NASDAQ: MPET www.magellanpetroleum.com SEAAOC Darwin 1 SEAAOC William H. Hastings 23 rd September, 2010; Darwin Exhibit 99.1 |

NASDAQ: MPET www.magellanpetroleum.com SEAAOC Darwin 2 Forward Looking Statements Except for historical information, this presentation contains forward looking statements and information with respect to net oil and gas reserve assertions, valuations and key development assumptions and timing, gas sales in Australia and its valuation, potential development projects, and exploration and drilling plans. These statements are subject to risks and uncertainties that could cause actual results to differ materially from those expressed or implied from such information. Among these risks and uncertainties are the ability of Magellan Petroleum Australia Limited (“MPAL”), with the assistance of the Company, to successfully and timely close the Evans Shoal acquisition, the ability of the Company to successfully secure financing and/or offtake opportunities necessary to implement a strategy for methanol development, pricing and production levels from the properties in which Magellan and MPAL have interests, the extent to which demand for methanol continues to grow in targeted markets, the extent to which methanol can be used as an economical fuel alternative, the extent of the recoverable reserves at those properties, the profitable integration of acquired businesses, including Evans Shoal, the future outcome of the negotiations for gas sales contracts for the remaining uncontracted reserves at both the Mereenie and Palm Valley gas fields in the Amadeus Basin, including the likelihood of success of other potential suppliers of gas to the current customers of Mereenie and Palm Valley production. In addition, Magellan, and its operating subsidiaries have exploration permits and face the risk that any wells drilled may fail to encounter hydrocarbons in commercially recoverable quantities. Any forward-looking information provided in this presentation should be considered with these factors in mind. Magellan assumes no obligation to update any forward-looking statements contained in this presentation, whether as a result of new information, future events or otherwise. Oil and gas issuers are required to include disclosure regarding proved oil and gas reserves in certain filings made with the U.S. Securities and Exchange Commission. Proved reserves are the estimated quantities of crude oil, natural gas, and natural gas liquids which geological and engineering data demonstrate with reasonable certainty to be recoverable in future years from known reservoirs under existing economic and operating conditions, i.e., prices and costs as of the date the estimate is made. The SEC also permits the disclosure of probable and possible reserves which are additional reserves that are less certain to be recovered. Investors are urged to consider closely the disclosures in Magellan’s periodic filings with the SEC available from us at the company’s website www.magellanpetroleum.com |

NASDAQ: MPET www.magellanpetroleum.com SEAAOC Darwin 3 Company Profile: Magellan Petroleum Corporation, through its wholly owned subsidiary, Magellan Petroleum Australia Limited, and its majority controlling interest in Nautilus Poplar LLC, is engaged in the exploration, development, and sale of oil and gas reserves worldwide. The Company’s operations are in Australia, North America, and in the United Kingdom. The Company has a differentiated business model guided by personnel with over 100 man-years of large oil company experience. Magellan adds value to large assets through unconventional commercial solutions such as Methanol production for high CO2 fields, and CO2 “tertiary” flooding in overlooked reservoir plays. The Company also holds 23,000 contiguous acres overlying Bakken oil shale. Company endeavors include a significant partner base; we work with Petronas, Shell, and Osaka Gas, and Northern Petroleum. Business Summary: Company Profile Pacific - Develop discovered/proven natural gas fields to service growing Fuel Oxygenate and Olefins demand in Asia; mainly China North America - Redevelop overlooked domestic onshore oil fields using Enhanced Oil Recovery techniques and new technologies |

NASDAQ: MPET Magellan Petroleum Corporation www.magellanpetroleum.com SEAAOC Darwin 4 Focus on Australian Plans * * * * * * |

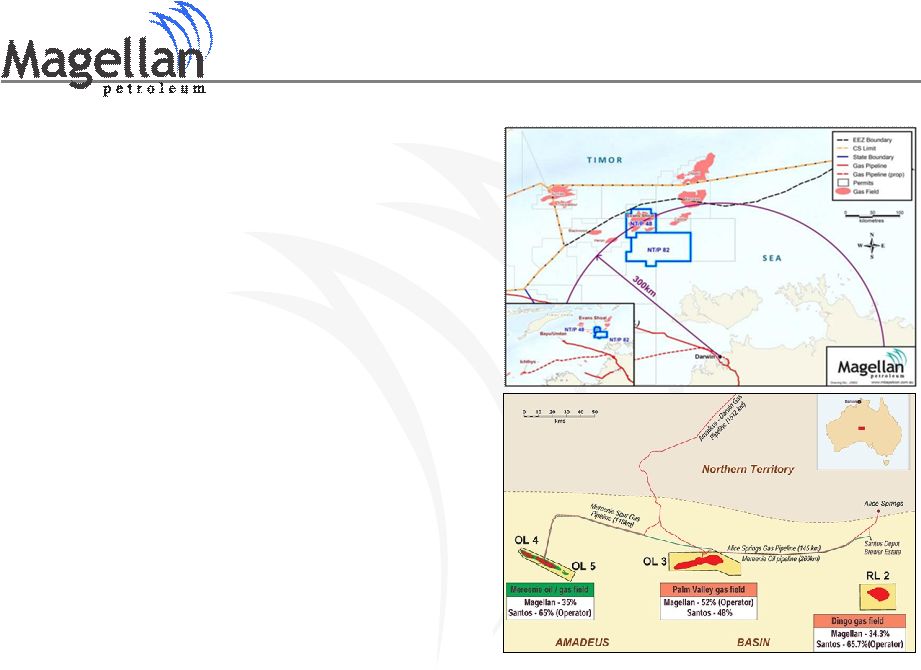

NASDAQ: MPET www.magellanpetroleum.com SEAAOC Darwin 5 • Long-time, onshore Australian Producer – In business since 1954 – 25 years of gas supply to Darwin uninterrupted – Three fields onshore, licenses offshore – P1 and P2 reserves, 2.8mmbbl and 49BCF net • Evans Shoal and NT/P82 offshore – Contracts to acquire highly prospective licenses offshore – Potential for significant and economic Methanol plan • Mereenie Oil Field, onshore Australia – Undrilled, significant contingent resources remain – Large oil ring with gas cap – Fuel gas for industrial development in Darwin – Substantial potential due to new drilling technology – Santos is the Operator • Palm Valley Gas Field, onshore Australia – Tight, highly fractured gas reservoir – Current supplier of Alice Springs volumes – Operator, Magellan Australia |

NASDAQ: MPET Magellan Petroleum Corporation www.magellanpetroleum.com SEAAOC Darwin 6 A New Direction Evans Shoal and Methanol * * * * * * |

NASDAQ: MPET www.magellanpetroleum.com SEAAOC Darwin 7 Evans Shoal and Methanol • Methanol production can use up to 25% CO2 in feedstock – Steam Methane Reforming o CH 4 + H2O = CO + 3H2 – Water Gas shift reaction o CO + H2O = CO2 + H2 – Methanol Synethesis o CO + 2H2 = CH3OH – Excess Hydrogen plus CO2 • CO2 +3H2 = CH3OH + H2O Market timing is good. Methanol leads to reduced oil imports and more efficient fuel consumption in Asia. It is a low-cost, environmentally-friendly feedstock for Olefins. Our project capitalizes on China’s large CAGR and emerging Methanol derivative Markets Methanol Evans Shoal • Key role in a larger value creation chain that ends up in Olefins or fuel markets in Asia • Ideally situated in shallow water close to existing facilities with good reservoir data • Larger Companies focus on bigger LNG business at fields that don’t require CO2 management • Evans Shoal has significant CO2 content |

Evans Shoal - Closest Supply Magellan Business Model Develop “discovered” resource for Asia Utilize Methanol as development tool; 1.Lowest cost Olefins feed (Polyethylene) 2.Methanol is mandated as fuel oxygenate in China 3.Methanol augments Chinese propane systems Gas Fields Key to China’s economy for next 50 years Process uses CO2 |

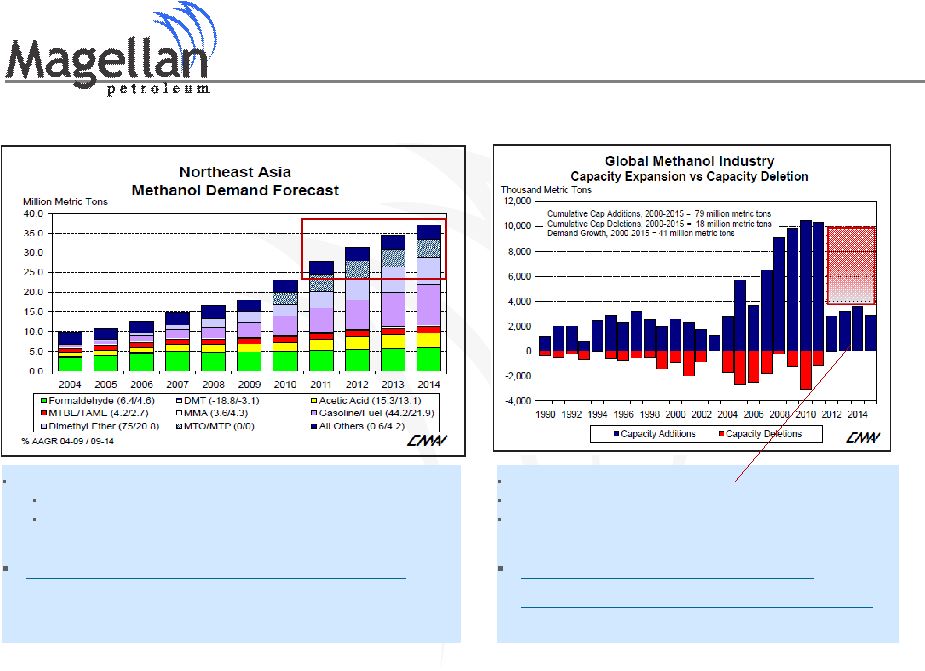

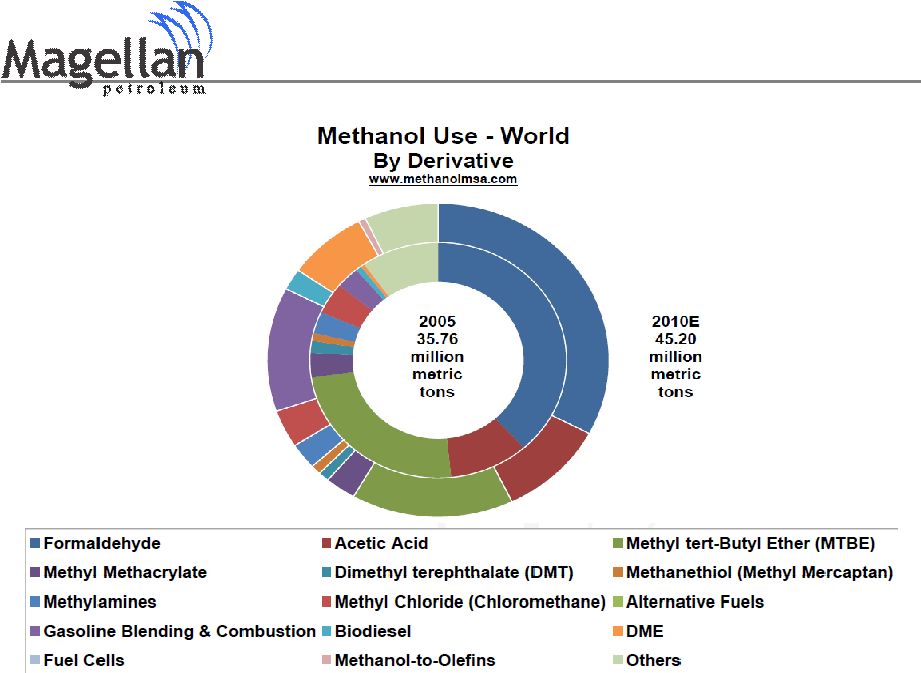

NASDAQ: MPET www.magellanpetroleum.com SEAAOC Darwin 9 Supply and Demand Methanol North East Asia Forecasted Annual Growth Rates of 13-15% Current 18mmtpy or 44% of Global Demand Forecasted 37mmpty or 57% of Global 19mmt Demand over 5years in NE Asia Iranian and Algerian “suggested plants” online 2014 Chinese Capacity is higher-cost Coal to Methanol Chile/New Zealand have Gas Supply constraints Iran and Algeria have the only proposed supply in 5 years Globally |

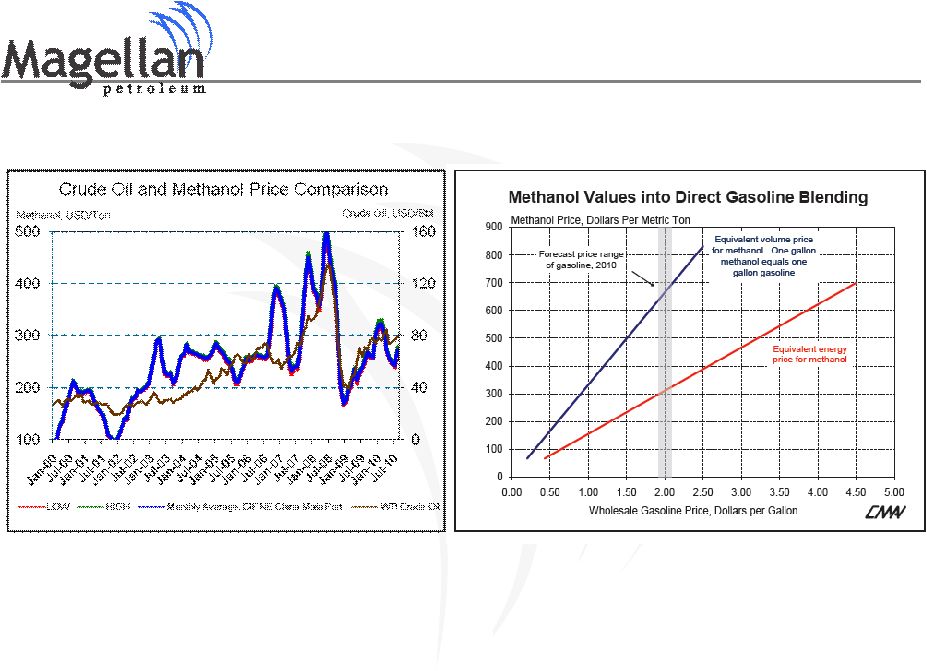

NASDAQ: MPET www.magellanpetroleum.com SEAAOC Darwin 10 Correlates to Oil, Cheaper than Gasoline Correlation Factor 0.81 |

NASDAQ: MPET www.magellanpetroleum.com SEAAOC Darwin 11 Pacific Methanol Market North East Asia Projected Annual Growth Rates of 13-15% Current 18mmtpy or 44% of Global Demand Forecasted 37mmpty or 57% of Global Demand Methanol Usage Vehicle fuel Propane Supplement Methanol to Olefins No new Pacific Methanol capacity planned 13% CAGR Indonesia 1mmt New Zealand .9mmt China 14mmt India .5mmt Malaysia 2.4mmt Russia 3.3mmt Europe 4.5mmt Iran 3.5mmt Saudi 6.6mmt Oman 1mmt Qatar .8mmt EG 1mmt Egypt 1.3mmt Libya .6mmt U.S. 1mmt Trinidad 6.5mmt Venezuela 1.4mmt Chile 4mmt Argentina .5mmt 2009 World Capacity – 68 mmT; 60% operating (excess capacity is high-cost lignite feed) |

NASDAQ: MPET www.magellanpetroleum.com SEAAOC Darwin 12 Asian Focus China imports 46% of Demand currently (8.3mmtpy) Forecasted to import 36% of Demand in 2014 (13.3mmtpy) Chinese Production 60% Coal (Higher-Cost Coal to Methanol) 22% Natural Gas 18% Coking Gas Chinese Utilization rate averages below 50% driven by costs and coal |

NASDAQ: MPET www.magellanpetroleum.com SEAAOC Darwin 13 Market Changing Fast |

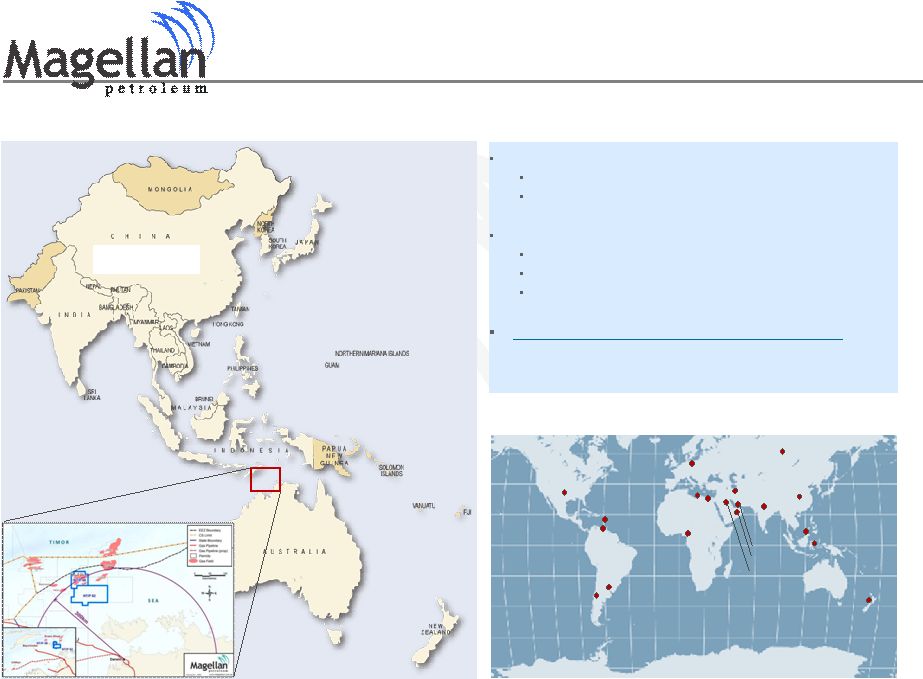

NASDAQ: MPET www.magellanpetroleum.com SEAAOC Darwin 14 Evans Shoal Competitive Advantage • Contract to acquire 40% interest in field – Other owners are Shell (25%), Petronas (25%), Osaka Gas (10%) • Hub Location (up to 80TCF in Bonaparte Basin) • Full 3D seismic coverage • Shallow water, huge structure • Close to markets, particularly China • Low marginal development cost • Proximity to Darwin and its facilities and port Up to 8 TCF - Methanol Central Darwin Bayu Undan LNG East Jetty NT Power Plants |

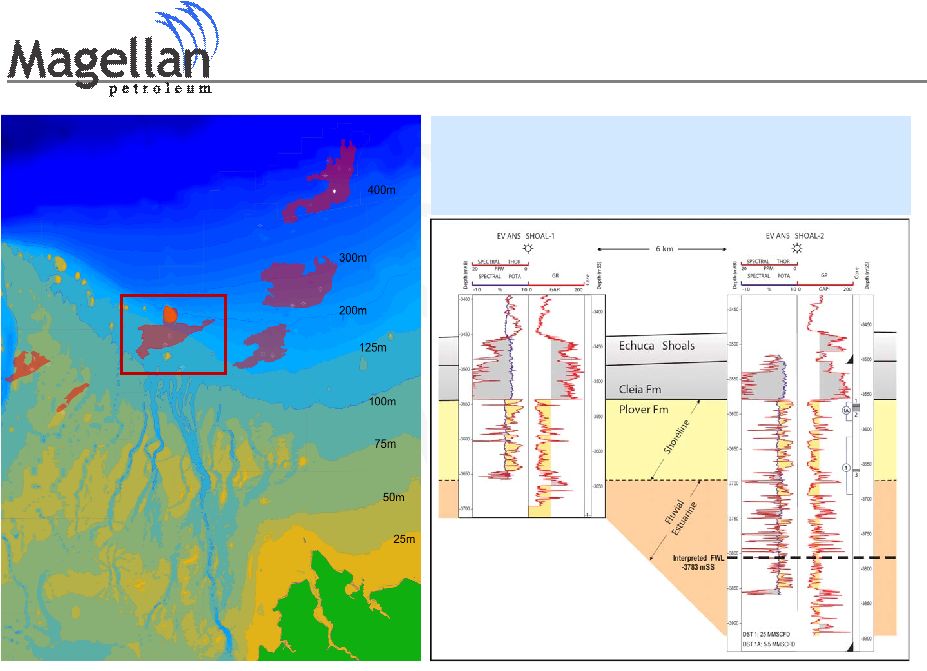

NASDAQ: MPET www.magellanpetroleum.com SEAAOC Darwin 15 Evans Shoal Abadi 10-14.5 TCF Inpex Evans Shoal Up to 8 TCF MPET-Shell-Petronas-Osaka Gas Caldita - Barossa 8 TCF COP-Santos Evans Shoal Heron /Blackwood 1.5 TCF MEO Australia • Evans Shoal-2 DST 25.5mmscf/d in upper third of Elang Plover • Drilled by Shell in 1998 to 3,850meters |

NASDAQ: MPET www.magellanpetroleum.com SEAAOC Darwin 16 Next Steps & Timeline Evans Shoal MAR10 – Enters into Agreement to purchase 40% interest in Evans Shoal from Santos JUNE 10 -Commonwealth / FIRB Letter stating “no objections” received AUG10 - Northern Territory Approval received Q4 10 - Methanol Site Development Gain approvals, establish team. Access to water, facilities, market is good Next to key existing projects & infrastructure Q410 – Santos Payment AUS$85mln (US$79 mln) Q4 10 - Financial and Offtake Partner(s) • Q4 10 – Development Strategy Key co-owner discussions Key development plan work next year New wells and targeted seismic 2011 - Further Testing / Offtake / Financing 2011 2012 2013 2014 Q3/10 Q4/10 Potential Private or Public Placement Finalize Initial Financial and Offtake Partners Cash US$35 mln Project Finance First Cash Flow Payment due to Santos Two wells Seismic add Wells #2-5 Wells 6 onward, Pipeline & Development Facilities First Production 2015 Next Well - 2011 FID |

NASDAQ: MPET www.magellanpetroleum.com SEAAOC Darwin 17 Corporate Profile Walter McCann Chairman Ex President, The American International University Chapel Hill, North Carolina J. Robinson West Chairman Designee Chair, Petroleum Finance Corp (PFC Energy) Washington, DC William Hastings President / CEO Portland, Maine Nikolay Bogachev Independent Investor President Young Energy Prize S.A Annisquam, Massachusetts J. Thomas Wilson Oil and Gas Advisor Denver, Colorado Ronald Pettirossi Head of Audit Committee Consultant-CPA Vero Beach, Florida Donald Basso Geologist, Advisor Calgary, Canada Robert Mollah Geophysical Consultant Brisbane, Australia Directors Bernstein Shur, Sawyer & Nelson 100 Middle Street West Tower Portland, Maine 04101 (207) 774-1200 Legal Counsel Management William H. Hastings Chief Executive Officer Antoine Lafargue Chief Financial Officer Susan M. Filipos Controller Daniel J. Samela Vice President, New Ventures J. Thomas Wilson Technical Advisor Jeffrey G. Tounge Manager, Commercial Operations Jeff Tounge Manager, Commercial Operations Magellan Petroleum Corp Tel: (207) 619-8504 Mob: (207) 850-0099 JTounge@magellanpetroleum.com Stock Transfer Agent American Stock Transfer & Trust 59 Maiden Lane New York, New York 10038 (800) 937-5449 (212) 936-5100 (718) 921-8336 fax Investor Relations Contact |

NASDAQ: MPET Magellan Petroleum Corporation www.magellanpetroleum.com SEAAOC Darwin 18 … A new direction * * * * * |