QuickLinks -- Click here to rapidly navigate through this document

Contents

| 2 | | Letter to Shareholders |

| 6 | | Our Consumer Business at a Glance |

| 8 | | Our Industrial Business at a Glance |

| 10 | | Introducing Zatarain's |

| 12 | | Improving Efficiency, Increased Effectiveness |

| 14 | | McCormick Worldwide |

| 15 | | Community Service |

| 16 | | Board of Directors, Corporate Officers and Operating Executives |

| 18 | | Management's Discussion and Analysis |

| 33 | | Report of Management, Report of Independent Auditors |

| 34 | | Financial Statements and Notes |

| 52 | | Historical Financial Summary |

| 53 | | Investor Information |

Company Description

McCormick is a global leader in the manufacture, marketing and distribution of spices, herbs, seasonings and other flavors to the entire food industry. Customers range from retail outlets and food service providers to food processing businesses. Founded in1889 and built on a culture of Multiple Management, McCormick has approximately 8,000 employees.

| |  |

| This year's annual report carries the scent of cinnamon bun. McCormick is in the business of flavor, creating flavors for foods you enjoy at every eating occasion. It might be baked goods, condiments, cookies, ice cream, beverages, snacks, fast-food meals, restaurant entrees or tasty, convenient meals made at home. McCormick brings great flavor to you every day. | |  |

Financial Highlights

for the year ended November 30 (millions except per share data)

| | 2003

| | 2002

| | % change

| |

|---|

| Net sales | | $ | 2,269.6 | | $ | 2,044.9 | | 11.0 | % |

| Gross profit | | | 898.6 | | | 799.5 | | 12.4 | % |

| | Gross profit margin | | | 39.6 | % | | 39.1 | % | | |

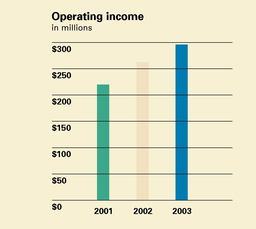

| Operating income | | | 295.5 | | | 262.4 | | 12.6 | % |

| | Operating income margin | | | 13.0 | % | | 12.8 | % | | |

| Net income from continuing operations | | | 199.2 | | | 173.8 | | 14.6 | % |

| | Percent to sales | | | 8.8 | % | | 8.5 | % | | |

| Earnings per share from continuing operations—diluted | | | 1.40 | | | 1.22 | | 14.8 | % |

| Average shares outstanding—diluted | | | 142.6 | | | 142.3 | | .2 | % |

| Dividends paid | | $ | 64.1 | | $ | 58.6 | | 9.4 | % |

| Dividends paid per share | | | .46 | | | .42 | | 9.5 | % |

| Capital expenditures, net of proceeds from sale of fixed assets | | | 81.7 | | | 93.9 | | -13.0 | % |

| Debt-to-total-capital | | | 43.8 | % | | 49.0 | % | 43.8 | % |

| Closing stock price | | $ | 28.69 | | $ | 23.79 | | 20.6 | % |

Our Mission

The primary mission of McCormick & Company is to profitably expand its worldwide leadership position in flavoring food and beverages.

Letter to Shareholders

Fellow shareholders,

McCormick had a remarkable year in 2003. We posted another year of record financial results and honed our portfolio of businesses. The Company was added to the S&P 500 Stock Index in March. Toward the end of the year, we announced key changes to our Board of Directors and top leadership team. And in 2003, our shareholders were rewarded with two dividend increases and excellent share price appreciation.

Record 2003 financial results

At the beginning of the year, with confidence in our business and ability to perform, we set several financial goals for 2003.

We exceeded our 3-7% sales growth goal, with an increase of 11% in 2003. This growth was achieved through the acquisitions of Zatarain's and Uniqsauces, favorable foreign currency, higher volumes from improved marketing, new distribution and robust new product launches.

Our 2003 target was to increase earnings per share 9-11%. With sales growth, higher operating income and other income, we achieved an increase of 15%.

Robert J. Lawless, Chairman, President & CEO

2

The consumer business turned in an excellent performance in 2003, with sales growth of 17%, including 6% related to acquisitions. We increased our promotion and advertising spending 16%, and still increased operating income 18%. Sales for the industrial business rose 5% in total, including 3% related to acquisitions. Strong sales to restaurants were more than offset by lower sales to food processors. Operating income was affected by the more modest sales increase as well as the higher cost of vanilla beans.

Other income of $13 million was reported in 2003. This included $5 million of interest income related to a purchase price refund for the acquisition of Ducros, and a one-time gain of $5 million related to the sale of an interest in non-strategic royalty agreements. Income from unconsolidated operations declined in 2003 due to the impact of higher raw material costs, increased competitive activity and unfavorable foreign currency on the Company's joint venture in Mexico.

A year of strategic growth

We accomplished a number of strategic actions in 2003.

- •

- Completed two key acquisitions. A key driver for growth is acquisitions that expand our flavor offerings as well as our geographic reach. Zatarain's adds the leading U.S. brand of authentic New Orleans-style food to our portfolio. Uniqsauces expands our condiment flavors and packaging formats in both the consumer and industrial segments in the European market. Together, these businesses add more than 6% to sales on an annual basis.

- •

- Sold non-core businesses. In last year's letter to shareholders, we reported "sales weakness in our packaging business and difficulties in our U.K. brokerage operation." After careful review in 2002, these businesses were identified as non-core and in 2003 were successfully divested.

- •

- Negotiated a $50 million purchase price reduction. McCormick received this payment as settlement of a lengthy negotiation related to our 2000 acquisition of Ducros.

- •

- Increased investment in sales growth. We increased spending 16% for promotion and advertising, and 6% for research and development. These investments helped drive an11% increase in sales in 2003 and funded a lineup of exciting new products for introduction in 2004. Today, more sophisticated, value-added products comprise nearly 70% of sales.

- •

- Expanded distribution. We penetrated the dollar store channel in the U.S. with both McCormick brand and private label products. We added distribution in new grocery chains in the U.S., Italy, Austria and Switzerland, and gained additional placement of our products in stores in France and China.

- •

- Achieved record margins. Employees throughout McCormick are implementing supply chain initiatives, streamlining work processes and focusing on the next stage of system implementation for our Beyond 2000 (B2K) program, which introduces significant technology and process improvements. We are improving margins and laying the foundation for future gains.

Together, these actions have positioned us for strategic growth. Today, more than ever, we are focused on flavor—making food taste great. Among our competitors, we have the broadest array of flavors, adding satisfying tastes to all types of food and beverages. Our brands are sold to consumers in nearly 100 countries around the world, and we supply numerous multi-national food processors and the largest restaurant chains in the world. Each day you are likely to experience the taste of McCormick, whether you cook at home, eat out or grab a snack.

3

The journey ahead

Our strategy is simple: improve margins, invest in the business and increase sales and profits. This is the key to our success and will continue to be our strategy going forward.

Margin improvement is our fuel for growth. Gross profit margin reached 39.6% in 2003, an increase of nearly 10 percentage points since 1998. We are well positioned for the next phase of margin improvement with supply chain teams, new system capabilities, improved processes, a more effective organization and strong leadership. It is with confidence that we project a significant reduction in expenses by 2006. The money we save will be deployed to increase sales, offset cost increases in raw materials, employee benefits or other expenses and drive higher profits.

Our outlook for sales is equally positive. Demand for our products continues to grow because consumers seek flavors that are bold and zesty, kid-friendly and fun, or ethnic and exotic—and McCormick consistently delivers in all these areas. Our reliability in developing and distributing superior flavors stems from our determination to remain a leader in the market. We are committed to developing talent. We have the ability to quickly change direction in response to evolving market conditions. We are proactive in meeting consumer demands. Our "take charge" attitude extends from the funding of acquisitions to the launch of effective promotional programs. And this is true globally, across the board. These strong capabilities support our goal of increasing sales 3-7% annually. Category growth, expanded distribution, new product introductions and acquisitions will all contribute to this growth.

Our business is not immune from the challenges of the marketplace, fluctuations in raw material prices, or benefit, energy and other expense increases. This fosters focus and tenacity. We expect continued strong sales and margin increases to generate annual earnings per share growth of 10-12% through 2007.

4

Our Core Values

We believe...

- •

- our people are the most important ingredient of our success.

- •

- our top priority is to continuously add value for our shareholders.

- •

- customers are the reason we exist.

- •

- our business must be conducted honestly and ethically.

- •

- the best way to achieve our goals is through teamwork.

Cash flow from operations, after net capital expenditures and dividends, of $350-$400 million is projected over the next three years. This cash will be used to invest in acquisitions, other business opportunities and share repurchase.

The acquisitions and divestments of 2003 have set us on a strong course; our vision of the journey ahead now has greater clarity. We have demonstrated our ability to execute and have put specific plans in place to maintain our momentum. And this is gaining attention. In March 2003, McCormick was added to the S&P 500 Stock Index, a landmark event for the Company. More importantly, we are proud to report that our shareholders have enjoyed returns exceeding those of most other food stocks.

Making changes while maintaining our values

No company can remain unaffected by significant changes in the marketplace. In our consumer business, customers have consolidated and their supply requirements have tightened. On the industrial side, there has been consolidation among certain competitors. In an environment which fosters stronger and more efficient corporations, it is imperative that we challenge ourselves to stay ahead of the curve, while still maintaining our core values at McCormick. For more than 70 years, we have benefited from our Multiple Management philosophy, which inspires employee participation and recognition. Our core values define who we are. We are committed to a diverse workforce and a spirit of inclusion, which makes it possible for us to work smarter, work better and work together.

For the first time in its history, the Company has a majority of independent directors.

This year, Margaret Preston of Mercantile Safe Deposit and Trust Bank was elected to our Board. In 2003, three extraordinary leaders retired from the Board in anticipation of their retirement from the Company: John Molan, Carroll Nordhoff and Robert Schroeder. We thank them for their significant contributions to this Company.

Senior level management changes were made to maintain the strength of our leadership team. The responsibility for our international consumer business now belongs to Mark Timbie who has been promoted to President—International Consumer Products Group. Alan Wilson was promoted to President—U.S. Consumer Products Division. As part of this organizational change, Iwan Williams was promoted to President—Europe, Middle East and Africa.

Along with these changes, the Board formed a Corporate Governance Committee of independent directors and adopted corporate governance principles.

Together, these initiatives will optimize our effectiveness in the marketplace, enable us to make smart business decisions and help us maintain our core values. Throughout McCormick, we are working as a team to build upon our momentum. I am confident that our people, strategy and enthusiasm will lead to great performance and higher value for our shareholders.

Robert J. Lawless, Chairman, President & CEO

5

Our Consumer BusinessAT A GLANCE

BUSINESS DESCRIPTION

McCormick's consumer business markets spices, herbs, extracts, seasoning blends, sauces, marinades and specialty foods.

Our customers span many retail outlets and include grocery, drug, dollar and mass merchandise stores.

2003 HIGHLIGHTS

- •

- Acquired Zatarain's, extending our range of flavors and adding strong growth opportunities.

- •

- Launched new products in the last 3 years that accounted for 5% of 2003 sales.

- •

- Expanded our channel of distribution for brand and private label products into a dollar store chain, a top-20 U.S. grocery retailer and grocery chains in Europe.

- •

- Consolidated all international consumer businesses under a new position: President—International Consumer Products Group.

- •

- For the first time in France, achieved additional product locations in grocery stores with innovative merchandising. Increased our store presence in China with additional product placements.

- •

- Cut by one-half the number of spice products and packaging formats in Canada to optimize customer profit and make way for new products.

2003 FINANCIAL RESULTS

Net sales rose 17% in 2003. The acquisition of Zatarain's and Uniqsauces accounted for 6% of the growth rate. Effective marketing and successful new products added another 5% of the increase. We also benefited from favorable foreign currency translation in 2003, which contributed 6% of sales growth.

Operating income rose 18% as a result of the sales increase and the initiatives to improve margins. This was despite some raw material cost increases and higher employee benefit costs. As a percent of net sales, operating income reached 19.4%.

2003 NET SALES BY REGION

We are driving growth in our global markets with great new products.

RIGHT:New wet and dry accompaniments capitalize on the rising popularity of salads. We provide the great textures, colors and tastes that, until recently, were only available in restaurants.BELOW:Our sensory and culinary experts develop innovative products that satisfy consumer demand for great taste and ease of preparation.

6

MARKET POSITION

Consumers love great flavor, but demand convenience.

As category leader, McCormick's new products, merchandising, website and other initiatives are designed to meet these needs.

Category growth in 2003 was 3% in the U.S. and even higher in certain international markets.

With both brand and private label products, we continue to gain market share. Today our share exceeds 40% in the U.S. and the U.K., and 50% in France and Canada.

While there are many competitors with a smaller share in our category, we are maintaining and growing our position through effective marketing and superior new products.

STRATEGY AND OUTLOOK

In 2003, investment in promotion and advertising (excluding acquisitions) increased 16%. We plan to increase sales through effective marketing, new products, channel expansion and brand acquisitions.

Interest in flavors—new, bold, exotic—continues to grow. But food preparation must be quick and easy. McCormick is satisfying this appetite for outstanding flavor and simple preparation with leading brands in key markets around the world.

FINANCIAL RESULTS

in millions

| | 2003

| | 2002

|

|---|

| NET SALES | | $ | 1,162.3 | | $ | 993.9 |

| OPERATING INCOME | | $ | 225.7 | | $ | 191.9 |

CONSUMER BRANDS

7

Our Industrial BusinessAT A GLANCE

BUSINESS DESCRIPTION

McCormick's industrial business markets spices, blended seasonings, condiments, coatings and compound flavors to other food processors and to the away-from-home channel both directly and through distributors and warehouse clubs.

The hugely popular family-style restaurants use McCormick's flavor expertise from one end of the menu to the other. From "white table cloth" restaurants to the global quick service chains, you will find the great taste of McCormick.

2003 FINANCIAL RESULTS

Net sales rose 5% in 2003. The acquisition of Uniqsauces contributed 3% of the growth rate and favorable foreign currency translation another 3%. Increased sales to restaurant customers were offset by reduced sales to food processors, due in part to price adjustments for lower cost commodities.

Operating income rose 3% generally in line with the sales increase when sales of the lower margin Uniqsauces business are excluded.

FINANCIAL RESULTS

in millions

| | 2003

| | 2002

|

|---|

| NET SALES | | $ | 1,107.3 | | $ | 1,051.0 |

| OPERATING INCOME | | $ | 110.2 | | $ | 107.3 |

2003 HIGHLIGHTS

- •

- Launched new products in the last 3 years that accounted for 16% of 2003 sales.

- •

- Recognized by customers with award for "best overall flavor company" in a survey conducted byFood Processing magazine. Also received awards from Sysco and Subway.

- •

- Acquired Uniqsauces, extending our range of condiments and packaging formats in Europe.

- •

- Increased share of quick service restaurant business in the U.S. with successful coatings, condiments and seasonings, including new salad dressings.

- •

- Continued to develop our global technical capabilities in 2003.

8

MARKET POSITION

Interest in flavors continues to grow. A report published by The Freedonia Group indicates that demand for flavors and flavor enhancers will grow 4.3% annually through 2006.

While McCormick has many competitors, we offer our customers the broadest range of flavor solutions in the industry. Our multifunctional sales teams work with customers to develop leading products that become marketplace winners.

Spending for product research and development has nearly doubled since 1998. Together, our development, application, culinary and sensory areas enable us to deliver consumer-preferred flavors.

STRATEGY AND OUTLOOK

Our customers are leaders in their industries—whether they are quick service restaurants, multi-national food processors, or major warehouse clubs. We are growing with these customers around the world, providing quality products and excellent service.

We are building our leadership position in flavors. By focusing resources on value-added products, we expect to grow sales and increase margins.

Our business is flavor, and we bring great taste to many of the foods you enjoy from leading food manufacturers. From snacks to soups, from beverages to baked goods, our consumer-preferred flavors can be found in a multitude of products.

INDUSTRIAL PRODUCTS

INGREDIENTS

Spices and herbs

Extracts

Essential oils and oleoresins

Fruit and vegetable powders

Tomato powder

COATING SYSTEMS

Batters

Breaders

Marinades

Glazes

Rubs

SEASONINGS

Seasoning blends

Salty snack seasonings

Side dish seasonings

(rice, pasta, potato)

Sauces and gravies

CONDIMENTS

Sandwich sauces

Ketchup

Mustards

Jams and jellies

Seafood cocktail sauces

Salad dressings

Flavored oils

COMPOUND FLAVORS

Beverage flavors

Dairy flavors

Confectionery flavors

PROCESSED FLAVORS

Meat flavors

Savory flavors

9

Introducing Zatarain's

| | Lawrence Kurzius, President & Chief Executive Officer—Zatarain's, discusses products with Merlin Walker, Pat Autin and Emma Byrd. | |  |

BELOW: Clinton Murphy and Inez Prestenback oversee the rice mix line.

BELOW RIGHT: Mona Rome and Lisa Miller perform quality checks. | |  | | Creative marketing and promotion help drive the growth of a century-old brand. |

| |  |

10

In June, we acquired Zatarain's, the leading New Orleans-style food brand marketed nationally in the United States. Founded in 1889, the same year as McCormick, Zatarain's markets flavored rice and dinner mixes, products to prepare and season seafood and many other items that add flavor to food and capture that unique style of New Orleans cuisine.

Zatarain's is headquartered near New Orleans in Gretna, Louisiana and has approximately 270 employees. While the business has its home in Louisiana and its strongest markets in the southeast U.S., distribution into retail grocery stores across the U.S. has grown in recent years. Though its products are distributed primarily through retail grocery channels, Zatarain's has entered the food service business as well.

The purchase of Zatarain's represents one more step in an important growth strategy that we have focused on in recent years. As with the Ducros acquisition in 2000, we continue to target leading brands of domestic or international products that provide flavor. We look for acquisitions to provide substantial growth and complement our established strategy of leadership in the development and marketing of flavors for food. Zatarain's is a positive step in our journey.

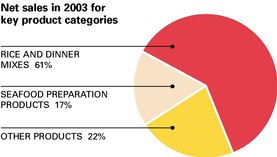

Zatarain's has annual sales of approximately $100 million. It has the number three national brand of rice mixes with a market share greater than 10%. The business achieved 15% annual sales growth from 1998 to 2002.

From a trade and consumer perspective, Zatarain's is a good synergistic fit. It gives us a presence in the convenient dinner mix category and allows us to leverage our distribution capabilities with Zatarain's seasonings, condiments, seafood boils and breadings. Because Zatarain's has such a strong position in New Orleans cuisine, there are a number of options for new products and broader categories. Using McCormick's culinary and sensory capabilities, we will work to capitalize on those possibilities through product innovation.

As part of our acquisition strategy, we seek brands that stand for the same attributes as McCormick—superior flavor and quality. We see Zatarain's as a strong brand with clear positioning and great growth potential. This management team has delivered exceptional growth the past several years. We plan to use our capabilities to accelerate Zatarain's growth in the United States and around the world. We are pleased to welcome Zatarain's, a company with a proud heritage, into the family of McCormick brands.

11

Improving Efficiency, Increased Effectiveness

Fuel for growth

McCormick has increased gross profit margin approximately 10 percentage points since 1998 on a comparable basis, and exceeded 39% in 2003. This margin increase has contributed to record financial results and has been our fuel for growth.

We have used this "fuel" to invest in:

- •

- marketing support for our leading brands around the world,

- •

- product research and development to support an active new products program, and

- •

- acquisitions that have extended our business into new categories and regions.

Improving efficiency

Efforts to improve efficiency throughout McCormick are driving margins and will lead to improved working capital:

- •

- streamlining actions such as facility consolidation, the rationalization of under-performing products and reduction in packaging formats, and

- •

- supply chain initiatives to achieve efficiencies across the whole spectrum—from the procurement of raw materials to processing customer payments.

As we implement our Beyond 2000 (B2K) program, improved knowledge and better tools will enable us to reach the next level of savings. B2K is a global initiative that is significantly improving our business processes through state-of-the-art technology. B2K will be implemented throughout the U.S. by mid-2004 and internationally by early 2006.

Increased effectiveness

Employees throughout McCormick are increasing their effectiveness and achieving measurable results.

Some are working on supply chain teams to optimize areas such as transportation. Others are sharing best practices as members of new work teams such as Financial Shared Services. As this program is implemented, employees are using new B2K technology to better serve our customers.

While changes of this magnitude are a challenge, employees throughout the world have a positive outlook. They are excited about the opportunity to learn new skills, forge new relationships and increase their effectiveness.

Outlook for improved margin

As we look ahead, our focus will extend from higher gross profit margin to improvements in operating profit margin achieved by capturing efficiencies in our operating expenses. Operating profit margin will also be positively affected by our development of more value-added products and our acquisition activity.

With the completion of our B2K implementation, we will achieve a higher level of efficiency. With the tools available and the supply chain initiatives and operational improvements underway, we expect to reduce costs significantly over the next few years.

By 2006, annual expense reductions are expected to reach $70 million, with $15 million achieved in 2004, another $25 million in 2005 and an additional $30 million in 2006.

The savings from these expense reductions will be invested to increase sales, offset higher costs for raw materials, employee benefits or other expenses, and achieve higher profits.

We are confident of our ability to improve margins and generate "fuel" for growth at McCormick.

12

| | Organizational changes in 2003 included the formation of Financial Shared Services.

SHOWN L TO R:

Kim Knight, Issie Hampton, Diane Grim, Mike Moscato, Laura Blanchard and Linda Huber work together on one of our Financial Shared Services teams. |

| | | |  |

| Our strategy is simple: improve margins, invest in the business and increase sales and profits. This is the key to our success and will continue to be our strategy going forward. | |  | | In October 2003, this facility in Canada was opened as part of a plant consolidation initiative. This was one of several major streamlining actions taken to improve margins. |

| | | Our focus will extend from higher gross profit margin to improvements in operating profit margin. | | |

13

McCormick Worldwide

14

Community Service

We work and reside in hundreds of communities around the world, and we make our presence felt. From the earliest years of our Company, employees have been active participants in their communities.Their efforts mirror the Company's long-standing commitment to be a benevolent and involved member in communities where we have facilities. The Company has a formalized program of charitable giving that grants funds to worthwhile causes. Civic, health, welfare, education and art projects receive the greatest attention. A primary focus of our community efforts is to help the disadvantaged through programs like Habitat-for-Humanity. The Company also is a strong supporter of numerous food banks through funding, food donations and employee volunteerism. Individual or small groups of employees around the world work to make life better for families and neighbors in need.

Through formal Company programs and countless employee volunteer hours, McCormick improves the quality of life in our communities. This coming year we will inaugurate the McCormick community Service Award. Several employees from throughout McCormick will be recognized for their community service, and grants will be made in their names to the organizations for which they volunteer. Our commitment to community enrichment starts at the highest levels of management and extends throughout the entire employee population around the world. We call it the "Power of People."

15

| |

Edward Dunn

Barry Beracha

Michael Fitzpatrick

Karen Weatherholtz |

Francis Contino

Robert Lawless

Margaret Preston

| |  |

| |

James Brady

William Stevens

Freeman Hrabowski

Robert Davey |

16

Board of Directors

Barry H. Beracha—61

Executive Vice President

Sara Lee Corporation (retired),

Chief Executive Officer

Sara Lee Bakery Group (retired)

food, household and body care products and apparel

Director since 2000*

James T. Brady—63

Managing Director, Mid-Atlantic

Ballantrae International, Ltd.

Ijamsville, Maryland

International management consultants

Director since 1998†

Francis A. Contino—58

Executive Vice President,

Chief Financial Officer & Supply Chain

McCormick & Company, Inc.

Director since 1998

Robert G. Davey—54

President—Global Industrial Group

McCormick & Company, Inc.

Director since 1994

Edward S. Dunn, Jr.—60

President, Dunn Consulting

Williamsburg, VA

Business consulting services

Director since 1998*

J. Michael Fitzpatrick—57

President & Chief Operating Officer

Rohm and Haas Company

Philadelphia, Pennsylvania

Paint & coatings, electronics, household

products, personal care and salt

Director since 2001*‡

Freeman A. Hrabowski, III—53

President, University of Maryland

Baltimore County

Baltimore, Maryland

Director since 1997‡

Robert J. Lawless—57

Chairman of the Board, President & Chief Executive Officer

McCormick & Company, Inc.

Director since 1994

Margaret M.V. Preston—46

Executive Vice President

Mercantile Safe Deposit & Trust Company

Baltimore, Maryland

Director since 2003†

William E. Stevens—61

Chairman, BBI Group

St Louis, Missouri

Mergers & Acquisitions

Director since 1988†

Karen D. Weatherholtz—53

Senior Vice President—Human Relations

McCormick & Company, Inc.

Director since 1992

- †

- Audit Committee member

- *

- Compensation Committee member

- ‡

- Corporate Governance Committee

Corporate Officers

Robert J. Lawless

Chairman of the Board, President & Chief Executive Officer

Allen M. Barrett, Jr.

Vice President—Corporate Communications

Paul C. Beard

Vice President—Finance & Treasurer

Francis A. Contino

Executive Vice President, Chief Financial Officer & Supply Chain

Robert G. Davey

President—Global Industrial Group

Stephen J. Donohue

Vice President—Strategic Sourcing

Dr. Hamed Faridi

Vice President—Research & Development

H. Grey Goode, Jr.

Vice President—Tax

Kenneth A. Kelly, Jr.

Vice President & Controller

Roger T. Lawrence

Vice President—Quality Assurance

Sharon H. Mirabelle

Vice President—Shared Services

Michael J. Navarre

Vice President—Operations

Robert W. Skelton

Senior Vice President, General Counsel & Secretary

Karen D. Weatherholtz

Senior Vice President—Human Relations

Jeryl Wolfe

Vice President—Global Business Solutions & Chief Information Officer

Joyce L. Brooks

Assistant Treasurer—Financial Services

W. Geoffrey Carpenter

Associate General Counsel & Assistant Secretary

Robert P. Conrad

Assistant Treasurer

Operating Executives

Arduino A. Bianchi

President & Managing Director—McCormick De Centro America, S.A. de C.V.

Randy L. Carper

Vice President & General Manager—Frito Worldwide Division

Tapan Chakrabarty

Vice President & Managing Director—Industrial-Asia Pacific

Robert G. Davey

President—Global Industrial Group

Keith E. Gibbons

President & Chief Financial Officer—La Cie McCormick Canada

Lazaro Gonzalez

President and Managing Director—McCormick Pesa, S.A. de C.V.

Randal M. Hoff

Vice President & General Manager—McCormick Flavor Division

Gavin Jacobs

Managing Director—McCormick South Africa Proprietary Limited

Lawrence E. Kurzius

President & Chief Executive Officer—Zatarain's

Charles T. Langmead

Vice President & General Manager—Food Service & Global Restaurant Divisions

Timothy J. Large

Managing Director—McCormick Foods Australia Pty. Ltd.

John G. McCormick

Vice President—Latin American Consumer Businesses

James M. Morrisroe

Vice President Flavour Group—Europe

Victor K. Sy

Vice President & Managing Director—Consumer—McCormick Far East

Mark T. Timbie

President—International Consumer Products Group

Iwan Williams

President—Europe, Middle East & Africa

Alan D.Wilson

President—U.S. Consumer Products Division

17

Management's Discussion and Analysis

Business Overview

McCormick & Co. is a global leader in the manufacture, marketing and distribution of spices, herbs, seasonings and flavors to the entire food industry. The Company's major sales, distribution and production facilities are located in North America and Europe and its products reach nearly 100 countries around the world. Additional facilities are based in Latin America, Australia, China, Singapore and South Africa. Approximately 38% of sales and 48% of total assets are outside the U.S. Accordingly, the Company has exposure to fluctuations in foreign currency exchange rates. These fluctuations impact the translation of sales, earnings, assets and liabilities from the local functional currency to the U.S. dollar. Operating units outside the U.S. that purchase raw materials such as spices and herbs in U.S. dollars are also impacted by fluctuations in foreign currency exchange rates.

The Company operates in two segments, consumer and industrial, which serve distinct customer bases. Customers for the consumer segment span a variety of retail outlets and include grocery, drug, dollar and mass merchandise stores. These customers are serviced either through direct shipments or through the food wholesale channel. Recently, consolidations in these industries have created larger customers, some of which are highly leveraged. Customers for the industrial segment include food processors and the restaurant industry, supplied both directly and through distributors and warehouse clubs. The consumer segment accounts for slightly more than half the sales of the Company and the Industrial segment slightly less than half. In line with the industry, the consumer segment has a higher overall profit margin than the industrial segment.

Products for the consumer segment include spices, herbs, extracts, seasoning blends, sauces, marinades and specialty food products. In 2003, 66% of net sales were in the Americas, 29% in Europe and 5% in the Asia/Pacific region. In its primary markets, the Company supplies both branded and private label products and has a leading share that is more than twice the size of the next largest competitor. The Company's strategy is to drive consumer segment growth through effective marketing, new products that meet consumer demand for convenience and great taste, channel expansion and brand acquisition.

Products for the industrial segment include spices, blended seasonings, condiments, coatings and compound flavors. In 2003, 74% of net sales were in the Americas, 18% in Europe and 8% in the Asia/Pacific region.

The Company has many competitors who also supply products to food processors, as well as restaurants, food service distributors and warehouse clubs. Among its competitors, McCormick has the broadest range of flavor solutions and has many key customers who are leaders in their respective industries. The Company will drive growth by building upon its customer relationships as it introduces higher-margin, value-added new products through the use of technology, and by pursuing strategic acquisitions.

The Company purchases a significant amount of raw materials from areas throughout the world. The most significant raw materials are vanilla, cheese, pepper, packaging supplies, garlic and onion. Some of these are subject to price volatility caused by weather and other unpredictable factors. The Company responds to this volatility in a number of ways including periodic raw material purchases, purchases of raw material for future delivery and customer price adjustments.

Between its consumer and industrial segments, the Company has the customer base and product development skills to provide flavor for all types of eating occasions, whether it is cooking at home, dining out, purchasing a quick service meal or enjoying a snack.

From its businesses, the Company generates a significant amount of cash that is used to support its operations and to fund shareholder dividends, acquisitions, capital expenditures and share repurchases.

2003 Highlights

Significant accomplishments and events in 2003:

- •

- The Company acquired Zatarain's, the leading U.S. brand of authentic New Orleans-style food. The Company also acquired Uniqsauces, expanding its condiment flavors and packaging formats in both the consumer and industrial businesses in the European market. Together these businesses on an annualized basis would have added more than 6% to 2003 sales.

- •

- Following a review in 2002, the packaging business and the U.K. brokerage operation were determined to be non-core to the Company. In 2003, the Company completed the divestiture of these businesses.

- •

- Payment of $50.0 million was received as settlement of a purchase price adjustment related to the acquisition of Ducros in 2000. An additional $5.4 million was received as interest on the purchase price adjustment.

- •

- The consumer segment achieved strong sales growth from new distribution gains, new product activity and effective marketing. New distribution gains

18

During the third quarter of 2003, the Company sold its packaging business and U.K. brokerage business. As a result, current and prior period sales and related expenses for these discontinued operations have been reclassified and reported as "Income from discontinued operations." Earnings per share for 2003 were $1.48, which included $1.40 from continuing operations, $.03 from discontinued operations, a $.06 gain on the sale of the discontinued operations and a $.01 charge from the cumulative effect of an accounting change. This charge was recorded in the fourth quarter and related to a change in accounting for the entity that holds the lease on a distribution center used by the Company.

For fiscal year 2003, McCormick reported sales from continuing operations of $2.3 billion, an increase of 11.0% above 2002. This exceeded the Company's objective of 3-7% annual sales growth.

The Company increased net income from continuing operations by 14.6% and diluted earnings per share from continuing operations by 14.8% for the fiscal year. This increase also exceeded the Company's objective to increase earnings per share 10-12% annually through 2007. In addition to the sales growth achieved in 2003, gross profit margin increased to 39.6% from 39.1% in 2002. In total, diluted earnings per share from continuing operations increased $0.18, comprised of $0.12 from higher sales and operating margin, $0.04 from acquisitions and $0.06 from other income, offset by a $0.04 decline in income from unconsolidated operations. The $0.06 increase in other income resulted principally from interest income on the purchase price adjustment from the acquisition of Ducros and a gain on the sale of an interest in non-strategic royalty agreements.

For the year ended November 30, 2003, the net cash provided by continuing operating activities was $195.4 million as compared to $205.3 million for 2002. For fiscal year 2003, cash from operations after net capital expenditures (capital expenditures less proceeds from the sale of fixed assets) and dividends paid was $49.6 million, which was below the Company's objective to exceed $100 million annually. The shortfall is primarily due to a strategic purchase of vanilla beans made during 2003 in response to a short supply for this raw material, and the timing of liability payments. At year-end, an incremental $40 million of the vanilla bean strategic purchase remained in inventory when compared to 2002.

Acquisitions

On June 4, 2003, the Company purchased Zatarain's, the leading New Orleans-style food brand in the United States, for $180.0 million in cash initially funded with commercial paper borrowings. Zatarain's manufactures and markets flavored rice and dinner mixes, seafood seasonings and many other products that add flavor to food. The acquisition of Zatarain's is consistent with the Company's strategy to acquire established brands to complement the Company's leadership in the development and marketing of flavors for food. The Company expects to utilize its expertise to further develop Zatarain's branded products and leverage existing consumer distribution channels to reach new customers. Zatarain's results of operations have been included in the Company's consolidated results from the date of acquisition. The excess of the purchase price over the estimated fair value of the net assets purchased was $172.9 million. The allocation of the purchase price is based on preliminary estimates, subject to revision, after asset values have been finalized. Revisions to the allocation, which may be significant, will be reported as changes to various assets and liabilities, including goodwill and other intangible assets. As of November 30, 2003, the goodwill balance included the entire excess purchase price of the Zatarain's acquisition, as the valuation of specific intangible assets has not yet been completed. The Company expects the final allocation of purchase price to result in a significant value for non-amortizable brands which is consistent with the basis for the acquisition. The Company does not anticipate significant amounts to be allocated to amortizable intangible assets and, therefore, the amount

19

of intangibles amortization is not expected to be material to the results of operations in future periods. On a full year basis, Zatarain's adds approximately $100 million in sales and a profit margin that is at the upper end of the Company's consumer segment.

On January 9, 2003, the Company acquired the Uniqsauces business, a condiment business based in Europe, for $19.5 million in cash. Uniqsauces manufactures and markets condiments to retail grocery and food service customers, including quick service restaurants. Uniqsauces' results of operations have been included in the Company's consolidated results from the date of acquisition. The purchase price of this acquisition was allocated to fixed assets and working capital. No goodwill was recorded as a result of this acquisition.

On April 29, 2003, the Company settled the purchase price adjustment from the acquisition of Ducros. The Company received payment of 49.6 million euros (equivalent to $55.4 million). Of the $55.4 million received, $5.4 million represents interest earned on the adjustment amount from the date of acquisition in accordance with the terms of the original purchase agreement. The interest income is included in "Other income, net" in the consolidated statement of income for the year ended November 30, 2003. The remaining $50.0 million was recorded as a reduction to goodwill related to the acquisition.

Discontinued Operations

Following a review in 2002, the packaging business and the U.K. brokerage operation were determined to be non-core to the Company. On August 12, 2003, the Company completed the sale of substantially all the operating assets of its packaging segment (Packaging) to the Kerr Group, Inc. Packaging manufactured certain products used for packaging the Company's spices and seasonings as well as packaging products used by manufacturers in the vitamin, drug and personal care industries. Under the terms of the sale agreement, Packaging was sold for $142.5 million and included the assumption of all normal trade liabilities. Of the $142.5 million, $132.5 million was received in cash and the remaining $10.0 million is estimated to be received over five years contingent on Packaging meeting certain performance objectives. The proceeds were used to pay off a substantial portion of the commercial paper borrowing related to the Zatarain's acquisition.The final purchase price is also subject to other contingencies related to the performance of certain customer contracts which could result in a decrease in the sale price. The Company recorded a net gain on the sale of Packaging of $11.6 million (net of income taxes of $7.9 million) in the third quarter of 2003. Included in this gain is a net pension and postretirement curtailment gain of $3.3 million and the write-off of goodwill of $0.7 million. The contingent consideration associated with the sale of Packaging will be recognized in the future as an adjustment to the gain based on the performance criteria established. The Company also entered into a multi-year, market priced agreement with the acquirer to purchase certain packaging products.

On July 1, 2003 the Company sold the assets of Jenks Sales Brokers (Jenks), a division of the Company's wholly-owned U.K. subsidiary, to Jenks' senior management for $5.8 million in cash. Jenks provides sales and distribution services for other consumer product companies and was previously reported as a part of the Company's consumer segment. The Company recorded a net loss on the sale of Jenks of $2.6 million (net of an income tax benefit of $0.6 million) in the third quarter of 2003. Included in this loss is a write-off of goodwill of $0.4 million.

The operating results of Packaging and Jenks have been reported as "Income from discontinued operations" in the consolidated statement of income. Prior periods have been reclassified, including the reallocation of certain overhead charges to other business segments. Interest expense has been allocated to discontinued operations based on the ratio of the net assets of the discontinued operations to the total net assets of the Company. The consolidated balance sheet and consolidated statement of cash flows have also been reclassified to present separately the assets, liabilities and cash flows of the discontinued operations.

Beyond 2000

Late in 1999, the Company initiated the B2K program as a global program of business process improvement. B2K is designed to re-engineer transactional processes, strengthen the product development process, extend collaborative processes with trading partners, optimize the supply chain and generally enhance the Company's capabilities to increase sales and profit. An integral part of B2K is the design and implementation of an enterprise wide state-of-the-art technology and information system platform.

In 2002, the Company implemented the initial phase of its B2K program and began using the new state-of-the-art technology and processes in a significant portion of U.S. operations, including its largest consumer operating unit. The rollout of B2K to the U.S. industrial operations will be completed during 2004. The Company anticipates that the rollout of B2K to its European operations will take place in 2005 with the rollout to its Canadian operations shortly thereafter. The Company will continue to integrate and optimize all of its businesses through broader

20

access to information and increased collaboration with its trading partners. Through B2K, employee time devoted to transaction execution will be reduced and more time will be devoted to the growth and effectiveness of the business.

The overall levels of capital spending and expense have increased from historical levels to support the B2K effort. To date, $101.5 million of costs associated with B2K have been capitalized and $18.1 million has been expensed. Additional capital spending of $28.0 million and an additional expense of $18.0 million is anticipated under this program. Capital costs under the B2K program are for computer hardware, software and software development and are reflected in property, plant and equipment in the consolidated balance sheet. Costs expensed under the B2K program include costs of business re-engineering, data conversion and training and are reflected in both cost of sales and selling, general and administrative expense in the consolidated statement of income.

Results of Operations—2003 compared to 2002

for the year ended November 30 (millions)

| | 2003

| | 2002

| |

|---|

| Net sales | | $ | 2,269.6 | | $ | 2,044.9 | |

| Gross profit | | | 898.6 | | | 799.5 | |

| | Gross profit margin | | | 39.6 | % | | 39.1 | % |

| Selling, general and administrative expense | | | 597.6 | | | 529.6 | |

| | Percentage of sales | | | 26.3 | % | | 25.9 | % |

| Operating income | | | 295.5 | | | 262.4 | |

| | Operating income margin | | | 13.0 | % | | 12.8 | % |

For the year ended November 30, 2003, McCormick reported sales from continuing operations of $2.3 billion, an increase of 11.0% above 2002. Sales benefited from the acquisition of the Zatarain's and Uniqsauces businesses, which accounted for 4.4% of the increase. Favorable foreign exchange rates added another 4.2%, and higher sales, particularly in the U.S. consumer business, contributed an additional 2.4% to sales.

Gross profit margin increased to 39.6% in 2003 from 39.1% in 2002. Gross profit margin was favorably impacted by global procurement efficiencies, cost reduction initiatives and a mix of more consumer sales, which generally have a higher gross profit margin, compared to industrial sales. Increases in commodity costs such as vanilla were offset by price increases, and higher margins from the Zatarain's business were offset by a lower gross profit margin from Uniqsauces.

Selling, general and administrative expenses were higher in 2003 than 2002 on both a dollar basis and as a percentage of net sales. These increases were primarily due to increased distribution expenses, decreased royalty income, increased employee benefit costs and higher advertising and promotional expenses. The increase in distribution expenses was primarily due to the addition of higher distribution costs associated with the Zatarain's business, higher fuel costs and higher costs necessary to service customers during the consolidation of facilities in Canada. The decrease in royalty income is due to lower sales in the McCormick de Mexico joint venture. The increase in employee benefit costs was mainly the result of higher pension costs in 2003 compared to 2002. In the consumer business, advertising and promotional expenses increased in support of the launch of several new products.

Pension expense was $22.1 million, $13.0 million and $9.2 million for the years ended November 30, 2003, 2002 and 2001, respectively. In connection with the valuation performed at the end of 2002, the discount rate was reduced from 7.25% to 7.0%; the expected long-term rate of return on assets was reduced from 10.0% to 9.0%; a more recent mortality table was adopted; and the salary scale was reduced from 4.5% to 4.0%. In connection with the valuation performed at the end of 2003, the discount rate was reduced from 7.0% to 6.0% and the expected long-term rate of return on assets was reduced from 9.0% to 8.5%. These changes are reflective of poor market returns in recent years and a continued low interest rate environment. The changes in assumptions along with investment returns below the assumed rate resulted in the increased pension expense in 2002 and 2003 and will continue to impact expense going forward. Pension expense in 2004 is expected to increase approximately 45%.

Interest expense from continuing operations decreased in 2003 versus 2002 due to favorable interest rates.

Other income increased to $13.1 million in 2003 compared to $0.7 million in 2002. In the second quarter of 2003, the Company received $5.4 million of interest income on the Ducros purchase price refund. Also, in the fourth quarter of 2003, the Company recorded a one-time gain of $5.2 million from the sale of an interest in non-strategic royalty agreements. The Company entered into these agreements in 1995 and since then has benefited modestly from tax credits and royalty income.

The effective tax rate for 2003 was 30.9%, down from 31.0% in 2002. A similar rate is expected in 2004.

Income from unconsolidated operations decreased 26.8% in 2003 when compared to 2002. This decline is mainly attributable to lower income from the McCormick de Mexico joint venture during the first half of 2003 and to a lesser extent, the Signature Brands joint venture in

21

the fourth quarter of 2003. The McCormick de Mexico business, which markets the leading brand of mayonnaise n Mexico, continues to experience profit pressure from aggressive competition, higher raw material costs and a weak peso versus the prior year. The Signature Brands business, a cake decorating business in the U.S., was impacted in part by the timing of customers' purchases of holiday products.

Income from discontinued operations was $4.7 million in 2003 compared to $6.0 million in 2002. Income from discontinued operations for 2003 includes 7 months of the operating results of Jenks and 81/2 months of the operating results of Packaging. Also included in discontinued operations in 2003 was a net gain on the sale of discontinued operations of $9.0 million. This consists of the gain on the sale of Packaging of $11.6 million partially offset by the loss on the sale of Jenks of $2.6 million. All amounts included in discontinued operations are net of income taxes.

In the fourth quarter of 2003, the Company recorded a cumulative effect of an accounting change that reduced net income by $2.1 million, net of tax. This charge was recorded in accordance with the adoption of certain provisions of a new accounting interpretation that required the consolidation of the lessor of a leased distribution center. Previously, this entity was not consolidated and the distribution center was accounted for as an operating lease. Consolidation of this entity increased fixed assets by $11.2 million, long-term debt by $14.0 million and minority interest by $0.5 million. The effect of consolidation of this entity in prior years would have reduced net income in 2002 and 2001 by $0.3 million.

Consumer Business

for the year ended November 30 (millions)

| | 2003

| | 2002

| |

|---|

| Net sales | | $ | 1,162.3 | | $ | 993.9 | |

| Operating income | | | 225.7 | | | 191.9 | |

| | Operating income margin | | | 19.4 | % | | 19.3 | % |

In 2003, sales from continuing operations for the consumer business increased 16.9% as compared to 2002. The acquisitions of Zatarain's and Uniqsauces contributed 6.3% of the sales increase and the impact of foreign exchange added another 5.8%. Sales rose 15.3% in the Americas, with Zatarain's contributing 7.1% of sales increase and foreign exchange contributing 0.9% of increase. The remaining 7.3% of sales increase was due primarily to higher volumes in the U.S. and Canada. In 2003, the Company achieved new distribution in the dollar store channel and with a major grocery retailer in the U.S. Sales in Europe rose 21.7%, with foreign exchange contributing 16.9% of increase, and the remaining increase due to the acquisition of Uniqsauces. Sales in the Asia/Pacific region increased 12.3%, with foreign exchange contributing 11.7% of the increase. Sales in this region were adversely affected by competitive conditions in Australia and an initiative to discontinue certain lower margin products in China.

Operating income from continuing operations for the consumer business reached $225.7 million, an increase of 17.6%. This is in line with the sales increase as the operating income margin (operating income as a percentage of sales) went up slightly from 19.3% in 2002 to 19.4% in 2003. The higher expenses of pension, promotion and advertising, distribution and certain commodities were offset by pricing actions and cost savings on supply chain initiatives. Special charges in the consumer business decreased to $1.8 million in 2003 from $2.7 million in 2002. Special charges in the consumer business for 2003 consisted of additional costs associated with the consolidation of production facilities in Canada and the realignment of consumer sales operations in Australia. Special charges in the consumer business for 2002 primarily consisted of severance, lease exit and relocation costs related to the workforce reduction and realignment of consumer sales operations in the U.S.

As discussed previously, the Company sold its Jenks brokerage business in the U.K. on July 1, 2003 and accordingly, results of this business have been reclassified from the consumer segment to discontinued operations.

Industrial Business

for the year ended November 30 (millions)

| | 2003

| | 2002

| |

|---|

| Net sales | | $ | 1,107.3 | | $ | 1,051.0 | |

| Operating income | | | 110.2 | | | 107.3 | |

| | Operating income margin | | | 10.0 | % | | 10.2 | % |

For the fiscal year 2003, sales from the industrial business rose 5.4% as compared to 2002. The acquisition of Uniqsauces contributed 2.7% of sales increase and foreign exchange added another 2.6%. Sales rose 0.4% in the Americas, with foreign exchange contributing 0.5% of the increase. In the Americas, the restaurant industry was affected by a slowdown in consumer traffic in 2003. While this adversely affected the Company's sales to food service distributors, direct sales to restaurant chains had strong growth resulting from successful new products and customer promotions of existing products. Sales to food processors were largely affected by lower pricing in response to a decrease in raw material costs, particularly for snack food seasonings. In Europe, sales rose 27.9% with

22

Uniqsauces contributing 17.7% of increase and foreign exchange contributing 12.0% of increase. The remaining decrease of 0.5% was due to lower demand for seasoning products, which more than offset strong condiment sales. In the Asia/Pacific region, sales increased 11.9%, with 5.9% of increase from foreign exchange and 6.0% from higher volume.

Operating income from continuing operations for the industrial business rose 2.7% to $110.2 million. Operating income margin was 10.0% in 2003 compared to 10.2% in 2002. The operating income increase was generally in line with the sales increase, excluding the Uniqsauces acquisition. This acquisition was strategically made for its condiment production facility and certain of its customer relationships. In the industrial segment, commodity cost increases and decreases are generally offset by pricing actions. However, in 2003 vanilla had a negative effect on operating income due to significant volatility in this commodity. The savings on supply chain initiatives were off-set by cost increases in pension and other benefit costs. Special charges in the industrial business increased to $2.3 million in 2003 from $1.8 million in 2002. Special charges in the industrial business for 2003 consisted of additional costs associated with the consolidation of production facilities in Canada and severance and other costs related to the consolidation of industrial manufacturing in the U.K. Special charges in the industrial business for 2002 primarily consisted of further severance and other costs related to the workforce reduction initiated in 2001 and further costs related to the closure of a U.S. distribution center.

Results of Operations—2002 compared to 2001

for the year ended November 30 (millions)

| | 2002

| | 2001

| |

|---|

| Net sales | | $ | 2,044.9 | | $ | 1,939.1 | |

| Gross profit | | | 799.5 | | | 737.5 | |

| | Gross profit margin | | | 39.1 | % | | 38.0 | % |

| Selling, general and administrative expense | | | 529.6 | | | 507.6 | |

| | Percentage of sales | | | 25.9 | % | | 26.2 | % |

| Operating income | | | 262.4 | | | 219.6 | |

| | Operating income margin | | | 12.8 | % | | 11.3 | % |

The Company adopted Statement of Financial Accounting Standard (SFAS) No. 142 effective December 1, 2001. In accordance with this pronouncement, the Company ceased amortization of goodwill and indefinite lived intangible assets. Prior year financial information has not been restated. The amounts reported for operating income and net income in 2001, in this section of the report, are therefore not comparable with the operating income and net income for 2002 and 2003.

On February 19, 2002, the Company's Board of Directors announced a two-for-one stock split of both classes of common stock, effective April 8, 2002. As a result of the stock split, the Company's shareholders received an additional common share for each share held. All per share amounts and numbers of shares outstanding in this report have been restated for the stock split for all periods presented.

Net sales from consolidated operations in 2002 increased 5.5% to $2.0 billion when compared to 2001 primarily as a result of volume. The favorable effect of foreign currency translation contributed 0.8% to this overall increase.

Gross profit margin increased to 39.1% in 2002 from 38.0% in 2001. Gross profit margins for the Company were favorably impacted by global procurement initiatives and ongoing efforts to improve efficiencies. In the consumer business, gross profit margin improvement was also due to favorable raw material costs. In the industrial business, gross profit margin also improved due to a shift in product mix to higher-margin, more value-added products. These favorable effects on the Company's food business gross margins were partially offset by implementation costs related to the B2K program.

Selling, general and administrative expenses in 2001 included goodwill amortization of $12.9 million. Excluding goodwill amortization in 2001, selling, general and administrative expenses were higher in 2002 than 2001 on both a dollar basis and as a percentage of net sales. These increases were primarily due to increased distribution, pension, and insurance costs, as well as increased spending related to the B2K program. The increased distribution costs were due to increased costs to service the Company's customers during the initial system implementation of B2K. Insurance costs increased concurrent with an industry-wide trend. While implementation expenses of B2K peaked in 2002, the future decrease in implementation expenses was expected to be slightly more than off-set by future increases in depreciation expense on the B2K systems that are implemented.

Interest expense decreased in 2002 versus 2001 due to favorable interest rates and lower average debt levels.

Other income decreased in 2002 compared to 2001. This decrease is attributable to exchange losses on foreign currency transactions.

The effective tax rate for 2002 was 31.0%, down from 32.6% in 2001. The lower tax rate was attributable to the elimination of goodwill amortization, which is generally a non-tax deductible expense. This effect is predominantly in international operations.

23

Income from unconsolidated operations increased to $22.4 million in 2002 versus $21.5 million in 2001. Unconsolidated operations consist primarily of our McCormick de Mexico and Signature Brands joint ventures.

Income from discontinued operations was $6.0 million in 2002 compared to $9.5 million in 2001. The packaging segment experienced softness in the first half of 2002 due to reduced demand for its customers' products, particularly tubes for personal care and cosmetics. Actions were taken in 2002 to adjust production activities, including a reduction in workforce. Late in 2001, the customer service function for Jenks was outsourced to its distributor. The distributor did not adequately control the customer service process, which led to $4.0 million of inventory and receivable write-offs in 2002. As a result of the sale of Jenks, these write-offs are included in income from discontinued operations on the consolidated income statement. All amounts included in discontinued operations are net of income taxes.

Consumer Business

for the year ended November 30 (millions)

| | 2002

| | 2001

| |

|---|

| Net sales | | $ | 993.9 | | $ | 944.1 | |

| Operating income | | | 191.9 | | | 160.5 | |

| | Operating income margin | | | 19.3 | % | | 17.0 | % |

In 2002, net sales for the consumer business increased 5.3% compared to 2001 primarily as a result of volume. The favorable effect of foreign currency fluctuations contributed 1.3% to this overall increase. Consumer sales in the Americas increased 3.9% from higher sales of core products and the introduction of new products. Sales in the Americas also benefited from a price increase that was offset in part by higher promotional trade allowance spending which is recorded as a reduction of sales. In Europe, sales increased 8.8% with 4.5% of increase due to foreign currency. The remaining 4.3% increase was attributable to favorable sales volume partially offset by unfavorable product mix. In the Asia/Pacific region, sales increased 7.1% with 2.9% of increase due to foreign currency. The remaining 4.2% increase was due primarily to higher volumes in China which generated 8.3% sales growth. Growth in China slowed in the fourth quarter of 2002 due to a strategic initiative that is underway. The Company is de-emphasizing some of its less profitable products in that market, such as ketchup and soy sauce, in order to focus on core products, such as spices and seasoning mixes, which have a higher margin.

In the consumer business, operating income margin was 19.3% in 2002 compared to 17.0% in 2001 due to global procurement initiatives, ongoing efforts to improve efficiencies, favorable raw material costs and decreased special charges. Special charges for the consumer segment decreased to $2.7 million in 2002 from $5.2 million in 2001. Special charges in the consumer business for 2002 primarily consisted of severance, lease exit and relocation costs related to the workforce reduction and realignment of consumer sales operations in the U.S. Special charges in the consumer business for 2001 primarily consisted of a product line elimination and a realignment of our sales operations in the U.K., and an overall workforce reduction.

Industrial Business

for the year ended November 30 (millions)

| | 2002

| | 2001

| |

|---|

| Net sales | | $ | 1,051.0 | | $ | 995.0 | |

| Operating income | | | 107.3 | | | 89.1 | |

| | Operating income margin | | | 10.2 | % | | 9.0 | % |

In 2002, net sales for the industrial business increased 5.6% versus 2001 primarily as a result of volume. The favorable effect of foreign currency fluctuations contributed 0.5% to this overall increase. Industrial sales in the Americas were up 5.5% due to strong sales, particularly of seasoning products and products sold to our food service customers. In Europe, sales increased 3.0% with 3.9% of increase from foreign exchange. The remaining 0.9% decrease was attributable to unfavorable product mix. In the Asia/Pacific region, sales increased 12.5% with 1.1% of increase from foreign exchange. The remaining 11.4% increase was due to increased volume predominantly in China as the Company continues to expand with its worldwide industrial customers.

In the industrial business, operating income margin was 10.2% in 2002 compared to 9.0% in 2001. The increase in operating income margin versus prior year is due to continued cost reduction initiatives and a continued shift in sales to higher-margin, more value-added products. This improvement was led by strong performance with U.S. food service customers and in the Asia/Pacific region. Special charges for the industrial business decreased to $1.8 million in 2002 from $6.0 million in 2001. Special charges in the industrial business for 2002 primarily consisted of further severance and other costs related to the workforce reduction initiated in 2001 and additional costs related to the closure of a U.S. distribution center. Special charges in the industrial business for 2001 related to the distribution center consolidation in the U.S., the consolidation of manufacturing in Canada and an overall workforce reduction.

24

Financial Condition

Continued strong cash flows from operations enabled the Company to fund operating projects and investments designed to meet the Company's growth objectives, make strategic acquisitions, and repurchase stock of the Company.

In the consolidated statement of cash flows, the changes in operating assets and liabilities are presented excluding the effects of changes in foreign currency exchange rates as these do not reflect actual cash flows. Accordingly, the amounts in the consolidated statement of cash flows do not agree with changes in the operating assets and liabilities that are presented in the consolidated balance sheet. In addition, the cash flows from operating, investing and financing activities are presented excluding the effects of discontinued operations.

In the consolidated statement of cash flows, cash provided by continuing operating activities was $195.4 million in 2003 compared to $205.3 million in 2002 and $188.7 million in 2001. Over the past three years, there has been an annual increase in net income from continuing operations which is an increasingly significant component of this cash flow. In 2003, 2002 and 2001, working capital items decreased cash flow. When 2003 is compared to 2002 the major use of funds from working capital was an increase in inventory due to the Company's strategic decision to carry a larger than normal inventory of vanilla beans in order to be in a position to meet the demands of its customers as the availability of quality beans has declined significantly. The change in other assets and liabilities in 2003 was mainly due to the timing of liability payments. When 2002 is compared to 2001, the increase in receivables is mainly due to strong sales in the fourth quarter of 2002. The increase in inventory in 2002 is due to higher levels to meet increased sales and the temporary effect of increased inventory as B2K was implemented at several of the Company's U.S. locations.

Continuing investing activities used cash of $100.7 million in 2003 versus $95.3 million in 2002 and $96.6 million in 2001. Net capital expenditures (capital expenditures less proceeds from the sale of fixed assets) were $81.7 million in 2003, $93.9 million in 2002 and $96.1 million in 2001. The reduction in capital expenditures in 2003 is due to less capital spending on B2K as the project was more capital intensive in 2002 and 2001. Capital expenditures in 2004 are expected to be slightly less than in 2003. Cash paid for the acquisitions of the Zatarain's and Uniqsauces businesses during 2003 was $202.9 million. Cash received from the sale of the Packaging and Jenks businesses during 2003 was $133.9 million. The Company also received $55.4 million during 2003 from the Ducros purchase price adjustment, of which, $5.4 million represented interest and is included in cash flows from continuing operating activities.

Continuing financing activities used cash of $131.3 million in 2003, $111.6 million in 2002 and $85.4 million in 2001. The Company's short-term borrowings increased only $17.2 million in 2003 as the Company was able to finance most of its investing and financing activities with cash flows from operations. In 2003, the Company purchased 4.5 million shares of common stock for $119.2 million under the Company's $250 million share repurchase program. As of November 30, 2003, $22.0 million remained under the $250 million share repurchase program. Without significant acquisition activity, the Company expects to complete this program by mid-2004. Anticipating this completion, the Company's Board of Directors authorized an additional $300 million of share repurchase. The Company expects this new program to extend into 2006. The common stock issued in 2003, 2002 and 2001 and the common stock acquired by purchase in 2002 and 2001 relates to the Company's stock compensation plans. In 2002, the Company repaid short-term borrowings based on cash flow generated from operations. In the first quarter of 2001, the Company finalized its medium-term note program for the Ducros acquisition and issued $300.0 million of notes, which replaced the existing commercial paper notes used to finance the transaction. In addition, during the third quarter of 2001, the Company retired $75.0 million of 8.95% fixed rate notes by issuing commercial paper.

Dividend payments increased to $64.1 million in 2003, up 9.4% compared to $58.6 million in 2002. Dividends paid in 2003 totaled $0.46 per share, up from $0.42 per share in 2002. In June 2003, the Board of Directors approved a 9.1% increase in the quarterly dividend from $0.11 to $0.12 per share. In November 2003, the Board of Directors approved an additional 16.7% increase in the quarterly dividend from $0.12 to $0.14 per share. Over the last 5 years, dividends have risen at a compounded annual rate of 10.5%.

The Company's pension plans had a shortfall of plan assets over accumulated benefit obligations at their 2003 and 2002 measurement dates of $166.6 million and $144.4 million, respectively. These shortfalls were due to the continued low interest rate environment and asset returns lower than assumed. As a result, the Company

25

recorded an additional minimum liability as required by Statement of Financial Accounting Standard (SFAS) No. 87 through a charge to other comprehensive income of $110.2 million ($69.1 million net of tax) in 2002 and $20.6 million ($14.4 million net of tax) in 2003 to increase accrued pension liabilities. Cash payments to pension plans were $27.2 million in 2003, $25.2 million in 2002 and $20.1 million in 2001. Minimum cash contributions to the plans required in 2004 are expected to be approximately $21 million. Future increases or decreases in pension liabilities and required cash contributions are highly dependent on changes in interest rates and the actual return on plan assets. The Company bases its investment of plan assets, in part, on the duration of each plan's liabilities. Across all plans, 68% of assets are invested in equities and 32% in fixed income investments.

The Company's ratio of debt-to-total-capital (total capital includes debt, minority interest and shareholders' equity) was 44.4% as of November 30, 2003, a decrease from 49.0% at November 30, 2002 and below the Company's target range of 45-55%. The decrease was primarily the result of an increase in shareholders' equity. Foreign currency had the effect of increasing shareholders' equity and accordingly, decreased the ratio of debt-to-total-capital by 4.5% in 2003. During the year, the Company's short-term debt varies, however, it is usually lower at the end of the year. The average short-term borrowings outstanding for the year ended November 30, 2003 and 2002 were $287.6 million and $297.5 million, respectively.

The reported values of the Company's assets and liabilities held in its non-U.S. subsidiaries and affiliates have been significantly affected by fluctuations in foreign exchange rates between periods. During the year ended November 30, 2003, the exchange rates for the Euro, British pound sterling, Canadian dollar and Australian dollar were substantially higher versus the U.S. dollar than in 2002. Exchange rate fluctuations resulted in an increase in accounts receivable of approximately $30 million, inventory of approximately $19 million, goodwill of approximately $81 million and other comprehensive income of $131 million since November 30, 2002.

The Company has available credit facilities with domestic and foreign banks for various purposes. The amount of unused credit facilities at November 30, 2003 was $454.0 million. Holders of $55.0 million of the Company's medium-term notes due in 2024 have a one-time option to require retirement of these notes in 2004. In the event the option is exercised, management has the ability and intent to refinance with long-term debt. Management believes that internally generated funds and the Company's existing sources of liquidity under its credit facilities are sufficient to meet current and anticipated financing requirements over the next 12 months. If the Company were to under-take an acquisition that requires funds in excess of its existing sources of liquidity, it would look to sources of funding from additional credit facilities or debt issuances.

Special Charges

In 2001, McCormick adopted a plan to streamline its operations. While 2001 was a record year for McCormick, the U.S. and global economies did not fare as well. Recognizing that it is not immune to the impact of these difficult financial times on its customers and consumers, the Company formalized a plan to more rapidly streamline its operations to meet the challenges that it, and all companies, faced in 2002 and in the future.