Exhibit 99.3

| 1 The Manitowoc Company Acquisition of Enodis plc April 14, 2008 |

| 2 NO OFFER OR SOLICITATION This presentation does not constitute an offer to sell or an invitation to purchase any securities or the solicitation of an offer for or buy any securities, pursuant to the acquisition or otherwise. Full details of the acquisition, which will be implemented by means of a UK scheme of arrangement under the UK Companies Act 2006, will be contained in the scheme document that will be circulated to Enodis shareholders. Copies of this presentation and any documentation relating to the acquisition must not be, directly or indirectly, mailed or otherwise forwarded, distributed or sent in or into or from any other jurisdiction where to do so would be unlawful. The directors of The Manitowoc Company, Inc. (“Manitowoc”) and MTW County Limited (“Bidco”) accept responsibility for the information contained in this presentation, except that the only responsibility accepted by them in respect of the information contained in this presentation relating to Enodis is to ensure that such information has been correctly and fairly reproduced and presented. Subject as aforesaid, to the best of the knowledge and belief of the directors of Manitowoc and Bidco (who have taken all reasonable care to ensure that such is the case), the information contained in this document for which they are responsible is in accordance with the facts and does not omit anything likely to affect the import of such information. |

| 3 SAFE HARBOR STATEMENT This presentation includes “forward-looking statements” intended to qualify for the safe harbor from liability under the Private Securities Litigation Reform Act of 1995. These statements are based on the current expectations of the management of Manitowoc and are subject to uncertainty and changes in circumstances. The forward-looking statements contained herein include statements about the expected effects on Manitowoc of the proposed acquisition of Enodis, the expected timing and conditions precedent relating to the proposed acquisition of Enodis, anticipated earnings enhancements, estimated cost savings and other synergies, costs to be incurred in achieving synergies, potential divestitures and other strategic options and all other statements in this presentation other than statements of historical fact. Forward-looking statements include, without limitation, statements typically containing words such as “intends”, “expects”, “anticipates”, “targets”, “estimates” and words of similar import. By their nature, forward-looking statements are not guarantees of future performance or results and involve risks and uncertainties because they relate to events and depend on circumstances that will occur in the future. There are a number of factors that could cause actual results and developments to differ materially from those expressed or implied by such forward-looking statements. These factors include, but are not limited to, unanticipated issues associated with the satisfaction of the conditions precedent to the proposed acquisition; issues associated with obtaining necessary regulatory approvals and the terms and conditions of such approvals; the inability to integrate successfully Enodis within Manitowoc or to realize synergies from such integration within the time periods anticipated; and changes in anticipated costs related to the acquisition of Enodis. Additional factors that could cause actual results and developments to differ materially include, among others, unanticipated changes in revenue, margins, costs, and capital expenditures; issues associated with new product introductions; matters impacting the successful and timely implementation of ERP systems; foreign currency fluctuations; increased raw material prices; unexpected issues associated with the availability of local suppliers and skilled labor; the risks associated with growth; geographic factors and political and economic risks; actions of Manitowoc competitors; changes in economic or industry conditions generally or in the markets served by the Manitowoc and Enodis; the state of financial and credit markets; unanticipated issues associated with refresh/renovation plans by national restaurant accounts; efficiencies and capacity utilization of facilities; issues related to new facilities and expansion of existing facilities; work stoppages, labor negotiations, and labor rates; government approval and funding of projects; the ability of customers to receive financing; and the ability to complete and appropriately integrate restructurings, consolidations, acquisitions, divestitures, strategic alliances, and joint ventures. Information on the potential factors that could affect Manitowoc is also included in its filings with the Securities and Exchange Commission, including, but not limited to, its Annual Report on Form 10-K for the fiscal year ended December 31, 2007. Manitowoc undertakes no obligation to update or revise forward-looking statements, whether as a result of new information, future events or otherwise. Forward-looking statements only speak as of the date on which they are made. |

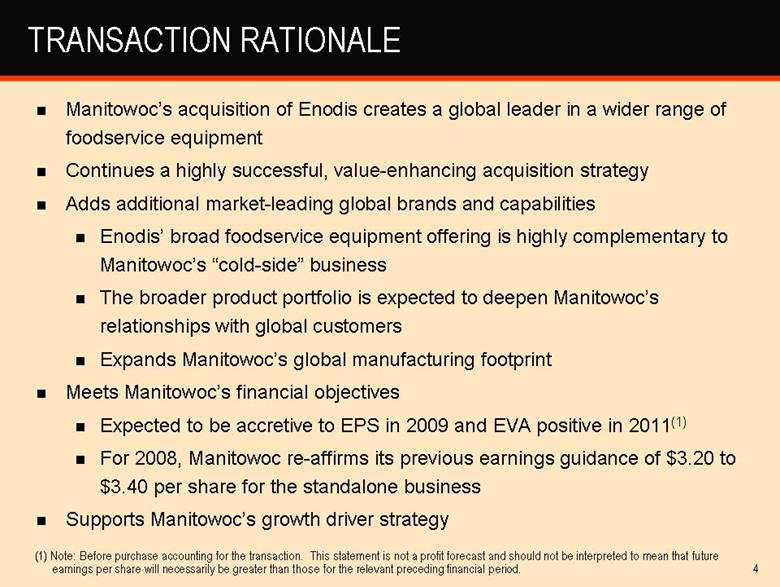

| 4 TRANSACTION RATIONALE Manitowoc’s acquisition of Enodis creates a global leader in a wider range of foodservice equipment Continues a highly successful, value-enhancing acquisition strategy Adds additional market-leading global brands and capabilities Enodis’ broad foodservice equipment offering is highly complementary to Manitowoc’s “cold-side” business The broader product portfolio is expected to deepen Manitowoc’s relationships with global customers Expands Manitowoc’s global manufacturing footprint Meets Manitowoc’s financial objectives Expected to be accretive to EPS in 2009 and EVA positive in 2011(1) For 2008, Manitowoc re-affirms its previous earnings guidance of $3.20 to $3.40 per share for the standalone business Supports Manitowoc’s growth driver strategy (1) Note: Before purchase accounting for the transaction. This statement is not a profit forecast and should not be interpreted to mean that future earnings per share will necessarily be greater than those for the relevant preceding financial period. |

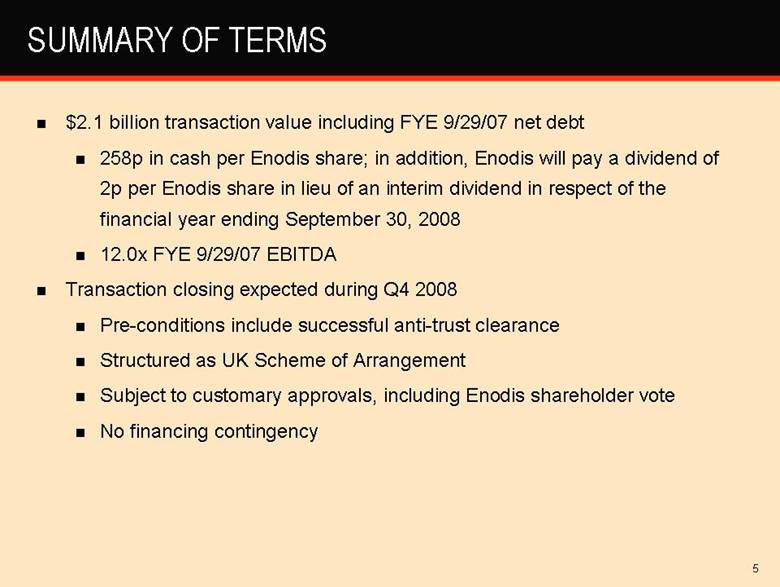

| 5 SUMMARY OF TERMS $2.1 billion transaction value including FYE 9/29/07 net debt 258p in cash per Enodis share; in addition, Enodis will pay a dividend of 2p per Enodis share in lieu of an interim dividend in respect of the financial year ending September 30, 2008 12.0x FYE 9/29/07 EBITDA Transaction closing expected during Q4 2008 Pre-conditions include successful anti-trust clearance Structured as UK Scheme of Arrangement Subject to customary approvals, including Enodis shareholder vote No financing contingency |

| 6 FOODSERVICE ACQUISITION PHILOSOPHY • Products/geographies outside our portfolio • Broaden low-cost manufacturing base • Components in adjacent categories to broaden customer relationships • Ability to expand channel to market and service network • International manufacturing and distribution • Speed of integration • Market leadership positions • Strong management teams |

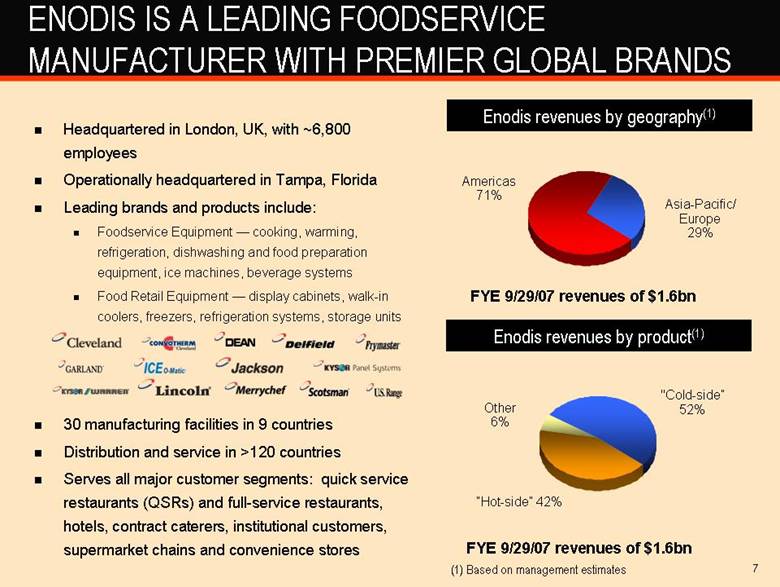

| 7 ENODIS IS A LEADING FOODSERVICE MANUFACTURER WITH PREMIER GLOBAL BRANDS Headquartered in London, UK, with ~6,800 employees Operationally headquartered in Tampa, Florida Leading brands and products include: Foodservice Equipment — cooking, warming, refrigeration, dishwashing and food preparation equipment, ice machines, beverage systems Food Retail Equipment — display cabinets, walk-in coolers, freezers, refrigeration systems, storage units 30 manufacturing facilities in 9 countries Distribution and service in >120 countries Serves all major customer segments: quick service restaurants (QSRs) and full-service restaurants, hotels, contract caterers, institutional customers, supermarket chains and convenience stores Asia-Pacific/Europe 29% “Hot-side” 42% Americas 71% “Cold-side” 52% Other 6% Enodis revenues by geography(1) Enodis revenues by product(1) FYE 9/29/07 revenues of $1.6bn FYE 9/29/07 revenues of $1.6bn (1) Based on management estimates |

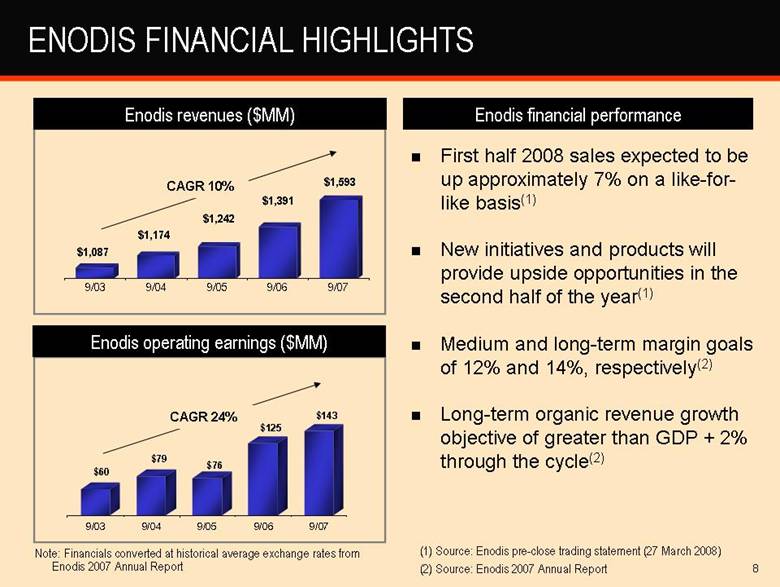

| 8 ENODIS FINANCIAL HIGHLIGHTS Enodis financial performance First half 2008 sales expected to be up approximately 7% on a like-for-like basis(1) New initiatives and products will provide upside opportunities in the second half of the year(1) Medium and long-term margin goals of 12% and 14%, respectively(2) Long-term organic revenue growth objective of greater than GDP + 2% through the cycle(2) Note: Financials converted at historical average exchange rates from Enodis 2007 Annual Report (1) Source: Enodis pre-close trading statement (27 March 2008) (2) Source: Enodis 2007 Annual Report CAGR 10% Enodis revenues ($MM) $1,087 $1,174 $1,242 $1,391 $1,593 9/03 9/04 9/05 9/06 9/07 $60 $79 $76 $125 $143 9/03 9/04 9/05 9/06 9/07 CAGR 24% Enodis operating earnings ($MM) |

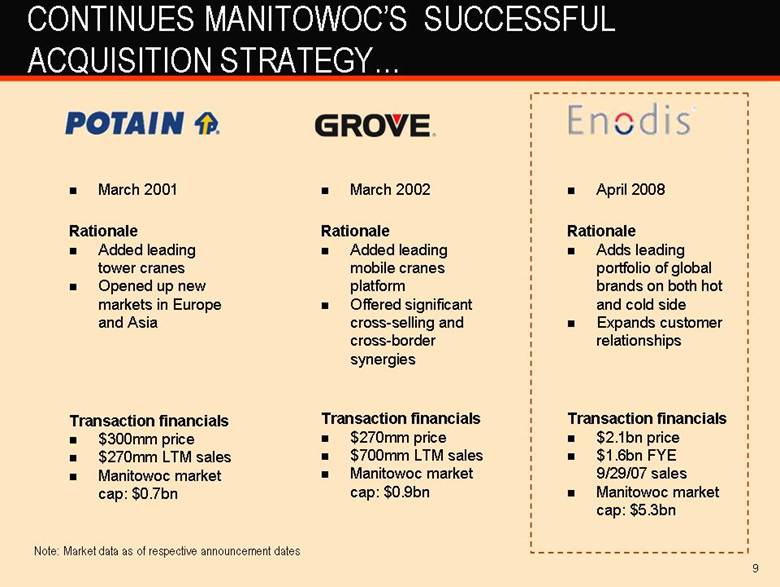

| 9 CONTINUES MANITOWOC’S SUCCESSFUL ACQUISITION STRATEGY... March 2001 Rationale Added leading tower cranes Opened up new markets in Europe and Asia Transaction financials $300mm price $270mm LTM sales Manitowoc market cap: $0.7bn March 2002 Rationale Added leading mobile cranes platform Offered significant cross-selling and cross-border synergies Transaction financials $270mm price $700mm LTM sales Manitowoc market cap: $0.9bn April 2008 Rationale Adds leading portfolio of global brands on both hot and cold side Expands customer relationships Transaction financials $2.1bn price $1.6bn FYE 9/29/07 sales Manitowoc market cap: $5.3bn Note: Market data as of respective announcement dates |

| 10 ...WHICH CAN BE REPLICATED IN FOODSERVICE Broadest product line in industry Global manufacturing to meet local needs Platform for technology and innovation Robust R&D/new product pipeline Best-in-class operator training Industry’s best aftermarket support End user financing options |

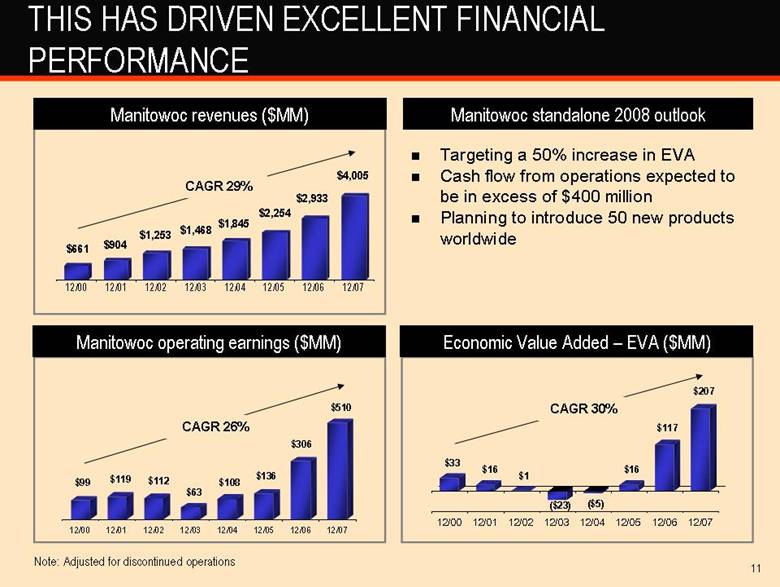

| 11 THIS HAS DRIVEN EXCELLENT FINANCIAL PERFORMANCE $99 $119 $112 $63 $108 $136 $306 $510 12/00 12/01 12/02 12/03 12/04 12/05 12/06 12/07 CAGR 29% CAGR 26% Manitowoc revenues ($MM) Manitowoc standalone 2008 outlook Manitowoc operating earnings ($MM) Targeting a 50% increase in EVA Cash flow from operations expected to be in excess of $400 million Planning to introduce 50 new products worldwide $33 $16 $1 ($23) ($5) $16 $117 $207 12/00 12/01 12/02 12/03 12/04 12/05 12/06 12/07 CAGR 30% Economic Value Added – EVA ($MM) $661 $904 $1,253 $1,468 $1,845 $2,254 $2,933 $4,005 12/00 12/01 12/02 12/03 12/04 12/05 12/06 12/07 Note: Adjusted for discontinued operations |

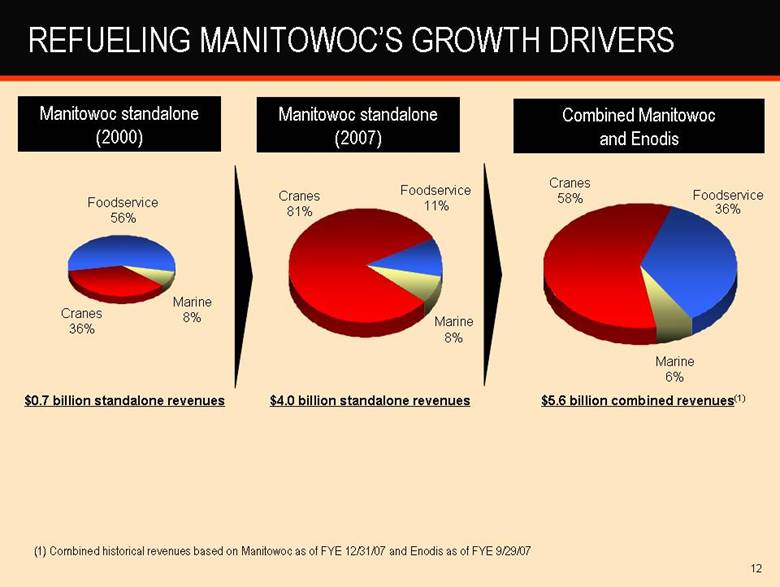

| 12 REFUELING MANITOWOC’S GROWTH DRIVERS Marine 6% Cranes 58% Foodservice 11% Marine 8% Cranes 81% Combined Manitowoc and Enodis Manitowoc standalone (2007) $5.6 billion combined revenues(1) $4.0 billion standalone revenues Foodservice 36% Manitowoc standalone (2000) Cranes 36% $0.7 billion standalone revenues Foodservice 56% Marine 8% (1) Combined historical revenues based on Manitowoc as of FYE 12/31/07 and Enodis as of FYE 9/29/07 |

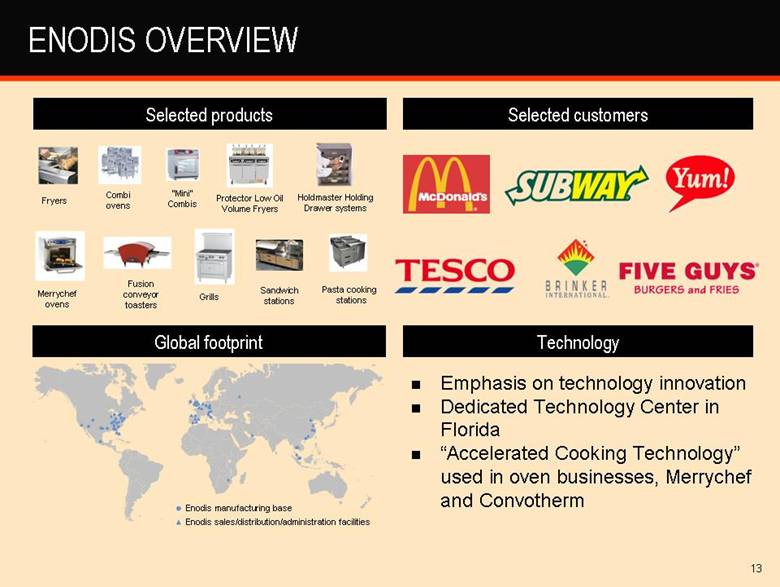

| 13 ENODIS OVERVIEW Selected products Selected customers Global footprint Technology Combi ovens Fryers “Mini” Combis Protector Low Oil Volume Fryers Holdmaster Holding Drawer systems Pasta cooking stations Sandwich stations Fusion conveyor toasters Merrychef ovens Emphasis on technology innovation Dedicated Technology Center in Florida “Accelerated Cooking Technology” used in oven businesses, Merrychef and Convotherm Grills Enodis manufacturing base Enodis sales/distribution/administration facilities |

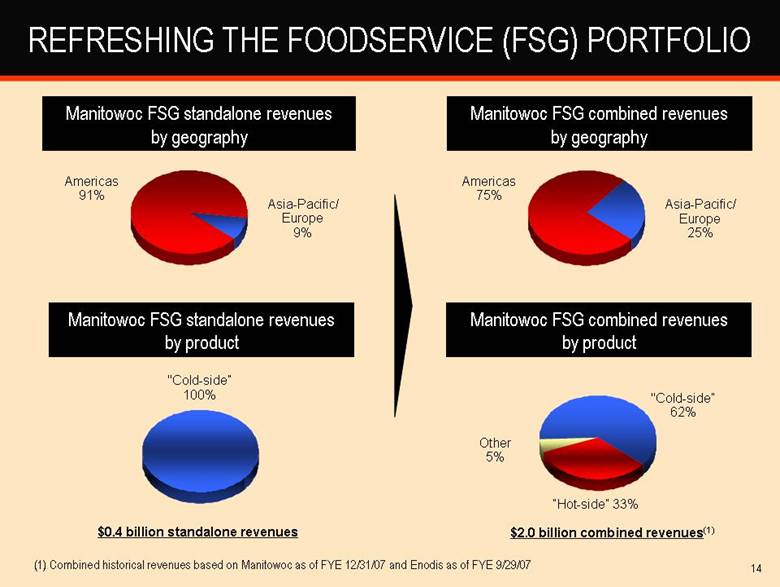

| 14 REFRESHING THE FOODSERVICE (FSG) PORTFOLIO $2.0 billion combined revenues(1) $0.4 billion standalone revenues Asia-Pacific/Europe 25% “Hot-side” 33% Americas 75% “Cold-side” 62% Other 5% Manitowoc FSG combined revenues by geography Manitowoc FSG combined revenues by product Asia-Pacific/Europe 9% Americas 91% “Cold-side” 100% Manitowoc FSG standalone revenues by geography Manitowoc FSG standalone revenues by product (1) Combined historical revenues based on Manitowoc as of FYE 12/31/07 and Enodis as of FYE 9/29/07 |

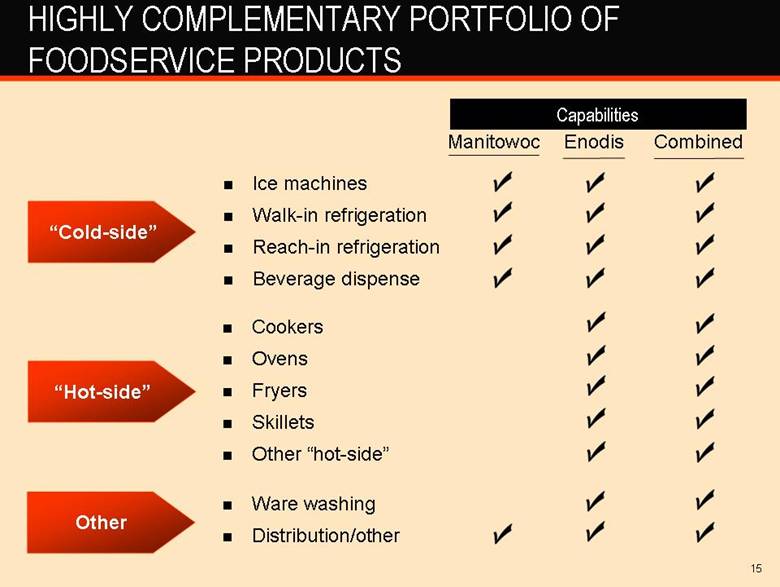

| 15 HIGHLY COMPLEMENTARY PORTFOLIO OF FOODSERVICE PRODUCTS Capabilities “Cold-side” “Hot-side” Other Manitowoc Enodis Combined lce machines Walk-in refrigeration Reach-in refrigeration Beverage dispense Cookers Ovens Fryers Skillets Other “hot-side” Ware washing Distribution/other |

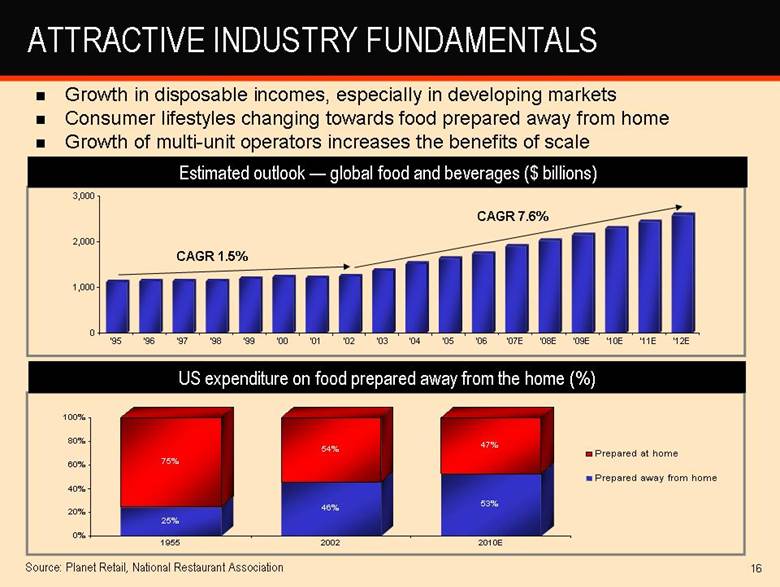

| 16 25% 75% 46% 54% 53% 47% 0% 20% 40% 60% 80% 100% 1955 2002 2010E Prepared at home Prepared away from home CAGR 7.6% 0 1,000 2,000 3,000 '95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07E '08E '09E '10E '11E '12E ATTRACTIVE INDUSTRY FUNDAMENTALS Estimated outlook — global food and beverages ($ billions) Growth in disposable incomes, especially in developing markets Consumer lifestyles changing towards food prepared away from home Growth of multi-unit operators increases the benefits of scale Source: Planet Retail, National Restaurant Association CAGR 1.5% US expenditure on food prepared away from the home (%) |

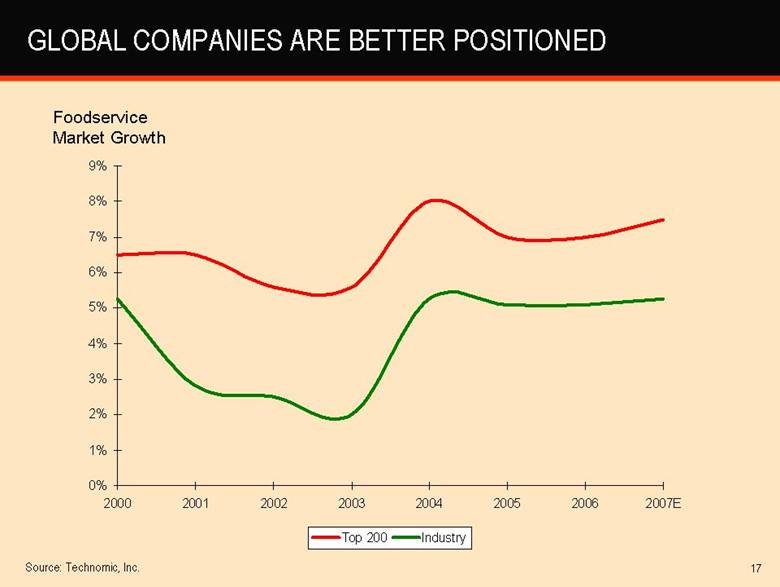

| 17 GLOBAL COMPANIES ARE BETTER POSITIONED 0% 1% 2% 3% 4% 5% 6% 7% 8% 9% 2000 2001 2002 2003 2004 2005 2006 2007E Top 200 Industry Foodservice Market Growth Source: Technomic, Inc. |

| 18 FULL PORTFOLIO BRINGS GREATER OPPORTUNITES New locations drive hot and cold equipment sales Key driver for cold side is replacements/renovation Key driver for hot side is menu change Large opportunity to partner with global accounts Access to hot side provides a better platform to leverage technology, use “voice of the customer” |

| 19 SIGNIFICANT SYNERGIES EXPECTED Run rate synergies of >$60 million expected in 2010 Approximately 50% expected to be realized in 2009 (note closing not expected until Q4 2008) Estimated $33 million of initial costs to achieve synergies Cost savings Consolidation of duplicated infrastructure Rationalization of administrative functions Transfer of best practices (e.g., lean manufacturing) Economies of scale in procurement Elimination of public company expenses Revenue synergies Cross-selling opportunities with complementary products Source Manitowoc components for Enodis walk-in refrigeration systems |

| 20 CONSERVATIVE FINANCING STRATEGY Unconditionally-committed financing Expect to retain existing credit ratings Rapid deleveraging ability Will consider potential longer-term financing subject to market conditions |

| 21 SUMMARY Balances Manitowoc’s business portfolio and establishes the company as a leader in foodservice equipment $2.1 billion transaction value including FYE 9/29/07 net debt 12.0x FYE 9/29/07 EBITDA $60+ million synergies expected Expected to be accretive to EPS in 2009 and EVA positive in 2011(1) Consistent with Manitowoc’s strategic imperatives: Profitable growth Innovation Customer focus Excellence in operations People and organizational development Aftermarket services Value creation (1) Note: Before purchase accounting for the transaction. This statement is not a profit forecast and should not be interpreted to mean that future earnings per share will necessarily be greater than those for the relevant preceding financial period. |

| 22 QUESTIONS |