Annual General Meeting 8 th December, 2010 Orlando Exhibit 99.1 |

Non-GAAP Measures Disclosure Forward Looking Statements Statements in this presentation which are not historical in nature are intended to be, and are hereby identified as, forward-looking statements for purposes of the Private Securities Litigation Reform Act of 1995. These statements about Magellan and Magellan Petroleum Australia Limited (“MPAL”) may relate to their businesses and prospects, revenues, expenses, operating cash flows, and other matters that involve a number of uncertainties that may cause actual results to differ materially from expectations. Among these risks and uncertainties are the ability of MPAL, with the assistance of the Company, to successfully and timely close the Evans Shoal acquisition, the likelihood and timing of the receipt of proceeds from the Young Energy Prize S.A. private placement transaction due to conditions stipulated in the Securities Purchase Agreement dated August 6, 2010, the ability of the Company to successfully develop a strategy for methanol development, pricing and production levels from the properties in which Magellan and MPAL have interests, the extent of the recoverable reserves at those properties, the profitable integration of acquired businesses, including Nautilus Poplar LLC, the future outcome of the negotiations for gas sales contracts for the remaining uncontracted reserves at both the Mereenie and Palm Valley gas fields in the Amadeus Basin, including the likelihood of success of other potential suppliers of gas to the current customers of Mereenie and Palm Valley production. In addition, MPAL has a large number of exploration permits and faces the risk that any wells drilled may fail to encounter hydrocarbons in commercially recoverable quantities. Any forward-looking information provided in this presentation should be considered with these factors in mind. The Company assumes no obligation to update any forward-looking statements contained in this presentation whether as a result of new information, future events or otherwise. Oil and gas issuers are required to include disclosure regarding proved oil and gas reserves in certain filings made with the U.S. Securities and Exchange Commission. Proved reserves are the estimated quantities of crude oil, natural gas, and natural gas liquids which geological and engineering data demonstrate with reasonable certainty to be recoverable in future years from known reservoirs under existing economic and operating conditions, i.e., prices and costs as of the date the estimate is made. The SEC also permits the disclosure of probable and possible reserves which are additional reserves that are less certain to be recovered. Investors are urged to consider closely the disclosures in Magellan’s periodic filings with the SEC available from us at the company’s website www.magellanpetroleum.com Management believes that EBITDA, the non-GAAP (Generally Accepted Accounting Principles) measure indicated by an asterisk (*) used in this presentation provides investors with important perspectives into the company’s ongoing business performance. The company does not intend for the information to be considered in isolation or as a substitute for the related GAAP measures. Other companies may define the measure differently. We define EBITDA as follows: earnings before the deduction of interest expenses, taxes, depreciation and amortization. |

NASDAQ: MPET www.magellanpetroleum.com AGM 2010 3 Magellan’s mission is to provide substantial growth and long-term value to shareholders by acquiring, developing and producing oil and natural gas resources using the following strategy: 1. Acquire and develop discovered, but “under-exploited” natural gas and oil reserves 2. Add value through unconventional commercial solutions 3. Be unique while maintaining a strong balance sheet and financial flexibility Mission Statement Mission and Strategy Success in executing plans will provide “proof of concept” Business Summary Pacific - Develop discovered/proven natural gas fields to service growing vehicle fuel oxygenate demand in Asia; mainly China North America - Redevelop overlooked domestic onshore oil fields using Enhanced Oil Recovery (EOR) techniques and new technologies |

NASDAQ: MPET www.magellanpetroleum.com AGM 2010 4 Change of Management Evans Shoal Announcement Montana Announcement Share Performance History |

NASDAQ: MPET www.magellanpetroleum.com AGM 2010 5 Earnings Comparison (in US$) FY2010 FY2009 (yoy %) Oil sales 9,886,592 11,479,660 -14% Gas sales 13,615,755 14,740,296 -8% Other production related revenues 5,022,210 1,970,621 155% Revenues $28,524,557 $28,190,577 1% Production costs (10,116,320) (8,153,263) 24% Exploratory and dry hole costs (1,273,268) (3,475,937) -63% Salaries and employee benefits (4,816,350) (1,708,997) 182% Auditing, accounting and legal services (1,947,901) (1,576,509) 24% Shareholder communications (551,408) (633,112) -13% Other administrative expenses (6,707,184) (3,969,658) 69% Total costs and expenses (25,412,431) (19,517,476) 30% Adjusted EBITDA* $3,112,126 $8,673,101 -64% Margin 11% 31% Depletion, depreciation and amortization (4,680,240) (6,785,952) -31% Accretion expense (748,209) (531,405) 41% Gain (loss) on sale of assets 4,767,688 (75,812) nm Operating income 2,451,365 1,279,932 92% Warrant expense (4,276,471) - Investment and other income 3,012,831 1,583,065 90% Income before income taxes 1,187,725 2,862,997 -59% Income tax expense (2,645,763) (2,198,422) 20% Net (loss) income (1,458,038) 664,575 -319% Net (loss) attributable to non-controlling interest in subsidiaries (10,766) - Net (Loss) income attributable to MPC ($1,468,804) $664,575 -321% EPS (basic and diluted) (0.03) 0.02 Operational Data: Oil sales (bbls) 139,409 153,297 -9% Australia 97,392 153,297 Nautilus 42,017 - Gas sales (bcf) 3.43 5.16 -34% Net realized price (A$ / mcf) 5.07 3.54 43% Notes: *Adjusted EBITDA represents EBITDA adjusted for non cash and none recurring items |

NASDAQ: MPET www.magellanpetroleum.com AGM 2010 6 Cash Flow Overview (in US$) FY2010 FY2009 Operating Activities: Net (loss) income ($1,458,038) $664,575 Depletion, depreciation and amortization 4,680,240 6,785,952 Accretion expense and Deferred Income Tax 1,670,143 (1,086,628) (Gain)/loss from disposal of assets (4,767,688) 12,072 Gain from sale of investments (1,975,286) - Stock-based compensation and change in warrant valuation 6,582,223 94,932 Exploration and dry hole costs and writeoffs - 365,236 Changes in working capital (1,511,172) 2,402,913 Net cash provided by operating activities $ 3,220,422 $ 9,239,052 Investing Activities: Additions to property and equipment (2,276,128) (2,430,184) Proceeds from sale of assets 7,280,402 27,728 Oil and gas exploration activities (567,343) (491,490) Net proceeds from sale of securities 2,821,137 (559,850) Marketable securities matured or sold 997,306 710,916 Deposit for purchase of Evans Shoal (13,751,850) - Purchase of interest in Nautilus / Poplar (11,084,556) - Increase in restricted cash (75,444) - Net cash (used) in investing activities $ (16,656,476) $ (2,742,880) Financing Activities: Debt principal payments (845,147) - Proceeds from borrowings 570,000 - Proceeds from issuance of stock and warrants 10,000,000 - Equity issuance costs - (259,879) Net Cash provided by (used in) financing activities $ 9,724,853 $ (259,879) Effect of exchange rate changes on cash and cash equivalents 2,613,893 (6,162,679) Cash at beginning of period 34,688,842 34,615,228 Change in Cash Position $ (1,097,308) $ 73,614 Cash at end of period $ 33,591,534 $ 34,688,842 |

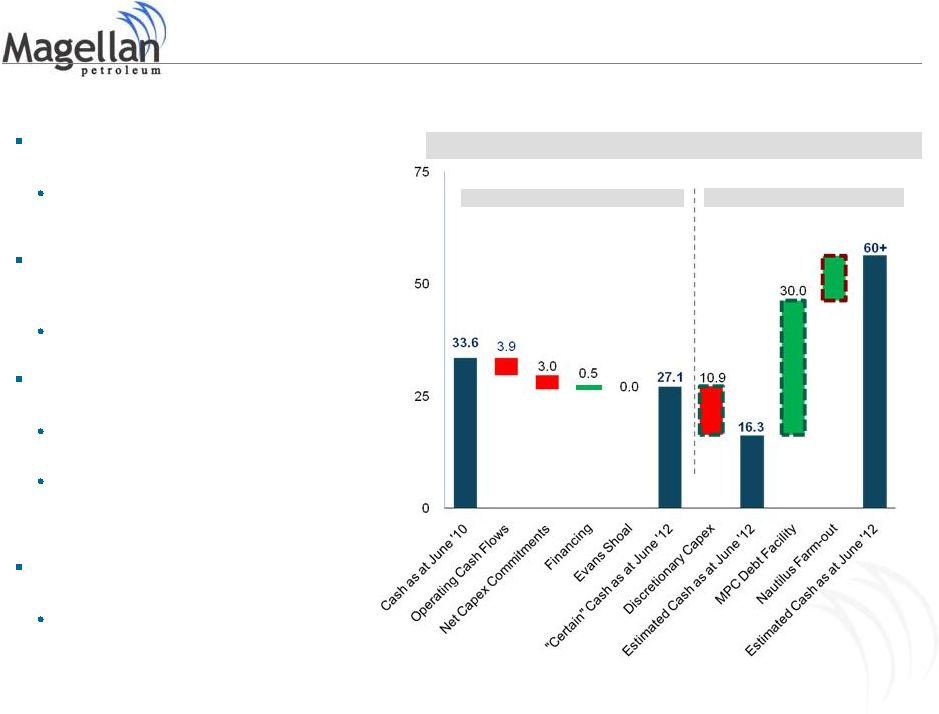

Cash Forecasts MAGELLAN’S CASH FORECASTS “CERTAIN” ESTIMATED Magellan’s cash position by end of June 2012 is expected to be US$27m This reflects Magellan’s budgeted current financial commitments and head office expenses Magellan’s discretionary CAPEX at the US Poplar fields is expected to be partially financed via farm- out This will have a positive cash impact in an amount to be negotiated In addition, the Company is negotiating a new borrowing base facility of approx. US$30m The borrowing base will be secured by the Company’s existing reserves The size of the facility could be materially increased when Mereenie enters into a new gas sales contract and/or significant additional reserves were proven at Poplar Magellan is actively seeking to market the gas from the Mereenie field in Australia Potential renewal with LNG developer in Darwin could add US$20-30m per annum TBD NASDAQ: MPET www.magellanpetroleum.com AGM 2010 7 |

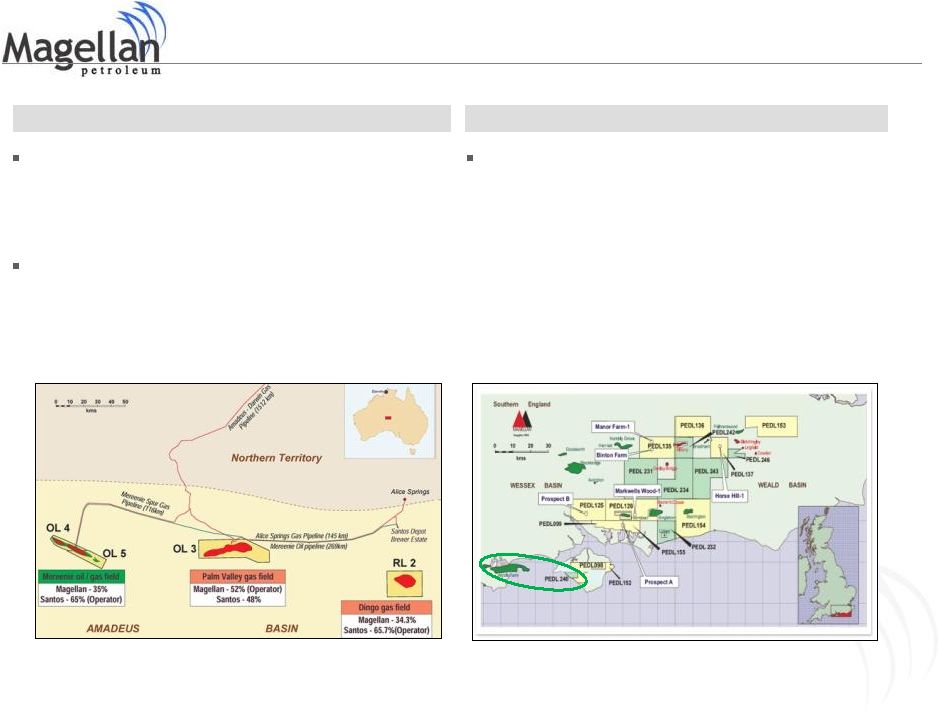

NASDAQ: MPET www.magellanpetroleum.com AGM 2010 8 Portfolio Overview Evans Shoal Up to 8 Tcf (gross) planned methanol development offshore Australia Payment due to Santos on Dec. 25 th , moving toward closing Ongoing discussions with Industry and Financial partners Poplar Current proved reserve base of 9.5 mmbbl in the Charles Formation only (1.75 mmbbls in PDP, 0.77 mmbbls in PDNP, and 6.96 mmbbls in PUD) Current production capacity of 290 bbls/d Significant new PUD bookings show current and future drilling Palm Valley/ Mereenie Mereenie gas sales contract expired in Sept. 2010 – optimistic for future monetization Currently producing approximately 500bbls/d (gross) Production cost reductions have been effective Palm Valley local gas sales contract expires in Jan 2012 Contingent resource base of 190+ BCF (gross) United Kingdom Markwells Wood -1 well current drilling to offset existing oil production Some licenses offset the large Wytch Farm field Deep Gas and Shale potential (farm-out discussions now) Four distinct portfolio segments |

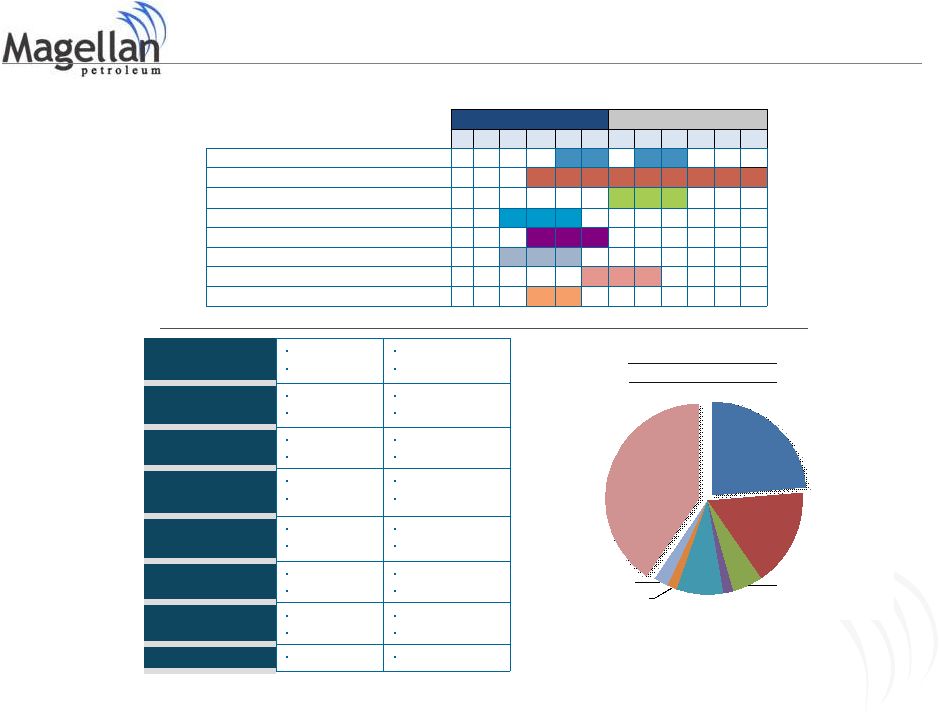

NASDAQ: MPET www.magellanpetroleum.com AGM 2010 9 Bakken (Possible Carry) $7.0 Charles Infill $5.0 Tyler Nisku $1.5 Red River $2.4 Greenhorn $0.5 NT09-1 $0.5 UK , $0.7 Evans Shoal (carried) $12.0 Future Capital Plan FY2011 FY2012 J F M A M J J A S O N D Bakken Development (possible carry) Charles Infill Tyler / Nisku Duperow / Red River Greenhorn Shale Core/Shallow Gas UK Follow Up Evans Shoal Delineation NT09-1 Reprocessing – Total CAPEX for 2011 is $29.6 mln – Less carries Total CAPEX for FY2011 is $11 mln – Bakken development will be determined with partner entry – Charles Infill is in preparation for CO2 pilot Bakken Number of wells Cost per well 2 $3.5 mln (carried) Charles Number of wells Cost per well 5 $1 mln Tyler / Nisku Number of wells Cost per well 1 $1.5 mln Greenhorn Shale Shallow Gas Number of wells Cost per well 1 $0.5 mln Duperow Red River Number of wells Cost per well 1 $2.4 mln UK Follow Up Number of wells Cost per well 0 $0.7 mln ES Delineation Number of wells Cost per well 1 $12 mln (carried) NT09-1 Seismic $0.5 mln Total Costs: $29.6mln Less Carries: $11 mln |

NASDAQ: MPET www.magellanpetroleum.com AGM 2010 10 General and Administrative Trends Human Resources New Ventures will necessitate the addition of new people Operations Staff Development expertise Government Relations Admin Administratively we will reorganize Centralized office near assets and field co-owners Rationalization of dual operator position in the Amadeus Basin Development Recent emphasis has been on execution and “proof of concept” Future efforts will begin to move toward further new development This will necessitate capital structuring work; including new share issues targeted at premiums to current prices for significant, value add developments Substantial value can be achieved through business combination with undervalued small cap energy companies |

AGM 2010 NASDAQ: MPET www.magellanpetroleum.com Evans Shoal |

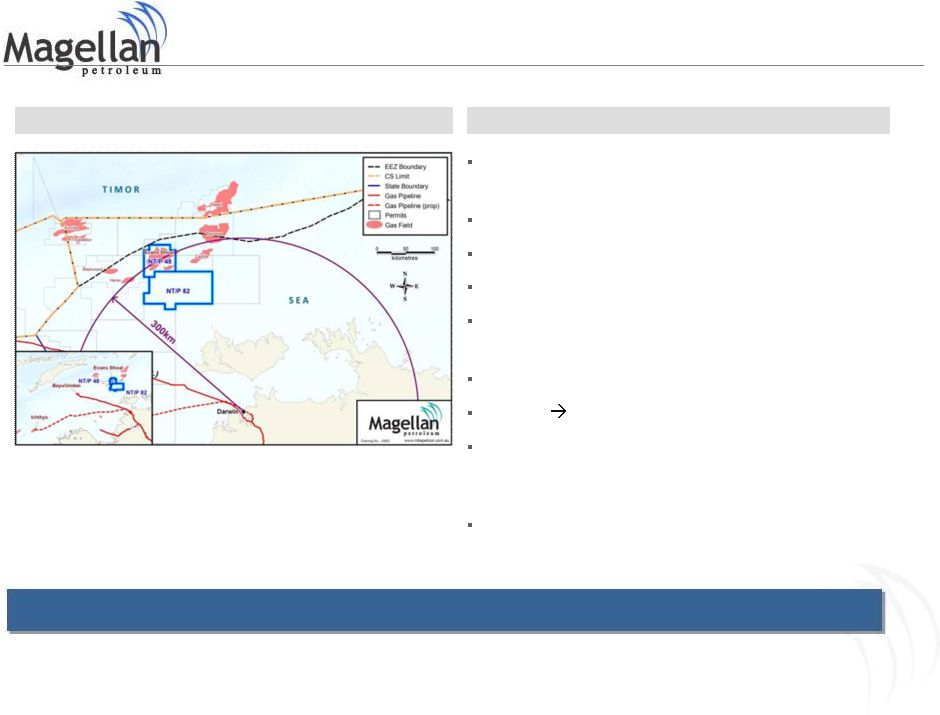

NASDAQ: MPET www.magellanpetroleum.com AGM 2010 12 Contract to acquire 40% interest in field • Partners are Shell (25%), Petronas (25%), Osaka Gas (10%) Gross reserves of up to 8TCF (including CO 2 ) Hub Location (up to 80 TCF in Bonaparte Basin) Also awarded NT09-1 Field is in relatively shallow water (50 feet to 475 feet) • Lower cost jack-up rigs capable at depths to 400 feet Full 3D seismic coverage done over 215 sq mile structure Darwin deepwater port & existing facilities Magellan will continue to conduct operations in an environmentally responsible manner and work in partnership with the indigenous community North East Asia methanol market Annual Growth Rates for consumption is expected to be 11%; likewise, imports are expected to grow at 8% annual rates (CMAI 1 ) Evans Shoal EVANS SHOAL STRATEGIC LOCATION Notes: (1) CAGR figures provided by CMAI, see slide 11 Evans Shoal reserves targeted (with CO 2 content) as Methanol feedstock |

NASDAQ: MPET www.magellanpetroleum.com AGM 2010 13 China Methanol Market Coastal • Most of Chinese demand is and will remain coastal • >50% of Chinese demand in East China and South China allowing for competition from imports Inland • Majority of coal-based producers in Northern and Western China are small-scale and inefficient (less than 130,000 tons) • Inability to compete with low-cost coastal imports ANALYSIS BY REGION MTO (METHANOL-TO-OLEFINS) TRANSPORTATION FUEL Methanol-based production effectively competing with naphtha (becoming expensive with rising oil price) Ability for coal producers to forward-integrate into the petrochemical chain, where value is generally derived from methanol to olefins, with polyolefins as a means to monetize olefins production Integrated and captive market with limited impact on price. Seen as price-taker where naphtha is setting prices Independence, diversification and security of Chinese fuel supply Regulation will be required to support growth and related infrastructures “Green fuel” allowing cleaner and more efficient combustion Methanol to play an important part in price setting with fuel applications expected to increase in a high oil price environment CHINA METHANOL MARKET MMTPA 2010 2020 Capacity 34.4 53.2 Production 12.8 39.9 Operating Rate 37% 75% Consumption 19.5 55.2 Net Imports (6.8) (15.3) |

Evans Shoal Structural Discussion Moving Forward AGM 2010 NASDAQ: MPET www.magellanpetroleum.com |

NASDAQ: MPET www.magellanpetroleum.com AGM 2010 15 Near term signing of MoU Work with co-owners of the field on a “go forward” plan Gain all necessary approval Evaluate capital restructuring plan -Begin strategic discussions regarding placement of debt or equity at appropriate prices. -Place standby debt facility Strategic Partner Historically supportive shareholder Assessed independently through special committee Provides an industrial plan with off take agreement that can be financed Elements of an MoU received -Downstream partners and project management -Upstream equity interest -Volume -Timing -Pricing Structure Initiate Darwin site award Various third party interests were evaluated at different stages Challenge to bring in a comparable process, especially with regard to timing Interest from Asian players is being considered: Korea, China Two over-arching considerations – Main decision factor is the certainty of proceeds – Enhance Shareholder value Mid term strategy – Implement near-term financial structure with plan to issue new shares or debt longer-term. – Complete off take agreement pursuant to MoU – Gain “Major Project” status in Darwin Rationale Evaluation of other options YEP most attractive option, after careful review of funding alternatives INDUSTRIAL PARTNER YEP OTHER NEXT STEPS |

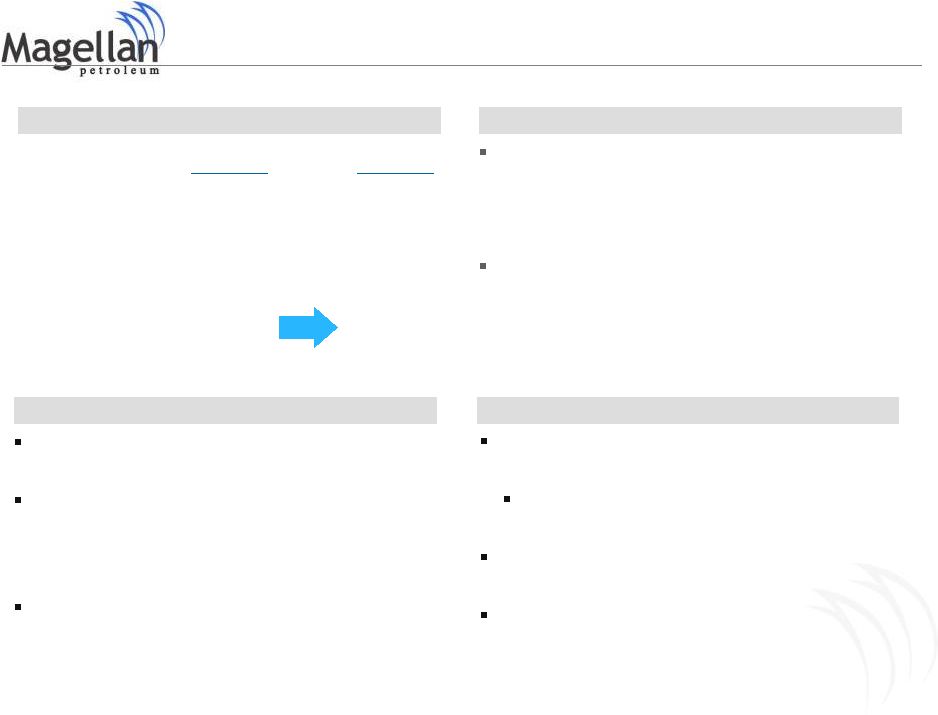

NASDAQ: MPET www.magellanpetroleum.com AGM 2010 16 Current Company Structure CURRENT AUSTRALIAN ORGANISATION Other Assets 27% (1) 73% 100% (1) Fully diluted with warrants • Mereenie • Palm Valley • Dingo • UK • Other Evans Shoal Asset Sale Deed YEP FREE FLOAT MAGELLAN MPAL / MGT |

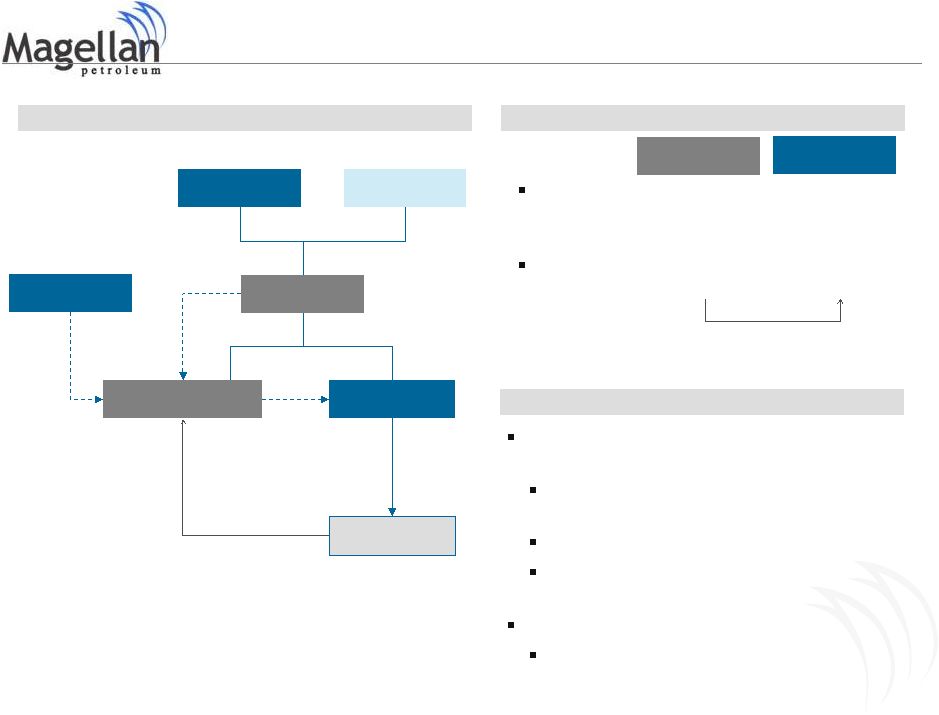

NASDAQ: MPET www.magellanpetroleum.com AGM 2010 17 Loan US$85m Acquisition Structure AT COMPLETION ECONOMICS FOLLOWING CONVERSION YEP MAGELLAN YEP FREE FLOAT / MGT MPAL (Old) - Properties 33% (1) 67% Evans Shoal Permit Loan US$70m +/- MPAL (New) - Group Convertible post PIPE US$15m (1) Includes exercise of 4.4m warrant shares and issuance of 5.2m PIPE#2 shares SHAREHOLDER VALUE Economic interest in first 3 Tcf Economic interest beyond first 3Tcf 51% 5% 49% 95% Call option to increase economic interest to 51%, at discount to NPV Significant value creation at attractive cost to Magellan $13.8m deposit and 5.2 mln shares @$3 to acquire approximately 110mmBOE Carried through first $26m FEED costs Option to increase economic interest to 51% in reserves beyond 3 Tcf at discount Enables the project to move forward Monetise major stranded gas assets in Australia YEP MAGELLAN |

North American Activities AGM 2010 NASDAQ: MPET www.magellanpetroleum.com |

NASDAQ: MPET www.magellanpetroleum.com AGM 2010 19 Currently holds 9.5 mmbbls of Proven net oil reserves (based on SEC rules) in the Charles formation Left relatively dormant for the last several decades, Poplar is a strong candidate for an aggressive infill program and CO 2 flood in order to maximize recovery Recent drilling results and existing wells show other pay zones exist within this acreage and include: • Shallow Gas in the Judith River Fm • Greenhorn Oil Shale Niobrara stratigraphic equivalent and Eagle Ford analog • Charles • Mission Canyon • Lodgepole • Bakken/Three Forks • Duperow • Red River Poplar Oil Fields POPLAR, MT STRATEGIC LOCATION EPU#119 The Poplar complex is a candidate for Tertiary CO 2 flooding. The success case with this EOR program is a 10% + incremental oil recovery profile |

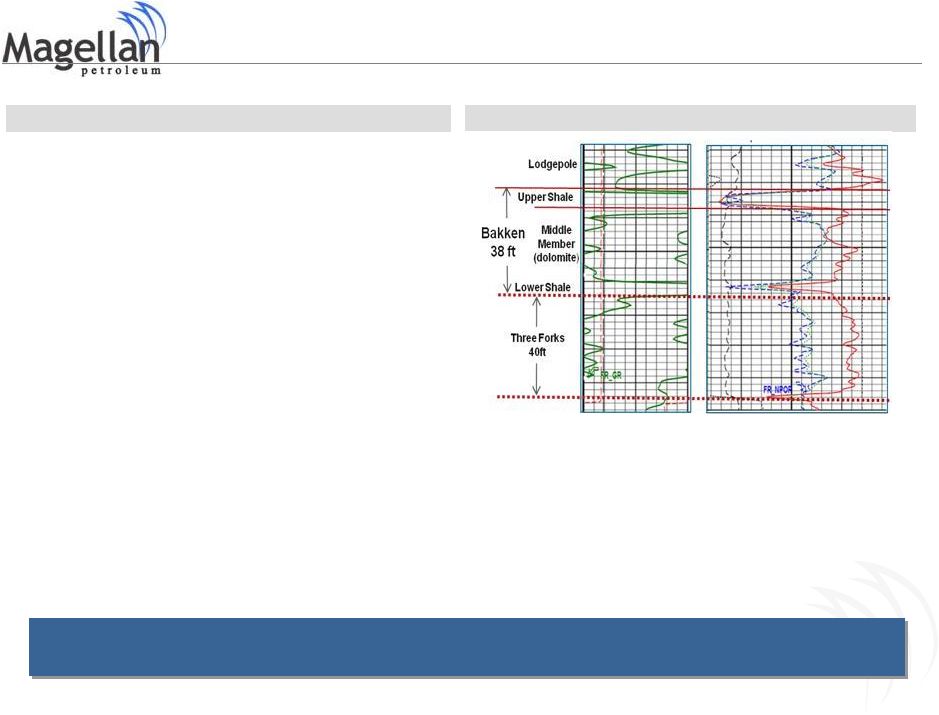

NASDAQ: MPET www.magellanpetroleum.com AGM 2010 20 Cased to the Nisku (7132 ft) on 11/12/2010. Well results as of today are as follows: • Shallow Judith River gas pressure seen • New Greenhorn Oil Shale (2282’) (Niobrara stratigraphic equivalent) is oil saturated and contains positive development characteristics. Core planned in 2011 • Tyler testing impractical due to high mud weights maintained through the Dakota. New well needed to test at lower mud weights. • Charles core completed and is currently under analysis. Logs showed excellent porosity and permeability in the B and C. Recompletion planned post-Nisku work. • Nisku formation penetrated but with high weight water-based mud. Relative permeability has been affected. Currently producing high water cut but are attempting to draw down pressure and place packers to isolate water and improve oil cut. Next move up to recomplete Charles. Montana Results: EPU #119 Well Magellan - EPU #119 Poplar MT EPU #119 WELL RESULTS BAKKEN FORMATION • Bakken and Three Forks core successfully obtained and analyzed 1.Gas as high as 9000 units seen in the Lodgepole 2.Substantial fracturing and fair to good porosity 3.Permeability was higher than that of Elm-Coulee 4.Middle Bakken is over pressured and mature 5.Core analysis indicates oil and gas saturation 6.Three Forks results were better than expected. Seven distinct, yet independent, stacked development intervals |

NASDAQ: MPET www.magellanpetroleum.com AGM 2010 21 Poplar Development Strategy Proven Reserves Optimize production from the existing PDP reserve base, and execute work program to bring the PDNP reserve base online Drill PUD locations starting in 2011 Additional Infill Move down to 40 or 80 acre spacing in the Charles reservoir in preparation for CO 2 flood CO 2 Pilot Initiate “Huff-n-Puff” CO 2 EOR pilot in 2Q 2012, including one injector and 4 producers. Full CO 2 Flood A full CO 2 flood would be implemented at the Field after successful pilot A successful CO 2 flood could result in additional recovery of 10% or 80 mmbbl Bakken Shale Various well penetrations and logs confirm the presence of the Bakken The recent EPU#119 well cored 61’ of Bakken/Three Forks formation. Prospective Zones Work program for other pay zones documented in the field: Shallow Gas in the Judith River Fm, Greenhorn Oil Shale, Mission Canyon, Lodgepole, Duperow, and Red River Seven distinct, yet independent, stacked development intervals |

AGM 2010 NASDAQ: MPET www.magellanpetroleum.com |

NASDAQ: MPET www.magellanpetroleum.com AGM 2010 23 United Kingdom drilling development • Offset drilling to existing oil production • Some licenses offset the large Wytch Farm field • Deep Gas and Shale potential (farm-out discussions now) Onshore UK & Australia AUSTRALIA UNITED KINGDOM Mereenie Oil Field, onshore Australia • Magellan is 35% • Sales contract expired in September 2010 • Contingent resources of 150 BCF and 2 mmbbls (gross) Palm Valley Gas Field, onshore Australia • Magellan is 52% and operator • Contingent resources of 40 BCF (gross) • Discussing new gas sales contract for remaining life of reserves |

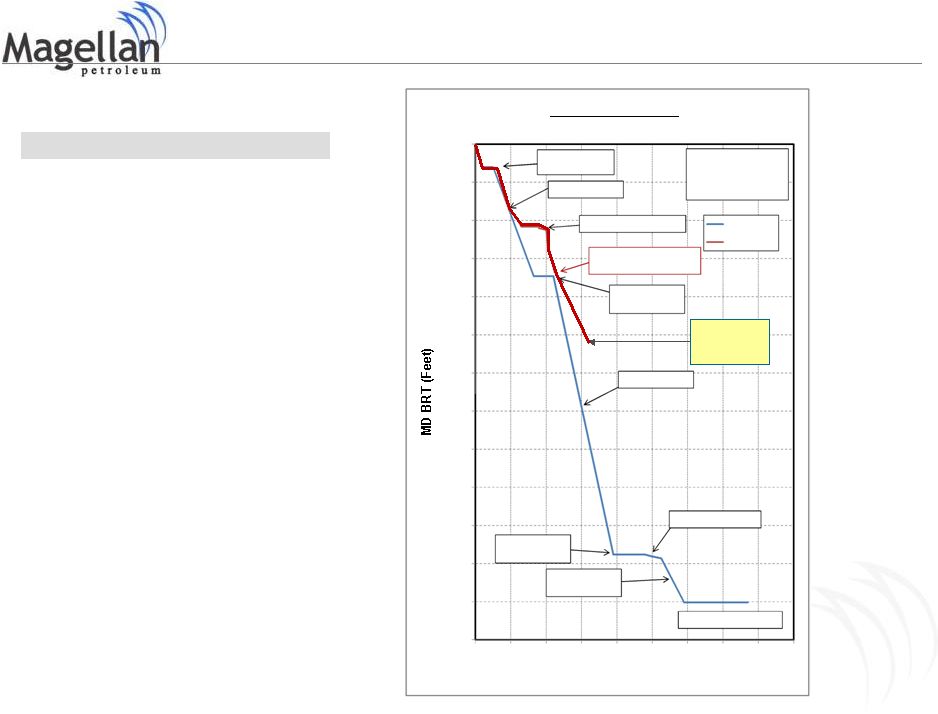

NASDAQ: MPET AGM 2010 24 0 500 1000 1500 2000 2500 3000 3500 4000 4500 5000 5500 6000 6500 Markwells Wood 1 Time Vs Depth Set 18?" Casing Location: PEDL 126 00°55'14.46"W 310 ft 50°54'31.59"N Drill 17½" hole Spuded: 21-Nov-2010 Cement off loss zones Prognosed Actual Day 11 Rpt: Depth 1682 ft 02-Dec 06:-0 hr GMT Set 13?" Casing 1730 ft Drill 12¼" hole Core 30 ft 8½" hole Set 9?" Casing 5381 ft Drill 8½" hole Well TD 6009 ft Log, Complete, Demob 0 5 10 15 20 25 30 35 40 45 DAYS UK Development Update Current Position – Spud Date November 21, 2010 – Late December logging, evaluation and completion – Structure drilled at significant angle to avoid area faulting – Subsequent testing without rig planned. Dependent on flow characteristics – Expected well cost of $4.4 million equivalent. Magellan held a 50% interest initially. 10% of that ownership has been farmed-out in return for payment of 20% of drilling costs. Magellan’s net cost is expected to be $1.3 million prior to initiation of testing. MARKWELLS WOOD 1 |

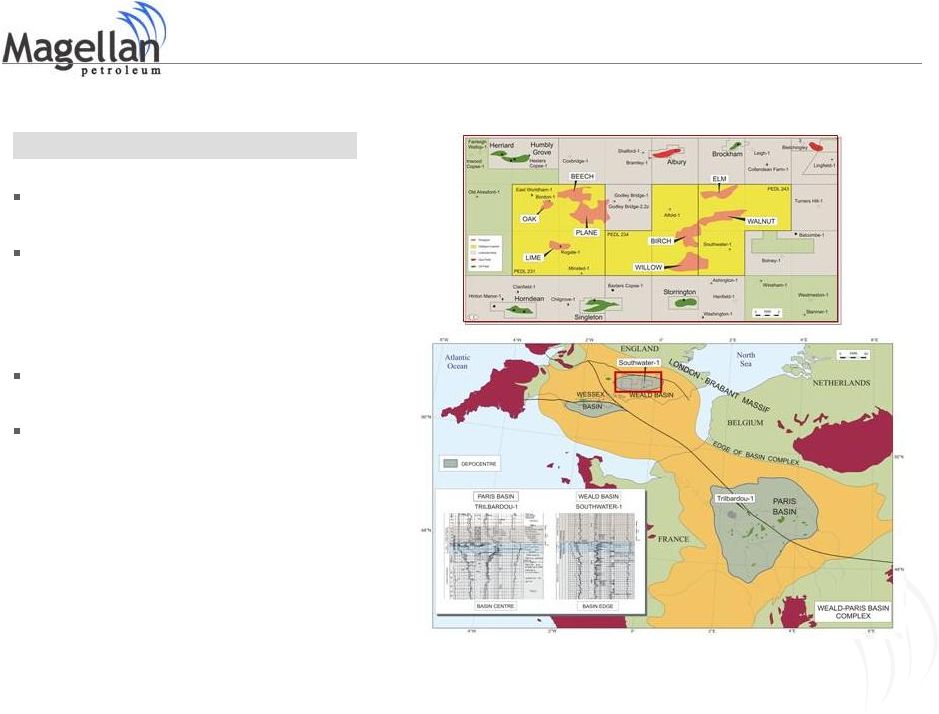

NASDAQ: MPET www.magellanpetroleum.com AGM 2010 25 The acreage is held by Celtique (50%, Operator) and Magellan (50%) The Weald Basin area is located in countryside south west of London, close to the large south east UK energy market and proximal to major gas trunk lines and refineries Licences cover contiguous 1,000 sq kms (247,000 acres) Actively marketing shale development farm in, likely will need to gain further data UK Shale Acreage Update SHALE POSITION |

New Opportunities and Shareholder Value AGM 2010 NASDAQ: MPET www.magellanpetroleum.com |

NASDAQ: MPET www.magellanpetroleum.com AGM 2010 27 New Opportunities Pacific Methanol Several over-looked gas fields have been identified as the next major fields for methanol development in the Pacific North American Oil & Gas Augment acreage in Montana Match under-valued gas purchasing companies with existing Upstream development opportunities Undervalued Small-Cap Energy Cos Consolidate smaller, yet valuable, energy companies via issuance of new share CO2 Sourcing Improve value proposition from CO 2 tertiary flooding via control of CO 2 sources No shortage of opportunity once current work is done |

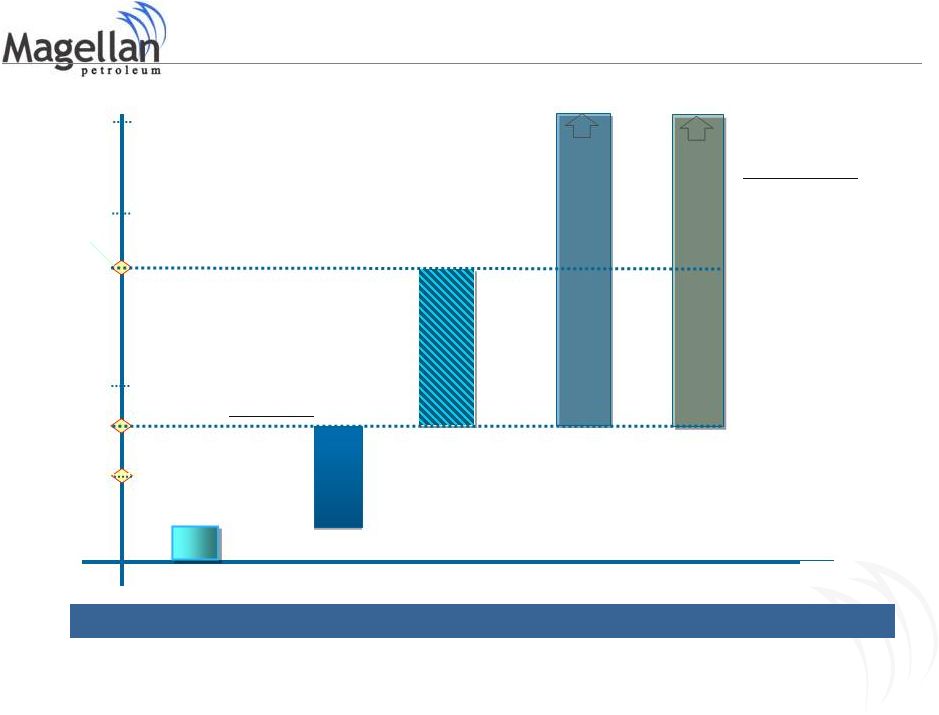

NASDAQ: MPET www.magellanpetroleum.com AGM 2010 28 100 200 300 400 US$ millions (net to Magellan) 500 Market Cap Liquidation (no gas value) Sale of Mereenie Gas Cash Note : Each module represents results of Excel economic evaluation Evans Shoal Methanol Value Future growth • Evans Shoal Gas Development •Montana Infill/Tertiary Work •Mereenie West-end Drilling • Potential UK Discovery •Undervalued Smallcap Acquisition Poplar Redevelopment Value Cash Position and Value PIPE2 @ $3 Magellan remains substantially undervalued pending “proof of concept” |

AGM 2010 NASDAQ: MPET www.magellanpetroleum.com |