UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D. C. 20549

FORM 10-K

(Mark One) |

ý | | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE |

| | SECURITIES EXCHANGE ACT OF 1934 (NO FEE REQUIRED) |

| | |

For the fiscal year ended December 31, 2005 |

| | |

OR |

| | |

o | | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE |

| | SECURITIES EXCHANGE ACT OF 1934 (NO FEE REQUIRED) |

Commission | | Registrant, State of Incorporation, | | IRS Employer |

File Number | | Address, and Telephone Number | | Identification Number |

| | | | |

1-2893 | | Louisville Gas and Electric Company | | 61-0264150 |

| | (A Kentucky Corporation) | | |

| | 220 West Main Street | | |

| | P. O. Box 32010 | | |

| | Louisville, Kentucky 40232 | | |

| | (502) 627-2000 | | |

| | | | |

1-3464 | | Kentucky Utilities Company | | 61-0247570 |

| | (A Kentucky and Virginia Corporation) | | |

| | One Quality Street | | |

| | Lexington, Kentucky 40507-1428 | | |

| | (859) 255-2100 | | |

| | | | |

| | Securities registered pursuant to section 12(g) of the Act: | | |

Louisville Gas and Electric Company |

5% Cumulative Preferred Stock, $25 Par Value |

$5.875 Cumulative Preferred Stock, Without Par Value |

Auction Rate Series A Preferred Stock, Without Par Value |

|

Kentucky Utilities Company |

none |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No ý

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No ý

Indicate by check mark whether the registrants (1) have filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrants were required to file such reports), and (2) have been subject to such filing requirements for the past 90 days. Yes ý No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ý

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12-b2 of the Exchange Act. (Check one):

Large accelerated filer o | Accelerated filer o | Non-accelerated filer ý |

Indicate by check mark whether the registrant is a shell company (as defined in Exchange Act Rule 12b-2). Yes o No ý

As of June 30, 2005, the aggregate market value of the common stock of each of Louisville Gas and Electric Company and Kentucky Utilities Company held by non-affiliates was $0. As of February 28, 2006, Louisville Gas and Electric Company had 21,294,223 shares of common stock outstanding, all held by E.ON U.S. LLC. Kentucky Utilities Company had 37,817,878 shares of common stock outstanding, all held by E.ON U.S. LLC.

This combined Form 10-K is separately filed by Louisville Gas and Electric Company and Kentucky Utilities Company. Information contained herein related to any individual registrant is filed by such registrant on its own behalf. Each registrant makes no representation as to information relating to the other registrant.

DOCUMENTS INCORPORATED BY REFERENCE

Not applicable.

INDEX OF ABBREVIATIONS

AEP | | American Electric Power Company, Inc. |

AFUDC | | Allowance for Funds Used During Construction |

AG | | Attorney General of Kentucky |

APBO | | Accumulated Postretirement Benefit Obligation |

ARO | | Asset Retirement Obligation |

CAIR | | Clean Air Interstate Rule |

CAMR | | Clean Air Mercury Rule |

Capital Corp. | | E.ON U.S. Capital Corp. (formerly LG&E Capital Corp.) |

CAVR | | Clean Air Visibility Rule |

Clean Air Act | | The Clean Air Act, as amended in 1990 |

CCN | | Certificate of Public Convenience and Necessity |

CO2 | | Carbon Dioxide |

Company | | LG&E or KU, as applicable |

Companies | | LG&E and KU |

CT | | Combustion Turbines |

CWIP | | Construction Work in Progress |

DOE | | Department of Energy |

DOJ | | Department of Justice |

DSM | | Demand Side Management |

ECAR | | East Central Area Reliability Region |

ECR | | Environmental Cost Recovery |

EEI | | Electric Energy, Inc. |

EITF | | Emerging Issues Task Force Issue |

E.ON | | E.ON AG |

E.ON U.S. | | E.ON U.S. LLC. (formerly LG&E Energy LLC and LG&E Energy Corp.) |

E.ON U.S. Services | | E.ON U.S. Services Inc. (formerly LG&E Energy Services Inc.) |

EPA | | U.S. Environmental Protection Agency |

EPAct 2005 | | Energy Policy Act of 2005 |

ERISA | | Employee Retirement Income Security Act of 1974, as amended |

ESM | | Earnings Sharing Mechanism |

Fidelia | | Fidelia Corporation (an E.ON affiliate) |

FAC | | Fuel Adjustment Clause |

FASB | | Financial Accounting Standards Board |

FERC | | Federal Energy Regulatory Commission |

FGD | | Flue Gas Desulfurization |

FIN | | FASB Interpretation |

FPA | | Federal Power Act |

FGD | | Flue Gas Desulfurization |

FIN | | FASB Interpretation |

FPA | | Federal Power Act |

FSP | | FASB Staff Position |

FT and FT-A | | Firm Transportation |

FTR | | Financial Transmission Right |

GSC | | Gas Supply Clause |

GFA | | Grandfathered Transmission Agreement |

IBEW | | International Brotherhood of Electrical Workers |

IMEA | | Illinois Municipal Electric Agency |

IMPA | | Indiana Municipal Power Agency |

IRC | | Internal Revenue Code of 1986, as amended |

IRP | | Integrated Resource Plan |

ITP | | Independent Transmission Provider |

Kentucky Commission | | Kentucky Public Service Commission |

KIUC | | Kentucky Industrial Utility Consumers, Inc. |

KU | | Kentucky Utilities Company |

KU Energy | | KU Energy Corporation |

KU R | | KU Receivables LLC |

Kv | | Kilovolts |

Kw | | Kilowatts |

Kwh | | Kilowatt hours |

LEM | | LG&E Energy Marketing Inc. |

LG&E | | Louisville Gas and Electric Company |

LG&E Energy | | LG&E Energy LLC (now E.ON U.S. LLC) |

LG&E R | | LG&E Receivables LLC |

LG&E Services | | LG&E Energy Services Inc. (now E.ON U.S. Services Inc.) |

LMP | | Locational Marginal Pricing |

LNG | | Liquefied Natural Gas |

Mcf | | Thousand Cubic Feet |

MGP | | Manufactured Gas Plant |

MISO | | Midwest Independent Transmission System Operator, Inc. |

MMBtu | | Million British thermal units |

Moody’s | | Moody’s Investor Services, Inc. |

Mva | | Megavolt-ampere |

Mw | | Megawatts |

Mwh | | Megawatt hours |

NNS | | No-Notice Service |

NOPR | | Notice of Proposed Rulemaking |

NOx | | Nitrogen Oxide |

OATT | | Open Access Transmission Tariff |

OMU | | Owensboro Municipal Utilities |

OVEC | | Ohio Valley Electric Corporation |

PBR | | Performance-Based Ratemaking |

PJM | | Pennsylvania, New Jersey, Maryland Interconnection |

Powergen | | Powergen Limited (formerly Powergen plc) |

PUHCA 1935 | | Public Utility Holding Company Act of 1935 |

PUHCA 2005 | | Public Utility Holding Company Act of 2005 |

ROE | | Return on Equity |

RTO | | Regional Transmission Organization |

RTOR | | Regional Through and Out Rates |

S&P | | Standard & Poor’s Rating Services |

SCR | | Selective Catalytic Reduction |

SEC | | Securities and Exchange Commission |

SERP | | Supplemental Executive Retirement Plan |

SFAS | | Statement of Financial Accounting Standards |

SIP | | State Implementation Plan |

SMD | | Standard Market Design |

SO2 | | Sulfur Dioxide |

SPP | | Southwest Power Pool, Inc. |

TEMT | | Transmission and Energy Markets Tariff |

Tennessee Gas | | Tennessee Gas Pipeline Company |

Texas Gas | | Texas Gas Transmission LLC |

Trimble County | | LG&E’s Trimble County Unit 1 |

TVA | | Tennessee Valley Authority |

USWA | | United Steelworkers of America |

Utility Operations | | Operations of LG&E and KU |

VDT | | Value Delivery Team Process |

Virginia Commission | | Virginia State Corporation Commission |

Virginia Staff | | Virginia State Corporation Commission Staff |

WNA | | Weather Normalization Adjustment |

PART I

Item 1. Business.

LG&E and KU are each subsidiaries of E.ON U.S. LLC (E.ON U.S.). Prior to December 1, 2005, E.ON U.S. LLC was known as LG&E Energy LLC. Previously, effective December 30, 2003, LG&E Energy LLC had become the successor, by assignment and subsequent merger, to all the assets and liabilities of LG&E Energy Corp. E.ON U.S. is a subsidiary of E.ON AG (E.ON), a German corporation. E.ON acquired LG&E Energy through its July 1, 2002 acquisition of Powergen plc, now Powergen Limited (Powergen), a United Kingdom company and holding company for E.ON UK plc, E.ON’s United Kingdom market unit operating parent. As contemplated in their regulatory filings in connection with the E.ON acquisition, E.ON, Powergen and E.ON U.S. completed an administrative reorganization to move the E.ON U.S. group from an indirect Powergen subsidiary to an indirect E.ON subsidiary. This reorganization was effective in March 2003. In early 2004, E.ON U.S. began direct reporting arrangements to E.ON.

LG&E and KU are now indirect subsidiaries of E.ON. As a result of these acquisitions and otherwise, E.ON and E.ON U.S. anticipate registering as holding companies under PUHCA 2005 and were formerly registered holding companies under PUHCA 1935.

In order to comply with PUHCA 1935, E.ON U.S. Services (formerly LG&E Energy Services), which was formed as a subsidiary service company of E.ON U. S., provides services to affiliated entities, including LG&E and KU, at cost as permitted under PUHCA 1935 and PUHCA 2005.

E.ON, its utility subsidiaries, including LG&E and KU, and certain of its non-utility subsidiaries are subject to certain regulation by the FERC under the FPA, PUHCA 2005 and the EPAct 2005, including with respect to record-keeping and reporting, acquisitions and sales of utility securities and properties, financial matters, and intra-system sales of goods and services. LG&E and KU believe that they have adequate authority (including financing authority) under existing FERC orders and regulations to conduct their business. LG&E and KU will seek additional authorization when necessary.

The utility operations (LG&E and KU) of E.ON U.S. have continued their separate identities as LG&E and KU. The preferred stock and debt securities of LG&E and KU were not affected by these transactions.

1

LOUISVILLE GAS AND ELECTRIC COMPANY

General

LG&E, incorporated in 1913 in Kentucky, is a regulated public utility that supplies natural gas to approximately 321,000 customers and electricity to approximately 394,000 customers in Louisville and adjacent areas in Kentucky. LG&E’s service area covers approximately 700 square miles in 17 counties and has an estimated population of one million. Included in this area is the Fort Knox Military Reservation, to which LG&E transports natural gas and provides electric service, but does not provide any distribution services. LG&E also provides natural gas service in limited additional areas. LG&E’s coal-fired electric generating plants, all equipped with systems to reduce SO2 emissions, produce most of LG&E’s electricity. The remainder is generated by a hydroelectric power plant and combustion turbines. Underground natural gas storage fields help LG&E provide economical and reliable natural gas service to customers. See Item 2, Properties.

Operating Revenues

For the year ended December 31, 2005, 69% of total operating revenues were derived from electric operations and 31% from natural gas operations. Electric and gas operating revenues and the percentages by class of service on a combined basis for this period were as follows:

(in millions) | | Electric | | Gas | | Combined | | % Combined | |

Residential | | $ | 276 | | $ | 265 | | $ | 541 | | 49 | % |

Commercial | | 221 | | 108 | | 329 | | 30 | % |

Industrial | | 128 | | 19 | | 147 | | 13 | % |

Public authorities | | 66 | | 19 | | 85 | | 8 | % |

Total retail | | 691 | | 411 | | 1,102 | | 100 | % |

Wholesale sales | | 259 | | 19 | | 278 | | | |

Gas transported | | — | | 5 | | 5 | | | |

Miscellaneous | | 37 | | 2 | | 39 | | | |

Total | | $ | 987 | | $ | 437 | | $ | 1,424 | | | |

See Note 12 of LG&E’s Notes to Financial Statements under Item 8 for financial information concerning segments of business for the three years ended December 31, 2005.

Electric Operations

The sources of LG&E’s electric operating revenues and the volumes of sales for the three years ended December 31, 2005, were as follows:

(in millions) | | 2005 | | 2004 | | 2003 | |

ELECTRIC OPERATING REVENUES | | | | | | | |

Residential | | $ | 276 | | $ | 241 | | $ | 223 | |

Commercial | | 221 | | 202 | | 188 | |

Industrial | | 128 | | 120 | | 112 | |

Public authorities | | 66 | | 62 | | 58 | |

Total retail | | 691 | | 625 | | 581 | |

Wholesale sales | | 259 | | 185 | | 170 | |

Provision for rate collections (refunds) | | — | | (11 | ) | (1 | ) |

Miscellaneous | | 37 | | 17 | | 18 | |

Total | | $ | 987 | | $ | 816 | | $ | 768 | |

2

(Thousands of Mwh) | | | | | | | |

ELECTRIC SALES | | | | | | | |

Residential | | 4,265 | | 3,923 | | 3,835 | |

Commercial | | 3,682 | | 3,534 | | 3,482 | |

Industrial | | 3,077 | | 3,019 | | 2,936 | |

Public authorities | | 1,268 | | 1,248 | | 1,251 | |

Total retail | | 12,292 | | 11,724 | | 11,504 | |

Wholesale sales | | 8,704 | | 7,819 | | 7,678 | |

Total | | 20,996 | | 19,543 | | 19,182 | |

LG&E set an annual peak load of 2,754 Mw on July 25, 2005, when the temperature reached 98 degrees Fahrenheit in Louisville. This was the highest hourly customer demand in LG&E’s history.

The electric utility business is affected by seasonal weather patterns. As a result, operating revenues (and associated operating expenses) are not generated evenly throughout the year. See LG&E’s Results of Operations under Item 7.

LG&E and KU currently maintain a 12% - 14% reserve margin range. At December 31, 2005, LG&E owned steam and combustion turbine generating facilities with a net summer capability of 3,105 Mw and an 80 Mw nameplate-rated hydroelectric facility on the Ohio River with a net summer capability of 48 Mw. See Item 2, Properties. LG&E also obtains power from other utilities under bulk power purchase and interchange contracts. At December 31, 2005, LG&E’s system net summer capability, including purchases from others and excluding the hydroelectric facility, was 3,259 Mw.

LG&E uses efficient coal-fired boilers, fully equipped with SO2 removal systems, to generate most of its electricity. LG&E’s weighted-average system-wide emission rate for SO2 in 2005 was approximately 0.54 lbs./MMBtu of heat input, with every generating unit below its emission limit established by the Kentucky Division for Air Quality.

LG&E and 11 other electric utilities are participating owners of OVEC, located in Piketon, Ohio. OVEC owns and operates two power plants that burn coal to generate electricity, Kyger Creek Station in Ohio and Clifty Creek Station in Indiana. LG&E owns 5.63% of OVEC’s common stock. Through March 2006, LG&E is entitled to receive 7% of OVEC’s output, and thereafter is entitled to receive 5.63%, representing approximately 124 Mw. In April 2004, OVEC and its shareholders, including LG&E and KU, entered into an Amended and Restated Inter-Company Power Agreement, to be effective beginning March 2006, upon the expiration of the current power contract among the parties. The parties received SEC approval under PUHCA 1935 of the Amended and Restated Inter-Company Power Agreement in February 2005.

LG&E is a member of the MISO, a non-profit independent transmission system operator that serves the electrical transmission needs of much of the Midwest. Membership was obtained when the MISO was formed in 1998 in response to and consistent with federal energy policy initiatives at that time. The MISO began commercial operations in February 2002. As a result, LG&E turned over operational control of its 100 Kv and above transmission facilities, but continues to control and operate the lower voltage transmission system subject to the terms and conditions of the MISO. As a transmission-owning member of the MISO, LG&E incurs costs under the MISO OATT. In April 2005, the MISO implemented its day-ahead real-time market (MISO Day 2), including a congestion management system. At the present time, LG&E is involved in regulatory proceedings at the Kentucky Commission and the FERC seeking authority to exit the MISO. On March 17, 2006, the FERC issued an order conditionally approving the request of LG&E and KU to exit the MISO. For further discussion, see Note 16 of LG&E’s Notes to Financial Statements under Item 8.

3

Gas Operations

The sources of LG&E’s gas operating revenues and the volumes of sales for the three years ended December 31, 2005, were as follows:

(in millions) | | 2005 | | 2004 | | 2003 | |

GAS OPERATING REVENUES | | | | | | | |

Residential | | $ | 265 | | $ | 223 | | $ | 199 | |

Commercial | | 108 | | 89 | | 78 | |

Industrial | | 19 | | 15 | | 14 | |

Public authorities | | 19 | | 15 | | 14 | |

Total retail | | 411 | | 342 | | 305 | |

Wholesale sales | | 19 | | 7 | | 12 | |

Gas transported | | 5 | | 6 | | 6 | |

Miscellaneous | | 2 | | 2 | | 2 | |

Total | | $ | 437 | | $ | 357 | | $ | 325 | |

| | | | | | | |

(Millions of cu. ft.) | | | | | | | |

GAS SALES | | | | | | | |

Residential | | 20,801 | | 21,402 | | 23,192 | |

Commercial | | 9,131 | | 9,144 | | 9,652 | |

Industrial | | 1,711 | | 1,736 | | 1,880 | |

Public authorities | | 1,574 | | 1,646 | | 1,746 | |

Total retail | | 33,217 | | 33,928 | | 36,470 | |

Wholesale sales | | 2,652 | | 1,221 | | 2,119 | |

Gas transported | | 12,549 | | 13,692 | | 13,683 | |

Total | | 48,418 | | 48,841 | | 52,272 | |

The natural gas utility business is affected by seasonal weather patterns. As a result, operating revenues (and associated operating expenses) are not generated evenly throughout the year. While natural gas usage patterns are seasonal, LG&E received approval from the Kentucky Commission for a WNA mechanism. The WNA mechanism adjusts the distribution cost recovery component of the natural gas billings of residential and commercial customers to normal temperatures during the heating season months of November through April, somewhat mitigating the effect of weather extremes. LG&E requested, and the Kentucky Commission approved, an extension of the current WNA mechanism through April 30, 2006. LG&E expects to file for another extension of the WNA before the next heating season begins in November 2006. See LG&E’s Results of Operations under Item 7.

LG&E has five underground natural gas storage fields that help provide economical and reliable natural gas service to ultimate consumers. By using natural gas storage facilities, LG&E avoids the costs associated with typically more expensive pipeline transportation capacity to serve peak winter space-heating loads. LG&E stores natural gas in the summer season for withdrawal in the subsequent winter heating season. Without its storage capacity, LG&E would be forced to buy additional natural gas and pipeline transportation services during the winter months when customer demand increases and when the prices for natural gas supply and transportation services are typically at their highest. Currently, LG&E buys competitively priced natural gas from several large suppliers under contracts of varying duration. LG&E’s underground storage facilities, in combination with its purchasing practices, enable it to offer natural gas sales service at rates generally lower than state and national averages. At December 31, 2005, LG&E had an inventory balance of gas stored underground of approximately 12.1 million Mcf of working gas valued at approximately $124.9 million.

4

A number of industrial customers purchase their natural gas requirements directly from alternate suppliers for delivery through LG&E’s distribution system. These large industrial customers account for approximately one-fourth of LG&E’s annual throughput.

During 2005, the maximum daily gas sendout was approximately 444,000 Mcf, occurring on January 17, 2005, when the average temperature for the day was 16 degrees Fahrenheit. Supply on that day consisted of approximately 221,000 Mcf from purchases, approximately 166,000 Mcf delivered from underground storage, and approximately 57,000 Mcf transported for industrial customers. For a further discussion, see Gas Supply under Item 1.

Rates and Regulation

Historically, E.ON, LG&E’s ultimate parent, has been a registered holding company under PUHCA 1935, and anticipates registering under PUHCA 2005. As a registered holding company, E.ON, its utility subsidiaries, including LG&E, and certain of its non-utility subsidiaries have been subject to extensive regulation by the SEC and the FERC with respect to numerous matters, including: electric utility facilities and operations, wholesale sales of power and related transactions, accounting practices, issuances and sales of securities, acquisitions and sales of utility properties, payments of dividends out of capital and surplus, financial matters and inter-system sales of non-power goods and services. In addition, PUHCA 2005 generally limited the ability of registered holding companies to acquire additional public utility systems and to acquire and retain businesses unrelated to the utility operations of the holding company. LG&E believes that it has adequate authority (including financing authority) under existing FERC orders and regulations to conduct its business and will seek additional authorization when necessary.

In August 2005, President Bush signed into law the EPAct 2005, significantly changing many federal statutes, repealing PUHCA 1935 as of February 8, 2006 and enacting PUHCA 2005. As part of the repeal of PUHCA 1935, the FERC was given more authority over the merger and acquisition of public utilities and more authority over the books and records of public utilities. Despite these increases in the FERC’s authority, LG&E believes that the repeal of PUHCA 1935 will lessen its regulatory burdens and provide more flexibility in the event of expansion.

Besides repealing PUHCA 1935, the EPAct 2005 is also expected to have substantial long-term effects on energy markets, energy investment and regulation of public utilities and holding company systems by the FERC and the DOE. The FERC and the DOE are in various stages of rulemaking in implementing the EPAct 2005. The precise impact of these rulemakings cannot be determined at this time.

The Kentucky Commission has regulatory jurisdiction over LG&E’s retail rates and service, and over the issuance of certain of its securities. The Kentucky Commission has the ability to examine the rates LG&E charges its retail customers at any time.

Pursuant to Kentucky law, the Kentucky Commission has established the boundaries of the service territory or area of each retail electric supplier in Kentucky (including LG&E), other than municipal corporations. Within this service territory, each such supplier has the exclusive right to render retail electric service.

5

LG&E’s retail electric rates contain an FAC, whereby increases and decreases in the cost of fuel for electric generation are reflected in the rates charged to retail electric customers. The Kentucky Commission requires public hearings at six-month intervals to examine past fuel adjustments, and at two-year intervals to review past operations of the fuel clause and transfer of the then current fuel adjustment charge or credit to the base charges. The Kentucky Commission also requires that electric utilities, including LG&E, file documents relating to fuel procurement and the purchase of power and energy from other utilities.

Prior to 2004, LG&E’s retail electric rates were subject to an ESM. LG&E and the Kentucky Commission agreed to a termination of the ESM relating to all periods after 2003. The ESM, initially in place for three years beginning in 2000, set an upper (12.5%) and lower (10.5%) limit for rate of return on equity. If earnings were above the upper limit, the excess earnings were shared 40% with ratepayers and 60% with shareholders; if earnings were below the lower limit, the earnings deficiency was recovered 40% from ratepayers and 60% from shareholders. By order of the Kentucky Commission, rate changes prompted by the ESM filing went into effect in April of each year subject to a balancing adjustment in successive periods. For discussion of current ESM matters, see Note 3 of LG&E’s Notes to Financial Statements under Item 8.

In June 2001, LG&E filed an application (“VDT case”) with the Kentucky Commission to create a regulatory asset relating to first quarter 2001 charges for a workforce reduction program. In December 2001, the Kentucky Commission approved a settlement in the VDT case and allowed LG&E to set up a regulatory asset of $141 million for the workforce reduction costs and begin amortizing these costs over a five year period starting in April 2001. The settlement reduced revenues by approximately $26 million through a surcredit on bills to ratepayers over the same five-year period. The surcredit represented net savings stipulated by LG&E. For discussion of current VDT matters, see Note 3 and Note 16 of LG&E’s Notes to Financial Statements under Item 8.

LG&E’s retail rates contain an ECR surcharge which recovers costs incurred by LG&E that are required to comply with the Clean Air Act and other environmental regulations. See Note 3 of LG&E’s Notes to Financial Statements under Item 8.

LG&E’s natural gas rates contain a GSC, whereby increases or decreases in the cost of natural gas supply are reflected in LG&E’s rates, subject to approval by the Kentucky Commission. The GSC procedure prescribed by order of the Kentucky Commission provides for quarterly rate adjustments to reflect the expected cost of natural gas supply in that quarter. In addition, the GSC contains a mechanism whereby any over- or under-recoveries of natural gas supply cost from prior quarters is to be refunded to or recovered from customers through the adjustment factor determined for subsequent quarters. In late 2005, as wholesale natural gas prices began to decrease, a monthly adjustment in the GSC was requested by LG&E and approved by the Kentucky Commission to pass the lower natural gas costs to the customers on a more timely basis.

Integrated resource planning regulations in Kentucky require LG&E and the other major utilities to make triennial filings with the Kentucky Commission of various historical and forecasted information relating to load, capacity margins and demand-side management techniques. LG&E filed its most recent IRP in April 2005. The AG and KIUC were granted intervention in the IRP proceeding. The Kentucky Commission issued its staff report on February 15, 2006, with no substantive issues noted and closed the case by Order dated February 24, 2006.

In December 2003, LG&E filed an application with the Kentucky Commission requesting adjustments in LG&E’s electric and natural gas rates. LG&E asked for general adjustments in electric and natural gas rates based on the twelve month test period ended September 30, 2003. The revenue increases requested were

6

approximately $64 million for electric and $19 million for gas. In June 2004, the Kentucky Commission issued an order approving increases in LG&E’s annual electric base rates of approximately $43 million (7.7%) and annual gas base rates of approximately $12 million (3.4%). The rate increases took effect on July 1, 2004.

Subsequently during 2004 and 2005, the AG conducted an investigation regarding the proceedings resulting in the rate increases. The AG requested information from LG&E and the Kentucky Commission and its staff regarding alleged improper communications between LG&E and the Kentucky Commission related to the rate proceedings. The AG also requested rehearing of the rate increase orders on the basis of these allegations, as well as calculational aspects of the increased rates. In February 2005, the AG submitted a confidential report on its investigation with the Kentucky Commission and filed a motion summarizing the report as containing evidence of improper communications and record-keeping errors by LG&E in respect of its activities with state governmental agencies, including the Kentucky Commission.

In December 2005, the Kentucky Commission issued an order noting completion of its inquiry, including review of the AG’s investigative report. The order concluded that no improper communications occurred during the rate proceedings. The order further established a procedural schedule through the first quarter of 2006 for considering the sole issue for which rehearing was granted: state income tax rates used in calculating the granted rate increases. This issue is estimated at less than $1 million annually. Upon resolution of this issue on rehearing, the initial rate increase orders could be subject to judicial appeal.

For a further discussion of regulatory matters, see Note 3 of LG&E’s Notes to Financial Statements under Item 8.

Construction Program and Financing

LG&E’s construction program is designed to ensure that there will be adequate capacity and reliability to meet the electric and natural gas needs of its service area. These needs are continually being reassessed and appropriate revisions are made, when necessary, in construction schedules. LG&E’s estimates of its construction expenditures can vary substantially due to numerous items beyond LG&E’s control, such as changes in interest rates, economic conditions, construction costs, and new environmental or other governmental laws and regulations.

During the five years ended December 31, 2005, gross property additions amounted to approximately $1 billion. Internally generated funds and external financings for the five-year period were utilized to provide for these gross additions. The gross additions during this period amounted to approximately 24% of total utility plant at December 31, 2005, and consisted of $807 million for electric properties and $164 million for natural gas properties. Gross retirements during the same period were $108 million, consisting of $81 million for electric properties and $27 million for natural gas properties.

Capital expenditures during the three years ending December 31, 2008, are estimated to be approximately $530 million. The major expenditures during this period relate to the development and construction of Trimble County Unit 2, of which LG&E’s portion totals approximately $120 million, and approximately $26 million for the redevelopment of the Ohio Falls hydro facility.

Coal Supply

Coal-fired generating units provided approximately 97% of LG&E’s net kilowatt-hour generation for 2005.

7

The remaining net generation for 2005 was provided by natural gas and oil-fueled combustion turbine peaking units and a hydroelectric plant. Coal is expected to be the predominant fuel used by LG&E in the foreseeable future, with natural gas and oil being used for peaking capacity and flame stabilization in coal-fired boilers or in emergencies. LG&E has no nuclear generating units and has no plans to build any in the foreseeable future.

LG&E maintains its fuel inventory at levels estimated to be necessary to avoid operational disruptions at its coal-fired generating units. Reliability of coal deliveries can be affected from time to time by a number of factors, including fluctuations in demand, coal mine production issues and other supplier or transporter operating difficulties.

LG&E has entered into coal supply agreements with various suppliers for coal deliveries for 2006 and beyond and normally augments its coal supply agreements with spot market purchases. LG&E has a coal inventory policy which it believes provides adequate protection under most contingencies. It had a coal inventory of approximately 1.1 million tons, or a 50-day supply, on hand at December 31, 2005.

LG&E expects to continue purchasing most of its coal, which has a sulfur content in the 2% - 4.5% range, from western Kentucky, southern Indiana, southern Illinois, Ohio and West Virginia for the foreseeable future. This supply is relatively low-priced coal, and in combination with its sulfur dioxide removal systems, is expected to enable LG&E to continue to provide electric service in compliance with existing environmental laws and regulations.

Coal is delivered to LG&E’s Mill Creek plant by rail and barge, Trimble County plant by barge and Cane Run plant by rail.

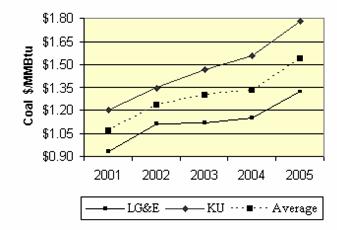

The historical average delivered cost of coal purchased and the percentage of spot coal purchases were as follows:

| | 2005 | | 2004 | | 2003 | |

Per ton | | $ | 30.37 | | $ | 26.25 | | $ | 25.56 | |

Per MMBtu | | $ | 1.32 | | $ | 1.15 | | $ | 1.12 | |

Spot purchases as % of all sources | | 14 | % | 7 | % | 1 | % |

The delivered cost of coal is expected to increase in 2006 due to the start of new contracts for 2006 and market conditions. LG&E increased spot purchases in 2005 and 2004 due to supply and transportation issues in the market.

Gas Supply

LG&E purchases natural gas supplies from multiple sources under contracts for varying periods of time, while transportation services are purchased from Texas Gas and Tennessee Gas.

LG&E transports natural gas on the Texas Gas system under Rate Schedules NNS and FT service. Effective November 1, 2005, LG&E’s winter season NNS levels are 184,900 MMBtu/day and its winter season FT levels are 36,000 MMBtu/day. LG&E’s summer season NNS levels are 60,000 MMBtu/day and its summer season FT levels are 36,000 MMBtu/day. LG&E provided Texas Gas with notice to terminate a portion of its FT agreement in the amount of 8,000 MMBtu/day effective November 1, 2006. As a result, LG&E will have FT service in the amount of 28,000 MMBtu/day, effective November 1, 2006. Each of the NNS agreements with Texas Gas is subject to termination by LG&E in equal portions during 2008, 2010 and 2011. Each of the FT

8

agreements with Texas Gas is subject to termination by LG&E during 2008 and 2011. LG&E also transports on the Tennessee Gas system under Tennessee Gas’ Rate Schedule FT-A. LG&E’s contract levels with Tennessee Gas are 51,000 MMBtu/day throughout the year. The FT-A agreement with Tennessee Gas is subject to termination by LG&E during 2007.

LG&E participates in rate and other proceedings affecting the regulated interstate natural gas pipelines that provide service to LG&E. Both Texas Gas and Tennessee Gas have several active proceedings in which LG&E is participating at the FERC. One of those proceedings is an application filed by Texas Gas with the FERC to increase its base rates. LG&E is participating in this proceeding with other interested parties. The rates of Texas Gas are, therefore, being billed subject to refund, and LG&E will refund to its customers any amounts which may be refunded to it as the result of the resolution of this proceeding before the FERC. The rates of Tennessee Gas are not being billed subject to refund.

LG&E also has a portfolio of supply arrangements of various terms with a number of suppliers designed to meet its firm sales obligations. These natural gas supply arrangements include pricing provisions that are market-responsive. These firm natural gas supplies, in tandem with pipeline transportation services, provide the reliability and flexibility necessary to serve LG&E’s natural gas customers.

LG&E owns and operates five underground natural gas storage fields with a current working gas capacity of approximately 15.1 million Mcf. Natural gas is purchased and injected into storage during the summer season when natural gas prices are typically lower, and is then withdrawn to supplement pipeline supplies to meet the gas-system load requirements during the winter heating season. See Gas Operations under Item 1.

The estimated maximum deliverability from storage during the early part of the heating season is expected to be in excess of 370,000 Mcf/day. Under mid-winter design conditions, LG&E expects to be able to withdraw in excess of 350,000 Mcf/day from its storage facilities. The deliverability of natural gas from LG&E’s storage facilities decreases as storage inventory levels are reduced by seasonal withdrawals.

LG&E relies upon its significant underground storage to mitigate the price volatility to which customers might otherwise be exposed. In 2000, the Kentucky Commission issued an order establishing Administrative Case No. 384 – “An Investigation of Increasing Wholesale Natural Gas Prices and the Impacts of such Increase on the Retail Customers Served by Kentucky’s Jurisdictional Natural Gas Distribution Companies”. Subsequent to this investigation, the Kentucky Commission issued an order on July 17, 2001, encouraging the natural gas distribution companies in Kentucky to take various actions, among them to propose a natural gas hedge plan. LG&E currently operates under a hedge plan proposed by LG&E beginning with the 2004/2005 winter heating season. This hedge plan relies upon LG&E’s underground natural gas storage to mitigate customer exposure to price volatility. In 2004, the Kentucky Commission approved LG&E’s proposed hedge plan, validating the effectiveness of storage to mitigate potential volatility associated with high winter natural gas prices by approving this natural gas hedge plan. The Kentucky Commission also ordered that LG&E need not file hedge plans in the future unless it intended to utilize financial hedging instruments.

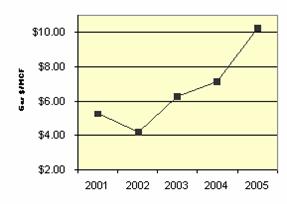

The average cost per Mcf of natural gas purchased by LG&E was $10.23 in 2005, $7.18 in 2004, and $6.30 in 2003. Natural gas prices in the unregulated wholesale market generally have increased significantly over the last few years beginning in 2000. For further discussion of wholesale natural gas prices, see Note 3 of LG&E’s Notes to Financial Statements under Item 8.

9

Environmental Matters

Protection of the environment is a major priority for LG&E. Federal, state, and local regulatory agencies have issued LG&E permits for various activities subject to air quality, water quality, and waste management laws and regulations. For the five-year period ending with 2005, expenditures for pollution control facilities represented $233 million or 24% of total construction expenditures. LG&E estimates that construction expenditures for environmental protection equipment from 2006 through 2008 will be approximately $40 million. For a discussion of environmental matters, see Note 10 of LG&E’s Notes to Financial Statements under Item 8.

Competition

At this time, neither the Kentucky General Assembly nor the Kentucky Commission has adopted or approved a plan or timetable for retail electric industry competition in Kentucky. The nature or timing of the ultimate legislative or regulatory actions regarding industry restructuring and their impact on LG&E, which may be significant, cannot currently be predicted. Some states that have already deregulated have begun discussions that could lead to re-regulation.

In February 2005, Kentucky’s Governor signed an executive order directing the Kentucky Commission, in conjunction with the Commerce Cabinet and the Environmental and Public Protection Cabinet, to ‘develop a Strategic Blueprint for the continued use and development of electric energy.’ This Strategic Blueprint is designed to promote future investment in electric infrastructure for the Commonwealth of Kentucky, to protect Kentucky’s low-cost electric advantage, to maintain affordable rates for all Kentuckians, and to preserve Kentucky’s commitment to environmental protection. In March 2005, the Kentucky Commission established Administrative Case No. 2005-00090 to collect information from all jurisdictional utilities in Kentucky, including LG&E, pertaining to Kentucky electric generation, transmission and distribution systems. LG&E responded to the Kentucky Commission’s first set of data requests at the end of March 2005 and to a second set of data requests in May 2005. The Commission held a Technical Conference in June 2005, in which all parties participated in a panel discussion. A final report was provided in August 2005 from the Kentucky Commission to the Governor. The Kentucky Commission issued an order and closed this proceeding on September 15, 2005. Some of the key findings from the report are:

• Kentucky’s electric utilities currently have adequate infrastructure as well as adequate planning to serve the needs of customers through 2025;

• Kentucky will need 7,000 megawatts of additional generating capacity by 2025;

• Kentucky’s electric transmission is reliable but intrastate power transfers are limited;

• Additional incentives to use renewable energy and educate the public on the benefits of renewables are needed;

• Financial incentives should be available for coal purification and other clean air technologies;

• A cautious approach should be taken toward deregulation; and

• Kentucky must be involved in federal decisions that impact its status as a low cost energy provider.

Over the last several years, LG&E has taken many steps to keep its rates low while maintaining high levels of customer satisfaction, including: an increase in focus on commercial, industrial and residential customers; an increase in employee involvement and training; and continuous modifications of its organizational structure. LG&E also strives to control costs through competitive bidding and process improvements. LG&E’s performance in national customer satisfaction surveys continues to be high.

10

KENTUCKY UTILITIES COMPANY

General

KU, incorporated in Kentucky in 1912 and incorporated in Virginia in 1991, is a regulated public utility that provides electricity to approximately 495,000 customers in over 600 communities and adjacent suburban and rural areas in 77 counties in central, southeastern and western Kentucky, to approximately 30,000 customers in 5 counties in southwestern Virginia and 5 customers in Tennessee. KU’s coal-fired electric generating plants produce most of KU’s electricity, the remainder is generated by hydroelectric power plants and combustion turbines. In Virginia, KU operates under the name Old Dominion Power Company. KU operates under appropriate franchises in substantially all of the 160 Kentucky incorporated municipalities served. No franchises are required in unincorporated Kentucky or Virginia communities. The lack of franchises is not expected to have a material adverse effect on KU’s operations. KU also sells wholesale electric energy to 12 municipalities. See Item 2, Properties.

Electric Operations

The sources of KU’s electric operating revenues and the volumes of sales for the three years ended December 31, 2005, were as follows:

(in millions) | | 2005 | | 2004 | | 2003 | |

ELECTRIC OPERATING REVENUES | | | | | | | |

Residential | | $ | 364 | | $ | 304 | | $ | 278 | |

Commercial | | 241 | | 207 | | 189 | |

Industrial | | 220 | | 190 | | 176 | |

Mine power | | 38 | | 32 | | 30 | |

Public authorities | | 83 | | 72 | | 66 | |

Total retail | | 946 | | 805 | | 739 | |

Wholesale sales | | 210 | | 160 | | 138 | |

Provision for rate collections (refunds) | | — | | 5 | | (8 | ) |

Miscellaneous | | 51 | | 25 | | 23 | |

Total | | $ | 1,207 | | $ | 995 | | $ | 892 | |

(Thousands of Mwh) | | | | | | | |

ELECTRIC SALES | | | | | | | |

Residential | | 6,599 | | 6,160 | | 6,001 | |

Commercial | | 4,466 | | 4,323 | | 4,210 | |

Industrial | | 5,459 | | 5,400 | | 5,110 | |

Mine power | | 803 | | 732 | | 722 | |

Public authorities | | 1,649 | | 1,597 | | 1,551 | |

Total retail | | 18,976 | | 18,212 | | 17,594 | |

Wholesale sales | | 5,781 | | 5,707 | | 5,591 | |

Total | | 24,757 | | 23,919 | | 23,185 | |

KU set an annual peak load of 4,079 Mw on July 25, 2005, when the temperature reached 94 degrees Fahrenheit. This was the highest hourly customer demand in KU’s history.

11

The electric utility business is affected by seasonal weather patterns. As a result, operating revenues (and associated operating expenses) are not generated evenly throughout the year. See KU’s Results of Operations under Item 7.

KU and LG&E currently maintain a 12% - 14% reserve margin range. At December 31, 2005, KU owned steam and combustion turbine generating facilities with a net summer capability of 4,433 Mw and a 28 Mw nameplate-rated hydroelectric facility with a summer capability of 24 Mw. See Item 2, Properties. KU also obtains power from other utilities under bulk power purchase and interchange contracts. At December 31, 2005, KU’s system net summer capability, including purchases from others and excluding the hydroelectric facility, was 4,678 Mw.

KU’s weighted-average system-wide emission rate for SO2 in 2005 was approximately 1.25 lbs./MMBtu of heat input, with every generating unit below its emission limit established by the Kentucky Division for Air Quality.

Under a contract expiring in 2020 with OMU, KU has agreed to purchase from OMU the surplus output of the 142-Mw and 265-Mw generating units at OMU’s Elmer Smith station. Purchases under the contract are made under a contractual formula resulting in costs which are expected to be comparable to the cost of other power purchased or generated by KU. Such power equated to approximately 8% of KU’s net generation system output during 2005. See Note 10 of KU’s Notes to Financial Statements under Item 8.

KU owns 20% of the common stock of EEI, which owns and operates a 1,000-Mw generating station in southern Illinois. Previously, KU was entitled to take 20% of the available capacity of the station under a pricing formula comparable to the cost of other power generated by KU. Such power equated to approximately 9% of KU’s net generation system output in 2005. The contract governing the purchases from EEI terminated on December 31, 2005. Subsequent to December 31, 2005, EEI has sold power under general market-based pricing and terms. KU has not contracted with EEI for power under the new arrangements, but maintains its 20% ownership in the common stock of EEI. Replacement power for the EEI capacity has been largely provided by KU generation.

KU and 11 other electric utilities are participating owners of OVEC, located in Piketon, Ohio. OVEC owns and operates two power plants that burn coal to generate electricity, Kyger Creek Station in Ohio and Clifty Creek Station in Indiana. KU owns 2.5% of OVEC’s common stock. KU’s share of OVEC’s output is 2.5%, approximately 55 Mw of generation capacity. In April 2004, OVEC and its shareholders, including KU and LG&E, entered into an Amended and Restated Inter-Company Power Agreement, to be effective beginning March 2006, upon the expiration of the current power contract among the parties. The parties received SEC approval under PUHCA 1935 of the Amended and Restated Inter-Company Power Agreement in February 2005.

KU is a member of the MISO, a non-profit independent transmission system operator that serves the electrical transmission needs of much of the Midwest. Membership was obtained when the MISO was formed in 1998 in response to and consistent with federal energy policy initiatives at that time. The MISO began commercial operations in February 2002. As a result, KU turned over operational control of its 100 Kv and above transmission facilities, but continues to control and operate the lower voltage transmission system subject to the terms and conditions of the MISO. As a transmission-owning member of the MISO, KU incurs costs under the MISO OATT. In April 2005, the MISO implemented its day-ahead real-time market (MISO Day 2), including a congestion management system. At the present time, KU is involved in regulatory proceedings at the Kentucky Commission and the FERC seeking authority to exit the MISO. On March 17, 2006, the FERC issued an order conditionally approving the request of KU and LG&E to exit the MISO. For further discussion, see

12

Note 15 of KU’s Notes to Financial Statements under Item 8.

Rates and Regulation

Historically, E.ON, KU’s ultimate parent, has been a registered holding company under PUHCA 1935, and anticipates registering under PUHCA 2005. As a registered holding company, E.ON, its utility subsidiaries, including KU, and certain of its non-utility subsidiaries have been subject to extensive regulation by the SEC and the FERC with respect to numerous matters, including: electric utility facilities and operations, wholesale sales of power and related transactions, accounting practices, issuances and sales of securities, acquisitions and sales of utility properties, payments of dividends out of capital and surplus, financial matters and inter-system sales of non-power goods and services. In addition, PUHCA 1935 generally limited the ability of registered holding companies to acquire additional public utility systems and to acquire and retain businesses unrelated to the utility operations of the holding company. KU believes that it has adequate authority (including financing authority) under existing FERC orders and regulations to conduct its business and will seek additional authorization when necessary.

In August 2005, President Bush signed into law the EPAct 2005, significantly changing many federal statutes, repealing PUHCA 1935 as of February 8, 2006 and enacting PUHCA 2005. As part of the repeal of PUHCA 1935, the FERC was given more authority over the merger and acquisition of public utilities and more authority over the books and records of public utilities. Despite these increases in the FERC’s authority, KU believes that the repeal of PUHCA 1935 will lessen its regulatory burdens and provide more flexibility in the event of expansion.

Besides repealing PUHCA 1935, the EPAct 2005 is also expected to have substantial long-term effects on energy markets, energy investment and regulation of public utilities and holding company systems by the FERC and the DOE. The FERC and the DOE are in various stages of rulemaking in implementing the EPAct 2005. While the precise impact of these rulemakings cannot be determined at this time, KU generally views the EPAct 2005 as legislation that will enhance the utility industry going forward.

The Kentucky Commission and the Virginia Commission have regulatory jurisdiction over KU’s retail rates and service, and over the issuance of certain of its securities. By reason of owning and operating a small amount of electric utility property in one county in Tennessee (having a gross book value of approximately $0.3 million) from which KU served 5 customers at December 31, 2005, KU is subject to the jurisdiction of the Tennessee Regulatory Authority. The Kentucky Commission, the Virginia Commission and the Tennessee Regulatory Authority have the ability to examine the rates KU charges its retail customers at any time.

Pursuant to Kentucky law, the Kentucky Commission has established the boundaries of the service territory or area of each retail electric supplier in Kentucky (including KU), other than municipal corporations. Within this service territory each such supplier has the exclusive right to render retail electric service.

KU’s Kentucky retail electric rates contain an FAC, whereby increases and decreases in the cost of fuel for electric generation are reflected in the rates charged to retail electric customers. The Kentucky Commission

13

requires public hearings at six-month intervals to examine past fuel adjustments, and at two-year intervals to review past operations of the fuel clause and transfer of the then current fuel adjustment charge or credit to the base charges. The Kentucky Commission also requires that electric utilities, including KU, file documents relating to fuel procurement and the purchase of power and energy from other utilities. The FAC mechanism for Virginia customers uses an average fuel cost factor based primarily on projected fuel costs. The fuel cost factor may be adjusted annually for over or under collections of fuel costs from the previous year.

Prior to 2004, KU’s Kentucky retail electric rates were subject to an ESM. KU and the Kentucky Commission agreed to a termination of the ESM relating to all periods after 2003. The ESM, initially in place for three years beginning in 2000, set an upper (12.5%) and lower (10.5%) limit for rate of return on equity. If earnings were above the upper limit, the excess earnings were shared 40% with ratepayers and 60% with shareholders; if earnings were below the lower limit, the earnings deficiency was recovered 40% from ratepayers and 60% from shareholders. By order of the Kentucky Commission, rate changes prompted by the ESM filing went into effect in April of each year subject to a balancing adjustment in successive periods. There is no ESM for Virginia retail electric rates. For discussion of current ESM matters, see Note 3 of KU’s Notes to Financial Statements under Item 8.

In June 2001, KU filed an application (“VDT case”) with the Kentucky Commission to create a regulatory asset relating to first quarter 2001 charges for a workforce reduction program. In December 2001, the Kentucky Commission approved a settlement in the VDT and allowed KU to set up a regulatory asset of $54 million for the workforce reduction costs and begin amortizing these costs over a five year period starting in April 2001. The settlement reduced revenues by approximately $11 million through a surcredit on bills to ratepayers over the same five-year period. The surcredit represented net savings stipulated by KU. For discussion of current VDT matters, see Note 3 and Note 15 of KU’s Notes to Financial Statements under Item 8.

KU’s Kentucky retail rates contain an ECR surcharge which recovers costs incurred by KU that are required to comply with the Clean Air Act and other environmental regulations. See Note 3 of KU’s Notes to Financial Statements under Item 8.

Integrated resource planning regulations in Kentucky require KU and the other major utilities to make triennial filings with the Kentucky Commission of various historical and forecasted information relating to load, capacity margins and demand-side management techniques. KU filed its most recent IRP in April 2005. The AG and KIUC were granted intervention in the IRP proceeding. The Kentucky Commission issued its staff report on February 15, 2006, with no substantive issues noted and closed the case by Order dated February 24, 2006.

The Commonwealth of Virginia passed the Virginia Electric Utility Restructuring Act in 1999. This act gave Virginia customers the ability to choose their electric supplier. Rates are capped at current levels through December 2010. The Virginia Commission will continue to require each Virginia utility to make annual filings of either a base rate change or an Annual Informational Filing consisting of a set of standard financial schedules. The Virginia Staff will issue a Staff Report regarding the individual utility’s financial performance during the historic 12-month period. The Staff Report can lead to an adjustment in rates, but through December 2010 rates are subject to the capped rate period and essentially “frozen”. However, KU may petition the Virginia Commission for a one-time adjustment in rates during the capped rate period. Effective July 1, 2003, the General Assembly of Virginia amended and reenacted Section 56-580 of the Code of Virginia with language that effectively exempts all KU Virginia service territory from retail choice until such time as retail choice is offered to customers in KU’s other service territories.

14

In December 2003, KU filed an application with the Kentucky Commission requesting an adjustment in KU’s electric rates. KU asked for a general adjustment in electric rates based on the twelve month test period ended September 30, 2003. The revenue increase requested was approximately $58 million. In June 2004, the Kentucky Commission issued an order approving an increase in KU’s annual electric base rates of approximately $46 million (6.8%). The rate increase took effect on July 1, 2004.

Subsequently during 2004 and 2005, the AG conducted an investigation regarding the proceedings resulting in the rate increase. The AG requested information from KU and the Kentucky Commission and its staff regarding alleged improper communications between KU and the Kentucky Commission related to the rate proceeding. The AG also requested rehearing of the rate increase order on the basis of these allegations, as well as calculational aspects of the increased rates. In February, 2005 the AG submitted a confidential report on its investigation with the Kentucky Commission and filed a motion summarizing the report as containing evidence of improper communications and record-keeping errors by KU in respect of its activities with state governmental agencies, including the Kentucky Commission.

In December 2005, the Kentucky Commission issued an order noting completion of its inquiry, including review of the AG’s investigative report. The order concluded that no improper communications occurred during the rate proceedings. The order further established a procedural schedule through the first quarter of 2006 for considering the sole issue for which rehearing was granted: state income tax rates used in calculating the granted rate increase. This issue is estimated at less than $1 million annually. Upon resolution of this issue on rehearing, the initial rate increase order could be subject to judicial appeal.

For a further discussion of regulatory matters, see Note 3 of KU’s Notes to the Financial Statements under Item 8.

Construction Program and Financing

KU’s construction program is designed to ensure that there will be adequate capacity and reliability to meet the electric needs of its service area. These needs are continually being reassessed and appropriate revisions are made, when necessary, in construction schedules. KU’s estimates of its construction expenditures can vary substantially due to numerous items beyond KU’s control, such as changes in interest rates, economic conditions, construction costs, and new environmental or other governmental laws and regulations.

During the five years ended December 31, 2005, gross property additions amounted to approximately $1 billion. Internally generated funds and external financings for the five-year period were utilized to provide for these gross additions. The gross additions during this period amounted to approximately 26% of total utility plant at December 31, 2005. Gross retirements during the same period were $106 million.

Capital expenditures during the three years ending December 31, 2008 are estimated to be approximately $1.5 billion. The major expenditures during this period relate to the development and construction of Trimble County Unit 2, of which KU’s portion totals approximately $510 million, and the installation of FGDs on Ghent and Brown units, totaling approximately $560 million.

Coal Supply

Coal-fired generating units provided approximately 97% of KU’s net kilowatt-hour generation for 2005. The remaining net generation for 2005 was provided by natural gas and oil-fueled combustion turbine peaking units

15

and hydroelectric plants. Coal is expected to be the predominant fuel used by KU in the foreseeable future, with natural gas and oil being used for peaking capacity and flame stabilization in coal-fired boilers or in emergencies. KU has no nuclear generating units and has no plans to build any in the foreseeable future.

KU maintains its fuel inventory at levels estimated to be necessary to avoid operational disruptions at its coal-fired generating units. Reliability of coal deliveries can be affected from time to time by a number of factors, including fluctuations in demand, coal mine production issues and other supplier or transporter operating difficulties.

KU has entered into coal supply agreements with various suppliers for coal deliveries for 2006 and beyond and normally augments its coal supply agreements with spot market purchases. KU has a coal inventory policy which it believes provides adequate protection under most contingencies. It had a coal inventory of approximately 1.1 million tons, or a 51-day supply, on hand at December 31, 2005.

KU expects to continue purchasing most of its coal, which has a sulfur content in the 0.7% - 3.5% range, from western and eastern Kentucky, West Virginia, southern Indiana, southern Illinois, Ohio, Wyoming and Colorado for the foreseeable future.

Coal is delivered to KU’s Ghent plant by barge, Tyrone and Green River plants by truck, and E.W. Brown plant by rail and truck.

The historical average delivered cost of coal purchased and the percentage of spot coal purchases were as follows:

| | 2005 | | 2004 | | 2003 | |

| | | | | | | |

Per ton | | $ | 42.45 | | $ | 37.69 | | $ | 34.57 | |

Per MMBtu | | $ | 1.78 | | $ | 1.56 | | $ | 1.47 | |

Spot purchases as % of all sources | | 15 | % | 14 | % | 11 | % |

KU’s historical average cost of coal purchased is higher than LG&E’s due to the lower sulfur content of the coal KU purchases for use at its Ghent plant and higher cost to transport coal to the E.W. Brown plant. The delivered cost of coal for 2006 is expected to increase due to the start of new contracts and market conditions.

Environmental Matters

Protection of the environment is a major priority for KU. Federal, state, and local regulatory agencies have issued KU permits for various activities subject to air quality, water quality, and waste management laws and regulations. For the five-year period ending with 2005, expenditures for pollution control facilities represented $269 million or 26% of total construction expenditures. KU estimates that construction expenditures for environmental control equipment from 2006 through 2008, will be approximately $680 million, of which approximately $560 million is related to the installation of FGDs at Ghent and Brown. For a discussion of environmental matters, see Note 10 of KU’s Notes to Financial Statements under Item 8.

Competition

At this time, neither the Kentucky General Assembly nor the Kentucky Commission has adopted or approved a plan or timetable for retail electric industry competition in Kentucky. The nature or timing of the ultimate

16

legislative or regulatory actions regarding industry restructuring and their impact on KU, which may be significant, cannot currently be predicted. Some states that have already deregulated have begun discussions that could lead to re-regulation.

In February 2005, Kentucky’s Governor signed an executive order directing the Kentucky Commission, in conjunction with the Commerce Cabinet and the Environmental and Public Protection Cabinet, to ‘develop a Strategic Blueprint for the continued use and development of electric energy.’ This Strategic Blueprint is designed to promote future investment in electric infrastructure for the Commonwealth of Kentucky, to protect Kentucky’s low-cost electric advantage, to maintain affordable rates for all Kentuckians, and to preserve Kentucky’s commitment to environmental protection. In March 2005, the Kentucky Commission established Administrative Case No. 2005-00090 to collect information from all jurisdictional utilities in Kentucky, including KU, pertaining to Kentucky electric generation, transmission and distribution systems. KU responded to the Kentucky Commission’s first set of data requests at the end of March 2005 and to a second set of data requests in May 2005. The Commission held a Technical Conference in June 2005, in which all parties participated in a panel discussion. A final report was provided in August 2005 from the Kentucky Commission to the Governor. The Kentucky Commission issued an order and closed this proceeding on September 15, 2005. Some of the key findings from the report are:

• Kentucky’s electric utilities currently have adequate infrastructure as well as adequate planning to serve the needs of customers through 2025;

• Kentucky will need 7,000 megawatts of additional generating capacity by 2025;

• Kentucky’s electric transmission is reliable but intrastate power transfers are limited;

• Additional incentives to use renewable energy and educate the public on the benefits of renewables are needed;

• Financial incentives should be available for coal purification and other clean air technologies;

• A cautious approach should be taken toward deregulation; and

• Kentucky must be involved in federal decisions that impact its status as a low cost energy provider.

Virginia has enacted a phase-in of customer choice through the Virginia Electric Restructuring Act, however, KU’s service territory has been effectively exempted from retail choice until such time as retail choice is offered to customers in KU’s other service territories.

Over the last several years, KU has taken many steps to keep its rates low while maintaining high levels of customer satisfaction, including: an increase in focus on commercial, industrial and residential customers; an increase in employee involvement and training; and continuous modifications of its organizational structure. KU also strives to control costs through competitive bidding and process improvements. KU’s performance in national customer satisfaction surveys continues to be high.

17

EMPLOYEES AND LABOR RELATIONS

LG&E had approximately 895 full-time regular employees and KU had approximately 925 full-time regular employees at February 28, 2006. Of the LG&E total, 621 operating, maintenance, and construction employees were represented by IBEW Local 2100. LG&E and employees represented by IBEW Local 2100 signed a three-year collective bargaining agreement in November 2005 with annual benefits re-openers. Of the KU total, approximately 150 operating, maintenance, and construction employees were represented by IBEW Local 2100 and USWA Local 9447-01. In August 2003, KU and employees represented by IBEW Local 2100 entered into a three-year collective bargaining agreement. KU and employees represented by USWA Local 9447-01 entered into a three-year collective bargaining agreement in August 2005 with authorized annual wage re-openers.

E.ON U.S. Services provides services to affiliated entities, including LG&E and KU, at cost as permitted under PUHCA 2005. On February 28, 2006, approximately 1,022 employees worked for E.ON U.S. Services.

18

Executive Officers of LG&E and KU at February 28, 2006:

| | | | | | Effective Date of | |

| | | | | | Election to Present | |

Name | | Age | | Position | | Position | |

| | | | | | | |

Victor A. Staffieri | | 50 | | Chairman of the Board, | | May 1, 2001 | |

| | | | President and Chief | | | |

| | | | Executive Officer | | | |

| | | | | | | |

John R. McCall | | 62 | | Executive Vice President, | | July 1, 1994 | |

| | | | General Counsel and | | | |

| | | | Corporate Secretary | | | |

| | | | | | | |

S. Bradford Rives | | 47 | | Chief Financial Officer | | September 15, 2003 | |

| | | | | | | |

Paul W. Thompson | | 49 | | Senior Vice President - | | June 7, 2000 | |

| | | | Energy Services | | | |

| | | | | | | |

Chris Hermann | | 58 | | Senior Vice President - | | February 14, 2003 | |

| | | | Energy Delivery | | | |

| | | | | | | |

Wendy C. Welsh | | 52 | | Senior Vice President - | | December 11, 2000 | |

| | | | Information Technology | | | |

| | | | | | | |

Martyn Gallus | | 41 | | Senior Vice President - | | December 11, 2000 | |

| | | | Energy Marketing | | | |

| | | | | | | |

Paula H. Pottinger | | 49 | | Senior Vice President - | | January 2, 2006 | |

| | | | Human Resources | | | |

Other Officers of LG&E and KU at February 28, 2006:

David A. Vogel | | 40 | | Vice President - Retail | | March 1, 2003 | |

| | | | and Gas Storage Operations | | | |

| | | | | | | |

Daniel K. Arbough | | 44 | | Treasurer | | December 11, 2000 | |

| | | | | | | |

Michael S. Beer | | 47 | | Vice President | | September 27, 2004 | |

| | | | Federal Regulation and Policy | | | |

| | | | | | | |

George R. Siemens | | 56 | | Vice President - External | | January 11, 2001 | |

| | | | Affairs | | | |

| | | | | | | |

D. Ralph Bowling | | 48 | | Vice President - | | August 1, 2002 | |

| | | | Power Operations WKE | | | |

| | | | | | | |

R. W. Chip Keeling | | 49 | | Vice President - | | March 18, 2002 | |

| | | | Communications | | | |

| | | | | | | |

John N. Voyles, Jr. | | 51 | | Vice President - | | June 16, 2003 | |

| | | | Regulated Generation | | | |

| | | | | | | |

Valerie L. Scott | | 49 | | Controller | | January 1, 2005 | |

19

The present term of office of each of the above executive and other officers extends to the meeting of the Board of Directors following the 2006 Annual Meeting of Shareholders.

There are no family relationships between or among executive and other officers of LG&E and KU. The above tables indicate officers serving as executive officers of both LG&E and KU at February 28, 2006. Each of the above officers serves in the same capacity for LG&E and KU.

Before he was elected to his current positions, Mr. Staffieri was Chief Financial Officer of LG&E Energy (now E.ON U.S.) and LG&E from May 1997 to February 1999 (including Chief Financial Officer of KU from May 1998 to February 1999) and President and Chief Operating Officer of LG&E Energy (now E.ON U.S.) from March 1999 to April 2001 (including President of LG&E and KU from June 2000 to April 2001).

Mr. McCall has been Executive Vice President, General Counsel and Corporate Secretary of LG&E Energy (now E.ON U.S.) and LG&E since July 1994. He became Executive Vice President, General Counsel and Corporate Secretary of KU in May 1998.

Before he was elected to his current positions, Mr. Rives was Senior Vice President - Finance and Business Development from February 1999 to December 2000 and Senior Vice President - Finance and Controller of LG&E Energy (now E.ON U.S.), LG&E and KU from December 2000 to September 2003.

Before he was elected to his current positions, Mr. Thompson was Group Vice President for LG&E Energy Marketing, Inc. from June 1998 to August 1999; Vice President, Retail Electric Business for LG&E from December 1998 to August 1999; and Senior Vice President - Energy Services for LG&E Energy (now E.ON U.S.) from August 1999 to June 2000.

Before he was elected to his current positions, Mr. Hermann was Vice President, Power Generation and Engineering Services, of LG&E from May 1998 to December 1999; Vice President Supply Chain and Operating Services from December 1999 to December 2000; and Senior Vice President - Distribution Operations, from December 2000 to February 2003.

Before she was elected to her current positions, Ms. Welsh was Vice President - Information Technology from February 1998 to December 2000 for LG&E Energy (now E.ON U.S.).

Before he was elected to his current positions, Mr. Gallus was Vice President, Energy Marketing from August 1998 to December 2000 for LG&E Energy (now E.ON U.S.).

Before she was elected to her current positions, Ms. Pottinger was Director, Human Resources from June 1997 to June 2002; and Vice President - Human Resources from June 2002 to January 2006.

Before he was elected to his current positions, Mr. Vogel was Vice President - Retail Services from December 2000 to March 2003.

In addition to being elected to his current positions, Mr. Arbough has held the positions of Director, Corporate Finance of LG&E Energy (now E.ON U.S.), LG&E and KU from May 1998 to present.

20

Before he was elected to his current positions, Mr. Beer was Senior Counsel Specialist, Regulatory from February 2000 to February 2001, and Vice President – Rates and Regulatory from February 2001 to September 2004.

Before he was elected to his current positions, Mr. Siemens held the position of Director of External Affairs for LG&E Energy (now E.ON U.S.) from August 1982 to January 2001.

Before he was elected to his current positions, Mr. Bowling was Plant General Manager at Western Kentucky Energy from July 1998 to December 2001; and General Manager Black Fossil Operations for E.ON U.K. in the United Kingdom from January 2002 to August 2002.

Before he was elected to his current positions, Mr. Keeling was Director, Corporate Communications for LG&E Energy (now E.ON U.S.) from February 2000 to March 2002.

Before he was elected to his current positions, Mr. Voyles was General Manager, Cane Run, Ohio Falls and Combustion Turbines, November 1998 to February 2003; and Director, Generation Services, February 2003 to June 2003.

Before she was elected to her current positions, Ms. Scott was Director, Trading Controls and Energy Marketing Accounting from February 1999 to September 2002, and Director, Financial Planning and Accounting – Utility Operations from September 2002 to December 2004.

Item 1A. Risk Factors

In addition to the other information in this Form 10-K and other documents furnished to or filed by LG&E and KU with the SEC from time to time, the following factors should be carefully considered in evaluating the Companies. Such factors could affect actual results and cause results to differ materially from those expressed in any forward-looking statements made by, or on behalf of, the Companies. Some or all of these factors may apply to LG&E or KU or both.

The electric and gas rates that LG&E and KU charge customers, as well as other aspects of the business, are subject to significant state and FERC regulation.

The rates that the Companies are allowed to charge for their services are a primary item influencing the results of operations, financial position, and liquidity of the Companies. The regulation of the rates that are collected from customers is determined, in large part, by governmental organizations outside the Companies’ control, including the Kentucky Commission, and for KU, the Virginia Commission and the Tennessee Regulatory Authority. These commissions regulate many aspects of utility operations, including financial and capital structure matters, siting and construction of facilities, terms and conditions of service, safety and operations, accounting and cost allocation methodologies and other matters. While rate regulation is premised on recovery of prudently incurred costs and reasonable rate of return on capital, such cannot be assured. Regulatory proceedings regarding all matters of operations can thus significantly affect the earnings, liquidity and business activities of the Companies.

Base rate increases of LG&E and KU approved during 2004 and currently being collected by the Companies in Kentucky remain the subject of continuing proceedings by the Kentucky Commission and the Attorney General. Proceedings regarding the expiration of VDT charges formerly included in the Companies’ rates in Kentucky

21

are also the subject of on-going proceedings.

Transmission and interstate market activities of LG&E and KU, as well as other aspects of the business, are subject to significant FERC regulation.

The Companies’ businesses are subject to regulation under the FERC covering matters including rates charged to transmission users and wholesale customers, interstate market structure and design, construction and operation of transmission facilities, acquisition and disposal of utility assets and securities, standards of conduct, cost allocations and financial matters. Existing FERC regulation, changes thereto or issuance of new rules in these areas, can affect the earnings, operations and other activities of the Companies.

LG&E’s and KU’s continued participation in the MISO, as well as changes in transmission and wholesale power market structures, could increase costs or reduce revenues.

LG&E and KU are members of the MISO and have transferred functional control of their transmission systems to the MISO. The Companies must incur MISO membership-related costs and charges established by the MISO and can be required to incur other expenses or make transmission and generation operating decisions as directed by the MISO. The MISO Day 2 markets, which began operation in April 2005, have represented a significant change in the wholesale power market structure and operation. Until the market matures, the effects on results of operations, financial position, or liquidity will remain difficult to predict.

LG&E and KU have commenced proceedings at the Kentucky Commission and the FERC seeking authority to exit the MISO. On March 17, 2006, the FERC issued an order conditionally approving the request of KU and LG&E to exit the MISO. For further discussion see Note 16 of LG&E’s Notes to Financial Statements and Note 15 of KU's Notes to Financial Statements under Item 8.

LG&E and KU undertake significant capital projects and are subject to unforeseen costs, delays or failures in such projects, as well as risk of full recovery of such costs.