoption of EITF 02-03, are unaudited.

| | Years Ended December 31 | ||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | 2003 | 2002 | 2001 | 2000 | 1999 | ||||||||||||

| | (in thousands) | ||||||||||||||||

| LG&E: | |||||||||||||||||

| Operating revenues: | |||||||||||||||||

| Revenues | $ | 1,093,933 | $ | 992,079 | $ | 962,959 | $ | 934,204 | $ | 847,879 | |||||||

| Provision for rate collections (refunds) | (412 | ) | 11,656 | 1,588 | (2,500 | ) | (1,735 | ) | |||||||||

| Total operating revenues | $ | 1,093,521 | $ | 1,003,735 | $ | 964,547 | $ | 931,704 | $ | 846,144 | |||||||

Net operating income | $ | 122,685 | $ | 117,914 | $ | 141,773 | $ | 148,870 | $ | 140,091 | |||||||

Net income | $ | 90,839 | $ | 88,929 | $ | 106,781 | $ | 110,573 | $ | 106,270 | |||||||

Total assets | $ | 2,888,928 | $ | 2,768,930 | $ | 2,448,354 | $ | 2,226,084 | $ | 2,171,452 | |||||||

Long-term obligations (including amounts due within one year) | $ | 798,054 | $ | 616,904 | $ | 616,904 | $ | 606,800 | $ | 626,800 | |||||||

LG&E's Management's Discussion and Analysis of Financial Condition and Results of Operation and LG&E's. Notes to Financial Statements should be read in conjunction with the above information.

4

Louisville Gas and Electric Company and Subsidiary

Management's Discussion and Analysis of Financial Condition and Results of Operations

GENERAL

The following discussion and analysis by management focuses on those factors that had a material effect on LG&E's financial results of operations and financial condition during 2003, 2002, and 2001 and should be read in connection with the financial statements and notes thereto.

Some of the following discussion may contain forward-looking statements that are subject to certain risks, uncertainties and assumptions. Such forward-looking statements are intended to be identified in this document by the words "anticipate," "expect," "estimate," "objective," "possible," "potential" and similar expressions. Actual results may materially vary. Factors that could cause actual results to materially differ include: general economic conditions; business and competitive conditions in the energy industry; changes in federal or state legislation; unusual weather; actions by state or federal regulatory agencies; actions by credit rating agencies; and other factors described from time to time in LG&E's reports to the SEC, including Exhibit No. 99.01 to its report on Form 10-K.

EXECUTIVE SUMMARY

Overview

LG&E continues profitable operations despite national and regional economic weakness and turmoil in the U.S. energy industry. LG&E enjoys a competitive cost advantage relative to the U.S. industry average and high customer satisfaction ratings. During 2003, LG&E and KU (the "Companies") were awarded first place in the region by J.D. Power in the 2003 Residential Customer Satisfaction Survey and a national first place in the Midsize Business Survey.